LOCAL AUTHORITIES - Office of the Auditor General · LOCAL AUTHORITIES . ii . ... 5.2.9....

197

THE REPUBLIC OF UGANDA OFFICE OF THE AUDITOR GENERAL ANNUAL REPORT OF THE AUDITOR GENERAL FOR THE YEAR ENDED 30 TH JUNE 2015 LOCAL AUTHORITIES

Transcript of LOCAL AUTHORITIES - Office of the Auditor General · LOCAL AUTHORITIES . ii . ... 5.2.9....

THE REPUBLIC OF UGANDA

OFFICE OF THE AUDITOR GENERAL

ANNUAL REPORT OF THE AUDITOR GENERAL

FOR THE YEAR ENDED 30TH JUNE 2015

LOCAL AUTHORITIES

ii

iii

Table of Contents PART I ............................................................................................................................ 1

1.0 INTRODUCTION ................................................................................................... 1

2.0 STATUS OF COMPLETION OF AUDITS .................................................................... 1

3.0 KEY AUDIT FINDINGS ........................................................................................... 3

4.0 CROSS CUTTING ISSUES IN LOCAL GOVERNMENTS ................................................ 9

PART II ..........................................................................................................................33

5.0 DETAILED REPORT OF LOCAL AUTHORITIES .........................................................33

5.1 ARUA BRANCH .............................................................................................33

5.1.1. ADJUMANI DLG .............................................................................................33

5.1.2. ARUA MC ......................................................................................................34

5.1.3. MARACHA DLG ..............................................................................................35

5.1.4. MOYO DLG ...................................................................................................37

5.1.5. MOYO TC......................................................................................................37

5.1.6. YUMBE DLG ..................................................................................................39

5.1.7. ZOMBO DLG .................................................................................................40

5.2 FORT-PORTAL BRANCH ................................................................................47

5.2.1. BUNDIBUGYO DLG ........................................................................................47

5.2.2. KARAGO TC ..................................................................................................48

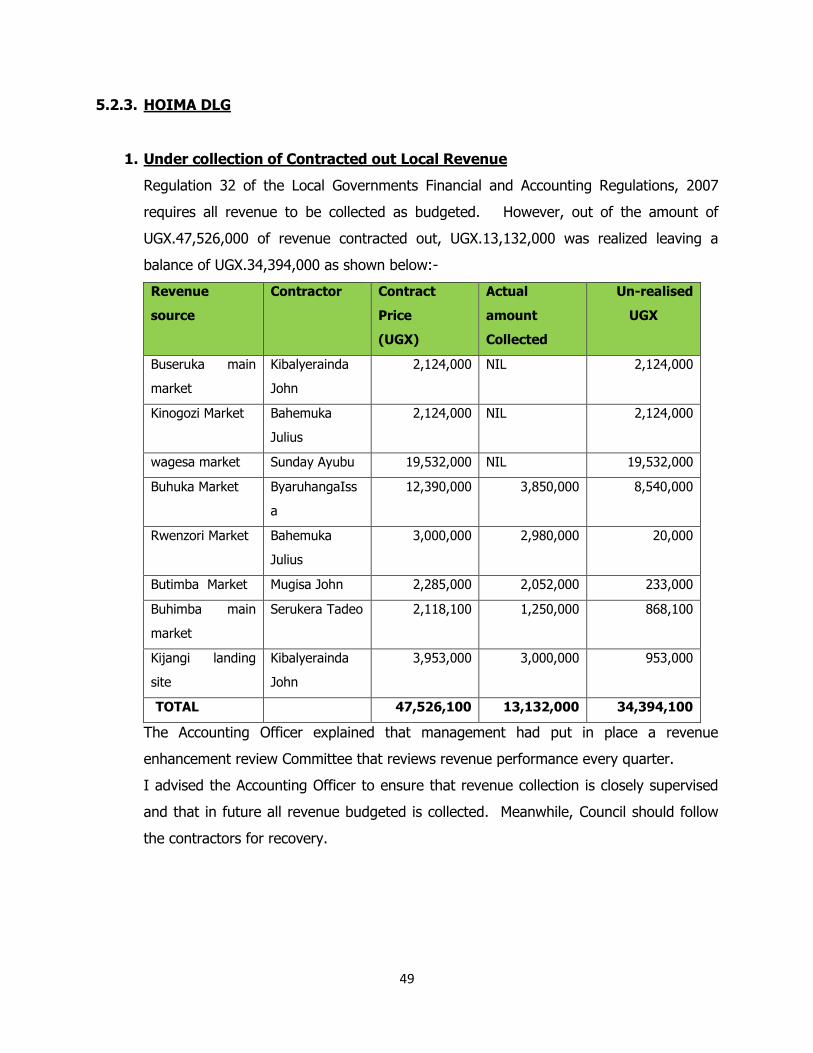

5.2.3. HOIMA DLG ..................................................................................................49

5.2.4. HOIMA MC ....................................................................................................50

5.2.5. KASESE DLG .................................................................................................50

5.2.6. KAGADI TC ...................................................................................................52

5.2.7. MASINDI MC .................................................................................................53

5.2.8. KYEGEGWA DLG ............................................................................................54

5.2.9. KIRYANDONGO DLG ......................................................................................54

5.2.10. BWEYALE TC .............................................................................................55

5.2.11. KYENJOJO TC ............................................................................................56

5.2.12. KATOOKE TC .............................................................................................56

5.2.13. NTOROKO DLG ..........................................................................................58

5.3 GULU BRANCH ..............................................................................................59

5.3.1. APAC DLG .....................................................................................................59

iv

5.3.2. AGAGO DLG ..................................................................................................61

5.3.3. ALEBTONG DLG ............................................................................................62

5.3.4. GULU DLG ....................................................................................................62

5.3.5. KOLE DLG .....................................................................................................64

5.3.6. KITGUM DLG ................................................................................................66

5.3.7. LAMWO DLG .................................................................................................69

5.3.8. LIRA DLG ......................................................................................................70

5.3.9. PADER DLG...................................................................................................72

5.4 JINJA BRANCH .............................................................................................74

5.4.1. BUGIRI DLG ..................................................................................................74

5.4.2. BUYENDE DLG ..............................................................................................74

5.4.3. IGANGA DLG .................................................................................................78

5.4.4. IGANGA MC ..................................................................................................81

5.4.5. JINJA DLG ....................................................................................................84

5.4.6. KAMULI DLG .................................................................................................87

5.4.7 KAYUNGA DLG ..............................................................................................89

5.4.8 KAYUNGA TC ................................................................................................89

5.4.9 LUUKA DLG ...................................................................................................90

5.4.10 LUUKA TC .....................................................................................................91

5.4.11 MAYUGE DLG ................................................................................................91

5.4.12 NAMUTUMBA DLG .........................................................................................93

5.4.13 NAMAYINGO DLG ..........................................................................................95

5.5 KAMPALA BRANCH .......................................................................................97

5.5.1 BUVUMA DLG ................................................................................................97

5.5.2 GOMBA DLG .................................................................................................98

5.5.3 LUWERO DLG ...............................................................................................99

5.5.4 WOBULENZI TC .......................................................................................... 104

5.5.5 MPIGI DLG ................................................................................................. 104

5.5.6 MUKONO DLG ............................................................................................. 105

5.5.7 MUKONO MC............................................................................................... 106

5.5.8 NAKASEKE DLG ........................................................................................... 107

5.5.9 NAKASONGOLA DLG .................................................................................... 107

5.5.10 ENTEBBE MC .............................................................................................. 107

5.6 MASAKA BRANCH .......................................................................................108

5.6.1 KALANGALA DLG ......................................................................................... 108

5.6.2 KIBOGA DLG ............................................................................................... 109

5.6.3 KIBOGA TC ................................................................................................. 109

v

5.6.4 LYANTONDE TC .......................................................................................... 110

5.6.5 MASAKA DLG .............................................................................................. 111

5.6.6 MITYANA DLG ............................................................................................. 111

5.6.7 MITYANA TC ............................................................................................... 112

5.6.8 MUBENDE DLG ............................................................................................ 113

5.6.9 RAKAI DLG ................................................................................................. 114

5.6.10 RAKAI TC ................................................................................................... 115

5.6.11 SEMBABULE TC ........................................................................................... 115

5.6.12 BUKOMANSIMBI TC ..................................................................................... 116

5.6.13 KALUNGU DLG ............................................................................................ 117

5.6.14 LWENGO DLG ............................................................................................. 117

5.6.15 LWENGO TC ............................................................................................... 118

5.6.16 MATEETE TC ............................................................................................... 119

5.7 MBALE BRANCH .........................................................................................121

5.7.1 BUDAKA DLG .............................................................................................. 121

5.7.2 BUDAKA TC ................................................................................................ 122

5.7.3 BUDUDA DLG .............................................................................................. 123

5.7.4 BUDUDA TC ................................................................................................ 124

5.7.5 BUKWO TC ................................................................................................. 124

5.7.6 BUSIA DLG ................................................................................................. 125

5.7.7 BUSIA MC ................................................................................................... 127

5.7.8 BUTALEJA DLG ............................................................................................ 128

5.7.9 KWEEN DLG ................................................................................................ 128

5.7.10 MANAFWA DLG ........................................................................................... 129

5.7.11 MBALE DLG................................................................................................. 130

5.7.12 SIRONKO DLG ............................................................................................. 132

5.7.13 BUDADIRI TC .............................................................................................. 133

5.7.14 TORORO DLG ............................................................................................. 134

5.7.15 TORORO MC ............................................................................................... 135

