MACQUARIE GROUP MANAGEMENT DISCUSSION … · presentation and to reflect the ... not intended to be...

88

MACQUARIE GROUP LIMITED ACN 122 169 279 MACQUARIE GROUP MANAGEMENT DISCUSSION AND ANALYSIS YEAR ENDED 31 MARCH 2011

Transcript of MACQUARIE GROUP MANAGEMENT DISCUSSION … · presentation and to reflect the ... not intended to be...

MA

CQ

UA

RIE

GR

OU

P M

AN

AG

EM

EN

T DIS

CU

SS

ION

AN

D A

NA

LYS

IS

MACqUArIE GrOUP LIMITED ACN 122 169 279macquarie.com.au

MACQUARIE GROUP MANAGEMENT DISCUSSION AND ANALYSISYEAR ENDED 31 MARCH 2011

Macquarie Group Head OfficeNo.1 Martin PlaceSydney NSW 2000Australia

Tel: +61 2 8232 3333

Registered OfficeMacquarie Group LimitedLevel 7, No.1 Martin PlaceSydney NSW 2000Australia

Tel: +61 2 8232 3333Fax: +61 2 8232 4330

Des

igne

d by

Fro

st*D

esig

n

Prin

t m

anag

emen

t by

Oct

opus

Sol

utio

ns

The Holey DollarIn 1813 Governor Lachlan Macquarie overcame an acute currency shortage by purchasing Spanish silver dollars (then worth five shillings), punching the centres out and creating two new coins – the ‘Holey Dollar’ (valued at five shillings) and the ‘Dump’ (valued at one shilling and three pence).

This single move not only doubled the number of coins in circulation but increased their worth by 25 per cent and prevented the coins leaving the colony. Governor Macquarie’s creation of the Holey Dollar was an inspired solution to a difficult problem and for this reason it was chosen as the symbol for Macquarie Group.

The Macquarie name and Holey Dollar device are registered trade marks of Macquarie Group Limited.

