Magna Global: Media Economy Report 20t4

21

Media Economy Report Vol. 04 MEDIA ECONOMY REPORT BETTER, SMARTER, FASTER: HOW DATA IS CHANGING OUR BUSINESS. January 2014 MAGNA GLOBAL Vol. 04 © 2014 MAGNA GLOBAL USA, Inc. All Rights Reserved All property, including trademarks, are the property of their respective owners and have, as applicable, been licensed for use. New Value Drivers Demand Supply

-

Upload

babelfish-brian-crotty -

Category

Marketing

-

view

580 -

download

3

Transcript of Magna Global: Media Economy Report 20t4

Med

ia E

cono

my

Rep

ort

Vol

. 04

MediaeconoMyRepoRt

BetteR, SMaRteR, FaSteR: How Data is CHanging our Business.

January 2014

Magna global

Vol. 04

© 2014 Magna global USa, Inc. all Rights Reservedall property, including trademarks, are the property of their respective owners and have, as applicable, been licensed for use.

new

Val

ue D

rive

rsD

eman

dS

uppl

y

Med

ia E

cono

my

Rep

ort

Vol

. 04

Pag

e 3

Dem

and

New

Val

ue D

rive

rsS

uppl

y

Page 06SupplyPervasive consumer connectivity generates tons of new data for targeting

Page 16deMandProgrammatic activity of all types now permeates digital media

Page 24new Value dRiVeRSTiming is becoming and increasingly important aspect of reaching receptive consumers

Page 34concluSion Insights for a competitive advantage

Strategies and technologies that have come of age in the

past two years in digital are now available to improve and

to transform ALL transactions across the traditional and

the digital landscape. Not only to make our media work

harder, but also to eliminate the low value, manual pro-

cesses that still dominate the current media work flow.

BuilDing the FutuRe

taBleof Contents

new ways of identifying who your customers are.

new ways of reaching and influ-encing them at critical moments.

new ways of discovering the 50% of advertising that works, and avo-iding the 50% that doesn’t.

We are in the midst of the next great transformative era

in the media business. The digital age, supported by

data, technology, and predictive analytics has created a

new opportunity to be more precise, more efficient, and

more effective with our clients’ media investments.

Programmatic trading, born out of necessity to harness

the explosion in display inventory along the digital long

tail, has blasted open the door to new ways of thinking

about media...

We want agencies staffers, clients, and media owners

to spend more time on high level custom solutions that

drive client business results, and less time on chasing

proposals, units, and invoices.

And, as we move toward automation, toward better use

of our people’s time, and toward better use of data and

technology, we create an opportunity where EVERYONE

can win. Let’s break out of the zero sum game between

agencies, clients, and media owners and seize this

opportunity to all grow together.

Marketers: Better understanding of customer behavior

and improved ROI with less waste.

Media owners: Better understanding of their viewers

with improved yield through audience optimization.

agencies: Time freed up for higher-value activity and

increased opportunity to be compensated based on

results instead of FTE hours.

Thank you to the dozens of real live humans that

contributed to this report on data and the improved

processes it creates. I hope that all of us, human and

machine, can work together this year to drive the

media business forward.

Best,

Todd Gordon

EVP, US Director

MAGNA GLOBAL

Smaller, more targeted audience most likely to buy

Big Data Does not Mean SMaRt data

Assumes all women with these characteristics behave

the same

Disregards males that may be in market for your product

or service

Decision based on opinions about what will drive

business rather than demonstrable indicators

PITfallS

Beginning with Demographic

sex

income

age

First Layer – begin with clear behaviors of likely buyers, e.g. visited website, searched for product, etc.

01

02 Algorithms and machine-based learning uncover previously unrecognizable patterns

Begin with Objective, e.g. sell more units

Past behavior is a better predictor of

future behavior than age or sex.

tRaditional approaCH

nuanced approaCH

Med

ia E

cono

my

Rep

ort

Vol

. 04

Pag

e 5

Dem

and

New

Val

ue D

rive

rsS

uppl

y

Med

ia E

cono

my

Rep

ort

Vol

. 04

Pag

e 7

Sup

ply

Dem

and

New

Val

ue D

rive

rs

Key

taK

eaw

ay

Traditionally, “supply” has simply referred to the potential audience available

to see an ad message. However, constant connectivity has created a double-

edged sword that both challenges our ability to capture consumer attention and

generates a host of new data points with which to identify receptive audiences.

“opportunity to see” is no longer enough—“likelihood to notice,” and ultimately,

“likelihood to purchase” are the characteristics we are striving for.

1. aligning data from across the behavioral spectrum—from media exposure

to sales results—creates a robust targeting methodology that drives better

decision making in national TV trading.

2. Moving from ratings to impressions in local TV trading will not only create

additional supply, but enable more automated transaction processes.

3. Impressions-based transactions will also create the opportunity for more

precise targeting locally.

4. In online media, the vast number of audience interactions allow marketers

to combine detailed behavioral data with contextual targeting.

5. for some categories, contextual targeting may actually be better at driving

online conversions than behavioral targeting.

Supply

Med

ia E

cono

my

Rep

ort

Vol

. 04

Pag

e 9

Sup

ply

Dem

and

New

Val

ue D

rive

rs

Effectiveness

Measurement &

Optimization

01

02

03

04

Planning & Buying Tools

Cross-platform reach and affinity

indices

Programmatic

Buying

auDienCe MeasureMent platFoRM (aMp)

Search

Sales

Digital leads

brand Perception Change

Identifies audiences and media

strategies that deliver results

for our clients.

Going beyond traditional age and sex demography to

identify receptive consumers is the first step in an

enhanced national TV planning and investment process;

one that follows the same targets through exposure and

TV ads

Digital ads

lift in awareness

Promotion type Purchase Intent

number of Integrations

ROS Vignette

Sneak Peek

Sponsorship

Stunted Programming Block with Sneak Peek

Total

In Show Integration

lift in Video Views

20477149107

46294142143

51187147123

12997145169

31281159163

160333148138

In P

erce

nt –

Q3

2012

th

ru Q

1 20

13

measures resulting brand outcomes. MAGNA GLOBAL’s

Audience Measurement Platform accomplishes this

by incorporating cost, observed media behavior, brand

health metrics, verified ad exposures, and sales data.

