![no · PDF fileE. Kendrick Ma] 16-3 Round 4 Kendrick Gustilo E. Kendrick C. Lewis Kendrick Maj 16-4 ... Johnson South port puni Jayden Bowles Citrus Wrestlin Mason Wislon](https://static.fdocuments.in/doc/165x107/5a8ed0e57f8b9a4a268d68c8/no-kendrick-ma-16-3-round-4-kendrick-gustilo-e-kendrick-c-lewis-kendrick-maj.jpg)

Looking Ahead Beyond 2015: Making Growth Work For The Poor Rogier van den Brink, Lead Economist and...

37

Looking Ahead Beyond 2015: Making Growth Work For The Poor Rogier van den Brink, Lead Economist and Program Leader, and Karl Kendrick Chua, Senior Country Economist Macroeconomics and Fiscal Management Global Practice Presentation to the Philippine Economic Society, November 14, 2014

-

Upload

katrina-hardy -

Category

Documents

-

view

217 -

download

0

Transcript of Looking Ahead Beyond 2015: Making Growth Work For The Poor Rogier van den Brink, Lead Economist and...

Looking Ahead Beyond 2015:Making Growth Work For The Poor

Rogier van den Brink, Lead Economist and Program Leader, and

Karl Kendrick Chua, Senior Country EconomistMacroeconomics and Fiscal

Management Global Practice

Presentation to the Philippine Economic Society, November 14, 2014

Contents1. Global trends—pessimistic

2. Philippine trends—optimistic

3. Inclusive growth—challenge

4. Opportunity—stars aligned, wind in your sails

5. Poverty projections—look good

6. Jobs challenge—remains

7. The way forward….

3

Recent economic and policy developments Global Recovery: Weak and Slow

Disappointing year

Global growth forecasts: revised further down

Trade: slower long-term growth

Outlook is pessimistic:

Summers’ “Secular Stagnation”

Lagarde’s “New Mediocre”

Rodrik’s pessimism about the “old” growth strategies

Developing countries: transition to a new environment Post-crisis growth slowdown widespread

Structural challenges abound

Recent economic and policy developments

Global growth:

3.2% >> 2.6%

Growth in developing countries:

5.3% >> 4.5%

Growth in high income countries:

2.2% >> 1.8%Source: World Bank Global Economic Prospects

Global growth has been downgraded since January

5

Medium-term global growth projections

Sources: World Development Indicators; DECPG Projections

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

-4

-2

0

2

4

6

8

10World High income countries Developing countries

GDP growth (percent)

6

Slower trade growth….

2005 20

020

020

06 200

200

2007 20

020

020

08 200

200

2009 20

020

020

10 201

201

2011 20

120

120

12 201

201

2013 20

120

120

14 201

20180

100

120

140World trade Trend 05-08 Trend 11-14

Index, 2008Q1 = 100

7

Rodrik on service sector and growth strategies in developing countries….

8

3% by 2030 is far from assured: Business as usual will not get us there

ScenarioHeadcount (percent)

Number of poor (million)

Average income growth of 4% p.a. in each country 3 252

Each country sustains avg per capita growth during past 20 years 6.8 573

Each country sustains avg per capita growth during past 10 years 4.8 405.4

Each country sustains avg per capita growth during past 10 years (survey-based growth) 6.7 564.8

Global Poverty in 2030 at $1.25 per day (2005 PPP),

assuming unchanged inequality

Source: World Bank, 2014, A Measured Approach to Ending Poverty and Boosting Shared Prosperity

…and growth is slowing.

9

Projecting the Changing Faceof Poverty to 2030

Source: World Bank, 2014, A Measured Approach to Ending Poverty and Boosting Shared Prosperity

10

The Philippines has experienced higher growth in the last decade..

-10

-5

0

5

10 Real GDP per capita (2000 prices) growth

Per

cent

Sources: National Statistics Office (NSO), WDI, World Bank staff estimatesNote: Red line at 2.5 percent (long run average)

Post war reconstruction

Debt-drivengrowth

Governance-led growth

11

..along with strong macro fundamentals..

