Streaming Video Content Over Streaming Video Content Over ...

1

brand investment and activation of live music & streaming platforms

mauro cellore

managing partner, mc[co] labs

2

To offer a strategic perspective on the live music streaming opportunity for brand marketers

considering an investment and activation of live music properties.

To provide an overview on the key drivers responsible to drive marketing ROI from the investment in live music content platforms.

To present a point of view on the evolution of music-related content marketing initiatives, as live experiences, artist engagement models and

content distribution fuse into multi-platform business models.

2

22

2

3

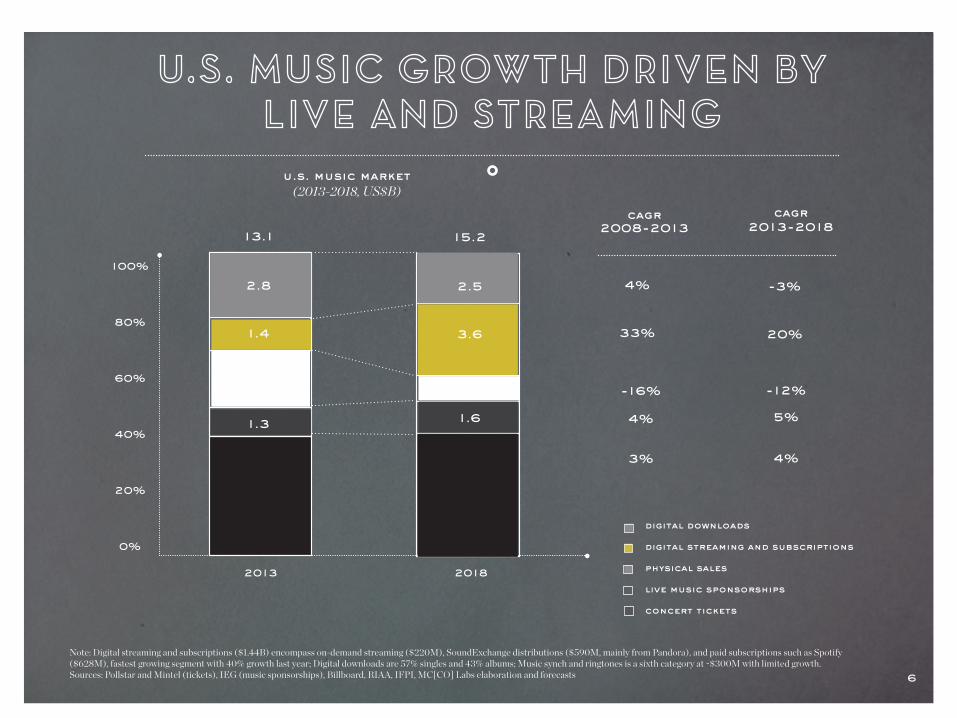

The ~$13B U.S. music industry is projected to grow at a 3% CAGR over the next four years, primarily driven by live music (sponsorships/tickets) and online streaming (audio and video). · Live music and online streaming counterbalance declining physical retail and flat digital download revenues. · The music industry still profiles as “superstar economy”, with highly concentrated demand patterns (<7% of artists driving ~75% of total music revenue).

Online music streaming is dominated by audio (~64%) and music videos (35%). · While audio streaming is primarily monetized through subscription models, music videos is advertising-based. Profitability is still widely challenged across all business models.

Brands have five key “entry points” into music: (1) Production (“record label” model), (2) Digital streaming, (3) Live music, (4) Promotional/marketing, and (5) Ventures / artist collaborations. · To date, branded music assets derived from these investment models are still “disconnected” and not integrated into higher yield platforms.

If left isolated operating at sub-scale, live streaming and live music sponsorship are both ROI challenged and inhibited by low differentiation, high entry costs, audience fragmentation and deal structures with partnering distributors. We have witnessed a 20- 40% value shortfall for live music investments compared to similar media dollar allocations.

Live streaming is currently <1% of the online music streaming market. Consumer demand continues to grow from a low base (~400M views annually). · Average live performances remain in the low 20-100K unique views, requiring large volumes of top concerts to support a real business case behind the investment. · Multi-artist (headliners) festivals and must-see events (e.g., Coachella, Bonnaroo) are the exceptions with viewers reaching >4M (500-800K for an individual concert). · Investment activity has picked up in the past 12 months, due to sizeable brand investments, new equity partnerships, and promoters/digital portal deals.

