Macedonia Gap Analysis May 2013 · Macedonia Gap Analysis Update ... , the EC notes that the...

29

1 Macedonia Gap Analysis Update Strategic Planning and Analysis Division, Program Office, E&E Bureau, USAID May 2013 Introduction This analysis is intended to update and build on our September 2012 gap analysis of Macedonia, and focus largely on where new data and new evidence have emerged since September 2012. Primary sources for this analysis include the EBRD, Transition Report (November 2012), the World Bank, World Development Indicators (latest online), World Bank, Doing Business (2013), the IMF, World Economic Outlook (April 2013), IMF, Central, Eastern and Southeastern Europe: Regional Economic Issues (April 2013), the Economist Intelligence Unit, Macedonia Country Report (first quarter 2013), Freedom House, Freedom in the World (January 2013), and the European Commission, Macedonia: Implementation of Reforms within the Framework of the High Level Accession Dialogue (April 2013). Highlights of Findings Reforms. Macedonia continues to lead the Balkans in macroeconomic reforms and is among the reform leaders in the Balkans in democratic reforms (Figure 1). Progress in macroeconomic reforms continues to be modest albeit steady in Macedonia and generally throughout the Balkans (Figures 2 and 3). According to the EBRD (November 2012), Macedonia advanced in financial sector reforms in 2012 and in competition policy and infrastructure reforms in 2011. The European Commission (EC) in its April 2013 report on the Implementation of Reforms in Macedonia noted that reforms (both economic and democratic) “continued to be carried out during the reporting period (i.e., from October 2012 to April 2013), despite the political crisis affecting the work of Parliament.” On economic reforms (or “strengthening the market economy”), the EC notes that the Macedonian government adopted in October 2012 an Action Plan for Youth Employment “that should help to tackle the problem of high level of youth unemployment by promoting more and better jobs for young people. The plan includes both structural and active measures.” In addition, a December 2012 amendment to the labor market laws focuses on improving labor market statistics and better identifying the real number of unemployed. Amendments to the Company law were also adopted by Parliament in December 2012, aimed at improving market exit of firms. According to the World Bank’s Doing Business dataset, Macedonia’s business environment (or microeconomic reforms) continues to be among the most favorable in E&E and in the world (Figures 4 and 5). Out of 185 countries, Macedonia ranks 23 nd . In E&E, only Estonia and Georgia have more favorable business environments by these measures. Macedonia’s progress in these reforms has been substantial in recent years; from nearly a 50 th percentile rank in 2006 to close to a 90 th percentile rank by 2011, and remaining the same in 2012. The most problematic constraints (or at least the constraints with the worst rankings) for businesses in Macedonia are “getting electricity” (101), “trading across borders” (76), “dealing with construction permits” (65), “resolving insolvency” (60) and “enforcing contracts” (59).

Transcript of Macedonia Gap Analysis May 2013 · Macedonia Gap Analysis Update ... , the EC notes that the...

1

Macedonia Gap Analysis Update

Strategic Planning and Analysis Division, Program Office, E&E Bureau, USAID

May 2013

Introduction

This analysis is intended to update and build on our September 2012 gap analysis of Macedonia, and

focus largely on where new data and new evidence have emerged since September 2012. Primary

sources for this analysis include the EBRD, Transition Report (November 2012), the World Bank, World

Development Indicators (latest online), World Bank, Doing Business (2013), the IMF, World Economic

Outlook (April 2013), IMF, Central, Eastern and Southeastern Europe: Regional Economic Issues (April

2013), the Economist Intelligence Unit, Macedonia Country Report (first quarter 2013), Freedom House,

Freedom in the World (January 2013), and the European Commission, Macedonia: Implementation of

Reforms within the Framework of the High Level Accession Dialogue (April 2013).

Highlights of Findings

Reforms. Macedonia continues to lead the Balkans in macroeconomic reforms and is among the reform

leaders in the Balkans in democratic reforms (Figure 1). Progress in macroeconomic reforms continues

to be modest albeit steady in Macedonia and generally throughout the Balkans (Figures 2 and 3).

