Malawi: MOBILIZING LONG-TERM FINANCE FOR …

164

Document of the World Bank 0 Report No: AUS0002033 . MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE FULL REPORT February 2021 FCI Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of Malawi: MOBILIZING LONG-TERM FINANCE FOR …

Document of the World Bank

0

Report No: AUS0002033

.

MALAWI: MOBILIZING LONG-TERM FINANCE FOR

INFRASTRUCTURE FULL REPORT

February 2021

FCI

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

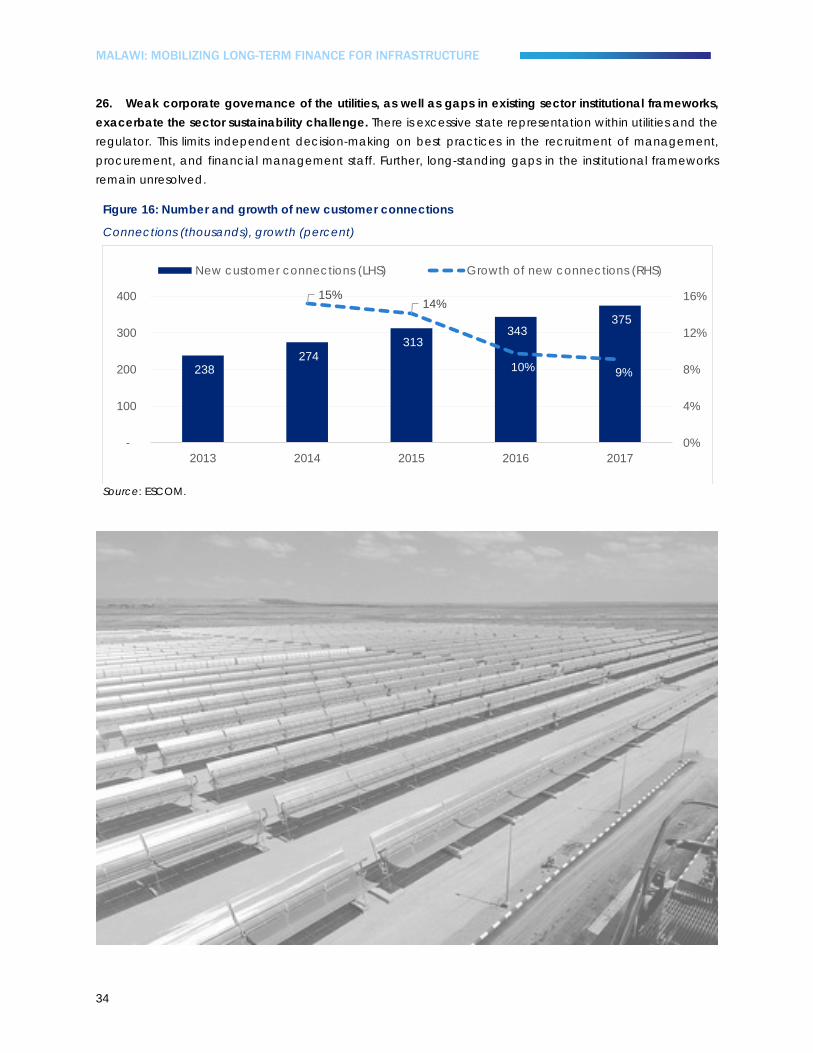

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

i

. © 2021 The World Bank 1818 H Street NW, Washington DC 20433 Telephone: 202-473-1000; Internet: www.worldbank.org Some rights reserved

This work is a product of the staff of The World Bank. The findings, interpretations, and conclusions expressed in this work do not necessarily reflect the views of the Executive Directors of The World Bank or the governments they represent. The World Bank does not guarantee the accuracy of the data included in this work. The boundaries, colors, denominations, and other information shown on any map in this work do not imply any judgment on the part of The World Bank concerning the legal status of any territory or the endorsement or acceptance of such boundaries. Rights and Permissions The material in this work is subject to copyright. Because The World Bank encourages dissemination of its knowledge, this work may be reproduced, in whole or in part, for noncommercial purposes as long as full attribution to this work is given. Attribution—Please cite the work as follows: “World Bank. 2021. Malawi: Mobilizing Long-Term Finance for Infrastructure. © World Bank.”

All queries on rights and licenses, including subsidiary rights, should be addressed to World Bank Publications, The World Bank Group, 1818 H Street NW, Washington, DC 20433, USA; fax: 202-522-2625; e-mail: [email protected].

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

Document of the World Bank

ii

Table of Contents Acknowledgments ...................................................................................................................................... viii

Executive Summary.......................................................................................................................................... 1

1 Background ............................................................................................................................................ 20

2 Infrastructure Investment Needs ......................................................................................................... 30

3 Why is Long-term Finance Not Flowing to Infrastructure Assets? ................................................. 39

4 Facilitating Access to Long-term Finance ....................................................................................... 84

References .................................................................................................................................................... 116

Annexes.......................................................................................................................................................... 123

Annex 1: Macroeconomic charts ................................................................................................................ 124

Annex 2: Financial sector charts .................................................................................................................. 133

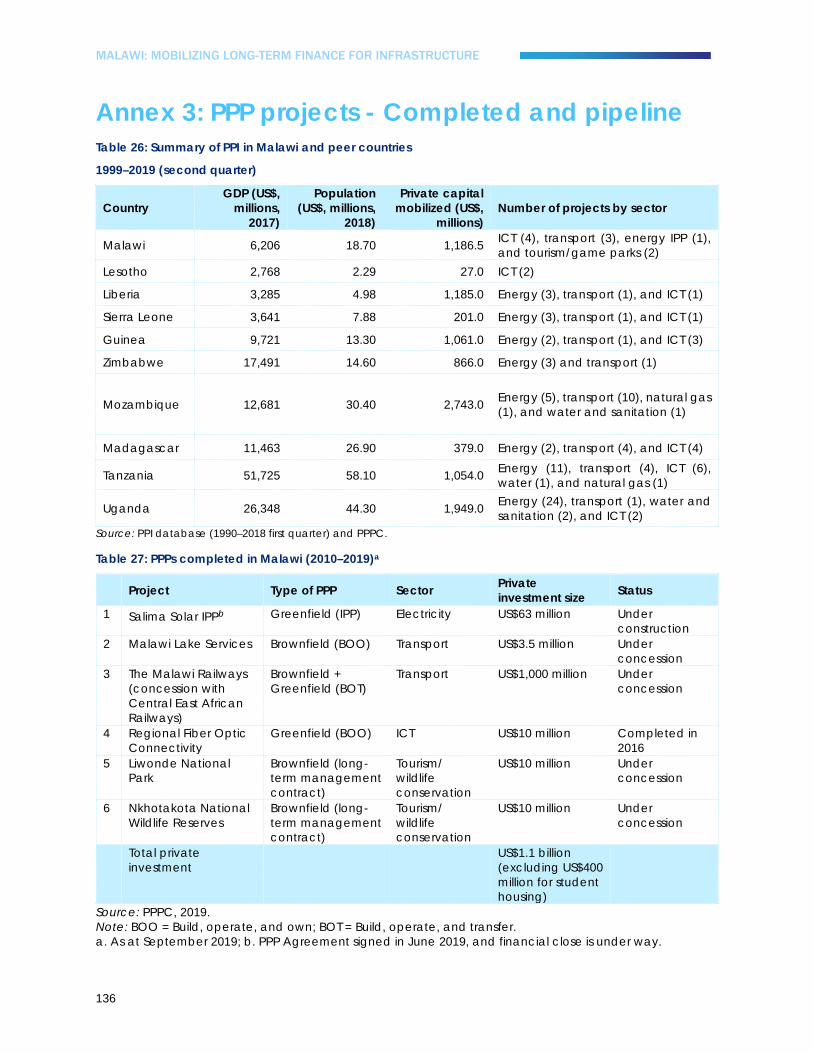

Annex 3: PPP projects - Completed and pipeline ...................................................................................... 136

Annex 4: Key issues affecting the performance and borrowing capacity of SOEs ................................ 138

Annex 5: Potential impact of COVID-19 on the infrastructure sector/SOEs and the financial system .. 147

Annex 6: Doing Business reforms undertaken by Malawi (2008–19) ......................................................... 150