And in addition to measuring more traditional TV ad

campaigns, AMP is able to track custom integrations and

sponsorships.

AMP pinpoints the relationship between TV

and digital ads by media type and the resulting

business outcomes.

Case stuDy ipG MediaBRandS client

Magna gloBal's cuStoM data Stack

Med

ia E

cono

my

Rep

ort

Vol

. 04

Pag

e 11

Sup

ply

Dem

and

New

Val

ue D

rive

rs

Enables data-driven targeting to optimize buying

efficiency and consumer reach

Delivers real-time analytics that provides audience

insight and enables on-the-fly buying optimization

local tV traDing49

.5

48.9

l a

38.2

37.7

D f

35.3

34.7

C HI

37.1

34.8

b o Sn Y

29.6

29.5

Increase in available Inventory Using Impressionslow Rated Half Hours vs. Total Half Hours

Ingest target data

and goals

Forecast

Generate schedule

Ingest CPMs and adjust

Provide recommendation

Segment creative

Impressions reporting

Adjustment of creative

and schedule

Place one multi-market execution

Confirm schedule and impressions

Insertion, verification, and invoicing

Export data

Provides a CPM-based model

that allows agencies to buy

across markets

agEnCIES

62Buying process

reduction

%

EfficiEncy up to

PRogRaMMaTIC bUYIng PlaTfoRM

Directly connects agencies

with 75% of US TV stations

buyl a D f C H I n Y b o S

wiDeorBit for local BRoadcaSt

97REaCH

US DMAs in %

Local television inventory has long been traded on ratings, but

fragmentation has reduced the average rating size, rendering them

unstable and unpredictable. Moving to impressions-based trading

would accomplish the following:

1. Create additional supply by

turning tiny, fickle percentages

into hard numbers that can be

aggregated.

2. Make local TV more comparab-

le to other media.

3. Enable more precise tar-

geting when combined with

additional qualitative data.

4. Feed into new, more efficient

buying processes for both

broadcast and cable inven-

tory.

1 2 3TaRgET ConSUMER foRECaST

anD Plan oPTIMIzaTIon

aUToMaTED ExECUTIon

anD ManagEMEnT

CaMPaIgn

oPTIMIzaTIon

Sup

ply

Dem

and

New

Val

ue D

rive

rsM

edia

Eco

nom

y R

epor

t V

ol. 0

3

P

age

13

Female 18-24 Female 18-24

Tennis enthusiast

Female 18-24

Read tennis racket reviews

Female 18-24

Added tennis rackets to cart

awaREnESS PURCHaSE & loYalTY

DEMogRaPHIC InTEREST InTEnT REMaRkETIng

caSe Study: Major real estate CoMpany using DouBleCliCK BiD Manager

1. Drive lowest possible cost per action

2. Prove value of display ads in driving results

goals Tactics Investment Mix

23%

20%34%

23%

Predictive Targeting 1

Contextual Targeting

1 anticipating actions based on previous behavior2 leveraging cookie pools built from company website

Behavioral Targeting

Re-Targeting 2

Contextual drove the highest

click-through rate – at a cost-

per-action 50% lower than be-

havioral or predictive targeting.

Result

Contextual Predictive behavioral Re-Targeting

0,04

0,06

0,08

0,10

0,12

%

0,02

0,00

Note: n=141 interactive marketers who combine contextual and audience targeting; numbers may

not add up to 100% due to rounding. Source: Forrester Consulting, "Display Media Buyers Value

Audience in Context"commissioned by Google, Sept. 18, 2012

My media buyer agency

recommended it

Higher performance than

using one type alone

Greater accuracy than

using one type alone

Another partner (such as

a search agency, portal or

network)

My DSP or trading desk

recommended it

35% of advertisers are using

contextual targeting in

their programmatic buys on

Google’s DoubleClick Bid Ma-

nager platform.

leadinG ReaSonS for Buying

17

1 1

21

59In Percent

35%

0

2575

50

keyword-contextualBased on the specific topic a user is reading on a web page

Category-contextualBased on the content cate-gory of the web page

language settings Of the browser

ConTExTUalbEHaVIoRal

IntentIn-market for pro-ducts or services

InterestsBased on online

browsing activity

RemarketingRe-engage based on

previous engagements

otherLookalike modeling, online-

to-offline, time of day

EnvironmentHow the ad renders based on user’s device

locationIncreased precision

DemographicAge, gender, income

level, geography

Combining tactics (audience + contextual) can drive better results across

the marketing funnel, and can be utilized across formats (display, video),

screens, and inventory types (open auction or private marketplaces).

online pRoGRaMMatic GoeS Beyond audience data witH Contextual targeting

1. Maximize share-of-voice using contextual targeting in addition to audience targeting,

2. Use both display and video formats

3. Exclude below-the-fold impressions

4. Increased focus on private market-places to augment open auction

Photo: David Sundberg/ESTo

what’s your definition of big data?

Big data is the next generation of data warehousing

and business analytics and is poised to deliver top line

revenues cost-efficiently for enterprises. The grea-

test part about this phenomenon is the rapid pace of

innovation and change; where we are today is not where

we’ll be in just two years and definitely not where we’ll

be in a decade. This new age didn’t suddenly emerge.

It’s not an overnight phenomenon. It’s been coming for

a while. It has many deep roots and many branches. In

fact, database marketers were pioneers of big data back

in the 1960s!

So why does it seem to be a hot topic now?