According to the EBRD (November 2012), Macedonia advanced in financial sector reforms in 2012 and in

competition policy and infrastructure reforms in 2011. The European Commission (EC) in its April 2013

report on the Implementation of Reforms in Macedonia noted that reforms (both economic and

democratic) “continued to be carried out during the reporting period (i.e., from October 2012 to April

2013), despite the political crisis affecting the work of Parliament.” On economic reforms (or

“strengthening the market economy”), the EC notes that the Macedonian government adopted in

October 2012 an Action Plan for Youth Employment “that should help to tackle the problem of high level

of youth unemployment by promoting more and better jobs for young people. The plan includes both

structural and active measures.” In addition, a December 2012 amendment to the labor market laws

focuses on improving labor market statistics and better identifying the real number of unemployed.

Amendments to the Company law were also adopted by Parliament in December 2012, aimed at

improving market exit of firms.

According to the World Bank’s Doing Business dataset, Macedonia’s business environment (or

microeconomic reforms) continues to be among the most favorable in E&E and in the world (Figures 4

and 5). Out of 185 countries, Macedonia ranks 23nd. In E&E, only Estonia and Georgia have more

favorable business environments by these measures. Macedonia’s progress in these reforms has been

substantial in recent years; from nearly a 50th percentile rank in 2006 to close to a 90th percentile rank by

2011, and remaining the same in 2012. The most problematic constraints (or at least the constraints

with the worst rankings) for businesses in Macedonia are “getting electricity” (101), “trading across

borders” (76), “dealing with construction permits” (65), “resolving insolvency” (60) and “enforcing

contracts” (59).

2

While democratic reforms in Macedonia are relatively advanced by Balkan standards, progress in these

reforms has largely stagnated since at least 2009, according to Freedom House (Figure 6). In 2011,

according to Freedom House in its Nations in Transit report, independent media and national

governance regressed in Macedonia, while all other democratic reform dimensions showed no

measurable change. 2012 democratic reform scores from Freedom House’s Nations in Transit report

will not be available until June 2013. In the meantime, and as rough proxy, we draw on Freedom

House’s political rights and civil liberties scores in its Freedom in the World report (January 2013), which

provides for broad democratization trends in the world in 2012. According to these data, Macedonia

made no gains in democratization in 2012; and in fact, across the Balkans, only Bosnia‐Herzegovina saw

measurable progress in democratization in 2012.

The EC, in its April 2013 report on Macedonia: Implementation of Reforms, provides a more nuanced

analysis of some trends in democratic reforms in Macedonia since September 2012. Overall, progress

and change has been mixed. From end‐December 2012 to end‐February, Macedonia experienced a

political stalemate which adversely affected the functioning of the Parliament and the organization of

local elections. The political crisis arose out of events which took place in the Parliament on December

24, 2012 and entailed the forcible removal of opposition political leaders as well as journalists. Despite

these events and this context, the EC reports some gains in media (including the adoption of an

amendment to the Criminal Code which decriminalized defamation and insult, and progress towards

training judges, lawyers, journalist and other practitioners on freedom of expression), in rule of law

(including modest gains in the capacity of the Supreme Court and the Administrative Court to handle

caseloads), and in electoral reform (including the adoption of amendments to the Electoral Code and the

Law on Financing of Political Parties).