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

Document of the World Bank

iii

List of figures Figure 1: An ecosystem approach to mobilizing long-term finance for infrastructure ......................................... 5 Figure 2: A coordinated framework of incentives for improved performance of SOEs ....................................... 9 Figure 3: Public investment ....................................................................................................................................... 22 Figure 4: Public capital stock .................................................................................................................................... 22 Figure 5: Cross-border finance to developing countries, 2000–16 ........................................................................ 23 Figure 6: PPP Investment (1998–2017) ...................................................................................................................... 24 Figure 7: Real GDP growth has been volatile and very low in per capita terms ................................................ 26 Figure 8: Malawi’s real GDP per capita has fallen behind peers ......................................................................... 26 Figure 9: The kwacha has depreciated against the US dollar…........................................................................... 27 Figure 10: Food and non-food inflation have decelerated .................................................................................. 27 Figure 11: Interest rate developments ..................................................................................................................... 27 Figure 12: Total investment selected countries ....................................................................................................... 27 Figure 13: Malawi electricity generation installed capacity ................................................................................. 31 Figure 14: Annual power generation ....................................................................................................................... 31 Figure 15: The structure of the electricity sector in Malawi .................................................................................... 33 Figure 16: Number and growth of new customer connections ............................................................................ 34 Figure 17: Access to improved water ...................................................................................................................... 35 Figure 18: Government water, sanitation and hygiene (WASH) spending .......................................................... 36 Figure 19: Average WASH spending of Malawi versus regional peers ................................................................. 36 Figure 20: Projects with private participation in Sub-Saharan Africa ................................................................... 41 Figure 21: PPP Investments ........................................................................................................................................ 41 Figure 22: Approach to assessing SOEs’ market readiness .................................................................................... 48 Figure 23: Distance-to-market score for each SOE ................................................................................................ 49 Figure 24: Accumulated nonresident portfolio flows to emerging markets since the start of various crises .... 56 Figure 25: Commercial and development and export finance institutions (DEFIs)/public debt for projects with private participation.......................................................................................................................................... 58 Figure 26: Local and international commercial debt ............................................................................................ 58 Figure 27: Commercial banks’ sources of funds and deposits maturity structure ............................................... 59 Figure 28: Commercial banks' asset composition and loan maturity structure .................................................. 59 Figure 29: Banks' investments in government securities and loans (2015–19) ...................................................... 60 Figure 30: Composition of banks loans by sector ................................................................................................... 61 Figure 31: Growth of bank lending by sector.......................................................................................................... 61 Figure 32: Distribution of the value of MAIIC approved and pipeline projects by sector .................................. 62 Figure 33: Distribution of the value of MAIIC approved and pipeline by project phase ................................... 62 Figure 34: Horizon IRRs ............................................................................................................................................... 64 Figure 35: Preqin indexa ............................................................................................................................................. 64 Figure 36: Aggregate asset allocation of 7 key markets (1998–2018) .................................................................. 65

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

Document of the World Bank

iv

Figure 37: Investors in infrastructure by type, 2015 versus 2019 ............................................................................. 65 Figure 38: Current allocations to alternative assets by asset class: Australian superannuation schemes vs. Global Pension Funds (percentage of total assets) ............................................................................................... 66 Figure 39: Allocation of pension funds AUM ........................................................................................................... 71 Figure 40: Allocation of life insurance AUM ............................................................................................................. 71 Figure 41: Market cap of listed companies ............................................................................................................. 71 Figure 42: Stock market liquidity ............................................................................................................................... 71 Figure 43: Life insurers' solvency ratio - Whole company level .............................................................................. 74 Figure 44: Life insurers' solvency ratio - Life fund level ............................................................................................ 74 Figure 45: The yield curve has been extending ...................................................................................................... 75 Figure 46: Domestic debt has shifted toward longer-maturing instruments ........................................................ 75 Figure 47: Infrastructure projects’ default rates (1966–2016) ................................................................................. 79 Figure 48: Drivers to locate in or consider future investment in Sub-Saharan Africa .......................................... 80 Figure 49: Factors affecting the decision to invest overseas ................................................................................. 80 Figure 50: Evolution of Malawi’s Doing Business (DB) ranking ............................................................................... 80 Figure 51: Malawi’s DB 2019 index scores: 100 = Best performance ..................................................................... 81 Figure 52: Proposed framework for developing project pipeline (PIM-PPP integrated framework) ................. 86 Figure 53: World Bank for infrastructure finance in Kenya ..................................................................................... 90 Figure 54: Various stages of project development and potential sources of funds ........................................... 91 Figure 55: IBNET - Global experience on impact of internal reforms on cash positiona ..................................... 99 Figure 56: Illustrative annual savings based on various internal reforms ............................................................ 100 Figure 57: Access to long-term liquidity to create the mortgage market in Tanzania, facilitated by the World Bank .......................................................................................................................................................................... 106 Figure 58: Potential capital markets instruments .................................................................................................. 108 Figure 59: Public domestic debt shifting from RBM to commercial banks and non-bank sector ................... 127 Figure 60: Domestic debt has been increasing, while external debt has declined ......................................... 127 Figure 61: High primary deficits and interest rates remain key drivers of total public debt ............................. 128 Figure 62: Fiscal deficits regularly overshoot budget levels ................................................................................. 128 Figure 63: Food inflation pressures have started subsiding in 2020 ..................................................................... 128 Figure 64: Inflationary pressures picked up on the regional front ....................................................................... 128 Figure 65: US dollar/MWK official and forex bureau (FXB) rates and spreads through May 6, 2020 ............... 129 Figure 66: US dollar/MWK rate versus selected currencies, real effective exchange rate index, through April 30, 2020 ..................................................................................................................................................................... 129 Figure 67: Private sector credit growth remained strong through March .......................................................... 129 Figure 68: Financial soundness indicators were healthy at the onset of the crisis ............................................ 129 Figure 69: PPP investment in Malawi (1998–2017) ................................................................................................. 130 Figure 70: PPP investment in Mozambique (1998–2017) ...................................................................................... 130 Figure 71: PPP investment in Zambia (1998–2017) ................................................................................................ 130 Figure 72: PPP investment in Tanzania (1998–2017) .............................................................................................. 130

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

Document of the World Bank

v

Figure 73: PPP investment in Kenya (1998–2017) .................................................................................................. 130 Figure 74: PPP investment in Uganda (1998–2017) ............................................................................................... 130 Figure 75: PPP investment in Rwanda (1998–2017) ............................................................................................... 131 Figure 76: PPP investment in Ghana (1998–2017) ................................................................................................. 131 Figure 77: PPP investment in Côte d'Ivoire (1998–2017) ....................................................................................... 131 Figure 78: PPP investment in Senegal (1998–2017) ............................................................................................... 131 Figure 79: PPP investment in Myanmar (1998–2017) ............................................................................................. 131 Figure 80: PPP investment in Bangladesh (1998–2017) ......................................................................................... 131 Figure 81: PPP investment in Nepal (1998–2017) ................................................................................................... 132 Figure 82: Regulatory capital .................................................................................................................................. 133 Figure 83: Liquidity ratios ......................................................................................................................................... 133 Figure 84: Private sector credit growth .................................................................................................................. 133 Figure 85: Financial soundness indicators .............................................................................................................. 133 Figure 86: ESCOM - Differentiated tariffs across consumers/uses ....................................................................... 140

List of tables Table 1: The theory of change - Summary of key recommendations and expected results ............................ 16 Table 2: Recommendations implementation summary ........................................................................................ 17 Table 3: Base, low, and high electricity demand forecast .................................................................................... 31 Table 4: Base case generation and transmission cost: 2020–40 ........................................................................... 32 Table 5: Net present value (NPV) for generation expansion scenarios ............................................................... 32 Table 6: WASH sector investments requirements .................................................................................................... 37 Table 7: Investment commitments and no. of projects with private participation in IDA countries ................. 41 Table 8: Capital investment requirements of SOEs ................................................................................................. 48 Table 9: Market readiness scores and borrowing capacity .................................................................................. 49 Table 10: Comparison of select liquidity and asset efficiency indicators of SOEs (2018) ................................... 55 Table 11: The size of the financial sector in Malawi ................................................................................................ 57 Table 12: Capital raising plan of MAIIC ................................................................................................................... 62 Table 13: Pension assets of select African countries (2018) ................................................................................... 68 Table 14: Assets of select African pension funds (2019) ......................................................................................... 68 Table 15: Life insurance assets of select African countries (2019) ........................................................................ 68 Table 16: Assets of select African SWFs/SIFs ............................................................................................................ 68 Table 17: Investment returns of select African institutional investors .................................................................... 69 Table 18: Institutional investors' assets (2014–19) ..................................................................................................... 70 Table 19: Comparison of stock market returns across select African markets .................................................... 72 Table 20: Tax rates and tax administration indicators in Malawi .......................................................................... 83 Table 21: Sample of numeric debt control measures .......................................................................................... 102 Table 22: Selected macroeconomic indicators ................................................................................................... 124

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

Document of the World Bank

vi

Table 23: Fiscal accounts ........................................................................................................................................ 126 Table 24: Outstanding bonds on the MSE ............................................................................................................. 134 Table 25: Stock market size and liquidity ............................................................................................................... 135 Table 26: Summary of PPI in Malawi and peer countries ..................................................................................... 136 Table 27: PPPs completed in Malawi (2010–2019)a .............................................................................................. 136 Table 28: Summary of infrastructure PPP pipeline in Malawi ............................................................................... 137 Table 29: Summary of ESCOM's expenditure ........................................................................................................ 141 Table 30: The potential COVID-19 impact on infrastructure sector/SOEs and the financial system - Malawi context ...................................................................................................................................................................... 148

