Magazine | MAY / JUNE 2015 - Luxembourg for finance · Magazine | MAY / JUNE 2015 Luxembourg fund...

32

Magazine | MAY / JUNE 2015 Luxembourg fund industry DEFINING THE FUTURE Exploring art and science INTRODUCING ROBOTS AT LUXEMBOURG'S MODERN ART MUSEUM Dossier FINTECH IN LUXEMBOURG FinTech and the future of banking How to make your business grow Building a mobile payment ecosystem Accelerating a FinTech business Mangopay goes international Developing a Bloomberg App Luxembourg start-up introduces Africa's first mobile clearing house

Transcript of Magazine | MAY / JUNE 2015 - Luxembourg for finance · Magazine | MAY / JUNE 2015 Luxembourg fund...

Magazine | MAY / JUNE 2015

Luxembourg fund industry

defining the future

Exploring art and scienceintroducing robots at luxembourg's modern art museum

Dossier

fintech in luxembourg

FinTech and the future of banking

How to make your business grow

Building a mobile payment ecosystem

Accelerating a FinTech business

Mangopay goes international

Developing a Bloomberg App

Luxembourg start-up introduces Africa's first mobile clearing house

Dear readers,

FinTech is probably the strongest contender for the buzz-word-of-the-year award. Everybody claims ownership of it and every financial center is positioning itself in this rapidly developing industry. Far from being only a hype, FinTech is a reality and every day more so. Whether in improving customer experience by creating new ways to deliver financial services, in helping to come to terms with regulatory issues by the development of new compliance software or in putting available data to commercial use, FinTech is ramifying into every corner of the financial industry. Its main actors are not only start-ups who develop new and even disruptive solutions but also established actors who are pivoting towards this new segment of the industry.

Luxembourg’s financial center, recently confirmed as the Number 1 in the Eurozone by the Global Financial Center Index, can itself boast a strong FinTech industry because of the market available in Luxembourg with all the financial players located there but also because it is a platform in the EU’s single market from where other national markets can easily and efficiently be covered. Luxembourg can leverage two of its fundamental strengths in this space: its international character and its openness to innovation. Both of these features will emerge very clearly in this magazine.

The articles that follow, lay out the FinTech ecosystem available in Luxembourg and tell some of the homegrown success-stories as well as explain the reasons behind the strategic choice by some players to opt for Luxembourg as a base. Together they reflect the can-do attitude and result-oriented environment available in Luxembourg. In one of these articles, for instance, Luxembourg’s financial regulator, the CSSF, talks about the future development of the regulatory framework and the challenges as well as opportunities in this context.

Technological innovation, albeit not financial, is also showcased in the article about robots guiding visitors through the Mudam, Luxembourg’s world-class modern art museum. These robots, developed in cooperation with the University of Luxembourg, are further examples of what the future holds.

Finally, in this edition we also interviewed Marc Saluzzi, the outgoing Chairman of Luxembourg’s Investment Fund Association ALFI on the future of the Luxembourg fund industry. Please allow me to take this opportunity to congratulate Marc on his remarkable achievements as Chairman of ALFI over the last four years as well as to express my very sincere appreciation for the excellent cooperation I personnally had with him during his tenure. I do hope we will be able to tap his vast expertise and his vision also in the future, for which the entire LFF team wishes him very well. Bon vent, Marc!

NICoLAS MACKEL

editorial | P.2

Nicolas mackel, CEO,

Luxembourg for Finance

luxembourg Fund industry | P. 3

luxembourg fund industry: defining the future

lFF: How do you see tHe Future growtH ProsPects For tHe luxembourg Fund industry?

ms: The past year has been a very good year for our industry. In September 2014, assets under management exceeded the highly symbolic 3,000 bn EUR threshold. After 19 months of uninterrupted growth, this figure today stands at over 3.5 trn EUR. The growth is largely driven by a rally in financial markets but also by net sales, i.e. new money flowing into our funds, proof of the confidence that international investors have in our Luxembourg fund range.

With interest rates at their lowest levels in decades, it can be hard to make a return on a savings product. That is likely to further motivate a growing

number of savers to invest at least part of their savings in the financial markets. Since investment funds are an efficient vehicle to invest in diversified portfolios, they are an attractive savings product. Further to this, Luxembourg based investment funds benefit from the fact that they are offered cross-border in 70 countries around the globe.

Regarding the immediate future, we believe that several trends and developments offer the Luxembourg fund sector excellent growth opportunities. The retrenching of banks from the financing of the real economy, the need for significant investments in infrastructure or a real pan European pension fund solution are the most significant of them. Combined with the opening of large pension fund systems to foreign funds like in Brazil, Australia or Mexico, we are definitely optimistic.

Assets under management of Luxembourg domiciled

funds reached a record 3,524 bn EUR at the

end of March 2015. The exceptionally high sales, which amount to a 30%

increase in the past twelve months, are proof of the

continuous confidence of the international investor in the

Luxembourg fund product.

The Grand Duchy is the global leader for the cross-

border distribution of investment funds, with the

result that today more than 75% of UCITS (investment

funds regulated at EU level) distributed internationally are based in Luxembourg.

Marc Saluzzi, the outgoing Chair of the Association

of the Luxembourg Fund Industry (ALFI), gives his

insight into the latest trends and prospects for the fund

industry.

luxembourg Fund industry | P. 4

lFF: tHe alFi euroPean resPonsible investing Fund survey 2015 Found tHat assets under management in euroPean resPonsible investment Funds saw comPound annual growtH oF 25 Percent between 2012 and 2014. How is luxembourg Positioned to take advantage oF tHe growing trend For resPonsible investment Funds and wHat does tHis oFFer investors?

ms: Since the creation of the Luxembourg Fund Labelling Agency LuxFLAG in 2006, the Luxembourg financial center has gained a steadily rising visibility in the area of responsible investing. While the focus was put on microfinance in a first stage, the sector is now embracing many different forms of ’responsible’ and ’impact’ investments. Luxembourg based funds are now managing 35% of all the assets under management in European responsible investment funds.

our survey revealed that responsible investing today is mainly driven by institutional investors. However, the report anticipates that by 2013, responsible investing will have become

a mainstream investment product. Luxembourg is particularly well positioned to benefit from this trend because it has a long experience in offering what the investor of the future will increasingly be looking for: tailored investment products, open and simple investment platforms and flexible and adaptable products which support him and his clients through their lives.

lFF: luxembourg is tHe leading centre For renminbi Funds outside asia. wHy Has luxembourg an edge on rmb investment Funds and wHat Potential is tHere For growing tHis Particular segment in luxembourg?

ms: Luxembourg realised very early that the Chinese currency is on its way to becoming a worldwide recognised reserve currency beside the USD, the Euro and the CHF and the potential this development offers the financial industry. Given that Luxembourg funds have a long tradition in innovation, it is only natural that promoters have started to offer investors the opportunity to invest in Renminbi denominated investment products. The potential for growing this segment

in Luxembourg evolves with the internationalisation of the Renminbi and with the expected progressive opening of the Chinese market for foreign investors. The fact that the 6 largest Chinese banks have established their European headquarters in Luxembourg has a very positive impact in this context as well.

Recently, the People’s Bank of China announced the granting of a 50 bn RMB RQFII quota to Luxembourg. The RQFII (RMB Qualified Foreign Institutional Investor) scheme was launched in Hong Kong in 2011 and has been expanded to other jurisdictions since 2013 enabling offshore RMB to be reinvested into the Mainland securities market. Chinese asset managers are following suit and setting-up their flagship European investment funds in Luxembourg. There are also several fund passporting projects in the pipeline in Asia.

