Managing Market Abuse briefing 16/07/15

39

Managing market abuse Practical responses to regulatory pressure Bovill briefing | London | 16 th July 2015 Mark Spiers, Mike Booth, Beth Cazalet

Transcript of Managing Market Abuse briefing 16/07/15

Managing market abusePractical responses to regulatory pressure

Bovill briefing | London | 16th July 2015

Mark Spiers, Mike Booth, Beth Cazalet

2

Today we’ll be looking at…

• the UK rules in this area – an overview

• the respective roles of compliance and front office teams

• obligations for controlling access to inside information

• effective and proportionate use of pre-trade controls

• how to effectively conduct post-trade surveillance.

Why think about Market Abuse now?

The FCA is focusing on the asset management industry more

The FCA has a greater appetite to pursue criminal convictions

or issue public sanctions

Reputational and financial risk continues to be a concern

Regulatory change over the last few years has taken

resources away from monitoring

MAD II is on the horizon

FCA Market Abuse Thematic Review

Source: Bovill analysis of TR 15-01, the larger the word the more times it has been used (removed the words - information, inside and firm)

Overview of the UK rules in this area

6

The Market Abuse Framework

Abusive behaviours

Qualifying investments

FSMA

MAR

Individuals Firms

7

Territorial Scope

UK

Qualifying

Investments

Prescribed

markets

Related

investments

8

Abusive behaviours

Insider dealingImproper

disclosure

Manipulating

transactions

Manipulating

devicesDissemination

Distortion and

misleading

behaviour

9

Criminal and Civil regime

Maximum criminal penalties:

• unlimited fine

• seven years imprisonment.

Civil disciplinary regime allows the FCA to impose:

• unlimited fine

• public statement about the behaviour

• injunction requiring the person to stop the abusive behaviour

• order for restitution – where the individual is required to return or make

good any profit made from the abusive behaviour

• require the payment of compensation to victims.

10

Qualifying investments & prescribed markets

Qualifying investments Prescribed markets

• transferable securities

• units in collective investment

undertakings

• money-market instruments

• financial futures contracts, including

equivalent cash-settled instruments

• forward interest rate agreements

• interest rate, currency and equity

swaps

• options

• derivatives on commodities

• + more

Defined as UK Recognised Investment

Exchanges, all other regulated markets in

the EEA and OFEX.

Auction Platforms (meaning a platform on

which auctions of emissions allowances

are traded) are also considered

prescribed markets.

Details of Recognised Investment Exchanges

are available at: fsa.gov.uk/register/exchanges.do

11

Focus areas for today

Insider dealing

Market manipulation

Rumours

Inside information

13

Market abuse

Insider dealing

Improper disclosure

Manipulating transactions

Manipulating devices

Dissemination

Distortion and misleading behaviour

14

Insider dealing

“Where an insider deals, or attempts to deal, in a

qualifying investment or related investment on the basis

of inside information relating to the investment in

question."

15

Inside information

Information of a

precise nature

Not generally

available

Relating to an

issuer or

qualifying

investments Would, if

generally

available, be

likely to have a

significant

effect on price

16

Improper Disclosure

“When an insider discloses inside information to another

person otherwise than in the proper course of the exercise of

his employment, profession or duties.”

17

Manipulating transactions

“Behaviour that consists of effecting transactions or orders to

trade (otherwise than for legitimate reasons and in conformity

with accepted market practices on the relevant market) which:

• give, or are likely to give, a false or misleading impression

as to the supply of, or demand for, or as to the price of, one

or more qualifying investments; or

• secure the price of one or more such investments at an

abnormal or artificial level.”

18

Manipulating devices

“Behaviour that consists of effecting transactions or orders to

trade which employ fictitious devices or any other form of

deception or contrivance.”

19

Dissemination

“Behaviour that consists of the dissemination of information by

any means which gives, or is likely to give, a false or

misleading impression as to a qualifying investment by a

person who knew or could reasonably be expected to have

known that the information was false or misleading.”

