Major Project (Ramit)

62

Investment Opportunities in Indian Telecom Infrastructure Sector Major Project report Submitted by: Ramit Malhotra In partial fulfillment for the Degree of MBA (Infrastructure) Submitted to: Department o f Po licy Studies TERI University Pl o t No. 10 Instituti onal A rea Vasant Kunj, New Delhi-70 INDIA 25 th , May 2009

Transcript of Major Project (Ramit)

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 162

Investment Opportunities in IndianTelecom Infrastructure Sector

Major Project report

Submitted byRamit Malhotra

In partial fulfillment for the Degree of MBA (Infrastructure)

Submitted toDepartment o f Policy Studies

TERI UniversityPlot No 10 Institutional AreaVasant Kunj New Delhi-70

INDIA

25 th May 2009

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 262

Declaration

This report has been prepared by Ramit Malhotra student of MBA (Infrastructure

program at TERI University

The Report has been prepared based on the information and documents made available

by ABC Limited It includes certain statements estimates and projections made by

promoters of the company Actual results may vary from the projected results contained

herein It should be recognized that projections of future events are inherently subject to

significant economic regulatory policy and competitive uncertainties or other force

majeure circumstances and that actual results for the periods covered thereby may vary

materially from the projected results There cannot be any assurance that the

assumptions or data upon which these projections have been based are accurate or that

the results contained in the projections will be realized

No representation warranty or undertaking (expressed or implied) is made and noresponsibility is accepted by me or PricewaterhouseCoopers or TERI University as to

the accuracy adequacy completeness or reasonableness of the facts opinions

estimates forecasts projections or other information set forth in this report or the

underlying assumptions on which they are based or the accurac y of any computer model

used and nothing contained herein is or shall be relied upon as a promise or

representation regarding the future events or performance of the project

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 362

TERI UniversityFINAL REPORT SUBMISSION FORM

1 Name of the student Ramit Malhotra

2 Program MBA (Infrastructure)

3 Name of the Internal Supervisor from TERI University Dr Saon Ray

4 Name of the external supervisor from Mrs Sakshi Marwah

5 Title of the research project Inves tment Opportunitiesin Indian TelecomInfrastructure Sector

6 Date of completion of project

Signature of the student

Signature of external guide Signature of internal guide

Name and des ignation Name and des ignation

Date Date

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 462

Acknowledgement

I offer my reverences to TERI University by whose efforts I have been able to complete

my major project at PricewaterhouseCoopers

The persons who shaped my efforts and provided the guidance to me are none other than

my renowned faculty members Dr Saon Ray Dr Kaushik Deb and Dr Neeraj Khera I

feel highly privileged to express my sincere regards and gratitude to them for their

dynamic leadership guidance careful supervision invaluable suggestions and liberal

attitude during the course of my dissertation

Also my endeavors at this project could not have been satisfactorily completed without

the active participation and co-operation of Mr Deepak Mahurkar Mr Manish Bhagla

Mr K Ramachanran and Mrs Sakshi Marwah I am really thankful to them for their

guidance and co-operation

I also acknowledge and express my deepest gratitude to all the team members of PwC

GRID for guiding me throughout the project I am indebted to them for extending their

valuable guidance comments suggestions and inspiration for this project

(RAMIT MALHOTRA)

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 562

Table of Contents

ABBREVIATIONS I

ABSTRACT II

LIST OF TABLES IV

LIST OF FIGURES IV

1 INTRODUCTION 1

2 OBJECTIVES 5

3 LITERATURE REVIEW 6

31 INTERNATIONAL EXPERIENCE IN INFRASTRUCTURE SHARING 6

32 DOMESTIC TELECOM MARKET ASSESSMENT 9 33 TELECOM MARKET - COMPETITIVE LANDSCAPE 11 34 TELECOM INFRASTRUCTURE OVERVIEW 13 35 TELECOM INFRASTRUCTURE - DOMESTIC MARKET 15 36 TELECOM INFRASTRUCTURE MARKET - COMPETITIVE LANDSCAPE 16

4 BUSINESS PLAN 19

41 PASSIVE INFRASTRUCTURE 19 42 INFRASTRUCTURE SHARING 19 43 INT RODUCTION TO THE BUSINESS 20 44 BUSINESS PROPOSAL 21 47 EXPANSION SCHEDULE 24 48 PROPOSED SERVICES 24 49 PROPOSED ORGANIZATIONAL STRUCTURE 25

5 METHODOLOGY 27

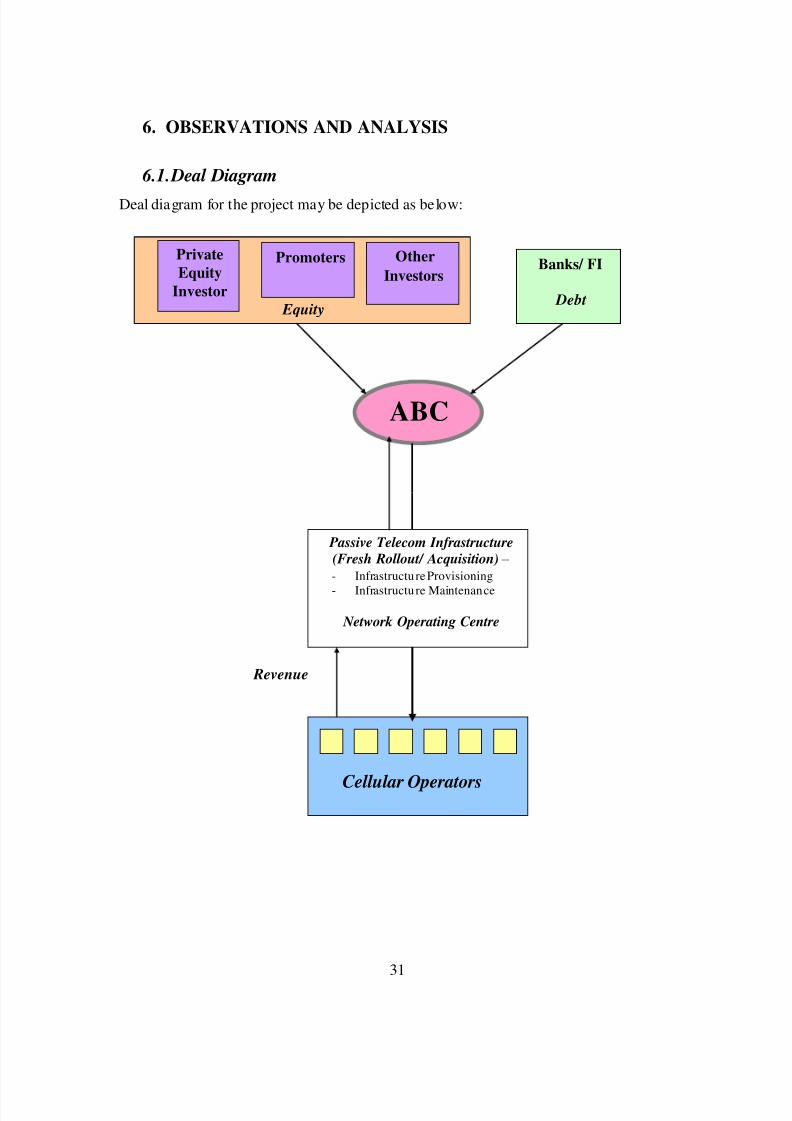

6 OBSERVATIONS AND ANALYSIS 31

61 DEAL DIAGRAM 31 62 FUNDING PLAN 32 63 RESULTS 32 64 SENSITIVITY ANALYSIS 34

7 RISK ASSESSMENT 39

8 CONCLUSION 41

REFERENCES 46

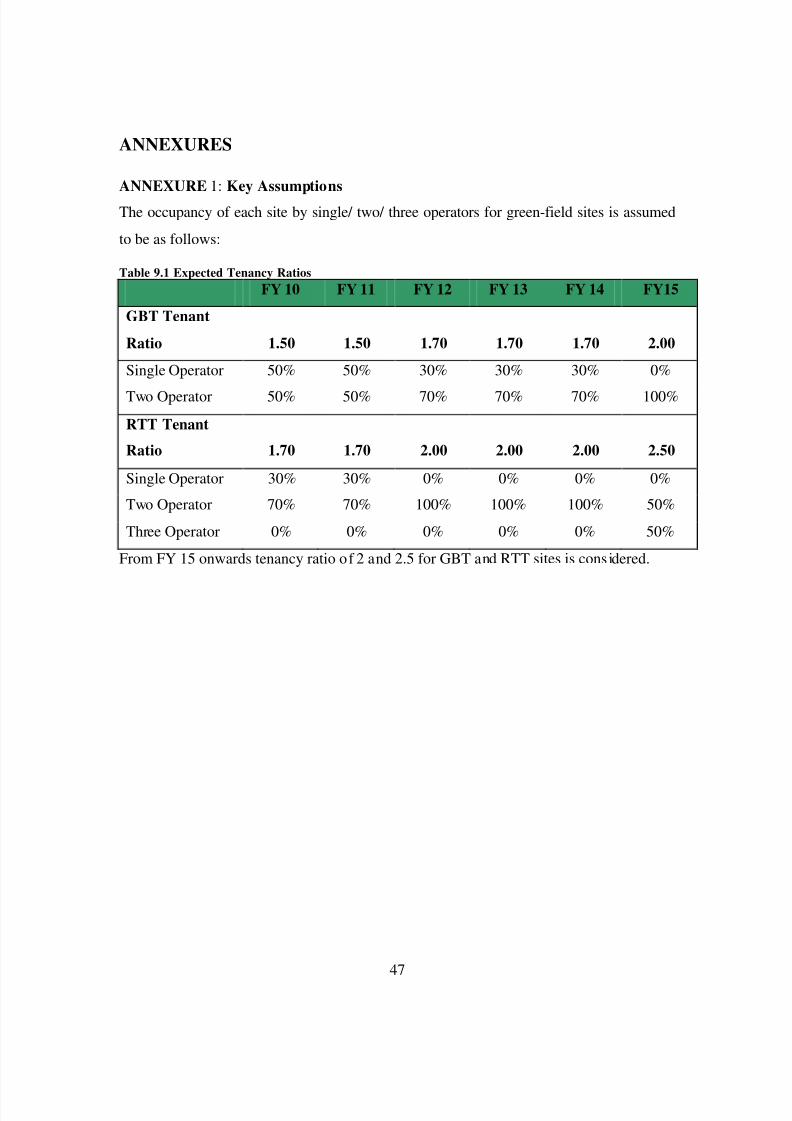

ANNEXURES 47

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 662

i

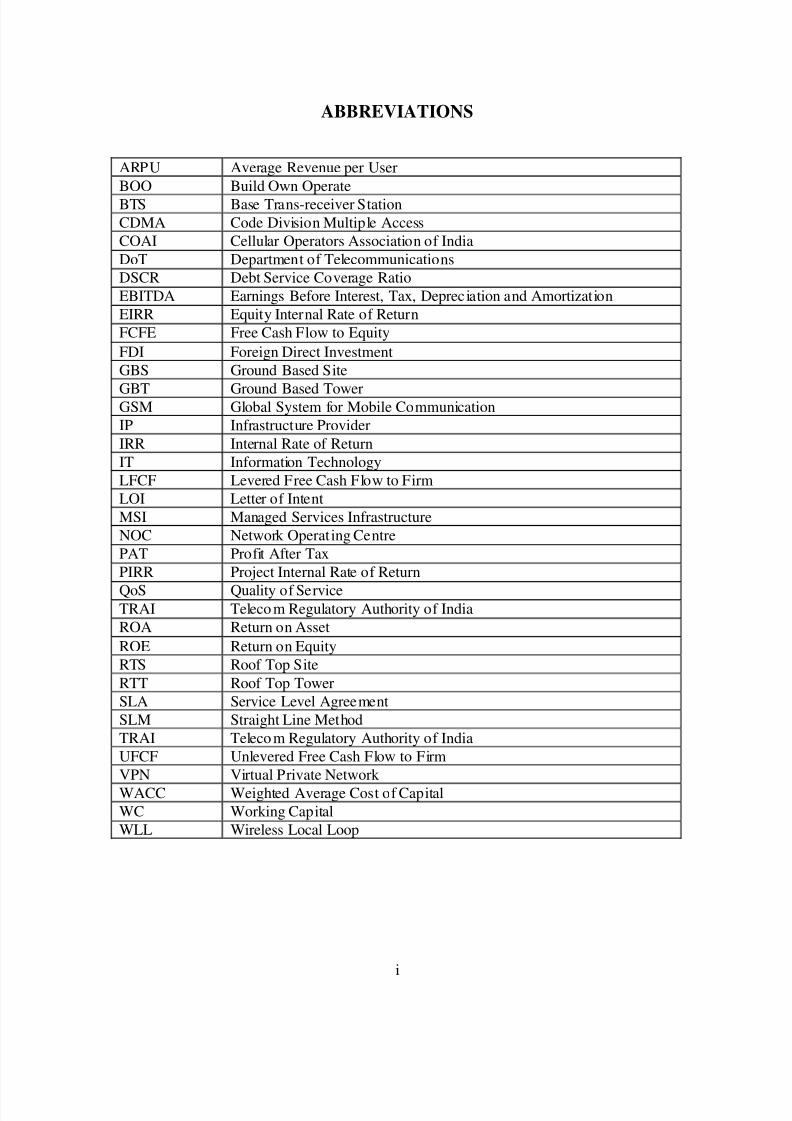

ABBREVIATIONS

ARPU Average Revenue per User BOO Build Own OperateBTS Base Trans-receiver StationCDMA Code Division Multiple AccessCOAI Cellular Operators Association of IndiaDoT Department of TelecommunicationsDSCR Debt Service Coverage RatioEBITDA Earnings Before Interest Tax Deprec iation and AmortizationEIRR Equity Internal Rate of ReturnFCFE Free Cash Flow to EquityFDI Foreign Direct InvestmentGBS Ground Based Site

GBT Ground Based TowerGSM Global System for Mobile CommunicationIP Infrastructure ProviderIRR Internal Rate of ReturnIT Information TechnologyLFCF Levered Free Cash Flow to FirmLOI Letter of IntentMSI Managed Services InfrastructureNOC Network Operat ing CentrePAT Profit After TaxPIRR Project Internal Rate of Return

QoS Quality of ServiceTRAI Teleco m Regulatory Authority of IndiaROA Return on AssetROE Return on EquityRTS Roof Top SiteRTT Roof Top TowerSLA Service Level AgreementSLM Straight Line MethodTRAI Teleco m Regulatory Authority of IndiaUFCF Unlevered Free Cash Flow to FirmVPN Virtual Private Network WACC Weighted Average Cost of CapitalWC Working CapitalWLL Wireless Local Loop

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 762

ii

ABSTRACTIndian telecom industry was dominated by government organization till 1991 after which

many private players have entered into this market Since its liberalization the industry

has experienced impressive growth because of strong demand investor friendlyregulatory schemes and strengthening economy At present India is the second largest

mobile market in the world and is also among the fastest growing mobile markets

globally The total number of mobile subscribers in India (ie the subscriber base) has

crossed 300 million with 30049 million subscribers as on 31st March 2008 (TRAI

database)

With increase in market competition and pressure on margins telecom service providers

are being forced to increase their focus on marketing and customer acquisition This has

led to opportunities in passive infrastructure outsourcing to independent third party

infrastructure providers and also sharing the infrastructure with other service providers

Recently Telecom Regulatory Authority of India has awarded new licenses to new

players such as Unitech Swan Telecom and S Tel Limited The significant expansion

plans of the new entrants and their need to optimize investments so that they can compete

with existing players will further drive the demand of passive infrastructure in the

country

ABC Limited is an independent infrastructure provider company which proposes to buildown and operate passive infrastructure sites for telecom service providers ABC Limited

is planning to raise capital to start its operation in FY 10 Based on the details regarding

capital expenditure operating expenditures and future expansion plans of ABC Limited

provided by the promoter of the company a detailed financial model has been prepared

and key financial ratios has been estimated to assess the financial feasibility and returns

on investment

Total investment required to meet the target of around 12000 tower sites (both GBT and

