Luck and entrepreneurial success - INSEADfaculty.insead.edu/urs-peyer/documents/2013-01-03...

44

Luck and entrepreneurial success Diego Liechti, Claudio Loderer, and Urs Peyer * January 3, 2013 Abstract How much of entrepreneurial performance is sheer luck compared to talent, experience, education, and hard work? Since luck is difficult to measure objectively, we ask a large number of entrepreneurs. According to those entrepreneurs, luck accounts for less than one third of performance variation. This self-reported assessment is affected but its magnitude cannot be explained by personal characteristics such as illusion of control. Luck, however, plays a significant role in individual management activities such as finding the appropriate business idea and choosing the right moment to enter a market. The perceived importance of luck in performance shapes actual decisions, including the entrepreneurial decision itself, the choice of financial leverage, and the choice of the industry in which to operate. What entrepreneurs believe is luck correlates with the unexplained variation in a model of entrepreneurial performance. The evidence also shows that experience, education, and hard work, the pillars of high work ethic, pay off. Keywords: luck, start-ups, entrepreneur, factors of success, performance JEL codes: G3, G02, M13 ◊ An earlier version of this paper was entitled: “What matters more for entrepreneurial success: Skills, personality, or luck?” We are indebted to Claude Federer from Creditreform, a business information provider specialized in rating credit risk, for giving us the addresses of firms from the official Swiss corporate register. Many thanks go to the employees, entrepreneurs, and managers who helped us refine and clarify our questionnaire, and to the many persons who took the time to participate in the survey. Moreover, we would like to thank Daniel Aeberhard, Demian Berchtold, Markus Senn, Jonas Stulz, Niklaus Stulz, Urs Wälchli, and Jonas Zeller for their various suggestions, and Demian Berchtold, Lorenzo Bretscher (especially), Anita Bühler, Jonas Friedrich, Adrian Michel, and Janine Taugwalder for their research assistance. Mike Jahn set up an invaluable scanner solution. We are particularly grateful to an anonymous referee and to Martin Weber (a discussant at the 2012 European Winter Finance Conference) as well as to Artur Baldauf, Evgenia Golubeva, Denis Gromb, Petra Jörg, Frauke Lammers, Philippe Mueller, Lukas Roth, and the seminar participants at the 2009 Conference of the Academy of Entrepreneurial Finance in Chicago, the 2010 European Financial Management Symposium in Montreal, the Law and Economics Workshop at Harvard University, the 2011 Interdisziplinäre Jahreskonferenz zur Gründungsforschung, the 2012 European Winter Finance Conference, and an INSEAD and ETH seminar for helpful comments and suggestions. This research is sponsored by the Swiss National Science Foundation. The article represents the view of the authors and all errors are our own. * Diego Liechti is from the Institut für Finanzmanagement, University of Bern, Switzerland and PPCmetrics AG, Claudio Loderer is from the Institut für Finanzmanagement, University of Bern, Switzerland, and Urs Peyer is from INSEAD, France.

Transcript of Luck and entrepreneurial success - INSEADfaculty.insead.edu/urs-peyer/documents/2013-01-03...

Luck and entrepreneurial success◊

Diego Liechti, Claudio Loderer, and Urs Peyer*

January 3, 2013

Abstract

How much of entrepreneurial performance is sheer luck compared to talent, experience, education, and hard work? Since luck is difficult to measure objectively, we ask a large number of entrepreneurs. According to those entrepreneurs, luck accounts for less than one third of performance variation. This self-reported assessment is affected but its magnitude cannot be explained by personal characteristics such as illusion of control. Luck, however, plays a significant role in individual management activities such as finding the appropriate business idea and choosing the right moment to enter a market. The perceived importance of luck in performance shapes actual decisions, including the entrepreneurial decision itself, the choice of financial leverage, and the choice of the industry in which to operate. What entrepreneurs believe is luck correlates with the unexplained variation in a model of entrepreneurial performance. The evidence also shows that experience, education, and hard work, the pillars of high work ethic, pay off.

Keywords: luck, start-ups, entrepreneur, factors of success, performance JEL codes: G3, G02, M13

◊ An earlier version of this paper was entitled: “What matters more for entrepreneurial success: Skills, personality,

or luck?” We are indebted to Claude Federer from Creditreform, a business information provider specialized in rating credit risk, for giving us the addresses of firms from the official Swiss corporate register. Many thanks go to the employees, entrepreneurs, and managers who helped us refine and clarify our questionnaire, and to the many persons who took the time to participate in the survey. Moreover, we would like to thank Daniel Aeberhard, Demian Berchtold, Markus Senn, Jonas Stulz, Niklaus Stulz, Urs Wälchli, and Jonas Zeller for their various suggestions, and Demian Berchtold, Lorenzo Bretscher (especially), Anita Bühler, Jonas Friedrich, Adrian Michel, and Janine Taugwalder for their research assistance. Mike Jahn set up an invaluable scanner solution. We are particularly grateful to an anonymous referee and to Martin Weber (a discussant at the 2012 European Winter Finance Conference) as well as to Artur Baldauf, Evgenia Golubeva, Denis Gromb, Petra Jörg, Frauke Lammers, Philippe Mueller, Lukas Roth, and the seminar participants at the 2009 Conference of the Academy of Entrepreneurial Finance in Chicago, the 2010 European Financial Management Symposium in Montreal, the Law and Economics Workshop at Harvard University, the 2011 Interdisziplinäre Jahreskonferenz zur Gründungsforschung, the 2012 European Winter Finance Conference, and an INSEAD and ETH seminar for helpful comments and suggestions. This research is sponsored by the Swiss National Science Foundation. The article represents the view of the authors and all errors are our own.

* Diego Liechti is from the Institut für Finanzmanagement, University of Bern, Switzerland and PPCmetrics AG, Claudio Loderer is from the Institut für Finanzmanagement, University of Bern, Switzerland, and Urs Peyer is from INSEAD, France.

- 1 -

Those who have succeeded at anything and don't mention luck are kidding themselves.

Larry King, American television and radio host

1 Introduction

Whether good or bad performance is the result of chance or things like talent and hard work is a

question that we regularly confront when witnessing other people’s exceptional performance in

sports, private life, or in the business world. Are some of Roger Federer’s most memorable shots

just fortuitous or the expression of his talents? Was the superior performance of Peter Lynch, the

famed manager of the Fidelity Magellan Fund, a reflection of luck or skills? The reason for our

keen interest is that we want to admire true, exceptional heroes and not just lucky people. We

also don’t want to blame ourselves for lack of success, if our failure is the result of happenstance.

And we want to believe in our own chances of success. If someone else can do it, it is

comfortable to know, then we can also do it—unless it’s pure luck.

This paper looks at the special case of entrepreneurs. Are successful entrepreneurs like Bill

Gates exceptionally skilled individuals or are they just lucky? Is it simply bad luck that one out

of every two entrepreneurial ventures that get started every year is gone five years later? It is

difficult to answer these questions because it is not clear what part of observed performance is

fortuitous and what is not. For example, is being at the right time at the right place pure

coincidence, the result of intuition, or the outcome of careful planning? It is hard to tell from the

outside. Allegedly, 3M’s Post-it notes were invented fairly accidentally when Art Fry found an

application for an adhesive developed by Spencer Silver, a colleague at 3M. If we had to tell

what fraction of the financial success of the Post-it notes was unintended, it would probably be

impossible to say without asking Art Fry and Spencer Silver directly. In trying to assess the

relevance of luck in entrepreneurial performance, this paper therefore does exactly that, namely

it asks entrepreneurs. They are, in principle, the only ones to know. What is not luck is the

result of things like talent as well as experience, education, and hard work, the pillars of high

work ethic. We therefore also look for evidence for the belief that these virtues pay off both in

the mind of entrepreneurs and in reality. The exposition uses the terms luck and chance

interchangeably.

