Managing Lifetime Wealth: retirement planning in the UK

39

Managing Lifetime Wealth: retirement planning in the UK Charting the course of retirement advice through a global pandemic, market volatility and continued regulatory change

Transcript of Managing Lifetime Wealth: retirement planning in the UK

Managing Lifetime Wealth: retirement planning in the UK

Charting the course of retirement advice through a global pandemic, market volatility and continued regulatory change

Foreword from Aegon

The last year has seen significant challenges as we have adapted to

the ongoing Covid-19 pandemic which has influenced all aspects

of our society and economy. We have become acutely aware of the

health impact of the pandemic but have also begun to understand

its effect on wealth. Financial advisers have been well positioned to

support their clients through this period, transitioning to the new

way of working with remote meetings and the huge acceleration of

digital processes.

Retirement advice continues to be a key driver of adviser business

and demand has been growing in recent years following the

introduction of the pension freedoms and as the UK population

ages. The pandemic has further highlighted the value of personalised

advice in retirement planning with many people reevaluating their

priorities and seeking help to navigate through stock market volatility.

Aegon is delighted to sponsor NextWealth’s comprehensive research for the second year

running. We hope that it will offer valuable insight to advisers and those within the retirement

advice industry to understand the latest views on some of the biggest industry trends.

The global pandemic provides the backdrop to this report and it looks to understand how

advisers have managed their approach through this. This includes the approach to portfolio

construction and recommendations of investment products such as multi-asset funds for

clients in decumulation. The regulatory environment continues to evolve and this report also

brings to light adviser attitudes towards the latest developments, in particular the new rules

for defined benefit transfer advice and investment pathways.

Aegon is committed to providing insight to advisers and their businesses to help support their

clients through the challenges they face. Many of the trends in this report will inform the

development of Aegon’s propositions which seek to provide the tools and solutions advisers

need. We hope you find this report both engaging and informative.

For more adviser focused insights and research please visit the Advice Makes Sense section

of our website:

https://www.aegon.co.uk/advisers/advice-makes-sense.html

Ronnie Taylor,

Chief Distribution Officer at Aegon

2

3

Contents

Introduction 4Methodology 4Executive Summary 51. Retirement Advice and Financial Advice Businesses 71.1 Covid-19 impact on retirement advice 71.2 Importance of retirement advice to financial advice businesses 102. Client Profile 112.1 Average value of retirement portfolios 122.2 Client objectives in retirement 132.3 Clients' hopes and fears 143. Retirement advice and investment approach 163.1 Retirement advice techniques 163.2 Structuring portfolios for retirement income 183.3 Withdrawal strategy 193.4 Taking tax-free cash at retirement 203.5 Impact of investment pathways 214. Investment products used in decumulation 224.1. Investment products used for retirement clients 224.2 DFM model portfolios 254.3 Adviser managed model portfolios 264.4 Use of proprietary multi-asset funds 264.5 Use of ESG funds and solutions 274.6 Use of property funds 285. Defined benefit pension transfer advice 295.1. Firms offering defined benefit transfer advice 295.2. Reasons for ceasing to offer DB transfer advice 305.3. Time taken to complete a DB transfer 315.4. Abridged advice for DB transfers 335.4. Abridged advice for DB transfers 34Conclusion Trends and opportunities ahead 35 Trend: Regulatory focus on value 35Trend: Shift to retirement assets for ongoing fees 35Trend: Simplification of systems and tools 36Opportunity: advice and solutions for clients with lower value portfolios 36Opportunity: Advice to drive behavioural change 36Respondent Profile 37

This report is kindly supported by Aegon and considers the increasingly important and fast-moving topic of retirement advice. There is plenty of evidence to show that helping clients plan for and manage retirement is growing in importance for advisers.

This report provides financial advisers with a benchmark for comparison to help them think through their own retirement advice process and to learn from the practices of other firms. It also offers stakeholders within the retirement advice industry insight into the new challenges facing advisers against the backdrop of the global pandemic, market volatility and a changing regulatory landscape. We publish this report each year and welcome any input for future updates. You can send feedback to [email protected].

Introduction

The report findings are based on quantitative and qualitative inputs:

• Online quantitative survey of 212 financial advisers conducted between 3 and 11 December 2020

• In-depth qualitative interviews with 10 financial advisers, conducted between 3 and 11 December 2020

Methodology

• Comparisons are offered to the January 2020 and July 2018 versions of this report which were also based on in-depth qualitative interviews with financial advisers and quantitative surveys of 227 and 267 financial advisers, respectively.

NB The term financial adviser is used throughout this report to refer to financial advisers and financial planners.

4

5

• Most advisers say client acquisition has been significantly more difficult since the start of the COVID-19 pandemic. Advisers servicing clients with smaller portfolios have felt the pinch most acutely.

• Most advisers say that portfolios have performed as expected through the market volatility of 2020. Nearly half said clients viewed the market fall in early 2020 as a buying opportunity.

58% of adviser assets are for clients receiving retirement advice.

Executive summary

Covid Impact Covid Performance

Importance of retirement advice to financial advice businesses

Client Profile Retirement at a Glance• Financial advisers that have offered defined

benefit (DB) advice have a larger average client portfolio size.

• Among advisers that provide DB transfer advice or have done so in the past, 43% report an average client portfolio size of 250K or more in comparison to 23% for those who have never provided DB transfer advice.

Average advised retirement client has assets of £270,000

Ad

vise

rs

47% AGREE clients saw themarket fall as a buying opportunity

54% ofclients

19% are phasing into retirement

35% of advised clients are fully retired

• Client objectives with retirement savings are most often to use savings to create a sustainable retirement income, followed by passing savings to a loved one. Financial advisers with larger average portfolio sizes are more likely to say that passing on wealth is a priority for the majority of clients.

• Client hopes and fears centre on the ability to maintain their standard of living in retirement. This is followed by concerns about health, running out of money and long-term care costs.

4 in 5 advisers ask clients about meaning,

purpose and happiness

Client objectives, hopes and fears

6

Retirement advice

Investment Proposition

• 58% of adviser assets are for clients receiving retirement advice.• Safe withdrawal rates are in flux as the 4% rule loses ground to modelling

tools

• 56% of advisers say they always or often recommend multi-asset or multi-manager funds to clients in drawdown, up from 36% last year. Growth is expected to continue, with 22% saying they will increase use in the next 3 years.

• Among those using multi-asset funds, 43% always or mainly use proprietary funds – where the firm that manages the money has custody of the assets.

• Smoothed multi-asset funds saw the most significant decline only 15% of financial advisers always or often recommend smoothed funds to clients, down from 23% last year.

• Half of advisers would never use a DFM for bespoke or model portfolios for clients in drawdown. But this may be set to change: 21% expect to increase use of DFM model portfolios in the next three years.

• Most advisers only consider ESG criteria as a result of a client request. Nearly one third say ESG credentials are among the factors considered when selecting managers or funds.

• 42% of advisers use property funds for clients in drawdown. About half of these would continue to use these funds if an FCA proposed notice period were introduced however most of those would use them less.

38% use a modelling tool such as Timeline, up from 28% last year

37% use a fixed rate (typically 4%), down from 41%

23% of clients take less of the tax-free lump sum at retirement, with most of these preferring to take tax-free cash via drip-feed drawdown

Top Investment Approaches to Retirement Income

Total return (39%)

Bucket (31%)

Income driven (25%)

(% Always use/ Use most of the time)

123

Defined Benefit Pension Tranfers• Among firms that have stopped offering defined benefit

(DB) transfer advice, most said the decision to stop was down to business risk or increases to PII premiums and excess.

• 81% of advisers say DB transfers take at least 3 months from the first conversation to completion. Nearly a quarter said it takes longer than 6 months. Two thirds say that transfer times have increased in the past year.

• 60% agree or strongly agree that abridged advice is an effective way to identify clients for whom a transfer is not suitable, up 14% from last year.

• Half of advisers providing DB transfer service offer abridged advice. Just over 30% don’t charge for this and 58% of those who charge levy a fee of less than £1,000.

% of advisers offering DB advice is declining

Defined Benefit Advice

-37

%

-46

%

56%

2018 2020 2021

41%

22%

An ageing population, the introduction of Pension Freedom and increasing complexity of managing retirement income has driven up demand for financial advice and is having an impact on the structure and focus of financial advice businesses. These changes continue to permeate the industry as we work through the implications of an ongoing global pandemic. In this section we explore the impact of the Covid-19 pandemic on retirement advice and the growing importance of retirement advice to financial advice businesses.

The global pandemic has changed the way we work and live. It has affected financial advice business growth and client behaviour. Advisers report that the pandemic’s biggest business impact has been on new client acquisition: 56% agreed that acquiring customers under current conditions has been significantly harder.

• The challenge of acquiring customers has been felt most acutely among advisers servicing clients with smaller portfolios. 59% of those with an average client portfolio size of less than £250k said client acquisition has been significantly more difficult under current conditions. The same is true for only half of advisers working with clients with an average portfolio size of more than £250k.

• There was some thought that the global pandemic, a rise in redundancies and an increased awareness of our own mortality might lead to an increase in demand for financial advice and retirement advice more specifically. While there was some disagreement, a net 27% of advisers told us they have seen demand for retirement advice increase. Advisers from larger firms measured by number of advisers and assets were more likely to say that they’ve seen no increase in demand, but, overall, demand for retirement advice has increased across firms of all sizes.

1. Retirement advice and financial advice businesses

1.1 Covid-19 impact on retirement advice

7

Figure 5: Covid-19 impact on business

17 %

7 %

5 %

6 %

40 %

48 %

38 %

34 %

21 %

38 %

35 %

47 %

21 %

7 %

18 %

12 %

1 %

3 %

1 %

Acquiring new clients issignificantly harder under

current conditions

Clients are now morefocused on their health and

longevity

Our business has been moreproductive because of

travel/meeting restrictions

We have seen demand forretirement advice increase

Strongly agree Agree Neither agree nor disagree

Disagree Strongly disagree Unsure

Net Agree(% Agree - %

Disagree)

33%

48%

21%

27%

Figure 6: Covid-19 impact on retirement investments

We also asked about the impact of Covid-19 on retirement investment portfolios. Figure 6 illustrates that, for the most part, portfolios have performed as expected. Nearly half of advisers also told us that clients viewed the market fall early in 2020 as a buying opportunity. Few have changed their investment strategy for clients in retirement as a result

of the pandemic and subsequent market shifts. While portfolios performed as expected, some advisers did encourage retired clients to draw income from cash reserves (or buffers) rather than sell when markets were down. One third of advisers said they advised clients to reduce or stop taking income from investments.

