LEVERAGED LOAN MONTHLY - Reutersshare.thomsonreuters.com/.../Leveraged_Loan_Monthly_nov_2016.pdf ·...

96

LEVERAGED LOAN MONTHLY THOMSON REUTERS LPC NOVEMBER 2016 Colm (C.J.) Doherty Director of Analysis [email protected] 646-223-6821 Hugo Pereira Senior Market Analyst [email protected] 646-223-6818

Transcript of LEVERAGED LOAN MONTHLY - Reutersshare.thomsonreuters.com/.../Leveraged_Loan_Monthly_nov_2016.pdf ·...

LEVERAGED LOAN MONTHLY THOMSON REUTERS LPC

NOVEMBER 2016

Colm (C.J.) Doherty Director of Analysis [email protected] 646-223-6821

Hugo Pereira Senior Market Analyst [email protected] 646-223-6818

LEVERAGED LOAN MONTHLY

Leveraged Loan Monthly - November 2016

2

Leveraged Loan Market Overview Slides 6-29

High Yield Bond Market Overview Slide 30-35

Investor Overview Slide 36-40

CLO Market Analysis Slide 41-60

Loan Fund Flows & Returns Slide 91-94

List of Recent CLOs / League Tables Slide 61-90

Key Points Slides 3-5

KEY POINTS

Leveraged Loan Monthly - November 2016

3

Primary Market: •Year to date leveraged loan issuance is at $751 billion, up 2% from the same period a year ago. Breaking it out by segment, pro rata volume at $387 billion is down 16%, while the $364 billion of institutional deal flow is up 34% . •Technology, retail and healthcare are the top industries in terms of leveraged loan issuance this year. •Overall institutional loan issuance is at $372 billion so far in 2016, a gain of around 34%. Refinancing activity has jumped by 51% this year, outpacing growth in new money issuance which is up 21% year over year. •High yield bond issuance amounted to $14.5 billion in November. Year-to-date issuance is at $204 billion, which is down 18% from the same period last year.

•So far in 4Q16, yields have tightened to their lowest level this year. In the large corporate market, new issue yields have tightened to an average of 4.99%, while middle market yields have declined to 6.24%.

•There was one institutional loan default in November, Bennu Oil & Gas LLC with $487 million of institutional loan debt. The trailing twelve month loan default rate fell to 1.9%.

Cont’d on next slide

KEY POINTS

Leveraged Loan Monthly - November 2016

4

Secondary Market: •Loan returns slipped in November, with 0pen-end loan fund returns averaging 0.21%, while the S&P/LSTA index gained 0.26%. Year to date, open-end loan funds have gained 7.7%, while the index is up 8.9%. •After a period of climbing prices in recent months, the secondary market edged lower in November. Institutional term loans finished the month off 14 bps at 96.61. The flow name SMi100 was down 39 bps to 98.68. •As of month-end November, 43% of loans are priced at 100-plus, down from 45% a month earlier. On a dollar weighted basis the par-plus share is higher at 52%. At the lower end of the price scale, 9% of credits are bid below 90 cents on the dollar, up marginally from 8% in the prior month.

•Looking across industries, the sectors bid highest are transportation (100.09), construction (100.02) and hotel & gaming (99.93). The largest sectors of technology and healthcare are bid at 97.93 and 97.97, respectively. •European flow names remain highly priced, edging 4 bps higher in November to an average bid of 100.57.

•The share of par-plus loans in U.S. CLOs slipped to 48% (from 51%) in November. In European deals, the share of par-plus loans continued to climb, reaching 73%.

Cont’d on next slide

KEY POINTS

Leveraged Loan Monthly - November 2016

5

CLOs / Loan Funds: •U.S. CLO issuance climbed to $10.6 billion in November, the highest monthly figure since June 2015. This brought YTD issuance to $65.1 billion, down from $91.4 billion in the same period last year. •U.S. refinancing and reset volume has surged in the last two months, with November hitting a record. In these two months, refinancings (including resets) have amounted to over $20 billion, bringing year to date volume to over $28 billion.

•CLO AAA discount margins averaged 147 bps in November, marginally tighter than the prior month. Discount margins on AAA tranches ranged from 140 bps to a high of 163 bps. •The European CLO market added €2 billion of issuance from five deals in November. Issuance now stand at €15.6 billion (38 deals) so far this year, up from €12.4 billion (31 deals) over the same period last year. •Assets under management increased to $441 billion for U.S. CLOs and to €68 billion for European CLOs. •Loan funds saw their fifth straight month of inflows, adding $2 billion in November (based on the most recent data available). This pushed flows into positive territory ($304 million) on a year to date basis.

•Loan mutual fund & ETF assets under management (market value) increased by 3% in November to $126 billion. In the last year, loan fund AUM is up 2%.

LEVERAGED LOAN MARKET OVERVIEW

*2016 loan volumes are based on the most recently available data and is subject to updates throughout the quarter.

LEVERAGED LOAN ISSUANCE: PRO RATA VS. INSTITUTIONAL - MONTHLY

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

Jan-

06

Apr

-06

Jul-0

6 O

ct-0

6 Ja

n-07

A

pr-0

7 Ju

l-07

Oct

-07

Jan-

08

Apr

-08

Jul-0

8 O

ct-0

8 Ja

n-09

A

pr-0

9 Ju

l-09

Oct

-09

Jan-

10

Apr

-10

Jul-1

0 O

ct-1

0 Ja

n-11

A

pr-1

1 Ju

l-11

Oct

-11

Jan-

12

Apr

-12

Jul-1

2 O

ct-1

2 Ja

n-13

A

pr-1

3 Ju

l-13

Oct

-13

Jan-

14

Apr

-14

Jul-1

4 O

ct-1

4 Ja

n-15

A

pr-1

5 Ju

l-15

Oct

-15

Jan-

16

Apr

-16

Jul-1

6 O

ct-1

6

Leve

rage

d Lo

an Is

suan

ce ($

Bils

.)

Pro rata Institutional

Leveraged Loan Monthly - November 2016

7

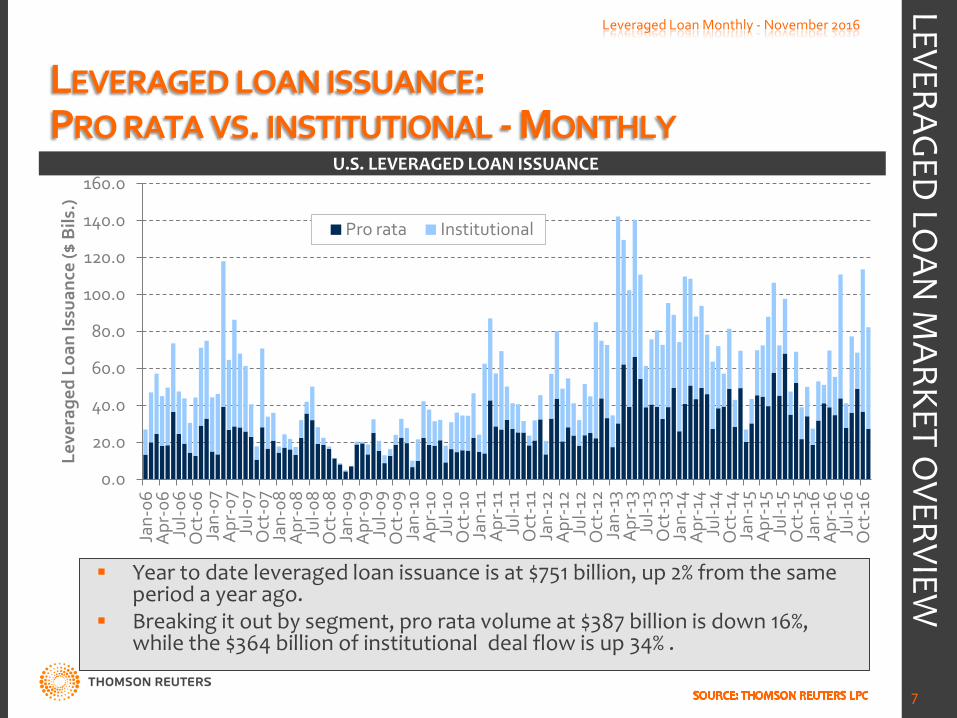

U.S. LEVERAGED LOAN ISSUANCE

Year to date leveraged loan issuance is at $751 billion, up 2% from the same period a year ago.

Breaking it out by segment, pro rata volume at $387 billion is down 16%, while the $364 billion of institutional deal flow is up 34% .

LEVERAGED

LOAN

MARKET O

VERVIEW

YTD LEVERAGED LOAN ISSUANCE BY INDUSTRY

8

-

LEVERAGED

LOAN

MARKET O

VERVIEW

Leveraged Loan Monthly - November 2016

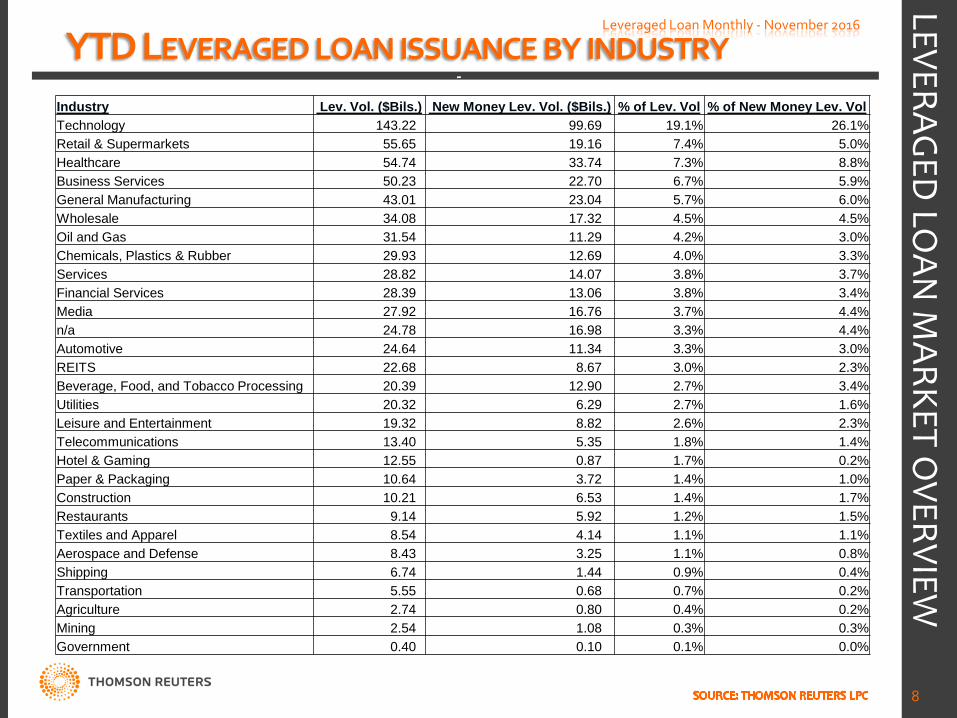

Industry Lev. Vol. ($Bils.) New Money Lev. Vol. ($Bils.) % of Lev. Vol % of New Money Lev. Vol Technology 143.22 99.69 19.1% 26.1% Retail & Supermarkets 55.65 19.16 7.4% 5.0% Healthcare 54.74 33.74 7.3% 8.8% Business Services 50.23 22.70 6.7% 5.9% General Manufacturing 43.01 23.04 5.7% 6.0% Wholesale 34.08 17.32 4.5% 4.5% Oil and Gas 31.54 11.29 4.2% 3.0% Chemicals, Plastics & Rubber 29.93 12.69 4.0% 3.3% Services 28.82 14.07 3.8% 3.7% Financial Services 28.39 13.06 3.8% 3.4% Media 27.92 16.76 3.7% 4.4% n/a 24.78 16.98 3.3% 4.4% Automotive 24.64 11.34 3.3% 3.0% REITS 22.68 8.67 3.0% 2.3% Beverage, Food, and Tobacco Processing 20.39 12.90 2.7% 3.4% Utilities 20.32 6.29 2.7% 1.6% Leisure and Entertainment 19.32 8.82 2.6% 2.3% Telecommunications 13.40 5.35 1.8% 1.4% Hotel & Gaming 12.55 0.87 1.7% 0.2% Paper & Packaging 10.64 3.72 1.4% 1.0% Construction 10.21 6.53 1.4% 1.7% Restaurants 9.14 5.92 1.2% 1.5% Textiles and Apparel 8.54 4.14 1.1% 1.1% Aerospace and Defense 8.43 3.25 1.1% 0.8% Shipping 6.74 1.44 0.9% 0.4% Transportation 5.55 0.68 0.7% 0.2% Agriculture 2.74 0.80 0.4% 0.2% Mining 2.54 1.08 0.3% 0.3% Government 0.40 0.10 0.1% 0.0%

