Managing Liquidity Banks can experience illiquidity when cash outflows exceed cash inflows. They can...

18

-

Upload

meryl-norton -

Category

Documents

-

view

218 -

download

0

Transcript of Managing Liquidity Banks can experience illiquidity when cash outflows exceed cash inflows. They can...

Managing LiquidityBanks can experience illiquidity when cash outflows

exceed cash inflows. They can resolve any cash deficiency either by

creating additional liabilities or by selling assets. Since some assets are more marketable than others in

the secondary market, the bank’s asset composition can affect its degree of liquidity.

At an extreme, banks could assure sufficient liquidity by using most of their funds to purchase treasury securities.

Use of securitization to Boost LiquidityThe process of securitization commonly involves the

sale of assets by the banks to a trustee, who issues securities that are collateralized by the assets.

Banks are more liquid as a result of securitization because they effectively convert future cash flows into immediate cash.

Managing Interest Rate RiskThe composition of banks balance sheet will determine

how its profitability is influenced by interest rate fluctuations.

If a bank expects interest rates to consistently decrease over time, it will consider allocating most of its funds to rate insensitive assets, such as long-term and medium-term loans as well as long-term securities.

If a bank expects interest rates to consistently increase over time, it will consider allocating most of its funds to rate sensitive assets such as short term commercial and consumer loans, long term loans with floating interest rates, and short term securities.

A major concern of banks is how interest rate movements will affect performance, particularly earnings

A more formalized comparison of the banks interest revenues and expenses is provided by the net interest margin, computed as

Net interest Margin = Interest revenues – Interest expense Total Assets/ Earning Assets

The change depends on: Whether the bank’s assets are more or less rate

sensitive than bank liabilitiesThe degree of difference in rate sensitivity And the direction of interest rate movements.

During a period of rising interest rates a bank’s net interest margin will likely decrease if its liabilities are more rate sensitive than its assets

For example: Suppose a large international bank records

$4 billion in interest revenues from its loans and security investments and $2.6 billion in interest expenses paid out to attract deposits and other borrowed funds. If the bank holds $40 billion in earning assets, its net interest margin is:

