LOOKING FORWARD - Workplace Benefit Solutions – Live ... · PDF fileLOOKING FORWARD TO...

20

Transitioning to a new 403(b) program Iowa Retirement Investors’ Club (RIC) LOOKING FORWARD TO RETIREMENT.

Transcript of LOOKING FORWARD - Workplace Benefit Solutions – Live ... · PDF fileLOOKING FORWARD TO...

Transitioning to a new 403(b) program

Iowa Retirement Investors’ Club (RIC)

LOOKING FORWARDTO RETIREMENT.

2

MassMutual Retiresmart℠▶ What’s happening?

This notice is being sent to you to advise you of important upcoming enhancements to the Iowa Retirement Investor’s

Club (RIC) 403(b) Plan (“the Plan”). Following an extensive review by Iowa RIC, it was decided to provide a new

investment product and enhance the recordkeeping platform used to access participant account activity.

• Effective March 7, 2016, all contributions will be deposited in a new MassMutual product. Deposits will be

made to similar investments as you had in the old product. (see Money Directed to the New Product section).

• Existing account balances will remain in the old product unless you choose to consolidate (see How do I move

my account from the old to new product? section).

• A new website for the new product will be available March 10, 2016 with updated resources and tools.

▶ Why the change?

Iowa RIC is committed to providing you with a convenient and cost-effective way to save for your retirement. Features

in the new product could potentially help you reach your retirement goals, including:

• The overall cost to administer the new product is being reduced by modifying the fee structure using a process

called “fee leveling” (see Fee Leveling section).

• Transitioning to a registered mutual fund line-up for new contributions (by active employees) and exchanged

assets from the old product will make following your investments easy and straightforward.

• Updated resources and tools accessed via the new RetireSmartSM participant website at

www.massmutual.com/iowaric.

▶ What happens to my old account?

Assets remain invested in the old product unless you move them to the new product (see How do I move my account

from the old to new product? section).

Notice to actively contributing employees – If you leave your assets in the old product, you will have two accounts

and it could be difficult to manage when accessing account information, making investment changes, or taking

distributions.

If you move your assets to the new product, you will have one account, allowing for one statement, one phone

number, and one website to access your account, manage investment selections and request withdrawals.

Consolidation may not be right for everyone. Individual situations will vary. Consider seeking consultation from your

independent financial advisor before consolidating.

3

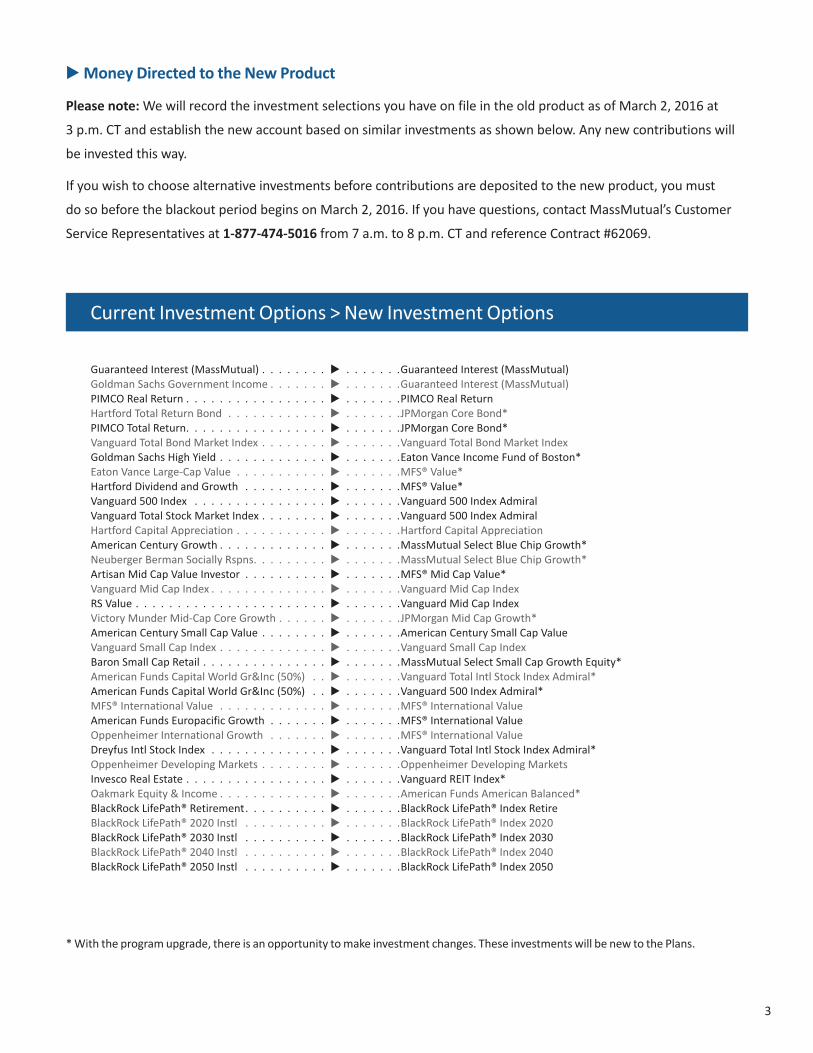

▶ Money Directed to the New Product

Please note: We will record the investment selections you have on file in the old product as of March 2, 2016 at

3 p.m. CT and establish the new account based on similar investments as shown below. Any new contributions will

be invested this way.

If you wish to choose alternative investments before contributions are deposited to the new product, you must

do so before the blackout period begins on March 2, 2016. If you have questions, contact MassMutual’s Customer

Service Representatives at 1-877-474-5016 from 7 a.m. to 8 p.m. CT and reference Contract #62069.

Current Investment Options > New Investment Options

Guaranteed Interest (MassMutual) . . . . . . . . ▶ . . . . . . .Guaranteed Interest (MassMutual)Goldman Sachs Government Income . . . . . . . ▶ . . . . . . .Guaranteed Interest (MassMutual)PIMCO Real Return . . . . . . . . . . . . . . . . . ▶ . . . . . . .PIMCO Real ReturnHartford Total Return Bond . . . . . . . . . . . . ▶ . . . . . . .JPMorgan Core Bond*PIMCO Total Return. . . . . . . . . . . . . . . . . ▶ . . . . . . .JPMorgan Core Bond*Vanguard Total Bond Market Index . . . . . . . . ▶ . . . . . . .Vanguard Total Bond Market Index Goldman Sachs High Yield . . . . . . . . . . . . . ▶ . . . . . . .Eaton Vance Income Fund of Boston*Eaton Vance Large-Cap Value . . . . . . . . . . . ▶ . . . . . . .MFS® Value*Hartford Dividend and Growth . . . . . . . . . . ▶ . . . . . . .MFS® Value*Vanguard 500 Index . . . . . . . . . . . . . . . . ▶ . . . . . . .Vanguard 500 Index AdmiralVanguard Total Stock Market Index . . . . . . . . ▶ . . . . . . .Vanguard 500 Index AdmiralHartford Capital Appreciation . . . . . . . . . . . ▶ . . . . . . .Hartford Capital AppreciationAmerican Century Growth . . . . . . . . . . . . . ▶ . . . . . . .MassMutual Select Blue Chip Growth*Neuberger Berman Socially Rspns. . . . . . . . . ▶ . . . . . . .MassMutual Select Blue Chip Growth* Artisan Mid Cap Value Investor . . . . . . . . . . ▶ . . . . . . .MFS® Mid Cap Value*Vanguard Mid Cap Index . . . . . . . . . . . . . . ▶ . . . . . . .Vanguard Mid Cap IndexRS Value . . . . . . . . . . . . . . . . . . . . . . . ▶ . . . . . . .Vanguard Mid Cap IndexVictory Munder Mid-Cap Core Growth . . . . . . ▶ . . . . . . .JPMorgan Mid Cap Growth*American Century Small Cap Value . . . . . . . . ▶ . . . . . . .American Century Small Cap ValueVanguard Small Cap Index . . . . . . . . . . . . . ▶ . . . . . . .Vanguard Small Cap IndexBaron Small Cap Retail . . . . . . . . . . . . . . . ▶ . . . . . . .MassMutual Select Small Cap Growth Equity*American Funds Capital World Gr&Inc (50%) . . ▶ . . . . . . .Vanguard Total Intl Stock Index Admiral*American Funds Capital World Gr&Inc (50%) . . ▶ . . . . . . .Vanguard 500 Index Admiral*MFS® International Value . . . . . . . . . . . . . ▶ . . . . . . .MFS® International ValueAmerican Funds Europacific Growth . . . . . . . ▶ . . . . . . .MFS® International ValueOppenheimer International Growth . . . . . . . ▶ . . . . . . .MFS® International ValueDreyfus Intl Stock Index . . . . . . . . . . . . . . ▶ . . . . . . .Vanguard Total Intl Stock Index Admiral*Oppenheimer Developing Markets . . . . . . . . ▶ . . . . . . .Oppenheimer Developing MarketsInvesco Real Estate . . . . . . . . . . . . . . . . . ▶ . . . . . . .Vanguard REIT Index*Oakmark Equity & Income . . . . . . . . . . . . . ▶ . . . . . . .American Funds American Balanced*BlackRock LifePath® Retirement. . . . . . . . . . ▶ . . . . . . .BlackRock LifePath® Index RetireBlackRock LifePath® 2020 Instl . . . . . . . . . . ▶ . . . . . . .BlackRock LifePath® Index 2020BlackRock LifePath® 2030 Instl . . . . . . . . . . ▶ . . . . . . .BlackRock LifePath® Index 2030 BlackRock LifePath® 2040 Instl . . . . . . . . . . ▶ . . . . . . .BlackRock LifePath® Index 2040 BlackRock LifePath® 2050 Instl . . . . . . . . . . ▶ . . . . . . .BlackRock LifePath® Index 2050

