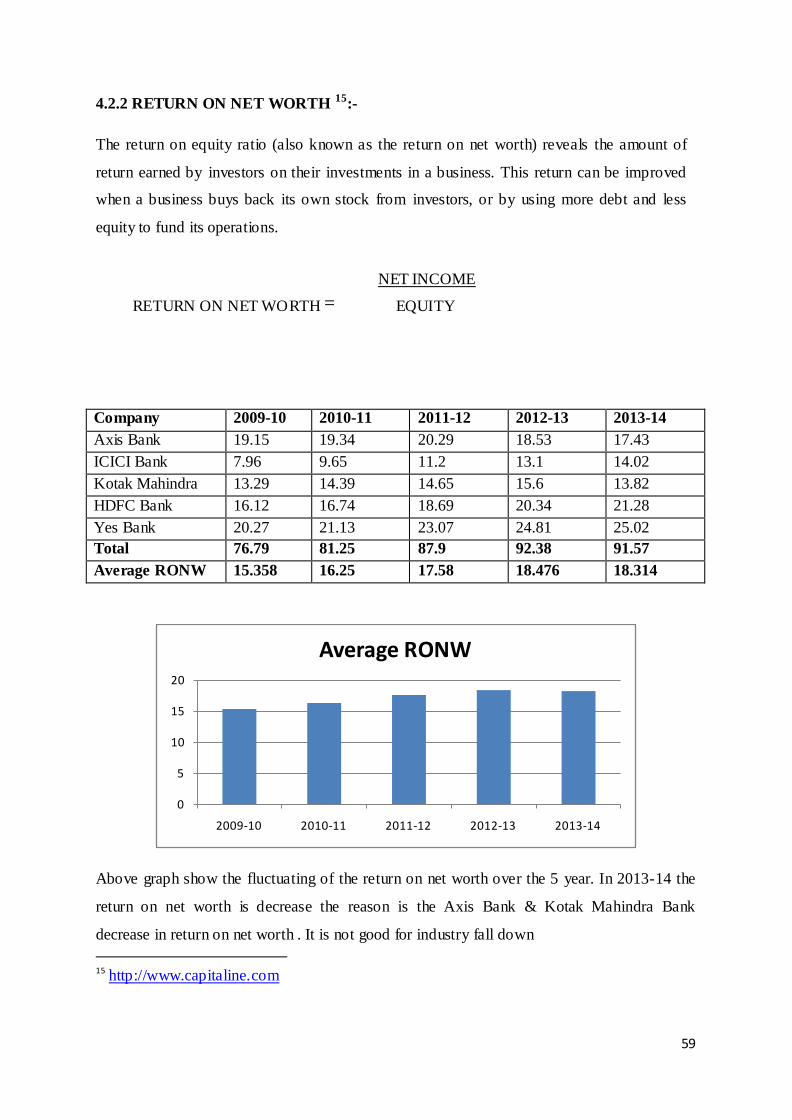

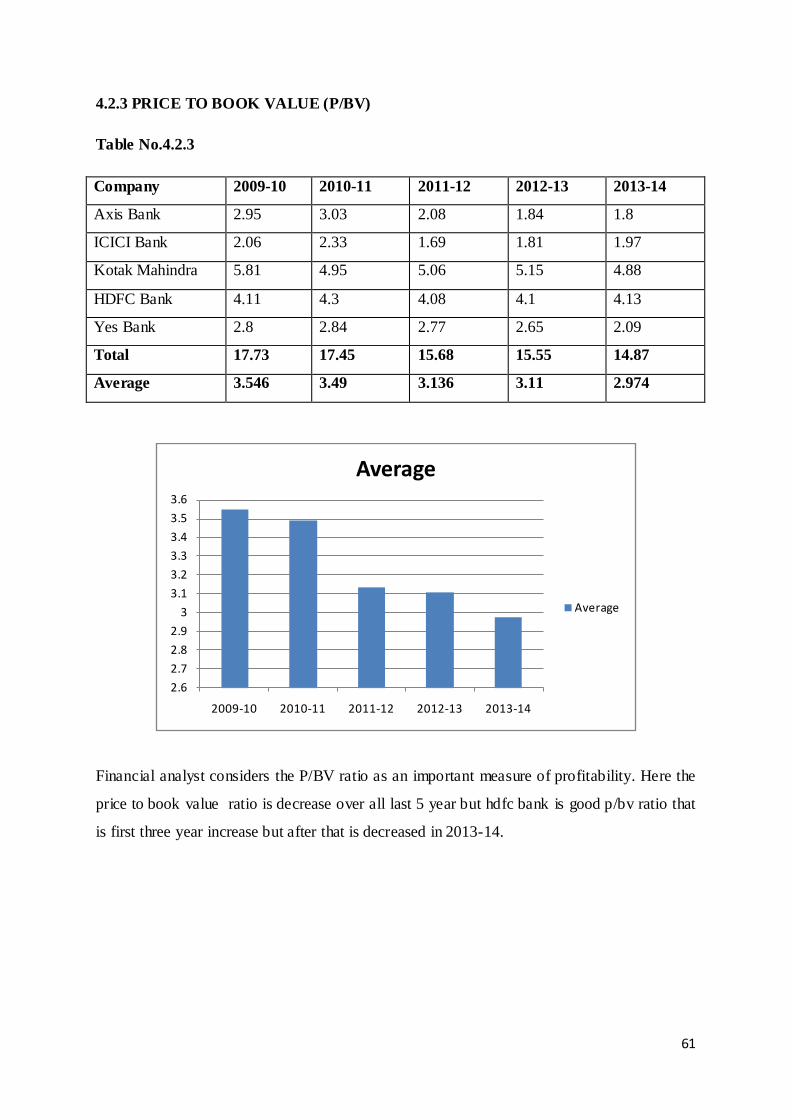

“MACRO ANALYSIS OF INADIAN BANKING SECTOR ”...

93

“MACRO ANALYSIS OF INADIAN BANKING SECTOR” Management Research Project -I Submitted In the partial fulfillment of the Degree of Master of Business Administration Semester-III By Name Exam No. Dave Avani 13044311021 Soni Soham K 13044311136 Patel Manthan K 13044311090 Patel Diptiben J 13044311165 Patel Ramkrushna S 13044311193 Patel Hardik P 13044311168 Patel Dhara 13044311161 Under the Guidance of: Prof. (Dr.) Mahendra Sharma Prof. & Head, V. M. Patel Institute of Management. & Dr. Harsha Jariwala Dr. Abhishek Parikh Faculty Members V. M. Patel Institute of Management. Submitted To: V. M. Patel Institute of Management, Ganpat University, Kherva. (December, 2014)

Transcript of “MACRO ANALYSIS OF INADIAN BANKING SECTOR ”...

“MACRO ANALYSIS OF INADIAN BANKING SECTOR”

Management Research Project -I

Submitted

In the partial fulfillment of the Degree of

Master of Business Administration

Semester-III By

Name Exam No. Dave Avani 13044311021 Soni Soham K 13044311136 Patel Manthan K 13044311090 Patel Diptiben J 13044311165 Patel Ramkrushna S 13044311193 Patel Hardik P 13044311168 Patel Dhara 13044311161

Under the Guidance of:

Prof. (Dr.) Mahendra Sharma

Prof. & Head,

V. M. Patel Institute of Management.

&

Dr. Harsha Jariwala

Dr. Abhishek Parikh

Faculty Members

V. M. Patel Institute of Management.

Submitted To:

V. M. Patel Institute of Management,

Ganpat University,

Kherva.

(December, 2014)

CERTIFICATE BY THE GUIDE

This is to certify that the contents of this report entitled “Macro Analysis Of Indian Banking Sector”

by Dave Avani, Soni Soham, Patel Mantan, Patel Dipti, Patel Dhara ,Patel Ramkrushna, Patel Hardik

submitted to V. M. Patel Institute of Management for the Award of Master of Business Administration

(MBA Semester -III) is original research work carried out by them under my supervision.

This report has not been submitted either partly or fully to any other University or Institute for award

of any degree or diploma.

Prof. (Dr.) Mahendra Sharma, Professor & Head, V. M. Patel Institute Of Management, Ganpat University. Kherva. Date : Place :

CANDIDATE’S STATEMENT

We hereby declare that the work incorporated in this report entitled “Macro Analysis Of Indian

Banking Sector” in partial fulfillment of the requirements for the award of Master of Business

Administration (Semester - III) is the outcome of original study undertaken by me and it has not been

submitted earlier to any other University or Institution for the award of any Degree or Diploma.

Dave Avani Soni Soham

Patel Manthan Patel Hardik

Patel Ramkrushna Patel Dipti

Patel Dhara

Date: 08/12/2014

Place: kherva ,

Ganpat university

i

PREFACE

Practical study plays a vital role in the field of education. It has been introduced for the student

to get practical knowledge along with theoretical knowledge only bookish knowledge is not right

way of learning anything especially for the management students. How management principals

are implemented in business can only be known through practical study, students can be very

well aware about industrial environment like problems, opportunity, different situation etc. this

helps the student to have better understanding and also give them a chance to show their skills

and ability.

The principal concern of this report is to reveal my learning of practical business scenario. In

writing this report I have drawn vast amount of the information from various senior people and

simultaneously supplemented by various other people, annual reports, letters, journals etc.

Here, I am presenting a project on the different concept that I saw, fill and experience, while the

work on the project report. I have tried my level best to do the proper justification with my work

in this project.

Dave AvaniY.

Soni Soham K.

Patel Manthan K.

Patel Dipti J.

Patel Ramkrushna S.

Patel Hardik P

Patel Dhara H.

ii

ACKNOWLEDGEMENT

It was really difficult for me to complete the management research project without getting co-

operation of certain people. In other words there are so many external people who directly or

indirectly help me in my management research project.

First of all, I am very grateful to our collage H.O.D. Prof. MAHENRA SHARMA for his able

leadership and our project Report who providing their valuable time and guideline to me

regarding the management Research project report.

I am also thankful to Dr.HarshaJariwala and Dr. Abhishek Parikh who gives guideline our group

to do management research report in their college and helped me by giving all the required

information for a period . I am also thankful to my friends who help me and guide me.

Dave AvaniY.

Soni Soham K.

Patel Manthan K.

Patel Dipti J.

Patel Ramkrushna S.

Patel Hardik P

Patel Dhara H.

