MANAGEMENT DECISIONS AND FINANCIAL ACCOUNTING REPORTS Baginski & Hassell Electronic presentation...

36

MANAGEMENT DECISIONS AND FINANCIAL ACCOUNTING REPORTS Baginski & Hassell Electronic presentation adaptation by Dr. Barbara L. Hassell & Dr. Harold O. Wilso

-

Upload

willa-richard -

Category

Documents

-

view

217 -

download

0

Transcript of MANAGEMENT DECISIONS AND FINANCIAL ACCOUNTING REPORTS Baginski & Hassell Electronic presentation...

MANAGEMENT DECISIONS AND FINANCIAL

ACCOUNTING REPORTSBaginski & Hassell

Electronic presentation adaptation byDr. Barbara L. Hassell & Dr. Harold O. Wilson

Chapter 6

Investment Decisions: (Investments in Productive Assets)

• Topics

– Property, plant and equipment

– Natural resources

– Intangible assets

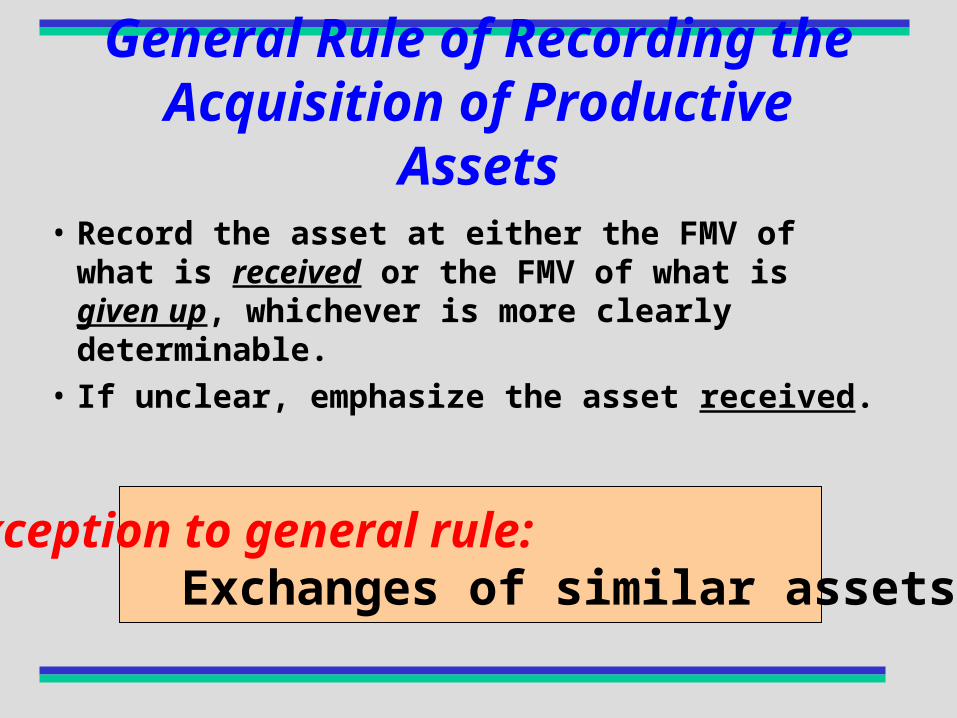

General Rule of Recording the Acquisition of Productive Assets

• Record the asset at either the FMV of what is received or the FMV of what is given up, whichever is more clearly determinable.

• If unclear, emphasize the asset received.

Exception to general rule: Exchanges of similar assets.