Implicitly, the literature defines luck as unexplained performance. Bertrand and

Mullainathan (2001), for example, define it as “observable shocks beyond the CEO’s control” (p.

- 2 -

901). Kahneman (2011) talks about “factors that the CEO does not control” (p. 205). The

problem is that we don’t know the correct functional form of the model of entrepreneurial

performance, nor do we know all of the relevant variables and their proxies. Additionally, the

necessary data might be impossible to collect or even to observe. Hence, unexplained

performance variation yields a noisy, possibly biased estimate of truly uncontrollable

performance shocks. Perhaps more important, it is not clear what drivers of performance we

want to condition our definition of luck on. Any definition of luck is conditional. For example,

if we start from an existing firm, and therefore take things like its industry, size, resources, and

the entrepreneur’s experience and talent as given, then unexpected performance is what we

cannot explain with these variables. However, if we go back in time before the firm has been

started and ask ourselves how much of the later performance is the result of chance, then many

of the variables we just took as given are the result of luck themselves. Whether a firm in the

computer business produces software or hardware, whether it is a global or a local player,

whether it is large or small, how experienced the entrepreneur is, etc. is itself a matter of chance.

If we go back long enough, every variable that drives performance, including the entrepreneur’s

personal characteristics, reflects at least in part luck. Talent, for example, is ultimately a matter

of genes (a random draw for the individual in question) and a number of uncontrollable

contingent situations such as family, location, environment, and time (see also the discussion in

Gladwell (2008)). As a result, the only possibility to assess the importance of luck in

entrepreneurship is to ask those individuals directly. To investigate the biases that arise from

selective memory, the temptation to rewrite history, or pride, we perform a battery of robustness

tests. To sum up, the main hypothesis of our paper is:

Hypothesis 1. Luck is very important for entrepreneurial success.

In our survey we therefore ask participants about the importance of luck in determining

entrepreneurial performance. While in a first pass we inquire about overall performance, in a

second pass we examine individual components of that performance the importance of luck for

different entrepreneurial management tasks (e.g., idea generation, finding financing, finding

customers).

Hypothesis 2. Luck is very important in the following management tasks: finding the

business idea, finding the optimal timing for entry, finding employees, gaining

- 3 -

customers, securing suppliers, receiving financing, establishing the necessary

business connections, and establishing necessary private connections.

However, we choose to be agnostic about a detailed definition of luck, and simply ask about

the relevance of uncontrollable events thereby relying on the implicit definition that

entrepreneurs have in mind. If nothing else, it is perceptions and beliefs that ultimately decide

entrepreneurial behavior. However, we do eventually test what entrepreneurs have in mind, and

investigate whether it correlates with the unexplained component in a standard model of

performance. Moreover, we examine whether and how these beliefs affect entrepreneurial

choices. Thus, we propose the following three hypotheses about the influence of the beliefs

about luck on their actual behavior:

Hypothesis 3. Individuals that believe luck is important for entrepreneurial success

are less likely to pursue an entrepreneurial career.

Hypothesis 4. Entrepreneurs that believe luck is important for entrepreneurial

success use less debt in the initial start-up financing.

Hypothesis 5. Serial entrepreneurs that believe they were lucky in their first venture

are more likely to stay in the same industry.

The basis for our investigation is a survey we conducted in Switzerland in 2007.1 About one

third of the respondents were entrepreneurs who had registered their businesses between 2002

and 2006. The rest was a control sample of non-entrepreneurs, including managers and

employees. The sample of entrepreneurs is similar to that used by Bitler, Moskowitz, and

Vissing-Jørgensen (2005), and Landier and Thesmar (2009). Based on the survey responses

from more than 3,000 entrepreneurs and 5,000 non-entrepreneurs, we find that entrepreneurs

believe luck is a less important factor in explaining performance variation than, for example,

hard work and education, and that it explains at best one third of entrepreneurial performance

variation. Only 15 percent of the entrepreneurs in the sample believe luck is a very important

factor in the overall performance of the start-up, whereas roughly 79 percent think that it is the

1 The survey was in three different languages. In the German version, the term for luck was “Zufall” (as opposed

to “Glück”). In the French version, it was “hasard,” and in the Italian version, it was “caso.”

- 4 -

least important factor. A big concern with our endeavor is that personal traits, such as

overconfidence, risk aversion, and illusion of control (Langer (1975)) might lead entrepreneurs

to underestimate the importance of luck. There is some evidence of that, but it does not affect

our conclusions. Moreover, even Bill Gates admits that luck played an immense role, so why

can’t the average entrepreneur tell the truth, especially if there is no payoff since they are filling

out an anonymous questionnaire and not giving a talk in front of people.2 Therefore, we do not

believe that the opinions of entrepreneurs are biased in general in the sense of Kahneman (2011).

After a principal component analysis, we can conclude that luck accounts for less than one third

of performance variation. Interestingly, however, a full 60 percent of our entrepreneurs believe

luck is very important in at least one out of eight entrepreneurial activities, such as finding the

relevant business idea or deciding about the optimal time to enter the market. The analysis

suggests that entrepreneurs take an average across various areas of entrepreneurial activities to

form an assessment of the importance of luck in the overall performance of new ventures.

Furthermore, we find that entrepreneurs’ assessment of the importance of luck affects their

behavior. For example, individuals who believe luck is an important determinant of performance

tend to shy away from an entrepreneurial career, consistent with the experimental results in

Camerer and Lovallo (1999). Moreover, when they do opt for such a career, their decisions, for

example the financial leverage choice, are affected by their perceptions. These results hold even

after controlling for a large number of characteristics, including the entrepreneurs’ risk aversion

and overconfidence.

Finally, as mentioned, we investigate what entrepreneurs mean by luck and test whether it

correlates with the unexplained variation in a standard regression model of performance. Even if

such models yield noisy measures of truly uncontrollable shocks to performance, we show that

this is the correct approach to gauge whether perceptions of luck are proxies for those shocks.

We find that what entrepreneurs believe is good (bad) luck correlates positively (negatively) and

significantly with that unexplained variation. Our analysis suggests that luck is responsible for

2 See Bill Gates Answers Most Frequently Asked Questions Bill Gates answers are also helpful to understand the

width of luck since he admits that he was lucky to have parents and friends that encouraged him and to have Paul Allen to work with. (http://download.microsoft.com/download/0/c/0/0c020894-1f95-408c-a571-1b5033c75bbc/billg_faq.doc).

- 5 -

less than one third of the performance in start-up firms. Interestingly, and consistent with

popular belief, hard work, experience, and education do contribute to actual success. It turns out

that the performance model we estimate with these data replicates many of the results reported in

the literature with secondary data.

Entrepreneurs are the engines of economic growth. This study contributes to a better

understanding of entrepreneurs, their motivations, and their decisions, and suggests ways to

nurture entrepreneurship and, ultimately, economic growth. If entrepreneurs believed success

were mostly a random event (as in Kihlstrom and Laffont (1979)), individuals with high self-

assessed skills, would probably be discouraged from opting for an entrepreneurial career

(Camerer and Lovallo (1999)). Second, perceptions about the importance of luck appear to

matter when entrepreneurs make decisions. Third, we present evidence that these perceptions

are not simply a psychological quirk, but are consistent with reality. Fourth, we contribute to the

literature that documents the importance of behavioral aspects in managerial behavior, in

general, and finance decisions, in particular. Fifth, and arguably foremost, the study helps assess

what proportion of growth seems to be sheer luck. Finally, and related, the evidence shows that

commitment, hard work, and dedication can overcome sheer luck, a finding that should be of

interest to educators, investors, policymakers, and regulators alike. In fact, we document that

these pillars of high work ethic do affect performance.