5.7.16 LWAKHAKHA TC .......................................................................................... 136

5.7.17 BULAMBULI DLG ......................................................................................... 136

5.7.18 BULAMBULI TC ........................................................................................... 138

5.7.19 BULEGENI TC .............................................................................................. 139

5.8 MBARARA BRANCH ....................................................................................139

5.8.1 BUSHENYI DLG ........................................................................................... 139

5.8.2 KABALE DLG ............................................................................................... 140

5.8.3 KATUNA TC ................................................................................................ 145

vi

5.8.4 HAMURWA TC ............................................................................................. 146

5.8.5 KABWOHE-ITENDERO TC ............................................................................. 147

5.8.6 KIHIHI TC................................................................................................... 148

5.8.7 KIRUHURA DLG ........................................................................................... 149

5.8.8 KISORO DLG ............................................................................................... 150

5.8.9 KISORO TC ................................................................................................. 151

5.8.10 MBARARA DLG ............................................................................................ 152

5.8.11 NTUNGAMO DLG ......................................................................................... 153

5.8.12 RWASHAMAIRE TC ...................................................................................... 158

5.8.13 RUKUNGIRI DLG ......................................................................................... 158

5.8.14 RUKUNGIRI MC ........................................................................................... 159

5.8.15 IGORORA TC .............................................................................................. 160

5.8.16 BUTOGOTA TC ............................................................................................ 160

5.8.17 SHEEMA DLG .............................................................................................. 161

5.8.18 BUGONGI TC .............................................................................................. 162

5.8.19 BUHWEJU DLG ............................................................................................ 162

5.8.20 RUBAARE TC ............................................................................................... 163

5.8.21 RUBIRIZI DLG ............................................................................................. 163

5.9 SOROTI BRANCH ........................................................................................164

5.9.1 ABIM DLG ................................................................................................... 164

5.9.2 ABIM TC ..................................................................................................... 167

5.9.3 BUKEDEA TC ............................................................................................... 169

5.9.4 KOTIDO DLG .............................................................................................. 169

5.9.5 KUMI DLG ................................................................................................... 171

5.9.6 MOROTO DLG ............................................................................................. 172

5.9.7 NAKAPIRIPIRIT TC ...................................................................................... 173

5.9.8 SOROTI DLG ............................................................................................... 173

5.9.9 SOROTI MC ................................................................................................ 174

5.9.10 NGORA DLG ................................................................................................ 176

5.9.11 NGORA TC .................................................................................................. 180

5.9.12 SERERE DLG ............................................................................................... 181

vii

LIST OF ACRONYMS

AO Accounting Officer

BOQs Bills of Quantity

CAO Chief Administrative Officer

CIID Criminal Investigation & Intelligence Department

DA District Administration

DC District Council

DEC District Executive Committee

DLG District Local Government

DLG District Local Government

DPAC District Public Accounts Committee

DSC District Service Commission

GOU Government of Uganda

HC I Health Centre I

HC II Health Centre II

HC III Health Centre III

HC IV Health Centre IV

HLG Higher Local Government

IAS International Accounting Standard

IDP Internally Displaced People

IFRS International Financial Reporting Standard

INTOSAI International Organization of Supreme Audit Institutions

LC I Local Council One

LC II Local Council Two

LC III Local Council Three

LC IV Local Council Four

LC V Local Council Five

LGA Local Government Act

LGBFP Local Government Budget Framework Paper

LGDP Local Government Development Programme

viii

LGFAM Local Government Financial and Accounting Manual

LGFAR Local Government Financial and Accounting Regulations

LGMSD Local Government Management of Service Delivery

LGPAC Local Government Public Accounts Committee

LLG Lower Local Government

LST Local Service Tax

MC Municipal Council

MoFPED Ministry of Finance Planning and Economic Development

MoLG Ministry of Local Government

MoPS Ministry of Public Service

NAA National Audit Act

NAADS National Agricultural Advisory Services

NDP National Development Plan

NSSF National Social Security Fund

OAG Office of the Auditor General

OPM Office of the Prime Minister

PAYE Pay As You Earn

PFAA Public Finance and Accountability Act

PHC

PPDA

Primary Health Care

Public Procurement and Disposal of Public Assets Authority

PFMA Public Finance Management Act

PSC Public Service Commission

PWDs People with Disabilities

SAI Supreme Audit Institution

SC Sub County

SFG School Facilitation Grant

TC Town Council

TC Town Clerk

UGX Uganda Shillings

ULGA Uganda Local Governments Association

UPE Universal Primary Education

URA Uganda Revenue Authority

URF Uganda Road Fund

ix

USMID Uganda Support to Municipal Infrastructure Development Program

VAT Value Added Tax

VFM Value For Money

WHT Withholding Tax

YLP Youth Livelihood Programme

IFMS Integrated Financial Management Systems

IPPS Integrated Personel and Payroll System

x

Definitions

Accountant General Means the person designated under Section 3 of the Public

Finance Management Act, 2015.

Accounting Officer means a person designated under Section 3 of the Public Finance

Management Act, 2015 as Accounting Officer and Section 64(1),

65 (2) (a) and 69(2) of the Local Governments Act 1997 Cap 243

of the Laws of Uganda as amended in respect of Chief

Administrative Officer of a District, Town Clerk of an Urban

Council and Sub-county Chief and Head teachers respectively.

Auditor General Means the Auditor General appointed under article 163(1) of the

Constitution of Uganda 1995, as amended.

Adverse opinion Means an opinion issued by the Auditor General whereby the

financial statements contain material misstatements or errors and

there is disagreement with management to the extent that it is

concluded that the financial statements do not represent a fair

presentation of the financial position of the entity as at the

financial year end.

Consolidated fund Means the consolidated fund of Uganda established under article

153 of the Constitution of Uganda 1995, as amended.

Disclaimer opinion Means an opinion issued by the Auditor General whereby the

financial statements contain material misstatements based on

limitations on scope of the audit work to the extent that there is

uncertainty on the fairness and truthfulness of the financial

statements and therefore an audit opinion cannot be given

because of the gravity of the uncertainty.

Doubtful Expenditure Means expenditure that has not been confirmed as genuine

considering the circumstances under which it was incurred.

Escrow account Means an account established in the custody of a third party to

hold revenues which will be disbursed upon the fulfillment of the

conditions specified.

xi

Emphasis of matter Refers to a matter that does not affect the Auditor’s Opinion but

is of such fundamental importance to users in understanding of

the financial statements so as to warrant its inclusion in the

Auditor’s report immediately after the opinion.

Financial year Refers to an accounting period of twelve months.

Force on Account Means construction works undertaken by use of a procuring and

Disposing Entity’s own personnel and equipment.

Generally accepted

accounting practice

Means accounting practices and procedures recognized by the

accounting profession in Uganda and approved by the Accountant

General as appropriate for reporting financial information relating

to Government, a Ministry or department, a fund, an agency or

other reporting unit and which are consistent with the Public

Finance Managemt Act, 2015 and any other relevant

appropriation Act.

Grade X Means Pupils who did not sit exams.

Grade U Means Children who failed or Un-graded.

Government Means the Government of Uganda.

Higher Local

Governments

Refers in the context of this report, Districts, Municipal Councils

and Town Councils.

Incompletely vouched Means expenditure that is not supported by adequate

accountability documents.

Internal audit Means a process to measure, evaluate and report to the

management of an entity on the efficiency of the system of

internal control used to ensure the validity of financial and other

information.

Internal control Means a set of systems to ensure that financial and other records

are reliable, complete and ensure adherence to the entity

Management policies, orderly and efficient conduct of the entity,

proper recording and safeguarding of assets and resources.

Local Government

Council

Means a Council referred to in article 180 of the Constitution.

Nugatory Expenditure Means wasteful expenditure.

xii

Qualified “except for”

opinion

Refers to the audit opinion issued by the Auditor General whereby

the material misstatements or errors are not pervasive and

“except for” these misstatements or errors being adjusted for the

rest of the financial statements fairly present in all material

respects the financial position of the entity.

Unqualified opinion Refers to the audit opinion issued by the Auditor General whereby

the financial statements contained no material misstatements or

errors.

Unvouched

Expenditure

Means funds spent without preparing vouchers or expenditure

that is not supported with payment vouchers.

1

PART I

1.0 INTRODUCTION

I am required by Article 163(3) of the Constitution of the Republic of Uganda 1995, (as

amended) Section 13, 16 and 19 of the National Audit Act 2008, Section 87 of the Local

Governments Act 1997 as amended and Section 51(4) of the Public Finance

Management Act 2015 to audit and report on Local Governments.

Under Section 82(4) of the Public Finance Management Act, 2015, I am now required to

submit to Parliament by 31st December annually a report of the Accounts audited by me

for the year immediately preceding. I am therefore issuing this report in accordance

with the above provisions.

