LiveWeLL Fixed index Annuity Updates/LiveWell FIA... · guarantee a stream of income in retirement...

12

LIVEWELL ® FIXED INDEX ANNUITY Issued by Midland National ® Life Insurance Company 19231I PRT 03-14 Administered by

Transcript of LiveWeLL Fixed index Annuity Updates/LiveWell FIA... · guarantee a stream of income in retirement...

1

LiveWeLL® Fixed index Annuity Issued by Midland National® Life Insurance Company

19231I PRT 03-14

Administered by

2

MAy Provide GuArAnteed incoMe For LiFe.retAin controL oF your Money.PotentiAL For Stock MArket-Linked GroWth.

The LiveWeLL® Fixed index AnnuiTy Provides you WiTh …

Guaranteed income stream in retirement if you choose

Optional Guaranteed Lifetime Withdrawal Benefit* provides guaranteed income for life and allows you to retain control of your money (available at an additional cost, ages 45-80)

Optional Guaranteed Minimum Death Benefit* provides option for legacy protection (available at an additional cost,

ages 45-80)

Long-term growth potential with interest credit (see page 4 for description)

No loss of premium due to market downturns or fluctuations

Tax deferral**

Issued by a company with strong financial ratings

If you’re like many Americans, one of your biggest retirement concerns is outliving your money.1 And frankly, it’s a valid concern.

After all, if you retire in your mid-sixties, you could easily go two or three decades2 without a paycheck. That’s why many people planning for retirement turn to Fixed Index Annuities.

Fixed Index Annuities not only provide safety of premium, but also guarantee a stream of income in retirement if a payout option is elected. Some Fixed Index Annuities offer an income rider that can guarantee income for life while allowing you to retain control of your money.

So—in addition to Social Security, a possible pension, and perhaps an IRA—a Fixed Index Annuity can provide you with a set amount of income you can rely on for life.

WhAT is A Fixed index AnnuiTy?A Fixed Index Annuity is a long-term, tax-deferred retirement planning solution that—in exchange for a premium payment—provides a guaranteed income stream during retirement. Your annuity has potential for stock market-linked growth, while also protecting the premium you pay.

Much of retirement planning revolves around having income during a period of time in which you won’t be working, or perhaps only working on a limited basis. That’s why a Fixed Index Annuity may make sense for those looking for an additional source of income during retirement.

Because with a Fixed Index Annuity, you can count on a set amount of money each month, quarter, year, or whatever payment schedule you choose if you elect a payout option.

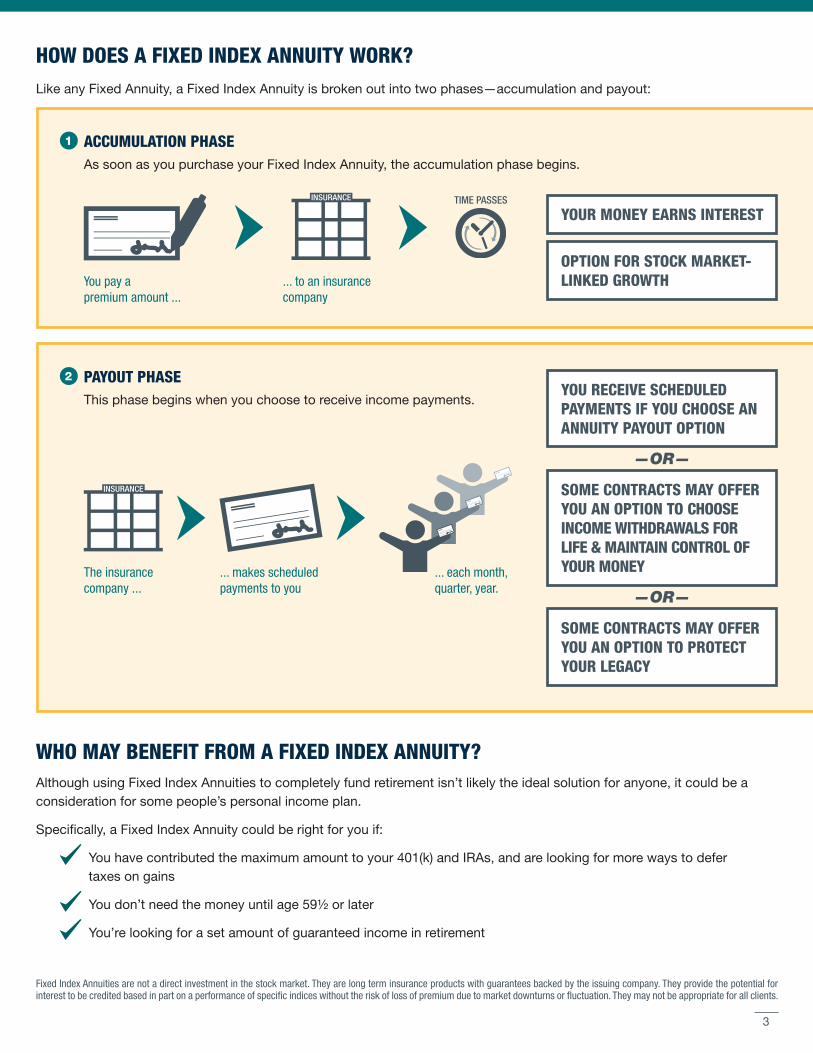

You pay a premium amount ...

... to an insurance company

Then the insurance company ...

... makes scheduled payments to you ...

... each month, quarter, year.

