Managed Futures

14

12/5/2014 There is no guarantee of profitability and futures trading presents a substantial risk of loss 1 What are Managed Futures? Managed futures are futures positions entered into by Professional money managers. These managers are known as commodity trading advisors (CTA) or commodity pool operators (CPO). Managers can invest in a large number of markets, including: • Energy (Crude, Unleaded Gasoline, Natural Gas, etc…) • Agriculture (Corn, Wheat, Soy Beans, Live Cattle, etc…) • Currencies (Euro, Yen, Swiss Franc, Canadian Dollar, etc…) • Equities (S&P 500, Dow, Nasdaq, Russell 2000, and others) Managers use a variety of trading methods depending on their expertise. Most of these are fundamentals, technical analysis, arbitrage or algorithmic. In many cases it is a combination of some or all of these.

-

Upload

bzinchenko -

Category

Economy & Finance

-

view

69 -

download

3

Transcript of Managed Futures

12/5/2014 There is no guarantee of profitability and futures trading presents a

substantial risk of loss

1

What are Managed Futures?

Managed futures are futures positions entered into by Professional money managers. These managers are known as

commodity trading advisors (CTA) or commodity pool operators (CPO). Managers can invest in a large number of markets, including:

• Energy (Crude, Unleaded Gasoline, Natural Gas, etc…) • Agriculture (Corn, Wheat, Soy Beans, Live Cattle, etc…) • Currencies (Euro, Yen, Swiss Franc, Canadian Dollar, etc…) • Equities (S&P 500, Dow, Nasdaq, Russell 2000, and others)

Managers use a variety of trading methods depending on their

expertise. Most of these are fundamentals, technical analysis, arbitrage or algorithmic. In many cases it is a combination of some or all of these.

12/5/2014 There is no guarantee of profitability and futures trading presents a

substantial risk of loss

2

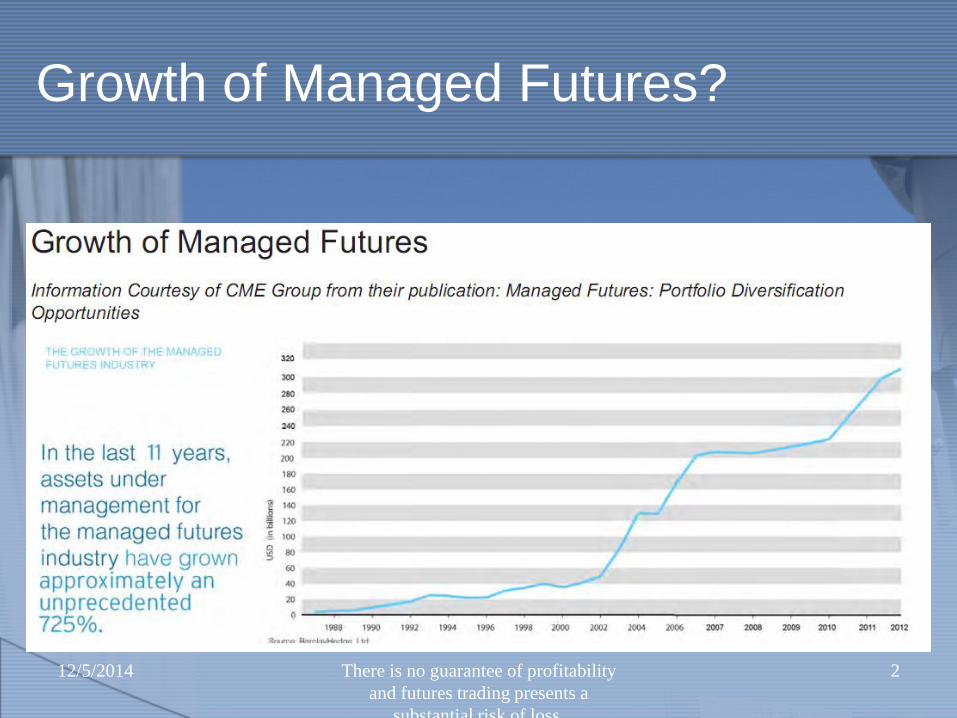

Growth of Managed Futures?

