MAERSK - THE NEW DIRECTION

80

MAERSK - THE NEW DIRECTION A.P. Moller - Maersk Capital Markets Day, 13 December 2016

Transcript of MAERSK - THE NEW DIRECTION

MAERSK - THE NEW DIRECTION A.P. Moller - Maersk Capital Markets Day, 13 December 2016

THE NEW DIRECTION

Søren Skou Chief Executive Officer

page 2

On 22nd September we announced the future Maersk: a strong container shipping, logistics and ports company

Transport & Logistics

The Maersk Line brand includes Safmarine, Seago Line, SeaLand, Mercosul Line and MCC Transport

Energy

• Managed and operated as individual business units

• More focused and structurally agile strategies to optimise value

• Intent to separate out of A.P. Møller - Mærsk A/S, creating value for shareholders in the process

• Managed and operated as an integrated company

• A one company structure with multiple brands

• Growing topline, earnings for our owners, and opportunities for our people

page 3

Two weeks ago we took the first step in realising this ambition

Hamburg Süd is a rare opportunity: A quality company with a willing seller

• In line with communicated consolidation ambition for Maersk Transport and Logistics

• Cement Maersk Line’s global leadership position and deliver growth to APM Terminals

• Build a strongly competitive platform in Latin America with dual branding similar to our position in Africa

• Create an unmatched product with a unique customer value proposition in Latin America, Oceania and Reefer segment

• Significant cost synergies by combining networks

Disclaimer: The proposed acquisition of Hamburg Süd is subject to regulatory approvals and due diligence

page 4

Energy is 25% of Group revenues – we plan to replace with organic and inorganic growth in Transport & Logistics

Maersk Group revenue and invested capital split (2015 FY)

33%

75% Revenue

25% Revenue

Invested capital

67% Invested capital

Energy Transport & Logistics

Hamburg Süd revenue

+15%

Note: Hamburg Süd revenue is 15% of the whole (i.e. 15pp on top of the 75% Transport and Logistics revenue). Disclaimer: The proposed acquisition of Hamburg Süd is subject to regulatory approvals and due diligence

page 5

Transport & Logistics

Our unique position in Transport & Logistics gives us a solid starting point to build on

Revenue, (USDbn) 23.7 4.2 2.7 0.7 0.7 32.1

Invested Capital, (USDbn) 20.1 6.0 0.2 1.1 0.4 27.8

Employees, (FTE) 29,500 22,000 10,800 4,000 5,300 71,600

Offices/countries, (#) 382/130 212/69 224/100+ 53/40+ 5/3 898/131 Key assets, (#) 620 vessels 72 terminals n/a 430 tugs 3 factories n/a

Note: Financial figures are for 2015. Total revenue is not adjusted for inter-company eliminations

The world’s biggest carrier, active in both global and intra-regional trades

Second to none refrigeration technology

Outstanding capabilities in Supply Chain Management and solid freight forwarding experience

Excellent port services

The world’s 4th largest container terminal operator with strong Africa, Latin America and East-West hub presence

page 6

Profitability is volatile with an average of 7% over the cycle, but we lack revenue growth

Revenue, (USDbn) ROIC, (%)

Note: Excludes inter-company eliminations and non-allocated overhead costs

ROIC Average

0%

4%

8%

12%

16%

2010 2011 2012 2013 2014 2015 2016Q1-Q3

33 35 36 35 36 32

21

0

5

10

15

20

25

30

35

40

2010 2011 2012 2013 2014 2015 2016Q1-Q3

page 7

Integrating also unlocks more immediate synergies across our brands - raising returns

Improved inland services

Optimised hub operations

Joint production planning

Cross-selling Increased terminal utilisation

Maersk Line

APM Terminals

Damco

Maersk Line

APM Terminals

Maersk Line

Maersk Container Industry

Maersk Line

APM Terminals

Damco

Svitzer

Maersk Line

APM Terminals

page 8

Maersk: The global integrator of container logistics…

Global integrator of container logistics - connecting and simplifying the global

supply chain

page 9

…providing global supply chain solutions with a great customer experience

Providing simple solutions to our

customers’ complex supply chain needs

Elevating the customer experience through

digital innovation

Offering the industry’s most competitive

container transport network to every market

in the world

page 10

01 02 03 04 Market is big and growing

Liner industry is changing and we will benefit

Low CAPEX need going forward

Industry is digitising – we are well positioned

impact the industries we operate in

FOUR FUNDAMENTALS

page 11

The transportation and logistics markets are big and growing

100

50

60

190

100

180

245

40

+900 Total

2PL Warehousing

Container Shipping

Air Cargo

Containerized intermodal

Container terminal and coastal storage

Contract logistics

4PL and supply chain services

Traditional Freight Forwarding

Revenue (USDbn, 2014)

Expected industry growth (’14 - ’20)

