Macroeconomics Monthly Report - Wirtualna Polskai.wp.pl/a/dibre/rmiesieczne/october2007.pdf · put...

65

Periodic Report Monthly Report October 2007 Equity market We maintain that a correction is already behind us. Bullish trends in world markets, in particular emerging markets, add to the attractiveness of Polish stocks while the WIG Index performs relatively poorly. With the expected appreciation of the zloty, this should incite foreign investors to take positions. Capital will start flowing to investment funds again on a more bullish sentiment, and we will see a lot of activity on the market, driven among others by short position closing by traders. Company News Banks. We remain bullish on the bank industry, and expect strong third- quarter earnings. Softer sentiment and lower trading volumes might be a drawback, but, overall, the industry is on a sharp upward curve. Our best bets in the sector are BZ WBK and Kredyt Bank. Gas & Oil. We expect a depreciation in refinery stocks due to a weakening dollar which is eating into invariably strong refining margins. Investors will be betting on a weaker third-quarter showing from PKN Orlen. Telecommunications. Our long-term outlook on telecom stocks remains bleak. In the month ahead, telecoms, and especially TPSA, will probably see a narrowing in the discount at which they trade to the strong European sector. IT. The lead story in September was the merger between Asseco Poland and Prokom Software. The long-awaited revival in public-sector has not happened, and we are afraid that this month’s parliamentary election will put off e-government projects further into the future. Metals As copper supply remains tight due to worker strikes in Peru, while demand from China continues to be strong, prices have shot up over $8,000/t, and show no signs of slowing. We expect upward revisions to the earnings consensus. Construction. Building companies will show strong third-quarter earnings thanks to two factors: higher prices of building services, and a retreat in materials prices from their record 2Q levels. Our top picks in the sector are Polimex, Elektrobudowa, Ulma Construccion Polska, and Erbud. Real-Estate Developers. Real-estate developers report that, after a summer lull, prices started to rise again in September. Profit margins decline from month to month. We expect that developers will offset the slowdown in prices by increasing sales volumes. Ratings. As of the date of this Monthly Report, we are upgrading our investment ratings on Emperia Holding (Hold) and Ulma Construccion Polska (Accumulate), and downgrading BZ WBK (Accumulate), Pekao (Hold), and PKN Orlen (Hold). BRE Bank Securities does not rule out offering brokerage services to an issuer of securities being the subject of a recommendation. Information concerning a conflict of interest arising in connection with issuing a recommendation (should such a conflict exist) is located on the final page of this report. Analysts: Michał Marczak (+48 22) 697 47 38 [email protected] Marta Jeżewska (+48 22) 697 47 37 marta.jeż[email protected] Krzysztof Radojewski (+48 22) 697 47 01 [email protected] Kamil Kliszcz (+48 22) 697 47 06 [email protected] Piotr Janik (+48 22) 697 47 40 [email protected] Kacper Żak (+48 22) 697 47 41 [email protected] Macroeconomic Analyst Janusz Jankowiak 3 October 2007 WIG vs. indices in the region BRE Bank Securities Equity Market Macroeconomics Avg daily trading volume Average P/E 2008 Average P/E 2007 WIG 61 196 16.8 14.2 PLN 1 652m 40000 45000 50000 55000 60000 65000 70000 2006-09-26 2007-01-22 2007-05-18 2007-09-11 pkt WIG BUX PX

Transcript of Macroeconomics Monthly Report - Wirtualna Polskai.wp.pl/a/dibre/rmiesieczne/october2007.pdf · put...

BRE Bank Securities

3 October 2007

Monthly Report BRE Bank Securities BRE Bank Securities

Periodic Report

Monthly Report October 2007

Equity market We maintain that a correction is already behind us. Bullish trends in world markets, in particular emerging markets, add to the attractiveness of Polish stocks while the WIG Index performs relatively poorly. With the expected appreciation of the zloty, this should incite foreign investors to take positions. Capital will start flowing to investment funds again on a more bullish sentiment, and we will see a lot of activity on the market, driven among others by short position closing by traders. Company News Banks. We remain bullish on the bank industry, and expect strong third-quarter earnings. Softer sentiment and lower trading volumes might be a drawback, but, overall, the industry is on a sharp upward curve. Our best bets in the sector are BZ WBK and Kredyt Bank. Gas & Oil. We expect a depreciation in refinery stocks due to a weakening dollar which is eating into invariably strong refining margins. Investors will be betting on a weaker third-quarter showing from PKN Orlen. Telecommunications. Our long-term outlook on telecom stocks remains bleak. In the month ahead, telecoms, and especially TPSA, will probably see a narrowing in the discount at which they trade to the strong European sector. IT. The lead story in September was the merger between Asseco Poland and Prokom Software. The long-awaited revival in public-sector has not happened, and we are afraid that this month’s parliamentary election will put off e-government projects further into the future. Metals As copper supply remains tight due to worker strikes in Peru, while demand from China continues to be strong, prices have shot up over $8,000/t, and show no signs of slowing. We expect upward revisions to the earnings consensus. Construction. Building companies will show strong third-quarter earnings thanks to two factors: higher prices of building services, and a retreat in materials prices from their record 2Q levels. Our top picks in the sector are Polimex, Elektrobudowa, Ulma Construccion Polska, and Erbud. Real-Estate Developers. Real-estate developers report that, after a summer lull, prices started to rise again in September. Profit margins decline from month to month. We expect that developers will offset the slowdown in prices by increasing sales volumes. Ratings. As of the date of this Monthly Report, we are upgrading our investment ratings on Emperia Holding (Hold) and Ulma Construccion Polska (Accumulate), and downgrading BZ WBK (Accumulate), Pekao (Hold), and PKN Orlen (Hold).

BRE Bank Securities does not rule out offering brokerage services to an issuer of securities being the subject of a recommendation. Information concerning a conflict of interest arising in connection with issuing a recommendation (should such a conflict exist) is located on the final page of this report.

Analysts:

Michał Marczak (+48 22) 697 47 38 [email protected] Marta Jeżewska (+48 22) 697 47 37 marta.jeż[email protected]

Krzysztof Radojewski (+48 22) 697 47 01 [email protected]

Kamil Kliszcz (+48 22) 697 47 06 [email protected] Piotr Janik (+48 22) 697 47 40 [email protected] Kacper Żak (+48 22) 697 47 41 [email protected]

Macroeconomic Analyst Janusz Jankowiak

3 October 2007

WIG vs. indices in the region

BRE Bank Securities

Equity Market Macroeconomics

Avg daily trading volume

Average P/E 2008

Average P/E 2007

WIG 61 196 16.8

14.2

PLN 1 652m

40000

45000

50000

55000

60000

65000

70000

2006-09-26 2007-01-22 2007-05-18 2007-09-11

pkt

WIG BUX PX

BRE Bank Securities

3 October 2007 2

Monthly Report BRE Bank Securities

Table of Contents 1. Equity market ........................................................................................ 3 2. Fund Flows ............................................................................................ 5 3. Current ratings by BRE Bank Securities S.A. ........................................ 6 4. Ratings statistics ................................................................................... 7 5. Macroeconomics ................................................................................... 8 6. Financial Sector ..................................................................................... 9

6.1. BPH ............................................................................................ 13 6.2. BZ WBK ...................................................................................... 14 6.3. Handlowy .................................................................................... 15 6.4. ING BSK ..................................................................................... 16 6.5. Kredyt Bank ................................................................................ 17 6.6. Millennium .................................................................................. 18 6.7. Pekao SA ................................................................................... 19 6.8. PKO BP ...................................................................................... 20

7. Gas & Oil, Chemicals .............................................................................. 22 7.1. Lotos ........................................................................................... 23 7.2. PGNiG ........................................................................................ 24 7.3. PKN Orlen .................................................................................. 25 7.4. ZA Puławy .................................................................................. 26

8. Telecommunications .............................................................................. 27 8.1. Netia ........................................................................................... 28 8.2. TP SA ......................................................................................... 29 9. Media ..................................................................................................... 31 9.1. Agora .......................................................................................... 32 9.2. WSiP ........................................................................................... 33 10. IT Sector ................................................................................................ 34 10.1. ABG Spin .................................................................................. 35 10.2. Asseco Poland .......................................................................... 36 10.3. ComArch ................................................................................... 37 10.4. Macrologic ................................................................................ 38 10.5. Prokom Software ...................................................................... 39 10.6. Sygnity ...................................................................................... 40 10.7. Techmex ................................................................................... 41 11. Metals .................................................................................................... 42 11.1. Kęty ........................................................................................... 42 11.2. KGHM ........................................................................................ 43 11.3. Koelner ...................................................................................... 44 12. Construction .......................................................................................... 45 12.1. Budimex ..................................................................................... 48 12.2. Elektrobudowa ........................................................................... 49 12.3. Erbud ......................................................................................... 50 12.4. Polimex Mostostal ...................................................................... 51 12.5. Rafako ....................................................................................... 53 12.6. Ulma Construccion Polska ......................................................... 53 13. Real Estate Developers ......................................................................... 54 13.1. Dom Development ..................................................................... 56 13.2. J.W. Construction ...................................................................... 57 13. Pharmaceutical Manufacturers and Distributors .................................... 58 13.1. Farmacol .................................................................................... 59 13.2. PGF ........................................................................................... 59 13.3. Prosper ...................................................................................... 60 13.4. Torfarm ...................................................................................... 60 14. Retail\Wholesale .................................................................................... 61 14.1. Emperia Holding ........................................................................ 61 14.2. Eurocash ................................................................................... 61 15. Others .................................................................................................... 62 15.1. Kogeneracja .............................................................................. 62 15.2. Mondi ......................................................................................... 62