Macquarie Group Limited Management Discussion and Analysis macquarie.com.au

Contents

1

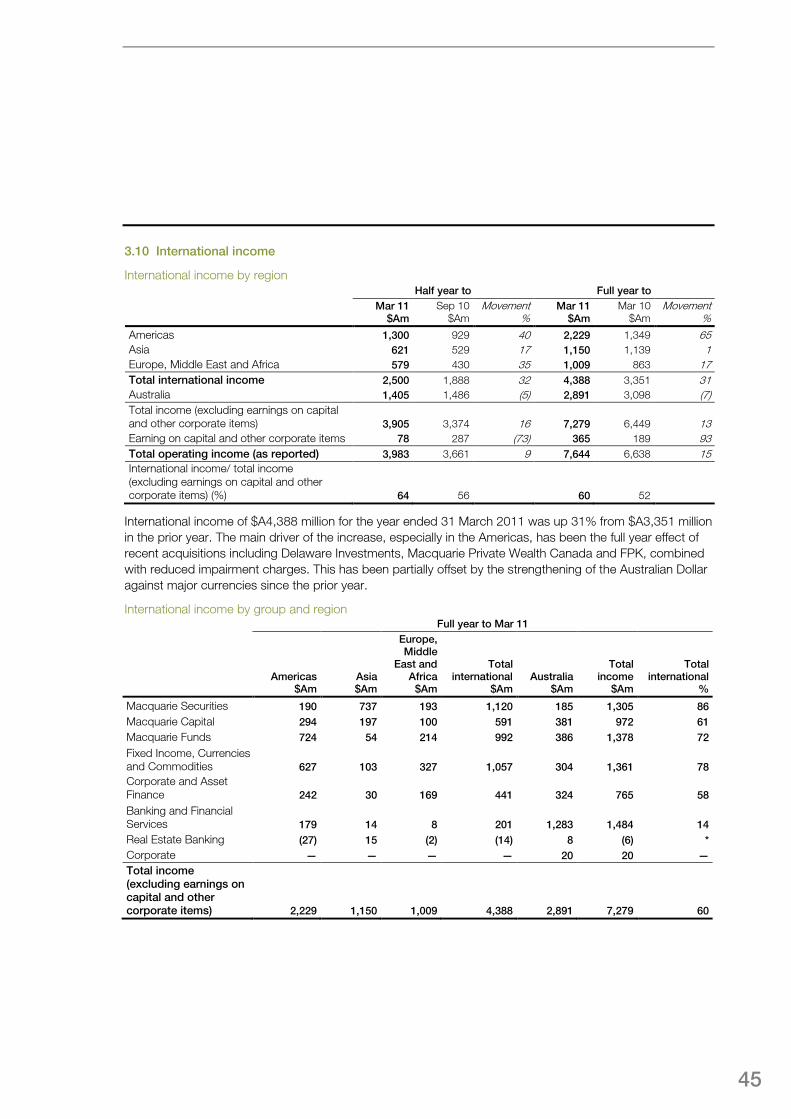

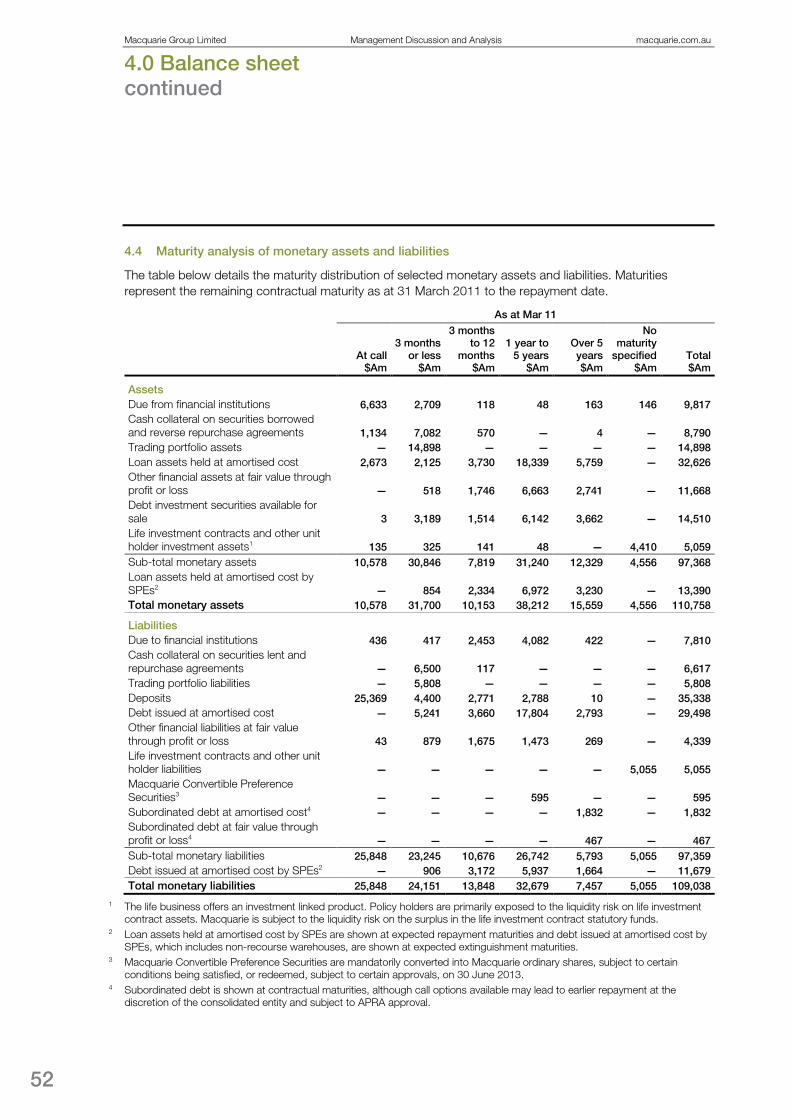

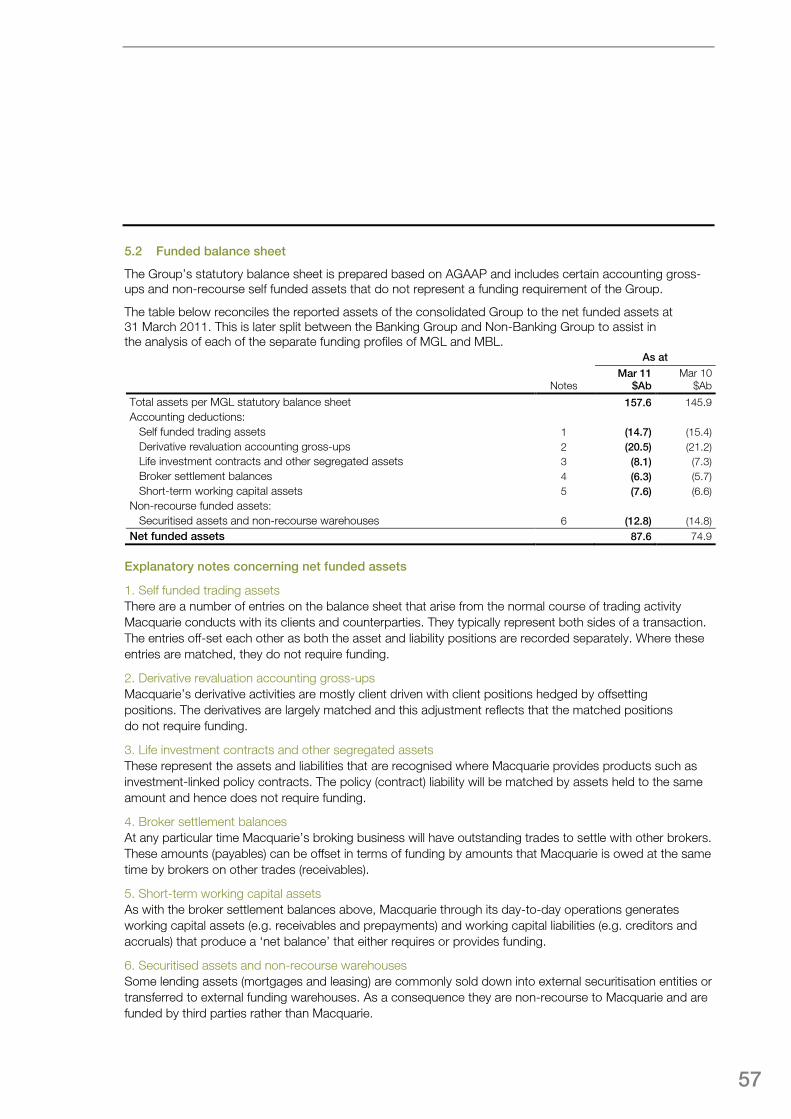

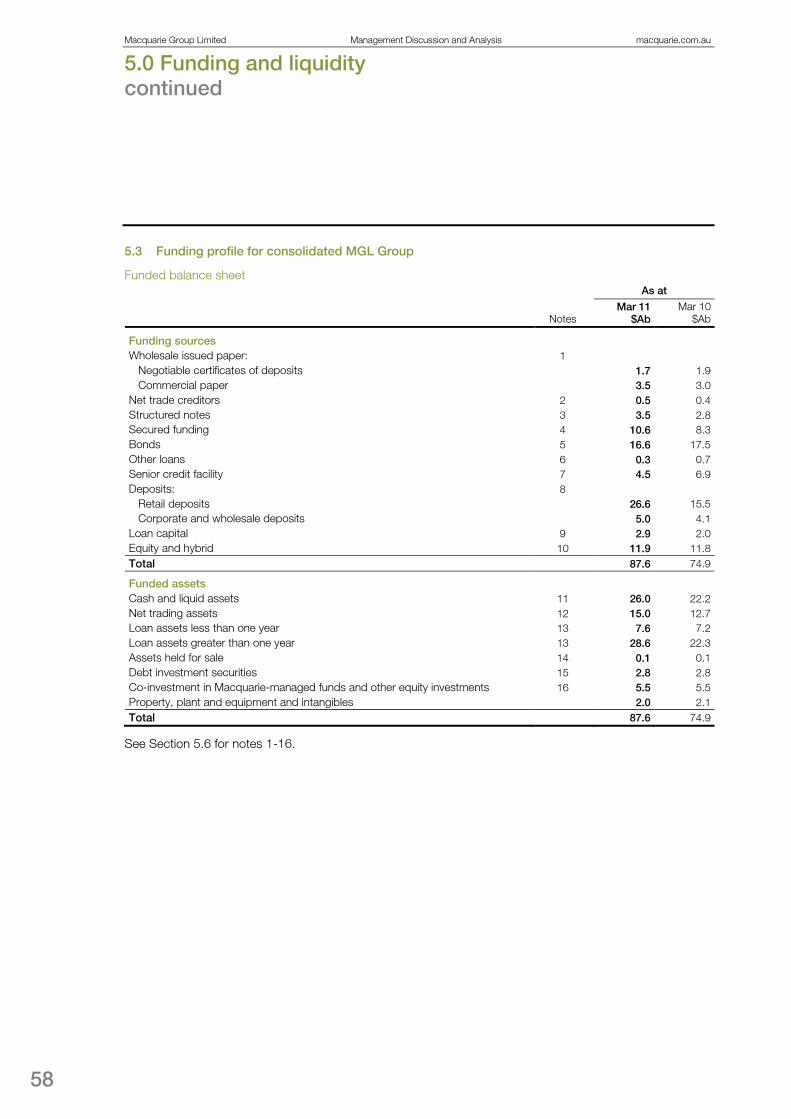

1.0 Result overview 3 1.1 Result overview 3 2.0 Income statement analysis 5 2.1 Net interest income 5 2.2 Fee and commission income 7 2.3 Net trading income 10 2.4 Share of net profits/(losses) of associates and joint ventures 12 2.5 Other operating income and charges 13 2.6 Operating expenses 15 2.7 Headcount 16 2.8 Income tax expense 17 3.0 Segment analysis 18 3.1 Basis of preparation 18 3.2 Macquarie Securities 24 3.3 Macquarie Capital 26 3.4 Macquarie Funds 30 3.5 Fixed Income, Currencies and Commodities 33 3.6 Corporate and Asset Finance 36 3.7 Banking and Financial Services 38 3.8 Real Estate Banking 41 3.9 Corporate 43 3.10 International income 45 4.0 Balance sheet 46 4.1 Statutory consolidated balance sheet 46 4.2 Loan assets 49 4.3 Equity investments 50 4.4 Maturity analysis of monetary assets and liabilities 52 5.0 Funding and liquidity 53 5.1 Overview 53 5.2 Funded balance sheet 57 5.3 Funding profile for consolidated MGL Group 58 5.4 Funding profile for Banking Group 61 5.5 Funding profile for Non-Banking Group 65 5.6 Explanatory notes concerning funding sources and funded assets 68 6.0 Capital 69 6.1 Overview 69 6.2 Banking Group capital 70 6.3 Non-Banking Group capital 73 7.0 Funds management 75 7.1 Assets under Management 75 7.2 Equity under Management 76 8.0 Glossary 77 9.0 Ten year history 82

Macquarie Group Limited Management Discussion and Analysis macquarie.com.au

2

Notice to readers

Date of this report

This report has been prepared for the year ended 31 March 2011 and is current as at 29 April 2011.

Comparative information and conventions

Where necessary, comparative figures have been restated to conform with changes in current year financial presentation and to reflect the effect of group restructures.

References to the prior year are to the 12 months ended 31 March 2010.

References to the first half are to the six months ended 30 September 2010.

References to the second half are to the six months ended 31 March 2011.

In the financial tables throughout this document “*” indicates that the percentage change in the balance was not meaningful, including instances where the absolute percentage movement was greater than 300% or where the result was a gain in one period but a loss in another, or vice versa.

Independent auditor’s report

This document should be read in conjunction with the Macquarie Group Limited Financial Report for the year ended 31 March 2011, which was subject to independent audit by PricewaterhouseCoopers.

PricewaterhouseCoopers’ Independent Auditor’s report to the members of Macquarie Group Limited dated 29 April 2011 was unqualified.

Disclaimer

The material in this update has been prepared by Macquarie Group Limited ABN 94 122 169 279 (“Macquarie”) and is current at the date of this update. The material in this update is general background information about Macquarie’s activities, is given in summary form and does not purport to be complete. It is not intended to be relied upon as advice to investors or potential investors and does not take into account the investment objectives, financial situation or needs of any particular investor. These should be considered, with or without professional advice, when deciding if an investment is appropriate.

Macquarie Group Limited Management Discussion and Analysis macquarie.com.au

1.0 Result overview

3

1.1 Result overview

Half year to Full year to

Mar 11 $Am

Sep 10 $Am

Movement %

Mar 11 $Am

Mar 10 $Am

Movement %

Income statement

Net interest income 670 605 11 1,275 1,080 18 Fee and commission income 1,896 1,995 (5) 3,891 3,721 5 Net trading income 762 606 26 1,368 1,299 5 Share of net profits/(losses) of associates and joint ventures accounted for using the equity method 94 85 11 179 (230) * Other operating income and charges 561 370 52 931 768 21 Net operating income 3,983 3,661 9 7,644 6,638 15 Employment expenses (1,994) (1,896) 5 (3,890) (3,101) 25 Brokerage and commission expenses (344) (441) (22) (785) (645) 22 Occupancy expenses (246) (237) 4 (483) (482) <1 Non-salary technology expenses (157) (159) (1) (316) (283) 12 Other operating expenses (467) (432) 8 (899) (833) 8 Total operating expenses (3,208) (3,165) 1 (6,373) (5,344) 19 Operating profit before income tax 775 496 56 1,271 1,294 (2) Income tax expense (197) (85) 132 (282) (201) 40 Profit after income tax 578 411 41 989 1,093 (10) Profit attributable to non-controlling interests (25) (8) 213 (33) (43) (23) Profit attributable to ordinary equity holders of Macquarie Group Limited 553 403 37 956 1,050 (9)

Key metrics

Expense to income ratio (%) 80.5 86.5 83.4 80.5 Compensation ratio (%) 46.6 47.9 47.3 42.9 Effective tax rate (%) 26.3 17.4 22.8 16.1 Basic earnings per share (cents per share) 163.3 119.2 282.5 320.2 Diluted earnings per share (cents per share) 158.5 117.1 275.9 317.4 Dividends per share (cents per share) 100.0 86.0 186.0 186.0 Dividend payout ratio (%) 62.7 73.4 67.3 60.4 Annualised return on equity (%) 10.2 7.4 8.8 10.1

Profit attributable to ordinary equity holders of $A956 million for the year ended 31 March 2011 decreased 9% from $A1,050 million in the prior year. Net profit for the second half of the year of $A553 million increased 37% from $A403 million in the six months to 30 September 2010. Recently acquired businesses, including Sal. Oppenheim, Macquarie Private Wealth Canada and Delaware Investments, contributed to increases in both operating income and operating expenses.

Macquarie Group Limited Management Discussion and Analysis macquarie.com.au

1.0 Result overview continued

4

Net operating income of $A7,644 million for the year ended 31 March 2011 increased 15% from $A6,638 million in the prior year. The main drivers of this increase were:

– an 18% increase in net interest income to $A1,275 million for the year ended 31 March 2011 from $A1,080 million in the prior year driven by an increase in corporate lending volumes, recent acquisitions of leasing portfolios and improved margins;

– equity accounted income from investments in associates and joint ventures of $A179 million for the year ended 31 March 2011, up from a net loss of $A230 million in the prior year driven by an improvement in the underlying results of investments. In addition, the prior year included equity accounted losses of $A82 million relating to fees paid by MAp Group, Southern Cross Media Group and Macquarie Infrastructure Group to terminate management agreements with Macquarie; and

– a 21% increase in other operating income to $A931 million for the year ended 31 March 2011 from $A768 million in the prior year driven by a 76% increase in net operating lease income from $A138 million in the prior year to $A243 million for the year ended 31 March 2011 and a significant increase in dividends/distributions received/receivable on investment securities available for sale from $A22 million in the prior year to $A126 million for the year ended 31 March 2011. In addition, there was a significant reduction in write-downs and impairment charges from a net expense of $A686 million for the prior year to a net expense of $A258 million for the year ended 31 March 2011.

Total operating expenses of $A6,373 million for the year ended 31 March 2011 increased 19% from $A5,344 million in the prior year. The increase was largely driven by:

– a 25% increase in employment expenses to $A3,890 million for the year ended 31 March 2011 from $A3,101 million in the prior year, which was due to the full year impact of acquisitions that contributed to a 17% increase in average headcount. The increase in employment expenses resulted in a compensation ratio of 47.3% for the year ended 31 March 2011, up from 42.9% in the prior year; and

– a 22% increase in brokerage and commission expenses to $A785 million from $A645 million in the prior year mainly due to the full year contribution of Delaware Investments.

Income tax expense for the year ended 31 March 2011 of $A282 million increased 40% from $A201 million in the prior year mainly as a result of reduced levels of writedowns and impairment charges. The effective tax rate of 22.8% for the year ended 31 March 2011 increased from 16.1% in the prior year.

2.0 Income statement analysis

5

2.1 Net interest income

Half year to Full year to Mar 11

$Am Sep 10

$Am Movement

% Mar 11

$Am Mar 10

$Am Movement

%

Interest revenue 2,667 2,637 1 5,304 4,591 16 Interest expense (1,997) (2,032) (2) (4,029) (3,511) 15 Net interest income (as reported) 670 605 11 1,275 1,080 18 Adjustment for accounting for swaps1 (41) (4) * (45) (117) (62) Adjusted net interest income 629 601 5 1,230 963 28

1 Australian Accounting Standards require derivatives hedging interest rate risk to be carried at fair value through trading income unless they form part of a qualifying hedge relationship. This distorts the analysis of net interest income and trading income in each operating group. To assist in the analysis of net interest margins, the impact of accounting for swaps used to economically hedge interest rate risk that is included in trading income for statutory purposes, has been adjusted against net interest income above.

Adjusted net interest income was $A1,230 million for the year ended 31 March 2011, up 28% from $A963 million in the prior year. The main drivers of the increase were improved margins and continued growth of the lending and finance leasing portfolio, including the acquisition of the GMAC portfolio in April 2010, and the full year impact of the acquisition of the Ford Credit portfolio in October 2009.

The table below provides further details of adjusted net interest income.

Analysis of net interest margins

Full year to Mar 11 Full year to Mar 10

Interest $Am

Average volume

$Am

Average spread

% Interest

$Am

Average volume

$Am

Average spread

% Mortgages 188 21,766 0.86% 183 22,399 0.82% Other lending areas 929 25,299 3.67% 680 23,113 2.94% Total net interest margin from interest bearing assets 1,117 47,065 2.37% 863 45,512 1.90% Other net interest income 113 100 Adjusted net interest income 1,230 963

Macquarie Group Limited Management Discussion and Analysis macquarie.com.au

2.0 Income statement analysis continued

6

Mortgages

Net interest income from mortgage assets of $A188 million is up 3% from $A183 million in the prior year. Average margins increased from 82 basis points in the prior year to 86 basis points in the year ended 31 March 2011. The impact of increased margins was partially offset by a reduction in average mortgage volumes which decreased 3% from $A22.4 billion at 31 March 2010 to $A21.8 billion at 31 March 20111

Other lending areas

resulting from run-off of the Australian residential mortgage portfolio and the impact of the stronger Australian Dollar on the Canadian mortgage portfolio.

Net interest income from other lending areas increased 37% from $A680 million in the prior year to $A929 million in the year ended 31 March 2011 largely as a result of average margins increasing from 294 basis points in the prior year to 367 basis points in the year ended 31 March 2011. This was largely due to a change in the product mix, including an increase in higher yielding loans and finance leases within Corporate and Asset Finance. Overall, average volumes have increased 9% to $A25.3 billion at 31 March 2011 from $A23.1 billion in the prior year. The growth in the Corporate and Asset Finance loan and finance lease portfolio, including the acquisition of the GMAC portfolio in April 2010, has been partially offset by a decrease in real estate loans and structured finance loans.

Other net interest income

Other net interest income includes earnings on capital offset by costs associated with excess liquidity and the funding cost of non-interest bearing assets. Other net interest income of $A113 million for the year ended 31 March 2011 increased 13% from $A100 million in the prior year. The movement was mainly due to an increased earnings base and a decrease in the Government guarantee fee resulting from reduced deposits subject to the guarantee. This was partially offset by the increase in the cost of funding non-interest bearing assets.

1 At 31 March 2011 $A8.8 billion (31 March 2010: $A11.2 billion) of the Australian mortgage portfolio was funded by third parties through external securitisations.