RTT) is estimated to be INR 36343 million ABC has planned to raise 70 of required

capital through long term debt and remaining as equity Results of financial model shows

that IRR for such project will be more than 18 and equity IRR will be around 36

provided that ABC will meet the above target of 12000 tower sites by FY14 Project IRR

is very sensitive to Capital costs tenancy ratio and monthly tariff for each site On the

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 862

iii

other hand equity IRR is sensitive to loan moratorium period and interest rate on long

term debt The project will generate enough cash flows to cover its debt obligation and

also to generate high return on equity invested

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 962

iv

LIST OF TABLESTable 31 Telecom Circles 17 Table 41 Expansion Plan 31

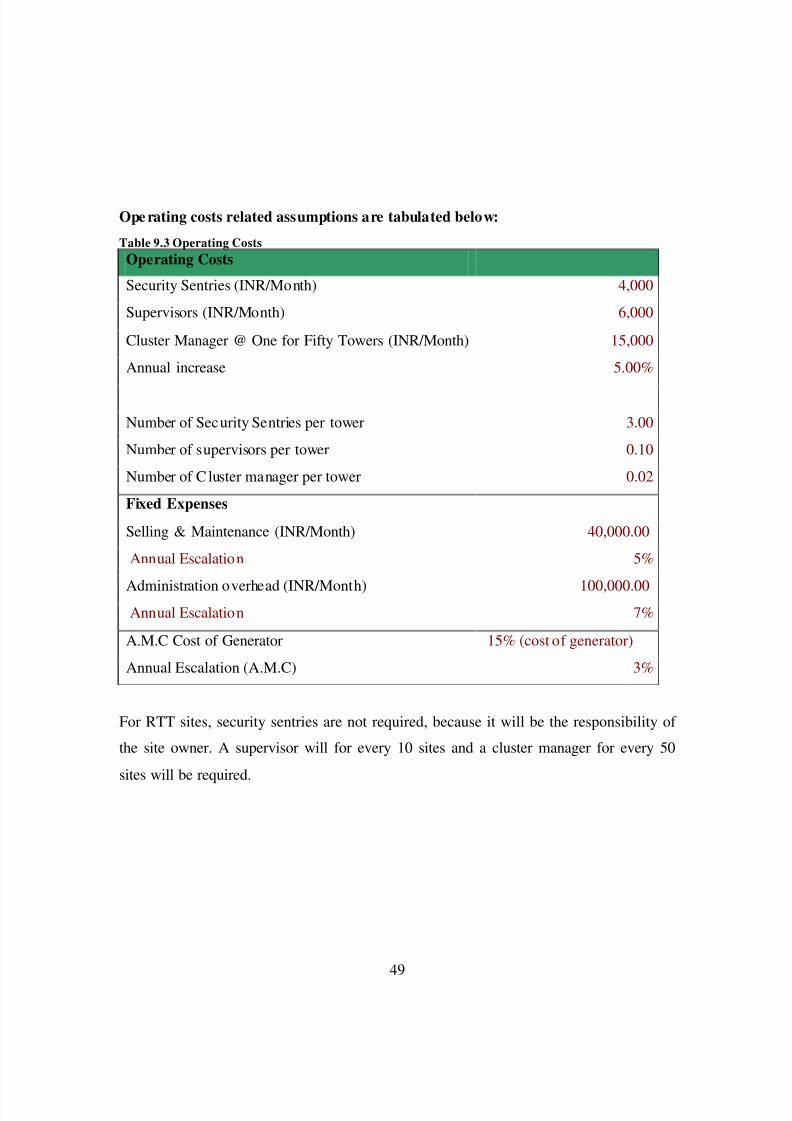

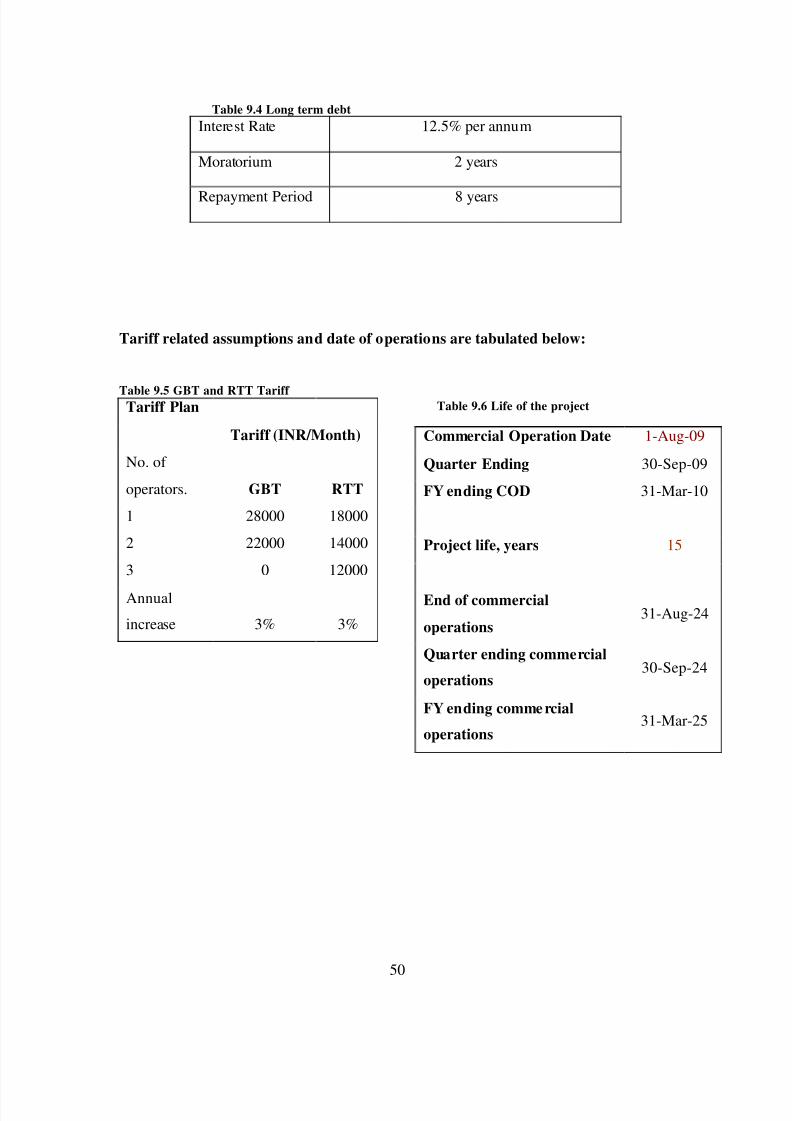

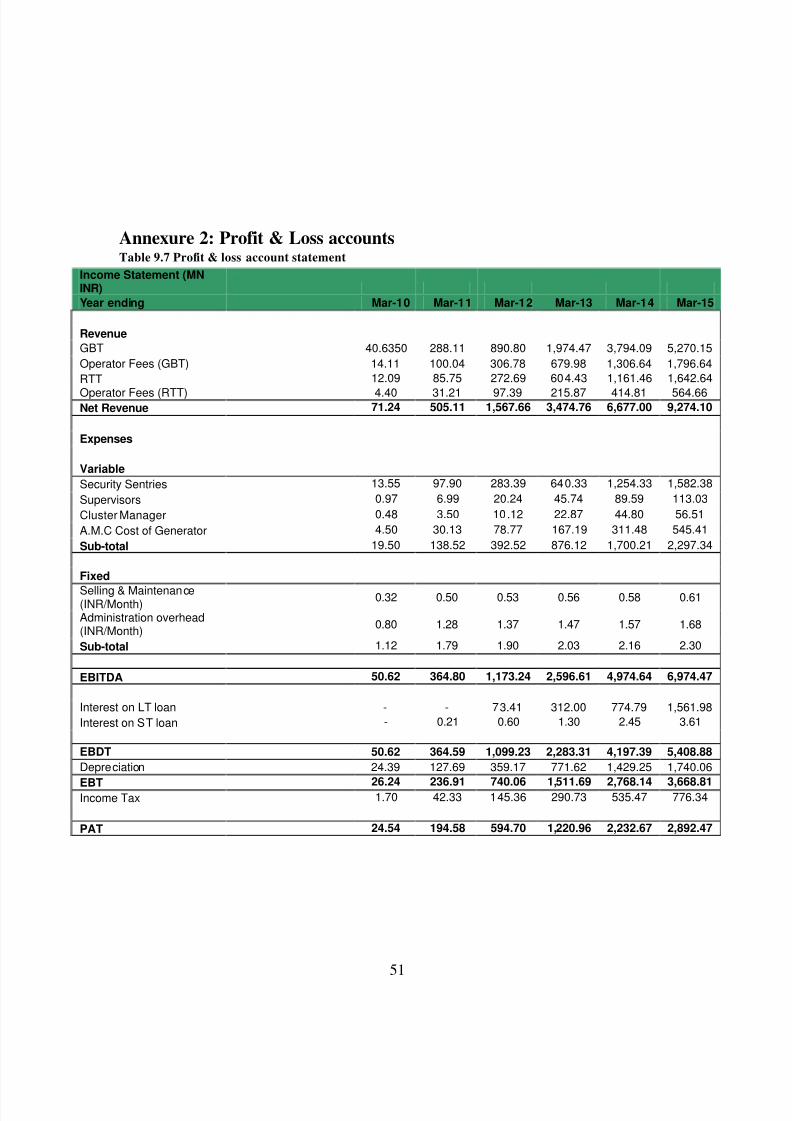

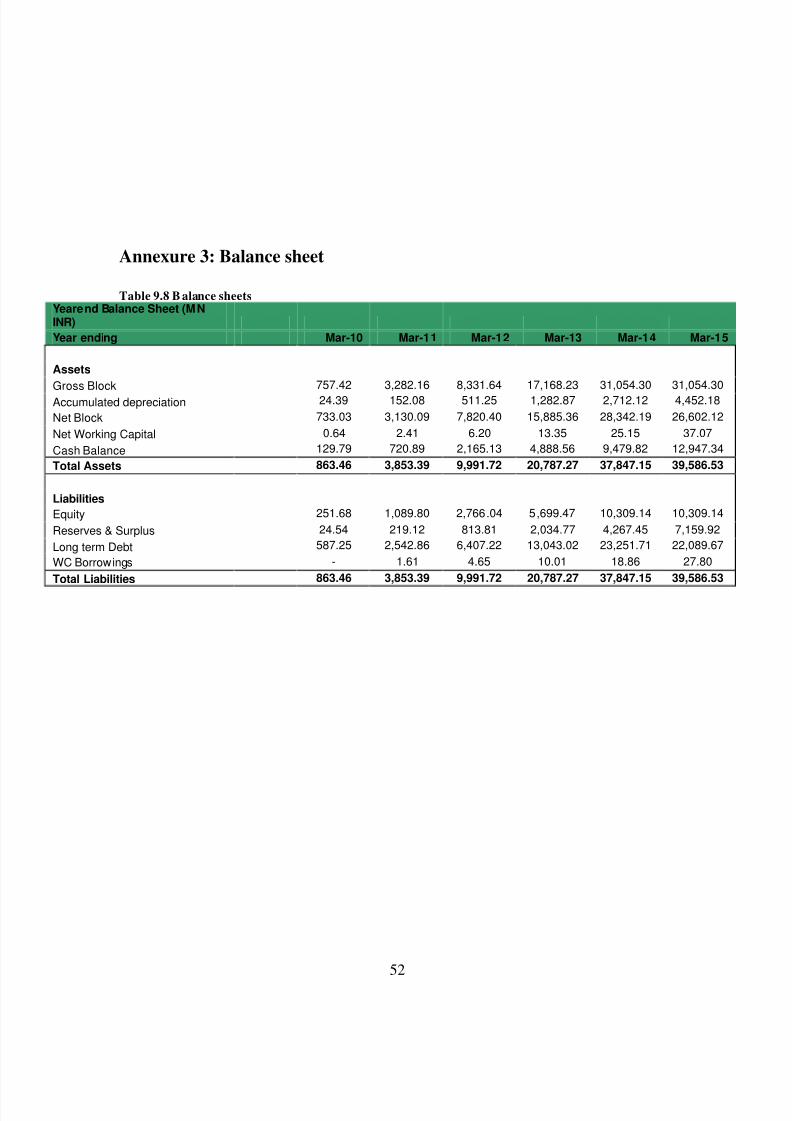

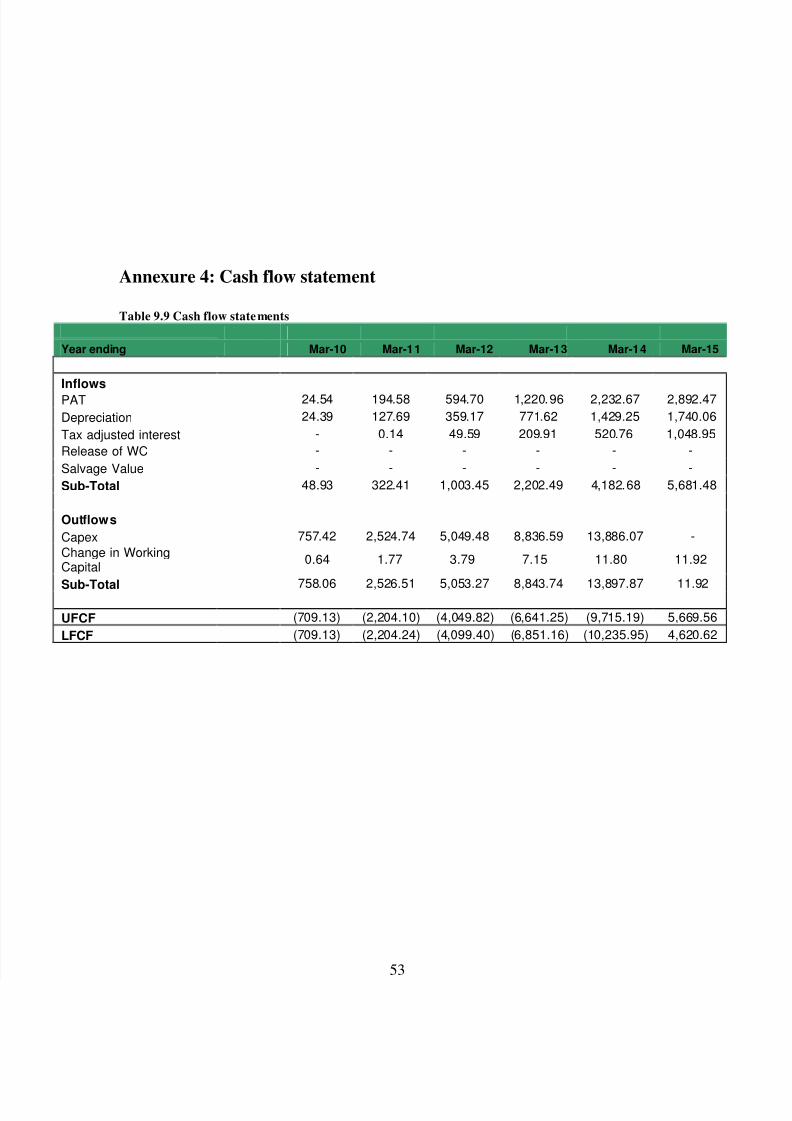

Table 61 Funding Proposal 39 Table 62 Income Statement 39 Table 63 Balance Sheet 40 Table 64 Key financial ratios 40 Table 65 Profitability ratios 41 Table 66 F inancial returns 41 Table 91 Expected Tenancy Ratios 50 Table 92 GBT and RTT Capital Cost 51 Table 93 Operating Costs 52 Table 94 Long term debt 52 Table 95 GBT and RTT Tariff 53 Table 96 Life of the project 53 Table 97 Profit amp loss acco unt statement 54 Table 98 Balance sheets 55 Table 99 Cash flow statements 56

LIST OF FIGURES

Figure 3-1 Growth of Subscriber base 10 Figure 3-2 Mobile Penetration Rate 10 Figure 3-3 Market Share 11

