LNG: cheaper for longer Asia Oil & Gas...

36

See important disclosures, including any required research certifications, beginning on page 34 ■ What's new Our short- and long-term (out to 2025E) analysis of the Asia-Pacific LNG market indicates that while it may be tight until 2016, new sources of LNG supply could alter the market’s dynamics in many ways. ■ What's the impact A rosy future for LNG demand. We believe gas demand will remain strong over the next decade, spurred on by policy initiatives, carbon- reduction schemes, and the increasing availability of relatively cheap unconventional gas. Key factors that could affect demand include Japan’s nuclear energy policy, China’s success in finding commercial quantities of shale gas, and whether or not LNG will see wider adoption as a transportation fuel. However, we expect significant growth in LNG supply. We estimate that about 41 new LNG projects are currently planned or under development, which could lead to LNG capacity more than doubling to 630mtpa by 2021. Most of these new LNG projects target Asia markets and will have to compete with existing projects. While some of these projects may not make it past the planning stage, there is still a plentiful supply of new LNG capacity that could easily fill an Asia demand gap of 155mtpa in 2025E. LNG prices likely to be lower in real terms. We expect an increase in spot LNG trading, greater competition between sellers, increasing price sensitivity from buyers, and further energy market deregulation to combine to reduce LNG prices over the next decade. In addition, the potential rise of North America LNG exports, which are indexed to lower Henry Hub gas prices, could add downward pressure to prices. Floating LNG (FLNG) becoming more accepted, but lacks scale. Over the past three years, the number of planned FLNG projects has increased from three to eight, indicating wider acceptance of its ability to monetise stranded gas resources. However, the eight projects only total about 28mtpa, which would not negatively affect the supply picture, in our view. ■ What we recommend In terms of direct investment exposure to LNG, Asia has very few stocks with decent exposure. We highlight four that are exposed to their respective domestic gas demand growth or would cater to global LNG supply growth: Perusahaan Gas Negara (PGAS) (PGAS IJ, IDR5,750, Buy [1]), ENN Energy (ENN) (2688 HK, HKD42.90, Buy [1]), Petronet LNG (Petronet) (PLNG IN, INR119.75, Outperform [2]) and Samsung Heavy Industries (SHI) (010140 KS, KRW35,050, Buy [1]). From a macro perspective, major LNG-importing countries would benefit from lower LNG prices, thus potentially increasing their competitiveness. As such, key sectors that could benefit include Japan and Korea gas utilities, while Australia LNG players are most at risk given their high cost of producing LNG relative to the new LNG-exporting areas, such as North America and East Africa. 5 July 2013 LNG: cheaper for longer • We forecast global LNG capacity to more than double over 2012- 21 and turn a tight market into a buyers’ market after 2016 • Stocks that should benefit from the LNG story include PGAS, ENN Energy, Petronet LNG and Samsung Heavy Industries • Key sectors that could benefit include Japan and Korea gas utilities: Australia LNG players seem most at risk Asia Oil & Gas Sector Key stock calls Source: Daiwa forecasts. Energy / Asia ex Japan Adrian Loh (65) 6499 6548 [email protected] Benjamin Lim (65) 6321 3086 b[email protected] New Prev. PT Perusahaan Gas Negara Tbk (PGAS IJ) Rating Buy Buy Target 7,100 7,100 Upside 23.5% ENN Energy (2688 HK) Rating Buy Buy Target 48.50 48.50 Upside 13.1% Samsung Heavy Industries (010140 KS) Rating Buy Buy Target 45,000 45,000 Upside 28.4%

Transcript of LNG: cheaper for longer Asia Oil & Gas...

See important disclosures, including any required research certifications, beginning on page 34

■ What's new Our short- and long-term (out to 2025E) analysis of the Asia-Pacific LNG market indicates that while it may be tight until 2016, new sources of LNG supply could alter the market’s dynamics in many ways. ■ What's the impact A rosy future for LNG demand. We believe gas demand will remain strong over the next decade, spurred on by policy initiatives, carbon-reduction schemes, and the increasing availability of relatively cheap unconventional gas. Key factors that could affect demand include Japan’s nuclear energy policy, China’s success in finding commercial quantities of shale gas, and whether or not LNG will see wider adoption as a transportation fuel. However, we expect significant growth in LNG supply. We estimate that about 41 new LNG projects are currently planned or under development, which could lead to LNG capacity more than

doubling to 630mtpa by 2021. Most of these new LNG projects target Asia markets and will have to compete with existing projects. While some of these projects may not make it past the planning stage, there is still a plentiful supply of new LNG capacity that could easily fill an Asia demand gap of 155mtpa in 2025E. LNG prices likely to be lower in real terms. We expect an increase in spot LNG trading, greater competition between sellers, increasing price sensitivity from buyers, and further energy market deregulation to combine to reduce LNG prices over the next decade. In addition, the potential rise of North America LNG exports, which are indexed to lower Henry Hub gas prices, could add downward pressure to prices. Floating LNG (FLNG) becoming more accepted, but lacks scale. Over the past three years, the number of planned FLNG projects has increased from three to eight, indicating wider acceptance of its ability to monetise stranded gas resources. However, the eight projects only total about 28mtpa, which would not negatively affect the supply picture, in our view. ■ What we recommend In terms of direct investment exposure to LNG, Asia has very few stocks with decent exposure. We highlight four that are exposed to their respective domestic gas demand growth or would cater to

global LNG supply growth: Perusahaan Gas Negara (PGAS) (PGAS IJ, IDR5,750, Buy [1]), ENN Energy (ENN) (2688 HK, HKD42.90, Buy [1]), Petronet LNG (Petronet) (PLNG IN, INR119.75, Outperform [2]) and Samsung Heavy Industries (SHI) (010140 KS, KRW35,050, Buy [1]). From a macro perspective, major LNG-importing countries would benefit from lower LNG prices, thus potentially increasing their competitiveness. As such, key sectors that could benefit include Japan and Korea gas utilities, while Australia LNG players are most at risk given their high cost of producing LNG relative to the new LNG-exporting areas, such as North America and East Africa.

5 July 2013

LNG: cheaper for longer

• We forecast global LNG capacity to more than double over 2012-21 and turn a tight market into a buyers’ market after 2016

• Stocks that should benefit from the LNG story include PGAS, ENN Energy, Petronet LNG and Samsung Heavy Industries

• Key sectors that could benefit include Japan and Korea gas utilities: Australia LNG players seem most at risk

Asia Oil & Gas Sector

Key stock calls

Source: Daiwa forecasts.

Energy / Asia ex Japan

Adrian Loh(65) 6499 [email protected]

Benjamin Lim(65) 6321 [email protected]

New Prev.PT Perusahaan Gas Negara Tbk (PGAS IJ)Rating Buy BuyTarget 7,100 7,100Upside 23.5%

ENN Energy (2688 HK)Rating Buy BuyTarget 48.50 48.50Upside 13.1%

Samsung Heavy Industries (010140 KS)Rating Buy BuyTarget 45,000 45,000Upside 28.4%

Asia Oil & Gas Sector 5 July 2013

- 2 -

Source: Daiwa forecasts

Sector stocks: key indicators

Share

Company Name Stock code Price New Prev. New Prev. % chg New Prev. % chg New Prev. % chg

Anton Oilfield Services Group 3337 HK 5.69 Buy Buy 7.00 7.00 0.0% 0.191 0.191 0.0% 0.262 0.262 0.0%

China Oilfield Services 2883 HK 14.42 Buy Buy 19.30 19.30 0.0% 1.074 1.074 0.0% 1.240 1.240 0.0%

CNOOC 883 HK 12.80 Buy Buy 19.70 19.70 0.0% 1.412 1.412 0.0% 1.399 1.399 0.0%

PetroChina 857 HK 8.96 Outperform Outperform 11.75 11.75 0.0% 0.717 0.717 0.0% 0.908 0.908 0.0%

Sinopec Corp 386 HK 5.25 Hold Hold 6.00 6.00 0.0% 0.632 0.632 0.0% 0.657 0.657 0.0%

Rating Target price (local curr.) FY1

EPS (local curr.)