* With the program upgrade, there is an opportunity to make investment changes. These investments will be new to the Plans.

4

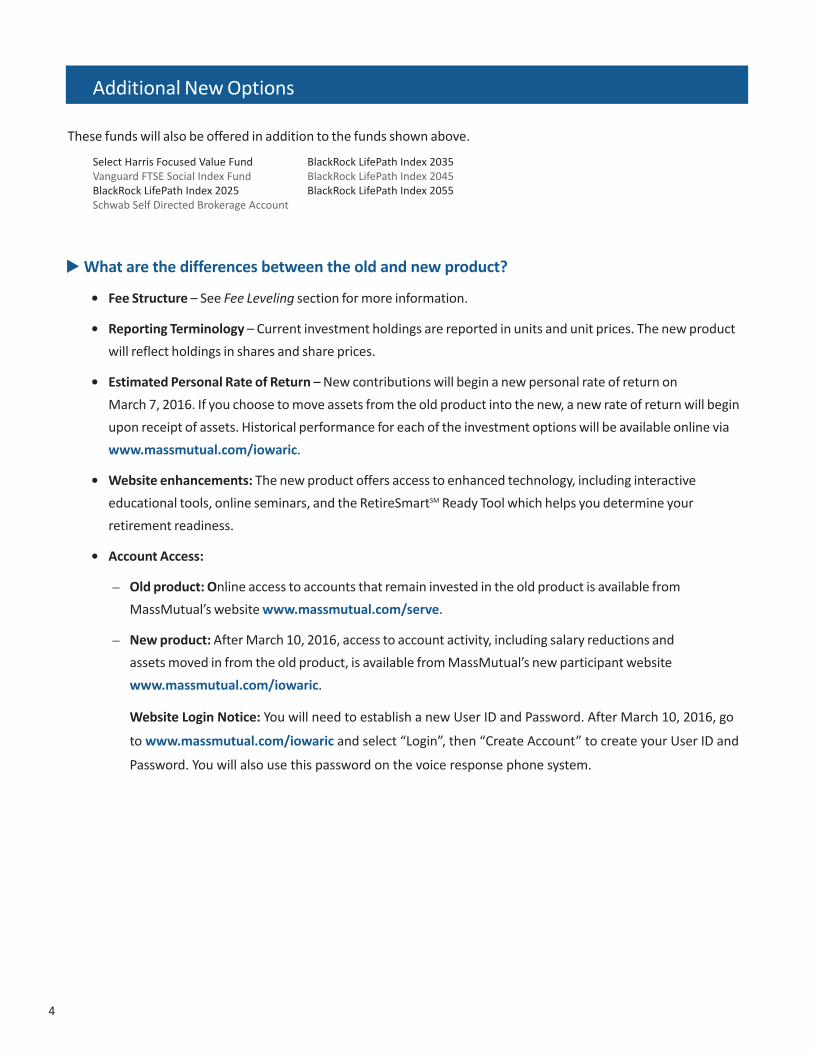

Select Harris Focused Value FundVanguard FTSE Social Index FundBlackRock LifePath Index 2025Schwab Self Directed Brokerage Account

BlackRock LifePath Index 2035BlackRock LifePath Index 2045BlackRock LifePath Index 2055

Additional New Options

These funds will also be offered in addition to the funds shown above.

▶ What are the differences between the old and new product?

• Fee Structure – See Fee Leveling section for more information.

• Reporting Terminology – Current investment holdings are reported in units and unit prices. The new product

will reflect holdings in shares and share prices.

• Estimated Personal Rate of Return – New contributions will begin a new personal rate of return on

March 7, 2016. If you choose to move assets from the old product into the new, a new rate of return will begin

upon receipt of assets. Historical performance for each of the investment options will be available online via

www.massmutual.com/iowaric.

• Website enhancements: The new product offers access to enhanced technology, including interactive

educational tools, online seminars, and the RetireSmartSM Ready Tool which helps you determine your

retirement readiness.

• Account Access:

– Old product: Online access to accounts that remain invested in the old product is available from

MassMutual’s website www.massmutual.com/serve.

– New product: After March 10, 2016, access to account activity, including salary reductions and

assets moved in from the old product, is available from MassMutual’s new participant website

www.massmutual.com/iowaric.

Website Login Notice: You will need to establish a new User ID and Password. After March 10, 2016, go

to www.massmutual.com/iowaric and select “Login”, then “Create Account” to create your User ID and

Password. You will also use this password on the voice response phone system.

• Fixed Account Rate:

– Old product: 4%

– New product: The Fixed Account rate will have the following schedule over the next six years:

Year 1 (through 12/31/16): 4.00%

Year 2 (1/1/17 – 12/31/17): 3.50%

Year 3 (1/1/18 – 12/31/18): 3.25%

Year 4 (1/1/19 – 12/31/19): 3.00%

Year 5 (1/1/20 – 12/31/20): 2.85%

Year 6 (1/1/21 – 12/31/21): 2.85%

• Loans: Loans will be offered in both products. You will not have the ability to transfer an outstanding loan

from the old to new product. If you have an outstanding loan from the old product, payments will continue

as scheduled.

• Death Benefit: The old product provides for a death benefit equaling the greater of contributions made or your

account value at the time of your death up to the age of 65. The new product provides the market value of your

account upon death.

• Existing Systematic Withdrawal Payments: If you are a former employee or retiree receiving a systematic

withdrawal payment and you choose to stay in the old product, your payments will continue as scheduled.

If you choose to transfer your account from the old to new product and are currently receiving a systematic

withdrawal payment, you will need to complete a new form (enclosed) to reestablish systematic

withdrawal payments.

▶ Moving money from the old to new product (Contract Exchange)

To move your old account assets to the new MassMutual product: Complete the enclosed 403(b) Internal Transfer

Form. All forms received in good order by MassMutual from the time of this mailing through April 15, 2016 will

be processed on April 18, 2016. Any forms received after April 18, 2016 will be processed as they are received in

good order.

If you need help completing paperwork, call MassMutual’s Concierge Team at 1-888-526-6905.

Important Note: Assets transferred to the new product will be applied to your current investment selections in the

new product account. Therefore, if you make investment selection changes in the new product prior to the asset

transfer, your monies will be invested based on those selections.

