Machinery costs - atlas.massey.ac.nzatlas.massey.ac.nz/courses/EP/Section 9 Machinery Costs...

23

138.255 Section 9 [Type text] 1 Machinery costs

Transcript of Machinery costs - atlas.massey.ac.nzatlas.massey.ac.nz/courses/EP/Section 9 Machinery Costs...

138.255 Section 9 [Type text]

1

Machinery costs

138.255 Section 9 [Type text]

2

Machinery Costs

9.1. MACHINERY COSTS

In this section we shall be considering the overall costs of machinery on farms, horticultural units

and machinery operation by contractors.

Highly mechanised agriculture faces tighter margins through competitive market conditions while at

the same time being required to meet changing public demand in what we eat, and in

environmental conditions we must operate within. One relevant example is soil conservation, here

the introduction of technology has potentially made the farmers life easier and given some

cultivation techniques a realistic chance of success.

There is a continuing demand for more timely operations. Timeliness is very important and late

sowing can for example lead to significant yield losses. The spring of 2009 was a good example

where in the Manawatu very wet conditions led to delays in preparing ground for cultivation.

Farmers need to work out what machine capacity they need in order to get tasks completed on time.

The same goes for contractors who need to work out the time available to do the work and then

calculate their capacity requirements. There is also a demand for better processing techniques to

improve food quality, reduce residues of chemicals and nutrients, the importance of this grows with

the affluence of the consumer.

During the early stages of mechanisation, the fall in the size of the total workforce is accompanied

by an increase in tractor ownership. When farms are fully mechanised, further labour shedding is

associated with a reduction in tractor ownership but the average tractor power is increased to

maintain the total tractor power available.

Machinery now accounts for between 35 and 50% of the fixed costs on cropping farms for example.

Machinery management is the study of the selection, operation and replacement of farm machines,

the same techniques can be applied to most industries where a fleet of machinery needs to be

operated. Forestry, horticulture and amenity horticulture are further examples closely related to

agriculture. In these land based industries the picture is more complex than a factory based

enterprise for example because so many of our planning decisions revolve around uncertainty due to

the weather. There is also greater variability in terms of operating terrain .

Costs can be classified as “fixed” and “variable”.

Fixed costs are not dependent upon the level of use of the machine.

Variable costs are directly related to the use of the machine.

Fixed costs can include:

1. Depreciation

2. Interest on capital invested

138.255 Section 9 [Type text]

3

3. Road tax and licensing

4. Insurance

5. Housing (assuming it can be allocated)

Variable costs include:

1. Repair and maintenance required

2. Fuel and oil

3. Labour

When considering “whole” farm costs labour is treated as a fixed cost. However when comparing

machinery systems we tend to treat it as a variable cost as it varies between systems and we are

very often comparing different systems or systems with different capacity and we may need to

compare costs per hour or per hectare.

9.2 FIXED COSTS

9.2.1 DEPRECIATION

The value of a machine is reduced throughout it’s life for the following reasons:

1. Worn parts so the machine can no longer perform as it previously did.

2. Increase in power consumption, labour and repair costs.

3. Availability of new more efficient machines

4. Machine capacity becomes inappropriate

9.2.1.1 Calculation Methods

Straight Line

Diminishing Balance

Geometrically adjusted diminishing balance.

9.2.1.2 Straight Line Method

N

S.P.)(P.P.D

138.255 Section 9 [Type text]

4

where: D = Annual Depreciation

P.P. = Purchase price of machine $

S.P. = Salvage value at the end of the assumed life of the machine

N = Estimated life of the machine

Advantages / Disadvantages

Underestimates the fall in value of an asset in the early years of ownership.

It is very simple and will give a guide to cost if you are considering keeping the asset for a long period

or all of its life.

9.2.1.3 Diminishing Balance Method

SV P P d n. .( )1

where: SV = Residual or resale value

d = Annual depreciation rate

n = Age of the machine

Advantages / Disadvantages

Method favoured by the IRD. (although there is a great deal of debate about the actual rates). It

does reflect the drop in value in the first few year of ownership more closely but still not that

accurately. It is a simple method.

The table below shows the rates used in widely accepted models from the USA in the sixties and

seventies. There has been very little work in recent years. The number of observations is the number

of machine transactions involved in the study. Smaller surveys can be subject to higher error

margins. These models are a reflection of the economic conditions at the time. In difficult economic

times, sales of new equipment may be reduced, which can put pressure on the price of second hand

machinery.

