Lloyd’s lass of usiness Event Political Risks 18th April...

45

Lloyd’s Class of Business Event Political Risks 18 th April 2013, Vienna, Austria BPL Global | 18 April, 2013 PRI Market – An Overview

Transcript of Lloyd’s lass of usiness Event Political Risks 18th April...

Lloyd’s Class of Business Event Political Risks 18th April 2013, Vienna, Austria

BPL Global | 18 April, 2013

PRI Market – An Overview

2

BPL Global

• Political Risk Insurance (PRI) broker

• Founded 1983

• Located in London, Paris, Hong Kong, Singapore

• Independent, employee owned

• International client base:

– major corporations and financial institutions

• Global Partners: USA, Italy, Brazil, Chile

3

BPL Global’s Focus

ECAs - Hermes, EKN, Exim,etc

- Some short term (ST)

- Mainly MLT* business

Monoline Credit

Insurers - Euler Hermes, Atradius, etc

- Short term, multi-buyer business

- About USD 6 – 7 billion premium

PRI Market

- Special & single risks

- Emerging markets focus

- About USD 1.5 billion premium

* MLT = medium and long term

4

PRI Market: Overview

Political

Risks

Non-Payment

Risks

Investment

insurance

• Equity form

• Lenders form

• Property damage

• Business interruption

• War Risks:

• Long, large,

and/or complex

risks for

exporters and

traders

• Trade finance

• Commodity finance

• Export finance

• Project finance

• Sovereign lending

• Corporate lending

Property based

political risk

insurance

Speciality trade

credit

Insurance

Credit

insurance

for banks

Emerging Market Risks

Risks related to political and

economic conditions in a

foreign country

• Civil unrest

• Terrorism

• Rebellion

• War/Civil War

• Confiscation

5

PRI Market: Insurers by rating

Companies:

AA Ducroire/ONDD

HCC

AA- ACE

Euler Hermes

Inter Hannover

Sovereign Risk

Zurich

A+ FCIA

QBE

A Aspen

Atradius (A.M. Best)

AXIS

AIG

Lancashire

Markel

A- Catlin Bermuda

Ironshore

Liberty International

Coface (Unistrat)

XL

Lloyd’s:

A+ Amlin

Ark

Ascot

Beazley

Catlin

Chaucer

Hardy

Hiscox

Kiln

Liberty LSM

Limit/QBE

MAP

Marketform

Novae

Pembroke

Starr

Talbot

6

Sovereign (ECA) ratings

AAA Germany

Netherlands

United Kingdom

Canada

AA+ USA

France

Austria

AA/AA- Belgium

China

Saudi Arabia

A/A- Brazil

South Africa

BBB+ Italy

Russia

BBB- India

Spain

7

Catlin

AIG

ONDD

Sovereign

Zurich

ACE

ATI

Dhaman

Lancashire

Starr

XL

Ark

Ascot

Canopius

Chaucer

HCC

Hiscox

Ironshore

Kiln

LAU

LIU

LSM

Marketform

Novae

Pembroke

Talbot

Atradius Amlin

Hardy

QBE/COF

ONDD ATI

Dhaman

LSM

Aspen

Axis

Beazley

Catlin

Coface

Euler

ICIEC

Jubilee

XL

Zurich

ACE

FCIA

HCC

Hiscox

Ironshore

Kiln

LAU

LIU

Marketform

Novae

Starr

Talbot

Atradius

Chaucer

Pembroke

QBE

Canopius

Hardy

Markel

AIG

PRI Market: Insurers by tenor

Maximum credit period (years)

Aspen

Axis

Beazley

Coface

Euler

FCIA

ICIEC

Jubilee

Comprehensive

Political only

1.5 2 3 5 4 7 10 15

8

PRI Market: Theoretical capacity per risk

(USDm)

Source: BPL surveys

0

200

400

600

800

1000

1200

1400

1600

1800

CF CR

2008

2009

2010

2011

2012

9

PRI Market: General characteristics

• Specialist

• Diverse

• Capacity driven:

– Country aggregates

– Buyer aggregates

• Subscription market

10

BPL Global – Broker acts for the

policyholder

• Capital providers:

– Specialist insurers and

reinsurers

– Underwriting agents act for

capital providers

– Role of Insurers: to make

sure PRI market works for

the capital providers

• Clients:

– Policyholders, being

exporters, investors and

financial institutions

– Brokers act as agent of

policyholders

– Role of Brokers: to make

sure the PRI market works

for clients

– Client/policyholder service,

not “distribution”

11

BPL Global: headline numbers

• Premium flow - 2012 : USD 250 million

• Claims collected - 1983 to 2012 USD 1.36 billion +

12

BPL Global – Bank Policies

• Bank Loan Comprehensive Non-Payment Policy

• Bank Loan Guarantor Non-Honouring Policy

• Trade Debt Comprehensive Non-Payment Policy

• Non-Honouring of Letter of Credit

• PRI “Lenders” Policies

13

BPL Global: recent export finance

transactions

• Angola Electrical Equipment 5 years

• Angola Airport upgrade 5 years

• Angola Transport infrastructure 5 years

• Azerbaijan Energy equipment 10 years

• Azerbaijan Energy equipment 6 years

• Ethiopia Wind energy 5 years

• Gabon Sports infrastructure 7 years

• Gabon Prison upgrade 5 years

• Ghana Telecoms 10 years

• Ghana Corp. jet 5 years

• Indonesia Military equipment 5 years

• Laos Telecoms 5 years

• Togo Military equipment 5 years

• Turkey Transport infrastructure 6 years

• Turkey Transport infrastructure 8 years

• Turkey Transport infrastructure 10 years

• Vietnam Industrial equipment 12 years

• Vietnam Industrial equipment 7 years

• Vietnam Power equipment 10 years

• Vietnam Water infrastructure 12 years

14

US$ m years

Ark

Amlin

Ascot

Beazley

Canopius

Catlin

Chaucer

Hardy

Hiscox

Jubilee

Kiln/IBS

Liberty

Market Form

Novae

Pembroke

Starr

Talbot

20

10

5

30

25

75

20

15

25

15

40

35

20

25

15

50

30

455

5

3

5

7

5

10

5

3

5

7

5

5

5

5

5

7

5

LLOYD’S : PUBLIC OBLIGORS Syndicates S&P Rating Max Limit Period

A+

A+

A+

A+

A+

A+

A+

A+

A+

A+

A+

A+

A+

A+

A+

A+

A+

15

US$ m years

Ark

Amlin

Ascot

Beazley

Canopius

Catlin

Chaucer

Hardy

Hiscox

Jubilee

Kiln/IBS

Liberty

Market Form

Novae

Pembroke

Starr

Talbot

-

10

5

20

12

65

7.5

15

25

10

40

3

20

10

2.5

25

10

270

-

3

5

7

5

7

5

2

5

5

5

2

5

5

3

5

5

LLOYD’S : PRIVATE OBLIGORS

Syndicates S&P Rating Max Risk Period

A+

A+

A+

A+

A+

A+

A+

A+

A+

A+

A+

A+

A+

A+

A+

A+

A+

16

COMPANIES : PUBLIC OBLIGORS

Companies S&P Rating Max Limit Period

US$ m years

ACE

Atradius

Aspen

Axis

AIG

Coface Unistrat

HCC

ICIEC

Ironsure

LAU/AWAC

Liberty Int’l

Lancashire

ONDD

Sovereign

XL

Zurich

Euler

AA-

A (AM Best)

A

A

A

A-

AA

Aa3 Moody’s

A-

A

A-

A

AA

AA-

A-

AA-

AA-

60

70

70

50

120

70

30

75

20

20

30

75

25

80

75

150

100

1120

10

5

7

7

15

6

5

20

5

7

5

5

15

15

10

15

7

17

COMPANIES : PRIVATE OBLIGORS

Companies S&P Rating Max Limit Period

US$ m years

ACE

Atradius

Aspen

Axis

AIG

Coface Unistrat

HCC

ICIEC

Ironsure

LAU/AWAC

Liberty Int’l

Lancashire

ONDD

Sovereign

Zurich

Euler

AA-

A (AM Best)