If you have not made investment changes in the new account prior to a transfer, the transferred assets will

be invested based on your investment selections in the old product as of March 2, 2016 and the corresponding

new investment options in the chart on page 3. Before you transfer assets to the new product, we encourage

you to verify your allocations and make changes, if needed, by logging into your new product account via

www.massmutual.com/iowaric or calling MassMutual’s Customer Service Center at 1-800-743-5274.

5

Assets moved out of the old product may not be reinvested in the old product. Consolidation may not be right for

everyone. Individual situations will vary. Consider seeking consultation from your independent financial advisor

before consolidating.

▶ Fee Leveling

Investors in the new product will experience a new fee structure called “fee leveling.” Simply put, fee leveling means

a more equitable sharing of fees between all participants.

• Currently, recordkeeping services are provided through a process called revenue sharing: each investment

option charges a fee, and then shares a portion of the fee with the recordkeeper. This means participants

who invest in a fund that provides a higher revenue-sharing percentage pay more of the overall

administrative costs.

• After the change to fee leveling, revenue sharing fees are removed and an annual flat fee of .20% is applied to

all investments, in addition to the standard investment fees, making expenses more equitable for everyone.

You will see the fee expressed as a dollar amount on your quarterly statement in the Expense Detail section

(pictured below). This reduces the overall cost to administer the Plan, resulting in potential cost savings to you

as a Plan participant.

SAVEALLOCATE CONSOLIDATE PLANSAVEALLOCATE CONSOLIDATE PLAN

Account Summary

ABC Organization Retirement Savings Plan Retirement Plan Statement account number: 12345-1-1-1

Cash 999%Bond 999%Stock 999%Asset Allocation 999%(includes Lifestyle/Lifecycle)

Total: 999%

Total: 100%

Asset Allocation 0%(includes Lifestyle/Lifecycle)

Stock 73%Bond 0%Cash 27%

Balances are rounded. Investments with less than 1% are not shown.

Investment Mix by Asset ClassBeginning Balance $73,843.02Contributions Participant $144.72 Employer $825.78Other Deposits $314.70Withdrawals $0Expenses $43.29Gain/Loss $8,964.69Ending Balance $86,589.27Vested Balance $86,589.27Change this Period $10,166.53

Vested balance includes your outstanding loan(s).

Rate of ReturnThis Period 11.94%Year-to-Date 8.03%

Estimated dollar-weighted rates of return based on cash flow in account. The calculation assumes an evenly distributed cash flow throughout applicable periods. Returns could be distorted by non-period transactions and may differ from the investment option performance because of the level and timing of cash flows.

Contact InformationFor additional information:

1-800-743-5274www.retiresmart.com

04/01/2014 – 06/30/2014

Birth Year: 1961 Hire Date: Not on file

ALLOCATE Research has shown that 90% of an investment’s return over time was based on how its assets were allocated and not on its specific investments. Log on to

www.retiresmart.com to take a risk quiz, or learn more about asset allocation and how to rebalance your account periodically with MassMutual’s Cruise Control feature. (Source: “Does Asset Allocation Policy Explain 40, 90, or 100 Percent of Performance?” by Roger G. Ibbotson and Paul D. Kaplan, ©2000, Association for Investment Management and Research.)

999999 999999 999999ACS 111111111111112222223333333444490 FP 1 B 1 1 A 10061 10087 **5 DGT

MR. KENNETH JONES, PLAN ADMINISTRATORABC ORGANIZATION RETIREMENT SAVINGS PLANP.O. BOX 123MIDDLE CITY, MA 12345

EDWARD SMITH10132 MAIN STREETMIDDLE CITY, MA 12345

6

For questions related to the old product

Call MassMutual at 1-800-528-9009 or log on to www.massmutual.com/serve.

For questions related to the timeline

Call MassMutual at 1-877-474-5016 from 7 a.m. to 8 p.m. CT and reference Contract #62069.

For questions related to the new product (after March 10, 2016)

Call MassMutual at 1-800-743-5274 or log on to the RetireSmartSM website via www.massmutual.com/iowaric.

Contact your local advisor:

We encourage you to call MassMutual’s Customer Service Center at 1-800-528-9009 before March 9, 2016 or

1-800-743-5274 after March 10, 2016 if you are unsure who your advisor is.

When will I be able to access my new account with MassMutual

After March 10, 2016, log on to the participant website via www.massmutual.com/iowaric and select “Create

Account” to create your new User ID and Password. You will also use this Password on the voice response phone

system. Then, you can access your account, learn more about your investment options, take an online risk quiz

to help determine what investment strategy is right for you and more – all to help you RetireSmartSM.

If assets remain in the old product, you will continue to access that account at www.massmutual.com/serve.

Get answers Help is just a click or call away:

SAVE LEARNALLOCATE CONSOLIDATE PLAN

7

8

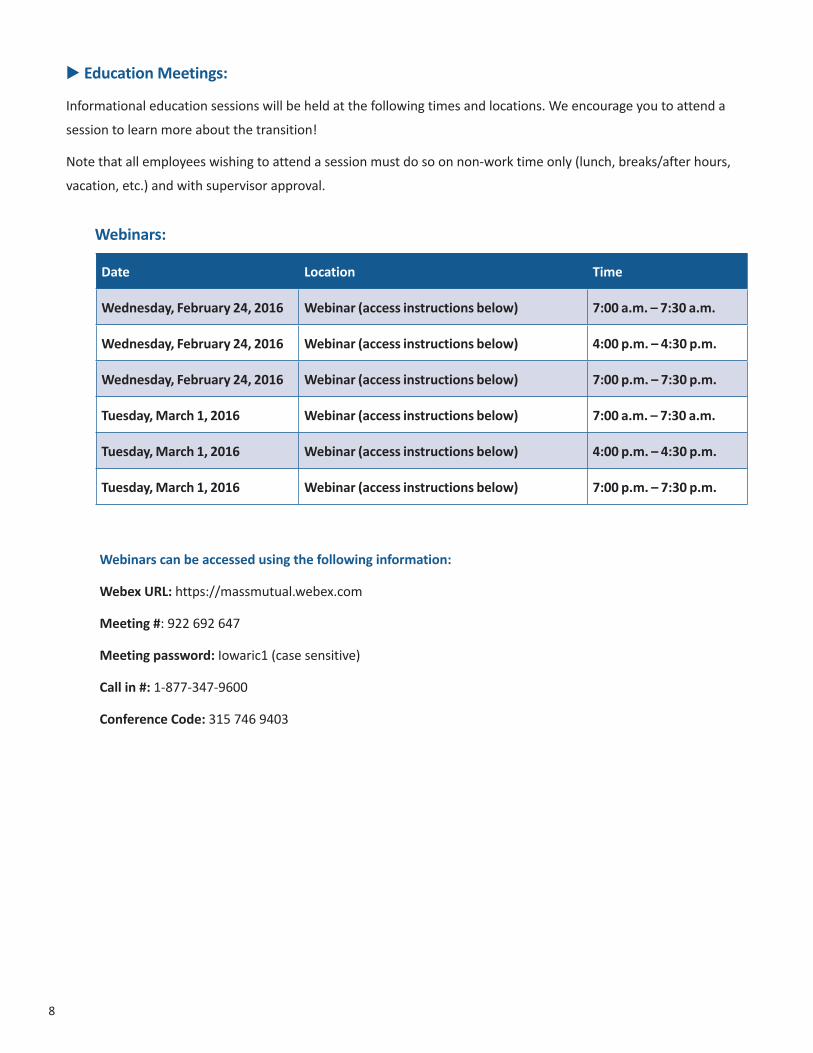

▶ Education Meetings:

Informational education sessions will be held at the following times and locations. We encourage you to attend a

session to learn more about the transition!

Note that all employees wishing to attend a session must do so on non-work time only (lunch, breaks/after hours,

vacation, etc.) and with supervisor approval.

Webinars can be accessed using the following information:

Webex URL: https://massmutual.webex.com

Meeting #: 922 692 647

Meeting password: Iowaric1 (case sensitive)

Call in #: 1-877-347-9600

Conference Code: 315 746 9403

Date Location Time

Wednesday, February 24, 2016 Webinar (access instructions below) 7:00 a.m. – 7:30 a.m.