FY2

Asia Oil & Gas Sector 5 July 2013

- 3 -

Contributors: Adrian Loh (65) 6499 6548 [email protected]

Benjamin Lim (65) 6321 3086 [email protected]

Maurine Wan (852) 2848 4451 [email protected]

Nirmal Raghavan(91) 22 6622 1018 [email protected]

Gary Zhou (852) 2773 8535 [email protected]

Sung Yop Chung (82) 2 787 9157 [email protected]

Asia LNG: premium pricing plus strong demand ....................................................................... 4 What’s so great about the Asia LNG market? .......................................................................... 4 A transformation may be coming ............................................................................................ 4 The tug of war between demand and supply ............................................................................ 5 What could derail the LNG train? ............................................................................................ 5 What we recommend ................................................................................................................ 5

LNG demand forecast: a rosy future ............................................................................................ 7 A rosy future .............................................................................................................................. 7 Demand-side factors to watch out for over the next 3-5 years ............................................... 8 A brief analysis of LNG demand by country ............................................................................ 9 What is Daiwa’s demand forecast for LNG? ........................................................................... 14

Supply growth outlook appears strong ...................................................................................... 15 A suppliers’ market in the next five years, but things will change ......................................... 15 Global LNG projects in detail ................................................................................................. 15 New supply routes have opened up in the past five years ...................................................... 17 Rising construction costs ........................................................................................................ 19 Moving towards a more liberalised LNG supply market ...................................................... 20

LNG pricing: change is afoot ..................................................................................................... 22 Catalysts for change ............................................................................................................... 22 LNG supply contracts: mainly long-term in nature .............................................................. 22 Understanding the current Asian LNG pricing model .......................................................... 23 What is the future for LNG pricing? ...................................................................................... 23

Floating LNG plans .................................................................................................................... 25 Background ............................................................................................................................. 25 Major drivers ........................................................................................................................... 25 Illustrative capital costs of FLNG versus onshore LNG ........................................................ 26 Applications of FLNG technology .......................................................................................... 26 Still a few hurdles .................................................................................................................... 27

Background on LNG .................................................................................................................. 29 History and properties ........................................................................................................... 29 Processing and transportation ............................................................................................... 29

Contents

Asia Oil & Gas Sector 5 July 2013

- 4 -

Asia LNG: premium pricing plus strong demand

Asia LNG remains an attractive market because of its size, its volume-growth outlook, and premium pricing

What’s so great about the Asia LNG market?

The Asia LNG market, in which Japan is the largest consumer, is typified by a high LNG price that comes closest to crude-oil price parity versus any other market globally, as seen in the following chart. Along with a high price, the Asia-Pacific region is seen as the one that provides the best demand outlook given the lack of natural resources in places such as Japan, South Korea, and Taiwan. In addition, LNG demand in Asia has continued to increase over the past 5-10 years due to the emergence of growing economies such as China, India and Indonesia, as well as the depletion of domestic natural-gas resources in countries such as Malaysia and Thailand. Gas prices of selected countries vs. OECD equivalent oil price

Source: BP Energy Review 2013

Note: All prices are CIF basis; NBP = National Balancing Point

Over the past two decades, Asia LNG buyers have had to operate in a sellers’ market, as the LNG supply raced

to catch up with demand that increased at a CAGR of nearly 9% over the 1992-2012 period. However, over the next decade, we see sufficient supply-side catalysts to lead to a buyers’ market.

A transformation may be coming

At the start of 2013, the global LNG industry was capable of producing 282mtpa and regasifying about 660mtpa, according to data from the International Group of LNG Importers (officially known as the Groupe International des Importateurs de Gaz Natural Liquéfié). Global LNG trade in 2012 was largely stagnant at 236.3mtpa, compared with the 240mtpa of net LNG trade movements for 2011. Some of the key issues that we see affecting the LNG market over the next few years, and which we address in this report, include the following.

• LNG exports from the US. LNG planning in the past couple of years has taken place under the shadow of potential LNG exports from the US. We believe that US LNG exports are inevitable, given the massive scale of the country’s shale gas resources and the current low gas prices in the country.

• Infrastructure improvements should help. US LNG exports should be aided by the Panama Canal expansion in 2014 that will enable US supplies to access Southeast Asia.

• The demand is there. We believe Asia LNG demand will continue to increase, especially given that nuclear-power plants are now out of favour.

• Pricing. Asia LNG buyers look at Henry Hub prices and note how low it is relative to their own purchase prices. Already, we have seen Asia buyers sign gas sales contracts that use FOB pricing based on Henry Hub pricing rather than oil-indexed pricing.

• Speed of development of other LNG export centres. The key among these are LNG projects in East Africa and West Africa. East Africa appears to be the largest threat to current LNG producers given the substantial resource and also the lack of a local market to absorb production. However, the key stumbling blocks in Mozambique and Tanzania are the political and legal systems, which do not appear robust enough for the potential volume of trading.

• The changing nature of China gas demand. With the country’s rapidly-growing gas market, it is unclear how China will divide up its market between the many different sources of gas, such as conventional domestic gas, shale and coal-bed methane, offshore Myanmar, Central Asia and

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

(USD/mmBtu)

Japan

OECD oil equivalent

EU

UK NBP

Canada (Alberta)

US Henry Hub

Asia Oil & Gas Sector 5 July 2013

- 5 -

Russia pipeline supplies, and LNG. Russia’s proposed pipeline link to China from West Siberia alone is likely to equal half the LNG Qatar put on the market between 2009 and 2011.

• New technology. With FLNG gradually gaining acceptance as a way to monetise small, stranded gas fields, this new technology could start to add incremental supply to the market from as early as 2015.

The tug of war between demand and supply

Over the past 20 years, global LNG demand has risen in a relatively linear fashion, while the capex-intensive nature of the industry has resulted in the lumpy supply of LNG into the market. This necessarily leads to periods of tightness as well as periods of oversupply. Over the next few years, we note that new supply projects will be more complex, more costly, and take longer to develop than in the past. Nevertheless, we believe there is a plentiful supply of cheap gas globally (eg, from North America shale), such that the current status quo may undergo a material disruption between now and 2025. As the LNG business expands, we expect a reshaping of the region’s commercial business models and LNG pricing trends. Specifically, we expect real LNG prices to fall in the next 10 years as the confluence of new US LNG tolling models, new trade flows, more short-term sales, and more liberal commercial terms exert downward pressure on LNG prices.

What could derail the LNG train?

Geopolitics. This includes key government decisions that could directly affect the Asia-Pacific LNG business. These include: Japan’s nuclear policy, US gas export policy, and China’s development of unconventional gas and India’s gas market reforms. Current high LNG prices. The high delivered LNG prices in China and India at present could negatively affect demand over the medium-to-long term, and perhaps artificially buoy their coal demand. The global economy. An economic downturn in Europe/the US could affect Asia economies and thus slow the adoption of natural gas and LNG.

What we recommend

In terms of direct plays on LNG, Asia has very few stocks available to investors. Some of the ones that we identify are as follows. Perusahaan Gas Negara, which is seeing volume growth through its floating storage and regasification unit (FSRU) projects, and more importantly is leveraged to Indonesia’s medium- and long-term gas-demand growth. After 2015, we expect the company to extend the reach of its distribution pipelines, which could provide another leg of volume growth for the company. In addition, it has deployed mobile refuelling units for compressed natural gas (CNG), and which could provide an incremental earnings base for PGAS as this is rolled out more intensively over the next 12-24 months. We highlight that its 2014E valuation appears very cheap, trading at a PER of 12.5x and a dividend yield of 5%. (See also: Upgrade to Buy on compelling valuations, published on 27 June 2013.) Petronet LNG may also benefit, due to its position as an LNG importer serving the India gas market. Should lower LNG prices eventuate, we believe this could result in increased gas demand and consumption in India given the market’s sensitivity to high prices. In addition, the company is looking at expanding its Dahej LNG terminal from 10mtpa to 15mtpa by the end of 2015, as well as potentially adding 5mtpa of new capacity on the east coast of India. Should this all go to plan, the company could see its LNG import capacity increase by 67% between 2012 and 2016. Based on our forecasts, the company’s stock is trading currently at an FY14E PER and PBR of 9.2x and 1.9x, respectively, and we forecast a 22% ROE for FY14. Although we forecast muted EPS growth over the next two years, we believe the company’s long-term fundamentals are strong. (See also: Flat earnings profile but strong long-term fundamentals, published on 28 December 2012.) ENN Energy. We forecast a 25% earnings CAGR for 2012-15, driven by China’s continuing gas shortage and a lack of new natural-gas sources over the next few years. For 2013, Daiwa expects 89% of the company’s projects to have access to new natural gas sources, which should allow ENN to expand at a faster organic rate than its other domestic peers. On top of its secured sources for natural gas, the company is also expanding its LNG and CNG vehicle-refuelling stations over the next three years. (See also: NDR feedback – a week in the US, published on 22 April 2013.)