-9

-6

-3

0

3

6Current account balance

Per

cent

of G

DP

Sources: WDI, Department of Budget and Management (DBM)Notes: The red line is at -3 percent. Current account balance has a series break in 1977 and in 2005.

..low and stable inflation..

12

Low and stable inflation in the last decade has led to increased real income for businesses and households

0

5

10

15

20

Perc

ent

CPI inflation

Sources: Philippine Statistics Authority, Bangko Sentral ng PilipinasNotes: The red line is at 5 percent.

-6

-5

-4

-3

-2

-1

0

1

2

0

10

20

30

40

50

60

70

80

90

Perc

ent o

f GD

P

National government deficit and debt

DebtDeficit (rhs)

Perc

ent o

f GD

P

Source: WB staff estimates using NSCB, BTr, and DOF data

..improving fiscal position..

13

Lower debt levels and deficit mean more fiscal space for pro-poor spending. In fact, social spending doubled in the last 4 years.

..and a history of successful reforms that made a big difference.

0

100

200

300

400

500

600

700

800

900

Hun

dred

tho

usan

ds

BPO sector - total employment

Source: BPAP

0

10

20

30

40

50

60

70

80

90

100

Mill

ions

Number of mobile phone subscribers

Source: WDI

0

5

10

15

20

25

30

Mill

ions

Number of internet users

Source: WDI

0

5

10

15

20

25

Mill

ions

Air transport, passengers carried

Source: WDINote: Data include passengers of both domestic and

international flights.

15

GDP growth decelerated somewhat to 6.0 percent in H1 2014 due to weak government consumption and public construction.

Private consumption continued to drive growth. But growth was third highest in the region behind only China

and Malaysia.

-15

-10

-5

0

5

10

15

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2011 2012 2013 2014

Pe

rce

nta

ge p

oin

t

Demand side: contribution to GDP Growth

Private consumption Govt consumption Capital formation

Statistical Discrepancy Net Exports GDP growth

Source: PSA

Recent economic and policy developments

Inclusive growth challenge:Creating more and better jobs, reducing poverty and protecting the vulnerable

Growth may be necessary but is not sufficient to ensure poverty reduction…

How broadly based growth is—i.e., how pro-poor the distribution

of growth is—also matters…

Raising the returns to labor—the main asset of the poor

by…

…increasing value-added per worker in

agriculture

…moving workers out of agriculture to higher value-

added activities in manufacturing and service

…as does how resilient growth is and the extent to which poor and vulnerable households are protected

from shocks

Putting in place

appropriate social

protection schemes

…and raising human capital

endowments

China’s incidence of growth:inclusive growth in several periods

Philippines?• Long history of policy distortions has

slowed the growth of agriculture and manufacturing in the last six decades.

• Incomplete structural transformation• Agricultural productivity has

remained depressed, manufacturing has failed to grow sustainably, and a low-productivity, low-skill services sector has emerged as the dominant sector of the economy.

Structural transformation?

0

10

20

30

40

50

60 Sector share to GDP

Agriculture Industry ServiceSource: NSCB

Perc

ent

0

10

20

30

40

50

60

70

Per

cent

Employment share by sector (detailed)

Agriculture Manufacturing Other industries Formal services Informal services

Source: LFSSource: LFS

-10

-5

0

5

10

15

20

10 20 30 40 50 60 70 80 90 100

Ave

rage

ann

ual

grow

th in

per

capi

ta c

onsu

mpti

on (

%)

Percentiles of the distribution of per-capita household consumption

PHILIPPINES: per-capita household consumption GROWTH INCIDENCE CURVES

1994-1997

2006-2009

2003-2006

2000-2003

1997-2000

Philippine incidence of growth:less so…

• A regional environment favorable to the Philippines

• Sound macroeconomic fundamentals

• A government committed to reform

• Widespread confidence

• Highly skilled, talented, English-speaking, youthful population

• Abundant natural resources

• Opportunity to build on momentum of reforms already successfully

implemented, for instance:

• Better public financial management, which created fiscal space

• Doubling of budgets for social services since 2010

• Conditional cash transfer and CDD programs

• Major improvements in transparency (Open Government)

A window of opportunity

The East Asia and Pacific (EAP)region is a global growth driver

21

EAP accounts for over 25% of world nominal GDP, and its share will continue to rise At current real growth rates of 7% annually,

developing EAP countries will add a further $7 trillion by 2019 China 2nd largest economy, Indonesia 10th

Increasing trade and FDI with all regions

China will remain growth driver in the region and globally Rethinking its growth model with greater focus on

sustainability Market-oriented reforms

Regional integration is increasing ASEAN integration in 2015 presents opportunities

for furthering reforms Nearly 50% of FDI in ASEAN countries originates

within EAP

Challenges and Risks Need to move forward with structural reforms and

investments to raise factor productivity and address vulnerabilities

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

0

2

4

6

8

10

12

14 Real GDP Growth (%) %

Developing EAP

Developing EAP exc China

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

0%

5%

10%

15%

20%

25%

30%

35% EAP Share of Global GDPChinaDeveloping countries excluding ChinaNewly Industrialized Economies*High income**

Forecast***

* Includes Hong Kong SAR, China; Taiwan, China; Singapore; and Korea. ** Includes Japan, Australia, New Zealand, and Brunei Darussalam.*** Differs by country; 34% of countries have their estimates start after 2013.

East Asia and ASEAN Growth Projections

22

Forecast2012 2013 2014 2015 2016

East Asia 6.0 6.1 6.0 6.1 6.1

Developing East Asia 7.4 7.2 6.9 6.9 6.8

China 7.7 7.7 7.4 7.2 7.1

Indonesia 6.3 5.8 5.2 5.6 5.6

Malaysia 5.6 4.7 5.7 4.9 5.0

Philippines 6.8 7.2 6.4 6.7 6.5

Thailand 6.5 2.9 1.5 3.5 4.0

Vietnam 5.2 5.4 5.4 5.5 5.8

Cambodia 7.3 7.4 7.2 7.5 7.2

Lao PDR 8.0 8.5 7.5 6.4 7.0

Myanmar 7.3 8.3 8.5 8.5 8.2

ASEAN 5.7 5.0 4.5 5.0 5.3

Developing EAP excluding China 6.2 5.2 4.8 5.3 5.1

World 2.5 2.4 2.6 3.2 3.3

High-income countries 1.5 1.3 1.8 2.3 2.4

Developing countries 4.8 4.8 4.5 5.0 5.3Source: World Bank, "East Asia and Pacific Economic Update: Enhancing Competitiveness in an Uncertain World", October 2014