Note: Total industry growth is weighted average by revenue Source: Transport Intelligence; Armstrong & Associates; Clarksons; World Bank ; IBIS World; IPC Research; Statista

3/4PL

Growth above global GDP growth Growth in line with global GDP growth Growth below global GDP growth

01 Market is big and growing | page 12

The liner industry is consolidating and top 5 share is growing

Consolidation wave is rolling again – 8 top 20 players disappeared in last 2 years

Wave 1

Wave 2

96 98 00 02 04 06 08 10 12 14 16 18 Wave 3

31% 27% 36% 43% 45% 57%

Announced, not closed top-5 market share

Disclaimer: The proposed acquisition of Hamburg Süd is subject to regulatory approvals and due diligenceNote: Long haul trades defined as non-intra-regional trades. Source: Alphaline

02 Changing industry |

53% 66% top-5 market share longhaul trades

page 13

Industry capacity (TEUm)

Note: 1) Assuming that all vessels of 25+ years of age are scrapped by 2025 2) Assumes constant utilisation and 3% p.a. headhaul demand growth Source: Maersk Line, Alphaliner

Current capacity is sufficient to satisfy industry demand in the foreseeable future

03 Low CAPEX need |

19

2

3

24

1

23 22

0

5

10

15

20

25

Deployed capacity Idle Orderbook Nominal capacityincluding orderbook

Scrapping 2022availablecapacity

2022requiredcapacity

1

2

page 14

Also in the terminal industry overcapacity is emerging

8.5%

4.4% 3.9% 5.1%

1.0% 1.8% 2.5%

7.9%

5.0%

2.4%

5.5%

0.9%

4.2%

3.4%

0%

2%

4%

6%

8%

10%

2011 2012 2013 2014 2015 2016E 2017E

Global terminal demand Global terminal capacity

Note: (1) Measured as total port throughput and capacity in TEU incl. empties and transshipments Source: Drewry

Growth, (y/y, %)1

page 15

Digital is changing the industry to the benefit of customers – and we are ready for it

Digitisation is changing the industry… …and we are embarking on the digital journey from a strong position

Customer experience will change

Lower cost to serve

Digital will drive asset productivity

Demarcation lines between industry participants will

change

We have customers, volumes, and brands

We have already invested heavily in digitising our foundation

We are investing in new digital products

We own the data generators – the foundation for digitisation

04 Digitisation | page 16

All of our Transport & Logistics businesses share four strategic “blades” that propel us forward

Growth • Organic • Inorganic • Cross-selling • New products

Great customer experience • Leverage insights across

our businesses • Superior products • Digital interfaces

Cost leadership • In everything we do • In all our businesses • “Lowest cost, lower every

year” culture • Exploit synergies

Competitive pricing • Providing value to our

customers • Enabled by cost leadership

and low cost to serve

page 17

We have set a strong management team to deliver on the strategy

Chief Executive Officer Søren Skou

Chief Executive Officer APM Terminals

(Chairman of Svitzer) Morten Engelstoft

Chief Commercial Officer Maersk Line

(Chairman of Damco) Vincent Clerc

Chief Operating Officer Maersk Line

(Chairman of Maersk Container Industry)

Søren Toft

Chief Human Resource Officer Ulf Hahnemann

General Counsel and Head of Corporate Affairs

Caroline Pontoppidan

Chief Financial, Strategy & Transformation Officer

Jakob Stausholm

page 18

Maersk: The global integrator of container logistics

Providing simple solutions to our customers’ complex supply chain needs

Elevating the customer experience through digital innovation Global integrator of container logistics

- connecting and simplifying the global supply chain

Extending the industry’s most effective and efficient delivery network to every

market in the world

page 19

CUSTOMER EXPERIENCE & GROWTH

Vincent Clerc Chief Commercial Officer Maersk Line

page 20

Unlock growth from better

CUSTOMER EXPERIENCE

In recent years, price has dominated the customer decision…

…digitisation and integrated solutions are game-changers to bring quality back into the equation…

…Maersk is uniquely positioned to increase the quality of the customer experience – a central element to unlock growth

page 21

The customer experience is central to our strategy

Growth

Great customer experience

Cost leadership

Competitive pricing

page 22

We are in a strong position to meet customer needs with digitisation and Transport & Logistics solutions

• Reliability

• Network coverage

• Financial stability

• Documentation

• Visibility

• Accessibility

• Integrated offerings

• New logistics services

• Digital services

All customers

Flow of goods Flow of information Extended solutions

Some customers

Traditionally served by carriers

Traditionally served by freight forwarders

To be served by Maersk

Will be transformed by digitisation

page 23

With our portfolio of digital initiatives, we continue to take the customer experience to new levels

Online documentation

Instant quotes and booking confirmation

New digital services

Track and trace

Documentation Visibility Accessibility Digital services

page 24

With Transport & Logistics we are able to vastly improve the customer offering

Innovation Expand product exposure

Coordinated chain of delivery

Tailor-made solutions

Reliability New logistics services Integrated offerings

page 25

Integrated offerings combine Damco’s product range and Maersk Line’s large customer base

