Managing Operational Risk - Citibank - Banking · PDF fileManaging Operational Risk Jaidev...

24

Managing Operational Risk Jaidev Iyer, Operational Risk Exprt

Transcript of Managing Operational Risk - Citibank - Banking · PDF fileManaging Operational Risk Jaidev...

Managing Operational Risk

Jaidev Iyer, Operational Risk Exprt

AGENDA

WHAT IS OPERATIONAL RISK

WHAT IS OPERATIONAL RISK

MANAGEMENT

WHAT IS THE VALUE

PROPOSITION

1

2

3

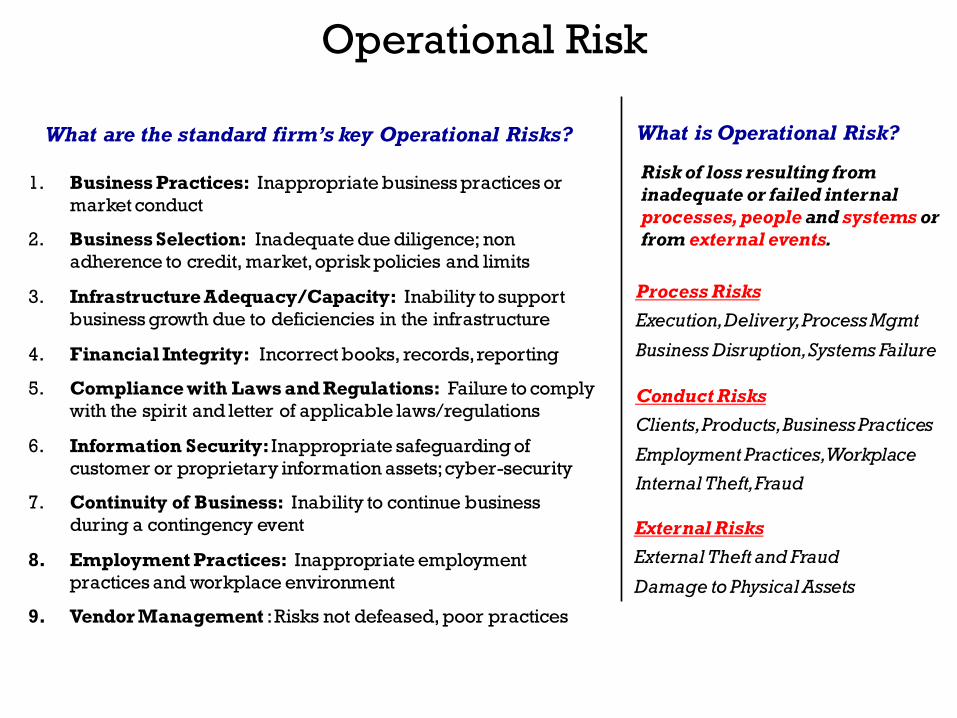

Risk of loss resulting from

inadequate or failed internal

processes, people and systems or

from external events.

What is Operational Risk?

1. Business Practices: Inappropriate business practices or

market conduct

2. Business Selection: Inadequate due diligence; non

adherence to credit, market, oprisk policies and limits

3. Infrastructure Adequacy/Capacity: Inability to support

business growth due to deficiencies in the infrastructure

4. Financial Integrity: Incorrect books, records, reporting

5. Compliance with Laws and Regulations: Failure to comply

with the spirit and letter of applicable laws/regulations

6. Information Security: Inappropriate safeguarding of

customer or proprietary information assets; cyber-security

7. Continuity of Business: Inability to continue business

during a contingency event

8. Employment Practices: Inappropriate employment

practices and workplace environment

9. Vendor Management : Risks not defeased, poor practices

What are the standard firm’s key Operational Risks?

Process Risks

Execution, Delivery, Process Mgmt

Business Disruption, Systems Failure

Conduct Risks

Clients, Products, Business Practices

Employment Practices, Workplace

Internal Theft, Fraud

External Risks

External Theft and Fraud

Damage to Physical Assets

Operational Risk

Operational Risk as a Discipline

Discipline Modern History Risk Mitigation Tools Risk Measurement

Credit

Risk

Age > 50 years

Portfolio view > 35 yrs

Quantitative > 20 yrs

Active mitigation >15 yrs

Target market/portfolio

Risk-based capital

Credit approval process

Assignments / participations

Credit derivatives

Value at Risk based on

• Prob. of Default – ORR

• LGD – FRR

Operational

Risk

Age <10 years

Portfolio view… TBD

Quantitative < 5 yrs

Active mitigation: culture?

