Macro, Money and International Finance€¦ · According to the Bank for International Settlements...

36

Macro, Money and International Finance Munich, 30 June & 1 July 2017 The RMB Central Parity Formation Mechanism after August 2015: A Statistical Analysis Yin-Wong Cheung, Cho-Hoi Hui and Andrew Tsang

Transcript of Macro, Money and International Finance€¦ · According to the Bank for International Settlements...

Macro, Money and

International Finance Munich, 30 June & 1 July 2017

The RMB Central Parity Formation Mechanism

after August 2015: A Statistical Analysis Yin-Wong Cheung, Cho-Hoi Hui and Andrew Tsang

The RMB Central Parity Formation Mechanism after

August 2015: A Statistical Analysis

Yin-Wong Cheung*

City University of Hong Kong

Cho-Hoi Hui

Hong Kong Monetary Authority

Andrew Tsang

Hong Kong Institute for Monetary Research

March 2017

Abstract

We study the renminbi (RMB) central parity formation mechanism following the August 2015 reform.

Statistical models are formulated to assess the linkages between the central parity and the alternative

variants of the RMB exchange rate, market volatility and selected control variables. In a linear

regression framework, we identify the roles of the onshore and offshore RMB exchange rates and the

US dollar index, but not the RMB currency basket index. However, the marginal effect of the RMB

index is revealed via a multiplicative interaction model that incorporates a condition variable given by

the volatility of the offshore RMB market. The offshore RMB volatility exerts a dampening effect on the

links between the central parity and its determinants, reflecting that Chinese authorities do not hesitate

to adjust their policy actions under threat of high volatility.

Keywords: China’s Exchange Rate Policy, Currency Basket, Multiplicative Interaction Model, Onshore

and Offshore RMB Rates, Volatility

JEL classification: F31, F33

* Email addresses: Cheung: [email protected], Hui: [email protected] and Tsang: [email protected].

Acknowledgements: Cheung gratefully thanks The Hung Hing Ying and Leung Hau Ling Charitable Foundation for its support. The views expressed in this paper are those of the authors, and do not necessarily reflect those of the Hong Kong Monetary Authority, Hong Kong Institute for Monetary Research, its Council of Advisers, or the Board of Directors.

1

Hong Kong Institute for Monetary Research Working Paper No.06/2017

1. Introduction

China’s foreign exchange policy has been in the limelight since the turn of the 21st century. For

instance, in the early 2010s, China was accused of manipulating the value of its currency, the

renminbi (RMB), when China had recorded huge trade surpluses. Specifically, countries, including the

USA, complained that China enjoyed unfair advantages in the global market by keeping the RMB at

an artificially low level.1

The focus has shifted from RMB valuation to the implications of a globalised RMB when China has

stepped up efforts after the 2007-8 global financial crisis to promote the use of its currency overseas.2

Benefitting from China’s trade prowess, the RMB has ascended quite fast in the global financial

system. For instance, the RMB swiftly advanced from being the 20th most commonly used world

payments currency in January 2012 to fourth in August 2015 before it fell back to sixth in December

2016 (SWIFT, 2013, 2015, 2017).

According to the Bank for International Settlements triennial central bank surveys, the average RMB

daily forex turnover has registered a significant gain in the global foreign exchange market to reach

202 billion in 2016 from 15 billion in 2007 (Bank for International Settlements, 2007, 2016).

Leveraging on the fast growth of offshore RMB markets, the Chinese currency replaced the Mexican

peso and became the most traded developing market currency and the eighth most traded currency in

the global market in the 2016 survey.

As fear of ignoring China’s foreign exchange policy increases, market participants have paid

increased attention to the RMB exchange rate, and are anxious to embrace the coming of a

globalised RMB.3 A case in point is the rippling global effect triggered by China’s attempt to revamp its

daily central parity formation mechanism; a la daily fixing mechanism in August 2015. On August 11,

1 Some empirical studies on the debate of RMB misalignments are Cheung, Chinn, Fujii (2007), Cline (2015), Frankel (2006),

Funke and Rahn (2005), Fischera and Hossfeld (2014), Funke and Gronwald (2008), Korhonen and Ritola, (2011), and Schnatz (2011).

2 Some studies on RMB internationalisation are Chen and Cheung (2011), Chen and Peng (2010), Cheung, Ma and McCauley

(2011), Eichengreen, Barry (2013), Eichengreen and Kawai (2015), Frankel (2012), and Prasad (2016).

3 The growing effect of financial spillovers from China is noted, for example, by the International Monetary Fund (2016). Some

recent empirical studies include Colavecchio and Funke (2008), Fratzscher and Mehl (2014), Kawai and Pontines (2016), and Shu, He and Cheng (2015).

2

Hong Kong Institute for Monetary Research Working Paper No.06/2017

2015, China issued a brief statement on fine-tuning its foreign exchange policy by setting the daily

RMB central parity rate against the US dollar with references to the previous day’s closing rate,

market demand and supply, and valuations of other currencies (People’s Bank of China, 2015a).

The policy change, accompanied by a 1.9% depreciation against the US dollar, stirred up

considerable unrest in financial markets; especially emerging ones, around the world. The volatile

response exemplifies the global influence of the Chinese currency. The official daily fixing becomes

the barometer to infer authorities’ stance on exchange rates, and the implied views on the Chinese

economy. The market participants, in addition to routine official statements, pay attention to the official

central parity to infer policy intentions.

The August 2015 policy modification is not the first time China asserted its desire to migrate toward a

currency basket approach to manage the RMB exchange rate; an approach that is widely perceived

to be appropriate for weakening the tie with the US dollar, and for transiting to exchange rate flexibility.

In July 2005, when China loosened its grip on the RMB, it said the currency would be managed

against an unspecified basket of currencies taking market demand and supply into consideration

(People’s Bank of China, 2005). A similar statement was made after the global financial crisis in July

2010 (People’s Bank of China, 2010).

Despite these pre-2015 policy statements, Frankel (2009) and Sun (2010), for instance, argue that the

RMB is still managed against the US dollar, or US dollar has a very large weight in the unspecified

currency basket. Ma and McCauley (2011) claimed China adopted a crawling peg that allowed the

RMB to appreciate and fluctuate within a moving band. The observed RMB exchange rate movement

does not convince the market that the dollar peg arrangement is weakening.

In December 2015, a few months after the August 2015 market turmoil, China posted the CFETS

RMB currency basket; including both its component currencies and their weights in the basket, and

reiterated the relevance of referencing the RMB to a currency basket (Guest Commentator of CFETS,

2015). While the publication of the currency basket is meant to enhance transparency, the market

was rattled by the RMB weakness extended into early January 2016 and the observed weak

association between the RMB value against the currency basket and the fixing. The market

participants conceive the CFETS currency basket plays a limited role in guiding their RMB

expectations, and revives their concern that the new RMB fixing mechanism is a decoy for playing

3

Hong Kong Institute for Monetary Research Working Paper No.06/2017

currency wars. Since then, the authorities on several occasions, reiterated that the RMB central parity

formation mechanism was re-designed to enhance the role of market forces, improve the level of

transparency and maintain exchange rate stability, and dispelled the market view that the revamp was

a disguised competitive devaluation policy.

Against this backdrop, we investigate the RMB central parity formation mechanism following the

August 2015 reform. Specifically, drawing the clue from official announcements and market

developments, we formulate our empirical models to assess the linkages between the central parity

and the alternative variants of the RMB exchange rate, market volatility, and selected control variables.

Specifically, the different RMB exchange rates include the onshore and offshore RMB exchange rates,

the US dollar index, and the RMB currency basket index.

To anticipate our results, we find that, within a linear regression framework, the onshore and offshore

RMB exchange rates and the US dollar play a significant role in determining the daily RMB central

parity, while the RMB currency basket index effect can be hard to detect. Nevertheless, the role of the

RMB index is revealed via a multiplicative interaction model that incorporates a condition variable

given by the volatility of the offshore RMB market. Note that the Chinese authorities dislike volatility

and, as demonstrated in the past, do not hesitate to adjust their policy actions when the threat of

volatility is felt. Indeed, we find that the offshore RMB volatility exerts a dampening effect on the links

between the central parity and its determinants. The results are robust to alternative specifications

and the presence of control variables.

In the next section, we offer some background information on the current Chinese foreign exchange

policy. Section 3 presents the results of estimating the empirical central parity models that are used to

investigate the roles of different versions of the RMB exchange rate and volatility. Section 4 discusses

empirical findings from alternative specifications. Some concluding remarks are provided in Section 4.

4

Hong Kong Institute for Monetary Research Working Paper No.06/2017

2. Background

Building upon its astonishing accomplishment in the trade arena, China has stepped up its efforts in

liberalising financial markets and the RMB exchange rate in particular. In July 2005, China announced

the adoption of a managed and regulated floating exchange rate regime based on market demand

and supply, and with reference to a basket of currencies (People’s Bank of China, 2005). The policy

was interrupted by the 2008-9 global financial crisis, and was resumed in July 2010 (People’s Bank of

China, 2010).