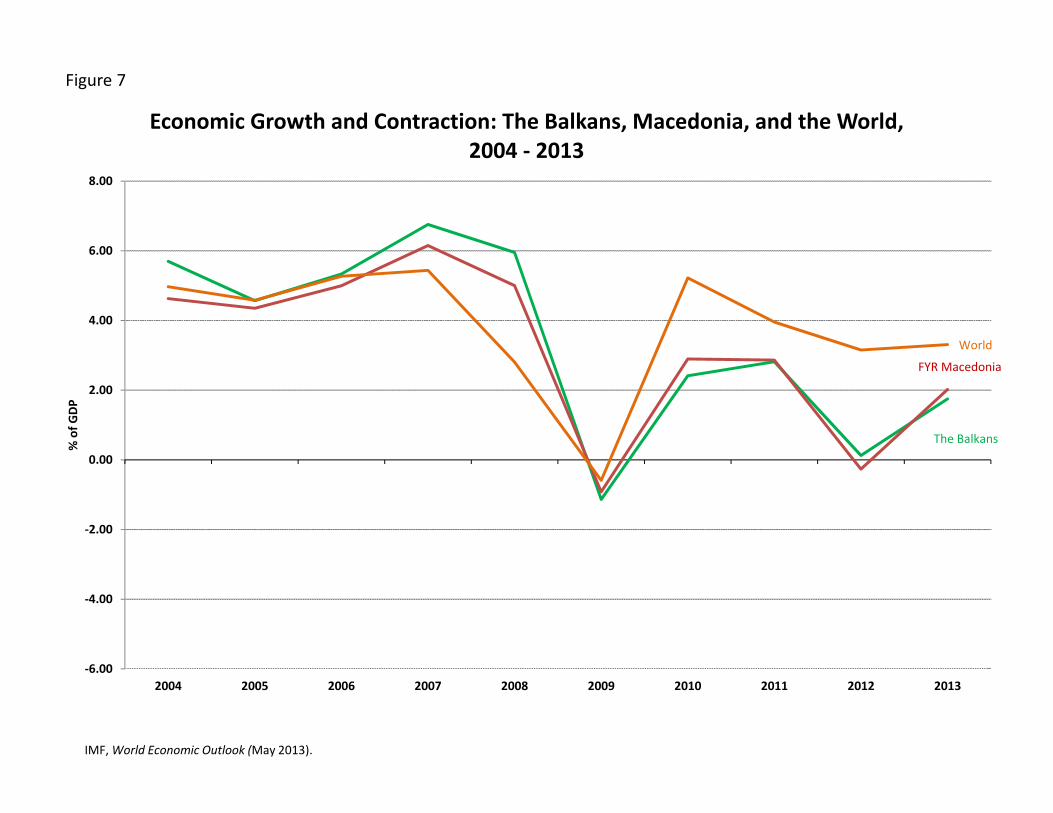

Macroeconomic performance. The pattern of economic growth in Macedonia has been very similar to

the pattern of growth in the Balkans, particularly since the global financial crisis in 2008‐2009 (Figure 7).

Economic growth in Macedonia (and the Balkans) was roughly comparable or greater than worldwide

economic growth in the immediate years leading up to the global financial crisis. Since 2009, however,

economic performance in Macedonia and throughout the Balkans has lagged significantly behind the

global norm, or, in other words, has been significantly worse in post‐ global crisis years compared to pre‐

global crisis years. In fact, Macedonia’s economy witnessed a recession in 2012, on the heels of the

2009 recession, and economic output overall in the Balkans was stagnant in 2012. The ongoing Euro

Area economic crisis is likely playing a very large role in the economic output stagnation in the Balkans.

Figure 8 supports this observation by highlighting the apparent close link between economic output

trends in Western Europe and Eastern Europe, closer post‐crisis than pre‐crisis.

The detrimental impacts of the Euro Area on Macedonia’s economy have been transmitted primarily

through weaker export demand, lower foreign direct investment (FDI), decreased bank credit flows, and

reduced remittances. Both the EIU (first quarter 2013) and the IMF (April 2013) have noted that a main

driver of economic growth in Macedonia (and in the Balkans more broadly) leading up to the global

financial crisis was the substantial influx of foreign capital, both FDI and bank credit flows. Since 2009,

according to the EIU, FDI flows to the Balkans have essentially collapsed. After reaching a record high of

$36.5 billion in 2008, FDI inflows plummeted to $16.5 billion in 2009 and again to $8.5 billion in 2010.

3

The EIU estimates FDI inflows to the Balkans in 2012 at $9.7 billion, or about one‐fourth the inflows

experienced in 2008. According to World Bank data, FDI inflows as a percent of GDP in Macedonia from

2004‐2008 averaged 6%; from 2009‐2011, it was significantly lower, 3.6% of GDP.

Almost half of Macedonia’s exports go to Western Europe (48% in 2011 to EU‐15), and almost one‐

fourth of Macedonia’s exports go to other countries in the Balkans (Figure 9). In other words, close to

three quarters of Macedonia’s exports go to economies currently mired in economic stagnation or crisis.