Trade Like A Quant

12/5/2014 There is no guarantee of profitability and futures trading presents a

substantial risk of loss

3

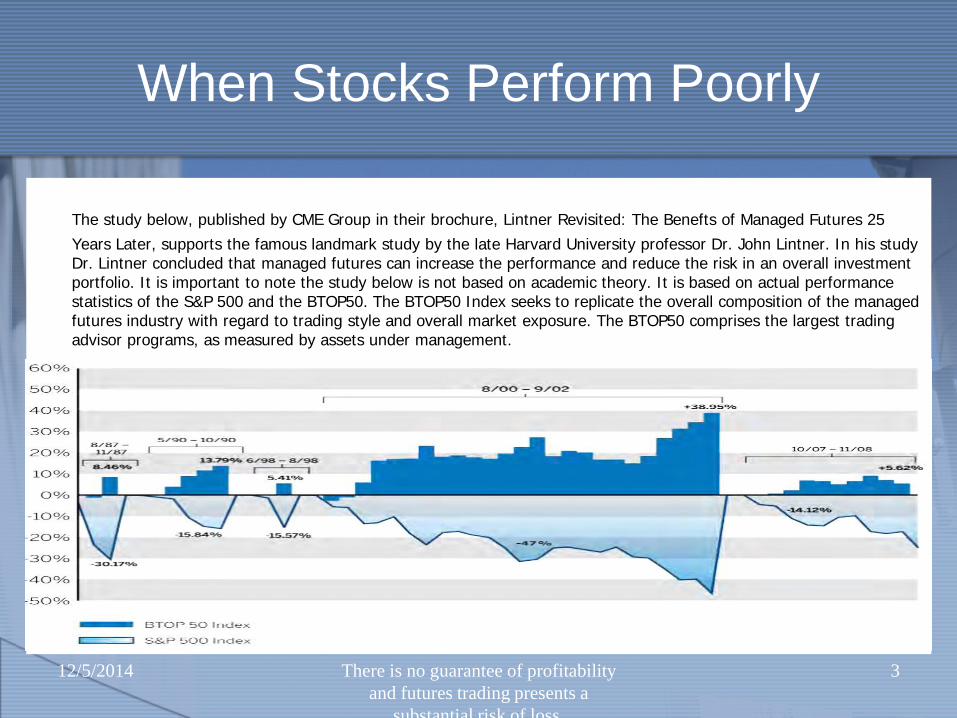

When Stocks Perform Poorly

The study below, published by CME Group in their brochure, Lintner Revisited: The Benefts of Managed Futures 25 Years Later, supports the famous landmark study by the late Harvard University professor Dr. John Lintner. In his study Dr. Lintner concluded that managed futures can increase the performance and reduce the risk in an overall investment portfolio. It is important to note the study below is not based on academic theory. It is based on actual performance statistics of the S&P 500 and the BTOP50. The BTOP50 Index seeks to replicate the overall composition of the managed futures industry with regard to trading style and overall market exposure. The BTOP50 comprises the largest trading advisor programs, as measured by assets under management.

