Loan and Advance Final

51

“LOAN AND ADVANCE MANGEMENT IN GOPINATH PATIL PARSIK JANATA SAHAKARI BANK LTD” IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR MASTER IN MANAGEMENT STUDIES (MMS) 2013-2015 STUDENT NAME: MANGESH SHANKAR SONAWANE ROLL NO : C22 SUBMITTED TO DR. V. N. BEDEKAR INSTITUTE OF MANAGEMENT STUDIES, THANE

-

Upload

mangesh-sonawane -

Category

Documents

-

view

140 -

download

1

Transcript of Loan and Advance Final

“LOAN AND ADVANCE MANGEMENT IN GOPINATH PATIL

PARSIK JANATA SAHAKARI BANK LTD”

IN PARTIAL FULFILLMENT OF THE REQUIREMENTS

FOR

MASTER IN MANAGEMENT STUDIES (MMS)

2013-2015

STUDENT NAME: MANGESH SHANKAR SONAWANE

ROLL NO : C22

SUBMITTED TO

DR. V. N. BEDEKAR INSTITUTE OF MANAGEMENT STUDIES,

THANE

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

2

STATEMENT BY THE CANDIDATE

I wish to state that the work embodied in this Project titled Loan &

Advances Management in Gopinath Patil Parsik Janata Sahakari Bank Ltd.

forms my own contribution to management. Wherever references have been

made to intellectual properties of any individual / Institution / Government / Private /

Public Bodies / Universities, research paper, text books, reference books, research

monographs, archives of newspapers, corporate, individuals, business / Government

and any other source of intellectual properties viz., speeches, quotations, conference

proceedings, extracts from the website, working paper, seminal work et al, they have

been clearly indicated, duly acknowledged and included in the Bibliography.

___________________

Date Signature of Student

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

3

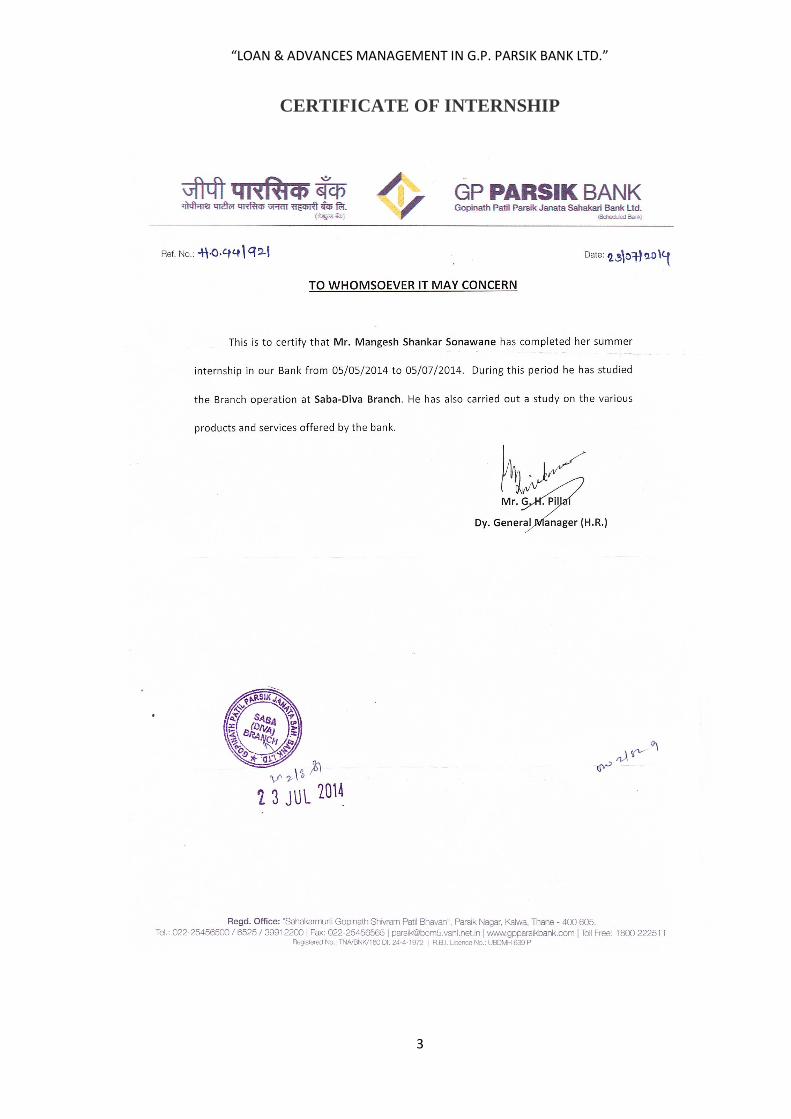

CERTIFICATE OF INTERNSHIP

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

4

ACKNOWLEDGEMENT

I would like to take this opportunity to express my deep and sincere gratitude

to “Gopinath Patil Parsik Janata Sahakari Bank Ltd.” Who gave me a chance to

show my capability and allowed me to carry out a project guide under Branch

Manager Mr. GAJANAN BABU KOLI.

I present my heartfelt gratitude towards Prof. Smita Jape for giving me this

opportunity to wide my horizons of understanding by giving me in the project on

“Loan & Advance Management in Gopinath Patil Parsik Janata Sahakari Bank Ltd.”

By working on this project, I got an opportunity to learn many aspects of

banking sector. The credit also goes to the timely guidance and support given by the

other banking staff Sr.Clerk Sanjay Thakur,Cashier Faisal Cheulkar and

Assistant Manager Premnath Patil who has helped me in enhancing my interest

and understanding of the intricacies involved with the subject.

Last, but not the least, I would like to thank everybody who has helped me in

the successful completion of the project. The whole experience was gratifying,

especially in terms of knowledge and information .

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

5

TABLE OF CONTENT

EXECUTIVE SUMMARY ............................................................................................... 8

CHAPTER 1: INDUSTRY PROFILE .............................................................................. 9

1.1 WHAT IS BANKING? .................................................................................... 9

1.2 STANDARD ACTIVITIES OF BANK ......................................................... 10

1.3 REVENUE GENERATION .......................................................................... 10

CHAPTER 2 : BANKING IN INDIA ............................................................................ 11

2.1 NATIONALIZATION .................................................................................. 12

2.2 LIBERALIZATION ...................................................................................... 12

2.3 INDIAN BANKING INDUSTRY ................................................................. 13

CHAPTER 3 : COMPANY PROFILE ........................................................................... 15

3.1 GOPINATH PATIL PARSIK JANATA SAHAKARI BANK LTD. ................... 15

3.2 HISTORY ..................................................................................................... 16

3.3 NATURE OF THE BUSINESS CARRIED ................................................... 17

3.4 VISION, MISSION AND COMPANY POLICY........................................... 18

3.5 AREA OF OPERATION .............................................................................. 20

3.6 OWNERSHIP PATTERNS ........................................................................... 20

CHAPTER 4 : SWOT ANALYSIS OF G.P. PARSIK BANK ..................................... 21

4.1 STRENGTH .............................................................................................................. 21

4.2 WEAKNESS ................................................................................................. 21

4.3 OPPORTUNITY ........................................................................................... 21

4.4 THREATS .................................................................................................... 21

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

6

CHAPTER 5 : FINANCIAL STATEMENT FOR THE YEAR ENDED 31st MAR,14. ........ 22

5.1 BACKGROUND .......................................................................................... 22

5.2 BASIS OF PREPARATION ......................................................................... 22

5.3 USE OF ESTIMATES ................................................................................. 22

CHAPTER 6 : LOAN AND ADVANCE MANAGEMENT ....................................... 29

6.1 TYPES OF LOAN ........................................................................................ 29

6.2 LOAN AND ADVANCE ............................................................................... 37

6.3 IMPORTANT POINT OF LOANS AND ADVANCES ................................. 40

CHAPTER 7 : RECOVERY OF LOANS ...................................................................... 41

7.1 MECHANISM .............................................................................................. 41

7.2 MEASURES BY BANK FOR RECOVERY DUES ...................................... 42

CHAPTER NO 8 : LITERATURE REVIEW ................................................................ 44

CHAPTER 9 : METHODOLOGY ................................................................................. 47

9.1 SOURCE OF PRIMARY AND SECONDRY DATA ................................... 47

9.2 LIMITATIONS ............................................................................................. 47

9.3 OBJECTIVES OF THE STUDY ................................................................... 48

9.4 SCOPE OF THE STUDY.............................................................................. 48

CHAPTER 10 : RECOMMENDATION AND SUGGESTIONS ................................ 49

CHAPTER 11 : CONCLUSION ..................................................................................... 50

CHAPTER 12 : REFERENCS ........................................................................................ 51

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

7

TABLE OF INTEREST RATE

TABLE 1 DEPRICIATION ................................................................................... 24

TABLE 2 HOUSING LOAN ................................................................................. 29

TABLE 3 HOUSING REPAIRS AND RENOVATION ........................................ 30

TABLE 4 CAR LOAN .......................................................................................... 31

TABLE 5 ARTICLE LOAN ................................................................................... 31

TABLE 6 GROUP LOAN ..................................................................................... 32

TABLE 7 MICRO AND SME ............................................................................... 32

TABLE 8 CASH CREDIT ..................................................................................... 33

TABLE 9 T.U.F ..................................................................................................... 34

TABLE 10 CASH CREDIT FACILITY .................................................................. 35

TABLE 11 EDUCATION LOAN ............................................................................ 35

TABLE 12 PROFESSIONAL LOAN ...................................................................... 36

TABLE 13 GOLD LOAN ....................................................................................... 36

TABLE 14 LOAN AGAINST TERM DEPOSIT ..................................................... 37

TABLE 15 YEARS PERFORMANCE (TABLE AND GRAPH)............................. 38

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

8

EXECUTIVE SUMMARY

This report is contains the introduction to Banks, which includes past, present

and future of banks and challenges for banking industry in future. Banks plays the

most important role in providing various services. Earlier the banks were engaged in

accepting and lending money. But in the recent past the scope of services provided by

the banks has changed. The growing competition requires prompt and efficient

services to the customers at reasonable time and cost. These days bank aim to provide

maximum satisfaction and quick service to their customers.

The next part of the report consists of the knowledge about the cooperative

banks in India. It includes history of cooperative bank in indianite features and service

provided by it in rural and urban sector. The structure of cooperative bank in India is

also includes in it.

Then a brief introduction of Gopinath Patil Parsik Janata Sahakari Bank

Ltd. comes in next part of the report which consist the history, management team and

objective made by Chairman MR. Ranjit Patil. The financial position of the bank as

per data of 2014 also includes in this part.