15%

3 %

5 %

6 %

2 %

75 %

44 %

36 %

28 %

22 %

6 %

7 %

39 %

23 %

29 %

27 %

35 %

12 %

26 %

29 %

36 %

44 %

9 %

8 %

13 %

15 %

The portfolios we use for retirementhave generally performed in line with

expectations

Clients have seen the market fall as abuying opportunity and invested new

cash

Illiquid holdings (e.g. property funds)have caused issues for retired clients

We have advised clients to reduce orstop taking income from investments

for the time being

We have delayed rebalancing clientportfolios because of market

volatility

We have fundamentally changed ourinvestment strategy for clients in

retirement

Strongly agree Agree Neither agree nor disagree

Disagree Strongly disagree UnsureNet Agree

(% Agree - % Disagree)

88%

34%

5%

-3%

-25%

-53%

8

Our in-depth interviews with financial advisers confirm that the pandemic has led some clients to reassess priorities and lifestyle. Early retirement was a common theme but so too was the desire to move out of urban centres.

“We’ve had a few people who have decided to retire early or have taken redundancy. People’s circumstances changed. Some changing thoughts on lifestyle. People not want-ing to live in city/London anymore. Looking at spending more time in rural areas.”

“A good extra 10% to 15% of clients are moving into retirement either early, having been made redundant or losing employment because they’ve had to close their company. So it’s a definite move this year. I’m hoping it will reverse but it’s noticeable at the moment that that’s what we’re doing”

Our interviewees also told us that things that were once theoretical became true in practice.

“The main thing about Covid-19 is that we’ve got some actual market volatility, that’s making people think a little bit more about it. Sequencing risk, that was this thing that was a conceptual thing that’s never happened, that suddenly happened.”

“For clients who have given me a hard time about holding a cash buffer, they finally did what I told them they’d do – they took cash rather than selling. The plan worked!”

9

One adviser also told us that clients started taking out less money, not because of market shifts but because they didn’t need the money:

Many of the changes brought on by Covid-19 should pass as we return to some form of business as usual. What is certain is that advisers have found that the tools they use to illustrate portfolios and to analyse scenarios have become more valuable than ever. We explore the use of tools in section 3.

“Our investment approach is a long-term investment approach. We recognise volatility and the impact of sequencing risk and all that stuff. But we manage that through cash. So we take a view on when to top up the cash accounts, if you like, but their income doesn’t come directly out of the markets. So therefore we can afford to ride it out. You saw this year, back in Springtime, we wouldn’t want to be drawing down money at that point, but we would never be drawing down anyway. At that stage, we would always have a cash balance. So it’s not changed our thinking directly at all.”

“Some clients have actually stopped taking income or reducing the income, because they weren’t spending any money, because they weren’t going anywhere.”

Our survey reveals that 58% of advised assets are for retirement clients. Financial advisers have lowered their projections for the speed of the shift of assets to retirement. Three years ago, advisers said that 53% of their assets were for clients receiving retirement advice and they projected that to grow to 60% in three years – representing a 13% change. Roll forward three years and advisers say that the increase will only be 9%, from 58% to 63%.

10

1.2 Importance of retirement advice to financial advice businesses

• 69% of advisers said that at least half of their assets are for clients seeking retirement advice. 5% said that all of their assets are for retirement advice.

• The most common single response was 70%, followed closely by 75%. Each was selected by only 7% and 6% of advisers, further illustrating the spread of responses.

Table 1: Average share of assets for clients receiving retirement advice

Figure 7: Looking ahead three years: Assets under advice, per adviser

Average adviser assets for clients receiving

retirement advice

Projection three years ahead – average adviser assets for clients

receiving retirement advice

Expected percentage

change

2021 58% 63% 9%

2020 60% 66% 10%

2018 53% 60% 13%

0 %

1 %

2 %

3 %

4 %

5 %

6 %

7 %

8 %

9 %

10 %

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2018 2020 2021

While the average is 58%, there was a wide variety in the share of assets forecast to be for clients in retirement, as illustrated in Figure 7.

On average, 58% of adviser assets are for

clients receiving retirement advice

Pension Freedom, and the associated changes to the inheritance tax treatment of pension savings, have fundamentally changed how retirement savings are used. On top of this, changes in working patterns have also affected what income people need in retirement and when they need it. More and more people are working beyond traditional retirement ages. No doubt part of this is driven by an increasing State Pension Age, but the idea that work stops at 60 or 65 has become increasingly alien.

However, employment rates in those over age 65 dipped significantly during 2020 as the pandemic took hold. Employment in this age group fell by nearly 12% between March and June 2020 compared to less than 1% for those aged 16 to 64, although this has recovered somewhat since then.

The very concept of retirement being a point in time when people move from full-time employment to not working at all is changing. Increasingly, whether by necessity or desire, retirement has become more of a transition period when people move from full-time to part-time employment before stopping work altogether. As figure 9 shows, those at older ages who are employed are more likely to have part-time employment and, interestingly, many of these will be part-time self-employed.

2. Client profile

11

Figure 8: Employment rate for those aged 65 and above

Source: ONS Labour Force Survey

This change to retirement being a transitionary period is reflected in the profile of advised clients as shown in Figure 10.

Figure 9: Employment type by single year of age

68697071727374

02 03 06 0

Full-Time Employee

75+

Full-Time Self-Employe d

10 40 50 70 10080 90

6061626364656667

5253545556575859

4445464748495051

3637383940414243

2829303132333435

2021222324252627

16171819

Ag

e

Proportion in employment

Part-Time Employee Part-Time Self-Employed

Other

Source: “Independent Review of the State Pension Age, Smoothing the Transition”, Cridland 2017. Contains public sector information licensed under the Open Government Licence v3.0.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Apr-92

Apr-93

Apr-94

Apr-95

Apr-96

Apr-97

Apr-98

Apr-99

Apr-00

Apr-01

Apr-02

Apr-03

Apr-04

Apr-05

Apr-06

Apr-07

Apr-08

Apr-09

Apr-10

Apr-11

Apr-12

Apr-13

Apr-14

Apr-15

Apr-16

Apr-17

Apr-18

Apr-19

Apr-20

Em

plo

ymen

t ra

te (%

)

Taken together, Pension Freedom and changing working patterns mean that retirement advice has become even more valu-able but also more complex. In particular, managing income sources to minimise the level of income tax paid will be crucial for those still earning. As we see later, the use of drip-feed drawdown is a big driver behind clients not taking the full cash lump sum at retirement. Using this approach, advisers can help clients achieve their overall desired income without paying too much income tax by using the tax-free lump sum to fund income while earning and deferring taxable pension income payments to a time where clients are no longer earning.

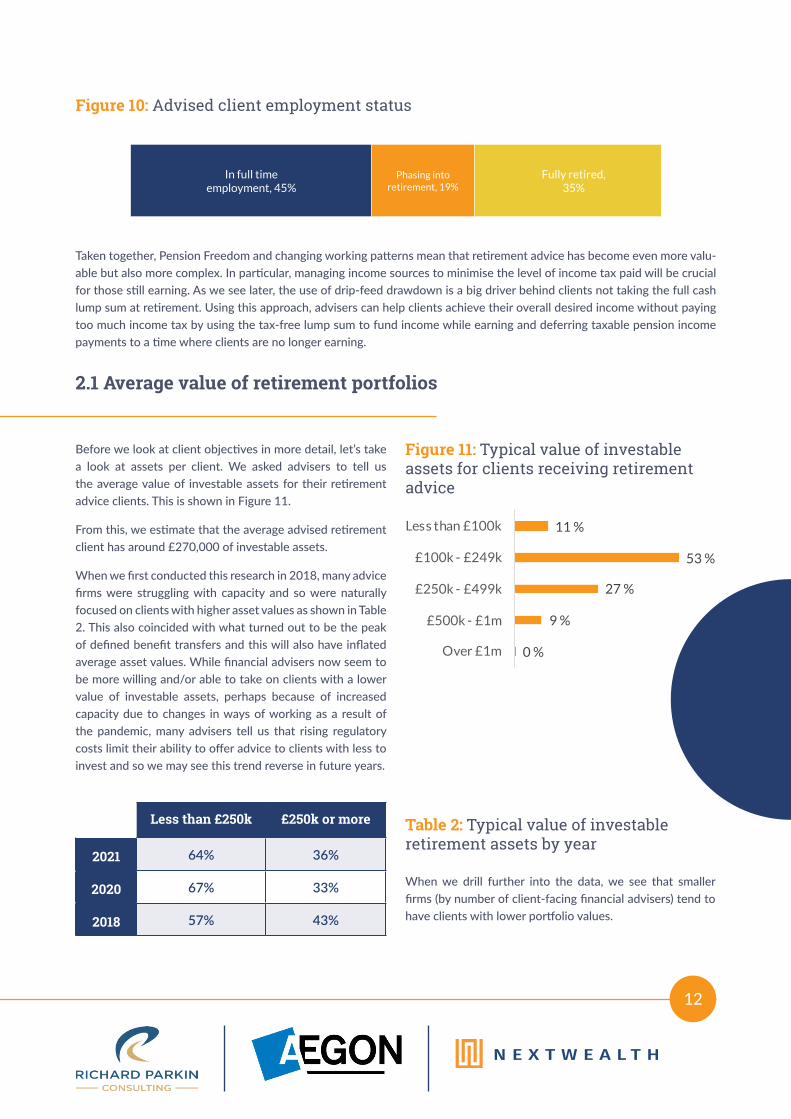

Figure 10: Advised client employment status

12

In full time employment, 45%

Phasing into retirement, 19%

Fully retired, 35%

Table 2: Typical value of investable retirement assets by year

Less than £250k £250k or more

2021 64% 36%

2020 67% 33%

2018 57% 43%

Before we look at client objectives in more detail, let’s take a look at assets per client. We asked advisers to tell us the average value of investable assets for their retirement advice clients. This is shown in Figure 11.

