LVT and AXI Philadelphia Task Force - Center for Study of ... PTRTF Presentation... · Land Value...

33

2009 [LVT AND AXI PHILADELPHIA TASK FORCE] Analysis and recommendations submitted to the Philadelphia Tax Reform Task Force Center for the Study of Economics 413 S. 10 th Street Philadelphia, PA 19147 Office: 215.923.7800 www.urbantools.org

Transcript of LVT and AXI Philadelphia Task Force - Center for Study of ... PTRTF Presentation... · Land Value...

2009

[LVT AND AXI PHILADELPHIA TASK FORCE] Analysis and recommendations submitted to the Philadelphia Tax Reform Task Force

Center for the Study of

Economics

413 S. 10th

Street

Philadelphia, PA 19147

Office: 215.923.7800

www.urbantools.org

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 2 Center for the Study of Economics | www.urbantools.org

Table of Contents

Introduction ....................................................................................... 3

City-Wide Values ................................................................................ 4

Land Value Taxation (LVT) .................................................................. 5

LVT Impact by Tax Class ................................................................ 6

LVT Impact by Council District .................................................... 11

Assessed Exemption of Improvements (AXI) ................................... 18

AXI Impact by Tax Class .............................................................. 18

AXI Impact by Council District ..................................................... 22

LVT and AXI by Neighborhood ......................................................... 28

Conclusions and Recommendations ................................................ 32

Supplemental Material .................................................................... 33

Table of Figures

Figure 1: Citywide Real Estate Assessment Totals ............................. 4

Figure 2: Revenue Neutrality Among Options ................................... 5

Figure 3: Overall Impact of LVT vs Current Tax .................................. 6

Figure 5: LVT Count of Increase vs. Decrease by Tax Class ................ 8

Figure 6: LVT Total Dollar Difference by Tax Class ............................. 9

Figure 7: LVT Average Dollar Difference by Tax Class ...................... 10

Figure 8: LVT Average Percent Change by Tax Class ........................ 11

Figure 9: LVT Residential Percentage Increase vs. Decrease by

Council District ................................................................................. 12

Figure 10: LVT Non-residential Percentage Increase vs. Decrease by

Council District ................................................................................. 13

Figure 11: LVT Residential Count of Increase vs. Decrease by Council

District .............................................................................................. 14

Figure 12: LVT Non-residential Count of Increase vs. Decrease by

Council District ................................................................................. 15

Figure 13: LVT Residential Average Dollar Difference by Council

District .............................................................................................. 16

Figure 14: LVT Non-residential Average Dollar Difference by Council

District .............................................................................................. 17

Figure 15: AXI vs Current Tax, Total and Average by Tax Class ........ 19

Figure 16: AXI Percentage Increase vs Decrease by Tax Class ......... 20

Figure 17: AXI Count of Increase vs Decrease by Tax Class ............. 21

Figure 18: AXI Residential Percentage Increase vs Decrease by

Council District ................................................................................. 22

Figure 19: AXI Non-residential Percentage Increase vs Decrease by

Council District ................................................................................. 23

Figure 20: AXI Residential Average Dollar Difference by Council

District .............................................................................................. 24

Figure 21: AXI Non-residential Average Dollar Difference by Council

District .............................................................................................. 25

Figure 22: AXI Residential Total Dollar Difference by Council District

.......................................................................................................... 26

Figure 23: AXI Non-residential Total Dollar Difference by Council

District .............................................................................................. 27

Figure 24: LVT Total Dollar Difference by Neighborhood ................ 28

Figure 25: LVT Average Dollar Difference by Neighborhood ........... 29

Figure 26: AXI Total Dollar Difference by Neighborhood................. 30

Figure 27: AXI Average Dollar Difference by Neighborhood ........... 31

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 3 Center for the Study of Economics | www.urbantools.org

Introduction

The Center for the Study of Economics is pleased to speak again before the Mayor’s Task Force. Testimony provided by many others and

ourselves has clearly narrowed the menu of choices to a few basic concepts: Philadelphia’s taxes are not progressive, they are too high, and

they are confusing and repellent to capital and labor. As Paul Levy said in earlier testimony we as a City must find a way to implement taxes

on subjects that are immobile. If that is where the taskforce moves, then we must repeat: land is immobile; buildings as an expression of

capital investment are mobile.

We believe that the facts and the theory point to a gradual shift and implementation of tax policy to one that removes most distortions that

effect personal, commercial and policy choices. To that end, we are happy to present summaries of our research into land value taxation,

and an alternative that relieves lower-end values properties of the burden of taxation, while maintaining revenue flows.

