MAKING THE LAST-MILE · PDF fileNEW AGE FOR AUSTRALIAN RETAIL Despite retail sales & the...

14

© GRA 2018 RETAIL WHITEPAPER Shanaka Jayasinghe, Senior Manager at GRA reviews last-mile fulfilment in Australia MAKING THE LAST-MILE PROFITABLE Shanaka Jayasinghe reviews last-mile fulfilment in Australia

Transcript of MAKING THE LAST-MILE · PDF fileNEW AGE FOR AUSTRALIAN RETAIL Despite retail sales & the...

© GRA 2018

RETAIL WHITEPAPER

Shanaka Jayasinghe, Senior Manager at GRA reviews

last-mile fulfilment in Australia

MAKING THE LAST-MILE PROFITABLE

Shanaka Jayasinghe reviews last-mile fulfilment in Australia

NEW AGE FOR AUSTRALIAN RETAIL

Despite retail sales & the online market-size increasing year after year, retailersremain challenged to turn a profit foronline channels.

Myer has taken the spotlight recently asit struggles to demonstrate progressagainst its turnaround strategy. Myer,however, isn’t the only retailer exposedby the new market conditions. FewAustralian retailers are ‘ready’ for online,particularly with Amazon’s entry.

We are currently experiencing one ofthe largest shifts in retail operatingmodels to date and supply chains areset to play a key role in this transition.Increasingly, executives are identifyingthe bounty of opportunity inautomation, predictive analytics andplugging into the sharing economy – allto delight the customer with speed,convenience, price and experience.

This paper explores the shortfalls oftraditional supply chain models inservicing online demand and whatcould be around the corner as creativesolution(s) to bridge the gap towardsprofitability in the future.

“1/3 Of All Purchases Will Be Online

By 2018”Research by Commonwealth Bank 2017

“Amazon has been dubbed the 'country killer' by analysts at

Morgan Stanley, yet Australian retailers remain optimistic in the face of the retail giant's arrival.”

© GRA 2018

ONLINE RETAIL FRAGMENTS VOLUME

Before we see what solutions might be in front of us, let’s first explore why is online fulfilment sochallenging?

The fragmentation of volume when servicing online demand goes against the inherent structure oftraditional retail supply chains. Traditional supply chain models are typically based on ‘aggregation ofvolumes’ and ‘asset utilisation’ to drive down unit costs for the storage and flow of inventory. Forinstance, retailers may consolidate freight movements or automate warehouse pick and packoperations to drive cost reductions.

Retailers have invested and designed the majority of their processes, warehouse systems and layoutsbased on cartonised and palletised store-fulfilment. Thus, many are slow to respond to the changingrequirements that arise with online orders – unit level operations.

In fact, historically, the emergence of 3PLs has arisen from ‘aggregation of volumes’ to justifyinvesting in processes, automation and technologies to drive greater efficiency. So we can start toappreciate the complexity and disruptive nature of fragmenting such volumes on a supply chainsoperations.

Process and technology investment which was based on largely cartonised fulfilment is now fragmented when we go online, to the ‘each’ level

© GRA 2018

© GRA 2017

FRAGMENTATION CREATES ADDITIONAL COMPLEXITY

So how does fragmenting volume add complexity for retail supply chains? Toillustrate this, in the context of the last-mile alone, we have summarised a simplifiedexample of just three (of many) reasons for the added complexity:

Distribution Centres (DCs) that were once geared for pallet or carton level movements

Now, must pick and despatch at an ‘each’ level – for online.

In financial terms, the labour costs ofpicking a carton of t-shirts (containing20) for a Bondi Junction store has nowgone up by at a multiple of 20 at the DCalone if we are relying on the sameprocesses to now pick one specific t-shirtfor Sam Smith in Balmain, NSW.

Amazon may have found a creative automated solution for this – utilising Kiva Robots, although, this too has its challenges. The key point however, is the majority of Australian retailers are lagging behind - relying on historical processes & technology geared for store fulfilment.

‘Acceptance of delivery’ is often a fail.It is estimated that ~23-35% of all online deliveriesfail on the first attempt due to the consumer notbeing available. Such deliveries are re-routed tolocal post offices or alternate pick-up locations.Guess who foots the bill? The retailer of course andthe consumer has the inconvenience of having topick-up their missed delivery.

Shipping direct to homes. Freight movements, which once were consolidated and shipped to10 - 100+ store locations are now fragmented and being shipped to potentially one of 9 millionhouseholds across Australia’s metro, regional, rural and remote areas.