To the best of our knowledge, this is one of the first empirical studies to attempt an appraisal

of the importance of luck in entrepreneurial performance. One significant exception is Gompers,

Kovner, Lerner, and Scharfstein (2010). According to that paper, successful entrepreneurs have

persistent market timing abilities as opposed to sheer luck—the reason, we show, could be that

these entrepreneurs work harder and are more talented. In the corporate finance literature,

Chang, Dasgupta, and Hilary (2010) find that CEOs’ abilities contribute to firm performance

over and above the effects of firm-specific assets and luck. Other studies have analyzed the

influence of luck on executive pay (e.g., Fama (1980), Bertrand and Mullainathan (2001)). The

issue of luck versus skills in performance is much more popular in the investment literature,

starting with Fama, Fisher, Jensen, and Roll (1969). More recently, Kosowski, Timmermann,

Wermers, and White (2006) conclude that a significant minority of mutual funds have skills that

allow them to outperform, while Fama and French (2010) conclude that most of the variation in

mutual fund alpha is driven by luck.

- 6 -

2 Sample description and characteristics

2.1 Sample selection

The survey was conducted in Switzerland at the end of 2007. Two questionnaires were used:

one for entrepreneurs and one for a control group of managers and employees randomly chosen

from the official Swiss telephone guide (both questionnaires can be downloaded from the

Internet at http://www.ifm.unibe.ch/). Following Bitler, Moskowitz, and Vissing-Jørgensen

(2005) and Landier and Thesmar (2009), entrepreneurs are individuals with an equity

participation in the firm they work for. The narrower definition by Gompers, Lerner, and

Scharfstein (2005) that requires that entrepreneurs also be the firm's founders or cofounders was

used as well. Unless explicitly stated, the analysis uses the broader definition. The results go

through with either definition.

The questionnaire for entrepreneurs was sent to 40,000 randomly selected chairmen of the

board, joint owners of companies with limited liability, and sole proprietors of start-ups under

the rationale that these individuals were likely to meet one of the two definitions of entrepreneur.

Their names were from the official Swiss Commercial Register. To make sure that these

individuals remembered the information we were seeking, we focused on recently founded firms,

namely those founded in 2002, 2004, or 2006. To ensure a random sample of firms, we applied

stratified sampling with starting year, legal form, and region as strata. The questionnaire focused

on seven topics: company founding, current company data, professional background and

education, personal characteristics, relative importance of luck, social environment, and personal

financial circumstances.

In designing our survey, we followed the procedure suggested by Graham and Harvey

(2001). Specifically, we first took a look at other questionnaires on entrepreneurship. Based on

those questionnaires and a careful review of the existing literature, we drafted a first version in

German and circulated it to a group of academics for feedback. We revised the questionnaire on

the basis of their critique and suggestions. Then we sought the advice of marketing and

psychology scholars on survey design and execution. In particular, we discussed measures to

maximize the response rate and minimize possible response biases. Thereafter, we sent the

questionnaire to a group of entrepreneurs and managers for a pretest. Having revised the

questionnaire based on their suggestions, we asked a communication specialist to look over the

design and wording of the questionnaire. Finally, we discussed the revised document with

- 7 -

several entrepreneurs and managers to make sure every question was understandable. The final

version was nine pages long and contained 54 questions, most of them with subparts.

The questionnaire for the control group contained the same questions (except for the two

company-related sections). It was sent to 23,202 individuals, namely managers and other

employees (public employees, teachers, engineers, mechanics, and commercial clerks) randomly

picked from the official Swiss telephone guide. For this sample, we used profession and region

as strata. Both questionnaires promised strict anonymity. Because Switzerland has three official

languages, each questionnaire had a German, a French, and an Italian version.

To increase the response rate, a cover letter and a postage-paid return envelope were

included. As a further incentive to participate, respondents could order an analysis report. After

two weeks, people were sent a reminder, and those who had misplaced the questionnaire were

given the possibility of obtaining a new copy by physical mail or e-mail, or from a Web site that

was created for that purpose. Over 300 individuals ordered a second copy. A telephone hotline

was also set up to answer questions.

A total of 8,245 individuals filled out one of the two questionnaires. The response rate of

more than 13 percent is comparable to that reported in other studies.3 Of the 8,245 respondents,

3,104 were entrepreneurs according to the broader definition, 2,778 were entrepreneurs

according to the more restrictive definition, and 5,141 were individuals from the control group.

4,410 individuals filled out the questionnaire completely. The responding individuals are similar

in terms of legal form, registration year, and Canton of registration with the overall population in

the official Swiss Commercial Register. To maximize the number of observations in the

analysis, whenever there are missing data, we use nondisclosure dummies (see, for example,

Himmelberg, Hubbard, and Palia (1999)). These binary variables equal one if a given

respondent does not disclose a particular piece of information, and zero otherwise; the variable

itself is given a value of zero for the respondents who don’t provide the information in question.

3 That rate is between 7 and 12% in surveys of CFOs (Graham and Harvey (2001), Brav, Graham, Harvey, and

Michaely (2005), and between 16 and 19% in surveys of entrepreneurs (Bosma, Van Praag, Thurik, and De Wit (2004) and Forbes (2005).

- 8 -

2.2 Sample description

In line with Bitler, Moskowitz, and Vissing-Jørgensen (2005), about 70 percent of the

entrepreneurs in our sample hold 100 percent of the firm’s equity, and 90 percent at least 50

percent. Eighty-nine percent founded their firm, 4 percent inherited it, and the rest bought it

from someone else (not shown). In 78 percent of the cases, the firm was funded initially by the

founder alone (not shown). Initial equity financing was as follows: 87 percent by the founder

himself, 9 percent by family and friends, 1 percent by strategic investors, and 1 percent by

business angels (not shown). Sixty firms in the sample, about 2 percent, have VC or business-

angel financing, compared with the less than 0.1 percent reported in Asker, Farre-Mensa, and

Ljungqvist (2011) for the U.S.

< Insert Table 1 here >

About 44 percent of the firms are sole proprietorships, 31 percent are companies with

limited liability, and 24 percent are corporations (Table 1). Companies with limited liability

have a minimum capital of CHF 20,000 (the exchange rate was about CHF 1.02 to the USD at

the time of the survey); all owners participate in firm management. Corporations have many of

the same characteristics as U.S. corporations; the minimum capital is CHF 100,000, half of it

paid in.

The entrepreneurs’ firms were very small when they were started. The median company

began with one employee, the average with 3, and the largest with 330 (Table 1). By the time

they made it into the sample, however, these firms had grown somewhat. The median company

has 2 employees, the average 5.6, and the largest 1,190. Ninety-one percent of the entrepreneurs

have worked for a firm before, but only 17 percent in a start-up (not shown). The companies that

acted as incubators are fairly evenly distributed across firm size: 24 percent of the entrepreneurs

worked for companies with more than 250 employees, and 29 percent for companies with fewer

than 10 employees (not shown). There are 13 different industries (industry allocation is based on

what respondents say). Most companies are either in IT or commerce (17 and 16 percent,

respectively), the fewest are in agriculture and energy (2 and 1 percent, respectively).

- 9 -

2.3 Performance measures

To measure performance, survey participants were asked about sales, earnings, personal income,

and initial invested capital. Based on the replies, and in keeping with Bitler, Moskowitz, and

Vissing-Jørgensen (2005), we construct three performance measures for the year 2006: an

industry-adjusted natural logarithm of sales, an industry-adjusted natural logarithm of aggregate

income, and an industry-adjusted return on the capital originally invested in the firm (ROI). The

definitions are in the Appendix. To minimize the impact of potential outliers, all performance

metrics are winsorized at the 5th and 95th percentiles.

Table 1 shows that the average firm has CHF 2 million in sales, with a median of CHF

200,000. The sales of the smallest firm are zero; those of the largest are CHF 2.5 billion.

Moreover, the average (median) aggregate income is CHF 169,000 (119,000), and the average

(median) ROI is 421 percent (220 percent). For tax purposes, entrepreneurs might choose to

draw salaries rather than paying out dividends. Hence, simply focusing on earnings could yield a

downward biased measure of firm performance. The problem is that the entrepreneurs disclose

only total personal income, not the income derived from the particular firm under investigation.