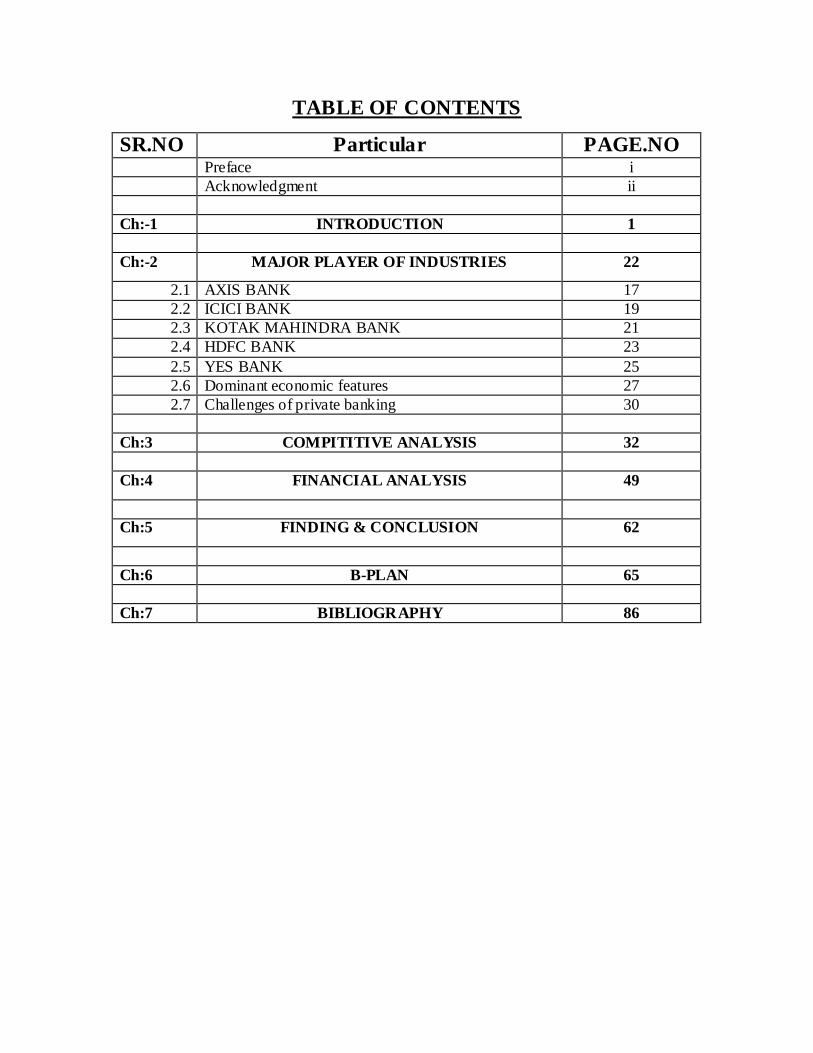

TABLE OF CONTENTS

SR.NO Particular PAGE.NO Preface i Acknowledgment ii

Ch:-1 INTRODUCTION 1

Ch:-2 MAJOR PLAYER OF INDUSTRIES 22

2.1 AXIS BANK 17 2.2 ICICI BANK 19 2.3 KOTAK MAHINDRA BANK 21 2.4 HDFC BANK 23 2.5 YES BANK 25 2.6 Dominant economic features 27 2.7 Challenges of private banking 30

Ch:3 COMPITITIVE ANALYSIS 32 Ch:4 FINANCIAL ANALYSIS 49

Ch:5 FINDING & CONCLUSION 62

Ch:6 B-PLAN 65

Ch:7 BIBLIOGRAPHY 86

1

Chapter 1 Introduction of the Industry

Sr.no Particulars Page.no

1.1 Introduction of indian banking 2

1.2 Need Of Bank 2

1.3 History of Indian Banking System 3

1.4 Classification of Banking Industry in India 7

1.5 Services provided by banking organizations 12

1.6 Types of Banks 14

2

1.1 Introduction:-

A bank is a financial institution that provides banking and other financial services to their

customers. A bank is generally understood as an institution which provides fundamental

banking services such as accepting deposits and providing loans. There are also nonbanking

institutions that provide certain banking services without meeting the legal definition of a

bank. Banks are a subset of the financial services industry. A banking system also referred as

a system provided by the bank which offers cash management services for customers,

reporting the transactions of their accounts and portfolios, throughout the day. The banking

system in India should not only be hassle free but it should be able to meet the new

challenges posed by the technology and any other external and internal factors. For the past

three decades, India’s banking system has several outstanding achievements to its credit. The

Banks are the main participants of the financial system in India. The Banking sector offers

several facilities and opportunities to their customers. All the banks safeguard the money and

valuables and provide loans, credit, and payment services, such as checking accounts, money

orders, and cashier’s cheques. The banks also offer investment and insurance products. As a

variety of models for cooperation and integration among finance industries have emerged,

some of the traditional distinctions between banks, insurance companies, and securities firms

have diminished. In spite of these changes, banks continue to maintain and perform their

primary role—accepting deposits and lending funds from these deposits.

1.2 Need of the Banks:-

Before the establishment of banks, the financial activities were handled by money lenders and

individuals. At that time the interest rates were very high. Again there were no security of

public savings and no uniformity regarding loans. So as to overcome such problems the

organized banking sector was established, which was fully regulated by the government. The

organized 1 banking sector works within the financial system to provide loans, accept deposits

and provide other services to their customers.

The following functions of the bank explain the need of the bank and its importance:

1 http://www.ibef.org/industry/banking-india.aspx

BANKING SYSTEM IN INDIA

3

• To provide the security to the savings of customers.

• To control the supply of money and credit

• To encourage public confidence in the working of the financial system, increase Savingsn

speedily and efficiently.

• To avoid focus of financial powers in the hands of a few individuals and

Institutions.

• To set equal norms and conditions (i.e. rate of interest, period of lending etc) to all

types of customers

1.3 History of Indian Banking System2:-

The first bank in India, called The General Bank of India was established in the year 1786.

The East India Company established The Bank of Bengal/Calcutta (1809), Bank of Bombay

(1840) and Bank of Madras (1843). The next bank was Bank of Hindustan which was

established in 1870. These three individual units (Bank of Calcutta, Bank of Bombay, and

Bank of Madras) were called as Presidency Banks. Allahabad Bank which was established in

1865, was for the first time completely run by Indians. Punjab National Bank Ltd. was set up

in 1894 with head quarters at Lahore. Between 1906 and 1913, Bank of India, Central Bank

of India, Bank of Baroda, Canara Bank, Indian Bank, and Bank of Mysore were set up. In

1921, all presidency banks were amalgamated to form the Imperial Bank of India which was

run by European Shareholders. After that the Reserve Bank of India was established in April

1935. At the time of first phase the growth of banking sector was very slow. Between 1913

and 1948 there were approximately 1100 small banks in India. To streamline the functioning

and activities of commercial banks, the Government of India came up with the Banking

Companies Act, 1949 which was later changed to Banking Regulation Act 1949 as per

amending Act of 1965 (Act No.23 of 1965). Reserve Bank of India was vested with extensive

powers for the supervision of banking in India as a Central Banking Authority. After

independence, Government has taken most important steps in regard of Indian Banking

Sector reforms. In 1955, the Imperial Bank of India was nationalized and was given the name 2 http://en.wikipedia.org/wiki/History_of_banking

4

"State Bank of India", to act as the principal agent of RBI and to handle banking transactions

all over the country. It was established under State Bank of India Act, 1955. Seven banks

forming subsidiary of State Bank of India was nationalized in 1960. On 19th July, 1969,

major process of nationalization was carried out. At the same time 14 major Indian

commercial banks of the country were nationalized. In 1980, another six banks were

nationalized, and thus raising the number of nationalized banks to 20. Seven more banks were

nationalized with deposits over 200 Crores. Till the year 1980 approximately 80% of the

banking segment in India was under government’s ownership. On the suggestions of

Narsimhan Committee, the Banking Regulation Act was amended in 1993 and thus the gates

for the new private sector banks were opened.

The following are the major steps taken by the Government of India to Regulate Banking

institutions in the country:-

1949 : Enactment of Banking Regulation Act.

1955 : Nationalization of State Bank of India.

1959 : Nationalization of SBI subsidiaries.

1961 : Insurance cover extended to deposits.

1969 : Nationalization of 14 major Banks.

1971 : Creation of credit guarantee corporation.

1975 : Creation of regional rural banks.

1980 : Nationalization of seven banks with deposits over 200 Corers.

1.3.1 Nationalization

By the 1960s, the Indian banking industry has become an important tool to facilitate the

development of the Indian economy. At the same time, it has emerged as a large employer,

and a debate has ensured about the possibility to nationalise the banking industry. Indira

Gandhi, the-then Prime Minister of India expressed the intention of the Government of India

(GOI) in the annual conference of the All India Congress Meeting in a paper entitled "Stray

thoughts on Bank Nationalisation". The paper was received with positive enthusiasm.

Thereafter, her move was swift and sudden, and the GOI issued an ordinance and nationalised

5

the 14 largest commercial banks with effect from the midnight of July 19, 1969. Jayaprakash

Narayan, a national leader of India, described the step as a "Masterstroke of political

sagacity" 3 Within two weeks of the issue of the ordinance, the Parliament passed the

Banking Companies (Acquisition and Transfer of Undertaking) Bill, and it received the

presidential approval on 9 August, 1969. A second step of nationalisation of 6 more

commercial banks followed in 1980. The stated reason for the nationalisation was to give the

government more control of credit delivery. With the second step of nationalisation, the GOI

controlled around 91% of the banking business in India. Later on, in the year 1993, the

government merged New Bank of India with Punjab National Bank. It was the only merger

between nationalised banks and resulted in the reduction of the number of nationalised banks

from 20 to 19. After this, until the 1990s, the nationalised banks grew at a pace of around 4%,

closer to the average growth rate of the Indian economy. The nationalised banks were

credited by some; including Home minister P. Chidambaram, to have helped the Indian

economy withstand the global financial crisis of 2007-2009.

1.3.2 Liberalization:-

In the early 1990s, the then Narsimha Rao government embarked on a policy of liberalisation,

licensing a small number of private banks. These came to be known as New Generation

tech-savvy banks, and included Global Trust Bank (the first of such new generation banks to

be set up), which later amalgamated with Oriental Bank of Commerce, Axis Bank(earlier as

UTI Bank), ICICI Bank and HDFC Bank. This move along with the rapid growth in the

economy of India revolutionized the banking sector in India which has seen rapid growth

with strong contribution from all the three sectors of banks, namely, government banks,

private banks and foreign banks. The next stage for the Indian banking has been setup with

the proposed relaxation in the norms for Foreign Direct Investment, where all Foreign

Investors in banks may be given voting rights which could exceed the present cap of 10%, at

present it has gone up to 49% with some restrictions. The new policy shook the banking

sector in India completely. Bankers, till this time, were used to the 4-6-4 method (Borrow at

4%; Lend at 6%; Go home at 4) of functioning.