Risk-based capital

Pace of business growth

Infra investment, planning

People management, training

Value at Risk based on

• Loss frequency

• Loss severity

Metrics / KRIs

Market

Risk

Age >30 years

Portfolio view >20 yrs

Quantitative >15 yrs

Active mitigation>10 yrs

Risk-based capital

Boundaries

Diversification

Hedging positions

Value at Risk based on

• Factor Sensitivity

• Potential Losses

4

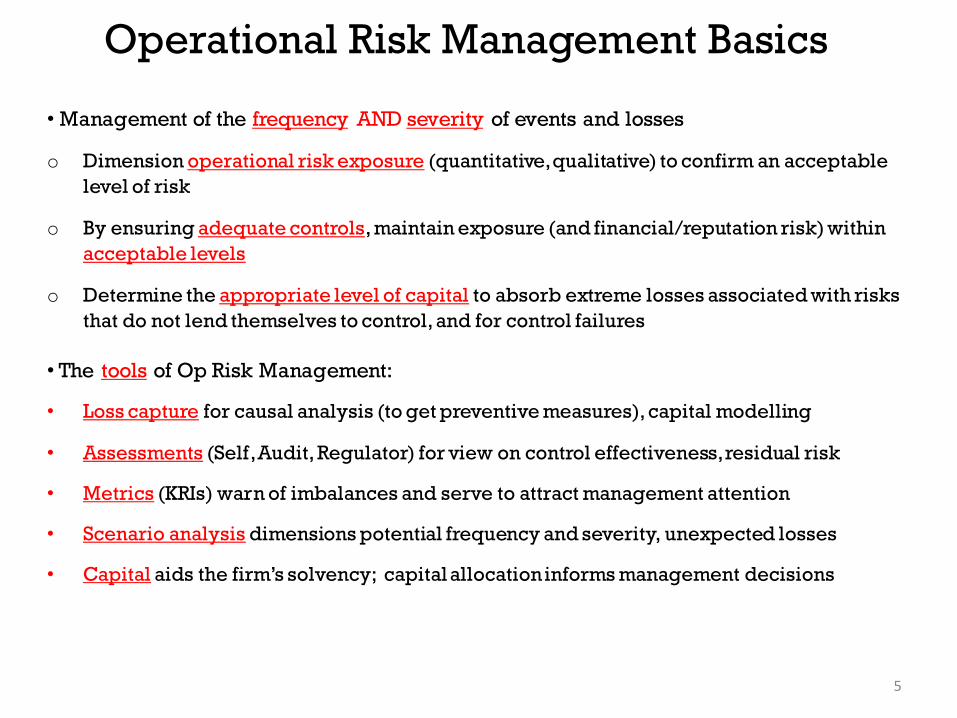

Operational Risk Management Basics

• Management of the frequency AND severity of events and losses

o Dimension operational risk exposure (quantitative, qualitative) to confirm an acceptable

level of risk

o By ensuring adequate controls, maintain exposure (and financial/reputation risk) within

acceptable levels

o Determine the appropriate level of capital to absorb extreme losses associated with risks

that do not lend themselves to control, and for control failures

• The tools of Op Risk Management:

• Loss capture for causal analysis (to get preventive measures), capital modelling

• Assessments (Self, Audit, Regulator) for view on control effectiveness, residual risk

• Metrics (KRIs) warn of imbalances and serve to attract management attention

• Scenario analysis dimensions potential frequency and severity, unexpected losses

• Capital aids the firm’s solvency; capital allocation informs management decisions

5

WHO IS LOOKING FOR IT ?

HOW AND WHEN?