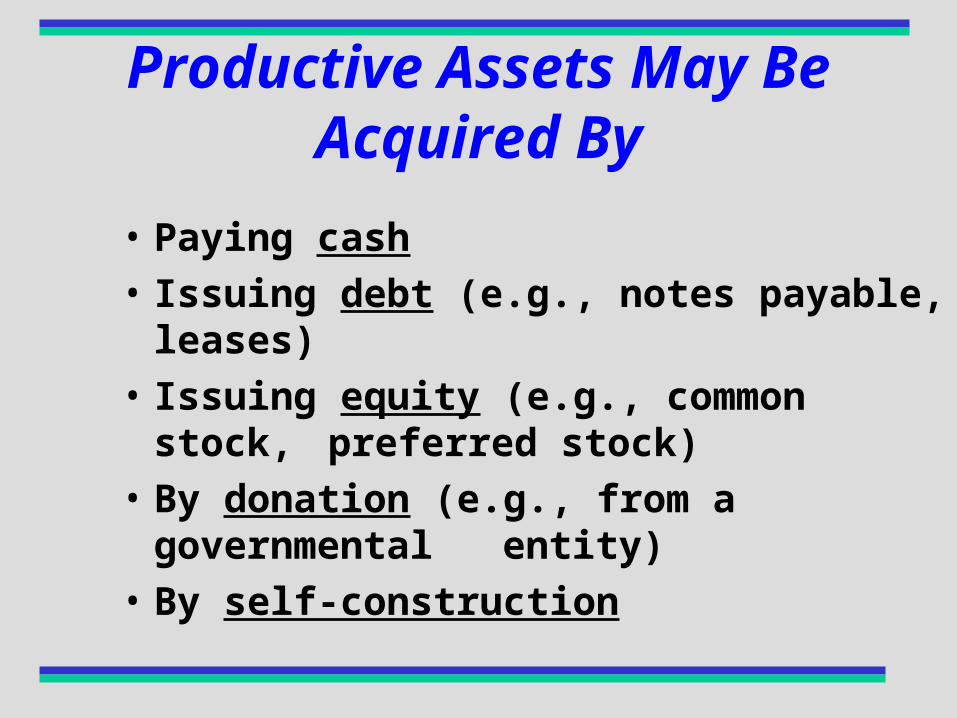

Productive Assets May Be Acquired By

• Paying cash

• Issuing debt (e.g., notes payable, leases)

• Issuing equity (e.g., common stock, preferred stock)

• By donation (e.g., from a governmental entity)

• By self-construction

Property, plant & equipment

PPEq defined: Assets that have the four characteristics of being [TURN] ...

• tangible,

• used in the operations of the business,

• relatively long-lived, and

• not intended for resale.

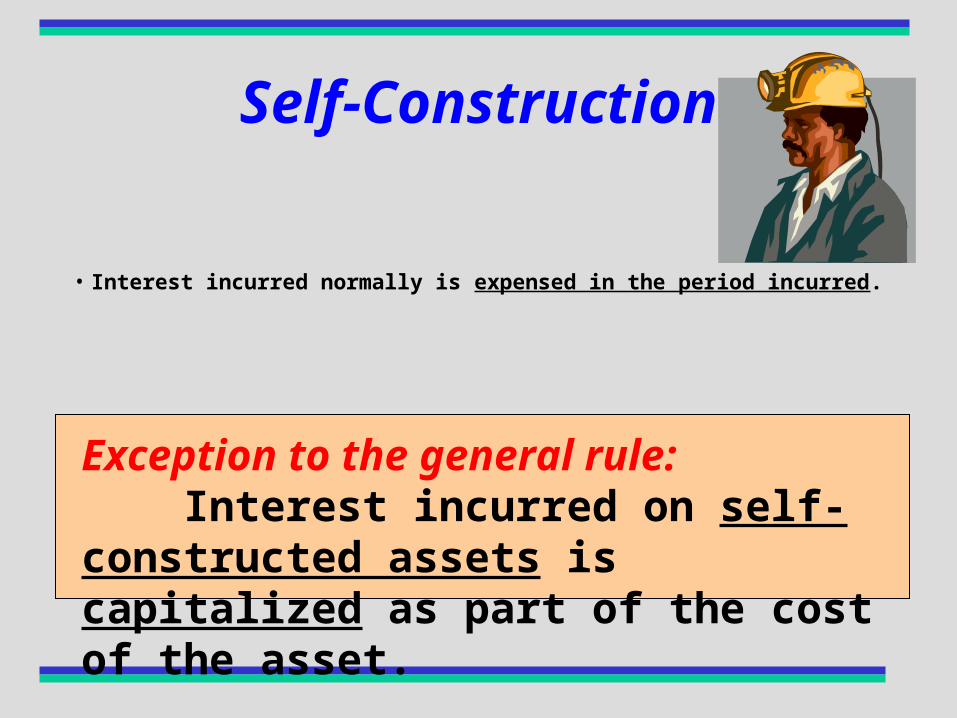

Self-Construction

• Interest incurred normally is expensed in the period incurred.

Exception to the general rule: Interest incurred on self-constructed assets is capitalized as part of the cost of the asset.

