MAIB Scheme Update - Actuaries Institute · MAIB Scheme Update . Christopher Hill– Chief...

39

MAIB Scheme Update Christopher Hill– Chief Operating Officer Motor Accidents Insurance Board

Transcript of MAIB Scheme Update - Actuaries Institute · MAIB Scheme Update . Christopher Hill– Chief...

MAIB Scheme Update

Christopher Hill– Chief Operating Officer Motor Accidents Insurance Board

History • MAIB came into existence on 1 December 1974 . The

second “no fault” CTP scheme in Australia ( just behind the Victorian MAB- now TAC)

• Long Term care benefits

• introduced in May 1991 • unlimited reasonable treatment and care , for those

requiring more than 2 hours care per day.

Scheme Features

Compensation under scheme • Statutory Benefits ( no fault), and • Common Law damages.

Statutory Benefits • medical and hospital expenses , • rehabilitation, • attendant care costs , • death benefits, and • disability allowance ( 80% coverage of lost earnings – up to a

time limit)

Scheme Features

Statutory Benefits cont. • Statutory limit of $400,000 • Exclusions for “No Fault” claims

• Drivers of unregistered vehicles • Reductions in Disability Allowance for DUI • Various serious offences involving a Motor Vehicle • Some off-road ( unregistered) vehicles • Motor Racing

• Inclusions • Driving or riding anywhere - not just on a Public Road

(relates to Common Law and Statutory Benefits) • No Material changes to legislation over last 2 years

Scheme Features

Scheme Features Common Law

• Unlimited access to Common Law (no thresholds) Limits to Common Law damages – • No interest on past losses • Civil Liability Act 2002

• General Damages – minor restrictions on small claims, • Economic Loss - 3 x AWE, • No Gratuitous Care, • 5% discount rate, • 25% presumed con. neg. for intoxication.

• Motor Accidents(Liabilities and Compensation) Act 1973

• Statutory reduction for failure to wear a seat belt.

Scheme Features

Premiums • Regulated pricing – review every 4 years by Office of the

Tasmanian Economic Regulator (OTTER)- formerly Government Prices Oversight Commission (GPOC).

• Based on recommendations – Premiums Order is made

specifying premium rates for vehicle classes and maximum yearly increases.

• Last review 2009 – in the middle of GFC. • Only one CPI increase in last 6 years.

Scheme Features

Key Risks • Investments markets – volatility

• Government Policy / Regulatory Changes – NDIS/NIIS • Fair Work Australia gender equity wage case – Attendant

Care costs • Plaintiff Lawyer advertising ( developing risk) – Pressure

on Common Law Damages

Financial Position

MAIB strives to maintain a balance between- • premium and investment income, • the cost of claims (including a prudential margin), and • the requirement to achieve a sustainable commercial

rate of return that maximises value for the State.