Then the meaning of certain terminology includes in this report .these terms

are related with the topic for example. Cash credit, lease, secured loan etc. the

objective of this section is only to make aware about certain terminology used by

bank regarding loan facility.

The next section of report i.e. training methodology consist title of objective

and limitation of study etc. this section basically giving the outline of the report.

Next section provides information about the loan and credit facility provided

by bank. This section consist various loans provided by bank the detail regarding

those loans, procedure to recover it, actual position of bank in loan area, and

recommendation and the various proposals that the Cooperative bank could apply for

maintaining its position in the region and to face future challenges and the suggestions

for the improvement.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

9

CHAPTER 1: INDUSTRY PROFILE

1.1 WHAT IS BANKING?

Banking is the business of accepting deposits of money from public For the

purpose of lending and investment. These deposits can have a distinct feature like

being withdrawn able by cheques, which no other financial institution can offer. In

Addition, banks also various financial services, which include:

● The Issue of demand draft & traveler‟s cheques.

● Credit cards / Debit cards

● Collection of cheques, bill of exchange.

● Locker deposit System

● Custodian services.

● Investment and Insurance Services.

The business of banking is highly regulated since banks deal with money

offered to them by the public and ensuring the safety of this public money is one of

the prime responsibilities of any bank. That is why banks are expected to be prudent

in their leading and investment activities. Every bank has a compliance department,

which is responsible to ensure that all the services offered by the bank, and the

processes followed are in compliance with the local regulations and the Bank‟s

corporate policy. The major regulations and act govern the banking business are: -

● Banking Regulation Act, 1949

● Foreign Exchange Management Act, 1999

● Indian Contract Act, 1872

● Negotiable Instruments Act, 1881

Bank lends money either for productive purposes to individual, firms, and

Corporate etc. for buying house property, cars and other consumer durables and for

investment Purposes to individuals and the others. However, banks do not finance any

Speculative activity. Lending is risk taking. The depositors of banks are also assured

of safety of their money by deploying some percentage of deposit in statutory

Reserves like SLR & CLR.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

10

1.2 STANDARD ACTIVITIES OF BANK

Banks act as payment agents by conducting checking or current accounts for

customers, paying cheques drawn by customers on the bank, and collecting cheques

deposited to customers' current accounts. Banks also enable customer payments via

other payment methods such as telegraphic transfer, and ATM.

Banks borrow money by accepting funds deposited on current accounts, by accepting

term deposits, and by issuing debt securities such as banknotes and bonds. Banks lend

money by making advances to customers on current accounts, by making installment

loans, and by investing in marketable debt securities and other forms of money

lending.

Banks provide almost all payment services, and a bank account is considered

indispensable by most businesses, individuals and governments. Non-banks that

provide payment services such as remittance companies are not normally considered

an adequate substitute for having a bank account.

Banks borrow most funds from households and non-financial businesses, and

lend most funds to households and non-financial businesses, but non-bank lenders

provide a significant and in many cases adequate substitute for bank loans, and money

market funds, cash management trusts and other non-bank financial institutions in

many cases provide an adequate substitute to banks for lending savings too.

1.3 REVENUE GENERATION

A bank can generate revenue in a variety of different ways including interest,

transaction fees and financial advice. The main method is via charging interest on the

capital it lends out to customers. The bank profits from the differential between the

level of interest it pays for deposits and other sources of funds, and the level of

interest it charges in its lending activities.

This difference is referred to as the spread between the cost of funds and the

loan interest rate. Historically, profitability from lending activities has been cyclical

and dependent on the needs and strengths of loan customers and the stage of the

economic cycle. Fees and financial advice constitute a more stable revenue stream

and banks have therefore placed more emphasis on these revenue lines to smooth their

financial performance.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

11

CHAPTER 2 : BANKING IN INDIA

Banking means accepting for the purpose of landing or investment of deposits

of money from the public repayable on demand or otherwise one withdraw able by

cheque, draft or otherwise.

Banking in India has its origin as early as the Vedic period. It is believed that

the transaction From money lending to money banking must have occurred even

before Manu, the great Hindu Jurist, who has devoted a section of his work to

deposits and advances and laid down the rules relating to rate of interest, During

Mugal Period, the native bankers played a very important role in lending money and

finance foreign trade and commerce.

During the days of the east- India Company, it was the turn of the agency

house to carry on the banking business the general bank of India was the first joint

stock bank to be established in the year 1786. The others that followed were the Bank

of Hindustan and the Bengal Bank. The Bank of Hindustanis reported to have

continued till 1906 while the other two failed in the meantime.

In the first half of the 19th century the east-India company established three

banks, the Bank of Bengal in1809, the Bank of Bombay in 1840 and the banks of

Madras in 1843.These three banks are also known as the presidency banks were

amalgamated in 1920 and a new Bank ± the imperial bank of India established ion

27th January 1921. With the passing of the state bank act 1955 the under taking of the

imperial Bank of India is taken over by the newly constituted the state bank of India.

The Indian banking sector has come a long way since independence, more so

since the nationalization of 14 major banks in 1969 and 6 banks in 1980. There has

been a substantial increase in banking business over the years, captured by the ratio of

banking business (credit plus deposits) to GDP. The test for structural breaks

suggested three breaks in the series of ratio of banking business to GDP, which

coincided with the major changes in the banking landscape viz., bank nationalization

of 1969, initiation of economic and banking sector reforms in the early 1990s, and the

high growth phase of the 2000 Over the years, the reach of banking has widened

significantly to include relatively under-banked regions, particularly in rural areas.

Commercial bank credit as per cent of GDP picked up steadily from 5.8 per cent in

1951 to 56.5 per cent by 2012. The population per bank branch came down from

64,000 in 1969 to 12,300 in 2012 (RBI, 2013).

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

12

2.1 NATIONALIZATION

The GOI issued an ordinance and nationalized the 14 largest commercial

banks with effect from the midnight of July 19, 1969. Jayaprakash Narayan, a national

leader of India, described the step as a "masterstroke of political sagacity." Within two

weeks of the issue of the ordinance, the Parliament passed the Banking Companies

(Acquisition and Transfer of Undertaking) Bill, and it received the presidential

approval on August 1969.

A second dose of nationalization of 6 more commercial banks followed in

1980. The stated reason for the nationalization was to give the government more

control of credit delivery. With the second dose of nationalization, the GOI controlled

around 91% of the banking business of India. Later on, in the year 1993, the

government merged New Bank of India with Punjab National Bank. It was the only

merger between nationalized banks and resulted in there reduction of the number of

nationalized banks from 20 to 19. After this, until the 1990s, the nationalized banks

grew at a pace of around 4%, closer to the average growth rate of the Indian economy.

2.2 LIBERALIZATION

In the early 1990s, the then Narsimha Rao government embarked on a policy

of liberalization, licensing a small number of private banks. These came to be known

as New Generation tech-savvy banks, and included Global Trust Bank (the first of

such new generation banks to be setup), which later amalgamated with Oriental Bank

of Commerce, Axis Bank(earlier as UTI Bank), ICICI Bank and HDFC Bank. This

move, along with the rapid growth in the economy of India, revitalized the banking

sector in India, which has seen rapid growth with strong contribution from all the

three sectors of banks, namely, government banks, private banks and foreign banks.

The next stage for the Indian banking has been set up with the proposed

relaxation in the norms for Foreign Direct Investment, where all Foreign Investors in

banks may be given voting rights which could exceed the present cap of 10%, at

present it has gone up to 74% with some restrictions. The new policy shook the

Banking sector in India completely. Bankers, till this time, were used to the 4-6-4

method (Borrow at 4%; Lend at 6%; Go home at 4) of functioning. The new wave

ushered in a modern outlook and tech-savvy methods of working for traditional-

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

13

banks. All this led to the retail boom in India. People not just demanded more from

their banks but also received more.

Currently (2007), banking in India is generally fairly mature in terms of

supply, product range and reach-even though reach in rural India still remains a

challenge for the private sector and foreign banks. In terms of quality of assets and

capital adequacy, Indian banks are considered to have clean, strong and transparent

balance sheets relative to other banks in comparable economies in its region. The

Reserve Bank of India is an autonomous body, with minimal pressure from the

government. The stated policy of the Bank on the Indian Rupee is to manage volatility

but without any fixed exchange rate-and this has mostly been true.

With the growth in the Indian economy expected to be strong for quite some

time -especially in its services sector-the demand for banking services, especially

retail banking, mortgages and investment services are expected to be strong. One may

also expect M &A‟s, takeovers, and asset sales.

In March 2006, the Reserve Bank of India allowed Warburg Pinups to

increase its stake in Kotak Mahindra Bank (a private sector bank) to 10%. This is the

first time an investor has been allowed to hold more than 5% in a private sector bank

since the RBI announced norm sin 2005 that any stake exceeding 5% in the private

sector banks would need to be vetted by them.

In the Indian Banking Industry some of the Private Sector Banks operating are

IDBI Bank, INGVyasa Bank, SBI Commercial and International Bank Ltd, Bank of

Rajasthan Ltd. and banks from the Public Sector include Punjab National bank,

Vijaya Bank, UCO Bank, Oriental Bank, Allahabad Bank among others. ANZ

Grindlays Bank, ABN-AMRO Bank, American Express Bank Ltd, Citibank are some

of the foreign banks operating in the Indian Banking Industry.

2.3 INDIAN BANKING INDUSTRY

The Indian Banking system has the Reserve Bank of India (RBI) as the apex

body for all relating to the banking system. It is the Combination of Banks of India

and bankers to all others banks as well.

The Indian Banking industry, which is governed by the Banking Regulation

Act of India, 1949 it can be broadly classified into two major categories, non -

scheduled banks and scheduled banks.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

14

I) Schedule Banks

These banks must have paid-up capital and reserve of mot less than

Rs.50,00,000. They must satisfy the RBI than its affairs are mot conducted in a

manner detrimental to the interests of its depositors. These are further classified as

follow:

● State co-operative Banks

● Commercial Banks

Scheduled banks comprise commercial banks and the co-operative banks. In

terms of ownership, commercial banks can be further grouped into nationalized

banks, the State Bank of India and its group banks, regional rural banks and private

sector banks (the old/ new domestic and foreign). These banks have over

67,000 branches spread across the country in every city and villages of all nook and

corners of the land.