From this, we estimate that the average advised retirement client has around £270,000 of investable assets.

When we first conducted this research in 2018, many advice firms were struggling with capacity and so were naturally focused on clients with higher asset values as shown in Table 2. This also coincided with what turned out to be the peak of defined benefit transfers and this will also have inflated average asset values. While financial advisers now seem to be more willing and/or able to take on clients with a lower value of investable assets, perhaps because of increased capacity due to changes in ways of working as a result of the pandemic, many advisers tell us that rising regulatory costs limit their ability to offer advice to clients with less to invest and so we may see this trend reverse in future years.

When we drill further into the data, we see that smaller firms (by number of client-facing financial advisers) tend to have clients with lower portfolio values.

2.1 Average value of retirement portfolios

Figure 11: Typical value of investable assets for clients receiving retirement advice

11 %

53 %

27 %

9 %

0 %

Less than £100k

£100k - £249k

£250k - £499k

£500k - £1m

Over £1m

13

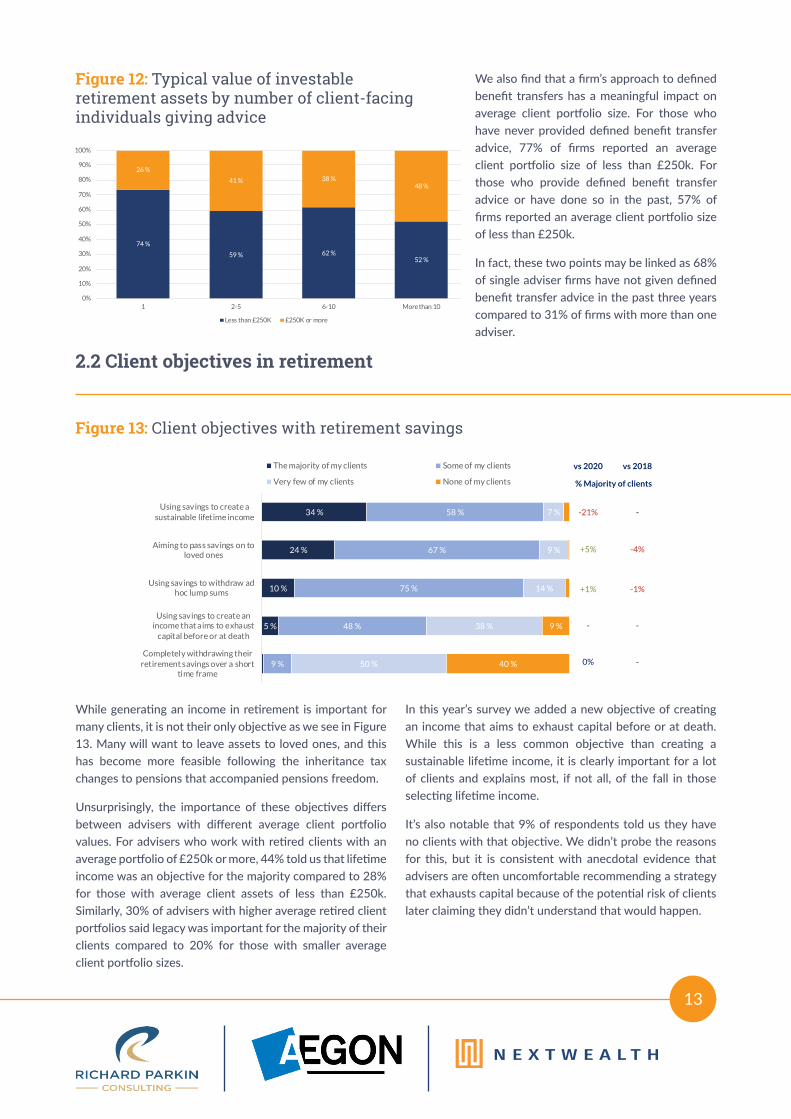

Figure 12: Typical value of investable retirement assets by number of client-facing individuals giving advice

Figure 13: Client objectives with retirement savings

We also find that a firm’s approach to defined benefit transfers has a meaningful impact on average client portfolio size. For those who have never provided defined benefit transfer advice, 77% of firms reported an average client portfolio size of less than £250k. For those who provide defined benefit transfer advice or have done so in the past, 57% of firms reported an average client portfolio size of less than £250k.

In fact, these two points may be linked as 68% of single adviser firms have not given defined benefit transfer advice in the past three years compared to 31% of firms with more than one adviser.

74 %

59 % 62 %52 %

26 %

41 % 38 %48 %

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 2-5 6-10 More than 10

Less than £250K £250K or more

2.2 Client objectives in retirement

While generating an income in retirement is important for many clients, it is not their only objective as we see in Figure 13. Many will want to leave assets to loved ones, and this has become more feasible following the inheritance tax changes to pensions that accompanied pensions freedom.

Unsurprisingly, the importance of these objectives differs between advisers with different average client portfolio values. For advisers who work with retired clients with an average portfolio of £250k or more, 44% told us that lifetime income was an objective for the majority compared to 28% for those with average client assets of less than £250k. Similarly, 30% of advisers with higher average retired client portfolios said legacy was important for the majority of their clients compared to 20% for those with smaller average client portfolio sizes.

In this year’s survey we added a new objective of creating an income that aims to exhaust capital before or at death. While this is a less common objective than creating a sustainable lifetime income, it is clearly important for a lot of clients and explains most, if not all, of the fall in those selecting lifetime income.

It’s also notable that 9% of respondents told us they have no clients with that objective. We didn’t probe the reasons for this, but it is consistent with anecdotal evidence that advisers are often uncomfortable recommending a strategy that exhausts capital because of the potential risk of clients later claiming they didn’t understand that would happen.

34 %

24 %

10 %

5 %

58 %

67 %

75 %

48 %

9 %

7 %

9 %

14 %

38 %

50 %

9 %

40 %

Using savings to create asustainable lifetime income

Aiming to pass savings on toloved ones

Using savings to withdraw adhoc lump sums

Using savings to create anincome that aims to exhaust

capital before or at death

Completely withdrawing theirretirement savings over a short

time frame

The majority of my clients Some of my clients

Very few of my clients None of my clients

vs 2020 vs 2018

% Majority of clients

-21% -

+5% -4%

+1% -1%

- -

0% -

When we talk to those advising retirement clients, we often hear that the adviser’s job extends beyond just dealing with financial matters to providing coaching on life after work.

Many advisers see these discussions as a useful way of understanding a client’s financial priorities to help them realise hopes and mitigate fears.

Figure 14: Advisers ask clients about meaning, purpose and happiness

14

2.3 Clients' hopes and fears

How?

24% Open conversation

16% What does retirement look like?

13% What is the money for?/ Priorities and goals

12% Open questions

6% Fact Find

5% Questionnaire to guide discussion/ specific questions

“From an investment proposition, retirement proposition, at a technical level, a governance level, I think that's largely done. But what can we do at a human level to have an impact on people's lives, help them make better decisions and stop them making bad ones? Connect more with what they really want to do rather than do the same as everyone else; that means we can be far more effective and open and hopefully help them be even happier.”

Yes, 78 %

No, 22 %

Generally, these hopes and fears seem to be consistent across clients of all advised firms with some interesting exceptions. 52% of the advisers with higher value retirement clients (£250k or more of investable assets) reported that the majority of their clients are seeking to maintain living standards in retirement compared to 31% of advisers with average client assets below £250k. Conversely, paying off debt was more important for clients of advisers with lower average retirement client portfolios.

As one might expect, advisers with wealthier clients had fewer clients who are concerned about running out of money, but one might also expect they would be less inclined to think about downsizing. However, we saw little evidence of this: a relative lack of interest in downsizing or releasing housing equity was reasonably consistent across all respondents.

Going forward, we expect that the role of the financial adviser will extend further into “retirement coaching” and become less focused on just dealing with products and investments. Indeed, a number of firms are already centralising their advice processes with field advisers concentrating on understanding the client needs and providing more holistic retirement support. Advisers will, of course, aim to help clients achieve their objectives, but it will be as important, if not more so, to improve their clients’ financial wellbeing. That is, to help their clients feel confident in their relationship with money and to feel that they have control over their financial future.

We note the burgeoning focus on financial wellbeing from financial planners who want to help clients achieve their goals, not just maximise the value of the portfolio. Aegon are proud supporters of the Initiative for Financial Wellbeing (IFW). For more information on the IFW, visit https://initiativeforfinancialwellbeing.org.uk/.

Figure 15: Client hopes and fears in retirement

15

39 %

12 %

12 %

11 %

10 %

4 %

43 %

61 %

57 %

63 %

56 %

48 %

41 %

37 %

50 %

36 %

17 %

26 %

28 %

23 %

28 %

42 %

50 %

54 %

44 %

56 %

1 %

3 %

4 %

6 %

6 %

8 %

8 %

6 %

8 %

Expect to maintain the same standard ofliving in retirement as before retirement

Are concerned about their health andlongevity or that of their loved ones

Are worried about running out of moneybefore they die

Are concerned about long-term care andcosts

Are planning to travel and/or live overseas

Are concerned about replacing the socialaspects of work

Intend to use retirement lump sums toclear outstanding debt

Are daunted by the prospect of life afterwork

Are considering downsizing or releasingequity from property

Intend to find part-time employmentand/or start a business in retirement

The majority of my clients Some of my clientsVery few of my clients None of my clients

There is no doubt that advising clients in retirement presents a different set of challenges from advising them in accumulation. In particular, client objectives in retirement, such as required income or legacy, while more complex, may be easier to articulate precisely than objectives in accumulation which may simply focus on maximising wealth within certain risk constraints.

Arguably, it may be more appropriate to consider risk in terms of the likelihood of meeting those objectives, and the potential shortfall if the objective is not met, rather

than focusing on investment volatility as is often the case in accumulation. Cash flow modelling is likely to be an important tool to support the definition and development of those objectives.