TIME PASSES

1 “Why You Should Purchase an Equity Indexed Annuity,” foxbusiness.com, Jan.2, 2013.2 “How Long Will You Live?” MoneyWatch, cbsnews.com, June 26, 2012. * This product feature is not available in all states.** Under current law, annuities grow tax deferred. Annuities may be subject to taxation during the income or withdrawal phase. The tax-deferred feature is not necessary for a tax-qualified plan. Neither Sammons Retirement Solutions® Inc., Midland National®, nor any financial professional acting on its behalf, should be viewed as providing legal, tax, or investment advice. Please consult with and rely upon your tax and legal professionals. A 10% IRS tax penalty may apply to withdrawals prior to age 59½.

3

Fixed Index Annuities are not a direct investment in the stock market. They are long term insurance products with guarantees backed by the issuing company. They provide the potential for interest to be credited based in part on a performance of specific indices without the risk of loss of premium due to market downturns or fluctuation. They may not be appropriate for all clients.

Who MAy BeneFiT FroM A Fixed index AnnuiTy?Although using Fixed Index Annuities to completely fund retirement isn’t likely the ideal solution for anyone, it could be a consideration for some people’s personal income plan.

Specifically, a Fixed Index Annuity could be right for you if:

You have contributed the maximum amount to your 401(k) and IRAs, and are looking for more ways to defer taxes on gains

You don’t need the money until age 59½ or later

You’re looking for a set amount of guaranteed income in retirement

hoW does A Fixed index AnnuiTy Work?Like any Fixed Annuity, a Fixed Index Annuity is broken out into two phases—accumulation and payout:

2 PAyouT PhAse This phase begins when you choose to receive income payments.

The insurance company ...

... makes scheduled payments to you

... each month, quarter, year.

your Money eArns inTeresT

oPTion For sTock MArkeT-Linked groWThYou pay a

premium amount ...... to an insurance company

1 AccuMuLATion PhAse As soon as you purchase your Fixed Index Annuity, the accumulation phase begins.

TIME PASSES

you receive scheduLed PAyMenTs iF you choose An AnnuiTy PAyouT oPTion

soMe conTrAcTs MAy oFFer you An oPTion To choose incoMe WiThdrAWALs For LiFe & MAinTAin conTroL oF your Money

soMe conTrAcTs MAy oFFer you An oPTion To ProTecT your LegAcy

—OR—

—OR—

4

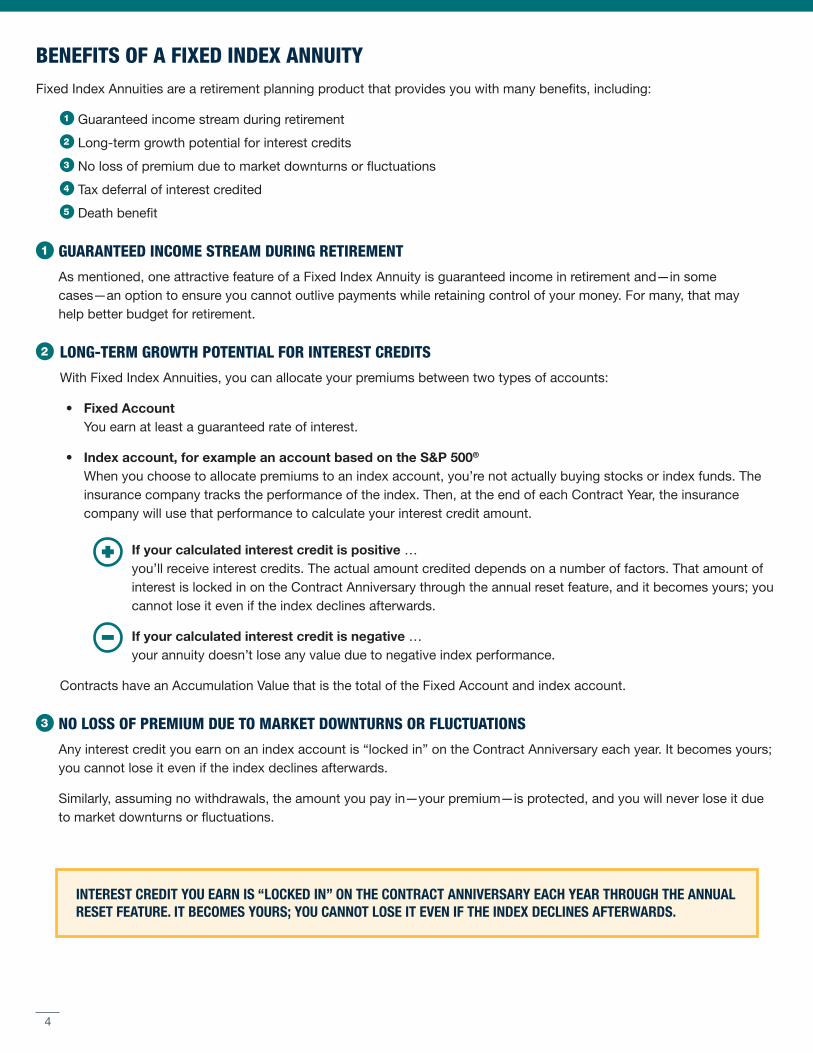

BeneFiTs oF A Fixed index AnnuiTyFixed Index Annuities are a retirement planning product that provides you with many benefits, including:

1 Guaranteed income stream during retirement

2 Long-term growth potential for interest credits

3 No loss of premium due to market downturns or fluctuations

4 Tax deferral of interest credited

5 Death benefit

1 guArAnTeed incoMe sTreAM during reTireMenT

As mentioned, one attractive feature of a Fixed Index Annuity is guaranteed income in retirement and—in some cases—an option to ensure you cannot outlive payments while retaining control of your money. For many, that may help better budget for retirement.