II) Non-Schedule Banks

These are banks, which are not included in the second schedule of the Banking

Regulations Act, 1965. It means they do not satisfy the conditions laid down by that

schedule. They are further classified as back:

● Central co-operative banks and primary credit societies

● Commercial Banks

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

15

CHAPTER 3 : COMPANY PROFILE

3.1 GOPINATH PATIL PARSIK JANATA SAHAKARI BANK LTD.

Gopinath Patil Parsik Jananta Sahakari Bank Ltd. (GPPJSB Ltd.) Founded on

21st May 1972, in a remote village in Kalwa (Thane District, Maharashtra), Gopinath

Patil Parsik Janata Sahakari Bank enjoyed tremendous patronage right since the

inception. It established under the leadership of Shri. Gopinath Shivram Patil and

other founding directors, the bank flourished and expanded its reach to Thane, Navi

Mumbai, Pune and Nashik. With an inspiring deposit base more than Rs 1100 Crores,

Gopinath Patil Parsik Janata Sahakari Bank is riding high on customer satisfaction

and trust. What is even more heartening is that the bank has helped many to meet their

financial needs.

They are currently operating through 46 fully-equipped branches and

4 Extension Counters. Gopinath Patil Parsik Janata Sahakari Bank is getting ready for

the next phase of rapid expansion.

Milestones

Scheduled Bank status on 30th January, 1998.

Ranked as the “The Best Urban Bank" among the 400 Urban Banks in

Maharashtra. (Three Times Award)

Only bank in Maharashtra with low/negligible rate of defaulters

CSR (Corporate Social Responsibility) Initiatives

Financial assistance to various Charitable Trust, Education of students

(member‟s), medical help to members

Nature conservation - plantation programmes in and around Thane

Closely associated with a Charitable Trust managing an Agricultural College

(Diploma), Secondary School and a Vruddhashram (Old-Age Home).

Recently, the committee has given the Founder's name to the Bank

"GOPINATH PATIL PARSIK JANATA SAHAKARI BANK"

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

16

3.2 HISTORY

In the year 1971 the Government of Maharashtra acquired all agricultural land

of 68 villages of Thane-Belapur belt in Thane district of Maharashtra, for the purpose

of setting up a new city i.e. “New Bombay”. Acquisition of land for New Bombay

project means compulsorily depriving several thousands of people of their means of

livelihood. Though Government was paying them money as compensation, but they

were parted away from their land, the only means of livelihood for them.

To equip the project affected persons and their family members with strength

and ability, to survive with new urban means of livelihood, it was necessary to

provide them financial assistance. With a view to provide financial assistance,

generate employment and means of livelihood, Late Shri.Gopinathdada Shivram Patil

along with a group of youngsters of Kalwa village took the initiative of formation of

Urban Co-operative Bank. These groups of youngsters were successfully running a

Consumer Co-operative Society by name “Kalwa Consumer Co - operative Society”.

This group of youngsters, on their study-tour to Western Maharashtra, for study of co-

operation, was fascinated by network and growth of cooperative societies and the role

played by Urban Cooperative Banks in the development of that region.

After the study tour, Late Shri.Gopinathdada Shivram Patil along with a group

of youngsters called a meeting of residents from Kalwa and nearby villages and took

the first step for the formation of the bank in December 1971 by collecting Share

Money. Collection of share money was the most difficult task at that time. In a village

where there were no banking facilities available, these youngsters started collecting

Rs. 50/- as contribution towards share capital by going door to door. In the year 1971

Rs.50/- was also a substantial amount and it took lot of efforts and hardship to collect

the required numbers of members.

The registration of “Parsik Janata Sahakari Bank Ltd.” was approved by Co-

operative Department in the month of April, 1972, with registration number

TNA/BNK/160 dated 24th April, 1972. The first branch office at Kalwa Naka was

opened on 21st May, 1972.The bank was named as “Parsik” because active

jurisdiction of bank was the west side area of Parsik Hill, which has range from

Kalwa to Belapur (the famous Parsik Railway Tunnel is situated in the same range).

“Parsik” also means Parshwanath (Lord Shiva), whose temple was existed on the hill

as per history. Bank achieved status of “Scheduled Bank” on 30th

January,1998.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

17

As an impact of the Trust shown in Late Shri. Gopinathdada Shivram Patil, an

amount of Rs.1 lac was collected within 3 months. For the first three to four years,

Bank was trying to maintain its existing Deposit but with consistent efforts of Late

Shri. Gopinathdada Shivram Patil and his team, Bank accelerated its pace of growth

in the forthcoming years. The Consistent and Dedicated efforts of Late Shri.

Gopinathdada Shivram Patil and his team brought dignity to the Bank in the form of

Padmabhushan Vasantdada Patil Puraskar continuously for 1995-96, 1996-97, 1997-

98 which was awarded by Maharashtra State Co-operative Banks Association in the

Mumbai Division. As a token of acknowledgment for Generosity, Consistency,

Dedication and Sacrifice made for the growth of Co-operation by Late Shri.

Gopinathdada Shivram Patil, Thane Municipal Corporation awarded him with the

most coveted THANE BHUSAN PURASKAR which is another feather in the Bank‟s

Reputation. Bank has been catering the needs of the society through its well-equipped

42 Branches spread in Thane, Mumbai, Navi Mumbai, Pune, Nashik, & Ichalkaranji

(Kolhapur). It has been permitted to extend its area of operation throughout the state

of Maharashtra. Bank is gradually progressing on the path of Consistency and

Dedication with Ethics, Principles and Discipline developed by Late Shri Gopinath

Shivram Patil for achieving the ultimate goal of Customer Satisfaction. Bank

equipped with CBS, NEFT/RTGS is in process for providing Net Banking, Mobile

Banking, Debit Card. Bank is gearing itself with increasing number of Branches

throughout Maharashtra in the near future.

3.3 NATURE OF THE BUSINESS CARRIED

Bank is an institution which deals in money and credit. It accepts deposits

from the public and grants loans and advances to those who are in need of funds for

various purposes. Banking is an activity which involves acceptance of deposits for the

purpose of lending or investing. In addition to accepting deposits and lending funds,

banking also involves providing various other services along with its main banking

activity. These are mainly agency services, but include several general services.

A banker is one who undertakes banking activities, accepting deposits and lending

money for different purposes. The Banking Regulation Act, 1949 defines banking as

an activity of accepting funds from the public for the purpose of lending or

investment.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

18

The essential features of banking activities are as follows -

i) Accepting deposits from public;

ii) Lending or investment of such deposits;

iii) Incidental to the activities of accepting deposits for lending or investing, banks

undertake activities like -

a) Promoting and mobilizing savings of the public;

b) Providing funds to trade and industry by way of discounting bills, overdraft, cash

credit facility, and transfer of funds from one place to another;

c) Providing agency services to customers, such as collection of bills, payment of

insurance premium, purchase and sale of securities, etc., and other general services,

such as issue

Of travelers‟ cheques, debit card locker facility, etc; Money deposited with the bank is

assured as far as its safety is concerned. Further the depositor is allowed to withdraw

it whenever required. Banks allow interest on deposits. Such interest helps in the

growth of funds deposited with the bank. Thus the rate of interest provided on

deposits acts as an incentive to the depositors.

3.4 VISION, MISSION AND COMPANY POLICY

I.VISION

To become the most respected Bank in the financial services space in India.

To emerge as a single window for meeting the financial and developmental needs of

the MSME sector to make it strong, vibrant and globally competitive, to position

Good Brand as the preferred and customer - friendly institution and for enhancement

of share - holder wealth and highest corporate values through modern technology

platform.

II.MISSION

To be among the pillars of the banking industry, a strong and resilient

institution committed to lasting partnerships with and superior service to our clients;

the well-being of our employees; fair return on equity for our shareholders; and

national growth and development as financial catalyst.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

19

TO OUR CLIENTS:

We shall always seek and preserve the trust and confidence of our clients and

customers. We shall offer a wide range of products that will meet the customer's life

aspirations. And we shall render excellent service to customers, treating them not only

as customers but as people.

TO OUR EMPLOYEES

Realizing the value of our employees in achieving our goals, we will

recognize their contribution to the efficient management of our institution. We shall

promote productivity and a sense of belonging.

TO OUR COMPANY

We shall pursue strength in our balance sheet and profitability in our

performance. Cognizant of the demands of our exacting responsibility, we commit,

without reservation, to apply the highest standards of probity, prudence, and

professionalism in our tasks.

TO OUR COUNTRY

We acknowledge our responsibility to our country and commit to mobilize our

resources in the interest of the economy. Recognizing the potential of our countryside,

we shall constantly endeavor to expand our reach and distribution network to make

meaningful contribution to entrepreneurial ventures.

III.COMPANY POLICY

Remain largely a retail focused organization, driving stickiness through

Knowledge and quality service.

Target the micro, small and medium enterprises mushrooming across the

country through a cluster approach for lending business.

Growth with focused team of dynamic professionals.

Fairness in all our dealings – employees, customers, vendors and shareholders

all included.

Transparency in what we do – and in how and why we do it.

Service orientation is our core value, imbibed by all sales as well as support

teams.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

20

3.5 AREA OF OPERATION

The legal transactions executed by a bank in its various bank departments and

local branches, and they ensure all transactions run smoothly. Depending on the focus

and size of the bank branch.Banking operations managers also concentrate on

improving the bank‟s customer service record and intervening when problems arise

Such as:

Providing loans,

Mortgages and investments,

Deposit scheme,

Services

No. of Shareholder 72515

No. of Branches 46

3.6 OWNERSHIP PATTERNS

Schedule Banks

These banks must have paid-up capital and reserve of mot less than

Rs.50,00,000. They must satisfy the RBI than its affairs are mot conducted in a

manner detrimental to the interests of its depositors. These are further classified as

follow:

● State co-operative Banks

● Commercial Banks

Scheduled banks comprise commercial banks and the co-operative banks. In

terms of ownership, commercial banks can be further grouped into nationalized

banks, the State Bank of India and its group banks, regional rural banks and private

sector banks (the old/ new domestic and foreign). These banks have over

67,000 branches spread across the country in every city and villages of all nook and

corners of the land.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

21

CHAPTER 4 : SWOT ANALYSIS OF G.P. PARSIK BANK

4.1 STRENGTH

Public sector undertaking. Thus has government backing

In This area for more than 42 years. Thus, Expertise in this field.

Increasing profit over the years.

High connectivity to common man in some parts of the country.

4.2 WEAKNESS

Risk adverse

Advertising is less thus weak brand Recognition as compared to major players.

Increasing NPA.

Lack of Training to employee.

Ignorance Marketing.

4.3 OPPORTUNITY

Rural areas.

Installation of more ATMs.

Small enterprise banking improved urban retail banking.

Becoming multi state bank.

Start Mobile and Internet Banking

4.4 THREATS

Highly competitive environment.

New bank licenses.

Economic Slowdown

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

22

CHAPTER 5 : FINANCIAL STATEMENT FOR THE YEAR ENDED 31st

MAR,14.

5.1 BACKGROUND

Gopinath Patil Parsik Janata Sahakari Bank Ltd. is a scheduled co-operative

bank providing wide range of banking and financial services through 46 branches. It

is governed by the Banking Regulation Act, 1949 (as applicable to co-operative

societies / banks) and the Maharashtra Co-operative Societies Act, 1960 and the rules

framed there under.