BRE Bank Securities

3 October 2007 3

Monthly Report BRE Bank Securities

Equity market Dismal US housing and job market data are raising concerns among investors worldwide, but especially in Poland. Neither fears about a financial crisis being triggered by the subprime credit crunch and the state of the US economy, nor predictions of a crash from the likes of Alan Greenspan, kept indexes across global stock markets from nearing or breaking the mid-July highs. If it is so bad, why is it so good? Are we seeing something from our part of the world that global fund managers are not? Is that why our WIG is one of the worst performing indexes in the world? We maintain that a correction is already behind us. We elaborated on the global factors that influence world stock markets in our past reports. As other markets remain strong, a weak WIG enhances the attractiveness of Polish equities, and we expect at least short-term foreign capital to invest. Capital will start flowing to investment funds again on a more bullish sentiment, and we will see a lot of activity on the market, driven among others by short position closing by some traders. One month after a surprise cut, the Fed decided to ease the discount rate again by a further 50pts, and, most importantly, to slash the base rate by 50pts, confirming our September predictions that economic growth is the Fed’s main concern, even at the expense of inflation. Macroeconomists say that if the spread between the discount rate and the Fed Funds Rate is sustained, the latter will be cut further (Commerzbank predicts a decline to 4% at the end of 1Q 2008). Such an aggressive easing is a response to a continued slowdown in the US job market (the unemployment rate is up to 5% from 4.6%) on the back of a housing slump and decreasing investments. As the real-estate market stabilizes and financial organizations start lending again (which is already happening), indebted households will also get back on track (restored liquidity). Lower interest expenses and a weak dollar should drive US corporate earnings, especially for exporters. The dollar depreciation is creating inflationary pressure. With risks still present, the climate for stock price hikes will be increasingly better, and, for the first time in a while, investors will once again believe in a soft landing. By easing policy, the Fed put pressure on the ECB, which was preparing for at least one more hike. The appreciation of the euro against the dollar while interest rates rise, is affecting the European economy; decreasing imports of materials are just one sign of an economic cooling. A rate hike would only deepen the imbalance (further strengthening of the euro), and that is why the ECB will most probably leave its key rate at 4%. Against this USA / Europe policy backdrop, the expected hikes by Poland’s Monetary Policy Council (RPP) will lead to an appreciation of the zloty, with an impact on exporter and importer earnings, providing a further incentive for foreign investors interested in Polish assets.

Most emerging market indexes, including the major ones: China, Brazil, and Asia, have broken over the local highs recorded in mid-July which were followed by a downturn in stocks spurred by the subprime credit crunch “announcement.” The Polish WIG index is 10% off the peak, and displays poor performance relative to most emerging market indexes. The main reason in our view is net selling of Polish equities by foreign capital paired with a lack of demand from

80

106

132

158

184

210

01/02/2007 03/22/2007 06/18/2007 09/06/2007

WIG BovespaKospi S&P500Shanghai Composite

Bovespa, Kospi, S&P500, WIG Indexes

Source: Bloomberg

BRE Bank Securities

3 October 2007 4

Monthly Report BRE Bank Securities

Polish institutions, and fear gripping retail investors since they got a bitter taste of a bear market, both in the primary and secondary markets. According to EmergingPortfolio.com, GEM funds reported $4 billion inflows in September. At the same time, EMEA funds lost $166 million. For comparison, Asia funds attracted $6 billion, and Latin America received $1.2 billion inflows. Except for EMEA, all emerging-market regions recorded considerable injections of “new” capital which more than offset the outflows recorded in late July/early August. The global situation (Asia and Latin America as the primary destinations) reflects on Poland. With no new foreign money flowing into European emerging markets, Polish investment fund companies (TFI) do not record any gains as the “depositors” are still shaken by the recent downslide. This lack is somewhat remedied by open pension funds (OFE), although it is obvious that some managers are underweight on equities relative to the average. When investment funds do not gather new cash, there is no fuel for growth. In our opinion, with liquidity as low as it is, entry into the Polish market of one or two large foreign investors will set the “local buying machine” in motion. An increase in the WIG index will bring capital back to TFIs (refer to last month’s Monthly Report for more in-depth predictions) - we think PLN 3-4bn inflows are a reasonable estimate. Furthermore, an improved sentiment will probably prompt some OFEs to close short positions. Last but not least, a rally will unlock the individual client funds locked into MidCaps, which were most affected by the downturn. A rising market does not bring about an appreciation in stocks across the board. After July, institutional investors will be much more picky with respect to low liquidity stocks. We can also expect that upward market momentum and improved liquidity will be seen as an opportunity to get rid of weaker stocks. We would advise against companies with large export sales, and firms exposed to rising grain prices. In turn, a strengthening zloty will drive the earnings of clothing, computer, and car-parts importers. These sectors also offer exposure to growing internal demand. We remain bullish on building and bank stocks, as well as certain IT stocks. We remain underweight on media and long-term underweight on telecoms; in the near term (one month), this sector will be recovering from the downslide, and displaying strong performance (TPSA could spike to PLN 23).

BRE Bank Securities

3 October 2007 5

Monthly Report BRE Bank Securities

Investment Funds (TFI) Investment funds saw the weakest inflows in August since June 2006, garnering a meager PLN 350 million compared to PLN 5.3 billion a month earlier. Money market funds recorded the largest gains, while equity funds saw 1.2bn outflows. Assets under management declined 2.5% to PLN 137.6bn, following on the heels of stock market falls. Open Pension Funds (OFE) Assets under management of open pension funds (OFEs) shed 0.8% at PLN 136.3bn in August. The equity component shrank 0.2ppts to 36%, and, given that the overall equity portfolio decreased less (-1.4%) than the broad market (WIG down 4.7%), this shrinkage was due to OFEs being overweight in debt and underweight in equities.

Fund Flows

TFI inflows/outflows by “equity component” funds and money market/debt funds

Source: Analizy Online

Emerging Market Funds Investors returned to emerging markets in September, pouring $11.4 billion into EM funds which saw a big improvement from August’s $5.8bn outflows. The inflows were particularly strong in the last week of September ($5.5bn). Asia, mainly China, saw gains over $6 billion, while EMEA funds (including Central Europe) where the only ones that saw outflows (-$0.2bn vs. -$1.0bn in August).

Weekly inflows/outflows for selected emerging market funds

Source: EmergingPortfolio.com

GEM

-3 000

-2 000

-1 000

0

1 000

2 000

3 000

4-01

4-03

4-05

4-07

4-09

4-11

4-01

4-03

4-05

4-07

4-09

mln USD

EMEA

-2 000

-1 500

-1 000

-500

0

500

1 000

4-01

4-03

4-05

4-07

4-09

4-11

4-01

4-03

4-05

4-07

4-09

mln USDmillions of $ millions of $

-2 000

-1 000

0

1 000

2 000

3 000

4 000

5 000

6 000

2006-07-01 2006-10-01 2007-01-01 2007-04-01 2007-07-01

PLN m

Equity, balanced, mixed fundsDebt, money-market, other funds

BRE Bank Securities

3 October 2007 6

Monthly Report BRE Bank Securities

Current Ratings by BRE Bank Securities S.A.

Stock Rating Target Price Date Issued

ABG SPIN Accumulate 7.50 2007-08-28 AGORA Hold 52.20 2007-09-05 ASSECO POLAND Buy 85.45 2007-10-02 BPH Accumulate 986.10 2007-09-04 BUDIMEX Hold 121.70 2007-05-29 BZWBK Accumulate 295.40 2007-10-03 COMARCH Reduce 185.80 2007-02-05 DOM DEVELOPMENT Hold 149.90 2007-09-25 ELEKTROBUDOWA Hold 221.50 2007-05-29 EMPERIA HOLDING Hold 134.17 2007-10-03 ERBUD Accumulate 100.00 2007-07-05 EUROCASH Sell 7.38 2007-02-05 FARMACOL Accumulate 62.90 2007-06-25 HANDLOWY Accumulate 127.10 2007-09-04 ING BSK Hold 921.50 2007-09-04 J.W. CONSTRUCTION Accumulate 56.90 2007-09-25 KĘTY Reduce 187.50 2007-07-27 KGHM Hold 119.00 2007-08-01 KOELNER Hold 53.72 2007-09-06 KOGENERACJA under revision 2007-06-06 KREDYT BANK Buy 27.40 2007-09-04 LOTOS Reduce 42.00 2007-08-16 MACROLOGIC Buy 58.43 2007-02-13 MILLENNIUM Accumulate 13.60 2007-09-04 MONDI Reduce 80.00 2006-12-05 NETIA Sell 3.80 2006-09-06 PEKAO Hold 263.50 2007-10-03 PGF under revision 2007-08-01 PGNiG Hold 5.14 2007-09-06 PKN ORLEN Hold 60.50 2007-10-03 PKO BP Hold 55.50 2007-09-04 POLIMEX MOSTOSTAL Accumulate 10.70 2007-09-05 PROKOM SOFTWARE Hold 150.30 2007-02-05 PROSPER Hold 27.00 2007-06-25 RAFAKO Reduce 11.40 2007-05-29 SYGNITY Buy 81.60 2007-08-28 TECHMEX under revision 2007-03-07 TELEKOMUNIKACJA POLSKA Reduce 20.20 2007-07-05 TORFARM Hold 95.3 2007-06-25 ULMA CONSTRUCCION POLSKA Accumulate 320.8 2007-10-03 WSiP Buy 18.1 2007-07-13 ZA PUŁAWY Accumulate 112.27 2007-09-06

BRE Bank Securities

3 October 2007 7

Monthly Report BRE Bank Securities

Ratings Issued In the Past Month

All Issuers who are clients of BRE Bank Securities

Statistics Sell Reduce Hold Accumula- Buy Sell Reduce Hold Accumulate Buy

count 2 6 16 10 5 0 2 6 3 2 % of total 5.1% 15.4% 41.0% 25.6% 12.8% 0.0% 15.4% 46.2% 23.1% 15.4%