VALUE IS ELUSIVE

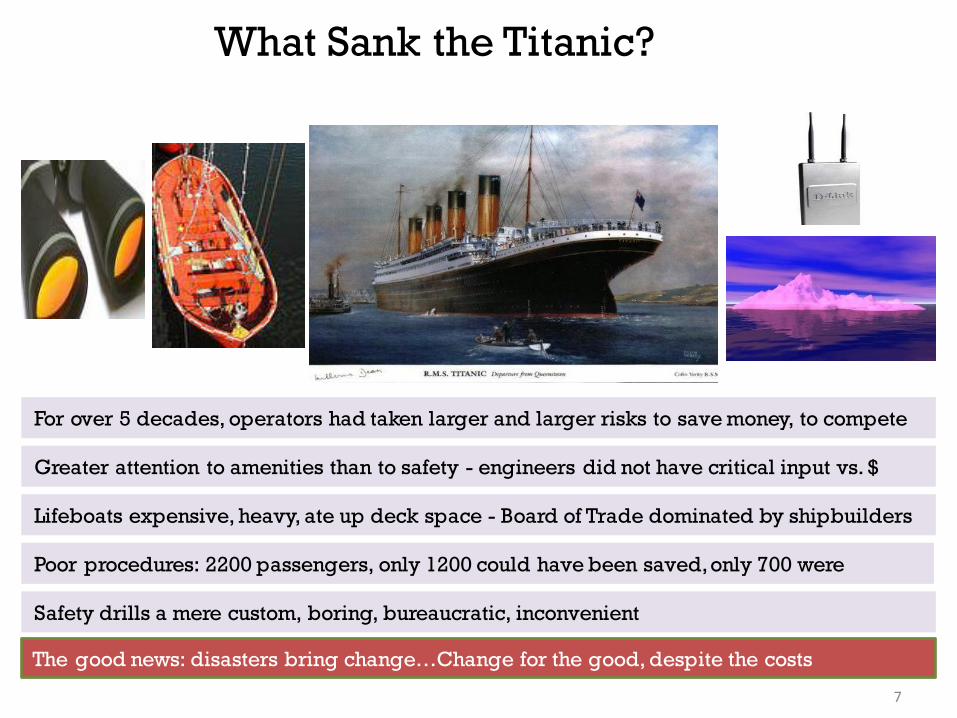

The good news: disasters bring change…Change for the good, despite the costs

Lifeboats expensive, heavy, ate up deck space - Board of Trade dominated by shipbuilders

Poor procedures: 2200 passengers, only 1200 could have been saved, only 700 were

Greater attention to amenities than to safety - engineers did not have critical input vs. $

For over 5 decades, operators had taken larger and larger risks to save money, to compete

Safety drills a mere custom, boring, bureaucratic, inconvenient

What Sank the Titanic?

7

The Problem with Operational Risk

• Potential losses are practically unbounded

– Exposure is undefined and undimensioned

– Losses are not capped, e.g by Credit Risk Limits or Market Risk Stop Losses

– Observed loss amounts are not simply related to firm size although some

evidence of deep pockets premium e.g lawsuits and regulatory settlements

– Loss severity distributions are fat-tailed

– The payoff profile is asymmetric

• Risks are not easily controlled in the short term

– Limited ability to ‘trade down’ or close positions’

– Risks often only recognized ‘ after the fact’

– Often significant lags between cause and effect

– Management and Measurement of Risk follow diverse paths

• Capital need is driven by the risk of infrequent but extremely large events

8

The Problem with OpRisk Management

• Ex-Ante vs Ex-Post: Historical, rear-view mirror … years on, we still know too little

• “What” are we Managing

• Who owns the “So-What”

• Tool-kit Elements disparate, outmoded: the dots are still un-join-able

• Same brush applied to High-Severity and High-Frequency risks

• Perceived focus on Measurement over Management; achievement of Neither

• Stakeholders tired of Assessments, Form-filling, Bean-Counting …that go Nowhere

• Regulators seen to focus on form, not substance.

• So Management says stay away from us, just keep the Regulators happy

• All in all, Default approach is therefore Compliance and Audit, not Risk

9

BEST PRACTICES IN

OPERATIONAL RISK

PROCESS VIEW !!!