The new wave ushered in a modern outlook and tech-savvy methods of working for the

traditional banks. All this led to the retail boom in India. People not just demanded more from

3 http://en.wikipedia.org/wiki/History_of_banking

6

their banks but also received more. Currently (2007), banking in India is generally fairly

mature in terms of supply, product range and reach-even though reach in rural India still

remains a challenge for the private sector and foreign banks. In terms of quality of assets and

capital adequacy, Indian banks are considered to have clean, strong and transparent balance

sheets as compared to other banks in comparable economies in its region. The Reserve Bank

of India is an autonomous body, with minimal pressure from the government. The stated

policy of the Bank on the Indian Rupee is to manage volatility but without any fixed

exchange rate-and this has mostly been true. With the growth in the Indian economy expected

to be strong for quite some time-especially in its services sector-the demand for banking

services, especially retail banking, mortgages and investment services are expected to be

strong. In March 2006, the Reserve Bank of India allowed Warburg Pincus to increase its

stake in Kotak Mahindra Bank (a private sector bank) to 10%. This is the first time an

investor has been allowed to hold more than 5% in a private sector bank since the RBI

announced norms in 2005 that any stake exceeding 5% in the private sector banks would

need to be voted by them. In recent years critics have charged that the non-government

owned banks are too aggressive in their loan recovery efforts in connection with housing,

vehicle and personal loans. There are press reports that the banks' loan recovery efforts have

driven defaulting borrowers to suicide.

1.3.3 Government policy on banking industry (Source:-The federal Reserve Act 1913

and

The Banking Act 1933)

Banks operating in most of the countries must contend with heavy regulations, rules enforced

by Federal and State agencies to govern their operations, service offerings, and the manner in

which they grow and expand their facilities to better serve the public. A banker works within

the financial system to provide loans, accept deposits, and provide other services to their

customers. They must do so within a climate of extensive regulation, designed primarily to

protect the public interests.

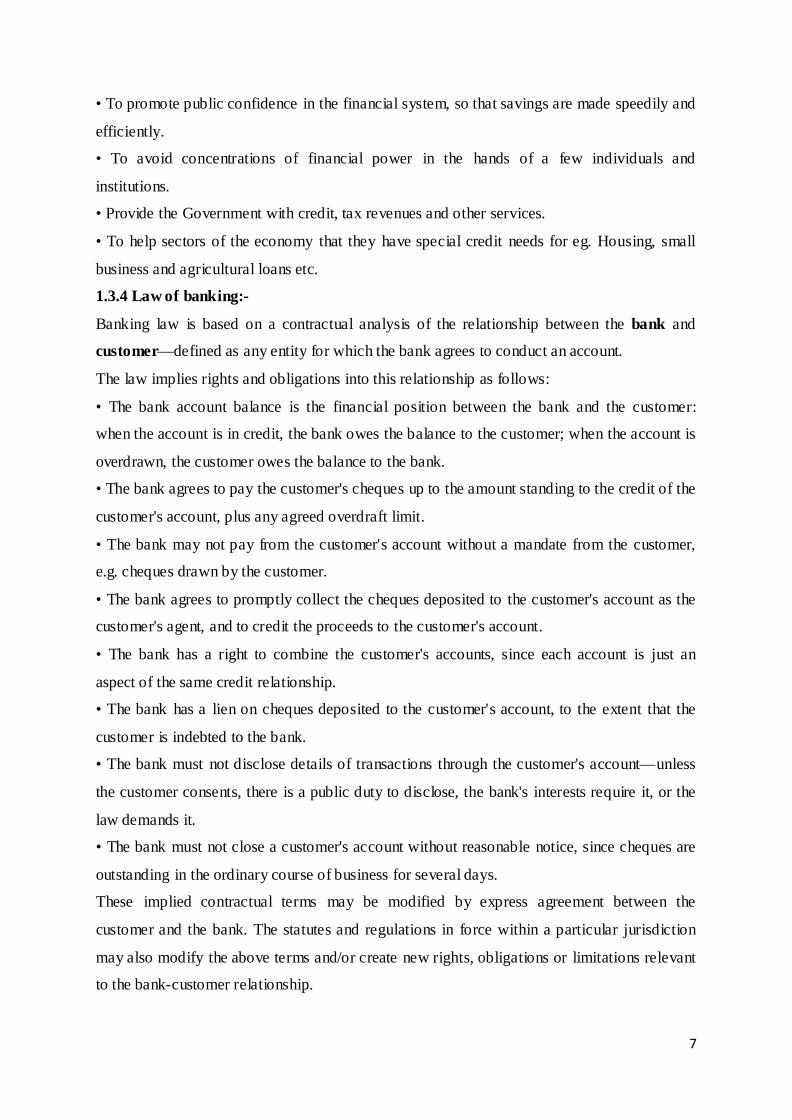

The main reasons why the banks are heavily regulated are as follows:

• To protect the safety of the public’s savings.

• To control the supply of money and credit in order to achieve a nation’s broad economic

goal.

• To ensure equal opportunity and fairness in the public’s access to credit and other vital

financial services.

7

• To promote public confidence in the financial system, so that savings are made speedily and

efficiently.

• To avoid concentrations of financial power in the hands of a few individuals and

institutions.

• Provide the Government with credit, tax revenues and other services.

• To help sectors of the economy that they have special credit needs for eg. Housing, small

business and agricultural loans etc.

1.3.4 Law of banking:-

Banking law is based on a contractual analysis of the relationship between the bank and

customer—defined as any entity for which the bank agrees to conduct an account.

The law implies rights and obligations into this relationship as follows:

• The bank account balance is the financial position between the bank and the customer:

when the account is in credit, the bank owes the balance to the customer; when the account is

overdrawn, the customer owes the balance to the bank.

• The bank agrees to pay the customer's cheques up to the amount standing to the credit of the

customer's account, plus any agreed overdraft limit.

• The bank may not pay from the customer's account without a mandate from the customer,

e.g. cheques drawn by the customer.

• The bank agrees to promptly collect the cheques deposited to the customer's account as the

customer's agent, and to credit the proceeds to the customer's account.

• The bank has a right to combine the customer's accounts, since each account is just an

aspect of the same credit relationship.

• The bank has a lien on cheques deposited to the customer's account, to the extent that the

customer is indebted to the bank.

• The bank must not disclose details of transactions through the customer's account—unless

the customer consents, there is a public duty to disclose, the bank's interests require it, or the

law demands it.

• The bank must not close a customer's account without reasonable notice, since cheques are

outstanding in the ordinary course of business for several days.

These implied contractual terms may be modified by express agreement between the

customer and the bank. The statutes and regulations in force within a particular jurisdiction

may also modify the above terms and/or create new rights, obligations or limitations relevant

to the bank-customer relationship.

8

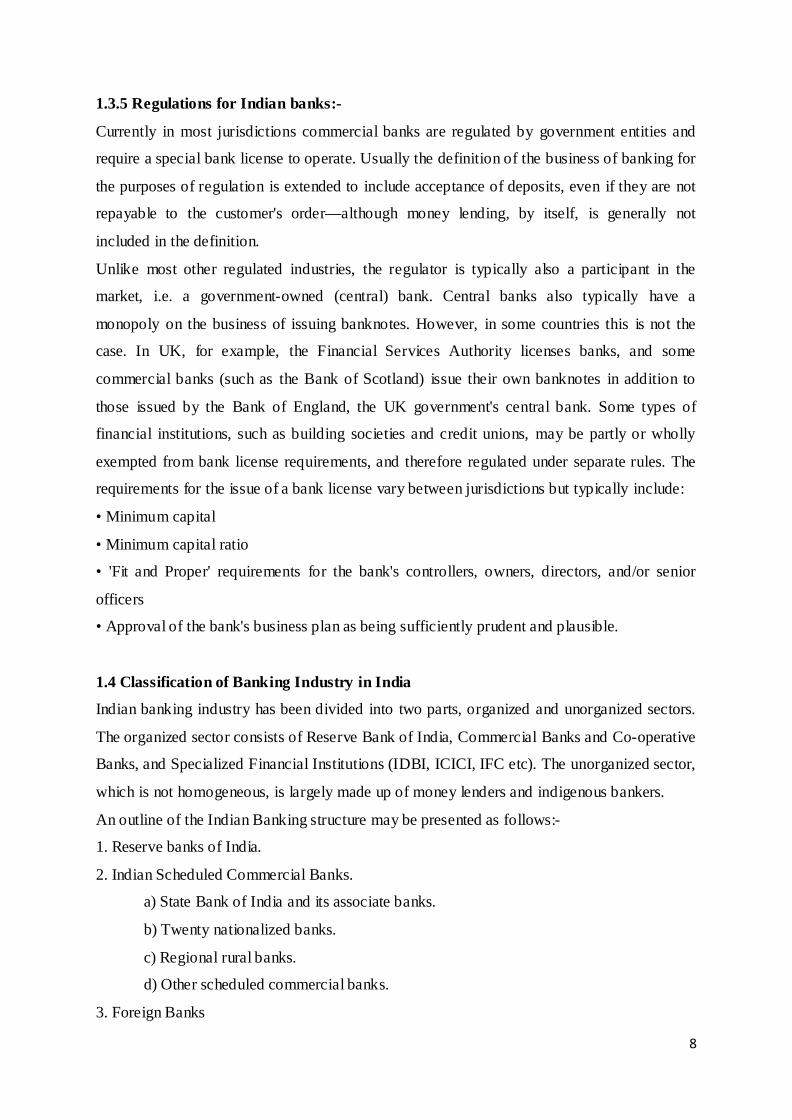

1.3.5 Regulations for Indian banks:-

Currently in most jurisdictions commercial banks are regulated by government entities and

require a special bank license to operate. Usually the definition of the business of banking for

the purposes of regulation is extended to include acceptance of deposits, even if they are not

repayable to the customer's order—although money lending, by itself, is generally not

included in the definition.