We will improve customer retention from capabilities in tailoring solutions and building strategic partnerships

We will achieve higher share of wallet from attracting more of customers’ total logistics spend e.g., via Damco’s supply chain solutions

12% of Maersk Line volume is today sold with inland service on top

Customs House Brokerage

Cargo Insurance

Supply Chain solutions

Inland transport

page 26

Damco is building on positive traction

…and continues to strengthen the position through a number of focus areas

Damco has stabilised after a difficult time…

• Stronger and expanded Supply Chain Solutions core business within selected verticals

• Innovation of product offerings

• Development of e-commerce solutions

• Cross-selling synergies with Maersk Line

• Automation of processes

01002003004005006007008009001,000

-160

-120

-80

-40

0

40

20

12

Q1

20

12

Q2

20

12

Q3

20

12

Q4

20

13

Q1

20

13

Q2

20

13

Q3

20

13

Q4

20

14

Q1

20

14

Q2

20

14

Q3

20

14

Q4

20

15

Q1

20

15

Q2

20

15

Q3

20

15

Q4

20

16

Q1

20

16

Q2

20

16

Q3

Underlying result Revenue

Revenue (USDm) Underlying result1 (USDm)

Note: (1) The 2012 figures are excluding tax effect on one-offs Source: Maersk

page 27

To translate better customer experience into growth, we continue to build a strong commercial foundation…

Strengthen sales capabilities

More focused frontline organisation

Deepen customer understanding

Improved sales coverage

page 28

…which has enabled us to pick up Maersk Line’s organic volume growth – and we will take it further

…and we continue to expand our commercial agenda

0%

4%

8%

12%

16%

2010 2011 2012 2013 2014 2015 2016 YTD

Maersk Line volume growth (Y/Y)(%)

Industry volume growth (Y/Y)(%)

We have managed to grow volume beyond industry growth while maintaining our EBIT-margin gap…

4pp 5pp 4pp 8pp 9pp 6pp 9pp

Maersk Line EBIT-margin gap to peers (%-points)

Better customer retention

Take prices online

Note: Peer group includes CMA CGM, APL, Hapag Lloyd, Hanjin, ZIM, Hyundai MM, K Line, CSAV, OOCL, NYK, MOL, COSCO, CSCL Source: Maersk Line, company reports

page 29

Our acquisition of Hamburg Süd will drive growth and bring several benefits to our customers

The acquisition will drive growth…

Revenue (2015, USDbn)

Source: Maersk Line, Alphaliner, company reports Note: (1) Maersk Line Q3 2016 interim report, Hamburg Süd 2015 key figures (container ships). Disclaimer: The proposed acquisition of Hamburg Süd is subject to regulatory approvals and due diligence

Capacity1

(TEUm)

…and benefit customers in different ways

• Access to world’s largest network with more direct services

• Better prices for customers from efficiencies

• Strong customer proposition from dual brands

• Unique reefer offering by combining two of the largest players

Maersk Line

Hamburg Süd

~3

~0.6

~24

~6

page 30

We can only achieve our full growth potential when we continuously meet the customer needs

…while we actively grow the foundation of our business – the container volume

Digitisation

Transport & Logistics

Commercial foundation

Acquisitions

Taking growth to new levels depends on our ability to meet customer needs…

page 31

OPTIMISED NETWORK

Søren Toft Chief Operating Officer Maersk Line

Morten Engelstoft Chief Executive Officer APM Terminals

page 32

Enables price competiveness

Enables organic, profitable growth

Makes inorganic growth value creating

is the foundation for growing our business…

COST LEADERSHIP

page 33

…and Maersk Line continues significant cost reductions

Maersk Line unit cost, (USD/FFE) The cost toolbox

Network rationalisation

Speed equalisation & Slow steaming

Improve utilisation

SG&A 2M Improve procurement

Inland optimisation

Deployment of larger vessels

Retrofits 1,600

1,800

2,000

2,200

2,400

2,600

2,800

3,000

3,200

3,400

12

Q1

12

Q2

12

Q3

12

Q4

13

Q1

13

Q2

13

Q3

13

Q4

14

Q1

14

Q2

14

Q3

14

Q4

15

Q1

15

Q2

15

Q3

15

Q4

16

Q1

16

Q2

16

Q3

CAGR: -9%

CAGR: -5% LTM: -11%

At fixed bunker price (200 USD/mt) At floating bunker price

page 34

Asset utilisation in Maersk Line has improved

Vessel utilization, (%) Container turn, (ratio)