12/5/2014 There is no guarantee of profitability and futures trading presents a

substantial risk of loss

4

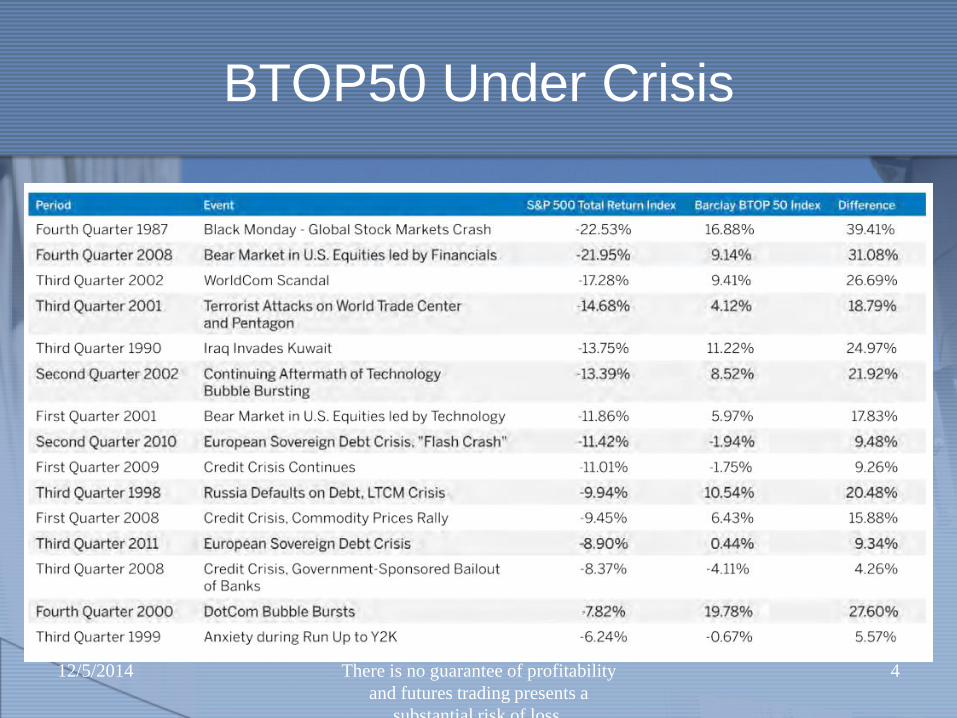

BTOP50 Under Crisis

12/5/2014 There is no guarantee of profitability and futures trading presents a

substantial risk of loss

5

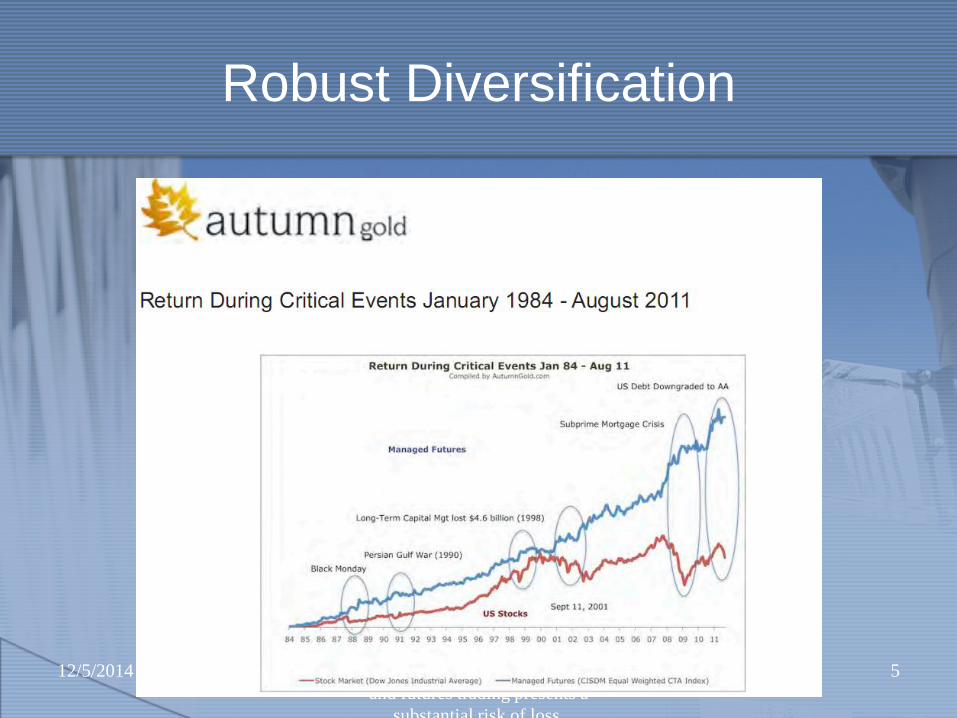

Robust Diversification

12/5/2014 There is no guarantee of profitability and futures trading presents a

substantial risk of loss

6

So Why Do Managers Use Futures?

• A futures contract represents a zero-sum game

between a buyer and a seller. • Gains realized by the buyer are offset by losses realized by the

seller (and vice-versa). • The futures exchanges keep track of the gains and losses every

day.

• Futures contracts are used for hedging and speculation. • Hedging and speculating are complementary activities. • Hedgers shift price risk to speculators. • Speculators absorb price risk.