3

4

Scale for brand marketers, however, appears to be elusive, underscoring business model challenges, distribution fragmentation, clutter and creative challenges inherent with the streaming model. · Consumer demand appears to be “capped” at 30-40M engaged digital viewers · Intention behind live streaming still anchored on a “content repurposing” strategic driver. · Content repurposing still lacks a compelling value proposition against the live experience.

However, live music streaming can have a place in a cross-platform music investment model for marketers with meaningful budgets and a clear music strategy. · Highly engaged fan base around music and music artists. · Possible direct-to-consumer distribution channel for music artists. · Integration opportunities with live music experience and other music assets.

To date Brand investments in live streaming has faced ROI challenges, driven by misaligned distribution models/partnerships, poor targeting and inefficient/sub scale resource allocation.

Live music ROIs can be improved by working on the creative, strategic and financial side of the investment, defining value-add creative initiatives on top of the live streaming platform, integrating live music sponsorships and artist collaborations and using cutting edge techniques for sizing and matching audience metrics with investment deployment.

Those initiatives require the augmentation of traditional marketing approaches with a dual creative/strategic skill set to lead opportunity assessment, partnership architecture design, artist deals and collaboration opportunities.

(cont’d)

4

5

music landscape

brand investment in music

live streaming

mc[co] labs

5

6

u.s. music market (2013-2018, US$B)

4%

33%

cagr 2008-2013

cagr 2013-2018

100%

80%

60%

40%

20%

0%

-3%

20%

2013 2018

Note: Digital streaming and subscriptions ($1.44B) encompass on-demand streaming ($220M), SoundExchange distributions ($590M, mainly from Pandora), and paid subscriptions such as Spotify ($628M), fastest growing segment with 40% growth last year; Digital downloads are 57% singles and 43% albums; Music synch and ringtones is a sixth category at ~$300M with limited growth.Sources: Pollstar and Mintel (tickets), IEG (music sponsorships), Billboard, RIAA, IFPI, MC[CO] Labs elaboration and forecasts

13.1

2.8

1.4

2.5

1.3

15.2

2.5

3.6

1.3

1.6

digital downloads

digital streaming and subscriptions

physical sales

live music sponsorships

concert tickets

-16%

4%

3%

-12%

5%

4%

6

7

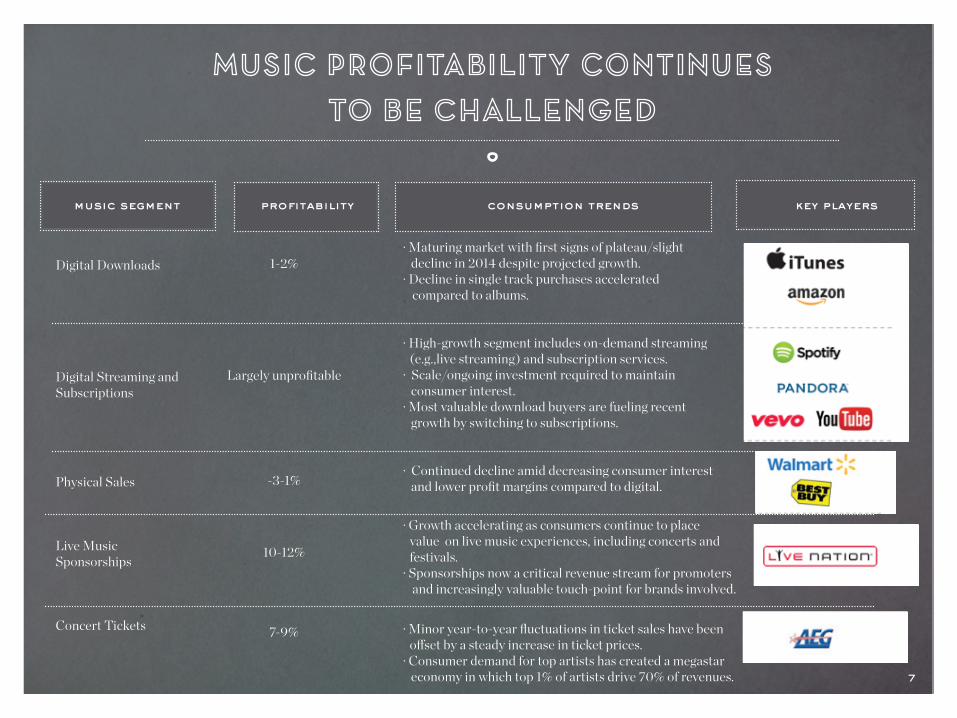

profitabilitymusic segment consumption trends key players

Digital Downloads

Digital Streaming and Subscriptions

Physical Sales

Live Music Sponsorships

Concert Tickets

1-2%

Largely unprofitable

-3-1%

10-12%

7-9%

· Maturing market with first signs of plateau/slight decline in 2014 despite projected growth.· Decline in single track purchases accelerated compared to albums.