Methods to Assess Interest Rate RisksGap Measurement ( Asset/ Liability

Management)Duration MeasurementRegression Analysis

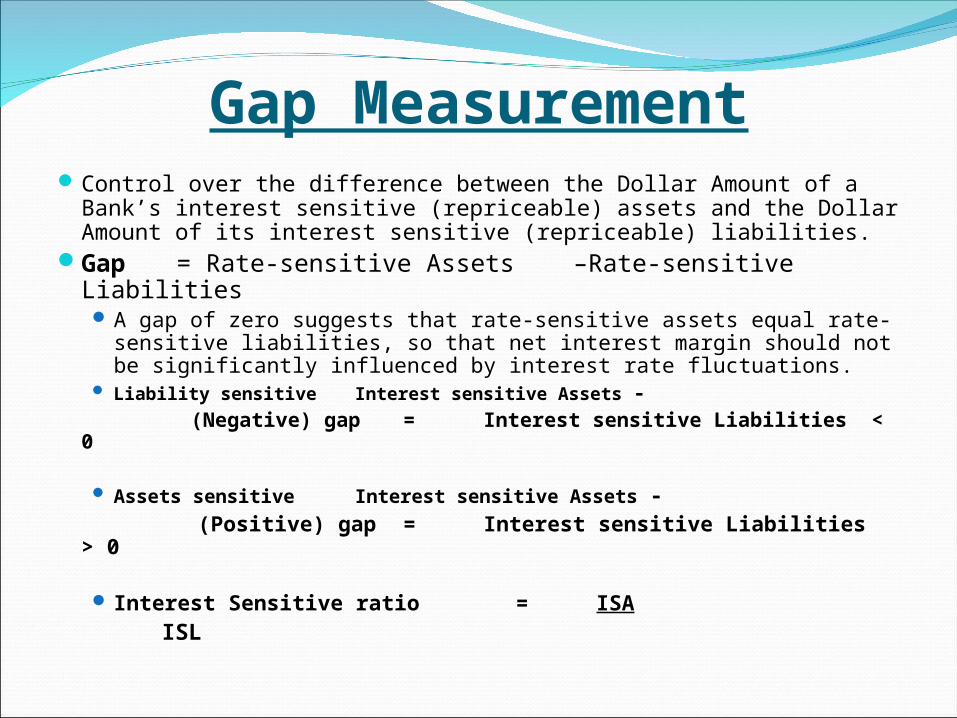

Gap MeasurementControl over the difference between the Dollar Amount of a

Bank’s interest sensitive (repriceable) assets and the Dollar Amount of its interest sensitive (repriceable) liabilities.

Gap = Rate-sensitive Assets –Rate-sensitive Liabilities A gap of zero suggests that rate-sensitive assets equal rate-

sensitive liabilities, so that net interest margin should not be significantly influenced by interest rate fluctuations.

Liability sensitive Interest sensitive Assets - (Negative) gap = Interest sensitive Liabilities < 0

Assets sensitive Interest sensitive Assets - (Positive) gap = Interest sensitive Liabilities >

0

Interest Sensitive ratio = ISA ISL

Duration ManagementA measure of the maturity and value sensitivity of a

financial asset that considers the size and the timing of all its expected cash flows

D = Σ Expected CF in Period t * Period t / (1+ YTM) t

Σ Expected CF in Period t (1+YTM) t

Instead of finding duration of individual asset/liability,

bank and other FI find duration of asset and liability portfolio.

The duration of an asset/liability portfolio is equal to the weighted average duration of individual components in that portfolio.

Example:A bond with $1000 par value offering an 8% coupon

rate with a yield to maturity of 14% and three years left to maturity has a duration of

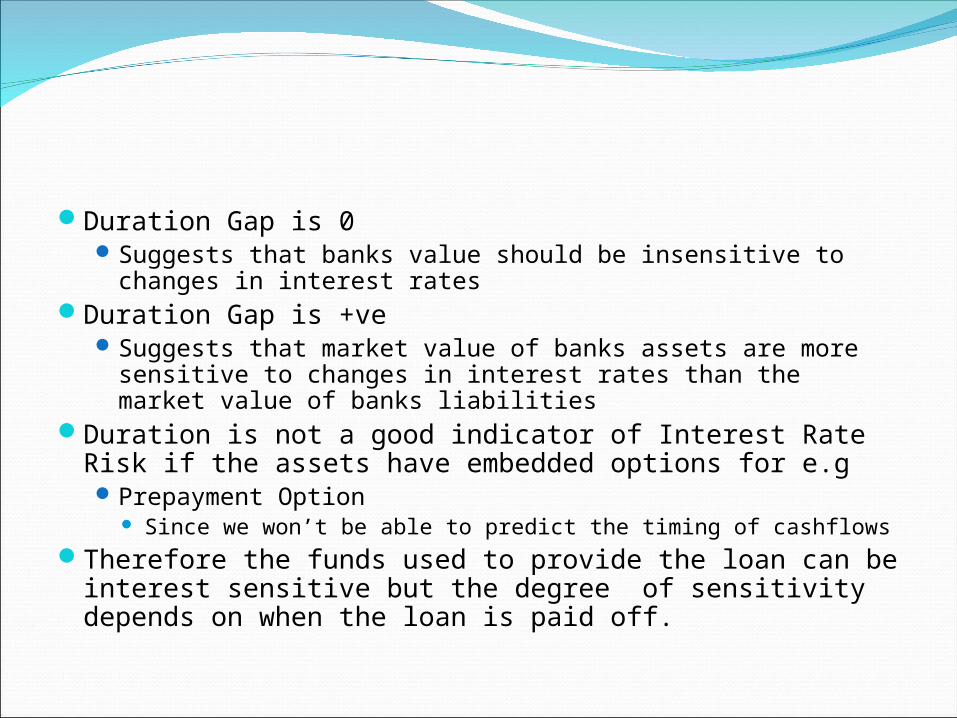

Duration Gap is 0 Suggests that banks value should be insensitive to

changes in interest ratesDuration Gap is +ve

Suggests that market value of banks assets are more sensitive to changes in interest rates than the market value of banks liabilities