The following chart shows various techniques used in delivering retirement advice. We asked advisers not just about their current use but, for those not using them today, whether they are likely to use them in the future.

Overall, use of these techniques is broadly consistent with what we reported in last year’s research. We would have expected to see more firms adopting cash flow modelling, scenario analysis and different sets of portfolios for retirement based on intentions stated in last year’s report, where around 10% of firms said they were likely to adopt these techniques over the next twelve months.

3. Retirement advice and investment approach

16

Figure 16: Techniques used to manage retirement income

3.1 Retirement advice techniques

44 %

51 %

34 %

41 %

31 %

6 %

19 %

12 %

11 %

9 %

9 %

11 %

9 %

11 %

6 %

22 %

11 %

19 %

24 %

18 %

20 %

7 %

25 %

13 %

35 %

Specific attitude to risk (ATR)questionnaire for retirement

clients

Cash flow modelling to estimate a client’s income needs year on

year

Specific set of fundchoices/portfolios for retirement

clients

Scenario analysis to assesspossible outcomes for different

market conditions

Different platforms/providers fordrawdown than accumulation

Have used this for 12 months or more Have introduced this in the past 12 months

Intend to use in the next 12 months May use in the future (more than 12 months away)

Do not intend to use

Make use

2021 vs 2020

50% -10%

71% +1%

47% -1%

52% No change

40% No change

17

Figure 17: Current use of retirement advice techniques by firm AuA

While there will inevitably be differences due to sampling from year to year, we conclude that there seems to have been limited development of retirement advice approaches over the past twelve months. This conclusion is consistent with what we hear from advisers directly. The business issues of dealing with the Covid-19 pandemic, and the challenges of volatile investment markets, have meant that innovation has been focused elsewhere.

It is interesting that the proportion of advisers who say they have no intention of adopting these techniques is virtually identical to last year’s survey. This further supports the idea that adviser attitudes to these techniques hasn’t changed significantly but that implementation has slowed.

There are some interesting variations in the use of these techniques across adviser firms as we see in Figure 17.

The most striking difference is in the use of a different Attitude to Risk (ATR) approach for retired clients. We see that larger firms are almost half as likely to use this than smaller firms. It’s not wholly clear why this should be the case though, in previous reports, we have found that larger firms sometimes find it more difficult to implement a consistent approach to advice across their business than smaller firms. The chart also suggests that larger firms are more likely to use cash flow modelling than smaller firms and are significantly more likely to use scenario analysis.

58 %64 %

45 %40 %

43 %

50 %

76 %

50 %

64 %

31 %30 %

77 %

45 %

59 %

48 %

Specific attitude to risk (ATR)questionnaire for retirement

clients

Cash flow modelling to estimate a client’s income

needs year on year

Specific set of fundchoices/portfolios for

retirement clients

Scenario analysis to assesspossible outcomes for

different market conditions

Different platforms/providersfor drawdown than

accumulation

Less than £50m £50m - £249m £250m or more

“There are advisers across the industry who are massively into cash flow, as the answer to everything. But in the main, most people use it because they think they have to justify an outcome rather than because they actually think it adds value to the outcome.”

It is interesting to note that over half of firms still use the same portfolios for retirement as they do for accumulation. There has been a lot of discussion of sequencing risk over recent years. However, investment markets have been relatively benign since Pension Freedom was introduced, delivering attractive returns with historically low volatility, at least until the pandemic hit. This may have contributed to firms not feeling they need to think very differently

about retirement investing, though we noted in last year’s report that there is extensive use of cash buffers for clients taking income which will have helped manage the impact of volatile markets. It will be interesting to see whether recent volatility and future market uncertainty lead more firms to think again about how they approach investing for clients seeking retirement advice.

As in previous years, we asked advisers how they approach investing for clients who are looking to take a regular income. The three main approaches to this are:• Total return approach – invest for total return with income payments funded by selling investments

• “Bucket” or time segmentation approach – dividing account into short, medium and long-term components to match future income needs

• Income-driven approach – income payments made from income paid on investments and perhaps topped-up by selling investments

The chart below details the extent to which our respondents use each approach.

Figure 18: Approach to structuring investment portfolios for retirement income

18

3.2 Structuring portfolios for retirement income

As in previous years, the total return approach remains most popular. This is consistent with the finding that most advisers use the same funds and portfolios for retirement as they do for accumulation since, generally, accumulation portfolios will be built on a total return basis.

What is notable though is that most advisers don’t just use a single approach and this pluralism seems to be increasing, albeit slowly. However, income-driven strategies are waning in popularity overall with 26% of advisers saying they never use them, up from 17% last year. Many advisers tell us that it’s not possible to meet client income expectations solely from natural investment income and so tend to discount

the income-oriented approach. No doubt this argument has become stronger given the impact of the pandemic on dividend payments and interest rates.

Our discussions with advisers also tell us that many are attracted to the “bucket” approach but find it difficult to implement. In particular, understanding when and how to rebalance between buckets is a challenge. Certainly, simply rebalancing on a regular basis undermines the main principle that underlies this approach which is to avoid having to realise assets at depressed market prices.

12 %

7 %

2 %

26 %

24 %

23 %

50 %

51 %

49 %

12 %

18 %

26 %

Total return approach

“Bucket” approach

Income-driven approach

Always use Use most of the time Sometimes use Never use

% Always use/ Use most of the time

2021 vs 2020 vs 2018

39% -9% -5%

31% -3% -2%

25% -3% -8%

19

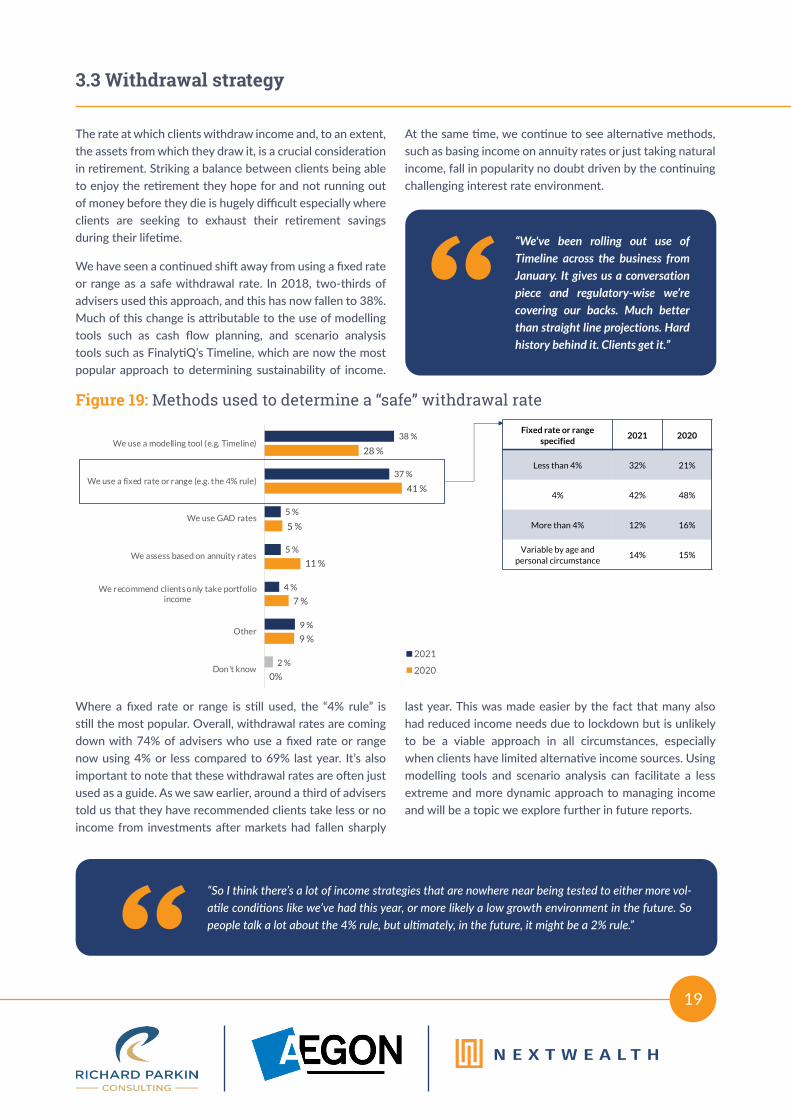

The rate at which clients withdraw income and, to an extent, the assets from which they draw it, is a crucial consideration in retirement. Striking a balance between clients being able to enjoy the retirement they hope for and not running out of money before they die is hugely difficult especially where clients are seeking to exhaust their retirement savings during their lifetime.

We have seen a continued shift away from using a fixed rate or range as a safe withdrawal rate. In 2018, two-thirds of advisers used this approach, and this has now fallen to 38%. Much of this change is attributable to the use of modelling tools such as cash flow planning, and scenario analysis tools such as FinalytiQ’s Timeline, which are now the most popular approach to determining sustainability of income.

At the same time, we continue to see alternative methods, such as basing income on annuity rates or just taking natural income, fall in popularity no doubt driven by the continuing challenging interest rate environment.

3.3 Withdrawal strategy

“We've been rolling out use of Timeline across the business from January. It gives us a conversation piece and regulatory-wise we’re covering our backs. Much better than straight line projections. Hard history behind it. Clients get it.”

Where a fixed rate or range is still used, the “4% rule” is still the most popular. Overall, withdrawal rates are coming down with 74% of advisers who use a fixed rate or range now using 4% or less compared to 69% last year. It’s also important to note that these withdrawal rates are often just used as a guide. As we saw earlier, around a third of advisers told us that they have recommended clients take less or no income from investments after markets had fallen sharply

last year. This was made easier by the fact that many also had reduced income needs due to lockdown but is unlikely to be a viable approach in all circumstances, especially when clients have limited alternative income sources. Using modelling tools and scenario analysis can facilitate a less extreme and more dynamic approach to managing income and will be a topic we explore further in future reports.

Figure 19: Methods used to determine a “safe” withdrawal rate

“So I think there’s a lot of income strategies that are nowhere near being tested to either more vol-atile conditions like we’ve had this year, or more likely a low growth environment in the future. So people talk a lot about the 4% rule, but ultimately, in the future, it might be a 2% rule.”