Marc saluzzi, Chairman of the Association of the Luxembourg Fund Industry (ALFI)

lFF: are you worried about tHe comPetitiveness oF ucits in tHe region, wHicH are currently widely sold tHrougHout asia?

ms: It is not a matter of competition between UCITS and regional passports. The aim of the UCITS regulation was to set a series of quality standards and to ensure a high level of investor protection, not necessarily to dominate in all markets. These standards, that have been constantly adapted and strengthened, have allowed UCITS funds to become over the years a worldwide recognised brand. The initiatives taken by some Asian countries to set up a similar passporting system can therefore be seen as a tribute to the UCITS success. But setting up such a system will take time – it took the UCITS label 20 years to reach the status it enjoys today – so I’m not overly worried about the Asian initiatives – provided that we (the European investment fund industry as a whole) manage to continue to ensure the high quality and the high level of investor protection that investors are now used to associate with UCITS and with Alternative Investment Funds.

lFF: tHe introduction oF tHe alternative investment Fund directive (aiFmd) Has Fuelled strong growtH in euroPean Fund domiciles. wHat are tHe main trends we see in tHe aiF sector in luxembourg and How do you see tHat develoPing in tHe coming years?

ms: The AIFMD has been introduced into Luxembourg law only in 2013, so that it is still a little bit too early to evaluate its full impact on our fund industry. What we can say is that today, 189 alternative investment fund managers have been authorised by the Luxembourg supervisory authority

luxembourg Fund industry | P. 5

(CSSF), which places Luxembourg in third place in Europe. The new type of limited partnership introduced alongside the implementation of the AIFMD has also been very well received by the alternative investment industry. Given the steadily rising demand for regulated investment products, we are confident that we will reach our objective of doubling the assets under management in Luxembourg alternative investment funds (Real Estate, Private Equity and hedge funds).

lFF: a key Project oF tHe new euroPean commission is tHe establisHment oF a caPital markets union, notably to reduce Fragmentation in Financial markets, diversiFy Financing sources and imProve access to caPital For business. wHat role do you see tHe luxembourg Financial centre, and more sPeciFically its Fund industry, in tHis ambitious Project?

ms: After years of intense – and expensive – regulation, it is time to let asset management companies concentrate on serving the investor and growing their business. Investment funds enable people to plan for their long-term financial security, they benefit from the economy and contribute to job creation. This coincides fully with the objective of the Capital Markets Union (CMU) project which is to integrate capital markets in order to finance jobs and growth more efficiently throughout the European Union. one concrete example that is relevant to our industry is the financing of SMEs by e.g. European Long Term Investment Funds (ELTIFs), pension schemes and debt funds. ALFI is very eager to see the CMU project go forward and on exploring the potential it offers the investment fund community.

lFF: looking aHead, wHat are tHe key oPPortunities and cHallenges For tHe asset management industry in luxembourg?

ms: From a technical point of view, the Luxembourg fund centre will continue to enhance its market infrastructure allowing it to service not only funds domiciled in Luxembourg, but also funds based abroad, thereby contributing to the evolution of Luxembourg from a fund domicile to a fully-fledged fund servicing center.

Regarding the challenges, the introduction of a financial transaction tax (FTT) that is back on the agenda remains a threat, since it will negatively impact financial activities that are considered essential to the functioning of the markets and the EU economy as a whole.

The investment fund industry will also have to cope with regulations initially not foreseen for the investment fund industry, such as those targeting systemically important institutions (SIFIs) and the shadow banking sector.

Last but not least, we see first signs of a growing risk that countries are trying to seal their markets off from foreign competitors, which is definitely an unfavourable development for a fund industry like ours whose business model is based on cross-border distribution.

But considering the opportunities which I have highlighted, we are very optimistic about the long term prospects of our industry in general and of our Luxembourg fund centre in particular. gm

Luxembourg’s financial centre provides an attractive environment for FinTech companies. With nearly 150 banks, 332 insurance and reinsurance companies, financial infrastructure companies such as the stock exchange and central securities depositories, as well as a world leading funds industry, the financial centre represents a significant potential client base for FinTech companies setting up in Luxembourg as Denis explains.

“Luxembourg is unique compared with other FinTech hubs in that financial services here form a much more significant share of the national economy. In Luxembourg, the FinTech industry exists on both sides of the financial landscape: financial services and technology. We have international FinTech companies, which have set up their headquarters in Luxembourg to be closer to their clients in the financial sector. We also have the new “disrupters” in the area of e-payments and e-money, that started to set up in Luxembourg a couple of years ago. So today, we have a nice set of FinTech companies coming from both sides which provides a good basis for developing this sector”.

The majority of FinTech companies are established firms of foreign origin, setting up in Luxembourg to benefit from the close proximity to clients and from the necessary talent pools, both in finance and technology, to develop their business. At present, there are around 150

| ThE FINTECh LANdSCApE IN LuxEMbOurgFINTECH

FintecH dossier | P. 6

In recent years, Luxembourg has been very successful in developing

a dynamic FinTech sector. A growing number of companies

from around the world, in particular start-ups, are opening

offices in Luxembourg to develop and market their product range.

Minister of Finance, Pierre Gramegna has made the further

development of the FinTech sector in Luxembourg one of his priorities. LFF talked to Pascal Denis, Partner

and Head of Advisory at KPMG Luxembourg who mapped and

analysed the Luxembourg FinTech sector with a view to defining

the future needs of the financial centres in terms of financial

technology readiness as well as enhancing its attractiveness for

new actors.

the fintech landscaPe in luxembourg

FinTech companies in Luxembourg, with roughly half of them providing IT infrastructure or IT services and the other half providing software or technology-based business services.

“If we look at the average age of a FinTech company here in Luxembourg, we see that almost two thirds have been started in the last three years, which gives you an idea of just how dynamic and young is the stage of acceleration that we are in. We see an alignment between the FinTech clusters that have developed and the clusters that exist in financial services. For instance we have a very strong FinTech cluster for private banking because of the expertise in wealth management in Luxembourg. Likewise, there are a large number of FinTech companies in the funds business which reflects Luxembourg’s position as the world’s second largest funds centre. We are also seeing a sustained inflow of new e-payments players as well as more recently a number of tech companies entering the insurance sector”, points out Denis.

next generation ict inFrastructure

Luxembourg offers the ideal environment to support new technology innovations in financial services. The country is ranked 9th worldwide when it comes to leveraging information and communication technologies (ICTs) for social and economic impact, according to the latest Global Information Technology Report published last month by the World Economic Forum. The report, which assesses 143 countries worldwide also ranks the Grand-Duchy as number one for international bandwidth and knowledge-intensive jobs. The importance of the ICT sector for the Luxembourg Government is also highlighted by the fact that the country is ranked as 4th and 5th, respectively in terms of Government success in ICT promotion and the importance of ICT to Government vision.

FinTech companies benefit from a best-in-class ICT infrastructure, in which the Luxembourg government has invested and strategically developed over the past decade. Luxembourg has one of the most modern data center parks in Europe, including 40% of all Tier IV data centres in Europe. As a low latency hub right in the centre of a number of major internet hubs in Europe, companies can serve Europe’s largest consumer markets out of just one physical location.

“based on the feedback from companies we met during the analysis, it is clear that proximity to potential clients is key for these companies, but the attractiveness of the Luxembourg FinTech ecosystem is also crucial, including access to a whole range of business services like incubators, law firms, service companies, IT hosting companies, university with its research center, data centers, and of course the presence of the big Four. The multilingual and skilled workforce is also a major asset”, explains Denis.

suPPortive FintecH ecosystem

The number of e-money and e-payment institutions in Luxembourg has tripled over the past three years and — bridging e-commerce and payment businesses — includes such big players as Amazon Payments,

FintecH dossier | P. 7

Pascal denisPartner,

Head of Advisory,

KPMG Luxembourg

Rakuten and Yapital of the German retail giant otto. These companies can benefit from a leading international financial centre and the EU passport to distribute services and products through 27 other European countries.