7

2.2 Fee and commission income

Half year to Full year to Mar 11

$Am Sep 10

$Am Movement

% Mar 11

$Am Mar 10

$Am Movement

%

Base fees 454 496 (8) 950 926 3 Performance fees 21 15 40 36 57 (37) Mergers and acquisitions, advisory and underwriting fees 529 402 32 931 1,085 (14) Brokerage and commissions 555 582 (5) 1,137 1,077 6 Other fee and commission income 300 454 (34) 754 532 42 Income from life investment contracts and other unit holder investment assets 37 46 (20) 83 44 89 Total fee and commission income 1,896 1,995 (5) 3,891 3,721 5

Total fee and commission income of $A3,891 million for the year ended 31 March 2011 increased 5% from $A3,721 million in the prior year largely due to the full year contribution of Delaware Investments to base fees and other fee and commission income.

Base and performance fees

Base fees of $A950 million for the year ended 31 March 2011 increased 3% from $A926 million in the prior year. This increase was driven by the full year impact of the acquisition of Delaware Investments, which increased Assets under Management (AUM) by $A151 billion in January 2010, reduced by the impact of the conversion of Cash Management Trust (CMT) to Cash Management Accounts (CMA) in July 2010, decreasing AUM by $A9.6 billion; the internalisation of certain Macquarie Infrastructure and Real Assets (MIRA) funds in the prior year; and the adverse impact of a stronger Australian Dollar on AUM denominated in foreign currencies. For further details of Assets under Management refer to Section 7.1.

Performance fees of $A36 million for the year ended 31 March 2011 decreased 37% from $A57 million in the prior year. The prior year included $A34 million from the sale of the Kukdong building by Macquarie Central Office CR-REIT.

Macquarie Group Limited Management Discussion and Analysis macquarie.com.au

2.0 Income statement analysis continued

8

The table below provides more detail on base and performance fees. Refer to Section 3 for a discussion of base and performance fees by operating group.

Half year to Full year to Mar 11

$Am Sep 10

$Am Movement

% Mar 11

$Am Mar 10

$Am Movement

%

Base fees Macquarie Funds Macquarie Investment Management 252 250 1 502 210 139 Macquarie Infrastructure and Real Assets 170 181 (6) 351 463 (24) Macquarie Specialist Investment Solutions 10 10 — 20 24 (17) Total Macquarie Funds 432 441 (2) 873 697 25 Other Operating Groups 22 55 (60) 77 229 (66) Total base fee income 454 496 (8) 950 926 3

Performance fees Macquarie Funds Macquarie Investment Management 11 7 57 18 9 100 Macquarie Infrastructure and Real Assets 4 8 (50) 12 12 — Macquarie Specialist Investment Solutions — — * — 1 (100) Total Macquarie Funds 15 15 — 30 22 36 Other Operating Groups 6 — * 6 35 (83) Total performance fee income 21 15 40 36 57 (37)

9

Mergers and acquisitions, advisory and underwriting fees

Mergers and acquisitions, advisory and underwriting fees of $A931 million for the year ended 31 March 2011 decreased 14% from $A1,085 million in the prior year reflecting lower levels of activity, especially in equity capital markets. Refer to Section 3.3 Macquarie Capital for details of significant transactions for the year ended 31 March 2011.

Brokerage and commissions

Brokerage and commissions income of $A1,137 million for the year ended 31 March 2011 increased 6% from $A1,077 million in the prior year mainly due to the acquisition by Banking and Financial Services of Macquarie Private Wealth Canada in December 2009, improving market conditions globally and increased brokerage revenues in the Fixed Income, Currencies and Commodities (FICC) futures execution and clearing markets.

Brokerage and commissions income from Macquarie Securities was broadly in line with the prior year. The Americas and Europe continued to grow, benefiting from recent acquisitions including Sal. Oppenheim in April 2010 and Fox-Pitt Kelton Group (FPK) in November 2009. This was offset by lower commissions in Asia and Australia due to reduced client activity as well as Asian revenues being negatively impacted by the stronger Australian Dollar.

Other fee and commission income

Other fee and commission income of $A754 million for the year ended 31 March 2011 increased 42% from $A532 million in the prior year. This increase was mainly due to distribution service fees in the Delaware Investments business, which offset with associated expenses that, for accounting purposes, are recognised in brokerage and commissions expense.

There has also been an increase in platform fees from higher average Wrap Funds under Administration compared to the prior year and the growth of the Macquarie Professional Series. The average Australian Wrap platform volumes during the year ended 31 March 2011 increased 6% on the prior year and Funds under Administration in the Macquarie Professional Series grew by 28%.

Income from life investment contracts and other unit holder investment assets

Income from life investment contracts and other unit holder investment assets of $A83 million for the year ended 31 March 2011 increased 89% from $A44 million in the prior year largely as a result of growth in the insurance inforce book. The inforce book is the aggregate annualised life insurance premium payable for policies issued by the life company, and still paying premiums, at the balance date.

Macquarie Group Limited Management Discussion and Analysis macquarie.com.au

2.0 Income statement analysis continued

10

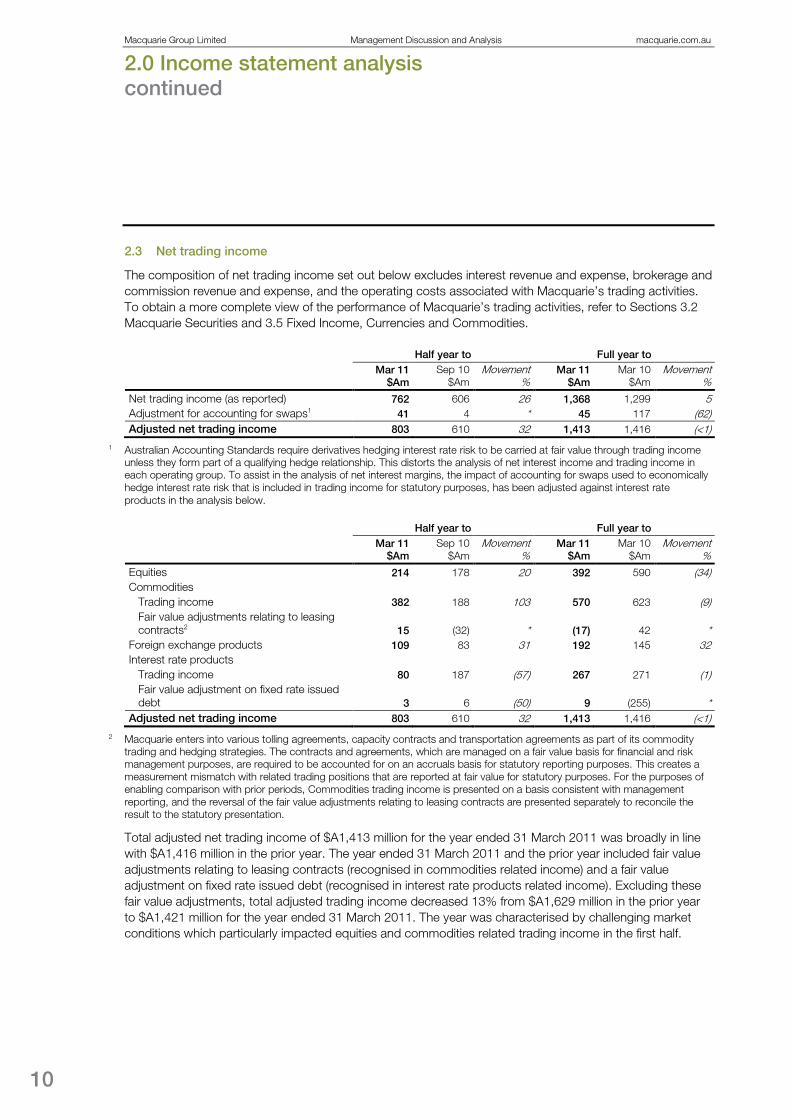

2.3 Net trading income

The composition of net trading income set out below excludes interest revenue and expense, brokerage and commission revenue and expense, and the operating costs associated with Macquarie’s trading activities. To obtain a more complete view of the performance of Macquarie’s trading activities, refer to Sections 3.2 Macquarie Securities and 3.5 Fixed Income, Currencies and Commodities.

Half year to Full year to Mar 11

$Am Sep 10

$Am Movement

% Mar 11

$Am Mar 10

$Am Movement

%

Net trading income (as reported) 762 606 26 1,368 1,299 5 Adjustment for accounting for swaps1 41 4 * 45 117 (62) Adjusted net trading income 803 610 32 1,413 1,416 (<1)

1 Australian Accounting Standards require derivatives hedging interest rate risk to be carried at fair value through trading income unless they form part of a qualifying hedge relationship. This distorts the analysis of net interest income and trading income in each operating group. To assist in the analysis of net interest margins, the impact of accounting for swaps used to economically hedge interest rate risk that is included in trading income for statutory purposes, has been adjusted against interest rate products in the analysis below.

Half year to Full year to Mar 11

$Am Sep 10

$Am Movement

% Mar 11

$Am Mar 10

$Am Movement

% Equities 214 178 20 392 590 (34) Commodities

Trading income 382 188 103 570 623 (9) Fair value adjustments relating to leasing contracts2 15 (32) * (17) 42 *

Foreign exchange products 109 83 31 192 145 32 Interest rate products

Trading income 80 187 (57) 267 271 (1) Fair value adjustment on fixed rate issued debt 3 6 (50) 9 (255) *

Adjusted net trading income 803 610 32 1,413 1,416 (<1)

2 Macquarie enters into various tolling agreements, capacity contracts and transportation agreements as part of its commodity trading and hedging strategies. The contracts and agreements, which are managed on a fair value basis for financial and risk management purposes, are required to be accounted for on an accruals basis for statutory reporting purposes. This creates a measurement mismatch with related trading positions that are reported at fair value for statutory purposes. For the purposes of enabling comparison with prior periods, Commodities trading income is presented on a basis consistent with management reporting, and the reversal of the fair value adjustments relating to leasing contracts are presented separately to reconcile the result to the statutory presentation.

Total adjusted net trading income of $A1,413 million for the year ended 31 March 2011 was broadly in line with $A1,416 million in the prior year. The year ended 31 March 2011 and the prior year included fair value adjustments relating to leasing contracts (recognised in commodities related income) and a fair value adjustment on fixed rate issued debt (recognised in interest rate products related income). Excluding these fair value adjustments, total adjusted trading income decreased 13% from $A1,629 million in the prior year to $A1,421 million for the year ended 31 March 2011. The year was characterised by challenging market conditions which particularly impacted equities and commodities related trading income in the first half.

11

Equities

Trading income from equities of $A392 million for the year ended 31 March 2011 decreased 34% from $A590 million in the prior year. The decrease was driven by challenging market conditions which impacted revenue throughout the year, particularly in the first half.

Retail and institutional product revenues were down across all regions with the exception of Europe which benefited from the acquisition of Sal. Oppenheim in April 2010. However, leading market share was maintained in core Asian markets. Arbitrage trading continued to make a strong contribution. Reduced volatility and liquidity in equities markets, especially in the first half, adversely impacted trading income.

The second half of the 2011 financial year provided some improvement over the first half with trading income from equities for the six months ended 31 March 2011 of $A214 million, up 20% from $A178 million in the six months ended 30 September 2010.

Commodities

Commodities trading income of $A570 million for the year ended 31 March 2011 decreased 9% from $A623 million for the prior year. Challenging trading conditions and lower client term hedging activity in some commodities markets during the year ended 31 March 2011 negatively impacted trading revenues, particularly in the first half. Energy markets occasionally experienced more difficult trading conditions with periods when the market moved away from fundamentals resulting in reduced income compared to the prior year.

Commodities trading income improved in the second half of the 2011 financial year with income of $A382 million for the six months ended 31 March 2011, up 103% from $A188 million in the six months to 30 September 2010. In metals and agricultural markets, client activity in term hedging improved in the second half of the year after a sporadic first half. Global weather events and geopolitical unrest in the Middle East led to significant volatility in a number of commodities markets during the year. Northern hemisphere energy revenues were stronger in the second half of the year reflecting the seasonal nature of the energy market.

Foreign exchange products

Trading income on foreign exchange products of $A192 million for the year ended 31 March 2011 increased 32% from $A145 million in the prior year, however the total net income from trading activities relating to foreign exchange products, including net interest income/expense, was down. Global volatility in currency markets remained suppressed and the higher Australian Dollar impacted the level of client term hedging. Together with some margin compression this had a negative impact on total net income from trading activities. Refer to Section 3.5 Fixed Income, Currencies and Commodities for further information.