138.255 Section 9 [Type text]

5

Estimated diminishing balance rates of depreciation. From ASABE Standards.

Category

Estimated depreciation rate

%

Average length of ownership years

Number of observations

Tractor 15 7 712

Combine 15 7 138

Balers 18 7 60

Potato Harvester 21 6 32

Forage Harvester 21 6 62

Sugar Beet Harvester 23 7 27

9.2.1.4 Geometrically adjusted method

Used by ASABE (American Society of Agricultural biological Engineers). It simply adds a first year

correction factor to reflect what happens when new machinery is used.

SV

PPSA SB n*

where: SA = First year correction factor

SB = Annual depreciation factor

Present standard expressed as: RVSV

PP =

Remaining value as a percentage of the original list price at the end of year n.

For

Tractors,

68(0.920)n

Combines, Self propelled windrowers, 64(0.895)n

Balers, Forage harvesters, blowers and self propelled sprayers,

56(0.885)n

All other field machines 60(0.885)n

Advantage: The method that most accurately reflects the reality of the situation.

138.255 Section 9 [Type text]

6

List the possible reasons for the large drop in initial value.

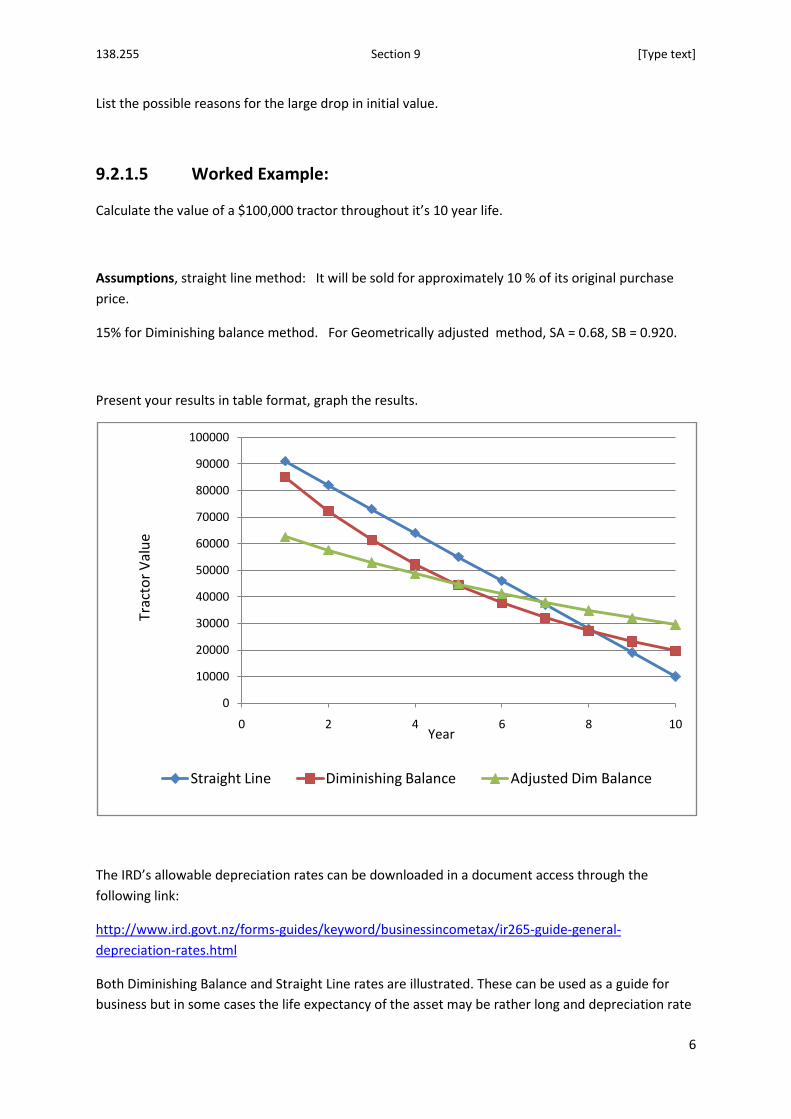

9.2.1.5 Worked Example:

Calculate the value of a $100,000 tractor throughout it’s 10 year life.

Assumptions, straight line method: It will be sold for approximately 10 % of its original purchase

price.

15% for Diminishing balance method. For Geometrically adjusted method, SA = 0.68, SB = 0.920.

Present your results in table format, graph the results.

