Management Presentation - ulkerbiskuvi.com.trœlker Management... · • This presentation contains...

35

Management Presentation April 2012 happy moments

Transcript of Management Presentation - ulkerbiskuvi.com.trœlker Management... · • This presentation contains...

Management Presentation

April 2012

happy moments

Disclaimer

1

• This presentation contains information and analysis on financial statements and is prepared for the sole purpose of providing

information relating to Ülker

• This presentation contains forward-looking statements which are based on certain expectations and assumptions at the time

of publication of this presentation and are subject to risks and uncertainties that could cause actual results to differ materially

from those expressed in these materials. Many of these risks and uncertainties relate to factors that are beyond Ülker’s

ability to control or estimate precisely, such as future market and economic conditions, the behavior of other market

participants, the ability to successfully integrate acquired businesses and achieve anticipated cost savings and productivity

gains as well as the actions of government regulators

• Readers are cautioned not to place undue reliance on these forward-looking statements, which apply only as of the date of

this presentation. Ülker does not undertake any obligation to publicly release any revisions to these forward-looking

statements to reflect events or circumstances after the date of these materials

• This presentation merely serves the purpose of providing information. It neither represents an offer for sale nor for

subscription of securities in any country, including Turkey. This presentation does not include an official offer of shares; an

offering circular will not be published

• This presentation is not allowed to be reproduced, distributed or published without permission or agreement of Ülker

• The figures in this presentation are rounded to provide a better overview. The calculation of deviations is based on figures

including fractions. Therefore rounding differences may occur

• Neither Ülker nor any of its managers or employees nor any other person shall have any liability whatsoever for any loss

arising from the use of this presentation

Agenda

2

Page

1. Introduction 3

2. Key Investment Highlights 8

3. Financial Snapshot 18

4. Ülker Strategy and Expectations 22

5. Appendices 24

Management speakers

Who are presenting today?

3

Mehmet Tütüncü

Chief Executive Officer Food &

Beverage

Gazi University, Mechanical

Engineering

Industrial and Organizational

Psychology, MS

Vice President, Ülker Bisküvi

and Çikolata

Yıldız Holding Executive

Committee Member

General Manager, Ülker

Bisküvi

General Manager, Best

Rothmans

Other positions

Education

Experience

31 years

16 years with Ülker

Nurtaç Ziyal

Yıldız Holding M&A, Business

Development & Investor Relations

General Manager

Friedrich Alexander

Universität, MBA

Marmara University, BA,

Business Administration

Head of Strategy, Yıldız Holding

Head of Strategy & Regulatory

Affairs, Avea

Associate Partner, Head of

Strategy & Marketing Service,

Accenture

Senior Manager, Arthur

Andersen

Other positions

Education

Experience

19 years

6 years with Ülker

Bora Yalınay

Group CFO, Confectionery

CPA

Bilkent University, BA,

Economics

Group Financial Controller,

Yıldız Holding

Audit Senior Manager,

Deloitte & Touche

Other positions

Education

Experience

15 years

3 years with Ülker

Cem Karakaş

Yıldız Holding CFO, Member

of Board of Directors

İstanbul University, Ph.D.,

Finance

Massachusetts Institute of

Technology, MBA, Finance

Middle East Technical

University, BS,

Management

CFO, Erdemir Group

Head of M&A, Oyak Group

General Manager, Oyak

Konut Real Estate

Other positions

Education

Experience

15 years

2 years with Ülker

Ülker: Leading name in Turkish confectionery

4

Biscuits

† Ülker Çikolata: Consolidated for the last quarter; Fresh cake: Not consolidated †† Stand alone figure

• Best recognized FMCG brand in the dynamic Turkish market

for 68 years

• Turkey’s leading producer of biscuits, chocolates, chocolate

covered products, crackers, wafers and cakes

• Spread out facilities representing the largest production

capacity in the domestic market and minimizing dependency

on single location

• Exports, mainly to the Middle East, Northern Africa and EU,

accounting for c.15% of sales volume

• Consolidated annual net sales of TL1.8† bn in 2011 and

estimated net sales of TL2.4 bn in 2012

• Yıldız Holding is the

parent company. It is

Turkey’s leading food

and beverages group

with annual gross

sales of TL11.6 bn as

at the end of 2011

• Yıldız Holding ranked

10th in “Global top 100

confectionery

producers list” by

Candy Industry in 2011

Shareholding Structure

• Net sales, 2010††: TL1.5 bn

• Market share 2011: 49%

• Capacity: 403 tons/year

• CUR: c.71% Biscuit

• Net sales, 2010††: TL0.2 bn

• Market share 2011: 40%

• Capacity: 45k tons/year

• CUR: c.73% Cake

• Net sales, 2010††: TL0.9 bn

• Market share 2011: 49%

• Capacity: 238k tons/year

• CUR: c.60% Chocolate

Topkapı: Biscuits,

c.62k tons/year

Topkapı: Chocolate,

c.203k tons/year

Hadımköy: Cake,

c.45k tons/year

Gebze: Biscuit &

cracker, c.49k

tons/year

Karaman: Biscuit, cracker,

chocolate, c.180k tons/year

Ankara: Biscuit,

c.112k tons/year

In Figures††

45%

21%

21%

12%2.0%

Yıldız Holding

Dynamic Growth FundFree float

Ülker Family

Önem Gıda

Silivri: Chocolate,

chocolate covered

biscuit, c.35k tons/year

Long lasting

relationships

with end users

enhance

brand

perception

Ülker: the “Best Recognized” FMCG brand

The Best in the

Sweet and Salty

Category

(Silver Effie Award,

Ülker Rondo, 2011)