Interest rate products

Trading income on interest rate products of $A267 million for the year ended 31 March 2011 was broadly in line with $A271 million in the prior year. Income in the year ended 31 March 2011 included gains on the sale of fixed rate bonds from the liquid assets portfolio by Group Treasury. These gains are offset by lower levels of income in FICC. Although FICC’s base of offerings has been expanded in the US and Asia over the last twelve months, income for the year ended 31 March 2011 is down, reflecting lower levels of client activity. The prior year was characterised by strong rallies in credit markets globally post the financial crisis, yielding strong returns in FICC’s interest rate related businesses.

Macquarie Group Limited Management Discussion and Analysis macquarie.com.au

2.0 Income statement analysis continued

12

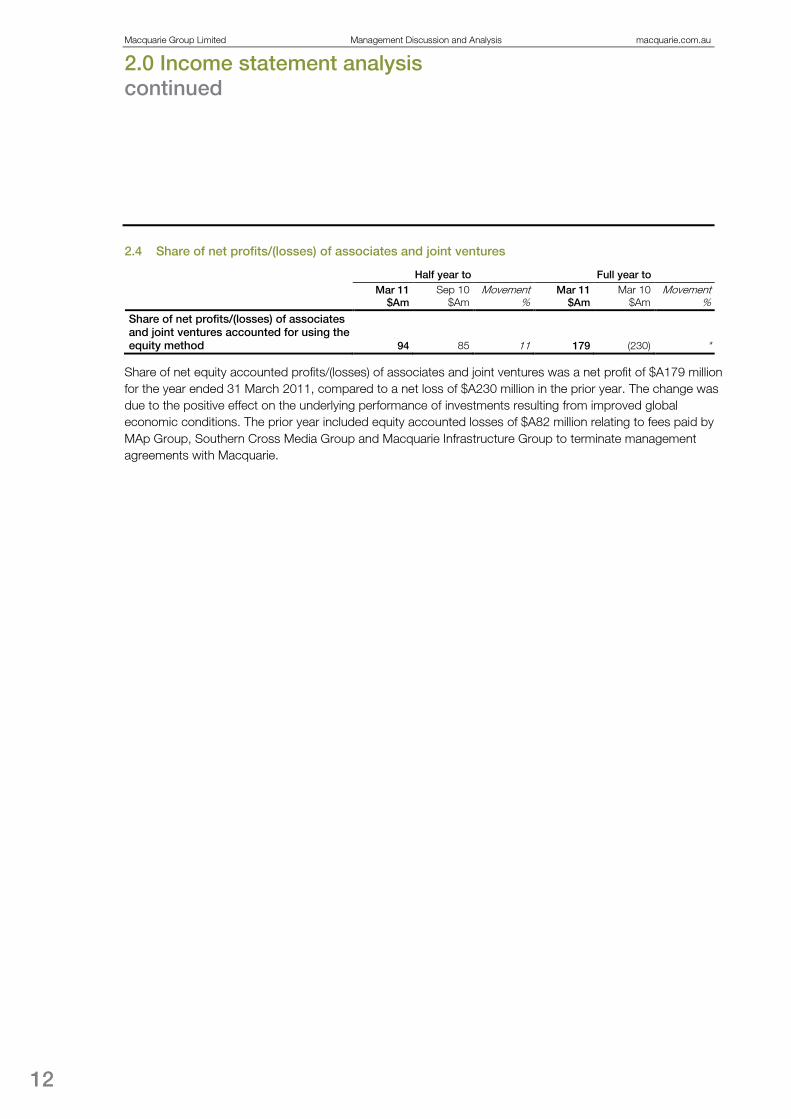

2.4 Share of net profits/(losses) of associates and joint ventures

Half year to Full year to Mar 11

$Am Sep 10

$Am Movement

% Mar 11

$Am Mar 10

$Am Movement

%

Share of net profits/(losses) of associates and joint ventures accounted for using the equity method 94 85 11 179 (230) *

Share of net equity accounted profits/(losses) of associates and joint ventures was a net profit of $A179 million for the year ended 31 March 2011, compared to a net loss of $A230 million in the prior year. The change was due to the positive effect on the underlying performance of investments resulting from improved global economic conditions. The prior year included equity accounted losses of $A82 million relating to fees paid by MAp Group, Southern Cross Media Group and Macquarie Infrastructure Group to terminate management agreements with Macquarie.

13

2.5 Other operating income and charges

Half year to Full year to Mar 11

$Am Sep 10

$Am Movement

% Mar 11

$Am Mar 10

$Am Movement

% Net gains on sale of investment securities available for sale 124 105 18 229 96 139 Impairment charge on investment securities available for sale (35) (3) * (38) (77) (51) Net gains on sale of associates (including associates held for sale) and joint ventures 10 9 11 19 50 (62) Impairment charge on investments in associates and joint ventures1 (23) (46) (50) (69) (357) (81) Impairment charge on disposal groups held for sale (16) — * (16) — * Gain on acquiring, disposing and change in ownership interest in subsidiaries, associates and businesses held for sale 63 33 91 96 393 (76) Gain on re-measurement of retained investments2 15 114 (87) 129 — * Impairment charge on non-financial assets (3) (4) (25) (7) (36) (81) Sale of management rights 14 — * 14 428 (97) Gain on repurchase of subordinated debt — — * — 55 (100) Net operating lease income3 167 76 120 243 138 76 Dividends/distributions received/receivable:

Investment securities available for sale 60 66 (9) 126 22 * Collective allowance for credit losses written back/(provided for) during the financial year (4) 9 * 5 2 150 Specific provisions (47) (86) (45) (133) (218) (39) Other income 236 97 143 333 272 22 Total other operating income and charges 561 370 52 931 768 21

1 Includes impairment reversals of $A10 million (31 March 2010: $A43 million). 2 Includes gains on re-measurement of retained ownership interests to fair value on the loss of control of investments in

subsidiaries and the loss of significant influence on investments in associates. 3 Includes rental income of $A401 million (31 March 2010: $A370 million) less depreciation of $A158 million (31 March 2010:

$A232 million) in relation to operating leases where the Consolidated Entity is the lessor.

Other operating income and charges was a net gain of $A931 million for the year ended 31 March 2011, an increase of 21% from $A768 million in the prior year.

Net gains on sale of investment securities available for sale of $A229 million for the year ended 31 March 2011 increased significantly from $A96 million in the prior year. The year ended 31 March 2011 included realisations of some investments in resource markets, particularly in the gold sector, and the sale of some debt securities held for liquidity management purposes by Group Treasury.

Impairment charges on investment securities available for sale, associates, disposal groups held for sale and non-financial assets totalled $A130 million in the year ended 31 March 2011, down 72% from $A470 million in the prior year. Lower impairment charges on Macquarie’s co-investments during the period compared to the prior year resulted from a stabilisation of global markets and improved operating conditions.

Macquarie Group Limited Management Discussion and Analysis macquarie.com.au

2.0 Income statement analysis continued

14

Gains on acquiring, disposing and change in ownership interests in subsidiaries, associates and businesses held for sale for the year ended 31 March 2011 was $A96 million, down 76% from $A393 million in the prior year. The year ended 31 March 2011 included $A33 million from the sale of Macquarie Asset Leasing Trust and $A23 million from the partial sell-down of ownership in the OzForex group of companies (OzForex). The prior year result included a gain of $A127 million from the financing of £157.5 million of Macquarie Income Preferred Securities, income from the sale of Macquarie Communications Infrastructure Management Limited and income from the sale of the majority of the real estate funds platform to Charter Hall Group.

Gains on reclassification of retained investments of $A129 million in the year ended 31 March 2011 includes gains from the reclassification of investments in MAp Group and OzForex to available for sale investments. On reclassification the retained stakes were required to be remeasured to fair value and the gain recognised in the income statement.

The gain on sale of management rights of $A14 million in the year ended 31 March 2011 relates to the sale of management rights in Macquarie Power and Infrastructure Corporation. The income of $A428 million in the prior year comprised $A345 million from Macquarie Airports, $A42 million from Macquarie Infrastructure Group and $A41 million from Macquarie Media Group.

Net operating lease income of $A243 million for the year ended 31 March 2011 increased 76% from $A138 million in the prior year mainly due to the acquisition by Corporate and Asset Finance of aircraft assets and associated operating leases from American International Group’s International Lease Finance Corporation (ILFC) throughout the year.

Dividends/distributions received/receivable on investment securities available for sale were $A126 million in the year ended 31 March 2011, increasing significantly from $A22 million in the prior year. The increase was largely attributable to distributions received from MAp Group subsequent to its reclassification from an investment in associate to an available for sale investment.

Net charges for specific and collective provisions of $A128 million in the year ended 31 March 2011 decreased 41% from $A216 million in the prior year, reflecting improved market and economic conditions.

Other income of $A333 million for the year ended 31 March 2011 increased 22% from $A272 million in the prior year largely due to the sale of net profit interests and royalties from participants in the metals and energy sectors.

15

2.6 Operating expenses

Half year to Full year to Mar 11

$Am Sep 10

$Am Movement

% Mar 11

$Am Mar 10

$Am Movement

%

Employment expenses Salary, commissions, superannuation and performance-related profit share (1,673) (1,596) 5 (3,269) (2,595) 26 Share based payments (181) (125) 45 (306) (224) 37 Provision for annual leave (4) (25) (84) (29) (21) 38 Provision for long service leave — (8) (100) (8) (8) —

Total compensation expense (1,858) (1,754) 6 (3,612) (2,848) 27 Other employment expenses including on-costs, staff procurement and staff training (136) (142) (4) (278) (253) 10 Total employment expenses (1,994) (1,896) 5 (3,890) (3,101) 25 Brokerage and commission expenses (344) (441) (22) (785) (645) 22 Occupancy expenses (246) (237) 4 (483) (482) <1 Non-salary technology expenses (157) (159) (1) (316) (283) 12 Professional fees (163) (133) 23 (296) (287) 3 Travel and entertainment expenses (92) (92) — (184) (160) 15 Advertising and communication expenses (66) (61) 8 (127) (99) 28 Other expenses (146) (146) — (292) (287) 2 Total operating expenses (3,208) (3,165) 1 (6,373) (5,344) 19

Total operating expenses of $A6,373 million for the year ended 31 March 2011 increased 19% from $A5,344 million in the prior year predominantly due to increases in employment expenses and brokerage and commission expenses reflecting the investment in and expansion of global platforms.

Employment expenses of $A3,890 million for the year ended 31 March 2011 increased 25% from $A3,101 million in the prior year mainly due to a 17% increase in average headcount during the year.

Brokerage and commission expenses of $A785 million increased 22% from $A645 million in the prior year. The increase in brokerage and commission expenses was mainly due to the full year contribution of Delaware Investments which was acquired in January 2010. The brokerage and commission expenses for Delaware Investments largely offsets with related distribution service fee income that, for accounting purposes, is required to be recognised in other fee and commission income (refer to Section 2.2 for further information).

Non-salary technology expenses of $A316 million for the year ended 31 March 2011 increased 12% from $A283 million in the prior year mainly due to increased investment in technology platforms, especially in Macquarie Securities and FICC.