Compared with a bilateral exchange rate, a currency basket index based on a weighted average of

multiple bilateral exchange rates represents a better overall measure of the value of a currency. In the

case of the RMB, the reference to a basket of currencies allows the currency to be more flexible

relative to the US dollar, which is a dominating global currency, and is a step toward RMB flexibility.

The official reference to a currency basket, however, does not sway the market’s focus on the bilateral

US dollar-RMB exchange rate. The de facto RMB movements reinforce the perception that the RMB

is heavily managed against the US dollar (Frankel, 2009; Sun, 2010).

As part of the financial liberalisation program, China has made progressive efforts to promote the use

of the RMB overseas. The nascent offshore RMB market was established in Hong Kong in 2010.

Subsequently, other offshore RMB centres sprang up in financial markets around the world. In these

offshore markets, the RMB is essentially traded like a convertible currency that is subject to global

market forces, and is dubbed CNH. Offshore RMB trading, among other functionalities, allows China

to gauge the international demand and supply of its currency in a less constrained setting (Cheung,

2015; He and McCauley, 2013; Maziad and Kang, 2012).

China’s efforts to globalise its currency were cumulated in 2015 to lobby the RMB to be included in

the International Monetary Fund’s (IMF) special drawing rights (SDR) basket.4 To enhance the odds

of acceptance to the basket, various financial market liberalising measures, including relaxing interest

rate controls and permitting full participation by foreign central banks and sovereign wealth funds in

4 SDR is a supplementary reserve asset created by the IMF under the Bretton Woods regime in 1969.

5

Hong Kong Institute for Monetary Research Working Paper No.06/2017

the domestic bond market, were instituted.5 The exchange rate policy was also refined to allow for an

increasing role of market forces. On August 11, 2015, the People’s Bank of China announced that the

RMB central parity against the US dollar will be set by referencing the previous day’s closing rate,

market demand and supply, and valuations of other currencies. The announcement, albeit brief,

induced volatile market responses in the midst of an accompanied 1.9% marked down of the central

parity rate.

China, in face of volatility, asserted its resolute intolerance to market volatility and instability, and

resorted to administrative measures and control policies to restore stability. China’s abrupt

interventions in financial markets, including the currency market in the summer of 2015 and the

subsequent months, remind the world that China still tightly controls its economy. China’s

determination to manage its economy according to its own terms has stirred concerns in the interna-

tional community. The inherent distrust of volatility appears to be at odds with the view that market

volatility and risk are likely consequences of pricing assets based on market forces.

The role of the currency basket approach in the new central parity formation mechanism was stressed

and emphasised in December when the CFETS RMB currency basket with its component currencies

and their weights was disclosed (Guest Commentator of CFETS, 2015).6 The disclosure in principle

enhances the transparency of the fixing mechanism. However, the market has to be convinced that

China’s intention is to adopt the currency basket management approach and not to use it to

camouflage its depreciation policy.

In response to the market’s bafflement, central bank officials on several occasions expounded China’s

foreign exchange policy (People’s Bank of China, 2016b; Wang, et al., 2016; Ma, 2016a). They

reiterated that the reference to demand and supply is in accordance with China’s on-going reform

policy of increasing the role of market forces in policy making, and the central parity is determined by

factors that include previous day’s closing and the variation of the currency basket. The new policy is

a controlled floating and not a pure flexible exchange rate arrangement. Controls and interventions

are in place to counter volatility caused by, say, speculation.

5 See, for example, International Monetary Fund (2015) for China’s RMB liberalisation efforts, People’s Bank of China (2015b)

for interest rate liberalisation update, and People’s Bank of China (2016a) for the official announcement of China’s inter-bank bond market.

6 The thirteen component currencies and their weights are: USD (26.4%), EUR (21.39%), JPY (14.68%), HKD (6.55%), GBP

(3.86%), AUD (6.27%), NZD (0.65%), SGD (3.82%), CHF (1.51), CAD (2.53%), MYR (4.67%), RUB (4.36%), and THB (3.33%).

6

Hong Kong Institute for Monetary Research Working Paper No.06/2017

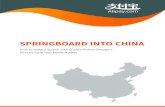

Figure 1 plots the CFETS RMB currency basket index (B), and three variants of the RMB exchange

rate against the US dollar; namely, the central parity rate (a la the daily fixing, P), CNY (the onshore

RMB rate, Y), and CNH (the offshore CNH rate, H). The sample period is from August 17, 2015, to

December 31, 2016.7 Visually, relative to the CFETS index, the three dollar-based rates display a

relative high level of comovement; with the period of April to October 2016 a possible exception.

Some descriptive statistics of these four rates, in log-difference forms to ensure these variables are

stationary, are presented in Table 1. Indeed, the change in fixing (lnP) has a correlation coefficient of

0.349 with the change in CNY (lnY) and of 0.516 with CNH (lnH). The correlation coefficient of lnP

and the change in CFETS RMB index (lnB), however, is0.046.8 Apparently, the observed variation

patterns do not buttress the importance of the RMB index in inferring the RMB central parity rate.

Further, the change in the central parity lnP displays a stronger degree of association with either

deviations from the onshore or offshore RMB rate (lnP - lnY or lnP - lnH) than with the deviations from

the CFETS RMB index (lnP - lnB). Apparently, the circumstantial evidence of weak association

between the central parity and the RMB index prompts market participants’ queries about the claimed

currency basket management policy framework. Statistical evidence on the central parity formation

mechanism is presented in the following sessions.

3. Is there a RMB index effect?

The official daily fixing is an instrument China used to manage the value of its currency.9 Before

August 2015, it is widely perceived that China sets the daily rate to fit its own policy and does not

necessarily take market forces into consideration. The August 2015 policy announcement targets the

mechanism of setting the RMB central parity against the US dollar. The Chinese central bank asserts

7 The RMB index value before December 2015 is computed based on the composition and weights of the announced currency

basket. Due to unusual turbulence, we excluded the first four business days under the new fixing mechanism.

8 lnP has a correlation coefficient of 0.562 with the US index compiled by the Intercontinental Exchange. For the period from

April 1 to December 31, 2016, the correlation coefficient between lnP and lnB is -0.1, which is still in magnitude less than

0.597, the one between the lnP and lnH.

9 The China Foreign Exchange Trading System, CFETS, is authorised by the People’s Bank of China to calculate and publish

the RMB central parity (à la the fixing); http://www.chinamoney.com.cn/fe/Channel/2781516.

7

Hong Kong Institute for Monetary Research Working Paper No.06/2017

that the new policy gives market forces a strengthened role in setting the RMB’s value, and is a step

toward a market-determined exchange rate. The policy shift, however, coincides with a switch from a

long-time RMB appreciation path to a depreciation one. As a result, market participants were

flummoxed. Despite the repeated emphasis on the relevance of the RMB value against a basket of

currencies and its stability, the market has its fixation with the bilateral US-RMB exchange rate, and

scrutinises official central parity rates for hints of shifts in the policy stance, or inconsistencies among

official views on the foreign exchange policy.

Despite the progress made in liberalising its currency, China maintains a tight grip on its exchange

rate and makes it clear that changes are introduced to increase flexibility and the role of market forces

to achieve controlled and managed convertibility but not necessarily free float. Against this backdrop,

we study the empirical characteristics of the RMB parity formation mechanism in the post-August

2015 period. Specifically, we assess the roles of a) the onshore and offshore markets, b) the US

dollar index and the CFEETS currency basket index, and c) market volatility.

3.1 The Basic Specification

Compared with the onshore rate, the offshore rate is subject to a lesser degree of invention and, thus,

reflects better market information.10

If these two rates play a role in determining the central parity

formation mechanism, what is their relative importance? To formally examine the effects of onshore

and offshore rates on the central parity, we consider the specification:

∆Pt = μ1+γ1(Pt-1–Yt-1)+γ2(Pt-1–Ht-1)+γ3∆Pt-1+γ4∆Yt-1+γ5∆Ht-1+t, (1)

where P, Y, and H are, respectively, the central parity rate, the onshore CNY rate and the offshore

CNH rate in logs. “∆” is the first-difference operator. Specification (1) is motivated by the fact that

these three RMB rates, even though determined differently, should be linked. This is because

onshore and offshore market rates embed information on demand and supply of the currency, and

arbitrage, even limited, is possible, as it is known that China’s capital controls are tight but not

10

Anecdotal evidence indicates that, before the second half of 2015, there was no invention in the CNH market. The information role of the offshore market and its links to the onshore rate are studied in, for example, Cheung and Rime (2014), Chung, Hui and Li (2012), Ding, Tse, and Williams (2014), Funke, Shu, Cheng and Eraslan (2015), and Leung and Fu (2014).

8

Hong Kong Institute for Monetary Research Working Paper No.06/2017

absolute.11

At the pre-test stage, the empirical links between these three rates are affirmed: each

series individually is a unit root process and they are cointegrated. Even though the cointegrating

coefficient estimates are not exactly unity, (P – Y) and (P – H); the two series of deviations from the

central parity are stationary I(0) processes and, thus, can be viewed as restricted cointegrating

relationships of (P, Y) and (P, H), respectively. These pre-test results, though not reported for brevity,

are available from the authors.