Wednesday, February 24, 2016 Webinar (access instructions below) 4:00 p.m. – 4:30 p.m.

Wednesday, February 24, 2016 Webinar (access instructions below) 7:00 p.m. – 7:30 p.m.

Tuesday, March 1, 2016 Webinar (access instructions below) 7:00 a.m. – 7:30 a.m.

Tuesday, March 1, 2016 Webinar (access instructions below) 4:00 p.m. – 4:30 p.m.

Tuesday, March 1, 2016 Webinar (access instructions below) 7:00 p.m. – 7:30 p.m.

Webinars:

9

Notes:

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

_______________________________________________________________________________

RISK DISCLOSURES FOR CERTAIN ASSET CATEGORIES – PLEASE NOTE THAT YOUR PLAN MAY NOT OFFER ALL OF THE INVESTMENT TYPES DISCUSSED BELOW.

Please consider an investment option’s objectives, risks, fees and expenses carefully before investing. This and other information about the investment option can be found in the applicable prospectuses or summary prospectuses, if any, or fact sheets for the investment options listed, which are available from your plan sponsor, the participant web site at www.retiresmart.com, or by contacting our Participant Information Center at 1-800-743-5274 between 8:00 a.m. and 9:00 p.m. ET, Monday through Friday. Please read them carefully before investing.

If a retirement plan fully or partially terminates its investment in the Guaranteed Interest Account (GIA), SF Guaranteed, Fixed Interest Account or SAGIC investment options, the plan receives the liquidation value of its investment, which may either be more or less than the book value of its investment. As a result of this adjustment, a participant’s account balance may be either increased or decreased if the plan fully or partially terminates the contract with MassMutual.

Generally target retirement date (lifecycle) investment options are designed to be held beyond the presumed retirement date to offer a continuing investment option for the investor in retirement. The year in the investment option name refers to the approximate year an investor in the option would plan to retire and likely would stop making new contributions to the investment option. However, investors may choose a date other than their presumed retirement date to be more conservative or aggressive depending on their own risk tolerance.

Target retirement date (lifecycle) investment options are designed for participants who plan to withdraw the value of their accounts gradually after retirement. Each of these options follows its own asset allocation path (“glide path”) to progressively reduce its equity exposure and become more conservative over time. Options may not reach their most conservative allocation until after their target date. Others may reach their most conservative allocation in their target date year. Investors should consider their own personal risk tolerance, circumstances and financial situation. These options should not be selected solely on a single factor such as age or retirement date. Please consult the prospectus (if applicable) pertaining to the options to determine if their glide path is consistent with your long-term financial plan. Target retirement date investment options’ stated asset allocation may be subject to change. Investments in these options are not guaranteed and you may experience losses, including losses near, at, or after the target date. Additionally, there is no guarantee that the options will provide adequate income at and through retirement.

Risks of investing in bond and debt securities investments include the risk that a bond issuer will default by failing to repay principal and interest in a timely manner (credit risk) and/or the risk that the value of these securities will decline when interest rates increase (interest rate risk).

Risks of investing in inflation-protected bond investments include credit risk and interest rate risk. Neither the bond investment nor its yield is guaranteed by the U.S. Government.

High yield bond investments are generally subject to greater market fluctuations and risk of loss of income and principal than lower yielding debt securities investments.

Investments in value stocks may remain undervalued for extended periods of time, and the market may not recognize the intrinsic value of these securities.

Investments that track a benchmark index are professionally managed investments. However, the benchmark index itself is unmanaged and does not incur fees or expenses and cannot be purchased directly for investment.

Investments in growth stocks may experience price volatility due to their sensitivity to market fluctuations and dependence on future earnings expectations.

Investments in companies with small or mid market capitalization (“small caps” or “mid caps”) may be subject to special risks given their characteristic narrow markets, limited financial resources, and less liquid stocks, all of which may cause price volatility.

International/global investing can involve special risks, such as political changes and currency fluctuations. These risks are heightened in emerging markets. Participants must submit purchase transactions for global and international investment options before 2:30 p.m. ET in order to receive that day’s price. Other trading restrictions may apply. Please see the investment’s prospectus for more details.

A significant percentage of the underlying investments in aggressive asset allocation portfolio options have a higher than average risk exposure. Investors should consider their risk tolerance carefully before choosing such a strategy.

An investment with multiple underlying investments (which may include RetireSmartSM and any other offered proprietary or non-proprietary asset-allocation, lifestyle, lifecycle or custom blended investments) may be subject to the expenses of those underlying investments in addition to those of the investment itself.

Investments may reside in the specialty category due to 1) allowable investment flexibility that precludes classification in standard asset categories and/or 2) investment concentration in a limited group of securities or industry sectors). Investments in this category may be more volatile than less-flexible and/or less-concentrated investments and may be appropriate as only a minor component in an investor’s overall portfolio.

Participants with a large ownership interest in a company or employer stock investment may have the potential to manipulate the value of units of this investment option through their trading practices. As a result, special transfer restrictions may apply. This type of investment option presents a higher degree of risk than diversified investment options under the plan because it invests in the securities of a single company.

Investments that invest more of their assets in a single issuer or industry sector (such as company stock or sector investments) involve additional risks, including unit price fluctuations, because of the increased concentration of investments.

A participant will be prohibited from transferring into most mutual funds and similar investments if they have transferred into and out of the same investment within the previous 60 days. Certain stable value, guaranteed interest, fixed income and other investments are not subject to this rule. This rule does not prohibit participants from transferring out of any investment at any time.

Excessive Trading Policy: MassMutual strongly discourages plan participants from engaging in excessive trading. The MassMutual Excessive Trading Policy helps protect the interests of long-term

10

11

investors like you. If you would like to view the MassMutual Excessive Trading Policy, please visit , MassMutual’s participant Web site at www.retiresmart.com. In addition, you cannot transfer into any investment options if you have already made a purchase followed by a sale (redemption) involving the same investment within the last sixty days. You may not request a transfer into certain international options between 2:30 and 4 p.m. ET of each business day.

This transition notice describes changes that we are making to the plan’s investment options. As a result, these changes will alter how your account is invested after the effective date of the change. The new investment options that were selected to replace the existing investment options have characteristics, including level of risk and rate of return, that are reasonably similar to the characteristics of the existing investment options. You either have, or in the near

future will, receive profiles for all of the investment options that will provide you with comparable information for the existing and new investment options. With this information, you will be able to decide whether you want to have the existing investments in your account automatically transferred to the new investment options. If you do not want to invest in the comparable new investment options, then the Transition Notice explains how you can make changes to the investment of your account prior to the transition. If you have previously exercised control over the investment of your account and you do not provide affirmative investment instructions contrary to the change prior to the effective date of the change, you will be treated as having affirmatively elected to invest your account in the new investment options.

RetireSmartSM is a registered service mark of MassMutual.

RS7221 116 C: 38618-00

© 2016 Massachusetts Mutual Life Insurance Company, Springfield, MA 01111-0001. All rights reserved. www.massmutual.com. MassMutual Financial Group is a marketing name for Massachusetts Mutual Life Insurance Company (MassMutual) [of which Retirement Services is a division] and its affiliated companies and sales representatives.

MassMutual Retirement Services (MMRS) is a division of Massachusetts Mutual Life Insurance Company (MassMutual) and affiliates.

