Managerial Accounting Rock & Roll All Nite Concepts ... Chapt… · Managerial Accounting Concepts...

14

Managerial Accounting Concepts & Principles Chapter 16 Teacher Version Rock & Roll All Nite

Transcript of Managerial Accounting Rock & Roll All Nite Concepts ... Chapt… · Managerial Accounting Concepts...

Managerial Accounting

Concepts & PrinciplesChapter 16

Teacher VersionRock & Roll All Nite

Paul Stanley’ Guitar Cracked Mirror

Going Price: $6,999.99 on Ebay

Paul Stanley would be nowhere without his guitar. Right? Of Course I am right!

What does this all have to do with Managerial Accounting?

● how to manufacture? ● how to account for costs?● how much to charge?● how many to sell to cover costs/make a profit?● how many employees needed for each section?● should we automate v cost of manufacturing each guitar?

In this chapter we will discuss:❏ Managerial Accounting❏ Management Process❏ Role of Managerial Accounting❏ Characteristics of Reports, Terms & Uses of Information

Financial vs Managerial AccountingFinancial

Information is reported at fixed intervals as financial statements

Information is used by external users:

ShareholdersCreditorsGovernment agenciesGeneral Public

Managerial

Information is designed to meet the specific needs of management

Information includes historical data: measure past operations and future decision making

Information is used by internal users.

Produce a Name TentYou will need:

Blank piece of paper

pen/pencil

You Must:

follow instructions precisely

Managerial AccountingInternals User Include principals in the hierarchy of the company.

Line Dept: provide goods/services

Staff Dept: provide assistance/advice to line

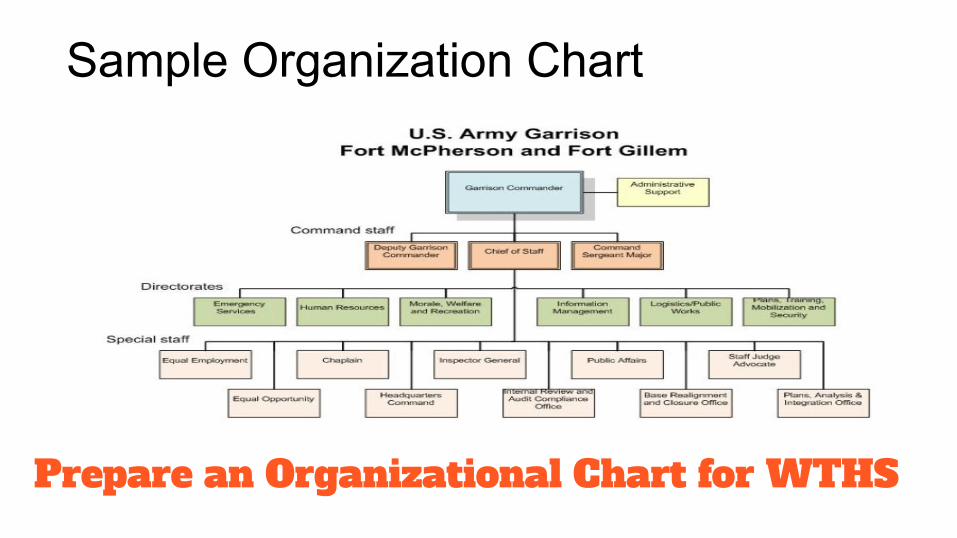

Prepare an Organizational Chart for WTHS

Sample Organization Chart

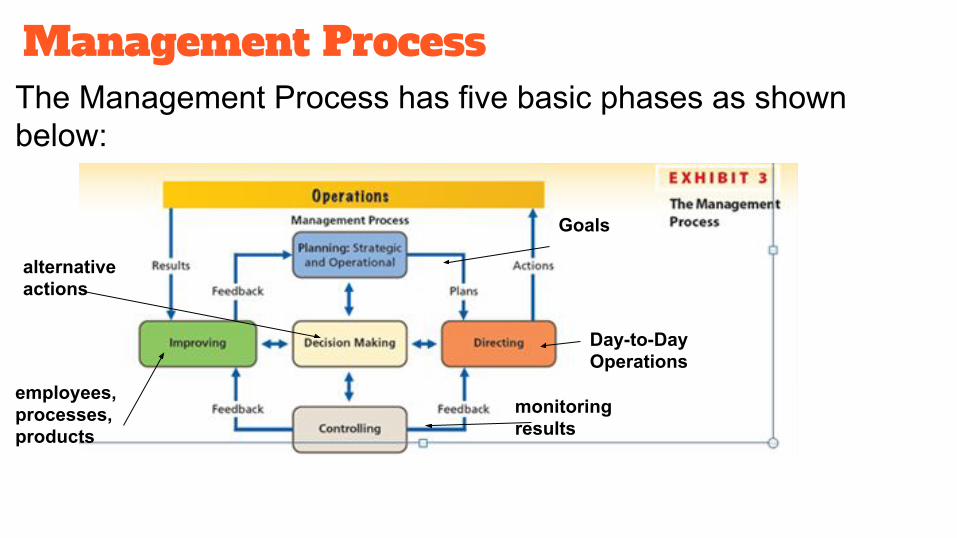

Management ProcessThe Management Process has five basic phases as shown below:

Goals

Day-to-Day Operations

monitoring results

employees, processes, products

alternative actions

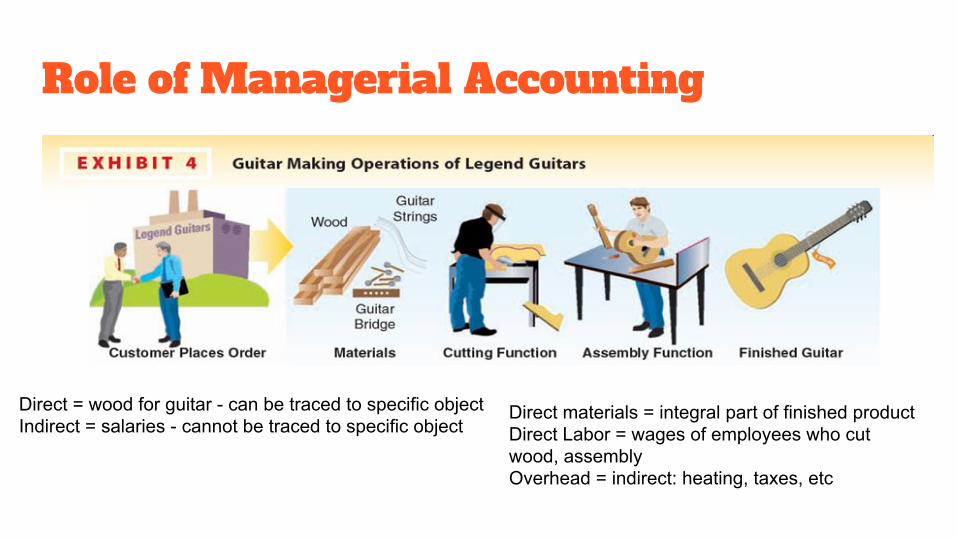

Role of Managerial Accounting

Direct = wood for guitar - can be traced to specific objectIndirect = salaries - cannot be traced to specific object

Direct materials = integral part of finished productDirect Labor = wages of employees who cut wood, assemblyOverhead = indirect: heating, taxes, etc

Merchandising v Manufacturing

Costs incurred by a Merchandiser: Purchase product to sell

Financial Statements● Retained Earnings and Cash Flow for

a manufacturing business are similar to service and merchandising business.

● Balance Sheet and Income Statement for a manufacturing business are more complex:

○ Manufacturer makes the products that it sells

○ Manufacturer must record and report product costs

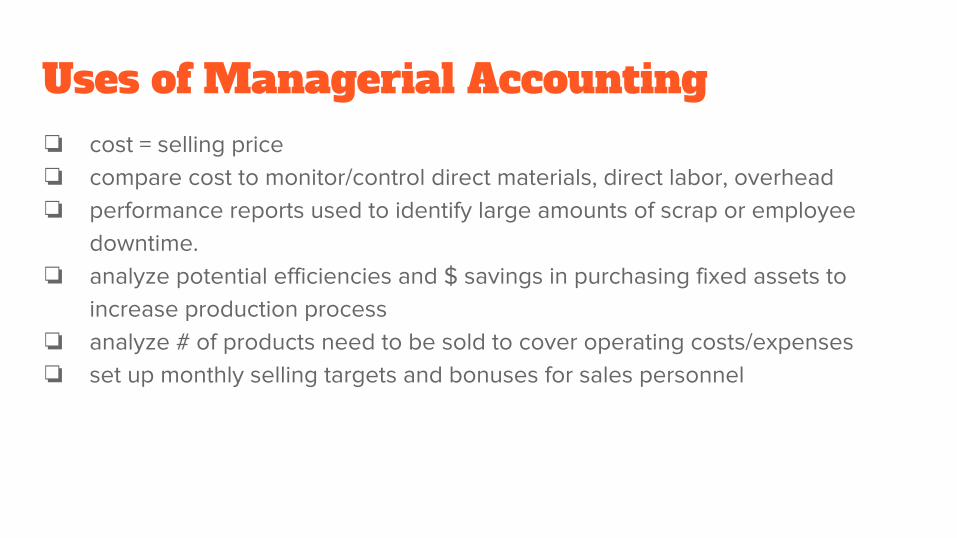

Uses of Managerial Accounting❏ cost = selling price❏ compare cost to monitor/control direct materials, direct labor, overhead❏ performance reports used to identify large amounts of scrap or employee

downtime.❏ analyze potential efficiencies and $ savings in purchasing fixed assets to

increase production process❏ analyze # of products need to be sold to cover operating costs/expenses❏ set up monthly selling targets and bonuses for sales personnel

Chapter 16 AssignmentsComplete the following exercises and problems. Hand in as a packet when completed.

exercise 16-1, 16-3, 16-4

exercise 16-5, 16-11, 16-13

problem 16-5A