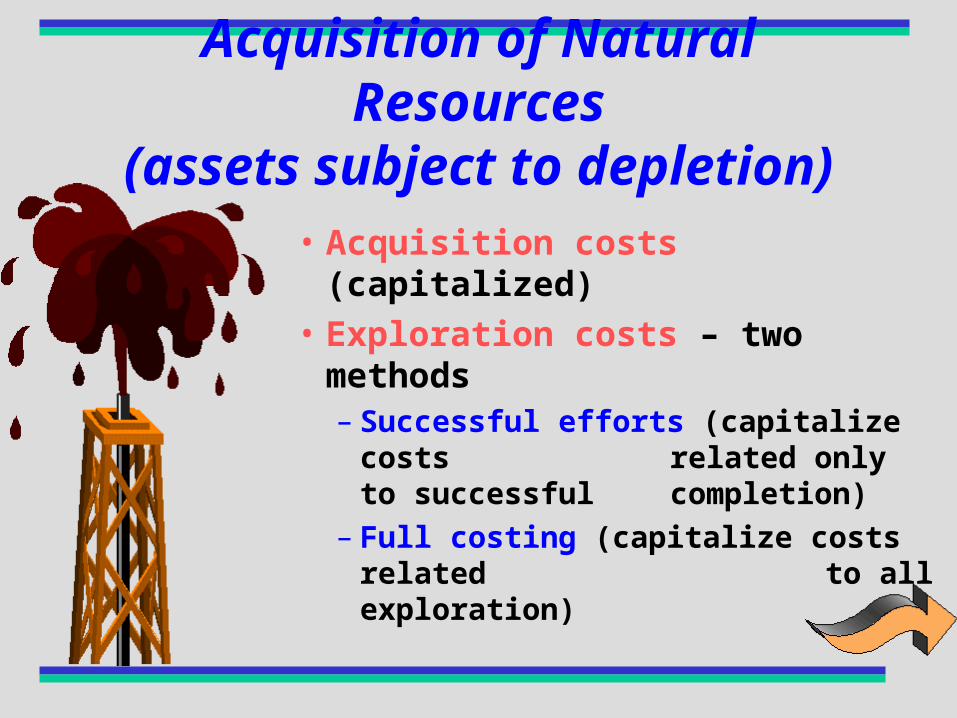

Acquisition of Natural Resources(assets subject to depletion)

• Acquisition costs (capitalized)• Exploration costs – two methods

– Successful efforts (capitalize costs related only to successful

completion)– Full costing (capitalize costs related

to all exploration)

• Development costs– Tangible: Capitalized as part of the asset (e.g.,

equipment)– Intangible: Capitalized as part of the natural

resource

• Estimated reclamation (restoration) costs (to be incurred at end of project) are part of depletion base.

Intangible Assets• Specifically identifiable

– Patents– Copyrights– Trademarks and tradenames– Franchises– Organization costs

• Unidentifiable– Goodwill

See anything?

Research and Development

• Expensed as incurred!

Note: R&D is viewed as an asset (capitalized) if related to services performed under contract for which reimbursement will be realized.

Expenditures After Acquisition

• Revenue Expenditures – Expensed (e.g., normal maintenance, etc.) by definition.

• Capital Expenditures – Capitalized (e.g., additions, betterments, etc.) by definition.

I wonder what they’ll debit?

Cost Allocation Processes

• Depreciation (applies to long-lived tangible assets): The estimated cost of the utility extracted from property, plant & equipment assets.

• Depletion (applies to natural resources): The cost of natural resource units removed (e.g., mined) from the source of such natural resources, for consumption or resale.

Observations ...Amortization is a term ordinarily applied to a “writing-off” of some defined intangible asset, similar to depreciation when used as a verb.

Depreciation accounting is the process of systematically allocating depreciation [expense] to time frames.

Cost Allocation Methods

• Straight-line (SL) technique– Uniform allocation to defined time frames.

• Declining-balance technique– Double (200%) declining balance (DDB)– 150% declining balance (1.5 DB)

• Units-of-output technique– Uniform allocation to defined units (of the

estimated output of the asset over its life)

Cost Allocation Processes and Methods

• Depreciable assets – Straight line is predominant method (*)

• Natural resources – Units-of-output is predominant method

• Intangible assets – Straight line is predominant method

(*) Note: The unit-of-output, e.g., flight hours, may be used on airplane motors, etc.

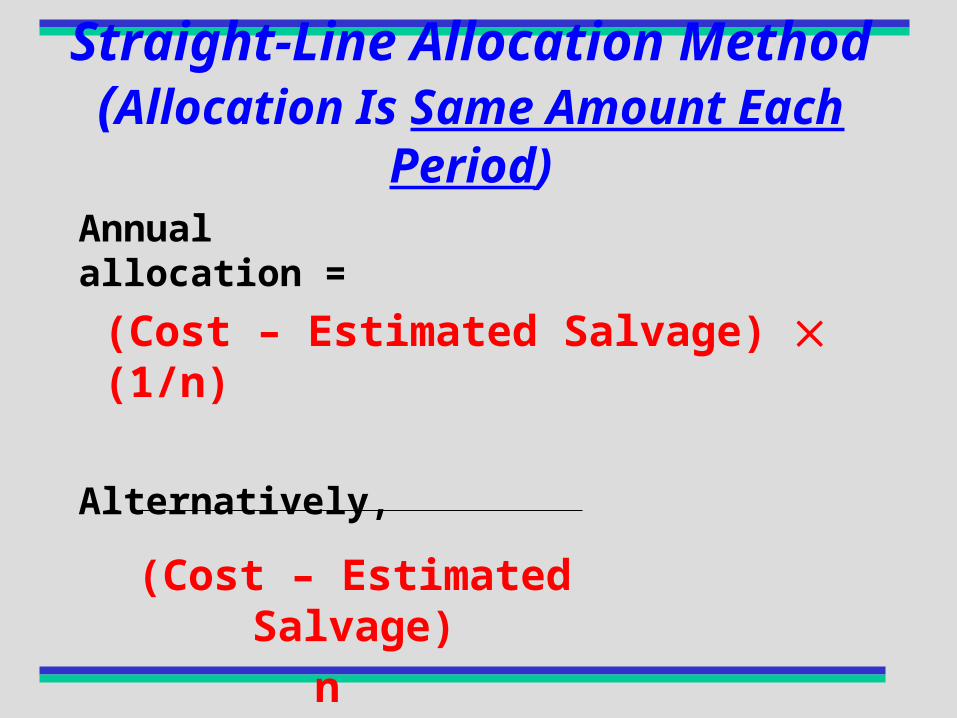

Straight-Line Allocation Method (Allocation Is Same Amount Each Period)