YTD INSTITUTIONAL LOAN ISSUANCE BY INDUSTRY

9

-

LEVERAGED

LOAN

MARKET O

VERVIEW

Leveraged Loan Monthly - November 2016

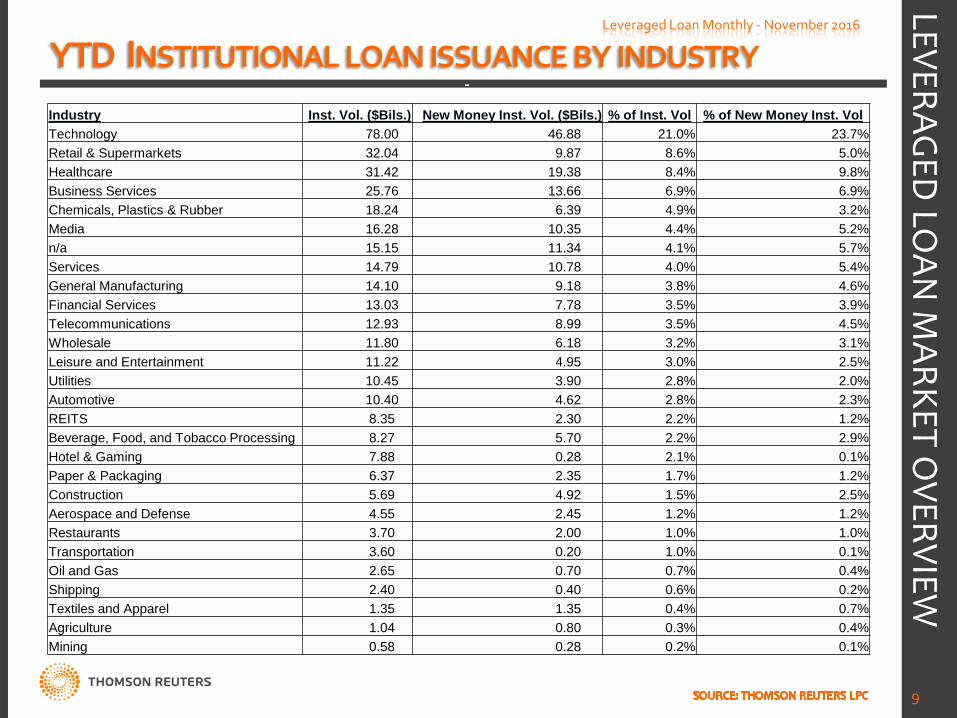

Industry Inst. Vol. ($Bils.) New Money Inst. Vol. ($Bils.) % of Inst. Vol % of New Money Inst. Vol Technology 78.00 46.88 21.0% 23.7% Retail & Supermarkets 32.04 9.87 8.6% 5.0% Healthcare 31.42 19.38 8.4% 9.8% Business Services 25.76 13.66 6.9% 6.9% Chemicals, Plastics & Rubber 18.24 6.39 4.9% 3.2% Media 16.28 10.35 4.4% 5.2% n/a 15.15 11.34 4.1% 5.7% Services 14.79 10.78 4.0% 5.4% General Manufacturing 14.10 9.18 3.8% 4.6% Financial Services 13.03 7.78 3.5% 3.9% Telecommunications 12.93 8.99 3.5% 4.5% Wholesale 11.80 6.18 3.2% 3.1% Leisure and Entertainment 11.22 4.95 3.0% 2.5% Utilities 10.45 3.90 2.8% 2.0% Automotive 10.40 4.62 2.8% 2.3% REITS 8.35 2.30 2.2% 1.2% Beverage, Food, and Tobacco Processing 8.27 5.70 2.2% 2.9% Hotel & Gaming 7.88 0.28 2.1% 0.1% Paper & Packaging 6.37 2.35 1.7% 1.2% Construction 5.69 4.92 1.5% 2.5% Aerospace and Defense 4.55 2.45 1.2% 1.2% Restaurants 3.70 2.00 1.0% 1.0% Transportation 3.60 0.20 1.0% 0.1% Oil and Gas 2.65 0.70 0.7% 0.4% Shipping 2.40 0.40 0.6% 0.2% Textiles and Apparel 1.35 1.35 0.4% 0.7% Agriculture 1.04 0.80 0.3% 0.4% Mining 0.58 0.28 0.2% 0.1%

U.S. INSTITUTIONAL LOAN AND HY BOND ISSUANCE

0.0

20.0

40.0

60.0

80.0

100.0

120.0 Ja

n-10

A

pr-1

0 Ju

l-10

Oct

-10

Jan-

11

Apr

-11

Jul-1

1 O

ct-1

1 Ja

n-12

A

pr-1

2 Ju

l-12

Oct

-12

Jan-

13

Apr

-13

Jul-1

3 O

ct-1

3 Ja

n-14

A

pr-1

4 Ju

l-14

Oct

-14

Jan-

15

Apr

-15

Jul-1

5 O

ct-1

5 Ja

n-16

A

pr-1

6 Ju

l-16

Oct

-16

Issu

ance

($ B

ils.)

HY Bonds

Inst. Loans

Leveraged Loan Monthly - November 2016

10

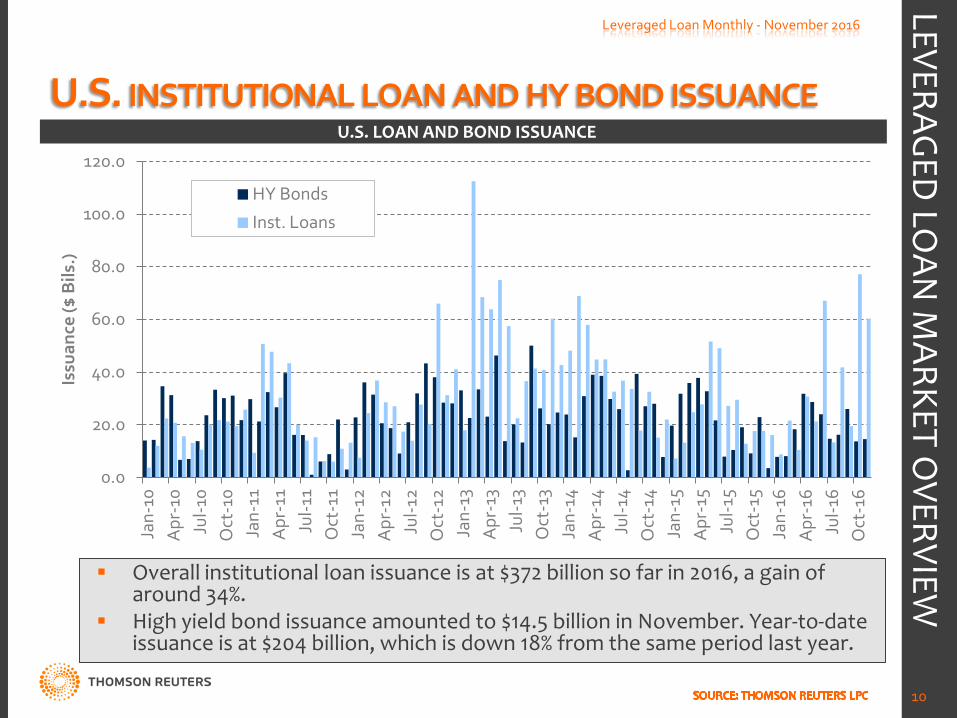

U.S. LOAN AND BOND ISSUANCE

Overall institutional loan issuance is at $372 billion so far in 2016, a gain of around 34%.

High yield bond issuance amounted to $14.5 billion in November. Year-to-date issuance is at $204 billion, which is down 18% from the same period last year.

LEVERAGED

LOAN

MARKET O

VERVIEW

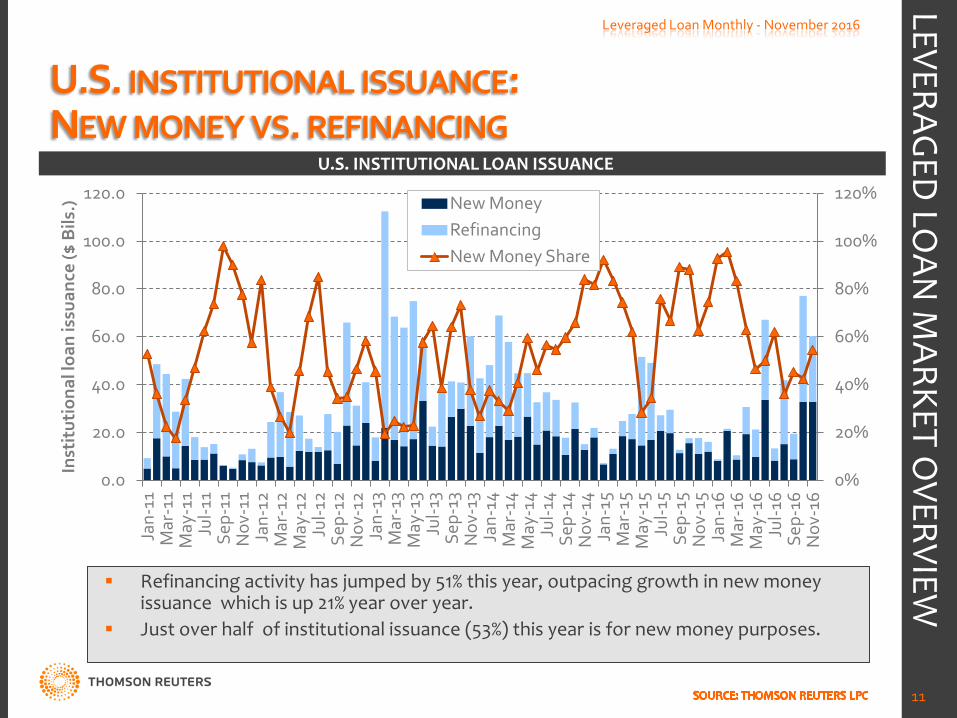

U.S. INSTITUTIONAL ISSUANCE: NEW MONEY VS. REFINANCING

0%

20%

40%

60%

80%

100%

120%

0.0

20.0

40.0

60.0

80.0

100.0

120.0

Jan-

11

Mar

-11

May

-11

Jul-1

1 Se

p-11

N

ov-1

1 Ja

n-12

M

ar-1

2 M

ay-1

2 Ju

l-12

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3 Se

p-13

N

ov-1

3 Ja

n-14

M

ar-1

4 M

ay-1

4 Ju

l-14

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5 Se

p-15

N

ov-1

5 Ja

n-16

M

ar-1

6 M

ay-1

6 Ju

l-16

Sep-

16

Nov

-16

Inst

itut

iona

l loa

n is

suan

ce ($

Bils

.) New Money

Refinancing New Money Share

Leveraged Loan Monthly - November 2016

11

U.S. INSTITUTIONAL LOAN ISSUANCE

Refinancing activity has jumped by 51% this year, outpacing growth in new money issuance which is up 21% year over year.

Just over half of institutional issuance (53%) this year is for new money purposes.