There are three main reasons:

1. A perfect computing storm. Big data analytics are the

natural result of four major global trends: Moore ’s

Law (which basically says that technology always gets

keith Camoosa

EVP

Research & Analytics

MAGNA GLOBAL

Michael Minelli

Head of Business Development

Information Services

MasterCard Advisors

Author of Partnering with the CIO

(Wiley, 2007) and Big Data Big

Analytics (Wiley, 2013)

cheaper), mobile computing (that smart phone or mo-

bile tablet in your hand), social networking (Facebook,

Foursquare, Pinterest, etc.), and cloud computing

(you don ’t even have to own hardware or software

anymore; you can rent or lease someone else ’s).

2. A perfect data storm. Volumes of transactional data

have been around for decades for most big firms, but

the flood gates have now opened with more volume ,

velocity, and variety— the three Vs. This makes it ext-

remely complex and cumbersome with current data

management and analytics technology and practices.

3. A perfect convergence storm. Traditional data

management and analytics software and hardware

technologies, open-source technology, and commo-

dity hardware are merging to create new alternatives

for IT and business executives to address big data

analytics.

Do you make a distinction between smart data & big

data?

In general, I see “smart data” as the lens to deriving

value from “big data”. This “lens” is a mix of smart

people, technology tools, and most importantly pro-

per direction from management on where the focus

and providing the ability for turning the insights into

action. This is why you see most executives looking

for use cases to help them to identify the low hanging

fruit. Once companies see results, it helps create a

data-driven culture.

How has big data & analytics changed marketing?

It wasn’t too long ago when marketers thought the

Holy Grail would be a corporate data warehouse.

Back then data systems were fairly new and users

didn’t know quite know what they wanted. IT was

operating under the adage “build it and they will

come.” Eventually users understood what an ana-

lytical platform was and worked together with IT to

define the business needs and approach for deriving

insights for their firm.

In today’s Big Data Age there is an interactional

model between various companies, creating more

social collaboration beyond your firm’s walls. This is

the only way marketers can cope with the major shift

in today’s consumer.

Today’s consumer has new options that better fit

their digital lifestyle. They can choose which marke-

ting messages they receive, when, where, and from

whom. They prefer marketers who talk with them, not

at them.

The linear concept of a traditional funnel, or even a

succession of lifecycle “stages,” is no longer a useful

framework for planning marketing campaigns and

programs. Today’s cross-channel consumer is more

dynamic, informed, and unpredictable. While using

a lifecycle model is still the best way to approach

marketing, today’s new cross-channel customer

is online, offline, captivated, distracted, satisfied,

annoyed, vocal, or quiet at any given moment.

Marketers must be ready with relevant marketing

at a moment’s notice. Marketing to today’s cross-

channel consumer demands a more nimble, holistic

approach, one in which customer behavior and pre-

ference data determine the content and timing—and

delivery channel—of marketing messages. Marke-

ting campaigns should be cohesive: content should

be versioned and distributable across multiple

channels. Marketers should collect holistic data pro-

files on consumers, including channel response and

preference data, social footprint/area of influence,

and more. Segmentation strategies should now take

into account channel preferences.

How should marketers think about approaching big

data and integrating it into their operations?

1. Start small. Identify the top three areas of high

potential impact.

2. Make sure your advertising team is fully leveraging

your direct/database marketing analytics talent.

3. Seek big data use cases from your peers—even if

they are in different industries.

4. Hire or consult some data scientists and engineers

that understand the “open source” technology

world. It’s amazing how much analytics innovation

is happening on a daily basis- and it’s free!

5. Create an R&D or lab function where people are

100% focused on testing new big data approaches

that can be implemented. It’s too hard to do it

with 10% of someone’s time.

6. Leverage the big data vendor community. They

often will put some skin in the game if you treat

them like a partner!

7. Make sure you have a good working relationship

with your technology colleagues—they need to be

an integral part of the team.

Med

ia E

cono

my

Rep

ort

Vol

. 04

Pag

e 15

Sup

ply

Dem

and

New

Val

ue D

rive

rs

paRtneRperspeCtive

& aQ

Med

ia E

cono

my

Rep

ort

Vol

. 04

Pag

e 17

Sup

ply

Dem

and

New

Val

ue D

rive

rs

Key

taK

eaw

ay

advertisers are no longer approaching programmatic as a segment of their

overall strategy; data and targeting permeates all aspects of digital planning,

and brands are demanding that media owners make their inventory available

for programmatic dollars, both real time and automated.

deManddiGital FoRMatS Migrating to pRoGRaMMatic

01

02

03

04

Remnant

inventory

Mid-tier

inventory

Customized & ‘native’

campaigns

non-standard campaigns are the only form of

display advertising that will remain largely

untouched by automated buying mechanisms.

Premium formats are starting to be

transacted programmatically. little of

it will be fully RTb, at least at first.

within 5 years in the US

(a bit longer elsewhere) the

overwhelming majority of

non-premium inventory

will be transacted

through pro-

grammatic, primarily

through RTb.

Premium

formats

Inventory that is easily standardized is quickly auto-

mated. While high-touch sponsorships and customized

campaigns will always require human stewardship,

anything in a commoditized size will be bought and sold

primarily by machines in the not-too-distant future.

Even at the high end where creative can’t be automa-

ted, other aspects of the transaction will be managed

by machines. This integration pyramid will be mirrored

in other media as programmatic methods encroach on

traditional ecosystems.

1. Programmatic spend no longer refers only to real-time bidding (RTb);

audience targeting now occurs via both real-time and non-real-time

methods, and as a result advertisers are accessing more and more premium

data-enhanced inventory.

2. global growth in digital programmatic trading was nearly 60% in 2013, and

will continue at nearly 40% this year.

3. while only the largest digital markets are already spending in a

programmatic fashion, the number of advertisers trading in this way will

rapidly increase as the ecosystem expands globally.

4. advertisers aren’t only thinking about programmatic spend as a direct

targeting tool; programmatic brand advertising is becoming more popular,

and is measurable with today’s suite of campaign tools.

5. long term growth of advertiser spend will depend on the availability of data

in emerging markets.

