Socioeconomic Determinants of Body Mass Index of Adult Chinese in the 1990s

Master thesis

M&As wealth effects and their determinants: The Chinese banking

industry between 2006-2013

By

Xiao Wu

ANR: 786873

M.S.D. Dwarkasing BSc. MSc, Supervisor

A thesis submitted in partial fulfillment

Of the requirements for the degree

Master of Science in Finance

School of Economics and Management

Tilburg University

-August 2014-

1

Contents 1. Introduction ....................................................................................................................................... 2

2. Literature review ............................................................................................................................... 5

2.1 Why do banks merge? ................................................................................................................. 5

2.2 Where are developing countries? ............................................................................................. 12

3. A brief history of Chinese banking industry .................................................................................... 14

4. Merger and bank data ..................................................................................................................... 16

5. Shareholder value creations in banking M&As ............................................................................... 19

5.1 The Event studies model and value creations in banking M&As .............................................. 20

5.2 Value creations of different types of M&As .............................................................................. 24

6. Determinants of wealth effects in banking M&As .......................................................................... 27

6.1 The regression model and determinants of excess returns ...................................................... 28

6.2 Robustness tests ........................................................................................................................ 31

7. Conclusion ....................................................................................................................................... 34

References .............................................................................................................................................. 37

2

1. Introduction

This paper studies the wealth effects of mergers and acquisitions and their determinants in

Chinese banking between 2006 and 2013. Over the last three decades, the financial services

industry has experienced profound consolidation waves in developed countries with the progresses

in technologies, releases of regulations and deepness of globalization. According to Securities Data

Corporation, the value of American deals totaled 673 billion Euros compared with around €1

trillion in Europe between January 2006 and December 2013. More recently, M&As in Chinese

banking have started to catch up. In the post-crisis era, the economic downturn in China associated

with potential credit losses and excess capacity in the banking industry imposes massive

profitability pressures on Chinese banks in the foreseeable future 1 . The attenuation of the

boundaries that limit foreign financial institutions operating in the mainland market is expected to

lead to fiercer bank competition. Under the serious competition, the Chinese banking industry is

experiencing an unprecedented M&A wave. There are more than 200 mergers announced or

completed in the Chinese banking sector over 2006-20132, totaling 27 million Euros in deal values.

Up to present, most of the available knowledge on M&As in the banking industry comes from

researches on developed economies, mainly the United States and the European Union. DeYoung

et al. (2009) review more than 150 empirical literature studies after 2000 concerning the industrial

countries. The authors summarize that North American bank mergers appear to be efficiency

improving, although the event-study literature presents a mixed picture regarding shareholder

value creations. And European bank mergers seemingly result in both efficiency gains and

shareholder wealth enhancements. Chinese M&A deals, while being important, have however

attracted less attention. This may be due to the recent trend of consolidations on the domestic

banking sector (2006-now) and difficulties in collecting data for Chinese banks. Besides, the

results found in industrial economies may not be similar in China because of the different industry

structure and regulations (Cybo-Ottone and Murgia, 2000).

1 Standard Poor’s: Diverging credit quality could result in varying degrees of resilience for the top 50 banks, China’s Top 50 Banks, September 2013. 2 The Chinese Banker, volume 2, 2013.

3

However, such an analysis of the Chinese experience is important for a number of reasons.

China has undoubtedly enormous economic impacts on the world. National GDP ranked number

two, and the annual GDP growth rate was 7.7% for 20133. Unlike the western markets, regulated

degrees of the most important and profitable industries in China, such as energy, communication

and finance, are extremely soaring. As a result of heavy regulations, banks have become the main

active players that dominate the financial industry. The high-inefficiency level caused by the lack

of competition of Chinese banks makes it attractive for potential acquirers to enter the market and

process consolidations (Berger et al., 2009). Whatever past experience is available would be useful

for players who are planning to drive a consolidation deal or campaign. To this aspect, experiences

from developed countries cannot be automatically applied to the Chinese environment where

regulations are much more restrict.

On the other hand, Andrade, Michell and Stafford (2001) propose that mergers and acquisitions

come in waves and concentrate in one specific industry, which are mainly caused by unexpected

industry-level shocks. This argument makes the research years from 2006 to 2013 become

crucially relevant. Within the sample period, occasional financial crisis occurred in 2008 and swept

across all around the world. Almost every active economy struggled with sovereign debt crisis,

weakened banking industries, low-consumption demands and high-unemployment rates. This

unexpected shock may accelerate the restructuring pace of the Chinese banking industry. Besides

the crisis, the domestic economic transformation welcomes the second phase where the emphasis

has shifted from partial privatization to excess capacity elimination. Foreign banks have more

freedom on the mainland market to open up new branches and merge with domestic banks. Hence,

domestic banks may choose consolidations to compete efficiently under the ailing economy.

This paper studies 82 completed mergers and acquisitions occurred in the Chinese banking

sector over 2006-2013. By means of event study methodology, the paper studies wealth creations

from M&As in a relatively short period (three months before the announcements and one month

after). Later on, regulatory arbitrage is examined by comparing excess returns between domestic

deals and foreign deals. The same methodology is applied to examine size effects by comparing

excess returns between large deals and small deals. Multivariate regressions regressing possible

3 Source: The National Bureau of Statistics of China

4

determinants on excess returns are conducted to explore what operating factors explain wealth

effects. Characteristics of banks are measured at various aspects: profitability, cost efficiency,

credit risk, liquidity risks, size, change in size and capital reserves. Performances of post-merger

banks are not examined in this paper due to the limitation of the data availability.

Two recent papers analyze minority-state takeovers in the partial privatization process of the

Chinese state-owned banks. Berger et al. (2009) apply a dynamic analysis on 38 Chinese banks

during 1994-2003, the results show that state-owned banks are the least efficient and foreign banks

are the most efficient. Taking minority foreign ownership of the state-owned Chinese banks will

improve ex-post performances significantly. Following the same approach, Lin and Zhang (2009)

analyze bank ownership reforms in China involving with 60 banks over 1997-2004. However, the

authors fail to find evidence that banks which are undergoing a foreign acquisition or public listing

gain performance improvements after ownership changes, which may be caused by fewer subsidies

from the government following ownership changes.

This paper finds favorable evidence for mergers and acquisitions in Chinese banking sector from

the view of shareholders. The findings suggest slight positive excess returns surrounding the

announcement date for both targets and acquirers, but the average excess returns for targets around

the announcement day [t-1, t+1] is -0.26%. An enormous run-up effect that 70% of excess returns

for the window [t-30, t+1] is achieved within one month prior to the announcement date indicating

the existence of information leaking in the Chinese market. No additional-excess returns are gained

in the post-announcement period for both acquirers and targets. As for determinants for value-

creation performances in M&As, engaging banks with higher profitability, cost efficiency, growth

rate, larger capital reserves and size appear to experience robust positive excess returns. Whereas,

credit risks negatively affect value-creation performances. The influence of liquidity risk on excess

returns is ambiguous.

The rest of the paper is organized as follows. Section 2 is a literature review on mergers and

acquisitions in the financial industry. Section 3 extends the review with the history of Chinese

banking industry. Section 4 describes the data sources and presents summary descriptive statistics.

Section 5 deals with the analysis and discussion based on the empirical result of the event studies.

5

Section 6 presents an extended discussion and analysis based on the multivariate regressions. And

section 7 concludes.

2. Literature review

This section reviews relevant literatures from two aspects: (1) Section 2.1 provides empirical

papers relating to various economic theories to explain why banks merge, such as shareholder

value maximization, performance improvements, product- and geographic diversification,

managerial incentives and governance regulations. (2) Section 2.2 goes through studies analyzing

cases in the Asian banking industry after the Crisis in 1997 to see the effects of M&As in

developing countries.

2.1 Why do banks merge?

Why do banks merge? Economic theory has provided considerable possible explanations.

Through consolidations, post-merger firms could achieve economies of scale and other synergies;

gain larger market powers, and perhaps form monopolies and oligopolies, therefore, become too-

big-to-fail (TBTF) corporations. Besides efficiency-related theory, relaxing of market disciplines

and self-serving attempts of managers could also make consolidations occur. Among all literatures

studying the reason why corporations merge, Mitchell and Mulherin (1996) build their model

based on a duplicating empirical feature: mergers come in wave, and are strongly clustered by

industry. This feature suggests that mergers might occur as reactions to unexpected shocks on

industry structure, such as an eruption of the financial crisis or an introduction of a new discipline.

Empirically, the American banking industry witnessed an unprecedented merger wave in twenty

century after the introduction of the Riegle-Neal Interstate Banking and Branching Efficiency Act4

4 Riegle-Neal Interstate Banking and Branching Efficiency Act allowed U.S. banks to branch interstate by consolidating out-of-state bank subsidiaries into a branch network and/or by acquiring banks of individual branches of banks through mergers or acquisitions

6

(Cornett, McNutt, & Tehranian, 2006). European financial markets experienced an M&A upsurge

after the introduction of the Euro (Huizinga, Nelissen, & Vennet, 2001).