RS-38515-00 Rev. 1.16

GPROCESS INTERCNVR

Iowa Retirement Investors Club (RIC) 403(b) Plan 403(b) INTERNAL TRANSFER FORM

Use this form to: Process an internal transfer of your account from the existing MassMutual Program (Group Number 750923) to the enhanced MassMutual Program (Group Number 62069-3) Do not use this form to: Transfer/Exchange to another provider within your plan. Use the 403(b) Contract Exchange or Transfer (Money) Out Form. The 403(b) Internal Transfer Form can be submitted to MassMutual with one of the following options: 1. Fax to: 877-526-2531 or 800-678-8645 or 2. Mail to: MassMutual Retirement Services, PO Box 1583, Hartford, CT 06144-1583 For Overnight Mail: MassMutual Retirement Services, 1 Griffin Rd N, Windsor, CT 06095-1512 Questions: Call MassMutual’s Customer Service Center 1-800-528-9009 for inquires on Group Number 750923 Group Number: 750923 Plan Name: Iowa Retirement Investors Club (RIC) 403(b) Plan Participant's Name: _______________________________ _________ ________________________________ first middle last Participant's Address: ___________________________________________________________________________ street ___________________________________________________________________________ city state zip Social Security No.:_______________________

TRANSFER INSTRUCTIONS

I hereby request a transfer of the amount indicated below from my Group Number 750923 account to my Group Number 62069-3 account with MassMutual Life Insurance Company. Important Note: Assets transferred to Group Number 62069-3 will be applied to your current investment allocations on that account. Please go online at www.massmutual.com/retiresmart or call MassMutual’s Customer Service Center at 1-800-743-5274 to verify your investment allocations or to make changes, if needed, for Group Number 62069-3 only. Amount of Transfer: Check one: Full Account Balance or Partial Account Balance: Amount to Transfer: $________________ Your partial withdrawal will be processed pro-rata across all of your contribution sources (including Roth sources, if any) and investments unless Special Instructions and Roth Instructions are provided below. Special Instructions for partial transfers out of Group Number 750923 only: ___________________________________________________________________________________________________________________ ___________________________________________________________________________________________________________________

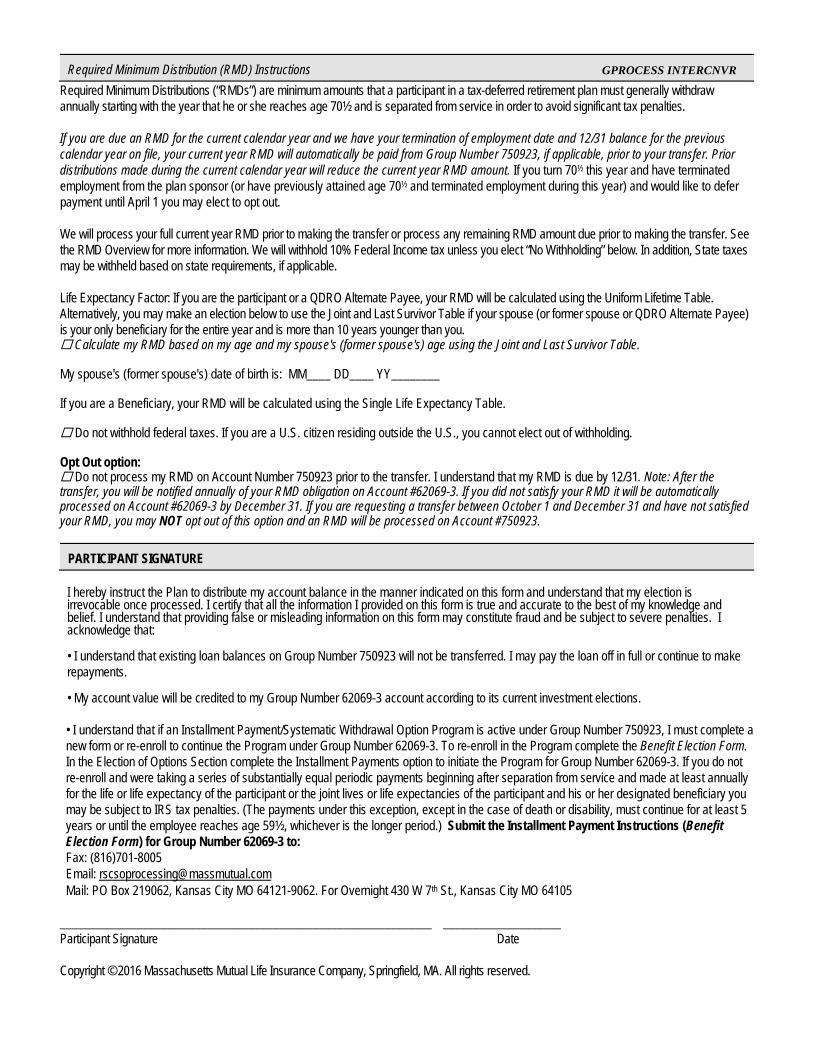

Required Minimum Distribution (RMD) Instructions GPROCESS INTERCNVR

Required Minimum Distributions (“RMDs”) are minimum amounts that a participant in a tax-deferred retirement plan must generally withdraw annually starting with the year that he or she reaches age 70½ and is separated from service in order to avoid significant tax penalties. If you are due an RMD for the current calendar year and we have your termination of employment date and 12/31 balance for the previous calendar year on file, your current year RMD will automatically be paid from Group Number 750923, if applicable, prior to your transfer. Prior distributions made during the current calendar year will reduce the current year RMD amount. If you turn 70½ this year and have terminated employment from the plan sponsor (or have previously attained age 70½ and terminated employment during this year) and would like to defer payment until April 1 you may elect to opt out. We will process your full current year RMD prior to making the transfer or process any remaining RMD amount due prior to making the transfer. See the RMD Overview for more information. We will withhold 10% Federal Income tax unless you elect “No Withholding” below. In addition, State taxes may be withheld based on state requirements, if applicable. Life Expectancy Factor: If you are the participant or a QDRO Alternate Payee, your RMD will be calculated using the Uniform Lifetime Table. Alternatively, you may make an election below to use the Joint and Last Survivor Table if your spouse (or former spouse or QDRO Alternate Payee) is your only beneficiary for the entire year and is more than 10 years younger than you. Calculate my RMD based on my age and my spouse's (former spouse's) age using the Joint and Last Survivor Table. My spouse's (former spouse's) date of birth is: MM____ DD____ YY________ If you are a Beneficiary, your RMD will be calculated using the Single Life Expectancy Table. Do not withhold federal taxes. If you are a U.S. citizen residing outside the U.S., you cannot elect out of withholding. Opt Out option: Do not process my RMD on Account Number 750923 prior to the transfer. I understand that my RMD is due by 12/31. Note: After the transfer, you will be notified annually of your RMD obligation on Account #62069-3. If you did not satisfy your RMD it will be automatically processed on Account #62069-3 by December 31. If you are requesting a transfer between October 1 and December 31 and have not satisfied your RMD, you may NOT opt out of this option and an RMD will be processed on Account #750923.

PARTICIPANT SIGNATURE

I hereby instruct the Plan to distribute my account balance in the manner indicated on this form and understand that my election is irrevocable once processed. I certify that all the information I provided on this form is true and accurate to the best of my knowledge and belief. I understand that providing false or misleading information on this form may constitute fraud and be subject to severe penalties. I acknowledge that:

• I understand that existing loan balances on Group Number 750923 will not be transferred. I may pay the loan off in full or continue to make repayments.

• My account value will be credited to my Group Number 62069-3 account according to its current investment elections. • I understand that if an Installment Payment/Systematic Withdrawal Option Program is active under Group Number 750923, I must complete a new form or re-enroll to continue the Program under Group Number 62069-3. To re-enroll in the Program complete the Benefit Election Form. In the Election of Options Section complete the Installment Payments option to initiate the Program for Group Number 62069-3. If you do not re-enroll and were taking a series of substantially equal periodic payments beginning after separation from service and made at least annually for the life or life expectancy of the participant or the joint lives or life expectancies of the participant and his or her designated beneficiary you may be subject to IRS tax penalties. (The payments under this exception, except in the case of death or disability, must continue for at least 5 years or until the employee reaches age 59½, whichever is the longer period.) Submit the Installment Payment Instructions (Benefit Election Form) for Group Number 62069-3 to: Fax: (816)701-8005 Email: [email protected] Mail: PO Box 219062, Kansas City MO 64121-9062. For Overnight 430 W 7th St., Kansas City MO 64105

_______________________________________________________________ ____________________ Participant Signature Date Copyright © 2016 Massachusetts Mutual Life Insurance Company, Springfield, MA. All rights reserved.

f6806 MassMutual Retirement Services, PO Box 219062, Kansas City MO 64121-9062 COMPLETE ALLPAGES For Overnight Mail: MassMutual Retirement Services, 430 W 7th St, Kansas City MO 64105

MassMutual Retirement Services (MMRS) is a division of Massachusetts Mutual Life Insurance Company (MassMutual) and affiliates.