Med

ia E

cono

my

Rep

ort

Vol

. 04

Pag

e 19

Sup

ply

Dem

and

New

Val

ue D

rive

rs

deFinition/Scope

ecoSySteM

1

Advertisers Publishers

Global Programmatic sPend

DSP'sagency Desks Exchanges

2013 2016 2017

Spain

Netherlands

France

Australia

Germany

United Kingdom

China

Japan

United States

2012 20152011

United States

80%

60% 59% 56%52%

40%33% 31%

23%

Netherlands United Kingdom France Australia Japan Germany Spain China

2014

25

50

30

60

30

70

90

30

80

20

40

15

3o

10

20

10

0

0

Dol

lar

%

Global Programmatic Spend ($bn)

Global Programmatic Market Share

2.8 $ 4.8 $7.5 $

9.9 $ 12.6 $15.2 $ 17.6 $

4.5 $7.6 $

12.1 $

16.7 $

22.1 $

27.7 $

33.3 $

2011 20152012 20162013 20172014

Data Providers

0

0

1

1

0

0

0

0

11

1

1

1

10

0

1

1

1

1

0

1

1

0

0 0

0

0

0

1

0

00

0

10

Driven by advanced technology and streamlining the traditional mediabuying workflow...

RTb

01

02

03

04

05

06

nRTb

Integrated with, and empowered by, media usage and consumer data...

Capable of adressing discrete impressions as opposedto packages of impressions, in a cost efficient way...

Targeting specific demographic groups or behavioral groups while being vendor-agnostic and content-agnostic...

Can be bought in "real-time", allowing feed-back loop and continued adjustment in campaign settings...

Matches demand and supply from multiple vendors and multiple buyers through bidding mechanisms...

11

11

1

1

11 1

1

1

1

1

1

1

1

1

1

0

0

0

0

0

00

0

0

0

0

00

0

0

01

1

0

0

While ‘programmatic’ was 2013’s marketing buzzword of the year,

the term itself has been used in various ways since its inception and

continues to evolve. To us, the difference between RTB and non-RTB

(automated) transactions within programmatic can be recognized by

whether the transaction is …

Med

ia E

cono

my

Rep

ort

Vol

. 04

Pag

e 21

Sup

ply

Dem

and

New

Val

ue D

rive

rs

The ecosystem to implement non-real time programmatic processes is already far along in its development.

TV

Radio

Out-of-Home

prograMMatiC for tRaditional MediadRiVeRS inhiBitoRS

Many networks and cable operators are hesitant to make their inventory available on automated platforms.

There is significant transactio-nal infrastructure in place that will take time to evolve.

Radio only represents 7% of to-tal spend globally so there isn't nearly the same drive behind programmatic development as there is for television.

Digital OOH is not a common existing element of most cam-paigns; programmatic dollars will have to grow organically and won't have much existing spend to cannibalize.

The tech infrastructure for hyper-targeting isn't wides-pread on digital radio, so it is largely limited to demographics by station for now.

Digital OOH inventory is unique so it's difficult to set standar-dized inventory types on which to bid. Location data will have to be very specific to give con-text to impressions.

The most money is spent in television, therefore the gre-atest gains are available from increases in efficiency.

Digital radio already has enough measurement in place to show the value of each ad and therefore the value of pro-grammatic efficiencies can be seen quantitatively.

Digital OOH inventory can be updated in real time (and po-tentially, in the future, depen-ding on who is observing).

Radio ads can be sold in real time as well as cross-channel, making it attractive as a part of broader ad campaigns.

The ecosystem is already developing with solutions like Vistar and Vukunet. Even before exchanges develop, program-matic direct will be offered.

Med

ia E

cono

my

Rep

ort

Vol

. 04

Pag

e 23

Sup

ply

Dem

and

New

Val

ue D

rive

rs

Media owneR perspeCtive

& aQ

bob lord

CEo of aol

networks

wanted to be involved. We firmly believe that

this approach will explode creativity in the

marketplace and enable agencies, advertisers

and publishers to focus on driving unprece-

dented client value and the most engaging user

experiences.

what proportion of your advertising sales are

you expecting to be automated in one year, in

three years?

It’s an interesting question for us because we

actually use the same platform to operate our

managed services business as our clients use

as self-service programmatic tools. So I guess I

would say 100% of our business will continue to

be run using programmatic/automated tools.

Can you comment on the drivers and obstacles

for mobile and video inventory on the road to

automation and programmatic?

The primary driver is consumer behavior, for

both mobile and video. No one in our industry –

brands, agencies or publishers – can afford to

ignore the dramatic movement by consumers to

multi-screen and video consumption. Obviously

as these trends continue, inventory constraints

will lessen, but the real issue is making sure the

platforms buyers use can access and analyze

from an inventory and screen-agnostic view.

Can you give us a sense of your inroads into

programmatic and automation following the aol

Programmatic Upfront of September 2013?

So we are very bullish on achieving our goal of moving

the conversation around programmatic from remnant

RTB to automation and efficiency. Over 650 people

attended the Upfront and over 300 additional clients in

fourteen cities have participated since. We’ve seen over

$50 million in commitments thus far so I feel very good

that we are changing the agency media model in real-

time. We have worked very hard to refocus our teams

and technologies on platforms that help agencies and

Vincent letang

EVP, Director

of forecasting

Magna global

brands scale across all screens and formats to solve

real business problems. And I believe we’re at the right

place at the right time given the structural and econo-

mic pressures digital is putting on the advertising and

media ecosystems.

what prompted your decision to join the Magna

Consortium on automation?

We continue to have tremendous respect for IPG Media-

brands and MAGNA’s leadership in a move to automating

the processes that can and should be automated to

drive more client and agency value. It was a very quick

decision once we heard the focus as to whether we

Key

taK

eaw

ay

as technology and data speed have improved, timing has become increasingly

important as a component of successful targeting. Relevance can hinge not

only on when the message is delivered to the consumer, but on the cadence of

subsequent communications.

new Value dRiVeRS

1. Consumers are twice as likely to interact with online ad content

when it is delivered in real-time.

2. Incorporating real-time content into online display ads improves

brand favorability and purchase intent.