The IRD’s allowable depreciation rates can be downloaded in a document access through the

following link:

http://www.ird.govt.nz/forms-guides/keyword/businessincometax/ir265-guide-general-

depreciation-rates.html

Both Diminishing Balance and Straight Line rates are illustrated. These can be used as a guide for

business but in some cases the life expectancy of the asset may be rather long and depreciation rate

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

0 2 4 6 8 10

Straight Line Diminishing Balance Adjusted Dim Balance

Year

Trac

tor

Val

ue

138.255 Section 9 [Type text]

7

used low. There is the provision to use a 20% loading but with some specialized machinery this may

not actually depict the true value. An example of this are self propelled forage harvesters. These are

expensive machines used almost entirely by contractors, The problem is that because contractors

require complete reliability from these machines there is no interest in secondhand machines once

the initial 2 to 3 seasons have been completed. Some of the manufacturers have deals where they

will refurbish the machine after 3 seasons in order to maintain reliability. If one of these machines

fail then it can be extremely expensive to repair and most parts are no longer held within New

Zealand, so there can be delays for clients, which is unacceptable. Contractors also use lease options

where they don’t actually own the machine but simply pay a fee for using it. Although these are

high cost machines to run leasing may be best in terms of regular outgoings which makes cashflow

budgeting easier.

9.2.2 INTEREST ON CAPITAL

Most machinery is purchased using some form of hire purchase agreement.

If a machine is purchased from the company’s own capital, an opportunity cost is charged.

The capital to invest in new machinery is either borrowed or is used from the farmers own capital

reserves. In the latter case an opportunity cost is imposed to account for the loss of income forgone

by using the capital. This situation was becoming increasingly rare as an ever- increasing number of

138.255 Section 9 [Type text]

8

farmers were using hire purchase schemes to ease cash flow. The proportion of purchases

completed this way will depend on farm income and farmer confidence. Finance companies are

increasingly flexible regarding the term of the loan, with maximum borrowing period being the

assumed economic life of the asset.

Calculation of interest charges used to be done on the basis of calculating the interest on the

average amount owing. With spreadsheets it is now feasible either to schedule payments directly

from the loan agreement or calculate the repayments and interest given the interest rate.

With Excel you can use the IPMT function.

9.2.2.1 Excel IPMT Function

Returns the interest payment for a given period for an investment based on periodic and constant

payments

Syntax IPMT(Rate, per, nper, pv,fv,type)