Annual allocation =

(Cost – Estimated Salvage) (1/n)

Alternatively,

(Cost – Estimated Salvage)

n

where, n = estimated useful life

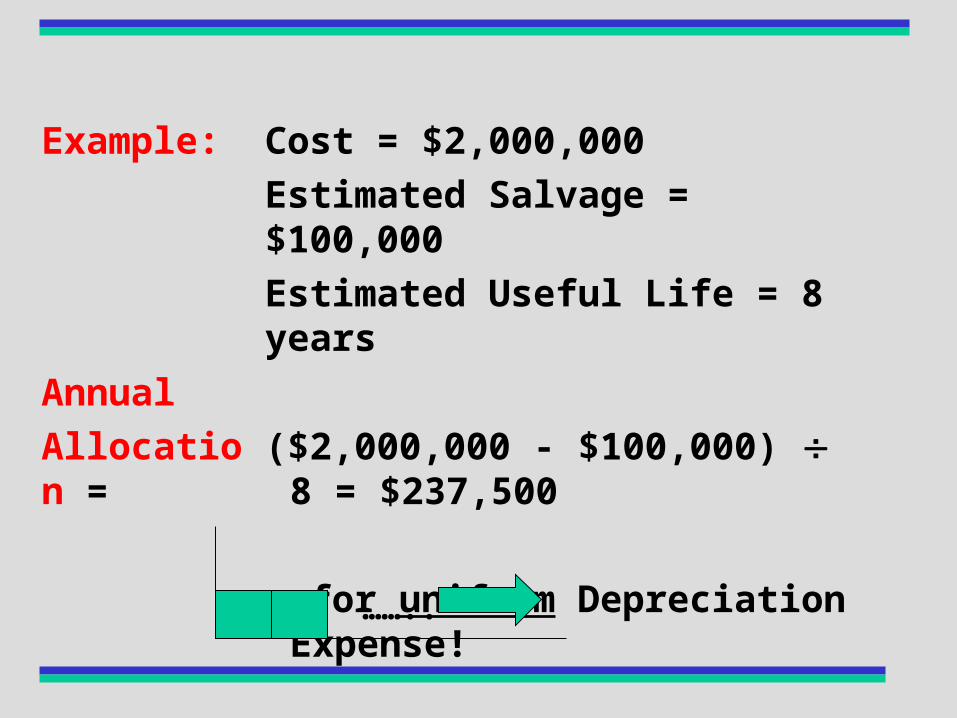

Example: Cost = $2,000,000

Estimated Salvage = $100,000

Estimated Useful Life = 8 years

Annual

Allocation = ($2,000,000 - $100,000) 8 = $237,500

for uniform Depreciation Expense!

……..

Declining-Balance Allocation Methods (Allocation Declines Each Period)

Annual

Allocation = (Beginning of the year book value)

(1 n)

(declining balance percentage)

Example: Cost = $2,000,000

Estimated Salvage = $100,000

Estimated Useful Life = 8 years

Use Double-Declining Balance

Year 1 Allocation to depreciation expense =

$2,000,000 (1 8) 200% = $500,000

Year 2 Allocation to depreciation expense =

($2,000,000 - $500,000) (1 8) 200% = $375,000

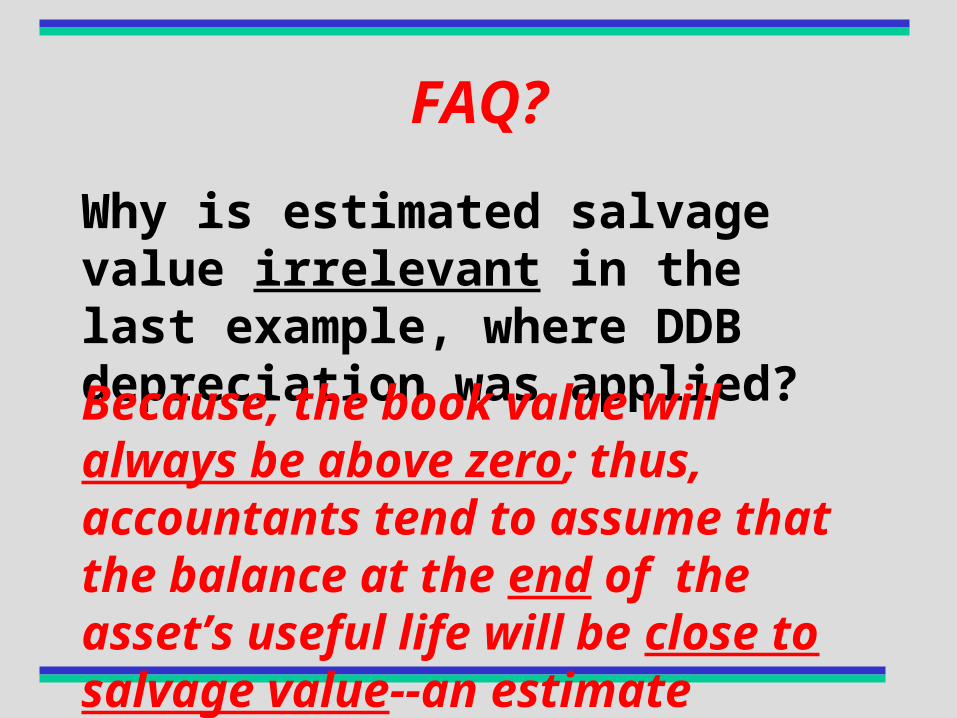

FAQ?