ANALYSIS, ANALYSIS

JOIN DOTS

SCENARIOS, CAPITAL

COMMUNICATE

1

2

3

4

5

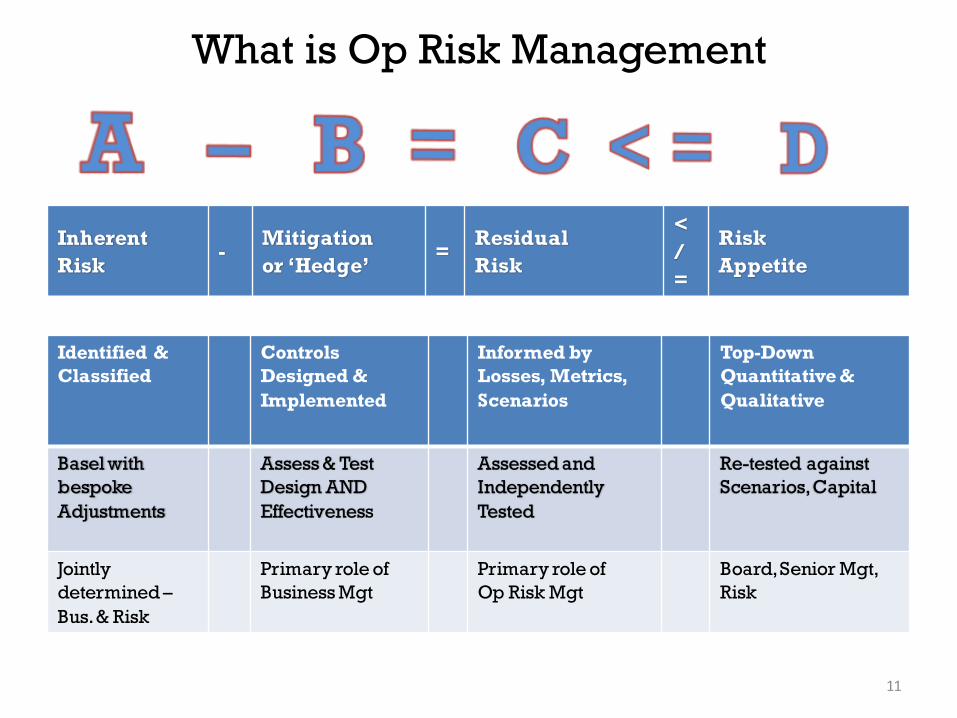

What is Op Risk Management

Inherent

Risk -

Mitigation

or ‘Hedge’ =

Residual

Risk

<

/

=

Risk

Appetite

Identified &

Classified

Controls

Designed &

Implemented

Informed by

Losses, Metrics,

Scenarios

Top-Down

Quantitative &

Qualitative

Basel with

bespoke

Adjustments

Assess & Test

Design AND

Effectiveness

Assessed and

Independently

Tested

Re-tested against

Scenarios, Capital

Jointly

determined –

Bus. & Risk

Primary role of

Business Mgt

Primary role of

Op Risk Mgt

Board, Senior Mgt,

Risk

11

An integrated, comprehensive and forward looking approach to risk

• Risk and control directly linked to process & outcomes: front, middle, back

• Clarity on the effort to manage objectives-based vulnerabilities

OpRisk Management Essentials

Embedded and entwined into organization, business, and culture

• Start with overall process framework (process maps, anybody ?!!)

• Identify Risk/s based on threat/s to meeting business objectives

• Define required Controls; Configure and Customize controls

• Compute and optimize resources (time, cost) to implement the controls

• Complete integration with process, people and technology for resilience

• Implement essential Assessments, Metrics, Scenarios, Capital charge

1

2

Speak one language across stakeholders (including Regulators)

• Vulnerability mapped to Basel risk classification for “same page”

• Isolate the ‘cost of control’ to set up the too-much-versus-too-little dialogue