List of boxes Box 1: Potential macroeconomic impact of COVID-19 ........................................................................................ 29 Box 2: The financing structure of the Nacala Railway Corridor project ............................................................... 43 Box 3: An example of procurement risks: Procurement for the Lake Malawi-Salima project ........................... 46 Box 4: Issuance of bonds by RFA .............................................................................................................................. 47 Box 5: Kenya infrastructure finance and World Bank support ............................................................................... 89 Box 6: RFA: Composition and nomination of board members ............................................................................. 96 Box 7: Potential (indicative) criteria for issuing guarantees ................................................................................. 103 Box 8: Pension funds in Tanzania: Risks emanating from political exposure ...................................................... 107 Box 9: GuarantCo: Local currency bond guarantee in Kenya .......................................................................... 110 Box 10: An example of a market-led investment vehicle: Meridiam (Europe, North America, and Africa) .. 113 Box 11: An example of a public-private investment vehicle: PINAI ................................................................... 114

vii

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

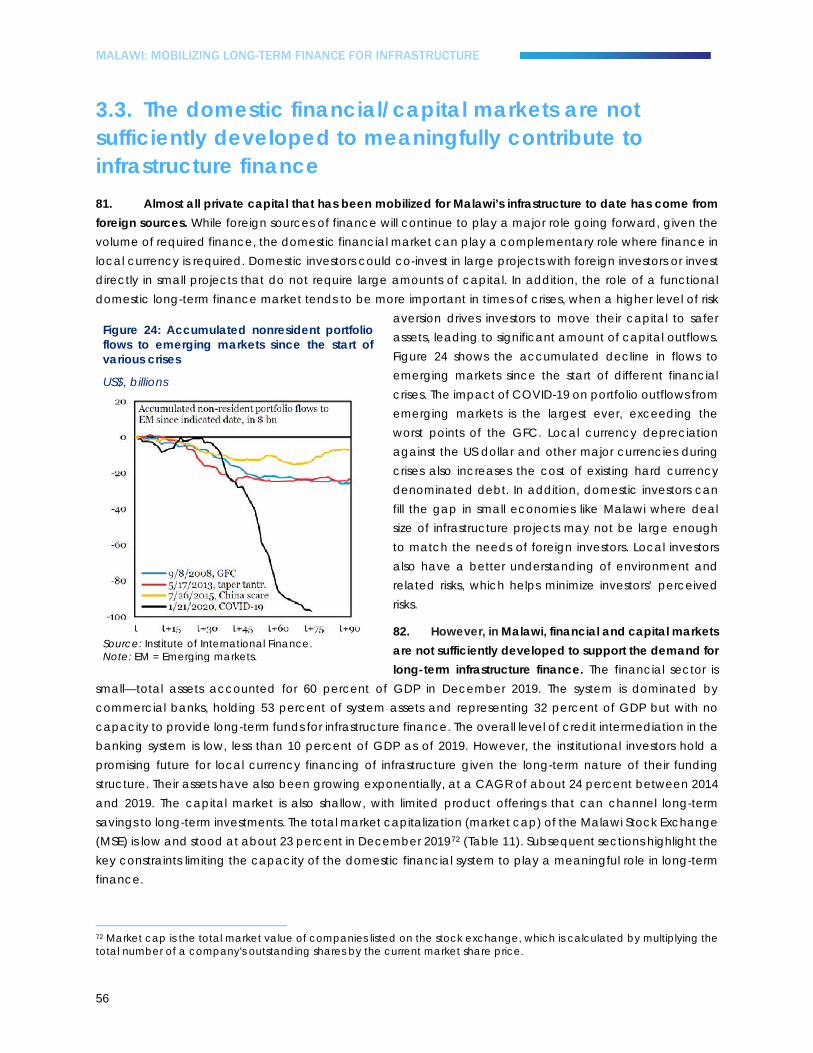

viii

Acknowledgments This report was prepared by a multidisciplinary team of World Bank staff and consultants in collaboration with the Government of Malawi. The team was led by Neema Mwingu (Senior Financial Sector Specialist and Task Team Leader) and included Anuradha Ray (Senior Financial Sector Specialist), Joel Turkewitz (Lead Public Sector Specialist), Johan Kruger (Consultant), Haeyoung Lee (Private Sector Development Specialist), Dhruva Sahai (Senior Financial Specialist), Kagaba Paul Mukiibi (Energy Specialist), Patrick Hettinger (Senior Economist), Odete Duarte Muximpua (Water Supply and Sanitation Specialist), Josses Mugabi (Senior Water Supply and Sanitation Specialist), Yi Yan (Extended Consultant), Sebastian Phillip Sarmiento-Saher (Consultant), William Nyambo Mwanza (Consultant), Yalenga Loraine Nyirenda (Consultant), Tamara Mwafongo (Team Assistant), Miriam Kalembo (Team Assistant) and MaryIrene Singili (Team Assistant). The report was prepared under the overall guidance of Mara K. Warwick (Country Director for Tanzania, Malawi, Zambia, and Zimbabwe), Hugh Riddell (Country Manager, Malawi), Greg Toulmin (former Country Manager, Malawi), and Niraj Verma (Practice Manager, Finance, Competitiveness and Innovation).

Since the commencement of the assessment, the team received valuable input from the following individuals: Yutaka Yoshino (Program Leader); Prajakta Ajit Chitre (Senior Infrastructure Finance Specialist), Jeffrey John Delmon (Senior Infrastructure Finance Specialist), Helen Mary Martin (Senior Public-Private Partnerships Specialist), Jing Zhao (Senior Financial Sector Specialist), Jane Jamieson (Senior Infrastructure Finance Specialist), and Silvia Maria Tanga (Investment Officer, International Finance Corporation). The team is grateful to the peer reviewers for their valuable inputs and comments: Arnaud D. Dornel (Lead Financial Sector Specialist), Fiona Elizabeth Stewart (Lead Financial Sector Specialist), Lizmara Kirchner (Senior Water Supply and Sanitation Specialist), and Gael Raballand (Lead Public Sector Specialist).

Throughout the preparation of this report, the World Bank has received excellent support and cooperation from the Government of Malawi and the private sector. The team would like to thank the following individuals within the government for their willingness to share their insights, information, and support with the team throughout the process: Mr. Lloyd Muhara (former Chief Secretary to the Government, Office of the President and the Cabinet [OPC]); Mr. Stuart Ligomeka (former Comptroller of Statutory Corporations, OPC); Mr. Cliff Chiunda (Principal Secretary, Administration - OPC and former Secretary to the Treasury); Ms. Seodi White (Chief Director, Public Sector Reforms Management Unit - Ministry of Economic Planning and Development); Mr. Peter Simbani (Principal Secretary, Ministry of Industry and former Acting Chief Director of Economic Planning and Development, Ministry of Finance [MoF]), Mr. Twaib Ali (Acting Director of Debt and Aid Management, MoF), Ms. Betty Ngoma (former Acting Director of Debt and Aid Management, MoF), Mr. Ambrose Mzoma (former Director of Pensions and Financial Sector Policy, MoF), Mr. Hetherwick Njati (former Director of Public Enterprises Reform and Monitoring Unit, MoF),Martha Chizimba (Chief Economist, Public Enterprises Reform and Monitoring Unit, MoF); Mr. Patrick Matanda (Principal Secretary, Ministry of Energy) and his staff, including Mr. Hastings Chipongwe (Director of Policy and Planning); Mr. Gray Nyandule Phiri (former Principal Secretary, Ministry of Agriculture, Irrigation, and Water Development) and

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

ix

his staff, including Ms. Emma Mbalame (Director of Water Supply and Sanitation);Mr. Joseph Mwandidya (former Principal Secretary, Ministry of Lands, Housing and Urban Development) and his staff; Dr. Dalitso Kabambe (former Governor of the Reserve Bank of Malawi); Dr. Grant Kabango (Deputy Governor, Economics and Supervision); Ms. Chimwemwe Kachingwe (former Director, Bank Supervision), Mr. Chitani Chigumula (Director, Pensions & Insurance Supervision); Mr. Lanjes Sinoya (Director, Bank Supervision); Mr. Kisukyabo Simwaka (Director, Economic Policy Research); Mr. Rodrick Wiyo (former Director, Financial Markets); Mr. George Chioza (former Director, Financial Sector Regulation); Mr. John Kamanga (Chief Executive Officer [CEO] of the Malawi Stock Exchange); Mr. William Liabunya (CEO of the Electricity Generation Company) and his staff; Dr. Allexon Chiwaya (CEO of the Electricity Supply Corporation of Malawi) and his staff; Mr. Dan Chaweza (CEO of the Blantyre Water Board) and his staff; Mr. Stewart Malata (CEO of the Roads Fund Administration) and his staff; Engineer Emmanuel Matapa (CEO of the Roads Authority) and his staff, including Mr. Joel Longwe (Regional Manager, Central Regional Office) and Mr. Patrick Kamanga (Project Engineer); Mr. Alfonso Chikuni (former CEO of Lilongwe Water Board) and his staff; Mr. Elias Hausi (Director General of the Public Procurement and Disposal of Assets Authority) and his staff; Mr. Timothy Mponela (Assistant Auditor General of the National Audit Office) and his staff; Eng. Titus C. Mtegha (CEO of the Northern Regional Water Board); Mr. Joshua Nthakomwa (Director of Investment, Promotion and Facilitation, Malawi Investment and Trade Center); and the staff from the Malawi Housing Corporation, in particular, Mr. Jordan Chipatala (Director of Finance); Mr. Leslie Majawa (Chief Operations Officer); and Mr. Chancy Chaguluka (Business Research and Development Manager).