1

2

3

© GRA 2018

We live in a big country. Our freight challenges are obvious. What is less obvious is theimpact of our market size. Low population density means we are often short on capital to fundsupply chain investments to make last-mile fulfilment profitable - compared to our globalpeers. This has meant that retailers investing in automation technologies have to date been toofew and far between due to the volumes being insufficient.

Despite being a similar size to Europe, Australia has about 3.2% of its population.

In considering automation investments, it is volume by product profile, not just volume alone,that is important. For example, it is extremely challenging (and expensive) to automate for aproduct profile that ranges from (1) pencils & pens to (2) desks and furniture. In order to justifycapital spend, critical mass in volume needs to exist per product profile. That is, we should lookto automate the pencils & pens distinct to the desks & furniture supply chains.

Amazon has identified a unique automation technology in its Kiva systems which provide anagile solution to automation for specific product profiles. www.amazonrobotics.com

98% of the population live in the areas painted light blue on the map

AUSTRALIA HAS A UNIQUE SET OF CHALLENGES

Area Population Population density

Australia 7.7M km2 24M 3.1 per km2

Europe 10.2M km2 743M 72.8 per km2

© GRA 2018

BARGAIN HUNTERS• Value-driven• Cost-conscious• Value seekers• Opportunists

FAST MOVERS• Utility-driven• Time poor• High-value items• Immediate need

COST SAVERS• Cost-driven• Time rich

THRILL SEEKERS• Experience-driven• Personal interest• Need for support

LAST-MILE FULFILMENT OPTIONS MUST ALIGN TO DIFFERENT TYPES OF CUSTOMERS

Although profits are of course the focus for business, last-mile is not just about cost efficiency, ithas evolved to be about a multitude of factors including responsiveness, customer experience andconvenience. To make things more complicated, what is important to one customer in last-miledelivery may not necessarily be important to another.

This is why we are seeing the emergence of the ‘personal supply chain’ where supply chain modelsare moving away from asking questions such as “How can my customer’s day fit into my supplychain?” to now asking “How can my supply chain fit in with my customer’s day?”

Check out these creative companies last-mile solutions that go beyond cost efficiency:• Enjoy (US-based company prioritising experience in LMF): https://www.enjoy.com• Volvo, In-Car Delivery (…just wow): https://youtu.be/WZUDHytwt3s• Pargo (since 2012, similar to Shipster by Australia Post) https://youtu.be/isrTTUVCMtI• Amazon Key (great innovation from Amazon): https://youtu.be/wn7DBdaUNLA

© GRA 2018

Technological innovations have driven profitability in the past, allowing supply chains to evolve froma back office type function, or cost centre, to now be a source of competitive advantage.

Can technology solve our last-mile challenge?

Historically, supply chain executives had influence over customer value by finding ways to drive downcost. We did this through process redesign, focussing on internal operations, leveraging volumes andreducing non-value processes. Examples of this include; the Ford assembly line, Taylorism andMcDonald’s restaurant operations. Over time, we got better at driving efficiencies and as processesevolved, we introduced technologies and systems to help us automate processes further and improvethe accuracy and effectiveness of operations. This era brought on the emergence of AdvancedPlanning Systems, MRP & DRP as well as WMS and RFID technologies to improve visibility andaccuracy of information flows for inventory management.

Fast-forward to today and as we know supply chain executives’ influence has expanded beyond justcost. Technology has proven effective in the past, although, technology alone going forward maynot be enough given (1) complexity of last-mile, (2) increasing nature of customer demands and (3)Australia’s unique set of challenges. We must be more creative than ever and than that of our globalpeers in identifying and executing effective last-mile solutions.

TECHNOLOGY HAS DRIVEN PROFITABILITY IN THE PAST

© GRA 2018

Cost centre Competitive AdvantageFrom… To…

STRATEGIC PARTNERSHIPS ARE THE WAY FORWARD

HOW WILL THESE CONVERGE?WHAT WILL THEY CREATE?

Big Data

Personal Computers

DemandSensing

3D Printing

Predictive Analytics

Smartphones

P2P Couriers

The Internet

Online Retail

Car drops

Physical Stores

Click & Collect

Drone Delivery

Strategic partnerships betweenorganisations will providegreater accessibility to storagelocations, delivery providers,delivery types and consumerinteraction points.

Strategic partnerships in conjunction with converging technologies will be the way forward to making the last-mile profitable.

As retailers increasingly ask themselves‘how does our supply chain fit intoour customer’s day?’ partnerships willemerge to bridge last-mile gaps.Retailers, through partnering, willshorten the last-mile for Australia andthis will make Australia a smaller andmore convenient place to shop online.