• Systematize the Control debate: existing, duplicate, expensive, useless

3

12

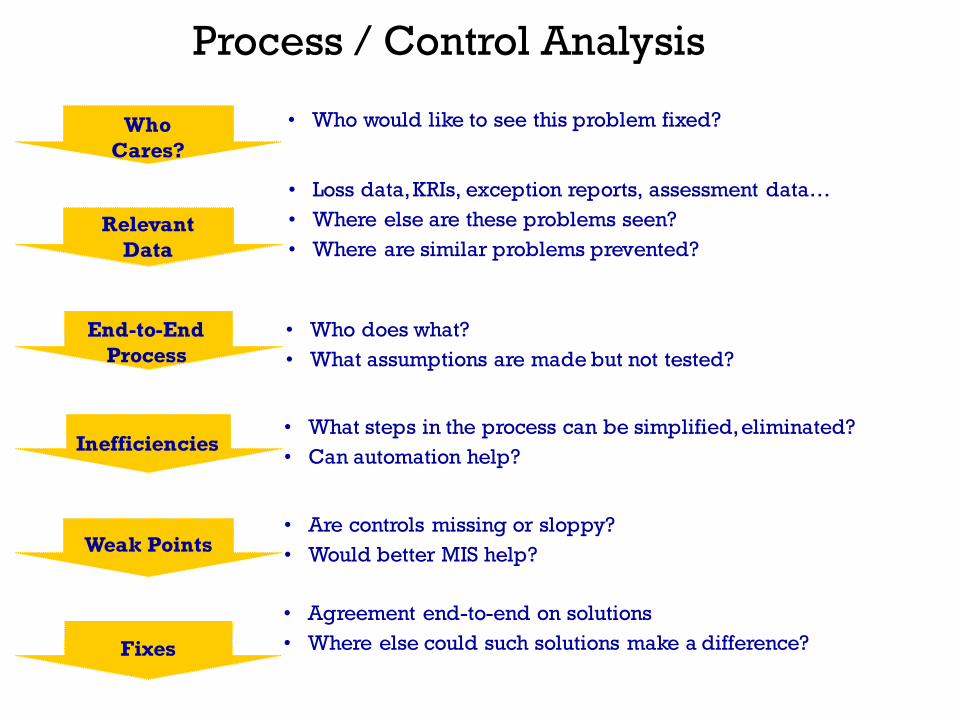

Process / Control Analysis

• Who does what?

• What assumptions are made but not tested?

• Are controls missing or sloppy?

• Would better MIS help?

• What steps in the process can be simplified, eliminated?

• Can automation help?

• Loss data, KRIs, exception reports, assessment data…

• Where else are these problems seen?

• Where are similar problems prevented?

End-to-End

Process

Inefficiencies

Weak Points

Fixes

Relevant

Data

Who

Cares?

• Who would like to see this problem fixed?

• Agreement end-to-end on solutions

• Where else could such solutions make a difference?

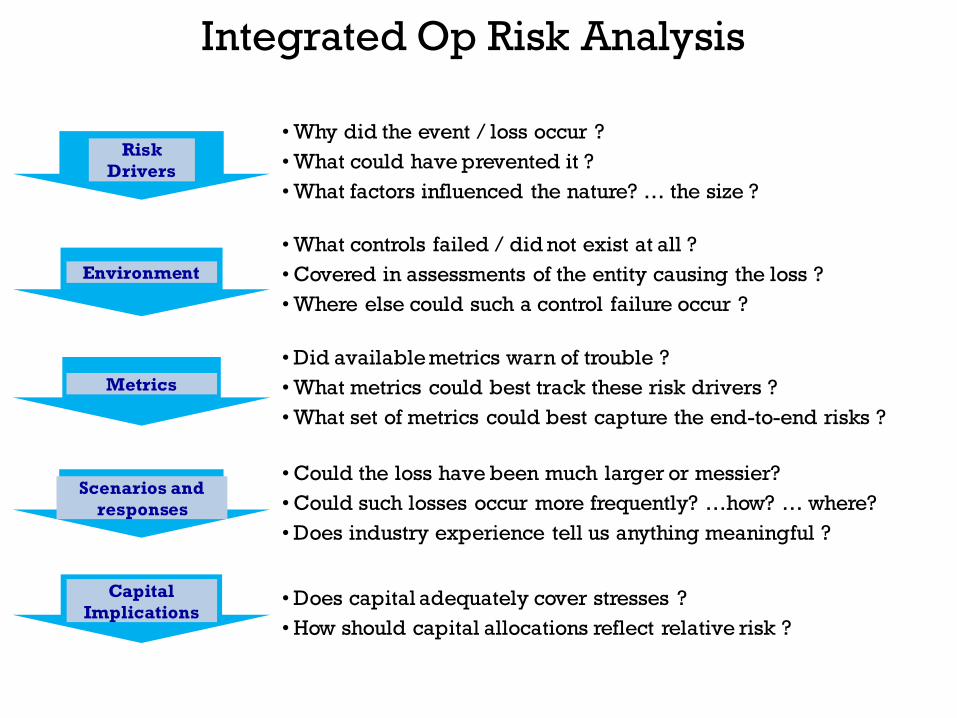

Integrated Op Risk Analysis

Risk

Drivers

• Why did the event / loss occur ?