Using our BRT database from April 2009, we believe these simulations will provide a clear picture of how land value taxation and the

assessment exemption for improvement alternative1 will work:

1. By Citywide

2. By Class

3. By council District

4. By Neighborhood

11

Land Value Tax (LVT) is a way of taxing land using a change in tax rates. For example, a drop of 10% in the building tax rate would require that revenue loss be made up by an increase in the tax

rate on land values. The direct effect is to put a greater reliance on publicly created value (land) rather than privately created wealth (buildings, commerce, or wages). A higher tax on land has the

acknowledged effect of removing the distortions on markets that traditional taxes create. Assessment Exemption on Improvements (AXI) is slightly different. Put simply, a blanket permanent

abatement of a certain dollar amount on a building is put into effect. The overall tax rate then rises accordingly, with a greater impact on land value. For example, if a building is worth $50,000 and

the AXI is $50,000, there will be no tax on the building. If the building were worth $500,000 then the owner would pay tax on $450,000. This has the effect of sometimes dramatically reducing tax

burden on lower valued properties, most often residential properties

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 4 Center for the Study of Economics | www.urbantools.org

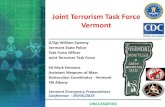

City-Wide Values

Using current BRT assessments, the city has to work with a total taxable value of $12.1 Billion, with $5.1 Billion of non-taxable value. The

value of taxable land is $2.9 Billion and the taxable value of buildings is $9.2 Billion.

The current combined tax rate applied to both land and buildings for city and school purposes is 82.64 mills. As many have thus far noted,

this tax system of equal tax rates on land and buildings creates a disincentive to build, rehab, or otherwise invest in real estate inside

Philadelphia’s borders. The 10-year tax abatement is an explicit acknowledgement of the high cost of construction in Philadelphia serving as

a barrier to it. We believe there are alternatives.

Figure 1: Citywide Real Estate Assessment Totals

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 5 Center for the Study of Economics | www.urbantools.org

Land Value Taxation (LVT)

The Center proposes two revenue neutral alternatives in these simulations. The first, land value taxation, (or LVT) employs tax rates of

171.684 mills on land value and 54.417 mills on building values, to provide revenue-neutrality. These rates would garner 50% of revenue

from land, and 50% of the revenue from buildings2. Figure 2 demonstrates revenue-neutrality for both alternatives compared to the current

system.

Figure 2: Revenue Neutrality among Options

2 These revenue split rates are identical to the Controller’s Tax Structure Report (2001) and the Tax Reform Commission Report (2003) simulations of land value taxation

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 6 Center for the Study of Economics | www.urbantools.org

LVT Impact by Tax Class Land Value Taxation (LVT) is the option discussed at the previous task force hearing on May 21, 2009. Figure 1 compares LVT to the current total and average tax

impact, both of which come out approximately the same.

Figure 3: Overall Impact of LVT vs. Current Tax

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 7 Center for the Study of Economics | www.urbantools.org

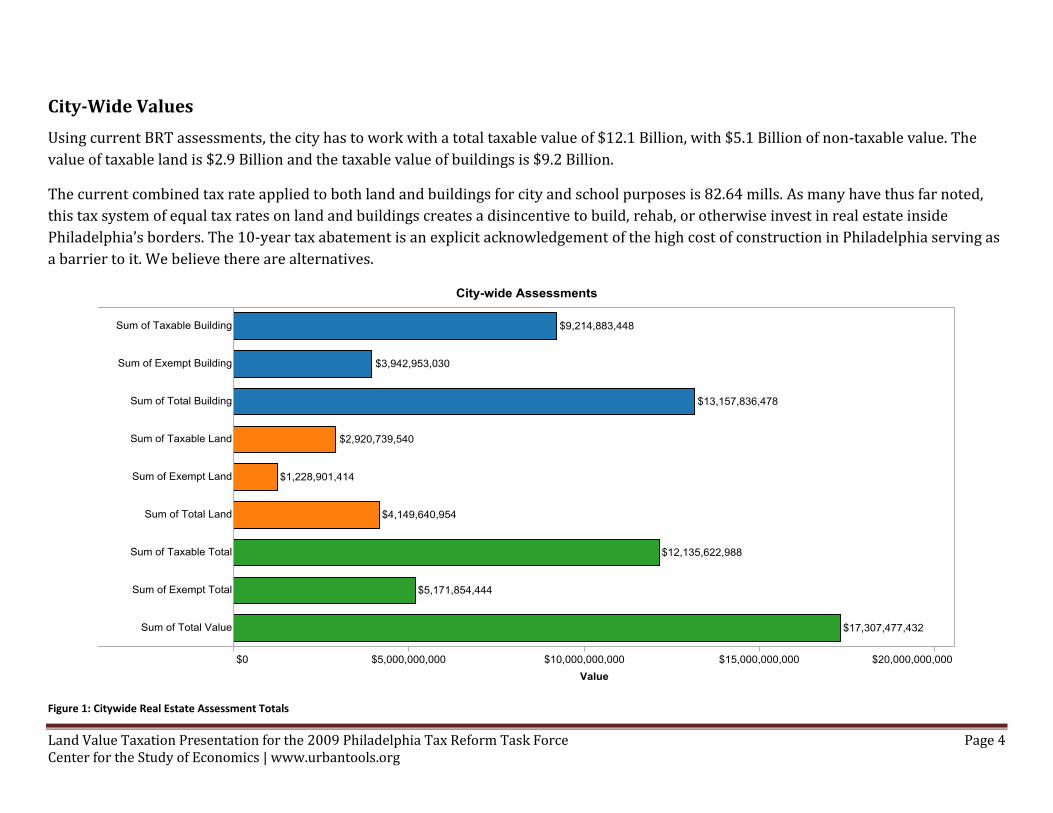

Figure 4 represents the change by class of property in Philadelphia. As every study or simulation of the past 20 years affirms, residential properties see a

reduction in tax incidence, while commercial and industrial properties – the sectors that have already departed the city–see an increase in liability.