Asia Oil & Gas Sector 5 July 2013

- 6 -

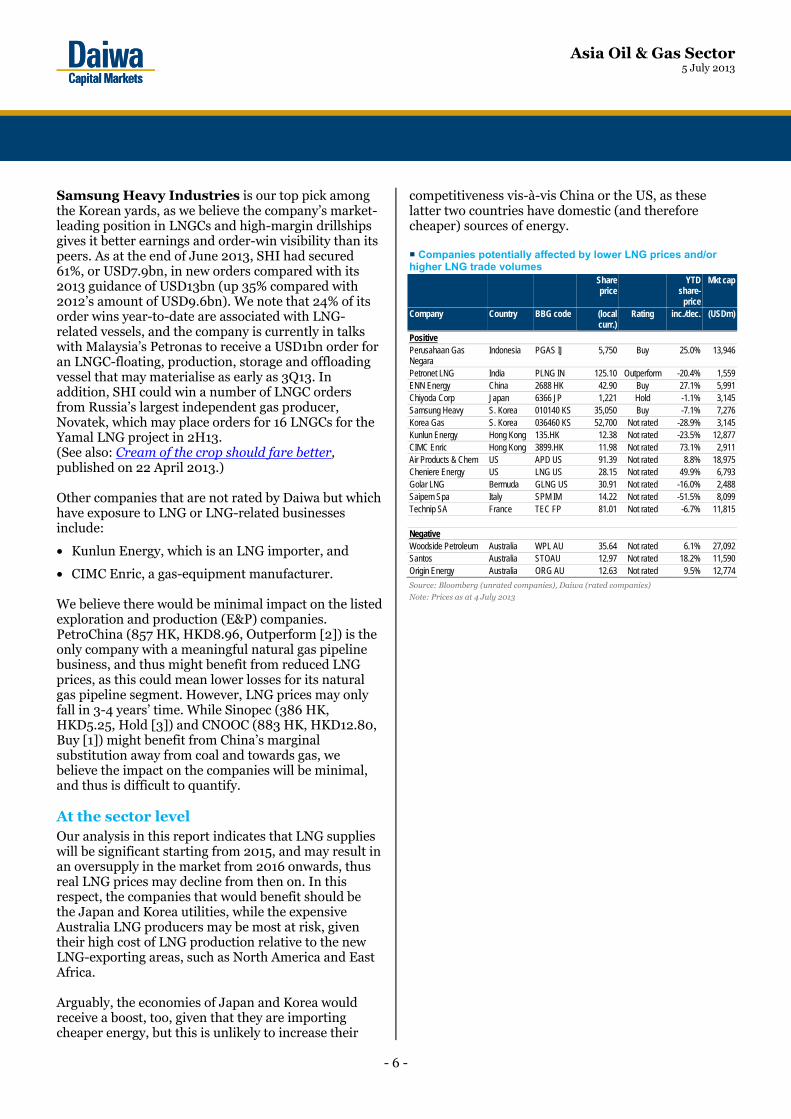

Samsung Heavy Industries is our top pick among the Korean yards, as we believe the company’s market-leading position in LNGCs and high-margin drillships gives it better earnings and order-win visibility than its peers. As at the end of June 2013, SHI had secured 61%, or USD7.9bn, in new orders compared with its 2013 guidance of USD13bn (up 35% compared with 2012’s amount of USD9.6bn). We note that 24% of its order wins year-to-date are associated with LNG-related vessels, and the company is currently in talks with Malaysia’s Petronas to receive a USD1bn order for an LNGC-floating, production, storage and offloading vessel that may materialise as early as 3Q13. In addition, SHI could win a number of LNGC orders from Russia’s largest independent gas producer, Novatek, which may place orders for 16 LNGCs for the Yamal LNG project in 2H13. (See also: Cream of the crop should fare better, published on 22 April 2013.) Other companies that are not rated by Daiwa but which have exposure to LNG or LNG-related businesses include:

• Kunlun Energy, which is an LNG importer, and

• CIMC Enric, a gas-equipment manufacturer. We believe there would be minimal impact on the listed exploration and production (E&P) companies. PetroChina (857 HK, HKD8.96, Outperform [2]) is the only company with a meaningful natural gas pipeline business, and thus might benefit from reduced LNG prices, as this could mean lower losses for its natural gas pipeline segment. However, LNG prices may only fall in 3-4 years’ time. While Sinopec (386 HK, HKD5.25, Hold [3]) and CNOOC (883 HK, HKD12.80, Buy [1]) might benefit from China’s marginal substitution away from coal and towards gas, we believe the impact on the companies will be minimal, and thus is difficult to quantify. At the sector level Our analysis in this report indicates that LNG supplies will be significant starting from 2015, and may result in an oversupply in the market from 2016 onwards, thus real LNG prices may decline from then on. In this respect, the companies that would benefit should be the Japan and Korea utilities, while the expensive Australia LNG producers may be most at risk, given their high cost of LNG production relative to the new LNG-exporting areas, such as North America and East Africa. Arguably, the economies of Japan and Korea would receive a boost, too, given that they are importing cheaper energy, but this is unlikely to increase their

competitiveness vis-à-vis China or the US, as these latter two countries have domestic (and therefore cheaper) sources of energy. Companies potentially affected by lower LNG prices and/or higher LNG trade volumes Share

price YTD

share-price

Mkt cap

Company Country BBG code (local curr.)

Rating inc./dec. (USDm)

Positive Perusahaan Gas Negara

Indonesia PGAS IJ 5,750 Buy 25.0% 13,946

Petronet LNG India PLNG IN 125.10 Outperform -20.4% 1,559 ENN Energy China 2688 HK 42.90 Buy 27.1% 5,991 Chiyoda Corp Japan 6366 JP 1,221 Hold -1.1% 3,145 Samsung Heavy S. Korea 010140 KS 35,050 Buy -7.1% 7,276 Korea Gas S. Korea 036460 KS 52,700 Not rated -28.9% 3,145 Kunlun Energy Hong Kong 135.HK 12.38 Not rated -23.5% 12,877 CIMC Enric Hong Kong 3899.HK 11.98 Not rated 73.1% 2,911 Air Products & Chem US APD US 91.39 Not rated 8.8% 18,975 Cheniere Energy US LNG US 28.15 Not rated 49.9% 6,793 Golar LNG Bermuda GLNG US 30.91 Not rated -16.0% 2,488 Saipem Spa Italy SPM IM 14.22 Not rated -51.5% 8,099 Technip SA France TEC FP 81.01 Not rated -6.7% 11,815 X Negative Woodside Petroleum Australia WPL AU 35.64 Not rated 6.1% 27,092 Santos Australia STOAU 12.97 Not rated 18.2% 11,590 Origin Energy Australia ORG AU 12.63 Not rated 9.5% 12,774

Source: Bloomberg (unrated companies), Daiwa (rated companies)

Note: Prices as at 4 July 2013

Asia Oil & Gas Sector 5 July 2013

- 7 -

LNG demand forecast: a rosy future

Gas demand should remain strong over the next decade, spurred on by policy initiatives, carbon-reduction schemes, and the increased use of unconventional gas

A rosy future

According to the International Energy Agency (IEA), global consumption of natural gas should increase by 49-65% over the 2011-35 period under its different demand scenarios. The agency highlights three key issues that could lead to the higher end of this natural gas consumption growth materialising:

• policy initiatives by various countries (not just Japan) to reduce dependence on nuclear power following the Fukushima disaster,

• carbon-reduction schemes, and

• the development of unconventional gas. As can be seen in the following chart, CO2 emissions in the US fell by 712mt, or -11%, over the 2007-12 period, partly due to increased fuel substitution towards shale gas. This meant that it saw the largest reduction in emissions among all countries or regions, and should provide future impetus for others to follow suit. Global CO2 emissions growth (2007-12)

Source: BP Energy Review 2013

If China is successful in discovering its own shale gas resources, this could be the biggest driver of emissions reduction over the next 10 years, in our view. It is an issue that the PRC Government would probably welcome keenly, given the air-pollution problems that have plagued the country over the past decade. According to the IEA’s projections, the vast bulk of the growth in gas demand is expected to come from non-OECD nations, particularly China and India, reflecting higher energy usage per capita as well as a rise in the share of energy derived from natural gas. In both countries, natural gas currently accounts for a relatively low proportion of energy consumption (see the following chart), but China in particular has a policy objective to roughly double the energy share of natural gas to more than 8% by 2015 in order to improve energy efficiency and energy diversification. Primary energy consumption by selected countries/regions

Source: BP Energy Review 2013

We also note that past LNG-demand projections have been conservative, as seen in the following chart, with forecasts revised up by nearly 35%, or about 70mtpa, in the space of three years. Top-four LNG importers in 2025E

Source: Wood Mackenzie

(712)(484)

8

432 482

847

2,697

(1,000)

(500)