Rate = Interest rate in period 12%

per = the particular period of the loan 1,2, ,10

nper = total number of payments 10

pv = is the present value of the total amount $40,000

Fv = is the future value $21,015.43

9.2.2.2 Interest Calculation

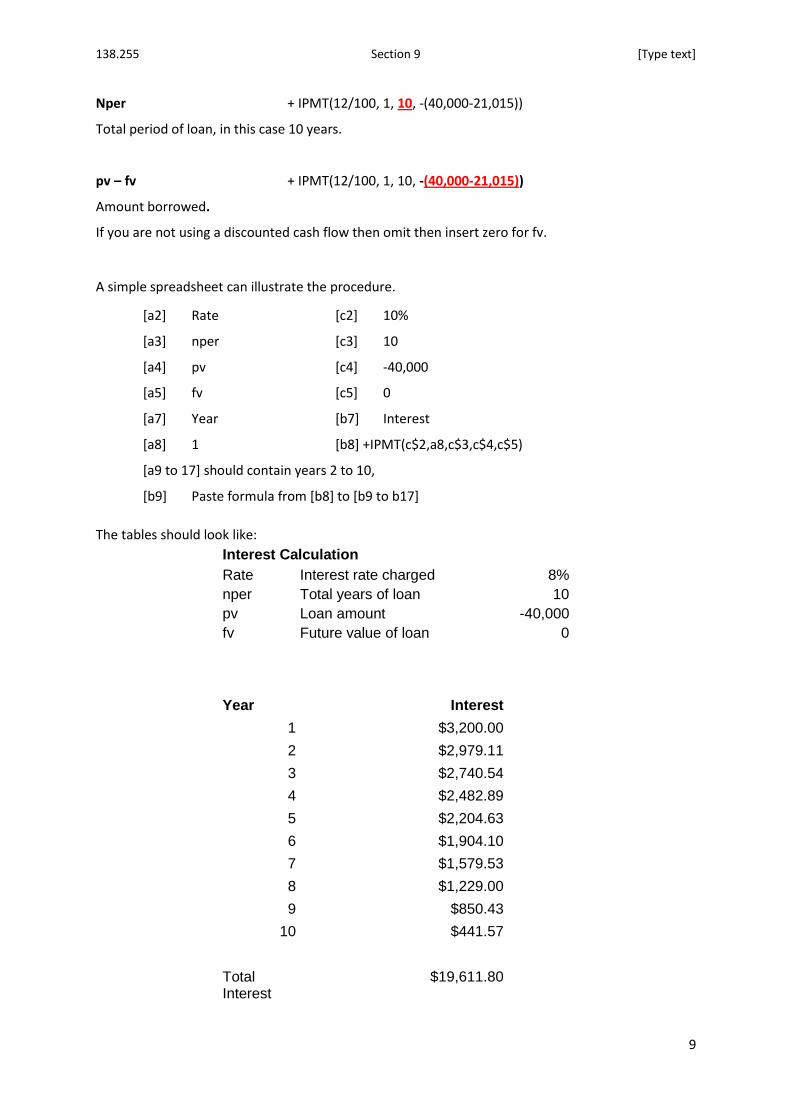

+ IPMT(12/100, 1, 10, -(40,000-21,015))

Returns the interest payment of the first year of the £18,985 loan

Rate + IPMT(12/100, 1, 10, -(40,000-21,015))

12% per year divided by 100 = 0.12.

per + IPMT(12/100, 1, 10, -(40,000-21,015))

Identifies the year in which the interest is calculated.

138.255 Section 9 [Type text]

9

Nper + IPMT(12/100, 1, 10, -(40,000-21,015))

Total period of loan, in this case 10 years.

pv – fv + IPMT(12/100, 1, 10, -(40,000-21,015))

Amount borrowed.

If you are not using a discounted cash flow then omit then insert zero for fv.

A simple spreadsheet can illustrate the procedure.

[a2] Rate [c2] 10%

[a3] nper [c3] 10

[a4] pv [c4] -40,000

[a5] fv [c5] 0

[a7] Year [b7] Interest

[a8] 1 [b8] +IPMT(c$2,a8,c$3,c$4,c$5)

[a9 to 17] should contain years 2 to 10,

[b9] Paste formula from [b8] to [b9 to b17]

The tables should look like:

Interest Calculation

Rate Interest rate charged 8%

nper Total years of loan 10

pv Loan amount -40,000

fv Future value of loan 0

Year Interest

1 $3,200.00

2 $2,979.11

3 $2,740.54

4 $2,482.89

5 $2,204.63

6 $1,904.10

7 $1,579.53

8 $1,229.00

9 $850.43

10 $441.57

Total Interest

$19,611.80

138.255 Section 9 [Type text]

10

9.2.3 Tax Insurance and Housing

These are often simply estimated as a percentage of the purchase price of the machine.

1. Road tax and licensing. Actual costs can be obtained from road licensing and tax.

2. Insurance If machinery is on a hire purchase agreement or financed in any way there may be a requirement to have it insured. A number of specialist insurers will give cover.

3. Housing (assuming it can be allocated) This may not be allocated to general machinery but some specialized machinery may have specific requirements. When running a fleet of machinery it would be wise to make provision for storage but this may be under general expenses rather than allocated to individual machines.

9.3 Machinery Running Costs (Variable Costs)

Variable costs. Costs directly attributable to specific enterprises. The main variable costs

are feeding stuffs (purchased and home-grown), veterinary and medicines, seeds

(purchased and home-grown), fertilisers, sprays and sundry livestock and crop costs.

For the purposes of running costs, our variable costs are:

Fuel and Oil cost

Repair and Maintenance cost

Labour cost

9.3.1 Fuel costs

In practical terms it is very difficult to give an exact figure for fuel consumption.

The fuel consumption of a tractor is governed by the amount of energy demanded at the

drawbar or through the Power Take-off Shaft (PTO).

Individual jobs vary. Tractors operate throughout the year on a range of tasks varying

from heavy duty work such as ploughing or forage harvesting to light chores.

Duty cycles vary within the same job. Even for ploughing, the fuel consumption of an

individual tractor varies considerably over the duty cycle and the average fuel

consumption is only ⅔ of the fuel consumption for peak power.

138.255 Section 9 [Type text]

11

Specific fuel consumption varies. Maximum fuel efficiency is achieved at 90% of

maximum power.