Finally, the team would like to thank the following stakeholders from the private sector and the development partners’ community, who provided inputs and advice during the assessment: Ms. Edith Jiya (CEO of Old Mutual Malawi), Mr. Mark Mikwamba (the Managing Director of Old Mutual Investment Group), Ms. Gillian Kachilaondo (CEO of Continental Asset Management), Mr. McFussy Kawawa (CEO of National Bank of Malawi), Mr. Jean Moukala (Acting CEO of the CDH Investment Bank), Mr. Kondwani Mlilima (Chief Risk Officer, Standard Bank), Mr. McLewen C. Sikwese (Head of Global Markets, Standard Bank), Mr. Daniel Dunga (Chief Investment Officer, NICO Asset Managers), Mr. Taz Chaponda (CEO of the Malawi Agriculture and Industrial Investment Corporation [MAIIC]), Ms. Fosters Sikwese (Enterprise Development Specialist, MAIIC), Mr. Armstrong Kamphoni (CEO of Cedar Capital), Mr. Davies B. Makasa (Principal Transport Engineer, African Development Bank); Jonathan Banda (Investment Officer, African Development Bank), Mr. Andrew Spahn (Deputy Director, Energy Office, Power Africa, United States Agency for International Development), and Mr. Thomas Haslett (Senior Energy Advisor, United States Agency for International Development).

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

x

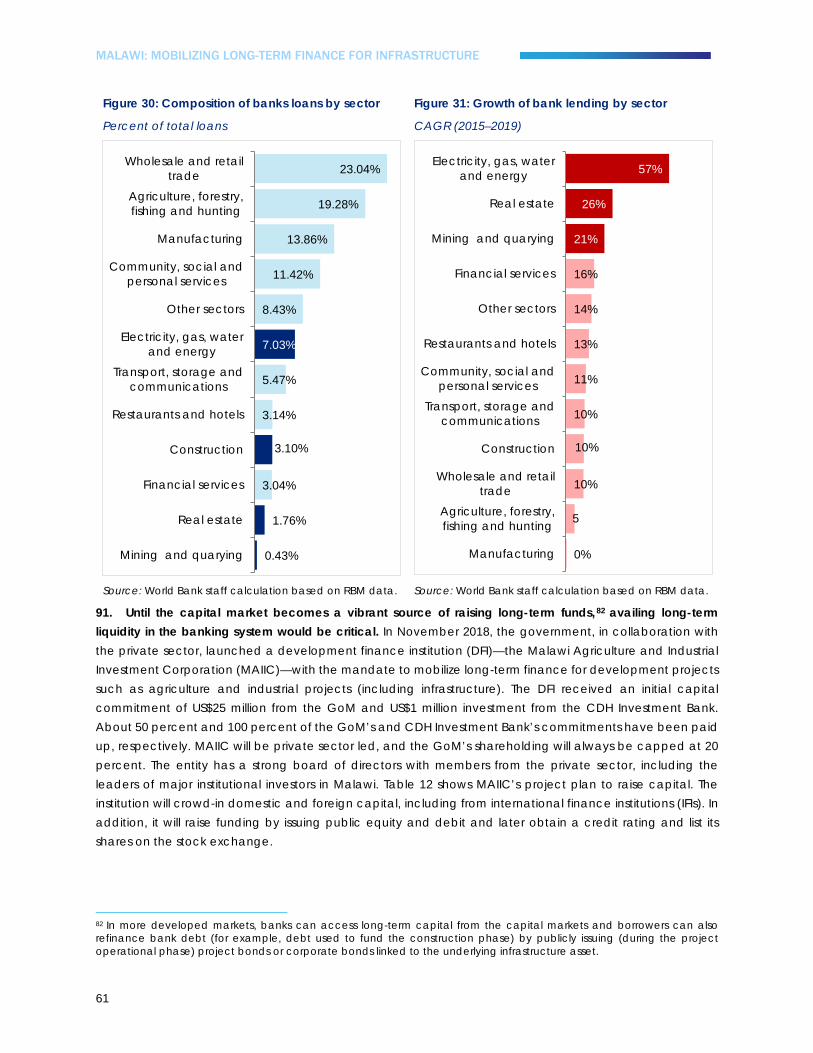

Acronyms ABS Asset-backed Securities AfDB African Development Bank AIIM Africa Infrastructure Investment Managers ATI African Trade Insurance Agency ATS Automated Trading System AUM Assets under Management BOO Build, Operate, and Own BOT Build, Operate, and Transfer BWB Blantyre Water Board CAGR Compound Annual Growth Rate CAPEX Capital Expenditure CDS Central Depository System CEO Chief Executive Officer COVID-19 Coronavirus Disease 2019 CPI Consumer Price Index CSD Central Securities Depository DB Doing Business DBJ Development Bank of Jamaica DEFIs Development and Export Finance Institutions DFI Development Finance Institution DSC Department of Statutory Corporations DSCR Debt Service Coverage Ratio DWS Department of Water and Sanitation ECA Export Credit Agency EGENCO Energy Generation Company EIB European Investment Bank EMDEs Emerging Markets and Developing Economies EPC Engineering, Procurement, and Construction EPCF Engineering, Procurement, and Construction and Finance EPPF Eskom Pension & Provident Fund ESCOM Electricity Supply Corporation of Malawi FONSIS SA Senegal’s Fonds Stratégique d’Invéstissments Forex/FX Foreign Exchange FSAP Financial Sector Assessment Program FSDEA Fundo Soberano de Angola FXB Foreign Exchange Bureau GCR Global Credit Rating GDP Gross Domestic Product GEPF Government Employees Pension Fund GFC Global Financial Crisis GNI Gross National Income GoM Government of Malawi IBNET The International Benchmarking Network for Water and Sanitation Utilities

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

xi

ICT Information and Communication Technology IDA International Development Association IFC International Finance Corporation IFI International Finance Institution IFPPP Infrastructure Finance Public Private Partnership IMF International Monetary Fund IPP Independent Power Producer IRP Integrated Resource Plan IRR Internal Rate of Return JV Joint Venture KfW Kreditanstalt für Wiederaufbau LIC Low-income Country LMIC Lower-middle-income Country LOE Letter of Expectations LUANAR Lilongwe University of Agriculture and Natural Resources LWB Lilongwe Water Board MAIIC Malawi Agriculture and Industrial Investment Corporation MCC Millennium Challenge Corporation MDAs Ministries, Departments, and Agencies MERA Malawi Energy Regulatory Authority MHC Malawi Housing Corporation MIGA Multilateral Investment Guarantee Agency MIRA Macquarie Infrastructure and Real Assets MoF Ministry of Finance MoEPD Ministry of Economic Planning and Development MSE Malawi Stock Exchange MTN Medium-term Note MV Medium Voltage NISA Nigeria Sovereign Investment Authority NPL Nonperforming Loan NPV Net Present Value NRW Nonrevenue Water NRWB Northern Region Water Board NSO National Statistical Office NWSC National Water and Sewerage Corporation O&M Operation and Maintenance ODA Official Development Assistance OECD Organisation for Economic Co-operation and Development OPC Office of the President and the Cabinet OPEX Operational Expenditure OTC Over-the-counter PAT Profit after Tax PERMU Public Enterprises Reform and Monitoring Unit PFMA Public Finance Management Act PIM Public Investment Management

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

xii

PINAI Philippine Investment Alliance for Infrastructure PPA Power Purchase Agreement PPDA Public Procurement and Disposal of Assets Authority PPF Project Preparation Facility PPI Private Participation in Infrastructure PPP Public-Private Partnership PPPC PPP Commission PPPU PPP Unit PSIP Public Sector Investment Program RBM Reserve Bank of Malawi REIT Real Estate Investment Trust RFA Roads Fund Administration SADC Southern African Development Community SAPP Southern African Power Pool SB Single Buyer SDGs Sustainable Development Goals SIF Strategic Investment Fund SMEs Small and Medium Enterprises SOE State-owned Enterprise SPV Special-purpose Vehicle SWF Sovereign Wealth Fund TCX Currency Exchange Fund UNICEF United Nations Children’s Fund WASH Water, Sanitation, and Hygiene WSIP Water Sector Investment Plan y-o-y Year-on-year ZCPN Zero-coupon Promissory Note

1

Executive Summary

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

2

Overview

1. This study 1 explores how the Government of Malawi (GoM) can mobilize long-term finance for infrastructure. Infrastructure development involves large amounts of up-front capital expenditure (CAPEX), which poor governments like Malawi struggle to meet given the small tax base, limited room to raise taxes, and the declining official development assistance (ODA).2 In Malawi, this is evidenced by the low level of public investment (which averaged 4.18 percent of the gross domestic product [GDP] between 1998 and 2017). As a result, the public capital stock per capital (a proxy for infrastructure stock) grew at a compound annual growth rate (CAGR) of only 0.88 percent during the same period.3 The large infrastructure investment requirements (about 8 percent of GDP annually for the few sectors and state-owned enterprises [SOEs] covered in this report) compared to the past low level of public investments, and given the growing population which is putting pressure on service delivery, necessitate urgent actions by the GoM to rethink the current modality of financing infrastructure. This study provides a framework for maximizing the volume of investment and finance for infrastructure projects, including the public-private partnership (PPP) projects and those undertaken by SOEs,4 which are the main channel of delivering infrastructure in Malawi. The report recommends how to leverage the large corpus of market-based finance5 from the private sector, coupled with a careful prioritization of where public finance from the GoM and its development partners is essential.