“The reason why these companies come to Luxembourg is because they want a foothold in Europe from where they can, in a regulated manner, develop their activities in multiple countries. Luxembourg has strict regulatory authorities, who are open-minded to innovation. Just to give you an example, the Luxembourg financial regulator, the CSSF was the first supervisory authority in Europe to take an official position on virtual currencies, defining them as scriptural money. Importantly, the CSSF stressed that financial activities involving virtual currencies (whether payment services or trading platforms) will need to be regulated”, says Denis.

access to establisHed Funding network

The Luxembourg government actively supports the research, development and innovation that has been fuelling the FinTech industry. There are a number of public and private incentives that complement each other that are available to companies, in addition to R&D support, attractive tax exemptions for Intellectual Property, as well as equity and bank financing. There is also a push from the government funded agencies offering support to the sector, to streamline and simplify access to funding to enable companies to start-up and develop quickly.

“Crucially, there is a strategic agenda at the political level to accelerate the development of the FinTech hub and that is driving a lot of new initiatives and funding opportunities”, points out Denis. “We are also seeing a growing interest in supporting FinTech companies from the more conservative sectors of the financial centre. For example, we are seeing more Family Offices and private banks trying to provide to their high-net-worth individual clients an easier access to investments in FinTech either directly or through an intermediary fund being managed by a bank or family office. We are also seeing more new players, like business angel networks and venture capitalists showing interest to establish strong links with Luxembourg”, Denis concludes. gm

“If we look at the average age of a FinTech company

here in Luxembourg, we see that almost two thirds

have been started in the last three years, which gives

you an idea of just how dynamic and young the

industry is".

FintecH dossier | P. 8

Pascal denis

scePticism is Part oF tHe game

History has shown that innovations are usually seen as a bad idea when first pitched. People are wary when you speak about disruption. Scepticism is part of the game.

Pierre-olivier Rotheval, Head of Innovation at BIL, explains: “Just look at Microsoft CEO Steve ballmer who first claimed that no one would be interested by the most expensive phone in the world, that didn’t even come with a keyboard which made it a terrible machine to email. The iphone has been one of the most important innovations in the last 30 years”.

The role of innovation and R&D has always been part of the business model of the industrial and manufacturing sector, looking to invent new technologies and products.

“It was not that banks did not innovate at all, but they followed the larger technological trends such as phones, telex and the internet. These were the technologies that brought the first big disruptions to banks and their service models”, Rotheval adds. “If you compare banks with FinTech companies, of course we are slower. The constraints are not the same. being regulated and being compliant has a price tag”.

Although most FinTech initiatives are relatively small and currently do not pose an immediate threat to major financial institutions, their rate of growth and the scalability of their platforms suggest that the banks should start responding sooner rather than later.

The role of technology and innovation has become ever more

important to banks all over the world. FinTech is changing the financial sector in as dramatic

a fashion as trains transformed transportation and the internet

transformed communication.

In recent years, Luxembourg has clearly demonstrated its ambition to become a leading FinTech hub.

LFF spoke with the management of BIL and BGL BNP Paribas about the reshaping of the banking sector and

how FinTech will change the way we handle our money.

fintech and the future of banking

| FINTECh ANd ThE FuTurE OF bANkINgFINTECH

FintecH dossier | P. 9

“Today, innovation is not the question… the question is at what pace banks can innovate”, says Marc Aguilar, Manager for digital innovation at BGL BNP Paribas. “I don’t believe that start-ups will succeed to disrupt banking the way they changed the book or coffee industry. The threat is not as strong as in other industries”.

But how can established financial institutions best deal with this new challenger?

Historically, the financial sector has mainly focused on designing new financial products. Now, a different approach is required, namely a strategy of co-operation.

According to Pierre-olivier Rotheval, there are three types of co-operation possible: banks that buy FinTech companies, banks that finance FinTech companies, and banks that agree collaboration deals to integrate certain technologies, such as with Digicash in Luxembourg.

“At bIL, we don’t exclude any of these options. We meet a lot of start-ups, including big players from foreign countries. Some are even bigger than us and are contemplating using Luxembourg as their headquarters”.

Investments in the FinTech field are reaching new highs. “Last week alone, more than 200 million dollars were invested worldwide in FinTech. We have never seen such figures before”, he adds.

growing investments

According to a new report by Accenture, global investment in FinTech ventures tripled from 4.05 bn USD in 2013 to 12.2 bn USD in 2014, with Europe being the fastest growing region in the world. Last year FinTech investment increased at more than three times the rate of overall venture capital investment.

While the United States still captures the lion’s share of FinTech investment, Europe experienced the highest growth rate with an increase of 215 percent to 1.48 bn USD in 2014.

But what is exactly causing this growth? one of the reasons is that there has been an increase in financial technology funding making it one of the most popular markets for start-ups. In addition, banking firms are increasingly partnering with the industry.

During the development stage, financial sector start-ups often encounter barriers. Through partnership with mature financial institutions, FinTech firms can access both growth capital and knowledge of critical industry issues, such as legislation and regulation. In turn, financial institutions can use the knowledge and intelligence gathered to make strategic choices and set future priorities.

FintecH dossier | P. 10

Pierre-olivier rotheval

Head of Innovation,

BIL

openness to start-ups is beneficial to bank employees.

“It opens up their mind. It is important to learn from the start-up culture, not only from their products. bankers need to understand what it means to be a start-upper”, adds Rotheval.

BGL BNP Paribas opened the lux future lab, providing office space, training, coaching and support for new entrepreneurial activity in Luxembourg.

“If you want to keep pace with new technologies you have to approach innovation at an international level”, explains Marc Aguilar. “We bring an international network as well as consultancy to the start-ups”.

tHe client

The Luxembourg financial centre is by definition international. If Luxembourg banks want to grow, it needs to use digital channels to attract and serve new clients. “This would require acquisition channels that allow banks to get customers outside Luxembourg without the need for them to come physically to Luxembourg”, explains Romain Girst, Director Retail Banking at BGL BNP Paribas.

What are the digital services that clients expect?

“We need to be more client-centric. Customers want simple and efficient solutions. It must be easier to do or not to be done at all. Web-banking solutions for all the transactions and different devices. No one wants to be excluded because of their device”, adds Romain Girst.

Speed is key. Especially young people want to be able to have an answer instantly. They barely make a phone call.

“These instant answers can be provided via channels such as on-line banking but some clients also expect a relationship with their banks via Whatsapp or Facebook. The challenge is that these channels are interesting but we cannot rely on then without having the necessary security systems in place”, continues Pierre-olivier Rotheval. “Most banks use legacy systems that are not real time systems. Clients want real time systems and immediate payments”.

Small businesses also like to consolidate bank accounts with a provider that could reduce the time involved in the loan application process and provide more certainty of the outcome. one of the examples mentioned by Rotheval is Kabbage, an online financing technology and data company based in the United States which lends money to small businesses and consumers. The company simplified the lengthy, manual loan application process to one that is 100% online and automated. “kabbage gives you an answers in less than 7 minutes for an amount of less than 100.000 uSd”.

FintecH dossier | P. 11

marc aguilar

Manager for digital innovation,

BGL BNP Paribas

romain girst

Director Retail Banking,

BGL BNP Paribas

wHatsaPP For Hnwi?

Another trend is that private bankers are increasingly turning to financial technology to enhance the client/advisor relationship, not just deliver self-service tools.

Hubert Musseau, CEo Wealth Management at BGL BNP Paribas, explains: “We must accompany our clients into the digital world. The client relationship has changed. We need to reinvent the way we manage the proximity with our clients and offer the right solution at the right time. FinTech is about change management”.

What about the role of the face-to-face meeting in wealth management?

“Yes, private banking is still a people to people business. but it is not sufficient. The modern private banker needs to offer digital solutions that brings him closer to the client”.

BGL BNP Paribas launched a satisfaction survey to understand its clients’ needs and expectations. “(u)hNWI are looking for basic functionalities that are often similar to regular clients. however, what is different is that they want more advisory. They want to have simple tools and information that allow them to take the right decision at the right time”, adds Musseau.

big data

Banks are always trusted with a lot of information regarding their clients. This information can help them to provide better services.