3. In a multi-screen campaign, the shorter the interval between TV and

online ad exposures, the more memorable the messages will be.

4. Sequential messaging across TV and online also improves positive

responses to the brand.

5. Many global internet users are in favor of their devices anticipating

their needs based on passively collected data.

Med

ia E

cono

my

Rep

ort

Vol

. 04

Pag

e 25

Sup

ply

Dem

and

New

Val

ue D

rive

rs

Med

ia E

cono

my

Rep

ort

Vol

. 04

Pag

e 27

Sup

ply

Dem

and

New

Val

ue D

rive

rs

ConsuMers 2x as likely to inteRact witH Content wHen it is Real-tiMe

inCorporating Real-tiMe content into aDs Drives FaVoRaBility & intent

tiMing MatteRS

12%12%

27%

24%

Real -Time Ad

Non Real-Time

Real -Time Ad

Non Real-Time

Total Audience

Brand Favorability Purchase Intent

In-Market Audience

Interactions with Intent: % of viewers who actively

and intently engage by:

Rolling over ad for min of 0.5 seconds

anD conducting a min. of one positive action(e.g. expand, click-through, play video, etc.)

01

02

68% 69%60% 58%

50

60

70

80

40

30

20

10

%

Sou

rce:

IPG

Lab

/AO

L S

tud

y: T

he

Pow

er o

f R

eal T

ime

ad Recall By tiMe (tv + online)

Gain In Metric With Sequential Exposures

(Sequential Exp. Minus 7+ Day Exp.)

A recent collaborative research study between the IPG Media Lab and multi-screen

audience aggregator Collective demonstrated that closely timed exposures across tele-

vision and online generated significant bumps in ad recall and key brand metrics.

Multi-ScReen planS Have Most to Gain FRoM condenSed tiMinG

TV only

Unaided Ad Recall

Aided Ad Recall

Overall Favourability

Likelihood To Recommend

Purchase Intent

+3%

+12%

0%

0%

-1%

TV + online

+12%

+21%

+4%

+9%

+10%

50

60

70

80

90

100

40

30

20

10

0

%

Sequential

With

in D

ay Part

Day Part - 1 D

ay

1 -3 Day

3-7 Day

7+ Day

48%42%

37%32%35%

Aided Ad Recall

Unaided Ad Recall

85%80%

71% 70%67%

63%

Strongly Agree

Agree

Neither Agree nor Disagree

Disagree

Strongly Disagree

17%

38%

30%

8%7%

antiCipatory coMputinG

gloBal internet users – “i expect technoloGy to intRoduce Me to new anD SuRpRiSinG expeRienceS”

Source: IPG Mediabrands/Microsoft, “The Future Laboratory,” May 2013

Q22. “I expect technology to introduce me to new and surprising experiences that are

uniquely tailored to me and that feel like coincidences”

“i expect BRandS to know Me and oFFeR Me soMetHing i DiDn’t even Know i wanteD”

“i aM MuCH More likely to Buy a pRoduct or serviCe froM a BranD tHat Delivers pleasantly SuRpRiSinG expeRienceS”

Source: IPG Mediabrands/Microsoft, “The Future Laboratory,” May 2013

Q29b. And still thinking about the brands or services that you interact with on a day- to -day

basis, on and offline, to what extent do you agree with the following statements

Source: IPG Mediabrands/Microsoft, “The Future Laboratory,” May 2013

Q23. “Which of the following statements best describes your attitude to how you discover things using technology?”

20%

i

“i love digital devices and services that provide me with new recom-mendations or content at the moment when i need them without me actively seeking them out."

“i like devices and services that provide me with recommendations that are based on my previous be-haviour online and are provided on regular basis.”

31%

13%

29%

31%

15%

12%20%

41%

28%

6% 5%

Strongly Agree

Agree

Neither Agree nor Disagree Disagree

Strongly Disagree

Med

ia E

cono

my

Rep

ort

Vol

. 04

Pag

e 29

Sup

ply

Dem

and

New

Val

ue D

rive

rs

The idea of targeting in real-time is to create a mutually

beneficial scenario for the brand and consumer—you’re

offering something they need. But what if you could anti-

cipate those needs before they even arise?

That is the promise of anticipatory computing, which,

rather than waiting for the user to make a query, uses

passively collected data streams like sound and location

to proactively provide information. It is already being

used in some mobile apps, and a survey of global internet

users performed in collaboration with Microsoft has re-

vealed that many are ready and willing for their devices to

anticipate their needs and recommend new experiences.

Med

ia E

cono

my

Rep

ort

Vol

. 04

Pag

e 31

Sup

ply

Dem

and

New

Val

ue D

rive

rs

what it Does - Sticky uses

eyetracking technology to

measure attention on display

advertising to provide insights

and marketing accountability

ad Experience - Premium

display ads

Marketing objective -

accountability & Measurement

what it Does - Vistar uses

mobile location data to inform

ooH buys that can be bought

programatically

ad Experience - Digital out of

Home

Marketing objective - awareness

what it Does - Triple lift powers

native visual ad content at scale

by automatically reformating

image assets to match the look

and feel of publisher's sites

ad Experience - native Visual

ads similar to Pinterest

Marketing objective - build

brand Image, awareness,

Conversion

what it Does - Idomoo integrates

real customer data into video

to create personalized content

rendered on the fly

ad Experience - Personalized

video typically delivered via

Marketing objective - Educate,

build Relationship, Sales

what it Does - Perch marries

motion-sensing cameras,

software and a projector to

detect product interaction at

shelf that can inform in-store

displays

ad Experience - In store media

displays using a projector

Marketing objective - Sales

StaRt-upS to watCH The explosive growth of connected media

devices in consumers’ hands and the resulting

data they provide has created numerous paths

to better targeting. new companies with

different ideas on how to harness that

information are cropping up all the time.

what It Does - Placed is a location-

driven consumer insights and

mobile ad intelligence service.