At GRA, we have already noticed anincreased appetite for retailers to (1)better understand cost-to-serve acrosschannels and (2) perform consumermapping exercises to better alignsupply chains to customer needs.

Partnerships today remain in theirinfancy as we are only starting to seesharing of infrastructure andsubscription style services. Examples ofthese include: “Simply Collect” byWoolworths, “Shipster” by AustraliaPost as well as Amazon Prime whichwill be here very, very soon.

Emerging subscription based and partnership models

© GRA 2018

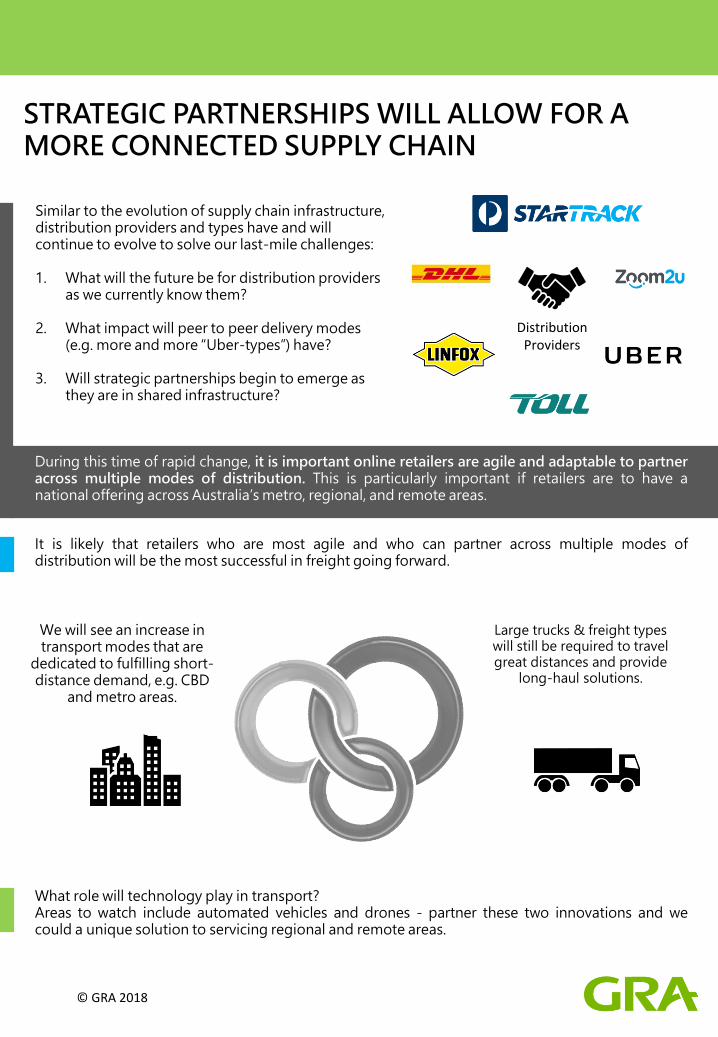

STRATEGIC PARTNERSHIPS WILL ALLOW FOR A MORE CONNECTED SUPPLY CHAIN

Distribution Providers

Similar to the evolution of supply chain infrastructure, distribution providers and types have and will continue to evolve to solve our last-mile challenges:

1. What will the future be for distribution providers as we currently know them?

2. What impact will peer to peer delivery modes (e.g. more and more “Uber-types”) have?

3. Will strategic partnerships begin to emerge as they are in shared infrastructure?

During this time of rapid change, it is important online retailers are agile and adaptable to partneracross multiple modes of distribution. This is particularly important if retailers are to have anational offering across Australia’s metro, regional, and remote areas.

It is likely that retailers who are most agile and who can partner across multiple modes ofdistribution will be the most successful in freight going forward.

What role will technology play in transport?Areas to watch include automated vehicles and drones - partner these two innovations and wecould a unique solution to servicing regional and remote areas.

Large trucks & freight types will still be required to travel great distances and provide

long-haul solutions.

We will see an increase in transport modes that are

dedicated to fulfilling short-distance demand, e.g. CBD

and metro areas.

© GRA 2018

The recent partnership established by Coles and Airtasker is a fantastic example of how retailers are

looking beyond their own walls to solve some of the last-mile challenges.

Coles, we all know, is a major player in food & grocery and Airtasker is a peer to peer jobs platform

which is now generating $100 million for Australian gig economy workers each year. It is an

interesting partnership, one that would have been unheard of five years ago, however, today we can

clearly see its relevance and application. It certainly strengthens Coles’ defences against Amazon

Fresh’s model.