Fuel efficiency varies with engine loading and reaches a maximum at about 90% of

maximum power.

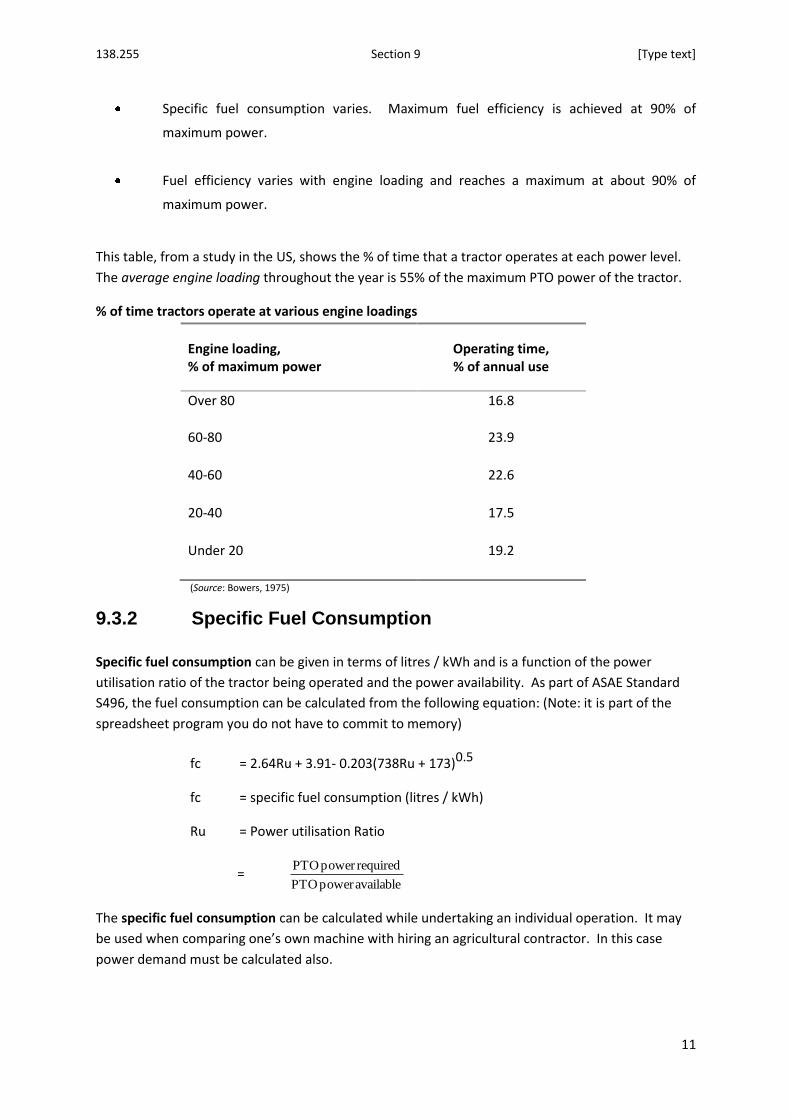

This table, from a study in the US, shows the % of time that a tractor operates at each power level.

The average engine loading throughout the year is 55% of the maximum PTO power of the tractor.

% of time tractors operate at various engine loadings

Engine loading, % of maximum power

Operating time, % of annual use

Over 80 16.8

60-80 23.9

40-60 22.6

20-40 17.5

Under 20 19.2

(Source: Bowers, 1975)

9.3.2 Specific Fuel Consumption

Specific fuel consumption can be given in terms of litres / kWh and is a function of the power

utilisation ratio of the tractor being operated and the power availability. As part of ASAE Standard

S496, the fuel consumption can be calculated from the following equation: (Note: it is part of the

spreadsheet program you do not have to commit to memory)

fc = 2.64Ru + 3.91- 0.203(738Ru + 173)0.5

fc = specific fuel consumption (litres / kWh)

Ru = Power utilisation Ratio

= availablepower PTO

requiredpower PTO

The specific fuel consumption can be calculated while undertaking an individual operation. It may

be used when comparing one’s own machine with hiring an agricultural contractor. In this case

power demand must be calculated also.