Figure 3-4 Licensed Circles 12 Picture 3 1 Telecom Tower 14 Figure 3-5 Telecom Infrastructure Market Players 16 Figure 3-6 Telecom Tower Growth Scenario 17 Figure 6-1 Project IRR vs GBT and RTT CAPEX 35 Figure 6-2 Project IRR vs GBT Tariff 36 Figure 6-3 Project IRR vs RTT Tariff 36 Figure 6-4 Project IRR vs Tenancy ratio for RTT sites and GBT sites 37 Figure 6-5 Equity IRR vs long term debt interest rate for different leverage level 37 Figure 6-6 Equity IRR vs long term debt repayment period at different level of moratorium periods 38

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 1062

1

1 INTRODUCTION

ABC Ltd 1 is an Infrastructure Provider company that builds owns operates and

maintains passive network infrastructure on a shared basis for mobile telecom operators

and ITES providers The Company was formed in Jan 2009 Its objective is to provide

network design and planning network deployment network operations amp maintenance

infrastructure management application management and professional services to telecom

operators and enterprises

The company is planning to raise capital in the form of equity and debt to start its

operation by Aug 09 The purpose of this project is to prepare detailed financial model

for assessment of feasibility of such projects building scenarios and sensitivity charts

calculation of risk and returns associated with the project and valuation of ABC Limited

subjected to present and expected future market conditions

ABCrsquos vision is to provide world class managed infrastructure amp allied services to the

service providers to optimize their service delivery capability In the initial years of

operation the company will focus on telecom sector with almost 100 of its proposed

capital expenditure till FY 14 earmarked for developing and owning passive

infrastructure for sharing among mobile service providers

Passive Telecom Infrastructure Sharing

Mobile networks have base stations (or cell sites) which have active and passive

infrastructure components Active components include the antenna trans-receivers

switches feeder cables Node B and microwave radio equipments Passive (or non-electronic) components include the land tower shelter air-conditioning equipment

diesel electric generator battery electrical supply technical premises and easements

pylons etc Passive infrastructure in a mobile network essentially involves acquiring land

1 Actual name o f the company is no t stated as per the instructions given by external supervisor

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 1162

2

setting up towers and electrical and civil works that needs to be in place before operators

can install the active infrastructure which brings mobile services to the consumers In a

typical cell site build-out almost 65 of the total cost is attributed to passive

infrastructure and 35 to active infrastructure In this report passive cell siteinfrastructure has also been henceforth referred to as towers or sites

Mobile operators are required to setup more and more BTS (cell) sites due to the

exponential growth of mobile subscribers in India (currently growing at almost 152

million subscribers a month) and limited availability of spectrum B and C Circles (where

traffic density may not be as high as metros and Circle A) are expected to drive future

subscriber growth and requirements for cell sites will be higher to ensure greater

coverage

To cover large stretch of almost 65000 Kilometers of national highways additional

18000 towers (one tower for every 3 Kilometers of highway) will be required in near

future to ensure better connectivity Proposed build out of 3G networks are expected to

further drive substantial growth in the number of towers over the next few years

However creating new infrastructure by each operator separately leads to duplicating

huge capital investments It also contributes to mushroom growth of telecom towers and

deteriorating skylines in urban areas which has already led to some local municipal and

state governments to regulate and restrict the erection of new mobile towers

The continued pressure on cellular tariffs higher infrastructure costs for network

deployment particularly in semi-urban and rural areas and compelling need to reduce

time to market for network roll outs have led operators to share and even outsource theirinfrastructure requirements from third party infrastructure providers like ABC GTL and

Indus towers

2 As published in ET 8 th May 09 Edition

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 1262

3

Sharing promotes capital efficiency as it allows more than one service provider to

leverage and ride on common infrastructure In its simplest form it involves two or more

operators jointly using the common passive infrastructure in a cell site While viewed

largely as a measure to reduce CAPEX and operating expense such sharing also leads toimprovement of service quality (by ensuring site space for service providers and reducing

black spots) and the environment (by reducing number of cell sites and towers)

In outsourcing operators take passive infrastructure and tower space from third party

infrastructure companies on a monthly rental basis to host their radio and transmission

equipments Outsourcing provides significant benefits to operators It enables them to

save on capital expenditure (it actually converts CAPEX into OPEX in the form of lease

rentals) and focus on their core activities of sales marketing and branding while leavingthe cumbersome task of managing the site development process and site operation and

maintenance to third parties who exclusively deal with such activities

Active infrastructure sharing is not popular across the globe for several reasons the most

important being increased inter dependency among competing service providers

However tower sharing and outsourcing of tower ownership is an accepted practice in

many developed markets In countries like USA UK and Australia there are

independently owned tower companies who rent tower space to various mobile operators

The United States has arguably the most developed independent mobile tower market

with independent tower companies owning over half of all mobile towers in that country

Mobile tower owners generate revenue by owning the towers and leasing space on the

towers to mobile telecommunications operators under long-term contracts Under this

business model ownership of the base station equipments coupled to the towers is

retained by the mobile telecommunications operators In addition to rental payments

mobile tower owners generally receive a fee for installing customers base station

equipment on the tower Mobile tower owners also receive services revenue for

operations and maintenance of the passive infrastructure Regulators all over the world

favor passive sharing of infrastructure

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 1362

4

The concept of passive infrastructure sharing is increasingly gaining market acceptance

in India So far it has been largely limited to bilateral sharing between operators in the

form of barter where the operators split the site related CAPEX and OPEX costs The

available information suggests that about 25 of the existing 90000 tower sites in Indiaare currently being shared for passive infrastructure predominantly in rural areas and

small towns

ABC Limited is expecting to get shortlisted by Department of Telecom for setting up

passive cellular infrastructure in rural areas with support from the Universal Services

Obligations (USO) Fund The recent announcements by some operators like Bharti

Hutch (Vodafone) Reliance Idea for mutual sharing of infrastructure through new

companies and entry of third party infrastructure providers has further expanded the

tower market in India

Results of detailed financial model indicate that with given expansion plans and

assumptions ABC will create value for its shareholders investors clients and promoters

The project is expected to generate high cash flows which will be sufficient enough to

pay back its debt liabilities and to generate and equity IRR of 36

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 1462

5

2 OBJECTIVES

The scope of work for this Study project involves the following

Market assessment for Indian telecom Infrastructure sector

Collection of data related to capital and operating costs (from promoter)

Forecasting operating costs

Preparation of detailed financial model

Calculation of UFCF ( Unlevered Free Cash Flows) LFCF (Levered Free Cash

Flows)

Estimation of Project and Equity IRRrsquos

Preparation of balance sheet PampL and cash flow statement for expected life

cycle of project

Sensitivity analysis and Scenario analysis

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 1562

6

3 LITERATURE REVIEW

31 International Experience in Infrastructure Sharing

Different countries have adopted different approaches in order to safeguard the level of

competitive independence between co-operating operators Measures include mandating

a distinct and differentiated cost base between operators the development of different

business plans marketing and distribution strategies and the independent development or

acquisition of content and services Requiring the independent control over the respective

frequency resources of each operator is also an important competitive safeguard

In the EU for example operators are allowed to share infrastructure as long as they

maintain full operational control of their network Sharing the radio access network is

permitted but sharing frequencies and the core network is not In particular the databases

used to administer subscriber and interconnection information are required to be kept

separate Exemptions however are generally granted in special cases which advance the

objectives of government policy and the economic benefits to the consumers of the

services It is important to note that any infrastructure sharing agreement could also be

subject to review by the EC Commission under Article 81 of the EC Treaty andor the EC

Merger Regulation

USA

In USA the number of wireless service subscribers has increased from 1284 million to

2433 million between December 2001 and December 2007 representing an increase of

approximately 88 and market penetration of approximately 70 The tower business in

USA is a $5 billion industry consolidated around four large players -- American Tower

(ATC) Crown Castle International (CCI ) SBA Communications (SBAC ) and GlobalSignal (GSL ) which control 40 of the approximately 210000 (P amp Lisa 2009) towers

across the US The primary business of these companies involves leasing antenna space

on multi-tenant communications sites to a variety of wireless carriers including radio and

3 Source CTIA-The Wireless Association Website

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 1662

7

television broadcast companies under long-term lease contracts Typically these leases

are long-term (five to 10 year) contracts with renewal terms at the option of the customer

Some co mpanies offer tower related services on a limited basis including site acquisition

zoning and permitting services and structural analysis services and project managementof antenna installations that support their site leasing operations and the addition of new

tenants and equipment on their sites

Towers are a relatively scarce asset in USA as zoning laws often do not permit a new

tower to be built in the immediate vicinity of an existing tower Tenant churn tends to be

low as towers are an integral part of the networks of the wireless service providers

Tenants own their own equipment (and therefore bear the technology risk) generally

handle installation and maintenance and pay for electricity and most ongoing assets

greatly simplifying the tower business model

Germany

In Germany the main concern faced by the regulator involved a possible threat to the

competitive independence of potential 3G operators that could result from a tight

integration of the networks as a result of infrastructure sharing Infrastructure Sharing is

allowed only if the mobile systems can be independently operated for example if they

can be shut down or maintained independently by software and that no customer data is

shared (OECD report 2004) In Germany the sharing of antennae and sites is relatively

common however the sharing of transmission management equipment and core

networks is not commonly done (Vogelsang 2002)

Sweden

In Sweden the regulator has agreed to allow significant infrastructure sharing for 3G

operators Each operator only has to cover 30 of the customers while for the remaining

70 infrastructure can be shared This is the approach being taken by the Europolitan

companies Vodafone Hi3G and Orange which jointly own 3G Infrastructure Services

However with competition concerns the regulator only allows radio components such as

antennas cables and base station electronics to be shared (Khurram Mahmood 2008)

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 1762

8

Singapore

In the case of Singapore the regulatorrsquos infrastructure sharing approach is guided by the

primary policy goal of encouraging facilities-based competition Under the current

regulatory framework licensees are generally not required to share any infrastructure that

it controls with its competitors Each licensee is expected to build or lease the use of the

infrastructure it requires Notwithstanding this however infrastructure sharing is

mandated in areas where there are clear space and operating constraints For 2G and 3G

licensees such matters relate to infrastructure in the Mass Rapid Transit and underground

road tunnels The regulator has also allowed the co-location of base stations and sharing

of transmission towers and masts to reduce the impact on the environment and to

minimize the inconvenience to building owners and residents (IDA 2009)

Malaysia

Taking a different approach in Malaysia operators owning network facilities have been

encouraged by the regulator to share infrastructure as a means of lowering costs and

expanding coverage as well as to avoid a duplication of resources To this effect a

Memorandum of Understanding to share infrastructure has been executed between the

mobile operators To further catalyze infrastructure sharing the concept of a third party

provider of facilities is also being promoted in Malaysia Under this concept of a third

party will build the infrastructure and lease capacity or space to existing se rvice

providers This concept not only provides ready-made sites but will also help reduce the

numbers of telecommunication towers that have to be dealt with by local authorities

(MAXIS 2009)

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 1862

9

32 Domestic Telecom Market assessment

The Indian Telecom Industry-Historical perspective

The Indian telecommunication industry was originally a government controlled

monopoly comprising three state owned operators

MTNL (which provided wire-line services in Mumbai and Delhi metropolitan

areas)

DOT (which provided wire-line services to rest of the country)

VSNL (which provided international services)

Liberalization started in 1991 with opening up of mobile services to private sectorparticipation The country was divided into 23 circles comprising of four metropol9otan

areas (Chennai Delhi Kolkata and Mumbai) and 19 other circles broadly defined by

parameters of states (K 2008) These 19 non-metropolitan circles have been categorized

as A B and C circles in descending order of their revenue generation potential (as

shown below)

Table 31 Telecom Circles

MetropolitanAreas Circle A Circle B Circle C

Delhi ChennaiMumbai Kolkata

Gujarat KarnatakaAP Tamil NaduMaharashtra

Punjab Kera laHaryana UP (West)Rajasthan UP(East) MP WestBengal

HP JampK North-East OrissaAssam Bihar

In 1997 TRAI was formed for regulating the operations and policy making process of

Indian telecommunication sector Since its liberalization India has experienced sustained

and impressive growth in its telecommunication sector primarily because of progressive

regulatory regime strong demand for mobile telecommunication services and

strengthening economy The country has achieved distinction of having worldrsquos lowest

tariff fastest growth ion subscriber base and availability of some of the cheapest mobile

handsets

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 1962

10

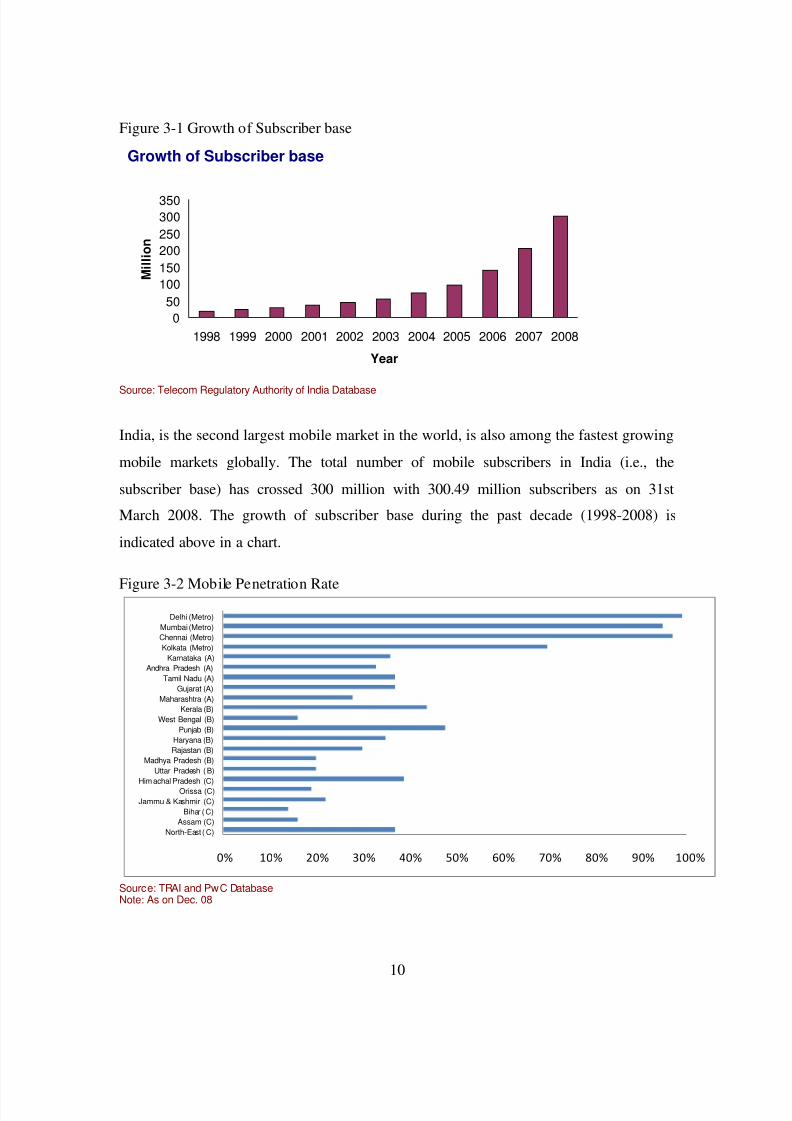

Figure 3-1 Growth of Subscriber base

Growth of Subscriber base

050

100150200250300350

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Year

M i l l i o n

Source Telecom Regulatory Authority of India Database

India is the second largest mobile market in the world is also among the fastest growing

mobile markets globally The total number of mobile subscribers in India (ie the

subscriber base) has crossed 300 million with 30049 million subscribers as on 31st

March 2008 The growth of subscriber base during the past decade (1998-2008) is

indicated above in a chart

Figure 3-2 Mobile Penetration Rate

0 10 20 30 40 50 60 70 80 90 100

North-East ( C)Assam (C)

Bihar ( C)Jammu amp Kashmir (C)

Orissa (C)Him achal Pradesh (C)

Uttar Pradesh ( B)Madhya Pradesh (B)

Rajastan (B)Haryana (B)

Punjab (B)West Bengal (B)

Kerala (B)Maharashtra (A)

Gujarat (A)Tamil Nadu (A)

Andhra Pradesh (A)Karnataka (A)