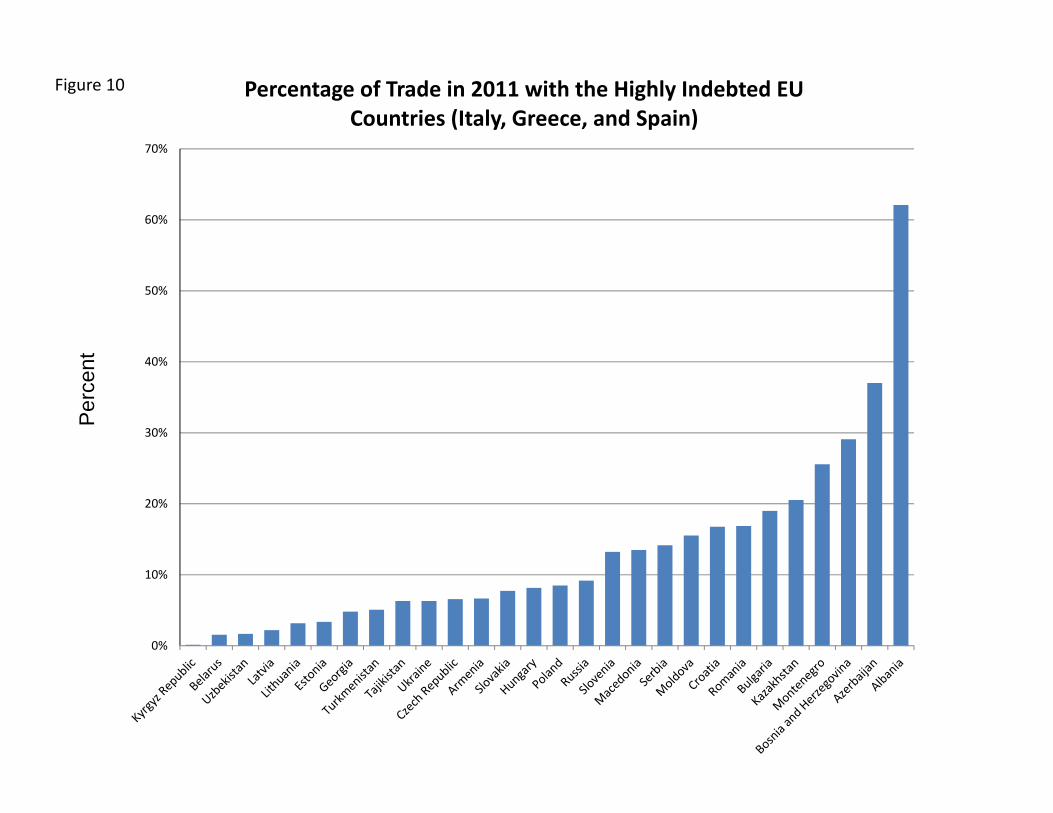

Economic exposure to the most vulnerable economies in Western Europe (specifically, to Italy, Greece,

and Spain) is high throughout the Balkans (at least through trade), particularly in Albania, Bosnia‐

Herzegovina, and Montenegro; and to a lesser though still significant extent in Macedonia (Figure 10).

The export sectors in the Balkans are small relative to GDP and have increased modestly in size since

2000 (Figure 11). Macedonia’s export share of GDP is larger than the Balkan average, though smaller

than the E&E graduates. After factoring in the fact that exports in Macedonia fell more than did GDP in

2012, there has been little if any growth of export share of GDP in Macedonia since 2000. Figure 12

underscores how little the Balkans trade relative to the other E&E sub‐regions. Figure 13 highlights that

Macedonia’s current account deficit is not nearly as problematic as elsewhere in the Balkans; nor is its

external debt particularly high relative to many E&E countries and nowhere near the order of magnitude

found in Greece, Italy, and Spain.

The labor market and physical and human capital. As noted in our September 2012 gap analysis, labor

market challenges continue to be substantial in Macedonia and throughout the Balkans. This includes

labor productivity which is dwarfed by labor productivity in the EU countries (Figure 14), and

unemployment rates which, while slowly decreasing, remain extraordinarily high (Figure 15). From

1995‐2009, labor productivity growth in Macedonia was slower than anywhere else in the Balkans

(Figure 14). The unemployment rate trends in Figure 15 show relatively little evidence of the 2008‐2009

global economic crisis, particularly in Macedonia, further underscoring the structural rather than cyclical

nature of unemployment in these economies. One explanation as to how it is possible that an economy

and society can maintain such extraordinarily high rates of unemployment sustained over the years is

that much employment is not sufficiently captured in the labor market statistics; much, in other words,

is found in the informal sector of the economy. This notion, in any event, is generally supported by the

measures of the shadow economy in Macedonia and elsewhere in Figure 16. In many countries where

unemployment rates are high, so too is the informal sector economic activity.