Figure 4: LVT Percent Increase vs. Decrease by Tax Class

Within each class of real property, the shift will result in greater or lesser tax liability for each parcel. In Figure 5, the green portion of the columns represents the

parcels that see a reduced tax bill; the red portion will see an increase.

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 8 Center for the Study of Economics | www.urbantools.org

Figure 5: LVT Count of Increase vs. Decrease by Tax Class

Within each class, the annual dollar change in tax incidence is presented in Figure 6. As theory would predict, residential property is most capital intensive on the

building side of the equation, and therefore would enjoy a greater reduction. The simulation demonstrates that outcome.

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 9 Center for the Study of Economics | www.urbantools.org

Figure 6: LVT Total Dollar Difference by Tax Class

Figure 7 provides the same outcome, but on an annual average basis. Citywide, these changes may appear modest, but the simulation can be changed in policy

to effect greater or lesser impact.

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 10 Center for the Study of Economics | www.urbantools.org

Figure 7: LVT Average Dollar Difference by Tax Class

Figure 8 demonstrates the annual percentage class change for each class. Both Class 1 and Class2 (Residential and Hotels/Apartments) show a significant annual

savings.

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 11 Center for the Study of Economics | www.urbantools.org

Figure 8: LVT Average Percent Change by Tax Class

LVT Impact by Council District Council districts are an easily recognizable part of the Philadelphia cityscape. As such, the Center has grouped its findings in this manner.

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 12 Center for the Study of Economics | www.urbantools.org

Figure 9 is clear that the Residential sector benefits greatly from LVT no matter the district. In general, the lower-valued residential properties in councilmanic

districts (Districts 6, 7 or 9) fare better .

Figure 9: LVT Residential Percentage Increase vs. Decrease by Council District

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 13 Center for the Study of Economics | www.urbantools.org

Non-Residential Properties in the 10 (Figure 10) council districts see less of a direct benefit, as many are land intensive and less capital-intensive. Many are

blighted, abandoned or are not put to best use.

Figure 10: LVT Non-residential Percentage Increase vs. Decrease by Council District

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 14 Center for the Study of Economics | www.urbantools.org

Broken out by Save or Increase by parcel (Figure 11) , the Council Districts again see benefit with LVT.

Figure 11: LVT Residential Count of Increase vs. Decrease by Council District

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 15 Center for the Study of Economics | www.urbantools.org

Non-residential parcels (Figure 12) vary more by council district. Yet, the changes are widely varied in many districts.

Figure 12: LVT Non-residential Count of Increase vs. Decrease by Council District

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 16 Center for the Study of Economics | www.urbantools.org

Figure 13 represents the average annual change per parcel in each council district. Established high value or up and coming districts (3, 5 or 8) experience little or

no change in tax liability, here expressed as an average.

Figure 13: LVT Residential Average Dollar Difference by Council District

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 17 Center for the Study of Economics | www.urbantools.org

Figure 14 representes the non-residential annual average shift with land value taxation. The reality of business taxation in Philadelphia should show that the

property tax would be preferable to the Business Privilege Tax.

Figure 14: LVT Non-residential Average Dollar Difference by Council District

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 18 Center for the Study of Economics | www.urbantools.org

Assessed Exemption of Improvements (AXI)

If Philadelphia were to move to a property tax (or preferably) a land value tax to increase competitiveness, consideration must be given to the large number of

retired homeowners on fixed incomes, owners of lower-valued residential (or commercial) real estate and renters. There are several traditional pathways to

provide ameliorations (See Supplements). Our proposal here illustrates what we call Assessment Exemption on Improvements (AXI). AXI exempts a dollar

amount of the taxable building value of a parcel. For the purposes of creating our simulation, CSE has chosen to exempt $10,460 (which is the median assessed

value of taxable buildings in Philadelphia). By reducing the taxable building assessment, the tax rate would be 124.522 mills (as opposed to 82.64 mills), and thus

the revenue would be the same.

Such a property tax system has been used in the past in other jurisdictions. For example, in Vancouver, British Columbia, land values were assessed at 100% of

market value, while buildings were assessed at only 50% of market value.

Our AXI proposal is simpler to understand, with powerful effects: enacts a permanent, universal abatement on a dollar amount of building value which will

proportionally exempt the greater part of a building from property tax, while a higher-valued parcel (Liberty Place, say) will see a statistically insignificant

building abatment, while seeing some increase on the land portion. The principles of vertical equity and ability-to-pay come into play.

We expect and hope that further research will be authorized by this task force or by city government. Granular examination of the data under AXI and LVT

simulations will demonstrate the feasibility of these programs, both under current assessments and under AVI.