0

500

1,000

1,500

2,000

2,500

3,000

US EU Japan Middle East India Rest of the World

China

(m tonnes)

23.9%

48.6%33.3% 29.6% 22.0%

8.7% 4.7%0%

20%

40%

60%

80%

100%

World Middle East EU/Eurasia US Japan India China

Gas Oil Coal Nuclear Hydro Renewables

0

25

50

75

100

125

Japan China India South Korea

2009 forecast 2012 forecast

(mtpa)Asia's top four importers of LNG may account for over 260mtpa of demand in 2025

Asia Oil & Gas Sector 5 July 2013

- 8 -

Demand-side factors to watch out for over the next 3-5 years

As can be seen in the following table, all of the major Asia countries depend on LNG as a fuel. Importantly, even traditional powerhouse LNG exporters such as Indonesia and Malaysia have, in recent years, been forced to import LNG to satisfy domestic power generation needs as they have moved away from coal or fuel oil-fired generation. Status of gas imports and exports for various Asia countries

Country Indigenous production LNG importer LNG exporter

Pipeline importer

Pipeline exporter

Japan South Korea Taiwan China Hong Kong India Thailand Indonesia Malaysia Singapore

Source: Daiwa

In this section, we examine a few demand-side factors that investors should watch out for over the next 3-5 years. LNG as a transportation fuel New LNG demand may come from using the gas as a transportation fuel. To date, this has been slow to happen due to the slow development of engine technology. However, we believe that in the next few years, this will be increasingly used as a fuel source. We note that in China, LNG fuel has already developed rapidly and LNG vehicles (both trucks and buses) are now being considered for long-distance routes. This should boost gas demand in China generally, and as a result may also increase the country’s LNG import demand. In addition, the use of LNG as a marine-transportation fuel has also been mooted in the past few years. However, the uptake has been disappointing due to a range of issues, such as the number of new ships being bought, the financing of a ship with new technology, charter agreements not encouraging the owners to reduce fuel-oil consumption, and a lack of LNG-refuelling infrastructure. Despite these factors, we believe that there is a positive outlook over the medium term as new environmental-protection agreements come into force. Both of these factors could result in an increase in LNG demand.

Economic recession Some Western economies, particularly in the EU, are still struggling economically, and as a result their future energy developments are unclear. This is likely to affect trade with Asia countries and may result in downward revisions to near-term Asia gas demand. Japan The world’s largest LNG market currently has a lot of uncertainty: first, regarding its long-term energy demand, and second, on the contribution that gas will make to the energy mix. The three broad options that have been under discussion range from 0-25%. In September 2012, the Japan Government proposed a nuclear-free energy policy by the 2030s, with a desire to get to that point before the 2030s. If this is implemented, then thermal-power generation, ie, LNG-based power generation, will take up the slack, in our view, and the proportion of gas within the power generation mix would increase materially. Options for Japan’s power generation mix in 2030

Source: Ministry of Economy, Trade and Industry (Japan)

Nuclear energy consumption of selected Asia countries

Source: BP Energy Review 2013

FSRU development New LNG demand is also likely to develop from a variety of new countries opting for FSRUs. According to Golar LNG, 50% of all new LNG import markets

15%25%

35%

30%25%

50%40% 35%

15% 15% 15%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Option 1 Option 2 Option 3

Nuclear Renewable Thermal Co-generation

0

50

100

150

200

250

300

350

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

China Japan S. Korea Taiwan

(Terawatt hours)

Asia Oil & Gas Sector 5 July 2013

- 9 -

since 2005 have opted for FSRUs rather than land-based terminals. The company attributes this to the fact that this technology is accepted by the oil majors, offer a low-cost/fast start-up option, provides access to high-value gas markets, and is flexible in terms of location (and mostly out of sight of the local population). We note that globally, about 25 projects are under development, although it is difficult to forecast accurately how many and how quickly they will develop. Global floating regasification fleet development

Source: Golar LNG

Shale gas competing with LNG As indicated in our China shale gas report published on 13 April 2012 (China shale: a long term paradigm shift), we believe that China shale gas is likely be a 2018+ play, while Indonesia shale gas may take even longer. The following chart points out the differences in terms of the accessibility and the ease of monetising shale in both the US and China. Key success factors in the US shale industry vs. China US China Rig and services availability Poor rig and services availability

Attractive geology Attractive geology Large domestic market Large domestic market Extensive pipeline network Extensive pipeline network Attractive fiscal terms Unknown fiscal terms

Supportive regulators Supportive regulators Landowners as royalty owners Government as royalty owners

Source: Daiwa

Note: Shaded areas represent poor characteristics

Currently, it looks as though the development of shale gas, and indeed other unconventional gas streams, in China will take some time. Despite the fact that the PRC Government has publicly stated that unconventional gas is a strategic imperative for the country, shale-gas exploration has yet to increase to the level where the 2015 production targets can be met, on our estimates. In March 2012, China’s National Energy Administration (NEA) released its targets for the

country’s shale-gas production. Apart from emphasising the need for foreign co-operation and better technology in developing the sector, the ambitious production targets include:

• 6.5bcm, or 229bcf of shale gas production by 2015, and

• 60-100bcm, or 2,118-3,530bcf of shale gas production, by 2020 (China’s 2010 gas production was 96.8bcm).

In our opinion, the shale-gas production target of 60-100bcm in 2020 is very bullish, as it implies a 56-73% CAGR over five years (2015-20). We believe the target is very ambitious and will be difficult to meet.

A brief analysis of LNG demand by country

China China’s gas demand has increased exponentially over the past decade and, as a result, looks set to change the country’s supply dynamics in the next few years. As can be seen in the following chart, the domestic gas supply has not been able to keep up with demand, and thus the country has had to build up its gas-import infrastructure. China: natural gas production vs. consumption

Source: BP Energy Review 2013

China now has a natural-gas market that comprises multiple supply sources with different prices (see the following map). As a result of this, price-tolerance levels vary greatly, depending on the income level for a province. We note that year-to-date in 2013, local governments have been reluctant to increase gas prices due to street protests. Nevertheless, the country has seen a rapid build-up of infrastructure over the past decade, and we believe this will continue for at least the next five years.

0

5

10

15

20

25

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014E

Newbuild Conversion

(No. of FSRU)

0

2

4

6

8

10

12

14

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Production Consumption

20-year CAGR:Gas production: 10.1%Gas consumption : 15.8%

(bcf/day)

Asia Oil & Gas Sector 5 July 2013

- 10 -

China: current and potential gas sources, and aggregate gas price (assuming price is oil indexed at USD95/bbl)

Source: Daiwa estimates

Note: * Due to start in 2H13

While natural gas’s share in China’s energy supply remained marginal in 2011, at only 5% of primary energy, demand has risen rapidly. Over 2001-11, natural-gas demand increased at a 17% CAGR, albeit off a low base. However, we note that gas demand is still small compared with coal demand in China. We attribute this to the following: 1) there are infrastructural constraints in the supply of domestic gas, and 2) coal prices continue to be cheap relative to gas. The main upside to gas demand over the next decade could come from an increase in the share of industrial feedstock usage and power generation, although we acknowledge that the latter may be difficult due to the pricing differential with coal. However, the government can assist in encouraging the use of gas-fired power generation by implementing supportive policies and subsidies. Shale gas. While shale-gas exploration activity is accelerating, large-scale commercial production

remains distant, and long-term production targets may be difficult to achieve. Shale-gas production: PRC Government targets vs. Daiwa forecasts

Source: Reuters, Daiwa forecasts

Note: Daiwa forecasts are combined shale gas and CBM production

Natural-gas price reform. This issue has been mooted for the better part of 12 months, and it remains

Potential gas imports

Potential new sources of domestic gas

Shale gas

CBM

CBM

LNG from Australia, Indonesia, Malaysia, Qatar:

USD15-18/mcf

Pipeline gas from Central and Eastern

Siberia:USD10-12/mcf

Pipeline gas from Central Asia:

USD11-12/mcf

Pipeline gas from Myanmar*:

USD8-9/mcf

Shale gas

CBMCurrent gas imports

229.5

2,824.0

353.0 529.5

0

500

1,000

1,500

2,000

2,500

3,000

2015E 2020E

PRC Gov't targets Daiwa forecasts

(bcf/year)

Asia Oil & Gas Sector 5 July 2013

- 11 -

to be seen whether China’s new government, which came into power in March 2013, will proceed with these reforms. The key obstacle is political, given that local governments in China have been complaining vociferously about high prices, and thus the central government will have to manage this issue. The country’s build-up of LNG receiving terminals, which reflects its strong LNG-demand outlook, has continued over the past year. These include the following.