Why is estimated salvage value irrelevant in the last example, where DDB depreciation was applied?

Because, the book value will always be above zero; thus, accountants tend to assume that the balance at the end of the asset’s useful life will be close to salvage value--an estimate anyway!

Units-of-Output Allocation Method (Allocation Varies Each Period Depending

upon Output)

Annual Allocation =

(Cost – Estimated Salvage) (Current Year’s Output)

Estimated Total Output

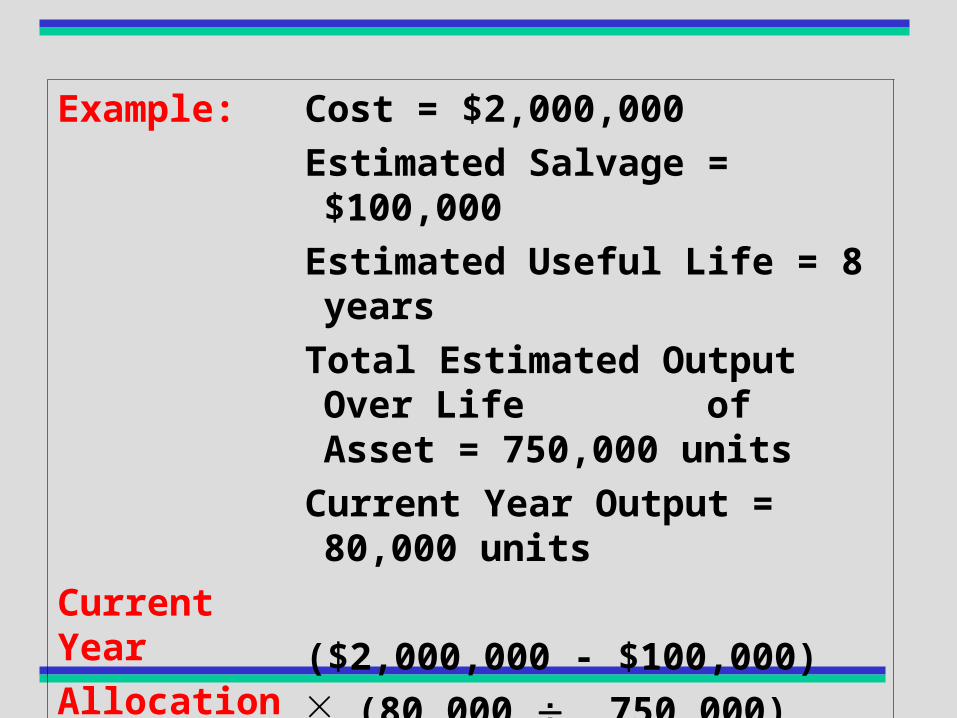

Example: Cost = $2,000,000

Estimated Salvage = $100,000

Estimated Useful Life = 8 years

Total Estimated Output Over Life of Asset = 750,000

units

Current Year Output = 80,000 units

Current Year

Allocation = ($2,000,000 - $100,000) (80,000 750,000)