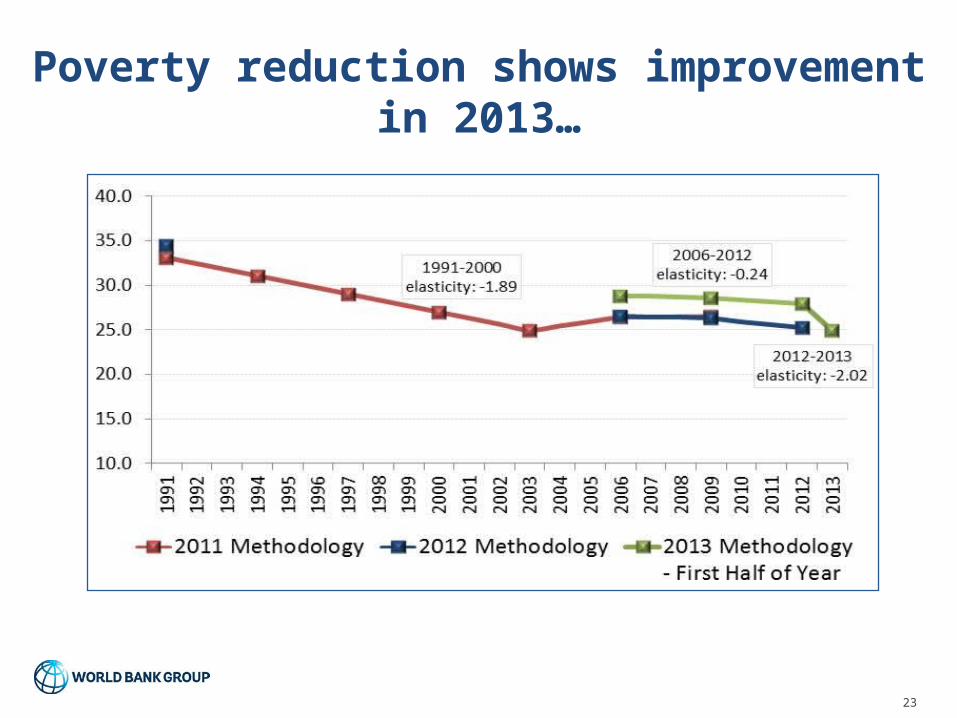

Poverty reduction shows improvement in 2013…

23

24

First half poverty incidence among the population fell by 3 ppt. to 24.9 percent, down from 27.9 percent in the same period in 2012.

This translates to around 2.5 million Filipinos uplifted from poverty. Job creation:

In 2013, still weak job creation. In 2014, better.

Jan Apr Jan Apr Jan AprUnemployment 7.2 6.9 7.1 7.6 7.5 7.0Underemployment 18.8 19.3 20.7 19.2 19.5 18.2Job creation (thousands) 1,005 1,001 519 -37 283 1,654

By industry:

Agriculture 132 323 -540 -621 121 323Industry 210 219 318 228 117 345Services 664 458 741 393 45 910

By sector:

Public sector 115 21 24 45 -35 -11Private sector 891 980 495 -82 318 1,665

By class of worker:

Wage and Salary 435 838 1,820 593 -994 914Self-employed 349 -15 -613 -225 705 445Unpaid workers 220 178 -688 -404 536 296

Source: LFS

2012 2013 2014

Note: January estimates exclude Region 8, whi le Apri l estimatesexclude the provnce of Leyte, due to the effects of typhoon Yolanda.

20

22

24

26

28

30

32

0

4

8

12

16

20

24

28

Pove

rty

inci

denc

e (p

erce

nt o

f pop

ulati

on)

Mag

nitu

de o

f poo

r (in

mill

ions

)

Poverty incidence and magnitude(first semester estimates)

Magnitude (in millions) Incidence (lhs)