· High-growth segment includes on-demand streaming (e.g.,live streaming) and subscription services.· Scale/ongoing investment required to maintain consumer interest.· Most valuable download buyers are fueling recent growth by switching to subscriptions.

· Continued decline amid decreasing consumer interest and lower profit margins compared to digital.

· Growth accelerating as consumers continue to place value on live music experiences, including concerts and festivals.· Sponsorships now a critical revenue stream for promoters and increasingly valuable touch-point for brands involved.

· Minor year-to-year fluctuations in ticket sales have been offset by a steady increase in ticket prices.· Consumer demand for top artists has created a megastar economy in which top 1% of artists drive 70% of revenues. 7

8

music artist concentration(2012, ww share of revenues)

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

93%

75%

25%

share of artists share of revenue

Limited “scale” in “long tail”

Challenged “discovery” economics

Power concentrated among mega artists and top labels

Increasing A&R talent costs

implications

7%

Notwithstanding recent technological advances and consumer adoption,the fundamentals of the “music super-economy” remain unchanged.

8

9

music landscape

brand investment in music

live streaming

mc[co] labs

9

10

production

digital streaming

live music

promotional marketing

1

2

3

4

5ventures/artistcollaborations "Record label” model

· Sourcing· Recording· Marketing and distribution

· Audio/radio model· Curation · Live music streaming

· Tickets · Sponsorships

· Media buys· Content sponsorship

10

11

70

60

50

40

30

20

10

0

production (“record label” model)

digital streaming (at scale)

promotional/marketing

Note: brand marketing music initiatives are defined as investments from major corporate sponsors (either sponsorships, production, or promotion) aligning their brand name and resources against a music program, platform or talent.Source: MC[CO] Labs elaboration based on IEG, AdWeek and Billboard data

ventures / artistcollaborations

live music

brand marketing investment initiatives in music properties(# of initiatives, 2012-2013)

11

12

60

50

40

30

20

10

0

2011 2012 2013

Key Insights

• Average scale investment in music sponsorship is increasing and surpassing the $50M mark for top spenders in 2013.

• Live music sponsorship spending is largely driven by EOS ticketing programs and associated live activations across the Auto, Financial Services and Beverage categories. Nike is the main music sponsor at scale outside of those leading categories.

• Live streaming is being pursued by a minority of large spenders, with budget allocations to digital streaming activation being normally in the 15-20% range.

• Live streaming is today still viewed as an “extension” of the live experience sponsorship with deal structures requiring marketing commitments to drive viewership and engagement on the branded content(*) Top spenders include companies such as Pepsi, Coca Cola, Toyota, American Express, CITI, Chase, Master Card,

Heineken

Note: Sponsorship spend by the top spenders above represents ~34% of total North American sponsorship spend in 2013.Source: MC[CO] elaborations based on IEG, Billboard, AdAge data corroborated with internal spending database and expert interviews

average annual music sponsorship spend by top 10 spenders (2011- 2013, US$M)

12

13

music landscape

brand investment in music

live streaming

mc[co] labs

13

14

Digital music is slowing down its growth and shifting platform mix, with music and ad models emerging as key contributors behind downloads.

from: download economy

• almost entirely download based

• “ownership” driven

• drm dependent

• simple platform

• aggregation driven

to: streaming economy

• downloads and streaming

• “cloud” based

• more fluid drm systems

• complex, intelligent platforms

• access driven

14

15

140

120

100

80

60

40

20

0

Streaming volumes are overwhelming compared to digital units sold; however per unit monetization clearly favors DTO (1$ per unit avg. vs. 0.005S/unit stream)

on demand streams digital units sold

1.5b

118b

on demand streams vs. digital music “units” sold (In B units, worldwide 2013)

15

16

streaming music breakdown(2013est, ww share of viewership and revenues)

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

$173B $1.4B

87%

share of streams/views

share of revenue

68%

Key Insights

· The fast-growing audio/music video streaming segment drove ~$1.4B in revenue in 2013, with 90% of revenue coming from audio streaming services such as Pandora and Spotify.