The results of estimating (1) and its variants are presented in Table 2. The one-lag specification is

supported by the absence of significant serial correlation in the estimated residuals.12

The individual

effects of the CNY and CNH are given under, respectively, columns 1a and 1b. If China uses only the

CNY rate to set the RMB central parity, then the results under column 1a show that the central parity

is affected by itself in a regressive manner, as indicated by the negative coefficient of the lagged

dependent variable, and by the onshore rate via the error correction mechanism given by the

deviation from the central parity term (P – Y) and the short- term effect given by the first difference

term ∆Y. The first difference term can be interpreted as a variable that captures short-term demand

and supply conditions in the onshore market.

Similar results are obtained under column 1b when only the CNH is considered. That is, individually,

either CNY or CNH offers similar information about the formation mechanism of the RMB parity rate.

An astute reader may point out the CNH specification offers a slightly larger adjusted R2 estimate

(33.1 %) than the CNY one (31.9%).

The last column in the Table reports the combined effects of the onshore and offshore rates. The

combined model, even with some insignificant coefficient estimates, yields a better explanatory power,

as given by the adjusted R2 estimate than its components. It is of interest to note that the onshore and

offshore rates contribute differently to the central parity formation mechanism: CNY affects via its

deviations from the central parity and CNH via its changes. One way to interpret these results is that

the central parity is set to reduce its gap from the onshore rate and to respond to market forces as

conveyed by the offshore rate. Recall that China says the central parity is based on, among other

11

Studies on China’s capital controls, see, for example, Chang, Liu and Spiegel (2015), Chen, and Qian (2016), Cheung, Steinkamp, and Westermann (2016), Gunter (1996), and Ma and McCauley (2008).

12 Further, all the one-lag specification reported in the subsequent analyses passed the residual tests.

9

Hong Kong Institute for Monetary Research Working Paper No.06/2017

things, the previous day’s CNY closing, and the offshore market is subject to a lesser degree of

distortions induced by controls and interventions.13

3.2 The Dollar, the Currency Basket and Volatility

The roles of the US dollar and the CFETS RMB currency basket index are investigated using

∆Pt = μ1+γ1(Pt-1–Yt-1)+γ2(Pt-1–Ht-1)+γ3∆Pt-1+γ4∆Yt-1+γ5∆Ht-1+γ6∆Ut-1+t, (2)

∆Pt = μ1+γ1(Pt-1–Yt-1)+γ2(Pt-1–Ht-1)+γ3∆Pt-1+γ4∆Yt-1+γ5∆Ht-1+ γ7∆Bt-1+t, and (3)

∆Pt = μ1+γ1(Pt-1–Yt-1)+γ2(Pt-1–Ht-1)+γ3∆Pt-1+γ4∆Yt-1+γ5∆Ht-1+γ6∆Ut-1+γ7∆Bt-1+t. (4)

The US dollar index (U) compiled by the Intercontinental Exchange is used to capture the US dollar

effect on the central parity.14

Both the US dollar index and the RMB currency basket index (B) in logs

are in first difference to achieve stationarity. The estimation results are given under columns “2” to “4”

in Table 3. The inclusion of the US dollar index noticeably improves the model’s performance. It is

statistically significant with the expected positive sign and increases the adjusted R2 estimate by

about one-third to 56.7% from 42.5%.15

The RMB index, though, has the expected negative sign, is

statistically insignificant and offers no marginal explanatory power.16

The strong presence of the US dollar effect is not surprising for a few reasons. First, despite China

making good progress in globalising the RMB, the US dollar remains the prominent international

currency that accounts for a lion’s share of global foreign exchange transactions. According to the

latest survey, as much as 95% of the RMB trading around the world was against the US dollar (Bank

13

There is a need to take into consideration of the CNH because of the remaining capital controls in the onshore market and the expanding offshore CNH market (Overholt, Ma and Law, 2016).

14 The index is a weighted average of the US dollar exchange rates against other major currencies supplied by around 500

banks. The variation of this index is similar to other trade-weighted index, such as the Fed’s dollar index and the Wall Street Journal USD index.

15 Given the low correlation (0.074) between the USD index and the CFETS RMB currency basket index, multicollinearity is not

a concern. In addition, since 2005, there is a marked diversion between the USD index and the BIS RMB currency basket index (Ma and McCauley, 2011). Therefore, the USD index and the CFETS RMB currency basket index can have different impacts on the RMB fixing.

16 If assuming only the CNY rate being used (as stated in People’s Bank of China, 2016b) and taking into account for the

movement of the RMB index to set the RMB central parity; that is, adding the RMB index to Model 1a in Table 1, the RMB index still offers no marginal explanatory power.

10

Hong Kong Institute for Monetary Research Working Paper No.06/2017

for International Settlements, 2016). Further, the US dollar is the key vehicle for international

transactions, and it accounts for close to 90% of the aggregate global foreign exchange trading

volume. Thus, it is hard to conceal the role of the US dollar in valuing the RMB. Second, China is

saddled with a history of managing the value of its currency against the US dollar. It is not

inconceivable that market participants in both domestic and foreign markets have to take time to

change their habits of making references to the US-RMB value.

The absence of evidence of the CFETS RMB index effect is unexpected, given the authorities’

repeated messages to the market of the importance of focusing on the RMB value against the

currency basket, rather than zooming in on only the bilateral US-RMB rate. It is, however, not easy to

establish the official position given the apparent lack of comovement between the CFETS RMB index

and the central parity noted in the previous session and the absence of statistical evidence in Table 3.

Will the RMB index effect be hidden behind market volatility/uncertainty? The results of estimating

∆Pt = μ1+γ1(Pt-1–Yt-1)+γ2(Pt-1–Ht-1)+γ3∆Pt-1+γ4∆Yt-1+γ5∆Ht-1+γ6∆Ut-1+γ7∆Bt-1+γ8Zt+t, (5)

are presented under the column labelled “5” in Table 3. The volatility variable Zt is given by the CNH

conditional volatility estimated from a GARCH specification and is based on information available at

time t-1.17

The choice of CNH volatility is motivated by the information role of the offshore market that

reflects market views on RMB valuation outside China. Other volatility proxies are discussed in the

subsequent analyses. The Zt yields a negative sign; a high level of CNH volatility/uncertainty

strengthens the daily RMB fixing against the USD, that helps alleviate negative market sentiment, but

the effect is not statistically significant. The inclusion of the variable does not have any material

impacts on the coefficient estimates of other variables and the adjusted R2 estimate of the model.

Both the Akaike and Schwarz information criteria (AIC and SIC) indicate that, in Tables 1 and 2, the

specification (2) explains the variability of the RMB central parity, even though the inclusion of the

CFETS RMB index (specification (4)) increases the adjusted R2 estimate by a mere 0.1% over (2).

The result attests to the relevance of the onshore and offshore RMB exchange rates and the US

17

Technically speaking, the GARCH volatility estimate is not pre-determined as it is estimated using information from the entire sample. Thus, we examined the predictive and not the forecastability of the model. In the pilot analysis, we found that the estimate used here and the GARCH volatility estimate obtained using rolling samples, with an initial sample from August 17 to December 14, 2015, have a correlation of 0.92.

11

Hong Kong Institute for Monetary Research Working Paper No.06/2017

dollar for characterising the central parity. The weak and insignificant effect of the RMB index is

qualitatively similar to the one reported in Cheung, Hui and Tsang (2016).

3.3 The Interaction Effect

Since 2005, the People’s Bank of China has mentioned the reference to a currency basket in its

foreign exchange policy statements in fits and starts. The revamp of the central parity formation

mechanism in August 2015 represents the latest attempt to shift the market’s focus on the value of

the RMB against the US dollar to one against a currency basket, which is a logical step towards

flexibility. Conceivably, the migration to a currency basket approach has to battle a stiff headwind

given the recent history of a de facto peg to the US dollar. The August 2015 policy admittedly did not

have a good start; it triggered turmoil in the global market and created market skepticism. The

repeated official explanations and disclosures, nevertheless, tend to lend support to the assertion of

pursuing a transparency foreign exchange policy based on a currency basket.

The transition to a free float for a country with China’s economic history and size is unprecedented. It

is well known that the Chinese authorities distrust market volatility. When the perceived volatility and

risk are heightened, the authorities do not hesitate to resort to controls and, if necessary, even

retribution. Thus, the adage “two steps forward, one step back”, or “one step back, two steps forward”,

is commonly used to describe China’s reform process. In reforming foreign exchange policy, the

People’s Bank of China has taken “tactical” adjustments and retreats from time to time in the face of

unfavorable market disruptions. In view of this, and given the unusual market uncertainties faced by

China and the global economy, we stipulate that the authorities will adjust the operation of the central

parity formation mechanism according to market conditions. Specifically, we anticipate that the role of

market forces will be weakened when market volatility is high. The volatility-dependence behaviour is

not likely to be captured by regression (5) when the volatility enters in a linear manner. In the following,

we use a multiplicative interaction model modified from (5) to capture volatility-dependence behaviour.