Kolkata (Metro)Chennai (Metro)Mumbai (Metro)

Delhi (Metro)

Source TRAI and PwC DatabaseNote As on Dec 08

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 2062

11

Indian telecom industry has experienced a high growth rate in Metros and class A circles

with coverage reaching around 90 and 35 respectively However coverage in the

Class B and Class C cities is still low at 15-25 Growth in Class B and Class C circles

has concentrated in urban area while penetration in rural area remains lower Thus futuregrowth is likely to come largely from Class B and C circles and rural areas Keeping this

in view larger players like Bharti Airtel Limited Reliance Communications Limited and

Bharat Sanchar Nigam Limited (BSNL) are largely focusing on increasing their

geographical coverage in Class B and C c ircles

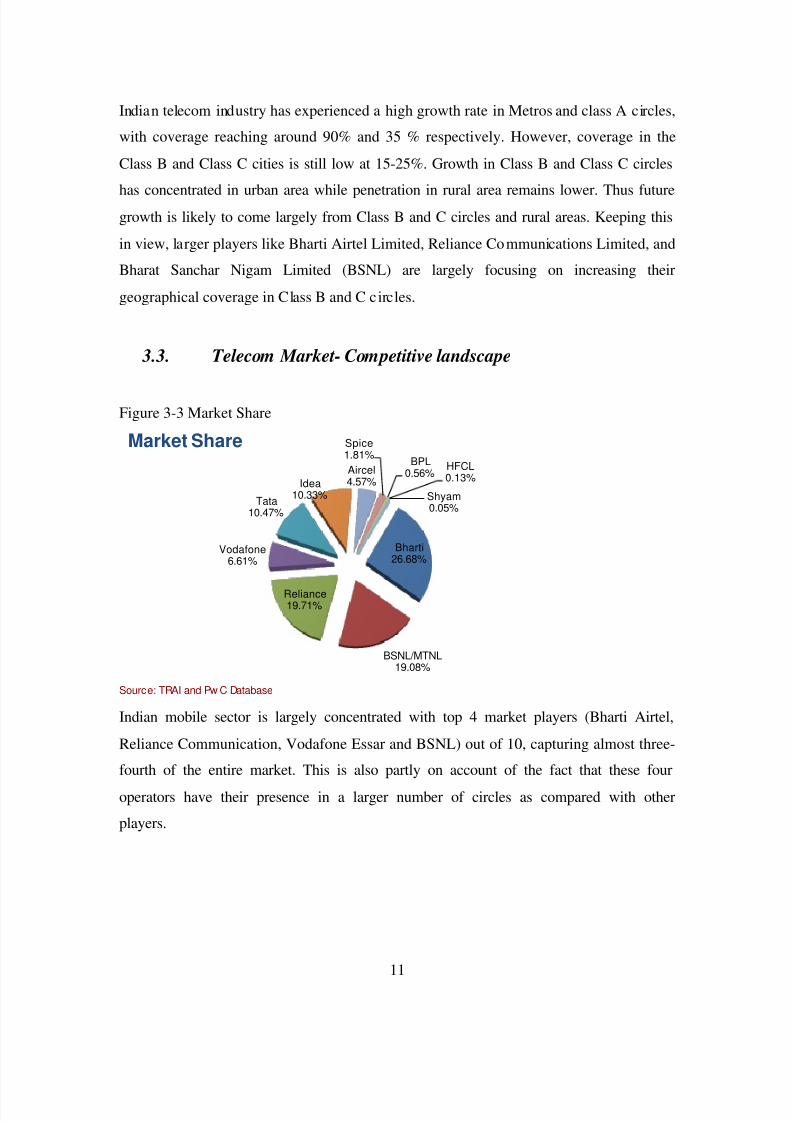

33 Telecom Market- Competitive landscape

Figure 3-3 Market Share

Bharti2668

BSNLMTNL1908

Reliance1971

Vodafone661

Tata1047

Idea1033

Aircel457

Spice181

BPL056

HFCL013

Shyam005

Market Share

Source TRAI and Pw C Database

Indian mobile sector is largely concentrated with top 4 market players (Bharti Airtel

Reliance Communication Vodafone Essar and BSNL) out of 10 capturing almost three-

fourth of the entire market This is also partly on account of the fact that these four

operators have their presence in a larger number of circles as compared with other

players

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 2162

12

Figure 3-4 Lice nsed Circles

0

5

10

15

20

25

Licensed Circles (Dec 07) New Circles (Sep 08)

Source TRAI and CRISIL Database

The competition in Indian telecom sector is expected to intensify in near future because

recently new licenses have been granted to some of the existing operators for new circles

and also to new entrants like Unitech Datacom Swan Telecom and Stel These new

players are expected to capture the rural and semi-urban cities of C ircle B and Circle C as

they are now expected to grow at a much faster rate Shorter network rollout time and

competitiveness in the industry will force these entrants to start the ir operation as early as

possible Tower companies like ABC will allow incumbents to start operations in a

particular region just by installing their electronics on the ready-to-use towers thereby

significantly shortening the ro llout time

Moreover a rapidly increasing subscriber base and spectrum crunch would force the

existing telecom operators to maintain the minimum level of QoS Thus to retain existing

subscribers by preventing subscriber churn operators will require additional

infrastructure in their existing areas of operation to be able to offer better QoS This will

also result in increase in demand for telecom infrastructure in the existing markets

(Ramachanran 2009)

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 2262

13

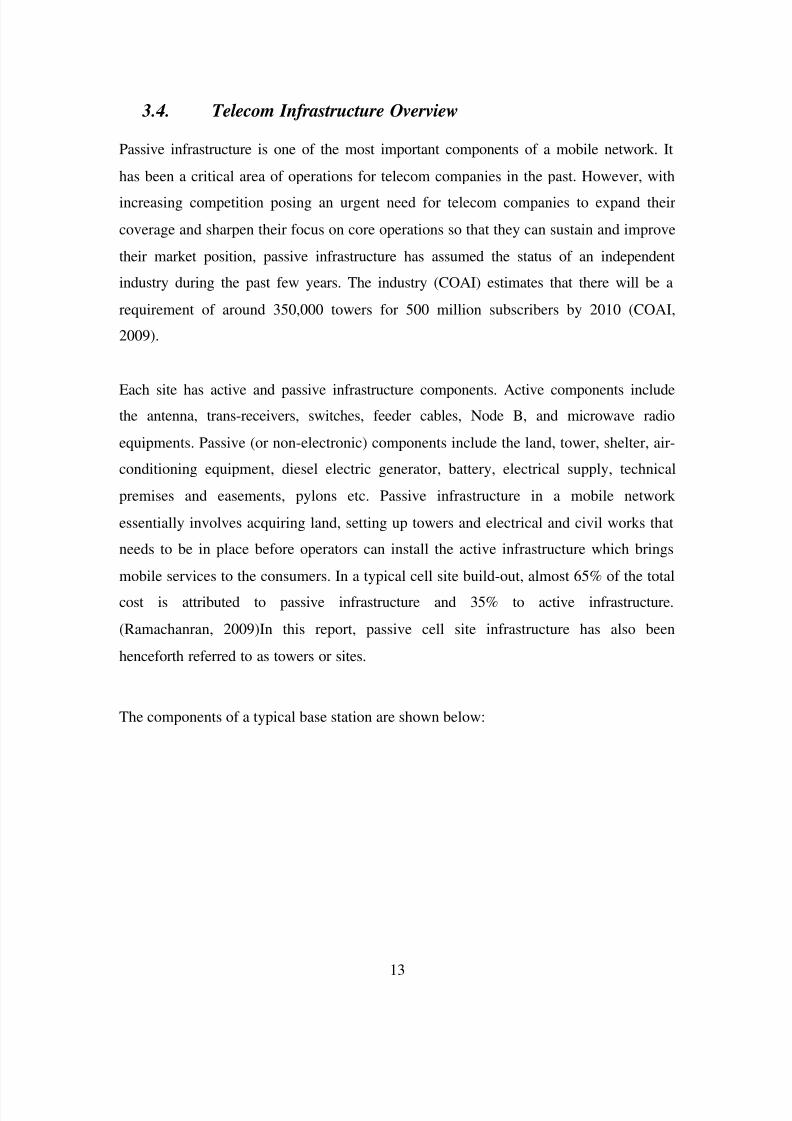

34 Telecom Infrastructure Overview

Passive infrastructure is one of the most important components of a mobile network It

has been a critical area of operations for telecom companies in the past However with

increasing competition posing an urgent need for telecom companies to expand their

coverage and sharpen their focus on core operations so that they can sustain and improve

their market position passive infrastructure has assumed the status of an independent

industry during the past few years The industry (COAI) estimates that there will be a

requirement of around 350000 towers for 500 million subscribers by 2010 (COAI

2009)

Each site has active and passive infrastructure components Active components includethe antenna trans-receivers switches feeder cables Node B and microwave radio

equipments Passive (or non-electronic) components include the land tower shelter air-

conditioning equipment diesel electric generator battery electrical supply technical

premises and easements pylons etc Passive infrastructure in a mobile network

essentially involves acquiring land setting up towers and electrical and civil works that

needs to be in place before operators can install the active infrastructure which brings

mobile services to the consumers In a typical cell site build-out almost 65 of the total

cost is attributed to passive infrastructure and 35 to active infrastructure

(Ramachanran 2009)In this report passive cell site infrastructure has also been

henceforth referred to as towers or sites

The components of a typical base station are shown below

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 2362

14

Picture 3 1 Telecom Tower

Telecom towers are broadly classified on the basis of their placement as Ground-basedand Roof-top

1 Ground-Based Tower Ground-based towers (GBTs) are taller (typically 200 to 400

feet) and are mostly used in rural and semi-urban areas because of the easy

availability of real-estate space there GBTs involve a capital expenditure in the range

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 2462

15

of Rs 3 to 4 million depending on the height of the tower land prices etc

(Ramachanran 2009)

2 Roof-Top Tower (RTT) Roof-top towers (RTTs) are generally placed on the roofsof high-rise buildings They are shorter (than GBTs) and more common in urban and

highly populated areas where there is paucity of real-estate space Typically these

involve a capital expenditure of Rs 15 to 2 million (Ramachanran 2009)

The height of a telecom tower determines the number of antennas that can be

accommodated which in turn determines the capacity of the towers apart from factors

such as location and geographica l conditions (wind speeds type of terrain etc)

35 Telecom Infrastructure- Domestic market

In India there are broadly two kinds of operators in the tower infrastructure industry

Tower infrastructure subsidiaries

Reliance Infratel Limited

Bharti Infratel Limited

Indus Towers Limited

Wireless TT Info Services Limited (WTTIL)

Independent tower infrastructure companies (ITICs)

GTL Infrastructure

Xcel Telecom

Essar Telecom Infrastructure

Aster Infrastructure

Bharat Telemast

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 2562

16

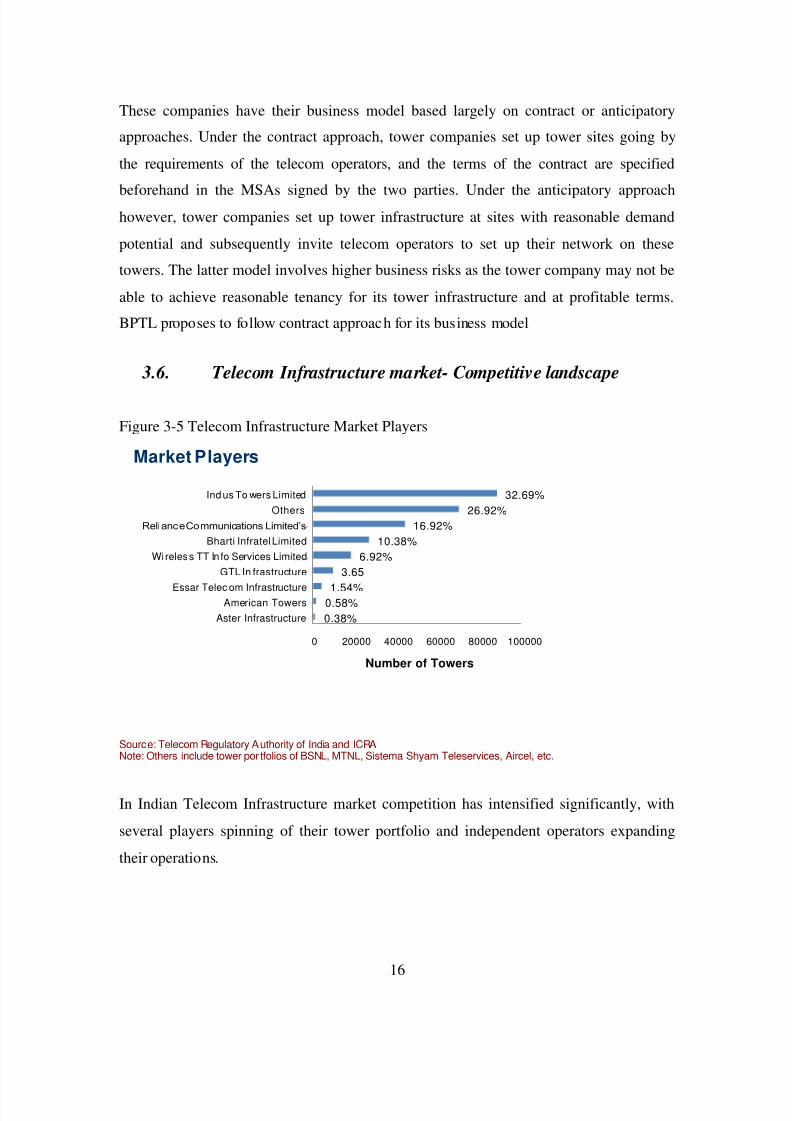

These companies have their business model based largely on contract or anticipatory

approaches Under the contract approach tower companies set up tower sites going by

the requirements of the telecom operators and the terms of the contract are specified

beforehand in the MSAs signed by the two parties Under the anticipatory approachhowever tower companies set up tower infrastructure at sites with reasonable demand

potential and subsequently invite telecom operators to set up their network on these

towers The latter model involves higher business risks as the tower company may not be

able to achieve reasonable tenancy for its tower infrastructure and at profitable terms

BPTL proposes to follow contract approach for its business model

36 Telecom Infrastructure market- Competitive landscape

Figure 3-5 Telecom Infrastructure Market Players

038058154

365692

10381692

26923269

0 20000 40000 60000 80000 100000

Aster InfrastructureAmerican Towers

Essar Telec om Infrastructure

GTL In frastructureWi reles s TT In fo Services Limited

Bharti Infratel Limited

Reli anc e Communications Limitedrsquos

OthersInd us To wers Limited

Number of Towers

Market Players

Source Telecom Regulatory Authority of India and ICRANote Others include tower por tfolios of BSNL MTNL Sistema Shyam Teleservices Aircel etc

In Indian Telecom Infrastructure market competition has intensified significantly with

several players spinning of their tower portfolio and independent operators expanding

their operations

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 2662

17

Bharti Airtel Limited Reliance Communications Limited and Tata Teleservices Limited

have hived off their tower assets into separate tower infrastructure subsidiaries namely

Bharti Infratel Limited Reliance Infratel Limited and Wireless TT Infoservices Limited

respectively Also Bharti Infratel Limited together with Vodafone Essar Limited and IdeaCellular Limited in a joint- venture agreement has created Indiarsquos largest tower

infrastructure company ndash Indus Towers Limited which has an estimated portfolio of

around 88000 towers (Anjan V amp N 2009) Whereas in past few years number of

independent tower infrastructure companies have ventured into the domestic telecom

tower industry These include GTL Infrastructure Limited Essar Telecom Infrastructure

Limited Xcel Telecom Private Limited (American Towers) Tower Vision India Private

Limited Aster Infrastructure Private Limited TVS Interconnect Systems Limited etc