2. Mobilizing finance, especially market-based finance, raises the question of how to fund (pay for) infrastructure, usually from two main sources, namely end-user charges/tariffs and tax revenues. The ability of Malawi to mobilize finance that can be repaid from tariffs will be limited by the high level of poverty, currently forcing the GoM to deal with tariff increases carefully.6 Experience from other countries shows that private investment and financing of infrastructure range from 0 to 1 percent of GDP, with a global average of about 0.5 percent. Data from the International Monetary Fund (IMF) show that, in the past two decades (1998–2017), investments in PPP projects globally averaged 0.51 percent of GDP.7 In addition, estimates by Thomson Reuters show that project finance loans totaled US$282.7 billion (0.33 percent of GDP), of which nearly half (48.7 percent) were loans to power projects.8 This estimate excludes financing through project bonds and equity financing.9 It should be noted that the ratio of investment and financing relative to GDP tends to be higher in low-income countries (LICs) and lower-middle-income countries (LMICs) than in

1 The study was carried out between February 2019 and June 2020. 2 According to the 2018 report of the Organization for Economic Co-operation and Development (OECD) on the Global Outlook for Financing for Sustainable Development, the growth of cross-border financing to poor countries from bilateral and multilateral development partners between 2000 and 2016 was lower than the growth of private capital flows, with a notable decline in multilateral flows post the global financial crisis (GFC). Bilateral and multilateral financing grew at a CAGR of 4 percent compared to 6 percent for private long-term debt/lending and 8 percent for portfolio investment (indirect investment into portfolios of assets such as stocks, bonds, real estate, and infrastructure, typically through investment funds). The CAGR of multilateral flows post the crisis (2009–16) was only 1 percent of GDP. 3 World Bank staff calculations based on IMF data. 4 There are four main channels of investing and financing infrastructure: (a) Direct procurement by the government through line ministries, departments, and agencies (MDAs) (this is out of the scope of this report); (b) Project finance/PPPs, which is financing of long-term infrastructure projects using a nonrecourse or limited-recourse structure. The debt and equity used to finance the project are paid back from the cash flow generated by the project without recourse to the project sponsor or the parent company; hence, lenders look at the debt servicing capacity of the project rather than that of the parent company. This is different from corporate (or balance sheet financing), where lenders provide finance to a company, which may be invested in specific projects, and have full recourse to total assets of the company in case of a default. (c) Private utilities (fully or partially privatized utilities) and/or concessions to a private sector company of state-owned assets. Currently, there are no private utilities in Malawi. (d) SOEs/state-owned utilities with varying degrees of commercialization. 5 Financing based on commercial terms provided by foreign and domestic commercial banks and capital markets investors. 6 End-user charges need to be affordable, otherwise consumers either cannot or will not pay. 7 Based on IMF Investment and Capital Stock Dataset, 2019. 8 https://practiceguides.chambers.com/practice-guides/project-finance-2019-second-edition. 9 In developing countries, equity financing accounts for 10–20 percent of project costs.

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

3

developed economies, since they need to invest more in infrastructure than rich countries The analysis based on IMF data shows an average ratio of 0.14 percent of GDP for high-income countries over the past two decades compared to 0.41 percent for LICs and 0.89 percent for LMICs.10 The ratio for Malawi is much lower than the average for LICs, that is, 0.07 percent of GDP in the two decades. Based on these trends, aiming for private investment and financing of about 0.5 percent of GDP annually could be a sustainable vision for Malawi.

3. Since the amount of private capital that can be mobilized relative to the size of the economy and the level of required investment would be small, public finance will remain the main source of financing infrastructure in Malawi in the foreseeable future. Malawi will need to mobilize a combination of three main types of long-term finance: (a) purely market-based sources of finance from foreign and domestic banks and capital market investors; (b) market-based and blended finance 11 from public financiers with commercial mandates such as the International Finance Corporation (IFC) and the Kreditanstalt für Wiederaufbau (KfW); and (c) public sources, that is, direct finance from tax revenues and concessional lending and grants from bilateral donors and multilateral lending institutions such as the World Bank (International Development Association [IDA]) and the African Development Bank (AfDB). These can be intermediated through the national budget or offered directly to projects or SOEs.

4. This report argues that the GoM should put in place measures to maximize market-based sources for projects and SOEs that are commercially viable or whose commercial viability12 could be enhanced and move from the current practice where almost all projects (whether commercially viable or not) are financed by public sources finance. A greater emphasis on additionality in the use of scarce public finance is recommended. Public finance could be best deployed to projects that cannot attract private capital (for example, social infrastructure projects) and those that require government contribution through PPP arrangements. Governments’ contribution in PPPs would vary depending on the commercial viability of the infrastructure sector or project, which is usually lower for power plants and potentially airports; higher for surface transport, water, and sanitation; and highest (almost 100 percent) for social infrastructure. For PPPs in which the majority or 100 percent of finance would come from the public, the motivation for engaging the private sector is not finance but to leverage private sector efficiency in project implementation. Public finance can also be best deployed to address market failures in the enabling environment, which will in turn improve the risk-return profile of projects and unlock the flow of market-based finance.

5. While affordability of fully commercial tariffs imposes limitations on mobilization of private capital, increased focus on infrastructure planning and implementation efficiency, both at the state and SOE level, can improve the fiscal space and borrowing capacity and thus increase the capacity to invest in additional infrastructure. Investment in infrastructure and related borrowing by the GoM or SOEs (including government guarantees to de-risk projects and SOEs), whether funded by tariffs or the state budget, contribute to further build-up of the national debt, which is already high (at 63 percent of GDP in 2019, which has increased from

10 The data include resource-based infrastructure projects which are funded through export/forex revenue of natural resources (for example, the Nacala Project in Mozambique and Malawi which is funded from coal export revenues). If only projects that are funded from domestic revenues (that is, user charges, government pay, or a combination of both) are considered, the ratio could be lower for some countries. 11 This is a package of finance that blends concessional finance from development partners and finance from commercial markets. This type of finance can be availed for projects with high potential impact but would not attract finance on purely commercial terms because the risks are considered too high and/or commercial returns are either unproven or not in line with the level of risk. 12 Commercial viability is achieved when project revenues from user charges exceed costs and yield sufficient returns to repay the cost of capital and when associated risks are considered reasonable by investors.

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

4

28 percent of GDP in 2007).13 Therefore, the GoM should always ensure the infrastructure investment program is affordable, both in terms of up-front investment capital and future resource requirements to maintain the already created infrastructure. The report presents recommendations on how this could be achieved by reforming the Public Investment Management (PIM) framework to help (a) reduce and preferably abandon spending on low-priority infrastructure; (b) encourage ministries, department, and agencies (MDAs) to leverage market-based finance for projects that can attract private capital; (c) enhance the efficiency of infrastructure procurement to ensure value for money; and (d) enhance the efficiency of infrastructure project implementation and monitoring, including leveraging private sector efficiency through PPPs. Improving the financial performance of SOEs through better governance and enhanced operational efficiency is also recommended. This will contribute to reduced government outlays in terms of (a) direct support to cover operational expenditure (OPEX), which should always be covered by commercial SOEs; (b) bailouts of poorly performing SOEs; and (c) payments related to defaults on government-guaranteed debt and improve borrowing capacity14 and ability to directly access market-based finance.

6. To manage the fiscal space and ensure the affordability of the infrastructure investment program, it is recommended that, during infrastructure planning, the GoM undertakes an up-front estimation of the potential fiscal impact of long-term deficits that may be created by infrastructure projects, whether projects are undertaken by SOEs or through PPPs and whether they are financed by the public or the private sector. This should include (a) in-depth economic and financial analyses of proposed projects and gauging of the level of outright and/or contingent government support that is needed to improve their commercial viability; (b) risk identification, quantification, and mitigation for PPP projects; and (c) continuous management/monitoring of outright and contingent liabilities and risks.