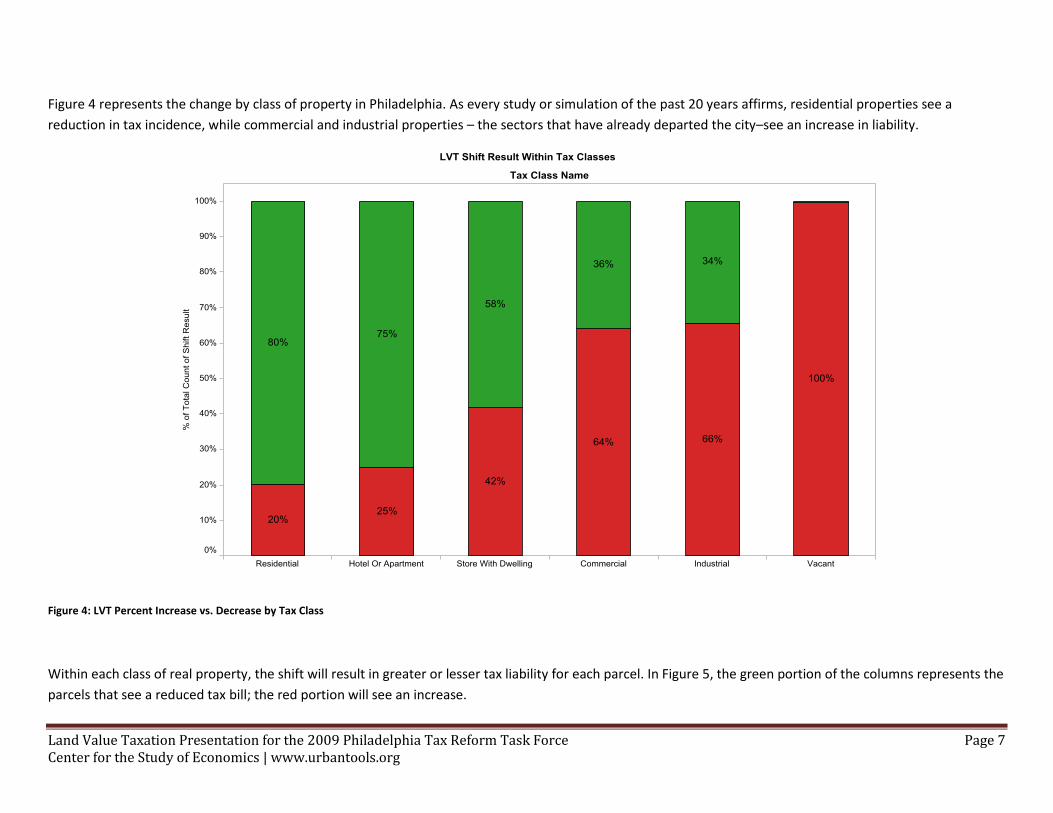

AXI Impact by Tax Class As Figure 15 demonstrates, AXI provides significant tax relief for residential properties while maintaining revenue levels, and suggests a way to shift additional

revenue from mobile labor and capital tax bases onto the property tax without across the board impacts on all classes of property.

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 19 Center for the Study of Economics | www.urbantools.org

Figure 15: AXI vs. Current Tax, Total and Average by Tax Class

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 20 Center for the Study of Economics | www.urbantools.org

Figure 16 shows the outcome by class of our AXI proposal. Note that the percentage amount of parcels that save increases fairly substantially. Compared with

Figure 4, the results favor classes 2 and 3, while improving classes 4 and 5. Grey sections represent tax-exempt.

Figure 16: AXI Percentage Increase vs. Decrease by Tax Class

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 21 Center for the Study of Economics | www.urbantools.org

Figure 17 Shows the parcel count changes with classes. Classes 1 through 3 see a majority decrease, while 4 through 6 experience an increase.

Figure 17: AXI Count of Increase vs. Decrease by Tax Class

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 22 Center for the Study of Economics | www.urbantools.org

AXI Impact by Council District The shift under AXI by council district is more pronounced in favor of residential properties (Figure 18) compared to LVT in Figure 9.

Figure 18: AXI Residential Percentage Increase vs. Decrease by Council District

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 23 Center for the Study of Economics | www.urbantools.org

Figure 19 is non-residential shift with AXI by council district. Savings by commercial properties, in generally less-desirable areas, are significant especially

compared with Figure 9, the LVT shift

Figure 19: AXI Non-residential Percentage Increase vs. Decrease by Council District

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 24 Center for the Study of Economics | www.urbantools.org

Figure 20 shows the annual average residential change by council district. All districts see savings, with lower valued districts seeing dramatic reductions.

Figure 20: AXI Residential Average Dollar Difference by Council District

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 25 Center for the Study of Economics | www.urbantools.org

Figure 21 shows the resulting average shift in burden onto non-residential classes.