Financial Position

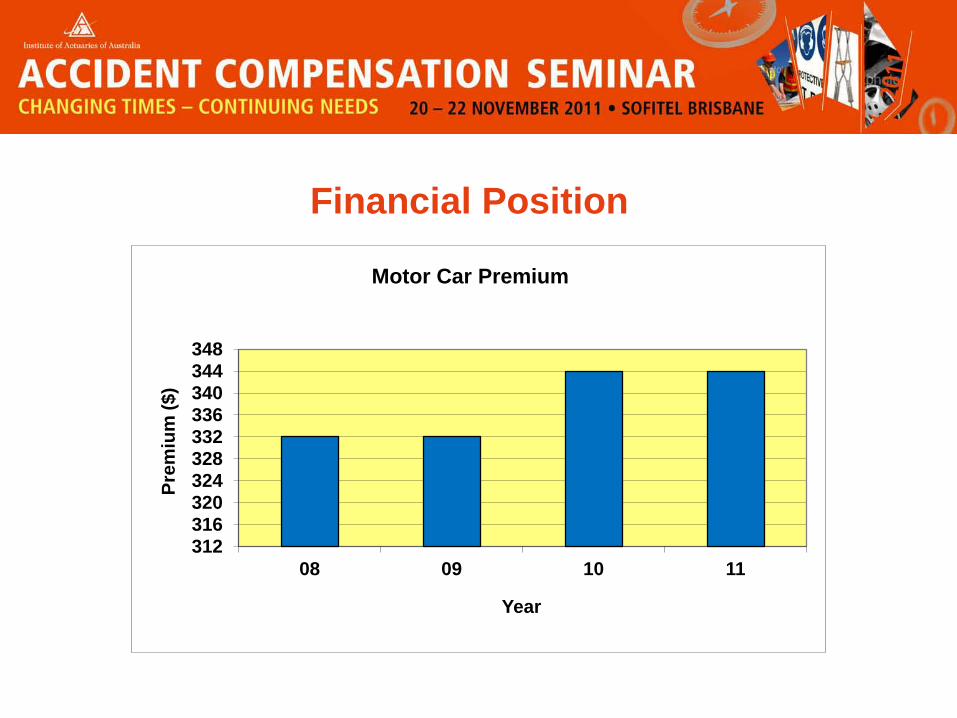

312 316 320 324 328 332 336 340 344 348

08 09 10 11

Prem

ium

($)

Year

Motor Car Premium

Financial Position

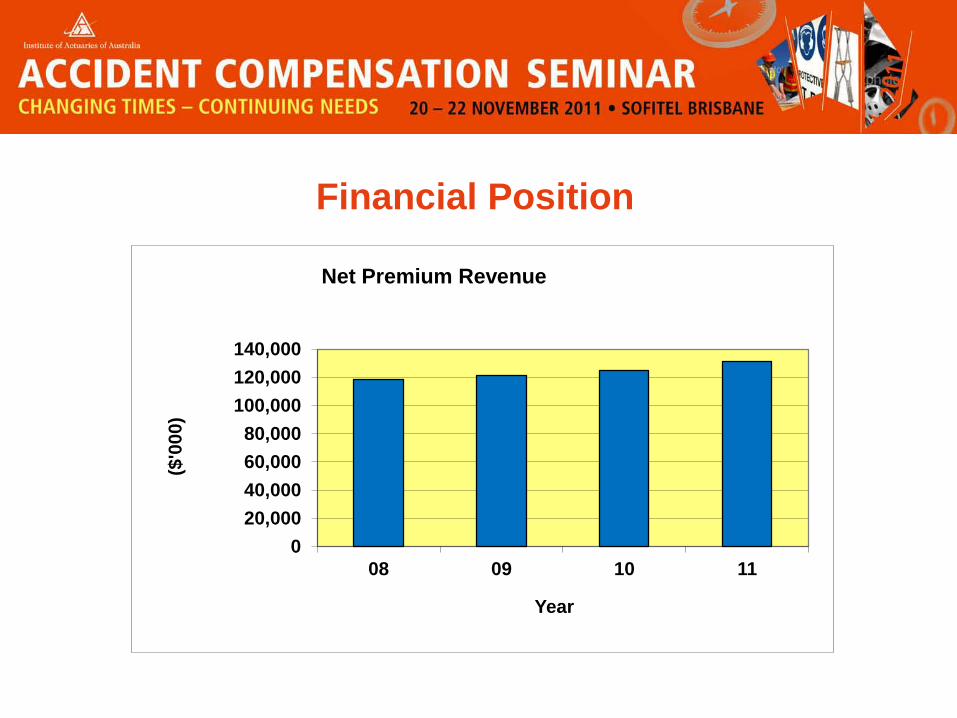

0 20,000 40,000 60,000 80,000

100,000 120,000 140,000

08 09 10 11

($'0

00)