Source: PSA, United Nations World Population Prospects

In 2013, poverty incidence declined significantly

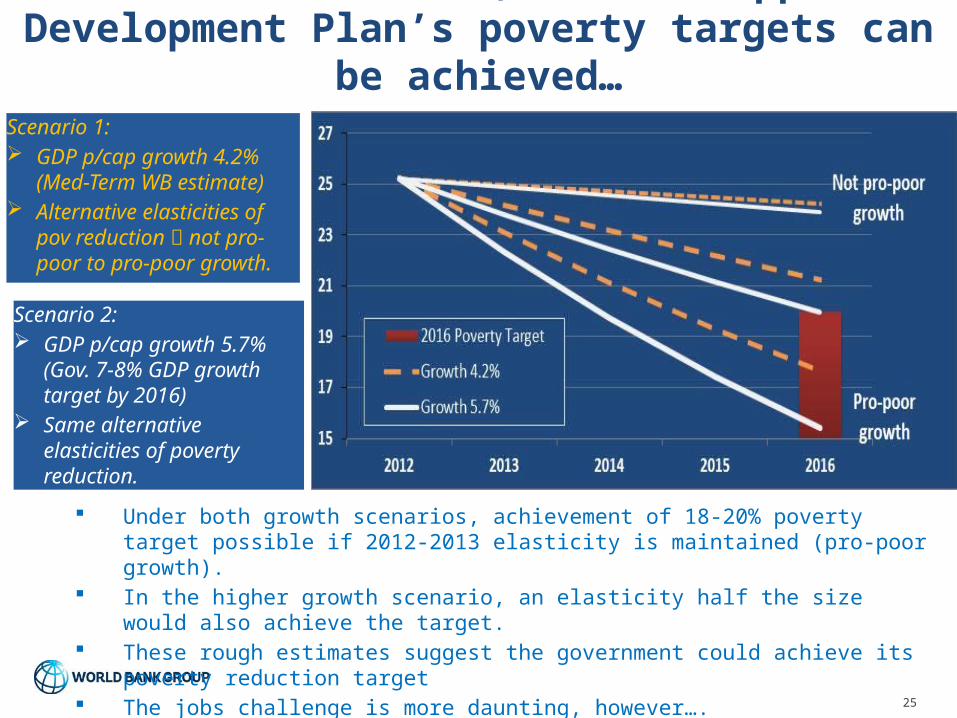

At current trends, the Philippine Development Plan’s poverty targets can be achieved…

25

Under both growth scenarios, achievement of 18-20% poverty target possible if 2012-2013 elasticity is maintained (pro-poor growth).

In the higher growth scenario, an elasticity half the size would also achieve the target. These rough estimates suggest the government could achieve its poverty reduction

target The jobs challenge is more daunting, however….

Scenario 1: GDP p/cap growth 4.2%

(Med-Term WB estimate) Alternative elasticities of

pov reduction not pro-poor to pro-poor growth.

Scenario 2: GDP p/cap growth 5.7%

(Gov. 7-8% GDP growth target by 2016)

Same alternative elasticities of poverty reduction.

More challenging: providing more and better jobs to the 15 million Filipino’s who are either

unemployed or underemployed

26

Jobs challenge Three million unemployed Seven million underemployed New entrants to the labor force number 1.15

million/year Informality accounts for 75 percent of

employment

Medium-term reform agenda:

27

Thematic reform areas

Enhancing competition

Simplifying business regulations

Securing property rights

Increasing investment in physical and human capital

0

1

2

3

4

5

6

Perc

ent o

f GDP

Education

0

1

2

3

Perc

ent o

f GDP

Health

0

1

2

3

4

5

Perc

ent o

f GDP

Infrastructure

Public Expenditure

Source: WDI and ADB estimatesNotes: Education and health figures are from 1995 to 2012 (Some countries have missing values for certain years.). Infrastructure data is from 2008 to 2012.

Investing on infrastructure, education and health

can help sustain inclusive growth

28

However, the Philippines has an investment deficit Spending on infrastructure, health and education has been lower than in

some neighboring countries. Low spending has contributed to weak health outcomes and lower quality

of education, and tremendous traffic. But recent trends are in the right direction…

Financing this trend needs more revenues…so reduce the tax gap

29

0.31.8

3.01.8

6.9

0.8

0.3

1.4

1.4

4.0

0

2

4

6

8

10

12

SEP CE CIT VAT Total

Actual Gap

(0.5)

-

0.5

1.0

1.5

2.0

2.5

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Using NSO imports Using BOC imports

BIR tax gap (in percent of GDP)(Actual collection plus collection gap)

BOC tax gap (in percent of GDP)

…and more reforms in areas such as real property tax.

30

21

23

25

48

27

0 10 20 30 40 50

1991-1995

1996-2000

2001-2005

2006-2010

2011-2012

Number of cities

Base Year of Property Valuation of Cities

Source: Official Page for the Joint Memorandum Circulars (JMCs) on Revision of SMVs and Property Assessments (2010-01) and Idle Land Taxation (2010-02).

1

3

6

14

36

20

0 10 20 30 40

1985

1991-1995

1996-2000

2001-2005

2006-2010

2011-2012

Number of provinces

Base Year of Property Valuation of Provinces

Source: Official Page for the Joint Memorandum Circulars (JMCs) on Revision of SMVs and Property Assessments (2010-01) and Idle Land Taxation (2010-02).

As of June 2014, around 80% of cities and 75% of provinces use outdated schedule of market values (SMVs) for collecting real property tax.