Unlike most other regulated industries, the regulator is typically also a participant in the

market, i.e. a government-owned (central) bank. Central banks also typically have a

monopoly on the business of issuing banknotes. However, in some countries this is not the

case. In UK, for example, the Financial Services Authority licenses banks, and some

commercial banks (such as the Bank of Scotland) issue their own banknotes in addition to

those issued by the Bank of England, the UK government's central bank. Some types of

financial institutions, such as building societies and credit unions, may be partly or wholly

exempted from bank license requirements, and therefore regulated under separate rules. The

requirements for the issue of a bank license vary between jurisdictions but typically include:

• Minimum capital

• Minimum capital ratio

• 'Fit and Proper' requirements for the bank's controllers, owners, directors, and/or senior

officers

• Approval of the bank's business plan as being sufficiently prudent and plausible.

1.4 Classification of Banking Industry in India

Indian banking industry has been divided into two parts, organized and unorganized sectors.

The organized sector consists of Reserve Bank of India, Commercial Banks and Co-operative

Banks, and Specialized Financial Institutions (IDBI, ICICI, IFC etc). The unorganized sector,

which is not homogeneous, is largely made up of money lenders and indigenous bankers.

An outline of the Indian Banking structure may be presented as follows:-

1. Reserve banks of India.

2. Indian Scheduled Commercial Banks.

a) State Bank of India and its associate banks.

b) Twenty nationalized banks.

c) Regional rural banks.

d) Other scheduled commercial banks.

3. Foreign Banks

9

4. Non-scheduled banks.

5. Co-operative banks.

1.4.1 Reserve bank of India

The reserve bank of India is a central bank and was established in April 1, 1935 in

accordance with the provisions of reserve bank of India act 1934. The central office of RBI is

located at Mumbai since inception. Though originally the reserve bank of India was privately

owned, since nationalization in 1949, RBI is fully owned by the Government of India. It was

inaugurated with share capital of Rs. 5 Crores divided into shares of Rs. 100 each fully paid

up. RBI is governed by a central board (headed by a governor) appointed by the central

government of India. RBI has 22 regional offices across India. The reserve bank of India was

nationalized in the year 1949. The general superintendence and direction of the bank is

entrusted to central board of directors of 20 members, the Governor and four deputy

Governors, one Governmental official from the ministry of Finance, ten nominated directors

by the government to give representation to important elements in the economic life of the

country, and the four nominated director by the Central Government to represent the four

local boards with the headquarters at Mumbai,Kolkata, Chennai and New Delhi. Local Board

consists of five members each central government appointed for a term of four years to

represent territorial and economic interests and the interests of cooperative and indigenous

banks.

The RBI Act 1934 was commenced on April 1, 1935. The Act, 1934 provides the statutory

basis of the functioning of the bank. The bank was constituted for the need of following:

- To regulate the issues of banknotes.

- To maintain reserves with a view to securing monetary stability

- To operate the credit and currency system of the country to its advantage.

Functions of RBI as a central bank of India are explained briefly as follows:

Bank of Issue: The RBI formulates, implements, and monitors the monitory policy. Its main

objective is maintaining price stability and ensuring adequate flow of credit to productive

sector.

Regulator-Supervisor of the financial system: RBI prescribes broad parameters of banking

operations within which the country’s banking and financial system functions. Their main

objective is to maintain public confidence in the system, protect depositor’s interest and

provide cost effective banking services to the public.

10

Manager of exchange control: The manager of exchange control department manages the

foreign exchange, according to the foreign exchange management act, 1999. The manager’s

main objective is to facilitate external trade and payment and promote orderly development

and maintenance of foreign exchange market in India.

Issuer of currency: A person who works as an issuer, issues and exchanges or destroys the

currency and coins that are not fit for circulation. His main objective is to give the public

adequate quantity of supplies of currency notes and coins and in good quality.

Developmental role: The RBI performs the wide range of promotional functions to support

national objectives such as contests, coupons maintaining good public relations and many

more.

Related functions: There are also some of the related functions to the above mentioned main

functions. They are such as, banker to the government, banker to banks etc….

• Banker to government performs merchant banking function for the central and the state

governments; also acts as their banker.

• Banker to banks maintains banking accounts to all scheduled banks.

Controller of Credit: RBI performs the following tasks:

• It holds the cash reserves of all the scheduled banks.

• It controls the credit operations of banks through quantitative and qualitative controls.

• It controls the banking system through the system of licensing, inspection and calling for

information.

• It acts as the lender of the last resort by providing rediscount facilities to scheduled banks.

Supervisory Functions:

In addition to its traditional central banking functions, the Reserve Bank performs certain

non-monetary functions of the nature of supervision of banks and promotion of sound

banking in India. The Reserve Bank Act 1934 and the banking regulation act 1949 have given

the RBI wide powers of supervision and control over commercial and co-operative banks,

relating to licensing and establishments, branch expansion, liquidity of their assets,

management and methods of working, amalgamation, reconstruction and liquidation. The

RBI is authorized to carry out periodical inspections of the banks and to call for returns and

necessary information from them. The nationalization of 14 major Indian scheduled banks in

July 1969 has imposed new responsibilities on the RBI for directing the growth of banking

and credit policies towards more rapid development of the economy and realization of certain

desired social objectives. The supervisory functions of the RBI have helped a great deal in

11

improving the standard of banking in India to develop on sound lines and to improve the

methods of their operation.

Promotional Functions: With economic growth assuming a new urgency since

independence, the range of the Reserve Bank’s functions has steadily widened. The bank now

performs a variety of developmental and promotional functions, which, at one time, were

regarded as outside the normal scope of central banking. The Reserve bank was asked to

promote banking habit, extend banking facilities to rural and semi-urban areas, and establish

and promote new specialized financing agencies.

1.4.2 Indian Scheduled Commercial Banks

The commercial banking structure in India consists of scheduled commercial banks, and

unscheduled banks.

Scheduled Banks : Scheduled Banks in India constitute those banks which have been

included in the second schedule of RBI act 1934. RBI in turn includes only those banks in

this schedule which satisfy the criteria laid down vide section 42(6a) of the Act. “Scheduled

banks in India” means the State Bank of India constituted under the State Bank of India Act,

1955 (23 of 1955), a subsidiary bank as defined in the s State Bank of India (subsidiary

banks) Act, 1959 (38 of 1959), a corresponding new bank constituted under section 3 of the

Banking companies (Acquisition and Transfer of Undertakings) Act, 1980 (40 of 1980), or

any other bank being a bank included in the Second Schedule to the Reserve bank of India

Act, 1934 (2 of 1934), but does not include a co-operative bank”. For the purpose of

assessment of performance of banks, the Reserve Bank of India categories those banks as

public sector banks, old private sector banks, new private sector banks and foreign banks, i.e.

private sector, public sector, and foreign banks come under the umbrella of scheduled

commercial banks.

Regional Rural Bank:

The government of India set up Regional Rural Banks (RRBs) on October 2, 1975 . The

banks provide credit to the weaker sections of the rural areas, particularly the small and

marginal farmers, agricultural laborers, and small entrepreneurs. Initially, five RRBs were set

up on October 2, 1975 which was sponsored by Syndicate Bank, State Bank of India, Punjab

National Bank, United Commercial Bank and United Bank of India. The total authorized

capital was fixed at Rs. 1 Crore which has since been raised to Rs. 5 Crores. There are several

concessions enjoyed by the RRBs by Reserve Bank of India such as lower interest rates and

refinancing facilities from

12

NABARD like lower cash ratio, lower statutory liquidity ratio, lower rate of interest on loans

taken from sponsoring banks, managerial and staff assistance from the sponsoring bank and

reimbursement of the expenses on staff training. The RRBs are under the control of

NABARD. NABARD has the responsibility of laying down the policies for the RRBs, to

oversee their operations, provide refinance facilities, to monitor their performance and to

attend their problems.

Unscheduled Banks: “Unscheduled Bank in India” means a banking company as defined in

clause (c) of section 5 of the Banking Regulation Act, 1949 (10 of 1949), which is not a

scheduled bank”.

1.4.3 NABARD

NABARD is an apex development bank with an authorization for facilitating credit flow for

promotion and development of agriculture, small-scale industries, cottage and village

industries, handicrafts and other rural crafts. It also has the mandate to support all other allied

economic activities in rural areas, promote integrated and sustainable rural development and

secure prosperity of rural areas. In discharging its role as a facilitator for rural prosperity,

NABARD is entrusted with:

1. Providing refinance to lending institutions in rural areas

2. Bringing about or promoting institutions development and

3. Evaluating, monitoring and inspecting the client banks

Besides this fundamental role, NABARD also:

• Act as a coordinator in the operations of rural credit institutions

• To help sectors of the economy that they have special credit needs for eg. Housing, small

business and agricultural loans etc.

1.4.4 Co-operative Banks :-

The corporate banking segment of banks typically serves a diverse range of clients, ranging

from small to mid-sized local businesses with a few millions in revenues to large

conglomerates with billions in sales and offices across the country.

1.5 Services provided by banking organizations :-

Banking Regulation Act in India, 1949 defines banking as “Accepting” for the purpose of

lending or investment of deposits of money from the public, repayable on demand and with

drawable by cheques, drafts, orders etc. as per the above definition a bank essentially

performs the following functions:-

13

• Accepting Deposits or savings functions from customers or public by providing bank

account, current account, fixed deposit account, recurring accounts etc.

• The payment transactions like lending money to the public. Bank provides an effective

credit delivery system for loanable transactions.

• Provide the facility of transferring of money from one place to another place. For

performing this operation, bank issues demand drafts, banker’s cheques, money orders etc.

for transferring the money. Bank also provides the facility of Telegraphic transfer or tele-

cash orders for quick transfer of money.

• A bank performs a trustworthy business for various purposes.

• A bank also provides the safe custody facility to the money and valuables of the general

public. Bank offers various types of deposit schemes for security of money. For keeping

valuables bank provides locker facility. The lockers are small compartments with dual

locking system built into strong cupboards. These are stored in the bank’s strong room and

are fully secured.

• Banks act on behalf of the Govt. to accept its tax and non-tax receipt. Most of the

government disbursements like pension payments and tax refunds also take place through

banks.

There are several types of banks, which differ in the number of services they provide and the

clientele (Customers) they serve. Although some of the differences between these types of

banks have lessened as they have begun to expand the range of products and\ services they

offer, there are still key distinguishing traits. These banks are as follows:

Commercial banks, which dominate this industry, offer a full range of services for

individuals, businesses, and governments. These banks come in a wide range of sizes, from

large global banks to regional and community banks.

Global banks are involved in international lending and foreign currency trading, in addition

to the more typical banking services.

