![Foreign Corrupt Practices Act - Legal Analysis · Foreign Corrupt Practices Act Legal Analysis ... The Foreign Corrupt Practices Act2 [“FCPA”] ... FCPA, which puts them in lower](https://static.fdocuments.in/doc/165x107/5adcc1907f8b9ae1408bf6eb/foreign-corrupt-practices-act-legal-corrupt-practices-act-legal-analysis-the.jpg)

MANAGING FCPA LITIGATION RISK IN BUSINESS … · The Foreign Corrupt Practices Act ... despite a...

25

http://delvacca.acc.com Drinker Biddle & Reath LLP Charles Leeper, Partner Mary Hansen, Partner VWR International LLC George Van Kula, SVP, General Counsel MANAGING FCPA LITIGATION RISK IN BUSINESS PARTNERING RELATIONSHIPS

Transcript of MANAGING FCPA LITIGATION RISK IN BUSINESS … · The Foreign Corrupt Practices Act ... despite a...

http://delvacca.acc.com

Drinker Biddle & Reath LLP Charles Leeper, Partner Mary Hansen, Partner VWR International LLC George Van Kula, SVP, General Counsel

MANAGING FCPA LITIGATION RISK IN BUSINESS PARTNERING RELATIONSHIPS

Anti-Bribery Provisions: Elements The Foreign Corrupt Practices Act (FCPA) prohibits:

• The offer, payment, promise to pay, or authorization of payment of

• Money or anything of value • To any foreign official • Directly or indirectly • To influence an official act or decision, induce an

official to do or omit an act, or secure an improper advantage

• In order to obtain or retain business

2

“Directly or Indirectly” • Payment to “. . . any person, while knowing that all or

a portion of such money or thing of value will be offered, given, or promised, directly or indirectly, to any foreign official . . .” 15 U.S.C. §78dd-1(a)(3).

• Exposure exists for “indirect” payments made through: • Subsidiaries • Distributors • JV Partners • Resellers • Sales Agents • Brokers • Consultants • Other Professional Services Firms

3

Actual Knowledge

• A company cannot insulate itself from liability by making the unlawful payments through another entity or individual.

• In Kozeny, government argued that defendant set up

an intermediate company to shield himself from FCPA liability, raising an inference that he had actual knowledge of bribes paid by fellow investor. 667 F.3d 127 (2d. Cir. 2011).

4

Constructive Knowledge

• “[K]nowledge is established if a person is aware of

a high probability of the existence of [a] circumstance, unless the person actually believes that such circumstance does not exist.”

15 U.S.C. §78dd-1(f)(2)(B)

5

Willful Blindness–Ignoring Red Flags

• Country risk • Above-market commissions paid to agents relating

to high risk transactions • Lack of due diligence on agents • Lack of internal audits of foreign subsidiaries;

inadequate audits • Pervasiveness of unlawful payments • Duration of unlawful payments

6

Liability for Subsidiary’s Payments

• When unlawful payments have been made by a subsidiary, traditionally a parent company was not held liable unless there was evidence of the parent’s involvement, or at the very least, “knowledge” of subsidiary’s conduct.

7

The Trend Toward Agency Liability • “[A] parent may be liable for its subsidiary's conduct

under traditional agency principles. The fundamental characteristic of agency is control. Accordingly, DOJ and SEC evaluate the parent's control-including the parent's knowledge and direction of the subsidiary's actions, both generally and in the context of the specific transaction-when evaluating whether a subsidiary is an agent of the parent.”