7. Catalyzing the long-term finance market for infrastructure and making well-thought-out choices in the use of public finance is more important now in light of the global coronavirus disease 2019 (COVID-19), as pressure on public resources increases to respond to the pandemic. As economic activities decline, financial inflows to both global and domestic financial institutions will decrease, money markets will become more volatile, and risk aversion will increase. Utilities that depend on end-user revenues are likely to experience decreased demand and increased levels of unpaid bills across commercial, industrial, and residential consumers, and as a result, suffer from liquidity strain and declining revenues (see Annex 5 for a detailed description of the COVID-19 impact). However, the crisis provides the opportunity for the GoM to “build-back-better” frameworks and systems that will improve the availability of long-term finance. The crisis can be leveraged to motivate and accelerate the needed reforms, which will help improve investors’ confidence and increase access to finance when markets return to normal. In addition, the crisis provides an even stronger case for building a more dynamic and resilient domestic long-term finance market. This will not only complement foreign capital flows but also act as a risk mitigant in future crises when projects struggle to attract finance from international investors due to increased risk aversion and capital flight to safety.

8. Mobilizing long-term finance is an agenda that will require a sustained engagement over a long period. Immediate actions by the GoM are needed, given the growing infrastructure gap and the negative impact

13 To enhance public debt transparency, the International Public Sector Accounting Standards Board and the IMF call for the consolidation of PPP debt, which is usually undertaken off the government balance sheet and government guarantees to attract private capital, which can carry hidden and sometimes higher costs than the traditional public financing, into the accounting of total public debt. This approach is currently taken by the IMF and the World Bank in debt sustainability assessments. 14 Borrowing capacity is determined by the ability of the company to generate discretionary/surplus cash flow, which is a function of revenue generation capacity, operational efficiency, efficient capital planning, and the cost of existing debt. Financiers may offer loans ranging from two to six times the level of earnings before interest, tax, depreciation and amortization (a company that exceeds these ratios is over-indebted) but would further subtract the cost of existing debt to determine the actual free cash flow and hence the capacity to absorb additional debt.

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

5

on economic growth and poverty. As this report indicates, the time is ripe to rebuild the relationship between finance and development in Malawi through a well-conceived program of activities that will help establish well-functioning financial/capital markets for long-term financing of public investments. Achieving this objective requires an array of well-coordinated activities relating to strengthening the PIM framework and institutions; ensuring macro-fiscal stability; enhancing bankability of infrastructure projects and SOEs; and deepening the financial/capital market through enabling regulations, testing new solutions, and building the capacity of the domestic financial market players (Figure 1).

9. More fundamentally, success will depend on the GoM establishing efficient mechanisms to coordinate and deliver a range of activities across government; making credible commitments to rule-based governance of SOEs; and providing policy and implementation consistency that is essential to get public officials and private investors to collaborate and adjust their behavior in accordance with laid-out rules and standards. Individual technical achievements in one or more of the identified areas are sustainable to the extent that they build upon each other to introduce rules, procedures, deals, and markets that generate benefits while preventing backsliding to older, familiar, but less efficient means of political and economic governance. In this manner, the technical work program proposed in this report aims to contribute to the larger effort to create a more efficient and transparent pathway for Malawi to mobilize infrastructure finance.

A large infrastructure gap with limited borrowing capacity necessitates reforms

10. The demand analysis in this report has been undertaken through the lenses of the energy and water sectors as illustrative sectors. In addition to being among the priority sectors of the GoM, the energy and (especially the urban) water supply sectors present relatively more immediate commercial opportunities for private investments. These sectors generate commercial revenues from users and have the potential to become self-sustaining. Borrowing capacity has been established for five SOEs in the two sectors: the Energy Generation Company (EGENCO), the Electricity Supply Corporation of Malawi (ESCOM), Lilongwe Water Board (LWB), the Northern Region Water Board (NRWB), and the Blantyre Water Board (BWB). To offer a critical mass for comparison, two more entities with end-user revenue generation capacity, that is, the Malawi Housing Corporation (MHC) and the Roads Fund Administration (RFA), have also been covered.

Figure 1: An ecosystem approach to mobilizing long-term finance for infrastructure

Source: World Bank staff.

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

6

11. The infrastructure investment needs in these sectors/SOEs are significant. In the energy and water supply and sanitation sectors alone, about US$7.6 billion would be needed over 15–20 years from 2020 or an annual investment of US$332 million (about 4 percent of 2019 GDP). The investment needs related to MHC and RFA amount to an additional annual requirement of US$326 million15 (a further 4 percent of 2019 GDP). The size of infrastructure investment needs, coupled with (a) decreasing fiscal space of the state, (b) limitations imposed by low affordability of commercial tariffs, (c) indifferent credit profiles of infrastructure SOEs, which limit their capacity to borrow, necessitate the prioritization of the infrastructure investment program and efficiency improvement. Of the seven SOEs covered in this report, only three have bankable demand/borrowing capacity, approximately US$35 million per year (or 0.44 percent of GDP).

12. The report recommends measures to revamp the framework for selecting, procuring, implementing, and monitoring public investment projects. Current practices in the identification, appraisal, and selection of public investment projects reflect the assumption that all projects will be financed by the government. Cost-benefit analysis of projects proposed by MDAs, including consideration of private sector financing as an option has not been undertaken. Reorienting the PIM framework and upgrading the institutional capacity to better plan and implement the public investment program should be the first critical step for the GoM to increase the fiscal space and maximize the volume of investment and finance into infrastructure. A new clear decision-making framework to prioritize private financing and conserve the scarce public resources is recommended in Section 4.1. Establishing a well-structured project preparation facility (PPF) is recommended to avail financial and technical resources for undertaking cost-benefit analysis, carrying out detailed feasibility studies, and supporting transaction structuring and monitoring during implementation, among others.

13. The GoM should also address the weak implementation of/noncompliance with procurement rules and the overall mismanagement of the project life cycle. Procurement of large and complex infrastructure projects is delicate and demanding and hence should follow structured and sequenced phases of the project life cycle within the limits of the existing legal and regulatory framework. Failure to do so (as evidenced in this report) will result in delays, cost overruns, frustrated expectations, and loss of credibility and trust. The report shows that procurement processes in Malawi are not always followed and only 25 percent of tenders go through an open and competitive process. The Public Procurement and Disposal of Assets Authority (PPDA) also reports that the overall compliance with the legal framework across entities has been varying and has fallen over time from 65 to 15 percent (IMF 2018). Addressing these issues will require a combination of (a) PPDA increasing efforts to enforce procurement rules and MDAs ensuring they undertake advance planning of procurement activities; (c) increasing transparency of the procurement process, including publishing information on procurement activities, publishing PPDA’s reports on MDAs’ compliance with procurement rules, ensuring the independence of procurement complaint reviews, and publishing their results; (d) training MDAs on procurement frameworks and regulations, including for the procurement of PPPs and independent power producers (IPPs); and (e) continuously monitoring project implementation and leveraging lessons to further improve procurement processes.

14. Operational improvements by SOEs and governance reforms by the GoM will be required to improve SOEs’ borrowing capacity. For example, the poor performance of ESCOM is a major impediment for the energy sector to attract private capital and is putting the sustainability of the sector at risk. As the transmission and distribution company, ESCOM is the only entity in the sector that generates revenues directly from

15 The detailed financial analysis of SOEs is based on audited financial statements of financial year 2017/18, which could be obtained for all SOEs to enable comparative analysis. However, new material developments observed in 2019 were included.

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

7

consumers, hence key to the funding of projects seeking private capital. However, it faces severe financial problems due to inefficiencies, low revenue generation capacity, and liquidity challenges. ESCOM’s financial performance had deteriorated to the extent that it had to request a bailout from the GoM in April 2018. This level of performance has affected (a) ESCOM’s ability to undertake regular operations and maintenance (O&M) and provide quality services and (b) customers’ willingness to pay for tariffs and the ability to raise tariffs, which in turn have limited ESCOM’s ability to borrow and invest, resulting in a vicious cycle of poor services and inability to increase tariffs. Given lessons from other countries such as South Africa,16 the GoM should pay attention to the sustainability of the electricity sector as a whole, starting with ESCOM as the offtaker.

15. Accessing private sector capital can bring with it a host of stringent but beneficial requirements, including much higher expectations of accuracy, timeliness, and transparency in financial operations, as well as proven technical/operational capacity of the SOEs. The right incentives (internal and external to SOEs) will need to be put in place to ensure that SOEs are motivated to make the desired changes. The study finds that, although cost-reflective tariffs17 and enabling environment reforms are important, SOEs can implement several internal reforms (within the control of their boards of directors and managements) to improve performance before resorting to external enabling environment/governance reforms. If SOEs can take actions such as increasing billing/collections (converting to prepaid meters) and thereby reducing outstanding receivables, reducing physical and commercial losses, reducing staff costs, and increasing last-mile connections, they could potentially save up to MWK 62 billion (~US$84 million) or 16 percent of total assets per year.18 EGENCO could save up to 8 percent of its total assets, while ESCOM, LWB, and BWB could save up to 4 percent each and NRWB up to 2 percent.