12/5/2014 There is no guarantee of profitability and futures trading presents a

substantial risk of loss

7

Managed Futures

Managed futures add real diversification to a portfolio: • Futures represent potential hedges against such factors as business

cycle movements and inflation or deflation risk. • CTAs often target many markets using multiple strategies. • CTAs can buy and sell futures, write or purchase options, and

speculate in bull or bear markets. They do not need to pursue a single view as a bull or a bear.

• Foreign exchange and financial index futures allow for global diversification without the need for a fine-grained focus on several thousand stocks or bonds worldwide.

• By their very nature commodities are dependent upon global factors.

• These characteristics make managed futures diverge from major markets, unlike certain hedge fund strategies.

12/5/2014 There is no guarantee of profitability and futures trading presents a

substantial risk of loss

8

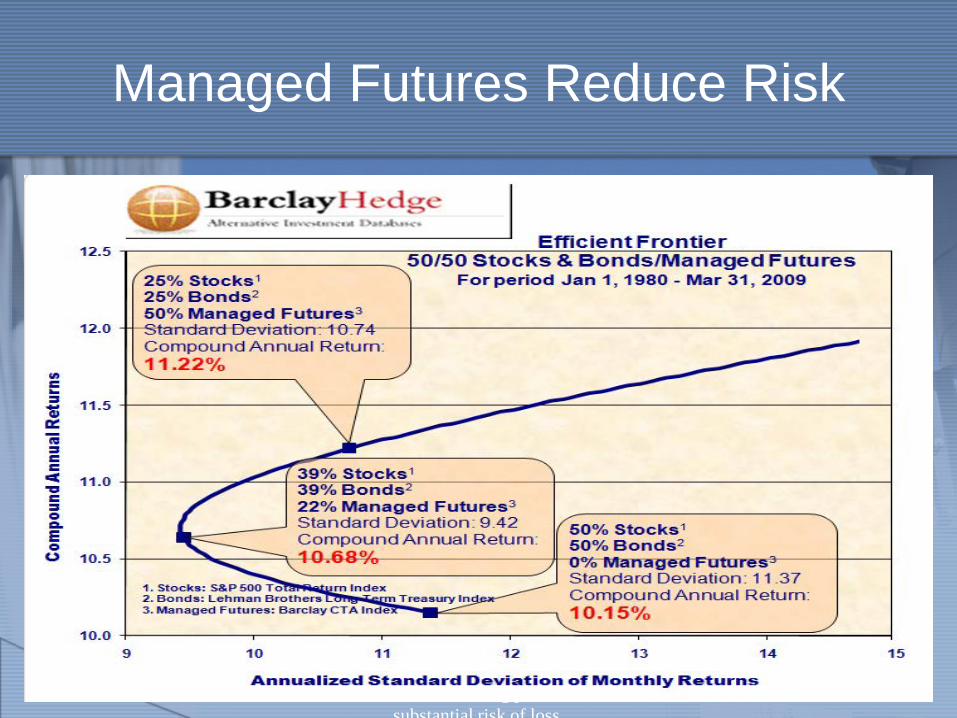

Managed Futures Reduce Risk

12/5/2014 There is no guarantee of profitability and futures trading presents a

substantial risk of loss

9

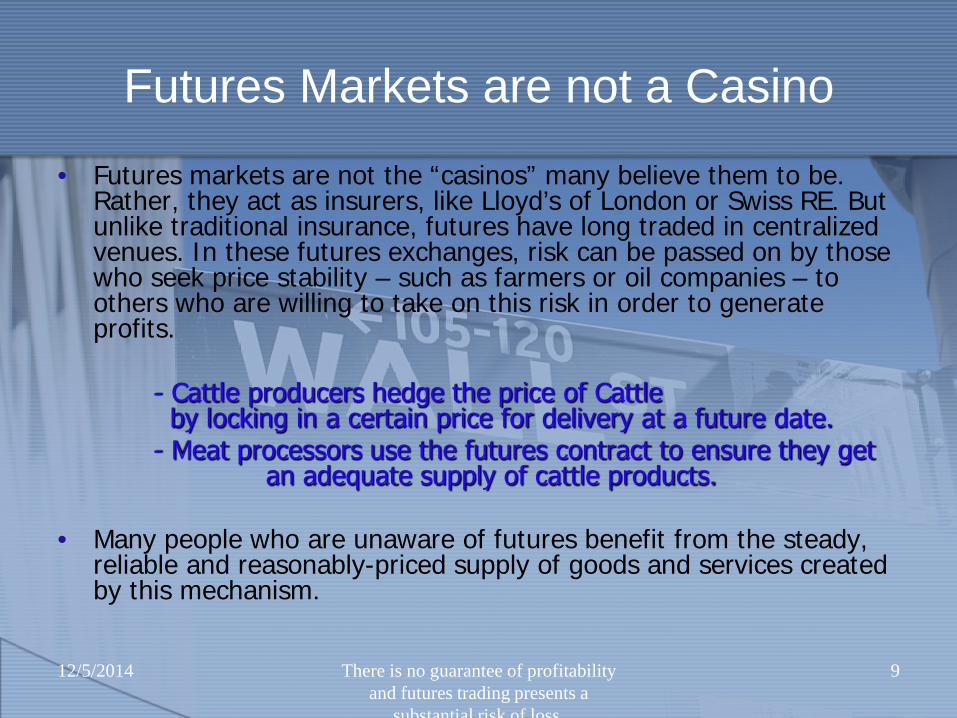

Futures Markets are not a Casino