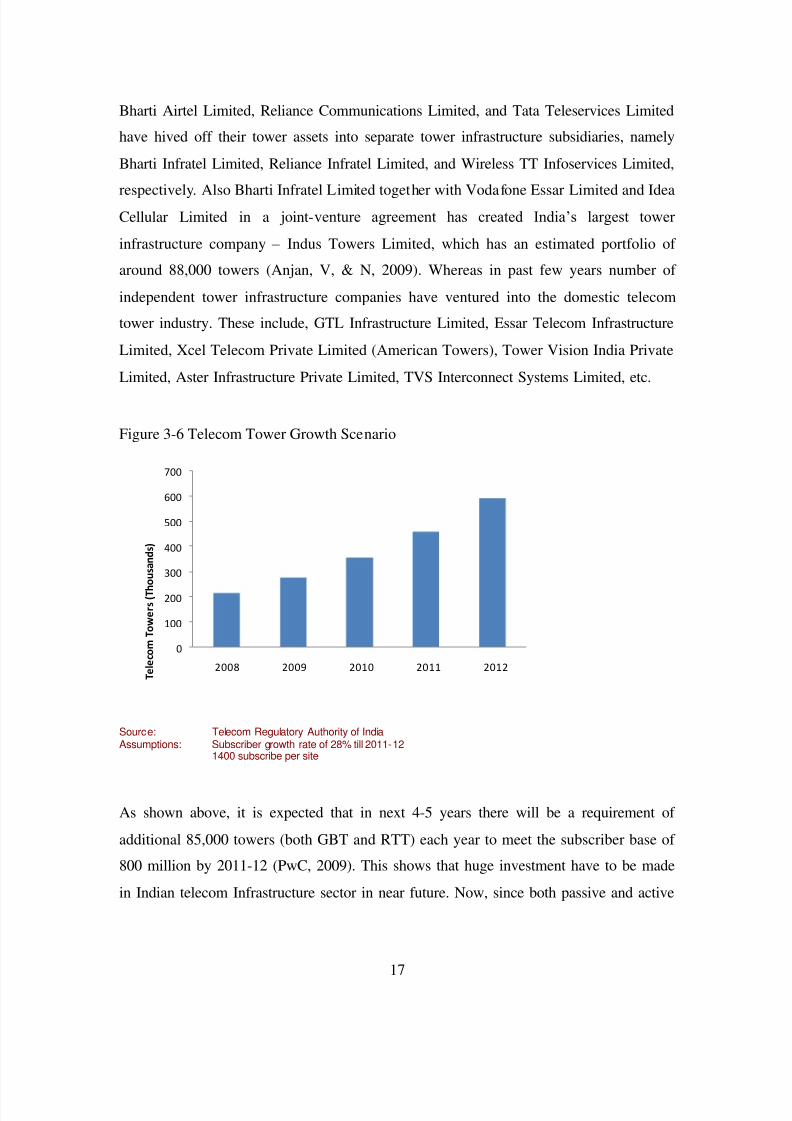

Figure 3-6 Telecom Tower Growth Scenario

0

100

200

300

400

500

600

700

2008 2009 2010 2011 2012 T e

l e c o m

T o w e r s

( T h o u s a n

d s )

Source Telecom Regulatory Authority of IndiaAssumptions Subscriber growth rate of 28 till 2011-12

1400 subscribe per site

As shown above it is expected that in next 4-5 years there will be a requirement of

additional 85000 towers (both GBT and RTT) each year to meet the subscriber base of

800 million by 2011-12 (PwC 2009) This shows that huge investment have to be made

in Indian telecom Infrastructure sector in near future Now since both passive and active

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 2762

18

infrastructure sharing is a llowed (except spectrum) Independent service providers will be

benefited Increase in subscriber base introduction of new technologies like 3G Wi-max

etc and increase in market healthy market competition in telecom services sector will

drive the growth in telecom infrastructure sector

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 2862

19

4 BUSINESS PLAN

41 Passive Infrastructure

Mobile networks have base stations (or cell sites) which have active and passive

infrastructure components Active components include the antenna trans-receivers

switches feeder cables Node B and microwave radio equipments Passive (or non-

electronic) components include the land tower shelter air-conditioning equipment

diesel electric generator battery electrical supply technical premises and easements

pylons etc Passive infrastructure in a mobile network essentially involves acquiring land

setting up towers and electrical and civil works that needs to be in place before operators

can install the active infrastructure which brings mobile services to the consumers In atypical cell site build-out almost 65 of the total cost is attributed to passive

infrastructure and 35 to active infrastructure

42 Infrastructure Sharing

Mobile operators are required to setup more and more BTS (cell) sites due to the

exponential growth of mobile subscribers in India (currently growing at almost 15 4

million subscribers a month) and limited availability of spectrum B and C Circles (wheretraffic density may not be as high as metros and Circle A) are expected to drive future

subscriber growth and requirements for cell sites will be higher to ensure greater

coverage

However creating new infrastructure by each operator separately leads to d uplicat ing

huge capital investments It also contributes to mushroom growth of telecom towers and

deteriorating skylines in urban areas which has already led to some local municipal and

state governments to regulate and restrict the erection of new mobile towers

The continued pressure on cellular tariffs higher infrastructure costs for network

deployment particularly in semi-urban and rural areas and compelling need to reduce

4 As published in ET 8 th May 09 Edition

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 2962

20

time to market for network roll outs have led operators to share and even outsource their

infrastructure requirements from third party infrastructure providers like BPTL GTL and

Indus towers It promotes capital efficiency as it allows more than one service provider to

leverage and ride o n common infrastructure In its simplest form it involves two or moreoperators jointly using the common passive infrastructure in a cell site While viewed

largely as a measure to reduce capital and operating expense such sharing also leads to

improvement of service q uality (by ensuring site space for service providers and reducing

black spots) and the environment (by reducing number of cell sites and towers)

In outsourcing operators take passive infrastructure and tower space from third party

infrastructure companies on a monthly rental basis to host their radio and transmission

equipments Outsourcing provides significant benefits to operators It enables them tosave on capital expenses (it actually converts capital expense into operating expense in

the form of lease rentals) and focus on their core activities of sales marketing and

branding while leaving the cumbersome task of managing the site development process

and site operation and maintenance to third parties who exclusively deal with such

activities

The concept of passive infrastructure sharing is increasingly gaining market acceptancein India So far it has been largely limited to bilateral sharing between operators in the

form of barter where the operators split the site related CAPEX and OPEX costs The

available information suggests that about 25 of the existing 90000 tower sites in India

are currently being shared for passive infrastructure predominantly in rural areas and

small towns

43 Introduction to the business

BPTL is an Infrastructure Provider company that builds owns operates and maintains

passive network infrastructure on a shared basis for mobile telecom operators and ITES

providers Its objective is to provide network design and planning network deployment

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 3062

21

network operations amp maintenance infrastructure management application management

and professional services to teleco m operators and enterprises

The company is planning to raise capital in the form of equity and debt to start its

operation by Aug 09 ABC rsquos vision is to provide world class managed infrastructure ampallied services to the service providers to optimize their service delivery capability In the

initial years of operation the company will focus on telecom sector with almost 100 of

its proposed capital expenditure till FY 14 earmarked for developing and owning passive

infrastructure for sharing among mobile service providers

44 Business Proposal

ABC will provide passive telecom infrastructure on build own operate (BOO) basis inboth ground based (GBS) as well as roof-top sites (RTS) It will undertake full range of

responsibilities in building owning and maintaining the sites and will serve as a single

window one-stop-shop provider of infrastructure services Typical responsibilities are

summarized below

Site planning keeping in view the network rollout plans of prospective customers

Site acquisition including entering into long-term agreements with land owners

Obtaining of necessary regulatory approvals

Erect ion and commissioning of tower and allied equipment

Provision of support services such as back-up power air-conditioning and

security

Provision of turnkey solutions to telecom companies such as sourcing of

equipment testing and maintenance

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 3162

22

Bharat Telemast Private Limited will identify the sites required for setting up the Passive

infrastructure by first of all getting a commitment from one operator who is called as

ldquoAnchor Operatorrdquo Then Bharat Telemast will go ahead to lease (or) buy out the site as

appropriate and commences construction of the cellular sites But the Cellular site will betypically designed for three to four operators While construction is in progress the

marketing team will work towards getting the second and third operator But care will be

taken in such a way that at least two operators are available at the time of completion of

construction

45 Sources of revenue

1 Infrastructure Provisioning Fees ndash fee paid by the operators on a monthly basisWith annual escalation

2 Site lease rental ndash Paid at actual on a monthly basis

3 Operations and maintenance charges Paid on a monthly basis

4 The contract also provides a fixed annual escalator

46 Attractiveness of business model

Stable and predictable cash flow business Once a tower asset is rented out it

usually generates a stable and predictable cash flow in the form of tower rentals

from occupants over the term of the MSA between the two parties

Low working capital requirement ABC rsquos business model is also characterized

by low working capital requirements as most of the operating expenses (such aselectricity and fuel and other variable operating expenses) are reimbursable by the

tenants on actual basis Moreover BPTL is may also be able to get rentals for the

towers in advance and also obtain better credit terms from their suppliers thus

further improving their working capital cycle

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 3262

23

High incremental profitability The operating costs associated with this

business are largely fixed in nature Thus each increment in tenancy is

accompanied by a minimal increase in costs This leads to a more thanproportionate increase in profits for every increase in occupancy

Reduction in capital investments due to present market conditions Due to

present market situation average capital requirement for RTT and GBT sites have

dropped from 2 million and 4 million to 15 million and 33 million ABC wishes

to grab this opportunity which will result in competitive advantage in near future

Extensive usage While on an average a GSM BTS can handle around 100-

1100 subscribers but in the case of high usage areas the figure can be as low as

600-700 subscribers which means a larger number of cell sites would be required

for the same area Moreover the country has the problem of spectrum scarcity

which increases the requirement of towers to maintain a reasonable leve l of

service quality

New entrants Many operators including Vodafone Essar Limited Idea Cellular

Limited Aircel Cellular Limited and Sistema Shyam Teleservices Limited have

received licenses as well spectrum in new circles which would enable them to

become pan-India operators in the next one-two years Also new licenses have

been issued to new players such as Unitech Swan Telecom and S Tel Limited

Given the significant expansion plans of new entrants over the medium term and

the need for them to optimize investments in order to maintain returns demand

for towers is expected to report a sharp increase

Shorter rollout time Indian telecom industry is highly competitive and doing

business for new entrant may not be easy Shorter network-rollout time would be

a critical success factor for the new entrants and a longer rollout time could meanloss of substantial market share to other operators Tower companies allow

players to start operations in a particular region just by installing their electronics

on the ready-to-use towers thereby significantly shortening the rollout time

New technologies 3G services are already launched in the country and to

augment their services various operators plan to launch Wi-Max services as soon

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 3362

24

as they receive additional spectrum from Government This would further

increase the demand for sharing of passive infrastructure

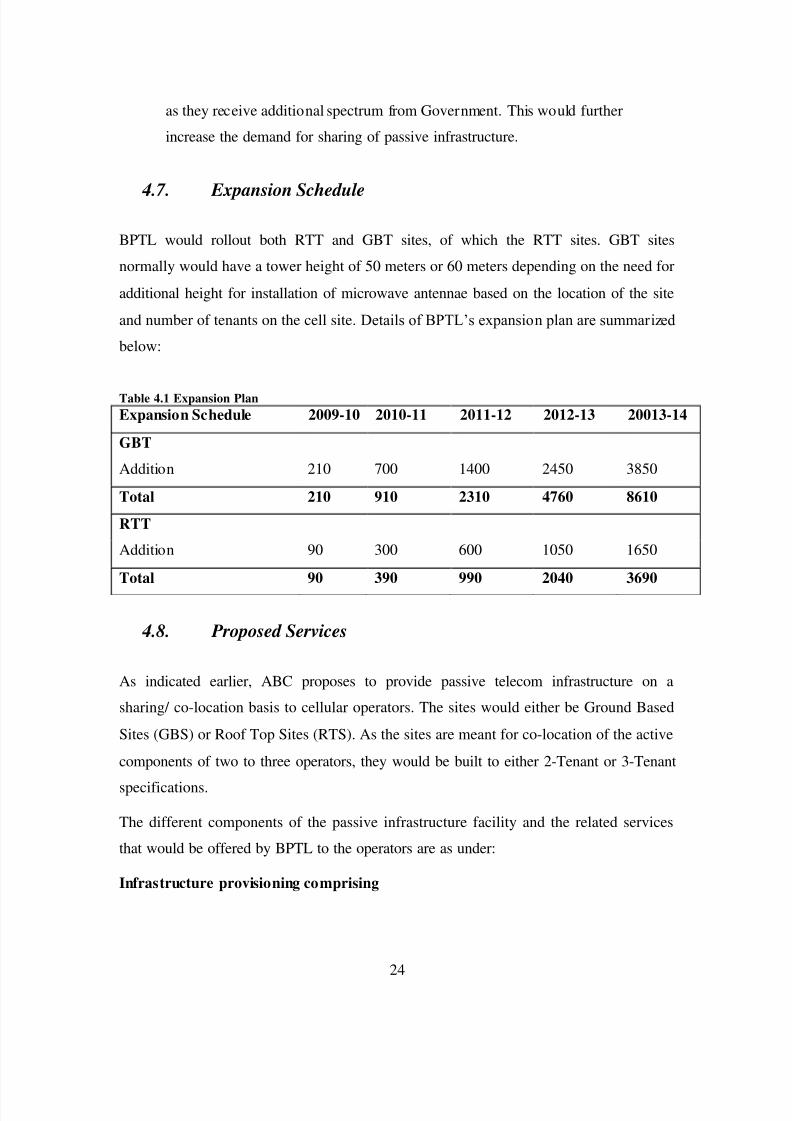

47

Expansion Schedule

BPTL would rollout both RTT and GBT sites of which the RTT sites GBT sites

normally would have a tower height of 50 meters or 60 meters depending on the need for

additional height for installation of microwave antennae based on the location of the site

and number of tenants on the cell site Details of BPTLrsquos expansion plan are summarized

below

Table 41 Expansion PlanExpansion Schedule 2009-10 2010-11 2011-12 2012-13 20013-14

GBT

Addition 210 700 1400 2450 3850

Total 210 910 2310 4760 8610

RTT

Addition 90 300 600 1050 1650

Total 90 390 990 2040 3690

48 Proposed Services

As indicated earlier ABC proposes to provide passive telecom infrastructure on a

sharing co-location basis to cellular operators The sites would either be Ground Based

