Making Sense of Home Loans - MoneySENSE/media/Moneysense/Videos... · Making Sense of Home Loans By...

21

1 Making Sense of Home Loans By Dennis Ng, CFP CM Financial Planning Association of Singapore Outline • How to set your budget for buying a home • Financing home purchases through CPF funds • Taking up a home loan • Is refinancing your home loan a good idea • Selecting a suitable home loan package

Transcript of Making Sense of Home Loans - MoneySENSE/media/Moneysense/Videos... · Making Sense of Home Loans By...

1

Making Sense of

Home Loans

By Dennis Ng, CFPCM

Financial Planning Association of Singapore

Outline• How to set your budget for buying a home

• Financing home purchases through CPF funds

• Taking up a home loan

• Is refinancing your home loan a good idea

• Selecting a suitable home loan package

2

How Big a Home to buy?• Don’t follow the “crowd”

• Don’t over-commit in buying a home

• Consider the remaining lease period and any implications on home loans

• Beware risk of retiring asset rich, but cash poor

How to Set Your Budget

for Buying a Home?

3

How Much to Borrow?• Rule of thumb: Debt-service ratio should be 35% or

lower

How to calculate?Step 1: total up your total monthly debt

repayment obligations

Step 2: estimate your gross monthly income

Step 3: Divide 1 by 2, ratio should be 35% or lower.

Example

Assumptions:Loan period 25 years, average interest rate 4%Borrower does not have other monthly debt obligations

$4,200$3,150$2,100$1,050Max Loan Instalment(35% debt service ratio)

$12,000$9,000$6,000$3,000Household income

4

Other Costs To Consider Besides Loan Instalment

• Downpayment (typically 10% to 20% of property value)

• Stamp duty, legal fees, transfer fees and other related costs in connection with the purchase

• Housing agent commission and fees (if you use their services)