16. SOEs have limited independence and autonomy and hence are not insulated from political interference. This increases risks for potential lenders and potential liabilities to the GoM. These institutional approaches constrain Malawi’s development in three ways: (a) by imposing huge opportunity costs on the economy in terms of suboptimal and/or forgone infrastructure investments; (b) by precluding market discipline to enhance SOEs’ financial viability, governance, and accountability standards; and (c) by posing macro-fiscal risks and crowding out the fiscal space. As a result, they lack the capacity to engage the private sector.

17. Reforming the weak governance framework and organizational structures and arrangements that will guide the relationship between the GoM and SOEs is necessary. The current governance frameworks in Malawi do not enable SOEs to be efficient and accountable. There is no separation between the function of the state as the owner of SOEs and the responsibility of the board of directors as the highest decision-making bodies within SOEs. The state is involved in the day-to-day management of SOEs, and political interference in SOEs’ decision-making processes is a common practice, with most decisions that are supposed to be made by boards and managements subject to government approval. 19 This is partly

16 South Africa is currently experiencing its worst energy crisis, characterized by power cuts, which reached 6,000 MW in 2019 and with additional 2,000 MW announced in January 2020. This has been caused by years of mismanagement of Eskom (the state-owned utility that generates 95 percent of South Africa’s power), governance failure, escalating costs, and the accumulation of unmanageable debt. 17 One of the key recommendations is for the GoM to ensure that there are regular tariff adjustments, at least to match inflation. Lack of regularity or long delays in tariff increases can erode a utility’s financial health rapidly. However, tariff increases should be tied to clear performance improvement targets. 18 This analysis was only done for six out of seven SOEs, which have similar operating models: EGENCO, ESCOM, LWB, BWB, NRWB, and MHC. 19 The lack of independence, with boards and executive managements taking directions from the state on how to run their business, removes the incentive to improve performance, instead expecting bailouts. In discussions, it was revealed

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

8

because boards of directors and executive managements have underperformed in the past, in some cases leading to bailouts of SOEs. In addition, most boards are large and lack diversity of skills (especially private sector skills), with a composition that is excessively skewed toward public sector representation and includes farmers, village chiefs, and so on, lacking the necessary expertise to govern utilities.20 It is recommended that the GoM undertakes reforms to professionalize and empower the board of directors and ensure they are composed in a way that helps them exercise objective and independent judgment, hire qualified and commercial-minded managements, improve SOEs’ performance, and instill confidence in the market that SOEs could be credible borrowers.

18. It should be noted that these improvements alone will not be sufficient to enhance SOEs’ performance. Implementing a coordinated framework of incentives that integrates reform actions by the GoM and a policy direction that will allow market forces to incentivize reforms within SOEs will be imperative (Figure 2). For example, the GoM needs to enable SOEs to focus on their commercial mandates by committing not to interfere with the day-to-day management of SOEs’ operations and putting in place other arrangements that insulate SOEs from political interference. However, complementary actions to increasingly bring in private partners into the financing of SOEs, either in the form of debt or equity, can impose new and more stringent financial and operational discipline within SOEs and enable them to operate with a higher level of efficiency. Overall, utilities’ reform efforts should be closely coordinated with the trajectory of macro-fiscal adjustments and greater financial sector development.

that SOEs usually expect bailouts from the GoM when they fail to repay their debt, which also creates moral hazards on the part of the private sector. Expectations that SOEs will always be bailed out can encourage irresponsible/excessive lending practices. 20 When forming SOE boards, the current practice in Malawi is to have as wide a representation as possible as a way to ensure the interest of the general public is well represented, resulting in the current composition. While the spirit of this practice could be warranted, it does not have to be this way. The interests of the public can best be served by ensuring SOEs are efficient and financially sustainable, which at the basic level is a function of the quality of SOE boards and their executive managements and the quality of the governance framework that enables SOE boards to effectively perform their duties.

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

9

Figure 2: A coordinated framework of incentives for improved performance of SOEs

Source: World Bank staff.

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

10

PPPs in infrastructure are not new in Malawi but require acceleration, continued reforms, and a champion

19. Use of PPPs/project finance through special-purpose vehicles (SPVs) should be encouraged going forward given the limited borrowing capacity of SOEs. It is to be noted that Malawi has limited experience in PPPs since its infrastructure has largely been financed through public sources. In fact, until early 2019, none of the sectors reviewed in this report had received finance from commercial sources. However, PPPs are not completely new in Malawi. The country has successfully attracted approximately US$1.2 billion of investments through PPP arrangements in the past two decades, of which US$1.1 billion was invested in the railway subsector (that is, the Nacala Railway Corridor). Other sectors included information and communication technology (ICT), inland water transport, and tourism. It should be noted that this is a negligible amount relative to GDP. PPP investments in Malawi averaged 0.07 percent of GDP over a 20-year period (1998–2017) compared to 0.5 percent in Uganda, 0.82 percent in Mozambique, and 0.92 percent in Zambia.21 The PPP landscape in the energy sector is slowly changing, following a legal reform that opened up the generation market to the private sector. A new hydropower PPP project (US$600 million) is under development, and in 2019, a solar project by an IPP (US$67 million) reached financial close.

20. Despite commendable progress made in the past years, especially for a small and economically fragile country like Malawi, the private sector participation/PPP agenda lacks a champion in the government to advance it. In addition, the PPP program is not well integrated into the PIM process and appraisal of proposed investment projects to determine the potential for private sector financing is not a common practice. As highlighted earlier, the viability of projects for private sector financing is not considered or factored in the design/selection of the public investment program. This is partly attributable to the lack of financial and technical resources to undertake detailed appraisals (including the development of all technical studies), which disincentivize MDAs to consider PPPs. PPPs imply a more advanced and efficient form of procurement of infrastructure process and services, which requires specialized skills, causing MDAs to prefer more traditional procurement methods, including unsolicited proposals. The inability to adequately prepare projects puts MDAs at a disadvantage when negotiating with the private sector, elevating their mistrust of the private sector. Consequently, taking a more systematic approach toward developing bankable investment projects, including PPPs, will be crucial. The proposed PPF should provide financial and technical resources needed to move potential PPP projects to bankability, build capacity and understanding among implementing MDAs on the benefits of PPPs, and facilitate dialogue between investors/market participants (foreign and domestic) on one end and MDAs on the other.

21. Accelerating private investments and the PPP program in particular will also require the government’s commitment to continue business environment/cross-cutting and sectoral reforms. Like many African countries, to attract investments into public infrastructure, Malawi must overcome investors’ deep-rooted perception of high risks that the market is unable to mitigate. Even purely private infrastructure developers will face challenges given their exposure to government contracts. Malawi can shift the mindset of investors by undertaking reforms to demonstrate to both domestic and cross-border investors that Malawi as an asset class holds a promising future. The GoM should focus on addressing risks emanating from macroeconomic instability, lack of transparency and inefficiencies in procurement framework and practices, inefficiency in project implementation, and the overall business environment, which are among the top risks that investors

21 It should be noted that investments in Mozambique and Zambia also include large resource-based investments, which contribute to higher ratios than the average for LICs and LMICs respectively. These levels of investments are partly responsible for the high level of total public debt, which as of 2018 stood at 110 percent of GDP in Mozambique and 78 percent in Zambia.

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

11

are concerned about when making decisions to invest in the Sub-Saharan African region. Promoting dialogue and investor communication are critical the reform process. Strengthening institutional capacity should be a cross-cutting theme for the GoM. As seen earlier, the lack of incentives to pursue private financing options is partly attributable to the lack of capacity across MDAs and within the financial market. A political champion to ensure the legitimacy and appropriate coordination to decisively move the agenda forward will be needed.

The domestic long-term financial market is nonexistent; however, the foundation for further market development is in place

22. The domestic financial market has not played a prominent role in financing of infrastructure to date. Almost all private capital mobilized for Malawi’s infrastructure to date has come from foreign sources. Although foreign sources of finance will continue to play a major role going forward given the volume of finance required, the domestic financial market can play a complementary role where finance in local currency is required. Domestic investors could co-invest in large projects with foreign investors or invest directly in small projects that do not require large amounts of capital.