Stock Rating Old Target Price Date Issued

AGORA Hold Accumulate 52.20 2007-09-05

ASSECO POLAND Buy Reduce 85.45 2007-10-02

BPH Accumulate Accumulate 986.10 2007-09-04

BZWBK Buy Hold 295.40 2007-09-04

DOM DEVELOPMENT Hold 149.90 2007-09-25

EMPERIA HOLDING Reduce Hold 134.17 2007-09-06

HANDLOWY Accumulate Hold 127.10 2007-09-04

ING BSK Hold Hold 921.50 2007-09-04

J.W. CONSTRUCTION Accumulate 56.90 2007-09-25

KOELNER Hold Reduce 53.72 2007-09-06

KREDYT BANK Buy Accumulate 27.40 2007-09-04

MILLENNIUM Accumulate Reduce 13.60 2007-09-04

PEKAO Accumulate Hold 263.50 2007-09-04

PGNiG Hold Accumulate 5.14 2007-09-06

PKO BP Hold Reduce 55.50 2007-09-04 POLIMEX MOSTOSTAL Accumulate Accumulate 10.70 2007-09-20

Ratings changed as of Monthly Report date

Stock Rating Old Target Price Date Issued

BZ WBK Accumulate Buy 295.40 2007-10-03

EMPERIA HOLDING Hold Reduce 134.17 2007-10-03

PEKAO Hold Accumulate 263.50 2007-10-03

PKN ORLEN Hold Accumulate 60.50 2007-10-03

ULMA CONSTRUCCION POLSKA Accumulate Hold 320.80 2007-10-03

Ratings Statistics

BRE Bank Securities

3 October 2007 8

Monthly Report BRE Bank Securities

Global factors such as the dollar’s weakness against the euro (at times as weak as 1.50) will be shaping the zloty’s performance going forward. The zloty’s value could reach 2.50 against the dollar and 3.70 against the euro. There might be temporary weakness (down to 2.80 and 3.85 respectively) due to heightened political risk (October elections, followed by government building). The risk will rise again in the second half of next year, when the zloty could depreciate on growing macroeconomic imbalance (public sector, current account deficits). Next year’s government budget deficit is expected to be higher in nominal terms than this year's, and it would be even worse if it were not for an accounting trick whereby some of the gains from our settlements with the EU were carried forward to the next year. This calls into question the soundness of the convergence plan presented to the European Commission to demonstrate compliance with the "Excessive Deficit Procedure." The government is constantly increasing mandatory expenditure. Indexation measures which we strove so hard to eliminate over the past years, are now being restored (social security indexed for inflation, higher base pay), potentially getting public finance in trouble once a seasonal economic slowdown sets in. Warnings have been voiced, and ignored, for months. The monetary policy is shaped by current macroeconomic data, although most investors are inclined to think that the Monetary Policy Council (RPP) is behind the curve, and that returning inflation to target requires further tightening. Granted, the scale of these expectations declined after a good inflation report for August (CPI dropped to 1.5%, all core-inflation indicators were down, with “net inflation” (excl. food and energy prices) as low as 1.2%). The yield curve seems to be more firmly anchored at the long end (due to expectations of a 50bps rate hike in a one-year horizon), than the short end (uncertainty as to the timing of the hikes). The inflation projections slated for October could decide about market performance. If the ECMOD, the National Bank of Poland’s inflation prognostics model, confirms the impact of food and energy prices on this year’s CPI, and the growing significance of rising ULC for 2008-2009 price trends, policy tightening expectations will increase, leading to a steepening of the yield curve along its entire length. GDP at current prices is expected to reach PLN 1252.5bn in 2008 compared to PLN 1156.9bn in 2007, marking a 8.2% increase. At first glance, the basic macroeconomic assumptions used to calculate the budget testify to a prudent, conservative, approach to revenue projections. The projected growth rate does seem a bit too optimistic (~5% would be more realistic than 5.5% for GDP), but the average annual inflation forecast is well undervalued (is: 2.3%, should be: 2.9%), as is salary growth (is: 3.6%, should be: 7%), and employment growth (is: 2%, should be: 4%). In theory, this makes for a potential PLN 4 billion in "extra" revenues. Including revenues posted under “non-refundable receipts from the EU and other sources,” next year’s government revenues are forecasted at PLN 281.8bn compared to this year’s expected PLN 230bn (ca. PLN 16bn more than projected in the Budget Act), marking a ca. 22.6% year-on-year increase, similar to that achieved from 2006 to 2007 – an ambitious goal. Receipts from settlements with the EU show a surprisingly bulky PLN 35.3 billion, implying that the government expects next year’s EU subsidies to be more than double this year’s inflows, and this in the first effective year of the new Financial Perspective, closing the clearance period for the assistance received in the period from 2004 to 2006. As for next year’s expenditures including EU prefinancing, it is estimated at PLN 310.4 billion, 19.7% more than this year. These estimates do not take into account the costs of leveling out retirement benefits calculated under the “old” pension system, estimated at PLN 1.2bn. The solutions adopted by the government in the budget plan, and objective factors such as Poland's contributions to the EU budget and debt service costs, increased the share of mandatory spending in total 2008 expenditure to 70.6% from 65.5% in 2007 (+12.1% in real terms). At the same time, discretionary spending is down 11.7%. If we added to this the additional expenditures proposed by MPs but not included in the budget projections, the share of mandatory spending would rise to 72%.

Macroeconomics

BRE Bank Securities

3 October 2007 9

Monthly Report BRE Bank Securities

Financial Sector Pengab up to 41.8 pts Pengab rose 5.3pts to 41.8pts in September, but is still lower than in September a year ago (43.4 pts), marking the four month of a y/y decline. The bank industry is still thriving, and will probably continue to for the rest of the year (the fourth quarter is always the best for banks). The reasons behind the year-on-year weakness in the sentiment index include a growing base, and far-reaching targets. The highest the Pengab was at since January 2004 was 44.1 pts in April. Compared to this, 41.8pts is still a very good result. Moody's: US subprime credit crunch in not affecting Polish bank ratings According to Moody’s, the subprime crisis is having a marginal impact on Polish banks, and no impact on their ratings. The agency points out that banks are increasingly focusing on retail clients and SMEs, which offer great growth opportunities and higher profit margins than corporate loans. But concentration on the Polish market means sustained competition. We agree. Poles are just starting to borrow money to buy homes. Ca. 1 million households do not own homes yet, hence, most loans are for first homes. Contrary to general belief, Polish banks apply sufficiently stringent home lending rules. Strong demand goes hand in hand with a generally strong economy where unemployment decreases and salaries rise. ZBP on home loan collateral According to the President of the Polish Bank Association (ZBP), there is no reason to worry about a subprime loan crisis happening in Poland. He believes that banks are safe thanks to stringent lending requirements concerning downpayment and LTV, and that home loans are well collateralized and controlled, and are financed with deposits. The ZBP reports that the ratio of bad debt to total home loans is 1.7%-1.8% compared to 3.3% three years ago. This improvement is a result of slower lending and application of new risk management methods. We agree with the ZBP that we could not be farther from a loan crisis, among others because we are at the beginning of a run on home loans, which are mostly taken to finance first homes. 2007 mortgage loan sales forecast The ZBP raised its sales forecast from PLN 54bn to PLN 57bn. 1H’07 home-loan sales amounted to PLN 27.6bn (incl. PLN 15bn zloty loans and PLN 12.6bn foreign currency loans), marking a 54.48% increase on a year earlier and a 22.5% increase from December 2006. The number of loans granted was 159,000 (up 16% y/y). An average facility was a little over PLN 180,000. Total mortgage loan debt at the end of June stood at PLN 95.5bn (up 50% y/y). These data are in line with our expectations, although one might have hoped for an even larger home-loan output considering the sales figures reported by banks after two months of 3Q. We are waiting for more information on sales, which, we think, are likely to exceed PLN 60bn. Cash war According to newspapers, banks are competing to lend cash. PKO BP has launched a new cash loan offer, where clients can borrow up to PLN 20,000 without collateral or proof of income from employers. All it takes is a statement of income and an ID. The new product is addressed to low-income clients, including retirees, and will be widely advertised. In turn, BZ WBK raised the financing cap from 15 to 20 salaries, lowered interest rates and the eligible income threshold, and cut the decision time to 5 minutes. ING BSK has also simplified lending procedures recently. The battle for retail customers is on, and cash loans will be the main weapon. Fees are not the main consideration for cash borrowers, who pay more attention to availability and service. Banks are turning toward cash loans because mortgage loans generate low margins. In December 2006, the value of consumer loans (incl. cash loans, installment plans, and car loans) stood at PLN 53bn, and increased to PLN 63bn in July 2007. Experts say that cash loans will rise by 30% annually in the next few years. More ATMs The number of ATMs is expected to increase by 1,000 to 11,000 this year. In Europe, the widest ATM network can be found in the UK (60,600), followed by Spain (close to 58,000), and Germany (53,600). According to RBR, there are currently 342,500 ATMs installed across Europe. Banks are deploying new ATMs with new branches as a way of reducing customer service costs. Banks earn on insurance sales The WSJ writes about the market of bancassurance, pointing out that banks are constantly increasing the fees charged for insurance sales. Insurers agree, saying that, in some cases, the charges reach levels at which the products are no longer profitable to sell. Still, insurance companies want to cooperate with banks, looking to benefit from their large sales networks. Life insurers sell 21% of policies via banks, compared to 11.6% a year ago. Banks are strengthening their positions as insurance distributors, and their role will continue to increase for a while. In the