The interaction model that uses the CNH conditional volatility as the conditioning variable is given by

∆Pt = μ1+γ1(Pt-1–Yt-1)+γ2(Pt-1–Ht-1)+γ3∆Pt-1+γ4∆Yt-1+γ5∆Ht-1+γ6∆Ut-1+γ7∆Bt-1+γ8Zt+γ11Zt*(Pt-1–Yt-1)

+γ21Zt*(Pt-1–Ht-1)+γ31Zt*∆Pt-1+γ41Zt*∆Yt-1+γ51Zt*∆Ht-1+γ61Zt*∆Ut-1+γ71Zt*∆Bt-1+t (6)

12

Hong Kong Institute for Monetary Research Working Paper No.06/2017

The specification offers a simple setup to study, conditional on volatility, the effect of a determining

factor on the central parity. The results of estimating several variants of (6) are reported in Table 4.

Before looking at some specific findings, we make a few observations. First, each specification with

interaction terms in Table 4, compared with its corresponding one in Table 2 and Table 3, has a larger

adjusted R2 estimate and better AIC and SIC values. That is, models with interaction terms offer a

good fit. Second, the coefficient estimates of the interaction terms have signs that are opposite to the

corresponding ones without the volatility condition variable. The signs of the latter group of variables

are the same as those presented in previous tables. That is, the pricing mechanism of these variables

weakens as volatility increases; a result that is in accordance with our previous mention of China’s

response to heightened volatility. Third, by dropping the two insignificant deviations from the central

parity interaction terms, we obtained the parsimonious specification

∆Pt = μ1+γ1(Pt-1–Yt-1)+γ2(Pt-1–Ht-1)+γ3∆Pt-1+γ4∆Yt-1+γ5∆Ht-1+γ6∆Ut-1+γ7∆Bt-1

+γ8Zt+γ31Zt*∆Pt-1+γ41Zt*∆Yt-1+γ51Zt*∆Ht-1+γ61Zt*∆Ut-1+γ71Zt*∆Bt-1+t, (7)

which is presented under column 5. (7) has the highest adjusted R2 estimate, and best AIC and SIC

values in Table 4.18

Note that all the variables under column 5, including the volatility variable Zt are

statistically significant with their expected signs.

One finding that stands out from Table 4 is the significance of the CFETS RMB currency basket index.

Once the volatility condition is multiplicatively factored in, a negative γ7 suggests that a stronger RMB

index (positive ∆B) is associated with a stronger RMB fixing (negative ∆P). The link between the RMB

index and the bilateral central parity weakens as volatility increases.

The marginal effect of the RMB index ∆B on the central parity ∆P; conditional on Z and its standard

error, are given by

∆Pt/ ∆Bt-1|Zt = Mt|Zt = γ7 + γ71 Zt, (8)

and

18

Dropping Z*(P–Y) and Z*(P–H), rather than (P–Y) and (P–H) results a better fit.

13

Hong Kong Institute for Monetary Research Working Paper No.06/2017

Mt|Zt, se = [var( 7γ̂ ) + 2

tZ var( 71γ̂ ) + 2Ztcov( 7γ̂ , 71γ̂ )]1/2

. (9)

Expressions (8) and (9) show that the RMB index effect and its significance cannot be read directly

from the two coefficient estimates γ7 and γ71; instead, they vary with the CNH volatility, and their

variances and covariance. To gauge a quantitative sense of the effect, we use the estimation results

reported under column 5 of Table 4 to generate Figure 2. The estimated marginal effect (the solid red

line) changes from negative to positive and its two-standard-error (broken green and blue lines)

confidence band widens as Zt increases. The effect changes in sign when the Zt crosses the value of

0.00281. The RMB index variable displays a significant negative marginal effect on the central parity

for 76.5% of the observations in the sample.19

For comparison purposes, we plot the marginal effect of the US dollar index ∆U on the central parity

∆P; conditional on Z in Figure 3. As volatility variable Zt increases beyond 0.00320, the US dollar

index effect turns negative from positive. Apparently, the confidence band in this figure is narrower

than the one in Figure 2. In the given sample period, the estimates implying a negative marginal effect

are statistically insignificant; only those implying a positive effect are statistically significant. The

significant marginal effect estimates constitute 91.4% of the sample observations.

The marginal effects of other determining factors can be assessed in a similar fashion. For brevity, we

included the graphs of marginal effects of the onshore and offshore RMB rates (∆Y and ∆H) in the

Appendix. The profiles of these two marginal-effect graphs are similar to the one depicted in the US

dollar index Figure 3. The estimated marginal effects of these two RMB rates are usually significant

with the expected sign; the onshore exchange rate and the offshore rate exhibit a significantly positive

impact on the central parity for, respectively, 91.1% and 99.1% of the sample observations.

Among these four RMB exchange rates, only the CFETS RMB index has a proportion of observations

that display significant marginal effects discernibly less than 90%. This may be a reason that the RMB

index effect is hard to detect when the multiplicative volatility condition is not explicitly accounted for.

In sum, the multiplicative interaction model reveals evidence that, within the broadly defined setting,

the implementation of the central parity formation mechanism varies according to market conditions.

19

There are three observations in the sample that are associated with a positive RMB index effect, a result that is likely to be a statistical artifact from estimation.

14

Hong Kong Institute for Monetary Research Working Paper No.06/2017

Specifically, the central parity is set based on information about its previous value, the previous CNY

closing rate, the value against the currency basket, the overseas demand and supply conditions

captured by the CNH and the US dollar value.

While the roles of the onshore CNY, the offshore CNH, and the US dollar index are easy to identify,

the role of the RMB index is illusive. Our analysis, nevertheless, shows that, once market volatility is

allowed for, we can unveil the link between the RMB index and the central parity. Indeed, our CNH

volatility measure tends to weaken the effects of the determining factors on the central parity; a

finding that is in line with the perception that, when volatility and risk are high and economic

conditions get tough, the Chinese authorities will strengthen administrative measures and, temporarily,

scale back the role of market forces (Zhou, 2016). The central bank considers the value against the

currency basket, but does not peg to the currency basket (Ma, 2016b).

4. Additional Analyses

4.1 Macro and Financial Variables

The parsimonious specification (7) (column 5, Table 4) explains over 60% of the variation of changes

in the daily central parity rate. The explanatory power is mainly driven by information on the different

RMB rates. Do other economic variables help explaining the central parity? The question is

addressed using the following regression equation:

∆Pt = μ1+γ1(Pt-1–Yt-1)+γ2(Pt-1–Ht-1)+γ3∆Pt-1+γ4∆Yt-1+γ5∆Ht-1+γ6∆Ut-1+γ7∆Bt-1

+γ8Zt+γ9Wt-1+γ31Zt*∆Pt-1+γ41Zt*∆Yt-1+γ51Zt*∆Ht-1+γ61Zt*∆Ut-1+γ71Zt*∆Bt-1+γ91Zt*Wt-1+t. (10)

Essentially, (10) is the specification (7) augmented by W that contains economic variables and its

interaction term Z*W. In this subsection, we discuss the results when a) FP; the difference between

offshore and onshore RMB one-month forward points in deliverable forwards, b) lnVIX; the change

in the well-known fear index, c) lnVXY; the JP Morgan emerging market currency volatility index, d)

FRD; a one-zero dummy variable to capture the possible effect of a drop in China’s foreign exchange

15

Hong Kong Institute for Monetary Research Working Paper No.06/2017

reserves on the date of announcement, and e) FRI; a one-zero dummy variable for an increase in

China’s foreign exchange reserves on the date of announcement are individually added to the

regression exercise.20

The FP variable is included to gauge the authorities’ response to the different offshore and onshore

market views on the future value of the RMB.21

The two volatility indexes are commonly used to

represent the global financial cycle that deems to be associated with the so-called risk-on and risk-off

phenomenon and affect movements of (emerging market) currencies (Cairns, Ho, and McCauley,

2007; Cheung and Rime, 2014; Fatum and Yamamoto, 2016; and Rey, 2013). The dummy variables

of foreign exchange reserves are used to assess if the parity rate responds to changes in China’s

holding of reserves, which is quite commonly mentioned in the media as capital outflow from China

has become apparent since 2015.

The results of estimating (10) are presented in Table 5. The effects of these macro and financial

variables appear weak. Only the offshore and onshore RMB forward differential variable, FP, is

statistically significant (column 1). The resulting specification, however, yields a smaller adjusted R2

estimate and worse AIC and SIC values than the model without the two FP-related variables. The

VIX and VXY-based variables are insignificant, but their presence improves the adjusted R2 estimate.

The two dummy variables of foreign exchange reserves are insignificant, either individually or jointly.

Given these results, we deem the effects of these macro and financial variables are weak, and the

parsimonious specification (7) that incorporated volatility-dependence behaviour offers a reasonable

characterisation of the central parity formation mechanism.

4.2 Asymmetric behaviour

The market turmoil triggered by the introduction of the central parity formation mechanism in August

2015 and the subsequent depreciation trend smacked of China’s inability to effectively communicate

20

We also experimented with variables that capture changes and volatility of stock prices and fund flows through Shanghai-Hong Kong Stock Connect, and found these variables have no significant effect. These results are hence not discussed for brevity.

21 A positive FP suggests the offshore RMB is expected to be weaker than the onshore one in the future. Also, according to

covered interest parity, the forward point differential can be considered as a proxy of interest rate differential.