Most

Recognized

Company

(AC Nielsen,

2nd place,

2010)

The “Brand

Award”

(International

Brands

Conference,

2011)

Best Recognized

Brands

Brand One Feels

Close To

# 1

# 2

# 3

# 4

# 5

• Strength of the brand is proven by national

and international awards

• Ülker has always been the “most recognized”

brand and “closest to consumers”

• Ülker brand essence and campaign theme:

“Happy moments with Ülker”

• Highly-popular sub-brands are in the market

for many years

Consistently

ranks as one

of the best

recognized

brands in

Turkey

Source: ACNielsen, public data † Arçelik is a household durable goods brand

5

†

Corporate governance

6

• 7 members, 3 of which are independent

• Encompasses 3 proactive committees, Audit, Corporate Governance and Early Detection of Risk Committees, where independent members dominate

• Simplified corporate structure improving transparency

• Diversified communication channels with investors

• Proactive attendance in investor meetings with participation in 7 local and international investor conferences in 2011. 117 investor meetings were performed in 2011

• New investor relations materials and enriched corporate website

• Expanding coverage through active communication with sector analysts. Has been covered by 7 analysts

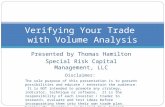

• Elimination of dividend privileges completed in 1Q 2012, giving equal dividend rights to each and every shareholder

• Employee rights are supported through comprehensive company-wide human resources policies

• Code of ethics regulating company – wide relations have been reviewed

• Improving environmental consciousness with the launch of green building project - carbon emission measurements confirm environment friendly production operations

Board of Directors

Public Disclosure

and Transparency

Shareholder Rights

Stakeholder Rights

Current

Structure

Corporate governance: Elimination of dividend-privileges of shares

Prior

Structure

7

• Cancellation of privilege

shares will be done by a

capital increase from

internal resources after the

share capital register. There

will not be any cash outflow

• All C shares will have the

same amount of dividend

right and there will be no

additional dividend privilege

attached to any share class

A 1,486 17.65% 4

B 732 17.65%

C 26,859,995,565 2

D 2,217 1

Total 26,860,000,000

Founder Certificates 22,171 11.76%

Share Class Number of Shares

Additional

Dividend

Privilege

Candidates

for Board

A 1,486 - 4

B 2,217 - 1

C 34,199,996,297 - 2

D - - -

Total 34,200,000,000

Founder Certificates - - -

Share Class Number of Shares

Additional

Dividend

Privilege

Candidates for

Board

Key Investment Highlights

Ülker story

The best recognized FMCG brand in Turkey

9

Distribution channel restructuring

– Simplification of distribution network to adopt to changing environment

– Route to a stronger but leaner distribution network

2

Corporate restructuring

– Ongoing transformation to a leaner and more sizable confectionery company by bringing all relevant companies under one umbrella and disposal of non-core assets

1

Unlocking brand potential by leveraging Ülker’s strongest sub-brands

– Leading brand since establishment

– Star sub-brand focus

– SKU optimization with focus on profitability

– Brand building programs, i.e. 360o marketing campaigns, social media, new ways of merchandising

3

A strong parent: Yıldız Holding, Turkey’s leading food and beverages group

– Started as a biscuit producer. Transformed into a mega FMCG group. Leveraged Ülker brand and penetration to launch several products in other segments

– Currently has operations in 6 sectors with TL11.6 bn gross sales in 2011

– Highly sought out as a local FMCG partner

5

Spread out production facilities

– Largest production capacity in the domestic market

– Minimizing dependency on single location

4

Biscuit production

Biscuit production

Corporate restructuring: Ülker previous structure: Too many layers was transformed into a leaner, more transparent structure

10 Production companies

1

† Indirect ownership structures

Atlas Domestic sales

İstanbul Exports: Ülker

branded products

Birleşik Exports: Non-Ülker branded products

Rekor Non-Ülker branded

products

Atlantik Chocolate sales

Godiva

Biskot Non-Ülker branded products (Biscuit &

chocolate production)

Ülker Çikolata†† Chocolate producer

51%

92%

Stake owned by Ülker Sales companies

İdeal Ülker branded

products (Biscuit & cracker production)

Biskot Non-Ülker branded products (Biscuit &

chocolate production)

Birlik Flour producer

Fresh Cake Cake production

Godiva

BIM Retail

Pendik Nişasta Starch production

Sağlam GYO REIT

Besler Oil and margarine

production

Hero Baby Baby food

Atlas Domestic sales

İstanbul Exports: Ülker

branded products

Birleşik

Exports: Non-Ülker

branded products

Rekor Non-Ülker branded

products 47%

84%

10%

25%

7%

24%

40%

10%

11%

• Previous structure:

- Multiple sales channels to promote

competition amongst sales agents

- Portfolio investments in various companies

• Layered structure, evolved due to fast growth and add-on acquisitions,

led to restructuring need

Structure† as of 31.12.2010

19%

92%

48%

91%

78%

98%

• Steps already taken:

- Ülker Çikolata, Fresh Cake and Atlantik Gıda were

acquired from Yıldız Holding

- İdeal, Birlik and Fresh Cake merged with Ülker

- Non-core operations were divested (Besler, Hero Baby,

Pendik Nişasta, BIM, Sağlam GYO)

- Part of Godiva shares divested

Financial assets

Current Structure†

Not operational as of March 1st, 2012 Will be merged with related production

companies by the end of 2012

Mavi Yeşil Ülker branded diet

products

74%

51%

99%

98% 78%

69%

Biscuit production

İstanbul Gıda

Exports: Ülker

branded products

Corporate restructuring:

Ülker target structure: Leaner with focus on core businesses

11

Target Structure

• Steps in progress:

- Merge of domestic sales subsidiaries to

related production companies

- Only export operations will remain as a

separate entity

- All domestic traditional channel sales

consolidated under single sales company

“Horizon”

1

Ülker Çikolata

Chocolate

producer

Biskot

Non-Ülker branded

products (Biscuit &

chocolate

production)

51%

92% 91%

Production companies Stake owned by Ülker Sales companies

Distribution channel restructuring:

Previous distribution system: Multichannel and layered sales network

12

• As confectionery goods remain at the

top spot for impulse purchases,

availability is the key factor

determining strength of a brand

• With c.220k sales points and c.70%

share in confectionery sales,

traditional channel dominates the

market

• Ülker’s previous domestic traditional

channel consisted of:

-235 distributors

-With c.90% nationwide coverage,

the largest food network in Turkey

• Changing market conditions dictate

restructuring in distributorship

system:

-Need for scale efficient and

organized distributors with

decreasing distributor margins

• Ülker aims to increase its operational

efficiency and margins through

restructure of its domestic traditional

distribution channel

% in domestic sales

Distribution

channels

İstanbul ††

(Ülker brand) Exports Channel Distributors

Biscuit,

Chocolate &

Cake Operations Birleşik ††

(Non-Ülker brand)

Pasifik † Domestic Modern

Channel

Organized

Retail

Chains

Biscuit,

Chocolate &

Cake Operations 25%

2

Other Food &

Beverage

Products

Atlantik

(Ülker brand)

Domestic

Traditional Channel

235

Distributors

Atlas

(Ülker brand)

Atlas

Chocolates

Biscuits

Cakes

Distributors

55%

†Yıldız Holding subsidiary ††Also responsible for sales of Yıldız Holding companies product portfolio

20%

Distribution channel restructuring:

Target: Traditional channel simplified for optimized and efficient reach

13

2

Current domestic traditional channel after restructuring:

• New sales company established in 2011

• More efficient route to market with stronger, but fewer distributors (104 vs. c.235) - same coverage in sales points

• Variety of products per sales point increased by %20

• Optimization process completed in March 2012

• Inefficiency

• High level distributor discounts • Execution difficulty

• Complexity

Main Challanges

Other Food &

Beverage

Products

Distributors

Domestic

Traditional

Channel

Biscuits

Chocolates

Cakes

Atlas

(Ülker brand)

235

Distributors

Atlantik

(Ülker brand)

Atlas

Previous

Structure:

Other Food &

Beverage

Products

Domestic

Traditional

Channel

Biscuits

Chocolates

Cakes

Horizon †

(New Sales

Company)

104

Distributors

Completed

New

Structure:

Result:

• Layers to be reduced • Better and faster execution

capability

• Fewer but stronger distributors • Decreasing distributor

discounts

• # of points visited: 140k

• % of invoice issued by visit:

75%-80%

† Owned by Yıldız Holding

• # of points visited: 175k

• % of invoice issued by visit:

90%

47% 48%42% 40%43% 40%

46% 49%

9% 12% 12% 11%

2008 2009 2010 2011Ülker Eti Other

55% 56%51% 49%

10% 11% 11%11%6% 6% 9%

11%

29% 26% 29% 29%

2008 2009 2010 2011Ülker Nestle Eti Other

57% 54% 50% 49%

32% 35% 36% 39%

11% 12% 13% 12%

2008 2009 2010 2011Ülker Eti Other

Unlocking brand potential:

Strong market share across the categories

14 † Retail market, Source: ACNielsen, Euromonitor

Market Share Development, Volume Based†

• Total size of biscuit, chocolate and cake markets is

estimated to be TL4.7 bn in value and 269k tons in

volume terms

• Loss of market share caused mainly by aggressive

product launch strategy originated by the competition

- In the short run highly demanded popular products

shifted market shares from Ülker to competition

Biscuit, Chocolate & Cake Markets†

3

Bis

cu

it

Ch

oc

ola

te

Cak

e

-10%

-5%

0%

5%

10%

15%

2007 2008 2009 2010 2011

Market Volume GrowthReal GDP Growth

strategy to competition’s attack:

• Defending the position by matching aggressive product

launches - 178 new SKUs in 2009 - 9/2011 period

• Launches supported through consistent marketing

campaigns

Unlocking brand potential:

Ülker: Streamlining product portfolio

15

3

2009 2010 2011 Future

Co

mp

eti

tio

n

• Aggressive product launches in 2008-2011 period

• New tastes, hybrid products and new packaging forms

introduced to the market

Ülk

er

2012

SKU attacks for market share by the competition

x

x

Easing SKU wars Market trends:

• Short run results:

- Highly demanded popular products shifted market

shares

• Medium term results:

- Decreasing margins due to increasing operational costs

- Increasing sales and marketing expenses

- Crowded SKU portfolios difficult to control

Imp

ac

ts o

n t

he

mark

et

.’s changing strategy and prospects for

the future:

• SKU management: Portfolio restructuring started

in late 2011

- Focus on star SKUs

- Delisting of unprofitable SKUs – Reduction from

502 SKUs in 2010 to c.370 SKUs in 2011

• Packaging & pricing optimization:

- Formulizing cost effective sizes, packaging and

pricing to quickly respond to changes in

consumer choices and raw material costs

• Brand building:

- Increasing investment on star SKUs

• Innovation:

- Introduction of new trends in snack formats to

grasp market share from newly developed and

unpackaged segments

Spread out production facilities

16 Biscuit

Chocolate

Topkapı, İstanbul Facility

• Biscuits

• Established in 1944

• Capacity: 62k tons/year

• 28 sqm closed & 15k sqm open

area

Hadımköy, İstanbul Facility

• Cake

• Established in 1992

• Capacity: 45k tons/year

• 27k sqm closed & 6k sqm open

area

Topkapı, İstanbul Facility

• Chocolate

• Established in 1991

• Capacity: 203k tons/year

• 68k sqm closed & 27k sqm

open area

Cake

Biscuit & chocolate

Gebze Facility

• Biscuit & cracker

• Established in 1997

• Capacity: 49k tons/year

• 41k sqm closed & 67k sqm

open area

Ankara Facility

• Biscuit

• Established in 1969

• Capacity: 112k tons/year

• 86k sqm closed & 123k sqm m2

open area

• The largest biscuit

manufacturing facility in the

Middle East

Karaman Facility

• Biscuit, cracker & chocolate

• Established in 1986

• Capacity: 180k tons/year

• 102k sqm closed & 116k

sqm open area

• Non-Ülker branded products

• 51% owned by Ülker

• Spread out facilities

representing the largest

production capacity in the

domestic market and

minimizing dependency

on single location

Silivri, İstanbul Facility

• Chocolate, chocolate

covered biscuit

• Established in 1995

• Capacity: 35k tons/year

• 12k sqm closed & 20k sqm total

area

4

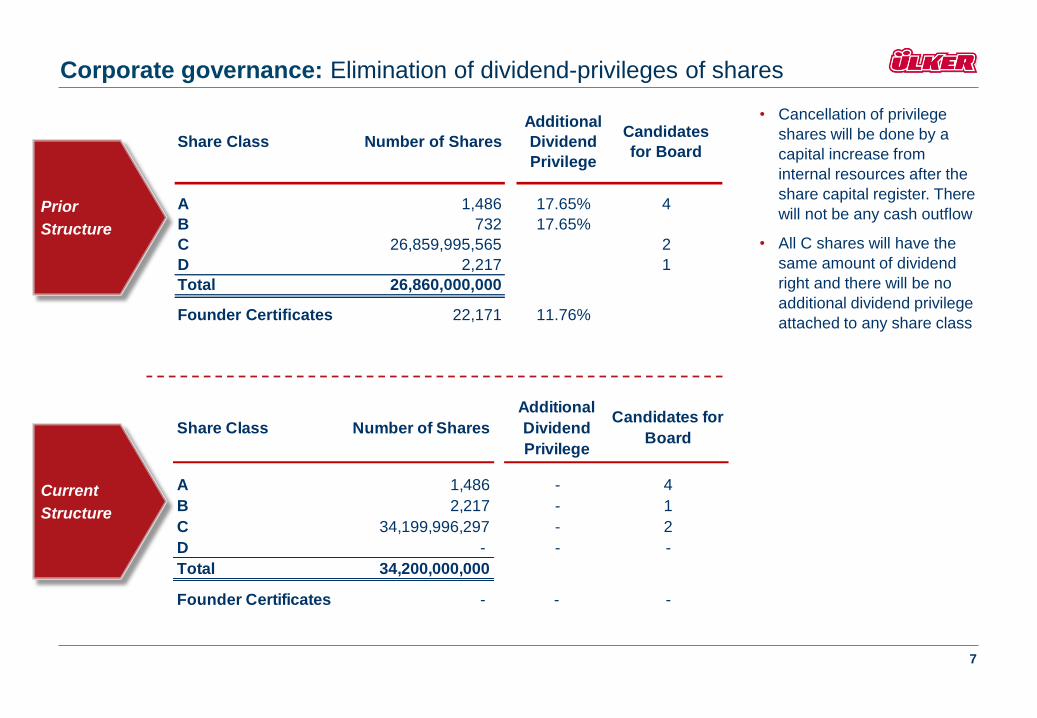

A strong parent:

Yıldız Holding

17

Food &

Beverages

Packaging

Finance

Retail

Real

Estate

Personal

Care

A prominent name in the Turkish food industry operating in confectionery,

margarine & liquid oils, culinary products, dairy products, beverages, fruit juice and frozen foods

Experience in managing international operations

JVs with leading international players Sole and first brand sought out for co-branding

Turkey's first food company to establish a nationwide distribution network

#1 Best recognized food brand #1 in biscuits & chocolates #2 in dairy products #1 in edible oils and fats #1 in overall baby food #1 in culinary products

Premium segment chocolate producer acquired in 2008

In excess of 200k sales points nationwide

c.90% coverage, second best after Coca cola

5

Financial Snapshot

1,506 1,5241,799

906 844

153 172

2009 2010 2011

Biscuit Chocolate Cake

265 269

328

97 8831 33

2009 2010 2011

Biscuit Chocolate Cake

Stable revenue generation, attention to increasing costs

19

Development of Sales, k tons

Development of Net Sales, TL mn

Merchandise sales

Exports as % of net sales

Raw Material Cost Index††

• Stable volume and turnover despite increasing

competition from other producers as well as substitute

products

• Limited pricing power due to inherent pricing difficulty

• Revenue drivers are mainly, occasional nominal price

increases, product redesigning, decrease in distribution

costs and volume growth compensate with market

growth

• Raw material costs have between 75%-85% share in

costs in all categories

• Margins hurt by increasing commodity prices as

continuously reflecting cost inflation to prices is difficult

% Sales from production † Following acquisition of Ülker Çikolata in 2011, chocolate operations has

been consolidated in 2011 figures for the last quarter †† Wheat and sugar base price is determined by the Turkish Government