• CNOOC’s first FSRU: in early 2012, the company began building an FSRU to be moored southeast of Nanjiang port in Tianjin harbour, Bohai Bay. Phase 1 of the project is due to start up in 2H13 and will be able to handle 2.2mtpa, while Phase 2 (start-up in 2015) would add a 3.8mtpa onshore terminal and include four 160,000m3 tanks.

• In mid-2012, China’s National Development and Reform Commission (NDRC) approved CNOOC’s plans to build a second LNG terminal in the southern city of Shenzhen. The Diefu terminal will be able to receive 4mtpa, although a start-up date has not been announced. Supporting its operations will be four 160,000 m3 LNG tanks.

• In late 2012, CNOOC commissioned its fourth LNG-receiving terminal, in Ningbo, Zhejiang Province, capable of importing 3.5mtpa.

• Sinopec’s proposal for a 3mtpa LNG receiving terminal in Lianyungang port, in eastern Jiangsu Province, received approval from the NDRC in 2Q13.

Japan Japan’s LNG-consumption patterns have changed markedly in the post-Fukushima disaster period, with LNG purchasing having been stepped up to plug the energy gap. Between 2010 and 2011, the country increased its LNG imports by 12.2% YoY; this was followed by another large increase of 11.1% YoY for 2012. While Japan saw a 9.8% YoY decline in LNG imports for May 2013, this was mainly the result of a sharp rise in fossil-fuel imports in May last year, as the country’s entire nuclear capacity was offline. Since then, two nuclear reactors have resumed operation, slightly easing the demand for imported fossil fuels. Japan’s new Nuclear Regulation Authority (NRA) is due to start safety checks of reactors that are currently idle before allowing them to restart. However, the NRA has said that these checks will take at least six months. According to estimates from Chevron, the nine-year period from 2011-20 may see Japan consume 96m tonnes more LNG than Chevron’s previous estimates prior to the Fukushima disaster. Assuming an LNG

price of USD10/mcf (ie, lower than current LNG prices), this would equate to an incremental USD50bn gas-import bill, which may have negative ramifications for the domestic economy. Japan: gas consumption vs. nuclear-power generation

Source: BP Energy Review 2013

Malaysia The country’s strong desire for supply diversity stems from the fact that gas production in peninsula Malaysia has been stagnant at about 6bcf/day since 2005, which has resulted in limited additional investment in new industries such as glass and plastics. Malaysia: natural-gas production vs. consumption

Source: BP Energy Review 2013

As a result, the government has plans, similar to those in Indonesia, to use imported LNG, with the 3.8mtpa Melaka LNG import terminal receiving its first cargo in April 2013 from Nigeria. Petronas has signed three LNG-import agreements in place at present: a 2.5mtpa 3.5-year contract with GDF Suez starting from August 2012, a 1.5mtpa 20-year contract with Qatargas starting in 2013, and an agreement with Statoil with undisclosed terms. The bulk of the country’s gas reserves are in east Malaysia, where the nine-train Bintulu LNG project is located. However, all of this gas is committed for exports, mainly to North Asia. Thus, we believe that

0

50

100

150

200

250

300

350

0

2

4

6

8

10

12

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Gas consumption (LHS) Nuclear consumption (RHS)

(bcf/day) (Terawatt hours)

0

2

4

6

8

10

12

14

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Production Consumption

(bcf/day)

20-year CAGR:Gas production : 5.4%Gas consumption : 7.2%

Asia Oil & Gas Sector 5 July 2013

- 12 -

any new gas finds in the country may be allocated to domestic usage. Indonesia The country has, in our view, been one of the most aggressive in Asia in re-focusing its gas resources for internal use rather than exporting them as LNG. This is because of its steady gas demand CAGR of 3.9% over the 1990-11 period, reaching an average of 3.46bcf/day in 2012. At the same time, Indonesia’s gas production has been stagnant at about 7.0bcf/day over the past 10 years, leading to concerns in the government that too much gas is being exported at the expense of domestic consumption. Indonesia: natural-gas production vs. consumption

Source: BP Energy Review 2013

As a result, we believe that an increasing share of new gas supply will be allocated to serve the domestic market, as there is unfulfilled gas demand in different regions for industry and power generation. While these two segments have readily available capacity or infrastructure to consume gas, they have no access to required supplies, which led the country to trigger the domestic-market obligation clauses in gas-sale contracts to supply industry and power generation. Thus, Indonesia’s first FSRU was put into operation in 2012, while another three are due to come onstream between 2014 and 2016. One positive move undertaken by the government was to increase gas prices in 2011 to reflect more accurately market dynamics. Over the next five years, continued regulatory support will be important to ensure that gas supply continues to increase. In 2Q13, Bloomberg news reports indicated that the LNG selling prices at various export projects were likely to be negotiated upwards. Over the next five years, Indonesia has a very active construction programme for both LNG export and import terminals.

• Abadi LNG. In early 2013, Inpex (operator and 60% owner) awarded the front end engineering and design contract for a 2.5mtpa FLNG vessel to develop the Abadi gas field off the Tanimbar Islands, Indonesia. The vessel will also have a condensate production capacity of 8,400bpd.

• Tangguh LNG expansion. In late 2012, the Indonesia Government approved BP’s plan to build a third LNG train at its Tangguh LNG project, which could cost about USD2bn. The train should add 3.8mtpa of liquefaction capacity at Tangguh and raise its total capacity to 11.4mtpa. BP Indonesia said the new train would sell 40% of its production in Indonesia, while the rest would be exported to buyers in the Asia-Pacific region.

• The first of four potential FSRUs. In mid-2012, Nusantara Regas (a joint venture between Pertamina and PGAS) started up the country’s first FRSU, a 3mtpa vessel in Jakarta Bay, West Java. In 1H14, PGAS will start up Indonesia’s second FSRU at Lampung in South Sumatra, while other plans call for an extra two FSRUs to be installed in the Sumatra-Java area by 2018.

India In the early 2000s, the future appeared bright for India’s natural-gas supply given large gas discoveries in the Krishna-Godavari basin off the country’s east coast. However, the reality has been far different, with insufficient natural-gas infrastructure built at the national level to meet domestic demand. As a result, India has had to rely increasingly on imported LNG, which is used as a substitute for coal for electricity generation. According to the latest data from the US Energy Information Administration, India’s power and fertiliser sectors accounted for 45% and 28%, respectively, of the country’s natural gas demand for 2010. The government has categorised these as priority sectors for domestic programmes, which ensures that they receive larger shares of any new gas supply than other consumers. The country’s 20-year CAGR in gas consumption (1992-2012) has outstripped supply, at 9.0% and 5.1% respectively. In 2012, India imported 15.1m tonnes of LNG, which accounted for about 38% of total gas demand in the country. India’s Ministry of Petroleum and Natural Gas projects that this trend of higher LNG imports will continue, with the country’s gas demand more than doubling over the next five years to 2018.

0

2

4

6

8

10

12

14

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Production Consumption

20-year CAGR:Gas production : 1.7%Gas consumption : 3.5%

(bcf/day)

Asia Oil & Gas Sector 5 July 2013

- 13 -

India: natural-gas production vs. consumption

Source: BP Energy Review 2013

The build-up of the country’s LNG importing infrastructure has faced material delays, as can be seen from the list of planned terminals mentioned below. Such delays, along with other wrangling among companies and the central and/or state governments, has prompted Wood Mackenzie and other industry analysts to caution LNG suppliers against counting too much on industry segments in India as a source of demand over the near-to-medium term. Currently, India has four LNG-receiving terminals, of which the Kochi and Dabhol terminals were only commissioned in 2013 (the other existing ones are located at Dahej and Hazira).

• The 5mtpa Kochi LNG receiving terminal, on which construction started in 2007, was finally commissioned in 1Q13 after having been delayed from its original start-up of 2010. Even then, the lack of pipeline capacity feeding the terminal will hold its initial operations to less than 1mtpa for at least a year, according to Petronet.

• In early January 2013, GAIL India commissioned its 5.0mtpa Dabhol LNG terminal at Ratnagiri, Maharashtra, about 210 miles south of Mumbai. The company has said that the new terminal should be expanded to a capacity of 7.5mtpa over the next 2-3 years, and thereafter to 10.0mtpa.