2.1.1 Value creations and post-merger performances in America before 2000

The pervasive view regarding value creations generated from M&As in the 1980s and 1990s is

that, on average, target’s stockholders gained robust excess returns whereas acquirer’s

shareholders experience negative excess returns (Berger et al. 1999, Houston et al., 2001). Hudgins

and Seifert (1996) find that, in mergers and acquisitions, only targets receive abnormal gains, and

acquirers do not earn or lose at the announcement date. Pilloff (1996) analyzes 48 American

mergers involving publicly traded banking institutions over 1982-1991. The findings indicate that

performances and consolidated abnormal returns appear to have no changes on average, in which

performances are measured by profitability, cost efficiency, financial condition, investment

strategy, and funding methods. However, results from related literature published since 2000

diverge from the pre-2000 consensus. In general, the recent studies suggest that both American

and European post-merger banks experienced efficiency improvements, but only European banks

gained value enhancements from M&As.

2.1.2 Value creations and post-merger performances in America after 2000

Among literatures that analyze value creations from M&As in America after 2000, Knapp et al.

(2005) find negative excess returns for shareholders in 80 large consolidations over 1980-1990.

Becher and Campbell (2005) examine 443 mergers between publicly traded banks announced

during the 1990s. The findings indicate that mergers involving a high degree of branch overlaps

experience significant wealth gains around the announcement in the pre-deregulation 1990s.

However, consolidated banks realize significant losses in the post-deregulation 1990s. The results

are in line with the hypothesis that an economic shock can materially accelerate the restructuring

of the industry and efficiently reallocate industry assets through M&As. In addition, Delong (2001)

notes that mergers focusing on both activity and geography enhance shareholder value by around

7

3% whereas the other types do not create value. In another paper, DeLong and DeYoung (2007)

find that positive excess returns to M&A announcements dissipate rather quickly, in general,

mergers did not improve post-merger financial performances, and investors are unable to

accurately predict the future performance of the consolidated bank.

Some literatures provide compelling evidences of efficiency improvements in American M&As.

Knapp et al. (2005) find profitability, credit quality and fee incomes of post-merger banks are

below the average level of the industry. Hagendorff and Keasey (2009) use accounting data to

compare M&As in American and European financial markets and find that post-merger banks

witness no improvements in profitability and cost efficiency although the American banks tend to

focus on revenue generation. However, Cornett et al. (2006) note that industry-adjusted operating

performances of merged banks experience significant increases after consolidations, as

consequences of both revenue enhancements and cost reduction activities. Moreover, the authors

also document a size effect, in that large bank mergers produce greater financial performance gains

than small bank mergers.

2.1.3 Value creations and post-merger performances in Europe after 2000

Empirical results in Europe present a more promising picture of banking mergers and

acquisitions. For wealth effects in European M&As, Beitel et al. (2004) note that more than 60%

of all 98 transactions occurred over 1985-2000 in Europe create value. The value creations for

target shareholders, as well as the improvements in financial performances, mainly result from

enrichments in management skills. Resti and Siciliano (2001) find positive shareholder wealth

effects on M&As by applying event study analysis of Italian bank mergers over 1992 and 1997.

Campa and Hernando (2005) analyze 66 successful mergers and acquisitions occurred between

1998 and 2002 in European financial industry. The authors find that target firms appear to obtain

positive excess returns while acquiring banks appear to suffer losses. Besides, the results indicate

that the wealth changes are mostly realized around the announcement days, and only 5% of the

wealth effect is generated one month prior to the announcement. Cybo-Ottone and Murgia (2000)

study 54 relatively large European mergers (assets in excess of $100 billion) occurred in banks,

8

insurance companies and security firms over 1988-1997. The results show positive abnormal

returns associated with the announcement of mergers between banks and bank to insurance deals.

A large volume of literatures provides empirical evidence of efficiency improvements in

European mergers and acquisitions. Huizinga et al. (2001) analyze consolidated banks’

performances after introducing the Euro. Cost efficiency of post-merger banks on average rises,

whereas, profitability decreases for large banks and increases for small banks. Fritsch (2007)

studies the long-term effects on targets involved with 84 M&A deals in 17 Central and Eastern

European countries. Applying median difference tests, the author finds that post-merger

corporations realize gains in profitability and cost efficiency compared to the ex-ante phase,

though the absolute values of profitability and cost-efficiency of post-merger bank in three years

after the acquisitions do not differ from those domestic banks without mergers and acquisitions.

Other literatures focusing on European financial M&As find performance improvements in

profitability and/or cost efficiency in the post-merger phase (Diaz et al, 2004, Campa and

Hernando, 2005, Altunbas and Marques, 2008).

The distinct results on M&As’ performances between America and Europe have attracted

attentions from many researchers. DeLong and DeYoung (2007) analyze the long-run financial

performances of 216 M&As in American which were announced and completed between 1987

and 1999. The authors observe that the short-run post-merger financial performances, as well as

the long-run post-merger financial performances are positively related to the numbers of M&As

that took place in the years prior to the deal announcements. The spillover knowledge in M&As,

characterized as “learning-by-observing”, is consistent with the generally moderate post-merger

performances in America during the 1990s and the gradually improved financial performances in

Europe during the 2000s. Besides the “learning-by-observing”, several literatures, such as Cybo-

Ottone and Murgia (2000), explain the different results between European market and American

market stemming from the differences in industry structures and regulations. Although some recent

studies suggest that consolidations may enhance revenues, Amel et al. (2004) argue that the gains

appear limited in magnitude, and vary by countries, industries and deals analyzed.

9

2.1.4 Other possible motivations for mergers and acquisitions

The failure of finding strong evidence of performance improvements in the post-merger period

has encouraged researchers to investigate alternative explanations behind the depressed results,

paying particular attention to alternative diversification, managerial and governance motives.

Greater product- and geographical diversification have accompanied the consolidation wave of

the financial sector. Conglomerates might have greater diversification to perform the tradeoff

between risks and expected returns better. Cornett et al. (2006) observe the merger wave in

American banking industry after introducing the Riegle-Neal Act. The authors find that activity-

focusing mergers realize greater performance gains than activity-diversifying mergers, and

geographical-focusing mergers perform better than geographical-diversifying mergers after

consolidations. A similar conclusion is documented in Cornett et al. (2003) that focusing

acquisitions realize higher excess returns than diversified acquisitions for acquirers. Lepetit et al.

(2006) note that banks engaged in cross-product diversification experience positive and significant

market reactions. Allen and Jagtiani (2000) find that nonbank activities, such as insurance and

securities, reduce the overall risk to the bank but increase systematic market risk. However,

diversification benefits are not sufficiently large to justify expanding bank powers into nonbank

securities and insurance underwriting activities. Whereas, Estrella (2001) observes that banks and

insurance companies have some important common factors that are highly correlated, and this

suggests that the corresponding mergers may have no favorable diversification outcomes.

Empirical results for geographic diversification are ambiguous. Berger et al. (2001) fail to find

evidence in cost efficiency improvements in cross-border mergers and acquisitions. However,

Elsas et al. (2010) document the improvements in profit efficiency and accounting returns for

cross-border deals in nine countries over 1996-2003. Altunbas and Marques (2008) focus on

influences of European banks’ strategic similarities on post-merger performances. The results

suggest that it is quite costly for domestic acquirers to integrate dissimilar institutions in terms of

loan portfolios, profitability and cost efficiency level, and size strategies. For cross-border mergers,

diversified effects on different loan and credit strategies between acquirers and targets appear to

conduct better post-merger performances, whereas dissimilar capital and cost structures tend to

negatively affect performances of consolidated corporations.

10

Managers may pursue their own objections ahead of shareholders’ interests. Self-serving

managers may want consolidations for empire building since their executive compensations are

based on firm sizes (Rosen, 2004). A positive relationship between total post-merger CEO

compensation and anticipated gains from mergers surrounding the announcement date is found in

the American large consolidation deals (Anderson, Becher, & Campbell, 2004). Meanwhile,

managerial hubris associated with firm sizes is likely to drive a higher probability of taking

mergers, as well as damage shareholder values in consolidations. Malmendier and Tate (2008) find

that the probability of making an acquisition is 65% higher for overconfident CEOs than non-

overconfident CEOs. Meanwhile, the market reaction at merger announcement made by over-

confident CEOs is significantly more negative than for non-overconfident CEOs. Moeller et al.