High unemployment rates in Macedonia and elsewhere in the Balkans are likely due to a combination of

demand and supply factors. On the demand side, sluggish economic growth and/or jobless growth no

doubt play a role. The low and slow growing labor productivity points to supply side issues. Low

productivity in turn is a function in large part of poor and/or eroding capital. Broadly defined, capital

refers to the physical, human, and, particularly in the context of the former communist countries, social

capital. Figures 17 and 18 show how low the physical capital stock is in the Balkans relative to the EU as

well as the E&E graduates. Fixed capital formation per labor force is six times higher in the EU than it is

in the Balkans (Figure 17); it is three times higher in the E&E graduates compared to the Balkans (Figure

18). These data also underscore that fixed capital formation per labor force has been very slow growing

in the Balkans.

4

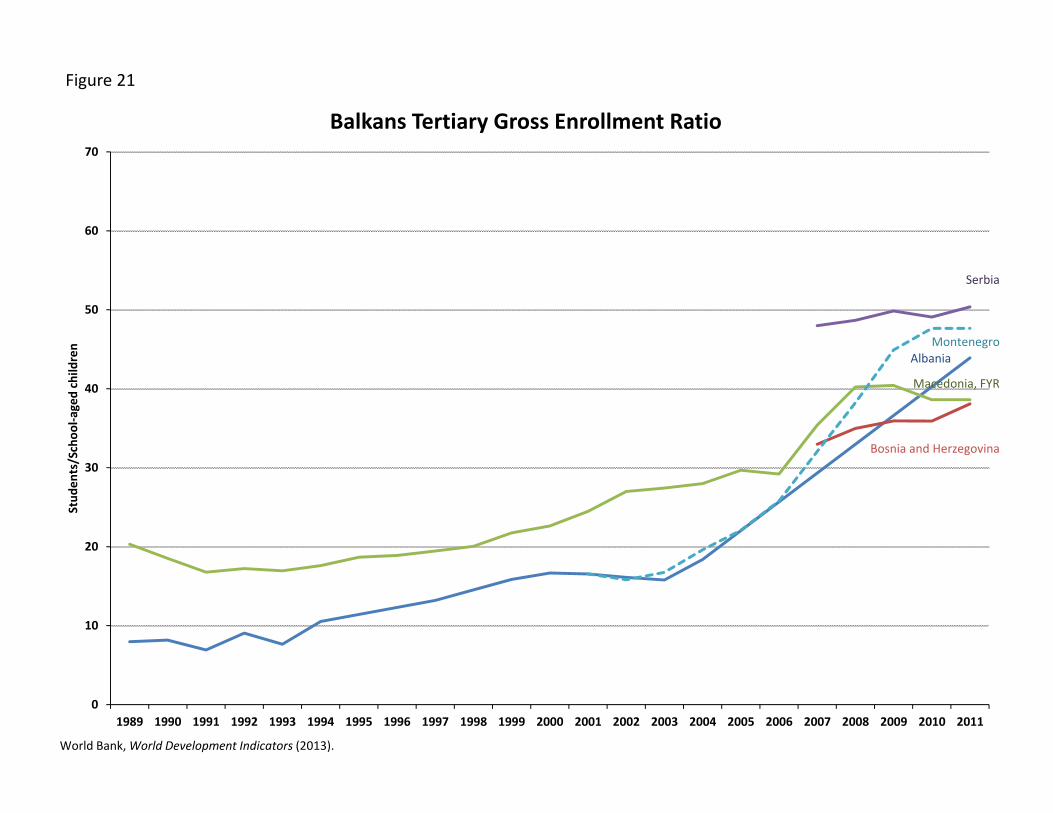

Figures 19‐24 address human capital aspects; i.e., trends in education. There continue to be a number

of indications that education challenges in Macedonia are significant. This includes tertiary enrollment

rates in Macedonia which are low by E&E standards, and a growth of these enrollments which has been

stagnant in recent years (Figure 21). Moreover, available evidence suggests that most of those enrolled

in tertiary education in Macedonia do not complete the education. According to World Bank data,

tertiary education enrollment was 40% in 2011. Yet only 15% of the population aged 30‐34 had

completed tertiary education by one survey (Figure 22).