5.2 BASIS OF PREPARATION

The financial statements have been prepared following the going concern

concept, on an accrual basis, unless otherwise stated, under the historical cost

convention, except for building acquired on merger with Ichalkaranji Mahila Sahakari

Bank Ltd, Ichalkaranji which is carried at revalued amount, and comply with the

generally accepted accounting principles in India, statutory requirements under the

Banking Regulation Act, 1949 & Maharashtra State Co-operative Societies Act, 1960,

circulars and guidelines issued by the Reserve Bank of India (RBI) from time to time,

the accounting standards issued by the Institute of Chartered Accountants of India

(ICAI), to the extent applicable, and current practices prevailing within the banking

industry in India.

5.3 USE OF ESTIMATES

The presentation of financial statements, in conformity with generally

accepted accounting principles, requires management to make estimates and

assumptions that affect the reported amounts of assets, liabilities, revenues and

expenses and the disclosure of contingent liabilities at the end of the reporting period.

Management believes that these estimates and assumptions are prudent and

reasonable. However, actual results could differ from estimates requiring an

adjustment to the carrying amounts of assets or liabilities which are recognized

prospectively in the future periods.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

23

A) Significant accounting policies:

1. Investments:

1.1) Classification of Investments:

For the purpose of disclosure in the Balance Sheet, Investments have been

classified under four groups, namely, Government Securities, other approved

securities, shares and bonds of PSUs and other investments.

1.2) Categorization of Investments:

In accordance with the guidelines issued by the RBI, the Bank has classified

its Investment portfolio into the following three categories:

“Held to Maturity” (HTM) – securities acquired with the intention to hold till

maturity.

“Held for Trading” (HFT) – securities acquired with the intention to trade.

“Available for Sale” (AFS) – securities which do not fall within the above two

categories.

1.3) Valuation of Investments:

Investments under “Held to Maturity” (HTM) category are carried at Book

Value. The premium paid, if any, on the investments under this category is amortized

over the residual life of the security as per guidelines of RBI and Policy adopted by

Bank. The profit / loss on investments acquired at a discount on face value, under this

category, are recognized only at the time of redemption / sale of the investment.

Investments under Available for Sale category are valued scrip-wise at lower of Cost

or Market Value. Net depreciation, if any, under each classification has been provided

for, net appreciation, if any, has been ignored.

Market Value, where market quotes are not available, is determined on the

basis of the “Yield to Maturity” (YTM) method as indicated by Primary Dealers

Association of India (PDAI) jointly with the Fixed Income and Money Market

Derivatives Association of India (FIMMDA). Appreciation/ Depreciation are

aggregated for each class of securities and net depreciation in aggregate for each

category as per RBI guidelines is charged to Profit and Loss Account. Net

appreciation, if any, is ignored.

1.4) The Bank is not holding any investments under Held for Trading (HFT) category.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

24

2. Advances:

2.1) The classification of advances into Standard, Sub-standard, Doubtful and Loss

assets as well as provisioning on Standard Advances and Non-Performing Advances

has been arrived at in accordance with the Income Recognition, Assets Classification

and Provisioning

Norms prescribed by the RBI from time to time till date.

2.2) The unrealized interest in respect of advances classified as Non-Performing

Assets is disclosed as “NPA Interest Receivable” as per RBI directives.

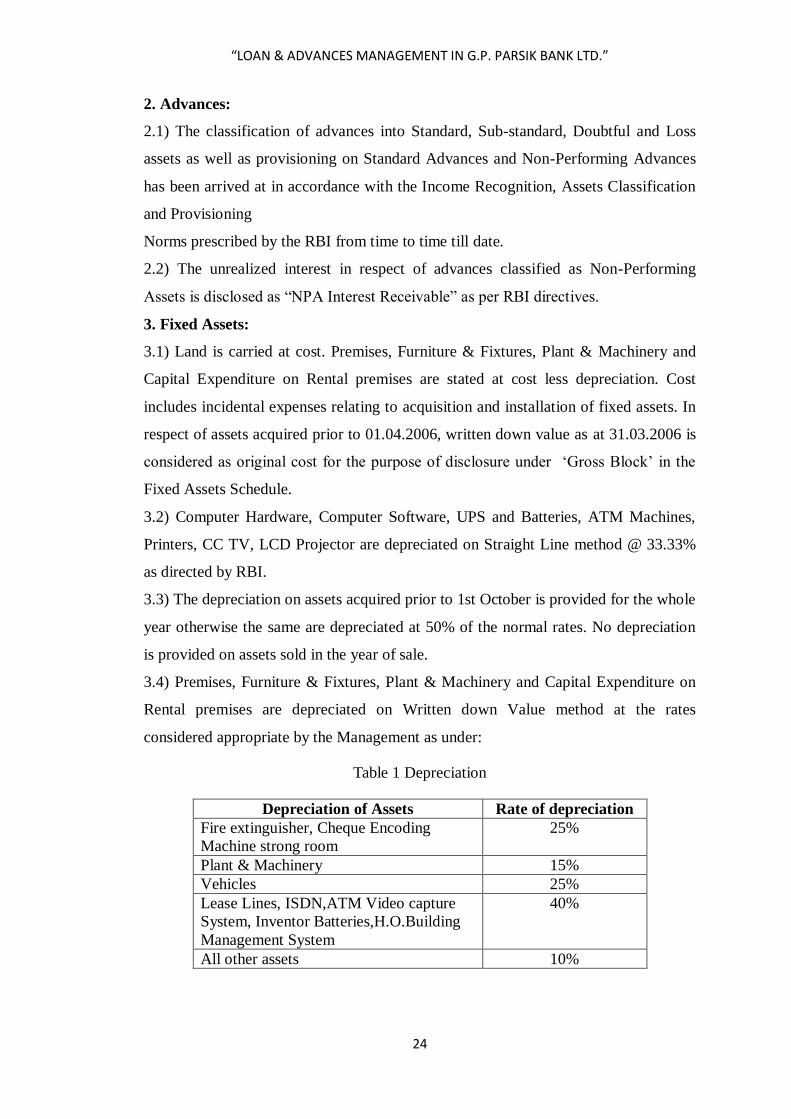

3. Fixed Assets:

3.1) Land is carried at cost. Premises, Furniture & Fixtures, Plant & Machinery and

Capital Expenditure on Rental premises are stated at cost less depreciation. Cost

includes incidental expenses relating to acquisition and installation of fixed assets. In

respect of assets acquired prior to 01.04.2006, written down value as at 31.03.2006 is

considered as original cost for the purpose of disclosure under „Gross Block‟ in the

Fixed Assets Schedule.

3.2) Computer Hardware, Computer Software, UPS and Batteries, ATM Machines,

Printers, CC TV, LCD Projector are depreciated on Straight Line method @ 33.33%

as directed by RBI.

3.3) The depreciation on assets acquired prior to 1st October is provided for the whole

year otherwise the same are depreciated at 50% of the normal rates. No depreciation

is provided on assets sold in the year of sale.

3.4) Premises, Furniture & Fixtures, Plant & Machinery and Capital Expenditure on

Rental premises are depreciated on Written down Value method at the rates

considered appropriate by the Management as under:

Table 1 Depreciation

Depreciation of Assets Rate of depreciation

Fire extinguisher, Cheque Encoding

Machine strong room

25%

Plant & Machinery 15%

Vehicles 25%

Lease Lines, ISDN,ATM Video capture

System, Inventor Batteries,H.O.Building

Management System

40%

All other assets 10%

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

25

4. Impairment of Assets

4.1) Fixed Assets are reviewed at each balance sheet date to ascertain whether there

are any indications that the carrying amount of any asset exceeds its realizable value.

5. Revenue recognition

5.1) Income is accounted on accrual basis as and when it is earned except for:

(a) The income on Non-Performing Assets is recognized on realization, as per

Reserve Bank of India directives.

(b) The commission on Letters of Credit / Guarantees and Dividends received from

shares of co-operative institutions are accounted on receipt basis.

(c) The interest on overdue / matured Fixed Deposits is accounted from September 1,

2008 at the rate applicable to Savings Bank Accounts as per RBI guidelines.

6. Employee Benefits

Defined Contribution Scheme:

The payment of Provident Fund is made to the Commissioner for Provident

Fund at rates prescribed in the Employees Provident Fund and Misc. Provisions Act,

1952 and is accounted for on accrual basis.

Defined Benefit Scheme

The bank has taken Employees‟ Group Gratuity Policy from Life Insurance

Corporation of India (LIC) and LIC is maintaining gratuity fund under a trust deed for

gratuity payments to employees. The premium / contribution paid to LIC under the

said policy are debited to Profit & Loss Account.

The bank has taken Employees‟ Group Leave Encashment policy from Life Insurance

Corporation of India (LIC) during the year under review to meet leave encashment

liability. The premium paid to LIC under the said policy is debited to Profit & Loss

Account.

7. Lease Payment

Operating lease payments are recognized as an expense in the Profit & Loss

Account on accrual basis for the financial year. In the opinion of the Bank, the leave

and license agreements entered into by the Bank for use of premises for its banking

business are cancellable.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

26

8. Income Taxes

Tax expense comprises of current tax and deferred tax. Current Income Tax is

measured on the basis of estimated taxable income for the year in accordance with the

provisions of Income Tax Act, 1961, and rules framed there under. Deferred tax for

timing differences between the book and taxable profits for the year is accounted for

using the current tax rates and law as on the Balance Sheet date.

9. Earnings per share

Basic earnings per share are calculated by dividing the net profit for the period

after tax (before appropriation) by weighted average number of equity shares

outstanding during the period.

10. Segment Reporting

The Bank has identified two Business Segments viz. Treasury Operations and

Other Banking Operations taking into account the nature of products and services, the

different risks and returns and the guidelines issued by RBI. Treasury Operations

includes all investment portfolio and profit / loss on sale of investments. The expenses

of this segment consist of interest expenses on funds borrowed from internal and

external sources and depreciation / amortization of premium on investments in Held

to Maturity category. Other Banking Operations include all other operations not

covered under „Treasury Operations‟.

B) Disclosures as required by the Accounting Standards (AS)

11. Effects to Cost of Acquisition of Merged Banks (AS 14)

During the FY.2010-11, the Bank had acquired The Ichalkaranji Mahila

Sahakari Bank Ltd, Ichalkaranji. In accordance with the merger order passed by the

Office of the Commissioner for Co-operation and Registrar of Co-operative Societies,

Maharashtra State, Pune 411 001 dated October 27, 2010 and „No Objection

Certificate‟ issued by the RBI, the effects to Amortization Reserve for the F.Y.2012-

13 are as under:

Particulars Ichalkaranji Mahila Sahakari Bank Ltd.