They measure billions of location

data points across the U.S.

using an opt-in panel of 100,000

participants

ad Experience - Survey questions

via mobile app

Marketing objective -

Measurement & attribution

aGency perspeCtive

what is the agency's role in an increasingly data-driven marketplace?

what is the biggest challenge to more widespread adoption

of programmatic buying?

Direct response advertisers have generally adopted

programmatic buying. what about brand advertisers?

Does scale matter in programmatic?

Is programmatic really this transformative force that many

in the industry suggest?

The Internet continues to expand and fragment at a rapid pace.

forrester Research appropriately labeled this dynamic the "Splinternet"

in a 2010 report. Consumers engage with content and advertising across

a wide spectrum of paid, owned, and earned media channels. These

changing media consumption habits have resulted in an underlying

media buying ecosystem that is constantly evolving, highly fragmented,

and massively complex. Targeted reach at scale while theoretically

achievable, hinges on the proper utilization and intersection of data

(huge amounts of it) and technology. So, agencies are now in the data

and tech business just as much as they are in the intelligence and

investment business. The agency’s role, in my opinion, has never been

more important. agencies need to insulate marketers from the complex

underlying circuitry involved and establish an agile programmatic

buying capability – with investments in talent, proprietary insights, and

technology partnerships – to power highly targeted conversations with

customers across devices and channels. It’s not a trivial undertaking by

any means and a massive opportunity for agencies.

There is no overarching agreement in the industry regarding the

definition or scope of programmatic. Programmatic has, for

many, come to represent remnant inventory, distressed CPMs,

and strictly direct-response tactics. This simplistic association

has understandably left the sell side wary. The buy side views

programmatic as the unprecedented opportunity to drive targeted

reach at scale through the use of data and technology across all

classes of inventory. So, in that sense, programmatic has a brand

problem! The good news is that programmatic is very much in its

infancy. I’m very optimistic that we can work together to fully realize

the potential transformative power of programmatic buying.

Direct response advertisers were quick to adopt programmatic

because it provides an unprecedented level of choice over

inventory (at the impression level) and near real-time measurability

and, as such, aligns very well with their marketing goal and

priorities. However, brand advertisers are starting to realize

that programmatic management of individual exposures, via the

use of first-and-third-party data and other indicators such as

content and context, has the potential to drive highly personalized

communications at scale in the right environments. we are

beginning to see a healthy increase in brand spend and I expect this

to continue and grow throughout 2014.

absolutely. Swaths of premium inventory are not currently

available on the open exchanges. The combination of scale plus

programmatic buying means that we can continue to bring leverage

to bear on our deals with premium publishers at the macro level yet

extract maximum value by applying programmatic techniques at

the micro individual exposure level.

Yes. well, that’s my personal opinion and I guess you can say that I’m

biased! as Stephen baker, technology journalist, said in a post in the

new York Times about a related topic:

“The Impact of new technologies is invariably misjudged because we

measure the future with yardsticks from the past.”

brian Hughes

SVP, audience

analysis Practice

lead at

Magna global

brian Hughes

brian Hughes

brian Hughes

brian Hughes

neeraj kochhar

EVP, Managing Director

Programmatic at

Magna global

neeraj kochhar

neeraj kochhar

neeraj kochhar

neeraj kochhar

Med

ia E

cono

my

Rep

ort

Vol

. 04

Pag

e 33

Sup

ply

Dem

and

New

Val

ue D

rive

rs

Med

ia E

cono

my

Rep

ort

Vol

. 04

Pag

e 35

Sup

ply

Dem

and

New

Val

ue D

rive

rs

contRiButoRSbrian Hughes @bhughes_magna

SVP, audience analysis Practice lead,

Magna global

Vincent letang @vletang_magna

EVP, Director of forecasting, Magna global

luke Stillman @lukestillman

forecasting Manager, Magna global

Janice finkel-greene

EVP, buying analytics, Magna global

keith Camoosa

EVP, Research & analytics, Magna global

Tanya kolosova

SVP, Director of Research and analytics, aMP,

Magna global

kara Manatt @karamanatt

VP, Consumer Research Strategy, IPG Media Lab

Jack Pollock @pollockj07

Senior analyst, IPg Media lab

Todd gordon @tpgtweets

EVP, US Director, Magna global

neeraj kochhar @neeraj_kochhar

Managing Director, Programmatic, Magna global

natalie bokenham @natlikethat

SVP, Managing Partner, Digital, UM

Design by

bureau oberhaeuser @oberhaeuserinfo

SuMMaRy CHeat sHeet new Value Drivers

1. Consumers are twice as likely to interact with online

ad content when it is delivered in real-time.

New Finding: The results are even better among the

in-market audience (i.e. those seeking to buy).

2. Incorporating real-time content into online display

ads improves brand favorability and purchase intent.

New Finding: Percent increases compared to non

real-time ads were between 13-19%.

3. In a multi-screen campaign, the shorter the interval

between TV and online ad exposures, the more

memorable the messages will be.

New Finding: The difference in unaided recall between

sequential exposures and those seven days apart

was 33%.

4. Sequential messaging across TV and online also

improves positive responses to the brand.

New Finding: The results for sequential exposures on

TV alone were not nearly as positive.

5. Many global internet users are in favor of their

devices anticipating their needs based on passively

collected data.

New Finding: More than 60% agreed that they would

be much more likely buy a product or service that

delivered “pleasantly surprising experiences.”

Supply

1. aligning data from across the behavioral spectrum—

from media exposure to sales results—creates a

robust targeting methodology that drives better

decision making in national TV trading.

New Finding: Past behavior is a better predictor of

future behavior than age and sex.

2. Moving from ratings to impressions in local TV

trading will not only create additional supply, but

enable more automated transaction processes.

New Finding: Inventory may increase by more than

30%, depending on the market.

3. Impressions-based transactions will also create the

opportunity for more precise targeting locally.

New Finding: Overlaying impressions with qualitative

and purchase data will make this possible.

4. In online media, the vast number audience

interactions allow marketers to combine detailed

behavioral data with contextual targeting.

New Finding: Contextual indicators can include

keywords, content categories, and location.