LEVERAGED

LOAN

MARKET O

VERVIEW

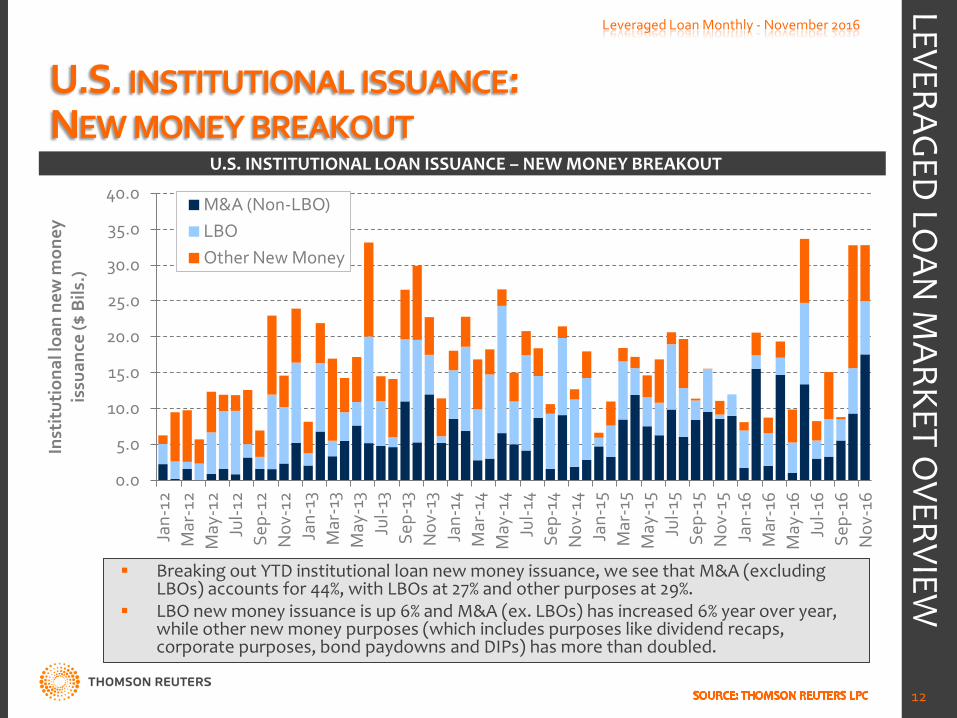

U.S. INSTITUTIONAL ISSUANCE: NEW MONEY BREAKOUT

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Jan-

12

Mar

-12

May

-12

Jul-1

2 Se

p-12

N

ov-1

2 Ja

n-13

M

ar-1

3 M

ay-1

3 Ju

l-13

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4 Se

p-14

N

ov-1

4 Ja

n-15

M

ar-1

5 M

ay-1

5 Ju

l-15

Sep-

15

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6 Se

p-16

N

ov-1

6

Inst

itut

iona

l loa

n ne

w m

oney

is

suan

ce ($

Bils

.)

M&A (Non-LBO) LBO Other New Money

Leveraged Loan Monthly - November 2016

12

U.S. INSTITUTIONAL LOAN ISSUANCE – NEW MONEY BREAKOUT

Breaking out YTD institutional loan new money issuance, we see that M&A (excluding LBOs) accounts for 44%, with LBOs at 27% and other purposes at 29%.

LBO new money issuance is up 6% and M&A (ex. LBOs) has increased 6% year over year, while other new money purposes (which includes purposes like dividend recaps, corporate purposes, bond paydowns and DIPs) has more than doubled.

LEVERAGED

LOAN

MARKET O

VERVIEW

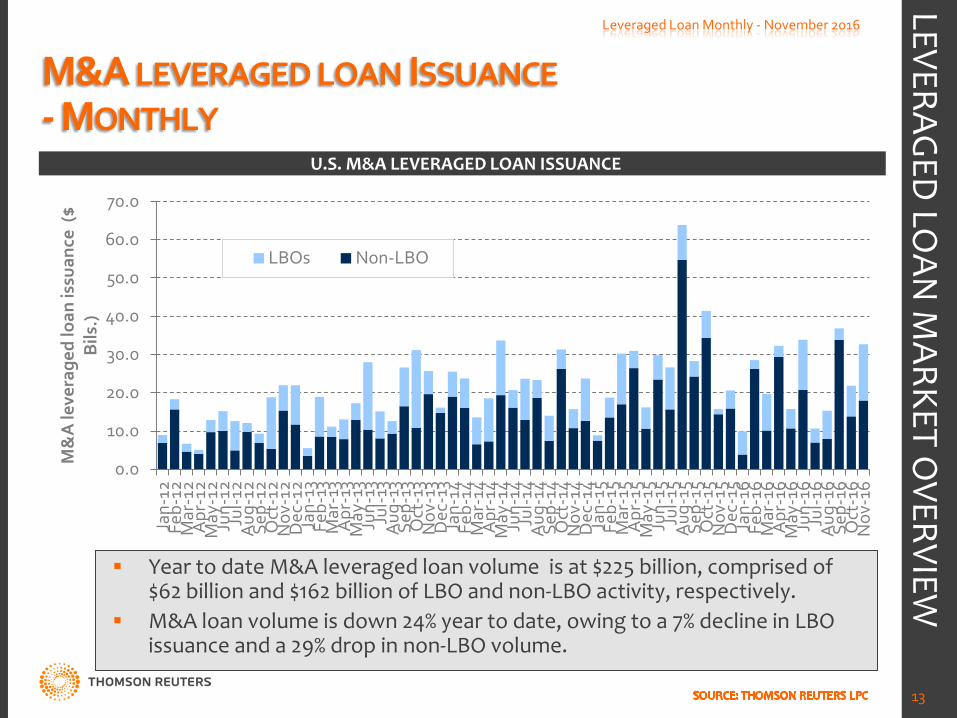

M&A LEVERAGED LOAN ISSUANCE - MONTHLY

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

Jan-

12

Feb-

12

Mar

-12

Apr

-12

May

-12

Jun-

12

Jul-1

2 A

ug-1

2 Se

p-12

O

ct-1

2 N

ov-1

2 D

ec-1

2 Ja

n-13

Fe

b-13

M

ar-1

3 A

pr-1

3 M

ay-1

3 Ju

n-13

Ju

l-13

Aug

-13

Sep-

13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb-

14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-1

4 A

ug-1

4 Se

p-14

O

ct-1

4 N

ov-1

4 D

ec-1

4 Ja

n-15

Fe

b-15

M

ar-1

5 A

pr-1

5 M

ay-1

5 Ju

n-15

Ju

l-15

Aug

-15

Sep-

15

Oct

-15

Nov

-15

Dec

-15

Jan-

16

Feb-

16

Mar

-16

Apr

-16

May

-16

Jun-

16

Jul-1

6 A

ug-1

6 Se

p-16

O

ct-1

6 N

ov-1

6

M&

A le

vera

ged

loan

issu

ance

($

Bils

.)

LBOs Non-LBO

Leveraged Loan Monthly - November 2016

13

U.S. M&A LEVERAGED LOAN ISSUANCE

Year to date M&A leveraged loan volume is at $225 billion, comprised of $62 billion and $162 billion of LBO and non-LBO activity, respectively.

M&A loan volume is down 24% year to date, owing to a 7% decline in LBO issuance and a 29% drop in non-LBO volume.

LEVERAGED

LOAN

MARKET O

VERVIEW

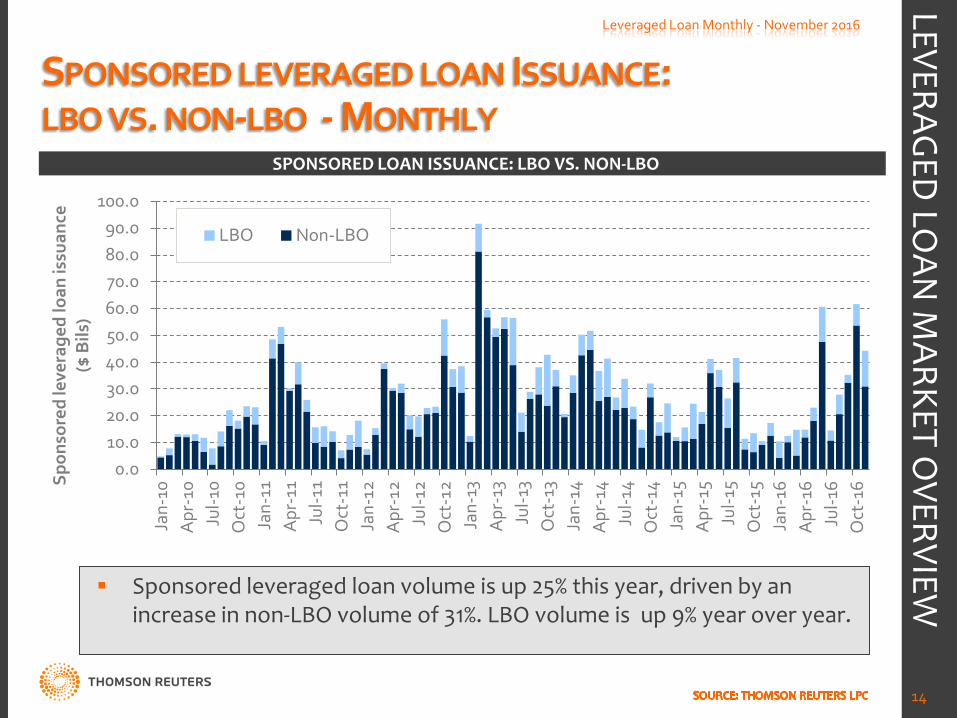

SPONSORED LEVERAGED LOAN ISSUANCE: LBO VS. NON-LBO - MONTHLY

0.0 10.0 20.0 30.0 40.0 50.0 60.0 70.0 80.0 90.0

100.0

Jan-

10

Apr

-10

Jul-1

0 O

ct-1

0 Ja

n-11

A

pr-1

1 Ju

l-11

Oct

-11

Jan-

12

Apr

-12

Jul-1

2 O

ct-1

2 Ja

n-13

A

pr-1

3 Ju

l-13

Oct

-13

Jan-

14

Apr

-14

Jul-1

4 O

ct-1

4 Ja

n-15

A

pr-1

5 Ju

l-15

Oct

-15

Jan-

16

Apr

-16

Jul-1

6 O

ct-1

6 Spon

sore

d le

vera

ged

loan

issu

ance

($

Bils

)

LBO Non-LBO

Leveraged Loan Monthly - November 2016

14

SPONSORED LOAN ISSUANCE: LBO VS. NON-LBO

Sponsored leveraged loan volume is up 25% this year, driven by an increase in non-LBO volume of 31%. LBO volume is up 9% year over year.

LEVERAGED

LOAN

MARKET O

VERVIEW

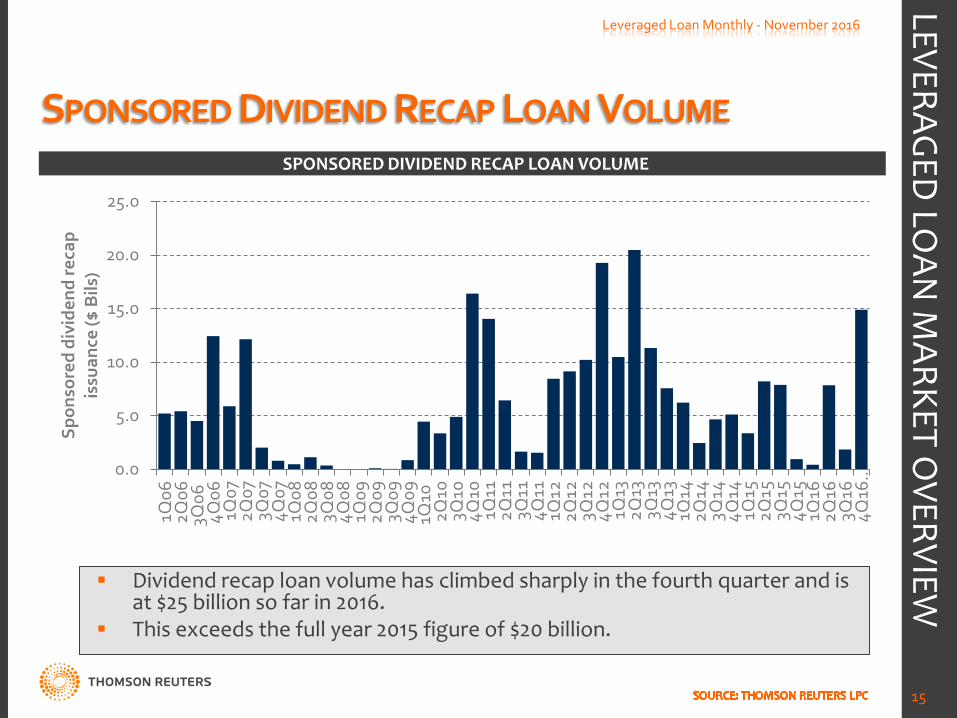

SPONSORED DIVIDEND RECAP LOAN VOLUME

0.0

5.0

10.0

15.0

20.0

25.0

1Q06

2Q

06

3Q06

4Q

06

1Q07

2Q

07

3Q07

4Q

07

1Q08

2Q

08

3Q08

4Q

08

1Q09

2Q

09

3Q09

4Q

09

1Q10

2Q

10

3Q10

4Q

10

1Q11

2Q

11

3Q11

4Q

11

1Q12

2Q

12

3Q12

4Q

12

1Q13

2Q

13

3Q13

4Q

13

1Q14

2Q

14

3Q14

4Q

14

1Q15

2Q

15

3Q15

4Q

15

1Q16

2Q

16

3Q16

4Q

16 …

Spon

sore

d di

vide

nd re

cap

is

suan

ce ($

Bils

)

Leveraged Loan Monthly - November 2016

15

SPONSORED DIVIDEND RECAP LOAN VOLUME

Dividend recap loan volume has climbed sharply in the fourth quarter and is at $25 billion so far in 2016.