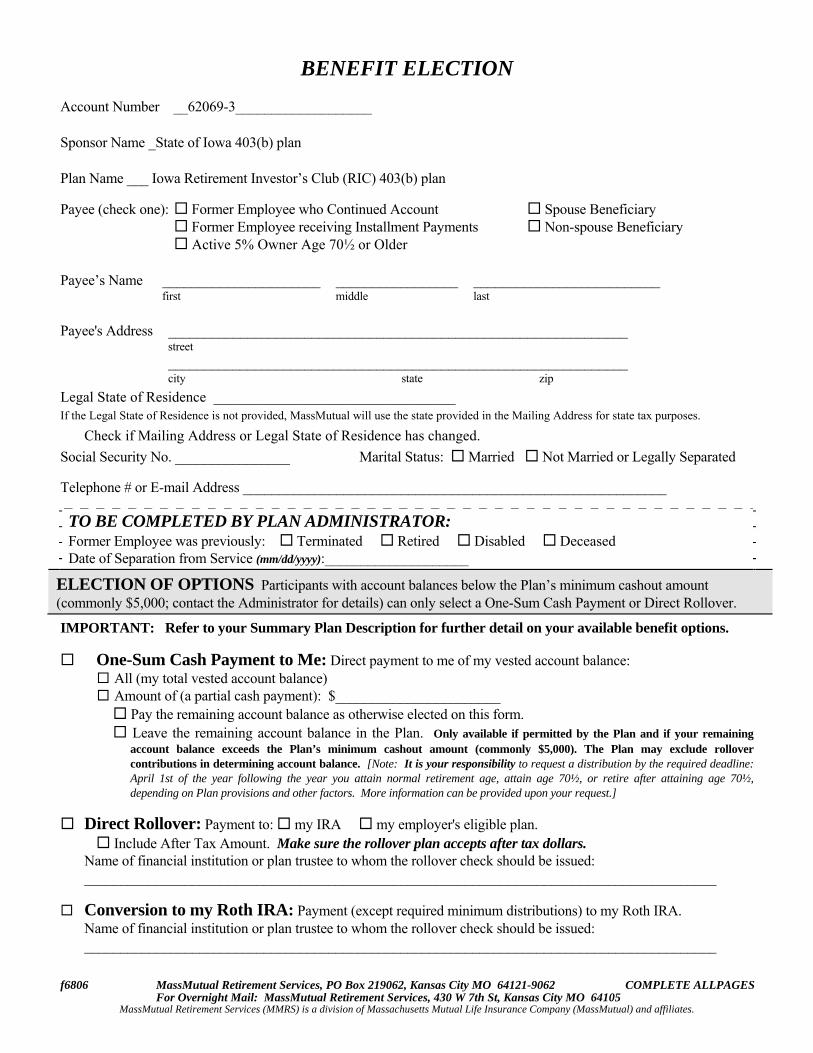

BENEFIT ELECTION Account Number __62069-3___________________ Sponsor Name _State of Iowa 403(b) plan Plan Name ___ Iowa Retirement Investor’s Club (RIC) 403(b) plan

Payee (check one): Former Employee who Continued Account Spouse Beneficiary Former Employee receiving Installment Payments Non-spouse Beneficiary Active 5% Owner Age 70½ or Older Payee’s Name ______________________ _________________ __________________________ first middle last Payee's Address ________________________________________________________________ street ________________________________________________________________ city state zip Legal State of Residence _________________________________ If the Legal State of Residence is not provided, MassMutual will use the state provided in the Mailing Address for state tax purposes.

Check if Mailing Address or Legal State of Residence has changed.

Social Security No. ________________ Marital Status: Married Not Married or Legally Separated

Telephone # or E-mail Address ___________________________________________________________

TO BE COMPLETED BY PLAN ADMINISTRATOR: Former Employee was previously: Terminated Retired Disabled Deceased Date of Separation from Service (mm/dd/yyyy):____________________

ELECTION OF OPTIONS Participants with account balances below the Plan’s minimum cashout amount (commonly $5,000; contact the Administrator for details) can only select a One-Sum Cash Payment or Direct Rollover.

IMPORTANT: Refer to your Summary Plan Description for further detail on your available benefit options.

One-Sum Cash Payment to Me: Direct payment to me of my vested account balance: All (my total vested account balance) Amount of (a partial cash payment): $_______________________ Pay the remaining account balance as otherwise elected on this form. Leave the remaining account balance in the Plan. Only available if permitted by the Plan and if your remaining

account balance exceeds the Plan’s minimum cashout amount (commonly $5,000). The Plan may exclude rollover contributions in determining account balance. [Note: It is your responsibility to request a distribution by the required deadline: April 1st of the year following the year you attain normal retirement age, attain age 70½, or retire after attaining age 70½, depending on Plan provisions and other factors. More information can be provided upon your request.]

Direct Rollover: Payment to: my IRA my employer's eligible plan. Include After Tax Amount. Make sure the rollover plan accepts after tax dollars. Name of financial institution or plan trustee to whom the rollover check should be issued: ________________________________________________________________________________________

Conversion to my Roth IRA: Payment (except required minimum distributions) to my Roth IRA. Name of financial institution or plan trustee to whom the rollover check should be issued:

________________________________________________________________________________________

f6806 MassMutual Retirement Services, PO Box 219062, Kansas City MO 64121-9062 COMPLETE ALLPAGES For Overnight Mail: MassMutual Retirement Services, 430 W 7th St, Kansas City MO 64105

MassMutual Retirement Services (MMRS) is a division of Massachusetts Mutual Life Insurance Company (MassMutual) and affiliates.

Installment Payments (if permitted by the Plan): Periodic payments from my account to start the first day of ______________ _____ month year

Payments are to be made: Monthly Quarterly Semi-Annually Annually. For a Fixed Period of _______ years (not to exceed life expectancy) For a Fixed Amount: Each payment should be a gross amount of: $____________. I understand that any

income tax withholding will be deducted from this amount. [Note: These payment amounts may need to be adjusted at age 70½ to meet IRS minimum distribution rules.] For the maximum period allowed by law: [Note: Changes to life expectancy and calculation method may be limited or not allowable based on the Plan document.] Life Expectancy: my life only my and my beneficiary's lives (beneficiary’s birth date ___________) Calculation Method: term certain (at time of first payment) recalculation (annually) mm/dd/yyyy

Joint and Survivor Annuity (if permitted by the Plan): A survivor annuity purchased from Massachusetts Mutual Life Insurance Company. After my death, 100% 75% 66⅔% 50% of the annuity payments should continue to my Joint Annuitant. The annuity election cannot be revoked.

Joint Annuitant's Name ___________________________________ Birth Date _________________________ Relationship ____________________________________________ Social Security No.__________________

Annuity (if permitted by the Plan): An annuity contract purchased from Massachusetts Mutual Life Insurance Company. The beneficiaries I previously designated continue under the Stipulated or Full Cash Refund Annuities. The annuity election cannot be revoked once payments commence.

Primary Beneficiary's Social Security No.______________ (Attach separate sheet with numbers if more than one beneficiary.)

Life Annuity Life Annuity with 120 Stipulated Payments Full Cash Refund Annuity Payments commencing: immediately at earliest retirement age (deferred)

LOAN DATA (if loans are permitted by the Plan)

Are there outstanding loans from the account? Yes No If "yes," I elect to: (if no item is elected below, the loan will be treated as a distribution): Enclose a Company check, certified check or money order issued to with this form paying off my

full loan balance (only available if still within the Plan’s cure period for loan repayments). Default on the outstanding loan balance and treat it as a distribution. If I elect installment payments of less than 10

years or a one-sum cash payment, federal income tax may be withheld on the defaulted loan amount.