“The customer base of banks is very valuable. banks face strong competition, but it is still the banks that have gained the trust and relationship with their client. banks have to leverage these points”, says Aguilar.

As the number of clients within an industry increases, banks are entrusted with more information in their systems that has to be stored securely. Big Data could simplify everything.

The banking industry can improve their professional relationships with their clients and be able to understand them better. It makes it easy for banks to offer schemes that are direct and personalised and tailor their marketing strategies accordingly.

When Big Data provides such detailed information to a bank its responsibility increases as well. They must protect the information and make sure that the information given to them is not misused in any way.

FintecH dossier | P. 12

Hubert musseau

CEo Wealth Management,

BGL BNP Paribas

exPansion to non-bank markets

FinTech will also bring banks to large non-bank markets in the developing world.

Paying by using your mobile phone is easier in Nairobi than it is in London or New York, thanks to Kenya’s world-leading mobile-money system, M-PESA.

“About 43% of the gdp of kenia flow through that service”, says Marc Aguilar. It lets people transfer cash using their phones, and is by far the most successful scheme of its type in the world.

M-PESA is now used by over 17 million Kenyans, equivalent to more than two-thirds of the adult population. lr

FintecH dossier | P. 13

jean guillDirector General, National Supervisory Authority, CSSF

lFF: How does tHe cssF see tHe Future develoPment oF tHe regulatory Frame-work For FintecH in luxembourg?

Jg: Even though the CSSF considers that some regulatory changes have to occur in order to accompany the FinTech development in Luxembourg, for example with regard to KYC requirements which should be updated taking into account the specific business models of digital finance, we believe that the existing regulatory framework is sufficiently comprehensive to integrate financial technology into the finance sector as a first stage. Further development of this sector will involve the enhancement of the regulatory process with the objective of having an inclusive regulatory environment for FinTech in Luxembourg, having identified the specific needs of this new industry.

lFF: wHat are tHe most imPortant cHallenges and oPPortunities to be taken into consideration For tHe develoPment oF tHis Framework?

Jg: It is a big opportunity for Luxembourg to embrace new financial technologies and we believe that the emergence of digital finance will change the competitive landscape for financial services. Challenges for Luxembourg will be to manage the integration of start-up activities as well as promoting and developing innovative digital financial products, by trying to apply financial regulation in a proportionate way to those new developments whilst assisting these new players in adapting to the specific culture and behaviour of the financial sector. A further challenge will be to convince traditional market players that the future is in digital finance.

For Luxembourg the opportunity would be to develop a highly specialised FinTech industry ready to provide services to any financial professional who will have to rely on outsourcing and third party services in order to remain competitive.

regulation

Jean guill, director general,

CSSF

raise caPital

For many founders, raising seed and early stage capital is the most stressful part of getting their startup off the ground. Founders who are unable to personally finance their early stage startup activities quickly discover the need to raise external funding.

In contrast to common opinion, governments are important early-stage financiers. In Luxembourg, public financial aid can complement private funding of young innovative start-up.

“public funding schemes are always co-financed, we cover usually around 40% of eligible costs of a project”, says Mario Grotz, Head of Innovation at the Ministry of Economy. “Our budget is specifically set aside for young innovative enterprises with a high growth potential. We actively address the funding needs of these businesses during their development phase by matching equity investments”.

Having worked for over 15 years in the field of innovation, Mr Grotz has seen the tremendous increase of innovative projects handled by the Ministry. “10 years ago we had a dealflow of around 100 projects and 10 start-ups created each year. Today, this number has increased enormously

how to make your business grow in

luxembourg

Start-ups will find several incubators and accelerators in

Luxembourg for different stages of their development. They range from private to public initiatives, each of them offering services to

cater for specific needs.

LFF showcases a selection of support initiatives alongside the usual founding process of a start-up having left the garage.

| hOW TO MAkE YOur buSINESS grOW IN LuxEMbOurgFINTECH

FintecH dossier | P. 14

to reach an amount of around 350 projects and 40 co-financed projects”. According to Grotz, the majority of these start-ups comes from the ICT sector while 5 to 10 are related to FinTech.

on top of the current funding scheme, the Ministry of Economy is working on a new funding vehicle, a seed investment of 15 to 20 million EUR dedicated to very early stage companies.

However, the success of a start-up rarely depends on public funding only, but also requires private sources, which can take the form of private equity, venture capital or angel money, a group of individuals, often former entrepreneurs themselves, who make small investments in new companies.

“Making the bridge between public and private financing is of crucial importance at such an early stage of a company’s lifecycle”, says Frédéric Becker, Head of Start-up Support at Luxinnovation, the national agency for innovation and research that was founded back in 1984 by several public entities.

The agency which has seen entrepreneurs from over 50 countries assists start-ups during their application process for public R&D and innovation funding schemes. It helps prepare application files prior to their submission to the Ministry of Economy, while also introducing entrepreneurs to private investors such as entrepreneurial ventures and business angels, the most frequent source of financing at the seed stage.

In 2014, Luxinnovation supported nearly 300 projects and has been involved in the establishment of 45 new start-ups, from which many are active in the field of e-payments, e-invoicing, crypto currencies and big data. Amongst them are Digicash and Paycash, two Luxembourg-founded successful payment services.

nurture your business

After having survived the early stages of development, start-ups will have to get to the next level by starting to grow. In fact, without proper advice, around 90% of start-ups fail during their first years. The role of tutors becomes increasingly important.

“Today start-ups run against time as innovation cycles become shorter and shorter”, says Karin Schintgen, Director of lux future lab. The future lab is the innovation platform of Luxembourg’s largest retail bank, BGL BNP Paribas. The lux future lab puts entrepreneurship and education at the core of its values. Two parallel programs, an entrepreneurial platform serving as an incubator for start-ups, and a training platform for its core clients - people at the cross-roads of their professional career - are at the applicants disposal.

“For the start-up, everything that takes their attention away from their market, clients and products is a real problem”, Ms Schintgen adds.Therefore the future lab acts as a facilitator providing affordable office space, training, consulting and access to a global network making sure

FintecH dossier | P. 15

Frédéric beckerHead of Start-up Support,

Luxinnovation

mario grotz

Head of Innovation,

Ministry of Economy

start-ups can learn from the best. one of lux future lab’s great assets is the access it offers to its own experts, key contacts, or business angels as well as its capacity to follow worldwide similar disruptive technology developments.

"Lux future lab is part of bgL’s Corporate Social responsibility (CSr). We wanted to go beyond the classic definition of CSr and back to the roots of our core business as a major economic actor in Luxembourg. by supporting entrepreneurship and training we ambition to impact the social and economic dynamics of our country and be where tomorrow’s economy will be born. In a global world start-ups need to go cross-border real fast and we nowadays operate incubators or technology hubs also in other countries such as France, belgium, Turkey, the uSA, China etc. So besides hosting, training and consulting we can also support our start-ups through our international networks”, she says.

What makes the future lab even more attractive to FinTech companies is its location in the heart of the city’s financial centre and close to major financial operators in the city centre.

As of today, the incubator hosts 16 innovative start-ups as well as 3 service providers coming from as far away as the USA, Canada or Japan.

Technoport, a national technology-oriented business incubator is another key player in the Luxembourg FinTech ecosystem. While applications are open to anyone whishing to set up a business, only the most viable and innovative will be granted the incubator’s guidance in setting up a business plan while benefiting from its global network.

“A concrete example is the one of a recent company that was looking for a first seed investor. We put them in touch with a potential investor who eventually decided to make a first investment in the company. This allowed them to hire a team, do a re-engineering and re-design of the product and launch the production of the first batch of their product”, says Diego De Biasio, CEo of the Technoport, which received 158 applications in 2014, from which 52% came from the pure ICT field.