A

A

A

A-

AA

Aa3 Moody’s

A-

A

A-

A

AA

AA-

AA-

AA-

30

70

70

35

75

70

30

75

20

12.5

30

75

7

-

50

100

749

10

5

7

7

15

6

5

20

5

7

5

5

5

-

7

7

18

Single Risk Process

1. Analyse the risk

2. Format the term sheet

3. Collate market responses (non-binding indications)

4. Devise the placement strategy

5. Prepare the information pack

6. Negotiate the wording

7. Bind cover

8. Provide post placement services

19

Providing post placement services

• Documentation

• Premium payment

• Reporting

– quarterly or 6 monthly review of policies

– regular reviews in event of potential loss: involve insurers

• Amendments to insured contract

– essential to inform insurers prior to making material

amendments

– endorse policy to add any additional works / values

• Extensions

• Notice of loss

• Claims

20

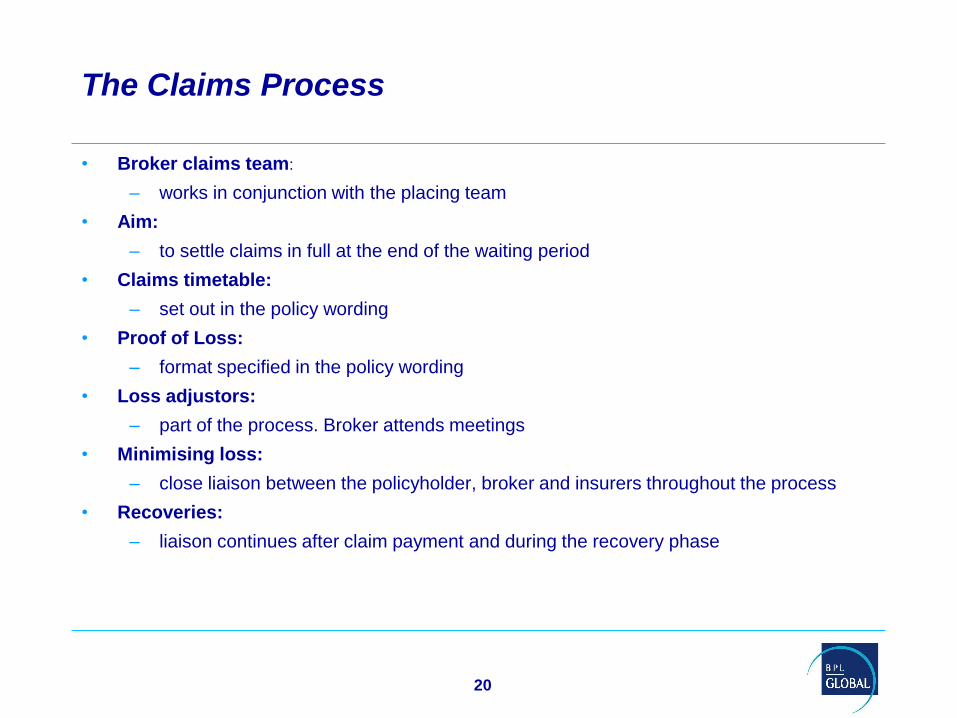

The Claims Process

• Broker claims team:

– works in conjunction with the placing team

• Aim:

– to settle claims in full at the end of the waiting period

• Claims timetable:

– set out in the policy wording

• Proof of Loss:

– format specified in the policy wording

• Loss adjustors:

– part of the process. Broker attends meetings

• Minimising loss:

– close liaison between the policyholder, broker and insurers throughout the process

• Recoveries:

– liaison continues after claim payment and during the recovery phase

21

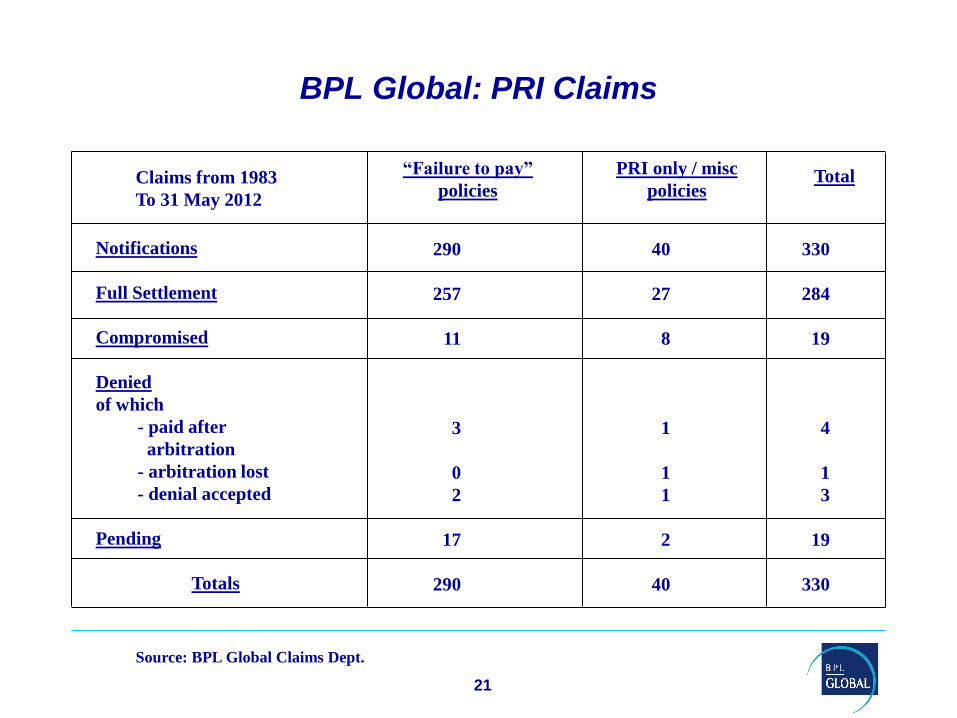

BPL Global: PRI Claims

“Failure to pay”

policies

PRI only / misc

policies Total

Notifications

Full Settlement

Compromised

Denied

of which

- paid after

arbitration

- arbitration lost

- denial accepted

Pending

Totals

290

257

11

3

0

2

17

290

40

27

8

1

1

1

2

40

330

284

19

4

1

3

19

330

Source: BPL Global Claims Dept.

Claims from 1983

To 31 May 2012

22

-50

0

50

100

150

200

250

300

350

400

Percentage

loss ratio

19 8 3 19 8 4 19 8 5 19 8 6 19 8 7 19 8 8 19 8 9 19 9 0 19 9 1 19 9 2 19 9 3 19 9 4 19 9 5 19 9 6 19 9 7 19 9 8 19 9 9 2 0 0 0 2 0 0 1 2 0 0 2 2 0 0 3 2 0 0 4 2 0 0 5 2 0 0 6 2 0 0 7 2 0 0 8 2 0 0 9 2 0 10

Year

BPL Global Portfolio : Historical Loss Ratios

Gross

Net

23

Financial Crisis: PRI Market Claims:

BPL’s November 2009 Estimate

• Estimated market aggregate figures: – Problem cases +/- USD 4 billion

– Likely paid claims: +/- USD 2.5 billion

– Paid, net of recoveries: USD 1 to 1.5 billion?

• Mainly private sector default

• Validating product

– Exporters and traders

– Banks and regulators

• PRI Market: Robust

24

BPL Global

Claims – 2007 & 2008 Years of Account

Full Settlement

Compromised

Total Settled

Denied/Disputed

Pending

Totals

Recoveries

621.6 67

8.4 3

630.0 70

9.0 1

60.0 8

699.0 79

160.0

USDm No. of cases

Choice in medium and long term (MLT) export credit insurance

BPL Global | 18 April, 2013

Change is coming

Change is coming

• De facto ECA monopoly

18 April 2013 Change is coming 26

• “Mixed market” ‒ ECAs and private insurers

competing

CHOICE

Two private markets

18 April 2013 Change is coming 27

Short term credit

insurance market

PRI Market ECAs

18 April 2013 Change is coming 28

• Short-term risk (mainly in EU and OECD)