Regional banks have numerous branches and automated teller machine (ATM) locations

throughout a multi-state area that provide banking services to individuals. Banks have

become more oriented toward marketing and sales. As a result, employees need to know

about all types of products and services offered by banks.

Community banks are based locally and offer more personal attention, which many

individuals and small businesses prefer. In recent years, online banks—which provide all

services entirely over the Internet—have entered the market, with some success.

14

However, many traditional banks have also expanded to offer online banking, and some

formerly Internet-only banks are opting to open branches.

Savings banks and savings and loan associations, sometimes called thrift institutions, are

the second largest group of depository institutions. They were first established as community-

based institutions to finance mortgages for people to buy homes and still cater mostly to the

savings and lending needs of individuals.

Credit unions are another kind of depository institution. Most credit unions are formed by

people with a common bond, such as those who work for the same company or belong to the

same labour union or church. Members pool their savings and, when they need money, they

may borrow from the credit union, often at a lower interest rate than that demanded by other

financial institutions.

Federal Reserve banks are Government agencies that perform many financial services for

the Government. Their chief responsibilities are to regulate the banking industry and to help

implement our Nation’s monetary policy so our economy can run more efficiently by

controlling the Nation’s money supply—the total quantity of money in the country, including

cash and bank deposits. For example, during slower periods of economic activity, the Federal

Reserve may purchase government securities from commercial banks, giving them more

money to lend, thus expanding the economy. Federal Reserve banks also perform a variety of

services for other banks. For example, they may make emergency loans to banks that are

short of cash, and clear checks that are drawn and paid out by different banks.

The money banks lend, comes primarily from deposits in checking and savings accounts,

certificates of deposit, money market accounts, and other deposit accounts that consumers

and businesses set up with the bank. These deposits often earn interest for their owners, and

accounts that offer checking, provide owners with an easy method for making payments

safely without using cash. Deposits in many banks are insured by the Federal Deposit

Insurance Corporation, which guarantees that depositors will get their money back, up to a

stated limit, if a bank should fail.

1.6 Types of Banks:-

Commercial banks operating in india can be categorized into two broad categories, public

sector and private sector.

[i] Public Sector Banks 4:- 4 http://en.wikipedia.org/wiki/History_of_banking

15

The public sector is the part of the economy concerned with providing various government

services. The composition of the public sector varies by country, but in most countries the

public sector includes such services as the military, police, public transit and care of public

roads, public education, along with healthcare and those working for the government itself,

such as elected officials. The public sector might provide services that a non-payer cannot be

excluded from (such as street lighting), services which benefit all of society rather than just

the individual who uses the service.

[ii] Private-sector banks 5:-

The private-sector banks in India represent part of the indian banking sector that is made

up of both private and public sector banks. The "private-sector banks" are banks where

greater parts of stake or equity are held by the private shareholders and not by government.

Banking in India has been dominated by public sector banks since the 1969 when all major

banks were nationalised by the Indian government. However since liberalisation in

government banking policy in the 1990s, old and new private sector banks have re-emerged.

They have grown faster & bigger over the two decades since liberalisation using the latest

technology, providing contemporary innovations and monetary tools and techniques.

The private sector banks are split into two groups by financial regulators in India, old and

new. The old private sector banks existed prior to the nationalization in 1969 and kept their

independence because they were either too small or specialist to be included in

nationalization. The new private sector banks are those that have gained their banking license

since the liberalization in the 1990s

5 http://www.ibef.org/industry/banking-india.aspx

16

Chapter 2 Major Players of Private Sector Banks

Sr.no Particulars Page.no

2.1 AXIS BANK 17

2.2 ICICI BANK 19

2.3 KOTAK MAHINDRA BANK 21

2.4 HDFC BANK 23

2.5 YES BANK 25

2.6 Dominant economic features 27

2.7 Challenges of private banking 30

17

Traded as

BSE: 532215

LSE: AXBC

NSE: AXISBANK

Industry Banking, Financial services

Founded 1994 (as UTI Bank)

Headquarters Mumbai, Maharashtra, India

Key people Dr.SanjivMishra(Chairman) Shikha Sharma (MD & CEO

Products Credit cards, consumer banking, corporate banking finance and

insurance,investment,banking, mortgage,loans, privatebanking, private

equity, wealth management

Revenue 340 billion (US$5.5 billion) (2012)

Operating income 94 billion (US$1.5 billion) (2012)

Net income 52 billion (US$840 million) (2012)

Total assets 3.4 trillion (US$55 billion) (2012)

Employees 42,420 (on 31-March-2014)

Website www.axisbank.com6

6 www.axisbank.com/

[1] AXIS BANK

18

[1] AXIS BANK :-

Axis Bank Limited (formerly UTI Bank) is the third largest private sector bank in India. It

offers financial services to customer segments covering Large and Mid-Corporates, MSME,

Agriculture and Retail Businesses. Axis Bank has its headquarters inMumbai, Maharashtra.

Axis Bank began its operations in 1994, after the Government of India allowed new private

banks to be established. The Bank was promoted in 1993 jointly by the Administrator of

the Unit Trust of India (UTI-I), Life Insurance Corporation of India (LIC), General Insurance

Corporation Ltd., National Insurance Company Ltd., The New India Assurance Company,

The Oriental Insurance Corporation and United India Insurance Company. The Unit Trust of

India holds a special position in the Indian capital markets and has promoted many leading

financial institutions in the country.

Axis Bank (erstwhile UTI Bank) opened its registered office in Ahmadabad and corporate

office in Mumbai in December 1993. The first branch was inaugurated on 2 April 1994

inAhmedabad by Dr. Manmohan Singh, the then Finance Minister of India.

In 2001 UTI Bank agreed to merge with and amalgamate Global Trust Bank, but the Reserve

Bank of India (RBI) withheld approval and nothing came of this. In 2004 the RBI put Global

Trust into moratorium and supervised its merger into Oriental Bank of Commerce.

UTI Bank opened its first overseas branch in 2006 Singapore. That same year it opened a

representative office in Shanghai, China.

UTI Bank opened a branch in the Dubai International Financial Centre in 2007. That same

year it began branch operations in Hong Kong. The next year it opened a representative office

in Dubai.

Axis Bank opened a branch in Colombo in October 2011, as a Licensed Commercial Bank

supervised by the Central Bank of Sri Lanka. Also in 2011, Axis Bank opened a

representative offices in Abu Dhabi.

In 2013, Axis Bank's subsidiary, Axis Bank UK commenced banking operations. Axis Bank

UK has a branch in London.

In 2014, Axis Bank upgraded its representative office in Shanghai to a branch.

19

Traded as BSE: 532174

NSE: ICICIBANK

NYSE: IBNBSE SENSEX Constituent

CNX Nifty Constituent

Industry Banking, Financial services

Founded 1994

Headquarters Mumbai, Maharashtra, India

Key people K. V. Kamath (Chairman) Ms.Chanda Kochhar (MD & CEO)

Products Credit cards, Consumer banking, corporatebanking, finance and

insurance,investment,banking, mortgage,loans, privatebanking, wealth

management

Revenue US$ 13.52 billion (2012)

Operating income US$ 2.12 billion (2012)

Net income US$ 1.60 billion (2012)

Total assets US$98.99 billion (2012)

Employees 81,254 (2012)

Website www.icicibank.com7

7 www.icicibank.com/

[2] ICICI BANK

20

[2] ICICI Bank:-

ICICI Bank is an Indian multinational banking and financial services company

headquartered in Mumbai, Maharashtra. As of 2014 it is the second largest bank in India in

terms of assets and market capitalization. It offers a wide range of banking products and

financial services for corporate and retail customers through a variety of delivery channels

and specialized subsidiaries in the areas of investment, life, non- life insurance, venture

capital and asset management. The Bank has a network of 3,820 branches and

11,162 ATMs in India, and has a presence in 19 countries.

ICICI Bank is one of the Big Four banks of India, along with State Bank of India, Punjab

National Bank and Bank of Baroda. The bank has subsidiaries in the United Kingdom,

Russia, and Canada; branches in United States, Singapore, Bahrain, Hong Kong, Sri Lanka,

Qatar and Dubai International Finance Centre; and representative offices in United Arab

Emirates, China, South Africa, Bangladesh, Thailand, Malaysia and Indonesia. The

company's UK subsidiary has also established branches in Belgium and Germany.

In March 2013, Operation Red Spider showed high-ranking officials and some employees of

ICICI Bank involved in money laundering. After a government inquiry, ICICI Bank

suspended 18 employees and faced penalties from the Reserve Bank of India in relation to the

activity.

ICICI Bank was established by the Industrial Credit and Investment Corporation of India

(ICICI), an Indian financial institution, as a wholly owned subsidiary in 1994. The parent

company was formed in 1955 as a joint-venture of the World Bank, India's public-sector

banks and public-sector insurance companies to provide project financing to Indian

industry. The bank was initially known as the Industrial Credit and Investment Corporation of

India Bank, before it changed its name to the abbreviated ICICI Bank. The parent company

was later merged with the bank.

ICICI Bank launched internet banking operations in 1998.

ICICI's shareholding in ICICI Bank was reduced to 46 percent, through a public offering of

shares in India in 1998, followed by an equity offering in the form of American Depositary

Receipts on the NYSE in 2000. ICICI Bank acquired the Bank of Madura Limited in an all-

stock deal in 2001 and sold additional stakes to institutional investors during 2001-02.

21

Traded as BSE: 500247

NSE: KOTAKBANK

Industry Financial service

Founded 1985 (as Kotak Mahindra Finance Ltd)

Headquarters Mumbai, Republic of India

Key people Uday Kotak (Founder & Executive Vice Chairman)

C. Jayaram (Joint MD)

Dipak Gupta (Joint MD)

Shankar Acharya (Chairman)

Products Deposit accounts, Loans,Investment services, Business banking

solutions, Treasury and Fixed income products etc.

Revenue 109.63 billion(US$1.8 billion)(2011)[1]

Net income 15.69 billion(US$250 million)(2011)

Website www.kotak.com8

8 www.kotak.com/

[3] KOTAK MAHINDRA BANK

22

[3] kotak Mahindra Bank:-

Kotak Mahindra Bank is the fourth largest Indian private sector bank by market

capitalization, headquartered in Mumbai, Maharashtra. The Bank’s registered office

(headquarter) is located at 27BKC, Bandra Kurla Complex, Bandra

East, Mumbai,Maharashtra, India.