Chapter 3 of this Annual Report to Parliament covers financial audits carried out on

District Local Governments, Municipal and Town Councils, Lower Local Governments,

Schools and Tertiary Institutions.

Part 1 of this chapter, I give an overview of the financial audit work carried out, status

of completion of the audits, a summary of the audit opinions issued on the financial

statements of the entities audited and the major audit findings in Local Governments

arising from the results of the audits carried out.

Part II gives the other significant audit findings on the Local Government entities

audited that need urgent attention.

I, therefore, urge all stakeholders to review this report with utmost interest and concern

to ensure effective implementation of the recommendations therein and ultimately

improve the lives of our people.

2.0 STATUS OF COMPLETION OF AUDITS

I am required to audit and report on a total of 1,786 accounts of Local Authorities,

Regional Referral Hospitals, Secondary Schools and Tertiary Institutions. I am pleased

to report that my office was able to audit and complete 1,168 accounts including all the

2

307 Higher Local Governments (HLGs) and 13 Referral Hospitals, 571 Lower Local

Governments (Sub-counties) and 277 secondary schools and tertiary institutions. The

table below shows the number of entities and the audit completion status:

Table 1: Number Of Entities And Audit Completion Status

Entities

Planned Number of Entities

Accounts Audited and Pending Audits

Audited Pending

Districts 111 111 -

Municipal Councils 22 22 -

Town Councils 174 174 -

Regional Referral Hospitals 13 13 -

Sub Counties and Divisions (FY 2013/2014)

1,189 571 618

Secondary Schools/Tertiary Institutions (Year 2013 and 2014)

277 277 -

Total 1,786 1,168 618

The detailed audit reports of thirteen regional referral hospitals are included in volume 2

of my report. Audit of 1,189 sub-counties for the financial year 2014/2015 remain

outstanding due to lack of funds.

Similarly, I was only able to audit 277 secondary schools and tertiary institutions out of a

population of 1,280 schools and tertiary institutions due to limited funding provided for

the audit.

2.1 Audit Opinions

The table below shows a summary of the audit opinions of HLG for the financial year

under review including a comparison with audit opinions of the previous two years.

Table 2: Summary of Audit Opinions for the three financial years

2012/2013 2013/2014 2014/2015

Opinion1 Local Govern

ments

Percentage

Local Governm

ents

Percentage Local Governments

Percentage

Un qualified 116 37.4% 213 69.38% 279 91

Except for (qualified)

183 60% 91 29.64% 27 8.7

3

Disclaimer 7 2.3% 03 0.98% 01 0.3

Adverse 0 0% 0 0% 0 0

TOTAL 307 100% 307 100% 307 100

From the table above, it is noted that unqualified opinions increased from 37.4% in

2012/2013, 69.38% in 2013/14 to 91% in 2014/15 while qualified opinions decreased

from 60% in 2012/13, 29.64% in 2013/14 to 8.7% in 2014/15. The disclaimer and

adverse opinions decreased from 2.3% in 2012/13 to 0.98% in 2013/2014 to 0.3% in

2014/2015. The above trends of opinion would suggest an improvement in the financial

management and accountability in the Local Governments.

The details of audit opinions issued for each entity regarding financial statements of

2014/15 are shown on pages 24-32.

3.0 KEY AUDIT FINDINGS

A summary of the key findings arising from the audit of Local Governments is

highlighted below:-

Lack of Consolidated Local Governments Annual Accounts

Section 52 (1) (b) of the PFM Act, 2015 requires the Accountant General within three

months after the end of the financial year to submit consolidated annual accounts of the

Local Governments.

However, contrary to the above provision, the Accountant General did not submit the

consolidated annual account of the Local Governments for audit.

Lack of a consolidated Local Government accounts denies the stakeholders financial

information for comparative analysis and decision making.

The Accountant General explained that it was not possible to consolidate the accounts

due to limited time for developing the templates, guidelines and sensitization of the

various Local Government staff that are necessary to implement the change required

under the new legislation.

4

I advised the Accountant General to initiate measures for the consolidation of Local

Government accounts to comply with the law.

Overpayment of Salary

Section (B-a) (7) of the General rules on Payment of Salaries in Public Service Standing

Orders,2010 requires salaries to be paid correctly, promptly and as a lump sum in

accordance with the approved salary structure for the Public Service.

However, Payroll analysis carried out revealed that a sum of UGX.6,567,322,457 was

paid in excess of the approved salary scales to various staff.

The Accounting Officers attributed overpayments to challenges encountered during

deCentralization of salary payments on the Integrated Financial Management system

(IFMS) and Integrated Personnel and Payroll System (IPPS) and outright errors during

the salary payment process. Many of the Accounting Officers explained that they had

initiated the process of recovering the overpaid amounts. I wait for evidence to that

effect.

Procurement Anomalies

33 Local Governments procured items worth UGX. 11,493,666,328 without following

Public Procurement Regulations and Guidelines. The amount is comprised of

UGX.310,619,509 which lacked procurement files , UGX.9,937,360,405 where there was

breach of procurement procedures, UGX. 1,029,688,268 involving inadequate contract

management and UGX.215,998,1468 of unauthorized contract variations. Consequently,

it becomes difficult to ascertain whether value for money was achieved. The

shortcomings were attributed to lack of technical capacity, understaffing and deliberate

flouting of PPDA regulations. There is need for the Accounting Officers to develop

capacity building strategies and to engage the Ministry of Public Service to address the

understaffing problem. In addition Accounting Officers are encouraged to invoke the

relevant sections of the Law for noncompliance.

Funds not Accounted for

Expenditure amounting to UGX 5,524,074,947 was identified as funds unaccounted for.

Consequently, I could not confirm that the funds were utilized for the intended

purposes. The delayed submission of accountability may also lead to falsification of

5

documents resulting into loss of funds. This was caused by failure of Accounting Officers

to enforce accountability controls and lack of Advances Ledger to monitor advances.

There is need for Accounting Officers to enforce controls relating to financial

management and accountability.

Under Collection of Local Revenue

Regulation 32 of the Local Governments Financial and Accounting Regulations, 2007

requires Councils to ensure collection of all budgeted revenue in an approved manner.

Review of revenue performance revealed significant under collection of Local revenue in

59 Councils amounting to UGX, 23,974,340,977.

The shortfall in revenue collection was attributed to failure to carry out revenue

enumeration and assessments, non-enforcement of contracts with private revenue

collectors, understaffing and incomplete revenue records. There seems to be little effort

in ensuring effective collection of Local revenue.

I advised the Accounting Officers to sensitize tax payers on the relevant taxes and to

develop strategies and enforce lawful measures to enhance revenue collections.

Irregular Levy of Development Tax

There were instances of irregular imposition of development tax totaling UGX.

409,672,340 on contracts by some Local Governments in a bid to enhance Local revenue

collections without approval of the Minister for Local Government contrary to the

regulations. There is a risk that such charges could compromise on quality of works and

increased costs of service delivery. The Accounting Officers explained that this was an

attempt by Councils to raise Local revenue for service delivery. There is need for the

Accounting Officers to seek for the appropriate authority prior to levying of the tax.

Understaffing

Audit revealed that the high levels of vacant posts in Local Government had not

significantly improved. The levels ranged from 14 % in Bududa District Local

Government to 87% in Luuka Town Council.

6

Understaffing overstretches the available staff beyond their capacity, creates job-related

stress to the fewer staff avaliable and negatively affects the level of public service

delivery to the community.

Understaffing was attributed to limited wage bill and a ban on recruitment by the

Ministry of Public Service. The Accounting Officers are advised to continue engaging the

Ministry of Public Service, the Ministry of Local Government and the Ministry of Finance

Planning and Economic Development to address the challenge. Meanwhile Government

is advised to address this phenomenon to ensure improvements in service delivery at the

Local level.

Assets Management

Lack of Land Titles

Out of 307 Local Governments, 118 entities representing 39% of the Local Governments

lacked land titles for the land where Council properties are located. There is a risk that

Council land is exposed to encroachment and disputes which later leads to litigation in

courts of law araising from land disputes between the Councils and the Communities.

The Accounting Officers attributed this to lack of funds to process land titles and the

absence of District Land Boards. There is urgent need for the Accounting Officers to

prioritize and allocate funds and ensure that the land titles are secured. The District

Councils are also advised to ensure that the District Land Boards are constituted.

Lack of Information Communication Technology (ICT) Policy

Local Governments are making considerable investments in the Information Technology

equipment and related software without the necessary human resource and proper

procedures to manage the IT resources. I have raised this issue continuously over the

last three years. There is a risk of loss of equipment and data maintained therein.

Although the regulations require the Accounting Officers to designate an Officer to

manage the information and communication technology resources, however the

Accounting Officers are experiencing difficulties in identifying the Officers with the

7

required competencies. It is recommended that the Ministry of Public Service should

review the organization structure of Local Governments to ICT personnel.

Financial Reporting

Financial Statements for Lower Local Governments

In my previous year report, I noted that there was still a problem with presentation of

financial statements in the Lower Local Governments. In the financial year under

review, the shortcomings were still identified. The anomalies include;

Non-adherence to presentation and disclosure requirements as per Local

Government Financial and accounting Manual 2007, for example, lack of cash flow

statements, schedule of commitments, and others.