38 %

37 %

5 %

5 %

4 %

9 %

2 %

28 %

41 %

5 %

11 %

7 %

9 %

0%

We use a modelling tool (e.g. Timeline)

We use a fixed rate or range (e.g. the 4% rule)

We use GAD rates

We assess based on annuity rates

We recommend clients only take portfolioincome

Other

Don't know

2021

2020

Fixed rate or range specified

2021 2020

Less than 4% 32% 21%

4% 42% 48%

More than 4% 12% 16%

Variable by age and personal circumstance

14% 15%

The concept of phased drawdown, where clients crystallise their retirement savings in stages, has been around for many years. Pension Freedom allows even greater flexibility so that, subject to having sufficient tax-free cash entitlement, income withdrawals can be structured as a mixture of tax-free cash and taxable income in whatever proportion best suits the client’s tax position.

We asked advisers the extent to which, over the past three years, clients have taken the tax-free lump sum at retirement.

Overall, the position is mixed with 23% of advisers saying fewer clients had been taking the tax-free lump sum at retirement with the same proportion saying more had taken it. Where advisers told us fewer clients were taking the lump-sum at retirement the reasons for this are shown in Figure 21.

Using drip-feed drawdown is the biggest reason for this. By taking the tax-free cash in stages, advisers can ensure clients’ total income tax liability is minimised, perhaps by keeping overall taxable income payments within personal income tax allowances or within the basic rate tax band.

Another benefit of deferring taking all the lump sum at retirement is that it can continue to grow and so provide a higher value of tax-free cash later in retirement. Another reasons given for not taking the full amount were that clients didn’t need the money. Also, as discussed earlier, many clients are choosing not to access pension savings until other retirement savings have been exhausted thereby reducing the value of their assets that are subject to inheritance tax on death.

Significantly: 7%

Slightly: 16%

54%

Slightly: 21%

MO

RE: 23%LESS: 2

3%

NO CHANGE

Figure 20: Proportion of clients taking tax-free lump sum at retirement

Figure 21: Reasons for clients taking less tax-free cash at retirement (n=48)

20

3.4 Taking tax-free cash at retirement

42 %

79 %

10 %

2 %

Ensuring the majority of their pension iskept invested with potential for growth

Increased use of drip feed drawdown tomeet income requirement while

minimising tax bills

Other

Don’t know/ prefer not to say

The FCA’s Retirement Outcomes Review introduced several new requirements for drawdown clients who choose not to take advice when first accessing their pension benefits. One of the most significant requirements is that non-advised clients going into drawdown should be presented with a choice of investment pathways. On taking tax-free cash, non-advised clients are asked about their intentions for using the remaining drawdown funds. The options they can choose from are:

• Option 1: I have no plans to touch my money in the next 5 years

• Option 2: I plan to use my money to set up a guaranteed income (annuity) within the next 5 years

• Option 3: I plan to start taking my money as a long-term income within the next 5 years

• Option 4: I plan to take out all my money within the next 5 years

The provider will then present the client with a fund per option which is designed to meet that objective. The individual then decides whether to invest in a pathway, make a different choice or stay invested where they are. While the FCA has not set out what the underlying investment options should be, a typical approach would be:

• Option 1: A growth-oriented fund

• Option 2: A fixed interest fund that aims to track changes in annuity prices

• Option 3: A cautious multi-asset or multi-asset income fund

• Option 4: A cash fund

Investment pathways were due to be introduced in August 2020, but their introduction was deferred until 1 February 2021 although a number of providers launched their solutions ahead of this. The original motivations for investment pathways were to avoid clients being defaulted into cash and to encourage them to think about how they might use the remaining funds. However, some see investment pathways as formalising a non-advised

guidance approach and suggest that they could result in fewer clients seeking advice on how to invest drawdown pension assets. Although a very recent innovation, we were keen to understand the extent to which advisers agreed with this assessment.

Overall, advisers appear relatively relaxed with few believing investment pathways will have a significant negative impact on the demand for advice. Those with lower average client values (less than £250k) see investment pathways as more of a threat with 39% of these advisers saying that investment pathways will reduce demand compared to 22% of advisers with average client investable wealth of £250k or more.

Moreover, some advisers believe that investment pathways will increase demand for advice. The rationale for this is that going through the pathways process will alert clients to the fact that decisions need to be made on future retirement plans, and this will spur them to seek advice to help understand their options in more detail.

21

3.5 Impact of investment pathways

Figure 22: Effect of investment pathways on the demand for retirement advice

1 %

32 %

44 %

11 %

13 %

It will reduce demand significantly

It will reduce demand a little

It will have no effect

It will increase the demand forretirement advice

Unsure

Reduced: 33%

22

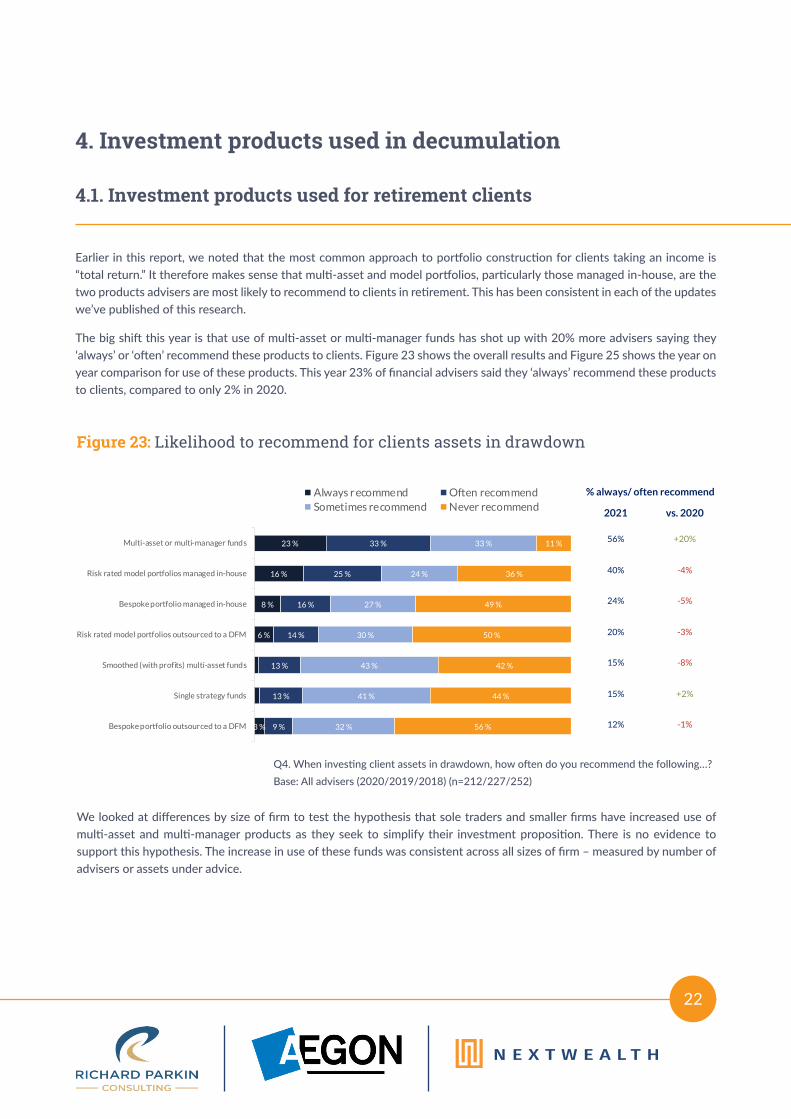

Earlier in this report, we noted that the most common approach to portfolio construction for clients taking an income is “total return.” It therefore makes sense that multi-asset and model portfolios, particularly those managed in-house, are the two products advisers are most likely to recommend to clients in retirement. This has been consistent in each of the updates we’ve published of this research.

The big shift this year is that use of multi-asset or multi-manager funds has shot up with 20% more advisers saying they ‘always’ or ‘often’ recommend these products to clients. Figure 23 shows the overall results and Figure 25 shows the year on year comparison for use of these products. This year 23% of financial advisers said they ‘always’ recommend these products to clients, compared to only 2% in 2020.

4. Investment products used in decumulation

4.1. Investment products used for retirement clients

We looked at differences by size of firm to test the hypothesis that sole traders and smaller firms have increased use of multi-asset and multi-manager products as they seek to simplify their investment proposition. There is no evidence to support this hypothesis. The increase in use of these funds was consistent across all sizes of firm – measured by number of advisers or assets under advice.

Figure 23: Likelihood to recommend for clients assets in drawdown

% always/ often recommend

2021 vs. 2020

56% +20%

40% -4%

24% -5%

20% -3%

15% -8%

15% +2%

12% -1%

23%

16%

8%

6%

33%

25%

16%

14%

13%

13%

9%

33%

24%

27%

30%

41%

43%

32%

11%

36%

49%

50%

44%

42%

56%

Multi-asset or multi-manager funds

Risk rated model portfolios managed in-house

Bespoke portfolio managed in-house

Risk rated model portfolios outsourced to a DFM

Single strategy funds

Smoothed (with profits) multi-asset funds

Bespoke portfolio outsourced to a DFM

Always r ecommend Often recommendSometimes recommend Never recommend

23 %

16 %

8 %

6 %

3 %

33 %

25 %

16 %

14 %

13 %

13 %

9 %

33 %

24 %

27 %

30 %

43 %

41 %

32 %

11 %

36 %

49 %

50 %

42 %

44 %

56 %

Multi-asset or multi-manager funds

Risk rated model portfolios managed in-house

Bespoke portfolio managed in-house

Risk rated model portfolios outsourced to a DFM

Smoothed (with profits) multi-asset funds

Single strategy funds

Bespoke portfolio outsourced to a DFM

Always recommend Often recommendSometimes recommend Never recommend

% always/ often recommend

2021 vs. 2020

56% +20%

40% -4%

24% -5%

20% -3%

15% -8%

15% +2%

12% -1%

Q4. When investing client assets in drawdown, how often do you recommend the following…? Base: All advisers (2020/2019/2018) (n=212/227/252)