88%

93%

66% 70%

91%

71%

50%

60%

70%

80%

90%

100%

jan

-14

mar

-14

maj

-14

jul-

14

sep

-14

no

v-1

4

jan

-15

mar

-15

maj

-15

jul-

15

sep

-15

no

v-1

5

jan

-16

mar

-16

maj

-16

jul-

16

sep

-16

4.5 4.7

3.8 4.0

4.6

3.9

3.2

3.6

4.0

4.4

4.8

5.2

14

Q1

14

Q2

14

Q3

14

Q4

15

Q1

15

Q2

15

Q3

15

Q4

16

Q1

16

Q2

16

Q3

Headhaul bottleneck Roundtrip Yearly averages Dry Reefer Yearly averages

Volume: +8% (y/y)

Note: Container turn is average number of times a container is shipped full per year (quarterly data annualised), volume, deployed capacity, invested capital are 16Q3 vs. 15Q3

Deployed capacity: +4% (y/y) Invested capital: -2% (y/y)

page 35

Maersk Line’s large proportion of short duration charter contracts enables capacity flexibility

Industry capacity split by owner type (%) Charter contract durations (TEUm)

4.9 4.9

1.3

0

1

2

3

4

5

6

7

> 12 monthcontract

< 12 monthcontract

Source: Alphaliner, Internal estimates

45% Operator owned

(carrier)

55% Non-operator owned (charter company)

0.8 0.6 0

1

2

3

4

5

6

7

< 12 monthcontract

> 12 monthcontract

Industry Maersk Line

Idle Chartered

page 36

Scale

To lead and remain competitive requires new levers across Maersk

Hub operations Digital assets Joint planning

Connected vessel Intelligent containers

Hamburg Süd Maersk Container Industry

APM Terminals

Disclaimer: The proposed acquisition of Hamburg Süd is subject to regulatory approvals and due diligence

page 37

Digital is changing the way we operate our assets

Data collection

Flow meter Control and alarm systems

Time stamps

Benefit: Better

network design

Sensors

Analytics engine

Data reports

Benefit: Improved fuel efficiency

Benefit: Reduced port stay

“pit stop”

page 38

Hamburg Süd is a great match for network and terminals

Note: Illustrative network. Disclaimer: The proposed acquisition of Hamburg Süd is subject to regulatory approvals and due diligence

Terminal volumes Network synergies Procurement synergies

page 39

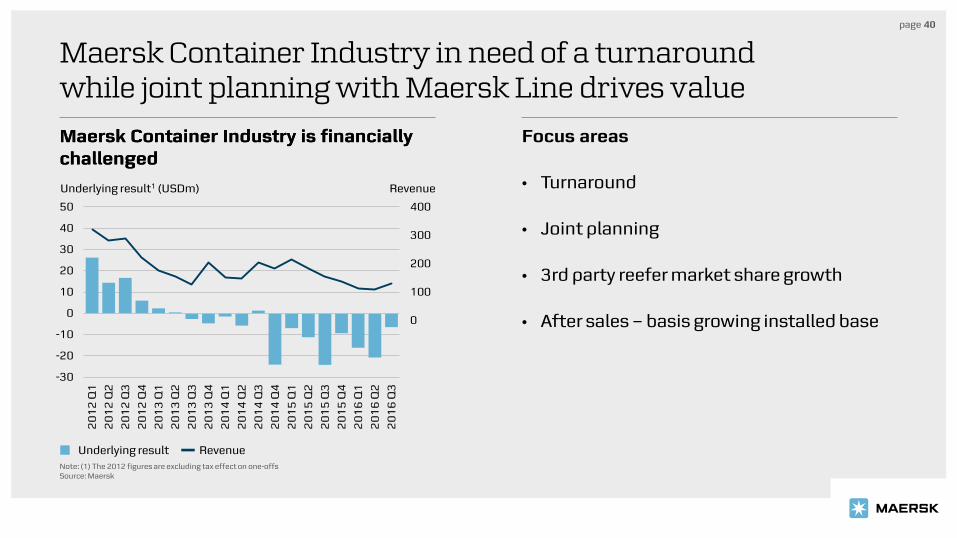

Maersk Container Industry in need of a turnaround while joint planning with Maersk Line drives value

Maersk Container Industry is financially challenged

Focus areas

• Turnaround

• Joint planning

• 3rd party reefer market share growth

• After sales – basis growing installed base

Maersk Container Industry is financially challenged

-200

-100

0

100

200

300

400

-30

-20

-10

0

10

20

30

40

50

20

12

Q1

20

12

Q2

20

12

Q3

20

12

Q4

20

13

Q1

20

13

Q2

20

13

Q3

20

13

Q4

20

14

Q1

20

14

Q2

20

14

Q3

20

14

Q4

20

15

Q1

20

15

Q2

20

15

Q3

20

15

Q4

20

16

Q1

20

16

Q2

20

16

Q3

Revenue Underlying result1 (USDm)

Note: (1) The 2012 figures are excluding tax effect on one-offs Source: Maersk

Underlying result Revenue

page 40

APM Terminals to benefit from Maersk Line’s growth and VSA partnerships

• Grow APM Terminals’ share of Maersk Line’s volume

• Maersk Line’s vessel sharing agreements supporting APM Terminals volume growth

• Impact from Hamburg Süd (from 2018)