As previously reported in our September 2012 gap analysis and in earlier analyses, Macedonia’s

education gap is due in part to relatively poor international test scores which reflect poorly on the

quality of Macedonia’s education system. New test scores emerged in early 2013 and correspond to

2011 performance in math (for 8th graders in forty‐two countries and 4th graders in fifty countries) and in

critical reading (for 4th graders in forty‐five countries). Macedonian 8th graders were included in the

math tests, in the Trends in Mathematics and Sciences Study or TIMSS 2013.

Figure 23 provides a sample of countries where 8th graders scored below the Intermediate International

Benchmark in 2011 in the TIMSS test. Figure 24 provides a sample of countries where the students

scored above the benchmark in 2011. The intermediate benchmark is one of four thresholds: advanced,

high, intermediate, and low. At the low benchmark (with a score of 400) students have some basic math

knowledge; they can add and subtract and read simple bar graphs and tables. At the intermediate

benchmark (with a score of 475), students can apply basic math knowledge in straightforward

situations; they can interpret bar graphs and tables to solve simple problems; i.e., a very basic threshold.

As shown in Figure 23, Macedonian 8th graders scored well below the intermediate benchmark in 2011,

closer to the low benchmark in fact. Moreover, these scores have been backsliding in Macedonia since

at least 1999. Of the ten E&E countries which participated in the TIMSS math tests for 8th graders in

2011, the students in Macedonia scored the lowest. In ascending order: Macedonia (426), Georgia

(431), Romania (458), Armenia (467), Ukraine (479), Kazakhstan (487), Lithuania (502), Slovenia (505),

Hungary (505), and Russia (539).

Macedonia Gap Analysis

USAIDE&E Bureau

Strategic Planning and Analysis DivisionMay 2013

Ratings are based on a 1 to 5 scale, with 5 representing most advanced worldwide. Freedom House, Nations in Transit (June 2012) and Freedom in the World (January 2013); and EBRD, Transition Report 2012 (November 2012).

Figure 1

Bulgaria

Croatia

Czech RepublicEstoniaHungary

LatviaLithuania

Poland

Romania

Slovak

Slovenia

Albania

Bosnia‐Herz

Kosovo

Macedonia

Montenegro

Serbia

Armenia

Azerbaijan

Belarus

Georgia

Moldova

Russia

UkraineKazakhstan

Kyrgyz Rep.

Tajikistan

Turkmenistan

Uzbekistan

1

2

3

4

5

1 2 3 4 5

Econ

omic Reforms

Democratic Reforms

Economic and Democratic Reforms, 2012

E&E Grads

Balkans

E&E Eurasia

CARs

Romania, Bulgaria, Croatia Threshold, 2006

Drawn from the EBRD Transition Report (2012 and earlier versions). The E&E Graduates (n=11) consist of Estonia, Hungary, Latvia, Lithuania, Poland, Slovakia, Slovenia, Czech Republic, Romania, Bulgaria, and Croatia. The Balkans (n=6): Albania, Bosnia & Herzegovina, Macedonia, Kosovo, Serbia, and Montenegro. E&E Eurasia (n=7): Armenia, Azerbaijan, Belarus, Georgia, Moldova, Russia, and Ukraine. The Central Asian Republics or the CARs (n=5): Kazakhstan, Kyrgyzstan, Tajikistan, Turkmenistan, and Uzbekistan.

Figure 2

E&E Graduates

Balkans

E&E Eurasia

CARs

1

1.5

2

2.5

3

3.5

4

4.5

5

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

1 to 5 Scale

Macroeconomic Reforms

Drawn from the EBRD Transition Report (2011 and earlier editions).