16

Hong Kong Institute for Monetary Research Working Paper No.06/2017

with the market. This confusion leads to different interpretations of the true motivation behind the

policy change. One common view in the media is that the new mechanism with a reference to

currency basket is the effort of devaluing the currency to boost the stalled economy. The central parity

is perceived to be set with the depreciation bias and responds asymmetrically to the dollar (or the

RMB index) movement. To shed insight on this claim, we re-estimate specification (7) by allowing the

coefficient estimates to assume different values when the US dollar appreciates. The results are

reported in Table 6. The Table also presents coefficient estimates that allow for asymmetric

responses to the direction of change of the RMB index.

The results indicate that the appreciation of the US dollar alters the effects of five of the thirteen

variables; namely lnP-lnH, lnB, lnU, Z*lnB and Z*lnU on the central parity. When these five

variables interact with a US dollar appreciation dummy variable, the interaction terms have statistically

significant coefficient estimates that have a sign opposite to their counterparts without the US dollar

interaction variable (Column 1, Table 6). That is, when the US dollar appreciates, the impacts (in term

of magnitude) of these variables on the central parity weakens. For instance, the response of the

central parity to the RMB index is likely to be stronger when the US dollar depreciates than

appreciates. The finding lends support to the view that the dollar movement has implication for the

operation of the central parity formation mechanism. While both the adjusted R2 and AIC estimates

support this model specification, the SIC estimate favours the model (7) that accounts for the

implications of the appreciation and depreciation of the US dollar.

The results presented under Column 2 of Table 6 indicate that, with the exception of lnP-lnH, the

parameter estimates of the model are not significantly influenced by the direction of change of the

RMB index. Both the AIC and SIC estimates favour the model (7) over the specification that

differentiates the parameter values across the two states of RMB index depreciation and appreciation.

That is, the central parity formation mechanism is mostly invariant to the depreciation and

appreciation of the CFETS RMB index.

We also investigated whether an increase in market uncertainty, as represented by the condition of

lnVIX > 0 or lnVXY>0 alters the model estimates. The results, which are given in the Appendix for

brevity, suggest these two conditions do not have a statistically significant implication for parameter

17

Hong Kong Institute for Monetary Research Working Paper No.06/2017

estimates. That is, the central parity formation mechanism adjusts to the CNH volatility, but not to the

risk measures represented by VIX and VXY.

4.3 Others

We examined a few other specifications. These regression results are discussed here but not

reported for brevity; they are available upon request.

For instance, we re-did the exercise with a shorter sample period from December 14, 2015, to

December 31, 2016, in which the CFETS RMB currency basket is public information. The findings,

especially pertaining to the US dollar index, the CFETS RMB index and the CNH volatility are

qualitatively the same as those reported above.

The CFETS currency basket assigns the largest weight of 26.4% to the US dollar. When we modified

the currency basket by dropping the US dollar from the list and re-did the exercise, we found

qualitatively similar results.

The cases of which the CFETS RMB index was replaced with either the RMB index based on the

Bank for International Settlements or the IMF SDR weights were also considered.22

The specifications

with these alternative RMB indexes perform less well than those with the CFETS RMB currency

basket index. That is, in terms of explaining the observed central parity, the CFETS index does a

better job.

5. Concluding Remarks

We study the empirical determinants of the RMB central parity formation mechanism following the

August 2015 reform. Based on official announcements and market developments, we examine the

responses of the central parity to its own past values, the onshore and offshore RMB exchange rates,

the US dollar index, and the CFETS RMB currency basket index. In a linear regression framework, we

22

These two alternative RMB indexes are included in the December 2015 posting for comparison purposes (http://www.pbc.gov.cn/english/130721/2988680/index.html).

18

Hong Kong Institute for Monetary Research Working Paper No.06/2017

identify the roles of the three bilateral exchange rates; namely the onshore and offshore RMB

exchange rates, and the US dollar index, but not the CFETS RMB currency basket index. A

combination of these three bilateral rates and the past central parity can explain 56.7% of the

variation of changes in the central parity. Despite the relatively high explanatory power,23

the puzzle is

the absence of the RMB index effect.

The puzzle can be resolved. The effect of the CFETS RMB currency basket index can be unveiled

using a multiplicative interaction model that incorporates the volatility of the offshore RMB exchange

rate. Our empirical results show that, after controlling for multiplicative CNH volatility conditions, the

CFETS RMB index displays a significant effect in 76.5% of the observations in our sample. Further,

the CNH volatility dampens the marginal effect of the CFETS RMB index, and this may be the cause

of the observed disconnect between the RMB index and the central parity. The CNH volatility also

attenuates the links between the central parity and the other determining factors. The results are in

accordance with the anecdotal evidence that China does not hesitate to strengthen control and

administrative measures in face of unwanted volatility.

Our empirical results reconcile the market’s skeptical view and the repeated official messages about

the reference to a currency basket. Despite the CFETS RMB index effect appears illusive; it can be

shown that, when the volatility interaction mechanism is accounted for, the RMB central parity

depends on factors including the currency basket as prescribed in official announcements and

communications. These factors explain over 60% of the variation in the daily central parity.

By the time we updated the sample period to the end of 2016, China expanded the number of

constituent currencies of the CFETS currency basket to 24 from 13 in 2017 (China Foreign Exchange

Trade System, 2016).24

By broadening the coverage, China reduces the US dollar weight to 22.4% in

the new currency basket from 26.4% in the original basket.25

The coverage expansion is in line with

23

Before August 2015, Cheung, Hui and Tsang (2016) show that a similar model with the US dollar index yields an adjusted R2

estimate of 34.3% and without the US dollar index 4.2%, which is comparable to the one from a typical daily exchange rate regression.

24 The 11 currencies added to the currency basket are: South African rand, Korean won, the United Arab Emirates dirham,

Saudi riyal, Hungarian forint, Polish zloty, Danish krone, Swedish krona, Norwegian krone, Turkish lira, and Mexican peso (China Foreign Exchange Trade System, 2016). It is stated that CFETS will annually assess its currency basket and, the assessment frequency may be more frequent.

25 The combined weight of the US dollar and currencies pegged to it (e.g. Hong Kong dollar, the United Arab Emirates dirham,

and the Saudi riyal) downs to 30.5% from 33%.

19

Hong Kong Institute for Monetary Research Working Paper No.06/2017

the strategy of diluting the US dollar role in setting the central parity, and re-directing the market focus

away from the bilateral US-RMB foreign exchange rate.

The jury is still out on the short-term effectiveness of the change. By bringing in other currencies, the

CFETS currency basket offers a good platform to soften the RMB’s link to the US dollar. Conceivably,

if the CFETS RMB index is tradeable, it will promote its acceptability among market participants.

Given China’s history of a de facto peg to the US dollar, the prominent global role of the US dollar,

and over 90% of RMB foreign exchange transactions being against the US dollar, it is not

unreasonable to anticipate that patience will be required to transit and migrate to a truly flexible RMB

regime. The transition process itself may not be linear. The empirical evidence presented above

attests to this point.

Our empirical evidence based on observations up to the end of 2016 documents the role of the US

dollar and, at the same time, lends support to August 2015 proclamation of the currency basket policy.

China’s foreign exchange rate policy, nevertheless, is evolving over time. It is warranted to examine

the central parity formation mechanism when sufficient new information and data are available.

20

Hong Kong Institute for Monetary Research Working Paper No.06/2017

References

Bank for International Settlements, 2007. Triennial Central Bank Survey of Foreign Exchange and

Derivatives Market Activity in 2007, Bank for International Settlements: Basel.

Bank for International Settlements, 2016. Triennial Central Bank Survey of Foreign Exchange and

Derivatives Market Activity in 2016, Bank for International Settlements: Basel.

Cairns, John, Corrinne Ho and Robert N. McCauley, 2007. Exchange rates and global volatility:

Implications for Asia‐Pacific currencies, BIS Quarterly Review (March), 41–42.

Chang, Chun, Zheng Liu and Mark M. Spiegel, 2015. Capital Controls and Optimal Chinese Monetary

Policy, Journal of Monetary Economics 74, 1–15.

Chen, Hongyi and Wensheng Peng, 2010. The Potential of the renminbi as an International Currency,

in Currency Internationalization: Global Experiences and Implications for the Renminbi, edited

by Wensheng Peng and Chang Shu, Chapter 5, 115–138, Palgrave Macmillan: UK.

Chen, Jinzhao and Xingwang Qian, 2016. Measuring ongoing changes in China’s capital controls: A

de jure and a hybrid index data set, China Economic Review 38, 167–182.

Chen, Xiaoli and Yin-Wong Cheung, 2011. Renminbi Going Global, China & World Economy 19 (Mar-

Apr), 1–18.

Cheung, Yin-Wong, 2015. The Role of Offshore Financial Centers in the Process of Renminbi

Internationalization, in Renminbi Internationalization: Achievements, Prospects, and

Challenges, edited by Barry Eichengreen and Masahiro Kawai, Chapter 7, 207–235,

Brookings Institution Press and Asian Development Bank.

Cheung, Yin-Wong, Menzie D. Chinn and Eiji Fujii, 2007. The Overvaluation of Renminbi

Undervaluation, Journal of International Money and Finance 26, 762–785.