5. for some categories, contextual targeting may

actually be better at driving online conversions than

behavioral.

New Finding: Cost must also be taken into account

when determining the success of different

targeting methods.

Demand

1. Programmatic spend no longer refers only to real-

time bidding (RTb); audience targeting now occurs

via both real-time and non-real-time methods, and

as a result advertisers are accessing more and more

premium data-enhanced inventory.

New Finding: Non real-time processes will make

premium publishers more comfortable with doing

business programmatically.

2. global growth in digital programmatic trading was

nearly 60% in 2013, and will continue at nearly 40%

this year.

New Finding: By 2017, the digital programmatic spend

across nine major markets will exceed $33 billion.

3. while only the largest digital markets are already

spending in a programmatic fashion, the number of

advertisers trading in this way will rapidly increase as

the ecosystem expands globally.

New Finding: An expansion of infrastructure in

emerging programmatic markets will make

this possible.

4. advertisers aren’t only thinking about programmatic

spend as a direct targeting tool; programmatic

brand advertising is becoming more popular, and is

measurable with today’s suite of campaign tools.

New Finding: The growth in available data in

developed markets has enabled highly personalized

communications at scale.

5. long term growth of advertiser spend will depend on

the availability of data in emerging markets.

New Finding: Data is the life-blood of the

programmatic ecosystem.

ConCluDing tweet

brian Hughes @bhughes_magnaData is inching us ever closer to that “Minority

Report” moment of real-time, one-to-one

messaging, regardless of location.

Med

ia E

cono

my

Rep

ort

Vol

. 04

Pag

e 37

Sup

ply

Dem

and

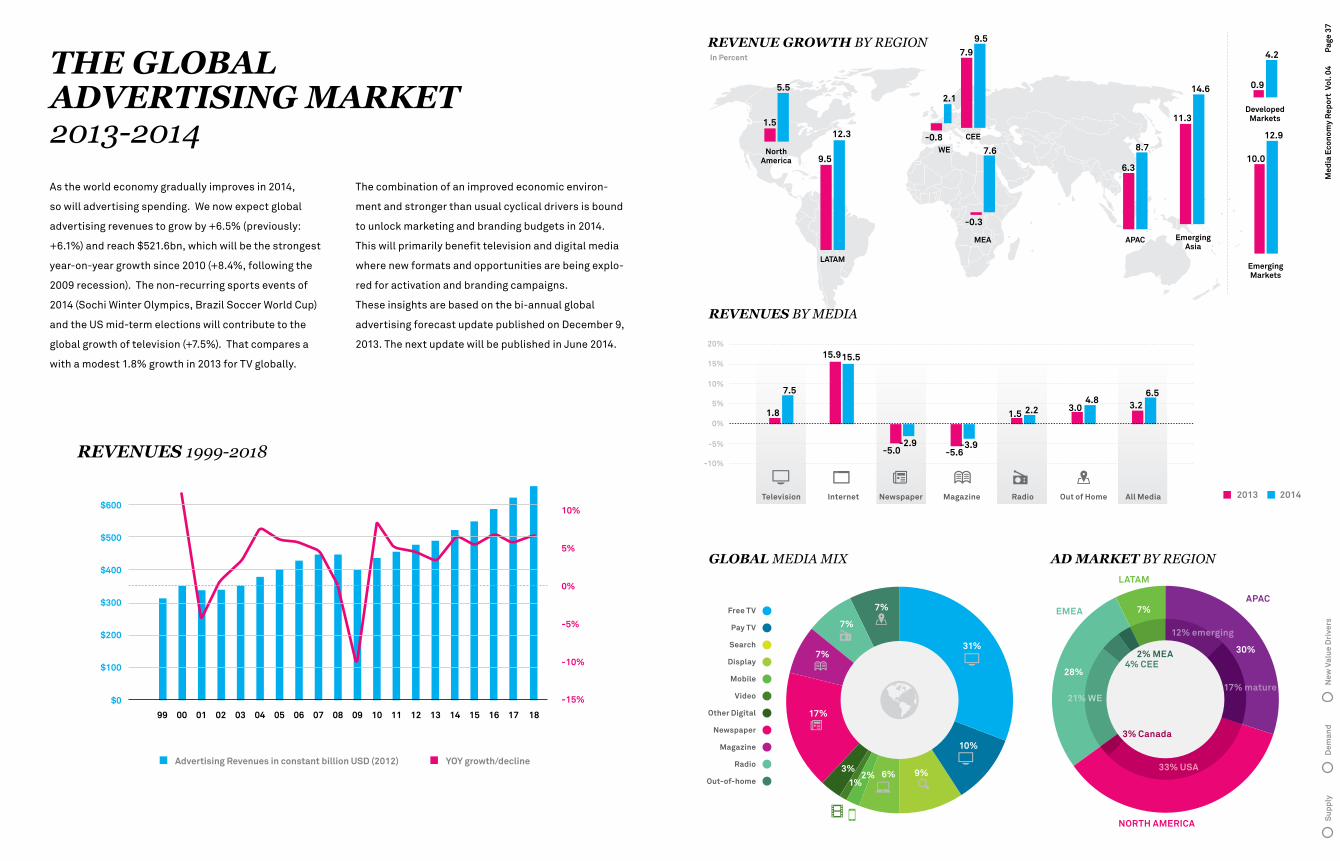

the GloBal adVeRtiSinG MaRket2013-2014As the world economy gradually improves in 2014,

so will advertising spending. We now expect global

advertising revenues to grow by +6.5% (previously:

+6.1%) and reach $521.6bn, which will be the strongest

year-on-year growth since 2010 (+8.4%, following the

2009 recession). The non-recurring sports events of

2014 (Sochi Winter Olympics, Brazil Soccer World Cup)

and the US mid-term elections will contribute to the

global growth of television (+7.5%). That compares a

with a modest 1.8% growth in 2013 for TV globally.