2 Long-TerM groWTh PoTenTiAL For inTeresT crediTs

With Fixed Index Annuities, you can allocate your premiums between two types of accounts:

• Fixed Account You earn at least a guaranteed rate of interest.

• Index account, for example an account based on the S&P 500® When you choose to allocate premiums to an index account, you’re not actually buying stocks or index funds. The insurance company tracks the performance of the index. Then, at the end of each Contract Year, the insurance company will use that performance to calculate your interest credit amount.

If your calculated interest credit is positive … you’ll receive interest credits. The actual amount credited depends on a number of factors. That amount of interest is locked in on the Contract Anniversary through the annual reset feature, and it becomes yours; you cannot lose it even if the index declines afterwards.

If your calculated interest credit is negative … your annuity doesn’t lose any value due to negative index performance.

Contracts have an Accumulation Value that is the total of the Fixed Account and index account.

3 no Loss oF PreMiuM due To MArkeT doWnTurns or FLucTuATions

Any interest credit you earn on an index account is “locked in” on the Contract Anniversary each year. It becomes yours; you cannot lose it even if the index declines afterwards.

Similarly, assuming no withdrawals, the amount you pay in—your premium—is protected, and you will never lose it due to market downturns or fluctuations.

INterest CreDIt you earN Is “LoCkeD IN” oN the CoNtraCt aNNIversary eaCh year throuGh the aNNuaL reset Feature. It beCoMes yours; you CaNNot Lose It eveN IF the INDex DeCLINes aFterwarDs.

5

beNeFICIarIes wILL GeNeraLLy reCeIve the aCCuMuLatIoN vaLue as a Death beNeFIt

4 TAx deFerrAL oF inTeresT crediTed If you have a 401(k) or IRA, you’re likely already familiar with the benefits of tax deferral.

Simply put, deferring taxes on gains helps you two ways:

• First, tax-deferred growth allows your money to grow faster because you earn interest on dollars that would otherwise be paid in taxes. Your premium earns interest, the interest compounds within the Contract, and the money you would have paid in taxes earns interest.

• Second, in most cases, when you’re ready to take withdrawals, you’re usually retired and earning little or no income, meaning you’ll likely be in a lower tax bracket. For that reason, the money you withdraw may be taxed at a lower rate. For tax treatment of withdrawals, please see your tax professional.

5 deATh BeneFiT

When an annuity Owner passes away before a payout option is elected, beneficiaries are guaranteed to receive the Accumulation Value as a death benefit; generally this means the Beneficiary is guaranteed to receive at least the amount of premium paid by the annuity Owner plus interest credit earned, assuming there have been no rider charges or withdrawals. This is called the “standard death benefit.” Beneficiaries can choose either a lump sum payment or a series of income payments.

soMe Things To consider When Looking For A Fixed index AnnuiTyLike many retirement solutions, Fixed Index Annuities may include benefits, riders, and other options to personalize for your retirement goals.

Some things you may want to consider when looking for a Fixed Index Annuity include:

guArAnTeed LiFeTiMe WiThdrAWAL BeneFiT (gLWB) oPTion—

• For an extra cost, you can have guaranteed income for life—so you likely won’t outlive payments.

• Typically chosen to supplement Social Security, pensions, and any other retirement savings, by providing a guaranteed income stream during retirement.

• You retain control of your money.

—OR—

guArAnTeed MiniMuM deATh BeneFiT (gMdB) oPTion—

• For an extra cost, your beneficiaries may receive an increased death benefit.

• Possible solution for those who want to provide a legacy to their heirs.

issued By A coMPAny WiTh sTrong FinAnciAL rATings—

• A Fixed Index Annuity is an insurance product for which an insurance company guarantees payouts beginning at an agreed-upon time for a predetermined duration (sometimes providing life-long income).

• It’s important to make sure you choose your Fixed Index Annuity from a company you can trust. One measure is the insurance company’s ratings for strength and stability, for example, their A.M. Best rating.

6

The LiveWeLL® Fixed index AnnuiTy AT A gLAnce— A guArAnTeed incoMe source during reTireMenTThe LiveWell® Fixed Index Annuity provides all of the benefits of a Fixed Index Annuity, including annuity payout options, plus optional riders that can provide legacy protection or income for life while retaining control of your money.

LiveWell® Fixed Index Annuity administered by Sammons Retirement Solutions® Inc. (SRSI) and issued by Midland National® Life Insurance Company

Issue Age For the Contract: Age 0-85

For the optional riders: Age 45-80

Type of Money Non-Qualified, Traditional IRAs, Roth IRAs, SEP-IRAs, and Inherited IRAs

Minimum Premium Contribution

•$10,000 Initial Premium for qualified and non-qualified dollars

•Additional premiums accepted

Maximum Initial Premium Contribution

$2 million (without prior approval)

Interest Crediting Methods Fixed Account—Initial interest rate guaranteed for 1 year, declared annually after that.

Index Account—Annual point-to-point with an index cap rate based on the S&P 500®. (For details, see page 7.)

•Rates declared annually at the discretion of the company.