0

50

100

150

200

250

300

350 Cocoa bean price index Palm oil price indexWheat price index Sugar Price Index

16% 8% 9% 16% 9% 15% 25%

22% 4% 7% 18% 5% 10% 20%

2009 2010 2011†

Biscuit Chocolate Cake 2011 consolidated figures

2009 2010 2011†

Biscuit Chocolate Cake 2011 consolidated figures

74%

79%

76%

77%

10%

4% 4%

9%

2%2%

8%

2009 2010 2011

Biscuit Chocolate Cake

Margins hit the bottom

20

EBITDA, TL mn

EBITDA Margins, %

Summary Financials†, TL mn

† Stand alone figures

• In 2012, Ülker is forecast to post net sales of

TL2.3-TL2.5 bn with an EBITDA margin changing

in 7.5%-8.5% range

• EBITDA margin is expected to reach 12% levels in

2014

• Gross margin is expected to improve with

stabilizing commodity prices and increased control

on cost base

†† Following acquisition of Ülker Çikolata in 2011, chocolate operations has been consolidated in 2011 financials for the last quarter

Biscuit 2009 2010 9/2011 2011††Net Sales 1,506 1,524 1,090 1,799Gross Profit 379 326 223 364GP Margin % 25% 21% 20% 20%EBITDA 144 67 42 75EBITDA Margin % 10% 4% 4% 4%

Biscuit 2009 2010 9/2011 2011††Net Sales 1,506 1,524 1,090 1,799Gross Profit 379 326 223 364GP Margin % 25% 21% 20% 20%EBITDA 144 67 42 75EBITDA Margin % 10% 4% 4% 4%

2009 2010 2011††

Biscuit Chocolate Cake 2011 consolidated figures

144

67 7578

173 14

2009 2010 2011

Biscuit Chocolate Cake

2009† 2010† 2011††

Biscuit Chocolate Cake 2011 consolidated figures

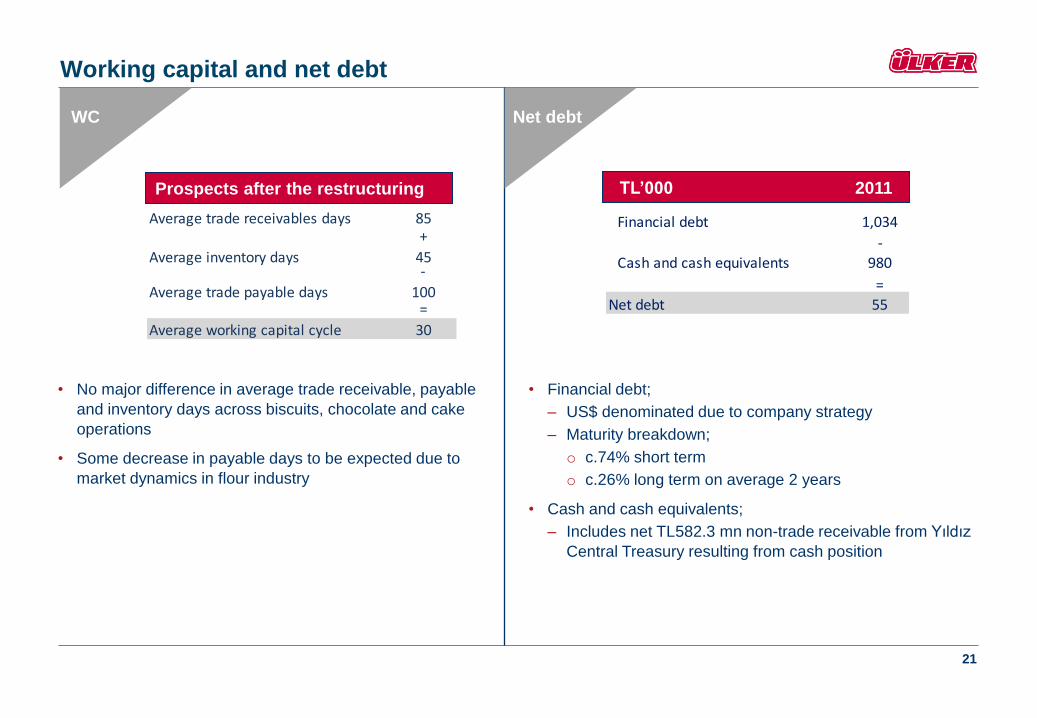

Working capital and net debt

21

WC Net debt

TL’000 2011

• Financial debt;

– US$ denominated due to company strategy

– Maturity breakdown;

o c.74% short term

o c.26% long term on average 2 years

• Cash and cash equivalents;