• Renovation and furnishing costs

Financing Home Purchases Through

CPF Funds

5

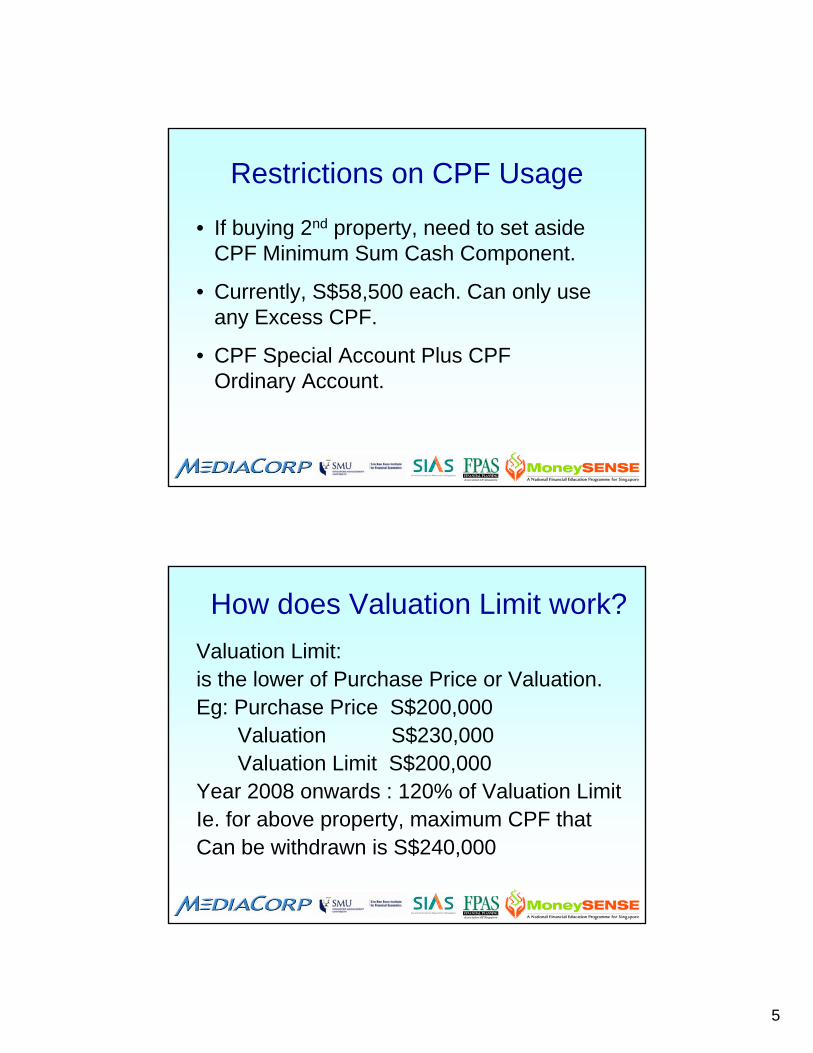

Restrictions on CPF Usage

• If buying 2nd property, need to set aside CPF Minimum Sum Cash Component.

• Currently, S$58,500 each. Can only use any Excess CPF.

• CPF Special Account Plus CPF Ordinary Account.

How does Valuation Limit work?Valuation Limit:is the lower of Purchase Price or Valuation. Eg: Purchase Price S$200,000

Valuation S$230,000Valuation Limit S$200,000

Year 2008 onwards : 120% of Valuation LimitIe. for above property, maximum CPF that Can be withdrawn is S$240,000

6

Beware: You might need to pay CASH for Loan Instalments !

• Downpayment 5% Cash S$10k, 15% CPF = S$30,000.

• Loan: 80% = S$160,000. Monthly instalment paid using CPF only. Total instalments payable over 30 years’loan period = S$242,843.92.

• CPF Cap of S$240,000 – last 49 months (4 years) Loan instalment fully payable using CASH only!

• 90% Loan, upfront 5% Cash, 5% CPF.• Last 61 months (5 years) of loan fully repayable using

Cash!

Reduced Contribution (%) to CPF Ordinary A/c as you age…Beware

12.58.503.561 to 65

208.5011.556 to 60

28.58.571351 to 55

34.58.571946 to 50

34.57.562136 to 45

34.56.552335 & below

TotalMedisaveSpecial OrdinaryAge

7

When using CPF for housing

• Buy a house that you can afford

• Don’t use all your CPF savings for housing

• Ensure that you finish paying your housing loan before your retirement age

Visit www.cpf.gov.sg for details and calculators on the use of CPF funds for home purchases

Taking Up a Home Loan

8

Taking up a Home LoanThings to note:• Make sure your debt-servicing ratio

below 35%• Make sure you have funds to cover

loan payment if property not rented out for 6 months

• Take note of the remaining lease period for lease properties

Taking up a Home LoanThings to note:

• Maximum tenor: match with your intended retirement age, or preferably 25 years.