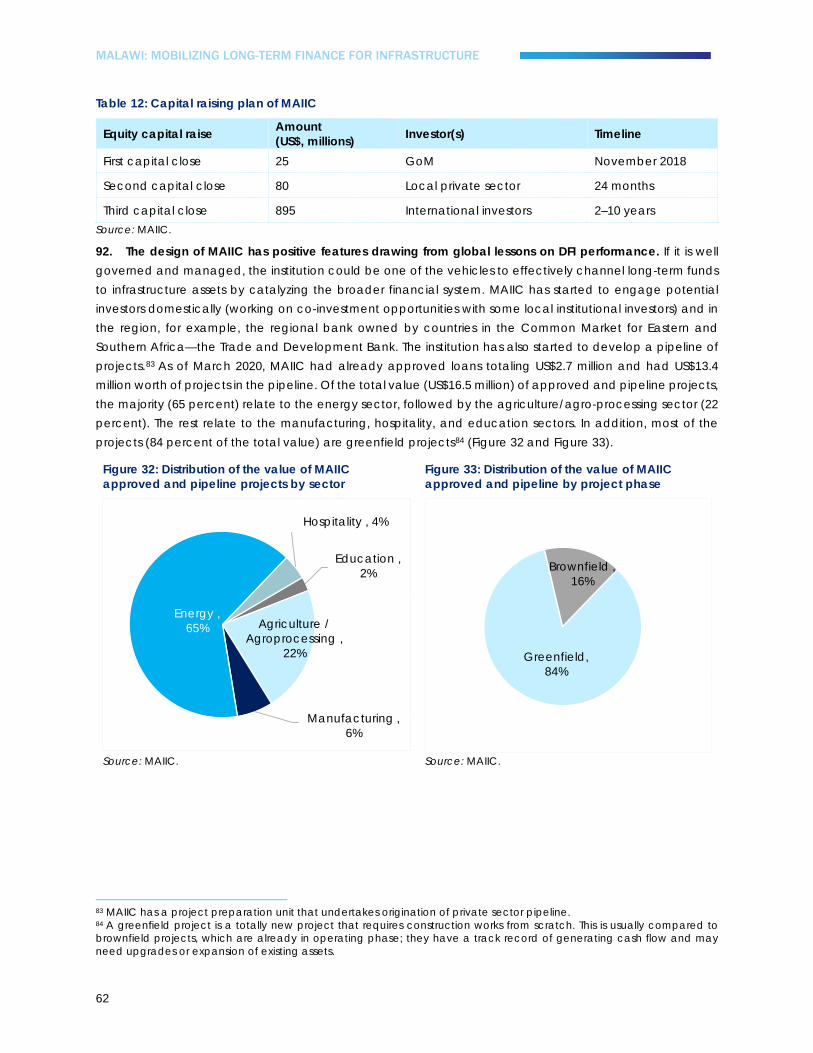

23. Commercial bank lending is important for infrastructure, especially during the construction phase and is a key source of financing infrastructure globally and in some emerging markets and developing economies (EMDEs).22 This is not the case in Malawi. There is no long-term lending at all, let alone lending for infrastructure. The funding structure of the banking system in Malawi does not match the long-term needs of infrastructure assets. In 2019, 100 percent of deposits (the main source of funding for banks) were maturing in less than one year. This is a significant mismatch in funding tenors versus the long-term nature of infrastructure financing. In the current state, banks will not be able to participate in the financing of infrastructure in a meaningful way. In the near to medium term, facilitating access to long-term lines of credit by banks, alongside measures to extend the maturity profile of liabilities, will therefore be key. Investing in building institutional capacity and channeling long-term funds through the recently established national development finance institution (DFI), that is, the Malawi Agriculture and Industrial Investment Corporation (MAIIC), to catalyze system-wide bank lending could also be considered. Banks could also leverage the capital market to raise long-term funds. In both cases, availability of a bankable pipeline of infrastructure projects and building the capacity of the banking system to undertake such intermediation would be critical.

24. Though the banking system lacks long-term funds, there is a growing corpus of long-term funds in the pension and life insurance systems that urgently require channeling to long-term assets. As of December 2019, total assets of institutional investors23 stood at MWK 1.9 trillion (US$2.5 billion), or 32 percent of GDP. These assets have been growing at a CAGR of 19 percent in the past six years. With very few investment options (mainly government bonds and listed equities—chasing only 15 listed stocks), these assets are suboptimally allocated, and the country faces the risk of an asset bubble in the stock market. If 10 percent of current institutional investors’ funds were to be allocated to infrastructure (the regulator is envisioning a maximum of 20 percent), it would make available about US$250 million to infrastructure provided a pipeline can absorb it. However, expectations within the government and the regulator regarding how much of institutional investors’ assets can be allocated to infrastructure in the medium term will need to be managed. A maximum

22 In 2019, total commercial debt of about US$15.6 billion was raised in EMDEs, of which 99 percent was from commercial banks. In addition, about 95 percent of all commercial debt was raised in the domestic markets, mainly in more advanced EMDEs in East Asia and Pacific, South Asia, Eastern and Central Europe, and Latin America and the Caribbean. In the Sub-Saharan Africa region, only South African banks are the most active. 23 Comprising pension funds and life insurance companies (which make up 85 percent of total assets in the industry), collective investment schemes, and other companies.

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

12

of 10 percent is what is being allocated by some of the pension funds in the most experienced economies in terms of infrastructure finance, such as Australia and Canada. Given the need to build capacity in Malawi, an allocation of 5 percent of institutional investors’ assets to infrastructure could be achieved in the medium to long term.

25. Encouraging prudent investing in infrastructure by pension funds is imperative and will require a robust regulatory framework. While the domestic pension funds have the potential to contribute to the country’s economic development through investments in infrastructure, their first responsibility is to protect their members’ assets and provide adequate retirement payment in the future. Therefore, they should not be coerced into investing in infrastructure projects that are not proven to be bankable; their investment decision must be made on a risk-return basis and be mindful of pensioners’ liquidity needs. The regulator should ensure a balance between encouraging pension funds to diversify their portfolio and contribute to infrastructure investments and ensuring they focus on their primary objective. As a matter of urgency, the draft regulation that has been prepared by the Reserve Bank of Malawi (RBM) to guide investments by pensions should be finalized soon.

26. Although Malawi is at a nascent stage of financial market development, several key foundational elements of a long-term finance market are in place. Progress toward developing capital market infrastructure 24 and the development of a yield curve (currently with bond durations of 10 years) are noteworthy features for Malawi’s long-term finance market development. Opportunities exist to build on the recent progress to nudge the market toward more long-term investments. Support for market creation can take several forms, including availing long-term liquidity in the banking system, increasing the supply of capital market debt issuances, developing enabling regulations, and building capacity of market participants. Given the limited capacity in the market currently, the government and the regulator should facilitate the expansion of the supply of traditional corporate/SOE bonds as a starting point/issuance of SOE bonds (at least two of the assessed SOEs have the capacity to access capital markets, and one of them has already privately placed two bonds with commercial banks). As the PPP program evolves over time and more bankable projects come onstream and become operational, opportunities for project bonds and for infrastructure SPVs to list their shares on the stock market will emerge. The study also proposes that in the medium term, the GoM should consider listing some of its shares in SOEs to mobilize long-term finance but more crucially to inject market discipline in SOEs through greater participation by institutional investors. The study recognizes the need for this to be done carefully considering the political economy in Malawi. This should be informed by adequate analysis, incorporated in an SOE ownership policy (which is recommended under this study) with clear sequenced milestones on how plans to divest shares in some SOEs will be implemented.

27. As a way to deepen the capital market in general, companies (as corporate bond issuers), including large corporations and commercial banks, could be encouraged to issue debt instruments. The current high ratio of loan concentration in the banking system is alarming and indicates the need for companies to move to the capital market, which should help further deepen the market. In December 2019, the largest single

24 In 2017, the Central Depository System (CDS), along with the Malawi National Switch and Automated Transfer System (which automated and simplified all settlement and clearing processes), were implemented. The CDS, which is the key element of the market infrastructure, facilitates trades on the treasury primary market and is capable of supporting registry, custody, settlement, and market data and information management in the primary and secondary markets for bonds and equities. The CDS is linked to the Automated Trading System of the Malawi Stock Exchange (MSE), which was launched in June 2018. All share certificates that were in physical form have been transformed into an electronic form to facilitate electronic transfers of shares. The trade settlement time has improved (less than three days).

MALAWI: MOBILIZING LONG-TERM FINANCE FOR INFRASTRUCTURE

13

borrower in the banking sector had an outstanding loan of 67 percent of core capital 25 of its lender (compared to the RBM’s limit of 25 percent26) and 21 percent of core capital of the entire system, which stood at MWK 215 billion (US$290 million). The largest outstanding loan of one of the smaller banks was 116 percent of core capital. It should be noted that banks are also exposed to the same borrowers. Large corporations also have direct loans from pension funds and life insurance companies, which has contributed to the growth of unlisted investments by institutional investors. Encouraging these corporations to either issue new bonds in the listed market or move their existing private debt with institutional investors to the listed market should be explored. This will benefit the market by (a) reducing concentration in the banking system and (b) increasing the supply of listed instruments (a more transparent market), which works well for institutional investors. In this regard, opportunities for demonstration transactions exist—through engagement with the regulator, investors, and potential issuers. The role of the MSE in promoting new listings and improving the listing regime will be critical.