The Philippines The country’s only gas field, the offshore Malampaya field operated by Shell, has been producing for 11 years, with production from this field going into power generation, the industrial sector, and CNG for transportation. Currently, the Malampaya joint venture (made up of Shell, Chevron and the Philippine National Oil Company) is working on Phase 2, which aims to extend the life of the field beyond 2023. Nevertheless, we believe that the country may need to develop an LNG-import capability if it is to expand its gas demand beyond the current customer base. In our view, the

country’s gas consumption is constrained only by the lack of an indigenous gas supply. We note that incremental power generation in the Philippines is geared towards coal-fired power plants, implying that natural gas will lose market share over time. Even if new sources of gas are discovered offshore Philippines, the mountainous terrain of the country and its geographic fragmentation may make supply a challenge. Thailand The country’s gas consumption, led by industrial and petrochemical demand, increased at a CAGR of 12.6% over the 1992-2012 period. However, its production CAGR over the same period was lower, at 8.2%. As a result, it has had to rely on gas imports from Myanmar since 2001 to meet in its demand needs, which is why we present an aggregated picture of the two countries’ production data in the following chart compared with Thailand’s consumption. Thailand & Myanmar: natural-gas production vs. consumption

Source: BP Energy Review 2013

Thailand’s LNG import strategy, implemented three years ago, was driven by its expectation that its major source of gas, the Gulf of Thailand, would hit peak production in the following 10 years, and thus the country could face a natural decline in reserves over the next 10-15 years. In addition, the recent opening up of Myanmar, and its potential industrialisation, could lead to less gas being available for consumption by Thailand in the foreseeable future. As recently as three years ago, the country raised the issue of nuclear power, but with the Fukushima disaster, these plans have been shelved. As a result, the government has accelerated plans to expand its current 5mtpa LNG regasification facility to 10mtpa in the next three years. The country currently imports LNG from Qatar, and over the long term could see LNG imports from PTT Exploration & Production’s (PTTEP TB, THB159, Sell, covered by Thanachart Securities)

0

2

4

6

8

10

12

14

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Production Consumption

20-year CAGR:Gas production: 5.1%Gas consumption : 9.0%

Demand gap met by LNG imports

(bcf/day)

0

2

4

6

8

10

12

14

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Thailand Myanmar Thailand consumption

20-year CAGR:Thailand's gas production: 8.2%Myanmar's gas production: 14.4%

Thailand's gas consumption : 12.6%

(bcf/day)

Asia Oil & Gas Sector 5 July 2013

- 14 -

proposed floating LNG project at the Cash/Maple gas field offshore Australia.

What is Daiwa’s demand forecast for LNG?

In our modelling (shown in the following chart), we forecast a 5.2% CAGR for LNG demand in the region over the 2011-25 period. This is based on the following assumptions:

• Asia GDP growth averages about 4% annually over the period, and

• Japan reduces its dependence on nuclear power from 25% to 15% of its primary energy demand.

In 2025, Japan is still likely to be the largest import market for LNG globally, with China moving into second place, and India and Korea in third and fourth, respectively. As a result of our modelling, we arrive at a demand gap of 155mtpa of LNG in 2025. In the next section of this report, we look at where the new supply could come from – both regionally and globally – to fill this gap for Asia. Asia-Pacific LNG demand vs. supply model

Source: Daiwa forecasts

Global LNG demand vs. supply model

Source: Daiwa forecasts

0

50

100

150

200

250

300

350

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

E20

14E

2015

E20

16E

2017

E20

18E

2019

E20

20E

2021

E20

22E

2023

E20

24E

2025

E

Supply - operational

Supply - under construction

(mtpa)

Asia-Pacific demand

Demand gap of 155mtpa in 2025

0

100

200

300

400

500

600

2012

2013

E

2014

E

2015

E

2016

E

2017

E

2018

E

2019

E

2020

E

2021

E

2022

E

2023

E

2024

E

2025

E

Supply Demand - Mid-case

Demand - Low-case Demand - High-case

(mtpa)

Asia Oil & Gas Sector 5 July 2013

- 15 -

Supply growth outlook appears strong

Our analysis indicates that global LNG capacity could more than double by 2021, thus creating a buyers’ market

A suppliers’ market in the next five years, but things will change

In the next five years out to 2017, we believe the global LNG market will remain reasonably tight given that within this timeframe, the demand/supply balance favours LNG suppliers over buyers due to robust new LNG demand in Japan and several other markets, and expected delays in new Australian supply projects. As a result, LNG imports are likely to be needed from the Middle East and the Atlantic Basin to keep the Asian market in equilibrium. Thus, short-term freight rates will likely remain strong due to these longer distance trade flows. A different world expected post 2017 We estimate that project sponsors globally are currently developing 35 projects (total unrisked capacity is 230mtpa) with most of these projects in competition to supply Asia. As can be seen in the chart below, we forecast a peak of around 410mtpa of global LNG capacity in 2020 with a natural decline taking over thereafter. Historical and forecast LNG supply

Source: Cedigaz, IEA, Daiwa estimates

Increasingly, unconventional gas supply is being planned as feedstock for these new LNG export projects. According to the IEA, 65% of global natural gas supply growth will come from unconventional sources over the 2010-35 period, as seen in the chart below. However, we note that 390bcm, or one-third, of this projected growth will come from China, which we view as overly optimistic given the current mixed results being reported by its shale gas exploration program. Nevertheless, even if we were to risk China’s unconventional gas supply at 50%, the total amount of 1,625bcm of gas supply would appear to make it a buyers’ market within the next five years. IEA: natural gas supply growth forecasts from 2010-35

Source: IEA

Over the past two years, conventional LNG project proponents have cited the possible levels of North American LNG exports from 2020 onwards as being a key risk factor that could see lower LNG prices, and therefore returns. Currently, nearly 20 permits to build around 150mtpa of capacity have been filed, which represents about one-third of US natural gas production in 2011. According to BG Group, between 20mtpa and 40mtpa of this 150mtpa may be in operation by 2020 and up to 60mtpa by 2025.

Global LNG projects in detail

In the table below, we present a list of global LNG plants that we think are likely to come onstream by 2018, which totals some 160mtpa of LNG. Importantly, this list excludes FLNG as well as most of the proposed North American LNG projects. If we include the FLNG projects and the North American projects, this would add another 193.6mtpa of LNG (28.3mtpa of FLNG and 165.3mtpa from North America) resulting in nearly 354mtpa of unrisked LNG supply by around 2020/21. Should all of this capacity come onstream, this would increase global LNG

0

50

100

150

200

250

300

350

400

450

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

E20

14E

2015

E20

16E

2017

E20

18E

2019

E20

20E

2021

E20

22E

2023

E20

24E

2025

E

(mtpa)

0

200

400

600

800

1,000

1,200

1,400

Conventional Unconventional

MENA

Russia

Rest of the World

China

USA

AustraliaIndiaEU

Rest of the World

IndonesiaCanada

(bcm)

Asia Oil & Gas Sector 5 July 2013

- 16 -

capacity by 126% from 282mtpa as at January 2013 to 636mtpa by around 2020/21, as shown in the chart below. Clearly, this would more than adequately supply the Asia-Pacific market – and even if we were to discount some of these projects, we still believe the weight of future supply would likely exert downward pressure on LNG prices. Potential global LNG capacity additions: 2013-21

Source: Daiwa estimates

Another factor that we have not taken into account is that of Asian shale gas, which we think bears careful monitoring in the next few years. How quickly or how

materially it will develop is unclear, but the potential is starting to emerge in North America, with several project sponsors and Asian buyers progressing a variety of new LNG plants to export unconventional gas. Longer term, shale gas developed directly in Asia could also become a new competitor to LNG, particularly if it is developed in China as a cost-effective alternative to LNG imports. As a result, it can be clearly seen from the many LNG plans that the market will remain a buyers’ one for the next decade. However as a cautionary note, we would add that the LNG industry has tended to overestimate supply growth, especially given what the future could hold: more and more expensive projects being developed in new locations and geography. Apart from the higher levels of complexity in such new locations and geography, higher levels of sovereign risk must also be taken into account. And as can be seen in Australia’s LNG industry, when so many projects compete for the same material and human resources, delays and cost escalations are inevitable.