In February 2003, Kotak Mahindra Finance Ltd, the group's flagship company was given the

licence to carry on banking business by the Reserve Bank of India (RBI). Kotak Mahindra

Finance Ltd. is the first company in the Indian banking history to convert to a bank.

As on June 30, 2014, Kotak Mahindra Bank has over 600 branches and over 1,100 ATMs

spread across 354 locations in the country.

Kotak Mahindra group, established in 1985 by Uday Kotak, is one of India’s leading

financial services conglomerates. In February 2003, Kotak Mahindra Finance Ltd. (KMFL),

the Group’s flagship company, received a banking license from the Reserve Bank of India

(RBI). With this, KMFL became the first non-banking finance company in India to be

converted into a bank – Kotak Mahindra Bank Limited (KMBL).

In a study by Brand Finance Banking 500, published in February 2014 by the Banker

magazine (from The Financial Times Stable), KMBL was ranked 245th among the world’s

top 500 banks with brand valuation of around half a billion dollars ($481 million) and brand

rating of AA+. KMBL is also ranked among the top 5 Best Ranked Companies for Corporate

Governance in IR Global Ranking.

23

9 www.hdfcbank.com/

"We understand your world"

Traded as BSE: 500180 NSE: HDFCBANK ,NYSE: HDB,BSE SENSEX Constituent CNX Nifty Constituent

Industry Banking, Financial services

Founded August 1994

Headquarters Mumbai, Maharashtra, India

Key people Aditya Puri (MD)

Products Credit cards, consumer banking, corporate banking,finance and insurance,investment banking, mortgage loans, private banking, private equity, wealth management

Revenue US$ 6.5 billion (March 2013)

Operating income US$ 1.87 billion (March 2013)

Net income US$ 1.1 billion (March 2013)

Total assets US$ 66.7 billion (May 2013)

Employees 69,065 (March 2013)

Website HDFCBank.com9

[4] HDFC BANK

24

[4] HDFC BANK:-

HDFC Bank Limited is an Indian banking and financial services company head quartered

in Mumbai, Maharashtra. It is the fifth largest bank in India by assets, incorporated in 1994. It

is the largest private sector bank in India by market capitalization as of 24 February 2014. As

on Jan 2 2014, the market cap value of HDFC was around US$26.88 billion, as compared

to Credit Suisse Group with US$47.63 billion. The bank was promoted by the Housing

Development Finance Corporation, a premier housing finance company (set up in 1977) of

India. According to the Brand Trust Report 2014, HDFC was ranked 32nd among India's

most trusted brands.

As of 31 March 2013, the bank had assets of INR 4.08 trillion. For the fiscal year 2012-13,

the bank has reported net profit of INR 69 billion, up 31% from the previous fiscal year. Its

customer base stood at 28.7 million customers on 31 March 2013.

As of 30 September 2013, HDFC Bank has 3,251 branches and 11,177 ATMs, in 2,022 cities

in India, and all branches of the bank are linked on an online real-time basis. The Bank has

overseas branch operations in Bahrain and Hong Kong.

HDFC Bank has two subsidiaries:

HDB Financial Services Limited (‘HDBFS’): HDBFS is engaged in retail asset financing. It

is a non-deposit taking non-bank finance company (NBFC). Apart from lending to

individuals, the company grants loans to micro, small and medium business enterprises. It

also runs call centers for collection services to the HDFC Bank’s retail loan products. HDFC

Bank holds 97.4% shares in HDBFS. As of March 31, 2013, HDBFS has 230 branches in 184

cities. During the FY 2012-13, HDBFS had turnover of INR 9.6 billion and profit after tax of

INR 1 billion. It has 6,404 employees as of 31 March 2013.

HDFC Securities Limited (‘HSL’): HSL is engaged in stock broking. As of March 31, 2013,

HDBFS has 194 branches across 150 cities. HDFC Bank has 62.1% shareholding in HSL.

During the FY 2012-13, HSL had turnover of INR 2.3 billion and profit after tax of INR 668

million. During the year, the Company received the “Best e-Brokerage Award - 2012” in the

Outlook Money Awards in the runner up category

25

Type Public company

Traded as BSE: 532648

NSE: YESBANK

Industry Banking & financial services

Founded 2004

Founders Rana Kapoor and Late Ashok Kapur

Headquarters Mumbai, India

Key people Rana Kapoor (Managing Director & CEO)[1]

Products

Corporate and Institutional Banking, Financial Markets, Investment

Banking, Corporate Finance, Retail Banking, Business and

Transaction Banking, and Wealth Management, NRI Banking,[2]

SMEs[3]

Revenue 99.8 billion (US$1.6 billion) (2013)[4]

Net income 11.7 billion (US$190 million) (2014)[4]

Total assets 603.6 billion (US$9.8 billion) (2014)[4]

Employees 8,798 (31-Mar-2014)[4]

Website www.yesbank. 10

10 www.yesbank.

[5] YES BANK

26

[5] YES BANK:-

YES BANK is a private bank in India with headquarters in Mumbai. It was founded in 2004

by promoters Ashok Kapur and Rana Kapoor, which had a collective shareholding of 29%.

Ashok Kapur was killed in a terrorist attack in 2008 in Mumbai. In 2010, the bank announced

the roll-out of a strategic blueprint, named Version 2.0 of the bank, to further accelerate its

business growth in the retail banking space, with the objective to achieve by 2015, a balance

sheet size of 1,500 billion, deposits of 1,250 billion, advances of 1,000 billion, a pan

India network of 900 branches and a human capital base of 12,750 by 2015

PRODUCT AND SERVICES:-

Corporate and Institutional Banking:

YES BANK deals in corporate investment services. This involves providing, for a fee,

financial advice to customers, generally corporate or individual investors.

Investment Banking:

YES BANK's Investment Banking division consists of domestic and cross-border Mergers

and Acquisitions, Joint Venture Advisory Services, Private Equity Placement as well as

Merchant Banking Services across select industry verticals.

Corporate Finance- YES BANK's Corporate Finance practice offers a combination of

advisory services and customised products to optimize risk based on "Knowledge Arbitrage"

Financial Marketing- The Financial Markets (FM) business model provides Risk

Management solutions related to foreign currency and interest rate exposures of clients.

Branch Banking:

• Business Banking: YES BANK is a major competitor in the business banking sector

of the Indian economy, especially amongst smaller- and medium-sized clients.

Business banking is centred primarily around Cash Handling, Payment, Direct

Banking, Liabilities and Investment, and Trade services.

• Retail Banking: Retail Banking is the general branch of banking, targeted at private

individuals. Customers are currently being handled by a branch network, composed of

over 550+ branches across the country with 1,139 ATMs, and Internet Banking

facilities

27

[1] Market size:-

The size of banking assets in Indiatotalled US$ 1.8 trillion in FY 13 and is expected to touch

US$ 28.5 trillion in FY 25.Bank deposits have grown at a compound annual growth rate

(CAGR) of 21.2 per cent over FY 06-13. In FY 13, total deposits were US$ 1,274.3 billion.

The revenue of Indian banks increased from US$ 11.8 billion to US$ 46.9 billion over the

period 2001-2010. Profit after tax also reached US$ 12 billion from US$ 1.4 billion in the

period.

Credit to housing sector grew at a CAGR of 11.1 per cent during the period FY 08-13. Total

banking sector credit is anticipated to grow at a CAGR of 18.1 per cent (in terms of INR) to

reach US$ 2.4 trillion by 2017. Share of private sector banks in India in total deposits have

increased to 18.8 per cent in FY13 from 17.1 per cent in FY05.

In FY 14, private sector lenders experienced significant growth in credit cards and personal

loan businesses. ICICI Bank saw 141.6 per cent growth in personal loan disbursement in FY

14, as per a report by Emkay Global Financial Services. The bank also experienced healthy

growth of 20.8 per cent in credit card dues, according to the report. Axis Bank's personal loan

business also grew 49.8 per cent, with its credit card business expanding by 31.1 per cent.

[2]Investments:-

HDFC Bank and state-owned United Bank of India plan to tap the equity markets to raise

funds to enhance capital base and lending. HDFC Bank plans to raise Rs 10,000 crore (US$

1.66 billion) while the board of Kolkata-based United Bank will seek approval for raising

about Rs 1,300 crore (US$ 216.47 million) by selling shares to increase its capital base.

Export-Import Bank of India (Exim Bank) will increase its focus on supporting project

exports from India to South Asia, Africa and Latin America, as per Mr Yaduvendra Mathur,

Chairman and MD, Exim Bank. The bank has moved up the value chain by supporting

project exports so that India earns foreign exchange. In 2012-13, Exim Bank had lent support

to 85 project export contracts valued at Rs 24,255 crore (US$ 4.03 billion) secured by 47

companies in 23 countries.

6. Dominant Economic Features

28

IndusInd Bank will soon begin its asset reconstruction business. The private-sector lender

plans to partner asset reconstruction companies (ARCs) for this venture. "I think our new

initiative, which is going to launch in the next two months, is about asset reconstruction. We

will do asset reconstruction within the bank but in tie-ups with ARCs. The business plan is

ready. We believe a huge stock of assets is coming into the ARCs as a business area that we

need to look at and we will exploit," as per Mr Romesh Sobti, CEO and MD, IndusInd Bank.

Jammu and Kashmir (J&K) Bank plans to increase its presence outside India. The bank is

looking to establish branches in London and Dubai to enhance its relationship with current

customers who have business interests in West Asia and Europe. "We have a number of

business relationships in these countries and it makes sense for us to have a presence there,"

as per Mr Mushtaq Ahmad, Chairman and CEO, J&K Bank.

[3] Government Initiatives:-

The RBI has announced a few measures in its bi-monthly monetary policy on June 3, 2014

which includes an increase in the foreign exchange remittance limit to US$ 125,000 from the

previous limit of US$ 75,000.

State Bank of India (SBI) has announced a one-year rural fellowship programme 'SBI Youth

for India (SBI YFI)' for 2014 to draft the country's youth to become change agents in the

country's rural regions. The programme is for young professionals who are keen to leadthe

change for a better India.

The RBI has simplified the rules for credit to exporters. Exporters can now receive long-term

advance credit from banks for up to 10 years to service their contracts. Exporters have to

have a satisfactory record of three years to receive payments from banks, who can adjust the

payments against future exports.

The RBI has enabled overseas investors, including foreign portfolio investors (FPIs) and non-

resident Indians (NRIs), to invest up to 26 per cent in insurance and related activities through

the automatic route.