(2004) observe that excess returns for small firms exceeds excess returns for large firms by 2.24%

around the announcement date, and large firms offer much more acquisition premiums than small

firms and enter acquisitions with negative synergy gains. The findings are in line with managerial

hubris. Similar results are documented in Schmid and Walter (2009), Brewer and Jagtiani (2007)

and Cybo-Ottone and Murgia (2000).

Although merging decisions are mainly motivated to maximize shareholder values, in practice,

governance regulations often affect consolidation occurrences more directly. Governments tend to

limit large mergers and acquisitions for avoiding over-concentrated markets and too-big-to-fail

(TBTF) institutions5. Once a bank develops to be mega-large and viewed as TBTF, it may have

the opportunity to exploit safety net subsidies (Mishkin, 2006). Shull and Hanweck (2001) observe

that the ten largest American banks pay less for funds than smaller banks and operate with lower

capitalization rates, which suggest that these banks enjoy advantages of TBTF implicit guarantees.

Penas and Unal (2004) find that the adjusted returns of merging banks’ bonds are positive and

significant across pre-merger and at-the-announcement period, which are primarily achieved from

gains by forming TBTF institutions. In contrast, consolidations are encouraged by the government

when the economy is shirking, as Malaysia in 1998 (Sufian, 2004). However, Hadlock et al. (1999)

find little evidence that governance is related to the probability of being acquired.

5 Trends in international migration annual report, OECD, 2007

11

Besides the economic situation, regulations and supervisions may also affect M&A decisions.

Regulatory arbitrage arises with cross-border consolidations when banks tend to change their

regulatory environment. There are two possible consequences of regulatory arbitrage for involved

banks: on the one hand, banks engaged in cross-border mergers can maximize shareholder values

and improve capital allocations through pursuing profitable investment opportunities which are

not allowed in their home country because of certain high risks. On the other hand, banks may

acquire targets in weakly regulated districts to invest in excessive risk-taking projects which have

a potential threat on shareholder values. Existing researches have shown that tough regulatory

restrictions on bank activities and barriers to foreign entry hurt banking sector performances (Barth,

Caprio, & Levine, 2006). In a recent paper, Houston et al. (2012) find a harmful “race to the

bottom” characteristic in cash flows that international bank tend to predominantly transfer funds

from countries with strict regulations to countries with fewer supervisions. The results indicate the

existence of regulatory arbitrage. In a relating paper, Ongena et al. (2013) note that banks from

countries with strict regulations on bank activities and capital reserve requirements appear to make

riskier loans abroad, which is consistent with the race-to-the-bottom view. A consistent result is

found in Fritsch (2007). The findings indicate that large acquirers from western countries with

restricted regulations intend to acquire targets in countries with a high GDP growth rate, as well

as low corporate income tax rates.

The effects of regulation arbitrage on cross-border mergers’ post-merger performances are

ambiguous in empirical works. Karolyi and Taboada (2014) analyze a sample of 916 majority

cross-border acquisitions combined with 7297 domestic consolidations announced between 1995

and 2012. The results show that target banks’ excess returns are significantly correlated with

differences between targets and acquirers in the quality of bank regulations. Targets realize higher

abnormal returns when acquirers are from countries with more restrictions on bank activities,

stricter capital requirements, strong private monitoring, and better regulatory quality. In contrast,

Hudgins and Seifert (1996) document that there is no significant difference in abnormal returns

based on whether the acquirer is domestic or foreign. Additionally, some papers hold the

indistinctive view that banks involved with cross-border deals may pursue the same benefits

associated with domestic deals, such as economics of scale and scope, rises in efficiency and

12

diversification between risks and revenues (Cornett and Tehranian, 1992; Berger et al., 1993;

Pilloff and Santomero, 1998).

2.1.5 Determinants of post-merger performances

Some papers link the shareholder gains with firm-specific factors to explain determinants of

gains in post-merger performances. Olson and Pagano (2005) identify that shareholder gains and

long-term performances are significantly determined by the acquirers’ sustainable growth rate

prior to the acquisition, post-acquisition changes in growth rate, and dividend payout. Fritsch

(2007) finds that higher profitability and cost efficiency of acquirers tend to strictly improve post-

merger performances of consolidated corporations. And loan growth after acquisitions is mainly

driven by country-specific factors. Penas and Unal (2004) analyze bond returns and bond credit

spreads around the announcements of mergers over 1991-1998. The results show that bondholders

of acquirers and targets gain significant positive bond returns, which is caused by the reductions

of cost of debts in the post-merger banks. The positive and statistically significant relation between

announcement-month bond and equity returns indicates that bank mergers do no shift wealth from

shareholders to bondholders. Focarelli et al. (2002) separately study 135 mergers and 66

acquisitions occurred in Italian banking industry between 1984 and 1996. By the means of

predicting pro forma balance sheet by consolidating the balance sheet of the banks involved in the

mergers, the authors find that mergers seek to improve incomes from providing a wider range of

services, but the improvements are offset by higher labor costs. After M&As, acquisitions aim to

restructure the loan portfolios of the target banks, and as a result, consolidated banks realize higher

profits.

2.2 Where are developing countries?

Unlike industrial economies, the consolidation pace of the financial industry is slow in

developing countries, as a result of heavy supervisions in the 1990s. However, this pace has been

accelerated with the development in economy, deepness in globalization and releases of

13

regulations. The first consolidation wave came in 1997 after the Asian financial crisis. From the

aspect of value creations, Crouzille and Lepetit (2008) analyze stock market reactions to the

announcement of bank M&As in eight East Asian countries over the 1997-2003 period. The results

show that engaged banks realize significantly negative excess returns during the crisis period

(1997-2000). The negative relations are mostly found in less mature banking systems which are

mainly led by local governments. Goddard et al. (2012) study 132 M&As involving banks in

emerging markets in Asia and Latin America from 1998 to 2009. The authors find that M&As

create shareholder values for targets. On the other hand, acquirers benefit from geographical

diversification and underperforming targets.

Empirical results on post-merger performances show favorable evidence for M&As in

developing economies. Sufian (2004) find that post-merger banks’ average efficiency level is

higher than the pre-merger period for Malaysia banks over 1998-2003, despite the fact that these

banks’ overall efficiency deteriorates significantly during the consolidation process. A size effect

is documented that banks with small or medium size benefit the most from M&As while the post-

merger large banks are still suffering from scale inefficiency. Ariff and Can (2009) study post-

restructured outcomes in banks which received restructuring subsidies from the IMF after the

Asian crisis. The authors find that East Asian banking efficiency improves in the post-IMF period,

but the magnitude of the recovery is limited to their pre-IMF level. In general, the restructured

banks are not significantly more efficient than their un-restructured counterparts. Perhaps more

importantly, they observe that bank efficiency is significantly affected by the measures of

restructuring. Bank recapitalization or partial privatization generates efficiency gains in short-run

period. Mergers and acquisitions, in contrast, experience efficiency losses in a short term. The

positive but insignificant improvements in foreign ownership entries may suggest that the potential

synergies in cross-section deals may accrue over a longer period that they do not test. An Indian

case provides favorable evidence for M&As that the market share of post-merger banks increases

(Goyal & Joshi, 2011).

Unfortunately, literature on Chinese mergers and acquisitions in the banking industry is

extremely scarce. Most relating studies focus on bank ownership reforms and corresponding

performances, because partial privatization associated with taking on minority foreign ownership

14

dominates the first phase of the Chinese banking transformation started from 1990s. Berger et al.

(2009) apply a dynamic analysis on 38 Chinese banks during 1994-2003, and they find that state-

owned banks are the least efficient and foreign banks are the most efficient. Taking minority

foreign ownership of the state-owned Chinese banks will improve ex-post performances

significantly. Following the same approach, Lin and Zhang (2009) analyze bank ownership

reforms involving with 60 banks over 1997-2004. They fail to find evidence that banks that

undergo a foreign acquisition or public listing gain performance improvements after ownership

changes, which may be caused by fewer subsidies from the government following acquisition or a

public listing. A selection effect is observed that, in ex-ante ownership-change phase, the Chinese

banks that are partially acquired by foreign firms or those that go public significantly outperform

compared to those that do not take ownership reforms. The findings suggest that the government

sells the equity of better banks first to attract foreign investors, which may help the process of

ownership reforms in China.

3. A brief history of Chinese banking industry

With the development of the economy, the modern Chinese banking system experienced three

stages in transformations. In the pre-1990s, the central government heavily controlled the banking

sector, and the state-owned banks were the only players on the financial market. During the 1990s

until 2001 when China entered the WTO, the market allowed for competition, resulting in the

establishments of city commercial banks and rural development banks. After 2001, the emphasis

in economic transformation focused on ownership reforms for state-owned banks and operating

allowances for foreign banks. However, the reform and openness of Chinese banking system are,

even though progressive, still slow.