Figure 21: AXI Non-residential Average Dollar Difference by Council District

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 26 Center for the Study of Economics | www.urbantools.org

Figure 22 indicates the total residential dollar change under the AXI proposal by council district. Economically at-risk districts (such as District 6 and 9) see great

benefit.

Figure 22: AXI Residential Total Dollar Difference by Council District

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 27 Center for the Study of Economics | www.urbantools.org

Figure 23 represents the total non-residential change by Council district using the AXI alternative

Figure 23: AXI Non-residential Total Dollar Difference by Council District

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 28 Center for the Study of Economics | www.urbantools.org

LVT and AXI by Neighborhood

Oxfo

rd C

ircle

Mayfa

ir

Cente

r C

ity E

ast

Tacony

Girard

Esta

tes

West O

ak L

ane

Ric

hmond

Cente

r C

ity W

est

Oln

ey

Fra

nkf

ord

Som

ert

on

Law

ncre

st

Junia

ta P

ark

Roxb

oro

ugh

Pennypack

Bustle

ton

South

Phila

delp

hia

Elm

wood

Eastw

ick

West Torr

esdale

Holm

esburg

Overb

rook

Whart

on

Byberr

y

Pennsport

Rhaw

nhurs

t

Cedarb

rook

East M

ount A

iry

Fox C

hase

Manayunk

Wynnefield

Kin

gsessin

g

Marc

oni Pla

za

East O

ak L

ane

Bridesburg

Ogontz

Harr

ow

gate

East G

erm

anto

wn

Logan

Tio

ga

Kensin

gto

n

Huntin

g P

ark

Str

aw

berr

y M

ansio

n

Poin

t B

reeze

Gra

ys F

err

y

Riv

erfro

nt

Haddin

gto

n

Alle

gheny W

est

Fairhill

Mill C

reek

Nort

h C

entr

al

Popla

r

Pow

elton

Fis

hto

wn

Univ

ers

ity C

ity

Cobbs C

reek

Germ

anto

wn

Wis

sahic

kon P

ark

Hartra

nft

Pennypack P

ark

West K

ensin

gto

n

Bre

wery

tow

n

East F

alls

West M

ount A

iry

Cedar P

ark

Belm

ont

Schuylk

ill

Chestn

ut H

ill

Fairm

ount

-$3,000K

-$2,000K

-$1,000K

$0K

$1,000K

Sum

of LVT $

Diff

ere

nce

$1,0

46K

$983K

$395K

$156K

$86K

$73K

$55K

$21K

$33K

$10K

$3K

$1K

$10K

$0K

-$22K

-$60K

-$51K

-$79K

-$101K

-$139K

-$127K

-$142K

-$161K

-$207K

-$185K

-$152K

-$180K

-$198K

-$234K

-$213K

-$219K

-$236K

-$253K

-$267K

-$319K

-$320K

-$595K

-$340K

-$440K

-$537K

-$697K

-$695K

-$756K

-$820K

-$813K

-$817K

-$932K

-$879K

-$848K

-$966K

-$953K

-$964K

-$967K

-$1,1

76K

-$978K

-$1,0

44K

-$1,1

45K

-$1,1

97K

-$1,3

31K

-$1,3

06K

-$1,3

46K

-$1,2

36K

-$1,4

78K

-$1,4

88K

-$1,7

07K

-$1,8

70K

-$2,1

99K

-$2,7

60K

-$2,8

35K

-$1,145K

-$697K

-$207K

$0K

LVT Neighborhood Residential Shift Overview: Total $ Difference

-$2,835K $1,046K

Sum of LVT $ Difference

Figure 24: LVT Total Dollar Difference by Neighborhood

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 29 Center for the Study of Economics | www.urbantools.org