Sites (GBS) or Roof Top Sites (RTS) As the sites are meant for co-location of the active

components of two to three operators they would be built to either 2-Tenant or 3-Tenant

specifications

The different components of the passive infrastructure facility and the related services

that would be offered by BPTL to the operators are as under

Infrastructure provisioning comprising

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 3462

25

Communication tower built to host multiple antennae

Weather-proof communication shelter with air-conditioning and power backup

arrangement

Diesel generating set and battery bank for power backup

A mobile standby generator to act as backup in case o f breakdown

Warehousing facility

Infrastructure operations and maintenance including

Regular operations and maintenance of the facility

Security of all the equipments at the site at all timesA dedicated team of technicians for a group of 40-50 sites to ensure effect ive and

efficient functioning of the components at all times

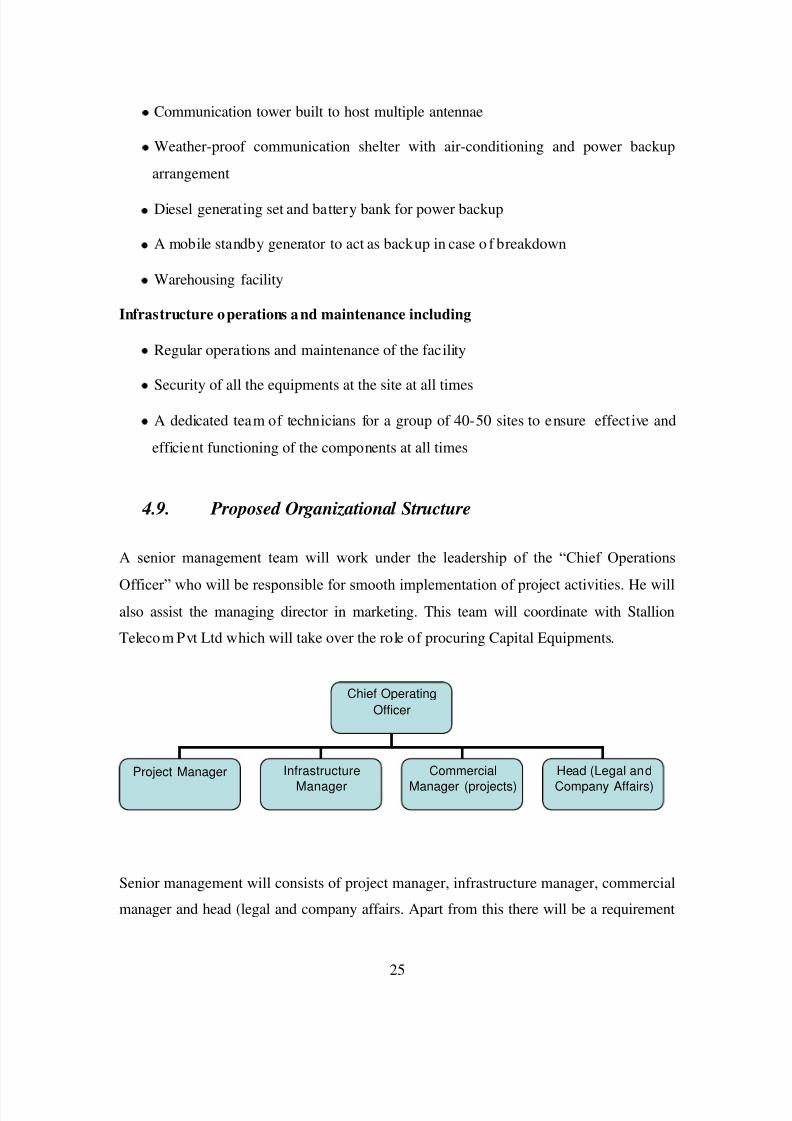

49 Proposed Organizational Structure

A senior management team will work under the leadership of the ldquoChief Operations

Officerrdquo who will be responsible for smooth implementation of proj ect activities He willalso assist the managing director in marketing This team will coordinate with Stallion

Telecom Pvt Ltd which will take over the role of procuring Capital Equipments

Senior management will consists of project manager infrastructure manager commercial

manager and head (legal and company affairs Apart from this there will be a requirement

Chief OperatingOfficer

Project Manager Infrastructure

Manager

Commercial

Manager (projects)

Head (Legal and

Company Affairs)

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 3562

26

of security sentries (3 per GBT site) supervisors (one for every 10 sites) and cluster

manager (one for every 50 sites)

Bharat Telemast will carry out the complete Project execution with the assistance of third party ldquoQuality control organizationrdquo and a third party ldquoProject management teamrdquo

Quality control and project management activities will be o utsourced to a third party

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 3662

27

5 METHODOLOGY

The changing face of infrastructure services creates a complex situation which demands

greater understanding of roles of competition regulatory structures and modes of

financing Knowledge of such things is a key decisive factor in building confidence

among investors promoters and government In project finance the project its assets

contract and cash flows are separated from promoter in order to permit credit appraisal

or loan to the project

As part of the financial feasibility analysis a series of related financial statements based

on projected sources and uses of funds during the development and operating phaseproject were created Financial statements consist of expenses associated with

development activities including capital costs like acquisition of land for GBT sites cost

of tower generator shelter batteries etc Most of the data regarding capital costs are

obtained from the promoter of ABC Limited All these capital costs related details are

provided in annexure 1

Assumption regarding depreciation capital structure operating expenses expansion

schedule tenancy ratios tariff or rent operatorrsquos fees and loan amortization schedule are

obtained from professional accountants Promoter and bankers of ABC Limited

Due to unknown factors that could influence the cost of towers or fees associated with

completing the project (soft costs) contingency costs were estimated at 5 of hard and

soft costs respectively If contingency is set too low developers could easily encounter

funding shortfalls upon slight changes in market forces All other costs were estimated

based on talking with industry professionals (Promoters)

A detailed financial model was prepared based on existing accounting standards and

following financial ratios were estimated

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 3762

28

EBITDA margin Profit and loss accounts for the estimated project period (15

Years) were prepared based on which estimated earnings before interests tax

depreciat ion and amortization were calculated for each year Detailed PampL

balance sheet and cash flow statements are provided in annexure 2 3 and 4

EBITDA = Total Revenue ndash (Variable expenses + Fixed Expenses)

EBITDA margin = EBITDA Total Revenue

PAT margin PAT is calculated by subtracting interests pa id on capital debt and

working capital debt depreciation and applicable corporate income tax from

EBITDA

PAT = EBITDA ndash Interest Payable ndash Depreciation ndash Income tax

PAT margin = PATTotal Revenue

Working Capital Working capital requirement is calculated by subtract ing

current liabilities from current assets Current assets are estimated based on 30

days cash requirement and current liabilities are estimated as half of salary

monthly expenses

WC = Current Assets ndash Current Liabilities

UFCF It is defined as the free cash flows available to the firm if the firm has

zero debt liability Purpose of ca lculat ing UFCF for project period is to determinethe project IRR

UFCF = PAT + Depreciation + Interest (tax adjusted) + Release of WC + Salvage

value of the assets ndash CAPEX ndash Change in WC

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 3862

29

LCFF It is defined as the cash floes available to the firm after paying interests on

long term and short term debts

LCFF = UFCF ndash Interest (tax adjusted)

FCFE It is defined as the free cash flow available to equity holders It is

determined to ca lculate equity IRR for equity investors It also includes the tax

benefits which are available as per the Income Tax Act

FCFE PAT + Depreciation + Salvage Value ndash Equity Investment ndash Long term debt

repayment

PIRR Project IRR is defined as the discount rate at which NPV (Net Present

Value) of UFCF is zero It is calculated by using following formula

UFCF 1 (1+PIRR) 0+ UFCF 2 (1+PIRR) 1+ UFCF 3 (1+PIRR) 2+ helliphelliphelliphelliphelliphellip = 0

UFCF 1 = UFCF at the end of first year of operation

UFCF 2 = UFCF at the end of second year of operation

PIRR = Project IRR

EIRR Equity IRR is defined as the discount rate at which NPV of FCFE is zero

It is calculated by using following formula

FCFE1 (1+EIRR) 0+ FCFE 2 (1+EIRR) 1+ FCFE 3 (1+EIRR) 2+ helliphelliphelliphelliphelliphellip = 0

FCFE1 = FCFE at the end of first year of operation

FCFE2 = FCFE at the end of seco nd year of operation

EIRR = Equity IRR

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 3962

30

WACC It is de fined as the percentage of return expected by the investors who

otherwise would have earned some return by investing in some other project

WACC = Cost of Debt (Debt Capital) + Cost of equity (Equity Capital)

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 4062

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 4162

32

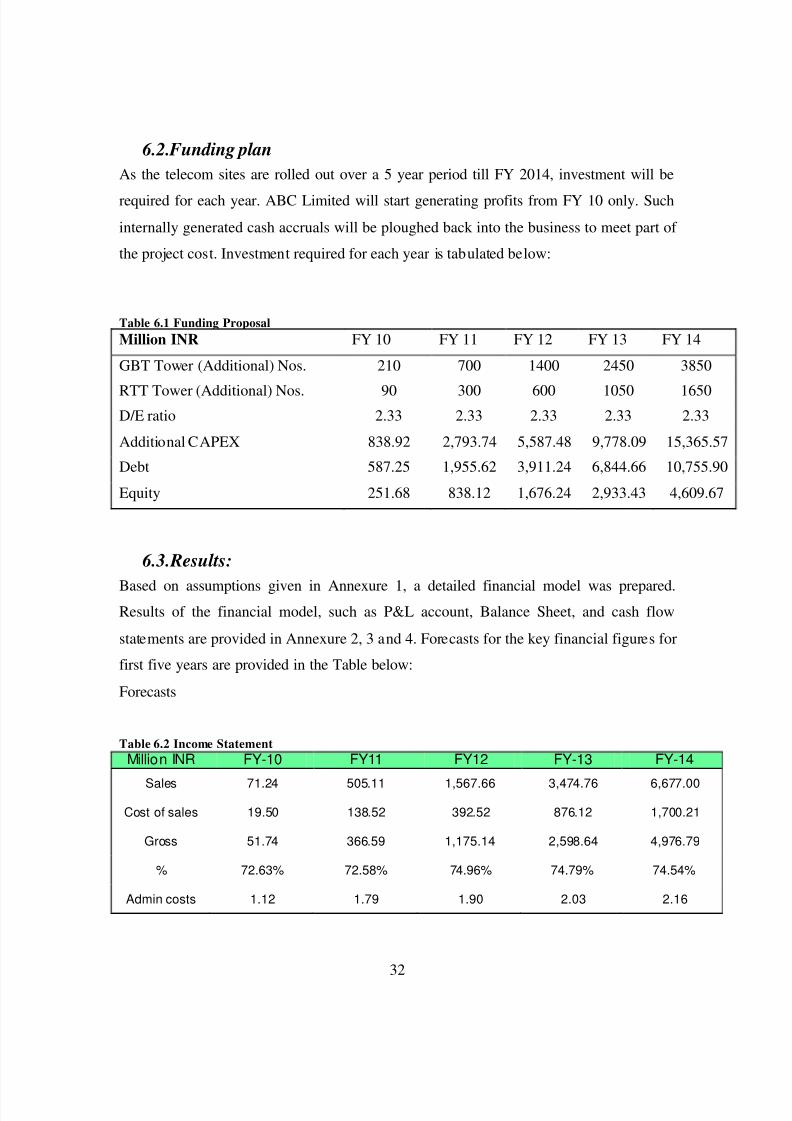

62 Funding planAs the telecom sites are rolled out over a 5 year period till FY 2014 investment will be

required for each year ABC Limited will start generating profits from FY 10 only Such

internally generated cash accruals will be ploughed back into the business to meet part of

the project cost Investment required for each year is tabulated below

Table 61 Funding ProposalMillion INR FY 10 FY 11 FY 12 FY 13 FY 14

GBT Tower (Additional) Nos 210 700 1400 2450 3850

RTT Tower (Additional) Nos 90 300 600 1050 1650DE ratio 233 233 233 233 233

Additional CAPEX 83892 279374 558748 977809 1536557

Debt 58725 195562 391124 684466 1075590

Equity 25168 83812 167624 293343 460967

63 Results

Based on assumptions given in Annexure 1 a detailed financial model was preparedResults of the financial model such as PampL account Balance Sheet and cash flow

statements are provided in Annexure 2 3 and 4 Forecasts for the key financial figures for

first five years are provided in the Table below

Forecasts

Table 62 Income StatementMillion INR FY-10 FY11 FY12 FY-13 FY-14

Sales 7124 50511 156766 347476 667700

Cost of sales 1950 13852 39252 87612 170021

Gross 5174 36659 117514 259864 497679

7263 7258 7496 7479 7454

Admin costs 112 179 190 203 216

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 4262

33

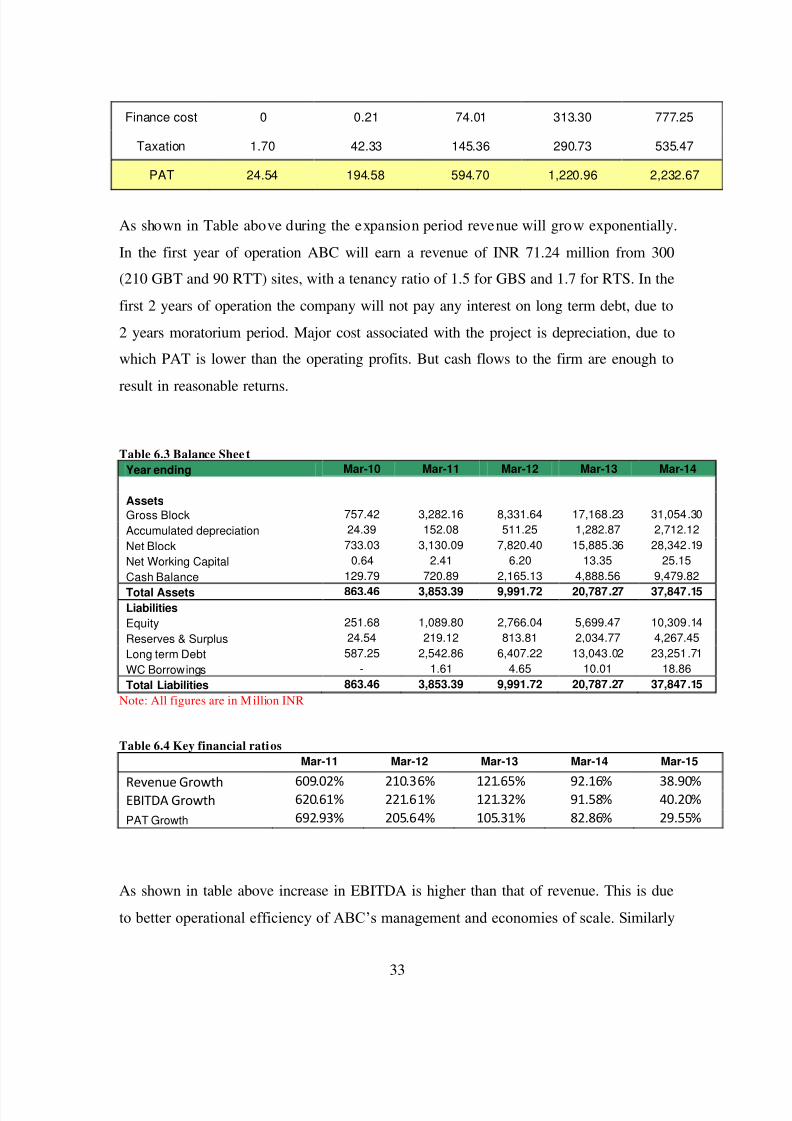

Finance cost 0 021 7401 31330 77725

Taxation 170 4233 14536 29073 53547

PAT 2454 19458 59470 122096 223267

As shown in Table above during the expansion period revenue will grow exponentially

In the first year of operation ABC will earn a revenue of INR 7124 million from 300

(210 GBT and 90 RTT) sites with a tenancy ratio of 15 for GBS and 17 for RTS In the

first 2 years of operation the company will not pay any interest on long term debt due to

2 years moratorium period Major cost associated with the project is depreciation due to

which PAT is lower than the operating profits But cash flows to the firm are enough to

result in reasonable returns

Table 63 Balance Shee tYear ending Mar-10 Mar-11 Mar-12 Mar-13 Mar-14

AssetsGross Block 75742 328216 833164 1716823 3105430Accumulated depreciation 2439 15208 51125 128287 271212Net Block 73303 313009 782040 1588536 2834219Net Working Capital 064 241 620 1335 2515Cash Balance 12979 72089 216513 488856 947982

Total Assets 86346 385339 999172 2078727 3784715LiabilitiesEquity 25168 108980 276604 569947 1030914Reserves amp Surplus 2454 21912 81381 203477 426745Long term Debt 58725 254286 640722 1304302 2325171WC Borrowings - 161 465 1001 1886Total Liabilities 86346 385339 999172 2078727 3784715

Note All figures are in Million INR

Table 64 Key financial ratiosMar-11 Mar-12 Mar-13 Mar-14 Mar-15

Revenue Growth 60902 21036 12165 9216 3890EBITDA Growth 62061 22161 12132 9158 4020

PAT Growth 69293 20564 10531 8286 2955

As shown in table above increase in EBITDA is higher than that of revenue This is due

to better operational efficiency of ABCrsquos management and economies of scale S imilarly