29

[4]Road Ahead:-

India's banking industrycould become the fifth largest banking sector globally by 2020 and

the third largest by 2025. These days, banks in India are turning their focus to servicing

clients and improving their technology infrastructure, which can help better customer

experience and give them a competitive edge. The popularity of internet and mobile banking

is at an all-time high, with customer relationship management (CRM) and data warehousing

anticipatedto drive the next wave of banking technology in the country.

[5] Product Innovation:-

ATMs in India have increased to 126,950 in 2013.ATM is banking industries characterized

by rapid product innovation and short product life cycles11

11 . http://www.ibef.org/industry/banking-india.aspx

30

Challenges Ahead Developing or acquiring the right technology12, deploying it optimally and

then leveraging it to the maximum extent is essential to achieve and maintain high service

and efficiency standards while remaining cost effective and delivering sustainable return to

shareholders. Early adopters of technology acquire significant competitive advances.

Managing technology is therefore, a key challenge for the Indian banking sector.

Banks are restricting their administrative folio by converting manpower into machine power

i.e. banks are decreasing manual powers and getting maximum work done through machine

power. Skilled and specialized man power is to be utilized and result oriented targeted staff

will be appointed. In India, currently, there are two types of customers – one who is a multi-

channel user and the other who still relies on a branch as the anchor channel. The primary

challenge is to give consistent service to customers irrespective of the kind of channel they

choose to use. Retention of customers is going to be a major challenge.

Banks need to emphasis on retaining customers and increasing market share. Information

technology poses both opportunities and challenges. Even with ATM machines and Internet

Banking, many consumers still prefer the personal touch of their neighbourhood branch bank.

Technology has made it possible to deliver services throughout the branch bank network,

providing instant updates to checking accounts and rapid movement of money for stock

transfers. However, this dependency on the network has brought IT department’s additional

responsibilities and challenges in managing, maintaining and optimizing the performance of

retail banking networks. Illustratively, ensuring that all bank products and services are

available, at all times, and across the entire organization is essential for today’s retails banks

to generate revenues and remain competitive. Besides, there are network management

challenges, whereby keeping these complex, distributed networks and applications operating

properly in support of business objectives becomes essential. Specific challenges include

ensuring that account transaction applications run efficiently between the branch offices and

data centers. Banks in India will now have to work towards a vision to have an enhanced

12 Sunita Agrawal1 and Ankit Jain, “Technological advancement in banking sector in india: challenges ahead”Journal of Reasearch in Commerce & Management, Vol.No.2,

[7] Challenges of private banking

31

retail delivery system. Such a system would include transformed branches, enhanced

telephone services, and leading-edge internet banking functions that provide a consistently

positive multi-channel experience for the customer.

Some of the challenges 13that the banks are facing today are:

Changing needs of customers.

Coping with regulatory reforms.

Restructuring and reorganizing banks' setup towards thinner and leaner administrative

offices;

Closing down and/or merging of unviable branches particularly in urban and

metropolitan branches;

Thinning spread.

Maintaining high quality assets.

Management of impaired assets.

Keeping pace with technology up-gradations.

Sustaining healthy bottom lines and increasing shareholder value

The banking sector in India has undergone significant transformation in the past few years.

However, the numerous challenges faced by banks such as increasing competition, pressure

on spreads, and systemic changes to align with international standards have necessitated a re-

evaluation of strategies and processes in order to remain competitive in this dynamic

environment. As per the census records, only 30.1 per cent of the rural households are

availing banking services. One of the reasons may be non-availability of bank branches in the

neighbourhood. The new business environment thus puts a premium on creativity and

innovation more than ever before. This calls for innovative solutions. Banks may have to go

for mobile banking services for a cluster of villages. Alternatively, technological institutions

have to come out with low-cost, self-service solutions/ ATMs. The government and the RBI

should actively support such research efforts.

13 www.abhinavjournal.com

32

Chapter 3 Strategy Analysis

Sr.no Particulars Page.no

3.1 PEST ANALYSIS 33

3.2 STRATEGIC GROUP MAPPING 34

3.3 THE COMPETITIVE PROFILE MATRIX (CPM) 35

3.4 THE EXTERNAL FACTOR EVALUATION (EFE) 37

3.5 SWOT Analysis 38

3.6 Industry Analysis – Five Force Model 43

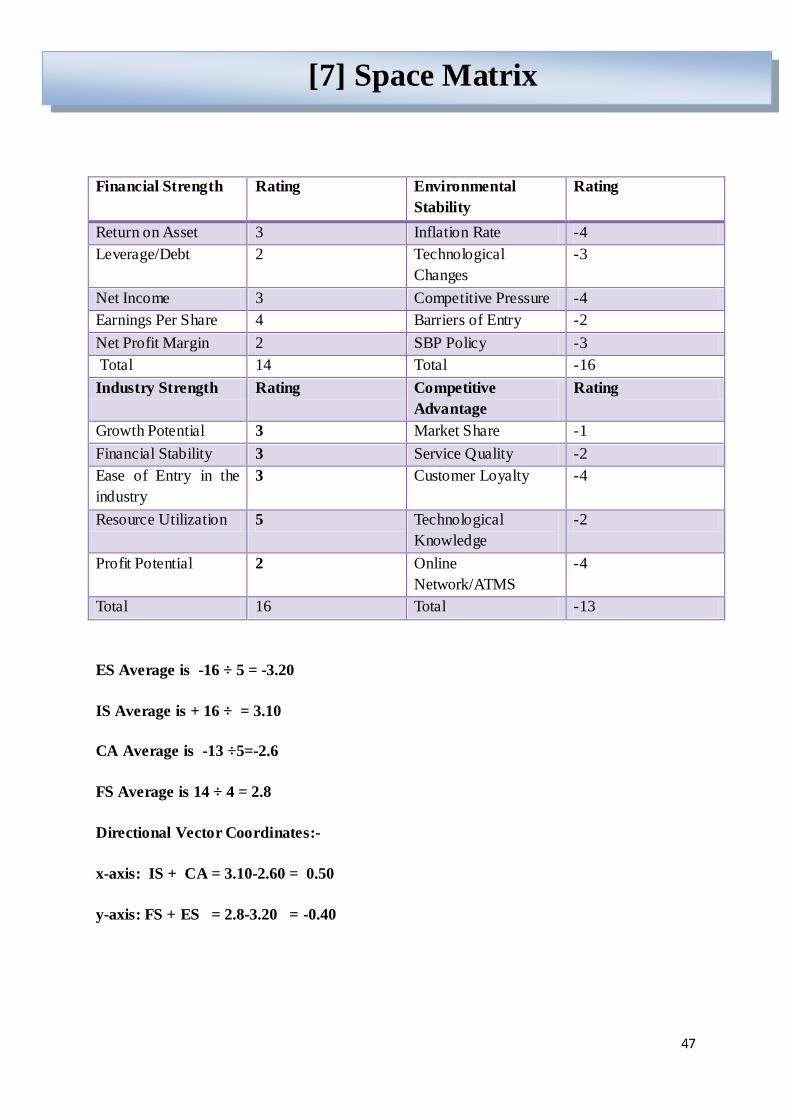

3.7 Space Matrix 47

33

3.1 PEST Analysis14:-

Political Aspect:-

Our private Bank has been confined by the regulation and policy formulated by different

government in the countries where they are operating. The company has been able to stick on

to policy given by each government to make sure that the company will be able to carry out

business operations successfully and effectively.

Economic Aspect:-

Our Private Bank is supposed to have steady and successful economic stabilize. In spite of

many dangers that they encounter in different part of the world, the management of Our

Private Bank sees to it that they would be able to surpass such struggles and strive to have a

better economic condition. The change in the Currency is also the economic factors to our

private bank.

Social Aspect:-

Our Private Bank will be affected by the situation of the society in which they are operating.

Along with this, Our Private Bank try harder to make sure that each society is given equal

chance to take advantage of the resources given by the organization. The company adhere to

having good reputation and relations in the society that they belong.

Technological Aspect:-

The emergence of information technology and internet affects how Our Private has been

operating in the past years. The company adopts different IT/IS systems and used internet to

reach their customer all over the world and to know the latest trends in the global business.

14 http://www.ukessays.com/essays/marketing/the-pest-analysis-for-private-bank-marketing-essay.php#ixzz3K5bexuC7

[1] PEST ANALYSIS

34

A strategic group consists of those industry members with similar competitive approaches

and positions in the market. Companies in the same strategy group can resemble one another

in any of several ways. They may have comparable profitability & efficiency

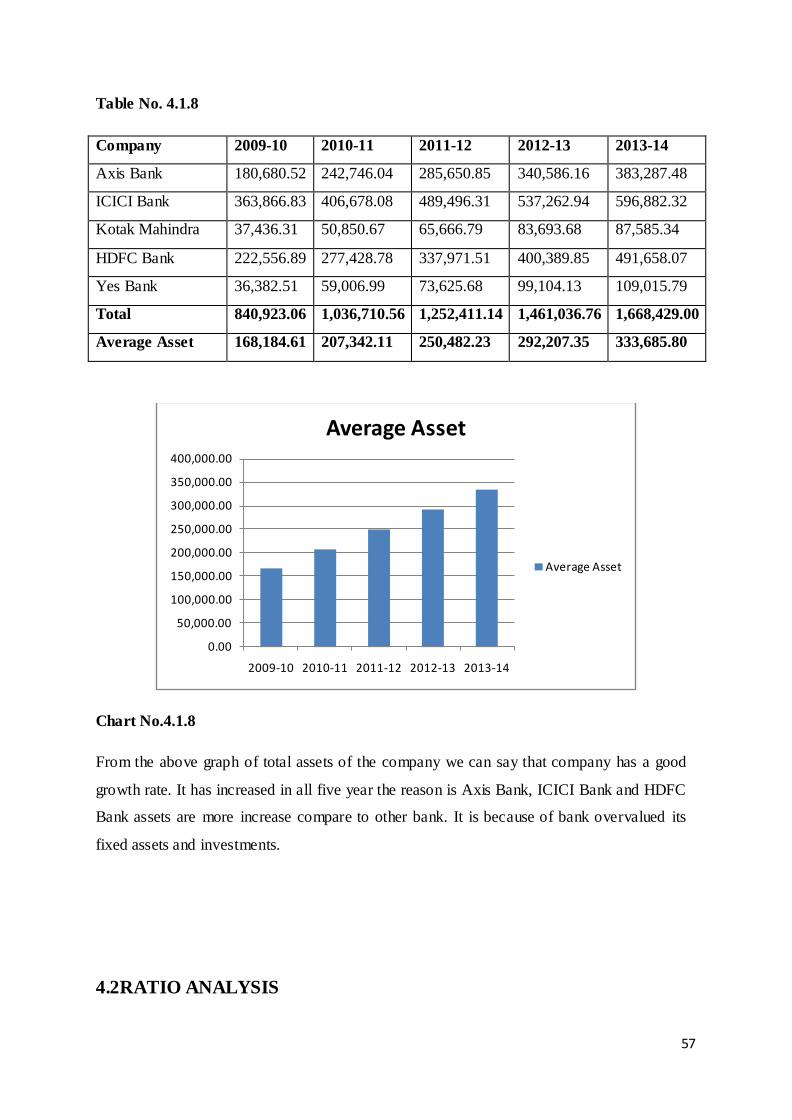

The above graph showing the group mapping of various company in banking industry. HDFC

BANK and KOTAK MAHINDRA bank are more competitor to each other the reason is

company return on assets and operating expenses to net profit value is nearest. The icici bank

company competitor is axis bank . So the group mapping helps to identify the nearest

competitor.