Amortization Reserve as on 01/04/2013 4,80,00,000

Amortization for F.Y.2013-14 1,60,00,000

Amortization Reserve as on 31/03/2014 6,40,00,000

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

27

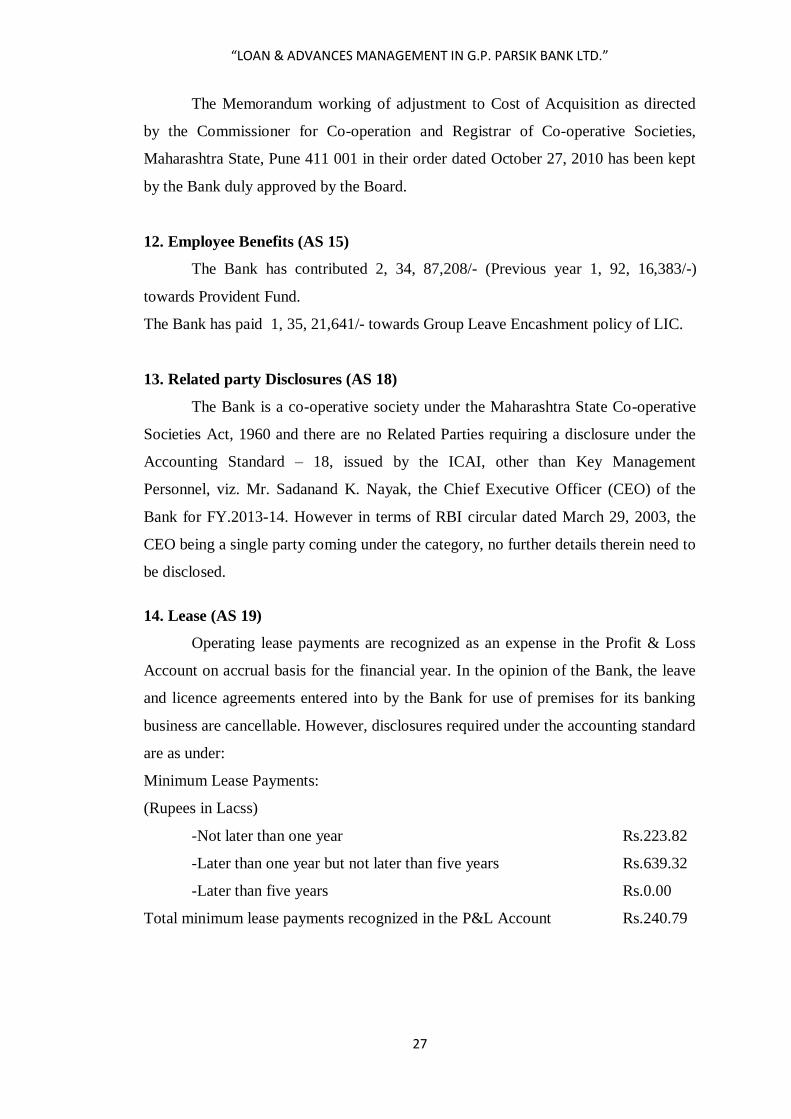

The Memorandum working of adjustment to Cost of Acquisition as directed

by the Commissioner for Co-operation and Registrar of Co-operative Societies,

Maharashtra State, Pune 411 001 in their order dated October 27, 2010 has been kept

by the Bank duly approved by the Board.

12. Employee Benefits (AS 15)

The Bank has contributed 2, 34, 87,208/- (Previous year 1, 92, 16,383/-)

towards Provident Fund.

The Bank has paid 1, 35, 21,641/- towards Group Leave Encashment policy of LIC.

13. Related party Disclosures (AS 18)

The Bank is a co-operative society under the Maharashtra State Co-operative

Societies Act, 1960 and there are no Related Parties requiring a disclosure under the

Accounting Standard – 18, issued by the ICAI, other than Key Management

Personnel, viz. Mr. Sadanand K. Nayak, the Chief Executive Officer (CEO) of the

Bank for FY.2013-14. However in terms of RBI circular dated March 29, 2003, the

CEO being a single party coming under the category, no further details therein need to

be disclosed.

14. Lease (AS 19)

Operating lease payments are recognized as an expense in the Profit & Loss

Account on accrual basis for the financial year. In the opinion of the Bank, the leave

and licence agreements entered into by the Bank for use of premises for its banking

business are cancellable. However, disclosures required under the accounting standard

are as under:

Minimum Lease Payments:

(Rupees in Lacss)

-Not later than one year Rs.223.82

-Later than one year but not later than five years Rs.639.32

-Later than five years Rs.0.00

Total minimum lease payments recognized in the P&L Account Rs.240.79

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

28

15. Intangible Fixed Assets (AS 26)

The Bank has identified intangible assets representing Computer Software and

shown separately in the Fixed Assets Schedule under fixed asset block “Intangible

Assets” giving details relating to Gross Block & Amortisation as prescribed by

Accounting Standard – 26 on Intangible assets issued by ICAI. Computer software is

amortized @33.33% on straight line method as per the directives of RBI.

16. Impairment of Assets (AS 28)

There is no material impairment of any of assets in the opinion of the Bank

and as such no provision under Accounting Standard – 28 issued by ICAI is required.

17. Contingent Liabilities

All letters of credit / guarantees are sanctioned to customers with approved

credit limits in place. The liability thereon is dependent on terms of contractual

obligations, devolvement, raising demand by concerned parties and the amount being

called up. These amounts are collateralized by margins, counter-guarantees and

secured charges.

D. Notes to Accounts

18. Investments

During the year, Bank has not shifted any securities from Available for Sale

category to Held to Maturity category and also from Held to Maturity category to

Available for Sale category. During the year, Bank has not sold any securities held

under AFS category.

19. Cash and Bank Balances

Fixed Deposits with other Banks include deposits aggregating to

1,75,50,000/- (Previous year 7,97,00,000/-) lodged as margin money to secure

issuance of Letters of Credit / Guarantees in respect of correspondent business.

20. Capital commitments

At March 31,2014, estimated amount of contracts remaining to be executed on

capital accounts amount to 5,51,250/- (Previous year ` 1,37,61,014/-).

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

29

CHAPTER 6 : LOAN AND ADVANCE MANAGEMENT

6.1 TYPES OF LOAN

1. HOUSING LOAN

Under this scheme the Parsik bank provides loans or financing for the

purchasing of flat or construction of house.

Table 2 Housing Loan

Purpose Purchase flat or Construction of House

Rate of interest @ 11.00% p.a. up to Rs 25 lacs for 5 years.

@ 11.50% p.a. up to Rs 25 lacs for 5yr-15yr.

@ 11.50% p.a. above Rs 25 lacs to 50 Lacs for 5 years

@ 12.00% p.a. above Rs 25 lacs to 50 lacs for 5yr to 15yr.

Eligibility Salaried / Businessman / Self Employed

Security Registered Mortgage of Flat to be Purchased / House to be

constructed

Repayment Maximum Up to 15 years.

Loan Amount Maximum up to 50 Lacs

E. M. I. per Rs. 1 Lacs

Rate of Interest 11.00% 11.50% 12.00%

5 years 2174 2199 2224

10 years - 1406 1435

15 years - 1168 1200

Eligibility:

Domicile of Mumbai City who wants to purchase/ construct the building or house within

the district.

Employee of Government/ self governed, semi government, leading banks, urban

cooperative bank/court, financial institution, education institutes etc.

Business man who fills income tax return for last 3 years.

Normally the age limit for applicant is 50 years but it can be extent up to 55 years in

certain special cases.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

30

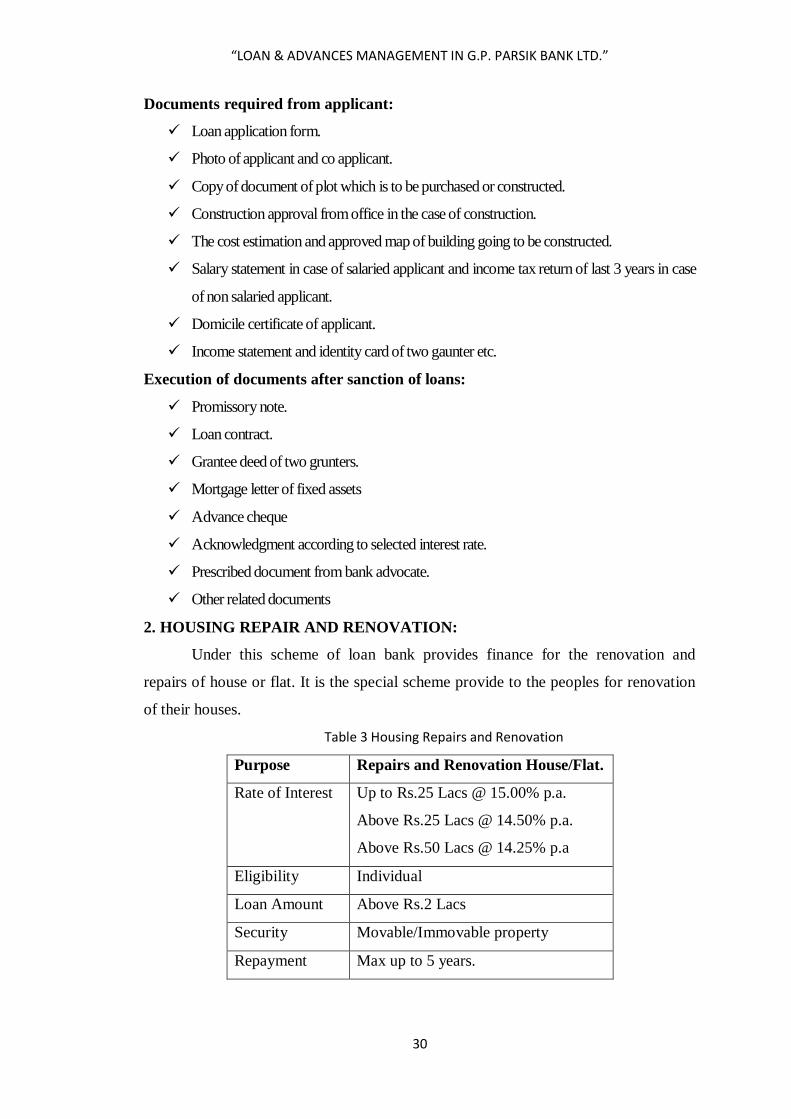

Documents required from applicant:

Loan application form.

Photo of applicant and co applicant.

Copy of document of plot which is to be purchased or constructed.

Construction approval from office in the case of construction.