• Maximum financing: 90%

• Loan instalment: check affordability

9

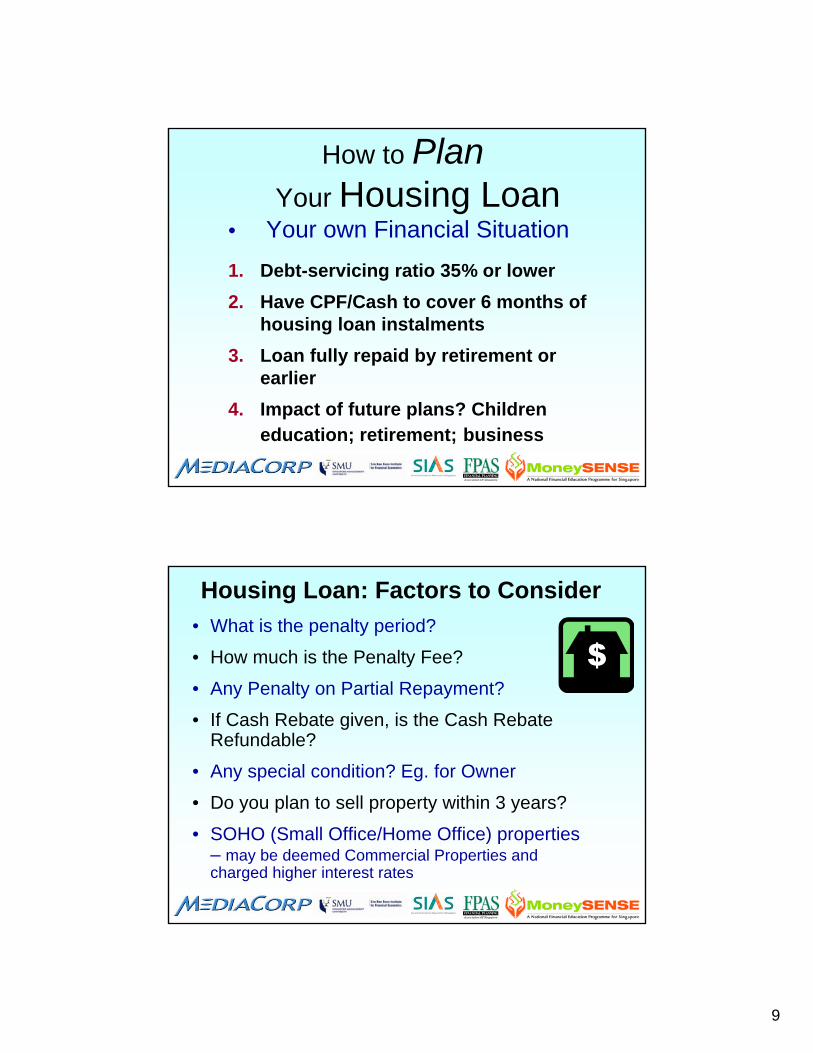

How to Plan Your Housing Loan

• Your own Financial Situation1. Debt-servicing ratio 35% or lower2. Have CPF/Cash to cover 6 months of

housing loan instalments3. Loan fully repaid by retirement or

earlier4. Impact of future plans? Children

education; retirement; business

Housing Loan: Factors to Consider• What is the penalty period?

• How much is the Penalty Fee?

• Any Penalty on Partial Repayment?

• If Cash Rebate given, is the Cash Rebate Refundable?

• Any special condition? Eg. for Owner

• Do you plan to sell property within 3 years?

• SOHO (Small Office/Home Office) properties – may be deemed Commercial Properties and charged higher interest rates

10

Fixed vs Floating Rate1. Fixed Rate packagesInterest rates fixed for 1 year to 5 years.Advantage: certainty of interest rates.Disadvantage: penalty if refinance/sell.

2. Floating Rate PackagesTraditionally, pegged to Bank’s Board Rates.Board Rates can change anytime.When interest rates fall, banks may not lower Board Rates.

Factors to Consider:• Fixed Rate vs Floating Rate?

Fixed Rate Packages are Typically Higher than Floating Rate Packages

Example:

1.60% 1.99%Private Property

1.60% 1.99%HDB Flat

Floating RateFixed Rate

11

SIBOR vs SOR3. SIBOR – Singapore Inter-bank Offered Rates

Average Market Interest rates banks charge to one another when lend/borrow from one another.

Advantage: Transparent, can check from Business Times. Banks cannot hold rates unchanged if market interest rates falls.

What Affects SIBOR?

• The 2 main factors that affect SIBOR are:

1. US Fed Rate and

2. liquidity (availability of funds) in Singapore banking sector.

12

Swap Offer Rate• SWAP Offer Rate (SOR) is the Singapore

Interbank Offer Rate + market reserve costs.

• It represents the average cost of funds used by banks in Singapore for commercial lending.

• Swap also account for the exchange rate of US$ vs S$. Thus, SOR tends to be more volatile than SIBOR. Sometimes, SOR is higher, sometimes SOR is lower than SIBOR.

2O Year Chart of 3 month SIBOR

13

Debt is a Double-Edged Sword

Similar to a Boomerang

Debt can work for you or against you.