· Growth in video viewership is driven mainly by Vevo, which is the only music video platform that has surpassed 40M MAU in the U.S.

· The high concentration of viewership and revenue among streaming distributors (primarily audio) has empowered a small number of key players to act as “gatekeepers” for the market.

· We estimate that audio (118B on-demand plays) and music Livestreamingvideos (55B views annually) lead viewership, leaving live music streaming with a miniscule sliver of the streaming segment.

· Although live concerts are growing at a fast rate (43% CAGR in 2013), the format is building on a low scale and continues to be challenged by underlying structural demand limitations · Format appeal compared to other music content options (e.g. music video) · Ad model (challenges in creating inventory) Small screen experience

32%

13%0.2%

live streaming video

audio

0.1%

16

17

live music streaming market(Streaming + On demand, unique viewers, ww 2012-2013)

400M

300M

200M

100M

0

total events 14,000 20,000

2012 2013

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

shares

distribution shares(Estimates market shares on total views, 2013)

other

yahoo! music

livestreaming sites

youtube/vevo

40%CAGR

(*) Destination includes destination sites set up to distribute the live musicexperience (e.g. Boiler Room)

(**) Livestreaming sites include Ustream (market leader), Livebeats, and iRockeNote: This chart considers primary streaming channels, even though someconcerts are streamed by multiple channels

destination

17

18

6

4

2

0

other online

high

average

Key Insights

Live concerts have been challenged to drive TV audiences at scale (min >1M viewers), except for globally distributed “must-see” events. · As such, live music has been progressively marginalized from TV Networks programming schedules.

The expansion of online video has been driving a renewed interest in the format from online distributors interested in the “scarcity” aspects of the live platform. · Leading to live streaming recent fast growth, primarily driven by supply dynamics. “There was a moment when everybody seemed to be pitching Average a live stream of concerts, whether audio or video,” says an unnamed digital executive. “It just didn’t make sense. It wasn’t what the consumer was trying to do.”- Billboard

However, online viewership results to date suggest that live music streaming continues to be structurally challenged to reach large scale audiences, except in a few notable exceptions. · “Large scale must see events” (Live 8, Coachella) · Mega star top tours

live streaming performance benchmarks(Unduplicated Viewership or “Uniques” in M)

other tv

onlinemegaartist

tvmegaartist

onlinefestival

headliners

tvmust see

event

18

19

brand marketer

· Potential production funding · Marketing commitment · Ancillary content

permormer/artist/management

promoter/venue

online distributors

other channels (if not covered by main deal)

pr amplification

• Vevo• Vimeo• Crackle

• Connected TVs • Mobile• Game platforms

live experiencestreaming

other contentstreaming

on demand streaming

19

20

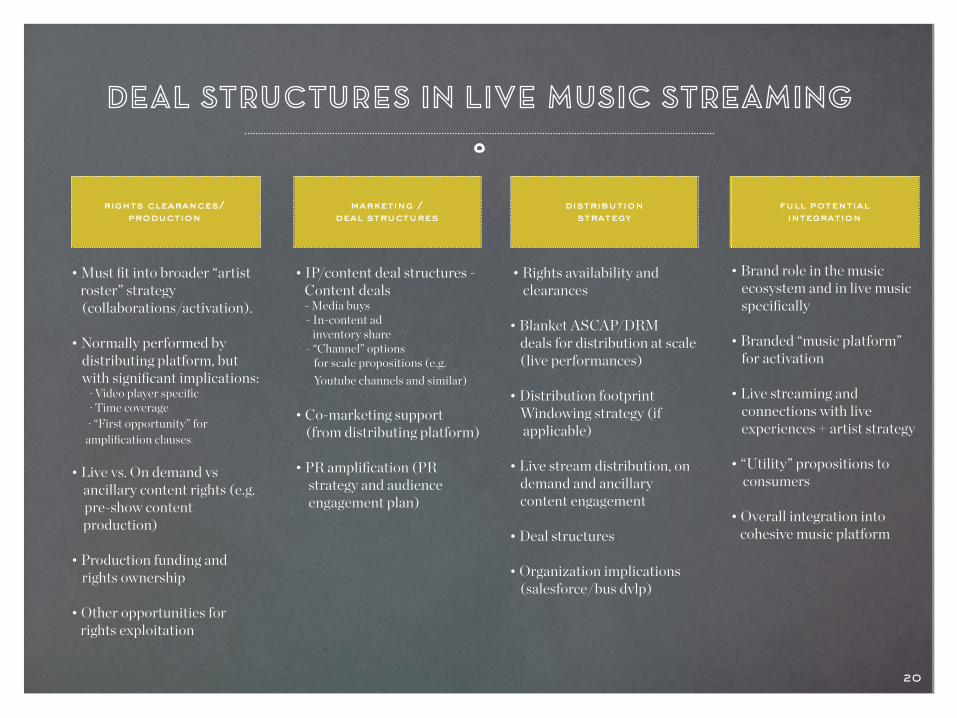

rights clearances/ production

marketing / deal structures

distribution strategy

full potential integration

• Must fit into broader “artist roster” strategy (collaborations/activation).