The cost estimation and approved map of building going to be constructed.

Salary statement in case of salaried applicant and income tax return of last 3 years in case

of non salaried applicant.

Domicile certificate of applicant.

Income statement and identity card of two gaunter etc.

Execution of documents after sanction of loans:

Promissory note.

Loan contract.

Grantee deed of two grunters.

Mortgage letter of fixed assets

Advance cheque

Acknowledgment according to selected interest rate.

Prescribed document from bank advocate.

Other related documents

2. HOUSING REPAIR AND RENOVATION:

Under this scheme of loan bank provides finance for the renovation and

repairs of house or flat. It is the special scheme provide to the peoples for renovation

of their houses.

Table 3 Housing Repairs and Renovation

Purpose Repairs and Renovation House/Flat.

Rate of Interest Up to Rs.25 Lacs @ 15.00% p.a.

Above Rs.25 Lacs @ 14.50% p.a.

Above Rs.50 Lacs @ 14.25% p.a

Eligibility Individual

Loan Amount Above Rs.2 Lacs

Security Movable/Immovable property

Repayment Max up to 5 years.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

31

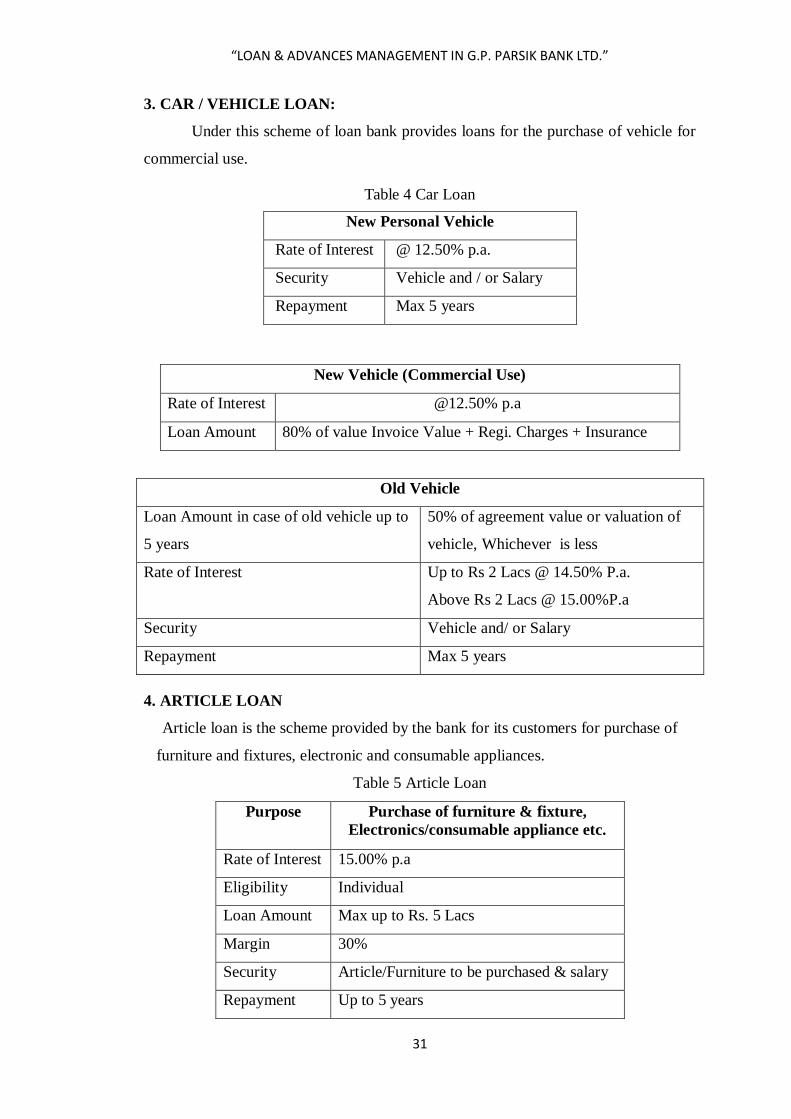

3. CAR / VEHICLE LOAN:

Under this scheme of loan bank provides loans for the purchase of vehicle for

commercial use.

Table 4 Car Loan

New Personal Vehicle

Rate of Interest @ 12.50% p.a.

Security Vehicle and / or Salary

Repayment Max 5 years

New Vehicle (Commercial Use)

Rate of Interest @12.50% p.a

Loan Amount 80% of value Invoice Value + Regi. Charges + Insurance

Old Vehicle

Loan Amount in case of old vehicle up to

5 years

50% of agreement value or valuation of

vehicle, Whichever is less

Rate of Interest Up to Rs 2 Lacs @ 14.50% P.a.

Above Rs 2 Lacs @ 15.00%P.a

Security Vehicle and/ or Salary

Repayment Max 5 years

4. ARTICLE LOAN

Article loan is the scheme provided by the bank for its customers for purchase of

furniture and fixtures, electronic and consumable appliances.

Table 5 Article Loan

Purpose Purchase of furniture & fixture,

Electronics/consumable appliance etc.

Rate of Interest 15.00% p.a

Eligibility Individual

Loan Amount Max up to Rs. 5 Lacs

Margin 30%

Security Article/Furniture to be purchased & salary

Repayment Up to 5 years

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

32

5. GROUP LOAN

In certain case where the employer under takes to deduct the loan installment

under sec 49 of Maharashtra State Co-op Act, 1960 and remit the same towards the

repayment of loan or undertakes to remit the monthly salary of employees directly to

the Bank till entire loan is repaid and information to that effect is given by bank.

In such case, Group loan may be considered, provided minimum number of

employees applying at a time in a group is 10.

Table 6 Group Loan

Purpose For purchase of customer durable go (with or without security of

consumer durable goods and/or for repayment of debts and/or for

housing repairing and/or for any other purpose

Rate of Interest 14.00%

Eligibility Min 10 employees of a single operation

Loan Amount Max up to Rs.3 Lacs

Repayment 5 to 7 years

6. MICRO, SMALL & MEDIUM ENTERPRISES LOANS (Against Mortgage)

Table 7 Micro and SME

Purpose Business Expansion, Purchasing

Machinery & Raw Material,

Setting New Project

Rate of Interest Up to Rs. 25 Lacs

Above Rs. 25 Lacs to Rs.50

Above R. 50 Lacs to Rs. 3 crores

Above Rs.3 crores

14.00%

As per Gradation

Eligibility Individual/Firm/Partner Ship

Firm/company,etc

Loan Amount As per requirement

Margin 30%

Security Immovable/movable property

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

33

7. TERM / CASH CREDIT LOAN FOR BUILDERS & CONTRACTORS

This is the loan scheme which is provided to the builders and contractor to the

completion of their projects. This also includes the loans to the contractors which are

doing government project as well as private projects.

Table 8 Cash Credit

Purpose Business expansion/Purchasing construction

equipments/Machinery/Raw Material

Eligibility Individual/Firm/Partnership/Company Etc

Loan

Amount

As per requirement

Rate of

interest

16.00%

Margin 30.00%

Repayment For Term Loan – Max 7 years

For Cash Credit Loan – Max period up to 12 months on renewable

basis.

Security Movable/Immovable property/Machinery

8. T.U.F. (Technology Up gradation Fund) SCHEME

The Indian Textile Industry occupies a unique position in the Indian Economy,

in terms of its contribution to industrial production, employment & exports. Given the

significance of this industry to the overall health of the Indian Economy, its

employment potential & the huge historical backlog of technology up gradation,

particularly in the context of the liberalization of the national industrial & trade policy

& globalization of textile trade, it is essential for the textile industry to have access to

timely & adequate capital at internationally comparable rates of interest in order to

upgrade its technology level. Bank has been extending financial assistance by

providing concessional Interest rate for purchase of machinery for textile business.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

34

Table 9 T.U.F

Eligibility Individuals / Partnership Firms

/ Companies Etc.

Margin Minimum up to 30% of

machinery invoice Quotation

Security Movable & Immovable

Properties

Repayment Maximum Period up to 84

months

Loan Amount Interest

A)Machinery Loan

Under TUF Scheme

Up to Rs 25 Lacs 14.00%

Above Rs.25 Lacs up to

Rs.50 Lacs

13.25%

Above Rs.50 Lacs 13.00%

B)Land & Building and

New plant & Machinery

U to p Rs. 25 Lacs 14.00

Above Rs.25 Lacs up to

Rs.50 Lacs

13.50%

Above Rs.50 Lacs 13.25%

C)Land & Building and

Old plant & Machinery

Up to Rs. 25 Lacs 14.50%

Above Rs.25 Lacs up to

Rs.50 Lacs

13.75%

Above Rs.50 Lacs 13.50%

9. CASH CREDIT FACILITY

This kind of fund based working capital facility is provided to

traders/manufacturers & the like. Bank has focus for extending cash credit facility to

small & medium size enterprises .Purpose of this loan to make working capital

requirement or additional stock purchase or Repayment of trade creditors.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

35

Table 10 Cash Credit Facility

Loan Amount Interest

Below Rs.50 Lacs 13.00%

Rs. 50 Lacs to 2 cores 12.75%

Above Rs.2Crores 12.25%

Eligibility Small Traders/ Manufacturer/

Partnership/Co.

Margin Minimum 30% of net inventory

Security Closing Stocks, Debtors,

Movable/immovable

Repayment Max period up to 12 months on

renewable

10. EDUCATION LOAN

To brighten the future of bright & committed students by extending financial

assistance to pursue higher professional / technical courses studies in India & Abroad

through Educational Universities / Institutes / Organizations of good reputation &

recognition.

Table 11 Education Loan

Purpose Higher Education

Rate of Interest Up to Rs.10 Lacs @ 11.00% p.a.