Figure 3

Albania

Bosnia & Herzegovina

Macedonia

Kosovo

Serbia

Montenegro

1

1.5

2

2.5

3

3.5

4

4.5

5

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

1 to 5 Scale

Macroeconomic Reforms in The Balkans

World Bank, Doing Business 2013 (2012). The analysis is based on 10 aspects: starting a business; dealing with construction permits; getting electricity; registering a property; getting credit; protecting investors; paying taxes; trading across borders; enforcing contracts; and resolving insolvency.

Figure 4

E&E Grads

The Balkans

Macedonia

0

10

20

30

40

50

60

70

80

90

100

2005 2006 2007 2008 2009 2010 2011 2012

Percen

tile Ra

nk

Business EnvironmentBe

tter Enviro

nmen

t

Figure 5

World Bank, Doing Business (2013), 185 countries are included in the analysis. The business environment is gauged based on 10 aspects: starting a business; dealing with construction permits; getting electricity; registering a property; getting credit; protecting investors; paying taxes; trading across borders; enforcing contracts; and resolving insolvency.

0

20

40

60

80

100

120

140

160

180

200

Rank

Business Environment in 2012

E&E Grads

The Balkans

E&E Eurasia

CARs

Others

Figure 6

Ratings from 1 to 5, with 5 representing greatest development of democratic reforms. Freedom House, Nations in Transit 2012; Freedom in the World, 2013.

E&E Graduates

Balkans

E&E Eurasia

CARs

Macedonia

1

1.5

2

2.5

3

3.5

4

4.5

5

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

1 to 5 Scale

Democratic Reforms

IMF, World Economic Outlook (May 2013).

Figure 7

The Balkans

FYR Macedonia

World

‐6.00

‐4.00

‐2.00

0.00

2.00

4.00

6.00

8.00

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

% of G

DP

Economic Growth and Contraction: The Balkans, Macedonia, and the World, 2004 ‐ 2013

IMF, World Economic Outlook (May 2013). The Euro Area consists of Austria, Belgium, Cyprus, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Malta, Netherlands, Portugal, Slovak Republic, Slovenia, and Spain.

Figure 8

The Balkans

FYR Macedonia

Euro Area

‐6.00

‐4.00

‐2.00

0.00

2.00

4.00

6.00

8.00

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

% of G

DP

Economic Growth and Contraction: The Balkans, Macedonia, and the Euro Area, 2004 ‐ 2013

IMF, Direction of Trade (2012).

Balkans12.38%

CARs0.00%

E&E Eurasia0.03%

E&E Grad2.34%

EU‐1568.28%

Other16.97%

Albania, Direction of Exports, 2011

Balkans23.05%

CARs0.71%

E&E Eurasia4.91%E&E Grad

13.69%

EU‐1548.11%

Other9.53%

Macedonia, Direction of Exports, 2011

Balkans19.22%

CARs0.13%

E&E Eurasia9.70%

E&E Grad25.96%

EU‐1536.10%

Other8.90%

Serbia, Direction of Exports, 2011

Balkans2.34%

CARs0.00%

E&E Eurasia1.60%

E&E Grad42.30%EU‐15

45.72%

Other8.04%

Bosnia and Herzegovina, Direction of Exports, 2011

Balkans3.78%

CARs0.00%

E&E Eurasia1.09%

E&E Grad40.98%EU‐15

39.82%

Other14.32%

Montenegro, Direction of Exports, 2011

Figure 9

Per

cent

0%

10%

20%

30%

40%

50%

60%

70%

Percentage of Trade in 2011 with the Highly Indebted EU Countries (Italy, Greece, and Spain)

Figure 10

World Bank, World Development Indicators (2013).

Figure 11

E&E Graduates

Balkans

Macedonia, FYR

0

10

20

30

40

50

60

70

80

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Percen

tage

of G

DP

Exports as a Percentage of GDP

Taken from IMF, Direction of Trade (2012).

Balkans1.51%

CARs6.85%

E&E Eurasia39.59%E&E Graduate

52.05%

% Total Exports from E&E Sub‐Regions, 2011Figure 12

EBRD, Transition Report 2010 and Transition Report 2012 and IMF, World Economic Outlook (2013).