Figure 24: Likelihood to recommend for clients assets in drawdown in 3 years

7%

18%

11%

8%

14%

6%

7%

13%

73%

75%

78%

71%

75%

76%

70%

5%

6%

8%

4%

10%

9%

8%

8%

6%

6%

Multi-asset or multi-manager funds

Risk rated model portfolios managed in-house

Bespoke portfolio managed in-house

Risk rated model portfolios outsourced to a DFM

Single strategy funds

Smoothed (with profits) multi-asset funds

Bespoke portfolio outsourced to a DFM

Increase significantly Increase a little Remain the sameDecrease a little Decrease significantly

% increase significantly/little

2021 vs. 2020

22% +8%

9% -15%

14% +1%

9% +1%

21% +2%

6% 0%

16% +1%

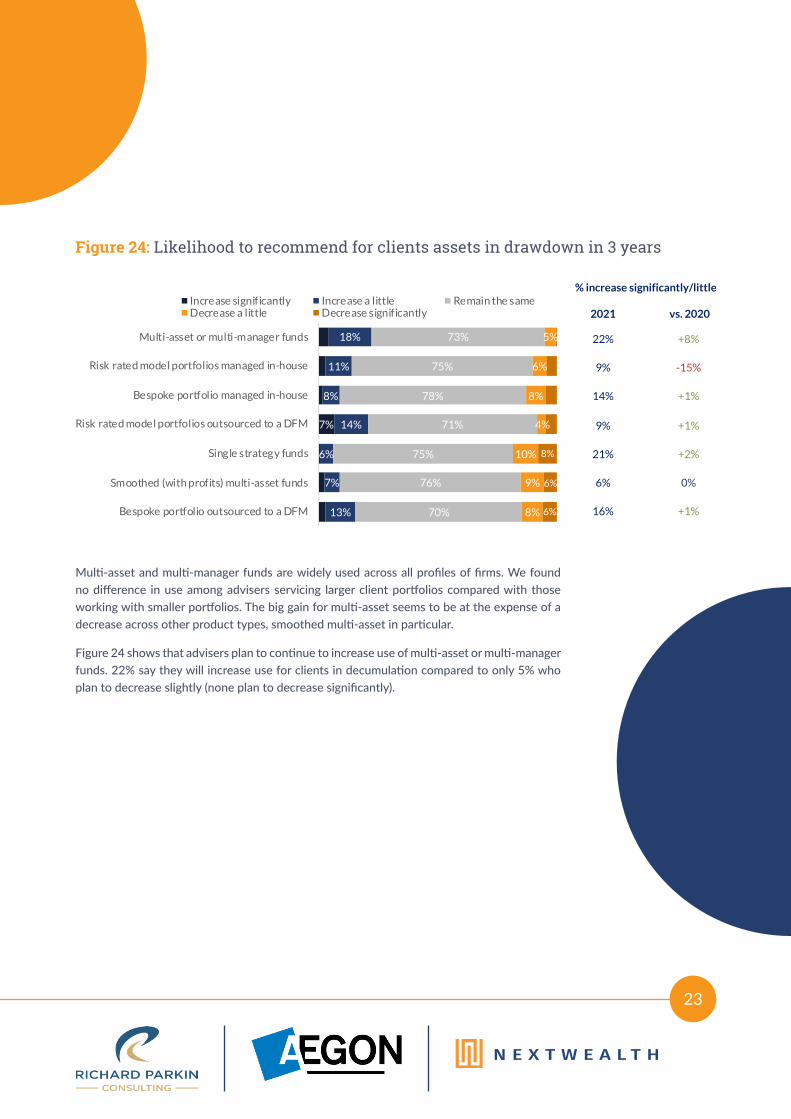

Multi-asset and multi-manager funds are widely used across all profiles of firms. We found no difference in use among advisers servicing larger client portfolios compared with those working with smaller portfolios. The big gain for multi-asset seems to be at the expense of a decrease across other product types, smoothed multi-asset in particular.

Figure 24 shows that advisers plan to continue to increase use of multi-asset or multi-manager funds. 22% say they will increase use for clients in decumulation compared to only 5% who plan to decrease slightly (none plan to decrease significantly).

23

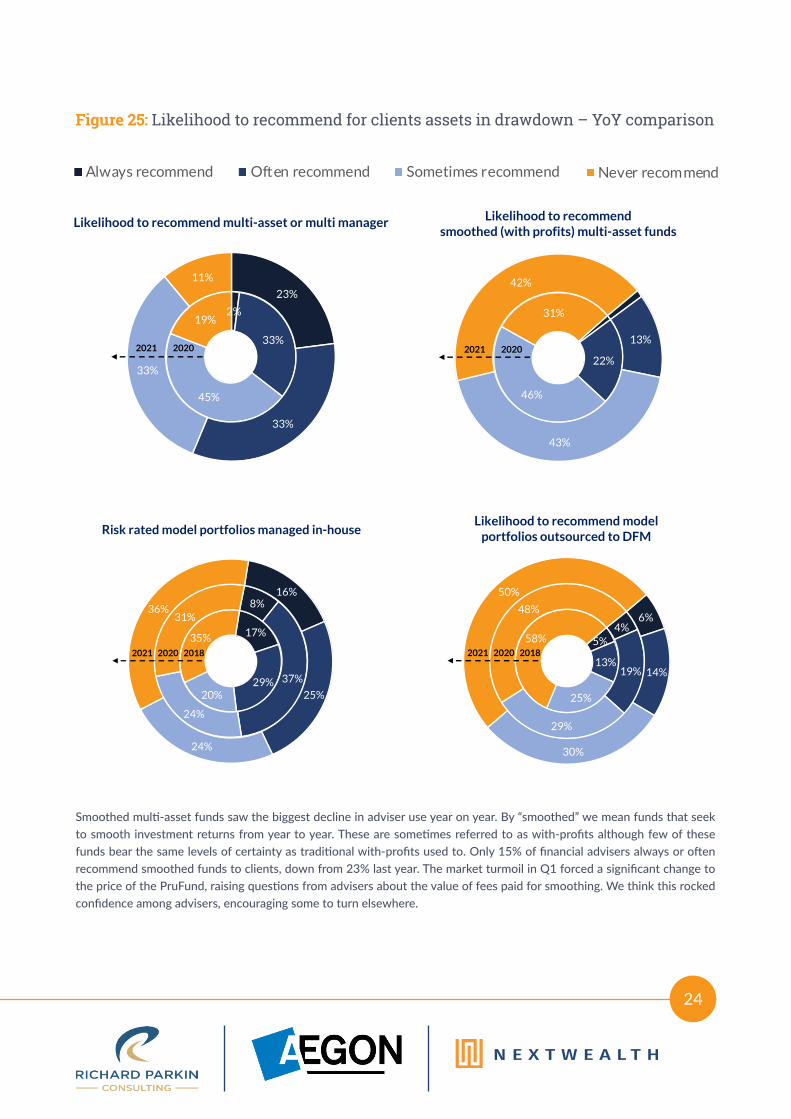

Figure 25: Likelihood to recommend for clients assets in drawdown – YoY comparison

16 %

8 %

17 %

25 %

37 %

29 %

24 %

24 %

20 %

36 %

31 %

35 %

2021

2020

2018

Always recommend Often recommend Sometimes recommend Never recommend

16 %

8 %

17 %

25 %

37 %

29 %

24 %

24 %

20 %

36 %

31 %

35 %

2021

2020

2018

Always recommend Often recommend Sometimes recommend Never recommend

16 %

8 %

17 %

25 %

37 %

29 %

24 %

24 %

20 %

36 %

31 %

35 %

2021

2020

2018

Always recommend Often recommend Sometimes recommend Never recommend

16 %

8 %

17 %

25 %

37 %

29 %

24 %

24 %

20 %

36 %

31 %

35 %

2021

2020

2018

Always recommend Often recommend Sometimes recommend Never recommend

Smoothed multi-asset funds saw the biggest decline in adviser use year on year. By “smoothed” we mean funds that seek to smooth investment returns from year to year. These are sometimes referred to as with-profits although few of these funds bear the same levels of certainty as traditional with-profits used to. Only 15% of financial advisers always or often recommend smoothed funds to clients, down from 23% last year. The market turmoil in Q1 forced a significant change to the price of the PruFund, raising questions from advisers about the value of fees paid for smoothing. We think this rocked confidence among advisers, encouraging some to turn elsewhere.

24

Likelihood to recommendsmoothed (with profits) multi-asset funds

22%

46%

31%

13%

43%

42%

20202021

17%

29%20%

35%

8%

37%

24%

31%

16%

25%

24%

36%

Risk rated model portfolios managed in-house

20202021 20185%

13%

25%

58%4%

19%

29%

48%6%

14%

30%

50%

Likelihood to recommend modelportfolios outsourced to DFM

20202021 2018

Likelihood to recommend multi-asset or multi manager

2%

33%

45%

19%

23%

33%

33%

11%

20202021

DFMs continue to have their fans and detractors. Half of advisers said they would ‘never’ outsource to a DFM either for model portfolios or bespoke portfolios. DFMs are sometimes perceived as expensive and better at growing portfolios than supporting withdrawals. There has been much talk about new propositions from DFMs to support retirement clients, but we’ve seen little true innovation as yet. One of the challenges is the agent as client framework under which DFMs offering services through 3rd party platforms typically operate. Agent as client usually means that the DFM can’t see the underlying client. This means the DFM cannot manage the tax or withdrawal strategy of individual clients.

Financial advisers do expect to increase use of DFM model portfolios: Figure 24 shows that 21% of advisers plan to increase use for clients in drawdown in the next three years. The objections we hear from advisers are a lack of product innovation to support clients in decumulation from DFMs and also the layering of costs.

On product innovation, we heard of two solutions in our research that address some of the DFM shortcomings. A large national is developing a series of target dated portfolios. As each target date approaches, the client and adviser decide if the client should take the income or invest in an annuity pot. The solution offers flexibility of income levels and reduces the cost of the annuity by deferring the purchase. Another innovative solution we heard about was a proposition combining a tool to model the withdrawal strategy integrated to DFM model portfolios.