Macquarie Group Limited Management Discussion and Analysis macquarie.com.au

2.0 Income statement analysis continued

16

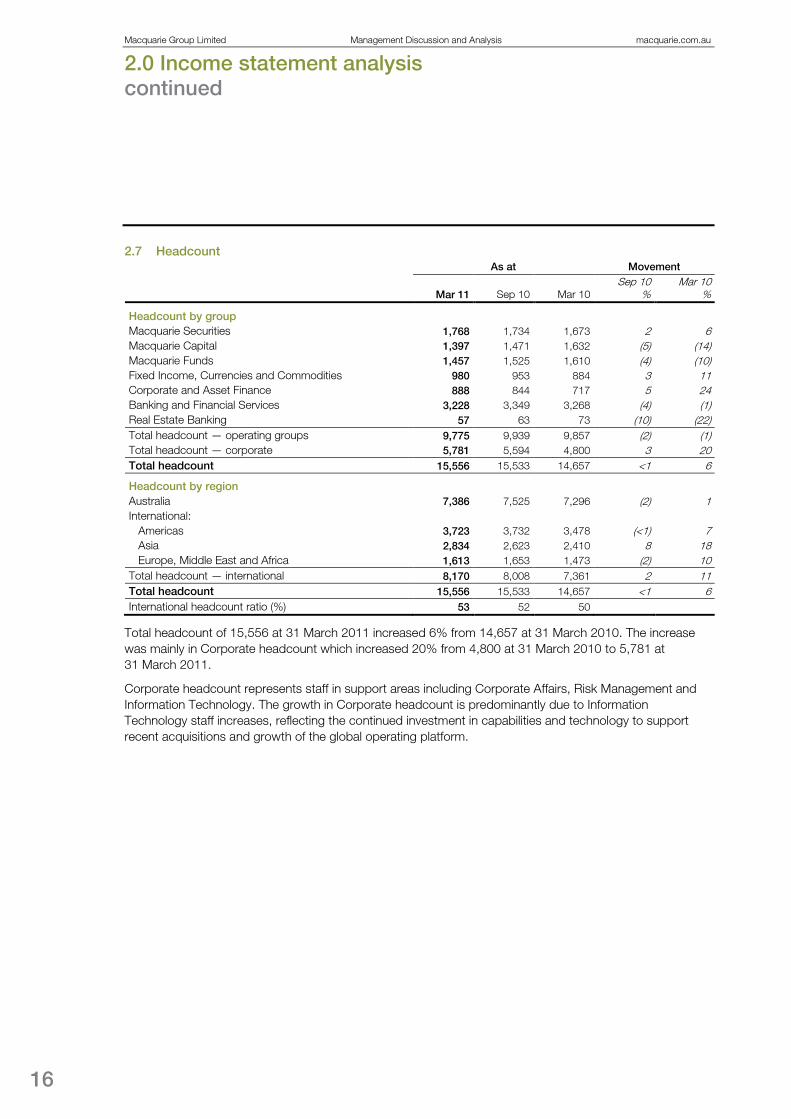

2.7 Headcount

As at Movement

Mar 11 Sep 10 Mar 10 Sep 10

% Mar 10

%

Headcount by group Macquarie Securities 1,768 1,734 1,673 2 6 Macquarie Capital 1,397 1,471 1,632 (5) (14) Macquarie Funds 1,457 1,525 1,610 (4) (10) Fixed Income, Currencies and Commodities 980 953 884 3 11 Corporate and Asset Finance 888 844 717 5 24 Banking and Financial Services 3,228 3,349 3,268 (4) (1) Real Estate Banking 57 63 73 (10) (22) Total headcount — operating groups 9,775 9,939 9,857 (2) (1) Total headcount — corporate 5,781 5,594 4,800 3 20 Total headcount 15,556 15,533 14,657 <1 6

Headcount by region Australia 7,386 7,525 7,296 (2) 1 International:

Americas 3,723 3,732 3,478 (<1) 7 Asia 2,834 2,623 2,410 8 18 Europe, Middle East and Africa 1,613 1,653 1,473 (2) 10

Total headcount — international 8,170 8,008 7,361 2 11 Total headcount 15,556 15,533 14,657 <1 6 International headcount ratio (%) 53 52 50

Total headcount of 15,556 at 31 March 2011 increased 6% from 14,657 at 31 March 2010. The increase was mainly in Corporate headcount which increased 20% from 4,800 at 31 March 2010 to 5,781 at 31 March 2011.

Corporate headcount represents staff in support areas including Corporate Affairs, Risk Management and Information Technology. The growth in Corporate headcount is predominantly due to Information Technology staff increases, reflecting the continued investment in capabilities and technology to support recent acquisitions and growth of the global operating platform.

17

2.8 Income tax expense Full year to

Mar 11

$Am Mar 10

$Am

Net profit before tax 1,271 1,294 Add back: write-downs, impairment charges and equity accounted gains/(losses) 79 854 Net profit before write-downs, impairment charges, equity accounted gains/(losses) and tax 1,350 2,148

Prima facie tax @ 30% 405 644 Income tax permanent differences (99) (187) Income tax expense (before impact of write-downs, impairment charges and equity accounted gains/(losses)) 306 457 Implied effective tax rate (%)1 23% 22%

Prima facie tax of write-downs, impairment charges and equity accounted gains/(losses) @ 30% (24) (256) Income tax expense 282 201 Actual effective tax rate (%)1 23% 16%

1 The effective tax rate is calculated on net profit before tax and after non-controlling interests. Non-controlling interests reduce net profit before tax by $A33 million for the year ended 31 March 2011 (31 March 2010: $A43 million).

The effective tax rate for the year ended 31 March 2011 was 23%, up from 16% in the prior year, largely due to reduced write-downs and impairment charges in the year ended 31 March 2011 compared to the prior year and a reduction in income tax permanent differences compared to the prior year.

The implied effective tax rate before the impact of write-downs and impairment charges is comparable to the prior year.

Macquarie Group Limited Management Discussion and Analysis macquarie.com.au

3.0 Segment analysis

18

3.1 Basis of preparation

AASB 8 ‘Operating Segments’ requires the ‘management approach’ to disclosing information about Macquarie’s reportable segments. The financial information is reported on the same basis as used internally by senior management for evaluating operating segment performance and for deciding how to allocate resources to operating segments. Such information is produced using different measures to those used in preparing the income statement.

For internal reporting and risk management purposes, Macquarie is divided into six operating groups and one division (generally referred to as “the Operating groups”).

Operating groups: – Macquarie Securities – Macquarie Capital – Macquarie Funds – Fixed Income, Currencies and Commodities – Corporate and Asset Finance – Banking and Financial Services

Division: – Real Estate Banking

In addition, there is a Corporate segment which includes Group Treasury, head office and central support functions. Items of income and expense within the Corporate segment include the net impact of managing liquidity for Macquarie, earnings on capital, non-trading derivative volatility, unallocated head office costs and employment related costs of central support functions (service areas), performance related profit share and share based payments expense, income tax expense and distributions to holders of CPS, MIS and MIPS.

Operating group restructures

Since 31 March 2010 there have been two significant restructures of operating groups and divisions. The restructures are effective from 1 April 2010, and comparative information presented in this document has been restated to reflect the current Group structure. – MIRA (formerly Macquarie Capital Funds) – this division of Macquarie Capital was transferred to

Macquarie Funds. – Real Estate Structured Finance (RESF) – this division of Real Estate Banking was transferred to

Corporate and Asset Finance.

Internal transactions

Any transactions or transfers between segments are determined on an arm’s length basis and are included within the relevant categories of income and/or expense. These transactions eliminate on aggregation/ consolidation. Over the page is a selection of the key policies.

19

Internal funding arrangements

Group Treasury has the responsibility for managing the overall funding for the Group, and operating groups obtain funding from Group Treasury. The interest rates charged by Group Treasury are determined by the types of assets being funded and the term of the funding, and are fully costed.

Operating Groups may only source funding directly from external sources generally when there is recourse only to the assets being funded and not to the Group.

Deposits are a funding source for Macquarie. Banking and Financial Services receives a deposit premium from Group Treasury on deposits they generate. This deposit premium is included within net interest income for segment reporting purposes.

Transactions between Operating groups

Operating Groups that enter into arrangements with other Operating groups must do so on an arm’s length basis. There is a requirement for accounting symmetry in such transactions.

Transactions between Operating groups are recognised in each of the relevant categories of income and expense as appropriate.

Service area recoveries

Service areas recover their costs to operating groups on either a time and effort allocation basis or a fee for service basis. Service areas include Corporate Affairs (Finance, Market Operations, Tax, Company Secretarial, Human Resources, Business Services, Corporate Communications and Investor Relations), Risk Management, Information Technology, Group Legal and Central Executive.

Service area recoveries are recognised within Other operating expenses in the income statement.

Internal management revenue/charges

Internal management revenue/charges are primarily used to recognise an Operating Group’s contribution to income tax expenses and benefits. Non-assessable income generated by an Operating Group results in a benefit added to that group’s operating result. Conversely a non-deductible expense results in a charge to the operating result. These management charges are offset by an equal and opposite amount recognised in the Corporate segment such that on aggregation the total nets to nil.

Internal management revenue/charges are reported separately in the income statement of each Operating group.

Presentation of segment income statements

The income statements in the following pages for each of the reported segments are in some cases summarised by grouping non-material balances together. All material or key balances have been reported separately to provide users with the most relevant information.

Macquarie Group Limited Management Discussion and Analysis macquarie.com.au

3.0 Segment analysis continued

20

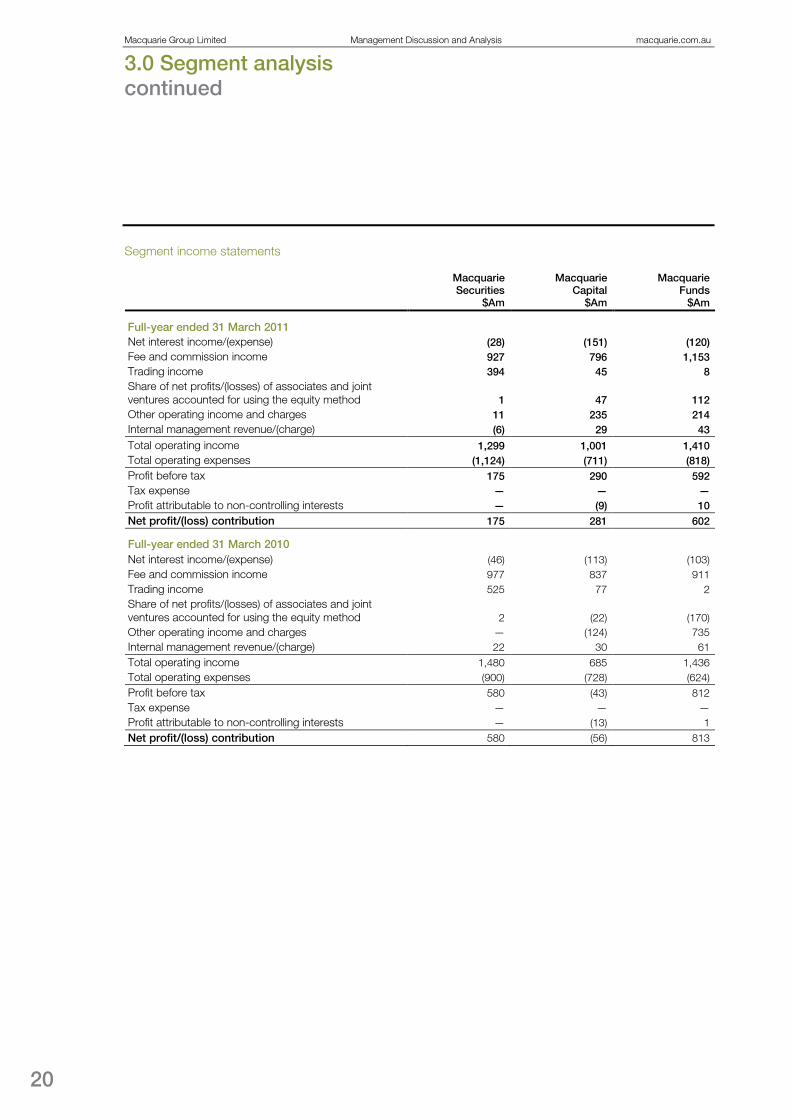

Segment income statements

Macquarie Securities

$Am

Macquarie Capital

$Am

Macquarie Funds

$Am

Full-year ended 31 March 2011 Net interest income/(expense) (28) (151) (120) Fee and commission income 927 796 1,153 Trading income 394 45 8 Share of net profits/(losses) of associates and joint ventures accounted for using the equity method 1 47 112 Other operating income and charges 11 235 214 Internal management revenue/(charge) (6) 29 43

Total operating income 1,299 1,001 1,410 Total operating expenses (1,124) (711) (818) Profit before tax 175 290 592 Tax expense — — — Profit attributable to non-controlling interests — (9) 10 Net profit/(loss) contribution 175 281 602

Full-year ended 31 March 2010 Net interest income/(expense) (46) (113) (103) Fee and commission income 977 837 911 Trading income 525 77 2 Share of net profits/(losses) of associates and joint ventures accounted for using the equity method 2 (22) (170) Other operating income and charges — (124) 735 Internal management revenue/(charge) 22 30 61 Total operating income 1,480 685 1,436 Total operating expenses (900) (728) (624) Profit before tax 580 (43) 812 Tax expense — — — Profit attributable to non-controlling interests — (13) 1 Net profit/(loss) contribution 580 (56) 813

21

Fixed Income,

Currencies and Commodities

$Am

Corporate and Asset

Finance $Am

Banking and Financial Services

$Am

Real Estate Banking

$Am Corporate

$Am Total $Am

(29) 583 713 (12) 319 1,275 171 5 752 12 75 3,891 954 (3) 6 (1) (35) 1,368

15 9 1 (5) (1) 179

250 171 12 — 38 931 55 21 10 (2) (150) —

1,416 786 1,494 (8) 246 7,644 (841) (285) (1,214) (34) (1,346) (6,373) 575 501 280 (42) (1,100) 1,271