Following the former Soviet Union model 6 , the Chinese socialist banking system was

established in the late 1940s. The central bank named People’s Bank of China (PBOC) was set up

6 Soviet Union Banking Model: there were only one central bank and several mono-banks. The central bank was the only dominant in the financial system which were in charge of making economic policies, issuing currencies, depositing, and granting of loans etc.. Mono-banks were ultimately under the orders of the same central authorities as the central bank, and allowed to operate in the assigned field.

15

in 1948 according to the mono-bank model. It played the double roles of both central and

commercial banks before 1966. During the Cultural Revolution, PBOC was temporarily stripped

of its currency issues and monetary control functions. Lately, it regained these obligations. China

began its first financial system reform in 1978. PBOC was split into four big state-owned banks,

Bank of China (BOC); China Construction Bank (CCB); Agricultural Bank of China (ABC) and

Industrial and Commercial Bank of China (ICBC), known as the Big Four nowadays. They were

initially restricted to only one sector of the economy as indicated in their names. The Big Four

started to compete after the releases of restrictions in 1985. Early or later, twelve national

shareholding commercial banks were set up to meet the ever growing demands in financial services.

During the period from 1990 until 2001, the Chinese banking system witnessed its second-round

reform. To solve the problematic loans that banks lent to state-owned enterprises, three policy

banks were set up in 1994 to play the role of policy lender. Later on, the Minister of Finance issued

32.6 billion Chinese yuans of 30-year government special bonds to recapitalize the Big Four. In

1995, according to the central bank law, urban and rural credit cooperatives were issued aiming at

encouraging establishments of city-level commercial banks in China. However, those city

commercial banks were still conducted by the state. At the same time, Chinese government

allowed foreign investors to acquire a quite small portion of equities of state-owned banks. As a

result of the first minority-shares takeovers in the Chinese banking sector, China Everbright bank

became the first domestic joint-equity bank.

Following the promised agenda after China entered the WTO, the government was expected to

release pegged interest rate, levy fair tax rate among bank players, reduce restrictions on ownership

takeovers and M&As, and greater freedom of operational and geographical scope in the Chinese

banking industry. However, these restrictions are still working since the government deemed that

it was not the best time for the domestic banking sector to open up perfectly. Hence, foreign banks

that wanted to enter the Chinese banking market slowed down and tried to look for solutions

through mergers and acquisitions. Meanwhile, a growing number of Chinese banks began to list

on the stock markets to finance its growing investments. In order to supervise the economic

reforming progresses, the Chinese government established the Chinese Banking Regulatory

Commission (CBRC) in 2003. In the same year, CBRC upgraded foreign investment limitations

16

up to 25% of any domestic bank, as well as ownership allowance up to 20% for personal investors,

subject to regulatory approval. Under the encouragements associated with limitations on foreign

banks’ operations in the mainland markets, many foreign banks started to purchase the stake of

healthy and promising domestic commercial banks. Due to the potential credit losses in the

Chinese banking industry and the non-performing loans that banks lent to the real-estate sector,

the Chinese Securities Regulatory Commission (CSRC) stopped approving domestic banks’ IPO

requests from year 2007 till now. This suspension of IPOs has slowed down the pace of M&As’

wave in the Chinese banking sector in recent years to some extent.

4. Merger and bank data

This section describes the data sources and presents summary descriptive statistics for the event

study analysis and multivariate regressions. The paper identifies 82 successful M&As involving

41 banks in the Chinese financial market. The relatively small size reflects the underdevelopment

of stock markets in the world largest nation. Many mergers and acquisitions cannot be examined

using event study methodology because the involved banks are not listed on the stock markets.

Some widely used criteria on mergers’ sample selections are relaxed in order to realize a sample

size sufficiently large to allow statistical analysis, such as investigating cases where acquirers take

full controls of targets, or where both targets and acquirers are listed banks.

The principal data sources which are eligible for inclusion of mergers and acquisitions in the

sample are Datastream and Zephyr. Daily stock prices adjusted for dividends from listed banks are

collected from Datastream. Meanwhile, Zephyr offers information about M&As in the Chinese

banking industry with the target and acquirer’s name, the announcement date, the completion date

and the amount of the deal. The deal value is defined by Zephyr as the consideration paid for the

actual stake acquired, excluding fees and expenses. Transactions are selected if they occurred in

China with the announcement date between 2006 and 2013. More restrictions are that (1) the

transaction is completed before the 31st December 2013, (2) either the target or the acquirer is a

Chinese bank, and (3) at least the acquirer is a public firm listed on the local stock exchange market.

17

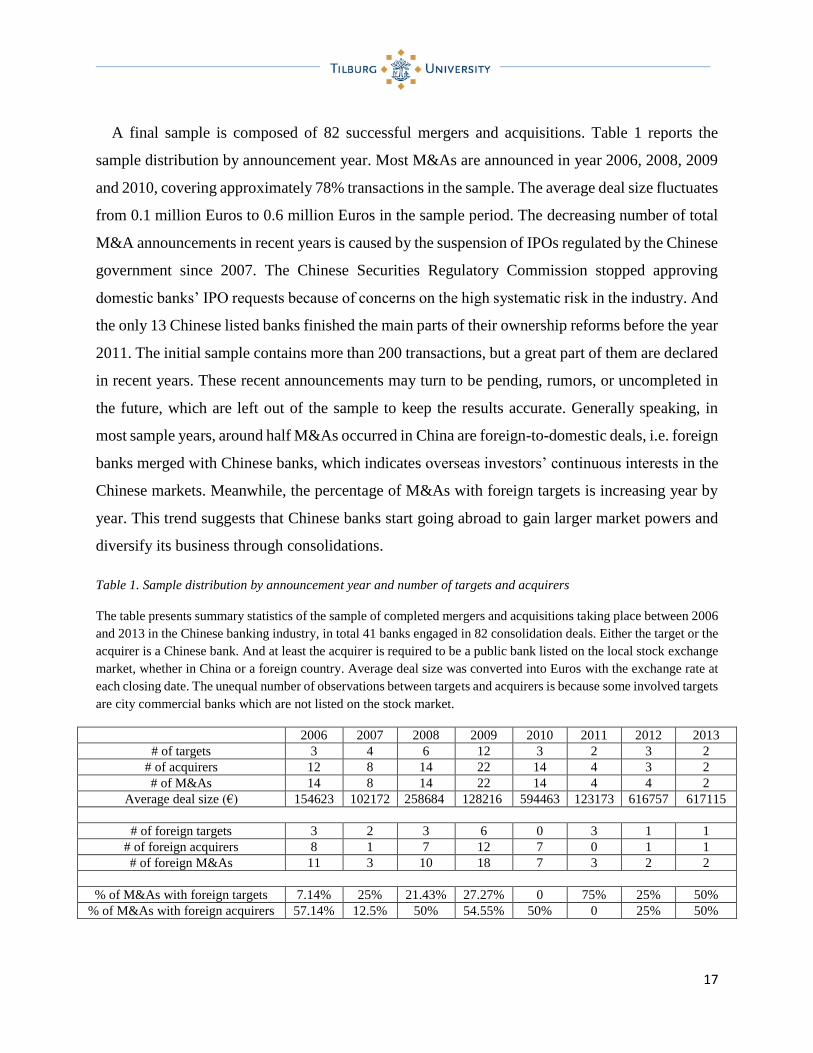

A final sample is composed of 82 successful mergers and acquisitions. Table 1 reports the

sample distribution by announcement year. Most M&As are announced in year 2006, 2008, 2009

and 2010, covering approximately 78% transactions in the sample. The average deal size fluctuates

from 0.1 million Euros to 0.6 million Euros in the sample period. The decreasing number of total

M&A announcements in recent years is caused by the suspension of IPOs regulated by the Chinese

government since 2007. The Chinese Securities Regulatory Commission stopped approving

domestic banks’ IPO requests because of concerns on the high systematic risk in the industry. And

the only 13 Chinese listed banks finished the main parts of their ownership reforms before the year

2011. The initial sample contains more than 200 transactions, but a great part of them are declared

in recent years. These recent announcements may turn to be pending, rumors, or uncompleted in

the future, which are left out of the sample to keep the results accurate. Generally speaking, in

most sample years, around half M&As occurred in China are foreign-to-domestic deals, i.e. foreign

banks merged with Chinese banks, which indicates overseas investors’ continuous interests in the

Chinese markets. Meanwhile, the percentage of M&As with foreign targets is increasing year by

year. This trend suggests that Chinese banks start going abroad to gain larger market powers and

diversify its business through consolidations.

Table 1. Sample distribution by announcement year and number of targets and acquirers

The table presents summary statistics of the sample of completed mergers and acquisitions taking place between 2006

and 2013 in the Chinese banking industry, in total 41 banks engaged in 82 consolidation deals. Either the target or the

acquirer is a Chinese bank. And at least the acquirer is required to be a public bank listed on the local stock exchange

market, whether in China or a foreign country. Average deal size was converted into Euros with the exchange rate at

each closing date. The unequal number of observations between targets and acquirers is because some involved targets

are city commercial banks which are not listed on the stock market.