– Includes net TL582.3 mn non-trade receivable from Yıldız

Central Treasury resulting from cash position

Average trade receivables days 85+

Average inventory days 45-

Average trade payable days 100=

Average working capital cycle 30

Prospects after the restructuring

• No major difference in average trade receivable, payable

and inventory days across biscuits, chocolate and cake

operations

• Some decrease in payable days to be expected due to

market dynamics in flour industry

Financial debt 1,034

-

Cash and cash equivalents 980

=

Net debt 55

Ülker Strategy and Expectations

Ülker strategy and expectations

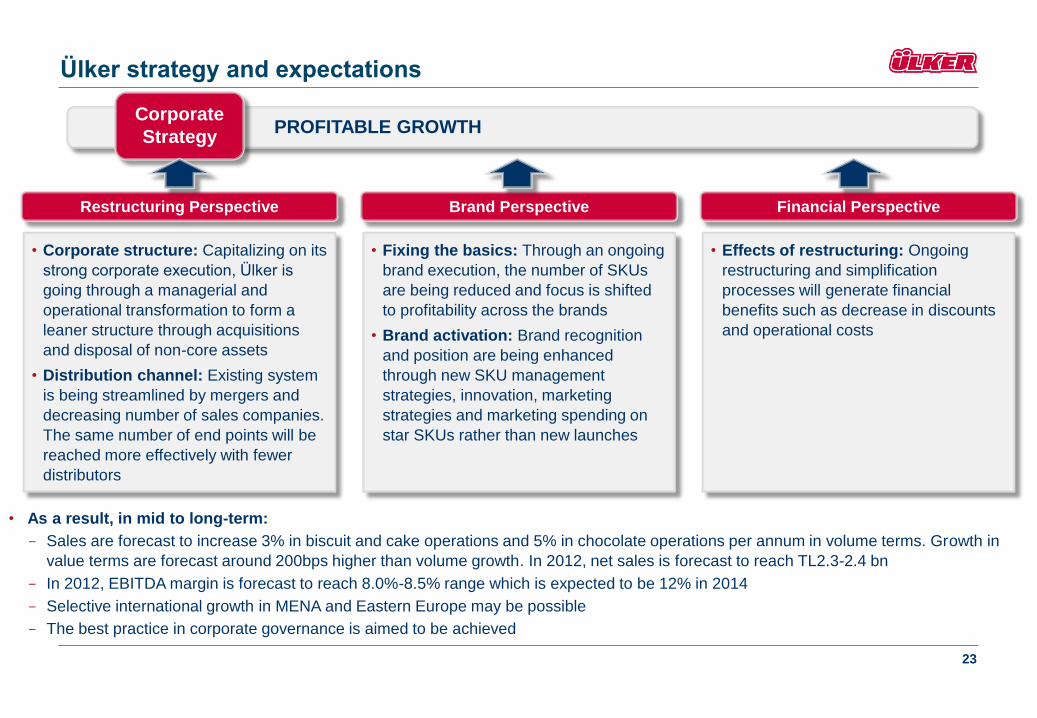

23

PROFITABLE GROWTH Corporate

Strategy

• As a result, in mid to long-term:

- Sales are forecast to increase 3% in biscuit and cake operations and 5% in chocolate operations per annum in volume terms. Growth in

value terms are forecast around 200bps higher than volume growth. In 2012, net sales is forecast to reach TL2.3-2.4 bn

- In 2012, EBITDA margin is forecast to reach 8.0%-8.5% range which is expected to be 12% in 2014

- Selective international growth in MENA and Eastern Europe may be possible

- The best practice in corporate governance is aimed to be achieved

Brand Perspective

• Fixing the basics: Through an ongoing

brand execution, the number of SKUs

are being reduced and focus is shifted

to profitability across the brands

• Brand activation: Brand recognition

and position are being enhanced

through new SKU management

strategies, innovation, marketing

strategies and marketing spending on

star SKUs rather than new launches

Restructuring Perspective

• Corporate structure: Capitalizing on its

strong corporate execution, Ülker is

going through a managerial and

operational transformation to form a

leaner structure through acquisitions

and disposal of non-core assets

• Distribution channel: Existing system

is being streamlined by mergers and

decreasing number of sales companies.

The same number of end points will be

reached more effectively with fewer

distributors

Financial Perspective

• Effects of restructuring: Ongoing

restructuring and simplification

processes will generate financial

benefits such as decrease in discounts

and operational costs

Appendices

A. Financial Statements

Income statements (TL mn) 2008 2009 2010 2011††

Sales Revenue 1,412 1,506 1,524 1,799

Cost of Sales (1,106) (1,128) (1,197) (1,435)

Gross Profit 306 378 326 364

Gross Profit Margin % 22% 25% 21% 20%

OPEX (235) (266) (286) (319)

Marketing, Sales and Distribution Expenses (182) (200) (228) (252)

General Administration Expenses (52) (65) (57) (65)

Research and Development Expenses (1) (1) (1) (3)

Other Operating Income / Expense 26 34 18 66

Operating Profit 97 146 58 111

Operating Profit Margin % 7% 10% 4% 6%

Share in net profit of inv. accounted for equity method (15) (3) (14) (13)

Finance Incomes / Expenses (58) 2 179 621

Profit Before Taxation 24 145 224 720

Tax Charge From Continued Operations (4) (25) (32) (51)

Net Profit 20 120 191 669

EBITDA 95 144 67 75

EBITDA Margin 6.7% 9.5% 4.4% 4.2%

Income statements

26 †9M 2011 income statement does not include chocolate operations

†† 2011 income statement does not include Fresh Cake figures, whereas chocolate operations has been consolidated solely for the last quarter