Debt is a Double-Edged Sword

Unable to recoup interest

Returns > Interest paid

No indication when you can clear the loan

Know when you can clear the loan

Find it difficult to pay the monthly loan instalments

Monthly loan instalments are affordable

When Debt is Works AGAINST You

When Debt Works FOR You

14

E.g. If you can sell your home at a higher price …

$1,200k$1,200kSelling price

$200k$1,000kCash/CPF

$800k$0Loan

$50k$0Loan interest

$150k [75%]$200k [20%]Profit[% of Cash/CPF]

80% DebtWithout Debt

E.g. If you have to sell your home at a lower price …

$200k$1,000kCash/CPF

$800k$0Loan

$50k$0Loan interest

- $250k [-125%]

-$200k [-20%]

Profit / Loss[% of Cash/CPF]

$800k$800kSelling Price

80% DebtWithout Debt

15

Should you always pay off your Home Loan first?

Evaluate the cost of borrowing • Interest rates for housing loans are generally

lower than interest rates charged on other loans. E.g:- Car loan: about 5%- Renovation loan: about 7%- Personal Credit: about 16%- Credit Card: about 24%

• Pay off loans with higher interest charges first

Is Refinancing Your Housing Loan a Good

Idea?

16

About Refinancing

What’s Refinancing?• When you switch to a new home

loan with your existing bank or another lender

Potential Benefit• Save $$$ as the interest rates could be

lower than your present home loan

Refinancing - Key Points to Consider

Are you better off:• Sticking to your current loan package;• Converting to different loan package with

your existing bank; or• Taking up a refinanced loan package with

a different bank?

17

Refinancing - Key Points to Consider

Compare following components in your current home loan package and in the refinancing packages you are considering:• Fees• Lock-in period• Repayment schedules • Advertised interest rates • Effective Interest Rates

Refinancing – Strategies to Consider

• Lock-in periodTypically Fixed Rate package come with 2 – 3 years Lock-in periodSIBOR/SOR package lock-in period: 0 to 3years

Shorter lock-in period gives you flexibilityto refinance or sell house in future

18

Example: Savings by Refinancing

Loan Amount: $300,000 Loan Period: 20 yearsSavings in first 3 years total $14,379.02

32,085.37($1,604.36)($1,817.94)2.60%4.00%Thereafter

3,718.10($1,604.36)($1,817.94)2.60%4.00%5

3,846.76($1,604.36)($1,817.94)2.60%4.00%4

3,965.92($1,604.36)($1,817.94)2.60%4.00%3

4,778.08($1,567.88)($1,817.94)2.35%2

5,635.02($1,531.90)($1,817.94)2.10%1

SavingsInstalmentsInstalmentsRatesRatesYear

Interest New Current NEWCurrent

4.00%

4.00%

Example: Savings by Refinancing

• Legal Fees: S$2,500 • less Subsidy provided by Bank S$1,200Nett Cost of Refinancing S$1,300• Less Interest Savings of S$ 17,614.78