= $202,667

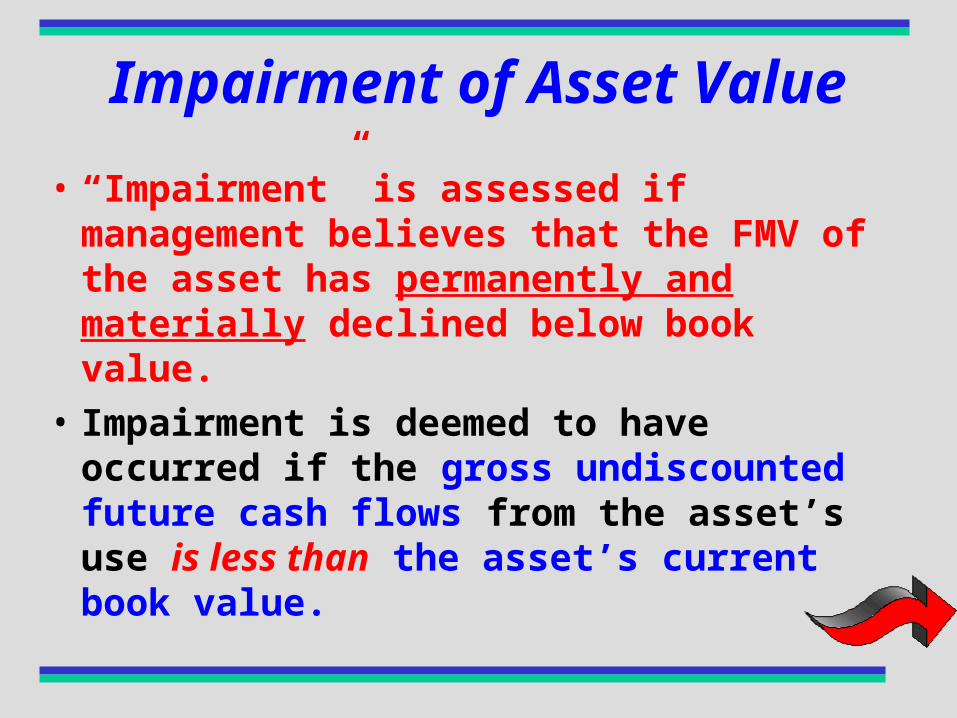

Impairment of Asset Value

• “Impairment” is assessed if management believes that the FMV of the asset has permanently and materially declined below book value.

• Impairment is deemed to have occurred if the gross undiscounted future cash flows from the asset’s use is less than the asset’s current book value.

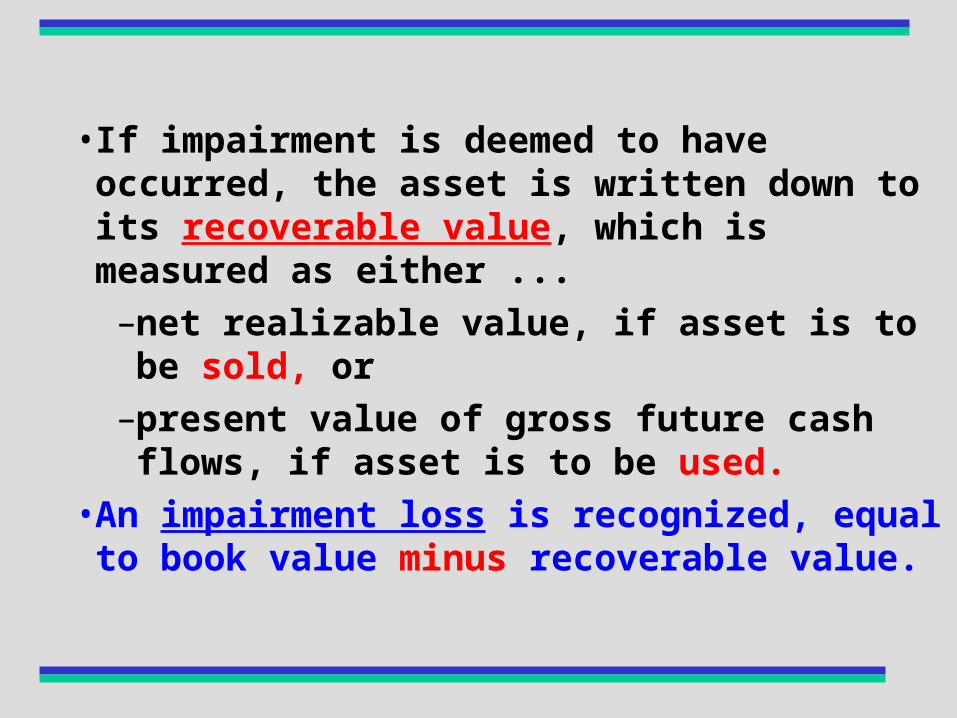

• If impairment is deemed to have occurred, the asset is written down to its recoverable value, which is measured as either ...

–net realizable value, if asset is to be sold, or

–present value of gross future cash flows, if asset is to be used.

• An impairment loss is recognized, equal to book value minus recoverable value.

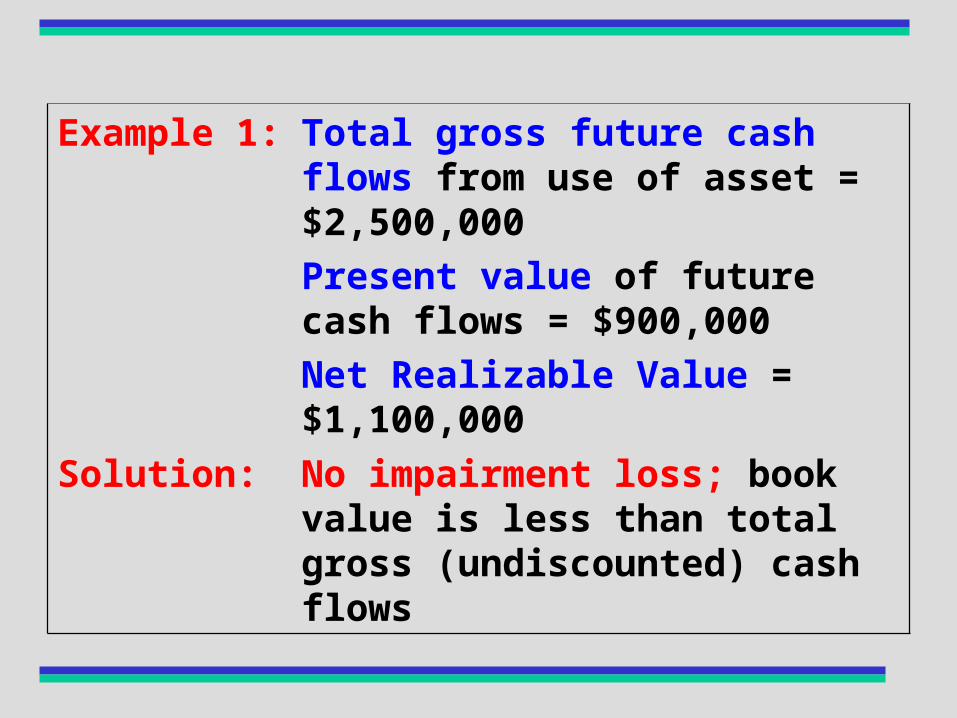

Impairment Examples

Facts:

Book Value = $2,000,000 cost - $750,000 accumulated depreciation = $1,250,000

Example 1: Total gross future cash flows from use of asset = $2,500,000

Present value of future cash flows = $900,000

Net Realizable Value = $1,100,000

Solution: No impairment loss; book value is less than total gross (undiscounted) cash flows

Example 2: Total gross future cash flows from use of asset = $900,000

Present value of future cash flows = $700,000

Net realizable value = $600,000

Solution: The asset is considered impaired because book value of $1,250,000 is greater than total gross (undiscounted) cash flows of $900,000

Financial Statement Effects:

The asset is written down to $600,000 if the asset is to be sold, and an impairment loss of $650,000 ($1,250,000 book value - $600,000 net realizable value) is recognized.

The asset is written down to $700,000 if the asset is to be used, and an impairment loss of $550,000 ($1,250,000 book value – $700,000 present value) is recognized.

Capital Budgeting

GO!

NO GO!

To invest or not to invest in a capital asset?

• Basic decision variables: IRR (internal rate of return) and NPV (net present value) analyses as criteria for a “GO” decision:

• IRR: Higher IRR projects are preferred; the IRR of a proposed project must exceed the firm’s after-tax cost of capital !

• NPV: Higher NPV projects are preferred; the NPV of a proposed project must be positive for acceptance!

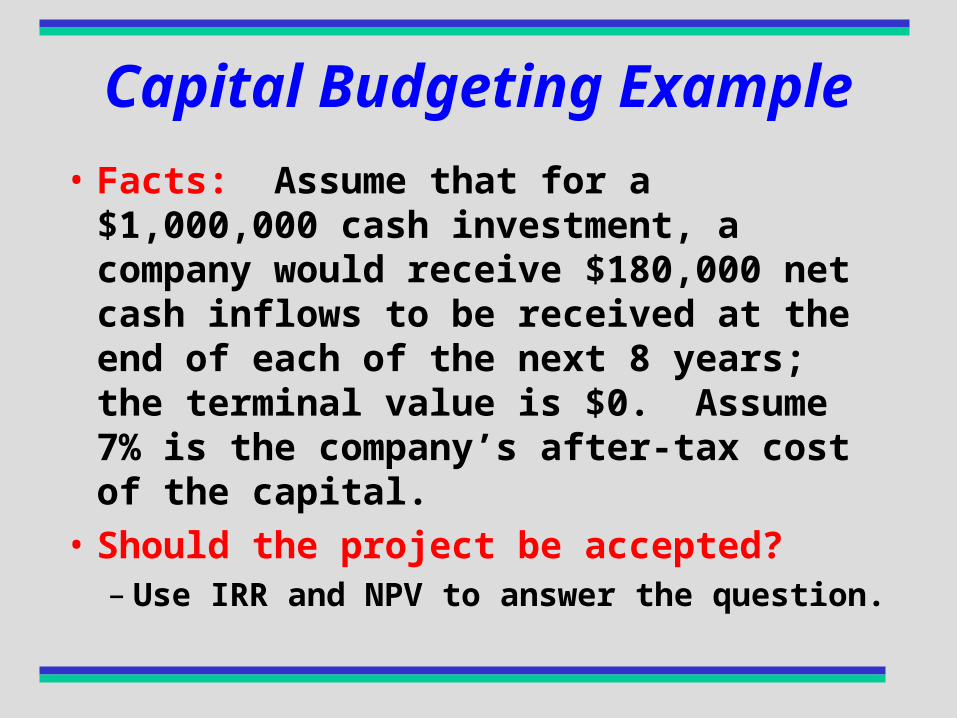

Capital Budgeting Example

• Facts: Assume that for a $1,000,000 cash investment, a company would receive $180,000 net cash inflows to be received at the end of each of the next 8 years; the terminal value is $0. Assume 7% is the company’s after-tax cost of the capital.

• Should the project be accepted? – Use IRR and NPV to answer the question.