The Technoport’s services don’t stop here. Aware of the crucial importance of being able to test out products before going on the market, the tech-oriented incubator offers access to the Fab Lab, a digital manufacturing laboratory that is part of a growing global network allowing entrepreneurs to do rapid prototyping, collect user feedback and pivot or iterate on the development of their projects.

be PrePared For tHe international maratHon

“Many initiatives, whether they are public or private, exist to assist companies in the early stages of their business. but when it comes to expanding globally, entrepreneurs start to face quite different and complex challenges”, says Laurent Probst, partner in charge of the PwC's Accelerator network.

FintecH dossier | P. 16

laurent Probst

Partner,

PwC Accelerator

diego de biasioCEo,

Technoport

“This situation poses even greater challenges for companies which have an international dNA as they see market traction and a push by their clients outside of their domestic area”, he adds.

The accelerator helps fill the critical knowledge and sophistication gaps that make it possible for ambitious SMEs with an international DNA to grow internationally.

Focusing on top-flight technology companies who already generate substantial revenues on their domestic market, PwC's Accelerator helps them mind the gap to international markets by fixing their internationalisation issues, and decomplexifying their internationalisation journey.

"Conquering global markets is neither a sprint nor a solo race, but is rather akin to running a marathon and it requires the involvement of very different partners at each step in the process. SMEs need to build ties with financial and institutional partners who will be able to help them gain a global reach. building a network is a prerequisite to conquering international markets. There are many advantages available, including fast access to business opportunities, new areas of expertise on a global scale and diversified sources of financing. With the Accelerator, entrepreneurs have access to a new network of partners in whom we already have confidence”, explains PwC.

PwC’s Accelerator has built a centralised ecosystem bringing together high-tech companies specialised investors, such as venture capitalists, private equity and family offices.

PwC's Accelerator has proven to be a pioneering platform designed to accelerate the connections between the different stakeholders.

HelPing set uP a winning team

“The most difficult challenge they, and indirectly we might face is the one of the team. We regularly face situations where individual projects owners need to find either a business profile or a technical person to develop their project”, says Diego De Biasio, CEo of Technoport.

In order to help entrepreneurs overcome this challenge, Technoport organises hackatons around different topics so that people from different backgrounds can meet and get to know each other.

“These events can be the right places to meet co-founders or people interested in joining new projects and help entrepreneurs in the process of finding punctual resources”, says the Technoport.

Setting up a winning team takes all its importance in the acceleration stage.

often start-ups don’t realise how important it is to build a team with a winning mentality. ob

FintecH dossier | P. 17

karin schintgen

Director,

Lux future lab

lFF: wHat are tHe beneFits For FintecH start-uPs in luxembourg?

rm: First of all, start-ups can benefit from various types of financial support from both the public administration and the private sector through grants, subsidies, and seed funding. Since 2010, Digicash has worked closely with the Ministry of Economy and Luxembourg’s investment bank (SNCI) to obtain funding.

Entrepreneurs can also count on high level advice and support delivered by national agencies such as Luxinnovation, the Big Four and international law firms based in Luxembourg. Some of these supportive agencies and firms have built programmes, incubators, accelerators or infrastructures designed specifically for start-ups.

When it comes to e-payments, which is our business, many leading global players have chosen to establish their European headquarters in Luxembourg. In addition to raising visibility and creating a prosperous environment for developing payment businesses, the high concentration of players eases the exchange of ideas and highlights best practice.

Digicash enables banks to be at the heart of the mobile payment

revolution by transforming your smartphone into a mobile

payment tool. Starting as an R&D project in 2010 co-funded by the

Luxembourg Government, Digicash has become Luxembourg’s

bank-led mobile payment network enabling retail banks’ clients

to make payments via an App installed on a smartphone.

In 2014, the company completed a 2.2 million EUR funding round

backed by its founders, the Luxembourg investment bank

(SNCI) and the Luxembourg Government, to start a new phase

of development both on a national and international level.

LFF spoke with Digicash Payments co-founder and all-round

entrepreneur, Raoul Mulheims.

building a mobile Payment ecosystem

in luxembourg

| buILdINg A MObILE pAYMENT ECOSYSTEM IN LuxEMbOurgFINTECH

FintecH dossier | P. 18

From an operational point of view, Luxembourg is one of the best places in the world to start a payment business and to obtain an EU license. In our experience, the Luxembourg regulator, the CSSF, has a vast experience in dealing with payment businesses and there are many advisors and consultants specialising in regulatory matters that are able to help out in this area. We obtained our license in less than six months – in other countries it can take up to 18 months.

I would also like to highlight that Luxembourg has very responsive and pragmatic public authorities. This helps us to move even faster and receive prompt advice.

lFF: wHat do you tHink about tHe availability oF HigHly-skilled and qualiFied workers in luxembourg?

rm: Luxembourg has become a hub for the recruitment of high-profile IT and financial specialists and attracts talented people from around the world. In particular, Luxembourg has the highest number of developers in the world per capita (39.8 developers per 1,000 people) above Iceland, Sweden and Israel, according to stackoverflow.com – a reference website for computer geeks.

An impressive 71% of Luxembourg’s workforce are foreigners which makes it a melting-point and ensures that new talent adapts quickly to daily life which has a genuine international feel.

lFF: is tHe Proximity to tHe Financial centre an asset?

rm: It is even mandatory! In our case, banks are our clients. We provide them with a powerful solution to fight against disintermediation and maintain their control over payments. From the beginning, our goal

FintecH dossier | P. 19

raoul mulheimsCo-founder,

Digicash Payments

digicash beacon terminal

was to create a new ecosystem in Luxembourg where all banks issue a common product. This setup required a strong partnership with all stakeholders. The Luxembourg state-owned BCEE was the first bank willing to take part in this adventure. PoST Luxembourg, BIL and BGL BNP Paribas followed. Luxembourg-headquartered banks have shown great open-mindedness to partner with small players.

This kind of partnership supports the start-ups that work under the FinTech label. However, proximity to the financial centre also encourages those who have adopted an innovative model based on user experience, as well as those who have chosen a new model based on a partnership with banks (for example, “PSF de support” or IT companies). There are also other hybrid models like ours, dealing with banks and integrating a highly innovative dimension based on user experience.

lFF: last year digicasH raised 2.2 million eur: wHy and How did you raise tHis money?

rm: our company together with the Luxembourg investment bank (SNCI) and the support of the Luxembourg Government, completed a new funding round of 2.2 million EUR in May 2014. The main contribution was made by Digicash founders. The SNCI and the Government (via a grant) covered the remainder of this seed funding round.

This funding has enabled us to consolidate Digicash’s mobile payment scheme and our activities in Luxembourg. our aim is for Digicash to become part of Luxembourg residents’ daily lives and we are succeeding. Today, the four main retail financial institutions in the country issue Digicash, making it available to over 80% of primary bank accounts. Furthermore, over 10% of the population has already downloaded the App. In order to increase its use, we are still developing our merchant network and we are planning the launch of several major innovations in the coming months such as the Digicash Beacon terminals and a P2P feature.

lFF: How do you want to take your Project internationally?

rm: Based on this success story, we now aim to provide international players with our premium digital payment technology. To do so, we will start a new funding round in the coming months in order to accelerate our international development. But for the moment, we are increasing our presence at international events and are deeply involved in the creation of a strong FinTech network in Luxembourg. In that context, LFF and Luxembourg Embassies help us to make contacts in many countries. The reputation of Luxembourg in financial matters is really helpful as we continue to export our products and services. gm

FintecH dossier | P. 20

It was Luxembourg’s reputation as the Eurozone’s leading financial centre that initially attracted Spallian to move to Luxembourg as Thibaud Prouveur explains.

"The Luxembourg financial centre is a global market, so if you are successful with a product in Luxembourg, there is a good chance it will work anywhere else".

ICT infrastructure and connectivity were important factors, and the company was able to switch quickly from its provider in France to one of Luxembourg’s state-of-the-art Tier IV datacentres. PWC Accelerator acted quickly to provide the company with offices so they could move seamlessly from Paris to Luxembourg, with the aim of going international quickly.