— — — — (282) (282) — — (5) — (29) (33)

575 501 275 (42) (1,411) 956

116 382 551 (37) 330 1,080 155 8 727 67 39 3,721

1,042 41 1 (6) (383) 1,299

11 (5) 2 (41) (7) (230) 37 7 (41) (102) 256 768 80 32 11 5 (241) —

1,441 465 1,251 (114) (6) 6,638 (614) (208) (984) (34) (1,252) (5,344) 827 257 267 (148) (1,258) 1,294

— — — — (201) (201) — (2) (6) — (23) (43)

827 255 261 (148) (1,482) 1,050

Macquarie Group Limited Management Discussion and Analysis macquarie.com.au

3.0 Segment analysis continued

22

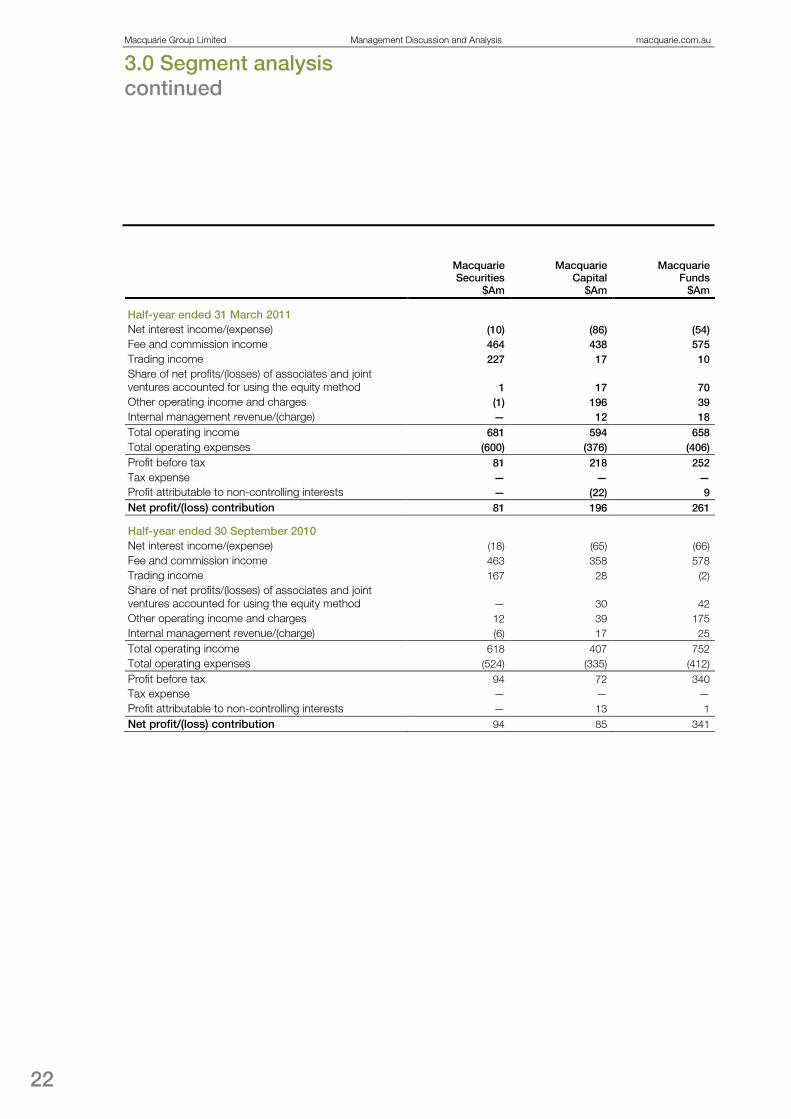

Macquarie

Securities $Am

Macquarie Capital

$Am

Macquarie Funds

$Am

Half-year ended 31 March 2011 Net interest income/(expense) (10) (86) (54) Fee and commission income 464 438 575 Trading income 227 17 10 Share of net profits/(losses) of associates and joint ventures accounted for using the equity method 1 17 70 Other operating income and charges (1) 196 39 Internal management revenue/(charge) — 12 18 Total operating income 681 594 658 Total operating expenses (600) (376) (406) Profit before tax 81 218 252 Tax expense — — — Profit attributable to non-controlling interests — (22) 9 Net profit/(loss) contribution 81 196 261

Half-year ended 30 September 2010 Net interest income/(expense) (18) (65) (66) Fee and commission income 463 358 578 Trading income 167 28 (2) Share of net profits/(losses) of associates and joint ventures accounted for using the equity method — 30 42 Other operating income and charges 12 39 175 Internal management revenue/(charge) (6) 17 25 Total operating income 618 407 752 Total operating expenses (524) (335) (412) Profit before tax 94 72 340 Tax expense — — — Profit attributable to non-controlling interests — 13 1 Net profit/(loss) contribution 94 85 341

23

Fixed Income, Currencies and

Commodities $Am

Corporate and Asset

Finance $Am

Banking and Financial Services

$Am

Real Estate Banking

$Am Corporate

$Am Total $Am

10 301 369 (6) 146 670 84 (6) 359 9 (27) 1,896

587 (1) 8 — (86) 762

— 3 1 3 (1) 94 158 112 19 3 35 561 28 9 8 (3) (72) —

867 418 764 6 (5) 3,983 (459) (150) (623) (20) (574) (3,208) 408 268 141 (14) (579) 775

— — — — (197) (197) — — — — (12) (25)

408 268 141 (14) (788) 553

(39) 282 344 (6) 173 605 87 11 393 3 102 1,995

367 (2) (2) (1) 51 606

15 6 — (8) — 85 92 59 (7) (3) 3 370 27 12 2 1 (78) —

549 368 730 (14) 251 3,661 (382) (135) (591) (14) (772) (3,165) 167 233 139 (28) (521) 496

— — — — (85) (85) — — (5) — (17) (8)

167 233 134 (28) (623) 403

Macquarie Group Limited Management Discussion and Analysis macquarie.com.au

3.0 Segment analysis continued

24

3.2 Macquarie Securities

Half year to Full year to Mar 11

$Am Sep 10

$Am Movement

% Mar 11

$Am Mar 10

$Am Movement

%

Net trading income (including net interest income)1 217 149 46 366 479 (24) Fee and commission income Brokerage and commissions 343 372 (8) 715 714 <1 Other fee and commission income 121 91 33 212 263 (19) Total fee and commission income 464 463 <1 927 977 (5) Share of net profits of associates and joint ventures accounted for using the equity method 1 — * 1 2 (50) Other operating income and charges (1) 12 * 11 — * Internal management revenue/(charge) — (6) (100) (6) 22 * Total operating income 681 618 10 1,299 1,480 (12)

Operating expenses Employment expenses (208) (174) 20 (382) (278) 37 Brokerage and commission expenses (136) (106) 28 (242) (218) 11 Other operating expenses (256) (244) 5 (500) (404) 24 Total operating expenses (600) (524) 15 (1,124) (900) 25 Net profit contribution 81 94 (14) 175 580 (70)

Non-GAAP metrics Headcount 1,768 1,734 2 1,768 1,673 6

1 The relative contribution of net interest income and trading income to income from trading activities can vary from period to period depending on the underlying trading strategies undertaken by Macquarie and its clients. As such, to obtain a more complete view of Macquarie Securities’ trading activities, net interest income has been combined with trading income above.

Macquarie Securities’ net profit contribution of $A175 million for the year ended 31 March 2011 decreased 70% from $A580 million in the prior year primarily due to reduced equity capital market activity in Australia and reduced levels of both institutional and retail client activity globally. Operating expenses have increased as a result of the full year impact of prior year acquisitions including FPK in November 2009, and the acquisition of Sal. Oppenheim in April 2010.

Net trading income (including net interest income)

Net trading income (including net interest income) of $A366 million for the year ended 31 March 2011 decreased 24% from $A479 million in the prior year.

As a result of challenging market conditions, retail and institutional product revenues were down across all regions with the exception of Europe which benefited from the acquisition of Sal. Oppenheim in April 2010. Despite this, leading market share was maintained in core Asian markets. The second half of the 2011 financial year provided some improvement over the first half.

Arbitrage trading continued to make a strong contribution to net trading income. Lower volatility and liquidity in the market, notably in the first half of the 2011 financial year, adversely impacted trading conditions.

25

Brokerage and commissions

Brokerage and commissions income of $A715 million for the year ended 31 March 2011 was in line with $A714 million in the prior year. Brokerage and commissions income predominantly includes transaction related fees from cash equities services provided to institutional clients. Revenues from the Americas and Europe continued to grow, benefiting from the FPK acquisition in November 2009 and Sal. Oppenheim acquisition in April 2010. This was offset by lower commissions in Asia and Australia due to reduced client activity as well as Asian revenues being negatively impacted by the stronger Australian Dollar.

Client rankings show the business is maintaining or improving rankings with clients and Macquarie is considered to be an improving global presence in securities markets.

Other fee and commission income

Other fee and commission income of $A212 million for the year ended 31 March 2011 decreased 19% from $A263 million in the prior year. Other fee and commission income consists primarily of equity capital markets fees. Capital raising activity was down in Australia and Europe compared to the prior year, however increased activity in America and Asia resulted in increased revenues in these regions, with notable transactions for the period including the listing of Agricultural Bank of China Limited on the Stock Exchange of Hong Kong as part of a $A22.1 billion dual listing in Hong Kong and Shanghai, featuring Macquarie Securities as joint bookrunner and joint lead manager.

Operating expenses

Total operating expenses of $A1,124 million for the year ended 31 March 2011 increased 25% from $A900 million in the prior year.

Employment expenses of $A382 million for the year ended 31 March 2011 increased 37% from $A278 million in the prior year. The increase was mainly due to the full year impact of prior year acquisitions including FPK in November 2009, the acquisition of Sal. Oppenheim in April 2010, and the build out of new business in Europe and America.

Brokerage and commission expenses of $A242 million for the year ended 31 March 2011 increased 11% from $A218 million in the prior year. The increase was primarily driven by the acquisition of the Sal. Oppenheim business in Europe (April 2010), higher rebates paid to clients in Asia and increased fee trades in the Stock Borrow Loan business.

Other operating expenses of $A500 million for the year to 31 March 2011 increased 24% from $A404 million in the prior year primarily driven by the full year impact of prior year acquisitions including FPK in November 2009, the acquisition of Sal. Oppenheim in April 2010, and the build out of new business in Europe and America. Other operating expenses were also impacted by increased investment in technology platforms during the year.

Macquarie Group Limited Management Discussion and Analysis macquarie.com.au

3.0 Segment analysis continued

26

3.3 Macquarie Capital

Half year to Full year to Mar 11

$Am Sep 10

$Am Movement

% Mar 11

$Am Mar 10

$Am Movement

%

Net interest expense (86) (65) 32 (151) (113) 34 Fee and commission income Mergers and acquisitions, advisory and underwriting fees 482 380 27 862 996 (13) Brokerage and commissions 22 21 5 43 33 30 Other fee and commission expense (66) (43) 53 (109) (192) (43) Total fee and commission income 438 358 22 796 837 (5) Net trading income 17 28 (39) 45 77 (42) Share of net profits/(losses) of associates and joint ventures accounted for using the equity method 17 30 (43) 47 (22) * Other operating income and charges Net gains on sale of equity investments 1 6 (83) 7 84 (92) Gain/(loss) on reclassification of retained investments (2) 19 * 17 — * Impairment charge on equity investments (22) (8) 175 (30) (387) (92) Impairment charge on non-financial assets (1) — * (1) (6) (83) Gain on acquiring, disposing and change in ownership interest in subsidiaries and businesses held for sale 33 8 * 41 27 52 Net operating lease income 62 30 107 92 66 39 Specific provisions and collective allowance for credit losses — (10) (100) (10) (4) 150 Other income 125 (6) * 119 96 24 Total other operating income and charges 196 39 * 235 (124) * Internal management revenue 12 17 (29) 29 30 (3) Total operating income 594 407 46 1,001 685 46

Operating expenses Employment expenses (207) (181) 14 (388) (386) 1 Brokerage and commission expenses (2) (4) (50) (6) (6) — Other operating expenses (167) (150) 11 (317) (336) (6) Total operating expenses (376) (335) 12 (711) (728) (2) Non-controlling interests1 (22) 13 * (9) (13) (31) Net profit/(loss) contribution 196 85 131 281 (56) *

Non-GAAP metrics Headcount 1,397 1,471 (5) 1,397 1,632 (14)

1 The non-controlling interests category adjusts reported consolidated profit or loss for the share that is attributable to non-controlling interests, such that the net profit or loss contribution represents the net profit or loss attributable to ordinary equity holders.