When investigating performance measures that involve personal income, we therefore focus on

only full-time entrepreneurs and ignore part-timers.

The sample is more comparable with that of Bitler, Moskowitz, and Vissing-Jørgensen

(2005) and Landier and Thesmar (2009) than with that of Gompers, Kovner, Lerner, and

Scharfstein (2010). Whereas only 7.3 percent of the firms in Gompers, Kovner, Lerner, and

Scharfstein (2010) are profitable and only 46.9 percent are able to generate any revenue, the

fraction of profitable firms in our sample is 96 percent. Bitler, Moskowitz, and Vissing-

Jørgensen (2005) report similar numbers. The reason for the difference from Gompers, Kovner,

Lerner, and Scharfstein (2010) could be that they concentrate on venture-capital (VC) backed

entrepreneurs.

2.4 Other variables

The survey data fall into three main categories: a) entrepreneurial skills, b) personal

characteristics, c) and firm-specific variables. Definitions are in the Appendix and descriptive

statistics in Table 2. Entrepreneurs have an average 24.4 years of working experience, 11.9

years in managerial positions. The cross-sectional variation in working and management

- 10 -

experience is fairly substantial. More than 20 percent of the entrepreneurs were successful in

their prior venture, and 8 percent were unsuccessful (not shown).

< Insert Table 2 here >

The personal characteristics indicate, among other things, that entrepreneurs are more

overconfident and less risk averse than non-entrepreneurs (Table 2). Thirty percent of the

entrepreneurs are part-timers. The firm-specific variables include size, organizational form,

ownership, VC backing, leverage, and a binary variable that captures regions with a Protestant

majority in the population. Size is, alternatively, the natural logarithm of the initial capital

raised at the start of the company (Bitler, Moskowitz, and Vissing-Jørgensen (2005)) and the

natural logarithm of the number of employees (Bitler, Moskowitz, and Vissing-Jørgensen

(2005)).

2.5 Non-response, survivorship, and self-selection bias

To examine the presence of non-response bias in the data, we compared the answers of early

respondents with those of late respondents (Graham and Harvey (2001)). Filion (1975) argues

that late respondents resemble non-respondents. According to a Wilcoxon rank-sum test, early

answers differed from late answers for 12 of the total 27 variables with confidence 0.95 (not

tabulated). Yet the differences were mostly related to firm characteristics, not with respect to

luck perceptions, education, experience, and personal characteristics. We replicated the analysis

for early and late respondents, separately. The conclusions were unaffected (not shown).

There could also be survivorship bias in the data, for unlucky firms eventually cease to exist

and cannot be surveyed. Based on data from the Bundesamt für Statistik und

Unternehmensdemographie, it is known that 80.7 percent of the firms that are started at any time

are still operating one year later, 69.8 percent after two years, and only 50.0 percent after five.

The results are qualitatively unchanged, however, when the analysis includes only entrepreneurs

that started their firm at the end of the sample period, namely in 2006. If there had been

survivorship bias, it would have been smaller in this cohort of firms, since they didn’t have much

time to disappear before we conducted the survey.

- 11 -

Another problem could be self-selection bias. It is possible that entrepreneurs of

unsuccessful firms are less likely to participate in a survey. Yet we do not believe this issue

poses a significant problem. First, close to 20 percent of the sample firms actually report

negative earnings during a period of overall economic growth. Second, we checked whether

early respondents differ from late respondents with respect to profitability. If unsuccessful

entrepreneurs were hesitant to participate, and if late respondents were similar to non-

respondents, then late respondents should have been less profitable than early respondents. Yet

mean and median comparison tests rejected this hypothesis (not shown).

There were two further concerns. One was that respondents might not answer truthfully.

We cannot exclude that. However, the nature of the questions does not seem to be particularly

confidential. More importantly, as we will see, we obtain results similar to those reported in the

literature. The second concern was that the questions might be misunderstood. This issue was

addressed in three different ways. First, wherever possible, we used questions from past surveys

reported in the literature. Second, the questions were pre-tested with a diverse sample of

entrepreneurs and employees. Third, respondents were asked to indicate which questions were

hard to understand. Only 9 percent did so. Dropping these individuals from the sample had no

material effect on the conclusions (not shown).

3 Luck perceptions

To assess hypothesis 1, i.e., the relevance of luck in performance, the survey asked: “How

important are the following aspects for business success: pure luck, experience, talent, effort,

education, and connections?” Respondents could score these factors from very important (1) to

quite unimportant (5). They could give the same score to different factors. In other words,

respondents could give all factors a 2, if they thought they were all fairly unimportant.

Participants were asked to mention other possible factors besides the six suggested. Only nine

out of every 100 respondents took advantage of this possibility. They mentioned things like

confidence, stamina, and family support. However, there was no consensus on any one of these

additional factors. Consequently, we assume that the six factors in question are exhaustive. This

is a conservative assumption, since it limits the number of factors that could potentially rank

ahead of luck to five. Since scores are subjective, they are not necessarily comparable across

respondents. We therefore use the scores provided by each respondent to infer his/her rankings

- 12 -

of the various factors. A ranking of 1 is assigned to the success factor with the respondent’s

highest score.4

3.1 Rankings of success factors

Table 3 details the answers from approximately 3,000 entrepreneurs. Panel A provides summary

statistics. With a median rank of 5, luck places far behind the other factors. In comparison,

effort, experience, and talent have a median rank of 1, and education and connections one of 2.

Panel B indicates that only about 15 percent of the respondents think luck is the most important

key to success, whereas a whopping 78 percent regard it as the least important. Effort comes out

on top of the rankings—about 75 percent of the entrepreneurs in the sample consider it the most

important basis for success, and only 15 percent believe it is the least important. Talent places

very close to effort. Then comes experience, whereas education and connections rank lower,

although considerably ahead of luck.

We also asked the question: “Can a start-up be financially successful without lucky random

events?” Possible answers were yes, in part, and no. Even though this question focuses on the

upside and addresses luck as a necessary condition, people who believe luck is very important

should also tend to believe that there is no success without luck. That is indeed the case. The

relation is positive and the chi-squared test highly significant (not shown). Hence, the answers

that people give seem to be consistent.

< Insert Table 3 here >

The obvious reservation is that the rankings in Table 3 are self-reported opinions—and

opinions are bound to be colored by personal circumstances. In what follows, we therefore test

whether these circumstances could have biased our conclusions. The analysis is conducted in

Table 4.

4 The drawback of translating scores into rankings is that we lose information about the distance between high and

low scores. However, the inferences are unaffected when we use the self-reported scores directly (not tabulated).

- 13 -

3.2 Analysis of scoring bias

We first test whether self-attribution bias affects the ranking of luck. Successful entrepreneurs

are more likely to ascribe their success to superior abilities and planning, whereas unsuccessful

entrepreneurs blame their failure on bad luck (Miller and Ross (1975) and Zuckerman (1979)).

We therefore split the sample according to various dimensions of performance. First, we focus

on actual performance. Well-performing firms have sales above the median in the group of peer

firms with the same age and in the same industry; the rest are poorly performing firms. When

we do that, the ranking of luck among the six factors of success is the same as the unconditional

ranking of Table 3 regardless of firm performance (not shown). Luck always ranks at the

bottom. The only difference we find is that entrepreneurs from firms that do better believe a bit

more strongly that the luck of the draw is not necessary to succeed—the corresponding

proportions are 62 percent among successful firms and 55 percent among unsuccessful ones.

The relative ranking is also unaffected for the remaining five factors. Effort, experience, and

talent are slightly more important than education and connections, regardless of performance.

The results are similar when splitting the sample into firms that, in the opinion of their

entrepreneurs, have performed worse than anticipated, as anticipated, or better (not shown).

Along the same lines, we also sorted the sample by whether the entrepreneur is a first-time

entrepreneur, and, if he is not, by whether the venture was successful or unsuccessful. The

conclusions remain the same (not shown). In general, we find no evidence that past performance

induces a self-attribution bias significant enough to affect the ranking of luck.