•Your Initial Premium may be allocated into these two accounts as you wish. You can transfer between accounts on each Contract Anniversary for the life of your annuity.

•Subsequent premiums will be placed in the Fixed Account. This premium will earn the current new money interest rate at the time of receipt. Each Contract Anniversary, this premium will be allocated according to your most recent allocation instructions.

Interest Rate Bands Your Accumulation Value on each Contract Anniversary will determine the interest rate band that will apply for the next Contract Year. On each Contract Anniversary, both the Fixed Account interest rate and index cap rate will be declared.

Band #1: <$100,000 Band #2: $100,000 - $249,999 Band 3: $>$250,000

Index Caps/Rates Ask your financial professional for current caps and interest rates.

Surrender Charge ScheduleSurrender charge structure may vary by state

Contract Year 1 2 3 4 5 6 7 8 9

Surrender Charge 8% 8% 8% 7% 6% 5% 4% 3% 0%

•While you always have full access to your money, if you choose to take a withdrawal in excess of the penalty-free amount or surrender the annuity early, a surrender charge (also known as a withdrawal charge) is assessed on the portion that exceeds the penalty-free amount. A breakdown of these charges is shown in the schedule above.

•Additional premiums deposited into existing Contracts will maintain the surrender charge schedule set forth by the Initial Premium.

•The surrender charge is eliminated after year 8.

Penalty-FreeWithdrawal Amount

•Starting in year 2, you may take 10% of your Accumulation Value (or RMDs if greater) without a withdrawal charge.

•Penalty-free withdrawal amount is not cumulative.

Surrender Value The Surrender Value is the amount that is available at the time of surrender. The Surrender Value is equal to the Accumulation Value, subject to Market Value Adjustment, less applicable surrender charges and state Premium Taxes. A surrender during the Surrender Charge Period could result in a loss of premium. The Surrender Value will never be less than the minimum requirements set forth by the state laws at the time of issue in the state where the Contract is delivered.

7

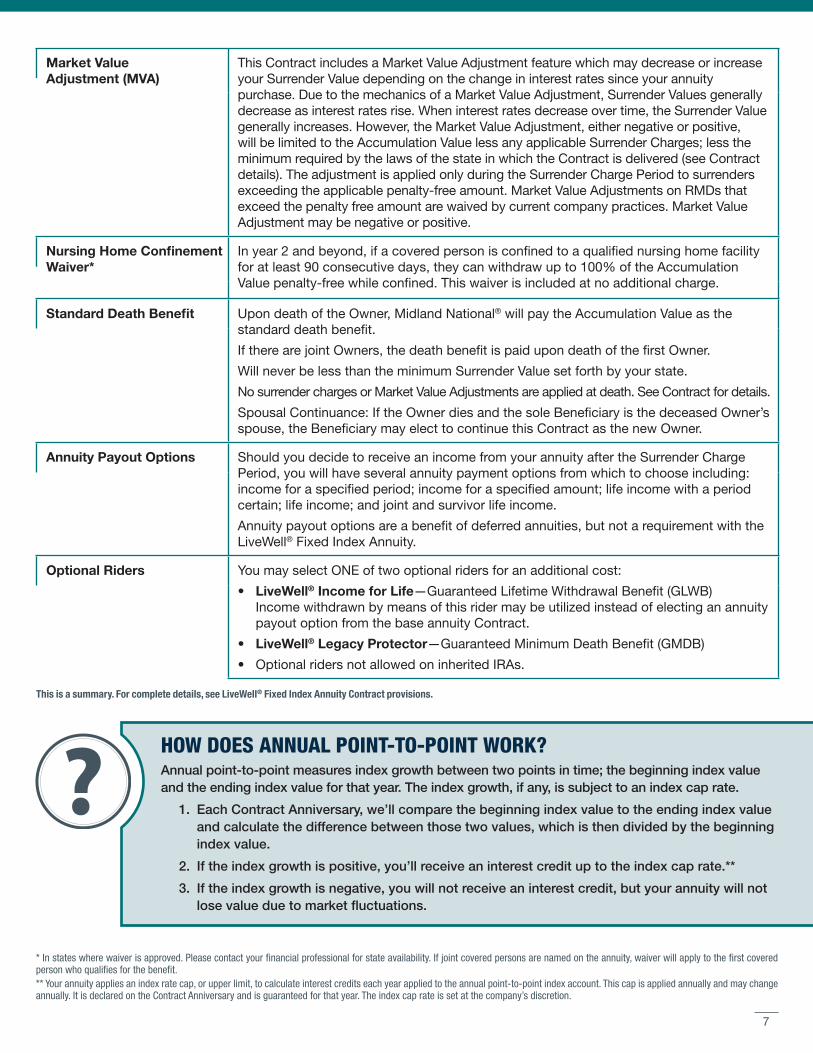

Market Value Adjustment (MVA)

This Contract includes a Market Value Adjustment feature which may decrease or increase your Surrender Value depending on the change in interest rates since your annuity purchase. Due to the mechanics of a Market Value Adjustment, Surrender Values generally decrease as interest rates rise. When interest rates decrease over time, the Surrender Value generally increases. However, the Market Value Adjustment, either negative or positive, will be limited to the Accumulation Value less any applicable Surrender Charges; less the minimum required by the laws of the state in which the Contract is delivered (see Contract details). The adjustment is applied only during the Surrender Charge Period to surrenders exceeding the applicable penalty-free amount. Market Value Adjustments on RMDs that exceed the penalty free amount are waived by current company practices. Market Value Adjustment may be negative or positive.