• Futures markets are not the “casinos” many believe them to be. Rather, they act as insurers, like Lloyd’s of London or Swiss RE. But unlike traditional insurance, futures have long traded in centralized venues. In these futures exchanges, risk can be passed on by those who seek price stability – such as farmers or oil companies – to others who are willing to take on this risk in order to generate profits.

- Cattle producers hedge the price of Cattle

by locking in a certain price for delivery at a future date. - Meat processors use the futures contract to ensure they get

an adequate supply of cattle products. • Many people who are unaware of futures benefit from the steady,

reliable and reasonably-priced supply of goods and services created by this mechanism.

12/5/2014 There is no guarantee of profitability and futures trading presents a

substantial risk of loss

10

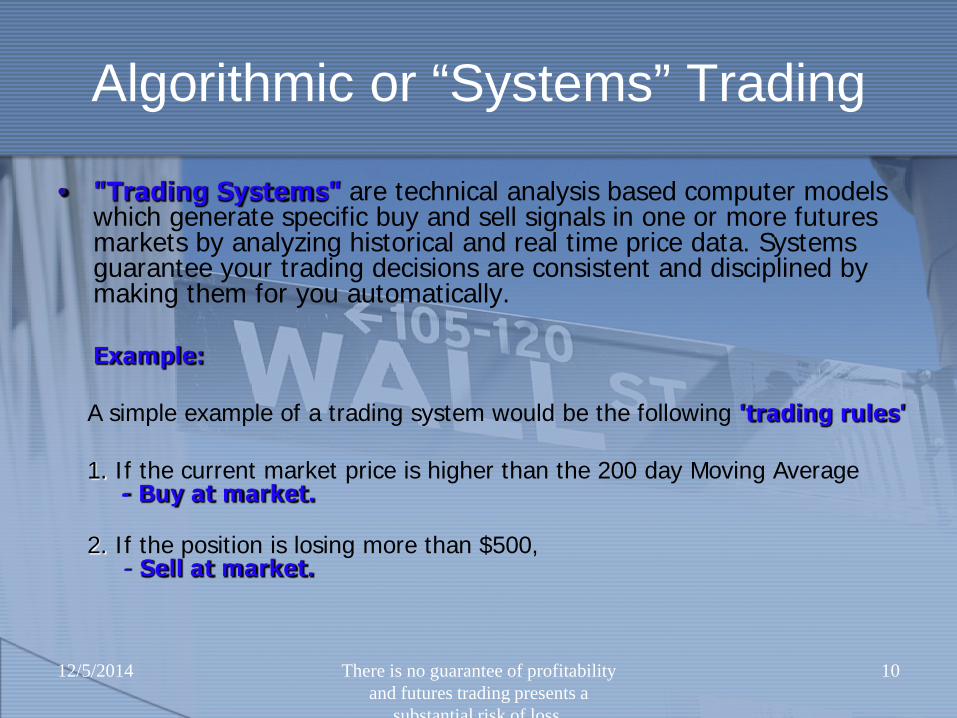

Algorithmic or “Systems” Trading

• "Trading Systems" are technical analysis based computer models which generate specific buy and sell signals in one or more futures markets by analyzing historical and real time price data. Systems guarantee your trading decisions are consistent and disciplined by making them for you automatically.