BRE Bank Securities

3 October 2007 10

Monthly Report BRE Bank Securities

future, direct insurance could take over. For now, direct sales are mainly used for car insurance. Soon, as insurers include more advanced products that are currently sold via banks, sales charges will have to go down. For now, insurance sales boost fee income for banks, virtually all of which have distribution agreements with insurance companies. Getin Bank, BRE Bank, and Kredyt Bank are offering policies from members of their fellow subsidiaries, and will not lose this source of income even as direct insurance expands. All in all, we think that insurers will continue to use banks as distribution channels, especially given that most of them are currently expanding their sales networks and increasing coverage. Record year for lease finance The value of leased assets increased 70% y/y to PLN 14.7bn in 1H’07. Car leases have a 62% share in the overall portfolio and are expected to stay high in the periods ahead on strong momentum in the automotive industry. The share of machine and equipment leases is on the rise (up from 25% a year earlier to 27% in 1H’07). Real-estate leases have a small, 8% share, but this following a 300% y/y surge in 1H. An obstacle to lease finance growth are certain tax regulations. We expect the upward trends to continue, with an increasing share of machine and equipment leases. Growth could slow down against an increasing comparable base, and margins could tighten due to fierce competition, but fast-paced volumes will offset this decline. Staff turnover in bank industry Parkiet reports that staff turnover is heaviest between the most aggressive market players. For instance, 687 people left Bank Handlowy by July, i.e. 12% of staff since the end of 2006, GE Money Bank lost 7.7% of staff, and Bank Millennium and ING BSK lost 7.6% of staff. At the same time, banks recorded a nominal increase in headcounts. The three leading banks are not affected by this trend for now. PKO BP has been downsizing for some time (with plans to cut staff by 1500 people a year), and 4.3% of its staff left in 1H, but net churn was only 2% thanks to new employees hired in the period. As for Pekao and BPH, turnover is smaller than a year ago despite the upcoming merger. Banks have to increase costs to hire new people. Aggressive players will lose personnel to competition. Heavy turnover is bound to continue as long as the industry is booming, driving salaries. We are not concerned about the impact of growing labor costs on operating efficiency, as higher salaries mean higher sales, and hence stronger revenues. Further, growing costs are not affecting efficiency ratios. At some point, banks will stop “buying” personnel from competition. Loan securitization The WSJ writes about banks who plan to securitize their loan portfolios. One of them is Millennium, which was going to securitize a PLN 800m lease portfolio in late September, and is considering doing the same with mortgage loans. Kredyt Bank has the same plan. Securitization helps banks retain their CAR at a safe level without increasing capital. It is a transaction whereby a bank sells its receivables to a specialized firm or fund in exchange for a portion of the receivables. Banks have been using securitization to clear their NPL portfolios, but are increasingly considering doing the same with non-loss loans. Millennium revealed plans to that effect during the 2Q’07 earnings announcement, without disclosing the size of the loan portfolio. If the WSJ is right, the bank will see a one-time gain which we did not take into account in our earnings projections for FY2007 or subsequent years. Similarly, we did not take securitization into consideration when making estimates for Kredyt Bank. In the west, securitization is a way of managing operating effectiveness, but, given how borrowers increasingly fall into default, banks might not get equally high prices for their portfolios as they have to date. On the other hand, securitized bad-debt portfolios are not very large compared to other countries. Securitization is no doubt good for effectiveness assuming that a bank can rebuild the portfolio. Lukas Bank wants 4-5 million accounts by 2012 The bank is preparing a strategy of evolving into a more universal financial services provider. To date, Lukas Bank has been known mainly as provider of cash loans, installment plans, and credit cards. Ranked 16th in equity, the bank is the runner up in the number of credit cards right after the leader, PKO BP. The new plan is to establish a stronger presence in savings and insurance sales, and develop own insurance products. Lukas also wants to establish more relationships with retail chains as well as firms with large customer bases, such as Orange. Recently, the bank launched services targeted to SMEs and hopes to increase its share in this market (companies with sales approximating PLN 3m) to 4% next year from ca. 3%. Also on Lukas’s agenda is sales expansion through 50 new branches and 20 credit centers in 2007 and 100 branch openings in 2008. By the end of next year, the sales network will consist of 450 branches and 180 credit centers, double what it is now. All these measures are aimed at acquiring ca. 500,000 new clients a year, meaning that the target client base will count 4.5-5 million compared to 2.3 million now. A move beyond consumer finance will show whether Lukas Bank has a chance of increasing market share. We do not know whether the bank plans to go into mortgage lending, but it would definitely help. The scale of Lukas Bank’s growth plans is comparable with Millennium, Poland’s eighth largest bank in terms of assets and equity, running

BRE Bank Securities

3 October 2007 11

Monthly Report BRE Bank Securities

370 branches (as of May 2007) and serving 842,000 clients (as of June 2007), which wants to increase the number of branches to 560 and the client base to 1.2 million by the end of 2009. Given that Lukas Bank has been selling its products through retail chains (installment plans, cash loans, credit cards), it might be hard to transform itself into a universal bank, especially since it will be competing with the largest financial providers in Poland. We suspect that Lukas’s plan is to win clients from competition. DnB NORD to announce three-year strategy in November The bank formed by the merger between DnB NORD and BISE is set to reveal a three-year strategy in November. Plans include increasing the number of branches to 100 by 2010 (from 50 plus 6 regional corporate centers), and launching new products. The new bank will keep the payment processing chain “Monetia” which consists of 200 branches, and plans to launch sales of selected financial products in 2008. These changes are expected to cost PLN 50 million in 2007 and 2008 (new branches, products, computer system). The combined assets of the two banks exceeded PLN 6 billion at the end of August, and are expected to increase to PLN 6.5bn by December. Net income amounted to PLN 12m year to August. Shareholders of both DnB Nord and BISE approved the merger, and are waiting for clearance from bank supervision. The new bank will remain a second-league player. According to a survey conducted at the end of 2006, PLN 6bn assets would rank it 20th (BISE was 27th, and DnB NORD was 31st). But the merged bank could have a stronger positioning in the corporate banking sector. Negotiations for Expander shares GE Investments narrowed down the list of bidders for a 49%) stake in Expander. The acquisition is expected to be finalized in 1Q’08. Meanwhile, Expander plans to open 8-10 new branches this year, and have 60 branches by the end of the year. The financial intermediary currently operates through 48 branches, half of them partner outlets, employing 263 consultants. We are waiting to hear who wins the bidding, and for how much. Loan sales via intermediaries reach PLN 11.6bn in 1H’07 The Central Statistical Office (GUS) reported that financial intermediaries sold PLN 11.6bn-worth of loans in 1H’07, marking a 48% increase y/y. The survey covered 35 agents who sold a total of 2.2 million facilities (17.5% more than a year earlier). The main sales drivers were cash loans (96% y/y), and mortgage loans (62% y/y). The average mortgage loan sold by intermediaries in 1H’07 was PLN 253,000, PLN 53,000 more than in 1H’06. Year to September, the home loan portfolio amounted to PLN 106.3bn, with PLN 5.1bn-worth extended in August, just a little less than in record-breaking July. 1H’07 mortgage loan sales stood at PLN 28bn. There is no data on sales volumes. Financial intermediaries are obviously on an upward momentum. Last year, the leading nine intermediated PLN 11bn-worth of credit facilities, and, this year, they sold the same amount after just six months. Getin Holding: Acquisition of ASK Investments Getin Holding signed an agreement to acquire ASK from Krzysztof Spyra, Jarosław Augustyniak, and Maurycy Kuhn, each selling 110 shares with a par value of EUR 100 (PLN 382.5). The total price paid for a 100% stake was EUR 33,000 (PLN 126.24 thousand). ASK Investments transferred its shareholdings in Noble Bank (15 million shares) to three companies: A. Nagelkerken Holding BV, HP Holding 3 BV, and International Consultancy Strategy Implementation BV, owned by Messrs Maurycy Kuhn, Jarosław Augustyniak, and Krzysztof Spyra respectively. Getin Holding: Getin Bank’s deposits at PLN 8.99bn (Aug’07) This after a PLN 2bn YTD increase. At the end of June, deposits stood at PLN 8.16bn at Getin Bank, and PLN 8.6bn across Getin Holding. Y/Y growth was reported at PLN 0.3bn in 1Q’07, and PLN 1.7bn in 2Q. This fast–paced growth is an effect of an intense advertising campaign in May and June. In September, the bank is starting a campaign to promote its term-deposit products. Getin Bank is committed to growing deposits to gain capital to finance lending, with the help of intense (and successful) advertising. Getin Holding: July/August loan sales at PLN 1.66bn The holding saw a whopping 79% y/y increase in sales, which remain unaffected by seasonal weakness. The largest increase was recorded in consumer loans, the business which offers the largest growth potential for Getin Bank, which reported a staggering 200% y/y increase in sales to PLN 250m. The bank’s CEO stressed that growth in sales of car loans and mortgage loans is achieved without increasing credit risk. Getin Holding has several subsidiaries for which loans sales are a key earnings driver. These include two banks selling their own products, Getin Bank and Metrobank, and financial intermediaries selling third-party facilities. Getin Bank generated PLN 2.8bn from sales of its own products in 1H'07 (PLN 665m from car loans, PLN 1.5bn from mortgage loans, and PLN 654m from cash loans), and Metrobank generated PLN 428m. All in all, “in-house output” amounted to PLN 3.247 billion. In the first half of 2007, average quarterly sales stood at PLN 1.623 billion. In 3Q’07, July and August alone saw a combined PLN 1.66bn,

BRE Bank Securities

3 October 2007 12

Monthly Report BRE Bank Securities

and September should traditionally bring even stronger sales, meaning that Getin Bank can look forward to a record quarter. Getin Holding: Acquisitions in Romania, Bulgaria Getin is restructuring its Ukrainian subsidiary Prikarpattya Bank, and looking for new acquisition targets in Romania and Bulgaria. The holding could also change its expansion plans for Russia: instead of looking for an existing bank with a license, it might build its own operations from scratch, and expand sales on the basis of the lease finance subsidiary Carcade. Bulgarian and Romanian acquisitions are in an early planning stage. Getin Holding sees these markets as offering great growth opportunities. As for Russia, organic growth is not going to bring results as fast as an acquisition would. Noble Bank: Mortgage loan sales In 2.5 years, sales of mortgage loans by Metrobank could account for 30%–40% of the group’s total sales (through Open Finance and Metrobank). Metrobank currently sells over PLN 100m-worth of loans a month and hopes to maintain this pace going forward. In 1H’07, the Noble Bank group sold PLN 2.35bn-worth of mortgage loans, of which 18% were its own products. According to the management, sales of in-house products will increase going forward. Sales of own products display faster growth rates than third-party product sales through Open Finance, largely because of a different base. Open Finance has been present on the market for a few years, and is a leading financial intermediary, while Metrobank started to sell its own products toward the end of last year, with success. Noble TFI: over PLN 1bn under management in 10 months The investment fund subsidiary of Noble Bank (76.2%) has garnered PLN 1bn AUM. PLN 640m of these assets are managed by Noble Funds FIO, and PLN 378m are managed by individuals. Noble TFI has been operating for 10 months. Noble Funds TFI posted a PLN 2.8m net income for 1H, and contributed 2.9% of the group’s banking income and 2.7% to net income. Robust growth in AUM could be expected. AUM stood at PLN 726m at the end of June, and soared by almost PLN 300m within three months. Noble Bank: Conquering Ireland Open Finance set up a company in Ireland to acquire clients and market Open Finance products. On June 7th, OF acquired 100,000 shares of the common stock (EUR 1 par value) of “Open Finance Marketing Ireland Limited” with a share capital of EUR 100,000. PLN 384.85 thousand). The company’s task is to reach Poles living in Ireland with Open Finance’s offer. Because it is small, it will not have much impact on Noble’s earnings.