2006 2007 2008 2009 2010 2011 2012 2013

# of targets 3 4 6 12 3 2 3 2

# of acquirers 12 8 14 22 14 4 3 2

# of M&As 14 8 14 22 14 4 4 2

Average deal size (€) 154623 102172 258684 128216 594463 123173 616757 617115

# of foreign targets 3 2 3 6 0 3 1 1

# of foreign acquirers 8 1 7 12 7 0 1 1

# of foreign M&As 11 3 10 18 7 3 2 2

% of M&As with foreign targets 7.14% 25% 21.43% 27.27% 0 75% 25% 50%

% of M&As with foreign acquirers 57.14% 12.5% 50% 54.55% 50% 0 25% 50%

18

The data for multivariate regressions come from two sources: excess returns for each event

window which are estimated using event studies, and balance-sheet-based indicators taken from

Bankscope. Profitability is measured by return on average equities (ROAE). Operating cost,

defined as operating cost over gross margin, captures cost efficiency. Following the motivations

proposed by Forcarelli et al. (2002), loan losses and interbank ratio measure credit risk and

liquidity risk respectively. Two indicators are designed to capture size effects: total assets and

change in size. Total assets indicate how large the involved bank is compared to other banks in the

industry. As for change in size, calculated as total assets in the announcement year (t) divided by

total assets in the year (t-1), exhibits how fast the involved bank is growing. Lastly, the capital

ratio measures how sufficient the involved bank is in capital reserves. The descriptive statistics of

the sample are presented in table 2 for both targets and acquirers before M&As.

Table 2.Descriptive statistics of balance-sheet-based indicators of target and acquirer banks before M&As

The table presents summary statistics on ex-ante merger announcement balance-sheet-based indicators for 41 listed

banks engaged in mergers and acquisitions in my sample. These balance-sheet-indicators include: total assets, change

in size, return on average equity, loan losses, interbank ratio, operating cost and capital ratio. Change in size is

calculated as total asset one year prior to the announcement over total asset in the year when announcement is declared.

Loan losses are defined as loan losses divided by total lending. Operating cost is operating cost divided by gross

margin. All the other indicators follow the definitions of Bankscope. Total assets are converted into Euros and in the

unit of millions.

Ex-ante characteristics of target banks

Mean 25th percentile Median 75th percentile

Total asset (million €) 252806 108426 229976 229976

Change in size 1.26 1.22 1.28 1.28

Return on average equity 20.348 15.52 19.01 28.35

Loan losses 2.27 2.13 2.47 2.49

Interbank ratio 207.29 152.14 203.82 247051

Operating cost 0.87 0.59 0.86 1.15

Capital ratio 11.987 11.34 11.34 13.34

Ex-ante characteristics of acquirer banks

Mean 25th percentile Median 75th percentile

Total asset (million €) 1160493 179471 1188879 1894157

Change in size 1.17 1.028 1.209 1.236

Return on average equity 7.23 8.49 16.14 20.82

Loan losses 2.06 1.27 2.46 2.79

Interbank ratio 153.61 46.60 129.45 246.86

Operating cost 0.64 0.53 0.65 0.83

Capital reserves 13.93 12.27 13.09 15.00

19

For banks involved in consolidations, targets were more profitable and grew faster than

acquirers on average prior to announcements. Whereas, acquirers outperformed than targets on

cost efficiency, credit risk and liquidity risk managements. As expected, the acquirers were around

4.5 times the size of targets on average, which may partially explain the more sufficient capital

reserves in acquirers than targets. The relatively higher growth rates and better performances in

profitability of glamour banks made them easier become targets on the merger markets. Value

banks are frequently larger banks with abundant capital reserves, which have better managerial

skills in cost efficiency, credit and liquidity risks, and tend to become acquirers in consolidations.

Similar results are concluded in Wheelock and Wilson (2000), who state that banks with low

capitalizations, high loan losses ratios, poor-quality loan portfolios, low earnings, and inefficient

managerial skills reflected in measures of cost inefficiency have a high probability to be acquired.

The selected sample has some limitations. As documented above, the size of the sample is

restricted because of the relative underdeveloped stock market in China. Although some widely

used criteria in M&A studies have been relaxed to make the sample exercisable, the asymmetric

distribution, associated with a relatively small size, may lead toward biases in estimating excess

returns. Data availability makes it impossible to observe post-merger performances in terms of

efficiency improvements. Moreover, focusing on the Chinese financial market may weaken the

findings on foreign deals because of limitations on observations.

5. Shareholder value creations in banking M&As

This section consists of two parts. The first part explains the settings for event studies and reports

results of excess returns for both targets and acquirers within different event windows. The second

part examines whether excess returns vary by types of mergers. Two subsamples are constructed,

which focus on domestic deals versus foreign deals and large deals versus small deals. Excess

returns, the differences between groups and their corresponding are reported.

20

5.1 The Event studies model and value creations in banking M&As

Under the semi-strong efficient markets hypothesis, stocks prices react positively (negatively)

to all publicly available information (e.g. announcements on mergers) that notified investors

expect will increase (decrease) long-run firm value. Event studies around the announcement date

(t) of mergers and acquisitions are performed here in order to observe stock market reactions facing

consolidations. Excess returns for targets and acquirers are analyzed through three distinct periods

around the announcement date: pre-announcement period (windows [t-90, t-1] and [t-30, t-1]),

announcement period (windows [t-1, t+1] and [t-30, t+1]), post-announcement period (window [t-

1, t+30]) and a robustness indicator that covers an extended event window ([t-30, t+30]). Excess

returns are defined as the difference between achieved shareholder returns of the involved banks

during the event window minus the expected normal returns as if these banks did not consolidate.

An estimation window of 120 days is taken from 220 days to 100 days prior to the announcement

to estimate expected returns using CAPM. Long-term effects are not taken into consideration since

it is believed that stock prices could be affected by too many other factors in a relatively longer

period besides M&A announcements. A further analysis is designed to measure whether there are

different performances between M&A types and deal sizes.

Table 3. Differences in Average Excess Returns by Window Length

The table reports means, medians, and percentages of negative values of excess returns by different window length.

Excess returns are calculated as the difference between returns after mergers and acquisitions and normal returns if

without M&As, measured using the CAPM. Symmetric risk indicator is calculated with OLS regressions over the

estimation window [t-220, t-100].

CAARs Median CAARs % negative

Targets Acquirers Targets Acquirers Targets Acquirers

Pre-announcement a

(t-30,t-1) 0.60% -0.79% -1.24% -0.87% 65.2% 63.2%

(t-90,t-1) 1.17% 0,48% 1.17% -1.44%* 39.1% 56.1%

Announcement a

(t-1,t+1) -0.26% 0.46% -0.14% 0.13% 52.2% 45.6%

(t-30,t+1) 0.85% 0.06% -0.72% -1.54%* 60.9% 57.9%

Post-announcement and the robustness indicator

(t-1,t+30) -3.53%** c -0.43% -1.75% -1.24% 60.9% 54.4%

(t-30,t+30) -3.36% c -1.24% -2.68% -4.19%* 60.9% 63.2%

- */**/*** denote significant at the 10%, 5% and 1%, reactively.

21

- An outlier is left out for these two windows. Excess returns for this transaction are respectively 0.51 and 1.32,

which are relatively too larger compared to the average reported in the table. The unusual results may be

caused by the selection of data. The target involved in this transaction is AIG finance (HONK KONG) limited,

which is not listed on the stock market. The stock prices of AIG are used instead.

The results of event studies on the whole sample are represented in table 3. Target companies

experience positive cumulative average excess returns surrounding the announcements of the

consolidations but a negative cumulative average excess return (-0.26%) around three days of

the announcement. Unlike Campa and Hernando (2005) which study European market and find a

tiny run-up effect, there is an enormous run-up effect that approximately 70% of positive excess

return in the window of [t-30, t+1] is realized in the period up to the day prior to the announcement

in the Chinese market. The existence of information leaking in the Chinese market may be a

potential reason behind this phenomenon. Under the circumstance of weak supervisions, it is easy

for financial consultants to access inside information. Therefore, they have incentives, and are

capable of taking arbitrages from M&A deals by buying in target firm stocks before the

announcement then selling it out on the announcement day since they believe that the market

usually gives positive reactions to the target firms in consolidations. The negative CAAR on [t-1,

t+1] may indicate that arbitragers dominate the market prices than individual investors. The

enormous amount of closing out the targets’ stocks lower the prices though many individual

investors buy in the targets on the announcement day. Confounding events may be another reason

for the enormous run-up effect. Stock prices may be affected by other confounding activities

happened in the event period, such as publications of annual reports. Notably, the cumulative

average excess return slowly decreases by 0.57% during sixty days prior to the announcement7,

but the difference is statistically insignificant. Overall, targets experience a negative cumulative

average return with the value of -3.36% in the window [t-30, t+30]. The massive negative CAAR

is mainly due to the sharp decreases in the post-announcement period. Due to the asymmetric

distribution of excess returns, medians are reported in table 3 to give a more comprehensive picture

of the results. The median excess returns tend to be smaller than the mean at each event window

7 The equality between the average excess returns for the window [t-90,t-1] and [t-30,t-1] fails to reject at any significant level, with a p-value of 0.7568.