Nursing Home Confinement Waiver*

In year 2 and beyond, if a covered person is confined to a qualified nursing home facility for at least 90 consecutive days, they can withdraw up to 100% of the Accumulation Value penalty-free while confined. This waiver is included at no additional charge.

Standard Death Benefit Upon death of the Owner, Midland National® will pay the Accumulation Value as the standard death benefit.

If there are joint Owners, the death benefit is paid upon death of the first Owner.

Will never be less than the minimum Surrender Value set forth by your state.

No surrender charges or Market Value Adjustments are applied at death. See Contract for details.

Spousal Continuance: If the Owner dies and the sole Beneficiary is the deceased Owner’s spouse, the Beneficiary may elect to continue this Contract as the new Owner.

Annuity Payout Options Should you decide to receive an income from your annuity after the Surrender Charge Period, you will have several annuity payment options from which to choose including: income for a specified period; income for a specified amount; life income with a period certain; life income; and joint and survivor life income.

Annuity payout options are a benefit of deferred annuities, but not a requirement with the LiveWell® Fixed Index Annuity.

Optional Riders You may select ONE of two optional riders for an additional cost:

• LiveWell® Income for Life—Guaranteed Lifetime Withdrawal Benefit (GLWB) Income withdrawn by means of this rider may be utilized instead of electing an annuity payout option from the base annuity Contract.

• LiveWell® Legacy Protector—Guaranteed Minimum Death Benefit (GMDB)

• Optional riders not allowed on inherited IRAs.

this is a summary. For complete details, see Livewell® Fixed Index annuity Contract provisions.

* In states where waiver is approved. Please contact your financial professional for state availability. If joint covered persons are named on the annuity, waiver will apply to the first covered person who qualifies for the benefit.** Your annuity applies an index rate cap, or upper limit, to calculate interest credits each year applied to the annual point-to-point index account. This cap is applied annually and may change annually. It is declared on the Contract Anniversary and is guaranteed for that year. The index cap rate is set at the company’s discretion.

hoW does AnnuAL PoinT-To-PoinT Work?Annual point-to-point measures index growth between two points in time; the beginning index value and the ending index value for that year. The index growth, if any, is subject to an index cap rate.

1. Each Contract Anniversary, we’ll compare the beginning index value to the ending index value and calculate the difference between those two values, which is then divided by the beginning index value.

2. If the index growth is positive, you’ll receive an interest credit up to the index cap rate.**

3. If the index growth is negative, you will not receive an interest credit, but your annuity will not lose value due to market fluctuations.

8

LiveWeLL® incoMe For LiFe oPTionAL guArAnTeed LiFeTiMe WiThdrAWAL BeneFiT (gLWB) riderLiveWell® Fixed Index Annuity administered by Sammons Retirement Solutions® Inc. (SRSI) and issued by Midland National® Life Insurance Company

Issue Age Age 45-80

LiveWell® Income for Life Available at issue only

Type of Benefit For Income - Optional Guaranteed Lifetime Withdrawal Benefit Rider

GLWB Value On the Issue Date, equals your Initial Premium. May increase due to additional premium and GLWB roll-ups.

Maximum GLWB Value 2 times net premium (premiums minus gross withdrawals)

GLWB Roll-Up Amount* On each Contract Anniversary, the GLWB Value increases by GLWB Roll-Up Percentage (8%) multiplied by net premiums.

GLWB Cost 0.85% of the GLWB Value taken from the Accumulation Value on each Contract Anniversary for as long as the rider is in effect

You have the option to elect lifetime income payments, but can retain control of your money.

Prior to electing lifetime income payments, if you make additional premium payments into your annuity, your GLWB Value will be equal to the current GLWB Value plus your additional premium payments. Additional premiums will not increase the Lifetime Payment Amount (LPA), but will increase the GLWB Value.

The GLWB Value cannot be withdrawn in a lump sum and is not available at surrender, or on or after the Maturity Date, or as a death benefit.

Not allowed on money from inherited IRAs.

Cannot be elected with LiveWell® Legacy Protector rider.

Lifetime Payment Election Date (LPED)

The date you select to begin LPA.

This date must be after the first Contract Year, and you must be at least 55 on this date.

Impact of Partial Withdrawals on the GLWB Value

Withdrawals Taken before the Lifetime Payment Election Date

Partial withdrawals Reduce GLWB Value proportionally

If partial withdrawals are Required Minimum Distributions (RMDs) from an IRA Reduce GLWB Value dollar-for-dollar

Withdrawals Taken after Lifetime Payment Election Date

Withdrawals in excess of LPA or Required Minimum Distributions (RMDs) Reduce GLWB Value proportionally

LPAs or Required Minimum Distributions (RMDs) Reduce GLWB Value dollar-for-dollar

With an Initial Premium payment of $100,000, you can secure a guaranteed annual payment of $10,000. This assumes Issue Age 50, the GLWB Value reaches the maximum value of $200,000, LPAs beginning at age 65, no withdrawals prior to lifetime income, and no additional premium.

LiveWeLL® incoMe For LiFe$200,000

$100,000 INITIAL PREMIUM The longer you wait to take withdrawals, the greater the payment amount

you can receive each year.

The GLWB Value decreases as withdrawals are taken, but if no excess withdrawals are made, the amount stays the same.

Grows at 8% simple interest guaranteedguArAnTeed incoMe For LiFe - $10,000 eAch yeAr

Age 50 65 8063

* GLWB Roll-Up Amount is based on simple interest (8% of net premium) rather than compound interest.