0.82

0.84

0.86

0.88

0.90

0.92

0.94

0.96

0.98

0 5 10 15 20 25 30

COMPANY PROFITABILITY [A]

EFFICIENCY [B]

[A] X[B] %

AXIS BANK 0.92 20.77 19.01 20.39 ICICI BANK 0.94 18.88 17.81 19.10 KOTAK MAHINDRA 0.83 25.01 20.88 22.40 HDFC BANK 0.86 24.55 21.14 22.68 YES BANK 0.96 14.95 14.37 15.41 TOTAL 93.20 100

[2] Strategic Group Mapping

PROFITABILI

EFFICIENC

ICICI BANK

YES BANK

HDFC BANK

AXIS BANK

KOTAK MAHINDRA

35

COMPETITORS HDFCBANK KOTAK

MAHINDRA

Critical Success

Factors

Weight Rate Score Rate Score

Financial Position 0.16 4 0.64 4 0.64

Service Quality 0.14 3 0.42 3 0.42

Market Share 0.09 4 0.36 2 0.18

Customer Loyalty 0.10 2 0.20 4 0.40

Bank charges/fees 0.12 2 0.24 4 0.48

Advertising and

Promotion

0.08 3 0.24 2 0.16

Work force

motivation

0.07 2 0.14 3 0.21

Online / ATM

Service

0.11 3 0.33 4 0.44

Geographic

Coverage

0.13 4 0.52 3 0.39

TOTAL 1.00 3.09 3.32

The Competitive Profile Matrix (CPM) :-

It is a tool that compares the firm and its rivals and reveals their relative strengths and

weaknesses.”

Understanding the tool :-

In order to better understand the external environment and the competition in a particular

industry, firms often use CPM. The matrix identifies a firm’s key competitors and compares

them using industry’s critical success factors. The analysis also reveals company’s relative

strengths and weaknesses against its competitors, so a company would know, which areas it

should improve and, which areas to protect.

[3]The Competitive Profile Matrix (CPM)

36

Weight

Each critical success factor should be assigned a weight ranging from 0.0 (low importance) to

1.0 (high importance). The number indicates how important the factor is in succeeding in the

industry. If there were no weights assigned, all factors would be equally important, which is

an impossible scenario in the real world. The sum of all the weights must equal 1.0. Separate

factors should not be given too much emphasis (assigning a weight of 0.3 or more) because

the success in an industry is rarely determined by one or few factors. In our project, the most

significant factors are Online ATM services (0.11), geographic coverage (0.13),service

quality(0.14), financial position(0.16 ).

Rating

The ratings in CPM refer to how well companies are doing in each area. They range from 4 to

1, where 4 means a major strength, 3 – minor strength, 2 – minor weakness and 1 – major

weakness. Ratings, as well as weights, are assigned subjectively to each company, but the

process can be done easier through benchmarking.

Score & Total Score

The score is the result of weight multiplied by rating. Each company receives a score on each

factor. Total score is simply the sum of all individual score for the company. The firm that

receives the highest total score is relatively stronger than its competitors. In our Project, the

strongest performer in the market is kotak mahindra (3.32 points) and its main competitor is

hdfc bank (3.09 points)

Benefits of the CPM:

• The same factors are used to compare the firms. This makes the comparison more

accurate.

• The analysis displays the information on a matrix, which makes it easy to compare the

companies visually.

• The results of the matrix facilitate decision-making. Companies can easily decide

which areas they should strengthen, protect or what strategies they should pur

37

Key Success Factors

Weight Rate Score

OPPORTUNITIES

Fragmented Market 0.12 4 0.48

Financial Leverage 0.11 3 0.33

Online Market 0.16 2 0.32

Innovation 0.07 4 0.28

New Services 0.05 4 0.20

New Technology 0.07 2 0.14

THREATS

Bad Economy 0.11 1 0.11

Volatile Currencies 0.08 2 0.16

International competitors 0.04 1 0.04

Mature Markets 0.07 2 0.14

Intense Competition 0.06 2 0.12

Govt Regulations 0.06 1 0.06

TOTAL 1.00 3.09

EFE Matrix Score of is 2.66 which is higher than the bench mark of 2.50

[4]The External Factor Evaluation (EFE)

38

SWOT analysis is a simple framework for generating strategic alternatives from a situation

analysis. It is a strategic planning method used to evaluate the Strengths, Weaknesses,

Opportunities, and Threats involved in a project or in a business venture. It involves

specifying the objective of the business venture or project and identifying the internal and

external factors that are favorable and unfavorable to achieving that objective.

The following diagram shows how a SWOT analysis fits into an environmental scan.

Situation Analysis

/ \

Internal Analysis External Analysis

/ \ / \

Strengths Weaknesses Opportunities Threats

Strengths Weaknesses [1] Strong Management [2] Real Estate [3] Pricing Power [4] Innovative Culture [5] Financial Leverage [6]Unique Products [7]Asset Leverage

[1] work inefficient [2]High Debt Burden [3] Outdated Technology [4]High Staff Turnover [5]Online Presence [6]Weak Supply Chain [7]Tarnished Reputation [8] Bad Acquisitions

Opportunities Threats [1]Fragmented Market [2]Financial Leverage [3]Online Market [4]Innovation [5]New Services [6]New Technology

[1]Bad Economy [2]Volatile Currencies [3]International competitor [4]Mature Markets [5]Intense Competition [6]Govt Regulations [7]Change in Tastes

[5] SWOT Analysis

39

[A]Strengths:-

[1] Strong Management:-

Strong management can help “private bank” reach its potential by utilizing strengths and

eliminating weakness. "Strong Management (Private Bank)" will have a long-term positive

impact on the this entity, which adds to its value. This qualitative factor will lead to a

decrease in costs. "Strong Management (Private Bank)" is a difficult qualitative factor to

defend, so competing institutions will have an easy time overcoming it

[2] Real Estate:-

Having the right real estate is essential to Private bank. Location matters, because it helps

consumers to utilize Private bank ’s offerings

[3]Pricing Power:

Customers typically rebel against price increases by switching to competing products, but if a

company has pricing power, customers will continue using Private bank’s products and

services. Private bank has the ability to charge customers higher prices."Pricing Power

(Private Bank ) has a significant impact, so an analyst should put more weight into it. "Pricing

Power (Private Bank ) will have a long-term positive impact on the this entity, which adds to

its value. This statements will have a short-term positive impact on this entity, which adds to

its value.

[4]Innovative Culture:-

An innovative culture helps Private bank to produce unique products and services that meet

their customer’s needs.

[5]Financial Leverage:-

Financial leverage allows Private bank to use their balance sheet to expand their business

and increase their profits.

[6] Unique Product:-

Unique products help distinguish Private bank from competitors. Private bank can charge

higher prices for their products, because consumers can’t get those products elsewhere.

40

[7]Assets Leverage

Asset leverage allows Private bank to use their best operational assets to expand their

business and improve their market share.

[8] Supply Chain:-

A strong supply chain helps Private bank obtain the right resources from suppliers and

delivery the right product to customers in a timely manner.

[B]Weaknesses:- [1] Work Inefficient:-

An inefficient work environment means that Private bank’s goods and services are not being

utilized properly.

[2] High Debt Burden:-

A high debt burden increases the risk that Private bank goes bankrupt if they make a poor

business decision. Increasing risks can increase Private bank ’s debt interest payments.

[3] Outdated Technology:-

A lack of proprietary technology and patents can hurt Private bank ’s ability to compete

against rivals.

[4] High Staff Turnover:-

High staff turnover can hurt Private bank ’s ability to compete, because replacing valuable

staff is expenses.

[5] Online Presence:-

The online market is essential for displaying information and selling products. A weak online

presence can result in lost opportunities for Private bank.

[6] Weak Supply Chain:-

A weak supply chain can delay the arrival of products to Private bank’s customers.

Unnecessary delays can hurt Private bank over the long run, because customers will cancel

orders.

41

[7] Tarnished Reputation:-

A tarnished reputation can hurt Private bank’s brand in the eyes of a consumer.

[8] Bad Acquisitions:-

Bad acquisition can hurt Private bank by increasing their costs and reducing the value of their

combined businesses. Acquisitions can also distract from the core business and merge

cultures that don’t complement each other.

[C]Opportunities:-

[1] Fragmented Market:-

Fragmented markets provide many opportunities for Private bank to expand and increase

market share. Fragmented markets have many small competitive who lack the cost

advantages of larger companies.

[2] Financial Leverage:-

Leveraging the balance sheet allows Private bank to quickly expand into other markets and

products, especially in fragmented industries.

[3] Online Market:-

The online market offers Private bank the ability to greatly expand their business. Private

bank can market to a much wider audience for relatively little expense.

[4] Innovation:-

Greater innovation can help Private bank to produce unique products and services that meet

customer’s needs.

[5] New Services:-

New services help Private bank to better meet their customer’s needs. These services can

expand Private bank’s business and diversify their customer base…

42

[6] New Technology:-

New technology helps Private bank to better meet their customer’s needs with new and

improved products and services. Technology also builds competitive barriers against rivals.

[4]Threats:- [1]Bad Economy:-

A bad economy can hurt Private bank’s business by decreasing the number of potential

customers…

[2]Volatile Currencies:-

Volatile currencies make Private bank’s investments difficult, because costs and revenues

change so rapidly

[3] International competitors:-

International competitors are numerous and difficult to combat, because they can have many

competitive advantages that give them an advantage over Private bank.

[4] Mature Markets:-