We think these innovative solutions address a number of shortcomings of DFM portfolios for retired clients. But advisers also want products to be straightforward enough for clients to understand. Many solutions that sound great in theory end up too complex to be used in practice.

On cost of DFMs, one financial adviser we interviewed lamented the challenge posed by the cumulative cost of the supply chain in a low growth environment.

25

4.2 DFM model portfolios

“But the challenge of that is, all in with their fees, it’s probably about 1.6%. So, in a low growth environment, if you’re a medium risk client, making maybe 4%. If you net off 1.6% and our ongoing adviser charge of 75 basis points, that takes you to 2.3%. If inflation is run-ning at two and a half, you’re losing money in real terms, aren’t you?”

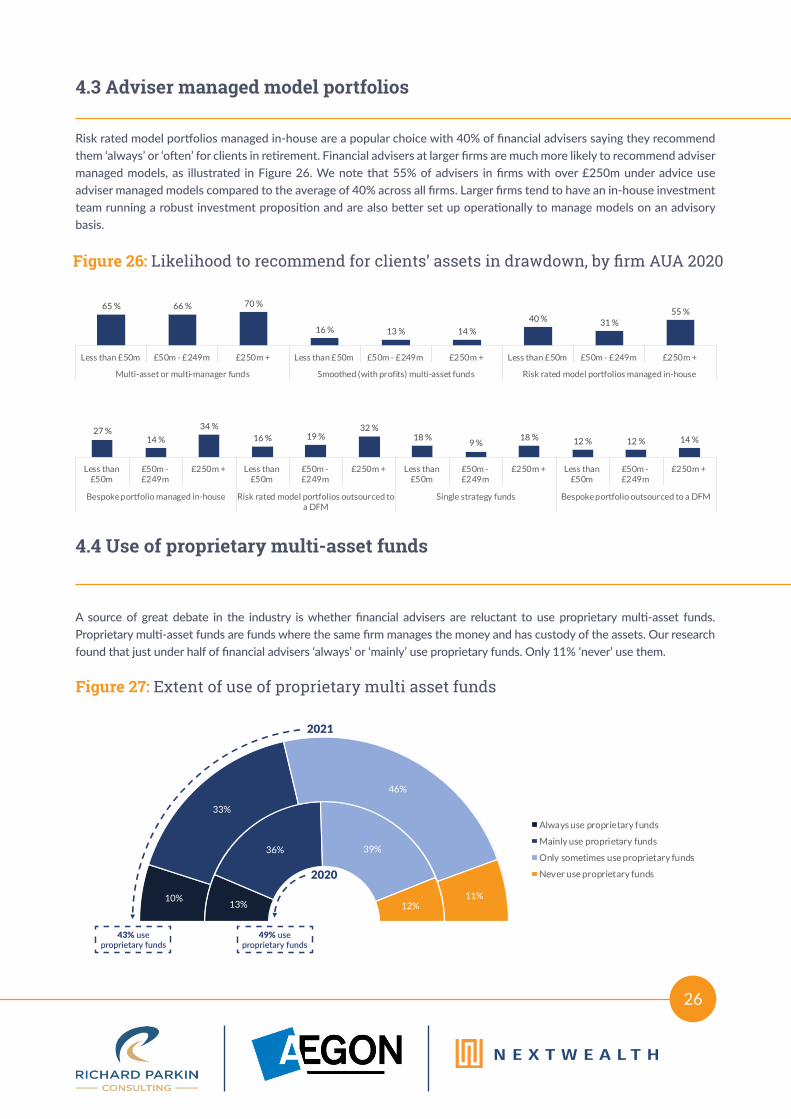

Risk rated model portfolios managed in-house are a popular choice with 40% of financial advisers saying they recommend them ‘always’ or ‘often’ for clients in retirement. Financial advisers at larger firms are much more likely to recommend adviser managed models, as illustrated in Figure 26. We note that 55% of advisers in firms with over £250m under advice use adviser managed models compared to the average of 40% across all firms. Larger firms tend to have an in-house investment team running a robust investment proposition and are also better set up operationally to manage models on an advisory basis.

A source of great debate in the industry is whether financial advisers are reluctant to use proprietary multi-asset funds. Proprietary multi-asset funds are funds where the same firm manages the money and has custody of the assets. Our research found that just under half of financial advisers ‘always’ or ‘mainly’ use proprietary funds. Only 11% ‘never’ use them.

26

Figure 26: Likelihood to recommend for clients’ assets in drawdown, by firm AUA 2020

Figure 27: Extent of use of proprietary multi asset funds

4.3 Adviser managed model portfolios

4.4 Use of proprietary multi-asset funds

65 % 66 % 70 %

16 % 13 % 14 %

40 % 31 %55 %

Less than £50m £50m - £249m £250m + Less than £50m £50m - £249m £250m + Less than £50m £50m - £249m £250m +

Multi-asset or multi-manager funds Smoothed (with profits) multi-asset funds Risk rated model portfolios managed in-house

27 %14 %

34 %16 % 19 %

32 %18 %

9 %18 % 12 % 12 % 14 %

Less than£50m

£50m -£249m

£250m + Less than£50m

£50m -£249m

£250m + Less than£50m

£50m -£249m

£250m + Less than£50m

£50m -£249m

£250m +

Bespoke portfolio managed in-house Risk rated model portfolios outsourced toa DFM

Single strategy funds Bespoke portfolio outsourced to a DFM

13%

36% 39%

12%10%

33%

46%

11%

Always use proprietary funds

Mainly use proprietary funds

Only sometimes use proprietary funds

Never use proprietary funds

2021

43% use proprietary funds

49% use proprietary funds

2020

ESG is a popular topic of discussion and has garnered much media attention in recent months. Other research from NextWealth suggests that most financial advisers take account of a client’s ethical considerations when constructing investment portfolios but few are integrating ESG criteria more broadly. About half of financial advisers say they consider ESG criteria only at the client’s request.

However, nearly one third say they consider ESG credentials among the criteria used to select and manage funds.

27

4.5 Use of ESG funds and solutions

Figure 28: Extent that Environmental, Social and Governance (ESG) issues are considered when building portfolios for retirement clients

Our interviewees confirmed that the demand is low from clients. That doesn’t mean they aren’t taking action. One adviser we spoke to has shifted to an ESG integrated DFM solution. He told us: “Clients aren’t asking about it. The industry is talking about it.”, but he concluded it was the right thing to do to make the shift.

Most of the advisers we spoke to are unsure how to approach determining a client’s ESG preferences and how to translate that into an investment portfolio.

“Problem we have is clients can be quite specific, like avoid tobacco or arms. Funds we use on the advisory side of the business, when we drill down, one of the funds will invest in something they don’t agree with.”

3 %

31 %

52 %

7 %

8 %

We apply a strict ESG screening process to allmanagers/funds selected

ESG credentials are amongst the factors we considerwhen selecting managers/funds

We consider ESG criteria only at the clients’ request

Other

Prefer not to say

Most agreed that there needs to be better standards in data and language to support wider adoption of ESG integrated investing.

28

“We’ve been kicking the can down the road really, with a view that until the rules came in… When we talk about this, what we’re constantly looking for is some sort of industry taxon-omy such that we can actually have a sensible conversation about this. We’ve sort of devel-oped our own in a way to lead people to where we think the answer is. When we talk about sustainable, responsible investing, it’s great, but every client’s going to be different.”

The closure of several property funds led the FCA to propose a set of rules to require a notice period for withdrawals. Property funds have been a good source of income in the past and a popular choice in portfolios for retired clients. We wanted to understand the impact this change might have on retire-ment portfolios. Among the 42% of advisers that say they use property funds, 51% say they will continue to use property funds if a 90 or 180-day notice period for withdrawals is introduced. One third say they would stop using these funds.

4.6 Use of property fundsFigure 29: Use of property funds and introduction of 90 or 180 day notice period for withdrawals

If a 90 or 180 day notice period for withdrawals was introduced, would you still expect to use these funds in decumulation portfolios?

23 %

28 %

33 %

16 %

Yes, continue to use

Yes, but use less

No, I would stop using

Don’t know/prefer not to say

If a 90 or 180 day notice period for withdrawals was introduced, would you still expect to use these funds in decumulation portfolios?

23 %

28 %

33 %

16 %

Yes, continue to use

Yes, but use less

No, I would stop using

Don’t know/prefer not to say

Yes, 42 %

No, 55 %

Don't know/ prefer not to say,

4 %

Our first report on retirement advice in 2018 was, in part, motivated by a desire to understand how the then booming market in defined benefit (DB) transfer advice would develop. Many of the advisers that we spoke to at that time were confident the market would continue to grow further but we were less convinced. The issues with mis-advice of British Steel scheme members were starting to emerge, professional indemnity insurers were getting nervous about the risk represented by advisers writing this business, and it was clear that the FCA was getting increasingly focused on the quality of advice being given.

5. Defined benefit pension transfer advice

29

Figure 30: Number of DB to DC pension transfers received

Source: FCA Retirement Income Data, September 2020

32,249

24,575

20,202 20,432

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Apr - Sept 2018 Oct 2018 - Mar 2019 Apr - Sept 2019 Oct 2019 - Mar 2020

DB transfer activity peaked at the end of 2017 and has declined sharply since then. While the Office of National Statistics has discontinued its time series on pension transfers, the number of DB to DC transfers is now included in the FCA’s annual Retirement Income Data analysis, and this is shown in Figure 30. This only provides data to the end of March 2020 and, while DB transfers do seem to have plateaued after further sharp falls, we expect volumes during the rest of 2020 continued to fall.

5.1. Firms offering defined benefit transfer advice

As the chart shows, the proportion of firms offering DB transfer advice has contracted significantly again, and certainly by a greater extent than foreseen in last year’s report. Currently only 22% of firms offer DB advice with 2% of firms saying they will leave the market in the next 12 months. Moreover, over a third of firms who still give DB advice have, or expect to, significantly reduce how much of this business they do.

30

Figure 30: Approach to providing DB transfer advice

“It’s very, very difficult to do this because there’s a load of people doing wrong things with people, because they don’t care. There’s a hell of a lot of people out there, we’re trying to do the right thing. And now they won’t try and do the right thing anymore. They just won’t get involved because it’s just not worth it.”