Figure 25: LVT Average Dollar Difference by Neighborhood

Oxfo

rd C

ircle

Mayfa

ir

Cente

r C

ity E

ast

Tacony

Girard

Esta

tes

West O

ak L

ane

Ric

hm

ond

Cente

r C

ity W

est

Oln

ey

Fra

nkf

ord

Som

ert

on

Law

ncre

st

Junia

ta P

ark

Roxb

oro

ugh

Pennypack

Bustle

ton

South

Phila

delp

hia

Elm

wood

Eastw

ick

West Torr

esdale

Holm

esburg

Overb

rook

Whart

on

Byberr

y

Pennsport

Rhaw

nhurs

t

Cedarb

rook

East M

ount A

iry

Fox C

hase

Manayunk

Wynnefield

Kin

gsessin

g

Marc

oni Pla

za

East O

ak L

ane

Bridesburg

Ogontz

Harr

ow

gate

East G

erm

anto

wn

Logan

Tio

ga

Kensin

gto

n

Huntin

g P

ark

Str

aw

berr

y M

ansio

n

Poin

t B

reeze

Gra

ys F

err

y

Riv

erfro

nt

Haddin

gto

n

Alle

gheny W

est

Fairhill

Mill C

reek

Nort

h C

entr

al

Popla

r

Pow

elton

Fis

hto

wn

Univ

ers

ity C

ity

Cobbs C

reek

Germ

anto

wn

Wis

sahic

kon P

ark

Hartra

nft

Pennypack P

ark

West K

ensin

gto

n

Bre

wery

tow

n

East F

alls

West M

ount A

iry

Cedar P

ark

Belm

ont

Schuylk

ill

Chestn

ut H

ill

Fairm

ount

-$600

-$400

-$200

$0

$200

$400

Avg. LVT $

Diffe

rence

$150

$428

$109

$39

$48

$20

$21

$5$11

$286

$1

$168

$2

$0

-$37

-$10

-$51

-$37

-$17

-$25

-$14

-$21

-$18

-$551

-$46

-$15

-$22

-$30

-$45

-$25

-$37

-$32

-$45

-$57

-$131-$88

-$206

-$31

-$82

-$131

-$131

-$137

-$184-$

114

-$89

-$180-$

107

-$101

-$160

-$106

-$222

-$112

-$119

-$128

-$145

-$113

-$126

-$123

-$166

-$118

-$135

-$149

-$111

-$116

-$183

-$186

-$246

-$246-$

168

-$145-$112

-$37$0

LVT Neighborhood Residential Shift Overview: Avg. $ Difference

-$551 $428

Avg. LVT $ Difference

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 30 Center for the Study of Economics | www.urbantools.org