• Short-term risk in emerging markets • MLT credit risk

Short term credit

insurance market

ECAs PRI Market

“Marketable” risk “Non-marketable” risk

PRI Market: growing appetite for MLT business

18 April 2013 Change is coming 29

Public buyers / borrowers (USD 1.75 billion)

Private buyers / borrowers (USD 1.2 billion)

100% 99% 81%

46% 26%

100% 90% 67% 10%

33%

3 years 5 years 7 years 10 years 15 years

MLT private market placement - Latin American borrower, USD 200 million+

18 April 2013 Change is coming 30

Higher rate

Lower rate

Placement rate

= Participant insurers indicated rate and line size

18 April 2013 Change is coming 31

“Market gap”

Short term credit

insurance market

ECAs PRI Market

“Marketable” risk “Non-marketable” risk

18 April 2013 Change is coming 32

“Market gap” “Market window”

ECAs and PRI market overlap

Short term credit

insurance market

ECAs PRI Market

“Marketable” risk “Non-marketable” risk

Berne Union 30 year record

18 April 2013 Change is coming 33

Net loss ratios*

18 April 2013 Change is coming 34

* Claims, net of recoveries, as a percentage of premium

9.4%

55.2% 55.3%

45.2%

Atradius 10 year average

2002 - 2011

Euler Hermes 8 year average

2005 - 2012 BPL Global 30 year private

market portfolio 1983 -

2012

Berne Union 30 years

1982 - 2011

Basel 2 : Unlevel playing field

18 April 2013 Change is coming 35

ECAs Private market

Basel 3 : Levels playing field

18 April 2013 Change is coming 36

BB AA A AA AAA 0 BBB 0 AAA A BBB BB

SACE

CESCE Coface Hermes

ECAs Private market

Aspen

Lloyd’s

ACE

Zurich

OeKB

Basel 2 :EU ECA level playing field

18 April 2013 Change is coming 37

BB AA A AA AAA 0 BBB 0 AAA A BBB BB

SACE

CESCE Coface

Hermes

OeKB

Basel 3 : EU ECAs not on level playing field

18 April 2013 Change is coming 38

“… trade distortions…”

18 April 2013 Change is coming 39

The change “…will create new ground for trade distortions, as the countries with better ratings will be able to offer a

competitive advantage to their exporters.” Raoul Ascari, COO, SACE

“The fact that Spanish exporters may not be able to complement their technical offers to their clients with

competitive financial packages puts them at a disadvantage in the face of their counterparts from

countries that are better rated…” Beatriz Reguero, COO, CESCE

18 April 2013 Change is coming 40

“Market gap” “Market window”

ECAs and PRI market overlap

Short term credit

insurance market

ECAs PRI Market

“Marketable” risk “Non-marketable” risk

EC definition of “marketable risk”

18 April 2013 Change is coming 41

Risk is considered “marketable” only if the capacity of the

private insurance market is “…sufficient to cover all

economically justifiable risks in the country or countries

concerned.”

27 February, 2013 Change is coming 42

“Market gap” “Market window”

ECAs and PRI market overlap

Short term credit

insurance market

ECAs PRI Market

“Marketable” risk “Non-marketable” risk

“Fully marketable” risk Risks that are “not fully marketable”/“capacity constrained”

Issues in “market window” / “market gap”

• ECAs should compete across “market window” / “market gap”

- Subject to observance of OECD Consensus

• Level playing field between ECAs/private insurers

- Premium taxes

• ECAs should observe subscription market best practice

- Revisit “co-operation”

18 April 2013 Change is coming 43

MLT private market placement - Latin American borrower, USD 200 million+

18 April 2013 Change is coming 44

Higher rate

Lower rate

Placement rate

= Participant insurers indicated rate and line size

Change in MLT insurance: the mixed market

18 April 2013 Change is coming 45

CHOICE