The partnership will initially see customers of 64 Coles stores having access to the peer-to-peer

economy to service their online demand. Coles will manage quality on the peer-to-peer platform by

accrediting “Coles Badges” to qualified Airtaskers.

It will open the door to further proliferation of delivery options as consumers can direct Airtaskers to

their own specific demands - whether that be late night deliveries, weekend deliveries, public

holiday deliveries, etc.

It is worth noting that Airtasker already has similar partnerships with IKEA, The Good Guys & Ebay

and in 2018, we will likely see a further increase in the number of partnerships in this space.

STRATEGIC PARTNERSHIPS – TAPPING INTO THE SHARING ECONOMY TO SOLVE LAST-MILE PROFITABILITY

© GRA 2018

THE POTENTIAL OF CLICK & COLLECT IS CURRENTLY UNTAPPED IN AUSTRALIAN RETAIL

Click & Collect provides customers with the option to order items online and pick them up in-store.

It reduces the burden of delivery for retailers and offers customers a way to avoid delivery charges,

or potentially obtain purchased items sooner.

Woolworths has invested heavily in Click & Collect

Dis-Chem South Africa 2017

The highly competitive food and grocery retailers of Australia have recently

followed the UK food and grocery markets and invested heavily in Click & Collect.

Woolworths in particular is looking at leveraging shared infrastructure in its roll-out

of ‘Simply Collect’, potentially playing a significant role in collect infrastructure —

having already partnering with external parties such as eBay and Sydney Trains.

© GRA 2018

CLICK & COLLECT MODES AND IMPLEMENTATION

• In-store pick-up

• Partner store pick-up (e.g. retail group)

• External Partner (e.g. train station, post-office, fuel station, café etc.)

• Car Boot Drop-offs

• Parcel Lockers

• Smart Home (e.g. Amazon Key)

Modes of Click & Collect

Closeness to store

Closeness to home

Implementing Click & Collect

Internal Alignment:

Particularly between the

store and online channel.

“Who gets the sale” is

often contentious.

Critical Mass in

Infrastructure: We need

enough ‘pick-up’

locations to make

collection more

convenient than the next

best alternative.

Consumer Adoption:

Customers must be

convinced of the value in

collection, typically this is

through convenience.

Requires investment

Requires interest to invest

© GRA 2018

CLICK & COLLECT ADOPTION – GLOBAL ANALYSIS

Click & Collect was born in France and is now a mainstream customer option across Europe. The

first Click & Collect offer appeared in 2000, followed by a second in 2008, although it was not until

2011 when rapid growth accelerated the concept to maturity. With over 3,000 pick-up locations in

2014. This trend has continued since!

The growth of Click & Collect uptake across the UK has followed a similar trend. Argos first

introduced Click & Collect in 2001, but it took 10 years to begin rapid uptake in 2011, as in France.

Today, retailers identify click &

collect as a competitive

advantage, so much so they are

even making acquisitions based

on trying to rapidly increase the

number of store locations to

provide distribution coverage.

In the last two years alone we

have seen both Amazon acquire

Wholefoods as well as

Sainsbury’s acquire Home Retail

Group.

750

1890

2721

3000

Second

entrantFirst

entrant

2000 2008 2011 2014

Source: GMA & BCG 2015, The Winner-Take-All Digital World for CPG

NUMBER OF CLICK & COLLECT LOCATIONS IN FRANCE

“Leveraging its acquisition of the Home Retail Group, Sainsbury will begin adding Argos branches or click-and-

collect distribution points inside almost all of its stores. The acquisition added 739 Argos outlets and three Habitat home-

furnishing stores to Sainsbury’s portfolio, which already consists of 601 supermarkets and 782 convenience stores

around the U.K.”Bloomberg 2016

© GRA 2018

At GRA, we are passionate about supply chains, excited to be a part of what's to come and feeling

encouraged by the increased appetite for supply chain innovation in Australian retail.

GRA’s Online Retail Offering:

• Online, end-to-end Supply Chain Diagnostic

• Online Network Optimisation

• Online Channel Cost To Serve Analysis

• Consumer Journey Mapping

• Online Supply Chain Strategy Development

• Click & Collect Strategy Design

• Delivery Pricing Strategy

• Warehouse Process, Layout & Technology Assessment

• Independent Fulfilment Centre Automation Assessment

• Delivery Provider Contract Negotiation

Contact us

Sydney (02) 9810 0229

Melbourne (03) 9421 4611

www.gra.net.au

Author: Shanaka JayasingheSenior Manager

GRA Sydney

Subscribe to GRA news: www.gra.net.au/subscribe

© GRA 2018

GRA – RETAIL SUPPLY CHAIN SERVICES