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 4362

34

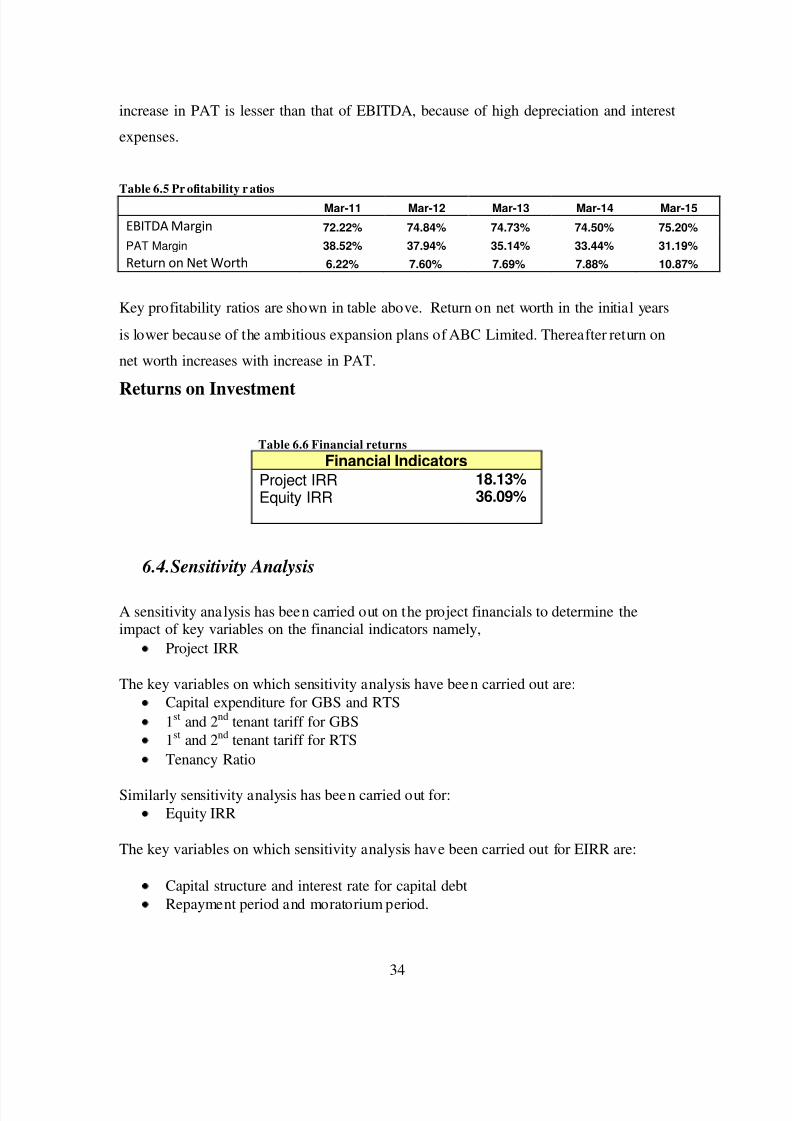

increase in PAT is lesser than that of EBITDA because of high depreciation and interest

expenses

Table 65 Pr ofitability r atios

Mar-11 Mar-12 Mar-13 Mar-14 Mar-15

EBITDA Margin 7222 7484 7473 7450 7520

PAT Margin 3852 3794 3514 3344 3119Return on Net Worth 622 760 769 788 1087

Key profitability ratios are shown in table above Return on net worth in the initial years

is lower because of the ambitious expansion plans of ABC Limited Thereafter return on

net worth increases with increase in PAT

Returns on Investment

Table 66 Financial returnsFinancial Indicators

Project IRR 1813Equity IRR 3609

64 Sensitivity Analysis

A sensitivity analysis has been carried out on the project financials to determine theimpact of key variables on the financial indicators namely

Project IRR

The key variables on which sensitivity analysis have been carried out areCapital expenditure for GBS and RTS1st and 2 nd tenant tariff for GBS1st and 2 nd tenant tariff for RTSTenancy Ratio

Similarly sensitivity analysis has been carried out forEquity IRR

The key variables on which sensitivity analysis have been carried out for EIRR are

Capital structure and interest rate for capital debtRepayment period and moratorium period

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 4462

35

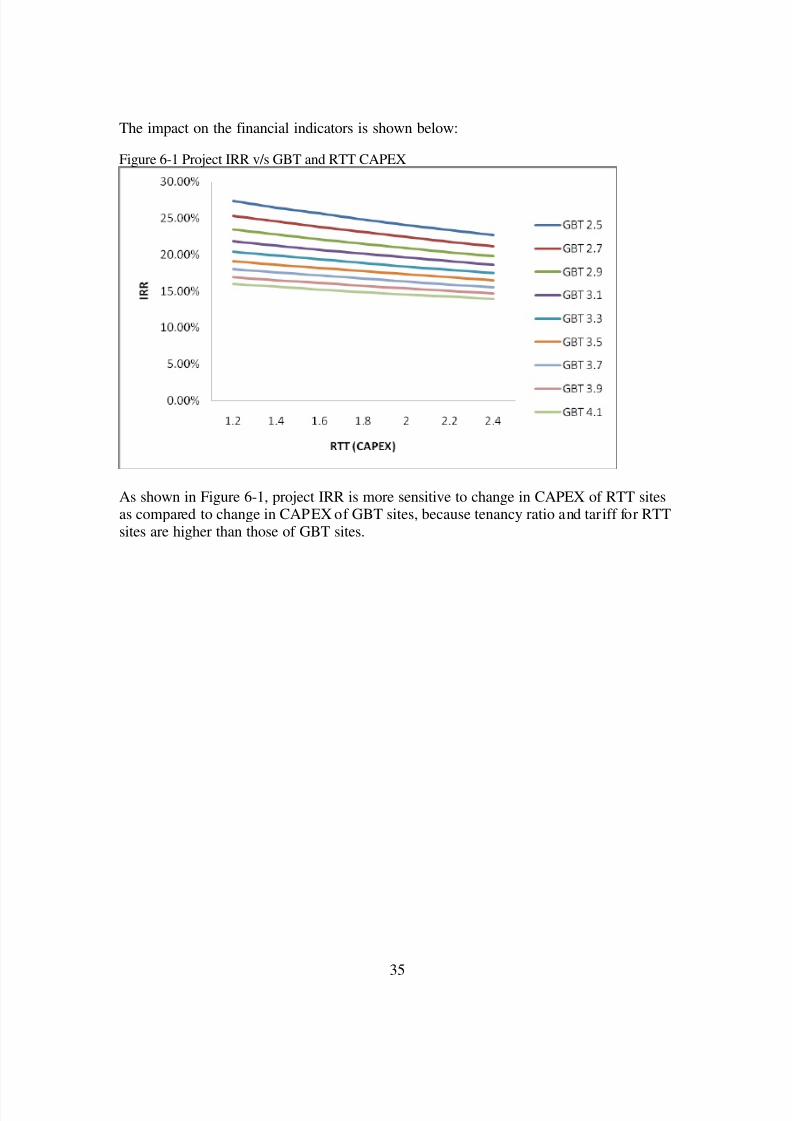

The impact on the financial indicators is shown below

Figure 6-1 Project IRR vs GBT and RTT CAPEX

As shown in Figure 6-1 project IRR is more sensitive to change in CAPEX of RTT sitesas compared to change in CAPEX of GBT sites because tenancy ratio and tariff for RTTsites are higher than those of GBT sites

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 4562

36

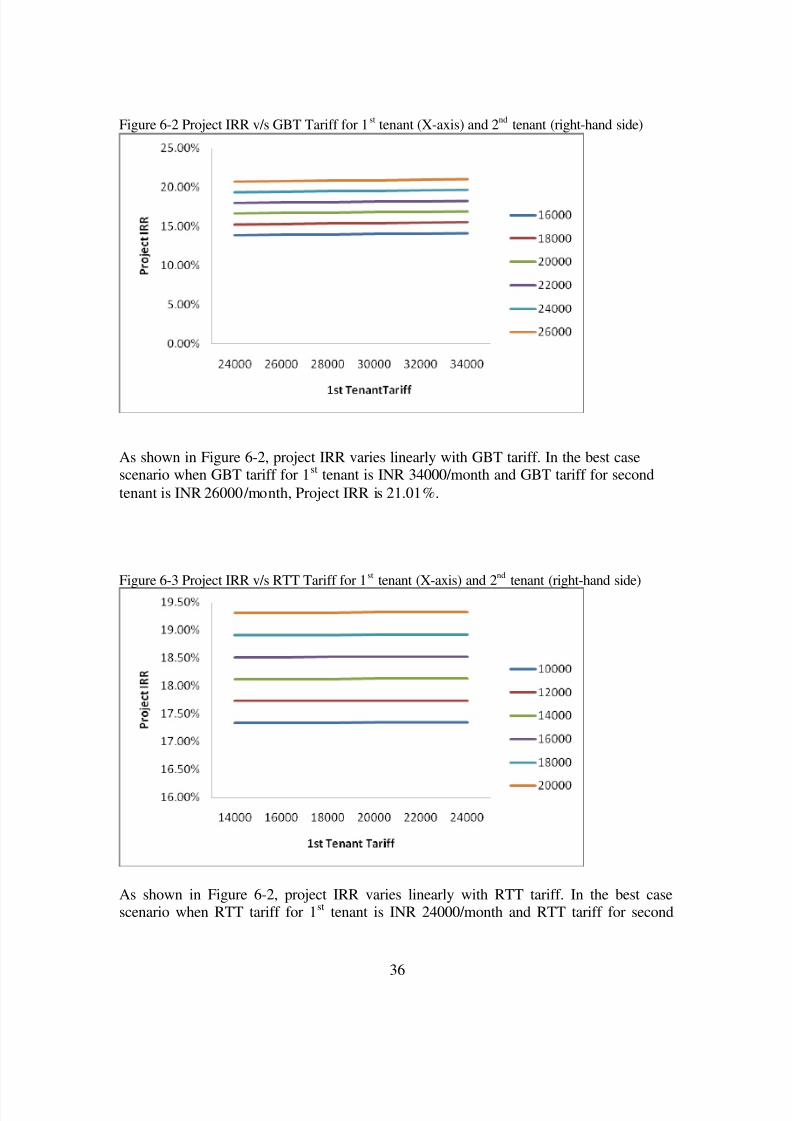

Figure 6-2 Project IRR vs GBT Tariff for 1 st tenant (X-axis) and 2 nd tenant (right-hand side)

As shown in Figure 6-2 project IRR varies linearly with GBT tariff In the best casescenario when GBT tariff for 1 st tenant is INR 34000month and GBT tariff for secondtenant is INR 26000month Project IRR is 2101

Figure 6-3 Project IRR vs RTT Tariff for 1 st tenant (X-axis) and 2 nd tenant (right-hand side)

As shown in Figure 6-2 project IRR varies linearly with RTT tariff In the best casescenario when RTT tariff for 1 st tenant is INR 24000month and RTT tariff for second

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 4662

37

tenant is INR 20000month Project IRR is 1932 Project IRR is more sensitivetowards RTT tariff than GBT tariff because in practical business situation RTT siteshave a tenancy ratio of more than two due to which effect of tariff for 1 st tenant almostget nullified after few years

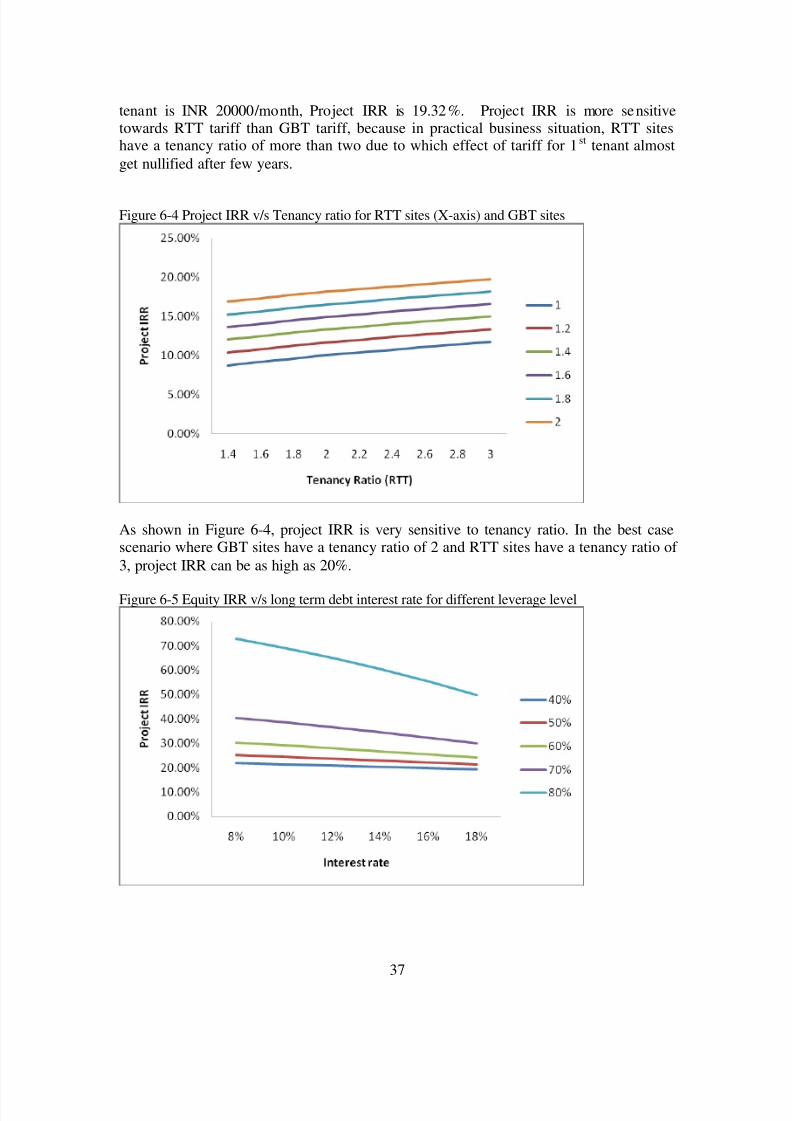

Figure 6-4 Project IRR vs Tenancy ratio for RTT sites (X-axis) and GBT sites

As shown in Figure 6-4 project IRR is very sensitive to tenancy ratio In the best casescenario where GBT sites have a tenancy ratio of 2 and RTT sites have a tenancy ratio of 3 project IRR can be as high as 20

Figure 6-5 Equity IRR vs long term debt interest rate for different leverage level

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 4762

38

As shown in figure 6-5 equity IRR is more sensitive to interest rate on long term debt forhigh level of leverage (lower debt equity ratio) because as the debt equity ratio increasesinterest paid on long term debt also increases significantly

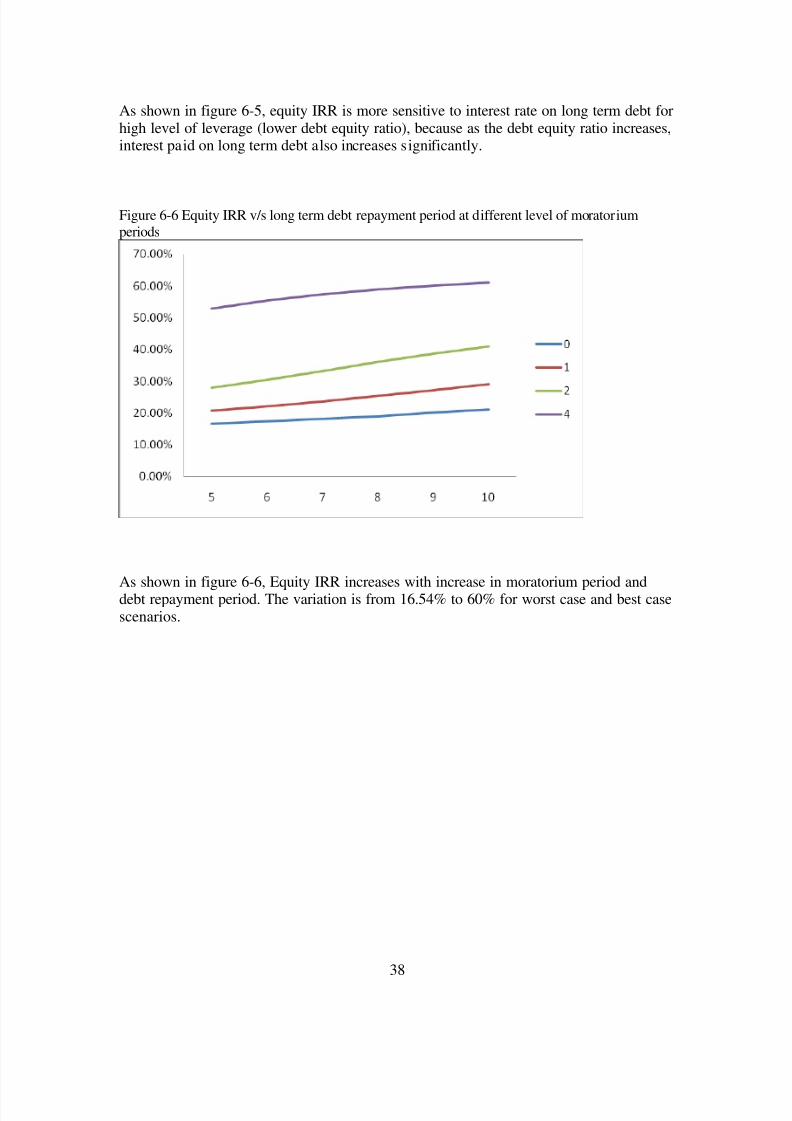

Figure 6-6 Equity IRR vs long term debt repayment period at different level of moratoriumperiods