In last year’s report we found that a significant proportion of firms had stopped providing DB transfer advice with 41% of firms offering it compared to 56% in 2018.

We asked those firms who have stopped, or intend to stop, giving DB transfer advice, and those who expect to significantly reduce the volume of this business, to rank the top three reasons that led to this decision.

5.2. Reasons for ceasing to offer DB transfer advice

44 %

34 %

2 %

8 %

13 %

0 %

40 %

17 %

3 %

15 %

23 %

2 %

We do not, and have not, provided DB advice inthe past 3 years

We used to provide DB advice but no longer doso

We provide DB advice but expect to stopproviding it in the next 12 months

We provide DB advice but have or expect tosignificantly reduce the volume of this

We provide DB advice and expect to continueto do so

We do not currently provide DB advice butintend to start doing so in the next 12 months 2021

2020

22% currently provide(2020: 41%)

31

Figure 32: Reasons for stopping or reducing the volume of DB transfer advice

30 %

30 %

10 %

18 %

3 %

3 %

4 %

75 %

75 %

37 %

34 %

20 %

16 %

11 %

Overall business risk of giving DB transferadvice

Increase in Professional Indemnity Insurancepremiums and excess

Limits imposed by PI insurer on volume ofbusiness

FCA supervisory activity

Lack of client demand

Proposed ban on contingent charging

Any other reason

Main Reason

Additional Reason

One of the key drivers of these decisions was the general risk of giving this type of advice. FOS compensation limits were increased from £150,000 to £350,000 for complaints referred to FOS after 1 April 2019 where the cause of complaint occurred after 1 April 2019. This limit has now been increased further to £360,000 and may well rise again in 2021. Combined with significant increases in professional indemnity insurance excesses and, in some cases, the exclusion of past DB transfer business from cover altogether, many firms could find themselves bankrupted by a small number of upheld complaints. Indeed, compensating DB transfer clients of failed advice firms is one of the main reasons for the sharp increase in FSCS levies on advisers.

Given this backdrop, and the further risk that the decline in markets as a result of the pandemic could increase compensation claims, we expect more firms will withdraw from the market completely over the coming year.

We asked advisers how long recent DB transfers had taken to complete.

Where advisers were able to answer this question, over 80% of transfers took at least 3 months with nearly a quarter of transfers taking more than 6 months. DB transfers are complex at the best of times involving significant client interaction, correspondence with the ceding scheme to understand benefits, and detailed analysis by the adviser. However, two-thirds of advisers told us that recent transfers have taken longer than usual to complete.

Figure 33: Time taken from initial conversation to completion of DB transfer

5.3. Time taken to complete a DB transfer

0 %

14 %

58 %

14 %

7 %

2 %

5 %

Less than 1 month

1 - 2 months

3 - 6 months

6 - 9 months

9 - 12 months

More than one year

Don’t know

32

Delays in the transfer process are not only frustrating for the client and their advisers but can lead to transfer values having to be recalculated. This in turn can lead to clients receiving a lower transfer than originally offered which could be a reason for complaint against the adviser. In the past, the main reason for delays was the tortuous process of gathering the necessary information on benefits from the ceding scheme provider. This traditional challenge was exacerbated by the effects of the pandemic lockdown on schemes' administration capacity and the Pensions Regulator also allowed schemes to suspend transfer activity between April and June 2020 because of the pandemic. However, it seems that recent delays are now as much due to firms’ stricter internal processes as they are to tardy responses from schemes.

Figure 34 Change in time to complete a DB transfer over past year

Figure 35: Cause of delay in completing recent pension transfer

52 %

3 %

0 %

42 %

3 %

Delay getting information from DBpension providers

Delay in processing by receivingprovider

Delay getting paperwork signed byclients due to social distancing

Longer process due to more stringentprocess in firm

Other, please specify

It has increased a lot,

30 %

It has increased a little, 36 %

Stayed the same, 23 %

Not sure, 11 %

3 %

19 %

52 %

13 %

0 %

0 %

13 %

Less than 2 weeks

2 - 4 weeks

1 - 2 months

3 - 6 months

6 - 9 months

9 - 12 months

Don’t know

Increased by..

33

Figure 36: Attitudes towards abridged advice

The FCA introduced a ban on contingent charging for DB transfer advice from 1 October 2020. This prevents firms from charging different levels of fee depending on what the outcome of the advice is. Prior to this, it was common for advisers not to charge a fee where the advice was not to transfer, or to charge an additional “implementation fee” where transfer was recommended. The FCA concern was that these arrangements incentivise advisers to recommend transfer.

While this ban may reduce the incentive for firms to recommend transfer, it also creates a barrier to clients seeking advice on DB transfers. Payment for transfer advice is almost always deducted from the transfer proceeds. If the advice is not to transfer, then the advice fee will have to be met directly by the client from other sources. Given the potential cost of this advice, the expectation is that few clients will be willing to take the risk of assessing whether they should transfer.

To help combat this, the FCA introduced “abridged advice” to allow advisers to identify where a transfer is unlikely to be in a client’s best interest. The expectation is that this will allow firms to identify these clients more cost-effectively than taking them through a full advice process.

Overall, advisers are more positive about abridged advice than they were a year ago with 60% now saying it’s an effective way of identifying clients for whom a transfer is not suitable. Moreover, only 11% of advisers disagreed with this, down from 19% last year. A third of advisers agreed that abridged advice would save sufficient time and be suitably priced to attract potential clients.

5.4. Abridged advice for DB transfers

(n=47 advisers that offer DB advice)

6 %

2 %

2 %

53 %

32 %

32 %

32 %

30 %

36 %

32 %

40 %

9 %

19 %

21 %

19 %

11 %

4 %

6 %

11 %

Abridged advice is an effectiveway of identifying clients for

whom a transfer is not suitable

As proposed, abridged advicewith full fact-find will savesufficient time to appeal to

customers

Abridged advice is a way ofidentifying individuals who qualify

for a carve out from thecontingent charging ban

Clients will be more willing to payfor abridged advice than full

transfer advice

Strongly agree Agree Neither agree nor disagree

Disagree Strongly disagree Unsure

% Strongly Agree/Agree

vs 2020% Strongly

Agree/Agree

60% +14%

34% -2%

32% N/A

34% -1%

34

Figure 37: Proportion of advisers offering DB advice who offer abridged advice

Figure 38: Whether, and how much, advisers charge for abridged advice

Of those advisers offering DB transfer advice, just over half offer abridged advice. A few (3%) of the respondents who do not offer full DB transfer advice do offer abridged advice. This may seem surprising, but it does allow these advisers to confirm that a transfer is unsuitable for their clients. Presumably, if the abridged advice process doesn’t conclude that a transfer is unsuitable, clients will be referred to another adviser if they want to pursue investigating the transfer option further.

While contingent charging has been banned for full DB transfer advice, it is still allowable for abridged advice and just under a third of advisers offer it for free. Of those who do charge, most offer the service for less than £1,000. While this is likely to be a significant cost, especially for those with limited wealth beyond their DB pension, it is significantly more affordable than full DB transfer advice.

5.4. Abridged advice for DB transfers

21 %

37 %

37 %

5 %

Up to £500

£500 - £1,000

More to £1,000

Don’t know/ prefer not say

66 %

31 %

3 %

Yes

No

Don't know/ prefernot to say

Yes, 51 %

No, 36 %

Don't know/ prefer not to say, 13 %

Yes, 66 %

No, 31 %

Don't know/ prefer not to …

The FCA has focused on value for money across the value chain and we expect that theme to continue in the years ahead. The December 2020 Evaluation of the impact of the Retail Distribution Review and the Financial Advice Market Review published by the FCA, confirmed this focus. The regulator has challenged the value of ongoing fees in particular. This could lead financial advisers to focus more on clients in decumulation where the value of ongoing advice is easier to justify. Accumulation is perceived as more straightforward and some question the need for ongoing annual reviews. Decumulation can be much more complex, requiring focus on managing the investment strategy and withdrawal strategy amid very little certainty.

This leads to our second trend, a continued shift to retirement assets. In our survey for this report, financial advisers said that 58% of their assets are for clients seeking retirement advice and they expect that to increase to 63% in three years’ time. While the shift to retirement assets has slowed over the four years since we first published our report on retirement advice, we think the gradual shift will continue.

Part of this is a result of the regulator’s focus on value which will force financial advice businesses to focus on areas where they deliver value on an ongoing basis, one of which is advice in decumulation. Managing retirement portfolios is also increasingly complex, which will also fuel demand.

The challenge is of course that while value may increase, the pot of money on which fees are being earned will in most cases decline while the work involved may increase. Financial advice businesses need to carefully consider how to charge for their services.

“The fee side of things with clients and decumulation, fees based on AUM. Clients become less profitable as time goes on. How does fixed fee model work in that space?”

Trend: Shift to retirement assets for ongoing fees

Trend: Regulatory focus on value

35

One financial adviser we spoke to put it this way:

“I think there’s been too much in the past with advisers finding three, four pots and going, ‘Well, you obviously want things in one place, don’t you?’ Because it’s easier. And I’ll now charge you for managing that pot that really didn’t need managing. And I think the FCA have really got to the point where, if people are in accumulation, they almost don’t need an adviser on a regular basis, whereas in decumulation advisers really need to add a lot more value. I think that by accident, the FCA sort of hit this year with a real focus on value and charges and adviser fees.”

Conclusion Trends and

opportunities ahead

There has been a proliferation of systems and tools to support retirement advice. One adviser put it this way:

“The tech thing becomes a pain. Platforms, cash flow modellers, Timeline – very bitty in terms of the whole process. Doesn’t help

the client journey.”

In a column in CityWire’s New Model Adviser, Jennifer Ellis of Wellington Wealth estimated that the firm deals with 42 different online systems across the providers they work with.

“We deal with 42 separate agencies, which means 42 online systems to learn and 42 online client journeys or wizards to remember.” (https://citywire.co.uk/new-model-adviser/news/learning-42-provider-systems-that-can-t-be-the-meaning-of-life/a1431762)

Some advisers see an opportunity to help clients make behavioural changes that will allow them to make better decisions.