Example: A simple example of a trading system would be the following 'trading rules' 1. If the current market price is higher than the 200 day Moving Average

- Buy at market.

2. If the position is losing more than $500, - Sell at market.

12/5/2014 There is no guarantee of profitability and futures trading presents a

substantial risk of loss

11

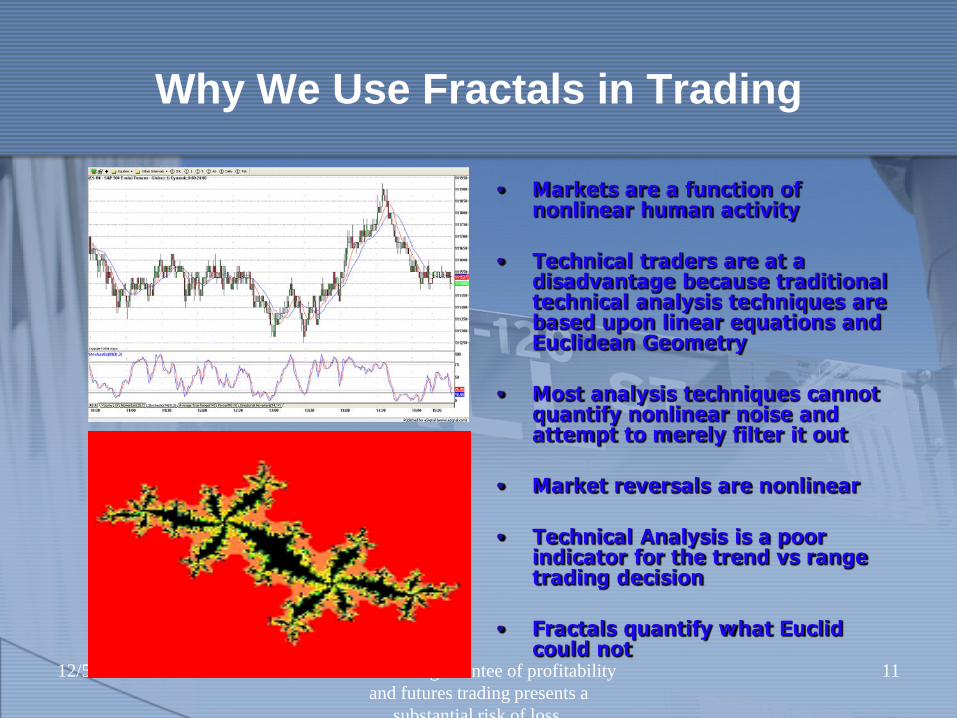

Why We Use Fractals in Trading

• Markets are a function of nonlinear human activity

• Technical traders are at a

disadvantage because traditional technical analysis techniques are based upon linear equations and Euclidean Geometry