32% of Maersk Line’s moves are with APM Terminals

Disclaimer: The proposed acquisition of Hamburg Süd is subject to regulatory approvals and due diligence

page 41

Hub terminals are essential to operating a reliable and cost effective network

Share of global Maersk Line volume that pass through key hubs 2016Q1-Q3 (%)

33%

21%

16%

13%

12%

11%

32%

9%

5%

0% 10% 20% 30% 40%

Tanjung Pelepas

Singapore

Algeciras

Salalah

Rotterdam

Tangier

Port Said

Jebel Ali

Balboa

48% of Maersk Line’s transhipment moves are with APM Terminals

Note: Total moves include empty and full container moves. Pass through includes loadings, discharges and containers that stay on the vessel during the port stay. Pass through numbers are not additive as a container can pass through several hubs on same journey

43% of Maersk Line’s moves are transhipment moves

APM Terminals 3rd party

page 42

Time is money – terminal performance as a source of strategic advantage

19 (76%)

6 (24%)

25 (100%)

0%

25%

50%

75%

100%

Crane operations Anchorage, piloting,morrring,

waiting time

Total

190 147

115 113

0

50

100

150

200

Hub 1 Hub 2 Hub 3 Hub 4

300,000 Hours of non-crane time per year

Average port stay, (hours)

Crane productivity in key transhipment hubs for EEE vessels, (moves/hr)

page 43

APM Terminals is adapting to new reality

A shift in focus and approach is required :

Capex led growth

Cost leadership

Asset utilisation

From

To

page 44

Cost leadership is required to win

We are under pressure… …and taking action

29 31

22

0

5

10

15

20

25

30

35

100

120

140

160

180

200

2014 2015 2016 YTD

Stardardisation Limit capex growth

Improve utilisation

SG&A

Digitisation

Improve procurement

Reduce Operating cost base

Decrease Cycle Times

Decrease Non-Productive Moves

Revenue/TEU (USD) EBIT*/TEU (USD)

Revenue/TEU EBIT*/TEU

* Consolidated terminals, excluding gains

page 45

APM Terminals has started the cost reduction journey

Cost per move Cost break down1 (FY 2015)

140

150

160

170

180

190

200

14Q1 14Q2 14Q3 14Q4 15Q1 15Q2 15Q3 15Q4 16Q1 16Q2 16Q3

CAGR: -2%

LTM: -7%

USD/move

50%

14%

14%

10%

8% 5%

Concession fee

Corporate costs

Labor costs

Service & admin costs

Variable operational costs

Depreciation

Note: (1) Cost breakdown for controlled terminal entities only

page 46

Integrated planning with Svitzer will deliver synergies for Maersk Line and APM Terminals

…and is a vital part of the port call value chain

• Direct supplier to shipping lines and terminals

• Value from bringing Svitzer into existing APM Terminals facilities

• Unique opportunity to collaborate on new projects

• An important part of our customers overall port experience

Svitzer is a stable business…

0

50

100

150

200

250

300

0

5

10

15

20

25

30

35

40

45

50

20

12

Q1

20

12

Q2

20

12

Q3

20

12

Q4

20

13

Q1

20

13

Q2

20

13

Q3

20

13

Q4

20

14

Q1

20

14

Q2

20

14

Q3

20

14

Q4

20

15

Q1

20

15

Q2

20

15

Q3

20

15

Q4

20

16

Q1

20

16

Q2

20

16

Q3

Revenue Underlying result1 (USDm)

Note: (1) The 2012 figures are excluding tax effect on one-offs Source: Maersk

Underlying result Revenue

page 47

APM Terminals is adapting to new reality

A shift in focus and approach is required :

Capex led growth

Cost leadership

Asset utilisation

From

To

page 48

Our key challenge is asset utilisation

Invested capital has outpaced topline … …but we have opportunities to improve

Disclaimer: The proposed acquisition of Hamburg Süd is subject to regulatory approvals and due diligence

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Q1

'13

Q2

'13

Q3

'13

Q4

'13

Q1

'14

Q2

'14

Q3

'14

Q4

'14

Q1

'15

Q2

'15

Q3

'15

Q4

'15

Q1

'16

Q2

'16

Q3

'16

Invested capital (USDm) Asset turn (revenue/invested capital)

Invested capital Asset turn

Maersk Line and Hamburg Süd

Other shipping line customers

Land side customers

page 49

Strategic partnerships with shipping line customers remain vital for APM Terminals

• Increased focus on customer experience – investments in technology and efficiency

• Ambition to grow market share through increased utilisation

• Partnering for value and joint growth

• Commercial independence with equal focus on growing business with all shipping line customers

page 50

Creating and sharing value for our land side customers through new products and services