• What could have prevented it ?

• What factors influenced the nature? … the size ?

Environment

• What controls failed / did not exist at all ?

• Covered in assessments of the entity causing the loss ?

• Where else could such a control failure occur ?

Metrics

• Did available metrics warn of trouble ?

• What metrics could best track these risk drivers ?

• What set of metrics could best capture the end-to-end risks ?

Scenarios and

responses

• Could the loss have been much larger or messier?

• Could such losses occur more frequently? …how? … where?

• Does industry experience tell us anything meaningful ?

Capital

Implications • Does capital adequately cover stresses ?

• How should capital allocations reflect relative risk ?

Scenario Analysis

• What controls can prevent an event?

• Do they exist and work well?

• Would existing metrics warn of trouble?

• Would it happen HERE?

• If so, how big could it be HERE?

• Is capital sufficient?

• Control improvements?

• Better metrics?

• What data is available about past frequency and scale?

• What factors drive the size of the impact?

• Do we face a previously unrecognized risk?

• In which businesses, regions?

Would it

Happen?

Fixes

Capital Impact

How big?

Could it

Happen?

Who Cares? • Who would be most hurt?

The derivation, treatment, and

configuration of controls

Pre Event

•Design

• Process Vulnerability

• Compensating Control

• Control Environment

• People & Technology

Monitoring

• Monitoring

• RSCA plan and checklists

• Span of control

• Residual risk indicators

• Control effectiveness

Post Event

• Incident Management

• Detection

• Mitigation

• Escalation

• Prevention

Process Outcome

Basel Classification

Business Rules

Control Objectives

Compensating Control

Key Risk Metrics

Cost of Control

Control Procedures

Escalation Paths

Supervisory Review

Assessment Checklists

Control Configuration

16

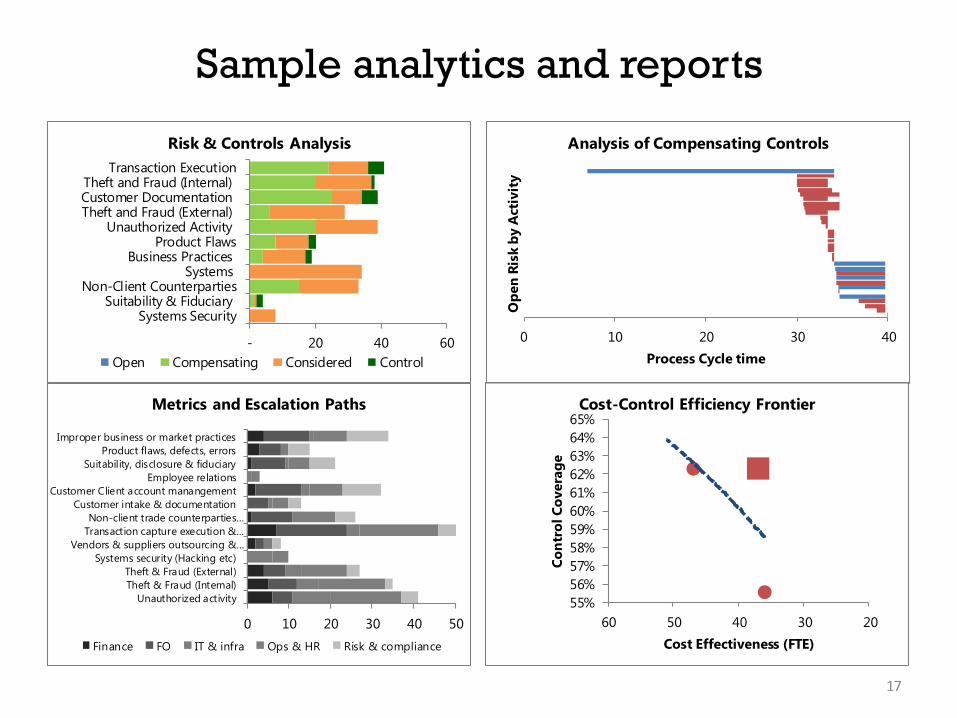

Sample analytics and reports

- 20 40 60

Systems SecuritySuitability & Fiduciary

Non-Client CounterpartiesSystems

Business PracticesProduct Flaws

Unauthorized ActivityTheft and Fraud (External)Customer DocumentationTheft and Fraud (Internal)