Duration is not a good indicator of Interest Rate Risk if the assets have embedded options for e.gPrepayment Option

Since we won’t be able to predict the timing of cashflows Therefore the funds used to provide the loan can be

interest sensitive but the degree of sensitivity depends on when the loan is paid off.

Methods to Reduce interest Rate RiskMaturity matchingUsing floating-rate loansUsing Interest Rate futures contractsUsing interest rate swapsUsing Interest rate caps

Managing Credit Risk The types of loans provided and securities purchased will determine

the overall default risk of the asset portfolio.

If a bank wants to minimize default risk, it can use most of its funds to purchase treasury securities, which are virtually free of default risk.

At the other extreme, a bank concerned with maximizing its return could use most of its funds for consumer and small business loans.

The ideal objective for managing assets is to simultaneously maximize return and minimize default risk, it must compromise. That is, it will select some assets that generate high return but are

subject to relatively high degree of default risk and also some assets that are very safe but offer a lower rate of return.

Over time, economic conditions change and can cause banks to adjust their asset portfolios accordingly. For example, banks generally reduce loans and increase their purchases of low-risk securities during recessionary periods.

Measuring Credit Risk

Determine the CollateralDetermine the Loan Rate

Some loans to high-quality customers are commonly offered at rates below the prime rate. Each bank has its own formula for setting loan rates.

From time to time, the competition among banks for the provision of, loans will change, causing banks to disregard or revise their loan rate formula.

Diversifying Credit RiskApplying Portfolio Theory

We should not consider the risk of a Loan made on a standalone basis rather we should gauge it’s correlation with the bank’s existing asset(Loan) portfolio.

Industry Diversification of LoansBanks should diversify their loans to assure that their

customers are not dependent on a common source of income.

Geographic Diversification of LoansInter national Diversification of Loans

Country Risk Analysis Industry Analysis

Selling LoansRevising Loan Portfolio’s in Response to Economic

Conditions

Managing Market RiskManaging Market Risk in other words means

to Manage their exposure to Systematic Risk or Beta.

Market Risk is usually measured usually using VAR (Value at Risk) methodBanks continually revise their estimates of

market risk in response to changing market conditions.

Interest Rate Risk is the most important component of Market Risk

Operating RiskRisks resulting from banks general business

operationsExchange Rate RiskSettlement Risk

Bank Capital ManagementLike other corporations, banks must determine the level

of capital that they should maintain. Bank operations are distinctly different from other types

of firms, since the majority of their assets generate more predictable cash flows. Thus, banks can use a much higher degree of financial leverage than other types of firms.

Banks must also consider the minimum capital ratio required by regulators. The minimum could possibly force the bank to maintain more capital than what it believes is optimal.

A common measure of the return to the shareholders is the return on equity, measured as

ROE = Net Profit After Taxes

Equity

If banks are holding an excessive amount of capital, they can reduce it by distributing a high percentage of their earnings to share holders. Thus, capital management is related to the

bank’s dividend policy.The argument on the other hand is that:

If the growing bank preferred to provide existing shareholders with a sizable dividend, it would then have to obtain the necessary capital through issuing new stock.

Bank RestructuringExpanding Operations i.e providing new servicesDiversifying their Asset portfolioBoosting their Capital Ratios

Bank AcquisitionA common form of Bank Restructuring is Growth through

AcquisitionsIntegrated Bank Management

That is management of Assets, Liabilities and Capital are integrated

This approach ensures that all bank policies will be inline with the economic forecast’s

The approach is necessary to manage Liquidity Risk, Interest Rate Risk and Credit Risk