Misstatement of account balances.

Non- preparation of primary books of accounts such as Ledgers, cash books, and

vote books.

Lack of Board of survey reports

Lack of Bank reconciliation statements and certificates of Bank balance.

Unbalanced Budgets

Lack of other statements, schedules and Notes to the accounts.

Missing budget figures in income and expenditure accounts.

Non-disclosure of losses.

Preparation of Financial statements is a stewardship role in which accountability for

application of resources entrusted to Accounting Officers is reported to the stakeholders.

Failure to present financial statements properly impairs interpretation and analysis of

entity performances. This is attributed to understaffing, lack of training, Low levels of

practical experience by clerks and non-adherence to the guidance provided in the Local

Governments’ Financial and Accounting Manual 2007 and other accounting standards.

Accounting Officers should liaise with responsible authorities to ensure the staffing gaps

are addressed and the necessary training undertaken.

8

Lack of Standard Financial Reporting Framework for Schools

It was observed that there was no standard financial reporting framework for secondary

schools. This was attributed to lack of financial and accounting manual. As a result,

there was no uniform classification and coding of account balances, format and

presentation of financial statements. Section 29 (2) (b) of Education (Board of

Governors) regulations require the board to prepare within three months financial

statements in the form approved by the Minister or District Secretary for Education.

There is need for the Minister or District Secretary for Education to prescribe the form of

the financial statements for the Secondary Schools in consultation with the Accountant

General.

Utilized Capacity Building Infrastructure Development Funds Under

(USMID)Project

It was observed that 14 Municipal Councils under the USMID project had not fully

utilized funds released to them amounting to UGX.63,141,565,615 comprising of

capacity building funds (UGX.6,079,544,830) and infrastructure development funds

UGX.57,062,020,785.

Failure to utilize the released funds reflects lack of effective implementation of project

programs disadvantaging the community who are intended to benefit from the program.

Management attributed the low absorption of the capacity Building funds to the failure

of the Municipal Councils to procure key retooling equipment for surveying, engineering

and environment among others partly due to lack of technical capacity to procure such

specialized equipment. In addition the delay to utilise the infrastructure development

funds was attributed to failure to attract responsive bidders for the jobs.

There is need to enhance the absorption capacity to ensure full utilization of the funds

released.

9

4.0 CROSS CUTTING ISSUES IN LOCAL GOVERNMENTS

The following cross cutting issues arose in the audit of Local Governments, namely:-

1. Revenue

Under collection of Local Revenue

Irregular levy of Development tax

2. Expenditure

Procurement anomalies

Funds not accounted for

Over payment of salaries

3. Internal control and Governance issues

Understaffing

Shoddy works/incomplete projects

Outstanding commitments

Lack of ICT policy

4. Assets management

Lack of land titles

Receivables

Un spent balances

Under absorption under USMID

The summary of these findings are in the table below and further detailed in table 8 on

pages 24-32.

10

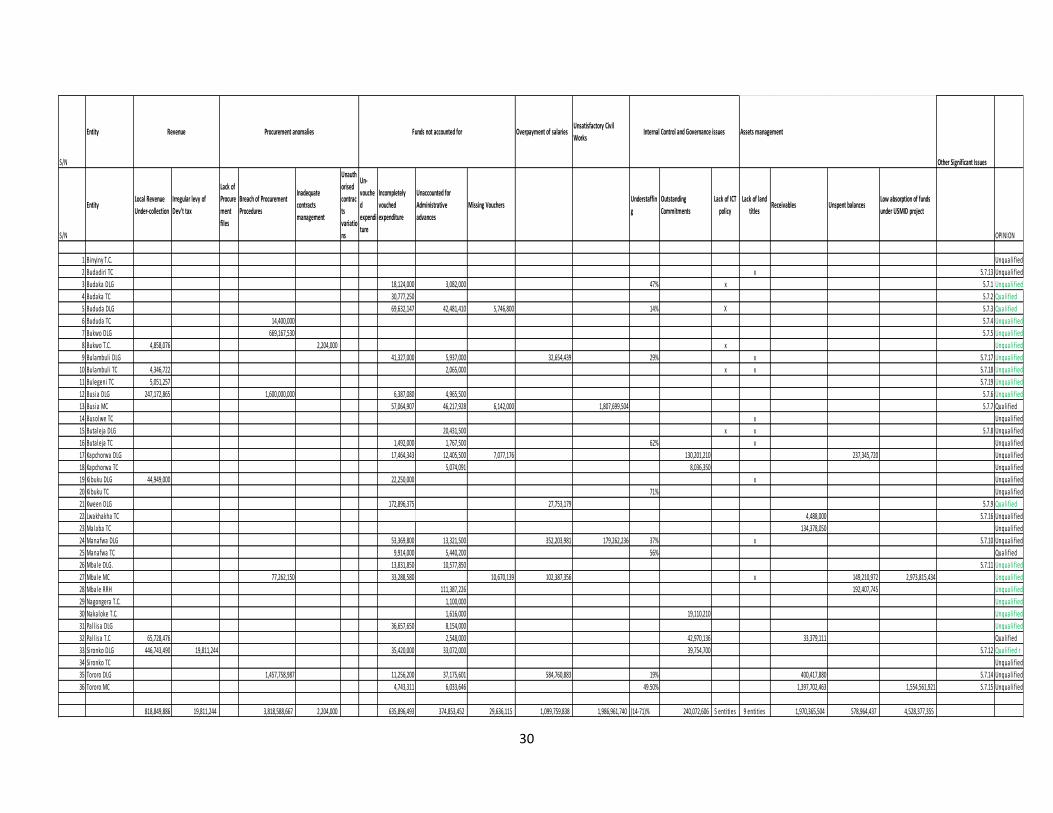

Table 3

AUDIT

FINDINGS FORTPORT

AL

JINJA KAMPALA MASAKA SOROTI MBALE MBARARA

Revenue

Irregular

levy of

Dev't tax

11,722,603 0 0 0 36,846,723 19,811,244 0

Expenditu

re

Internal

control

and

Governan

ce issues

Understaffi

ng46%to 58% 47% to 87% 34%- 70% 40% - 66% 22 – 80.3% 14%-71% 26%-62%

Lack of ICT

Policy4 entities 2 Entities 1 entity 5 Entities 10 Entities

Assets

managem

ent

Lack of land

titles19 entities 17 Entities 3 entities 10 entities 9 Entities

Key

Matters that require immediate action at almost no cost.

Matters that require immediate action at a low cost.

Matters that require immediate action, high cost and intervention of other stakeholder .

2,689,465,010 5,067,803,137 3,245,456,345 4,528,377,355 11,681,947,823 63,142,505,615

379,976,896 578,964,437 5,904,514,170

Un-utilized

Capacity

Building and

Infrastructu

re

Developmen

t Funds

under

(USMID

project)

4,780,442,890 7,119,004,037 21,279,231,573 2,750,777,445

Unspent

balances 91,477,502 288,894,036 1,765,395,052 2,750,777,445 49,028,802

498,275,411 70,372,992 650,970,031 1,970,365,504 156,337,165 14,602,705,594

1 entity 15 entities 10 entities 34 Entities

Receivables 475,932,609 6,365,144,394 4,415,307,488

114,164,545 240,072,606 136,827,279 3,115,454,282

5 entities

41% to 77% 20% to 77%

Outstanding

commitment

s

115,352,053 1,571,052,270 723,900,885 214,084,644

97,743,325 2,303,623,818 1,986,961,740 765,195,275 8,022,354,999

174,999,798 1,099,759,836 1,567,134,564 6,567,322,457

Unsatisfact

ory civil

works

1,562,460,312 600,009,488 706,361,041

1,040,386,060 828,148,546 5,524,074,947

Overpayme

nt of

salaries

45,008,211 792,202,445 460,097,809 62,437,379 2,314,711,035 50,971,380

9,919,000 11,493,666,328

Funds not

accounted

for

128,324,569 567,312,919 444,336,515 21,356,000 1,584,962,320 396,061,472 513,186,546

Procuremen

t anomalies1,650,770,174 3,546,240,840 639,542,697 1,257,893,736 103,661,000 464,846,214 3,820,792,667

785,717,478 794,012,515 818,849,886 3,567,380,977 23,974,340,977

79,540,437 261,751,333 409,672,340

Local

Revenue

Under-

collection

414,300,516 2,203,694,151 347,784,620 13,933,568,408 1,109,032,426

Summary of Significant Cross Cutting Issues per OAG Branch Offices

OAG REGIONAL OFFICES

ARUA GULU Total

11

4.1 REVENUE

4.1.1 Under collection of Local Revenue

Regulation 32 of the Local Governments Financial and Accounting Regulations, 2007

requires Councils to ensure collection of all budgeted revenue in an approved manner

and the revenue banked intact in Council accounts. However, a review of revenue

performance of 138 Councils revealed that under colletion of Local Revenue amounting

to UGX. 23,974,340,977.