However, there could be other biases. Table 4 tests whether entrepreneurs with an internal

locus (illusion) of control, i.e., people who believe they have their life under control (see, e.g.,

Langer (1975)), score the importance of luck differently. We find that, while entrepreneurs with

an internal locus of control do indeed give luck a significantly lower rank than respondents with

an external locus of control (median test), luck remains the least important determinant of

performance in both groups. Significantly more entrepreneurs believe no luck is necessary for

success when they have an internal locus of control (69 percent vs. 55 percent).

< Insert Table 4 here >

- 14 -

Conceivably, the more confident and less risk averse entrepreneurs might underestimate the

importance of luck. We therefore test if the ranking remains the same if we group entrepreneurs

by degree of risk aversion and overconfidence. Yet luck clearly remains the least important

success factor regardless of subsample, and the ranking of the remaining factors is unaffected

(not shown).

We also inquired into whether survival changes the opinion of entrepreneurs. We therefore

distinguished between seasoned and rookie entrepreneurs. Rookie entrepreneurs assign luck a

significantly higher average rank, yet luck remains the least important success factor also for

them (not shown). The same goes for age. Younger entrepreneurs assign significantly more

importance to luck, yet they also rank it last (not shown). We also find that individuals who

profess that their career was accidental give luck an average rank of 4.1, whereas individuals

whose career followed a deliberate path give it a rank of 5.4. Both groups, however, believe luck

is the least important factor of success (not shown). The same conclusion follows when

distinguishing different industries.

Overall, we therefore find some evidence that the perceptions about the importance of luck

are distorted by personal situations, abilities, or past experience. However, that does not affect

the ranking of luck. The strength of our inference should be moderated, however, by the fact that

our tests might be correlated. For example, overconfident people are also less risk averse; the

correlation between the two variables is –0.32 (not shown). We therefore repeat the analysis in a

multivariate context using an ordered logit regression (not shown). The results support the

conclusion that luck ranks last among the six factors of success considered.

3.3 Perceptions of non-entrepreneurs

It could be that entrepreneurs as a group have a warped perception of reality. After all,

entrepreneurs are more overconfident and less risk averse than non-entrepreneurs (Table 2). We

therefore compare the assessments provided by these two groups of economic agents (not

shown). Surprisingly, the rankings provided by non-entrepreneurs, managers in particular, are

almost identical to those observed for entrepreneurs. Luck is at the bottom of the rankings, and

the other success factors maintain their relative level of importance. The same holds when

comparing entrepreneurs and government employees.

- 15 -

The similarity in the answers could be genuine, but it could also suggest that it was

secretaries who filled out the questionnaire. To test this, we hypothesize that delegation would

be more likely to occur in larger firms, since there are no secretaries in small firms to begin with.

However, the ranking of luck is unrelated with firm size (not shown). Moreover, and contrary to

the notion that secretaries filled out the questionnaire, entrepreneurs and non-entrepreneurs differ

significantly in many of their other answers, including those relating to personal characteristics

(Table 2).

Overall, entrepreneurs appear to think in the same way as people who chose a different

career. Luck is always the least important success factor. Together with the evidence presented

in the preceding section of no significant perception bias, we therefore find no reason to believe

that entrepreneurs misread reality.

Our results have striking implications for the contribution that luck makes to performance.

If the six factors were uncorrelated, and if they were equally important, then each one would be

responsible for at most 1/6th (17 percent) of firm performance. And, since luck is actually the

least important success factor, it would explain even less than that. In what follows, we want to

take a closer look at this conclusion.

3.4 Principal component analysis

The conclusion rests on the assumption that there are in fact six independent success factors. To

test that, Panel C of Table 3 computes Kendall rank correlation coefficients between all the

different pairs of factor rankings. Because of the large number of observations, most coefficients

are significantly different from zero with confidence 0.95 or better, even if they are all

numerically fairly small. The only sizable coefficients are those linking experience, talent,

education, and effort, four personal characteristics that are easily transferable to other firms or

industries. Connections and especially luck are uncorrelated with the remaining factors.

A conservative interpretation of the panel is that there are only three fundamental factors of

success: transferable personal characteristics, connections, and luck. If so, luck would be

responsible for one third of performance variation at most. To investigate this formally, we

perform a principal component analysis. The limitation of this analysis is that we have to use

actual scores (as opposed to ranks). Three components explain 66 percent of total variation (not

shown). For an interpretation, Table 5 performs a varimax rotation of these three components.

- 16 -

The rotation maximizes the variance of the squared loadings and tends to generate components

with loadings of unity and zero. The first component loads on transferable personal

characteristics. The second component has a loading of 0.92 on connections, and minor loadings

on the remaining variables. The third component has a loading of 0.93 on luck, and negligible

loadings on the rest. If so, given that luck ranks last in importance and is one of three

uncorrelated components, it should in fact not explain more than 33 percent of firm performance.

We cannot exclude, however, that there might be additional factors that explain performance. If

so, the importance of luck would seem to be even smaller than 33 percent.

< Insert Table 5 here >

One possible reason for this limited role of luck could be that, as pointed out in Bhidé

(2000), entrepreneurs don’t typically pursue radically new ideas but mostly follow comparatively

safe strategies and replicate or modify ideas seen in previous employment. We come back to this

issue in the conclusions.

4 Entrepreneurial activities and luck

According to the evidence, we cannot reject the conclusion that, overall, luck plays a

comparatively limited role in overall performance. And since there is no reason to believe that

these perceptions are the result of bias, there is also no reason to believe that they do not

correspond to reality. One might need luck to come up with a highly successful product, but

even a moderately good product can be turned into a success with hard work, experience, and the

proper connections. Conversely, even a potentially great product that one stumbles upon does

not guarantee success unless it is supported by the appropriate expertise, hard work, and

connections. Yet a moderate role in performance doesn’t necessarily mean that luck is of little

relevance in general. Entrepreneurial success is a function of all the different activities that

enable firms to bring their products and services to market. Hence, luck could be very important

in some of those tasks and yet, if its overall relevance is an average across tasks, it might end up

having only little impact on overall performance.

To find out our hypotesis 2, the questionnaire asked respondents to indicate the importance

of luck in eight different areas, namely the identification of the right business idea, the decision

- 17 -

of when to enter the market, the hiring of employees, the gaining of customers, the securing of

suppliers, the obtaining of financial support, the establishing of business connections, and the

setting up of private connections. For each one of these activities, people were asked to score the

importance of luck from very important (1) to quite unimportant (5). We want to examine what

fraction of entrepreneurs believes luck is very important in at least one of these activities, and

test whether more entrepreneurs do so than the 15 percent we find in the case of overall firm

performance (Table 3). Moreover, we test whether there is any evidence that the rank assigned

to luck in performance is an average of the ranks given to luck in the individual activities.

Table 6 reports summary statistics. To avoid interpersonal comparisons of scores, we used

the scores given to the importance of luck in the eight different management areas to infer the

personal rankings of the importance of luck across the eight business activities. Finding the

business idea, gaining customers, and establishing business connections are management sectors

where luck is believed to play a very important role, as evidenced by median rank of 1 of these

factors. With a median rank of 2, establishing private connections and deciding when to enter

the market are areas where luck is slightly less important. Finding employees has a median rank

of 3. And obtaining suppliers and financing are activities least subject to the vagaries of chance

(median rank of 4).

< Insert Table 6 here >

There is no evidence that respondents provide undifferentiated assessments and simply

assign the same score to luck across management tasks. To see this, we used these personal

scores and conducted a principal component analysis and a varimax rotation (not shown). Luck

in each individual management activity loads only on one of seven factors (with a coefficient of

1). Hence, luck plays a separate role in each individual management activity. The exception is

that luck in private and business connection is driven by the same factor.