• Normally performed by distributing platform, but with significant implications:

· Video player specific · Time coverage· “First opportunity” for

amplification clauses

• Live vs. On demand vs ancillary content rights (e.g. pre-show content production)

• Production funding and rights ownership

• Other opportunities for rights exploitation

• IP/content deal structures - Content deals - Media buys - In-content ad inventory share - “Channel” options for scale propositions (e.g. Youtube channels and similar)

• Co-marketing support (from distributing platform)

• PR amplification (PR strategy and audience engagement plan)

• Rights availability and clearances

• Blanket ASCAP/DRM deals for distribution at scale (live performances)

• Distribution footprint Windowing strategy (if applicable)

• Live stream distribution, on demand and ancillary content engagement

• Deal structures

• Organization implications (salesforce/bus dvlp)

• Brand role in the music ecosystem and in live music specifically

• Branded “music platform” for activation

• Live streaming and connections with live experiences + artist strategy

• “Utility” propositions to consumers

• Overall integration into cohesive music platform

20

21

700

600

500

400

300

200

100

0

5 concerts/oneoffs

distributor equity

235m

200

400

150

24050

100

theoretical delivery gap

high

low

tv music sponsorship

online music sponsorship

Stand-alone live streaming platforms are exposed to low yield returns.

media investment vehicle comparison(M consumer impressions delivered on a sample $6M capital allocation, annual comparison)

avg 250M

21

22

music landscape

brand investment in music

live streaming

mc[co] labs

22

23

brand goals

music strategy

role and vision

platform design

investment monitoring

SCALE +INTEGRATION

ReachEngagement

Media Investment ROI

Other brands’ investments Content clutter

Distributors’ shares

• Content format demand• Distributors’ shares

• New entrant investments

Intangible marketing benefits Media comparison ROI

business model

partnerships / deals

music assets

resources / capabilities

market forces competitive dynamics

23

24

Founded by former Bain and WME strategists with deep media experience, MC[CO] Labs is a strategic advisory venture headquartered in Los Angeles and specializing in content strategy and investments across the media and marketing

ecosystems.

•

We partner with content investors, global marketing leaders and media entrepreneurs to support the evaluation, structuring and execution of “big prize

opportunities”

•

We engage across the entire growth execution spectrum, from consumer discovery, to ideation, strategic planning, creative collaborations and investment/deal

valuation.

• Our track record was built over 100+ growth/content strategy initiatives, $3B+ of media/marketing partnerships and $70B+ of media related investments across the

full spectrum of company size, stage and steps of the media value chains.

24

25

music platformstrategy

music strategy music opportunityvaluation

deal structuring analysis

Strategic goal setting

Content model design

Genre/Talent prioritization

Investment approach and sequencing

Music Platform Vision

Consumer Experience /Value proposition

Strategic Architecture & Design

Investment sizing and ROI targets

Strategic partnership architecture

Distribution strategy

Deal valuation (rights, talent,

strategic partnerships)

Long-term investment in music asset building for marketing amplification

25

26

agencies

marketersip creators

distributors (labels, promoters. digital)

Operational experience at market leading talent agency with leading music position.

Multiple projects in collaboration with agencies and their clients, focusing on the design of investment platforms in

media and entertainment content.

Worked with marketers across industries developing content strategies and platform investment thesis with

focus on sports, music and film.

10 cases in the past 2 years

Worked with IP creators, artists and right- holders defining multiplatform strategies to maximize the value of

their rights

Over 15 cases in the past 3 years

26

![Optimized Video Streaming over Cloud: A Stall-Quality ... · opportunity by 2019 [4]. In this paper, we will give a novel approach to an optimized cloud-based-video streaming. Since](https://static.fdocuments.in/doc/165x107/5ed1016a9fd38404692fd0c6/optimized-video-streaming-over-cloud-a-stall-quality-opportunity-by-2019-4.jpg)