As shown in figure 6-6 Equity IRR increases with increase in moratorium period anddebt repayment period The variation is from 1654 to 60 for worst case and best casescenarios

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 4862

39

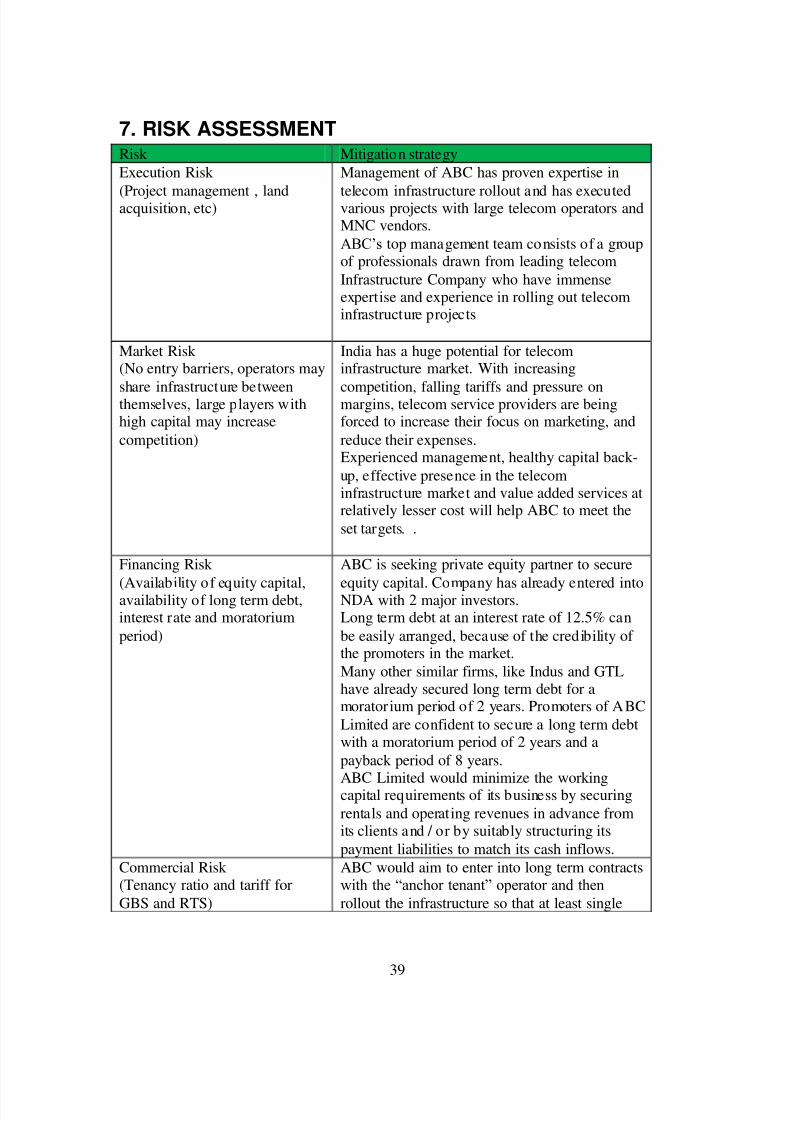

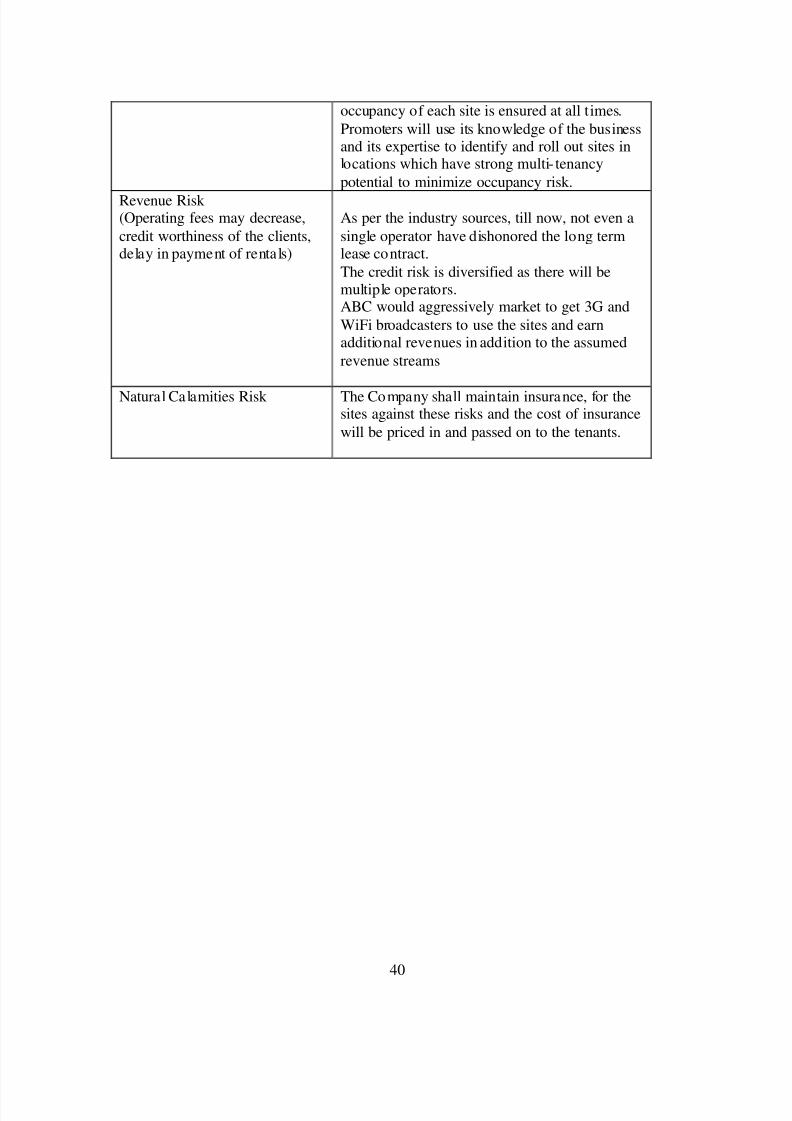

7 RISK ASSESSMENTRisk Mitigation strategyExecution Risk

(Project management landacquisition etc)

Management of ABC has proven expertise in

telecom infrastructure rollout and has executedvarious projects with large telecom operators andMNC vendorsABCrsquos top management team consists of a groupof professionals drawn from leading telecomInfrastructure Company who have immenseexpertise and experience in rolling out telecominfrastructure projects

Market Risk (No entry barriers operators may

share infrastructure betweenthemselves large players withhigh capital may increasecompetition)

India has a huge potential for telecominfrastructure market With increasing

competition falling tariffs and pressure onmargins telecom service providers are beingforced to increase their focus on marketing andreduce their expensesExperienced management healthy capital back-up effective presence in the telecominfrastructure market and value added services atrelatively lesser cost will help ABC to meet theset targets

Financing Risk

(Availability of equity capitalavailability of long term debtinterest rate and moratoriumperiod)

ABC is seeking private equity partner to secure

equity capital Company has already entered intoNDA with 2 major investorsLong term debt at an interest rate of 125 canbe easily arranged because of the credibility of the promoters in the marketMany other similar firms like Indus and GTLhave already secured long term debt for amoratorium period of 2 years Promoters of ABCLimited are confident to secure a long term debtwith a moratorium period of 2 years and apayback period of 8 years

ABC Limited would minimize the workingcapital requirements of its business by securingrentals and operating revenues in advance fromits clients and or by suitably structuring itspayment liabilities to match its cash inflows

Commercial Risk (Tenancy ratio and tariff forGBS and RTS)

ABC would aim to enter into long term contractswith the ldquoanchor tenantrdquo operator and thenrollout the infrastructure so that at least single

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 4962

40

occupancy of each site is ensured at all t imesPromoters will use its knowledge of the businessand its expertise to identify and roll out sites inlocations which have strong multi- tenancypotential to minimize occupancy risk

Revenue Risk (Operating fees may decreasecredit worthiness of the clientsdelay in payment of rentals)

As per the industry sources till now not even asingle operator have dishonored the long termlease contractThe credit risk is diversified as there will bemultiple operatorsABC would aggressively market to get 3G andWiFi broadcasters to use the sites and earnadditional revenues in addition to the assumedrevenue streams

Natural Calamities Risk The Company shall maintain insurance for thesites against these risks and the cost of insurancewill be priced in and passed on to the tenants

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 5062

41

8 CONCLUSION

India is the fastest growing wireless telecom market in the world The continuing

growth in the number of wireless subscribers and MoUs and increasing trend of

outsourcing of business processes to India has led to growing demand for large

investments in the telecom infrastructure in the country

However with increasing competition falling tariffs and pressure on margins

telecom service providers are being forced to increase their focus on marketing

customer acquisitions and branding and minimize their efforts and overheads in

project management and asset acquisition

Further with rising prices of steel cement and real estate the cost of developing

and owning passive infrastructure is increasingly becoming a costly proposition

for most operators and service providers

The compulsion on the part of service providers to reduce their operating costs

and capital expenditure requirements has led to opportunities in passiveinfrastructure outsourcing to independent third party infrastructure providers and

also sharing the infrastructure with other service providers It is expected that

cellular operators will outsource their communications site infrastructure needs as

a means of accelerating access to their markets and preserving capital rather than

constructing and operating their own communications sites and maintaining their

own communications sites service and deve lopment capabilities

Passive infrastructure is highly capital intensive and an integral part of the cellular

service providersrsquo networks Yet being a simple and low technology asset it is

amenable to outsourcing and sharing By transferring the responsibility of

ownership development and maintenance of passive infrastructure service

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 5162

42

providers have an opportunity to transfer a substantial part of their business risk to

third parties

Most telecom operators are facing capacity constraints on their networksCoverage obligations increasing pressure to improve network quality and

competition has led to aggressive roll out plans by existing cellular operators

Installation of cell sites has become a cumbersome process as there are a number

of clearances required and involves labor-intensive micro management

Availability of ready infrastructure from third party providers would enable the

operators to reduce their time to market and accelerate their access to their

customers Cellular service providers generally want to move quickly when

adding more sites and co-location on an existing site is always faster than

building

Ownership and maintenance of telecom towers and other infrastructure by third

parties is an established practice in developed nations like USA and is

increasingly gaining market acceptance in India

The Indian government is seriously considering promoting the infrastructure

sharing route between the telecom operator and private players to achieve future

national tele-density targets and improve rural telecom penetration

ABC being an independent entity with no business conflicts with other service

providers in the telecom space will be best positioned and have an early mover

advantage to capitalize on this emerging opportunity

Further the task of operating and maintaining the passive infrastructure in the cell

is increasingly becoming a cumbersome exercise for the service providers to

handle ABCrsquos composite offering to build passive infrastructure for the cellular

operators and also operate and maintain them will provide a turnkey solution to

address the infrastructure needs of the service providers

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 5262

43

The business model proposed to be followed by ABC is fairly simple with stable

and predictable cash flows as is the case with the business model of the tower

renting companies in USA Most contracts are long term for a period 10 or moreyears with annual price escalators generally ranging from 3 to 4 However

wireless carriers normally tend to renew rentals because suitable alternative sites

may not exist or be available and repositioning a site in a carrierrsquos network is

expensive and may adverse ly affect network quality

Site ownership and operations is a ldquoscalerdquo business operating administration

marketing expenses etc do not rise as quickly as revenues when portfolios are

expanded Incremental operating costs associated with adding wireless tenants to

a communications site are minimal Therefore as additional tenants are added to a

site the substantial majority of incremental revenue contributes to margin

expansion Most tower companies have high EBITDA margins as may be seen

from the financial indicators of some of the tower rental companies in USA

It is expected that site location and capacity price and quality of service and

successful execution of contracts will be the most significant competitive factors

in this business

ABCrsquos revenue and returns on investment will be primarily driven by its ability

to

o Increase the utilization of the space and infrastructure capacity owned by it by

increasing the number of tenants per site and renting out to maximum number

of users As discussed above return on capital employed (PIRR and EIRR) arevery sensitive to tenancy ratio In worst case scenario project IRR can be as

low as 8 and in the best case scenario it can be as high as 20

o Develop acquire sites of strategic importance and high growth potential that

will enable them to secure better commercial terms from users and attract

more number of tenants Infrastructure provisioning fees rentals for sites are

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 5362

44

extremely location sensitive There is a potential to acquire more land than

that of required to capitalize on the increase in real estate prices

o Develop sites in a cost effective manner ABC would consider purchasing

land only for those GBS sites which have sufficient demand and arestrategically located Else for most of its sites land will be leasehold As

shown above returns (PIRR and EIRR) are very sensitive to capital costs In

the worst case scenario project IRR can be as low as 15 whereas it can as

high as 27 in the best case scenario

o Negotiate and secure long term contracts with good credit quality users with

built in price escalation provisions to mitigate financing risk

o Leverage and secure long term financing at attractive terms and involve in

active treasury management to keep low financing cost Results of the

sensitivity analysis indicate that equity IRR can be as high as 60 foe a

moratorium period of 4 years and interest rate of 10

o Minimize working capital requirements

o Maintain low operating and administration expense

o Secure better OampM margins from operators and retain a healthy share of it in

ABC

o Maintain high service standards and build strong customer relationships

The business would have the potential to capture new revenue opportunities

around the existing assets As demand for towers is expected to grow and as

operators migrate to speedier next-generation wireless technologies they will

need the towers and associated passive infrastructure to transmit their new

services in addition to their existing offerings In addition to increasing capacity

and coverage and improving the quality of their networks cellular serviceproviders are deploying high speed data networks driving incremental demand of

sites The business therefore has potential upsides in the form of adding

customers (tenants) in wireless broadband third generation (ldquo3Grdquo) and wireless

data capabilities and also other incremental value propositions by way of hosting

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 5462

45

Billboards Hoardings etc in some of the high visible sites owned and maintained

by it

Based on the assumptions and subject to satisfactory resolution of the key risks

factors project cash flows will be able to meet debt service obligations

This business model is a lucrative investment option for a private equity player

because valuation of each site will increase in the coming years due to

improvement in market conditions increase in the value of land and increase in

the demand for passive infrastructure in rural and semi-urban areas

882019 Major Project (Ramit)

httpslidepdfcomreaderfullmajor-project-ramit 5562

46

REFERENCESAnjan G V A amp N M (2009) telecom infrastructure industry in india GurgaonICRA

Bessler W Norsworthy J amp Shusterman T (2001 12 1) Mergers in the UStelecommunications industry and market valuationeffects IEEE p 288

COAI (2009 march 14) Subscriber Figures Retrieved march 14 2009 fromCOAIcom httpwwwcoaicomstatisticsphp

IDA (2009 march 23) Highlights Retrieved march 23 2009 from idagovsghttpwwwidagovsghomeindexaspx

K R (2008) Time for new business model Delhi Cybermedia

MAXIS (2009 march 8) the malaysian telecommunications industry Retrieved march9 2009 from maxiscommyhttpwwwmaxiscommypersonalabout_usinvestorprospectusprospectus4pdf

P J amp Lisa A (2009) Stimulas spending and American Telecom Industry USACoracle group