A proposed tax reform package to finance investments

31

Raising tax revenues efficiently and equitablyFirst phase: raising tax revenues

Rationalize tax incentives to reduce redundancy;Enact a tax expenditure ceiling

Reduce the number of VAT exemptions; use the NHTS-PR to protect vulnerable Filipinos

Centralize the valuation of real properties and, if needed, levy a national surtax to enhance equity

Index petroleum excise taxes once prices have fallen or automatic increase in excise tax once fuel price falls to enhance equity

Second phase: lowering tax rates and further broadening the base

Reduce the corporate income tax rate while increasing the gross income earned to enhance equity

Reduce the highest marginal tax rate for personal income tax and reduce the number of brackets

Consolidate all laws and regulations on tax incentives into one code

Simplify the tax regime for micro and small firms into a single tax on turnover to reduce compliance cost

Broad reform coalitions are necessary. Without a broad coalitions, reforms made under a strong president can be reversed, as the country’s history has shown.

Stakeholders need to focus on a package of reforms to support inclusive growth. Given the political economy, individual reforms will face strong opposition.

Example: sin tax reform

These coalitions can form at many levels and around many themes

Country needs to come together and seize this unique window of opportunity

…not to be missed!

“Working together” is not just a nice slogan…

Example: shipping industry

33

Philippines EAPWeak competition Share of primary routes served by a single operator (%) 40 NAHigh shipping costs Share of logistics costs to wholesale price (%) 24-53 20High shipping costs Share of shipping and port handling costs to wholesale price (%) 8.4 NAHigh shipping costs Share of shipping and port handling costs to retail price (%) 4.9 NASmall domestic trading volumes Domestic market throughput (millions of metric tons) 74 782Low quality of services Rank in liner shipping connectivity (out of 157) 66 17Poor port infrastructure Rank in quality of port index (out of 148) 116 47Low profitablity Average return on equity (%) 1 NAOld vessel age Average age of ships (years) 30 22Poor safety standards Average number of yearly accidents 228 32Poor safety standards Average number of yearly casualties 303 60Sources: World Bank (2013), World Economic Forum (2013), JBIC (2002), Securities and Exchange Commission, MARINA, National Statistical Coordination Board, World Development Indicators, and Board of Maritime Inquiry, UNCTAD (2011), Various country statistical officesNote: Average age of ships used was global average in the absence of dataSelect East Asia and the Pacific countries are Singapore, Hong Kong, China, Malaysia, Thailand, Viet Nam, and IndonesiaA group of 5 international comparator shipping firms from the region were used for average return on equity

Sector Features Measurement Indicator

Example: what to about rice prices?

Rice Policy in the Philippines 34

Jan-

00

May

-01

Sep-0

2

Jan-

04

May

-05

Sep-0

6

Jan-

08

May

-09

Sep-1

0

Jan-

12

May

-13

Sep-1

40

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Philippines

Vietnam

Thailand

Wh

ole

sa

le p

ric

es

, US

D/k

g

In September 2014, 1kg of rice cost PHP 41 in Philippine supermarkets. Consumers in Vietnam were paying the equivalent of PHP 16.

Source: FAO GIEWS Price Tool

Government

• Enhance programs to reduce food prices without farm profits falling

• Provide universal social protection, health insurance, basic education

• Simplify business regulations, for firms of all sizes

Businesses

• Support reforms that promote competition to level the playing field

• Support freedom of association and collective bargaining

• Partner with government and organize training for workers to create and upgrade skills

Labor

• Actively participate in dialogue and include informal workers

• Recognize valid forms of flexible contracts

• Reduce calls to hike minimum wages, as food prices fall.

Civil society

• Ensure broad-based participation and support for this type of agreement.

• Monitor commitments made

• Support evidence-based policy making, performance-informed budgeting (media, Open Government)

Example of a balanced package of reforms:

Thank you

Rogier van den Brink, Lead Economist and Program Leader, and

Karl Kendrick Chua, Senior Country EconomistMacroeconomics and Fiscal

Management Global Practice