This implies that all planned activities for the year were not implemented. This was

attributed to lack of revenue enumeration and assessment and failure to supervise

collection of contracted revenue. There is need for the Accounting Officers to carry out

revenue assessments, maintain proper revenue records, sensitize the tax payers and

strengthen controls relating to collection of revenue.

With regard to 571 Lower Local Governments (Sub Counties), an amount of UGX

1,586,709,507 remained uncollected during the period.

The shortfall in revenue collection was attributed to; failure to carry out revenue

enumeration and assessments, non-enforcement of contracts with private revenue

collectors, understaffing and incomplete revenue records. There seems to be little effort

in ensuring effective collection of these revenue sources.

I advised the Accounting Officers to sensitize tax payers and develop strategies and

enforce lawful measures to enhance revenue collection.

4.1.2 Irregular Levy of Development Tax

The Local Governments Act part IV, Other Revenues section 13 (o), requires that any

other source of revenue has to be approved by the Minister for Local Government before

its assessment and collection. However, Fourteen (14) Councils collected funds

amounting to UGX 409,672,340 in form of taxes from contracts funded by conditional

grants without the Ministers approval contrary to the law. There is a risk that such

charges could compromise on quality of works and increased costs of service delivery.

The Accounting Officers explained that this was an attempt by Councils to raise Local

12

revenue for service delivery. There is need for the Accounting Officers to seek for the

appropriate authority prior to levying of the tax.

4.2 EXPENDITURE

4.2.1 Procurement Anomalies

The Public Procurement and Disposal of Public Assets (PPDA) Act 2003, and the Local

Government PPDA Regulations 2006 require that all public procurement of goods,

services and works comply with the procurement law. However, 33 Local Governments

procured items and services worth UGX.11,493,666,328 without following Public

Procurement Regulations and guidelines as shown in the table below:

Table 4 Procurement Anomalies

Category Amount (UGX) %age

Breach of procurement procedures 9,937,360,405 86.5%

Contract management weaknesses 1,029,688,268 8.9%

Lack of procurement files and records 310,619,509 2.7%

Unauthorised contract variation 215,998,146 1.9%

Total 11,493,666,328 100%

In addition the analysis of the 571 audited sub-counties revealed that procurements

worth UGX.2,299,303,377 had irregularities related to lack of procurement records and

failure to follow the procurement procedures.

The shortcomings were attributed to lack of technical capacity, understaffing and

deliberate flouting of PPDA regulations. There is need for the Accounting Officers to

develop capacity building strategies and to engage the Ministry of Public Service to

address the understaffing problem. In addition Accounting Officers are encouraged to

invoke the relevant sections of the Law for noncompliance with the regulations.

4.2.2 Funds not Accounted For

Regulation 43 (2) of the Local Government Financial and Accounting Regulations 2007,

require Administrative advances to Council employees to be authorized by the Chief

13

Executive and accounted for within a month. During the year under review

UGX.5,524,074,947 in respect of HLGs comprising of administrative advances,

incompletely vouched expenditure, unvouched expenditure and doubtful expenditure

remained outstanding as shown in the table below:-

Table 5 Funds not accounted for

Category Amount (UGX) Percentage

Unaccounted for Administrative advances 2,440,991,267

44.2%

Incompletely vouched expenditure 1,765,173,438

32%

Missing Vouchers 1,317,910,242

23.8

Total 5,524,074,947 100%

In addition, UGX 3,364,681,447 remained outstanding in the 571 Lower Local

Governments (Sub Counties) audited as shown below;

Table 6: Funds not accounted for in 571 Lower Local Governments

Category Amount (UGX) Percentage

Incompletely vouched 556,447,976 17.5%

Unaccounted for expenditure 160,909,108 5.1%

Unvouched expenditure 653,359,179 20.5%

Outstanding administrative advances 1,810,370,086 56.9%

Total 3,181,086,349 100%

Consequently, I could not confirm that the funds were utilized for the intended

purposes. The delayed submission of accountability may also lead to falsification of

documents resulting into loss of funds. This was caused by failure by Accounting

Officers to enforce accountability controls and lack of advances ledger to monitor

advances. There is need for Accounting Officers to enforce controls relating to financial

management and accountability.

14

4.2.3 Overpayment of Salary

Section (B-a) (7) of the General rules on Payment of Salaries in Public Service Standing

Orders,2010 requires salaries to be paid correctly, promptly and as a lump sum in

accordance with the approved salary structure for the Public Service.

However, Payroll analysis carried out revealed that a sum of UGX 6,567,322,457 was

paid in excess of the approved salary scales to various staff.

The Accounting Officers attributed overpayments to challenges encountered during

deCentralization of salary payments on the Integrated Financial Management system

(IFMS) and Integrated Personnel and payroll system (IPPS) and outright errors during

the salary payment process. Many of the Accounting Officers explained that they had

initiated the process of recovering the overpaid amounts. I wait for evidence to that

effect.

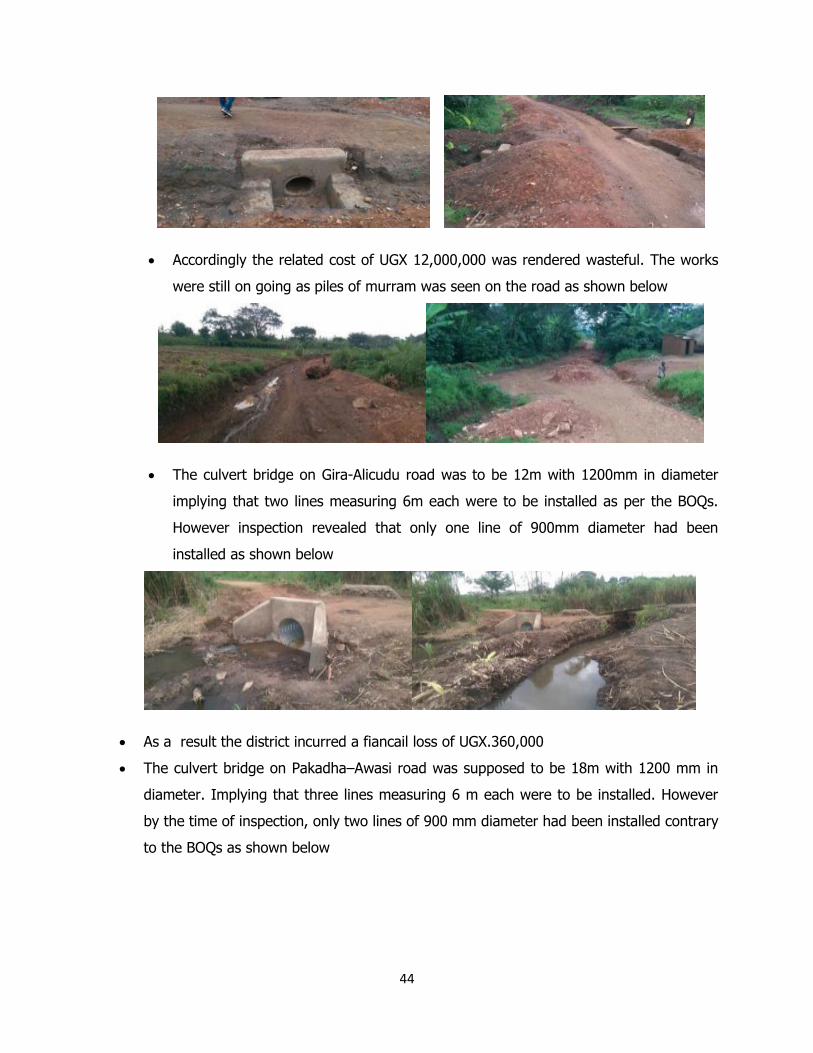

4.2.4 Unsatisfactory Civil Works

Section 14 of the PPDA regulations require an Accounting Officer to have the overall

responsibility of the successful execution of the procurement, disposal and contract

management processes and ensure that implementation of the contract as per the

agreed terms. Audit inspection of the works in the roads, water, schools, health centres

and other buildings revealed that there were several projects with unsatisfactory

construction works amounting to UGX. 8,022,354,999. This implies that value for

money may not have been achieved. The Accounting Officers attributed this anomaly to

inadequate technical staff, delayed procurement process and inadequate capacity of the

Local contractors to execute the works.

I advised the Accounting Officers to enhance monitoring and supervision of contracts to

avoid such reoccurrences and to source for competent contractors.

4.3 INTERNAL CONTROL AND GOVERNANCE ISSUES

4.3.1 Under Staffing

The audit revealed high levels of vacant posts in Local Government has not significantly

improved. The levels ranged from 14 % in Bududa District Local Government to 87% in

Luuka Town Council.

15

Understaffing overstretches the available staff beyond their capacity, creates job-related

stress to the fewer staff and negatively affects the level of public service delivery to the

community.

This was attributed to limited wage bill and a ban on recruitment by the Ministry of

Public Service.

I advised the Accounting Officers to continue engaging the Ministries of Public Service,

Local Government and Finance Planning and Economic Development to address the

challenge. Meanwhile Government is advised to address this phenomenon to ensure

improvements in service delivery at Local level.