"Everything was set up for us. We had access to conference rooms, so we could meet with potential clients and investors immediately without coming across as being small and new in Luxembourg", Thibaud adds.

The accelerator set about putting the company in touch with different types of financiers who could not only provide funding, but business accuman and financial sector expertise.

"We had very influential investors helping us with the development of our business plan and making sure that we were developing our product in the right place. What we didn’t want was back seat investors who would only be looking to make money quickly with a short term investment strategy".

The accelerator not only helped Spallian to go global faster, but it also provided them with local market intelligence and access to business networks.

In 2012, French software company, Spallian identified a new market

opportunity to develop a cutting edge tool dedicated to

international asset managers. In such a competitive landscape it

needed to act quickly, and turned to Luxembourg’s PWC Accelerator to

help them find the right partners to develop the product.

LFF talked with Thibaud Prouveur, Partner and Sales Director at Spallian to find out why the company moved

to Luxembourg to access funding and to leverage the financial centre

client base to develop their solution.

accelerating a fintech business

in luxembourg

| ACCELErATINg A FINTECh buSINESS IN LuxEMbOurgFINTECH

FintecH dossier | P. 21

mapping and dashboard visualisation of big data© S

palli

an

"What pWC have helped us with, and this has been the major thing they have done apart from all the intelligence they put into our business plan, was introduce us to the key players. They looked at our product and said, look you should go to see the head of asset management at this bank, you should go to see the head of wealth management at this bank. They introduced us to all these people, and that is how we started developing and tailoring the software".

It was an introduction to the CEo of one of Luxembourg’s leading custodian banks that led to the development of the company’s latest product which will launch in June. The bank was looking to create a product around big data and data analytics as Thibaud explains.

"The bank was looking to offer extra services to it’s clients and differentiate itself from other custodian banks. It realised that it had vast amounts of data that it was not exploiting, so it was looking for ways to leverage it".

Spallian was tasked with developing a software product that the bank could offer to asset managers worldwide to help them understand more about the market and exploit the available data to enhance their business development.

"It is a tool that asset managers don’t have so far, so it is a strategically important project for us”, points out Thibuad. “It couldn’t have been done from paris, it could only have been done from Luxembourg because of its unique ecosystem and the close proximity to key players. IT is recognised in Luxembourg and companies are willing to invest more in new technology than they would in France. here, banks view FinTech as part of new revenue streams, and as long as there is a return on their investment, they are willing to make the investment".

Spallian successfully applied for an R&D grant from the Luxembourg Government, and it benefits from a tax refund on salaried staff involved in R&D. The support is potentially worth up to one million euros over three years as Thibaud explains.

"r&d support is common across Europe to support innovation but most often businesses face long delays in being able to access that funding. In France, for example, you get your refund two years down the line, but in Luxembourg, the tax rebate is paid every quarter, which makes a big difference in terms of cash flow”.

Last year Spallian moved to new offices in the heart of Luxembourg’s city centre. The financial support is enabling the business to expand their staff count to ten, with the aim of the doubling that figure in the next twelve months.

"In Luxembourg, we have found highly skilled staff. Labour laws, which allow for a trial period of six months to be included in an employment contract, have also allowed us to take a chance and test fresh talent which is key to our future development". gm

FintecH dossier | P. 22

thibaud Prouveur

Partner and Sales Director,

Spallian

mapping and dashboard visualisation of big data in luxembourg

© S

palli

an

In 2012, the French company Leetchi.com was looking for a base to develop a new FinTech payment solution for marketplace, crowdfunding platforms and collaborative economy players. one of the main technical challenges it faced was to implement a payment management system which was international and respected European regulations.

“We needed to apply for an e-money issuer license and at that time it wasn’t available in France, so we decided to look at what was available in other countries. We had the choice of Spain, uk, belgium or Luxembourg”, explains Mazeries. “We really didn’t have to think that much, because Luxembourg has everything we need: a solid financial regulator, a banking hub where we could develop a strong network of banking partners, and given Luxembourg’s geographical position in the heart of Europe, a good place to attack European markets”.

suPPortive regulatory Framework

MANGoPAY selected a Luxembourg law firm to accompany the business on it’s quest for an e-money issuer license. “It was as difficult to obtain the license in Luxembourg as it would have been in any other country”, points out Mazeries. “The financial regulator, the CSSF, wanted to go deeply into compliance and anti-money laundering (AML) requirements. What pleased us most was the business perspective the CSSF

Launched in May 2013, MANGoPAY offers a FinTech payments solution

for marketplaces, crowdfunding platforms and collaborative

economy players. The business is part of The Leetchi group which runs

the leading European online group payment solution, Leetchi.com.MANGoPAY chose to set up its

headquarters in Luxembourg to develop the business and secure

a financial service license to facilitate growth.

LFF spoke with MANGoPAY Director, Romain Mazeries (CEo of

Leetchi Corp SA).

mangoPay goes international

| MANgOpAY gOES INTErNATIONALFINTECH

FintecH dossier | P. 23

had on our product and understanding of what we were doing and the potential solutions”.

In order to enable the business to distribute its payment technology across the European Union, MANGoPAY set about establishing a network of banking partners.

“Luxembourg is a small but very internationally focused country, so bankers are opened minded and have a unique cross-border expertise. From our bank in Luxembourg, we were able to open accounts with twelve different banking partners across the Eu. For a start-up, it was also significant that the cost was minimal in terms of fees and the process was relatively straightforward”.

Luxembourg’s data centers offer a full range of services including colocation services, virtual private servers, managed hosting and web hosting. With over 40,000 m2 of net floor space in 19 data centres across country, Mazeries set about exploring the full range of data services available.

“We needed a dedicated and very special infrastructure not only to meet our specific IT needs but to assure the regulatory authorities and our investors”, points out Mazeries. “The data center we selected, in terms of security is one of the best in the world, but it is also a global leader in innovation. We have a great relationship with our data centre which has followed our needs, and it has changed its way of thinking and its products to support us. It’s something we appreciate and because we are a small company it is very important that we have this insurance”.

With more than 350 European clients since its launch in April 2013, Mazeries hopes MANGoPAY can become a champion for Luxembourg, to inspire more entrepreuners and to give the country’s growing FinTech sector more visibility.

“It is a great country to develop your business from, and attack the European market and to grow internationally. Our aim now is to open up to new markets”. gm

FintecH dossier | P. 24

romain mazeries

Director,

Mangopay

Can psychology help us better understand financial markets and provide us with hands-on stock picking strategies? Behavioural finance theorists suggest they can and this led Colin, at the time a fund manager in Luxembourg, to begin his investigation into how the use of factor-based algorithms could help asset managers beating the market.

"After the internet bubble exploded, the forecasting value of sell-side analysts was questioned, as roughly 80% of them had a buy or Strong buy rating just before the collapse. In the following years, academics found that they indeed had value, but probably not in the way initially thought. Several pieces of research also identified other inefficiencies in the stock market that could be exploited, mainly explained by behavioural patterns. They are the foundation of several Smart betas”, explains Colin.

The idea behind the financial platform is to enable professional money managers to use stock selection and asset allocation models based on so-called market anomalies, now also known as Smart Betas. The “behave!” application equips the client to create his own investment universe or import a portfolio, and backtest it with various models exploiting inefficiencies which have been shown to exist for an extended period of time in various markets and countries, avoiding forward looking and survivorship biases.

The Luxembourg company AlphaSearch, now sells its software

on the Bloomberg App store. Its newest platform, "behave! Pro",

exploits anomalies and inefficiencies in worldwide equity markets mainly explained by behavioural biases. The

software is used around the world by investment professionals to support

stock selection and sector allocation.