Other highlights (TL mn) 2008 2009 2010 2011

Short-Term 484 540 451 764

Long-Term 345 241 508 270

Total Financial Liabilities 829 781 959 1,034

Net Debt 203 (36) 48 55

EPS (TL) 0.06 0.38 0.69 2.45

Balance sheets (TL mn) 2008 2009 2010 2011

Current Assets 1,121 1,486 1,512 1,824

Non-current Assets 913 1,243 1,374 847

Total Assets 2,034 2,729 2,886 2,670

Current Liabilities 901 1,254 785 1,262

Non-current Liabilities 377 289 573 312

Shareholders Equity 756 1,186 1,527 1,097

Total Liabilies & Shr Equity 2,034 2,729 2,886 2,670

Balance sheets and highlights

27 9M 2011 balance sheet includes chocolate operations

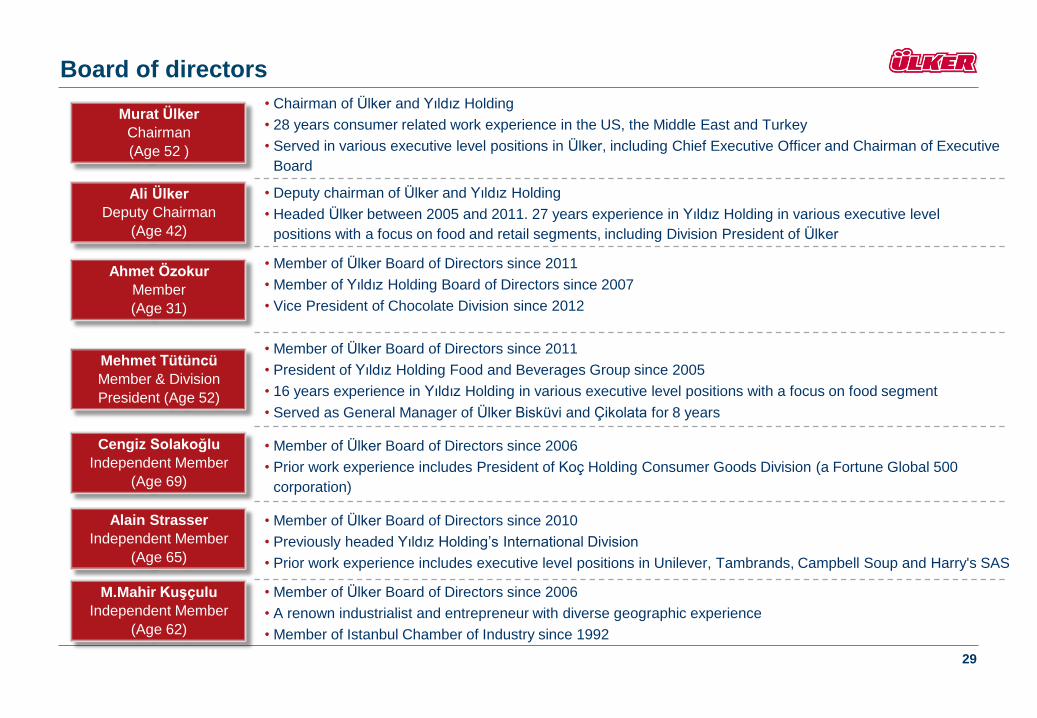

B. Board of Directors

• Member of Ülker Board of Directors since 2006

• Prior work experience includes President of Koç Holding Consumer Goods Division (a Fortune Global 500

corporation)

Board of directors

29

Murat Ülker

Chairman

(Age 52 )

Ali Ülker

Deputy Chairman

(Age 42)

Ahmet Özokur

Member

(Age 31)

Mehmet Tütüncü

Member & Division

President (Age 52)

Cengiz Solakoğlu

Independent Member

(Age 69)

M.Mahir Kuşçulu

Independent Member

(Age 62)

Alain Strasser

Independent Member

(Age 65)

• Chairman of Ülker and Yıldız Holding

• 28 years consumer related work experience in the US, the Middle East and Turkey

• Served in various executive level positions in Ülker, including Chief Executive Officer and Chairman of Executive

Board

• Deputy chairman of Ülker and Yıldız Holding

• Headed Ülker between 2005 and 2011. 27 years experience in Yıldız Holding in various executive level

positions with a focus on food and retail segments, including Division President of Ülker

• Member of Ülker Board of Directors since 2011

• Member of Yıldız Holding Board of Directors since 2007

• Vice President of Chocolate Division since 2012

• Member of Ülker Board of Directors since 2011

• President of Yıldız Holding Food and Beverages Group since 2005

• 16 years experience in Yıldız Holding in various executive level positions with a focus on food segment

• Served as General Manager of Ülker Bisküvi and Çikolata for 8 years

• Member of Ülker Board of Directors since 2010

• Previously headed Yıldız Holding’s International Division

• Prior work experience includes executive level positions in Unilever, Tambrands, Campbell Soup and Harry's SAS

• Member of Ülker Board of Directors since 2006

• A renown industrialist and entrepreneur with diverse geographic experience

• Member of Istanbul Chamber of Industry since 1992

C. Yıldız Holding

Yıldız Holding – A household name in Turkish food sector

• Turkey’s leading Food & Beverages Group

• One of the Turkey’s leading and oldest

conglomerates - founded in 1944

• Consistently ranked among Turkey's most

respected companies

• Operating 70 companies – 14 of group

companies listed on Turkey's 500 largest

manufacturing companies

• Has formed partnerships with many foreign

international companies including Cargill,

Kellogg’s, Eckes Granini & McCormick

• 54 factories – 9 located abroad, Belgium, USA,

Italy, Saudi Arabia, Pakistan, Egypt, Ukraine,

Kazakhstan, Romania

• Employs a workforce of 30,000

• Consolidated gross sales of TL11.6 bn generated

from more than 70 countries in 2011

31

Development of Turnover, TL bn

Selected Partners Selected Products

Packaging

Edible oils

Cakes Chocolates Dairy

Biscuits Beverage

Personal Care

910.1 10.5

11.6

2008 2009 2010 2011

Yıldız Holding – A leading, world-class food and beverages group

32

Finance

Retail

Personal

Care

Packaging

Food &

Beverages

Yıldız Holding

Listed Companies

Real

Estate

Listed Yıldız Holding Companies

Company MCAP†

(TL mn)

Revenue††

(TL mn)

Saf REIT 1,188 6

Bizim Toptan 890 1,733

Gözde Financial

Services 498 77

Kerevitaş 191 210

FFK Fon

Leasing 77 13

Duran Doğan 35 63

† Market capitalization as of March 6th, 2012 † † Revenue figures show 2011 full year for Bizim Toptan and 9M2011 for other companies

2011 • Yıldız Holding and SCA established a 50%-50% partnership in 2011

• Partnership is responsible for the production and marketing of Yıldız Holding’s line of brand name personal

care products

Yıldız Holding – Successful track record of partnerships

2003

2005

1993

2009

• Yıldız Holding and Cerestar 50% - 50% partnership was established in 1993

• The partnership was renewed between Ülker and Cargill after the acquisition of Cerestar by Cargill