This exceeds the full year 2015 figure of $20 billion.

LEVERAGED

LOAN

MARKET O

VERVIEW

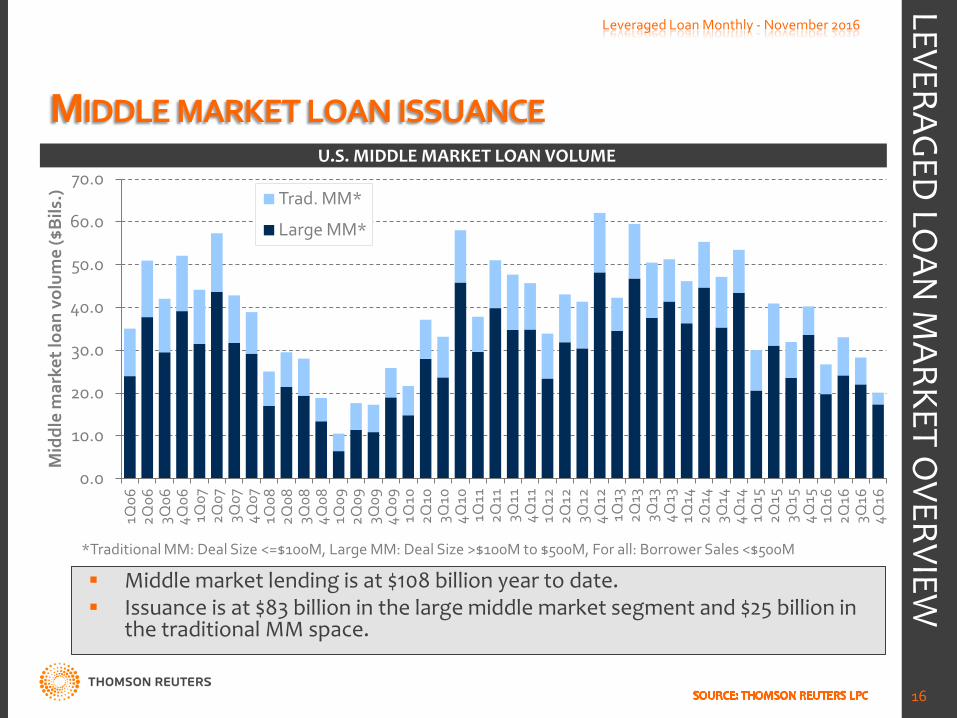

MIDDLE MARKET LOAN ISSUANCE

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

1Q06

2Q

06

3Q06

4Q

06

1Q07

2Q

07

3Q07

4Q

07

1Q08

2Q

08

3Q08

4Q

08

1Q09

2Q

09

3Q09

4Q

09

1Q10

2Q

10

3Q10

4Q

10

1Q11

2Q

11

3Q11

4Q

11

1Q12

2Q

12

3Q12

4Q

12

1Q13

2Q

13

3Q13

4Q

13

1Q14

2Q

14

3Q14

4Q

14

1Q15

2Q

15

3Q15

4Q

15

1Q16

2Q

16

3Q16

4Q

16

Mid

dle

mar

ket l

oan

volu

me

($B

ils.)

Trad. MM*

Large MM*

Leveraged Loan Monthly - November 2016

16

U.S. MIDDLE MARKET LOAN VOLUME

Middle market lending is at $108 billion year to date. Issuance is at $83 billion in the large middle market segment and $25 billion in

the traditional MM space.

LEVERAGED

LOAN

MARKET O

VERVIEW

*Traditional MM: Deal Size <=$100M, Large MM: Deal Size >$100M to $500M, For all: Borrower Sales <$500M

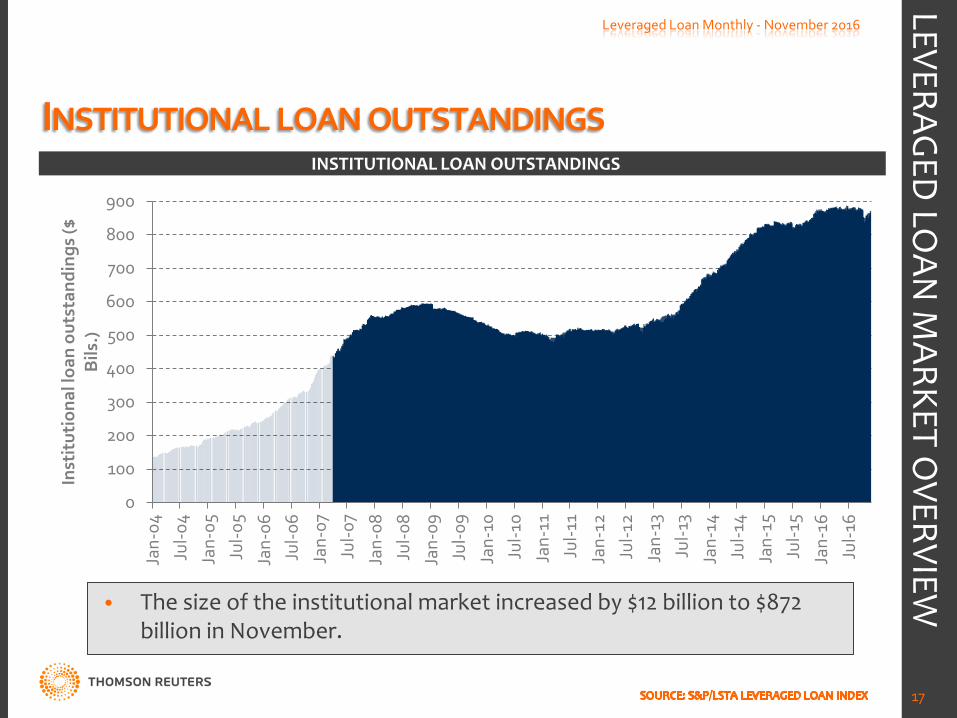

INSTITUTIONAL LOAN OUTSTANDINGS

0

100

200

300

400

500

600

700

800

900

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16

Jul-1

6

Inst

itut

iona

l loa

n ou

tsta

ndin

gs ($

B

ils.)

Leveraged Loan Monthly - November 2016

17

INSTITUTIONAL LOAN OUTSTANDINGS

• The size of the institutional market increased by $12 billion to $872 billion in November.

LEVERAGED

LOAN

MARKET O

VERVIEW

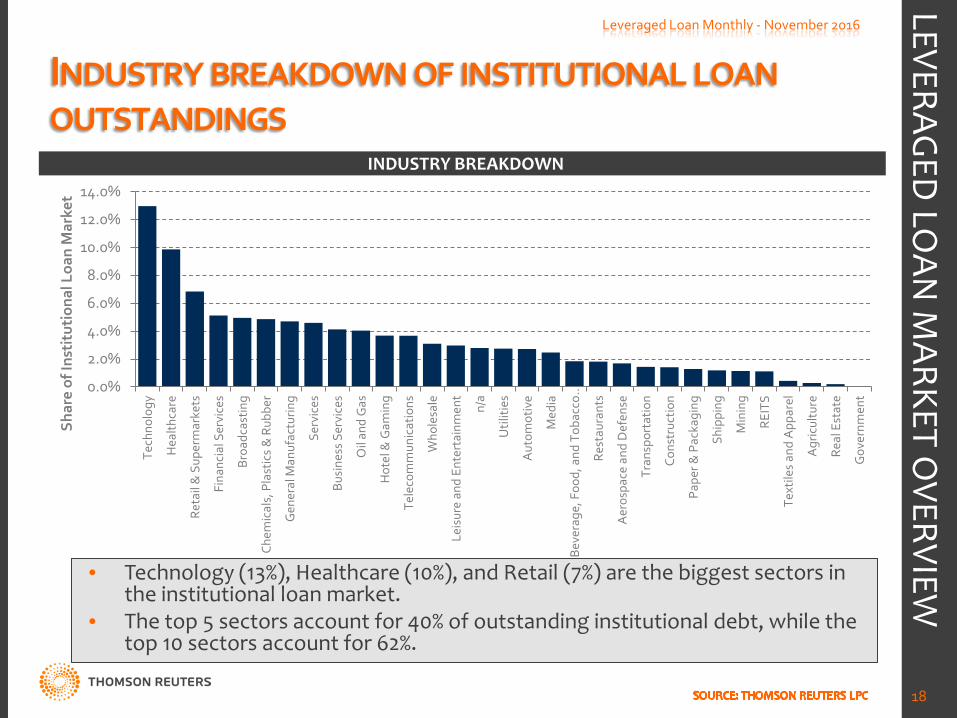

INDUSTRY BREAKDOWN OF INSTITUTIONAL LOAN OUTSTANDINGS

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Tech

nolo

gy

Hea

lthca

re

Reta

il &

Sup

erm

arke

ts

Fina

ncia

l Ser

vice

s

Broa

dcas

ting

Chem

ical

s, P

last

ics

& R

ubbe

r

Gen

eral

Man

ufac

turin

g

Serv

ices

Busi

ness

Ser

vice

s

Oil

and

Gas

Hot

el &

Gam

ing

Tele

com

mun

icat

ions

Who

lesa

le

Leis

ure

and

Ente

rtai

nmen

t

n/a

Util

ities

Aut

omot

ive

Med

ia

Beve

rage

, Foo

d, a

nd T

obac

co …

Rest

aura

nts

Aer

ospa

ce a

nd D

efen

se

Tran

spor

tatio

n

Cons

truc

tion

Pape

r & P

acka

ging

Ship

ping

Min

ing

REIT

S

Text

iles

and

App

arel

Agr

icul

ture

Real

Est

ate

Gov

ernm

ent

Shar

e of

Inst

itut

iona

l Loa

n M

arke

t

Leveraged Loan Monthly - November 2016

18

INDUSTRY BREAKDOWN

• Technology (13%), Healthcare (10%), and Retail (7%) are the biggest sectors in the institutional loan market.

• The top 5 sectors account for 40% of outstanding institutional debt, while the top 10 sectors account for 62%.

LEVERAGED

LOAN

MARKET O

VERVIEW

PRIMARY MARKET YIELDS

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

1Q10

Ju

l-10

Nov

-10

Mar

-11

Jul-1

1 N

ov-1

1 M

ar-1

2 Ju

l-12

Nov

-12

Mar

-13

Jul-1

3 N

ov-1

3 M

ar-1

4 Ju

l-14

Nov

-14

Mar

-15

Jul-1

5 N

ov-1

5 M

ar-1

6 Ju

l-16

Nov

-16

Ave

rage

yie

ld

Large Corporate Market

Middle Market

Monthly

Leveraged Loan Monthly - November 2016

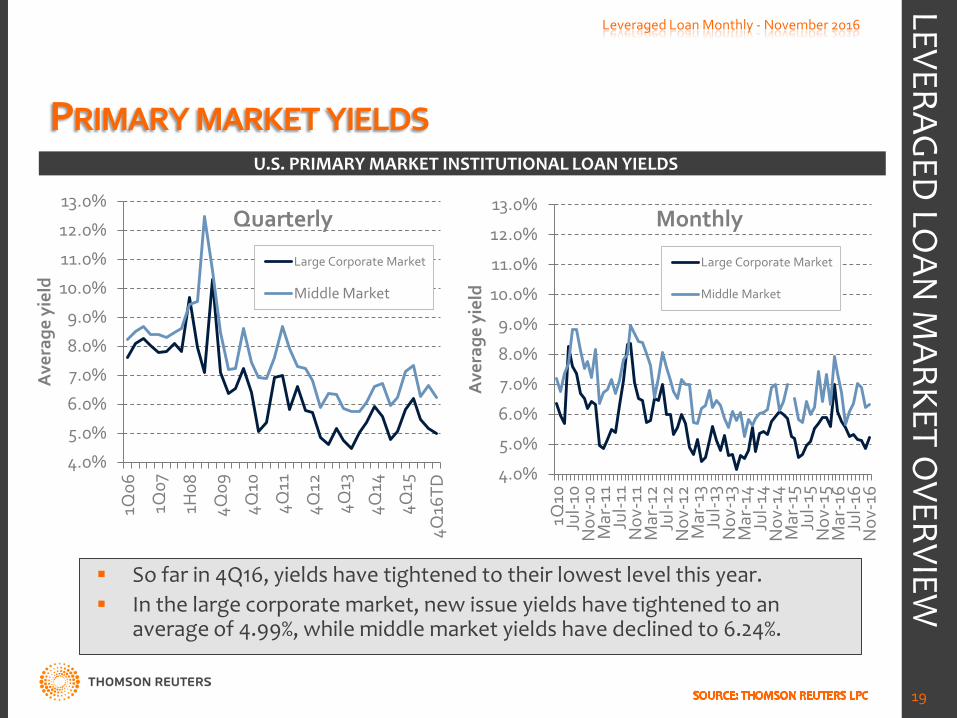

19

U.S. PRIMARY MARKET INSTITUTIONAL LOAN YIELDS

So far in 4Q16, yields have tightened to their lowest level this year. In the large corporate market, new issue yields have tightened to an

average of 4.99%, while middle market yields have declined to 6.24%.