22

in pre- and at- announcement period. However, the proportion of transactions experience negative

excess returns for targets strongly fluctuated from 39% to 65%, depending on the event window.

Unlike general results that are usually found in most literatures, acquirers experience slight

positive cumulative average excess returns of the order of 0.5% around the announcement except

the CAAR equals to -0.79% within the window [t-30, t-1]. The unusual negative cumulative

average excess return in one month prior to the announcement may also be due to information

leakages and arbitragers. Owing to the fact that irrational investments are more serious in China

compared to other developed economies, acquirers experience a positive average excess return on

the announcement day. Self-attributing, which continuous works on both arbitrageurs and

individual investors, makes misjudgments repeatedly happen.

The findings indicate that both targets and acquirers realize value creations from M&As in

China, and in general, shareholders of targets benefit more than shareholders of acquirers except

on the announcement day, which suggests that the M&As investigated in this paper can be regarded

as economically successful from the perspective of shareholders. The results of targets are in line

with most literatures, but inconsistent for acquirers. Andrade et al. (2001) analyze a comprehensive

sample totaling 8512 mergers between 1973 and 1998 in America. The results show positive

abnormal returns for targets but insignificant negative excess returns for acquirers. However, they

observed a 16% average abnormal return for targets around the announcement [t-1, t+1], which is

quite different from these findings. Campa and Hernando (2005) uncover that shareholder returns

to the target companies are positive on average upon the announcement of the transaction while

returns to shareholders of the acquiring companies are slightly negative in the European banking

industry over 1998-2002. Moreover, unlike the enormous run-up effect (70%) for targets in my

sample, they observe that most of this return is realized on the days surrounding the announcement,

with a small run-up effect up (around 5%) to three months prior to the announcement. This serious

information-leaking problem in Asian countries has been documented in previous literature

(Goddard et al., 2012).

The lack of statistical significance in table 3 might arise because of two reasons: the deal

characteristics and the small sample associated with asymmetric distributions. Deal characteristics

refer to that some mergers are minority-stake takeovers among the 82 deals in the sample, which

23

means that acquirers have less control power or even cannot control targets. It would be difficult

for the consolidated banks to minimizing operating costs by rationalizing the branch of networks,

improving management skills and achieving higher economies of scale. For this type of M&As,

investors may lower their expectations of post-merger performances on consolidated banks, and

forasmuch, passively react to the announcements on the stock market. The excess returns on

minority-stake takeovers would statistically be lower than majority-stake takeovers. Moreover,

average and median values substantially differ as a result of the highly asymmetric distribution of

excess returns, which jointly with a small sample size, may explain the lack of statistically

significance in most cases.

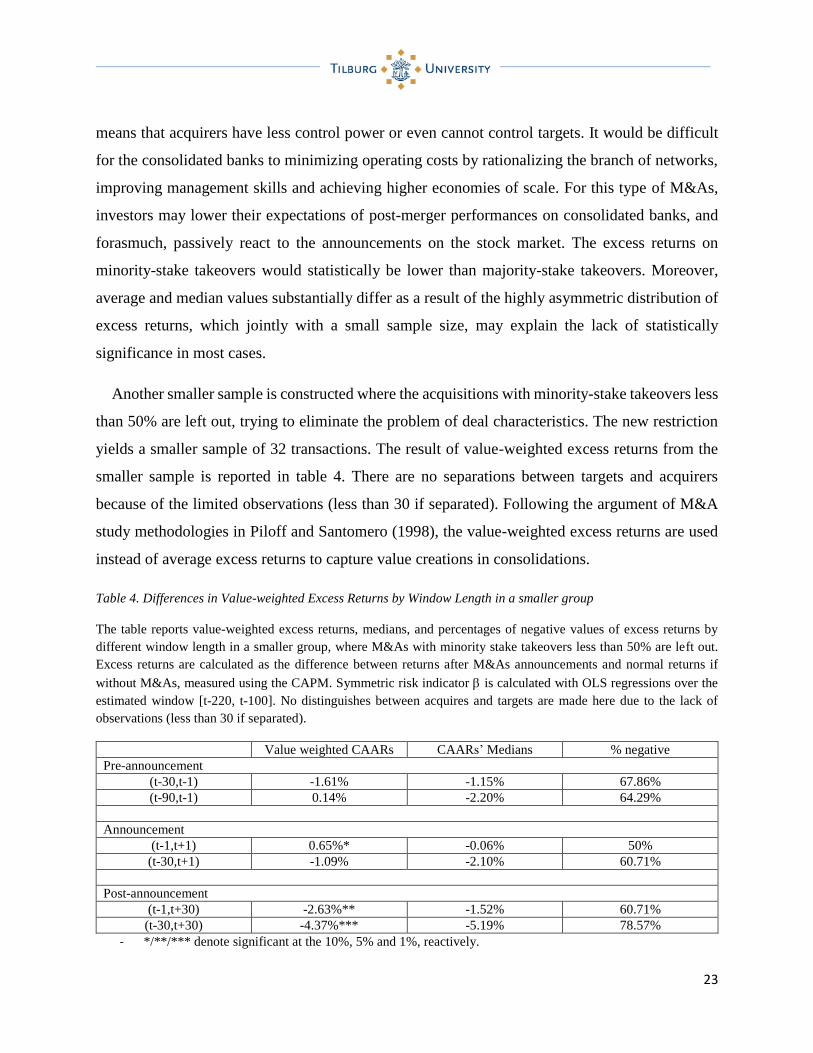

Another smaller sample is constructed where the acquisitions with minority-stake takeovers less

than 50% are left out, trying to eliminate the problem of deal characteristics. The new restriction

yields a smaller sample of 32 transactions. The result of value-weighted excess returns from the

smaller sample is reported in table 4. There are no separations between targets and acquirers

because of the limited observations (less than 30 if separated). Following the argument of M&A

study methodologies in Piloff and Santomero (1998), the value-weighted excess returns are used

instead of average excess returns to capture value creations in consolidations.

Table 4. Differences in Value-weighted Excess Returns by Window Length in a smaller group

The table reports value-weighted excess returns, medians, and percentages of negative values of excess returns by

different window length in a smaller group, where M&As with minority stake takeovers less than 50% are left out.

Excess returns are calculated as the difference between returns after M&As announcements and normal returns if

without M&As, measured using the CAPM. Symmetric risk indicator is calculated with OLS regressions over the

estimated window [t-220, t-100]. No distinguishes between acquires and targets are made here due to the lack of

observations (less than 30 if separated).

Value weighted CAARs CAARs’ Medians % negative

Pre-announcement

(t-30,t-1) -1.61% -1.15% 67.86%

(t-90,t-1) 0.14% -2.20% 64.29%

Announcement

(t-1,t+1) 0.65%* -0.06% 50%

(t-30,t+1) -1.09% -2.10% 60.71%

Post-announcement

(t-1,t+30) -2.63%** -1.52% 60.71%

(t-30,t+30) -4.37%*** -5.19% 78.57%

- */**/*** denote significant at the 10%, 5% and 1%, reactively.

24

From table 4, merger and acquisition firms experience a positive cumulative average excess

return within three days around the announcement with the value of 0.65%, which is significant at

10% level, indicating a possible positive synergy effect. However, the negative cumulative average

excess return of -1.61% within the window [t-30, t-1] may suggest information leakages. Value

destroying after the announcements seems serious in this case. The value-weighted excess returns

decrease by 3.28%8 in one month after the announcements. A similar result is documented in

Cybo-Ottone and Murgia (2000). After analyzing 54 M&As in 14 European financial markets over

1988-1997, they observe that combined abnormal returns of acquirer and target witness a positive

and significant market reaction around a short period of eleven days [t-5, t+5] surrounding the

announcement date. The only positive excess returns on the announcement day suggest that

positive excess returns to M&A announcements dissipate rather quickly, which is in line with the

hypothesis proposed by DeLong and Deyoung (2007) that investors are unable to accurately

predict the future performances of the consolidated bank.

5.2 Value creations of different types of M&As

This section analyzes whether the market expectations vary for different types of mergers. Two

different types of mergers are examined: foreign deals versus domestic deals, and large deals

versus small deals.