Year

Net Premium Revenue

Financial Position

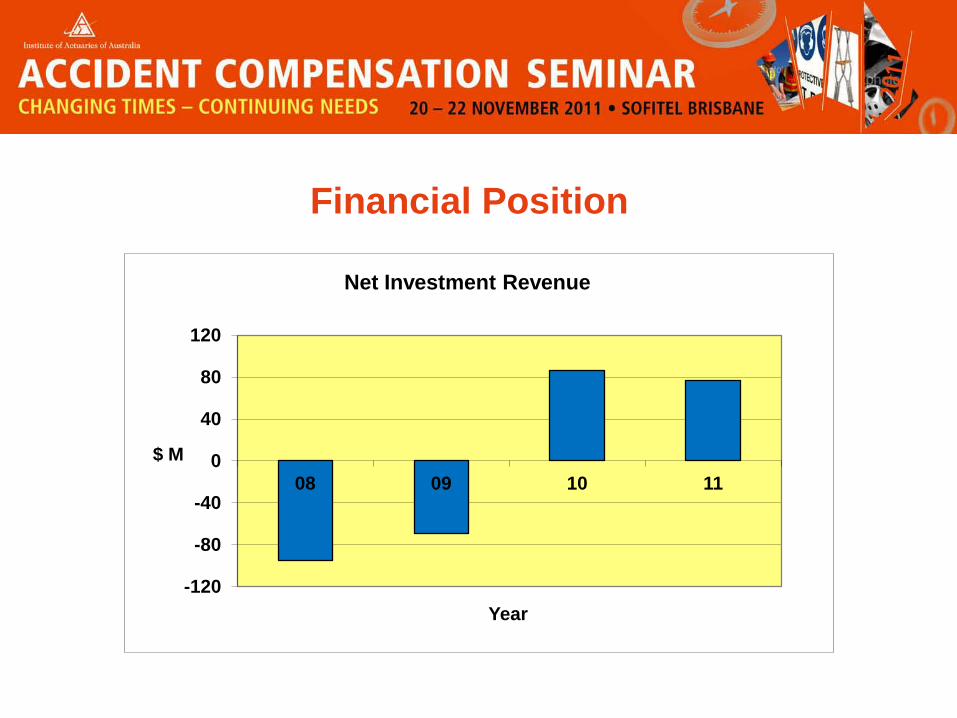

-120

-80

-40

0

40

80

120

08 09 10 11 $ M

Year

Net Investment Revenue

Financial Position

-15

-10

-5

0

5

10

15

08 09 10 11 %

Year

Investment Return

Financial Position

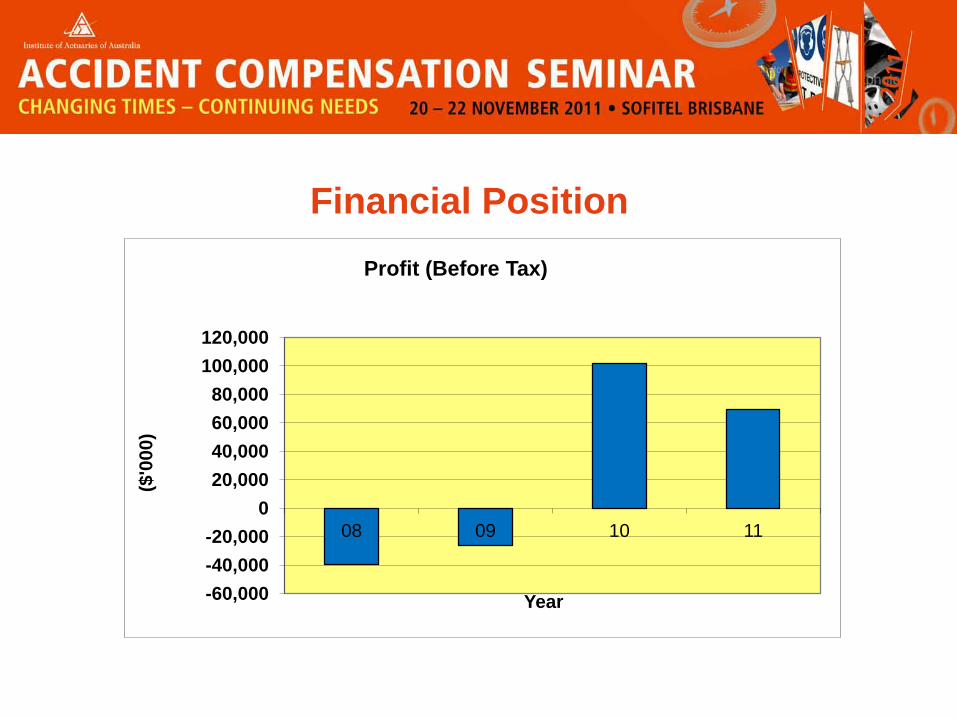

-60,000 -40,000 -20,000

0 20,000 40,000 60,000 80,000

100,000 120,000

08 09 10 11

($'0

00)

Year

Profit (Before Tax)

Financial Position

0

20

40

60

80

100

08 09 10 11

$ M

Year

Tax/Dividend Paid (Cash Basis)

Financial Position

600

640

680

720

760

08 09 10 11

$ M

Year

Net Claim Liabilities

MAIB not regulated by the Australian Prudential Regulatory Authority (APRA) APRA minimum capital requirement standards for insurers do not apply to MAIB. Solvency calculated by dividing outstanding claims liabilities by net assets (including a prudential margin of 20%) Set target solvency in the range 20% - 25% Apart from 2009 ( GFC) MAIB has maintained its solvency within target range over last 6 years