LEVERAGED

LOAN

MARKET O

VERVIEW

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

1Q06

1Q07

1H08

4Q09

4Q10

4Q11

4Q12

4Q13

4Q14

4Q15

4Q16

TD

Ave

rage

yie

ld

Large Corporate Market

Middle Market

Quarterly

INSTITUTIONAL LOAN FLEX ACTIVITY

-3%

-2%

-1%

0%

1%

2%

3%

-60

-50

-40

-30

-20

-10

0

10

20

30

40

Jan-

12

Feb-

12

Mar

-12

Apr

-12

May

-12

Jun-

12

Jul-1

2 A

ug-1

2 Se

p-12

O

ct-1

2 N

ov-1

2 D

ec-1

2 Ja

n-13

Fe

b-13

M

ar-1

3 A

pr-1

3 M

ay-1

3 Ju

n-13

Ju

l-13

Aug

-13

Sep-

13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb-

14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-1

4 A

ug-1

4 Se

p-14

O

ct-1

4 N

ov-1

4 D

ec-1

4 Ja

n-15

Fe

b-15

M

ar-1

5 A

pr-1

5 M

ay-1

5 Ju

n-15

Ju

l-15

Aug

-15

Sep-

15

Oct

-15

Nov

-15

Dec

-15

Jan-

16

Feb-

16

Mar

-16

Apr

-16

May

-16

Jun-

16

Jul-1

6 A

ug-1

6 Se

p-16

O

ct-1

6 N

ov-1

6

Ave

rage

flex

Num

ber o

f fle

xes

# of flexes up/down

Avg. yield adjustment up/down

Leveraged Loan Monthly - November 2016

20

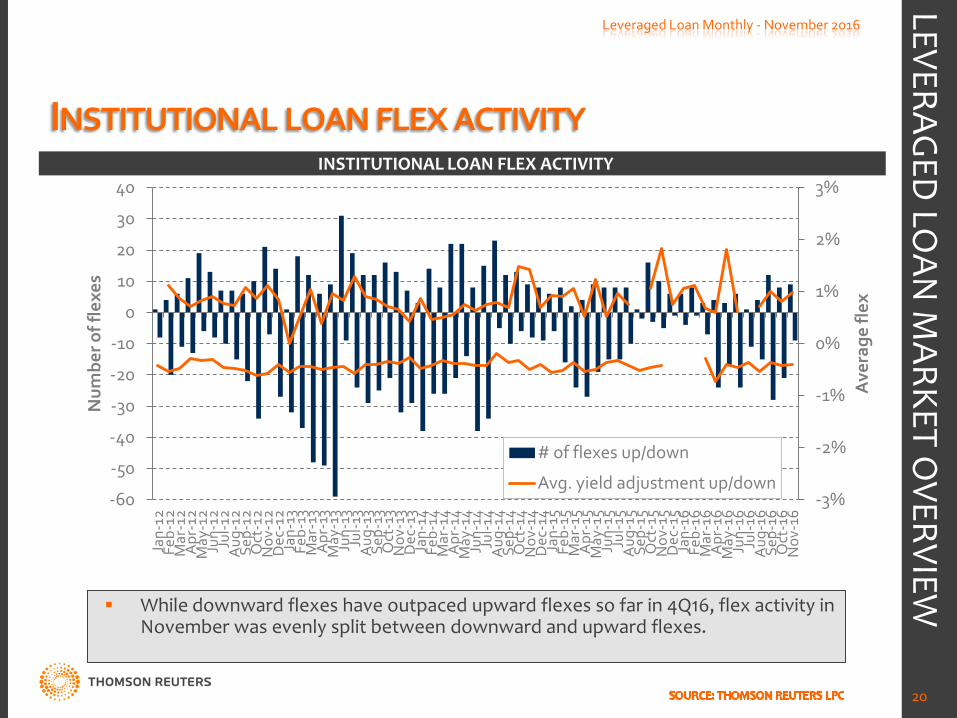

INSTITUTIONAL LOAN FLEX ACTIVITY

While downward flexes have outpaced upward flexes so far in 4Q16, flex activity in November was evenly split between downward and upward flexes.

LEVERAGED

LOAN

MARKET O

VERVIEW

INSTITUTIONAL LEVERAGED LOAN DEFAULTS

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Jan-

15

Feb-

15

Mar

-15

Apr

-15

May

-15

Jun-

15

Jul-1

5

Aug

-15

Sep-

15

Oct

-15

Nov

-15

Dec

-15

Jan-

16

Feb-

16

Mar

-16

Apr

-16

May

-16

Jun-

16

Jul-1

6

Aug

-16

Sep-

16

Oct

-16

Nov

-16

Def

ault

rate

Par

val

ue o

f def

ault

ed in

stit

utio

nal

loan

s ($

Bils

.)

Leveraged Loan Monthly - November 2016

21

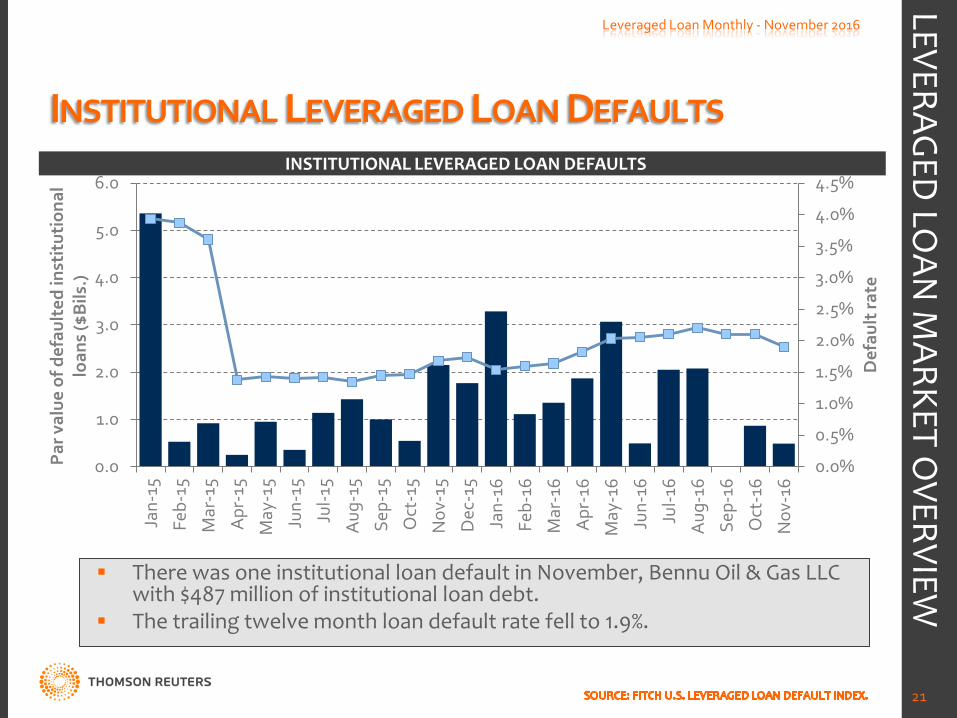

INSTITUTIONAL LEVERAGED LOAN DEFAULTS

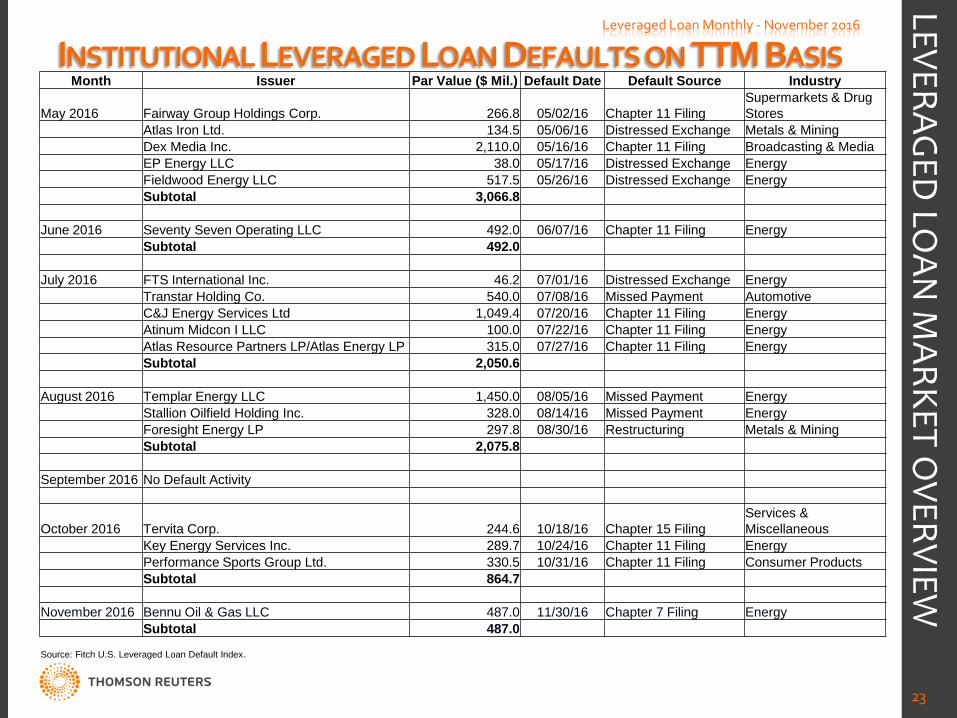

There was one institutional loan default in November, Bennu Oil & Gas LLC with $487 million of institutional loan debt.

The trailing twelve month loan default rate fell to 1.9%.

LEVERAGED

LOAN

MARKET O

VERVIEW

INSTITUTIONAL LEVERAGED LOAN DEFAULTS ON TTM BASIS Leveraged Loan Monthly - November 2016

22

LEVERAGED

LOAN

MARKET O

VERVIEW

Cont’d on next slide

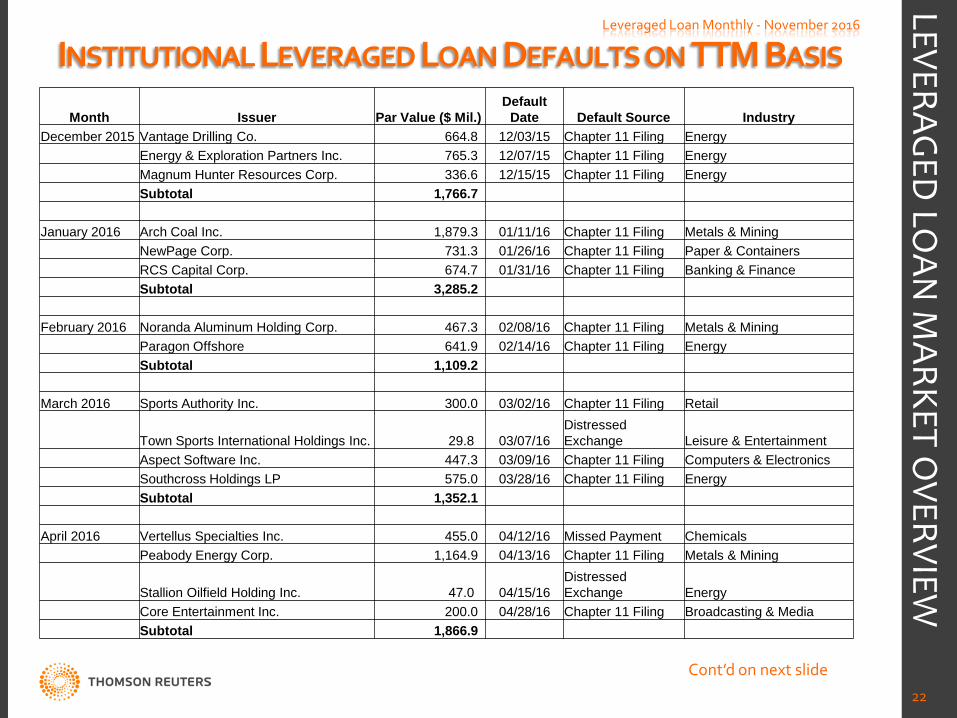

Month Issuer Par Value ($ Mil.) Default

Date Default Source Industry December 2015 Vantage Drilling Co. 664.8 12/03/15 Chapter 11 Filing Energy Energy & Exploration Partners Inc. 765.3 12/07/15 Chapter 11 Filing Energy Magnum Hunter Resources Corp. 336.6 12/15/15 Chapter 11 Filing Energy Subtotal 1,766.7 January 2016 Arch Coal Inc. 1,879.3 01/11/16 Chapter 11 Filing Metals & Mining NewPage Corp. 731.3 01/26/16 Chapter 11 Filing Paper & Containers RCS Capital Corp. 674.7 01/31/16 Chapter 11 Filing Banking & Finance Subtotal 3,285.2 February 2016 Noranda Aluminum Holding Corp. 467.3 02/08/16 Chapter 11 Filing Metals & Mining Paragon Offshore 641.9 02/14/16 Chapter 11 Filing Energy Subtotal 1,109.2 March 2016 Sports Authority Inc. 300.0 03/02/16 Chapter 11 Filing Retail