Solution:

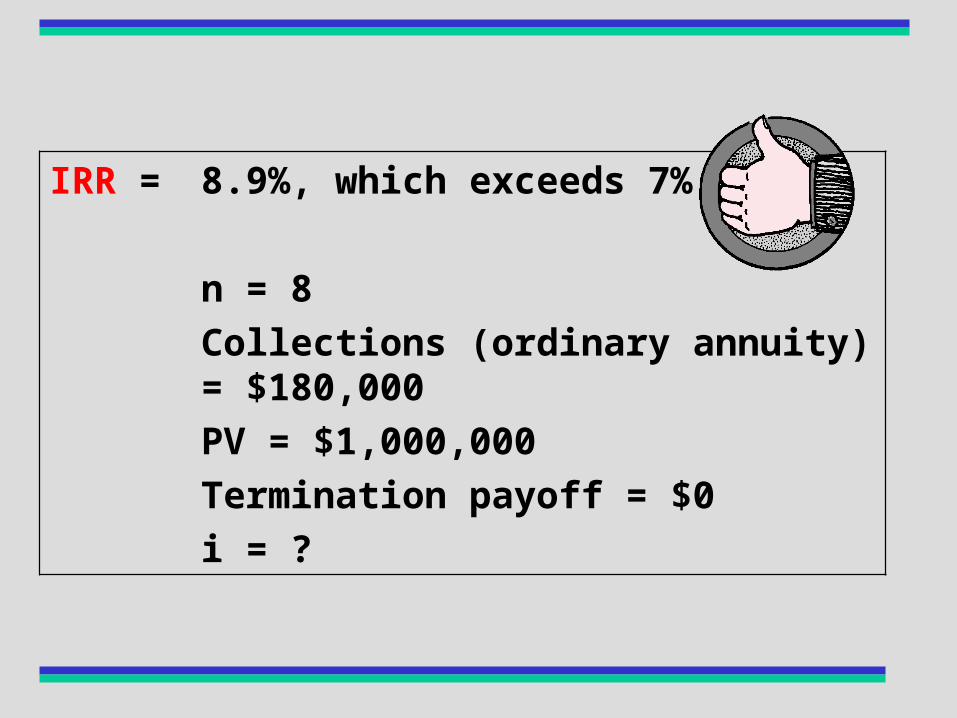

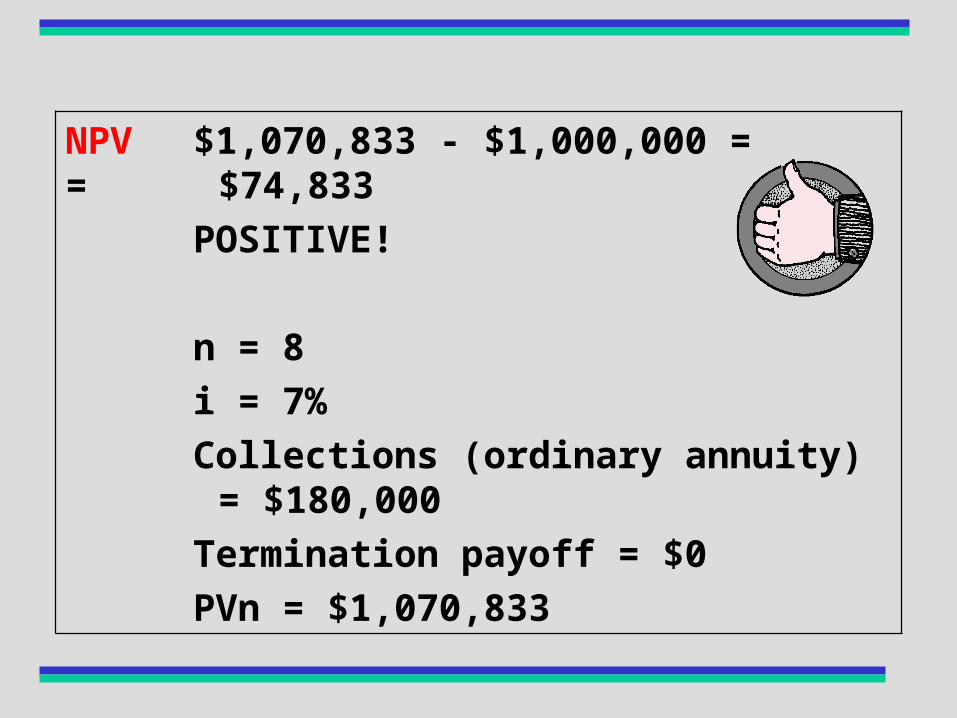

The project is worth considering . It has a positive NPV, and the IRR is greater than the after-tax cost of capital.

The project should be compared to other projects demanding approximately the same capital commitments when management decides which project to fund.

IRR = 8.9%, which exceeds 7%

n = 8

Collections (ordinary annuity) = $180,000

PV = $1,000,000

Termination payoff = $0

i = ?

NPV = $1,070,833 - $1,000,000 = $74,833

POSITIVE!

n = 8

i = 7%

Collections (ordinary annuity) = $180,000

Termination payoff = $0

PVn = $1,070,833

End of Chapter 6

![GRETCHEN GEIBEL IN THE SUPERIOR COURT OF …[Geisel] to inspect the premises. [Hassell] paid the $1,300.00 but inspection of the home did not occur. [Hassell] appeared again before](https://static.fdocuments.in/doc/165x107/5e90e4a5970d2e6d1e1b70df/gretchen-geibel-in-the-superior-court-of-geisel-to-inspect-the-premises-hassell.jpg)