4.3.2 Outstanding Commitments

Regulation 11(d) of the Local Government Financial and Accounting Regulations, 2007

requires the Head of Finance to ensure that commitments are not approved unless there

is sufficient and committed funds available. However, a number of Higher Local

Governments for the year under review failed to adhere to the commitment control

system which resulted in committing Councils beyond the available financial resources.

Consequently twenty two entities accumulated outstanding commitments amounting to

UGX.3,115,454,282.

The outstanding commitments can lead to litigation or confiscation of Council assets if

not settled timely. The Accounting Officers attributed the anomaly to under collection of

Local revenue and shortfall in release of grants from Central Government.

I advised the Accounting Officers to adhere to provisions of the commitment control

system to eliminate arrears and ensure financial discipline.

4.3.3 Lack of Information Communication Technology Policy

Section 110 of the LGFAR (2007) requires the Chief Executive to designate an officer to

ensure that adequate Information and Communication Technology policies are

established and are applied to enable adequate security and protection over computers

and data held on computers or information systems operated by Council. It was

16

observed that Local Governments are making considerable investments in the

Information Technology equipment and related software without the necessary human

resource and proper procedures to manage the IT resources. There is a risk of loss of

equipment and data maintained therein.

Although the regulations require the Accounting Officers to designate an Officer to

manage the Information and Communication Technology resources, however the

Accounting Officers are experiencing difficulties in identifying the Officers with the

required competencies. It is recommended that the Ministry of Public Service should

review the organization structure of Local Governments to cater for ICT personnel.

4.4 ASSETS MANAGEMENT

4.4.1 Lack of Land Titles

Regulation 9 (j) of the Local Government Financial and Accounting Regulations, 2007

require the Accounting Officers to ensure safe custody of all assets of Council. It was

observed that out of 307 Local Governments, 118 entities representing 39% of the Local

Governments lacked land titles for the land where Council properties are located. There

is a risk that Council land is exposed to encroachment and disputes. The Accounting

Officers attributed this to lack of funds to process land titles and absence of District

Land Boards. There is urgent need for the Accounting Officers to prioritize and allocate

funds and ensure that the land titles are secured. The District Councils are also advised

to ensure that the District Land Boards are constituted.

4.4.2 Receivables

Paragraph 2.3.2.3 of the Local Governments Financial and Accounting Manual 2007

states that money owed to Council represents an asset that is idle, as it denies the

Council the opportunity of using the money to provide services promptly. Thirty two

(32) Local Governments failed to collect outstanding revenue from different sources

amounting to UGX.14,602,705,594. This was attributed to laxity on the part of the

Accounting Officers to follow up collection of the debts.

17

Uncollected revenue adversely affect service delivery and have an additional risk of loss

of revenue. I advised the Accounting Officers to develop debt recovery strategies to

ensure that all outstanding debts are collected.

4.4.3 Unspent balances

Section 17(2) of the Public Finance and Management Act, 2015 requires a vote that does

not expend money that was appropriated to the vote for the financial year at the end of

the financial year to repay the money to the consolidated fund.

It was however, observed that in thirteen (13) entities UGX 5,904,514,170 in respect of

conditional grants remained unexpended at year end and was not returned to the

consolidated fund contrary to the law.

The Accounting Officers attributed the shortcoming to the late release of funds and

promised to repay back the funds to the consolidated fund.

I advised the Accounting Officers to ensure that the funds are repaid to the consolidated

fund.

4.4.4 Utilized Capacity Building Infrastructure Development Funds Under

(USMID) Project

It was observed that 14 Municipal Councils under the USMID project had not fully

utilized funds released to them amounting to UGX.63,141,565,615 comprising of

capacity building funds (UGX.6,079,544,830) and infrastructure development funds

UGX.57,062,020,785.

Failure to utilize the released funds reflects lack of effective implementation of project

programs disadvantaging the community who are intended to benefit from the program.

Management attributed the low absorption of the Capacity Building funds to the failure

of the Municipal Councils to procure key retooling equipment for surveying, engineering

and environment among others partly due to lack of technical capacity to procure such

18

specialized equipment. In addition the delay to utilise the infrastructure development

funds was attributed to failure to attract responsive bidders for the jobs.

There is need to enhance the absorption capacity to ensure full utilization of the funds

released.

4.5 SECONDARY SCHOOLS AND TERTIARY INSTITUTIONS

4.5.1 Financial Statements for Secondary Schools, Primary Schools and

Health Centres

Regulations 61-64 of the Local Governments Financial and Accounting Regulations 2007

require District Hospitals, Health Units, Secondary Schools and Primary Schools to

prepare and submit financial statements to the Chief Executive on regular basis as

indicated below;

Table 7 Financial Statements for Secondary Schools, Primary Schools and Health Centres

Entity Period Chief Executive

District Hospitals Monthly and Annually Chief Administrative Officer

Health Units Monthly Sub-county Chief and copy

Administrative Units

Secondary Schools Each academic term and

Calendar year

Chief Administrative Officer

Primary Schools Each Academic term Sub-County Chief

The regulations further provide that where a Head Teacher and the In-charge of the

Primary Schools and Health centre respectively are unable to prepare the financial

statements, assistance may be sought from the sub accountant of the Sub-county.

Regulations 70 requires the Chief Executive to submit the accounts prepared in

accordance with these regulations to the Auditor General for audit.

In my audit reports for the two previous years, I observed that the entities lacked clear

guidance on the nature of books of accounts and specific financial statements to be

prepared. The primary schools and Heath Centres also lacked the necessary manpower

to prepare the books. These issues have not been addressed.

19

It is advised that the Ministry of Finance Planning and Economic Development together

with Ministry of Local Government issue relevant accounting manuals and guidelines for

preparation of financial records and statements in the schools and Health Centres.

4.5.2 Financial Statements for Lower Local Governments

In my audit reports for the two previous years, I noted that there was still a problem

with presentation of financial statements in the Lower Local Governments. In the

financial year under review, the shortcomings were still identified. The anomalies

include;

Non-adherence to presentation and disclosure requirements as per Local

Government Financial and accounting Manual 2007, for example, lack of cash flow

statements, schedule of commitments, and others.

Misstatement of account balances.

Non- preparation of primary books of accounts such as Ledgers, cash books, and

vote books.

Lack of Board of survey reports

Lack of Bank reconciliation statements and certificates of Bank balance.

Unbalanced Budgets

Lack of other statements, schedules and Notes to the accounts.

Missing budget figures in income and expenditure accounts.

Non-disclosure of losses.

Preparation of Financial statements is a stewardship role in which accountability for

application of resources entrusted to Accounting Officers is reported to the stakeholders.

Failure to present financial statements properly impairs interpretation and analysis of

entity performances. This is attributed to understaffing, lack of training, Low levels of

practical experience by clerks and non-adherence to the guidance provided in the Local

Governments’ Financial and Accounting Manual 2007 and other accounting standards.

Accounting Officers should liaise with responsible authorities to ensure the staffing gaps

are addressed and the necessary training undertaken.

20

4.5.3 Other Irregularities in Management of Schools and Tertiary Institutions

The analysis of 100 schools and tertiary Institutions out of the audited population of

277, revealed the following crosscutting issues;

1. Revenue shortfall

The analysis revealed revenue shortfall of UGX 3,045,515,542 in respect of 19

entities. The revenue shortfall implies that some planned activities were not

implemented. The shortfalls were attributed to Central Government budget cuts,

fees defaulters and shortfalls in student’s enrollments. There is need for the

Accounting Officers to continue liaising with the Ministry of Education and Sports and

other stakeholders to enhance revenue mobilization and collection.

2. Funds not accounted for

Audit revealed that funds amounting to UGX. 170,243,404 in 58 entities remained un

accounted for contrary to the Regulations. In the absence of accountabilities, it

becomes difficult to confirm that the funds were utilized for the intended purposes.

Delayed accountability of funds may lead to falsification of documents and loss of

funds. The delays to present accountabilities are attributed to laxity of the

Accounting Officers to enforce the internal controls regarding accountability. There is

need for the Accounting Officers to enforce controls relating to financial

management and accountability.

3. Noncompliance with PPDA Act and the Regulations

Out of the sample of 100 entities, audit observed noncompliance with the PPDA Act

and the Regulations in 52 schools and tertiary institutions. The most common

problems identified included the following;

Lack of consolidated procurement plans

Lack of prequalified list of suppliers

Failure to maintain procurement records

Application of inappropriate procurement methods with less competition with a

risk of higher costs.

21

Lack of procurement officers

Consequently, value for money may not have been achieved from the procurements

executed. These irregularities were attributed to lack of procurement Officers in the

school staff structure. The guidelines 4.1 and 4.2 of PPDA (Schools) define the

structure through which public procurement activiites are carried out in schools. It

requires that Schools with a budget not exceeding UGX.45 million shall employ one

procurement officer and schools with budget exceeding UGX.45 million shall employ

two procurement officers. However, the Accounting Officers explained that the

approved structure of the schools lacks the position of the procurement officer.

There is need for the Accounting Officers to engage the Ministry of Public Service,

Ministry of Local Governmnent and Ministry of Education and Sports in consultation

with the PPDA so that procurement officers are provided for in the school structure.