Town Sports International Holdings Inc. 29.8 03/07/16 Distressed Exchange Leisure & Entertainment

Aspect Software Inc. 447.3 03/09/16 Chapter 11 Filing Computers & Electronics Southcross Holdings LP 575.0 03/28/16 Chapter 11 Filing Energy Subtotal 1,352.1 April 2016 Vertellus Specialties Inc. 455.0 04/12/16 Missed Payment Chemicals Peabody Energy Corp. 1,164.9 04/13/16 Chapter 11 Filing Metals & Mining

Stallion Oilfield Holding Inc. 47.0 04/15/16 Distressed Exchange Energy

Core Entertainment Inc. 200.0 04/28/16 Chapter 11 Filing Broadcasting & Media Subtotal 1,866.9

INSTITUTIONAL LEVERAGED LOAN DEFAULTS ON TTM BASIS Leveraged Loan Monthly - November 2016

23

LEVERAGED

LOAN

MARKET O

VERVIEW

Month Issuer Par Value ($ Mil.) Default Date Default Source Industry

May 2016 Fairway Group Holdings Corp. 266.8 05/02/16 Chapter 11 Filing Supermarkets & Drug Stores

Atlas Iron Ltd. 134.5 05/06/16 Distressed Exchange Metals & Mining Dex Media Inc. 2,110.0 05/16/16 Chapter 11 Filing Broadcasting & Media EP Energy LLC 38.0 05/17/16 Distressed Exchange Energy Fieldwood Energy LLC 517.5 05/26/16 Distressed Exchange Energy Subtotal 3,066.8 June 2016 Seventy Seven Operating LLC 492.0 06/07/16 Chapter 11 Filing Energy Subtotal 492.0 July 2016 FTS International Inc. 46.2 07/01/16 Distressed Exchange Energy Transtar Holding Co. 540.0 07/08/16 Missed Payment Automotive C&J Energy Services Ltd 1,049.4 07/20/16 Chapter 11 Filing Energy Atinum Midcon I LLC 100.0 07/22/16 Chapter 11 Filing Energy Atlas Resource Partners LP/Atlas Energy LP 315.0 07/27/16 Chapter 11 Filing Energy Subtotal 2,050.6 August 2016 Templar Energy LLC 1,450.0 08/05/16 Missed Payment Energy Stallion Oilfield Holding Inc. 328.0 08/14/16 Missed Payment Energy Foresight Energy LP 297.8 08/30/16 Restructuring Metals & Mining Subtotal 2,075.8 September 2016 No Default Activity

October 2016 Tervita Corp. 244.6 10/18/16 Chapter 15 Filing Services & Miscellaneous

Key Energy Services Inc. 289.7 10/24/16 Chapter 11 Filing Energy Performance Sports Group Ltd. 330.5 10/31/16 Chapter 11 Filing Consumer Products Subtotal 864.7

November 2016 Bennu Oil & Gas LLC 487.0 11/30/16 Chapter 7 Filing Energy Subtotal 487.0

Source: Fitch U.S. Leveraged Loan Default Index.

U.S. SECONDARY MARKET BID LEVELS

90.0

92.0

94.0

96.0

98.0

100.0

102.0

Jan-

11

Mar

-11

May

-11

Jul-1

1 Se

p-11

N

ov-1

1 Ja

n-12

M

ar-1

2 M

ay-1

2 Ju

l-12

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3 Se

p-13

N

ov-1

3 Ja

n-14

M

ar-1

4 M

ay-1

4 Ju

l-14

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5 Se

p-15

N

ov-1

5 Ja

n-16

M

ar-1

6 M

ay-1

6 Ju

l-16

Sep-

16

Nov

-16

Avg

. Bid

(% o

f par

)

Multi-quote Inst. TLs All Inst. TLs SMi100

Leveraged Loan Monthly - November 2016

24

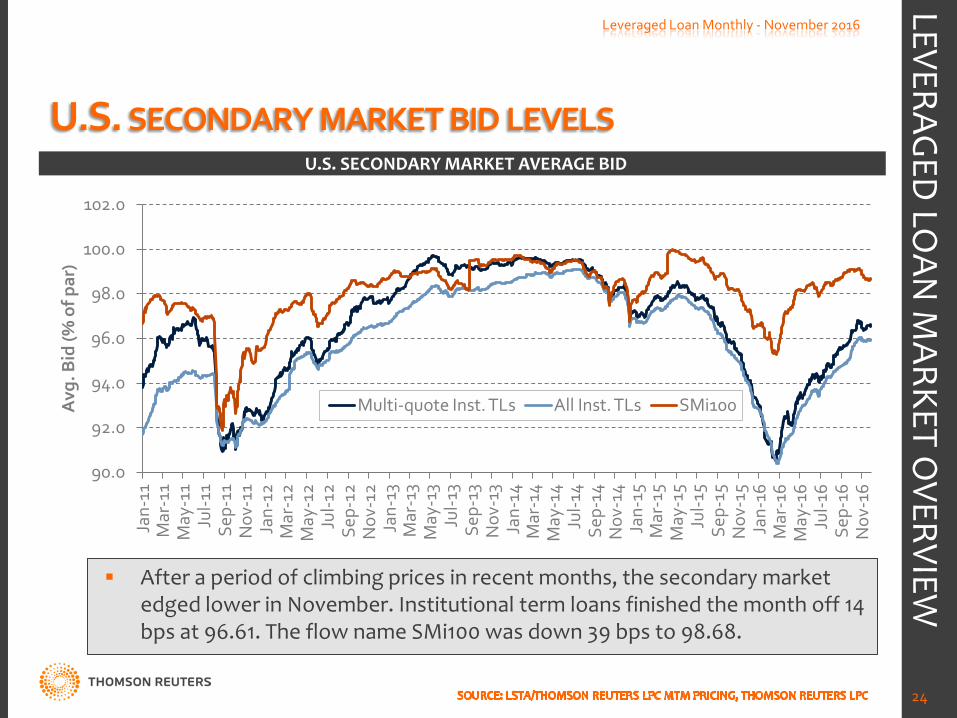

U.S. SECONDARY MARKET AVERAGE BID

After a period of climbing prices in recent months, the secondary market edged lower in November. Institutional term loans finished the month off 14 bps at 96.61. The flow name SMi100 was down 39 bps to 98.68.

LEVERAGED

LOAN

MARKET O

VERVIEW

DISTRIBUTION OF SECONDARY MARKET BIDS

0%

10%

20%

30%

40%

50%

60%

<70 70 to <80 80 to <85 85 to <90 90 to <95 95 to <98 98 to <99 99 to <100 100 to <101

>=101

Shar

e of

loan

s / d

olla

r vol

ume

Avg. bid (% of par)

# of loans $ weighted

Leveraged Loan Monthly - November 2016

25

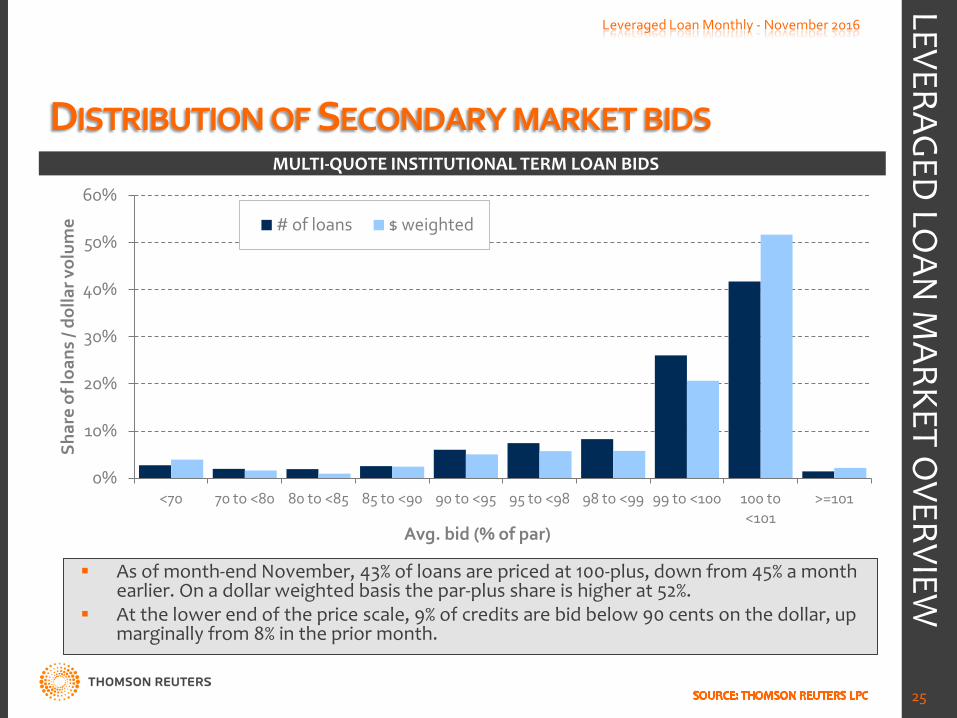

MULTI-QUOTE INSTITUTIONAL TERM LOAN BIDS

As of month-end November, 43% of loans are priced at 100-plus, down from 45% a month earlier. On a dollar weighted basis the par-plus share is higher at 52%.

At the lower end of the price scale, 9% of credits are bid below 90 cents on the dollar, up marginally from 8% in the prior month.

LEVERAGED

LOAN

MARKET O

VERVIEW

PAR-PLUS & 101-PLUS MARKET SHARE

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Jan-

12

Mar

-12

May

-12

Jul-1

2 Se

p-12

N

ov-1

2 Ja

n-13

M

ar-1

3 M

ay-1

3 Ju

l-13

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4 Se

p-14

N

ov-1

4 Ja

n-15

M

ar-1

5 M

ay-1

5 Ju

l-15

Sep-

15

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6 Se

p-16

N

ov-1

6

Shar

e of

loan

s bi

d >=

100

& >

=101

100-plus

101-plus

Leveraged Loan Monthly - November 2016

26

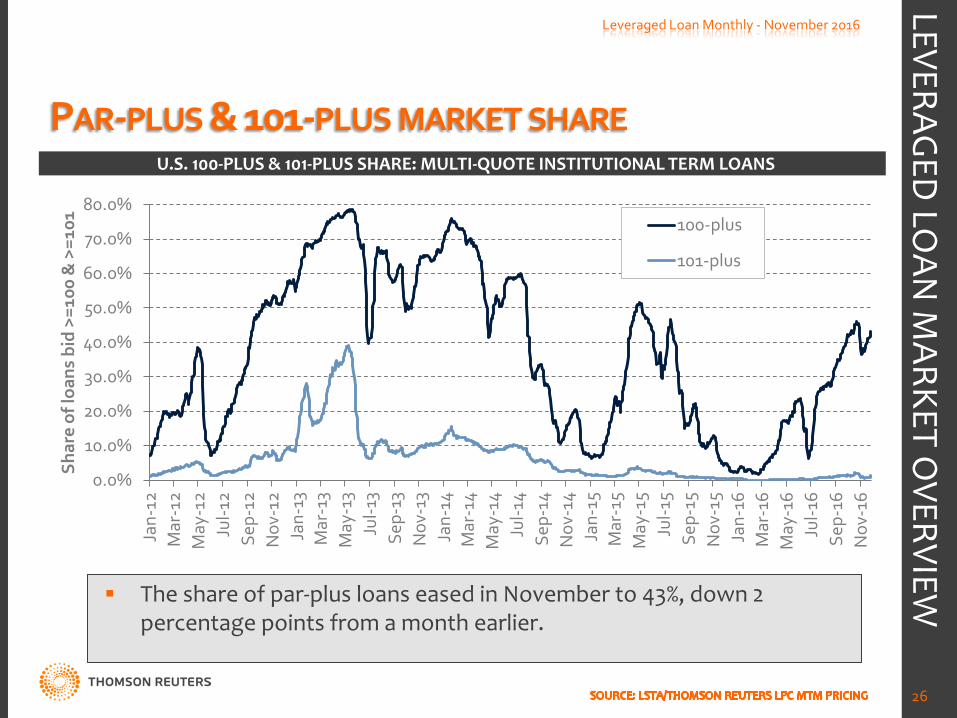

U.S. 100-PLUS & 101-PLUS SHARE: MULTI-QUOTE INSTITUTIONAL TERM LOANS

The share of par-plus loans eased in November to 43%, down 2 percentage points from a month earlier.