INCOME TAX WITHHOLDING

FEDERAL WITHHOLDING: Distributions of pre-tax contributions plus interest on all contributions are subject to federal income tax. Federal income tax law requires that 20% of the taxable amount of a distribution be withheld, unless the payment is directly rolled over to an eligible employer plan or an IRA. Installment and annuity payments payable over life expectancy or 10 years or more are not eligible to be rolled over, and you have the choice to have federal income tax withheld (if no election is made, MassMutual will withhold federal income tax). Please read the Special Tax Notice(s). Contact your tax advisor or the IRS if you have any questions concerning tax withholding. One-Sum Cash Payment or Direct Rollover or Installments of Less than 10 Years: I read the Special Tax Notice(s) and: Withholding does not apply as this is a direct rollover of the entire taxable portion of my payment. Deduct the 20% mandatory federal income tax withholding from the taxable portion of my payment. Deduct the 20% mandatory federal income tax withholding from the taxable portion of my payment and an

additional amount of $_____________. Installments/Annuities of 10 Years or More or Based on Life Expectancy: I elect to have federal income tax: not withheld withheld.

If "withheld" is elected for installment or annuity payments, complete below (refer to IRS instructions for Form W-4P for more information):

a. Deduct ____% federal income tax withholding from the taxable portion of each payment. b. I want 10% federal income tax withholding from the taxable portion of each payment and the following

additional amount withheld from each payment: $____________.

f6806 MassMutual Retirement Services, PO Box 219062, Kansas City MO 64121-9062 COMPLETE ALLPAGES For Overnight Mail: MassMutual Retirement Services, 430 W 7th St, Kansas City MO 64105

MassMutual Retirement Services (MMRS) is a division of Massachusetts Mutual Life Insurance Company (MassMutual) and affiliates.

STATE WITHHOLDING: Contact your tax advisor or your state’s tax department if you have any questions concerning state tax withholding. Refer to the State Tax Information document for important information regarding State Withholding in your Legal State of Residence. If you make an election that is not in compliance with your state’s regulations, MassMutual will default to your state’s requirements.

No State Tax Withholding Election I have read the State Tax Information document and I elect to have no state income tax withheld from my

payment(s).

Voluntary State Income Tax Withholding I have read the State Tax Information document and I elect to have the following voluntary state income tax withheld

from my payment(s) (choose one): ____% $________ (whole dollar amount) ___ based on my state's tax table formula, if applicable (MassMutual will apply the default tax allowance)

Additional State Income Tax Withholding I have read the State Tax Information document and I elect to have an additional ____% or $________ (whole dollar

amount) state income tax withheld from my payment(s).

METHOD OF PAYMENT

Direct deposit to a bank account of which I am an account holder - Deposited within 3 business days from date of processing.

This option is NOT available for Rollovers.

To elect Direct Deposit, you must select either Checking or Savings and you must provide a voided check or copy of a pre-printed, account-specific deposit slip or a bank specification sheet from your bank for validation.

Checking Savings

___________________________________ __________________________________________ _______________________________________ Bank Name Bank ABA/Routing (9 digits) Bank Account No.

Please note that we can only send funds via direct deposit to banks with a valid U.S. routing number.

I understand that if I do not fully complete this section or the bank account information I have provided is invalid, a check will be mailed. I understand that a reprocessing fee may be charged to my account if the direct deposit is declined by my financial institution. Subsequent withdrawals will be processed in the same manner (up to 180 days from the date of the original distribution) unless I notify MassMutual in writing to distribute the money differently. I also authorize MassMutual to initiate a debit to my account for any overpayment or payments made in error.

Send payment by check - Allow up to 10 business days for postal service delivery.

SIGNATURES

I understand that I have a right to a 30-day election period. I further acknowledge that I am waiving the 30-day election period by making an affirmative election on this distribution form. I understand there may be a charge for each distribution processed or a one-time installment or annuity set-up fee deducted from my account balance and, if all required items are not completed on this form, payment will be delayed. If electing direct deposit, by signing below I certify that I am an account holder on the bank account listed above. _______________________________________________ _______/_______/_______ Payee Date _______________________________________________ _______/_______/_______ Plan Administrator Date Copyright ©2011 Massachusetts Mutual Life Insurance Company, Springfield, MA. All rights reserved.

Required Minimum Distributions Overview What are Required Minimum Distributions? Required Minimum Distributions (“RMDs”) are minimum amounts that a participant in a tax-deferred retirement plan account must generally withdraw annually starting with the year that he/she reaches 70½ in order to avoid significant tax penalties. Beneficiary RMDs must generally begin in the year after the participant dies. Alternate payee (under a QDRO) RMDs must begin when the associated participant's RMDs are required to begin. The date on which the plan participant, beneficiary or alternate payee must begin receiving RMDs from his or her account is generally referred to as the “Required Beginning Date” or “RBD”. When must I begin to receive a RMD? Participants, beneficiaries and alternate payees (under a QDRO) must start receiving RMDs by the date indicated in the chart below. Note: The terminated/ retired/active statuses mentioned in the chart refers to participant employment status with the employer that sponsors the Plan. What is a Required Beginning Date? Generally, the RBD is April 1st following the year the participant attains age 70½ or retires (e.g., terminates employment), whichever is later. For a participant who is a 5% Owner (see definition below)*, there is generally no ability to defer the RBD until after retirement; accordingly, for 5% Owners, the RBD is April 1st following the year the participant turns age 70½, whether or not he/she is retired. The participant's RBD also determines when a beneficiary or alternate payee (under a QDRO) must begin taking RMDs.

Types of Applicant Participants: • I turned 70½ this calendar year and, • I am retired or have terminated employment and, • This is my first RMD • I am 70½ or older and, • I retired or have terminated employment in a prior year and, • This is not my first RMD

• I am a 5% owner and • I am 70½ or older in the current calendar year and • I am not retired Beneficiaries: • I am a spouse or non-spouse beneficiary of a participant who died after his/her RBD • I am a spouse beneficiary of a participant who died before his/her RBD • I am a non-spouse beneficiary of a participant who died before his/her RBD • I am a non-person beneficiary (e.g., charity, estate) of a participant who died before his/her RMD. QDRO Alternate Payees: • I am a QDRO Alternate Payee

RMD Due Dates

• Your 1st RMD is due by 12/31 this calendar year, but you may elect to defer its payment until 4/1 next calendar year (your RBD). • Note: If you defer your 1st RMD until 4/1 next year, you still will be required to take your 2nd RMD by 12/31 next year resulting in two required payments in one tax year. • You are required to receive your RMD by 12/31. • Your 1st RMD is due by 12/31 but you may elect to defer its payment until 4/1 next calendar year (your RBD). • If this is not your 1st RMD, the RMD is due by 12/31. • Note: If you defer your 1st RMD until 4/1 next calendar year, you still will be required to take your 2nd RMD by 12/31 next year resulting in two required payments in one tax year. • You are required to receive an RMD by 12/31 of the calendar year following the participant's death. Note: If the participant did not receive his/her yearly RMD before death, the participant's RMD must be paid to his/her designated beneficiary(ies) in the year of death. • Yearly RMDs (Life expectancy Rule Option) - You may elect to receive RMDs starting 12/31 of the calendar year following the participant's death based on your life expectancy. If you are the participant's only primary beneficiary you may elect to defer RMDs until 12/31 of the year the participant would have attained age 70½. • Single Sum Payment (5-Year Rule Option) - You may elect to receive the participant's entire account balance by 12/31 of the 5th anniversary of the participant's death. You may request a lump sum payment in the 5th year or partial/installment payments for up to 5 years. • Yearly RMDs (Life expectancy Rule Option) - You may elect to receive RMDs starting 12/31 of the calendar year following the participant's death based on your life expectancy. • Single Sum Payment (5-Year Rule Option) - You may elect to receive the participant's entire account balance by 12/31 of the 5th anniversary of the participant's death. You may request this as a lump sum payment in the 5th year or partial/installment payments for up to 5 years. • The participant's entire account balance must be paid by 12/31 of the 5th anniversary of the participant's death under the 5-Year Rule. You may request a lump sum payment in the 5th year or partial/installment payments for up to 5 years. • Generally, your RMD is due when the participant's RMD is due (even if you are not age 70½).