Transaction Execution

Risk & Controls Analysis

Open Compensating Considered Control

0 10 20 30 40

Process Cycle time

Op

en

Ris

k b

y A

ctiv

ity

Analysis of Compensating Controls

55%

56%

57%

58%

59%

60%

61%

62%

63%

64%

65%

2030405060

Co

ntr

ol C

overa

ge

Cost Effectiveness (FTE)

Cost-Control Efficiency Frontier

0 10 20 30 40 50

Unauthorized activity

Theft & Fraud (Internal)

Theft & Fraud (External)

Systems security (Hacking etc)

Vendors & suppliers outsourcing &…

Transaction capture execution &…

Non-client trade counterparties…

Customer intake & documentation

Customer Client account manangement

Employee relations

Suitability, disclosure & fiduciary

Product flaws, defects, errors

Improper business or market practices

Metrics and Escalation Paths

Finance FO IT & infra Ops & HR Risk & compliance

17

0.0001

0.001

0.01

0.1

1

10

100

1000

0.1 1 10 100 1000 10000 100000

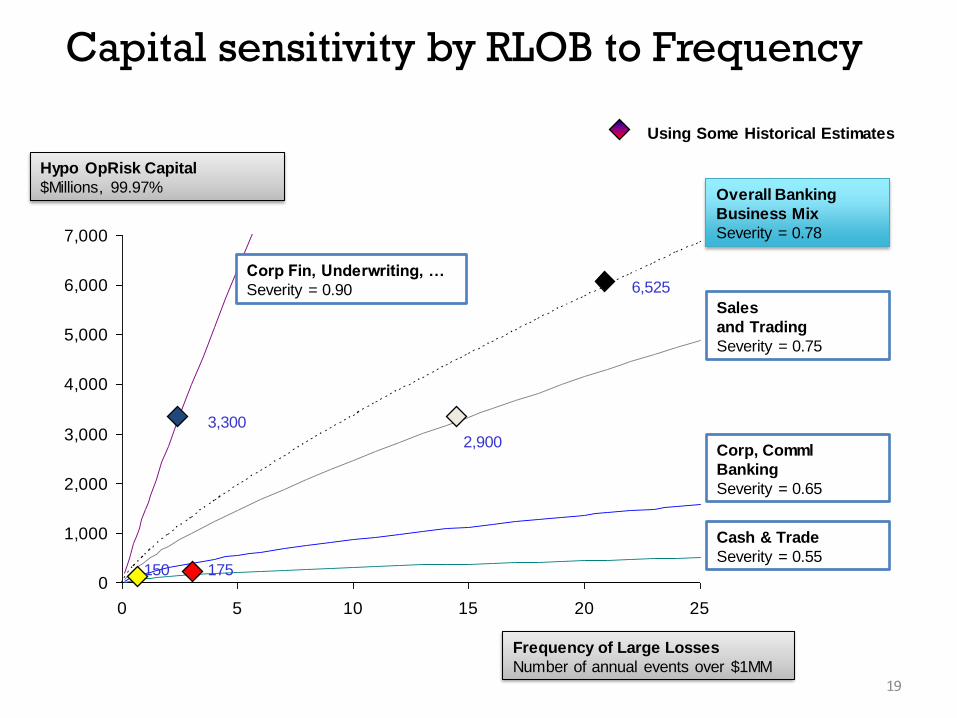

Capital : Three Fundamental Questions

Operational Event Frequency

Annual Events over Threshold

Loss Size

Question 1:

What is the

expected

frequency of

events over a

loss threshold?

Question 2: How rapidly does

loss probability decline with

size of loss (inverse slope = tail

parameter)?