Nett Gain =S$16,314.78

19

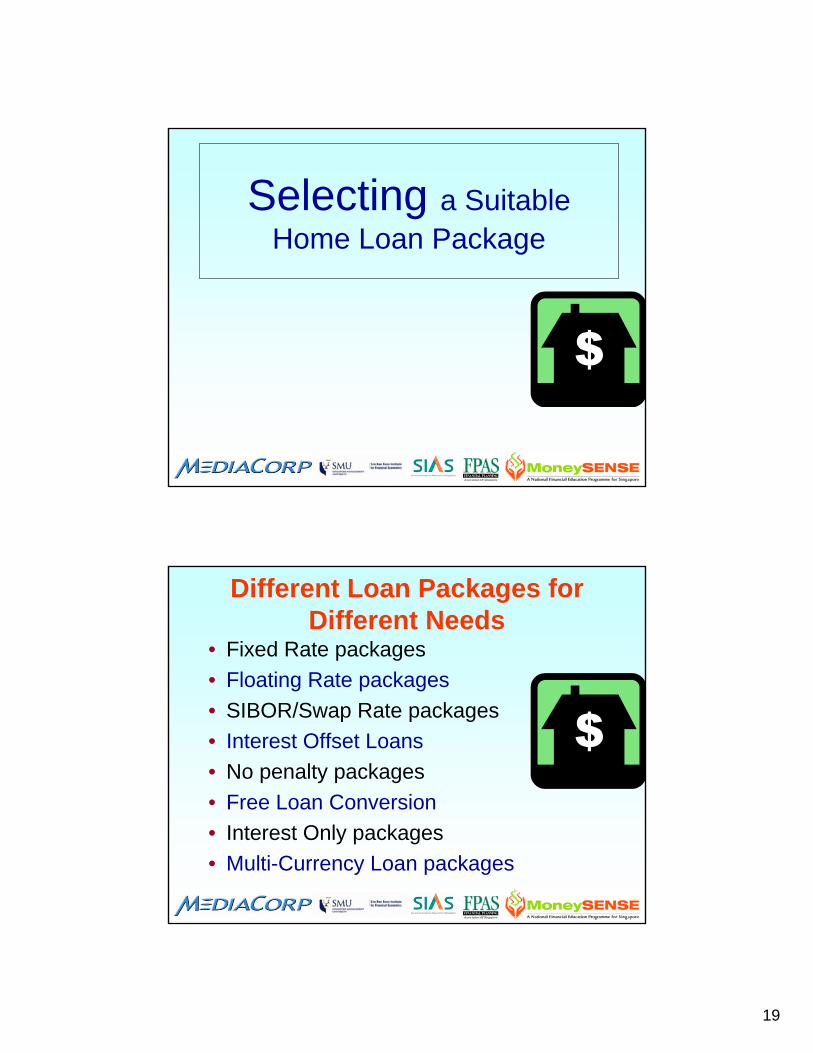

Selecting a Suitable Home Loan Package

Different Loan Packages for Different Needs

• Fixed Rate packages• Floating Rate packages• SIBOR/Swap Rate packages• Interest Offset Loans• No penalty packages• Free Loan Conversion• Interest Only packages• Multi-Currency Loan packages

20

Shop Around for a Loan Package that Best Fits Your Financial

CircumstancesCompare features such as:• Interest rates

– advertised rates - Effective Interest Rates

• Lock-in period and Fees• Cancellation Fees• Bank Subsidies for fees for valuation, legal

and conveyancing services and fire insurance

Shop Around for a Loan Package that Best Fits Your Financial

Circumstances• Ask questions.

- Refer to the MoneySENSE-ABS consumer guide at www.moneysense.gov.sg“Key Questions to Ask the Bank Before Taking a Home Loan”

• Don’t make a hasty decision based on advertisements, headline rates or gifts

21

Thank You…

Important Information• All expressions of opinion are subject to change without notice. Although information in this document has been obtained from sources believed to be reliable, MoneySENSE and its partners do not warrant the accuracy or completeness and accept no liability for any direct or consequential losses arising from its use.• This document is for informational purposes only and does not constitute a solicitation to buy or sell securities. • Past performance is no guarantee of future returns.• Forecasts may not be attained. • The value of investments and the income from them may go down as well as up and you may not get back the amount invested. • The value of investments may rise or fall due to changes in the rate of exchange in the currency in which the investments are denominated if it is different from the investor's own currency. • There are additional risks associated with international investments, including foreign, political, currency and economic factors to consider.• Information for this publication is provided by FPAS.• Throughout this document where charts indicate that a third party (parties) is the source, please note that the source references the raw data received from such parties.• Investment products are not bank deposits and are not subject to the provision of the "Deposit Insurance Act 2005 (Cap 77A)" of the republic of Singapore nor eligible for deposit insurance coverage under the deposit insurance scheme.and are subject to investment risks, including the possible loss of the principal amount invested. Past performance is not indicative of future results, prices can go up or down. Investors investing in funds denominated in non-local currency should be aware of the risk of exchange rate fluctuations that may cause a loss of principal.All applications for units in the unit trusts must be made on the application forms accompanying the prospectus, which are available from branches/offices of the distributors. Investors should read the prospectus before deciding whether to invest in units in the unit trusts.There can be no assurance that these market conditions will remain in the future. Past performance does not guarantee future results. Actual results may differ materially from the forecasts/estimates. Views, opinions, trends and prices expressed are subject to change without prior notice and are expressed solely as a general market commentary and do not constitute investment advice or a guarantee of returns as individual situations may vary.