• Most analysis techniques cannot

quantify nonlinear noise and attempt to merely filter it out

• Market reversals are nonlinear • Technical Analysis is a poor

indicator for the trend vs range trading decision

• Fractals quantify what Euclid

could not

12/5/2014 There is no guarantee of profitability and futures trading presents a

substantial risk of loss

12

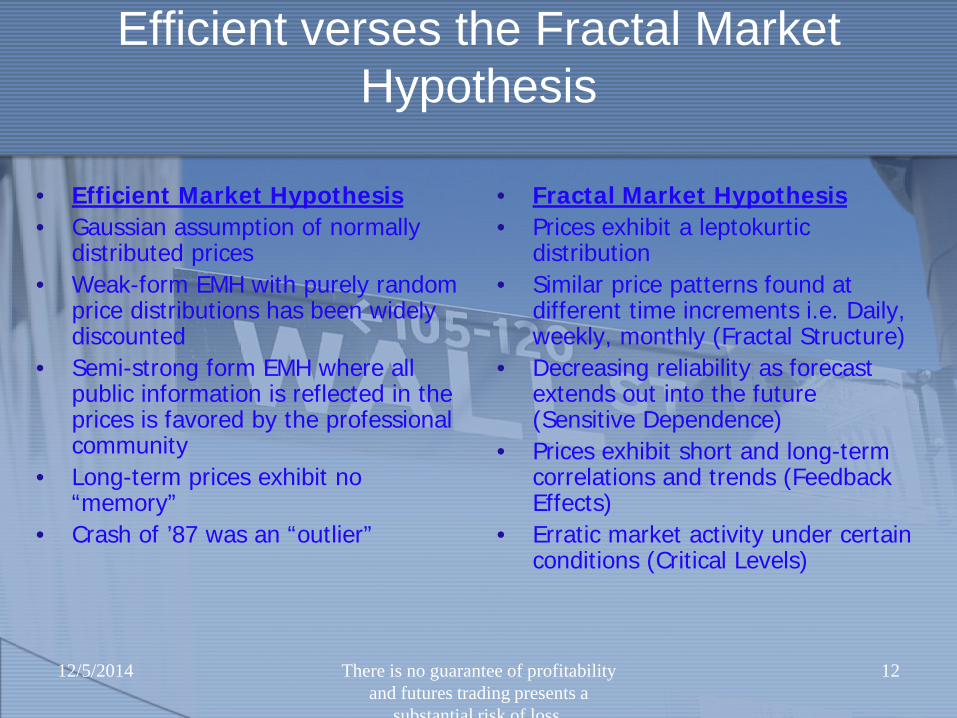

Efficient verses the Fractal Market Hypothesis

• Efficient Market Hypothesis • Gaussian assumption of normally

distributed prices • Weak-form EMH with purely random

price distributions has been widely discounted

• Semi-strong form EMH where all public information is reflected in the prices is favored by the professional community

• Long-term prices exhibit no “memory”

• Crash of ’87 was an “outlier”

• Fractal Market Hypothesis • Prices exhibit a leptokurtic

distribution • Similar price patterns found at

different time increments i.e. Daily, weekly, monthly (Fractal Structure)

• Decreasing reliability as forecast extends out into the future (Sensitive Dependence)

• Prices exhibit short and long-term correlations and trends (Feedback Effects)

• Erratic market activity under certain conditions (Critical Levels)