138.255 Section 9 [Type text]

12

9.3.3 Fuel Cost

FC = fc * P * pf

where:

FC = $/h

fc = specific fuel consumption l/kWh

P = equivalent PTO power required kW

pf = fuel price (……… $/litre)

The total annual fuel cost can be derived multiplying FC by the annual hours. Estimates of average

annual fuel consumption vary. Estimates range from 70% of the fuel consumption for peak power

from some references down to 40%. Clearly these differences in utilisation may be partly due to the

type of tractors being analysed and hence the work they are required to perform. An analysis from a

survey of tractor tasks according to power for Germany revealed that as power increases the

proportion of time spent on tillage also increases.

9.3.4. Average Annual Fuel Consumption

The average fuel consumption has been approximated from tractor test data. In the US the main

testing station is the Nebraska Tractor Testing Centre which is situated at Nebraska State University.

Website: http://tractortestlab.unl.edu/

Average fuel consumption is approximated as Qavg = 0.305 x P pto

where Qavg is average fuel consumption in L/h

and Ppto is maximum PTO power in kW.

Fuel consumption is clearly dependent on the use of the tractors and machinery. Tractor use in

Germany (Estimation excluding dairy farms) shows the allocation of tractors hour against the engine

power. Larger tractors spend more time on tillage while smaller tractors spend more time on

applying fertiliser and front end loading and other on-farm servicing operation. A similar trend is

likely in New Zealand.

138.255 Section 9 [Type text]

13

(Source: Renius, 1987, 1992)

9.3.5. Typical Fuel Requirements.

Typical fuel requirements for individual field operations is given in this table

Operation Fuel consumption

l/ha

Subsoiling

Ploughing

Heavy cultivation

Light cultivation

Rotary cultivation

Forage harvesting

Combine harvesting

Potato harvesting

15

21

13

8

13

15

11

21

9.3.6. Oil Costs

Oil costs typically represent about 5% of the fuel consumption costs.

Oil consumption is defined as the volume of engine crankcase oil per hour replaced at the

manufacturer’s recommended change intervals.

It is assumed that engine oil is replaced every 200 hours of use. Maybe less in dusty conditions or

when the engine is working at peak load.

OC = Volume of oil every 200 hrs Cost $/litre

0

20

40

60

80

100

120

30 80 130

Sowing, plant protection & cultiv ation,

fertilizing, front end loading, on-farm

operations.A

Vera

ge t

ime p

ort

ion

Rated engine power (kW)

Harv esting

Transport

Tillage

138.255 Section 9 [Type text]

14

9.4 REPAIRS & MAINTENANCE

Repair costs are another important part of machinery costs. The more a machine is used, the

greater is its need for repairs.

However, some machine components have surfaces that rust, rot or otherwise deteriorate over the

years. Repair costs caused by deterioration, though not necessarily affected by the amount of use,

are still considered an operating cost.

The longer agricultural machinery is used, the more repairs are needed to maintain “reliability”.

Reliability is hard to measure with a formula as it expresses the amount of confidence placed in a

machine to perform without an unplanned time loss due to breakdown.

Repair costs should be considered as a necessary and important part of machinery ownership.

Repairs are essential in order to maintain a high level of reliability. Machinery repair costs consist of

the full financial outlay for parts and labour either at the dealers or on the farm. These charges are

in themselves non-standard; labour costs for main dealerships with well equipped workshops are

considerably higher than at a local garage, reflecting the different level of overheads. In addition,

the differences in operator care, in soils, in crops and in climate produce a broad range of repair

costs for similar machines. Ideally, an accurate record of repair and maintenance costs should be

kept for each machine on the farm. As a guide, however, average repair costs are influenced by the

size of the machine, as reflected by its price, and the amount of use.

With the growth in the average size of new tractors and machines, greater productivity is possible.

But this greater productivity means that it is even more important to avoid breakdowns or to be able

to make repairs quickly. Even one hour during periods of critical operations in farming is valuable,

e.g. a breakdown due to a planting delay can lead to yield loss but it is an indirect cost and does not

often feature.

Yield loss cost is probably more important than the direct cost of repairs. Make it a goal, once a

machine is purchased, to provide necessary maintenance and repairs to keep it running at a high

level of reliability.

Listed here are some of the factors affecting repair and maintenance costs:

Repair and maintenance costs are the single most difficult item to predict. There are so many

variable factors:

Work load.

Operator

Inherent machine qualities

Machine age

Operating conditions

138.255 Section 9 [Type text]

15

9.4.1 Sources of R&M costs

With any machine there are 4 main types of repairs:

Routine replacement of wearing parts

Typical examples of routine wear (or replacement) include ploughshares, discs, tine

points, tyres and batteries. Even with the best of care, replacement will be necessary

sooner or later.