Financial Position - Solvency

Financial Position - Solvency

0.0 5.0

10.0 15.0 20.0 25.0 30.0 35.0

06 07 08 09 10 11

%

Year

Solvency Level

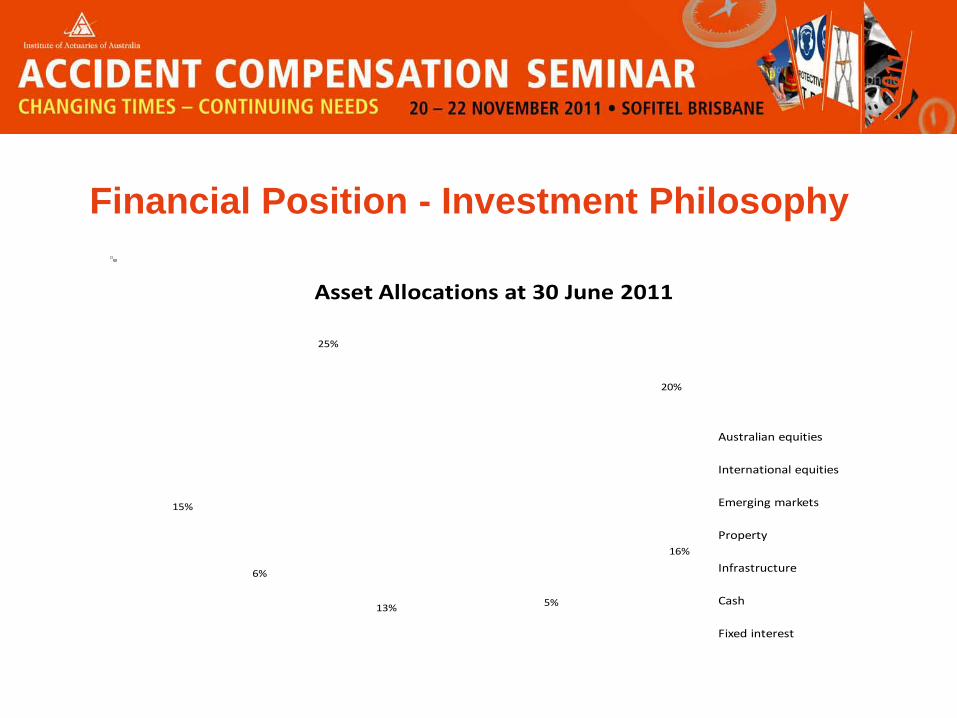

• Ensure investments achieve long-term real growth to maintain

an acceptable level of solvency.

• 35% / 65% defensive / growth asset split

• Increased average return but with increased volatility

• Diversified portfolio- • nine (9) different classes, • both in Australia and overseas, • nineteen (19) Fund Managers