Marine Quayside Yard Gate Inland Services

Cargo Managers

Land side customers

Cargo Owners

Truck & Rail Operators

Equipment owners

Regulators

Shipping Lines

Truck visit Efficiency

Container Weighing

Storage options

Fast Track options

Inland Service depots

Container lifecycle services

Predictable, reliable & efficient service

Digital platform

Data based insights

page 51

Achieving growth through disciplined approach to invested capital

From period of heavy investments in new capacity…

…to maximise what we have

• No new greenfield investments

• No increase in invested capital beyond what already is committed (approx. USD 2bn)

• Non-strategic divestments to invest for increased T&L value

• Derive value from portfolio management

#terminals

0

10

20

30

40

50

60

70

80

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Legal entity

Fully separated from Maersk Line

Global port acquisition

TCB acquisition

Source: Maersk, Drewry

page 52

Integrated operations in West Med has shown 15% throughput increase with low CAPEX

Large improvements in Algeciras and Tangier…

0

20

40

60

80

100

120

140

160

180

0

10

20

30

40

50

60

70

80

2013 2014 2015 2016YTD

Weekly moves, (‘000) Cost/move, (USD)

Change: +15%

Change: -20%

• Collaboration project initiated in 2013

• Operates at 109% of design capacity achieved by integrating operational processes

• Port productivity up 14% ytd achieved through joint planning of berth windows and stowage

• Improvements achieved with limited capex

…driven by joint Maersk Line and APM Terminals operations

Moves Cost/move (right scale)

page 53

APM Terminals is taking action to best manage cost and growth

A shift in focus and approach :

Capex led growth

Cost leadership

Asset utilisation

From

To

page 54

Jakob Stausholm Chief Financial, Strategy & Transformation Officer

DIGITISATION Screenshot to be updated

Thursday afternoon

page 55

Transforming a 100+ year old company is not easy – requires a fit for purpose IT setup

IT center in Maidenhead, UK

Annual IT spend USD ~800m

IT Foundation

~1,900 people employed in IT

Accessing the right competences by establishing an IT centre in Maidenhead, UK (Thames Valley) in 2013

Transport & Logistics IT organisation

5 key IT centres in UK, Denmark, US, Netherlands and India

page 56

32% 50%

0%

20%

40%

60%

80%

100%

2012 2016E

Maersk Line has already invested significantly in improving the IT foundation

Reduced IT run budget to free up money for building

Fixing and re-implementing back bone software

Moving infrastructure to public/private hybrid cloud

Implementing major IT and process transformation program Build

Split of IT budget*

Run

Note: * Maersk Line only

Cost leadership

Capability building

Started a number of key projects

IT Foundation

Replacing legacy systems

page 57

Radically changing the customer experience – making my.maerskline.com one of the largest B2B transaction sites

Easier to do business online with Maersk Line…

Note: * May take longer due to local procedures and legislation

Examples of improvements: 2014 Today 2018 Easier to become customer: from 2-3 days 2 hours* 2-3 minutes

Faster to book: from +2 hours 22 minutes 5 seconds

Faster to amend: from +1 hour 25 minutes seconds

1% Manual

58% Website

24% EDI

…drives online transactions

Booking channel, 2016 YTD

17% 3rd party portals

IT Foundation

Manual transactions reduced by a factor of 30x over last 4 years

page 58

Improving the IT foundation is just the first step

IT foundation Digital transformation

DIGITAL ASSETS

ANALYTICS NEW DIGITAL

BUSINESSES

IT SETUP FIXING BACKBONE

ONLINE CUSTOMER

EXPERIENCE

page 59

We are building the required capabilities within digital technology and changing the way we work

Capabilities & people

Organisation

Culture

Infrastructure

Mixing a new breed of talent with our world class shipping people – hired numerous PhDs and Post docs in fields such as Machine Learning, Applied Mathematics, and Operational Research

Separate IT and Digital organisations working directly with business product owners to unlock value

Training and using Scrum methodology; created Design Centre for facilitating agile working methods

All digital product development will take place on one common platform

Digital Transformation

page 60

Advanced analytics opens up a whole new playground of opportunities supporting our strategy Examples

Predictive maintenance – vessels and containers

Operational optimisation

Commercial decision-making

Selling services

Real time network optimisation for bunker savings

Which customers to target – how to reach

How to optimise cargo mix within restrictions

Generate lead pipeline

Logistics chain advisory

Container repairs and empty moves

Aggregating and selling trade data

Weather data from vessels

Intelligent pricing engine

Automated stowage

Analytics

page 61

Accurate forecasting for empty container repositioning will save millions of dollars

USD 2.1bn spend per year on repositioning empty containers*

Difficult to forecast need for containers per location due to high fluctuation in demand

Accuracy of existing model was poor – business lost trust

Improving existing model through advanced analytics

x15 increase in accuracy

Note: * Maersk Line only

Example

Analytics

page 62

We are building a portfolio of digital products through various innovation methods and rapid prototyping