Global LNG projects due to come onstream between 2013 and 2019 Project Participants Start-up Capacity Cost Cost Current status mtpa USDm USD/t Conventional gas Angola LNG Sonangol, Chevron, BP, Total, ENI 2Q13 5.2 10,000 1,923 ConstructionDonggi-Senoro LNG Medco Energi, Pertamina, Mitsubishi, Kogas 4Q14 2.0 3,700 1,850 ConstructionGorgon LNG Shell, Exxon, Chevron, Osaka Gas, Tokyo Gas, Chubu Electric 2Q15 15.6 55,000 3,526 ConstructionIchthys LNG Inpex, Total 4Q16 8.4 34,000 4,048 ConstructionPNG LNG Exxon, Oil Search 2Q14 6.9 19,000 2,754 ConstructionSabine Pass LNG Cheniere 3Q15 18.0 6,000 333 ConstructionWheatstone LNG Chevron, Apache, Kufpec, Kyushu Electric, Tokyo Electric 3Q16 8.9 29,000 3,258 ConstructionBrass LNG NNPC, EBI, ConocoPhillips, Total 2016 10.0 15,000 1,500 PlannedGulf LNG InterOil 2016 3.8 9,300 2,447 PlannedMozambique LNG Anadarko, PTTEP, BPCL, Videocon 2018 20.0 N/a N/a PlannedOlokola LNG NNPC, Shell, Chevron N/a 11.0 N/a N/a PlannedYamal LNG Novatek, Total 2017 16.5 20,000 1,212 PlannedTotal 126.3 X Unconventional gas Australia-Pacific LNG ConocoPhillips, Origin Energy, Sinopec 2015 9.0 25,200 2,800 ConstructionGladstone LNG Santos, Petronas, Total, Kogas 2015 7.8 18,500 2,372 ConstructionQueensland Curtis LNG BG 2014 8.5 20,500 2,412 ConstructionFisherman's Landing LNG LNG Ltd 2015 3.8 1,700 447 PlannedKitimat LNG Chevron, Apache 2015 5.0 4,500 900 PlannedBC LNG LNG Partners LLC 2019 1.8 N/a N/a PlannedTotal 34.1

Source: Companies, Daiwa

282

636

126 34

165 28

0100200300400500600700

LNG

cap

acity

as

at

Jan

2013

Conv

entio

nal L

NG

Unco

nven

tiona

l LNG

N. A

mer

ica

LNG

FLNG

Tota

l by

2021

(mtpa)

An addition of 354mtpa of capacity

Asia Oil & Gas Sector 5 July 2013

- 17 -

New supply routes have opened up in the past five years

Over the past five years, the shale gas revolution in North America has opened up both Canada and the US as potential new LNG supply sources for Asia. In addition, the tremendous exploration success seen in East Africa – and in particular Mozambique – has potentially planted that region as a future LNG exporter by the end of this decade. We estimate that, assuming peak production in the early 2020s, these three areas could contribute around 242mtpa to the global LNG trade on an unrisked basis. Relative ranking of key development issues and risks (note: 1 = good, 3 = bad) Issue USA Canada E.Africa Comment Level of overall infrastructure required

Full value chains needed in E. Africa; Upstream and pipelines required in Canada; less overall infrastructure needed in the US.

Risk of not getting export permits

Canadian and E. African Governments reasonably committed to large-scale exports. US situation more fluid.

Financing risk Financing is a major issue for all supply basins, bigger one for greenfield plays.

Reserve risk Limited resource risk in all three supply regions.

Contractual complexity Canada/E. Africa offering a bundled FOB/Ex-ship deal. US. is complicated requiring multiple agreements.

Opposition to Governments’ direct/indirect involvement

E. African projects enjoy direct support of host governments while Canada is pro-project. US political leaders likely to be more cautious.

Political risk

Source: Galway Group

Canada – British Columbia Like the US, Canada has seen a similar amount of shale gas plays being opened up by oil and gas companies. The country has a number of prospective shale gas targets in various stages of exploration and exploitation in British Columbia, Alberta, Saskatchewan, Ontario, Quebec, New Brunswick and Nova Scotia. While the country has negligible shale gas production due to the lack of demand within the country, and the US gas-export market being closed off due to low natural gas prices, the natural inclination for land owners is to look westwards towards the lucrative Asian LNG markets. As a result, there are currently four projects planned to come onstream between 2018 and 2019 with a total of 42mtpa of capacity.

Canada: planned and proposed LNG export terminals

Canada Partners Quantity

(mpta) Approval

statusProposed

start-upKitimat LNG Apache, Chevron 2 x 5.0 Approved 2016Petronas LNG Petronas, Japex 3 x 6.0 Review 2018BC LNG LNG Partners 1.8 Approved 2019Shell LNG Shell, Kogas, Mitsubishi,

PetroChina 12.0 Approved 2020

Total 41.8

Source: Companies

Of Canada’s four projects, the three that have received approvals are:

• Kitimat LNG: The two-train Kitimat LNG project, targeting start-up in 2016, is in front-end engineering and design at present. Its National Energy Board licence allows export of 10mtpa. In January 2013, Chevron entered the project by announcing plans to buy 50% of Kitimat LNG and the proposed Pacific Trail Pipeline, and 50% in 644,000 acres in the Horn River and Liard shale gas basins in British Columbia.

• BC LNG: In 2012, Canada’s Ministry of Natural Resources approved a 20-year export licence for the BC LNG Export Cooperative following similar approval by the NEB in February 2012 for export capacity of 1.8mtpa. The company is owned by LNG Partners LLC, Houston, and HN DC LNG LP, each with 50%.

• Shell LNG: Received approval in early 2013 from Canada’s National Energy Board (NEB) to export its proposed plant near Kitimat, British Columbia. The license authorises the company to export up to 24mtpa for 25 years with start-up targeted for 2020. This project is a joint venture of Shell Canada (Not rated), Korea Gas (Not rated), Mitsubishi Heavy Industries (7011 JP, JPY596, Buy [1]), and PetroChina (857 HK, HKD8.96, Outperform [2]).

US Gulf Coast According to our estimates, the US has around 151mtpa of planned LNG export projects (on an unrisked basis) that could come onstream in the next 5-8 years. This 151mtpa represents 45% of the global LNG trade movements in 2011 which is a significant expansion of LNG export capacity, if it all comes to fruition. LNG markets in Asia, Europe and Latin America have been watching the debate in the US over whether it would allow LNG exports of some or none of its shale gas. In December 2012, under commission from the US Department of Energy, NERA Consulting issued a report on the likely effect of US LNG exports on the domestic economy.

Asia Oil & Gas Sector 5 July 2013

- 18 -

Its scenario analysis for global LNG supply and demand concluded that in all its cases, US LNG exports would not harm the US economy, and that its forecast increase in Henry Hub gas prices would be modest as a result of such LNG exports. Post this report, the LNG industry is awaiting decisions on several proposed US LNG export projects, especially those requesting approval to export to countries with which the US does not have a Free Trade Agreement (FTA). US: planned and proposed LNG export terminals Project name Location Quantity Approval status Proposed (mtpa) DOE FTA DOE non-FTA FERC Start-upSabine Pass LNG Sabine Pass, LA 17.0 Approved Approved Approved 2016Freeport LNG Freeport, TX 2 x 10.8 Approved Review Prefield 2017Cameron LNG Cameron, LA 13.0 Approved Review Prefield 2017Cove Point LNG Cove Point, LA 7.7 Approved Review n/a 2017Lake Charles LNG Lake Charles, LA 15.5 Approved Review Prefield 2018Jordan Cove LNG Jordan Cove, OR 15.5 Approved Review Prefield 2017Carib Energy LLC n/a 0.3 Approved Review n/a n/aGulf Coast LNG Brownsville, TX 21.6 Review Review n/a 2018Gulf LNG Pascagoula, MS 11.6 Approved n/a n/a n/aCambridge Energy n/a 2.0 Review n/a n/a n/aOregon LNG Warrenton, OR 9.7 Approved Review Prefield n/aSB Power Solutions n/a 0.5 Approved n/a n/a n/aSouthern LNG Co. n/a 3.8 Approved n/a n/a n/aExcelerate Liq. Solutions

Port Lavacca, TX 10.7 Under review

n/a n/a n/a

Total 150.5

Source: Companies, Federal Energy Regulatory Commission

Note: FTA = Free Trade Agreement countries only; Prefield = pre-project field studies

Thus far, only the Cheniere Energy-led Sabine Pass LNG project has received all the export approvals and begun construction. In 1Q13, Cheniere Energy (Not rated) filed with the US Federal Energy Regulatory Commission (FERC) to add a fifth and sixth LNG train to the Sabine Pass project, as well as filed with the US Department of Energy for approvals for those trains to export to both FTA and non-FTA countries. To illustrate the demand for US LNG, all of the capacity from trains 1-4 has already been sold to BG (5.5mtpa), Gas Natural Fenosa (3.5mtpa), Kogas (3.5mtpa), and GAIL (3.5mtpa). Alaska – another potential new supply source for Asia? Between 2010 and 2012, two separate groups proposed a c.1,800km mostly buried pipeline from the Prudhoe Bay field on Alaska’s North Slope (ANS) to South-central Alaska where a 15-18mtpa LNG export plant and port would be located. These two groups are: 1) ExxonMobil, ConocoPhillips and BP, which are the main ANS oil and gas producers, and the Canadian pipeline company TransCanada, and 2) the Alaska Gasline Port Authority, which has proposed a government-owned Valdez LNG project.