Macquarie Capital’s net profit contribution of $A281 million for the year ended 31 March 2011 increased from a loss of $A56 million in the prior year primarily due to lower impairment charges, partially offset by reduced advisory income.

27

Net interest expense

Net interest expense of $A151 million for the year ended 31 March 2011 increased 34% from $A113 million in the prior year. The expense mainly relates to the funding cost of principal investments. The increase is primarily due to higher interest rates during the year ended 31 March 2011 compared to the prior year.

Mergers and acquisitions, advisory and underwriting income

Mergers and acquisitions, advisory and underwriting income of $A862 million for the year to 31 March 2011 decreased 13% from $A996 million in the prior year reflecting lower levels of equity capital markets activity. The volume and value of deals in which Macquarie participated for the year ended 31 March 2011 (547 deals valued at approximately $A159 billion) was higher compared to the prior year (448 deals valued at approximately $A121 billion).

Significant advisory deals completed for the year ended 31 March 2011 included: – Co-developer, financial adviser, and equity underwriter for the $US2.1 billion Denver Fastracks Eagle P3

project. The first US rail public-private partnership (PPP), it involves a 35-year concession to design, build, finance, operate and maintain two greenfield commuter rail lines and associated rolling stock for the Denver metro area;

– Financial adviser to Cintra Infraestructuras, S.A. and Meridiam Infrastructure Finance S.à.r.l. on the $US2.7 billion Interstate 635 Managed Lanes Project to develop, finance, construct and maintain 13 miles of managed lanes in Dallas County, Texas;

– Adviser to Eiffarie (owned by Macquarie Atlas Roads, Macquarie European Infrastructure Fund, Macquarie European Infrastructure Fund II and French construction company, Eiffage), on the acquisition of a further 13.7 per cent interest in Autoroutes Paris-Rhin-Rhone (APRR);

– Adviser and lender to TPG Capital and Carlyle Group on the $A2.7 billion acquisition of Healthscope Limited, via scheme of arrangement;

– Lead sponsor and sole financial adviser on the €100 million Irish Schools PPP Bundle 2 project which will provide six new schools and subsequently 4,700 pupil places. This is the second Macquarie sponsored PPP to reach close in Ireland;

– Joint sponsor, joint bookrunner and joint lead manager for the listing of Agricultural Bank of China Limited on the Stock Exchange of Hong Kong as part of a $A22.1 billion dual listing in Hong Kong and Shanghai;

– Joint lead manager and bookrunner on Sino-Ocean Land’s $US900 million issue of perpetual subordinated convertible securities, the largest international equity-linked issuance ever for a mainland Chinese property developer, and one of the first convertible securities to achieve balance sheet equity treatment for an Asian Corporate (ex Japan);

– Financial adviser to a consortium of Macquarie-managed funds on the acquisition of 100% of Ceske Radiokomunikace. The transaction represents one of the largest telecommunications transactions in Central and Eastern Europe in calendar year 2010;

– Financial adviser to Macquarie-managed funds on the acquisition of 100 per cent of Thyssengas from RWE. Thyssengas is the owner and operator of a regulated supra-regional gas transmission network in Germany, transporting almost 10 billion cubic metres of natural gas annually to 56 downstream networks;

– Financial adviser to a consortium comprising Global Infrastructure Partners, Industry Funds Management, QIC Global Infrastructure and the Abu Dhabi Investment Authority on the acquisition of the 99-year lease of the Port of Brisbane for consideration valued at $A2.1 billion;

– Financial adviser, debt arranger and equity bridge provider to Southern Cross Media Group Limited for the takeover offer for Austereo Group Limited;

Macquarie Group Limited Management Discussion and Analysis macquarie.com.au

3.0 Segment analysis continued

28

– Sole sponsor, joint global coordinator, joint bookrunner and joint lead manager on the $US369 million ($US425 million post-greenshoe) Initial Public Offering (IPO) of China Suntien Green Energy Corporation Limited on the Hong Kong Stock Exchange. China Suntien is one of the leading clean energy companies in Northern China;

– Sole global coordinator, sole sponsor, joint bookrunner and joint lead manager on the $US204 million IPO of Global Dairy Holdings Limited on the Hong Kong Stock Exchange. Global Dairy is one of the top ten locally-branded milk powder companies in the Peoples’ Republic of China;

– Joint bookrunner on a $US183 million equity offering for InterOil Corporation, an integrated energy company focused in Papua New Guinea;

– Joint global coordinator, joint bookrunner and transaction adviser, on the IPO of Royal Bafokeng Platinum Limited on the Main Board of the Johannesburg Stock Exchange for $US433 million listing;

– Exclusive financial adviser and sole bookrunner to the Government of the Republic of Ghana for a $US215 million sell down in AngloGold Ashanti Limited ordinary shares by way of an accelerated bookbuild;

– Joint financial adviser to the Administrators of The Griffin Coal Mining Company Pty Ltd on the sale of coal mining assets to Indian company Lanco Infratech Ltd. This transaction represents the largest inbound investment from an Indian company into the Australian resources sector;

– Financial adviser to CoreLogic, a leading provider of information, analytics and business services, on the sale of employer e-services and litigation support businesses, collectively First Advantage, to Symphony Technology Group; and

– Sole sponsor, sole global coordinator and joint bookrunner on the $US200 million Hong Kong IPO of Top Spring International Holdings Limited. The deal represented the first real estate IPO (Asia-ex Japan) in 2011.

Other fee and commission expense

Other fee and commission expense of $A109 million for the year ended 31 March 2011 decreased 43% from $A192 million in the prior year. For Macquarie Capital, other fee and commission expense predominantly relates to internal transactions with other Operating Groups. The decrease is due to lower payments to Macquarie Securities on equity underwriting transactions, which were well down on the prior year due to reduced equity capital markets activity, partially offset with receipts from Corporate and Asset Finance relating to the acquisition of aircraft assets and associated leases from AIG’s International Lease Finance Corporation.

Net trading income

Net trading income of $A45 million for the year ended 31 March 2011 decreased 42% from $A77 million in the prior year. The year ended 31 March 2011 included profits in relation to listed and unlisted equity investments, interest rates swaps and warrants and options. The income in the prior year included a realised profit in relation to a United States listed investment and an unrealised profit on warrants and options.

Share of net profits/(losses) of associates and joint ventures accounted for using the equity method

Improved operating conditions resulted in net equity accounted profits of $A47 million for the year ended 31 March 2011 compared to a net loss of $A22 million in the prior year. Net equity accounted profits of $A20 million were recognised in the year ended 31 March 2011 for listed associates and $A27 million for unlisted associates.

29

Net gains on sale of equity investments

Net gains on sale of equity investments of $A7 million for the year ended 31 March 2011 decreased significantly from $A84 million in the prior year. The year ended 31 March 2011 included a gain on an unlisted investment in the infrastructure industry. The prior year included income from the sale of Moto Hospitality and Puget Energy.

Gains on reclassification of retained investments

Gains on reclassification of retained investments of $A17 million predominantly relates to a gain recognised when Macquarie lost significant influence over an equity accounted investment on IPO and was required to revalue its retained investment to fair value.

Impairment charge on equity investments

Impairment charges on equity investments of $A30 million for the year ended 31 March 2011 decreased significantly from $A387 million in the prior year reflecting the improving market and economic conditions.

Gain on acquiring, disposing and change in ownership interest in subsidiaries and businesses held for sale

The gain on acquiring, disposing and change in ownership interest in subsidiaries and businesses held for sale of $A41 million for the year ended 31 March 2011 increased 52% from $A27 million in the prior year. The gain in the year ended 31 March 2011 included income from the sale of the Macquarie Asset Leasing Trust.

Operating expenses

Total operating expenses for the year ended 31 March 2011 were $A711 million, a reduction of 2% from $A728 million in the prior year.

Employment expenses for the year ended 31 March 2011 were $A388 million, broadly in line with $A386 million in the prior year. Other operating expenses of $A317 million for the year ended 31 March 2011 decreased 6% from $A336 million in the prior year mainly due to lower average headcount and favourable FX movements.

Macquarie Group Limited Management Discussion and Analysis macquarie.com.au

3.0 Segment analysis continued

30

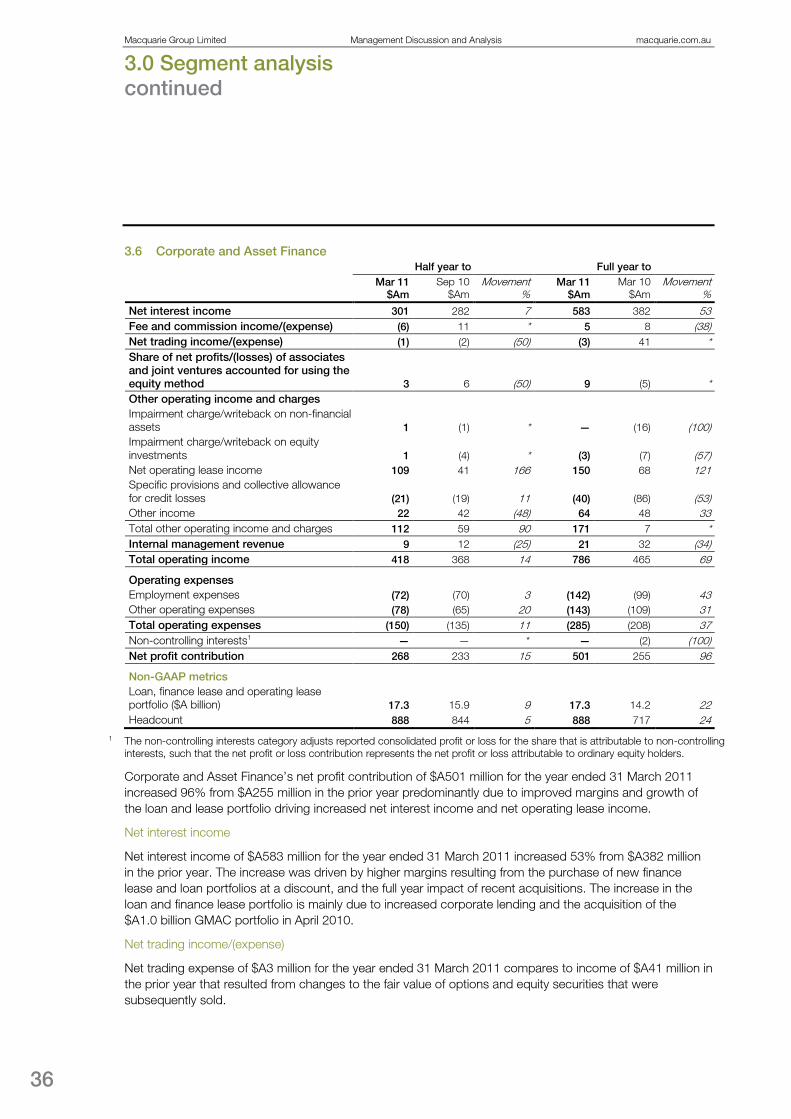

3.4 Macquarie Funds

Half year to Full year to Mar 11

$Am Sep 10

$Am Movement

% Mar 11

$Am Mar 10

$Am Movement

%

Net interest expense (54) (66) (18) (120) (103) 17 Fee and commission income Base fees 432 441 (2) 873 697 25 Performance fees 15 15 — 30 22 36 Mergers and acquisitions, advisory and underwriting fees 18 3 * 21 39 (46) Brokerage and commissions 13 17 (24) 30 33 (9) Other fee and commission income 97 102 (5) 199 120 66 Total fee and commission income 575 578 (1) 1,153 911 27 Net trading income/(expense) 10 (2) * 8 2 300 Share of net profits/(losses) of associates and joint ventures accounted for using the equity method 70 42 67 112 (170) * Other operating income and charges Impairment charge/writeback on equity investments (27) 4 * (23) 31 * Impairment charge on non-financial assets — — * — (6) (100) Gain/(loss) on acquiring, disposing and change in ownership interest in subsidiaries and businesses held for sale (4) (1) 300 (5) 238 * Gain on reclassification of retained investments — 95 (100) 95 — * Sale of management rights 14 — * 14 428 (97) Specific provisions and collective allowance for credit losses (8) (5) 60 (13) (9) 44 Other income 64 82 (22) 146 53 175 Total other operating income and charges 39 175 (78) 214 735 (71) Internal management revenue 18 25 (28) 43 61 (30) Total operating income 658 752 (13) 1,410 1,436 (2)

Operating expenses Employment expenses (159) (153) 4 (312) (248) 26 Brokerage and commission expenses (69) (67) 3 (136) (101) 35 Other operating expenses (178) (192) (7) (370) (275) 35 Total operating expenses (406) (412) (1) (818) (624) 31 Non-controlling interests1 9 1 * 10 1 * Net profit contribution 261 341 (23) 602 813 (26)

Non-GAAP metrics Assets under management ($A billion) 305.1 312.5 (2) 305.1 311.0 (2) Headcount 1,457 1,525 (4) 1,457 1,610 (10)

1 The non-controlling interests category adjusts reported consolidated profit or loss for the share that is attributable to non-controlling interests, such that the net profit or loss contribution represents the net profit or loss attributable to ordinary equity holders.