*A 5% Owner, as defined in Internal Revenue Code Section 416, is an individual who owns more than 5% of company stock or business interest; or a spouse, child, grandparent or parent of a 5% Owner. Ownership for RMD purposes is determined as of the plan year ending in the calendar year the participant attains age 70 ½. Once a participant is considered a 5% Owner, he/she is generally always considered a 5% Owner for RMD purposes, even though he/she may no longer be considered a 5% Owner for other plan purposes (e.g., non-discrimination testing.)

RS-35031-01 Rev. 12.14 Page 1 of 3

The information contained in this overview is not intended or written as specific legal or tax advice and may not be relied on for purposes of avoiding any federal tax penalties. Neither MassMutual nor any of its employees or representatives is authorized to give legal or tax advice. You must rely on the advice of your own independent tax counsel.

Can the Plan's distribution provisions be different than the RMD rules under the Internal Revenue Code (IRC)? Yes. It is possible that the Plan document may require that participant, beneficiary and/or alternate payee (under a QDRO) distributions begin earlier than as required by law. The Plan may also restrict and/or prescribe the form(s) of payment you can elect (i.e., lump sum, partial payment, installments, annuity). Please refer to the Plan Document or the plan administrator to see what rules apply to you. Note: The chart above reflects the general RMD rules under the IRC. When must I take annual RMDs? After you receive your first RMD, annual RMDs must be paid by 12/31 of each year. This is also true for beneficiaries who elect the Life Expectancy Rule. For beneficiaries who elect the 5-Year Rule, the participant's entire account balance must be paid by 12/31 of the 5th calendar year following the participant's date of death. What happens if I do not meet the RMD rules? Failure to meet the RMD requirements may result in a 50% Federal excise tax payable to the IRS by you. This tax is based on the RMD amount due for the tax year but which was not paid to you. To report and pay the federal excise tax due, you will need to file an IRS Form 5329. File this form with your IRS tax return. In some cases you may be eligible to apply for a waiver of these excise tax penalties. You should refer any questions concerning your individual tax situation to your accountant or other tax professional. MassMutual does not provide legal or tax advice. How is the RMD calculated? Your RMD amount is determined by applying a distribution period set by the IRS to your account balance at the end of the previous year. If you are a participant, to calculate your RMD: • Find your age on the IRS Uniform Life Table* as of the close of the current year. • Locate the corresponding distribution period. • Divide your account balance as of 12/31 of the prior year by your distribution period. *See IRS Publication 590. Do different RMD calculation rules apply to beneficiaries? Yes. Beneficiary RMDs are determined using the Single Life Expectancy table. Special rules may apply depending on whether you are a spouse, non-spouse or a non-person beneficiary. Please refer to the Plan document or IRS Publication 590. Generally, if the participant died before his/her RBD, and you are a surviving spouse, look up your age on the Single Life Expectancy table and divide your account balance as of 12/31 of the prior year by the distribution period from the table each year and RMD is due. If you are a nonspouse, for the first year your RMD is due look up your age on the Single Life Expectancy table and divide your account balance as of 12/31 of the prior year by the distribution period from the table. For each subsequent year's distribution period, subtract one ("1") for the original distribution period. If the participant dies on or after his/her RBD, the RMD distribution period is the greater of the beneficiary's life expectancy or participant's remaining life expectancy had he or she lived. Do different RMD calculation rules apply to alternate payees (under a QDRO)? Yes. If you are a former spouse you will generally be treated as a surviving spouse for purposes of applying the RMD rules. Your account is not aggregated with the participant's account to determine the RMD. Thus, RMDs will be paid to both you (determined using your account balance) and the participant (determined by using the participant's account balance). The same participant RMD calculation method applies as described above. If you are 10 years younger or fewer than the participant, the distribution period is based on the Uniform Lifetime Table, which is based on the participant's age. If you are more than 10 years younger than the participant, the distribution period on the Joint and Last Survivor expectancy Table is based on your age and the participant's age. Please refer to the Plan document or IRS Publication 590. How will a withdrawal during the year affect my RMD? Any amounts withdrawn from your Plan during the year will be applied to your RMD payment. For instance, if your current year RMD is $5,000 and you take $2,000 in withdrawals during the year you will be required to take an additional $3,000 before that calendar year's RMD due date. Note: Any corrective distributions (e.g., excess deferrals) or loan defaults that result in taxable distributions which you may have received during the calendar year do not count towards that calendar year's RMD

Rev. 12.14 Page 2 of 3

The information contained in this overview is not intended or written as specific legal or tax advice and may not be relied on for purposes of avoiding any federal tax penalties. Neither MassMutual nor any of its employees or representatives is authorized to give legal or tax advice. You must rely on the advice of your own independent tax counsel.

The information contained in this overview is not intended or written as specific legal or tax advice and may not be relied on for purposes of avoiding any federal tax penalties. Neither MassMutual nor any of its employees or representatives is authorized to give legal or tax advice. You must rely on the advice of your own independent tax counsel.

Rev. 12.14 Page 3 of 3

What if I have multiple accounts? • Aggregation of Plan Types - You cannot satisfy this Plan's RMD by combining it with an account you may have in the same type of plan (e.g., another 401(k) plan with another employer) or a different type of plan(e.g., 401(a), 401(k), 403(b), 457(b) or IRA) for which you are the account holder. However, if you have more than one 403(b) contract with the same employer, you may combine the contracts and have the total RMD owed on all the contracts paid to you from one or more of the 403(b) contracts. IRAs may also be combined for RMD purposes.

• Aggregation of Multiple Provider Investments - Some plans of the same employer (e.g., 403(b), 457(b)) may permit you to invest your plan account with more than one provider. In that case, you may have the RMD paid to you from one or more accounts that are connected to the same type of plan with the same employer.

What are my tax considerations? • Federal 10% income tax withholding will be applied to the taxable portion of your periodic RMD payments (unless you elect out of withholding or a different withholding amount). If you are a U.S. citizen residing outside the U.S. you may not elect out of withholding. • State income taxes may also be required to be withheld. • Withholding is for pre-payment of federal (or state) income tax. You may be subject to additional federal and/or state taxes when you file your income tax return for the year. • Your RMD cannot be directly or indirectly rolled over. If an RMD is due for the year, the RMD must be paid first before. If an RMD is due for the year, the RMD must be paid first before any subsequent distribution made in the form of a direct rollover. • If your address is outside of the United States, a Citizenship Statement is required to be submitted with your RMD Election Form. If this form is not received, MassMutual will withhold 30% Federal income tax towards taxes from your payment. What form do I complete? Complete the Required Minimum Distribution Request (RMD Form). You may obtain a copy of the applicable RMD form from your plan administrator or by contacting us at the phone number listed on page 1 of the distribution form. How will MassMutual process my RMD? • We will process your RMD upon receipt of a completed RMD or Beneficiary Form that is in Good Order. • We will calculate your RMD using the information you submitted on the RMD or Beneficiary Forms. It is your responsibility to inform MassMutual if your marital status and/or withholding elections have changed since submitting the form by contacting us at the phone number listed on page 1 of the distribution form before your scheduled payment(s). It is also your responsibility to ensure that you receive the total RMD due from the Plan for the year. Next steps • Determine if you are due a RMD after reviewing this document. • Complete the RMD or Beneficiary Form. • Return the completed form as instructed on the distribution form. • Consult with the plan sponsor and/or your own legal and/or tax advisors, as appropriate for your specific circumstances. Your retirement planning decisions are based on your personal situation. You may want to consult with your investment or tax advisor. The information contained in this overview is not intended or written as specific legal or tax advice and may not be relied on for purposes of avoiding any federal tax penalties. Neither MassMutual nor any of its employees or representatives is authorized to give legal or tax advice. You must rely on the advice of your own independent tax counsel. For more information on RMDs you may want to consider referring to IRS Publication 590, Individual Retirement Arrangements (IRAs), which contains similar RMD rules as retirement plans as well as the distribution period tables used for RMD calculations and the IRS Retirement Topics page on their website entitled Required Minimum Distribution (RMDs). These materials can be found at IRS.gov. For more information about the Plan's distribution rules, refer to the Plan document, your plan's Summary Plan Description (SPD) or contact the plan administrator.