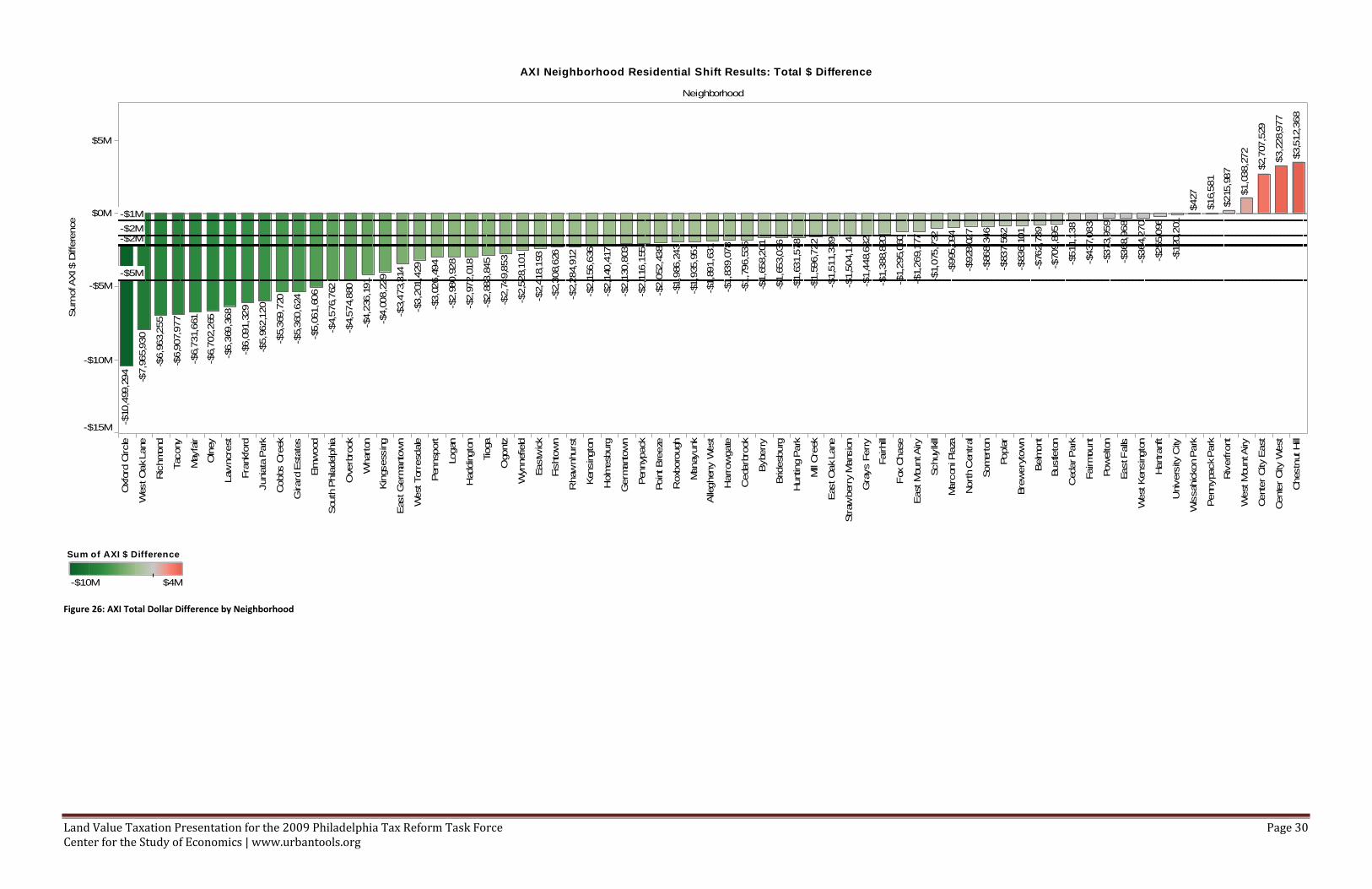

Figure 26: AXI Total Dollar Difference by Neighborhood

Neighborhood

Oxfo

rd C

ircle

West O

ak L

ane

Ric

hm

ond

Tacony

Mayfa

ir

Oln

ey

Law

ncre

st

Fra

nkfo

rd

Junia

ta P

ark

Cobbs C

reek

Girard

Esta

tes

Elm

wood

South

Phila

delp

hia

Overb

rook

Whart

on

Kin

gsessin

g

East G

erm

anto

wn

West Torr

esdale

Pennsport

Logan

Haddin

gto

n

Tio

ga

Ogontz

Wynnefield

Eastw

ick

Fis

hto

wn

Rhaw

nhurs

t

Kensin

gto

n

Holm

esburg

Germ

anto

wn

Pennypack

Poin

t B

reeze

Roxb

oro

ugh

Manayunk

Alle

gheny W

est

Harr

ow

gate

Cedarb

rook

Byberr

y

Bridesburg

Hunting P

ark

Mill C

reek

East O

ak L

ane

Str

aw

berr

y M

ansio

n

Gra

ys F

err

y

Fairhill

Fox C

hase

East M

ount A

iry

Schuylkill

Marc

oni Pla

za

Nort

h C

entr

al

Som

ert

on

Popla

r

Bre

wery

tow

n

Belm

ont

Bustle

ton

Cedar P

ark

Fairm

ount

Pow

elton

East F

alls

West K

ensin

gto

n

Hartra

nft

Univ

ers

ity C

ity

Wis

sahic

kon P

ark

Pennypack P

ark

Riv

erfro

nt

West M

ount A

iry

Cente

r C

ity E

ast

Cente

r C

ity W

est

Chestn

ut H

ill

-$15M

-$10M

-$5M

$0M

$5M

Sum

of A

XI $ D

iffe

rence

$3,5

12,3

68

$3,2

28,9

77

$2,7

07,5

29

$1,0

38,2

72

$215,9

87

$16,5

81

$427

-$120,2

01

-$255,0

96

-$364,2

70

-$368,9

68

-$373,9

59

-$437,0

83

-$511,1

38

-$709,8

95

-$762,7

39

-$836,1

01

-$837,5

62

-$868,3

46

-$928,0

27

-$995,0

94

-$1,0

75,7

32

-$1,2

69,1

77

-$1,2

95,0

60

-$1,3

88,8

20

-$1,4

48,6

32

-$1,5

04,1

14

-$1,5

11,3

39

-$1,5

96,7

22

-$1,6

31,5

78

-$1,6

53,0

36

-$1,6

58,2

01

-$1,7

96,5

35

-$1,8

39,0

78

-$1,8

91,6

31

-$1,9

35,9

51

-$1,9

86,2

43

-$2,0

52,4

38

-$2,1

16,1

55

-$2,1

30,8

03

-$2,1

40,4

17

-$2,1

56,6

36

-$2,2

84,9

12

-$2,3

08,6

26

-$2,4

18,1

93

-$2,5

28,1

01

-$2,7

49,8

53

-$2,8

88,8

45

-$2,9

72,0

18

-$2,9

80,9

28

-$3,0

26,4

94

-$3,2

01,4

29

-$3,4

73,3

14

-$4,0

08,2

29

-$4,2

36,1

91

-$4,5

74,8

80

-$4,5

76,7

62

-$5,0

61,6

06

-$5,3

60,6

24

-$5,3

69,7

20

-$5,9

62,1

20

-$6,0

91,3

29

-$6,3

69,3

68

-$6,7

02,2

65

-$6,7

31,6

61

-$6,9

07,9

77

-$6,9

63,2

55

-$7,9

65,9

30

-$10,4

99,2

94

-$5M

-$2M-$2M

-$1M

AXI Neighborhood Residential Shift Results: Total $ Difference

-$10M $4M

Sum of AXI $ Difference

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 31 Center for the Study of Economics | www.urbantools.org