Cheung, Yin-Wong, Cho-Hoi Hui and Andrew Tsang, 2016. The Renminbi Central Parity: An

Empirical Investigation, HKIMR Working Paper, No.10/2016.

Cheung, Yin-Wong, Guonan Ma and Robert N. McCauley, 2011. Renminbising China’s foreign assets,

Pacific Economic Review 16 (Feb), 1–17.

Cheung, Yin-Wong and Dagfinn Rime, 2014. The Offshore Renminbi Exchange Rate: Microstructure

and Links to the Onshore Market, Journal of International Money and Finance 49, 170–189.

Cheung, Yin-Wong, Sven Steinkamp, and Frank Westermann, 2016. China’s Capital Flight: Pre- and

Post-Crisis Experiences, Journal of International Money & Finance 66 (September), 88–112.

China Foreign Exchange Trade System, 2016. Public Announcement of China Foreign Exchange

Trade System on Adjusting Rules for Currency Baskets of CFETS RMB Indices,

http://www.chinamoney.com.cn/english/svcnrl/20161229/2049.html.

Colavecchio, Roberta and Michael Funke, 2008. Volatility Transmissions between Renminbi and Asia-

Pacific On-shore and Off-shore U.S. Dollar Futures, China Economic Review 19, 635–648.

Chung, Tsz-Kin, Cho-Hoi Hui and Ka-Fai Li, 2012. Determinants and Dynamics of Price Disparity in

Onshore and Offshore Renminbi Forward Exchange Rate Markets, Hong Kong Institute for

Monetary Research Working Papers, No.24 / 2012.

21

Hong Kong Institute for Monetary Research Working Paper No.06/2017

Cline, William R., 2015. Estimates of Fundamental Equilibrium Exchange Rates, May 2015, Peterson

Institute for International Economics, Policy Brief, PB 15 – 8.

Ding, David, Yiuman Tse, and Michael Williams, 2014. The Price Discovery Puzzle in Offshore Yuan

Trading: Different Contributions for Different Contracts, The Journal of Futures Markets, 34(2),

103–123.

Eichengreen, Barry, 2013. Renminbi Internationalization: Tempest in a Teapot? Asian Development

Review 30, 148–164.

Eichengreen, Barry and Masahiro Kawai, eds, 2015. Renminbi Internationalization: Achievements,

Prospects, and Challenges, Brookings Institution Press for ADBI.

Fatum, Rasmus and Yohei Yamamoto, 2016. Intra-Safe Haven Currency Behaviour during the Global

Financial Crisis, Journal of International Money & Finance 66, 49–64.

Frankel, Jeffery A., 2006. On the Yuan: The Choice between Adjustment under a Fixed Exchange

Rate and Adjustment under a Flexible Rate, CESifo Economic Studies 52 (2), 246–75.

Frankel, Jeffrey A., 2009. New Estimation of China's Exchange Rate Regime, Pacific Economic

Review 14(3), 346–360.

Frankel, Jeffrey A., 2012. Internationalization of the RMB and Historical Precedents, Journal of

Economic Integration 27, 329–65.

Fratzscher, Marcel and Arnaud Mehl, 2014. China’s Dominance Hypothesis and the Emergence of a

Tri‐polar Global Currency System, The Economic Journal 124(581), 1343–1370.

Fischera, Christoph and Oliver Hossfeld, 2014. A consistent set of multilateral productivity approach-

based indicators of price competitiveness – Results for Pacific Rim economies, Journal of

International Money and Finance 49A, 152–169.

Funke, Michael and Marc Gronwald, 2008. The Undisclosed Renminbi Basket: Are the Markets

Telling Us Something about Where the Renminbi–US Dollar Exchange Rate is Going? The

World Economy 31, 1581–1598.

Funke, Michael and Jörg Rahn, 2005. Just how undervalued is the Chinese renminbi? World

Economy 28, 465–89.

Funke, Michael, Chang Shu, Xiaoqiang Cheng and Sercan Eraslan, 2015. Assessing the CNH-CNY

pricing differential: Role of fundamentals, contagion and policy, Journal of International Money

and Finance 59, 245–262.

Guest Commentator of CFETS, 2015, http://www.chinamoney.com.cn/fe/Info/15850969, and

http://www.pbc.gov.cn/goutongjiaoliu/113456/113469/2988677/index.html.

Gunter, Frank R, 1996. Capital flight from the People’s Republic of China: 1984–1994, China

Economic Review 7, 77– 96.

He, Dong, and Robert N. McCauley, 2013. “Offshore Markets for the Domestic Currency: Monetary

and Financial Stability Issues”, in The Evolving Role of China in the Global Economy, edited

by Yin-Wong Cheung and Jakob de Haan, 301–37. MIT Press.

International Monetary Fund, 2016. Global Financial Stability Report, April 2016, International

Monetary Fund: Washington, D.C.

22

Hong Kong Institute for Monetary Research Working Paper No.06/2017

International Monetary Fund, 2015. Press Release: IMF Executive Board Completes the 2015 Review

of SDR Valuation, http://www.imf.org/en/news/articles/2015/09/14/01/49/pr15543.

Kawai, Masahiro and Victor Pontines, 2016. Is there really a renminbi bloc in Asia?: A modified

Frankel–Wei approach, Journal of International Money and Finance 62, 72–97.

Korhonen, Iikka and Maria Ritola, 2011. Renminbi Misaligned — Results from Meta-regressions, in

Asia and China in the Global Economy, edited by Yin-Wong Cheung and Guonan Ma,

Chapter 4, 97–122, World Scientific Publishing Company.

Leung, David and John Fu, 2014. Interactions between CNY and CNH Money and Forward Exchange

Markets, Hong Kong Institute for Monetary Research Working Papers, No.13 / 2014.

Ma, Guonan and Robert N. McCauley, 2008. The Efficacy of China’s Capital Controls – Evidence

from Price and Flow Data, Pacific Economic Review 13, 104–23

Ma, Guonan and Robert N. McCauley, 2011. The evolving renminbi regime and implications for Asian

currency stability, Journal of the Japanese and International Economies 25 (1), 23–38.

Ma, Jun, 2016a. RMB rate to depend more on basket of currencies: PBOC economist,

http://news.xinhuanet.com/english/2016-01/12/c_134999156.htm

Ma, Jun, 2016b. PBOC’s Ma Says Yuan Exchange Rate Increasingly Transparent,

https://www.bloomberg.com/news/articles/2016-06-07/pboc-s-ma-says-yuan-exchange-rate-

is-increasingly-transparent-ip5gutpk

Maziad, Samar and Joong Shik Kang, (2012). RMB Internationalization: Onshore/Offshore Links, IMF

Working Paper, No. WP/12/133.

Overholt, William H., Guonan Ma and Cheung Kwok Law, 2016. Renminbi Rising: A New Global

Monetary System Emerges, Wiley.

People’s Bank of China, 2005. Public Announcement of the People’s Bank of China on Reforming the

RMB Exchange Rate Regime, http://www.pbc.gov.cn/english/130721/2831438/index.html.

People’s Bank of China, 2010. Further Reform the RMB Exchange Rate Regime and Enhance the

RMB Exchange Rate Flexibility, http://www.pbc.gov.cn/english/130721/2845862/index.html.

People’s Bank of China, 2015a. The PBC Announcement on Improving Quotation of the Central

Parity of RMB against US Dollar, http://www.pbc.gov.cn/english/130721/2941603/index.html.

People’s Bank of China, 2015b. China Monetary Policy Report Quarter Three, 2015, Monetary Policy

Analysis Group of the People’s Bank of China.

People’s Bank of China, 2016a. Public Notice No. 3 [2016],

http://www.pbc.gov.cn/english/130721/3037272/index.html.

People’s Bank of China, 2016b. China Monetary Policy Report, Quarter One, 2016, Monetary Policy

Analysis Group of the People’s Bank of China.

Prasad, Eswar. 2016. The Renminbi’s Ascendance in International Finance, in Policy Challenges in a

Diverging Global Economy, edited by Reuven Glick and Mark M. Spiegel, 207-256, Federal

Reserve Bank of San Francisco: San Francisco, CA.

Rey, Hélène, 2013. Dilemma not Trilemma: The Global Financial Cycle and Monetary Policy

Independence, manuscript.

23

Hong Kong Institute for Monetary Research Working Paper No.06/2017

Schnatz, Bernd, 2011. Global Imbalances and the Pretence of Knowing FEERs, Pacific Economic

Review 16, 604–615.

Shu, Chang, Dong He and Xiaoqiang Cheng, 2015. One currency, two markets: the renminbi's

growing influence in Asia-Pacific, China Economic Review 33(April), 163–178.

Sun, Jie, 2010. Retrospect of the Chinese Exchange Rate Regime after Reform: Stylized Facts during

the Period from 2005 to 2010, China and the World Economy 18(6), 19–35.

SWIFT, 2013. RMB Tracker — April 2013, SWIFT.

SWIFT, 2015. Renminbi’s Stellar Ascension: Are You on Top of It, RMB Tracker, Sibos 2015 edition,

SWIFT.

SWIFT, 2017. RMB Tracker — January 2017, SWIFT.