LEVERAGED

LOAN

MARKET O

VERVIEW

SECONDARY MARKET BIDS – BY SECTOR

0%

2%

4%

6%

8%

10%

12%

14%

50 55 60 65 70 75 80 85 90 95

100 105

Tran

spor

tatio

n

Cons

truc

tion

Hot

el &

…

Rest

aura

nts

REIT

S

Bus

ines

s …

Chem

ical

s, …

Leis

ure

and …

Fina

ncia

l …

Bev

erag

e, …

Aut

omot

ive

Hea

lthca

re

Tech

nolo

gy

Gen

eral

…

Tele

com

mun

i…

Med

ia

Serv

ices

Aer

ospa

ce …

Who

lesa

le

Util

ities

Min

ing

Reta

il &

…

Agr

icul

ture

Pape

r & …

Ship

ping

Text

iles

and …

Oil

and

Gas

Shar

e of

loan

s

Avg

. Bid

(% o

f par

)

Leveraged Loan Monthly - November 2016

27

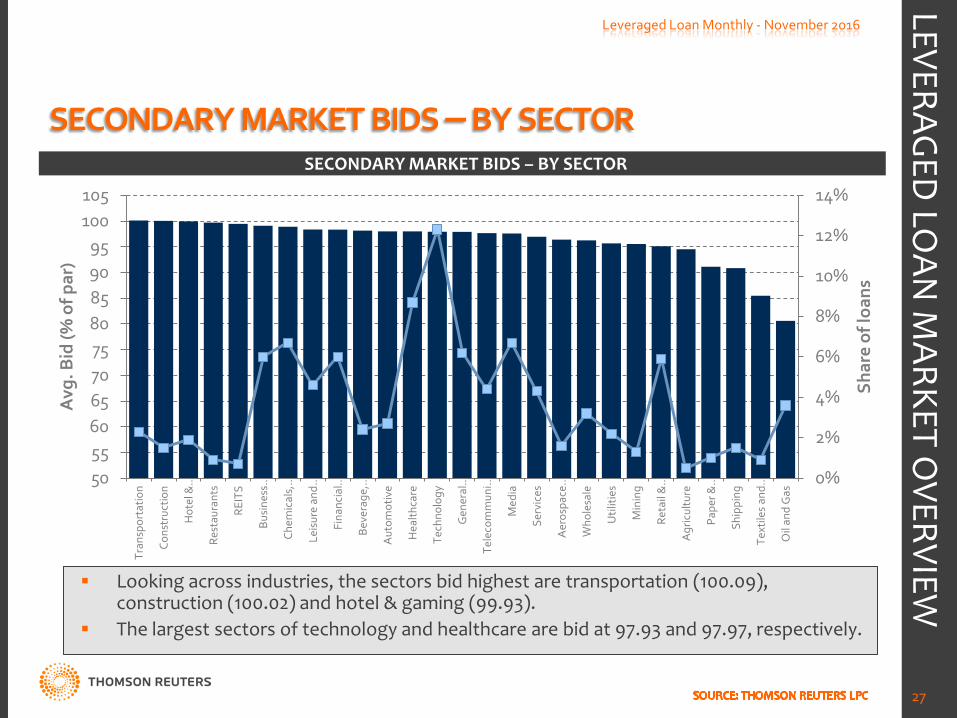

SECONDARY MARKET BIDS – BY SECTOR

Looking across industries, the sectors bid highest are transportation (100.09), construction (100.02) and hotel & gaming (99.93).

The largest sectors of technology and healthcare are bid at 97.93 and 97.97, respectively.

LEVERAGED

LOAN

MARKET O

VERVIEW

SECONDARY MARKET BID LEVELS: COVENANT-LITE & SECOND-LIENS

75.0

80.0

85.0

90.0

95.0

100.0

105.0

Jan-

11

Mar

-11

May

-11

Jul-1

1 Se

p-11

N

ov-1

1 Ja

n-12

M

ar-1

2 M

ay-1

2 Ju

l-12

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3 Se

p-13

N

ov-1

3 Ja

n-14

M

ar-1

4 M

ay-1

4 Ju

l-14

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5 Se

p-15

N

ov-1

5 Ja

n-16

M

ar-1

6 M

ay-1

6

Avg

. Bid

(% o

f par

)

Cov-lite 2nd Lien TL Multi-quote Inst. TLs

Leveraged Loan Monthly - November 2016

28

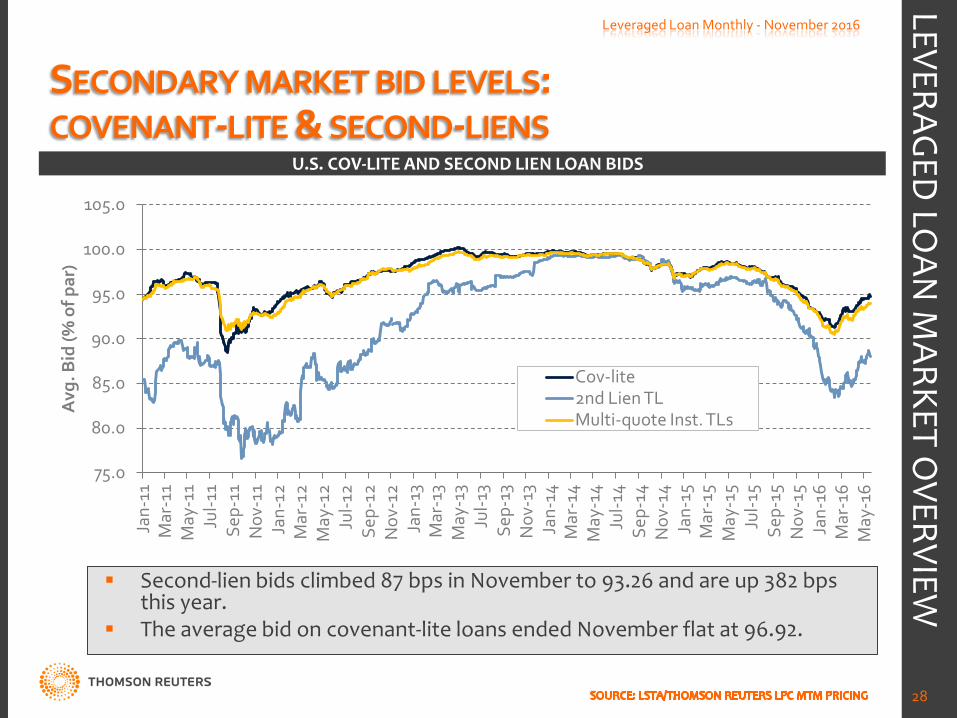

U.S. COV-LITE AND SECOND LIEN LOAN BIDS

Second-lien bids climbed 87 bps in November to 93.26 and are up 382 bps this year.

The average bid on covenant-lite loans ended November flat at 96.92.

LEVERAGED

LOAN

MARKET O

VERVIEW

SECONDARY MARKET BID LEVELS: EUROPE

88.0

90.0

92.0

94.0

96.0

98.0

100.0

102.0

Jan-

11

Mar

-11

May

-11

Jul-1

1 Se

p-11

N

ov-1

1 Ja

n-12

M

ar-1

2 M

ay-1

2 Ju

l-12

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3 Se

p-13

N

ov-1

3 Ja

n-14

M

ar-1

4 M

ay-1

4 Ju

l-14

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5 Se

p-15

N

ov-1

5 Ja

n-16

M

ar-1

6 M

ay-1

6 Ju

l-16

Sep-

16

Nov

-16

Avg

. Bid

(% o

f par

)

European Leveraged 40

U.S. SMi100

Leveraged Loan Monthly - November 2016

29

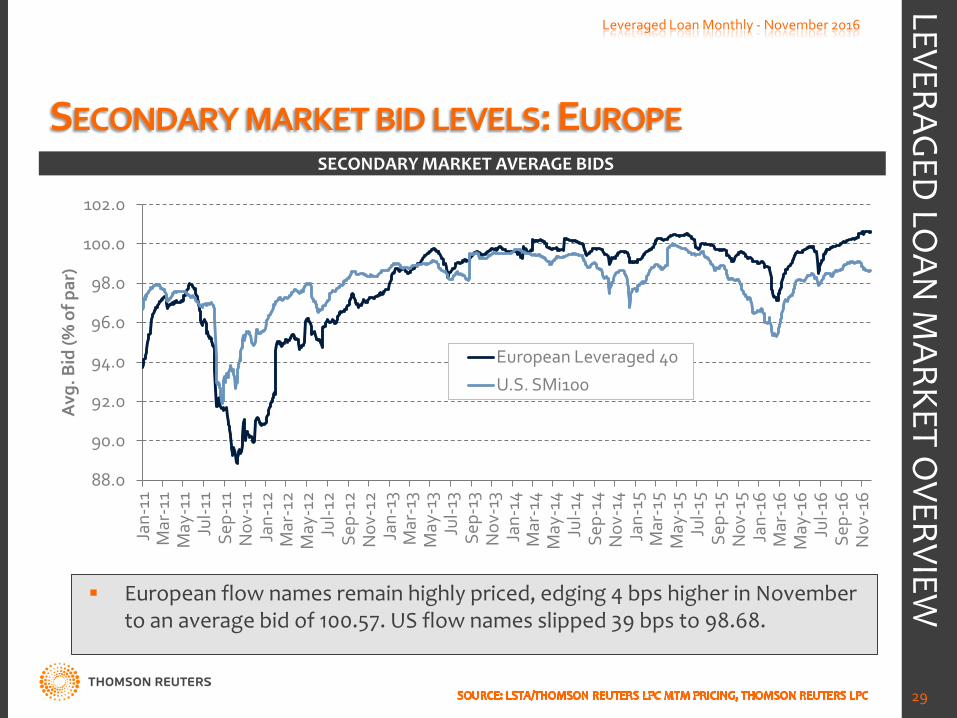

SECONDARY MARKET AVERAGE BIDS

European flow names remain highly priced, edging 4 bps higher in November to an average bid of 100.57. US flow names slipped 39 bps to 98.68.

LEVERAGED

LOAN

MARKET O

VERVIEW

U.S. HIGH YIELD BOND MARKET OVERVIEW

HIGH YIELD BOND ISSUANCE

0

10

20

30

40

50

60

70

80

90

100

0

10

20

30

40

50

60

Jan-

10

Mar

-10

May

-10

Jul-1

0 Se

p-10

N

ov-1

0 Ja

n-11

M

ar-1

1 M

ay-1

1 Ju

l-11

Sep-

11

Nov

-11

Jan-

12

Mar

-12

May

-12

Jul-1

2 Se

p-12

N

ov-1

2 Ja

n-13

M

ar-1

3 M

ay-1

3 Ju

l-13

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4 Se

p-14

N

ov-1

4 Ja

n-15

M

ar-1

5 M

ay-1

5 Ju

l-15

Sep-

15

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6 Se

p-16

N

ov-1

6

# o

f Iss

ues

Pro

ceed

s (U

S$ B

ils.)

Proceeds (US$ Bils.)