Favorable evidence on foreign advantage hypothesis has been documented in Berger et al. (2009)

that foreign stake-takeovers benefit Chinese banks on efficient performances. It is believed that

the entry of foreign investors can bring advanced managerial skills and better diversification

between returns and risks. However, it is argued that there exists barriers, such as differences in

languages, cultures and currencies, which obstruct the full realization of potential synergies in

foreign M&As (Berger et al., 2001). Hence, targets may benefit from domestic acquisitions since

acquirers know the local markets and customers better, and are able to rationally restructure

8 Differences in both post-announcement window ([t-1, t+30] - [t-1 t+1]) and robustness test ([t-30, t+30] - [t-30, t+1]) with the window of [t-30, t+30] are the same here with a value of -3.28, which are significant at 5% level.

25

business to eliminate overlaps on products and branches. This argument is classified as home

advantage hypothesis.

Besides home/foreign advantage hypothesis, regulatory arbitrage may arise in cross-border

merger and acquisition activities. Banks may engage in cross-border mergers in order to pursue

profitable opportunities if the banks come from heavily regulated countries where they are not

allowed to engage in certain risks, but value-creating activities. On the contrary, banks may acquire

targets in weakly regulated districts for searching high-risk investments, which may threaten

shareholder values (Karolyi & Taboada, 2014). To further explore whether cross-border deals

realize different excess returns than domestic deals, the sample is correspondingly separated into

two subgroups: foreign deals and domestic deals. If both the target and acquirer are Chinese banks,

the deal is defined as a domestic deal. And if either target or acquirer is a foreign bank, it is treated

as a foreign deal. The results are reported in the upper panel of table 5.

Table 5. Differences in Cumulative Average Abnormal Returns by type of Merger

The upper panel of the table reports average excess returns for foreign and domestic deals. Domestic deal is defined

as, in an M&A, both targets and acquirers are Chinese banks. The merger is regarded as foreign deal if either target

or acquirer is a foreign bank. The bottom panel reports average returns for large and small deals. Small and large deals

are determined by the deal value over total assets of the involved bank’s total assets in the announcement year. If the

ratio is larger than the median ratio, the deal is classified as a large deal. Otherwise, it is classified as a small deal.

Excess returns are calculated as the difference between returns after mergers and acquisitions announcements and

normal returns if without M&As, measured using the CAPM. Symmetric risk indicator is calculated with OLS

regressions over the estimated window [t-220, t-100].

(t-30,t-1) (t-90,t-1) (t-1,t+1) (t-30,t+1) (t-1,t+30) (t-30,t+30)

A. Domestic vs. Foreign a

Targets Foreign 3.60% 2.29% -0.45% -0.70% b -1.80% b -1.58% b

Domestic -0.75% 4.71% 0.65% 1.28% -10.38%*** -9.75%***

Difference 4.35% -2.42% -1.1% -1.98% 8.58%** 8.17%*

p-value 0.6252 0.7111 0.5966 0.6615 0.0361 0.0773

Acquirers Foreign -1.48% 0.48% -0.67% -1.42% -1.52% -3.57%

Domestic 1.56% 0.37% 2.99%*** 3.54%* 0.91% 1.46%

Difference -3.04% 0.11% -3.66%** -4.96%* -2.43% -5.03%

p-value 0.2859 0.4563 0.0215 0.0937 0.4772 0.2804

B. Small deals vs. Large deals a

Targets Large deals -0.56% 3.99% 0.26% -1.28% -3.86%* -5.40%*

Small deals 6.79% 2.34% 1.15%* 7.41% 1.59% 12.47%

Difference -7.36% 1.66% -0.89% -8.69% -5.44% -17.87%

p-value 0.2915 0.7450 0.6109 0.2828 0.3666 0.1689

26

Acquirers Large deals -1.23% -1.18% 0.31% -0.84% -0.53% -2.54%

Small deals -0.55% -0.81% 0.61% 1.08% 0.63% 0.35%

Difference -0.68% 1.99% -0.30% -1.92% -1.15% -2.89%

p-value 0.7901 0.5577 0.8397 0.4748 0.7083 0.4869

a. */**/*** denote significant at the 10%, 5% and 1%, reactively.

b. An outlier is left out for these three windows. Excess returns for this transaction are respectively 0.78%, 0.51%

and 1.32%, which are relatively too larger compared to the average reported in the table. The unusual results

may be caused by the selection of data. The target involved in this transaction is AIG finance (HONG KONG)

limited, which is not listed on the stock market. The stock prices of AIG are used instead.

Within the announcement window, domestic acquirers experience positive excess returns, while

foreign acquirers realize negative ones. And on the announcement date (window [t-1, t+1]),

domestic acquirers appear to yield 3.66% higher excess returns than foreign acquirers9. The

findings are in line with home advantage hypothesis that domestic acquirers have better knowledge

on local markets and customers. A domestic merger could timely benefit the acquirer on achieving

potential synergies that realize economies of scales and scopes, gain larger market powers and

better diversified. During the post-announcement period, excess returns decrease for both national

and foreign acquirers, but the difference is still negative indicating that national acquirers

outperform than foreign acquirers on equity markets. For targets, a similar result holds around the

announcement date, consistently with home advantage hypothesis. However, foreign targets gain

higher excess returns than domestic targets within the post-announcement period10.

The lower excess returns for foreign deals compared to domestic deals are in line with a great

volume of literatures (Amel et al., 2004; Correa, 2009; and Vennet, 2002). In contrast with Hudgins

and Seifert (1996), there are statistically significant differences in excess returns between domestic

and foreign mergers. However, it is ambiguous whether the differences come from country barriers

or regulatory arbitrage. Foreign deals may pursue the same benefits associated with domestic deals

(Berger et al., 1993), but the existent barriers obstruct the full realization of potential synergies in

foreign M&As. In this case, home advantage hypothesis dominates the wealth effects in M&As.

On the other hand, the non-significant destroying of value for foreign deals may suggest another

reason that regulatory arbitrage is working in the negative direction in China. Foreign acquirers

that merge with domestic targets and domestic targets that merge with foreign acquirers may take

9 The equality between the foreign excess return and the domestic excess return is rejected at 5% significant level. 10 The significantly large negative excess returns for domestic targets within post-merger announcement window are caused by the few observations with relatively larger excess returns.

27

excessive risk-taking investments in the targets’ countries. Since these investments are not allowed

in their home countries because of the certain high risks. As a result, foreign deals experience

negative excess returns because that shareholder values are threatened to decrease in the future.

Following the method in Campa and Hernando (2005), the sample is split into two subgroups

depending on the size of the deal in order to observe whether different sizes of deals affect excess

returns. Banks engaged in large deals are expected to experience lower excess returns surrounding

the announcements. The post-merger bank may face insufficient funds to finance its investments

and restructure the consolidated firm since the mergers will cost too much. Size of the deal

measures whether the merger is big or small compared to the total assets of engaged firms on the

announcement date. If the ratio of deal value over total assets is larger than the median in the

sample, the deal is classified as a large deal. If the ratio is smaller than the median, it is classified

as a small deal. The results are reported in the bottom panel of table 5.

Targets engaged in small deals experience positive excess returns around the announcement

date, while targets engaged in large deals generally realize negative excess returns. A similar result

holds for acquirers that small deals generate higher excess returns than large deals. The great

differences on excess returns between targets engaged in large and small deals in post-

announcement phase provides favorable evidence of the hypothesis that acquirers may spend too

much on M&As and will have insufficient funds to finance restructuring and investments

following consolidations. The results are in line with Moeller et al. (2004) to some extent, who

finds that a few very large M&A deals result in large destruction on value of shareholders.

6. Determinants of wealth effects in banking M&As

This section consists of two parts and aims to explore determinants of value creations

surrounding announcement dates. The first part represents methodology and results associated

with the analysis. The second part provides robustness tests by controlling for bank-fixed effects,

year-fixed effects and bank-year-fixed effects.