Innovation/ Idea generation

Prototyping Industrialisation

Various methods:

• Partnerships

• Internal innovation

• Start-up incubation

• External events

Outcomes:

• Add to existing business

• New revenue streams

~15 prototypes at the moment

New Digital Business

page 63

Example

100+ trucking companies on-boarded since August

Promising results in short time, potential for exponential growth

Note: * Currently being piloted in North America for trucking only

New Digital Business

Online reverse auction place for inland transport*. Increases ability to sell inland products to our end-customers

Transparent prices, simple process and improved planning

First step in making end-to-end shipping a seamless experience

Prototyping

Spotlanes.com creating opportunities in inland transport

page 64

Our intent: Create a digital world of logistics page 65

Vincent Clerc Chief Commercial Officer Maersk Line

Morten Engelstoft Chief Executive Officer APM Terminals

Jakob Stausholm Chief Finance, Strategy & Transfor-mation Officer

TRANSPORT & LOGISTICS PERFORMANCE

page 66

0%

2%

4%

6%

8%

10%

12%

14%

16%

20

10

20

11

20

12

20

13

20

14

20

15

20

16

YT

D

Historical returns for combined companies have been reasonable

Note: Figures are excluding allocations and eliminations. Source: Maersk

7% Average annual ROIC 2010-2016YTD

USD 1.8bn

Average annual NOPAT 2010-2016YTD

Aggregate of main businesses in Transport & Logistics excluding residual activities and overheads

page 67

Unlocking of integration synergies will happen gradually over the coming three years

Synergies from integration

Revenue growth

Cost savings and other benefits

~2pp ROIC

Note: Timing and size of each synergy are illustrative only, as the exact timing and size of each synergy will differ. The overall synergy level of 2pp ROIC is, however, of high certainty.

Phasing of synergies

2017 2018 2019 Total

~2pp

Commercial synergies

Overhead savings

Operational efficiencies

page 68

We have generated free cash flow and we are implementing strict capital discipline

Transport & Logistics has generated FCF of USD 5.5bn over the last four years

Note: Excluding the acquisition of Hamburg Süd

Lower future CAPEX in Transport & Logistics

2.8

3.4 3.3

2.2

~3.3

3.5-4.0

1.5-2.0

0.0

1.0

2.0

3.0

4.0

5.0

20

13

20

14

20

15

YT

D2

01

6

20

16

E

20

17

E

20

18

E -

20

20

E

USDm Yearly gross CAPEX (USDbn)

Operating cash flow FCF Investing flow

-2,000

-1,500

-1,000

-500

0

500

1,000

1,500

2,000

Q3

12

Q4

12

Q1

13

Q2

13

Q3

13

Q4

13

Q1

14

Q2

14

Q3

14

Q4

14

Q1

15

Q2

15

Q3

15

Q4

15

Q1

16

Q2

16

Q3

16

Main CAPEX items for 2017 11 x 19K TEU vessels 9 x 14K TEU vessels

Average gross CAPEX

3.2

2.5

Source: Maersk

page 69

Key financials

Jan-Sep 2016 Jan-Sep 2015 Segment variance Segment result ROIC Segment result ROIC

Maersk Line -230 -2% 1,485 10% -1,715

APM Terminals 351 6% 526 12% -175

Damco 27 17% 18 8% 9

Svitzer 73 8% 91 11% -18

MCI -44 -14% -42 -15% -2

Transport & Logistics total 117 2,078 -1,901

To be covered in the

following sections

Note: Figures are excluding allocations and eliminations. Source: Maersk

page 70

Maersk Line

page 71

Freight rate has been under pressure from tough market conditions…

Growth (y/y %)

3.1% 3.5%

6.4% 6.2% 5.6%

6.5%

4.9% 4.3%

3.5%

1.4% 1.8% 0.3%

1.6% 2.1%

1.7%

5.5% 5.3% 5.9% 5.7% 5.5% 5.2% 5.4%

6.4% 7.3%

7.9% 8.7% 8.5%

7.2%

5.3%

3.0%

1.5%

1,400

1,600

1,800

2,000

2,200

2,400

2,600

2,800

3,000

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Q1 13 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16E

Freight rate, (USD/FFE)

Head haul demand Maersk Line freight rate (rhs)

Source: Maersk Line, Alphaliner

Nominal supply

CAGR -2.2%

CAGR -17.8%

N/A

page 72

…which has driven down our profitability – relative still ahead of industry

Core EBIT-margin (%)

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Q111

Q211

Q311

Q411

Q112

Q212

Q312

Q412

Q113

Q213

Q313

Q413

Q114

Q214

Q314

Q414

Q115

Q215

Q315

Q415

Q116

Q216

Q316

Industry slumps 6 quarters 5 quarters 5 quarters so far

Gap to peers (%-pts)