BRE Bank Securities

3 October 2007 13

Monthly Report BRE Bank Securities

Analyst: Marta Jeżewska19 Last Recommendation: 2007-09-04(PLN m) 2006 2007F change 2008F change 2009F change Basic data (PLN m)Net interest income 2 175.5 2 238.9 2.9% 2 346.1 4.8% Number of shares (m) 28.7Interest margin 3.5% 3.5% 3.6% MC (current price) 26 720.4Revenue f/banking oper. 3 533.6 3 646.0 3.2% 3 873.0 6.2% Free float 25.3%Operating profit 1 853.8 2 171.2 17.1% 2 195.8 1.1%Gross profit 1 633.6 1 895.1 16.0% 1 898.6 0.2%Net prof it 1 267.8 1 493.7 17.8% 1 491.6 -0.1%

ROE 19.2% 21.1% 20.0% Price change: 1 month 0.4%P/E 21.1 17.9 17.9 Price change: 6 month -9.5%P/BV 3.9 3.7 3.5 Price change: 12 month 12.8%D/PS 30.0 36.2 42.7 42.6 Max (52 w eek) 1 088.0Dyield (%) 3.2 3.9 4.6 4.6 Min (52 w eek) 802.0

Current price: PLN 930.5 Target price: PLN 986.1BPH (Accumulate)

650

800

950

1100

1250

2006-09-26 2007-01-18 2007-05-14 2007-09-03

BPH WIG

Returns on BPH shares are still conditioned on the market valuation of Pekao, and the selling price of the Mini-BPH. At Pekao’s current price (PLN 253.2/share), BPH shareholders could get PLN 835.56 for each share transferred to Pekao. Further, our valuation methodology assumes that BPH shareholders will get PLN 117 per share in a tender offer which we expect GE Money to hold for the shares of Mini-BPH outstanding after it is taken over from UniCredit. This would figure to PLN 952 per share of BPH at the current price level. We have a PLN 263.5 target on Pekao, and rate the stock as an ACCUMULATE. BPH is an ACCUMULATE as well, with a 6% upside potential. Management reshuffle BPH’s supervisory board appointed Messrs Kazimierz Łabno and Carl Normann Voekt to the Management Board. At the same time, retiring VP in charge of operations, information, and services Anton Knett tendered his resignation. GINB sure to allow BPH division There is a general consensus that the General Inspectorate for Bank Supervision (GINB) is going to give a green light to the division of BPH and merger with Pekao. We have not had any doubt about that since April 2006, when, after weeks of negotiating, UniCredit reached an agreement with the Polish government about how to carry out the spin-off. The Commission for Bank Supervision (KNB) is holding its next meeting at October 3rd.

BRE Bank Securities

3 October 2007 14

Monthly Report BRE Bank Securities

Analyst: Marta Jeżewska44 Last Recommendation: 2007-10-03(PLN m) 2006 2007F change 2008F change 2009F change Basic data (PLN m)Net interest income 1 034.2 1 248.6 20.7% 1 498.4 20.0% 1 689.0 12.7% Number of shares (m) 73.0Interest margin 3.3% 3.5% 3.7% 3.7% MC (current price) 19 115.6Revenue f/banking oper. 2 365.2 2 933.2 24.0% 3 484.9 18.8% 3 931.4 12.8% Free float 29.5%Operating profit 1 084.1 1 531.7 41.3% 1 895.3 23.7% 2 149.0 13.4%Gross profit 516.3 758.2 46.9% 1 067.0 40.7% 1 254.0 17.5%Net prof it 758.2 1 067.0 40.7% 1 254.0 17.5% 1 389.7 10.8%

ROE 20.7% 25.0% 25.6% 25.2% Price change: 1 month -0.1%P/E 25.2 17.9 15.2 13.8 Price change: 6 month -7.3%P/BV 4.8 4.2 3.7 3.3 Price change: 12 month 31.4%D/PS 6.0 6.0 8.8 10.3 Max (52 w eek) 315.3Dyield (%) 2.3 2.3 3.3 3.9 Min (52 w eek) 192.5

BZ WBK (Accumulate)Current price: PLN 262 Target price: PLN 295.4

170

210

250

290

330

2006-09-26 2007-01-18 2007-05-14 2007-09-03

BZ WBK WIG

We continue to have a positive outlook on BZ WBK, but are downgrading it from Buy to ACCUMULATE after a recent rally. The stock still offers a 12.7% upside potential. Because the bank follows a strategy of growth across all business lines, a weakness in one line will not have any impact on long-term growth. BZ WBK trades at a close-to 7% discount to the industry's FY‘07E P/E. Efforts aimed at increasing retail loan sales (mainly cash loans, but also mortgage loans), paired with a strong presence in the corporate segment (corporate loans surged 24% y/y in June), will reinforce the bank’s presence in commercial banking. Revamping the mortgage loan offer BZ WBK has an ambition to increase sales over PLN 800m (the bank sold PLN 806m-worth of loans in 1H), and expand the mortgage loan portfolio at a much faster rate than the 33% recorded at the end of June 2007. January will see big changes in the home loan offering According to the bank, the portfolio will accelerate in 2H compared to 1H. Faster growth in mortgage loans will translate to an increasing number of clients using BZ WBK’s other services. It is hard to predict the impact of relaxed lending procedures on loan sales, which we expect to increase 34% in FY2007. 2H should be better than 1H in this respect thanks to seasonal strength driving sales volumes. Cash loan portfolio to expand at least 50% BZ WBK hopes that its cash loan portfolio will increase at least at the same rate in FY2007 as in FY2006, when it surged 54%. At the end of June, cash loans stood at PLN 1.19bn (+51% y/y). The bank lent cash to 22 thousand borrowers in 1Q, up to 27 thousand in 2Q. Sales are expected to advance with support from external channels such as mobile sales and credit agents, as well as e-banking. BZ WBK launched a new, widely advertised cash loan offer in September. 50% y/y growth is in line with our expectations. The bank is strengthening its presence in the retail lending market (in particular cash loans and mortgage loans), It has plans to open 50 branches and ca. 100 franchise outlets in 2007. BZ WBK is committed to its versatile growth strategy. We are reiterating a positive rating on the bank. BZ WBK to launch private banking in 2008 BZ WBK’s managers think that Polish clients have accumulated enough wealth to qualify for private banking services, and are increasingly reaching for complex financial products and seeking foreign investments. Private banking is an element of the bank’s growth strategy. BZ WBK has not revealed what minimum net worth it will require. A new product lines is a good move. Rising salaries, increasing knowledge about bank services among the general population, and growing savings, will drive demand for private banking services.

BRE Bank Securities

3 October 2007 15

Monthly Report BRE Bank Securities

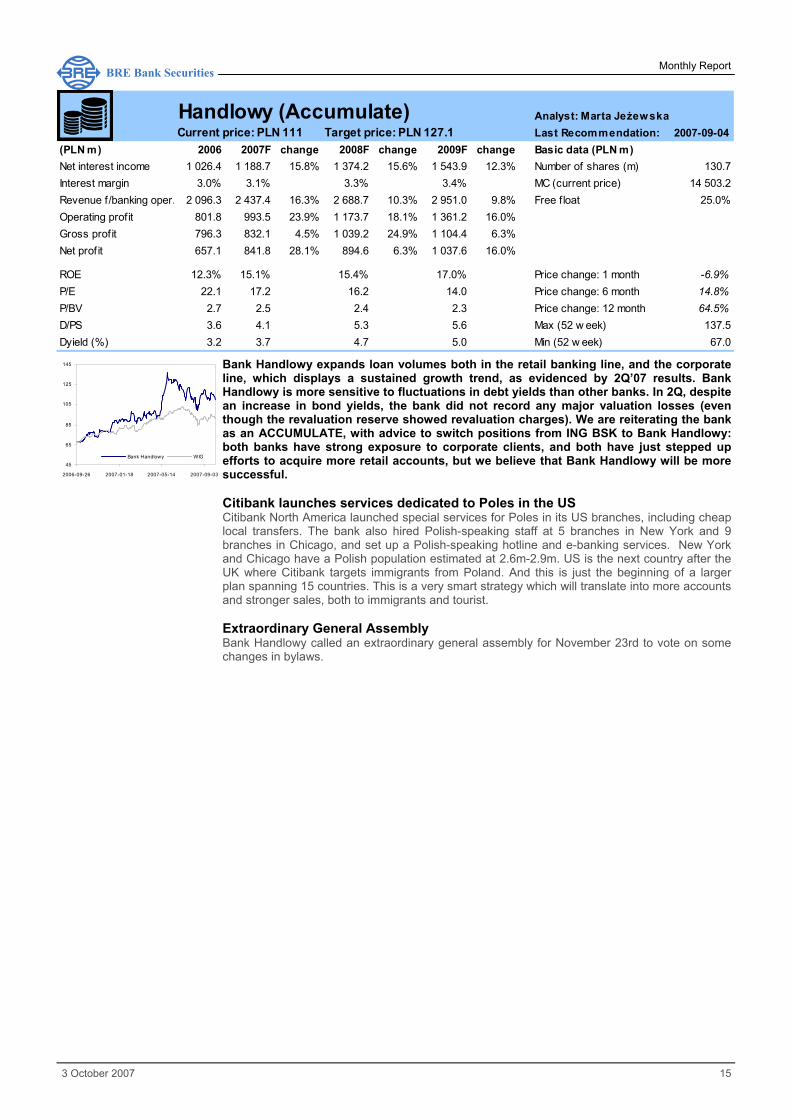

Analyst: Marta Jeżewska12 Last Recommendation: 2007-09-04(PLN m) 2006 2007F change 2008F change 2009F change Basic data (PLN m)Net interest income 1 026.4 1 188.7 15.8% 1 374.2 15.6% 1 543.9 12.3% Number of shares (m) 130.7Interest margin 3.0% 3.1% 3.3% 3.4% MC (current price) 14 503.2Revenue f/banking oper. 2 096.3 2 437.4 16.3% 2 688.7 10.3% 2 951.0 9.8% Free float 25.0%Operating profit 801.8 993.5 23.9% 1 173.7 18.1% 1 361.2 16.0%Gross profit 796.3 832.1 4.5% 1 039.2 24.9% 1 104.4 6.3%Net prof it 657.1 841.8 28.1% 894.6 6.3% 1 037.6 16.0%