LFF spoke with Alexandre Colin, founder of AlphaSearch.

develoPing a bloomberg aPP in

luxembourg.

| dEvELOpINg A bLOOMbErg App IN LuxEMbOurgFINTECH

FintecH dossier | P. 25

“Our aim was to build a platform that enabled the user to define his own investment universe, apply the proprietary models that we have developed based on price, volume and numerous consensus data published by analysts. The user would then apply these models to the universe that they have created to search for price Momentum, Earnings Momentum or value anomalies that they can exploit. Typically, the fund or portfolio manager would use the decile ranking produced by behave! to either screen for new buy or sell ideas in his own investment universe, or combine it with his fundamental and technical analysis. We also have traders who target shorter term investment horizons, and hence generally use models built around earnings momentum. We are in the process of adding a new Low volatility model, in order to cover all generic Smart betas, an investment strategy which exhibits the advantages of both passive and active management”, points out Colin.

unique ecosystem For growtH

Luxembourg’s financial centre offered the ideal environment to support Colin as he set about developing his product.

“There has always been a spirit of entrepreneurship in Luxembourg and it has always been very easy to start a company: administration is very light and the government has always been very pragmatic. The international nature of Luxembourg also makes it very easy to set up a new company and find the competences you need would it be legal, accounting or IT”.

Beyond finding a ready market for his services, Luxembourg was also the perfect location to grow and develop AlphaSearch internationally.

“It’s often taken for granted but the location of the grand duchy within Europe and the proximity of the airport makes it very easy to prospect in an efficient manner. Also, when you go abroad, if you say you come from Luxembourg, it’s a recognised financial centre, so I would say that it definitely adds to your credibility when your are a new company as you market your services abroad”.

staying one steP aHead oF tHe market

In 2012, the company was invited by Bloomberg to launch "behave!" on their app portal, which is now distributed around the world through the 320,000 Bloomberg Professional terminals.

“There is always competition, but there are few actors delivering the type of turn-key service that we offer. In fact, the real competition comes from the target users themselves when they have developed their own filters or models, but which are usually less sophisticated than what we offer, or cumbersome to update and maintain. And this is where outsourcing can make a difference. As we continue to relentlessly improve our software and models, we are confident that we will continue to thrive from our base in Luxembourg”.

Looking ahead, the company plans to take advantage of the Bloomberg distribution network by closely targeting the Asian market where the behavioral anomalies can also be strong. gm

FintecH dossier | P. 26

alexandre colin

Founder,

AlphaSearch

Services allowing consumers to perform banking and payment operations on their mobile phones are rapidly advancing in Africa, leading the way for the rest of the world.

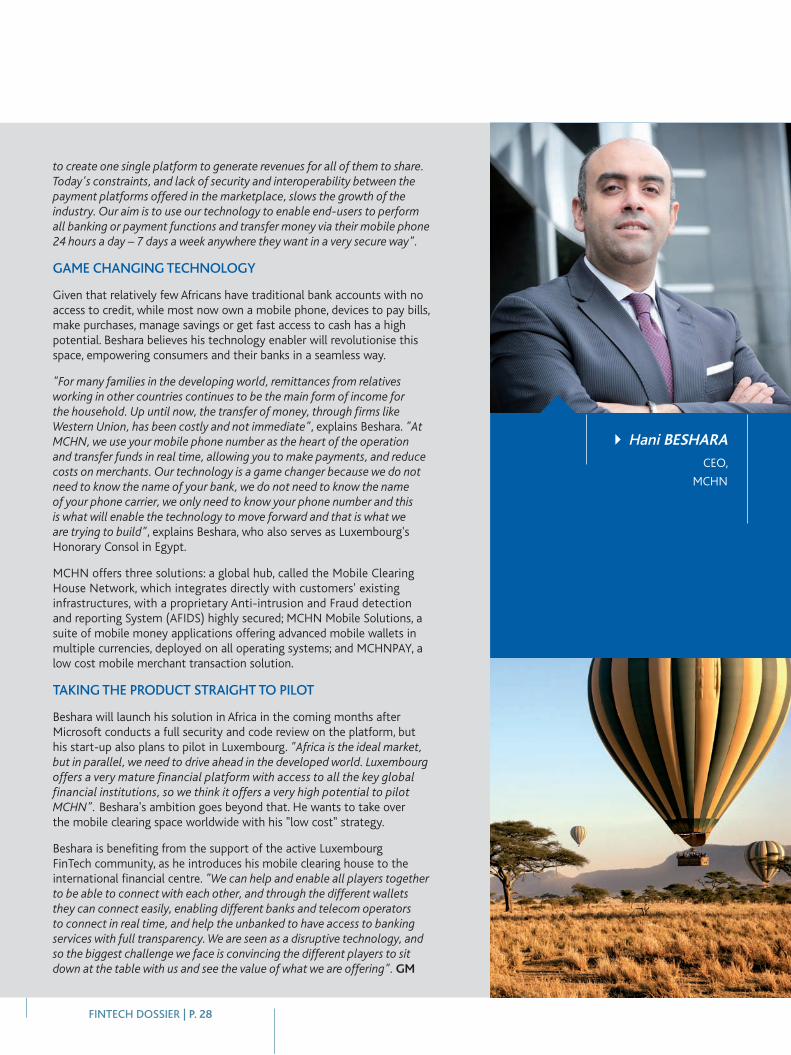

"Mobile phones have penetrated African markets on an astronomical scale because they are a cheap alternative to the expensive and limited landline phone service. As a result, each African has one to two mobile phones so this is why Africa is the first market globally when it comes to mobile money", explains MCHN CEo Hani Beshara.

In 2010, the visionary entrepreneur chose Luxembourg as the headquarters for his company financially backed by two global entrepreneurs - olivier Dassault and Jean Claude Mimran. "We were encouraged by the support on offer from the government and that led us to set up in Luxembourg. The grand duchy is a very supportive environment for start-ups: SkYpE started in Luxembourg, you have other companies, from the uS and Asia, who are also here", adds Beshara whose ambition is to go global out of Luxembourg.

In 2011, the business was selected to join the prestigious Microsoft BizSpark one program, made up of some of the strongest start-ups from over 100 countries around the world. Beshara, with the backing of Microsoft, soon began working with telecom operators and banks across Africa to build low-cost payment hubs, to facilitate economic growth across the continent.

"The main problem you have in Africa today is that you have a variety of players - different banks, telecommunications companies - and everyone is doing their own thing. They don't have one system that allows the different actors into the mobile payment market to communicate with each other

luxembourg start-uP introduces africa's

first mobile clearing house

| LuxEMbOurg STArT-up INTrOduCES AFrICA'S FIrST MObILE CLEArINg hOuSEFINTECH

FintecH dossier | P. 27

A Luxembourg start-up, The Mobile Clearinghouse Network (MCHN), is launching the first mobile clearing house in Africa

and beyond, interconnecting all financial institutions, banks,

payment technologies and wireless carriers under a secure platform. The company, backed by Microsoft, aims

to create low cost, interoperable, agnostic cashless societies, to enable instant monetary and non-monetary

transactions.

MCHN CEo and founder Hani Beshara talks to LFF about his

revolutionary plans to usher the developing world into a new

age of opportunity and financial development.

FintecH dossier | P. 28

to create one single platform to generate revenues for all of them to share. Today's constraints, and lack of security and interoperability between the payment platforms offered in the marketplace, slows the growth of the industry. Our aim is to use our technology to enable end-users to perform all banking or payment functions and transfer money via their mobile phone 24 hours a day – 7 days a week anywhere they want in a very secure way".

game cHanging tecHnology

Given that relatively few Africans have traditional bank accounts with no access to credit, while most now own a mobile phone, devices to pay bills, make purchases, manage savings or get fast access to cash has a high potential. Beshara believes his technology enabler will revolutionise this space, empowering consumers and their banks in a seamless way.

"For many families in the developing world, remittances from relatives working in other countries continues to be the main form of income for the household. up until now, the transfer of money, through firms like Western union, has been costly and not immediate", explains Beshara. "At MChN, we use your mobile phone number as the heart of the operation and transfer funds in real time, allowing you to make payments, and reduce costs on merchants. Our technology is a game changer because we do not need to know the name of your bank, we do not need to know the name of your phone carrier, we only need to know your phone number and this is what will enable the technology to move forward and that is what we are trying to build", explains Beshara, who also serves as Luxembourg's Honorary Consol in Egypt.