Question 3: What

is the required

confidence level

for capital: 99.9%

Capital is the

extrapolated

loss at chosen

confidence

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

0 5 10 15 20 25

Frequency of Large Losses

Number of annual events over $1MM

Hypo OpRisk Capital

$Millions, 99.97%

Corp Fin, Underwriting, …

Severity = 0.90 Sales

and Trading

Severity = 0.75

Corp, Comml

Banking

Severity = 0.65

Cash & Trade

Severity = 0.55

Overall Banking

Business Mix

Severity = 0.78

Using Some Historical Estimates

Capital sensitivity by RLOB to Frequency

3,300

6,525

2,900

150 175

19

SUMMARY

What did we learn from the Crisis

o Organizations try too hard to avoid learning from their own mistakes

o The sustainability tradeoff for financials cos. is not growth vs prudence, but with

o The Monday-Tuesday-Wednesday syndrome is unsustainable

o “Culture” means how we do business, to optimize that tradeoff

o Models don’t kill markets, people do

o The risk-taker is your first-line of defense, but all Three Lines matter

o We must evolve a common idea of what a Risk Manager is or does

o ‘Our people are our greatest assets’ needs to be real, insofar as Asset Risks

o Silos are fatal;: the way risk manifests is irrelevant, labels are redundant

o Join-the-dots intelligence is the only worthwhile investment in Risk Mgt

o There needs be sufficient premium on quantity and quality of communication

21

Risk in the post-crisis era

• Market & Credit Risk are transactional, substitutable, arbitrageable, inseparable

• Op Risk is corporate, top-down, about Infrastructure and Reputation

• But it is also inseparable from other Risk-types, and substitutable

• Operational Risk and Compliance also no longer separable

• Severity and Frequency management are 2 different schools within OpRisk

• A singular measure of Risk (e.g. VaR) is very good, and very bad

• Portfolio strategies must incorporate crisis correlations

• Time is nigh for a solution to the holistic stress-testing conundrum

22

“History only teaches us that we will be surprised, again and again”

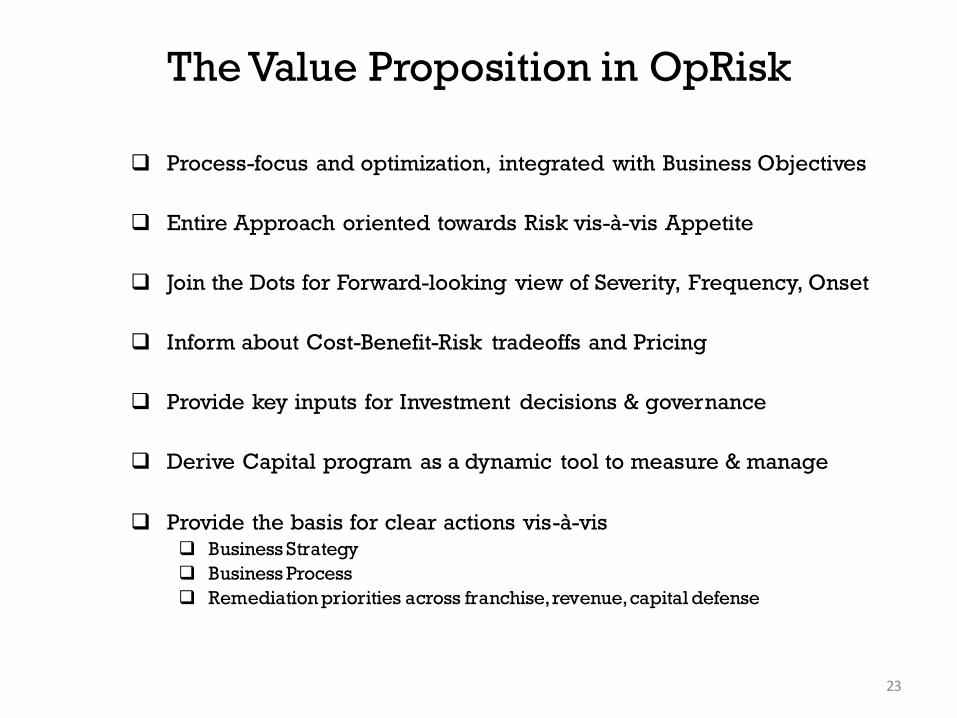

The Value Proposition in OpRisk

Process-focus and optimization, integrated with Business Objectives

Entire Approach oriented towards Risk vis-à-vis Appetite

Join the Dots for Forward-looking view of Severity, Frequency, Onset

Inform about Cost-Benefit-Risk tradeoffs and Pricing

Provide key inputs for Investment decisions & governance

Derive Capital program as a dynamic tool to measure & manage

Provide the basis for clear actions vis-à-vis Business Strategy

Business Process

Remediation priorities across franchise, revenue, capital defense

23

Thank you!

Questions?

24