ROE 12.3% 15.1% 15.4% 17.0% Price change: 1 month -6.9%P/E 22.1 17.2 16.2 14.0 Price change: 6 month 14.8%P/BV 2.7 2.5 2.4 2.3 Price change: 12 month 64.5%D/PS 3.6 4.1 5.3 5.6 Max (52 w eek) 137.5Dyield (%) 3.2 3.7 4.7 5.0 Min (52 w eek) 67.0

Current price: PLN 111 Target price: PLN 127.1Handlowy (Accumulate)

45

65

85

105

125

145

2006-09-26 2007-01-18 2007-05-14 2007-09-03

Bank Handlowy WIG

Bank Handlowy expands loan volumes both in the retail banking line, and the corporate line, which displays a sustained growth trend, as evidenced by 2Q’07 results. Bank Handlowy is more sensitive to fluctuations in debt yields than other banks. In 2Q, despite an increase in bond yields, the bank did not record any major valuation losses (even though the revaluation reserve showed revaluation charges). We are reiterating the bank as an ACCUMULATE, with advice to switch positions from ING BSK to Bank Handlowy: both banks have strong exposure to corporate clients, and both have just stepped up efforts to acquire more retail accounts, but we believe that Bank Handlowy will be more successful. Citibank launches services dedicated to Poles in the US Citibank North America launched special services for Poles in its US branches, including cheap local transfers. The bank also hired Polish-speaking staff at 5 branches in New York and 9 branches in Chicago, and set up a Polish-speaking hotline and e-banking services. New York and Chicago have a Polish population estimated at 2.6m-2.9m. US is the next country after the UK where Citibank targets immigrants from Poland. And this is just the beginning of a larger plan spanning 15 countries. This is a very smart strategy which will translate into more accounts and stronger sales, both to immigrants and tourist. Extraordinary General Assembly Bank Handlowy called an extraordinary general assembly for November 23rd to vote on some changes in bylaws.

BRE Bank Securities

3 October 2007 16

Monthly Report BRE Bank Securities

Analyst: Marta Jeżewska017 Last Recommendation: 2007-09-04

(PLN m) 2006 2007F change 2008F change 2009F change Basic data (PLN m)Net interest income 936.3 1 071.1 14.4% 1 235.9 15.4% 1 399.1 13.2% Number of shares (m) 13.0Interest margin 2.1% 2.0% 2.1% 2.1% MC (current price) 11 962.7Revenue f/banking oper. 1 755.4 2 110.6 20.2% 2 397.9 13.6% 2 658.5 10.9% Free float 18.5%Operating profit 539.6 772.6 43.2% 949.3 22.9% 1 107.7 16.7%Gross profit 705.6 753.3 6.8% 857.2 13.8% 914.9 6.7%Net prof it 591.4 684.4 15.7% 729.7 6.6% 848.4 16.3%

ROE 16.2% 17.5% 17.2% 18.3% Price change: 1 month 0.2%P/E 20.2 17.5 16.4 14.1 Price change: 6 month 18.2%P/BV 3.2 2.9 2.7 2.5 Price change: 12 month 36.2%D/PS 27.5 27.9 32.3 28.0 Max (52 w eek) 1 075.0Dyield (%) 3.0 3.0 3.5 3.0 Min (52 w eek) 670.5

ING BSK (Hold)Current price: PLN 919.5 Target price: PLN 921.5

600

700

800

900

1000

1100

2006-09-26 2007-01-18 2007-05-14 2007-09-03

ING BSK WIG

ING BSK has a strong positioning in corporate banking, and runs a successful securities brokerage business and investment fund company (a member of ING International), all of which gave a 30% boost to its second-quarter earnings. The momentum in volumes propels operating income before provisions which rose 14% y/y in 2Q’07 and over 21% y/y in 1H’07, in line with our expectations. We revise our CAGR estimates for ING BSK’s operating income before provisions to 43% in FY2007, 23% in FY2008, and 17% in FY2009 We are confident that the bank will meet our earnings expectations, which, we think, are already fully priced in its stock. We are reiterating a HOLD rating. Sale of NPLs ING BSK is going to sell its corporate loss loans with a total nominal value of PLN 827.2m (PLN 676.8m principal, PLN 150.4m interest) in 4Q’07 or 1Q’08. Assuming that the bank sells the NPLs for 10% - 15% of their nominal value, the impact on operating income could range from PLN 83m to PLN 124m (PLN 67-100m to net income). The actual price will depend on the outcomes of the buyer’s audit. ING BSK has provisions recognized against the total of its loss loans. The bank might decide to pay out the whole amount of the subsequent reversals as dividends to shareholders, either in 2008, or 2009. The sale will add PLN 5.2-7.7 per share (0.5% - 0.9% of the current market price), and will not have influence either on the bank’s stock performance, or our target price. Purchase of shares in “Centrum Banku Śląskiego” ING BSK purchased a 40% stake ub Centrum Banku Śląskiego (CBS) for EUR 5mln , i.e. PLN 18.865m (36 716 shares with a par value of PLN 1000). ING BSK has a 100% stake in ING Development, owner of the remaining 60% stake in CBS, meaning that, after the deal is final, the bank will own 100%. Centrum Banku Śląskiego was established in 1998 to build the two office buildings of ING BSK. Management Board reshuffle Mr. Ian B. Clone tendered his resignation as Vice-President of the Management Board effective December 1st for personal reasons. He will be replaced by Mr. Oscar Edward Swan subject to approval by the Commission for Bank Supervision. News without impact on stock performance. Mr. Swan has been with ING BSK since 2004, most recently as Head of Market Risk Management. Previously, he worked in financial market risk management at BZ WBK from 2002, and earlier still, he held a position with ING BSK.

BRE Bank Securities

3 October 2007 17

Monthly Report BRE Bank Securities

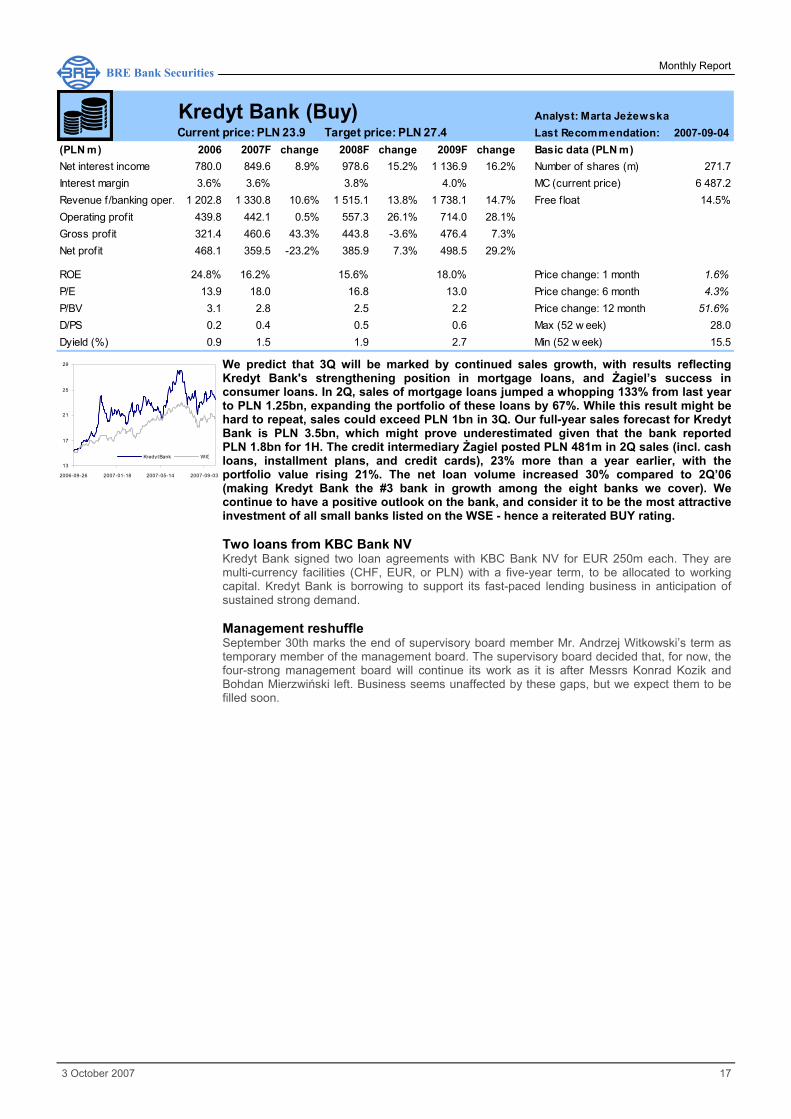

Analyst: Marta Jeżewska011 Last Recommendation: 2007-09-04(PLN m) 2006 2007F change 2008F change 2009F change Basic data (PLN m)Net interest income 780.0 849.6 8.9% 978.6 15.2% 1 136.9 16.2% Number of shares (m) 271.7Interest margin 3.6% 3.6% 3.8% 4.0% MC (current price) 6 487.2Revenue f/banking oper. 1 202.8 1 330.8 10.6% 1 515.1 13.8% 1 738.1 14.7% Free float 14.5%Operating profit 439.8 442.1 0.5% 557.3 26.1% 714.0 28.1%Gross profit 321.4 460.6 43.3% 443.8 -3.6% 476.4 7.3%Net prof it 468.1 359.5 -23.2% 385.9 7.3% 498.5 29.2%