MCHN offers three solutions: a global hub, called the Mobile Clearing House Network, which integrates directly with customers' existing infrastructures, with a proprietary Anti-intrusion and Fraud detection and reporting System (AFIDS) highly secured; MCHN Mobile Solutions, a suite of mobile money applications offering advanced mobile wallets in multiple currencies, deployed on all operating systems; and MCHNPAY, a low cost mobile merchant transaction solution.

taking tHe Product straigHt to Pilot

Beshara will launch his solution in Africa in the coming months after Microsoft conducts a full security and code review on the platform, but his start-up also plans to pilot in Luxembourg. "Africa is the ideal market, but in parallel, we need to drive ahead in the developed world. Luxembourg offers a very mature financial platform with access to all the key global financial institutions, so we think it offers a very high potential to pilot MChN". Beshara's ambition goes beyond that. He wants to take over the mobile clearing space worldwide with his "low cost" strategy.

Beshara is benefiting from the support of the active Luxembourg FinTech community, as he introduces his mobile clearing house to the international financial centre. "We can help and enable all players together to be able to connect with each other, and through the different wallets they can connect easily, enabling different banks and telecom operators to connect in real time, and help the unbanked to have access to banking services with full transparency. We are seen as a disruptive technology, and so the biggest challenge we face is convincing the different players to sit down at the table with us and see the value of what we are offering". gm

Hani beshara

CEo,

MCHN

modern art museum | P. 29

introducing robots at luxembourg's

modern art museum

The CoRobots @Mudam Project will be introduced to the public and visiting European Union leaders in July to launch Luxembourg's Presidency of the EU. The exhibition "Eppur Si Muove”, is curated together with the Paris “Musée des Art et Métiers”.

“When I was working in paris, I was living across from the Louvre, and I always got lost in the Egyptian department; I could never find an exit close by”, chuckles scientist Patrice Caire, head of this Robotics project, who is charged with creating the “intelligent museum” whereby, visitors can call on robots to guide and inform them.

The initial financial backing for the three-year project comes from the City of Luxembourg. It wants to explore how robots of different kinds and capabilities

can cooperate together in museums across the city to enable visitors to benefit from more personalised visits. “It’s a test to see how useful it could be for Luxembourg. but it also allows us to address scientific questions like navigation and acceptance of robots – because robots do not always have a good image – so it will be interesting for the public to see what two different kinds of robots can do together”, explains Caire.

“The biggest challenge is to be able to present something which is scientifically still cutting edge and something which is aesthetically interesting and entertaining for the public", says Caire, a research scientist at SnT. “To have drones and humanoid robots cooperating together in a museum is completely unheard of and this project will put Luxembourg on the map in terms of information and communications technology (ICT)”.

A trip to Luxembourg's Mudam Museum will soon

get a whole lot easier, thanks to two robots who will

interact with visitors as part of an exhibition exploring the link between art and science. The CoRobots @

Mudam Project, supported by the City of Luxembourg,

in collaboration with the University of Luxembourg's Interdisciplinary Centre for

Security, Reliability and Trust (SnT), will explore what the

museum of the future could look like.

Pierre vasseur, composer the corobots @mudam Project

Julie, the humanoid robot © d

r pat

rice

Cai

re

© d

r pa t

rice

Cai

re

making tHe engine roar | P. 30

award-winning team

The SnT is still young but it has already won awards for their projects including the convivial healthcare system (Robo-CoPAINS) which improves patients’ autonomy by using robots as caretakers. These robots can autonomously call for help to, for example, a health care centre or within the neighbourhood, if they detect an accident. To make these systems secure in terms of privacy and reliability is one thing, but another important factor is conviviality, trusting the system and accepting a humanoid robot who is monitoring your behaviour in your private home. Therefore, user-friendly robots were recruited to be the interface between users and their smart homes as Caire explains.

“The difficulty with robotics is that people are used to seeing many excellent science fiction movies with great special effects, where robots can do everything. but this is very far from the real world. When we design robots, there is a tremendous amount of coding and implementation, and so many hardware problems. The reality is hard, and far from what we see in science fiction”, points out Caire.

cutting edge science

The robots group is part of the SnT, which aims to establish Luxembourg as a European centre for excellence and innovation in the field of safe, reliable and trustworthy ICT. The task of designing and building a robot with complex artificial intelligence requires an enormous amount of theoretical research to reach this level of professionalism including software testing and security and privacy techniques.

The robots are being developed from the university’s Automation Research Group headed by Prof. Voos, conveniently located just a short walk from the museum. The team is developing vision-based controls,

under Dr. olivares-Mendez, using cameras and other sensors, information from which is processed onboard to guide the robots indoors. The robots will have AI and will be able to interact with the public and say for example, "hello, what do you think?". "We develop algorithmics which analyse the speech of the people talking, and in the near future the robot will be able to reorient and reply in the same manner”, points out Caire.

HelPing a multilingual robot to Find His voice

The humanoid robots can understand 26 languages and will speak 3 languages, mirroring the multilingualism of Luxembourg city. To invent the voice of the robots and create the sound environment, Caire has called on the help of renowned French composer Pierre Vasseur. “You have to enter the world of robotics in the future and ask yourself what is the sound of a robot, what is the music of the robot. This will be different abstract worlds meeting to bring an experience for the visitors which will be new. You will hear sounds you will have never heard before“, explains Vasseur.

From broadway to tHe mudam

Two film and theatre directors, Ayshea Halliwell and Miha Manea from London will also support Caire as she sets about creating the robots show, which will entertain, and inform visitors of all ages. The drone will fly in the museums octagonal room, interacting with the visitors and the humanoid robot. The show will be both educational and entertaining adds Caire. “This is a brand new field for museums and audiences, so we have to choreograph the show. The concept for the show is still a bit secret, but what I will say is that the robots will interact with each other like two comedians, so it will not only be educational but hopefully funny as well“, enthuses Caire.

modern art museum | P. 30

© Sciences relations www.sciencerelations.de

dr patrice caire and Corobots @ Mudam project team

© 3

d-m

odel

by

M. O

livar

es-M

ende

z

Corobots @ Mudam project

Tom (flying on the left) and Julie © d

r pat

rice

Cai

re

robots will assist museum staFF and visitors

The show will be launched in July, but work is already under way for the second phase of the project to enable robots to not only guide and enhance the visitors experience, but to support the staff in their every day tasks.

“We are working on applications that will enable drones to not only fly on their own, but use manipulators, for example, to carry or pick things up. While this idea comes with many challenges, once fully developed, it will lead to all kinds of uses, such as cleaning public buildings and applications of robotic manipulators in space”, concludes Caire. gm

diary

insurance euroPe 2015

27 may 2015

Join around 400 insurance industry leaders from across Europe and worldwide for the 7th International Conference on the globalisation of the insurance industry. Please do not hesitate to pass by the LFF booth !

luxembourg renminbi Forum 2015

3 June 2015

The second edition of the Luxembourg Renminbi Forum organised by LFF will be held at the Philharmonie in Luxembourg. The full day conference will bring together a European audience of high-level practitioners, major political figures and key decision-makers to share their views on the latest developments on the internationalisation of the Chinese currency.

iFn euroPe - luxembourg 2015

10 June 2015

Following its highly successful debut, the IFN Europe Forum, the most important Islamic finance event in Europe, sponsored by LFF will take place at the Luxembourg Chamber of Commerce.

Private wealtH mexico Forum 2015

16 June 2015

The Private Wealth Mexico Forum, sponsored by LFF, takes place in Mexico City. The forum brings together international private bankers, wealth managers, family businesses and family offices for a one day conference discussing strategies to protect, preserve and grow wealth.

Financial mission to cHina 2015

21 – 25 sePtember 2015