Table 7 therefore tests whether luck in individual management activities is seen as being

substantially more critical than in overall performance. The test focuses on the instances in

which entrepreneurs give the importance of luck the maximum possible score of 5, and therefore

avoids interpersonal comparisons. Close to 60 percent of the responding entrepreneurs do so for

at least one of the eight management tasks considered; 40 percent do it for at least two tasks, 25

- 18 -

percent for at least three, and 16 percent for at least four. By comparison, and as already

mentioned, only 15 percent assign luck the highest score in overall firm performance (Panel B of

Table 3). Thus, the majority of entrepreneurs view luck as being very important in at least one

management area, but only 15 percent believe it plays the most important role in overall

performance. This finding is consistent with our conclusion that personal characteristics such as

self-attribution and illusion of control cannot explain the low ranking assigned to luck in overall

performance. Otherwise, luck would be equally unimportant across management areas.

< Insert Table 7 here >

Yet why is there a difference in importance in individual management areas versus in the

overall performance? We hypothesize that entrepreneurs assess the relevance of luck in

performance by taking an average of its relevance across different management tasks. Different

weights in that average could reflect the different relevance of individual management tasks for

overall performance.

For a formal test of this proposition, we run a probit regression. The dependent variable,

importance of luck, equals 1 if the entrepreneur assigns luck the highest possible score of 5 in

importance as a determinant of performance and zero otherwise. The arguments are binary

variables equal to 1 if the entrepreneur believes luck is very important in the management area in

question (and zero otherwise). The results are in Table 8. With the exception of financing, all

the arguments have a significant coefficient. The importance of luck in performance therefore

seems to derive from the importance of luck in individual management tasks. Moreover, all

coefficients are smaller than 1, and their sum (if we include the intercept) equals 1.06, consistent

with the claim that the importance of luck in overall performance is a weighted average of the

scores in the individual management tasks. However, note that the relevance of luck in securing

suppliers is negatively related to luck’s overall importance. The possible interpretation is that

being lucky enough to lock up the right suppliers reduces the firm’s exposure to overall chance

because of the advice these suppliers provide. The explanatory power of the regression,

however, is limited. As suggested also by the significant intercept, there are probably other

sources or dimensions of luck outside the eight management areas considered.

- 19 -

< Insert Table 8 here >

In sum, luck in entrepreneurial success appears to derive from luck in various management

areas. Moreover, about 60 percent of the entrepreneurs believe luck plays a very important role

in at least one of those areas.

5 Perceived luck and decision making

The next question is whether perceptions affect decisions, and how. To answer it, note that

entrepreneurs who assign luck an important role believe that a significant part of firm

performance is the result of fortuitous events. Hence, assuming they are risk averse, they will

tend to either avoid situations that expose them to chance or try to be in a position to manage the

consequences of chance. We examine the following situations: (a) the entrepreneurial career

decision (hypothesis 3); (b) the use of debt in the initial start-up financing (hypothesis 4); and (c)

the decision to switch industry for repeat entrepreneurs (hypothesis 5).

5.1 The decision to become an entrepreneur

We model the decision to pursue an entrepreneurial career with a probit regression that borrows

from the extant literature (see, for example, the survey articles of Bhidé (2000), Rauch and Frese

(2000), and Parker (2004)). The difference is that we expand the set of regression arguments

with the scores assigned by respondents to the various drivers of entrepreneurial success. We

therefore estimate the following model:

Entrepreneuri = ai + ßi×(perceived importance of luck, perceived importance of other success

factors, control variables, identification variables)i + νi , (1)

where νi is a standard disturbance term, and entrepreneur is a binary variable equal to one if the

individual in question is an entrepreneur, and zero otherwise. Strictly taken, since we use cross-

sectional data, equation (1) does not model the decision to become an entrepreneur but rather the

probability of being one. Being an entrepreneur is the result of both a career decision and of the

probability of survival (Evans and Leighton (1989)). The results remain the same, however,

when we focus on the subset of entrepreneurs who started their company during the last year in

the sample. For them, given that they have been operating for at most one year, becoming an

- 20 -

entrepreneur should be the same as being one. We test whether the prospect of being exposed to

luck discourages an entrepreneurial career. The more strongly a risk-averse individual believes

that success is driven by random chance, the more reluctant he should be to opt for an

entrepreneurial career, as suggested by the experimental evidence in Camerer and Lovallo

(1999). It is not clear, though, how the perceptions about the importance of the remaining five

success factors affect that decision. They should all matter, since, as we saw, they are believed

to determine entrepreneurial success, but we cannot tell how. Believing, for example, that

education is important should encourage educated individuals to join the entrepreneurial ranks,

but it will deter uneducated people.

Table 9 reports the estimation results. In column (1), the coefficient of importance of luck is

negative and significant, as predicted. Believing that performance is a matter of luck does

indeed discourage people from going for an entrepreneurial career. Note that the variable

importance of luck is measured with the score provided by respondents. We measure the

importance of the remaining factors of success the same way. The results, however, remain

essentially the same when we measure importance with a binary variable (important vs.

unimportant). Using scores provides more variation in the measurement of these individual

factors.

< Insert Table 9 here >

Individuals who believe education is important are also deterred. As we mentioned, this

result could be driven by people who feel they lack the appropriate education. In contrast,

individuals who believe effort and connections are important are more likely to pursue an

entrepreneurial career, possibly because they are willing to put in the necessary effort and have

the necessary connections. We also find, however, that individuals who score experience and

talent as important success factors are not more likely to become entrepreneurs.

In column (2), we replace the subjective scores of the success factors (other than importance

of luck) with the actual proxies for those factors. The new variables are:

a) working, industry and management experience, three proxies for experience;

b) previously successful entrepreneur (previously unsuccessful entrepreneur), a proxy for skills,

according to Gompers, Kovner, Lerner, and Scharfstein (2010));

- 21 -

c) previously unemployed, a proxy inversely related with skills;

d) number of children, a proxy inversely related with effort;

e) foreigner, a proxy directly related with effort, under the assumption that foreigners are more

likely to put in an extra effort to compensate for the lack of proper connections. For

entrepreneurs, we could also measure effort with the variable part-time entrepreneur. The

problem is that we don’t have that information for non-entrepreneurs. We will use this

variable, however, in the subsequent analysis of entrepreneurial performance;

f) education and balanced education, two proxies for education; and

g) connections, a proxy for connections.

Under this specification, importance of luck maintains its negative and significant

coefficient. As for the other success factors, working and management experience, education,

the willingness to put in a higher effort, and connections (Honig and Davidsson (2000))

encourage an entrepreneurial career. However, longer industry experience has a negative

coefficient, possibly because industry-specific knowledge depreciates over time or because

longer industry experience is associated with better remuneration, which raises the opportunity

costs of entrepreneurship. Moreover, previously successful entrepreneurs don’t seem to be more

likely to get involved in another start-up. It is previously unsuccessful entrepreneurs who tend to

try again. Hence, the possible stigma associated with failure discussed in Landier (2006) does

not seem to discourage entrepreneurs from taking another crack. Failed entrepreneurs seem to

believe they have their chances, consistent with a deep market for failed entrepreneurs (Gromb

and Scharfstein (2005)). Along similar lines, previously unemployed individuals are also more

likely to embark on an entrepreneurial career, a regularity already noted by Evans and Leighton

(1989).

Column (3) repeats the estimation with the addition of the interaction variable importance of

luck*high management experience. High management experience is a binary variable equal to 1

if the individual’s management experience is in the highest quartile of the sample distribution,

and equal to zero otherwise. The purpose is to test whether the relevance of luck provides

different motivations, depending on people’s abilities. The hypothesis is that individuals with

good abilities are discouraged from becoming entrepreneurs if they believe performance is

mostly a matter of luck (Camerer and Lovallo (1999)). The evidence is consistent with this

hypothesis. The coefficient of the interaction term is negative and significant. The remaining

- 22 -

coefficients remain essentially unchanged. Note that the coefficient of importance of luck alone

loses its statistical significance.