Wang, Shuo, Jiwei Zhang and Kan Huo, 2016. Transcript: Zhou Xiaochuan Interview,

http://english.caixin.com/2016-02-15/100909181.html.

Zhou, Xiaochuan, 2016. No basis for persistent RMB depreciation: China’s central bank governor,

http://news.xinhuanet.com/english/2016-04/17/c_135285240.htm

24

Hong Kong Institute for Monetary Research Working Paper No.06/2017

Appendix

A1. Data Description

Notation Variable Source

Pt The RMB central parity rate Bloomberg

Yt CNY exchange rate Bloomberg

Ht CNH exchange rate Bloomberg

Bt CFETS RMB Index Based on raw data from Bloomberg

Ut USD index Bloomberg

Zt CNH conditional volatility estimated from a GARCH specification

Based on raw data of Ht from Bloomberg

VIXt VIX index Bloomberg

VXYt JP Morgan emerging market currency volatility index

Bloomberg

FRDt A one-zero dummy variable to capture the possible effect of a drop in China’s foreign exchange reserves

Based on statistics from State Administration of Foreign Exchange (SAFE)

FRIt A one-zero dummy variable for an increase in China’s foreign exchange reserves

Based on statistics from SAFE

FPt CNH-CNY 1-month forward-point differential Bloomberg

25

Hong Kong Institute for Monetary Research Working Paper No.06/2017

A2. Marginal Effects of Onshore and Offshore RMB Rates

Figure A2.1 Marginal effect of Y on P

Figure A2.2 Marginal effect of H on P

Marginal effects of % of significant observations Threshold of Z

H 99.1 0.00450 Y 91.1 0.00316

26

Hong Kong Institute for Monetary Research Working Paper No.06/2017

A3. Results of estimating the RMB central parity equation (7) that allows for asymmetric responses to positive changes in lnVIX or lnVYX

1 2

No Dummy t-1 Dummy No Dummy t-1 Dummy

v (lnPt-1-lnYt-1) -0.373 ***

0.303 -0.350 ***

0.231 (-2.889) (1.241) (-2.594) (1.031) (lnPt-1-lnHt-1) -0.024 -0.035 -0.083

*** 0.070

*

(-0.941) (-0.925) (-2.921) (1.900) lnPt-1 -1.214

*** 0.730 -0.809

* -0.648

(-3.967) (1.039) (-1.683) (-1.015) lnYt-1 1.381

*** 0.309 1.374

* 0.613

(3.011) (0.437) (1.871) (0.672) lnHt-1 0.521

*** -0.156 0.373

** 0.048

(2.777) (-0.347) (2.213) (0.157) lnBt-1 -0.726 -0.371 -1.389

*** 0.662

(-1.469) (-0.507) (-3.336) (0.858) lnUt-1 0.466

*** 0.352 0.698

*** -0.029

(2.977) (1.091) (3.679) (-0.088) Zt -0.627

*** 0.720 -0.421

* 0.265

(-2.926) (1.469) (-1.839) (0.548) Zt*lnPt-1 342.394

*** -315.226 186.572 211.103

(3.375) (-1.184) (1.048) (0.894) Zt*lnYt-1 -379.841

** -16.289 -399.542 -131.485

(-2.564) (-0.069) (-1.567) (-0.429) Zt*lnHt-1 -106.209

** 40.905 -68.744

* 13.151

(-2.444) (0.287) (-1.680) (0.145) Zt*lnBt-1 231.332 101.059 470.797

*** -270.436

(1.300) (0.383) (3.192) (-0.966) Zt*lnUt-1 -109.984

* -129.695 -201.198

*** 12.396

(-1.964) (-1.091) (-2.849) (0.103) Constant 1.39E-03

** -1.78E-03 5.44E-04 8.88E-06

(2.460) (-1.421) (0.942) (0.007) Adj. R

2 0.635 0.645

AIC -10.447 -10.474 SIC -10.129 -10.156 # Observations 336 336

Note: The table presents the results of estimating the RMB central parity equation (7) that allows for asymmetric responses to positive changes in lnVIX or lnVYX. ***, **, and * respectively indicate significance at the 1%, 5%, and 10% level. Robust t-statistics are given in parenthesis underneath coefficient estimates. Adjusted R

2 estimates are

provided in the row labelled “Adj. R2”.

27

Hong Kong Institute for Monetary Research Working Paper No.06/2017

Table 1 Descriptive Statistics lnP lnY lnH lnB (lnP - lnY) (lnP - lnH) (lnP - lnB)

Mean 0.00024 0.00025 0.00022 -0.00018 -0.00064 -0.00381 -2.70005

SD 0.00207 0.00168 0.00272 0.00198 0.00150 0.00464 0.05408

Correlation

lnP 1.000

lnY 0.349 1.000

lnH 0.516 0.501 1.000

lnB -0.046 0.231 0.044 1.000

(lnP - lnY) -0.509 -0.336 -0.277 0.228 1.000

(lnPt-1 - lnH) -0.389 -0.279 -0.415 0.056 0.462 1.000

(lnP - lnB) 0.049 0.080 0.045 0.006 0.079 0.400 1.000

Note: The table presents selected descriptive statistics of the four RMB exchange rates, namely the RMB central parity against the US dollar (P), the onshore RMB exchange rate (Y), the offshore RMB exchange rate (H), and the CFEETS RMB currency basket index (b). The sample period covers August 17, 2015 to December 31, 2016.

Table 2 The Roles of Onshore and Offshore RMB Exchange Rates 1a 1b 1

v (lnPt-1-lnYt-1) -0.451***

-0.378 ***

(-5.736) (-3.345) (lnPt-1-lnHt-1) -0.091

*** -0.033

(-4.159) (-1.633) lnPt-1 -0.255

*** -0.188

*** -0.208

***

(-3.847) (-4.084) (-2.609) lnYt-1 0.475

*** 0.219

(5.678) (1.428) lnHt-1 0.352

*** 0.270

***

(9.271) (5.369) Constant -9.71E-05 -1.34E-03 -1.84E-04 (-0.918) (-1.088) (-1.586) Adj. R

2 0.319 0.331 0.425

AIC -9.891 -9.909 -10.054 SIC -9.846 -9.863 -9.986 # Observations 336 336 336

Note: The table presents the results of estimating the RMB central parity equation (1). ***, **, and * respectively indicate significance at the 1%, 5%, and 10% level. Robust t-statistics are given in parenthesis underneath coefficient estimates. Adjusted R

2 estimates are provided in the row labelled “Adj. R

2.”

28

Hong Kong Institute for Monetary Research Working Paper No.06/2017

Table 3 The Roles of the US Dollar Index, the RMB Index and Volatility 2 3 4 5

v (lnPt-1-lnYt-1) -0.397 ***

-0.352 ***

-0.353 ***

-0.367 ***

(-3.442) (-2.761) (-2.811) (-2.769) (lnPt-1-lnHt-1) -0.029 -0.034

* -0.031 -0.035

*

(-1.520) (-1.694) (-1.603) (-1.868) lnPt-1 -0.214

*** -0.224

** -0.240

*** -0.231

**

(-2.800) (-2.423) (-2.690) (-2.590) lnYt-1 0.196 0.248 0.246 0.236

(1.275) (1.360) (1.328) (1.273) lnHt-1 0.131

*** 0.268

*** 0.126

*** 0.120

***

(3.347) (5.248) (3.150) (2.821) lnBt-1 -0.034 -0.057 -0.052

(-0.568) (-0.969) (-0.899) lnUt-1 0.170

*** 0.171

*** 0.171

***

(8.207) (8.196) (8.058) Zt -0.154 (-0.628) Constant -1.78E-04

* -1.80E-04 -1.71E-04

* 2.19E-04

(-1.838) (-1.545) (-1.776) (0.350) Adj. R

2 0.567 0.424 0.568 0.567

AIC -10.335 -10.050 -10.334 -10.330 SIC -10.255 -9.970 -10.243 -10.227 # Observations 336 336 336 336

Note: The results of estimating the RMB central parity equations (2) to (5) are presented under columns labelled (2) to (5). The volatility measure (Z) is the estimate of the CNH conditional volatility obtained from a GARCH(1,1) model. ***, **, and * respectively indicate significance at the 1%, 5%, and 10% level. Robust t-statistics are given in parenthesis underneath coefficient estimates. Adjusted R

2 estimates are provided in the row labelled “Adj. R

2.”