ALB

B‐H

KOS

MAC

SER

KAZKYR

TAJ

TRK

UZB

RUS

ARM

BEL

GEO

MOL

UKRBUL

CRO

HUN

LAT

LITPOL

ROMSLK

SLV

EST

GREECE

SPAIN

ITALY

USA

0

20

40

60

80

100

120

140

160

180

200

‐20.0 ‐15.0 ‐10.0 ‐5.0 0.0 5.0 10.0

External Deb

t % of G

DP, 201

1

Current Accounts % of GDP, 3 Year Average 2010‐2012

Current Account Balance & External Debt in 2010‐2012

Balkans

CARs

E&E Eurasia

E&E Grad

Other

SurplusDeficit

MON (‐21.37,45.64)

AZE (25.08, 14.94)

Figure 13

I. Gill and M. Raiser, Golden Growth: Restoring the Luster of the European Economic Model, World Bank (2012).

0

10

20

30

40

50

60

70

80

90

1995 2009

Labor productivity in E&E vs. EU-15(constant 2005 US$, thousands)

Figure 14

Albania

Serbia

Montenegro

Bosnia and Herz

Macedonia

Kosovo

0

10

20

30

40

50

60

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Percen

tage

Unemployment Rates in the Balkans

Eurostat (2012) and IMF World Economic Outlook (2013). Data on Kosovo from European Commission, Kosovo 2010 Progress Report, Brussels, 9 November 2010.

Figure 15

Shadow EconomyPercentage of Official Economy (2007)

0

10

20

30

40

50

60

70

I. Gill and M. Raiser, Golden Growth: Restoring the Lustre of European Economic Model, World Bank (2012).

Per

cent

age

Figure 16

EU

Balkans

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Constant 200

5 USD

(PPP

)

Physical (Fixed) Capital per WorkerFigure 17

World Bank,World Development Indicators (2013).

World Bank,World Development Indicators (2013).

Alban

Macedonia

Serbia

Balkan

E&E Grad

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000

2005 2006 2007 2008 2009 2010

USD

/Worker

Fixed Capital Formation in Central and Eastern Europe (per labor force)

Figure 18

Upper secondary education includes ISCED 3, which is the final stage of secondary education. It begins at age 15‐16 and lasts three to five years. UNICEF, TransMONEE Database 2012 (Accessed 2‐12‐2013).

E&E Grads

Balkans w/o Kosovo

E&E Eurasia

CARs

Macedonia

0

20

40

60

80

100

120

Stud

ents/Schoo

l‐aged Ch

ildren

Upper Secondary Education Enrollment in Eastern Europe & Eurasia

Figure 19

E&E Grad

Balkans

E&E Eurasia

CARs w/o Turkmenistan

0

10

20

30

40

50

60

70

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Stud

ents/Schoo

l‐aged child

ren

Tertiary Gross Enrollment Ratio

World Bank, World Development Indicators (2013).

Figure 20

World Bank, World Development Indicators (2013).

Albania

Bosnia and Herzegovina

Macedonia, FYR

Serbia

Montenegro

0

10

20

30

40

50

60

70

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Stud

ents/Schoo

l‐aged child

ren

Balkans Tertiary Gross Enrollment Ratio

Figure 21

I. Gill and M. Raiser, Golden Growth: Restoring the Luster of the European Economic Model, World Bank (2012).

Tertiary Education Attainment

% of populationages 30‐34

0

5

10

15

20

25

30

35

EU15 E&E Graduates Serbia Macedonia Russia Armenia Ukraine

Figure 22

International Association for the Evaluation of Educational Achievement (IEA), Trends in International Mathematics and Sciences Study (TIMSS) (2013).

Intermediate International Benchmark

Oman

Indonesia

Romania

Macedonia

Thailand

Malaysia

360

380

400

420

440

460

480

500

520

1995 1999 2003 2007 2011

TIMSS Score

Functional Literacy: International Test Scores in Math for 8th Graders (Below the Benchmark)

Figure 23

IEA, TIMSS (2013).

Intermediate International Benchmark

South Korea

US

Lithuania

Russia

Slovenia

Hungary

440

460

480

500

520

540

560

580

600

1995 1999 2003 2007 2011

TIMSS Score

Functional Literacy: International Test Scores in Math for 8th Graders(Above the Benchmark)

Figure 24