Above Rs.10 Lacs up to Rs.20 Lacs @ 12% p.a

Loan Amount Up to Rs.10 Lacs for studies in India

Up to Rs.20 Lacs For Studies in Abroad

Security Tangible collateral security owned by parents or

Guarantors, Whole Life insurance Policy on the life

of the student, For loan Amount

Repayment Max 12 months, Including Moratorium

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

36

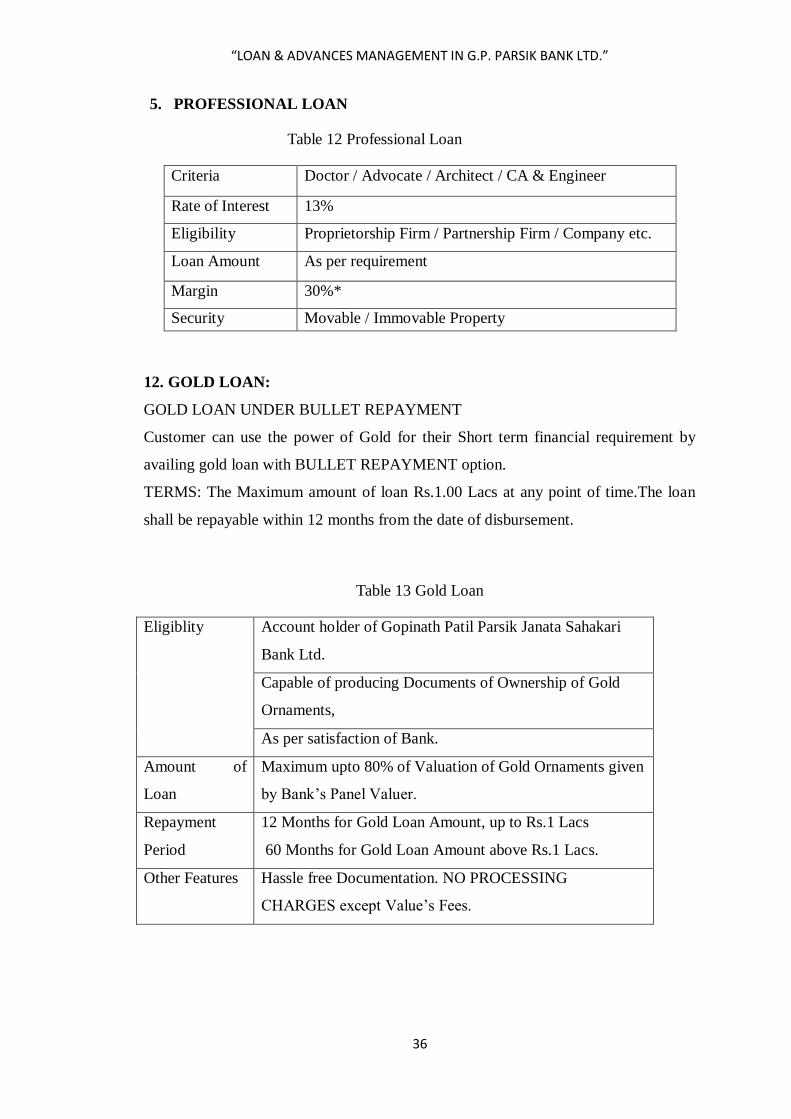

5. PROFESSIONAL LOAN

Table 12 Professional Loan

Criteria Doctor / Advocate / Architect / CA & Engineer

Rate of Interest 13%

Eligibility Proprietorship Firm / Partnership Firm / Company etc.

Loan Amount As per requirement

Margin 30%*

Security Movable / Immovable Property

12. GOLD LOAN:

GOLD LOAN UNDER BULLET REPAYMENT

Customer can use the power of Gold for their Short term financial requirement by

availing gold loan with BULLET REPAYMENT option.

TERMS: The Maximum amount of loan Rs.1.00 Lacs at any point of time.The loan

shall be repayable within 12 months from the date of disbursement.

Table 13 Gold Loan

Eligiblity Account holder of Gopinath Patil Parsik Janata Sahakari

Bank Ltd.

Capable of producing Documents of Ownership of Gold

Ornaments,

As per satisfaction of Bank.

Amount of

Loan

Maximum upto 80% of Valuation of Gold Ornaments given

by Bank‟s Panel Valuer.

Repayment

Period

12 Months for Gold Loan Amount, up to Rs.1 Lacs

60 Months for Gold Loan Amount above Rs.1 Lacs.

Other Features Hassle free Documentation. NO PROCESSING

CHARGES except Value‟s Fees.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

37

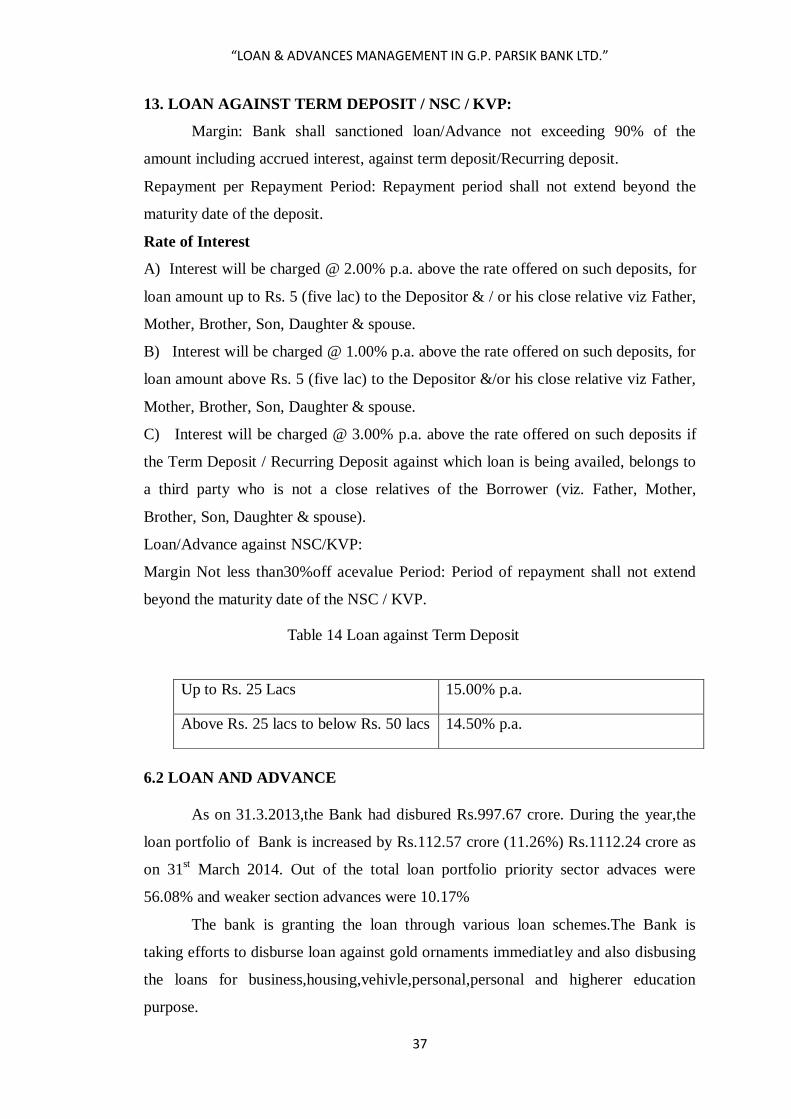

13. LOAN AGAINST TERM DEPOSIT / NSC / KVP:

Margin: Bank shall sanctioned loan/Advance not exceeding 90% of the

amount including accrued interest, against term deposit/Recurring deposit.

Repayment per Repayment Period: Repayment period shall not extend beyond the

maturity date of the deposit.

Rate of Interest

A) Interest will be charged @ 2.00% p.a. above the rate offered on such deposits, for

loan amount up to Rs. 5 (five lac) to the Depositor & / or his close relative viz Father,

Mother, Brother, Son, Daughter & spouse.

B) Interest will be charged @ 1.00% p.a. above the rate offered on such deposits, for

loan amount above Rs. 5 (five lac) to the Depositor &/or his close relative viz Father,

Mother, Brother, Son, Daughter & spouse.

C) Interest will be charged @ 3.00% p.a. above the rate offered on such deposits if

the Term Deposit / Recurring Deposit against which loan is being availed, belongs to

a third party who is not a close relatives of the Borrower (viz. Father, Mother,

Brother, Son, Daughter & spouse).

Loan/Advance against NSC/KVP:

Margin Not less than30%off acevalue Period: Period of repayment shall not extend

beyond the maturity date of the NSC / KVP.

Table 14 Loan against Term Deposit

6.2 LOAN AND ADVANCE

As on 31.3.2013,the Bank had disbured Rs.997.67 crore. During the year,the

loan portfolio of Bank is increased by Rs.112.57 crore (11.26%) Rs.1112.24 crore as

on 31st March 2014. Out of the total loan portfolio priority sector advaces were

56.08% and weaker section advances were 10.17%

The bank is granting the loan through various loan schemes.The Bank is

taking efforts to disburse loan against gold ornaments immediatley and also disbusing

the loans for business,housing,vehivle,personal,personal and higherer education

purpose.

Up to Rs. 25 Lacs 15.00% p.a.

Above Rs. 25 lacs to below Rs. 50 lacs 14.50% p.a.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

38

Last 10 Years Bank's Progress (Rs in Lacs)

Table 15Years Performance

This is the graph which presents the growth of the bank in last ten years. Each

and every year bank growth in all their fields such as share capital, deposits loans,

asset funds, customer base, net profits and provides the greatest dividend of 15% p.a.