4. Noncompliance with the Income Tax Obligations

The analysis revealed that Taxes totaling to UGX 160,117,688 were not deducted in

the form of Pay As You Earn (PAYE) and Withholding Tax (WHT) in 15 schools. Non-

compliance with the tax law attracts fines and penalties from the tax body. This was

attributed to lack of awareness of the Income Tax law. There is a need by the

Accounting Officers to engage URA for sensitization on tax obligations to achieve tax

compliance.

5. Assets Management

Lack of Land Titles

It was observed that 33 schools representing 34% of the sampled schools and

Tertiary Institutions lacked land titles for the land where their properties are located.

This was attributed to the reluctance by the founding bodies to surrender ownership

of land and lack of funding to process land titles. This creates a risk of

encroachment and land disputes. There is need for the accounting officers to engage

the founder bodies and also prioritize funds allocation to secure the land titles.

22

Lack of Fixed Assets Register

The analysis revealed that 11 schools representing 11% of the sampled schools did

not maintain fixed assets registers. In the absence of fixed assets registers the

verification of the fixed assets is rendered difficult. This anormaly was attributed to

management laxity in ensuring that the details of the fixed assets owned by the

entity are properly recorded. The Accounting Officers are advised to ensure that the

Assets Registers are established.

Understaffing

The audit revealed high levels of vacant posts in 17 Schools. The levels ranged from

16% at Kasese Senior Secondary School to 88% in Uganda Technical College Kyema.

Understaffing hampers service delivery and may lead to poor academic performance.

The understaffing was attributed to the recruitment ban by the Ministry of Public and

the wage bill ceiling. Accounting Officers should engage the Ministry of Education,

Ministry of Public Service and the Education Service Commission to ensure that the

vacant posts are filled.

Governance

Audit observed that board meetings were not regularly convened to discuss strategic

matters affecting the institutions as required by the Regulations. In some instances,

the tenure of the boards had expired. The failure to convene the meetings regularly

was attributed to lack of funding. The Ministry of Education was also cited for

delaying to renew or appoint Board members. There is need for Accounting Officers

to prioritize and fund Board meetings and also follow up with the Ministry of

Education to ensure that Board members are appointed timely.

6. Lack of Standard Financial Reporting Framework

It was observed that there was no standard financial reporting framework for

secondary schools. This was attributed to lack of financial and accounting manual.

As a result, there was no uniform classification and coding of account balances,

format and presentation of financial statements. Section 29 (2) of Education (Board

of Governors) regulations require the board to prepare within three months financial

statements in the form approved by the Minister or district secretary for Education.

23

There is need for the Minister or District Secretary for Education to prescribe the

format of the financial statements for the Secondary Schools in consultation with the

Accountant General.

Inspection of the Schools and Tertiary Institutions Infrastructure

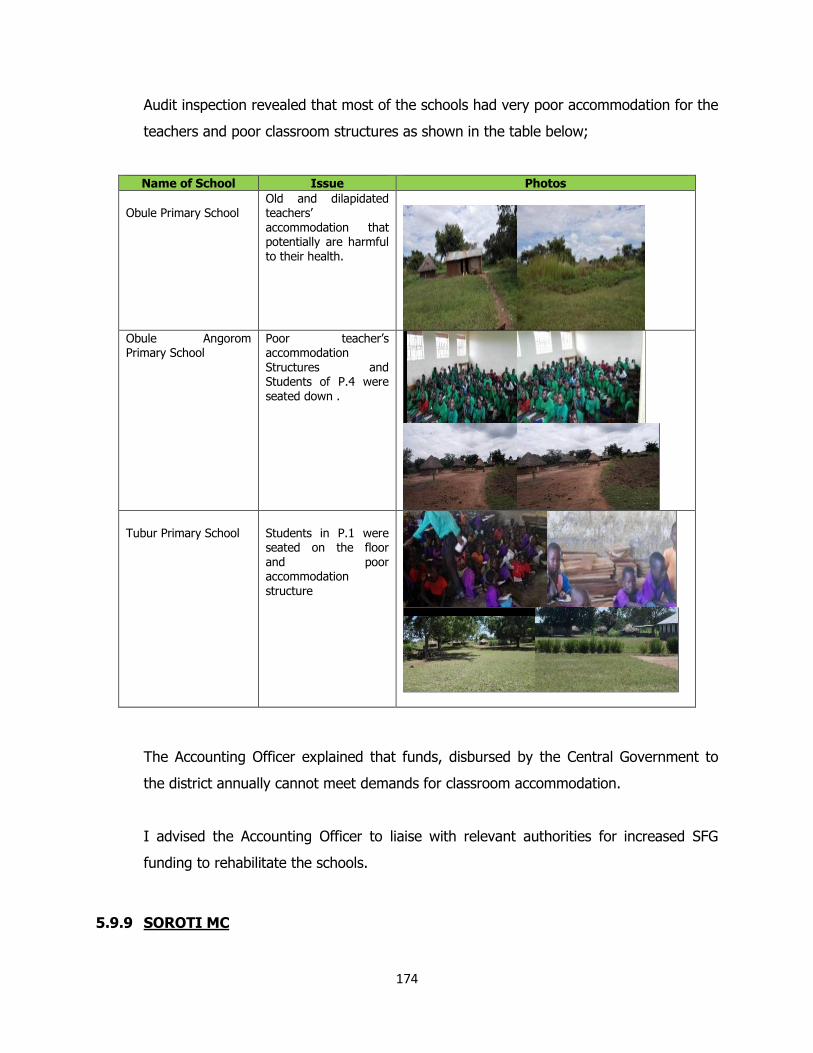

Audit inspection revealed inadequate classrooms, inadequate staff accommodation,

condemned structures with asbestos sheets, and lack of sick bays, inadequate

computer equipment, lack of laboratories and lack of lightening conductors. These

inadequacies impact adversely on the academic performance of the institutions. This

was attributed to lack of funds for infrastructure development. There is need for

Accounting Officers to liaise with the Ministry of Education and Ministry of Finance

for the requisite funding.

24

Table 8 Details of Significant Crossing Cutting Issues per OAG Branch Offices

Local

Revenue

Under-

collection

Irregular

levy of Dev't

tax

Procurement

anomaliesOverpay

ment of

salaries

unstafactory civil

worksUnderstaffing Lack of ICT policy Lack of Land Title Unspent balance

Un utilised

Capacity Building

and Infrastructure

Development Fund

under USMID

Others Type of Opinion

S.nos Entity

Breach of

Procurement

Procedures

Un-vouched

expenditure

Incompletel

y vouched

expenditure

Unaccounte

d for

Administrati

ve advances

Arua Branch

1 Adjumani DLG 10,609,950 0 0 0 Unqualified Para 5.1.1.1

2 Adjumani TC 86,523,128 0 0 0 0 Unqualified

3 Arua DLG 0 0 0 0 27,607,069 0 51% x Unqualified

4 Arua MC 0 0 0 0 0 489783196 46% 4,780,442,890 Unqualified 5.1.2.1

5 Koboko DLG 0 1,640,160,224 0 0 4,559,057 24,000,000 62% x Unqualified

6 Koboko TC 0 0 0 0 0 0 Unqualified

7 Maracha DLG 0 0 0 11,810,000 11,856,589 37,602,440 25% Unqualified 5.1.3.1

8 Maracha TC 0 0 0 0 0 0 52% Unqualified

9 Moyo DLG 0 11,722,603 0 45,815,000 25,044,000 0 29,381,000 Unqualified 5.1.4.1

10 Moyo TC 0 0 0 0 0 Unqualified 5.1.5.1

11 Nebbi DLG 76,931,170 0 0 11,873,000 0 49% Unqualified

12 Nebbi TC 61,012,973 0 0 0 0 Unqualified

13 Paidha TC 0 0 0 0 0 Unqualified

14 Pakwach TC 0 0 0 0 0 Unqualified

15 Yumbe DLG 103,310,117 0 0 0 985,496 430,233,040 x 2,021,502 Unqualified 5.1.6.1

16 Yumbe TC 86,523,128 0 0 0 0 Unqualified

17 Zombo DLG 0 0 0 12,894,750 0 467,436,259 x 89,456,000 Para 6.1.7.1 Unqualified 5.1.7

18 Zombo TC 0 0 0 5,916,000 0 58% x Unqualified

TOTALS 414,300,516 1,650,770,174 45,815,000 67,537,750 45,008,211 1,562,460,312 91,477,502 4,780,442,890

Other

SIGNIFICANT

ISSUES

Revenue Expenditure Internal control & Governance Asset management

Funds not accounted

25

EntityLocal Revenue

Under-collection

Irregular levy

of Dev't tax

Breach of

Procurement

Procedures

Inadequate

contracts

management

Unauthorised

contracts

variations

Incompletely

vouched

expenditure

Unaccounted

for

Administrative

advances

Missing Vouchers Payroll Unsatifactory

Civil works Payables

Understa

ffing %

Managem

ent of

ICT

Lack of

land

titles

Receivables Unspent

balances

LOW

ABSORPTION OF

USMID FONDSOther

issues Opinion

other

siginificant

issues

FORT PORTAL

Buliisa District 25,294,915 2,433,760,448 10,500,000 19,705,820 18,000,000 59% X 86,406,128 Unquallified