Financial Position – Investment Philosophy

Financial Position - Investment Philosophy

20%

16%

5%13%

6%

15%

25%

Asset Allocations at 30 June 2011

Australian equities

International equities

Emerging markets

Property

Infrastructure

Cash

Fixed interest

Claims Management

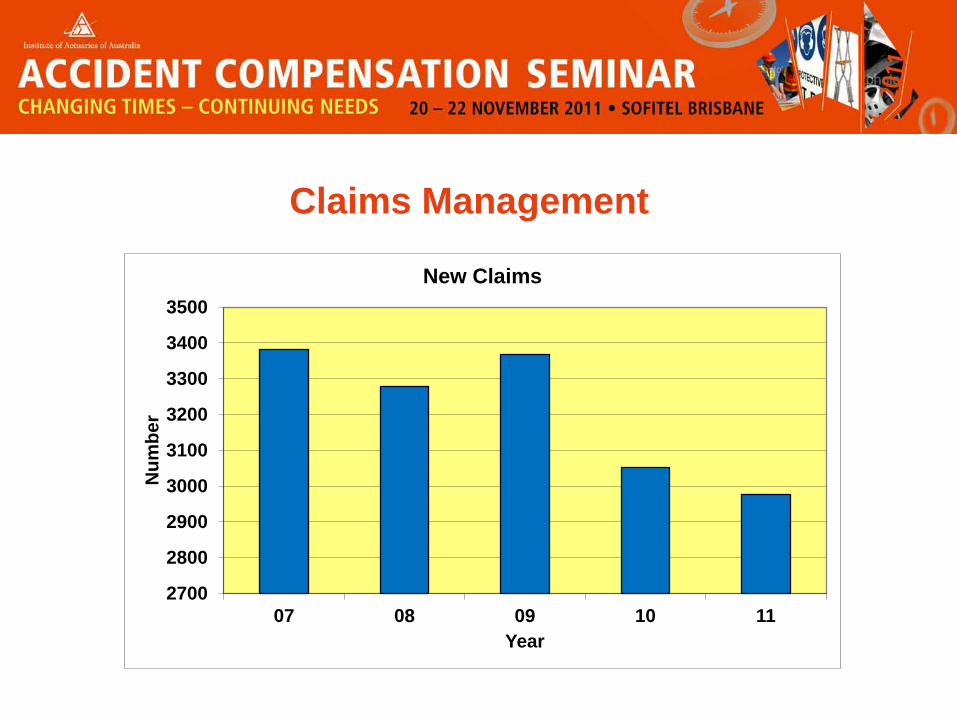

Claims • Claim numbers continue to drop-

• Yearly claim numbers at record low • Open claims count at near record low

• Statutory Benefits payments stable • Common Law Damages payments stable-

• Common Law claim numbers dropping • Average claims cost increasing • No superimposed inflationary pressures

• Approx 2% per annum increase in registered motor vehicles

Claims Management

2700

2800

2900

3000

3100

3200

3300

3400

3500

07 08 09 10 11

Num

ber

Year

New Claims

Claims Management

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

05 06 07 08 09 10 11

Num

ber

Year

Open Claims

Claims Management

0 1 2 3 4 5 6 7 8

08 09 10 11

No.

of C

laim

s pe

r 1,0

00 V

ehic

les

Year

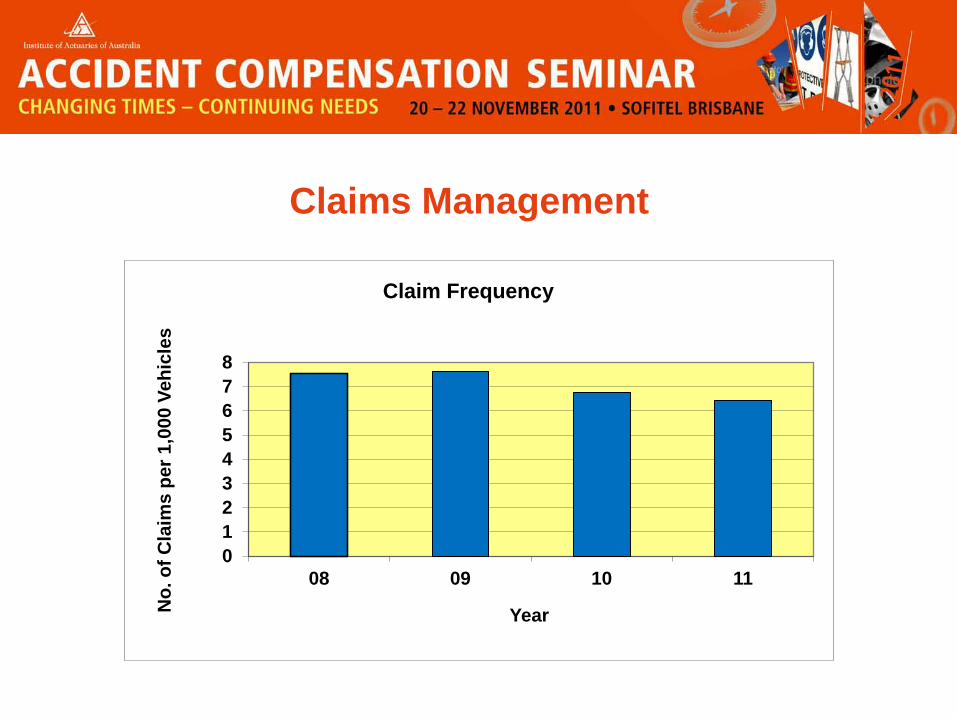

Claim Frequency

Claims Management

62

64

66

68

70

72

74

76

78

80

82

06/07 07/08 08/09 09/10 10/11

$M

Financial Year

Claim Payments

Paid

Claims Management

• Existence of both Statutory Benefits and Common Law assists in managing claimant rehabilitation.