But if a rigid maintenance schedule is followed and the equipment or machine is not

abused, an increase or 50% - 100% in parts life can result, depending on the nature of the

part.

Except for excessive abuse, the life of ploughshares, discs and other soil engaging parts is

usually determined by the soil characteristics. Other parts, like tyres and batteries, have

a life that is affected by maintenance and operating environment.

Repair of accidental damage

Machinery accidents can happen even with the best of operators. But carelessness or

rushing a job is far more likely to cause costly accidents. Unfortunately, these types of

accidents often involve a frame, axle, housing or some other part that is hard to replace.

Often these types of parts are not stocked by a dealer, or the total damage to the

machine is quite extensive.

With good management, few, if any, repairs of this nature are needed. Using good

judgement can eliminate most accidental breakage.

Repairs through operator neglect. (Neglecting overhaul and repairs)

Sometimes, the “time” is not taken to perform needed maintenance or minor repairs.

Neglected maintenance and minor repairs almost always lead to more serious problems.

Remember that putting off maintenance and minor repairs can be costly. Use a good

out-of-season repair programme, together with a rigid daily inspection and service

schedule, help avoid expensive repairs.

Routine overhauls

Machines are overhauled to replace worn or defective parts and restore original

performance. Overloading and poor maintenance practices can accelerate these repairs

by 100% or more. Records of repair costs compiled by the Agricultural Engineering

Department of the University of Illinois, in the US, showed that with good management,

repair costs can be reduced by 25% or more. Poor management can raise repair costs

25% above the average.

138.255 Section 9 [Type text]

16

Machinery is becoming more reliable through better quality standards during

manufacture.

Repair & maintenance costs increase towards the end of a machine's life.

The degree to which this happens depends on the complexity of the machine.

There have been a large number of surveys carried out to examine repair and maintenance costs.

Each survey proves one thing: there is a huge amount of variation; but there is certain agreement

regarding the best way to express these costs.

The general method has been to express cumulative repair and maintenance (R&M) costs as a % of

the purchase price of the machine, throughout the life of the machine. In the case of agricultural

tractors economic life is assumed to be between 10K and 12K hours, although some studies have

suggested an economic life as short as 7K hours. Because of the huge variation in the survey data

collected most models should only be used as a “rule of thumb”.

R&M Cost equation takes the general form:

TAR = Rf1(X)Rf2

Where TAR = Total Accumulated Repair costs expressed as a percentage of the purchase price

X = Accumulated hours / 1000

Rf1, Rf2, = Repair cost coefficients.

The ASAE has published a number of models in editions of the ASAE Yearbook. Most models have

followed the from of the above equation but the values of coefficients Rc1 & Rc2 have changed as

more data has become available and a newer generation of tractors is surveyed and the result has

been a reduction in expected R&M costs when expressed as a percentage of purchase price. This is

due increased reliability and quality of machine and better machinery management on farms in

some instances, or a combination of both.

9.4.2 Annual R&M Costs

Example calculation

A $100,000 tractor operates for 800 hours per year.

Rf1 = 0.007, Rf2 = 2

What are the accumulated R&M costs after 7 years?

TAR = 0.07(5600/1000)2

= 0.219 of initial purchase price

138.255 Section 9 [Type text]

17

= 0.219 100,000

= $21,900

Repair costs in year 7 = (Accumulated costs in year 7) minus (accumulated costs in year 6)

Cost after 6 years:

TAR = 0.007(4800/1000)2

= $16,128

Repair cost in year 7 = 21,900 - 16,128

= $5,772

Annual R&M Charges (800 hours of annual use)

Cumulative R&M Costs

$

$

0

2000

4000

6000

8000

10000

1 2 3 4 5 6 7 8 9 10YEAR

0

10000

20000

30000

40000

50000

1 2 3 4 5 6 7 8 9 10

YEAR

138.255 Section 9 [Type text]

18

9.5 LABOUR COSTS

Labour charge for machinery operations

= operator’s hourly rate (£) time required (hr)

Operator’s hourly rate should include

National Insurance

employer’s liability insurance

overtime

any other benefits

The labour charge for machinery operations costs are simply calculated by multiplying the operator’s

hourly rate by the time required. The operator’s hourly rate should include NI, employer’s liability

insurance, overtime and any other benefits.