SEC/DOJ Resource Guide at 27-28

8

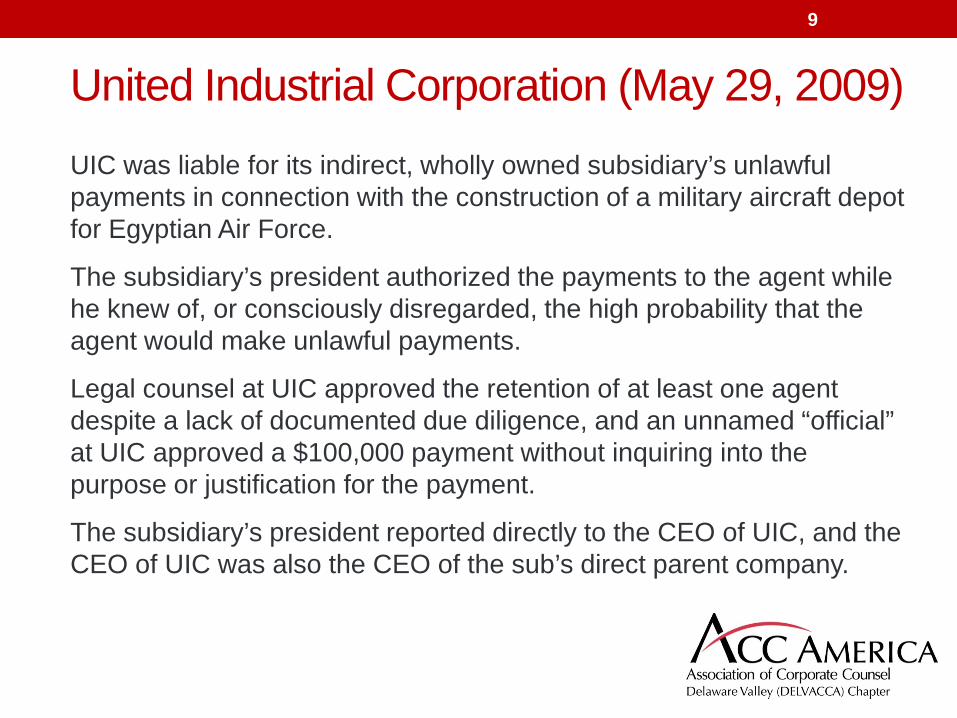

United Industrial Corporation (May 29, 2009)

UIC was liable for its indirect, wholly owned subsidiary’s unlawful payments in connection with the construction of a military aircraft depot for Egyptian Air Force.

The subsidiary’s president authorized the payments to the agent while he knew of, or consciously disregarded, the high probability that the agent would make unlawful payments.

Legal counsel at UIC approved the retention of at least one agent despite a lack of documented due diligence, and an unnamed “official” at UIC approved a $100,000 payment without inquiring into the purpose or justification for the payment.

The subsidiary’s president reported directly to the CEO of UIC, and the CEO of UIC was also the CEO of the sub’s direct parent company.

9

Smith & Nephew (Feb. 6, 2012)

SEC settled with English-based medical device company traded on the NYSE.

DOJ settled with the wholly owned subsidiary in Delaware.

Foreign subsidiaries used a Greek “distributor” to make unlawful payments to doctors employed by government owned health agencies.

Payments disguised as “marketing services.”

Evidence demonstrating the VP of International Sales at the U.S. subsidiary knew and, at least implicitly, approved the unlawful payments.

No indication that anyone at U.K. parent was involved or had knowledge of the unlawful payments.

DPA with U.S. subsidiary included an FCPA count.

10

Lufthansa Technik AG (Mar. 14, 2012)

German provider of aircraft-related services.

Indirect parent of BizJet International Sales and Support Inc., a provider of aircraft maintenance, repair and overhaul services based in Tulsa, Oklahoma.

According to BizJet’s DPA, BizJet made unlawful payments to Mexican officials either directly or through a shell company owned and operated by a BizJet sales manager.

BizJet paid approximately a criminal fine of $11.8 million to resolve the criminal charges.

At the same time, Lufthansa entered into a NPA related to BizJet’s FCPA violations.

The NPA makes no mention of the basis of Lufthansa’s liability.

11

Tyco International Ltd (Sept. 25, 2012)

Settled SEC charges that it violated the FCPA and books and records and internal control provisions (12 payment schemes)

• Tyco liable for unlawful payments in one scheme based solely upon the fact that four high-level Tyco officers were also officers of the subsidiary.

• Tyco paid approximately $13.1 million to settle the charges.

Tyco also entered into a NPA with DOJ for books and records violations (14 payment schemes).

• NPA specifically required that Tyco’s policies and procedures address third-party relationships as well as merger and acquisition transactions.

• Tyco’s subsidiary in Dubai pleaded guilty to conspiracy to violate the FCPA.

• Tyco paid $13.68 million.

12

Ralph Lauren Corporation (Apr. 22, 2013)

RLC’s Argentine subsidiary made approximately $593,000 in unlawful payments to government and customs officials to improperly secure the importation of Ralph Lauren Corporation's products. (Paid approximately $1.6 million to SEC and DOJ.) SEC found that RLC lacked meaningful anti-corruption compliance and control mechanisms over the subsidiary. The SEC’s NPA summarily declared, without factual support, that the subsidiary’s “General Manager was an agent and employee of” Ralph Lauren Corporation. DOJ’s NPA states that the GM was “hired by” RLC.