• Outcome- • Need to bring Common Law claims is reduced; • Claimant “loss” reduced through early rehabilitation; • Already compensated for majority of loss.

• Long term care –

• Awards for significant injuries are not high (reduces ambitious claims by lawyers)

• Threshold of 2 hours care per day is easily identified.

Claims Management

Early claims reporting by – • Hospitals • Media ( newspapers) • Police • Injured Claimants Easy access to claim forms – • Hospitals • Service Tasmania centres • Online Early intervention and relationship building

Claims Management

Prompt Claims Management • Applications for benefits processed on day of

receipt

Robust assessment of entitlements • Eligibility criteria must be met • IT system flags caps and limits

Regular claims reviews • Peer review of all claims

Claims Management

Specialist services outsourced

• Specialist Facilities Manager and Attendant Care provider engaged;

• Separate panels for • Legal; • Rehabilitation; and • Investigations.

• Service level agreements in place to ensure quality and consistency of service

Daily Care

Segregated management of daily care claims • includes potential daily care claims, and • children with head injuries

Small caseloads • caseloads of approx. 50 claims

Daily Care

Reserves • Reviewed at least annually • Actuarial valuation based on individual claims Standardised support needs assessments of injury related care and support was introduced early 2010 Purpose built care facilities and housing in Hobart, Launceston and the North West Tasmania.

Daily Care - Support Needs Assessment

• Support Needs Assessments panel introduced in February 2010.

• The main aims in establishing SNA's were to introduce:

• A standard assessment tool for the provision of consistency in reporting;

• Evidence based assessments; • Clear support program hours, objectives and goals, • Provides specific data for reporting into the future.

• Successful first 12 months.

• Adoption by Panel Providers in their broader work

Accident Prevention

• Sponsorship of the Road Safety Advisory Council (formerly Road Safety Task Force) since 1996

• Motorcycle Safety Strategy

• Infrastructure

• Injury Prevention and Management Foundation

Road Safety Advisory Council

• Partnership – Police, DIER, MAIB

• Reviewed every three years ( latest Review 2011)

• Funding – in excess of $33 million since 1996

• Driver education

• Additional Police personnel

• Automatic Number Plate Recognition

Road Safety – Serious Accidents

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

0

100

200

300

400

500

600

700

800

900

1,000

Dec-

96

Jun-

97

Dec-

97

Jun-

98

Dec-

98

Jun-

99

Dec-

99

Jun-

00

Dec -

00

Jun-

01

Dec-

01

Jun-

02

Dec-

02

Jun-

03

Dec-

03

Jun-

04

Dec-

04

Jun-

05

Dec-

05

Jun-

06

Dec-

06

Jun-

07

Dec-

07

Jun-

08

Dec-

08

Jun-

09

Dec-

09

Jun-

10

Dec-

10

Jun-

11

Num

ber O

f Reg

ister

ed V

ehic

les

Num

ber o

f Ser

ious

Cla

ims

Rece

ived

Serious Claims V's Registered Vehicles

Road Safety - Fatalities

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0.14

0.16

06/07 07/08 08/09 09/10 10/11

Rat

e pe

r 1,0

00 V

ehic

les

Financial Year

Fatalities per 1,000 Vehicles

Motorcycle Safety Strategy

• Subsidised refresher training

• Education campaign

Infrastructure

• $1M per annum for three years from 2006/2007 for the State’s Black Spot Program.

• Programs included • installation of wire rope safety barriers at locations on

the Southern Outlet near Hobart, the Tasman Highway

at Mornington and on the Bass Highway (NW). • Major road upgrade in Hobart • A variety of road safety related remedial works to be

undertaken by nine (9) local authorities state-wide.

Injury Prevention and Management Foundation

Established as part of the Scheme legislation. Objectives : • promote measures that will reduce the number and severity

of accidents; • support measures that will lead to a better outcome for those

suffering injury; and • lend support to organisations dedicated to the care of persons

who have been seriously injured as the result of a motor accident.

Up to 1% of gross premium income is set aside for project funding. Injury Prevention and Management Foundation Charities Committee established in January 2002.

Summary

• Long established scheme providing “no fault “ benefits and Common Law

• 20 Years of daily care regime

• Prudently managed and fully funded scheme • Declining claim numbers and stable costs