0

50000

100000

150000

200000

Am

on

ut

Last 10 years performance

Share Capita

Deposits

Loans

Assets Fund

Customer Base

Net Profit

Dividend

Year

Share

Capital Deposits Loans

Asset

Fund

Customer

Base

Net

Profits Dividend

2004-05 1104.59 52042.79 21762.46 7925.91 46612 752.63 15%

2005-06 1254.05 59317.84 26310.61 8897.01 48505 1028.65 15%

2006-07 1457.17 70488.24 32340.40 10638.84 50871 468.28 15%

2007-08 1845.67 88013.54 45535.87 11406.69 54424 1540.16 15%

2008-09 2242.75 94341.95 55482.54 13336.83 58096 1743.26 15%

2009-10 2534.71 116717.20 60059.64 15199.18 61240 1837.09 15%

2010-11 3076.62 139803.30 72207.09 18214.10 65073 2072.32 15%

2011-12 3673.96 146049.03 86405.06 21209.72 68837 2130.91 15%

2012-13 4253.86 16300.99 99967.46 24103.69 72512 2275.94 15%

2013-14 4715.40 183513.10 111224.22 26918.03 74696 2421.75 15%

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

39

Year

Share

Capital Deposits Loans

Assets

Fund

Customer

Base

Net

Profit

2004-05 100.00 100.00 100.00 100.00 100.00 100.00

2005-06 113.53 113.98 120.90 112.25 104.06 136.67

2006-07 116.20 118.83 122.92 119.58 104.88 45.52

2007-08 126.66 124.86 140.80 107.22 106.98 328.90

2008-09 121.51 107.19 121.84 116.92 106.75 113.19

2009-10 113.02 123.72 108.25 113.96 105.41 105.38

2010-11 121.38 119.78 120.23 119.84 106.26 112.80

2011-12 119.42 104.47 119.66 116.45 105.78 102.83

2012-13 115.78 114.55 115.70 113.64 105.34 106.81

2013-14 110.85 109.69 111.26 111.68 103.01 106.41

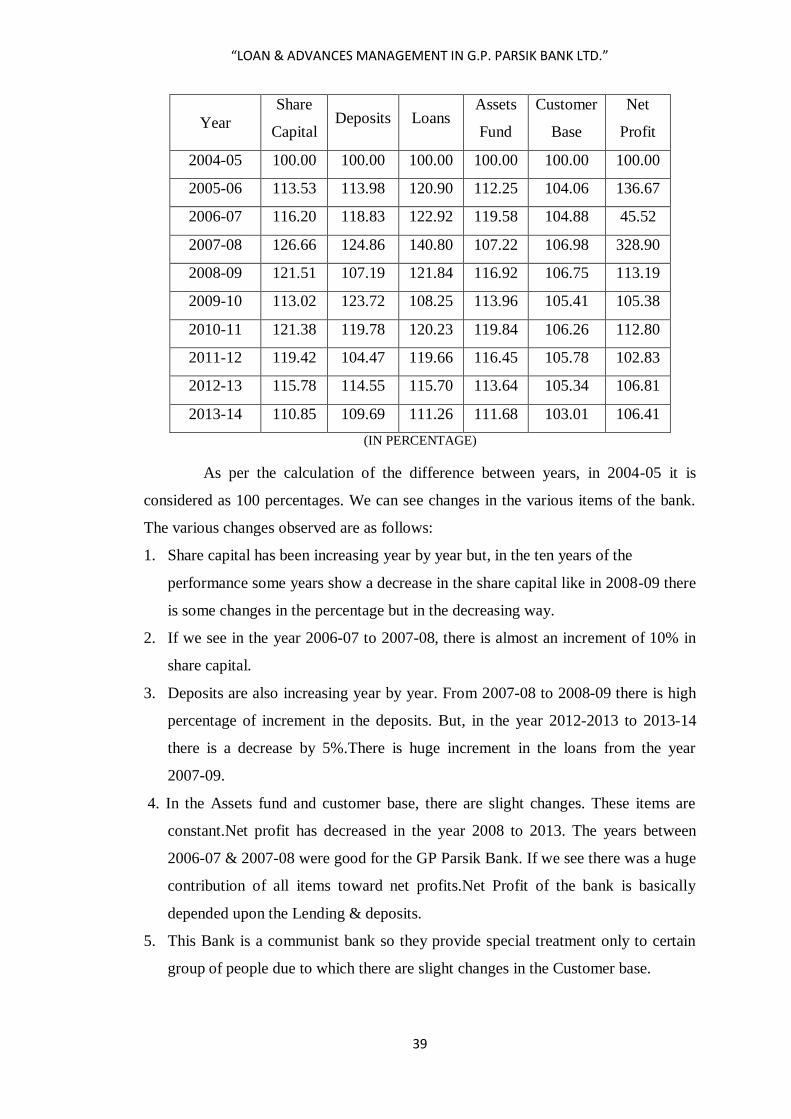

(IN PERCENTAGE)

As per the calculation of the difference between years, in 2004-05 it is

considered as 100 percentages. We can see changes in the various items of the bank.

The various changes observed are as follows:

1. Share capital has been increasing year by year but, in the ten years of the

performance some years show a decrease in the share capital like in 2008-09 there

is some changes in the percentage but in the decreasing way.

2. If we see in the year 2006-07 to 2007-08, there is almost an increment of 10% in

share capital.

3. Deposits are also increasing year by year. From 2007-08 to 2008-09 there is high

percentage of increment in the deposits. But, in the year 2012-2013 to 2013-14

there is a decrease by 5%.There is huge increment in the loans from the year

2007-09.

4. In the Assets fund and customer base, there are slight changes. These items are

constant.Net profit has decreased in the year 2008 to 2013. The years between

2006-07 & 2007-08 were good for the GP Parsik Bank. If we see there was a huge

contribution of all items toward net profits.Net Profit of the bank is basically

depended upon the Lending & deposits.

5. This Bank is a communist bank so they provide special treatment only to certain

group of people due to which there are slight changes in the Customer base.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

40

6.3 IMPORTANT POINT OF LOANS AND ADVANCES

a) Loans, cash credits and / or overdrafts and discount and purchase of bill may be

granted to members on security or securities mentioned below or other security or

securities approved by the Board or without security.

Personal security and / or surety / sureties of other member (s) or nominal

member(s)

Collateral security of movable and immovable property.

Industrial, mercantile, agricultural and other marketable commodities

or machinery under pledge, hypothecation or charge of the Bank.

Companies, debentures and fixed deposits with the Bank.

– vehicles.

permitted by Reserve Bank of India.

b) Loans and advances may be granted to non-members against the security of their

term deposits with the Bank.

c) Loans may be granted to nominal members as per RBI guidelines.

d) The Board shall frame detailed loan regulations/ policy prescribing the procedure

for sanction of loans, margins to be maintained, proportion of unsecured loans, proper

terms and conditions and the nature of securities acceptable for loans and advances

for different purposes in accordance with the guidelines of the Reserve Bank of India,

higher financing agency and the Registrar from time to time.

e) The application for Loans / Advances shall be dealt with by the Board / Sub-

committees who may grant the same or any portion thereof on such terms and

conditions, as they think fit or may refuse the same without being under any

obligation to assign reason for doing so. The board of directors shall give valid reason

while sanctioning the loan proposals / taking favorable decisions for which the chief

executive officer has given adverse remarks.

f) All loans and advances shall be governed by guidelines issued by Reserve Bank of

India from time to time.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

41

CHAPTER 7 : RECOVERY OF LOANS

The banks have introduced various deposit schemes which induce the common

man to save more money. The urban cooperative banks accept deposits for the

purpose of lending. It is the primary duty to and the function of the urban co operative

banks to safeguard the interest of the depositors. Whenever deposits are accepted, the

bank agrees and undertakes to repay the amount of deposits with interest to the

depositor and maturity. The ownership of the deposit amount vests with the customer

and the custody of the deposit amount are with the banker. So whenever advances and

loans are sanctioned to shareholders / members of the bank, the banker has to take

extreme care to see that the borrower repays the amount of loan with interest so as to

enable the banker to repay the amount of deposit with interest to the customer.

7.1 MECHANISM

This is necessary to ensure that every borrower has a proper repaying capacity

for repayment of the amount of loans and advances that would be sanctioned.

Securities are also taken to ensure that in case the borrower fails to repay the amount

of loan, the securities can be attached and sold out and the debts can be liquidated.

Even with this background, though there is a detailed scrutiny of loan

application, it is observed that there are very few cases, where the judgment of the

bankers fails. In such „fail cases‟ the borrowers are not ready and willing to repay the

amount of loan, the securities can be attached and sold out and the debts can be

liquidated.

Following are some points which banks takes care while lending money:

Date of sanction of loan

Amount of loan sanctioned

Rate of interest that would be charged

Last date of repayment of loan

Period for which the loan is granted

Details regarding securities offered

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

42

7.2 MEASURES BY BANK FOR RECOVERY DUES

Whenever, a borrower commits breach of agreement in respect of repayment

of schedule of the amount of loans with interest etc., we safely say that there are

'OVERDUES ' in the Loan Account. Once the Loan A/c is an overdue A/c i.e. the

borrower has committed default in repayment of loan amount as per the dates

specified in the Agreement, the n the Banker has necessarily to adopt measures which

will result into recovery of overdue amounts.

Whenever the borrower commits default in repayment of loan amount,

immediately the bank should serve ' Preliminary Notices' on the principal

borrower and the sureties advising them to repay the amount of overdue with

interest etc. Such Preliminary Notices should invariably mention information

which is of factual nature relating to

Amount of loan sanctioned.

Date of sanction of loan.

Names of the sureties.

(iv) Amount of the loan sanctioned.

Amount of over dues with interest etc. on a particular date.

Addition to the above it must also be communicated the bank shall proceed to

take further action against the principal borrower and sureties in case of failure

to repay the amount of loan/over dues. It has been often said 'A' stitch in time

saves nine'. Thus, the banker must be vigilant; right from the disbursement of

loan amount till the recovery of the entire loan amount. There should be

effective supervision over the amount of loan sanctioned

Recovery through salary / wages

After issue of such preliminary notices, there may be a positive response from

the principal borrower and he may repay the amount of defaulted loan

installment, or the principal borrower and the surety may approach the

authorities of the bank and may explain their genuine difficulties regarding

repayment of loan amount or there may offer to repay the dues partially. There

may be cases where there is no response from the borrower / sureties.

With this background, the bank should precede further to devise such steps

which will result in recovery of dues. Under various State Cooperative Acts

(e.g. Section 49 of M.C.S. Act 1960)it has been provided that if a member of a

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

43

society. /Bank authorizes his Employer to make deduction from his

salary/wages, in order to satisfy the claims of the society/Bank, and then on

receipt of requisition letter from the concerned Bank, the Employer shall

proceed to make deduction from the salary/wages from the concerned

employee/member to meet the claims of the Bank. The Employer must

remit the amount so deducted immediately to the Bank concerned.

Non-compliance of these provisions under the State Cooperative Act shall be

constructed as' offence' and further Civil and Criminal action can be instituted

against such Erring Employer.

In addition to the above, there are provisions under the Indian Payment of

Wages Act 1936(vide Section 7(2) and Section 7(2) (j) which stipulates that

the Employer shall make deduction from the salary/wages of an Employee to

satisfy the claims of the Cooperative Society / Banks.

Settlement of Disputes:

Based on the noting of the Management, the Board of Directors may pass a

Resolution authorizing the Manager/or such other officer to file "Dispute

Application´ in the Co-op. Court against the defaulting principal borrower and

his sureties. Section 91 of the MCS Act empowers the co-operative courts to

decide on „Disputes‟ and Section 95 further empowers the court to direct

attachment of property before announcement of the award which is called

Attachment before award or order and interlocutory order if it is satisfied that

the parties to the dispute are likely to remove/ dispose of whole or part of his

property. Section 95 similarly empowers the Registrar / Officer authorized by

him to take the above measures in case of disputes referred to him. The prayer

clause normally consists of following important points –

The opponents may be held responsible to repay the entire amount of loan

with interest.

If the opponents fail to pay the amount of loan, the disputant may be entitled

to attach the movable and immovable property of the opponents.

The disputant may be entitled to sell the attached property and recover the

amount due from the opponents.

Any other orders to meet the ends of justice.

“LOAN & ADVANCES MANAGEMENT IN G.P. PARSIK BANK LTD.”

44

CHAPTER NO 8 : LITERATURE REVIEW

The Review Committee on NPE‟ 1986 recommended introduction of

institutional loans, while raising fees in higher education sector, as a strategy for

releasing pressure on the government kitty. Though it agreed that such an

arrangement is the need of the hour, yet it mentioned that educational loans do

involve certain problems in India. They were mentioned as- Psychologically, people