29

Hong Kong Institute for Monetary Research Working Paper No.06/2017

Table 4 A Multiplicative Interaction Model of the Central Parity Formation Mechanism Model 1 2 3 4 5

v (lnPt-1-lnYt-1) -0.613 -0.571 -0.343 -0.234 -0.245 **

(-1.224) (-1.038) (-0.722) (-0.454) (-1.990) (lnPt-1-lnHt-1) -0.120 0.012 -0.111 -0.026 -0.047

**

(-0.667) (0.084) (-0.616) (0.184) (-2.469) lnPt-1 -0.923

** -0.791

* -1.267

*** -1.202

*** -1.174

***

(-2.423) (-1.949) (-3.435) (-3.128) (-3.643) lnYt-1 1.311

** 1.073

* 1.936

*** 1.765

*** 1.689

***

(2.243) (1.817) (3.445) (3.348) (3.996) lnHt-1 0.871

*** 0.525

*** 0.807

*** 0.447

*** 0.439

***

(6.360) (3.942) (6.171) (3.640) (3.516) lnBt-1 -0.841

*** -1.048

*** -1.019

***

(-2.618) (-3.093) (-2.941) lnUt-1 0.562

*** 0.634

*** 0.633

***

(4.338) (4.459) (4.225) Zt -0.233 -0.386 -0.298 -0.483 -0.344

*

(-0.673) (-1.281) (-0.822) (-1.598) (-1.721) Zt*(lnPt-1-lnYt-1) 108.762 75.360 50.125 -5.620 (0.659) (0.435) (0.325) (-0.036) Zt*(lnPt-1-lnHt-1) 24.694 -17.055 18.223 -25.354 (0.390) (-0.331) (0.284) (-0.507) Zt*lnPt-1 250.066

* 205.236 349.851

*** 328.006

** 318.467

***

(1.892) (1.435) (2.767) (2.418) (2.675) Zt*lnYt-1 -365.935

* -294.939 -540.483

*** -490.485

*** -462.423

***

(-1.863) (-1.498) (-2.918) (-2.872) (-3.307) Zt*lnHt-1 -178.219

*** -106.917

*** -160.476

*** -83.578

*** -80.410

**

(-4.683) (-2.979) (-4.432) (-2.619) (-2.589) Zt*lnBt-1 266.015

** 340.484

*** 329.476

***

(2.355) (2.778) (2.653) Zt*lnUt-1 -147.942

*** -174.365

*** -174.380

***

(-3.131) (-3.335) (-3.165) Constant 3.58E-04 8.06E-04 5.18E-04 1.05E-03 6.74E-04 (0.387) (1.015) (0.539) (1.321) (1.326) Adj. R

2 0.499 0.623 0.508 0.636 0.638

AIC -10.174 -10.453 -10.187 -10.485 -10.495 SIC -10.038 -10.294 -10.028 -10.303 -10.336 # Observations 336 336 336 336 336

Note: The results of estimating alternative versions of the RMB central parity equation (6) are presented under columns labelled (1) to (4). Column (5) reports the results from the parsimonious specification (7) given in the text. ***, **, and * respectively indicate significance at the 1%, 5%, and 10% level. Robust t-statistics are given in parenthesis underneath coefficient estimates. Adjusted R

2 estimates are provided in the row labelled “Adj. R

2.”

30

Hong Kong Institute for Monetary Research Working Paper No.06/2017

Table 5 The Roles of Selected Macro and Financial Variables Model 1 2 3 4 5

v (lnPt-1-lnYt-1) -0.232 * -0.217

* -0.222

* -0.249

** -0.251

**

(-1.882) (-1.778) (-1.835) (-2.095) (-2.100) (lnPt-1-lnHt-1) -0.045

** -0.045

** -0.043

** -0.052

*** -0.048

**

(-2.381) (-2.353) (-2.174) (-2.803) (-2.582) lnPt-1 -1.187

*** -1.187

*** -1.248

*** -1.197

*** -1.209

***

(-3.324) (-3.394) (-3.517) (-3.809) (-3.902) lnYt-1 1.897

*** 1.716

*** 1.670

*** 1.614

*** 1.574

***

(4.280) (4.393) (4.050) (3.807) (3.710) lnHt-1 0.272

* 0.474

*** 0.432

*** 0.443

*** 0.466

***

(1.730) (3.395) (3.408) (3.407) (3.581) lnBt-1 -1.088

*** -1.042

*** -1.066

*** -1.074

*** -1.069

***

(-2.751) (-2.976) (-3.101) (-3.183) (-3.160) lnUt-1 0.645

*** 0.601

*** 0.639

*** 0.677

*** 0.683

***

(3.916) (3.814) (4.401) (4.534) (4.571) FPt-1 -0.053

**

(-2.098) lnVIXt-1 -0.006

(-0.810) lnVXYt-1 0.014

(0.464) FRUt-1 0.002 0.002 (0.503) (0.474) FRIt-1 0.002 (0.340) Zt -0.309 -0.303 -0.358

* -0.332

* -0.328

*

(-1.586) (-1.472) (-1.788) (-1.771) (-1.735) Zt*lnPt-1 326.962

** 316.589

** 336.229

** 330.426

*** 335.305

***

(2.460) (2.402) (2.513) (2.834) (2.925) Zt*lnYt-1 -522.917

*** -465.943

*** -451.899

*** -436.426

*** -425.628

***

(-3.493) (-3.676) (-3.322) (-3.053) (-2.974) Zt*lnHt-1 -30.737 -96.865

** -80.226

** -81.774

** -86.274

***

(-0.650) (-2.573) (-2.535) (-2.516) (-2.647) Zt*lnBt-1 354.647

** 333.032

*** 340.651

*** 350.464

*** 348.042

***

(2.488) (2.641) (2.760) (2.925) (2.898) Zt*lnUt-1 -180.626

*** -160.248

*** -177.034

*** -190.590

*** -193.020

***

(-2.976) (-2.808) (-3.360) (-3.444) (-3.484) Zt*FPt-1 14.967

*

(1.867) Zt*lnVIXt-1 2.808

(1.032) Zt*lnVXYt-1 -2.012

(-0.177) Zt*FRDt-1 -1.150 -1.107 (-0.705) (-0.678) Zt*FRIt-1 -1.120 (-0.577) Constant 5.94E-04 5.91E-04 7.45E-04 6.41E-04 6.57E-04 (1.198) (1.130) (1.448) (1.370) (1.394) Adj. R

2 0.641 0.644 0.644 0.640 0.642

AIC -10.497 -10.506 -10.505 -10.495 -10.494 SIC -10.315 -10.324 -10.323 -10.313 -10.290 # Observations 336 336 336 336 336

31

Hong Kong Institute for Monetary Research Working Paper No.06/2017

Note: The results of estimating alternative versions of the RMB central parity equation (10) are presented. See the text

for definitions of FP, lnVIX, lnVXY, FRD, and FRI. ***, **, and * respectively indicate significance at the 1%, 5%, and 10% level. Robust t-statistics are given in parenthesis underneath coefficient estimates. Adjusted R

2 estimates

are provided in the row labelled “Adj. R2.”

32

Hong Kong Institute for Monetary Research Working Paper No.06/2017

Table 6 The Central Parity Formation Mechanism Allowing for Asymmetric Responses to Positive Changes in the US Dollar Index or the RMB Index Model 1 2

No Dummy t-1 Dummy No Dummy t Dummy

v (lnPt-1-lnYt-1) -0.223 ** 0.036 -0.139 -0.275

(-2.225) (0.161) (-0.716) (-1.116) (lnPt-1-lnHt-1) -0.122

*** 0.151

*** -0.076

*** 0.086

**

(-4.810) (4.461) (-3.232) (2.290) lnPt-1 -0.478 -0.960 -1.774

*** 0.634

(-0.991) (-1.464) (-4.558) (0.698) lnYt-1 1.137

** 0.452 2.348

*** 0.056

(2.418) (0.605) (3.703) (0.065) lnHt-1 0.306 0.109 0.279 0.052

(1.464) (0.437) (1.180) (0.166) lnBt-1 -2.085

*** 1.837

*** -1.700

*** 0.722

(-3.660) (2.656) (-2.840) (0.962) lnUt-1 1.126

*** -0.988

** 0.767

*** -0.512

(4.878) (-2.378) (3.222) (-1.313) Zt -1.037

** 0.583 -0.197 -0.851

*

(-2.379) (0.975) (-0.770) (-1.778) Zt*lnPt-1 48.615 328.406 521.166

*** -206.731

(0.269) (1.384) (3.528) (-0.596) Zt*lnYt-1 -299.557

** -41.860 -695.257

*** -27.051

(-2.055) (-0.178) (-2.920) (-0.088) Zt*lnHt-1 -49.176 -36.069 -2.771 -66.196

(-0.781) (-0.505) (-0.038) (-0.755) Zt*lnBt-1 716.436

*** -675.929

*** 572.569

** -263.114

(3.582) (-2.772) (2.591) (-0.979) Zt*lnUt-1 -362.838

*** 342.429

** -234.859

*** 209.181

(-4.313) (2.245) (-2.772) (1.465) Constant 2.07E-03

* -3.28E-04 1.26E-04 2.67E-03

**

(1.777) (-0.211) (0.192) (2.083) Adj. R

2 0.680 0.648

AIC -10.578 -10.483 SIC -10.260 -10.165 # Observations 336 336

Note: The table presents the results of estimating the RMB central parity equation (7) that allows for asymmetric

responses to positive changes in the US dollar index or the CFETS RMB currency basket index. ***, **, and *

respectively indicate significance at the 1%, 5%, and 10% level. Robust t-statistics are given in parenthesis

underneath coefficient estimates. Adjusted R2 estimates are provided in the row labelled “Adj. R

2”.

33

Hong Kong Institute for Monetary Research Working Paper No.06/2017

Figure 1 RMB exchange rates & CFETS Index

34

Hong Kong Institute for Monetary Research Working Paper No.06/2017

Figure 2 Marginal effect of B on P

Figure 3 Marginal effect of U on P