Column (4) replaces high with low management experience in the interaction term. Low

management experience is a binary variable equal to 1 if the individual’s experience is in the

lowest quartile of the sample distribution, and equal to zero otherwise. Individuals with low self-

assessed skills could be attracted to an entrepreneurial career if they believe in the importance of

luck, since they may see better chances to succeed (Hogarth and Karelaia (2008)). The evidence,

however, contradicts this conjecture. This interaction term has a negative and significant

coefficient as well. These individuals might be afraid that their lack of experience could make it

more difficult to deal with the consequences of adverse developments.

The regressions include a number of control variables that describe personal characteristics

(not shown to save space). Several of their coefficient estimates have the same sign and

significance observed elsewhere in the literature with non-survey data. This increases our

confidence in the usefulness of our survey data. The coefficient of internal locus of control, for

example, is positive and highly significant. Hence, individuals who believe they control their

life are more likely to opt for an entrepreneurial career. Perhaps not surprisingly, people in

Protestant regions are also more likely to try an entrepreneurial career, possibly because they

believe in the virtues of high work ethic. Moreover, risk aversion has a negative effect

(Brockhaus (1980), Stewart Jr. and Roth (2001)) and overconfidence has a positive one,

consistent with Holtz-Eakin, Joulfaian, and Rosen (1994) and Camerer and Lovallo (1999).

Furthermore, divorced individuals have a higher propensity for trying an entrepreneurial career,

which they might see as the opportunity for a change. The opposite seems to be the case for

married people. The risk of failure is probably too large to take. We also find that women are

significantly less likely to enter the entrepreneurial ranks. Finally, personal age has a nonlinear

impact, in line with Van Gelderen, Thurik, and Bosma (2006). The probability of becoming an

entrepreneur first increases until age 33, and then it declines.

The regressions also include five identification variables used later in our Heckman two-

stage analysis of firm performance. The first one is career by chance, a binary variable that

identifies individuals who claim to have chosen their career by chance. Similarly, need for

achievement, a psychological trait often mentioned in the management and psychology literature

(Zhao and Seibert (2006)), also has a positive and significant coefficient. We also find that

- 23 -

personal wealth encourages the entrepreneurial decision (Hurst and Lusardi (2004)). The same

goes for individuals who worked for small firms (Barnett and Dobrev (2005), Sørensen (2007))

and, in part, for people with entrepreneurial parents (Blanchflower and Oswald (1998)).

In conclusion, the results in Table 9 therefore indicate that the entrepreneurial decision is

shaped by what people believe, particularly about the role that luck plays in bringing about

success. Consistent with our predictions, those who believe luck is important tend to be reluctant

to embark on an entrepreneurial career. Perceptions about the importance of the other success

factors and the proxies for those factors also matter. In spite of all the measurement errors, these

results are economically significant. To assess that, we used a binary variable to distinguish

cases in which luck was deemed to be of some importance (scores larger than 1) as opposed to

no importance at all (scores equal to 1). When we repeat the estimation with that definition (not

shown), we find that individuals who assign luck at least some importance are about 7 percent

less likely to become entrepreneurs. As it turns out, this effect is similar to that of believing that

connections are important, but about half the discouraging effect of being a woman.

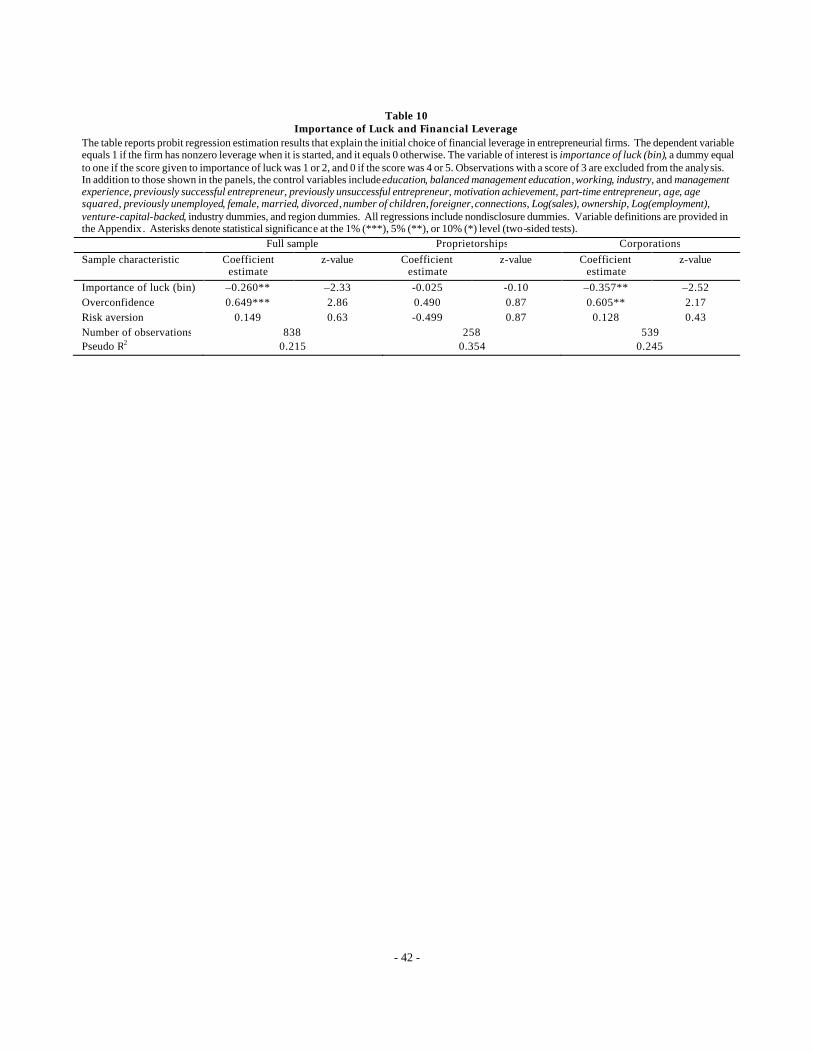

5.2 Luck perceptions and financial leverage

We also want to know whether the perceived importance of luck shapes financing choices. In

Landier and Thesmar (2009), optimistic entrepreneurs prefer short-term debt. We hypothesize

that, holding risk aversion constant, entrepreneurs who believe luck plays an important role in

performance choose lower leverage to reduce their exposure to the risk of financial distress.

Formally, we estimate probit regressions of leverage on the binary variable importance of luck

(bin). The specification is the same as that of column (2) of Table 9. The dependent variable,

financial leverage, is binary, and it equals 1 if the firm relies on debt financing, and 0 otherwise.

As it turns out the maximum leverage is 11 percent in proprietorships, compared with 47

percent in limited-liability companies, and 38 percent in corporations. Moreover, 74 percent of

the proprietorships in the sample have no debt at all, compared to 66 percent in limited-liability

companies, and 59 percent in corporations. Possibly, proprietorships are unable to access the

debt market. Hence, our predictions apply to limited- liability companies and corporations only.

Estimation results are in Table 10. Consistent with the prediction, importance of luck in the

full sample has a negative and significant coefficient: The higher the importance of luck, the

lower the firm’s financial leverage. Capital structure decisions are therefore not only affected by

- 24 -

optimism (as in Landier and Thesmar (2009)), but also by views about the importance of luck.

The table also reports the coefficients of selected control variables. Overconfidence has a

positive and significant coefficient, possibly because it induces people to downplay the risks of

insolvency, while risk aversion is unrelated with leverage. When splitting the sample into

proprietorships and corporations, we see that the significance of importance of luck (bin) comes

in fact from corporations.