9

LiFeTiMe PAyMenT AMounTs

With the LiveWell® Income for Life optional rider, you choose how frequently you would like to receive your LPAs: monthly, quarterly, semi-annually, or annually. When you are ready to begin lifetime payments from your LiveWell® Income for Life rider, your LPA will be determined and you will receive a predictable amount of income for the rest of your life—or you and your spouse’s life— even if the Accumulation Value and the GLWB Value are both reduced to zero (as long as you only take withdrawals equal to the LPA).

• You must notify us in writing when you would like to begin receiving your LPAs. Once LPAs begin, GLWB roll-up will no longer be applied.

• When you first elect LPAs, your payments will be based on your current GLWB Value multiplied by a percentage based on the youngest GLWB covered person’s age. See Lifetime Payment Percentage (LPP) chart for details. The longer you wait to take withdrawals, the greater the income you can receive each year.

• LPA refers to the amount you may withdraw each year under the LiveWell® Income for Life rider.

• GLWB Value is used to compute the LPA.

• For joint GLWB covered persons, the LPP is based on attained age of the youngest covered person.

• LPA is NOT subject to Market Value Adjustment (MVA) or surrender charges.

• If a Required Minimum Distribution (RMD) is required, you will be allowed to take the greater of the LPA or the RMD for this Contract without reducing your LPA.

• After the Lifetime Payment Election date, LPA is not recalculated with subsequent premium.

hoW To cALcuLATe gLWB vALue

100% of net premiums

GLWB Roll-Up Amount

Adjustments for any withdrawals from the Contract

GLWB Value

For tax treatment of LPAs, please see your tax advisor. Under current tax law, income payment from this Contract may be taxed as ordinary income. Additionally, if taken prior to age 59½, the income payments may be subject to a 10% IRS penalty.

Attained AgeIndividual GLWB Covered Person

Joint GLWB Covered Persons*

55 4.0% 3.50%

56 4.1% 3.60%

57 4.2% 3.70%

58 4.3% 3.80%

59 4.4% 3.90%

60 4.5% 4.00%

61 4.6% 4.10%

62 4.7% 4.20%

63 4.8% 4.30%

64 4.9% 4.40%

65 5.0% 4.50%

66 5.1% 4.60%

67 5.2% 4.70%

Lifetime Payment Percentage (LPP)

Attained AgeIndividual GLWB Covered Person

Joint GLWB Covered Persons*

68 5.3% 4.80%

69 5.4% 4.90%

70 5.5% 5.00%

71 5.6% 5.10%

72 5.7% 5.20%

73 5.8% 5.30%

74 5.9% 5.40%

75 6.0% 5.50%

76 6.1% 5.60%

77 6.2% 5.70%

78 6.3% 5.80%

79 6.4% 5.90%

80+ 6.5% 6.00%

*Based on the age of younger GLWB covered person

10

LiveWell® Fixed Index Annuity administered by Sammons Retirement Solutions® Inc. (SRSI) and issued by Midland National® Life Insurance Company

Issue Age Age 45-80

LiveWell® Legacy ProtectorAvailable at issue only

Type of Benefit For Legacy Protection- Guaranteed Minimum Death Benefit Optional Rider

GMDB Amount On the Issue Date, equals your Initial Premium at issue. May increase due to additional premium and GMDB Roll-Up Amount, up to maximum GMDB Amount or age 85 of the oldest GMDB covered persons.

Maximum GMDB Amount 2 times net premium

GMDB Roll-Up Amount* On each Contract Anniversary, the GMDB Amount increases by the amount of the GMDB Roll-Up Percentage (5%) multiplied by net premiums.

GMDB Cost 0.35% of the GMDB Amount taken from the Accumulation Value on each Contract Anniversary for as long as the rider is in effect.

If you make additional premium payments into your annuity, your GMDB Amount will be equal to the current benefit base plus your additional premium payments.

Not allowed on money from inherited IRAs.

Cannot be elected with LiveWell® Income for Life rider.

Impact of Partial Withdrawals on GMDB Amount

Partial withdrawals Reduce GMDB Amount proportionately

If partial withdrawals are RMDs from an IRA Reduce GMDB Amount dollar-for-dollar

LiveWeLL® LegAcy ProTecTor oPTionAL guArAnTeed MiniMuM deATh BeneFiT (gMdB) rider

* Assuming no withdrawals or subsequent premiums, your GMDB Amount is guaranteed to grow at 5% simple interest (GMDB Roll-Up Percentage) until the oldest GMDB covered person reaches age 85 or you reach the maximum GMDB Amount (double your net premium), whichever occurs first. The annual roll-up is applied only on Contract Anniversaries.Please note that neither Sammons Retirement Solutions® Inc., Midland National®, nor any financial professional acting on its behalf, should be viewed as providing legal, tax or investment advice. Consult with and rely on your own qualified professional.This is not life insurance. Upon payout of the death benefit, the growth on the GMDB Amount will be taxed to your Beneficiary as ordinary income. Neither Midland National®, Sammons Retirement Solutions®, nor any financial professional selling on their behalf should be viewed as providing legal, tax, or investment advice. Consult with and rely on your own qualified professional.

If your objective is to provide a legacy for your heirs, the LiveWell® Fixed Index Annuity offers the optional LiveWell® Legacy Protector Guaranteed Minimum Death Benefit (GMDB) rider.