13

Watts Water Technologies (Oct. 13, 2011) Books and Records and Internal Control Violations based upon unlawful payments made by wholly owned subsidiary in China. Watts acquired the subsidiary in April 2006–first time Watts had a business that sold products to a government entity. Payments predated the acquisition and were the result of a sales incentive policy allowing sales employees to use commissions to make unlawful payments. The policy was never translated into English. Watts did not implement adequate internal controls or conduct adequate FCPA training for its employees in China until 3 years after the acquisition. Cease-and-Desist Order, $3.8 million.

14

Johnson & Johnson (Apr. 8, 2011)

FCPA violations based upon subsidiaries’, employees’ and agents’ unlawful payments to, among others, doctors in Greece.

At the time J&J acquired DePuy, DePuy used distributors to market products and to facilitate the unlawful payments.

Over time, certain U.S. J&J “executives” learned of the payments.

J&J’s internal audit department eventually became aware of the payments.

J&J paid over $48 million to the SEC to settle the FCPA, books and records and internal controls violations.

J&J paid $21.4 million and entered into a DPA with DOJ to resolve the criminal charges.

15

The Monetary Risk of Non-Compliance

Summary of FCPA Actions Over the Last 3 ½ Years $2,181,381,838 Collected

2013 YTD 2012 2011 2010

DOJ Actions 2 10 10 15

Fines $12,642,000

$130,400,000

$360,114,000

$868,915,000

SEC Actions 3 10 13 19

Disgorgement and PJI

$9,340,842

$106,010,348

$138,332,817

$509,839,182

Penalties $0 $16,015,649 $9,580,000 $20,192,000

Totals $21,982,842

$252,425,997

$508,026,817

$1,398,946,182

16

Q. What Can You Do to Minimize Corporate Exposure?

A. Allocate Limited Due Diligence Dollars to Riskiest Relationships.

17

Levels of Due Diligence for Proposed Business Partners

• Public Record/Politically Exposed Persons/Press Checks • Questionnaires • Reference checks • Review of PBP’s compliance program • Field visit/interviews • Analyze compliance with local regulatory requirements • Contract Warranties/Certifications/Audit Clauses • Training Requirements • Routine review of compensation/discounts/allowances

18

Proposed Business Partners Logic Path to Assess Need for Enhanced Due Diligence

• What service will the PBP provide for the Client? • What is the business justification for that service? • What are the proposed payment terms? • Would that service likely require the PBP to interact with foreign government officials (“FGO”)?

19

Proposed Business Partners Logic Path to Assess Need for Enhanced Due Diligence • What is the role of the PBP when it interacts with FGO (e.g., supplier, broker, common carrier, other regulated entity) and expected frequency of interaction?

• In what foreign country will the PBP interact with FGO?

• Might the PBP be a government “instrumentality”?

20

Proposed Business Partners Logic Path to Assess Need for Enhanced Due Diligence

• If the PBP will acquire products from the Client for resale:

• Will the PBP take title to the products?

• Will the PBP hold itself out as an agent or representative of the Client?

• Will the PBP use the Client’s logo or any of its trademarks in conducting the PBP’s business?

• How will pricing be established for the products purchased by the PBP (e.g., list price, volume discounts, special promotions)?

21

Proposed Business Partners Logic Path to Assess Need for Enhanced Due Diligence

• If the PBP will acquire products from the Client (Cont.):

• Will the Client set the price at which the PBP may re-sell the client’s products?

• Will the Client reimburse the PBP for marketing expenses?

• Will the Client provide any sales training to the PBP?

• What other control or direction, if any, will the Client exert in regard to the PBP?

22

Proposed Business Partners Logic Path to Assess Need for Enhanced Due Diligence

• Will the Client’s payments to the PBP represent a substantial portion (more than 25%) of the PBP’s annual revenues?

• Does the PBP have its own anti-corruption compliance program?

• Where negative, or potentially negative information regarding a PBP is not a matter of public record or otherwise subject to ready verification, will the management of the PBP agree to be interviewed by the Client’s compliance personnel?

23

Red Flags • Reputation/culture of locale (Africa, former Soviet

Union, Central/South America) • PBP has ties to foreign government officials or

political party • PBP is recommended by foreign official • PBP has no code of conduct • PBP resists certification requests and/or requests

for information regarding ownership structure, sub-agents, etc.

• PBP seeks above-market commissions

24

Red Flags • PBP seeks cash promotional allowances

• PBP requests payment to third-party or offshore accounts, or to accounts unrelated to the transaction

• Invoices from PBP show unusually large “credits” • Imprecise descriptions of services/goods sold,

inadequate support/detail in invoices • High travel/entertainment expenses • Round-numbered charges/repetitive charges

in equal amounts

25