28

6.1 The regression model and determinants of excess returns

The event studies exhibited above only measure returns during a short period around the merger

announcements and are based solely on market expectations of consolidation announcements. To

further explore the determinants of value reactions surrounding announcement dates, multivariate

regressions are applied with balance-sheet indicators based on cumulative excess returns generated

from event studies. The basic regression is

𝐶𝐴𝑅𝑖,𝑗,𝑡 = 𝛼0 + 𝛼1 ∗ 𝑅𝑂𝐴𝐸𝑗,𝑡 + 𝛼2 ∗ 𝐴𝑠𝑠𝑒𝑡𝑠𝑗,𝑡 + 𝛼3 ∗ 𝐶ℎ𝑎𝑛𝑔𝑒 𝑖𝑛 𝑠𝑖𝑧𝑒𝑗,𝑡 + 𝛼4

∗ 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝑐𝑜𝑠𝑡𝑠𝑗,𝑡 + 𝛼5 ∗ 𝐿𝑜𝑎𝑛 𝑙𝑜𝑠𝑠𝑒𝑠𝑗,𝑡 + 𝛼6 ∗ 𝐼𝑛𝑡𝑒𝑟𝑏𝑎𝑛𝑘 𝑟𝑎𝑡𝑖𝑜𝑗,𝑡 + 𝛼7

∗ 𝐶𝑎𝑝𝑖𝑡𝑎𝑙 𝑟𝑒𝑠𝑒𝑟𝑣𝑒𝑠𝑗,𝑡 + 𝛼8 ∗ 𝐷𝑜𝑚𝑒𝑠𝑡𝑖𝑐 𝑑𝑒𝑎𝑙𝑖,𝑡 + 𝛼9 ∗ 𝐿𝑎𝑟𝑔𝑒 𝑑𝑒𝑎𝑙𝑖,𝑡 + ℰ𝑖,𝑗,𝑡

Where i represents an M&A transaction, j represents a bank, and t represents a year. Dependent

variable is cumulative excess returns for each transaction at every event window, which are

generated using event studies. Independent variables are characteristic indicators for each bank in

the announcement-declared year.

Various balance-sheet-based indicators measure different firm-specific characteristics. Returns

on average equities intend to measure the profitability of corporations. Total assets in the form of

natural log measure the sizes of involved banks in the merging year. Olson and Pagano (2005)

identify that shareholder gains are significantly determined by the acquirers’ sustainable growth

rate to the acquisition. Change in size is designed to examine the growth-generating-value

hypothesis, which is calculated by total assets in the announcement year divided by total assets in

one year before the announcement. This is different and weakly correlated with total assets11. If a

change in size of the firm is high, it means that this firm is in the growing path, which provides

them more incentives and extra funds to finance an M&A. Investors may also expect the

consolidated firms will experience growth after the M&A by enjoying its advanced management

skills and operating cost controls etc., and, therefore, a change in size is positively related with

CARs. In line with Campa and Hernando (2005), operating costs, which are calculated by

11 The correlation between total assets and change in size is -0.4 and significant at 1% level for the sample of acquirers. The correlation drops to -0.2 for target sample and is statistically insignificant at any conventional level.

29

operating costs over gross margins, are used to assess cost efficiency. Operating costs allow us to

see how costs are associated with revenue-generating activities and whether or not the business

can be operated more efficiently. Credit risks are estimated by loan losses of the involved bank in

the announcement year. Net interbank ratios are designed to appraise liquidity risks. If the bank is

lack of liquidities, it needs to borrow from other banks for financing its investments. Hence, the

interbank ratio would be high. Capital reserves aim at ensuring that the corporation has adequate

funds to at least partially finance its investment projects. Domestic dummy is a variable set to one

if both the acquirer and target are Chinese banks, and set to zero otherwise. Large dummy is a

variable set to one if the deal value over the involved bank’s assets is larger than the median in the

sample, and set to zero otherwise. Table 6 specifically explains each indicator with its symbol,

definition, and how it is calculated.

Table 6. Definition and description of independent variables in the regressions

The table represents the symbols, definition, and description of the independent variables in the regressions.

Definitions for most indicators are following Bankscope illustrations except change in size and operating costs.

Domestic deal and large deal are two dummy variables following the definition in event studies of this paper.

Indicator name Symbol Measurement goal Definition

Return on average equities ROAE Profitability Net income/average stockholders’ equities

Change in size ∆size Change in size Total assets_t/Total assets_t-1

Operating costs OC Cost efficiency Operating costs/gross margin

Loan losses LL Credit risk Loan losses/total lending

Interbank ratio IntR Liquidity risk Interbank assets/ interbank liability

Capital ratio CapR Capital reserves Core equity capital/total risk-weighted assets

Total assets TA Total assets Ln (total assets)

Domestic deal ND Deal type Dummy variable. If both the acquirer and target

are domestic banks, it equals 1; otherwise 0

Large deal LD Deal size Dummy variable. If deal value over involved

bank’s total assets is larger than the median of

the sample, it equals 1; otherwise 0

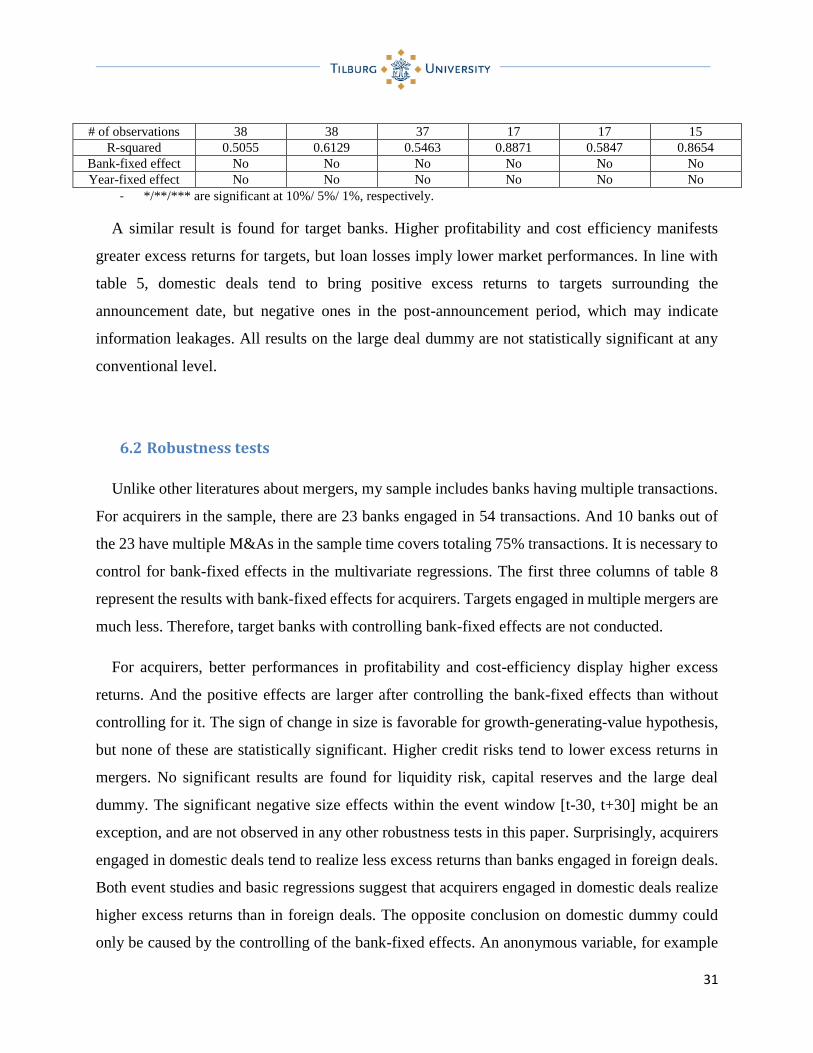

Given that excess returns are estimated from event studies, I use robust OLS in the estimation

to allow for heteroscedasticity. The results for basic regressions are reported in table 7. For

acquirers, signs of all coefficients are the same as expected. Changes in size and capital reserves

generally have significant positive effects on excess returns in mergers and acquisitions, but the

magnitude of change in size effects on excess returns is bigger than capital reserves. The findings

are consistent with growth-generating-value hypothesis. Increasing in size means that the bank is

30

in fast-growing path, accordingly, the bank has more incentives and is capable of taking M&As

and corresponding restructurings and investments. Meanwhile, investors may have greater faiths

that the consolidated bank can create higher shareholder values in the foreseeable future, and,

therefore, invest in the involved firms. Large capital reserves imply the bank has sufficient money

to finance its investments, including M&As and restructuring processes after consolidations.

Hence, sufficient capital reserves encourage investors to positively react to engaged banks. Within

the event window [t-1, t+1], profitability, cost efficiency and total assets are positively correlated

with excess returns at any conventional significant level. In contrast, loan losses imply lower

excess returns. As for size effects, unlike results documented in most papers (e.g. Moeller et al.,

2004), larger acquirers tend to realize higher excess returns than smaller acquirers at any event

window. And all the results are significant at 1% level. In general, liquidity risk does not dominate

in mergers since interbank ratio has no crucial effects on excess returns. Unfortunately, no results

for the domestic dummy or the large deal dummy are statistically significant.

Table 7. Regression exploring determinations of excess returns in M&As12

This table represents results of robust OLS regressions for each event window with clustering by bank ID. The

dependent variable in all regressions is estimated average excess returns over different window in days indicated in

each column. Independent variables are aiming at capturing characteristic for each bank at different aspects: ROAE

measures for profitability; Change in size assesses the growth rate of the bank; operating costs demonstrates cost