The GMDB Amount is available as a death benefit if greater than the Accumulation Value. If premiums are added or withdrawals taken, the GMDB Amount can increase or decrease. The GMDB Amount will never exceed the maximum amount of twice net premiums. The annual cost of the rider will not reduce the GMDB Amount.

hoW do i cALcuLATe My gMdB AMounT?

100% of net premiums

GMDB Roll-Up Amount

Adjustments for any withdrawals from the Contract

GMDB Amount

LiveWeLL® LegAcy ProTecTor

With an Initial Premium payment of $100,000, you can secure a guaranteed minimum death benefit of up to $200,000 maximum GMDB Amount. This assumes at least 20 years from Initial Premium payment to death benefit and no withdrawals.

$100,000 INITIAL PREMIUM

$125,000

$200,000 MAxIMUM$150,000 $175,000

Amount your heirs receive in the form of a death benefit.Grows at 5% simple interest guaranteed

Age 60 65 8070 75 85

LiveWeLL® LegAcy ProTecTor vALue

Your Beneficiary can choose the GMDB Amount in either a lump sum or a series of income payments.

The LiveWell® Legacy Protector rider is not life insurance. Upon payout of the death benefit, the growth on the GMDB Amount may be taxed to your Beneficiary as ordinary income.

11

hoW Much incoMe do you need during reTireMenT?You’ve likely heard rules of thumb on this matter, such as:

“You should withdraw no more than 4% of funds each year...”

“You’ll need 80% of your current income per year during retirement...”

The fact is, ensuring you have enough to live comfortably and transfer a legacy to heirs depends on a multitude of criteria.

Include these four steps in conversations with your financial professional to be sure you’re as prepared as possible to meet your retirement goals:

Verbalize what you want your retirement to look like. Will you continue working? Do you want to travel? Does being a snowbird sound appealing? These are the types of things you must consider now to make these goals a reality.

Review what you have in place—or don’t have in place— to get you there. Review your portfolio. Are you prepared to support your goals? Do you have savings in place? Have you set up a fixed income stream?

Create and implement a realistic, sustainable plan. With the help of your financial professional, take stock of the retirement plans you have in place. Along with savings, make sure you can withstand market changes with things like fixed income streams, such as a Fixed Index Annuity.

Meet annually with your financial professional. This is important to continually monitor your plans, make adjustments, and stay on track.

sTArT or Fine-Tune your FinAnciAL PLAn TodAy WiTh your FinAnciAL ProFessionAL.

12

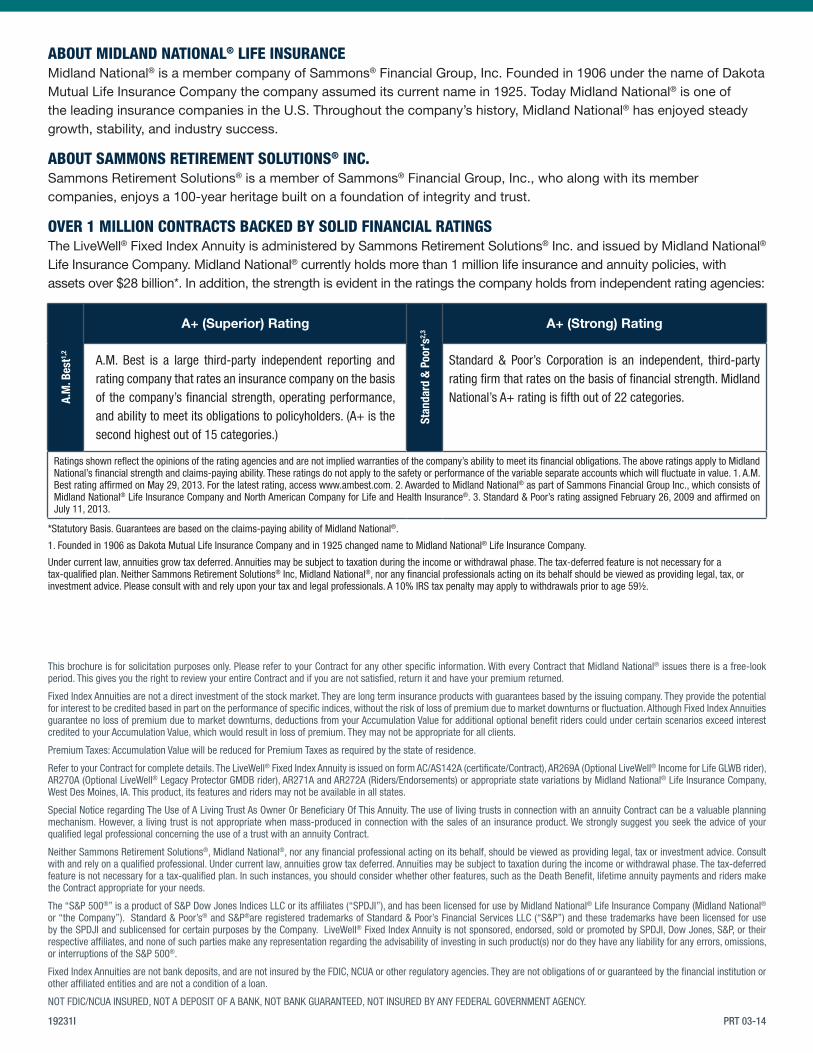

ABouT MidLAnd nATionAL® LiFe insurAnceMidland National® is a member company of Sammons® Financial Group, Inc. Founded in 1906 under the name of Dakota Mutual Life Insurance Company the company assumed its current name in 1925. Today Midland National® is one of the leading insurance companies in the U.S. Throughout the company’s history, Midland National® has enjoyed steady growth, stability, and industry success.