Note: Peer group includes CMA CGM, APL, Hapag Lloyd, Hanjin, ZIM, Hyundai MM, K Line, CSAV, OOCL, NYK, MOL, COSCO, CSCL. Peer average is TEU-weighted. EBIT margins are adjusted for gains/losses on sale of assets, restructuring charges, income/loss from associates. Maersk Line’ EBIT-margin is also adjusted for depreciations to match industry standards (25 years). OOCL and COSCO Q3 2016 EBIT-margin is estimated based on previous half years’ gap to Maersk Line as they do not publish quarterly results. Source: Maersk Line, company reports

Gap to peers (rhs) Peer group Maersk Line

page 73

36% Spot (<1 month)

20% Short term

(1-3 months)

45%

Long term (>3 months)

By contract type

0

200

400

600

800

1,000

1,200

1,400

1,600

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Q1

-10

Q3

-10

Q1

-11

Q3

-11

Q1

-12

Q3

-12

Q1

-13

Q3

-13

Q1

-14

Q3

-14

Q1

-15

Q3

-15

Q1

-16

Q3

-16

Maersk Line (USD/FFE)

CCFI (Index) SCFI (Index) Note: 1. Oct 2009 = 1000 for SCFI, January 1998 =1000 for CCFI Source: Maersk

16Q3 vs. 16Q2: Maersk Line: +5.5% CCFI composite: +7.5% SCFI composite: +29.5%

Index1 USD/FFE

Maersk Line rates correlate with SCFI/CCFI but with lower volatility partly due to contracts

Average rate Volume split, Jan to Sep 2016

page 74

Freight rates out of China have bottomed out versus rest of the world in Q3

Freight rate Volume split, Jan to Sep 2016

49% North-South

15% Intra region

36% East-West

By trade

1,000

1,500

2,000

2,500

3,000

3,500

Q1

13

Q2

13

Q3

13

Q4

13

Q1

14

Q2

14

Q3

14

Q4

14

Q1

15

Q2

15

Q3

15

Q4

15

Q1

16

Q2

16

Q3

16

Rest of world China export

USD/FFE

page 75

APM Terminals

page 76

Revenue under pressure

Total revenue

Source: APM Terminals

APM Terminals revenue model

31% Yard & Gate

2% Marine

Services

51% Quay incl. hub

revenue

Revenue split

16% Other services (incl. trucking and container sales)

(USDm)

850

900

950

1,000

1,050

1,100

1,150

Q1

12

Q2

12

Q3

12

Q4

12

Q1

13

Q2

13

Q3

13

Q4

13

Q1

14

Q2

14

Q3

14

Q4

14

Q1

15

Q2

15

Q3

15

Q4

15

Q1

16

Q2

16

Q3

16

Revenue Revenue from TCB

page 77

Despite reduced segment result, existing terminals deliver 8-10% ROIC

Profits have declined with new industry fundamentals…

…operating terminals continue to deliver well but burdened by projects

Segment result, (USDm) ROIC, (2016 Q3 YTD, %)

-150-100

-500

50100150200250300350

Q1

12

Q2

12

Q3

12

Q4

12

Q1

13

Q2

13

Q3

13

Q4

13

Q1

14

Q2

14

Q3

14

Q4

14

Q1

15

Q2

15

Q3

15

Q4

15

Q1

16

Q2

16

Q3

16

8.4% 9.9%

-1.7%

6.2%

-2%

0%

2%

4%

6%

8%

10%

12%

Total Implementations incl TCB

Consolidated businesses

Q3 2016 invested capital (USDbn)

7.9 2.2 2.0 3.7

JV & Associates

Underlying result Gain/loss and impairment

8.9%

Source: APM Terminals

page 78

APM Terminals’ implementation projects

Project Opening Details Investment (100% share)

Lázaro Cárdenas, Mexico 2017 • Signed 32-year concession agreement for new deep-water • Will add 1.2m TEU in annual throughput

USD 0.9bn

Ningbo, China 2016 • Major gateway port • 67%/33% (Ningbo Port Group/APM Terminals) share of investment and operation

USD 0.7bn

Izmir, Turkey 2016 • New 1.5m TEU deep-water container and general cargo terminal USD 0.4bn

Moin, Costa Rica 2018 • Signed 33-year concession for new deep-water terminal USD 1.0bn

Savona-Vado, Italy 2017 • Signed 50-year concession agreement for new deep-sea gateway terminal USD 0.4bn

Abidjan, Ivory Coast 2018 • Is expected to be the second most busy container terminal in West Africa USD 0.6bn

Tema, Ghana TBD • Will add 3.5m TEU of annual throughput • JV project with Bolloré (42.3%) and Ghana Ports & Harbours Authority (15.4%)

USD 0.8bn

TM2, Tangier 2019 • Signed 30-year concession agreement • Will add 5m TEU

USD 0.9bn

Note: TEU and investment numbers are 100% of the projects

page 79

Thank you