Figure 27: AXI Average Dollar Difference by Neighborhood

Neighborhood

Oxfo

rd C

ircle

West O

ak L

ane

Ric

hm

ond

Tacony

Mayfa

ir

Oln

ey

Law

ncre

st

Fra

nkfo

rd

Junia

ta P

ark

Cobbs C

reek

Girard

Esta

tes

Elm

wood

South

Phila

delp

hia

Overb

rook

Whart

on

Kin

gsessin

g

East G

erm

anto

wn

West Torr

esdale

Pennsport

Logan

Haddin

gto

n

Tio

ga

Ogontz

Wynnefield

Eastw

ick

Fis

hto

wn

Rhaw

nhurs

t

Kensin

gto

n

Holm

esburg

Germ

anto

wn

Pennypack

Poin

t B

reeze

Roxb

oro

ugh

Manayunk

Alle

gheny W

est

Harr

ow

gate

Cedarb

rook

Byberr

y

Bridesburg

Hunting P

ark

Mill C

reek

East O

ak L

ane

Str

aw

berr

y M

ansio

n

Gra

ys F

err

y

Fairhill

Fox C

hase

East M

ount A

iry

Schuylkill

Marc

oni Pla

za

Nort

h C

entr

al

Som

ert

on

Popla

r

Bre

wery

tow

n

Belm

ont

Bustle

ton

Cedar P

ark

Fairm

ount

Pow

elton

East F

alls

West K

ensin

gto

n

Hartra

nft

Univ

ers

ity C

ity

Wis

sahic

kon P

ark

Pennypack P

ark

Riv

erfro

nt

West M

ount A

iry

Cente

r C

ity E

ast

Cente

r C

ity W

est

Chestn

ut H

ill

-$1,000

-$500

$0

$500

$1,000

$1,500

Avg. AX

I $ D

iffere

nce

$1,5

28

$389

$303

$285

$576

$488

$142

-$198-$

73

-$125

-$139

-$370

-$63

-$285

-$78

-$188

-$190

-$393

-$109

-$157

-$345

-$298

-$249

-$244

-$154

-$361-$

181

-$415

-$287

-$251

-$678

-$365

-$438

-$330

-$276

-$473

-$215

-$204

-$315

-$464

-$405

-$414

-$318

-$404

-$563

-$473

-$583

-$334

-$334

-$507-$

333

-$350

-$473

-$371

-$488

-$526

-$564

-$588

-$573-$434

-$656

-$551

-$657

-$674

-$599

-$688-$

521

-$621

-$624

-$551

-$404

-$298

-$154

AXI Neighborhood Residential Shift Results: Avg. $ Difference

-$688 $1,528

Avg. AXI $ Difference

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 32 Center for the Study of Economics | www.urbantools.org

Conclusions and Recommendations

1. A healthy city or jurisdiction relies on property tax. It is the last redoubt of tax revenue in a recession. It is the most stable tax. Move the city

towards real property tax. Philadelphia’s current menu of taxes that hurt the city makes the case that taxes on wages and business should be

replaceable by a real property tax. The “three-legged stool “proviso of good tax policy has never been found more wanting than at present.3

2. To make the real property tax responsive to city revenue needs and fulfill the canons of taxation:

a. It should bear as lightly as possible on production -- least impeding the growth of the general fund, from which taxes must be paid and the

community maintained.

b. It should be certain -- offering the least opportunity for abuse and corruption, and the least temptation for evasion.

c. It should bear equally -- giving no one an advantage, nor putting another at a disadvantage.

3. To accomplish that, we recommend that AVI be implemented as soon as possible.

4. Before the AVI comes into effect, the current property tax should be turned into a land value tax (LVT), or an assessment exemption for

improvements (AXI) as soon as possible as a way to improve the distribution of burden of the current property tax. AXI may require city or state

enabling legislation.

5. The Task Force should include the reform of the property tax into its final report, requesting a more intensive study of both alternatives

presented to the task force today.

6. Our alternative programs allow for greater reliance on the property tax without hurting low and fixed income property owners. Our alternative

is an attempt to introduce ability-to-pay and vertical equity into Philadelphia’s chaotic tax system.

Final Definitions:

1. Land Value Tax (LVT) is a shifting of the current flat millage rate into a higher tax rate on assessed taxable land and assessed taxable buildings.

2. Assessment Exemption for Improvements (AXI) is a permanent across the board dollar-amount abatement for all taxable buildings. The effect

on lower valued buildings is of a greater percentage drop in tax liability on the building. The abatement for a much higher valued building

would be correspondingly less. As higher-end construction has enjoyed extant abatements and other tax forgiveness programs, and brings

greater rental and market price returns, it is our position that the AXI program directs tax relief for the most at-risk neighborhoods and citizens.

3 “Tax students, especially at the state level, ply their trade by invoking one metaphor above all others: the three-legged stool. It rests on the claim that a sound and

successful tax regime for any government needs to rely on a three tax bases: income, property and sales. This is repeated so often that it passes today without much examination.”State Tax Notes, Vol.35, No.6, 2 February 2005, pp.377-381 Dr.H. William Batt

Land Value Taxation Presentation for the 2009 Philadelphia Tax Reform Task Force Page 33 Center for the Study of Economics | www.urbantools.org

Supplemental Material

See the following supplements submitted to the task force for more background information:

1. David Brunori: To Preserve Local Government, It's Time to Save the Property Tax, 1998

2. Bill Batt and Joshua Vincent 2007: Use and desirability of standard property tax relief measures. Testimony before Pennsylvania General

Assembly: Tools to Make the Pennsylvania Property Tax More Progressive

3. Wallace Oates and Robert Schwab: The Impact of Urban Land Taxation: The Pittsburgh Experience, 1996 Lincoln Institute of Land Policy

4. Letter from Mayor Stephen Reed, Harrisburg, PA to Mayor James Ruberto of Pittsfield Mass, October, 2006

5. "Final Report: Valuation of Land and Improvements in Philadelphia" By Roger A. McCain, Paul Jensen, and Stephen Meyer, Drexel

University, 2002