Macquarie Funds’ net profit contribution of $A602 million for the year ended 31 March 2011 decreased 26% from $A813 million in the prior year. The prior year included significant gains from listed fund initiatives, while the year ended 31 March 2011 benefited from the full year effect of the acquisition of Delaware Investments in January 2010. Excluding the gains from listed fund initiatives in both years, net profit contribution increased 105%.

31

Net interest expense

Net interest expense of $A120 million for the year ended 31 March 2011 increased 17% from $A103 million in the prior year. This was primarily driven by the full year effect of funding of the investment in Delaware Investments and higher interest rates on MFG’s other investments.

Base fees

Base fee income of $A873 million for the year ended 31 March 2011 increased 25% from $A697 million in the prior year. The increase in base fee income was largely a result of the full year effect of the acquisition of Delaware Investments, which increased AUM by $A151 billion in January 2010. The increase in AUM was partially offset by decreases due to listed fund initiatives undertaken including Macquarie Airports and Macquarie Infrastructure Group, and the strengthening of the Australian Dollar against major currencies.

Refer to Section 7 for details of Macquarie Funds’ AUM and Equity under Management.

Performance fees

Performance fee income of $A30 million for the year ended 31 March 2011 increased 36% from $A22 million in the prior year. The increase is primarily due to additional performance fees from the sale of co-investments and a performance fee from Macquarie Atlas Roads.

Mergers and acquisitions, advisory and underwriting fees

Mergers and acquisitions, advisory and underwriting fees of $A21 million for the year ended 31 March 2011 decreased 46% from $A39 million in the prior year. Fees earned in the prior year primarily related to listed real estate funds transactions. The majority of the Australian listed real estate funds management platform was sold to Charter Hall Group in March 2010.

Other fee and commission income

Other fee and commission income includes distribution service fees earned by Delaware Investments, structuring fees, capital protection fees, income from True Index products and internal fees received for managing and administering investment products on behalf of Banking and Financial Services.

Other fee and commission income of $A199 million for the year ended 31 March 2011 increased 66% from $A120 million in the prior year mainly due to distribution service fees in the Delaware Investments business, which offset associated expenses that, for accounting purposes, are recognised in brokerage and commissions expense.

Share of net profits/(losses) of associates and joint ventures using the equity method

Net equity accounted profits of $A112 million for the year ended 31 March 2011 compare with a loss of $A170 million in the prior year. The result in the prior year was driven by the significant market disruption associated with the global financial crisis and the resultant deterioration of the underlying results of the investments held by funds. The prior year also included equity accounted losses of $A82 million related to fees paid by MAp Group, Southern Cross Media Group and Macquarie Infrastructure Group to terminate management arrangements with Macquarie. The profit for the year ended 31 March 2011 reflects improved economic and operating conditions for the investments.

Impairment charge/writeback on equity investments

Impairment charges on equity investments of $A23 million for the year ended 31 March 2011 primarily relate to the writedown of unlisted investments. The writeback of impairment charges of $A31 million in the prior year primarily related to Macquarie Infrastructure Company and Southern Cross Media Group.

Macquarie Group Limited Management Discussion and Analysis macquarie.com.au

3.0 Segment analysis continued

32

Gain/(loss) on acquiring, disposing and change in ownership interest in subsidiaries and businesses held for sale

The gain on acquiring, disposing and change in ownership interest in subsidiaries and businesses held for sale of $A238 million in the prior year primarily related to income from the sale of Macquarie Communications Infrastructure Management Limited, income in relation to the internalisation of management of Ardent Leisure Group and income from the sale of the majority of the Australian listed real estate funds management platform to Charter Hall Group. There were no significant items in the year ended 31 March 2011.

Gain on reclassification of retained investments

In early September 2010, Macquarie lost significant influence over MAp Group and consequently reclassified its retained investment to available for sale. On reclassification, Macquarie was required to re-measure its retained stake in MAp Group to fair value. The gain on reclassification of this investment was $A95 million.

Sale of management rights

Income from the termination of management arrangements of $A14 million in the year ended 31 March 2011 related to the sale of the management rights of Macquarie Power and Infrastructure Corporation. Fees to terminate management arrangements of $A428 million in the prior year related to the sale of the management rights of MAp Group ($A345 million), Macquarie Infrastructure Group ($A42 million) and Southern Cross Media Group ($A41 million).

Other income

Other income of $A146 million for the year ended 31 March 2011 increased significantly from $A53 million in the prior year. The income for the year ended 31 March 2011 included distributions from MAp Group of $A83 million subsequent to its reclassification from an investment in associate to an available for sale investment. Other income also included a gain on the disposal of MFG’s investment in Intoll ($A11 million).

Operating expenses

Total operating expenses of $A818 million for the year ended 31 March 2011 increased 31% from $A624 million in the prior year.

Employment expenses increased 26% from $A248 million to $A312 million mainly as a result of the full year effect of the acquisition of Delaware Investments in January 2010.

Brokerage and commission expenses of $A136 million for the year ended 31 March 2011 increased 35% from $A101 million in the prior year. The increase in brokerage and commission expenses is primarily related to distribution expenses in the Delaware Investments business that offset related distribution service fee income that, for accounting purposes, is recognised in other fee and commission income.

Other operating expenses increased 35% from $A275 million to $A370 million mainly as a result of the full year effect of the acquisition of Delaware Investments in January 2010.

33

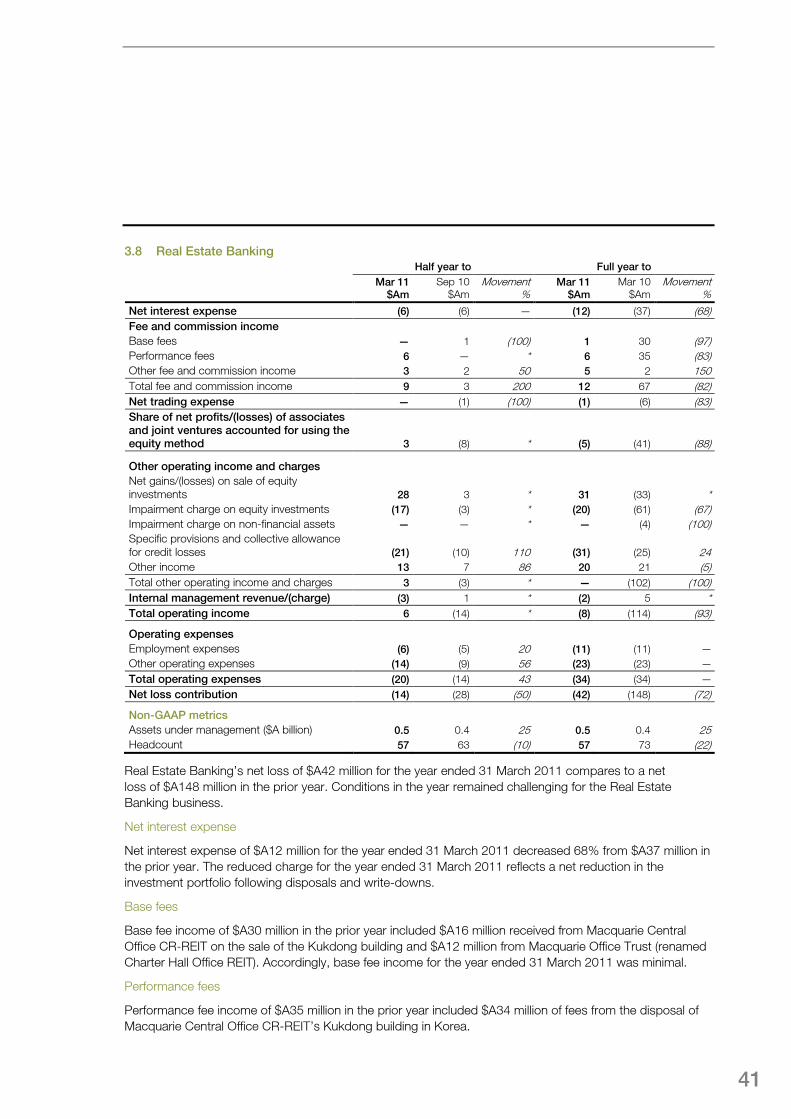

3.5 Fixed Income, Currencies and Commodities

Half year to Full year to Mar 11

$Am Sep 10

$Am Movement

% Mar 11

$Am Mar 10

$Am Movement

%

Net trading income (including net interest income)1,2 Commodities3 421 197 114 618 671 (8) Foreign exchange products 25 13 92 38 93 (59) Interest rate products 136 150 (9) 286 352 (19) Fair value adjustments relating to leasing contracts3 15 (32) * (17) 42 * Total net trading income (including net interest income) 597 328 82 925 1,158 (20) Fee and commission income Brokerage and commissions 45 42 7 87 69 26 Other fee and commission income 39 45 (13) 84 86 (2) Total fee and commission income 84 87 (3) 171 155 10 Share of net profits of associates and joint ventures accounted for using the equity method — 15 (100) 15 11 36 Other operating income and charges Net gains on sale of equity investments 87 52 67 139 64 117 Impairment charge on equity investments (7) (2) 250 (9) (3) 200 Specific provisions and collective allowance for credit losses 1 12 (92) 13 (53) * Other income 77 30 157 107 29 269 Total other operating income and charges 158 92 72 250 37 * Internal management revenue 28 27 4 55 80 (31) Total operating income 867 549 58 1,416 1,441 (2)

Operating expenses

Employment expenses (179) (123) 46 (302) (209) 44 Brokerage and commission expenses (82) (91) (10) (173) (138) 25 Other operating expenses (198) (168) 18 (366) (267) 37

Total operating expenses (459) (382) 20 (841) (614) 37 Net profit contribution 408 167 144 575 827 (30)

Non-GAAP metrics Headcount 980 953 3 980 884 11

1 The relative contribution of net interest income and trading income to income from trading activities can vary from period to period depending on the underlying trading strategies undertaken by Macquarie and its clients. As such, to obtain a more complete view of Fixed Income, Currencies and Commodities’ trading activities, net interest income has been combined with trading income above. The categories of trading income above are based on business lines within Fixed Income, Currencies and Commodities.

2 There were no impairments taken through trading income for the year ended 31 March 2011 (31 March 2010: $A20 million). 3 Macquarie enters into various tolling agreements, capacity contracts and transportation agreements as part of its commodity

trading and hedging strategies. The contracts and agreements, which are managed on a fair value basis for financial and risk management purposes, are required to be accounted for on an accruals basis for statutory reporting purposes. This creates a measurement mismatch with related trading positions that are reported at fair value for statutory purposes. For the purposes of enabling comparison with prior periods, Commodities trading income is presented on a basis consistent with management reporting, and the reversal of the fair value adjustments relating to leasing contracts are presented separately to reconcile the result to the statutory presentation.

Macquarie Group Limited Management Discussion and Analysis macquarie.com.au

3.0 Segment analysis continued

34

Fixed Income, Currencies and Commodities’ (FICC) net profit contribution was $A575 million for the year ended 31 March 2011, a decrease of 30% from $A827 million in the prior year. Total operating income of $A1,416 million was down 2% from $A1,441 million in the prior year. FICC experienced challenging trading conditions and subdued client activity in a number of markets during the first half of the year with client activity beginning to show signs of improvement in the second half of the year. The 37% growth in operating expenses to $A841 million for the year ended 31 March 2011 from $A614 million in the prior year reflects the investment in new capabilities in credit sales and trading, the extension of these platforms from the US into Europe and the establishment of new capabilities in rates, currencies and credit sales and trading in Asia.

Commodities trading income