• Cargill is the biggest family owned company in the world

• Yıldız Holding and Hero AG of Switzerland 50% - 50% partnership was established in 2003

• Ülker Hero Baby is the first domestic baby food brand of Turkey

• Products have been exported to certain overseas destinations via the distribution network of Hero

• For the first time Hero brand is used with another name

• Yıldız Holding and Kellog established a 50% - 50% partnership in 2005

• Ülker is the first and the only firm in the world Kellog has used dual branding

• Ülker became the only brand name that was allowed to appear beside the Kellogg’s name on labels of its

products

• Yıldız Holding and Gumlink established a 50%-50% partnership in 2009

• Partnership is producing innovative products in the gum and confectionery sectors and aims to surpass

US$400 mn turnover in 5 years

2010 • Yıldız Holding and SCA established a partnership in 2010

• Partnership is providing tea under OBAÇAY brand

2010 • Yıldız Holding and McCormick established a 50%-50% partnership in 2010

• Partnership is providing high quality branded herbs and spices range

2010 • Yıldız Holding and Eckes Granini established a 50%-50% partnership in 2010

• Production of innovative products in the Turkish fruit juice sector

33

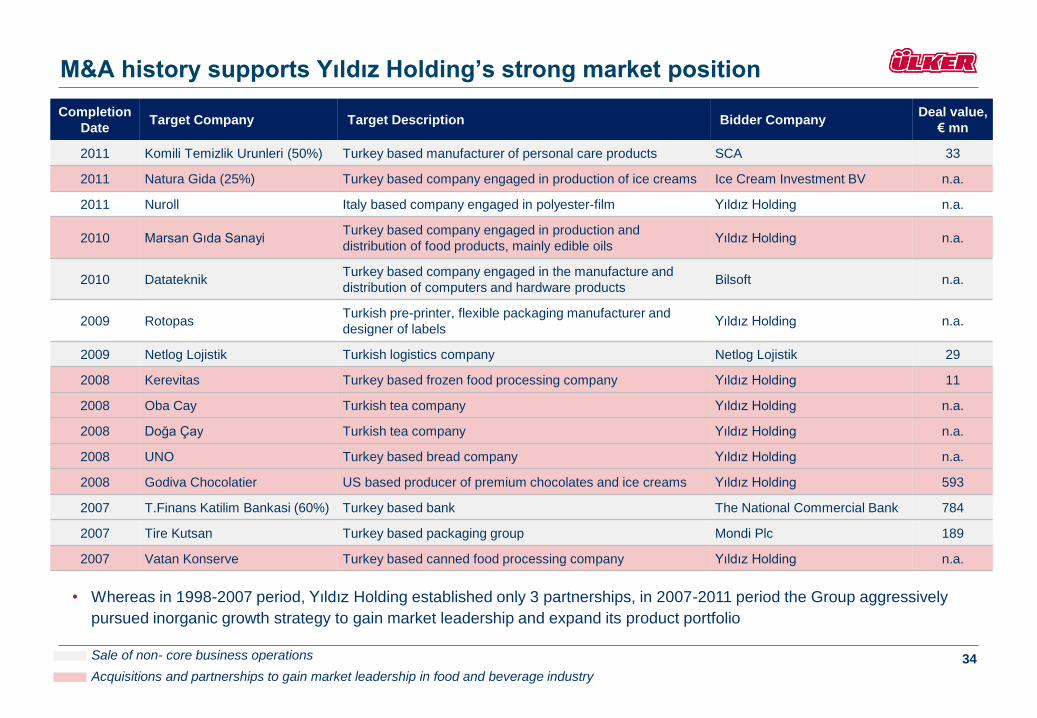

M&A history supports Yıldız Holding’s strong market position

34

Completion

Date Target Company Target Description Bidder Company

Deal value,

€ mn

2011 Komili Temizlik Urunleri (50%) Turkey based manufacturer of personal care products SCA 33

2011 Natura Gida (25%) Turkey based company engaged in production of ice creams Ice Cream Investment BV n.a.

2011 Nuroll Italy based company engaged in polyester-film Yıldız Holding n.a.

2010 Marsan Gıda Sanayi Turkey based company engaged in production and

distribution of food products, mainly edible oils Yıldız Holding n.a.

2010 Datateknik Turkey based company engaged in the manufacture and

distribution of computers and hardware products Bilsoft n.a.

2009 Rotopas Turkish pre-printer, flexible packaging manufacturer and

designer of labels Yıldız Holding n.a.

2009 Netlog Lojistik Turkish logistics company Netlog Lojistik 29

2008 Kerevitas Turkey based frozen food processing company Yıldız Holding 11

2008 Oba Cay Turkish tea company Yıldız Holding n.a.

2008 Doğa Çay Turkish tea company Yıldız Holding n.a.

2008 UNO Turkey based bread company Yıldız Holding n.a.

2008 Godiva Chocolatier US based producer of premium chocolates and ice creams Yıldız Holding 593

2007 T.Finans Katilim Bankasi (60%) Turkey based bank The National Commercial Bank 784

2007 Tire Kutsan Turkey based packaging group Mondi Plc 189

2007 Vatan Konserve Turkey based canned food processing company Yıldız Holding n.a.

Sale of non- core business operations

Acquisitions and partnerships to gain market leadership in food and beverage industry

• Whereas in 1998-2007 period, Yıldız Holding established only 3 partnerships, in 2007-2011 period the Group aggressively

pursued inorganic growth strategy to gain market leadership and expand its product portfolio