ROE 24.8% 16.2% 15.6% 18.0% Price change: 1 month 1.6%P/E 13.9 18.0 16.8 13.0 Price change: 6 month 4.3%P/BV 3.1 2.8 2.5 2.2 Price change: 12 month 51.6%D/PS 0.2 0.4 0.5 0.6 Max (52 w eek) 28.0Dyield (%) 0.9 1.5 1.9 2.7 Min (52 w eek) 15.5

Kredyt Bank (Buy)Current price: PLN 23.9 Target price: PLN 27.4

We predict that 3Q will be marked by continued sales growth, with results reflecting Kredyt Bank's strengthening position in mortgage loans, and Żagiel’s success in consumer loans. In 2Q, sales of mortgage loans jumped a whopping 133% from last year to PLN 1.25bn, expanding the portfolio of these loans by 67%. While this result might be hard to repeat, sales could exceed PLN 1bn in 3Q. Our full-year sales forecast for Kredyt Bank is PLN 3.5bn, which might prove underestimated given that the bank reported PLN 1.8bn for 1H. The credit intermediary Żagiel posted PLN 481m in 2Q sales (incl. cash loans, installment plans, and credit cards), 23% more than a year earlier, with the portfolio value rising 21%. The net loan volume increased 30% compared to 2Q’06 (making Kredyt Bank the #3 bank in growth among the eight banks we cover). We continue to have a positive outlook on the bank, and consider it to be the most attractive investment of all small banks listed on the WSE - hence a reiterated BUY rating. Two loans from KBC Bank NV Kredyt Bank signed two loan agreements with KBC Bank NV for EUR 250m each. They are multi-currency facilities (CHF, EUR, or PLN) with a five-year term, to be allocated to working capital. Kredyt Bank is borrowing to support its fast-paced lending business in anticipation of sustained strong demand. Management reshuffle September 30th marks the end of supervisory board member Mr. Andrzej Witkowski’s term as temporary member of the management board. The supervisory board decided that, for now, the four-strong management board will continue its work as it is after Messrs Konrad Kozik and Bohdan Mierzwiński left. Business seems unaffected by these gaps, but we expect them to be filled soon.

13

17

21

25

29

2006-09-26 2007-01-18 2007-05-14 2007-09-03

Kredyt Bank WIG

BRE Bank Securities

3 October 2007 18

Monthly Report BRE Bank Securities

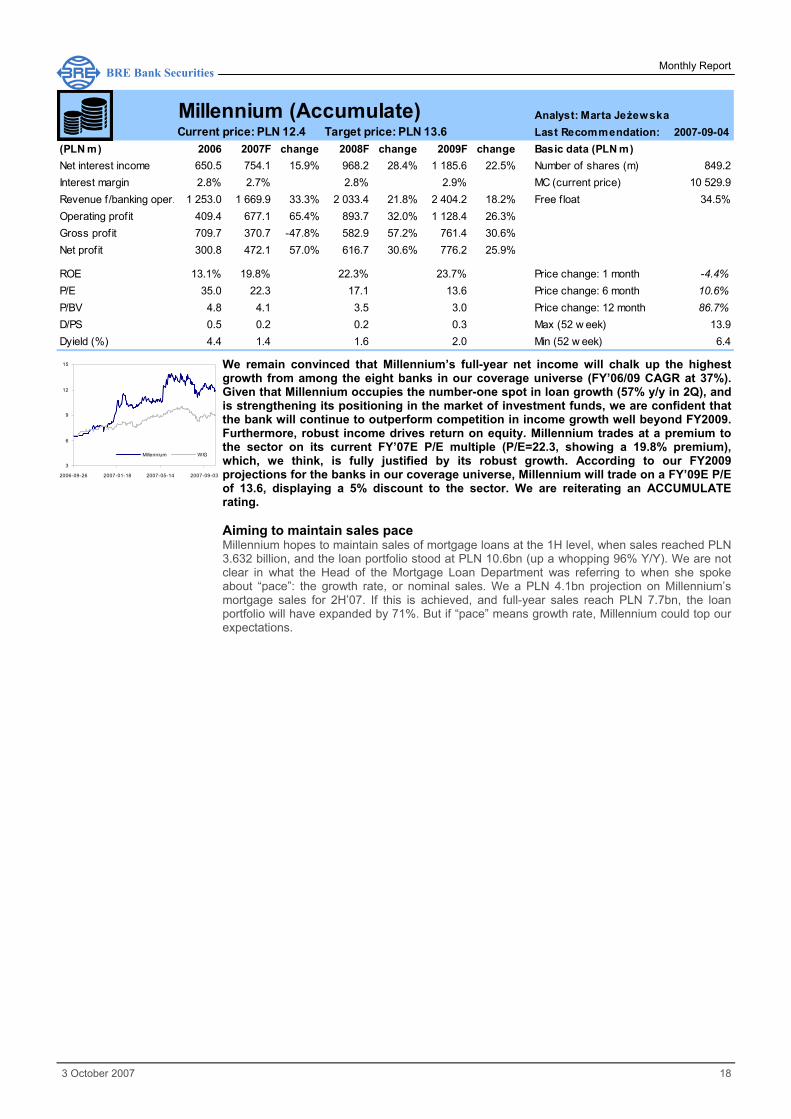

Analyst: Marta Jeżewska16 Last Recommendation: 2007-09-04(PLN m) 2006 2007F change 2008F change 2009F change Basic data (PLN m)Net interest income 650.5 754.1 15.9% 968.2 28.4% 1 185.6 22.5% Number of shares (m) 849.2Interest margin 2.8% 2.7% 2.8% 2.9% MC (current price) 10 529.9Revenue f/banking oper. 1 253.0 1 669.9 33.3% 2 033.4 21.8% 2 404.2 18.2% Free float 34.5%Operating profit 409.4 677.1 65.4% 893.7 32.0% 1 128.4 26.3%Gross profit 709.7 370.7 -47.8% 582.9 57.2% 761.4 30.6%Net prof it 300.8 472.1 57.0% 616.7 30.6% 776.2 25.9%

ROE 13.1% 19.8% 22.3% 23.7% Price change: 1 month -4.4%P/E 35.0 22.3 17.1 13.6 Price change: 6 month 10.6%P/BV 4.8 4.1 3.5 3.0 Price change: 12 month 86.7%D/PS 0.5 0.2 0.2 0.3 Max (52 w eek) 13.9Dyield (%) 4.4 1.4 1.6 2.0 Min (52 w eek) 6.4

Millennium (Accumulate)Current price: PLN 12.4 Target price: PLN 13.6

3

6

9

12

15

2006-09-26 2007-01-18 2007-05-14 2007-09-03

Millennium WIG

We remain convinced that Millennium’s full-year net income will chalk up the highest growth from among the eight banks in our coverage universe (FY’06/09 CAGR at 37%). Given that Millennium occupies the number-one spot in loan growth (57% y/y in 2Q), and is strengthening its positioning in the market of investment funds, we are confident that the bank will continue to outperform competition in income growth well beyond FY2009. Furthermore, robust income drives return on equity. Millennium trades at a premium to the sector on its current FY’07E P/E multiple (P/E=22.3, showing a 19.8% premium), which, we think, is fully justified by its robust growth. According to our FY2009 projections for the banks in our coverage universe, Millennium will trade on a FY’09E P/E of 13.6, displaying a 5% discount to the sector. We are reiterating an ACCUMULATE rating. Aiming to maintain sales pace Millennium hopes to maintain sales of mortgage loans at the 1H level, when sales reached PLN 3.632 billion, and the loan portfolio stood at PLN 10.6bn (up a whopping 96% Y/Y). We are not clear in what the Head of the Mortgage Loan Department was referring to when she spoke about “pace”: the growth rate, or nominal sales. We a PLN 4.1bn projection on Millennium’s mortgage sales for 2H’07. If this is achieved, and full-year sales reach PLN 7.7bn, the loan portfolio will have expanded by 71%. But if “pace” means growth rate, Millennium could top our expectations.

BRE Bank Securities

3 October 2007 19

Monthly Report BRE Bank Securities

Analyst: Marta Jeżewska016 Last Recommendation: 2007-10-03(PLN m) 2006 2007F change 2008F change 2009F change Basic data (PLN m)Net interest income 2 377.0 2 485.4 4.6% 2 740.9 10.3% 2 942.5 7.4% Number of shares (m) 167.1Interest margin 3.7% 3.5% 3.5% 3.5% MC (current price) 42 310.5Revenue f/banking oper. 4 656.4 5 115.5 9.9% 5 664.8 10.7% 6 184.9 9.2% Free float 43.1%Operating profit 2 335.2 2 605.8 11.6% 3 027.8 16.2% 3 443.8 13.7%Gross profit 1 873.6 2 203.8 17.6% 2 580.2 17.1% 2 995.2 16.1%Net prof it 1 787.5 2 087.7 16.8% 2 423.9 16.1% 2 746.1 13.3%

ROE 20.7% 22.8% 24.7% 26.2% Price change: 1 month 2.2%P/E 23.6 20.3 17.5 15.4 Price change: 6 month -4.7%P/BV 4.8 4.5 4.2 3.9 Price change: 12 month 28.0%D/PS 7.4 9.0 10.5 12.2 Max (52 w eek) 271.7Dyield (%) 2.9 3.6 4.1 4.8 Min (52 w eek) 195.1

Current price: PLN 253.2 Target price: PLN 263.5Pekao (Hold)

We expect the Commission for Bank Supervision (KNB) to give a green light for the division of BPH and its merger with Pekao during its meeting in October. The merger machine was put in motion in April 2006, when UniCredit reached an agreement with the State Treasury. Even with the merger preparations going full swing, Pekao is constantly improving its earnings performance and meeting market expectations. Clients have not been scared away by the media buzz, and we expect them to stay with Pekao even after the merger: Thanks largely to bank supervision’s sluggishness, the bank has had time to prepare for a seamless transition. Other perks for clients include a much wider branch network and free cash withdrawals from BPH ATMs. Pekao’s stock rose 3.6% since our last rating (September 4th), prompting a downgrade from Accumulate to HOLD. Sale of shares in Anica System Pekao’s subsidiary Pekao Fundusz Kapitałowy sold 1.5269 million shares of common stock to Anica System with a par value of PLN 0.2 each (PLN 305.38 thousand in total), representing 33.84% of share capital and 13.49% of votes, to Asseco Poland for a total price approximating PLN 22.6m. The book value of these shares was PLN 4.376m. They had been purchased as a long-term investment. The sale will make a small addition to Pekao’s consolidated 3Q’07 earnings (it was sealed on September 28th), namely, PLN 18.2m will be credited to pre-tax income, and PLN 14.76m to net income. The proceeds account for 2.7% of the bank’s 2Q’07 pre-tax income and net income, and 0.8% of the FY2008 net income .