12/5/2014 There is no guarantee of profitability and futures trading presents a

substantial risk of loss

13

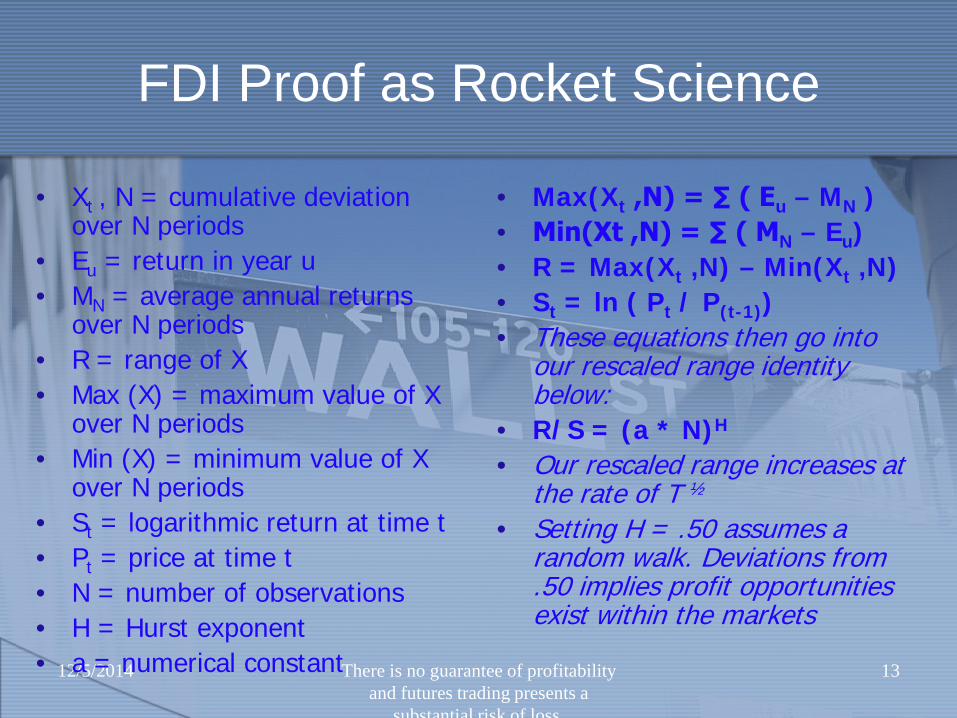

FDI Proof as Rocket Science

• Xt , N = cumulative deviation over N periods

• Eu = return in year u • MN = average annual returns

over N periods • R = range of X • Max (X) = maximum value of X

over N periods • Min (X) = minimum value of X

over N periods • St = logarithmic return at time t • Pt = price at time t • N = number of observations • H = Hurst exponent • a = numerical constant

• Max(Xt ,N) = ∑ ( Eu – MN ) • Min(Xt ,N) = ∑ ( MN – Eu) • R = Max(Xt ,N) – Min(Xt ,N) • St = ln ( Pt / P(t-1)) • These equations then go into

our rescaled range identity below:

• R/S = (a * N)H

• Our rescaled range increases at the rate of T ½

• Setting H = .50 assumes a random walk. Deviations from .50 implies profit opportunities exist within the markets

12/5/2014 There is no guarantee of profitability and futures trading presents a

substantial risk of loss

14

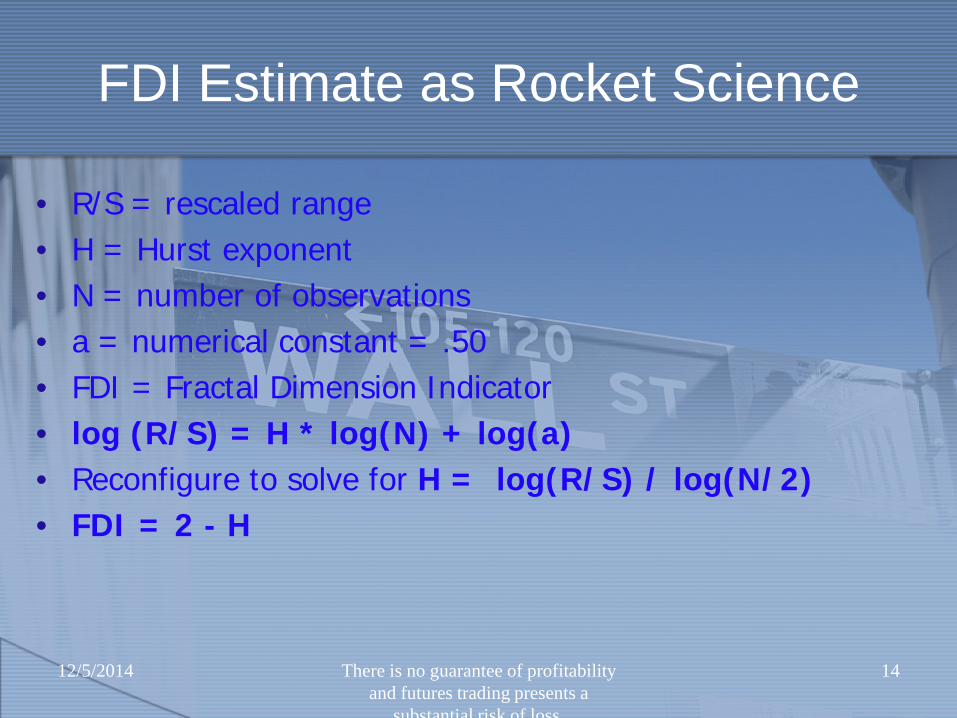

FDI Estimate as Rocket Science

• R/S = rescaled range • H = Hurst exponent • N = number of observations • a = numerical constant = .50 • FDI = Fractal Dimension Indicator • log (R/S) = H * log(N) + log(a) • Reconfigure to solve for H = log(R/S) / log(N/2) • FDI = 2 - H