This calculation for the labour charge infers that labour is available by the hour, on a casual basis,

whereas the real value of labour at the time for which it is required may be considerably higher

because of its opportunity cost. It may be necessary, e.g. to hire permanent staff to ensure their

availability at a critical time of the year. In such circumstances, the annual cost is more appropriate

than the hourly labour cost. Provided that this aspect of labour availability is borne in mind, the

hourly labour charge is an important component of machinery operating costs for systems

comparisons at the enterprise level.

9.6 PUTTING IT ALL TOGETHER

The operating costs of a tractor can be calculated by including:

Depreciation

Interest on Capital

Tax & Insurance

Repairs & Maintenance

Fuel & Oil

Labour

138.255 Section 9 [Type text]

19

9.6.1 SPREADSHEET EXAMPLE

Tractor Operating Costs per hour

When considering average operating cost, in this example, minimum cost in year 6.

Considering discount has a major effect as figures are based on list price.

Inflation has not been considered.

No account taken of extra inconvenience due to additional breakdown.

Economics should not be the only consideration.

9.7 Fleet Management

9.7.1 Two main tasks for machinery manager:

1) Calculate the optimum fleet for their needs.

2) Calculate the best replacement policy for individual machines.

Each part of the system will have it’s own issues to resolve, for example in terms of tractor selection

three stages could be considered:

Maximum tractor power demand

Tractor fleet size

Tractor power mix

10

20

30

1 2 3 4 5 6 7 8 9 10

Co

st/

h

Year

Av.

Annual

138.255 Section 9 [Type text]

20

State the main factors governing the above:

1)

2)

3)

The problem of selecting tractor power seems to dominate thinking and usually approached as being

an intuitive process. The problem with relying on intuition is that it is based on managerial

experience, takes years to learn and it is not readily transportable to other problems or scenarios.

Analytical procedures are now available to obtain a more accurate estimate of tractive performance

from particular soils, weather and tyre data can be used to predict machinery requirements.

9.7.2 TIME FRAME:

Most machinery assets have a life of 10 - 15 years, therefore there is a need for long term

planning.

It is not always possible to implement plans immediately, but the manager must always have

long term goals.

To ensure a reasonable degree of efficiency in mechanisation management over a long period it is

essential to have a long term plan for replacement of major capital items. It is best to try and spread

replacement fairly evenly even though machines will have different replacement periods.

Planning difficulties:

Farming, horticulture and forestry are subject to greater variability than other businesses,

State some of the sources of variability in these businesses:

9.7.3 RECENT RESPONSES TO CHANGE:

Changing cropping pattern in order to maximise the production of profitable crops.

Simplifying the machinery system required to service the range of crops grown.

Continued increase in farm size to achieve economies of scale.

Use of contractors, machinery rings and machinery hire to reduce capital investment.

138.255 Section 9 [Type text]

21

9.7.4 ACHIEVING A BALANCE

Optimum machinery management is achieved when the overall profitability of the farm is

maximised. This economic goal is not necessarily the equivalent to minimising machinery costs for a

number of reasons.

Over mechanisation: Higher costs particularly fixed costs.

Under mechanisation: Physical requirements of the farm are not met. Financial

performance deteriorates.

As mentioned previously margins in agriculture have tended to decline in the long term.

Implications for mechanisation planning are clear. When setting up a mechanised system the whole

farm needs to be examined and maybe changed. A further response has been greater specialisation

leading to major changes in work patterns.

9.7.5 CHANGES IN WORK PATTERN

Desired change in an economic sense can cause other difficulties, concentration of work

pattern is a particular problem for cropping systems. For example in Europe

In trying to improve economic performance farmers have increasingly specialised in one

crop or one crop group. For example winter wheat is being grown more and more at the

expense of spring cereals but this has led to an increased concentration in work load.

Consequences of this are:

A larger percentage of the farm is dealt with using one machinery set.

Increased timeliness pressure because of the predominance of one cropping pattern.

These two factors make it more difficult to maximise the utilisation of resources such as machinery.

9.7.6 EFFECT OF FARM SIZE

List some of the effects of farm size

Larger farms have been more successful at reducing mechanisation costs

State possible reasons for this:

138.255 Section 9 [Type text]

22

9.8 REFERENCE MATERIALS:

Available in the library:

Lincoln University, Financial Budget Management 2002

Choosing and using Farm Machinery. Brian Witney.

Read the farm machinery sections in some of the following:

Farmers Weekly

Power Farming

Rural news, etc. etc.

138.255 Section 9 [Type text]

23