20

Distortion and misleading behaviour

“Behaviour that (not falling within the definitions of

Manipulating Transactions, Manipulating Devises or

Dissemination):

• is likely to give a regular user of the market a false or

misleading impression as to the supply of, demand for or

price or value of, qualifying investments; or

• would be, or would be likely to be, regarded by a regular

user of the market as behaviour that would distort, or would

be likely to distort, the market in such an investment.”

21

Market abuse

Mark Stevenson

Deliberately manipulated gilt price

hoping to sell to the Bank of England

as part of Quantitative Easing.

£662,700

Banned

Michael Coscia

Using his own algorithm he placed

thousands of false orders (layering)

taking advantage of price movements. £600,000

David Einhorn

Instructed the sale of shares in

Punch Taverns on the basis of inside

information£3 million

Paul Milsom

An approved person with sensitive and

valuable information – betrayed trust

by disclosing inside information

relating to forthcoming transactions.

£245,000

plus 2 years

in prison.

22

Controlling access to inside information

If one person has it

I assume everyone

has is

If one entity in the

group has it I assume

the whole group has

it

I use the investment

analysts as a buffer

between the inside

information and the

Manager

I have a designated

person responsible for

dealing with soundings

There are data

read restrictions

in system

I tell everyone

I have Chinese

walls between

teams

The network

drives are only

accessible by

particular people

Front office vs Compliance

24

Where do the responsibilities reside?

1. Identifying

inside

information

2. Preventing

market

manipulation

3. Detecting

market

manipulation

4. Lifting trade

restrictions

5. Conducting

surveillance

6. Keeping the

insider /

restricted list

7. Approving

PA deals

9. Oversight of

MAR

technology

solutions

8. Implementing

MAR

controls

Risk based monitoring for

Market Abuse

What are we trying to do?

• Treat the Clients Fairly / Conflicts of Interest

• Protect the markets from abuse

• Protect the firm from regulatory disciplinary action

• Look good in due diligence reviews

Monitoring for market abuse – the goal?

26

27

The Broking

Arm of an

Investment

House

A Corporate

Finance

Department

Secure

Printers

publishing

offering

documents

Asset

Manager

using OTC

products

Dick:

Doesn’t PA

deal

because he

has “skin in

the game”

by owning

his fund.

Navinder:

Sole trader

using HFT

strategy

Harry:

PA deals

frequently but

whose

requests are

often denied

Sue:

IT contractor

assisting

with the

servers

The biggest risk?

28

Identifying your risks

Do you understand

the potential abuse

areas surrounding

your

client and PA deals?

Do you

understand the

systems you

have in place

to carry out

client and PA

deals?

Do you understand the

MAR controls that you

have in place when

carrying out client and PA

deals?