160

200

240

280

320

2006-09-26 2007-01-18 2007-05-14 2007-09-03

Pekao WIG

BRE Bank Securities

3 October 2007 20

Monthly Report BRE Bank Securities

Analyst: Marta Jeżewska016 Last Recommendation: 2007-09-04

(PLN m) 2006 2007F change 2008F change 2009F change Basic data (PLN m)Net interest income 3 808.7 4 454.3 16.9% 5 117.5 14.9% 5 920.0 15.7% Number of shares (m) 1 000.0Interest margin 3.9% 4.2% 4.4% 4.5% MC (current price) 56 300.0Revenue f/banking oper. 6 038.9 7 025.5 16.3% 7 964.7 13.4% 9 031.2 13.4% Free float 43.1%Operating profit 2 705.8 3 580.8 32.3% 4 287.2 19.7% 5 156.1 20.3%Gross profit 2 167.0 2 701.5 24.7% 3 324.8 23.1% 3 880.1 16.7%Net prof it 2 149.1 2 617.2 21.8% 3 051.8 16.6% 3 671.1 20.3%

ROE 22.9% 24.0% 24.2% 25.3% Price change: 1 month 2.8%P/E 26.2 21.5 18.4 15.3 Price change: 6 month 15.4%P/BV 5.6 4.8 4.2 3.6 Price change: 12 month 51.1%D/PS 0.8 1.0 1.3 1.5 Max (52 w eek) 59.0Dyield (%) 1.4 1.7 2.3 2.7 Min (52 w eek) 35.8

PKO BP (Hold)Current price: PLN 56.3 Target price: PLN 55.5

30

35

40

45

50

55

60

65

2006-09-26 2007-01-18 2007-05-14 2007-09-03

PKO BP WIG

PKO BP’s second-quarter results were a testimonial to its sales strength. Net loans surged 26% y/y, as did assets under management of investment funds (increase in market share from 9.81% at March 2007 to 10.42% at June). These trends continued in 3Q, with PKO TFI recording assets of PLN 15.875bn and an 11.4% market share at the end of August. A booming market is driving sales and revenues. Our current financial projections for the bank are based on its revised long-term financial targets. We believe that the bank can keep net ROE at 25% and C/I ratio around 39%. We are reiterating a HOLD rating. PKO BP / PZU merger a tough nut According to Treasury Minister Wojciech Jasiński, a merger between PZU and PKO BP is a needed, but highly complex undertaking. We agree. Newspapers got to PKO BP / PZU merger plans According to Rzeczpospolita, a plan is in the works for PKO BP to take over PZU. The paper claims that there were two plans. One, later rejected, was to form a new company which would take over both PKO BP and PZU to form a holding company. The other plan, which was accepted according to the paper, is to transfer PZU to PKO BP in two stages. In the first stage, a portion of PZU’s shares will be transferred to PKO BP in exchange for the bank’s new shares. The State Treasury’s interests will increase from 51.5% to 66% max. The number of shares so transferred would depend on PZU’s valuation. PKO BP’s shareholders would have to approve the issue by an 80% majority. In the second stage, the State Treasury will transfer the outstanding interests in PZU in exchange for special bonds issued to PZU. PKO BP would not pay for all the shares, as a portion of the consideration would be offset against Eureko’s claims against the State Treasury (which might be as high as PLN 9bn according to the paper). The success of this plan depends on the State Treasury’s actual rights to dispose of PZU shares. The Treasury claims Eureko has no rights to these shares. A merger between PKO BP and PZU would have two major benefits: it would produce Poland’s largest financial institution comparable to major international players, and provide a huge capital infusion to the State Treasury. Another advantage would be that all risks arising from the Eureko dispute would be transferred from the State Treasury to PKO BP. We are skeptical. The scenario outlined by Rzeczpospolita would expose minority shareholders to considerable risk. When and how long the processes would start is unknown. Minority shareholders could agree to this marriage only if they are convinced that there is something for them to gain. In its early stages, it would certainly generate more complications and risks than benefits. What is more, we are on the verge of early parliamentary elections, and, since the State Treasury is PKO BP’s majority shareholder, if its members are replaced as a result of the election, the bank’s strategy could be changed completely. If the shareholder structure stays intact, the merger scenario could be developed further. PKO BP / PZU merger plans unlawful In their comments to the PKO BP / PZU merger plans, newspapers wrote that a two-stage takeover by PKO BP of the Treasury’s shares in PZU would be illegal. According to the KNF, these shares cannot be contributed in kind, but have to be paid for in cash. In similar cases in the past, the KNF did not allow stock-for-stock transactions when Getin Holding wanted to take over TU Europa. According to the State Treasury, the scenarios outlined by Rzeczpospolita was just one of many. Another problem is the plan’s incompliance with bank regulations, which say that banks can receive non-cash contributions only in the form of real estate or equipment. Furthermore, according to legal experts, the State Treasury could not be relieved of responsibility in the Eureko dispute because Eureko’s claims are subject to international

BRE Bank Securities

3 October 2007 21

Monthly Report BRE Bank Securities

agreements between Poland and the Netherlands. The legal details of the merger plan have not been worked out yet, and the information reported by Rzeczpospolita was just a blueprint which is subject to change. The fact is that the State Treasury is facing a challenge of integrating two large institutions, both in need of deep restructuring, while remaining deep in dispute with Eureko. At some point, PKO BP’s shareholders are going to take a vote to approve the merger. Anyway, a marriage between PKO BP and PZU can be seriously considered only after the fall election, and this provided that the current administration is reelected, or that whoever replaces is also in favor of the merger. PKO BP looking for advisor regarding partnership with PZU At the end of July, the State Treasury announced that it was going to work toward building a bank-and-insurance group resting on two pillars: PKO BP and PZU, but did not specify the action plan. Next week, the ministry is going to send out requests for advisory service offers to leading investment banks. In light of today’s revelations by Rzeczpospolita, the advisory could actually concern merger issues. Sales revolution PKO BP is implementing a scheme to improve sales, supported by an incentive plan currently being tested at a number of selected branches. The goal is to grow sales by 30%, expand cross-selling, realign the work organization, and improve the corporate image. The incentive scheme, based on individual performance among the sales force, will be tried in two regions in 4Q, and rolled out throughout all locations in 2008. PKO BP has undertaken a number of measures to improve sales. One of such measures are easy cash loans for non-clients, granted without proof of employment, aimed at increasing revenues through higher interest rates on high-risk loans. We like the bank’s ideas and the management’s efforts to keep the best people. In 1H, PKO BP revealed a new strategy plan for 2007–2012, and, assuming that the recent measures are a part of this plan, they must have been discounted by investors. PLN 3.267bn mortgage loan sales in just two months PKO BP sold PLN 3.267bn-worth of mortgage loans in July and August, marking a whopping 83% increase on the same period a year ago (PLN 1.788bn). 1H’07 sales came close to PLN 8bn (up 65% y/y), and 2Q’07 sales were PLN 4.4bn. The bank is consistently generating growth. If the pace recorded in July/August is sustained in September, the bank will have sold PLN 4.9bn loans (or even more). These are impressive, but expected figures. Sales in 2Q’07 amounted to PLN 4.4bn. PKO BP’s sales are also an indication of a general uptrend in mortgage lending experienced by banks across the board. PLN 1.05bn consumer loan sales in just two months Consumer loan sales in July and August chalked up a 25% increase on a year earlier (PLN 840m). 2Q’07 sales approximated PLN 1.6bn. PKO BP expects sales to grow further on a new offer targeted to the mass customer, especially low-income borrowers and seniors. PKO BP has put much effort in accelerating consumer lending. The new loan products are sure to drive sales, but not faster than market expectations. Our valuation model for the bank is based an a prediction of a 25% y/y increase in consumer loan sales in FY2007. Growth after 2Q stood at 17.9%, including a 7.6% y/y rise in mass lending, and an 84.4% surge in the private banking segment. We are confident that PKO BP will continue to grow its consumer loan business. Credit card sales PKO BP had issued 991.6 thousand credit cards at the end of August, compared to 971.7 thousand at the end of 2Q. The bank says that it will hit the 1 million mark in a matter of weeks by focusing on galvanizing client activity – the number of card transactions rose 30% y/y. At the end of 3Q’06, PKO BP had 737,000 cards in circulation. The number of issuances increased almost 25% from the end of September 2006 to the end of August 2007. The transaction volume increases in line with card issuances, but could generate stronger fee income. Bond offering PKO BP’s management board resolved to make an offering of ten-year bearer bonds callable five years from the issue date, nominated either in zlotys, or in euros. The purpose of this debt offering was not stated. The bonds will be available in Poland only. We can guess that this offering, as well as the recent subordinated loan, are aimed at financing of current operations, especially the lending business.

BRE Bank Securities

3 October 2007 22

Monthly Report BRE Bank Securities