< Insert Table 10 here >

5.3 Luck perceptions and the decision to switch industry

Finally, we examine whether perceived abnormal performance affects the decision of repeat

entrepreneurs to stay in the same industry or to switch to a different one. According to the

evidence (not shown), serial entrepreneurs that decide to remain in the same industry are without

exception entrepreneurs who believe they performed better than expected, i.e., had good luck. In

contrast, serial entrepreneurs who decided to switch industry for their new start-up invariably

think they did worse than expected in their previous venture, i.e., they believe they experienced

bad luck. Hence, perceptions about chance affect the industry which entrepreneurs decide to

operate in.

6 Perceived luck and unexplained performance

The last step in the analysis is to clarify what entrepreneurs have in mind when they think of

luck. All our questions referred to luck as unexpected events. Of course, there is no guarantee

that respondents had that in mind when they answered. As a validation test, we therefore

investigate whether what is unexpected to entrepreneurs correlates with the unexplained

component in a standard model of entrepreneurial performance.

6.1 The performance regression

For our test, we need more than simply the variable importance of luck, since that variable

measures a hypothetical importance. Here, we want an assessment of luck in specific cases. As

possible proxies, we therefore use two measures of actual luck, namely good luck (a binary

- 25 -

variable equal to 1 if the entrepreneur says performance was better than expected, and equal to 0

otherwise) and bad luck (a binary variable equal to 1 if the entrepreneur says performance was

worse than expected, and equal to 0 otherwise).5 In 37 percent of the cases, entrepreneurs say

they had good luck, in 13 percent they say they had bad luck. In the remaining 50 percent of the

cases, they claim to have performed as expected. The performance model we use is similar to

that in Bitler, Moskowitz, and Vissing-Jørgensen (2005) and Gompers, Kovner, Lerner, and

Scharfstein (2010). Formally, we estimate the following cross-sectional regression:

Performancei = a i + ßi×(skills, personal characteristics, control variables)i + ε i , (3)

where i indicates the entrepreneur and his firm, and ε i is the unexplained component. As stated

in the introduction, there are various reasons to believe this unexplained component is a noisy,

and possibly biased proxy of luck. We can therefore represent it as the sum of three terms:

Unexplained component of performance = ε = true luck + bias + noise. (4)

Hence, if our subjective proxies for luck (good luck, bad luck) measure what we believe they

measure, they should be correlated with unexplained performance via the true luck component.

To alleviate the concern that our proxies are systematically influenced by characteristics that also

lead to bias in unexplained performance, we include a large number of control variables for

personal characteristics, as well as firm characteristics and time.

In the following analysis, we first estimate equation (3) without the two proxies for luck in

order to estimate what fraction of performance can be explained by the standard performance

5 This measure of unexpected performance is related but different from Landier and Thesmar’s (2009) measure of

optimism. Landier and Thesmar have information on the anticipated sales at the time of firm founding. Optimism is the difference between actual and anticipated sales at the time of founding. Our measure of unexpected performance relies on an ex-post measure of expectations. Consequently, if recall is imperfect or if expectations are revised over time, our measure of unexpected performance differs from Landier and Thesmar’s (2009) measure of optimism. For an alternative measure of optimism, see Puri and Robinson (2007).

- 26 -

model. Later, we add the proxies for luck to test whether these proxies correlate with the

unexplained variation in performance.

6.2 Estimation results

Because entrepreneurs are unlikely to be drawn from a random sample of individuals, we

perform the analysis of equation (3) with a Heckman two-stage estimation procedure.

Entrepreneurs might possess unobserved characteristics related to entrepreneurial performance

that could bias the estimates of equation (3) (Hamilton (2000)). We therefore use the model of

entrepreneurial career choice in equation (1) as the first stage. Although the non-linearities of

the probit model might already fulfill the exclusion restrictions (Wooldridge (2002)), we rely on

the identification variables described in the discussion of equation (1) above. In the second-stage

regression, we estimate the performance regression (3) with the addition of the inverse Mills

ratio from the first stage.

When estimating the second-stage regression equation (3), the number of observations

differs across performance proxies as not all respondents provided the necessary information.

There are 2,348 observations for sales, 1,511 for aggregate income, and 1,433 for return on

initial capital (ROI). Depending on the proxy for performance, the model explains 6.9 percent

(return on initial capital), 13.1 percent (aggregate income), and 37.6 percent (sales) of the cross-

sectional variation in industry-adjusted performance, respectively (not shown).

We then estimate the performance regression (3), augmented with the two proxies good luck

and bad luck. If they are related to unexplained performance, the two proxies should have power

to explain the error term in (3). Furthermore, whereas good luck should have a positive

coefficient, bad luck should have a negative one.

The evidence in Table 11 confirms all three predictions. Both variables have highly

significant coefficients regardless of how we measure performance. Moreover, they have a

symmetric effect—the absolute value of their coefficients is practically identical, except in the

regression that examines the return on invested capital. An alternative interpretation of the

negative coefficient of our bad luck variable could be optimism since optimistic entrepreneurs

are more likely to be disappointed with their business progress (Hmieleski and Baron (2009)).

However, since we control for unobserved heterogeneity, optimism should not distort our results.

- 27 -

< Insert Table 11 here >

The two luck variables have also tangible explanatory power, which can be shown in two

different ways. First, we compute the difference in R-squared when adding the two variables in

the regression equation. When we do so, we obtain incremental differences in R-squared values

of 5.5 percent (sales), 10.2 percent (income), and 4.6 percent (ROI), respectively. This

corresponds to a relative increase in explanatory power of 15 percent (sales), 63 percent

(income), and 47 percent (ROI). This procedure assumes that the luck variables are orthogonal

to the model’s other arguments. As an alternative, we employ the method suggested by Kruskal

(1987) and average the differences in R-squared observed when entering the proxies for luck in

regressions involving all possible combinations of the arguments in the model.6 Under this

approach, the contribution of luck to the R-squared of the regressions is 8.3 percent (sales), 12.8

percent (income) and 5.0 percent (ROI), respectively.

The implication of all this is that what entrepreneurs have in mind when they envision

chance is correlated with unexplained performance variation. Hence, perceived luck is

unexpected performance shocks. Remember, however: not only is the assessment of luck self-

reported, but also the performance measures are. The analysis also allows for interesting

comparisons with the extant literature, which has used performance regression models such as

(3) quite extensively. In the following, we briefly describe how our survey-based estimation

results compare with earlier studies that have used other sources of data.

Table 11 also reports the coefficient estimates of the various control variables. A brief look

shows that the success factors are indeed related to performance, and mostly in line with the

extant literature. In particular, management experience has generally a positive effect, consistent

with Kaplan, Sensoy, and Strömberg (2009). So does, at least marginally, industry experience,

as in Chatterji (2009). Similarly, part-time entrepreneur has a significantly negative relation

with sales, in agreement with the notion that a feeble effort weakens performance. Number of

6 For example, to obtain the relative importance of x1 in the case of a regression with two independent variables

(x1, x2), we take the average of two changes in R-squared. The first change is that observed when x1 is the only regressor compared to a regression without any independent variables. The second change is that computed when going from a regression with x2 as the only regressor to a regression with both independent variables.

- 28 -

children, another proxy for effort (entrepreneurs of larger families might have to work harder to

maintain them), has a positive coefficient, at least in the case of sales. Likewise does foreigner.

Foreigners probably have to compensate for weaker networks and institutional knowledge with a

greater effort. These results are compatible with those of Bitler, Moskowitz, and Vissing-

Jørgensen (2005). Furthermore, both proxies for education and talent (education and balanced

education) have positive and significant coefficients. However, previously successful

entrepreneur and previously unsuccessful entrepreneur, two other proxies for talent, are

unrelated with performance. This latter finding seems to contradict Gompers, Kovner, Lerner,

and Scharfstein (2010) who find performance persistence among previously successful

entrepreneurs. Yet previous success could be a proxy for variables included here but not in that

paper, such as management experience and management education.7 The results also show that,

having been unemployed before becoming an entrepreneur has generally a negative effect,

possibly because formerly unemployed people are less talented entrepreneurs, consistent with

Evans and Leighton (1989). Finally, the last success factor, connections, has insignificant

coefficients.