ABouT sAMMons reTireMenT soLuTions® inc.Sammons Retirement Solutions® is a member of Sammons® Financial Group, Inc., who along with its member companies, enjoys a 100-year heritage built on a foundation of integrity and trust.

over 1 MiLLion conTrAcTs BAcked By soLid FinAnciAL rATingsThe LiveWell® Fixed Index Annuity is administered by Sammons Retirement Solutions® Inc. and issued by Midland National® Life Insurance Company. Midland National® currently holds more than 1 million life insurance and annuity policies, with assets over $28 billion*. In addition, the strength is evident in the ratings the company holds from independent rating agencies:

19231I PRT 03-14

This brochure is for solicitation purposes only. Please refer to your Contract for any other specific information. With every Contract that Midland National® issues there is a free-look period. This gives you the right to review your entire Contract and if you are not satisfied, return it and have your premium returned.

Fixed Index Annuities are not a direct investment of the stock market. They are long term insurance products with guarantees based by the issuing company. They provide the potential for interest to be credited based in part on the performance of specific indices, without the risk of loss of premium due to market downturns or fluctuation. Although Fixed Index Annuities guarantee no loss of premium due to market downturns, deductions from your Accumulation Value for additional optional benefit riders could under certain scenarios exceed interest credited to your Accumulation Value, which would result in loss of premium. They may not be appropriate for all clients.

Premium Taxes: Accumulation Value will be reduced for Premium Taxes as required by the state of residence.

Refer to your Contract for complete details. The LiveWell® Fixed Index Annuity is issued on form AC/AS142A (certificate/Contract), AR269A (Optional LiveWell® Income for Life GLWB rider), AR270A (Optional LiveWell® Legacy Protector GMDB rider), AR271A and AR272A (Riders/Endorsements) or appropriate state variations by Midland National® Life Insurance Company, West Des Moines, IA. This product, its features and riders may not be available in all states.

Special Notice regarding The Use of A Living Trust As Owner Or Beneficiary Of This Annuity. The use of living trusts in connection with an annuity Contract can be a valuable planning mechanism. However, a living trust is not appropriate when mass-produced in connection with the sales of an insurance product. We strongly suggest you seek the advice of your qualified legal professional concerning the use of a trust with an annuity Contract.

Neither Sammons Retirement Solutions®, Midland National®, nor any financial professional acting on its behalf, should be viewed as providing legal, tax or investment advice. Consult with and rely on a qualified professional. Under current law, annuities grow tax deferred. Annuities may be subject to taxation during the income or withdrawal phase. The tax-deferred feature is not necessary for a tax-qualified plan. In such instances, you should consider whether other features, such as the Death Benefit, lifetime annuity payments and riders make the Contract appropriate for your needs.

The “S&P 500®” is a product of S&P Dow Jones Indices LLC or its affiliates (“SPDJI”), and has been licensed for use by Midland National® Life Insurance Company (Midland National® or “the Company”). Standard & Poor’s® and S&P®are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”) and these trademarks have been licensed for use by the SPDJI and sublicensed for certain purposes by the Company. LiveWell® Fixed Index Annuity is not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, or their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of the S&P 500®.

Fixed Index Annuities are not bank deposits, and are not insured by the FDIC, NCUA or other regulatory agencies. They are not obligations of or guaranteed by the financial institution or other affiliated entities and are not a condition of a loan.

NOT FDIC/NCUA INSURED, NOT A DEPOSIT OF A BANk, NOT BANk GUARANTEED, NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY.

a.M

. bes

t1,2

A+ (Superior) Rating

stan

dard

& P

oor’s

2,3

A+ (Strong) Rating

A.M. Best is a large third-party independent reporting and rating company that rates an insurance company on the basis of the company’s financial strength, operating performance, and ability to meet its obligations to policyholders. (A+ is the second highest out of 15 categories.)

Standard & Poor’s Corporation is an independent, third-party rating firm that rates on the basis of financial strength. Midland National’s A+ rating is fifth out of 22 categories.

Ratings shown reflect the opinions of the rating agencies and are not implied warranties of the company’s ability to meet its financial obligations. The above ratings apply to Midland National’s financial strength and claims-paying ability. These ratings do not apply to the safety or performance of the variable separate accounts which will fluctuate in value. 1. A.M. Best rating affirmed on May 29, 2013. For the latest rating, access www.ambest.com. 2. Awarded to Midland National® as part of Sammons Financial Group Inc., which consists of Midland National® Life Insurance Company and North American Company for Life and Health Insurance®. 3. Standard & Poor’s rating assigned February 26, 2009 and affirmed on July 11, 2013.

*Statutory Basis. Guarantees are based on the claims-paying ability of Midland National®.

1. Founded in 1906 as Dakota Mutual Life Insurance Company and in 1925 changed name to Midland National® Life Insurance Company.

Under current law, annuities grow tax deferred. Annuities may be subject to taxation during the income or withdrawal phase. The tax-deferred feature is not necessary for a tax-qualified plan. Neither Sammons Retirement Solutions® Inc, Midland National®, nor any financial professionals acting on its behalf should be viewed as providing legal, tax, or investment advice. Please consult with and rely upon your tax and legal professionals. A 10% IRS tax penalty may apply to withdrawals prior to age 59½.