While the Alaskan Gasline Port Authority does not have any capex estimates as yet, the ANS producers have estimated their project will cost between USD45bn and USD65bn, which includes the cost for a gas treatment plant, the liquefaction plant, as well as infrastructure such as the pipeline, and an LNG storage and a tanker terminal. At a construction cost of USD3,000-3,600/tpa, this project would be at the expensive end of LNG projects globally. Alaska’s natural gas projects

Source: Office of the Federal Coordinator for Alaska Natural Gas Transportation Projects

Mozambique, East Africa According to Anadarko, the 10mtpa USD15bn Mozambique LNG project has about 35tcf to over 65tcf of recoverable natural gas as feedstock. Importantly, it could be starting LNG exports in 2018 and producing around 20mtpa by 2020. Mozambique: discovery and reserves announcement timeline

Source: Anadarko, ENI

0

20

40

60

80

100

120

140

Jan-

10

Mar

-10

May

-10

Jul-1

0

Sep-

10

Nov-

10

Jan-

11

Mar

-11

May

-11

Jul-1

1

Sep-

11

Nov-

11

Jan-

12

Mar

-12

May

-12

Jul-1

2

Sep-

12

Nov-

12

(tcf)

1st d

isco

very

2nd

disc

over

y3r

d di

scov

ery

4th

disc

over

y

1st a

ppra

isal

wel

l

Asia Oil & Gas Sector 5 July 2013

- 19 -

Three new global LNG trade routes that should open up from 2015 onwards

Source: BG, Daiwa

Rising construction costs

Over the past 15 years, we have witnessed significant cost inflation in the construction of greenfield LNG plants. In the 1980s, the cost of building a greenfield LNG liquefaction plant was around USD350 per tonne of annual LNG production. The cost had dropped to around USD200 per tonne by the early 2000s as materials and energy costs declined on the back of lower energy prices, but started to skyrocket from 2004, reaching around USD1,000 per tonne by 2008. Why did costs escalate so sharply from 2004-08?

• Low availability of engineering, procurement and construction (EPC) contractors as a result of the extraordinarily high number of oil and gas projects globally in the mid- to late-2000s.

• High raw-material prices as a result of the surge in demand from fast-growing economies such as China.

• A lack of skilled and experienced workers in the LNG industry.

• The devaluation of the US Dollar against most global currencies.

In addition, we note that several new projects that were started post 2008 have seen their costs escalate due to their complexity, geography, environmental constraints or lack of infrastructure. Given the fact that so many projects are now using pioneering technology (coal-bed methane feed gas, floating liquefaction, deepwater, CO2 sequestration etc), we think it is realistic to expect that, barring a new breakthrough in construction costs, new LNG projects will generally be more expensive than in the past. Current LNG construction costs versus historical levels

Source: Companies, Daiwa estimates

British Columbia to Japan3,950 nautical miles

US Gulf Coast to Japan9,300 nautical miles

East Africa to Japan6,750 nautical miles

Traditional LNG trade routes:Qatar to Japan6,300 nautical milesAustralia to Japan3,700 nautical miles

350 200 4001,000

2,502 2,528

3,700

0500

1,0001,5002,0002,5003,0003,5004,000

1980

s

Early

200

0s

Mid

200

0s

Late

200

0s

Conv

entio

nal L

NG

Aust

ralia

n CB

M-

base

d LN

G

FLNG

(USD per tonne of annual LNG production)

Current LNG construction costs are 2.5x those seen

five years ago

Asia Oil & Gas Sector 5 July 2013

- 20 -

Construction costs at the project level at present

Source: IEA, Companies

Note: Dark blue = producing; light blue = proposed; orange = under construction; Sabine Pass relates only to Phase 1; East Africa LNG costs are a range of estimates

Australian costs: the only way is up Just in the past 18 months, we have seen Australia’s large LNG production projects announcing big cost overruns. Nevertheless, the projects’ construction schedules are continuing apace.

• A 6% cost overrun at Woodside’s AUD15bn one-train 4.3mtpa Pluto LNG project in the Carnarvon Basin, Western Australia, which started operations in 2Q12, one year behind schedule.

• A 15% cost increase for Santos’s two-train, 7.8mtpa coal-bed methane-based Gladstone LNG project in Queensland, in northeast Australia. In addition, the company said it needs to find more feedstock gas ahead of the AUD18.5bn project’s planned 2015 start-up.

• A 36% cost increase for BG Group’s two-train, 8.5mtpa Queensland Curtis Island LNG project. This cost increase to USD20.4bn, up from USD15bn, was attributed to regulatory costs, changes to the project, and a stronger Australian dollar.

• A 41% cost increase for Chevron’s Gorgon LNG expansion to USD52bn versus the USD37bn cost estimate when the project received Final Investment Decision in September 2009. While around USD5bn of this increase has been attributed to the strong Australian Dollar, poor productivity at the remote Barrow Island site off Western Australia, labour costs and weather delays have also taken a toll. Apart from the cost increase, first cargoes from the project have been delayed until 1Q15 instead of late 2014.

In addition, we also highlight the 20% cost increase to USD19bn that ExxonMobil announced for its PNG LNG project in Papua New Guinea in November 2012. This was attributed to unfavourable exchange rates, delays caused by disgruntled workers and landowners.

Fortunately for the project, there has been no delay to its start-up and delivery of gas in 2014. Shipping costs have also been increasing We note that the new LNG supply routes (such as from the US, Canada or East Africa) are now generally moving the cargoes longer distances to market. When more trade flows move from the US Gulf Coast (USGC) to Asia in the latter part of this decade, the shipping distances will be nearly 10,000 nautical miles, which is double the average shipping journey for a traditional route like Australia-to-Japan. According to CWC Insights, shipping costs from the USGC to Asia could be around USD4/mcf by 2015 which we note is much higher than Cheniere Energy’s estimate of USD3/mcf. Delivery cost of LNG to Asian markets

Source: Cambridge Energy Research Associates

Moving towards a more liberalised LNG supply market

With the large number of LNG projects coming onstream globally over the next 10 years, especially if new North American exports develop a critical mass and LNG projects are owned by a new group of sellers, we believe new business models may also emerge which could lead to a more liquid and more liberalised LNG market compared to what we have today. Already, we have seen various companies moving towards such a change and it is highly likely that the LNG market of today will be less restrictive and more liberalised going forward. These new business models include:

• Free On Board (FOB) sales at Henry Hub pricing and full destination flexibility, which may reduce short-term volatility in pricing.

• Utility companies have been farming into upstream acreage in the US in order to form a vertically

800

940

1,00

0

1,02

6

1,50

0

1,73

1

1,85

0

2,08

3

2,40

0

2,75

4

2,80

0

3,25

8

3,33

3

3,50

0

3,65

1

4,04

82,50

0

0500

1,0001,5002,0002,5003,0003,5004,0004,500

Sabi

ne P

ass

Kitim

at L

NG

Darw

in

Qat

arga

s 4

East

Afri

ca L

NG

Ango

la L

NG

Dong

gi-S

enor

o

Sakh

alin

2

Que

ensl

and

Curti

s

PNG

LNG

APLN

G

Whe

atst

one

Gor

gon

Prel

ude

FLNG

Plut

o

Icht

hys

(USD per tonne of production)

1.90 1.503.80 2.50

4.80 5.00 4.30 3.002.60

3.30 4.20

4.20 6.004.30 2.50 4.50

4.70

1.30

0.502.30

0.80 0.70 1.10 2.70 1.70 3.10

0.002.004.006.008.00

10.0012.0014.00

Mid

dle

East

Brow

nfie

ld

Paci

fic

Brow

nfie

ld

W. A

frica

G

reen

field

Paci

fic

Gre

enfie

ld

Paci

fic

Gre

enfie

ld

WC

Cana

daG

reen

field

USG

CBr

ownf

ield

E. A

frica

Gre

enfie

ld

Arct

icG

reen

field

Upstream Liquefaction Shipping

Asian oil-indexed LNG price (2015-2035)

(USD/mcf)

Asia Oil & Gas Sector 5 July 2013

- 21 -

integrated supply chain, mostly as a risk management technique. We see the trend continuing.

• LNG buyers building a diversified portfolio of supply from a variety of sources and business models in order to balance and manage their contractual and operational procurement risks.

• An Asian short-term pricing index may evolve which would be the reference for both physical and paper transactions.

• The emergence of a secondary market for LNG due to the potential influx of players in the market which would increase liquidity, thus allowing buyers and sellers to optimise their portfolios and balance their short-term supply and demand needs using short-term sales. Thus, the market would need to move away from individual sellers’ Master Sales Agreements and adopt standard general terms and conditions for buying and selling spot cargoes.