Pre and post trade controls

30

Discussion of pre-trade controls

Insider

dealing

Designated person

maintains the

restricted list

Restrictions coded

into trade order

system

Staff training

Hard blocks

implemented

Regular

attestations in

relation to PA

dealing

PA dealing

approval process

Informal

attendance by

compliance at

investment

meetings

Market

manipulation

Second pair of

eyes review pre

trade

Position limits

coded into the

trade order system

Clear statement of

the trading

strategy

Separate dealing

desk

Exception

reports based

on your risks

produced

31

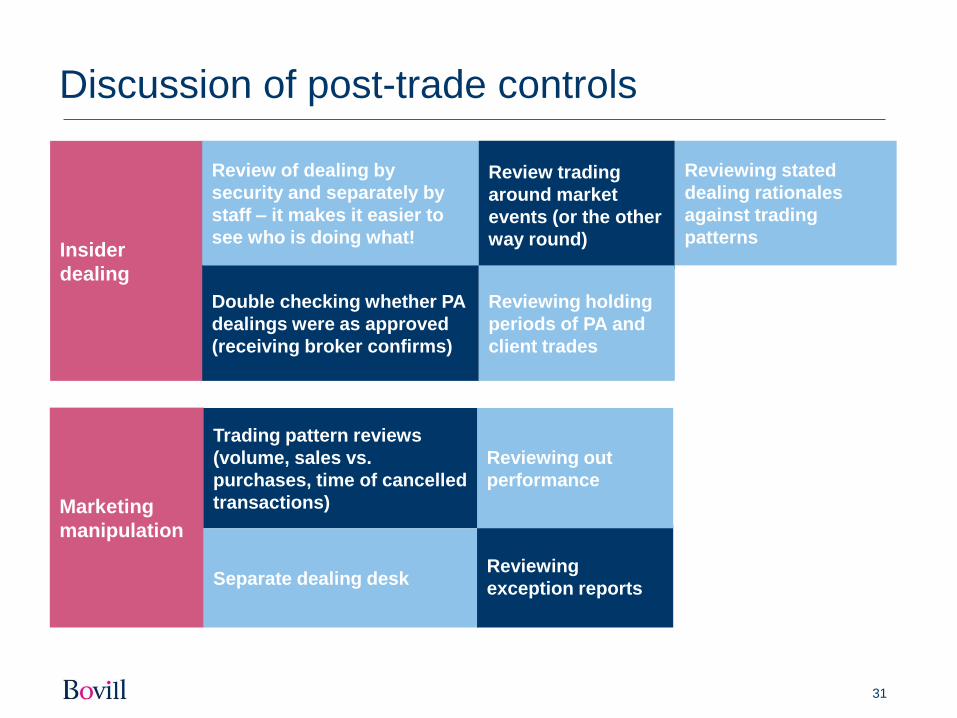

Discussion of post-trade controls

Insider

dealing

Review of dealing by

security and separately by

staff – it makes it easier to

see who is doing what!

Double checking whether PA

dealings were as approved

(receiving broker confirms)

Review trading

around market

events (or the other

way round)

Reviewing holding

periods of PA and

client trades

Reviewing stated

dealing rationales

against trading

patterns

Marketing

manipulation

Trading pattern reviews

(volume, sales vs.

purchases, time of cancelled

transactions)

Separate dealing deskReviewing

exception reports

Reviewing out

performance

Thinking about your controls

32

How do I know that the controls we put in place are working – especially if

they are automatic system controls?

When were the automatic control rules last reviewed and updated?

Are our automatic system controls based around guideline restrictions and

PA dealing requests or do they also consider client deals and manipulating

transactions?

What are the exception reports actually telling me about particular

individuals or desks?

Am I seeing any correlation between phone calls or Bloomberg chat and

dealing that is a concern?

33

Thinking about your controls

Market abuse may be a “one-off” event, but just as likely to be on-going.

Look out for:

• “Forgetting” to get PA deals approved

• PA dealing in securities that are clients’ investable universe but not in

client portfolio

• What has happened in the market or sector the security is based in

• Dealing in derivatives based on securities in clients’ portfolios

• Volumes of cancelled transactions

• Dealing frequency

• Transactions outside agreed parameters or strategy

• Trading after stop list block.

We can’t do it all – what is most important?

34

Where to start

Basic Better Best

Waiting in the wings

• Widens inside information and disclosure definitions

• Harmoises insider dealing and unlawful disclosure

• Widens market manipulation applicability

• Legislates for market soundings

• Widens requirements for suspicious transaction and order reports

(STORs)

MAD II – selected impacts

36

Putting it into practice

38

Market abuse control framework

Managing the risk insider information is not

identifiedA

Controlling access to insider informationB

Pre-trade controlsC

Personal account dealingD

Post trade surveillanceE

TrainingF

A

B

E

Mark

et in

form

atio

n

Investm

ent m

anag

em

ent firm

Bro

kers

/ dire

ct a

ccess

Preventative controls Detective controls

Com

plia

nce

C

D

F

39

Questions