ReVenueS 1999-2018

-10%

$200

0%

$100

-5%

$600

$500

$400

10%

$300

5%

$0 -15%

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

advertising Revenues in constant billion USD (2012) YoY growth/decline

aPaCEMEa

laTaM

ad MaRket By region

2% MEa4% CEE

21% wE

3% Canada

33% USa

12% emerging

17% mature

30%

7%

28%

noRTH aMERICa

GloBal MeDia Mix

free TV

Pay TV

Search

Display

Mobile

Video

other Digital

newspaper

Magazine

Radio

out-of-home

31%

10%

9%6%2%1%

3%

17%

7%

7%

7%

ReVenue GRowth By regionIn Percent

20142013

-0.8WE

2.1

CEE

7.99.5

NorthAmerica

1.5

5.5

APAC

6.3

8.7

EmergingAsia

11.3

14.6

LATAM

12.3

1.8

-5.0 -5.6

7.5

15.9

1.53.0

15.5

2.24.8 3.2

6.5

9.5

MEA

7.6

-0.3

DevelopedMarkets

0.9

4.2

ReVenueS By MeDia

Emerging Markets

10.0

12.9

15%

20%

10%

5%

0%

-5%

-10%

Television Internet Newspaper Magazine Radio Out of Home All Media

The combination of an improved economic environ-

ment and stronger than usual cyclical drivers is bound

to unlock marketing and branding budgets in 2014.

This will primarily benefit television and digital media

where new formats and opportunities are being explo-

red for activation and branding campaigns.

These insights are based on the bi-annual global

advertising forecast update published on December 9,

2013. The next update will be published in June 2014.

New

Val

ue D

rive

rs

-2.9 -3.9

Med

ia E

cono

my

Rep

ort

Vol

. 04

Pag

e 39

Sup

ply

Dem

and

tHe gloBal aDvertising MaRket 2013

Reading this map: the size of each country is pro-portional to advertising spending in billion USD; the color reflects the level of spend per capita, akin to the intensity of advertising pressure: green is very low (less than $50), red is very high ($400 and more). This map reveals that the US alone represents a third of global advertising market while some large countries by surface or population, like India or Russia, remain largely underdeveloped.

advertising Spending in $ per capita (2013)

$0 $100 $200 $300 $400 $500 $600

1bn5bn

10bn

in USD

Billion Dollars

to

tal

M

ar

Ket

siz

e

490

Sri lanka$143

Pakistan$308

Croatia $251

france

$13,376

nl$4,090

aR UY

China

$44,100

Canada

$13,004

USa

$156,546 bulgaria $252

Ua

Serb

ia $173

new zealand$1,406

austria $3,036

Switzerland$3,863

Dk

belgium$2,463

germany

$23,621

greece$940

Turkey$3,327

Saudi arabia$1,707

bahrain $121Hong kong$3,032

kazakhstan$329

kuwait$534

$936

lV $97

lebanon$188

lT $144

Pl$2,463

HU

Cz$1,303

korea

$8,083

Philippines$1,438

Mexico$3,739

Qatar $236

Slovak Republic $384

Romania $406$620

Russia

$10,876

India

$6,882

Taiwan$1,939

United kindom

$22,092

Italy

$8,122 Spain$5,434

Japan

$52,070

EE $110

Egypt$2,456

South africa$4,541

kenya$536

Morocco$420 oman

$161

Thailand$4,341

Vietnam$711

UaE

australia

$13,234

Malaysia$2,637

Singapore$2,012 Indonesia

$6,326brazil$17,804

Co$4,914

VE

IE

noSE

fInortHaMeriCa

latinaMeriCa

asia paCifiC

europe

MiDDle east

afriCaPanama$514

EC PE

$431

$446

$729

$1,231

Chile $1,419

$5,788

$1,147

PT

$673

Costa Rica$694

PuertoRico$918

$2,105

$3,450$3,031

$1,592

$1,258

New

Val

ue D

rive

rs

aBout MaGna GloBal

MAGNA GLOBAL is the strategic global media unit of IPG Mediabrands,

comprised of two key divisions.

MAGNA GLOBAL Investment harnesses the aggregate power of all IPG

media investments to create power and leverage in the market, drive

savings and efficiencies, and ultimately make smarter, more effective

media investments on behalf of our clients. With a stated goal of re-

aching 50% automated buying by 2016, the team in North America in-

vests across digital, programmatic, broadcast and all traditional media

platforms and is therefore considered the most comprehensive buying

and negotiating unit in the media industry. The architects of the MAGNA

Consortium – a powerful committee of executives from A&E Networks,

AOL, Cablevision, Clear Channel Media and Entertainment, ESPN and

Tribune – MAGNA North America is also dedicated to shaping industry

automation and audience specific buying.

MAGNA GLOBAL Intelligence has set the industry standard for more

than 50 years by predicting the future of media value. MAGNA GLOBAL

Intelligence produces more than 40 annual reports on audience trends,

media spend and market demand, and ad effectiveness. For more in-

formation, please visit www.magnaglobal.com or follow us on Twitter

@MAGNAGLOBAL.

aBout ipG MediaBRandS

We were founded by Interpublic Group (NYSE: IPG) in 2007 to manage all

of its global media-related assets. Today that means we manage and in-

vest $37 billion in global media on the behalf of our clients, employ over

8,500 diverse and daring marketing communication specialists worldwi-

de and operate our company businesses in more than 130 countries.

A proven entity in helping clients maximize business results through in-

tegrated, intelligence-driven marketing strategies, IPG Mediabrands is

committed to driving automated buying, pay-for-performance and digi-

tal innovation solutions through its network of media agencies including

UM, Initiative, BPN, Orion Holdings, and ID Media. Its roster of special-

ty service agencies including MAGNA GLOBAL, Mediabrands Audience

Platform, Mediabrands Publishing, IPG Media Lab, Ensemble, and Iden-

tity offer technologies and industry moving partnerships that are reco-

gnized for delivering unprecedented bottom line results for clients. For

more information, please visit www.ipgmediabrands.com or follow us on

Twitter @IPGMediabrands.