Buliisa Town Council X Qualified

Bundibugyo District 445,286,662 194,450,332 146,338,827 230,375,671 697,623,483 Unquallified 5.2.1.1

Bundibugyo Town Council 11,591,985 X Unquallified

Butunduzi Town Council 1,934,518 Unquallified

Bweyale Town Council X Unquallified 5.2.10

Fort Portal Municipal C 1,370,375,848 15,489,480 40% X 777,379,086 Unquallified

Fort Portal Regional RH Unquallified

Hima Town Council 4,081,600 Unquallified

Hoima District 13,132,000 18,820,850 6,500,000 137,417,000 50% Unquallified 5.2.3.1

Hoima Municipal Council 18,454,400 26,084,928 61% X X 6,341,624,951 Unquallified 5.2.4.1

Hoima Regional RH Unquallified

Kabarole District 608,104,970 X Unquallified

Kagadi Town Council 21,547,814 5,350,500 Unquallified 5.2.6.1

Kakumiro Town Council 77% Unquallified

Kamwenge District 2,730,000 823,821 27% X X Unquallified

Kamwenge Town Council 55,162,338 2,360,000 73% Unquallified

Kanara Town Council 57% Unquallified

Karago Town Council 64% X X Unquallified 5.2.2.1

Karugutu Town Council 87,672,401 65% Unquallified

Kasese District 38,448,323 5,000,000 365,437,300 26% 167,284,497 Unquallified

Kasese Municipal C 22,840,000 21,890,103 Unquallified 5.2.5.1

Katooke Town Council 1,047,500 13,563,401 46% X Unquallified 5.2.12

Katwe Kabatoro TC 69,315,876 200,351,881 Unquallified

Kibaale District 39% Unquallified

Kibaale Town Council 44,617,580 1,166,200 55% X Unquallified

Kibiito Town Council 3,212,000 66% Unquallified

Kibuku Town Council 3,410,000 Unquallified

Kigorobya Town Council 60% Unquallified

Kigumba Town Council 55% X Unquallified

Kijura Town Council 68% Unquallified

Kiko Town Council 12,923,264 55% Unquallified

Kiryandongo District 9,839,000 7,009,394 34,444,192 Unquallified 5.2.9

Kiryandongo Town Council 60% Unquallified

Kyarusozi Town Council 52% X Unquallified

Kyegegwa District 15,797,199 18,657,100 2,324,023 24% Unquallified 5.2.8.1

Kyegegwa Town Council 3,285,628 Unquallified

Kyenjojo District 12,735,000 14,583,900 17% Unquallified 5.2.11

Kyenjojo Town Council 39% Unquallified

Masindi District 71,256,267 41% X Unquallified

Masindi Municipal C 141,324,048 30,000,000 210,474,068 3,290,000 X Unquallified 5.2.7.1

Mpodwe Lhubiriha TC 26% Unquallified

Muhoro Town Council 11,657,387 59% Unquallified

Ntoroko District 34,000,000 49% X Unquallified 5.2.13

Nyahuka Town Council 72,473,072 X 288,894,036 Unquallified

Rubona Town Council Unquallified

Rwebisengo Town Council 1,250,000 Unquallified

Rwimi Town Council 75% X Unquallified

TOTAL - FORTPORTAL 2,203,694,151 79,540,437 3,119,768,626 210,474,068 215,998,146 51,794,400 276,318,825 239,199,694 792,202,445 600,009,488 115,352,053 15 - - 475,932,609 288,894,036 7,119,004,037 - -

REVENUE PROCUREMENT ANOMALIES FUNDS NOT ACCOUNTED FOR INTERNAL CONTROL AND GOVERNANCE ISSUES Assets management

26

Procurement anomalies Funds not accounted for

Understaffi

ng Assest Management Unspent balances

Under absorption of

funds under USMID Types of Opinion

OTHER

SIGNIFICANT

Entity

Under collection

local revenue

Irregular levy of

Development tax

Lack of

Procuremen

t files

Breach of

Procuremen

t

Procedures

Inadequate

contracts

manageme

nt

Unauthoris

ed

contracts

variations

Un-vouched

expenditure

Incompletel

y vouched

expenditure

Unaccounted for

Administrative

advances

Missing

Vouchers

Overpayment

of salaries Lack of land titlesReceivables

8

1 ADUKU TC 67 X Unqual i fied

2 AGAGO DLG 62,693,485 25,449,200 66 Unqual i fied 5.3.2

3 AGAGO TC X Unqual i fied

4 ALEBTONG DLG 57 X Unqual i fied 5.3.3

5 ALEBTONG TC 77 X Unqual i fied

6 AMOLATAR DLG 27,224,132 39,929,500 3,531,125 47 Unqual i fied

7 AMOLATAR TC 77 Unqual i fied

8 AMURU DLG 50,029,306 83,166,346 125,942,346 Qual i fied

9 AMURU TC Unqual i fied

10 AMURU TC Unqual i fied

11 ANAKA TC Unqual i fied

12 APAC DLG 85,520,700 54.450,679 1,765,395,052 Qual i fied 5.3.1

13 APAC TC 77 Unqual i fied

14 AYER TC X Unqual i fied

15 DOKOLO DLG 14,186,821 22,979,000 Unqual i fied

16 DOKOLO TC Unqual i fied

17 GULU DLG 330,564,366 210,883,447 Unqual i fied 5.3.4

18 GULU MC 18,867,000 44 6,365,144,394 14,505,711,262 Unqual i fied

19 GULU RRH Unqual i fied

20 KALONG TC 50 X Unqual i fied

21 KITGUM DLG Unqual i fied 5.3.6

22 KITGUM TC Unqual i fied

23 KOLE DLG X Unqual i fied 5.3.5

24 LAMWO DLG 72,381,163 37,218,100 Unqual i fied 5.3.7

25 LAMWO TC X Unqual i fied

26 LIRA DLG 32,955,855 Unqual i fied 5.3.8

27 LIRA MC 6,773,520,311 Unqual i fied

28 LIRA RRH Unqual i fied

29 NAMASALE TC Unqual i fied

30 NWOYA DLG 37,975,969 66 Unqual i fied

31 OTUKE DLG 25,381,700 20 X Unqual i fied

32 OTUKE TC 69 Unqual i fied

33 OYAM TC Unqual i fied

34 PADER DLG 35,236,426 67,849,000 32,334,357 Qual i fied 5.3.9

35 PADER TC Unqual i fied

36 PADIBE TC 17,220,254 X Unqual i fied

37 PATONGO TC Unqual i fied

TOTAL 347,784,620 261,751,333 444,336,515 405,647,130 6,365,144,394 1,765,395,052 21,279,231,573

Revenue

27

Lack of

Procuremen

t files

Breach of

Procuremen

t Procedures

Inadequate

contracts

managemen

t

Unauth

orised

contrac

ts

variatio

ns

Un-

vouche

d

expendi

ture

Incomplete

ly vouched

expenditur

e

Unaccounted

for

Administrativ

e advances

Missing

Vouche

rs

Lack

of land

titles

ReceivablesUnspent

balances

Low absorption

of funds under

USMID project

OPINION

BUGEMBE TC 137,886,844 4,017,250 57.50% X Unqualifed

BUGIRI DLG 490, 392,030 5.4.1.1 Unqualifed

BUGIRI TC 119,645,710 47% 13,301,500 Unqualifed

BUSEMBATIA TC 13,535,480 X Unqualifed

BUYENDE DLG 5.4.2 Unqualifed

BUWENGE TC X Unqualifed

BUYENDE TC 18,969,463 46% 5,658,463 X Unqualifed

JINJA DLG Unqualifed

JINJA MC 1,846,307,177 815,181,449 X 2,707,996,392 2,750,777,445 2,750,777,445 Unqualifed

IGANGA DLG Unqualifed

IGANGA MC 37,380,748 13,733,000 47% 452,957,716 X 5.4.3 Unqualifed

JINJA DLG 5.4.4 Unqualifed

KAKIRA TC 47% X 37,298,200 5.4.5 Unqualifed

KALIRO DLG X Unqualifed

KALRO TC 262,332,542 58,340,453 Unqualifed

KAMULI DLG Unqualifed

KAMULI TC 33%) 25,994,540 X 56,754,080 5.4.6 Unqualifed

KAYUNGA DLG 50,214,828 Unqualifed

KAYUNGA TC 14,417,402 X 5.4.7 Unqualifed

LUGAZI TC 417,568,212 X 374, 832,206 5.4.8 Unqualifed

LUUKA DLG 252,703,836 124,078,436 2,841,000 X Unqualifed

LUUKA TC 131,685,444 87% X 5.4.9 Unqualifed

MAYUGE DLG 8,971,108,256 7,684,723 X 5.4.10 Unqualifed

MAYUGE TC 61, 555,274 4,782,000 X 16,157,164 5.4.11 Unqualifed

NAMAYINGO DLG 4,537,004 Unqualifed

NAMAYINGO TC X 5.4.13 Unqualifed

NAMUTUMBA DLG 25,072,231 27% X Unqualifed

NAMUTUMBA TC 71.70% X 9,657,800 5.4.12 Unqualifed