# of Issues

Leveraged Loan Monthly - November 2016

31

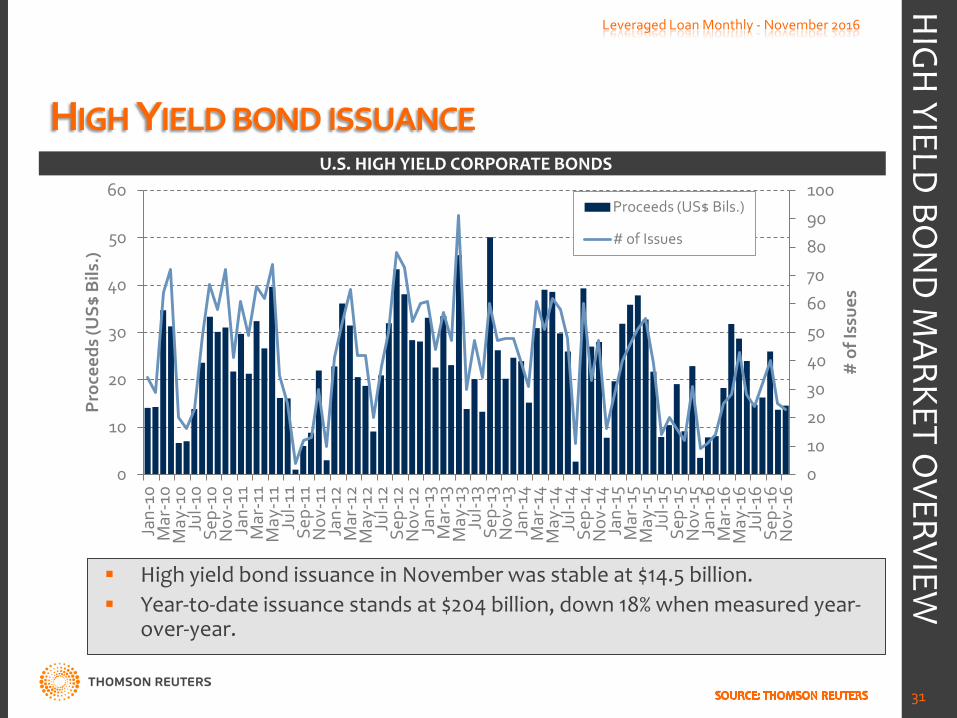

U.S. HIGH YIELD CORPORATE BONDS

High yield bond issuance in November was stable at $14.5 billion. Year-to-date issuance stands at $204 billion, down 18% when measured year-

over-year.

HIG

H YIELD

BON

D M

ARKET OVERVIEW

HIGH YIELD BONDS ISSUANCE - YTD BY INDUSTRY

0

10

20

30

40

50

60

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0 Fi

nanc

ials

Med

ia a

nd

Ente

rtai

nmen

t

Ener

gy a

nd

Pow

er

Mat

eria

ls

Indu

stria

ls

Hea

lthca

re

Hig

h Te

chno

logy

Tele

com

mun

icat

ions

Reta

il

Cons

umer

St

aple

s

Cons

umer

Pr

oduc

ts

Real

Est

ate

# o

f Iss

ues

Pro

ceed

s (U

S$ B

ils.)

Proceeds (US$ Bils.)

# of Issues

Leveraged Loan Monthly - November 2016

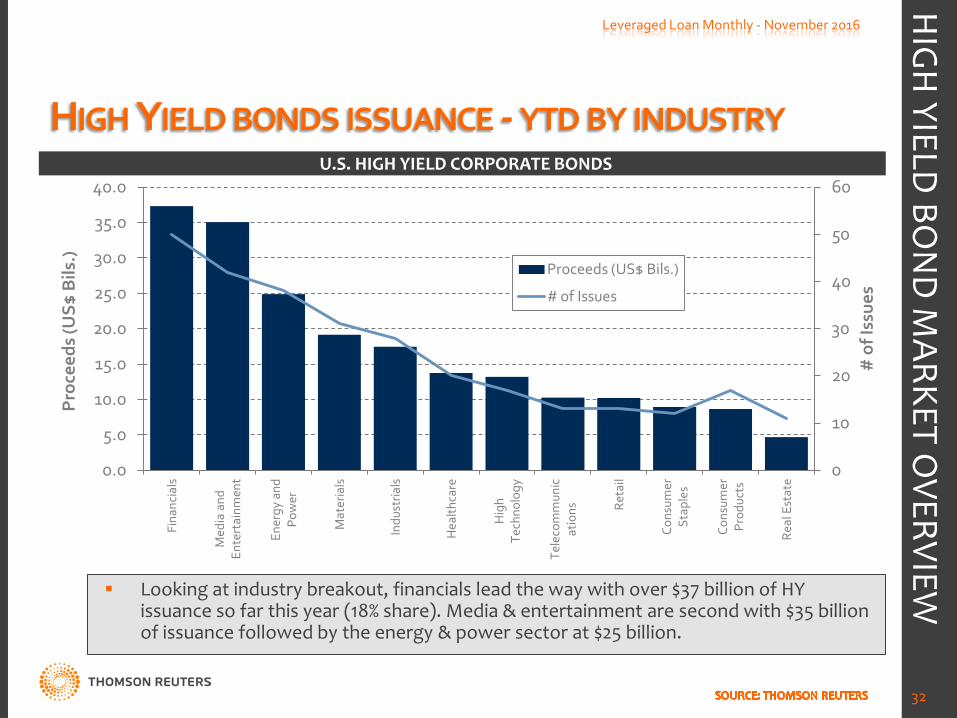

32

U.S. HIGH YIELD CORPORATE BONDS

Looking at industry breakout, financials lead the way with over $37 billion of HY issuance so far this year (18% share). Media & entertainment are second with $35 billion of issuance followed by the energy & power sector at $25 billion.

HIG

H YIELD

BON

D M

ARKET OVERVIEW

HIGH YIELD BONDS ISSUANCE - YTD BY SUB-INDUSTRY

5

10

15

20

25

30

0.0

5.0

10.0

15.0

20.0

25.0

Oth

er …

O

il &

Gas

Ca

ble

Cred

it …

Met

als

& …

H

ealth

care

…

Food

and

…

Pow

er

Food

& …

Co

ntai

ners

& …

Ca

sino

s &

…

Com

pute

rs &

…

Mac

hine

ry

Aut

omob

iles …

Br

oadc

astin

g Bu

ildin

g/Co

n…

Tele

com

mun

…

Mot

ion …

Pr

ofes

sion

al …

Sp

ace

and …

O

ther

…

Hos

pita

ls

Hot

els

and …

H

ealth

care

…

Adv

ertis

ing

& …

Se

mic

ondu

ct…

Ch

emic

als

Text

iles

& …

So

ftw

are

Aer

ospa

ce &

…

Cons

truc

tion …

Tr

ansp

orta

ti…

Oth

er R

etai

ling

Brok

erag

e Pi

pelin

es

Ass

et …

Ph

arm

aceu

ti…

AFI

NA

NCE

E-

com

mer

ce …

RE

ITs

Oth

er T

elec

om

Oth

er R

eal …

Re

al E

stat

e …

Wire

less

H

ome …

W

ater

and

…

Publ

ishi

ng

Insu

ranc

e In

tern

et …

H

ome …

IT

Con

sulti

ng …

A

ppar

el …

Ed

ucat

iona

l …

Oth

er …

Pa

per &

…

Toba

cco

# o

f Iss

ues

Pro

ceed

s (U

S$ B

ils.)

Proceeds (US$ Bils.)

# of Issues

Leveraged Loan Monthly - November 2016

33

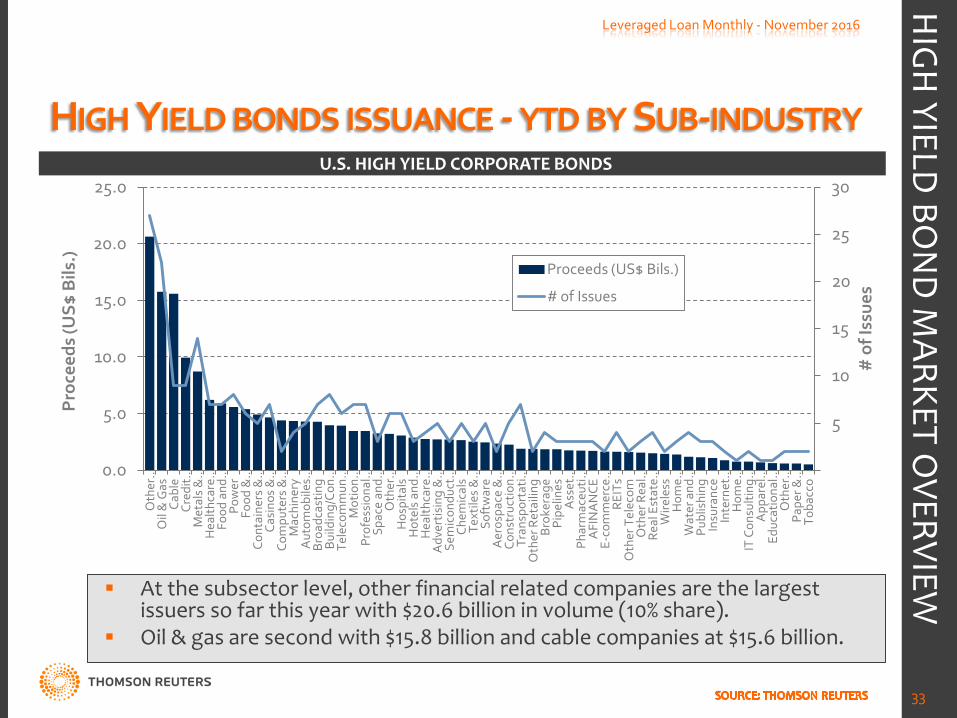

U.S. HIGH YIELD CORPORATE BONDS

At the subsector level, other financial related companies are the largest issuers so far this year with $20.6 billion in volume (10% share).

Oil & gas are second with $15.8 billion and cable companies at $15.6 billion.

HIG

H YIELD

BON

D M

ARKET OVERVIEW

HIGH YIELD BOND ISSUANCE – YTD BY RATING

10

20

30

40

50

60

70

80

0.0

10.0

20.0

30.0

40.0

50.0

60.0

BB+ BB BB- B+ B B- CCC+ CCC CCC- C NR

# o

f Iss

ues

Pro

ceed

s (U

S$ B

ils.)

Proceeds (US$ Bils.)

# of Issues

Leveraged Loan Monthly - November 2016

34

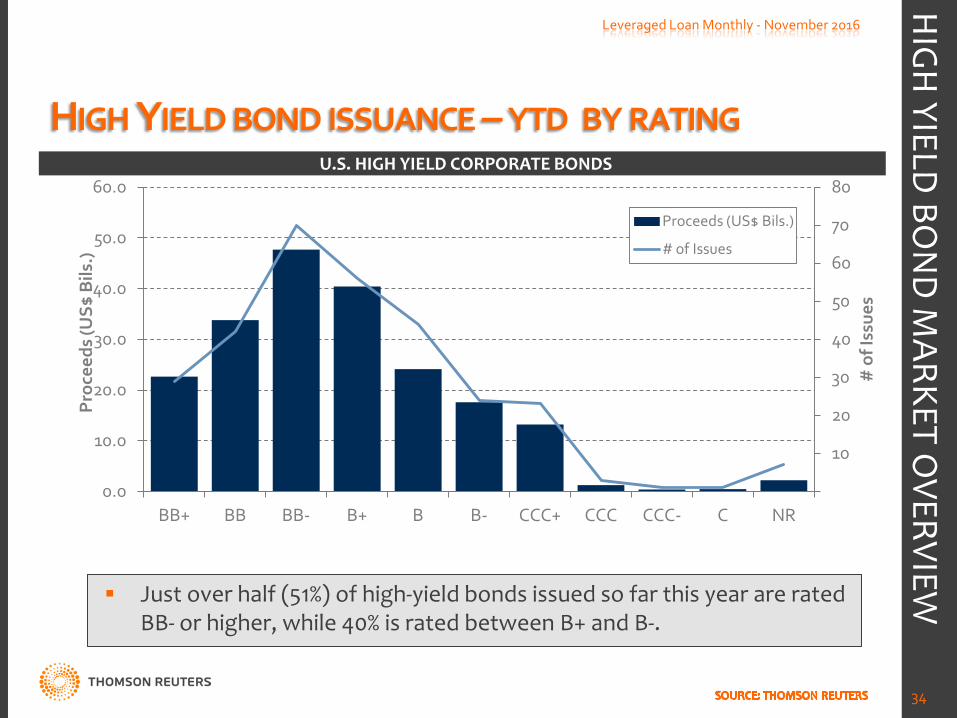

U.S. HIGH YIELD CORPORATE BONDS

Just over half (51%) of high-yield bonds issued so far this year are rated BB- or higher, while 40% is rated between B+ and B-.

HIG

H YIELD

BON

D M

ARKET OVERVIEW

HY BOND FUND FLOWS – MUTUAL FUND VS. ETF BREAKOUT*

Leveraged Loan Monthly - November 2016

35

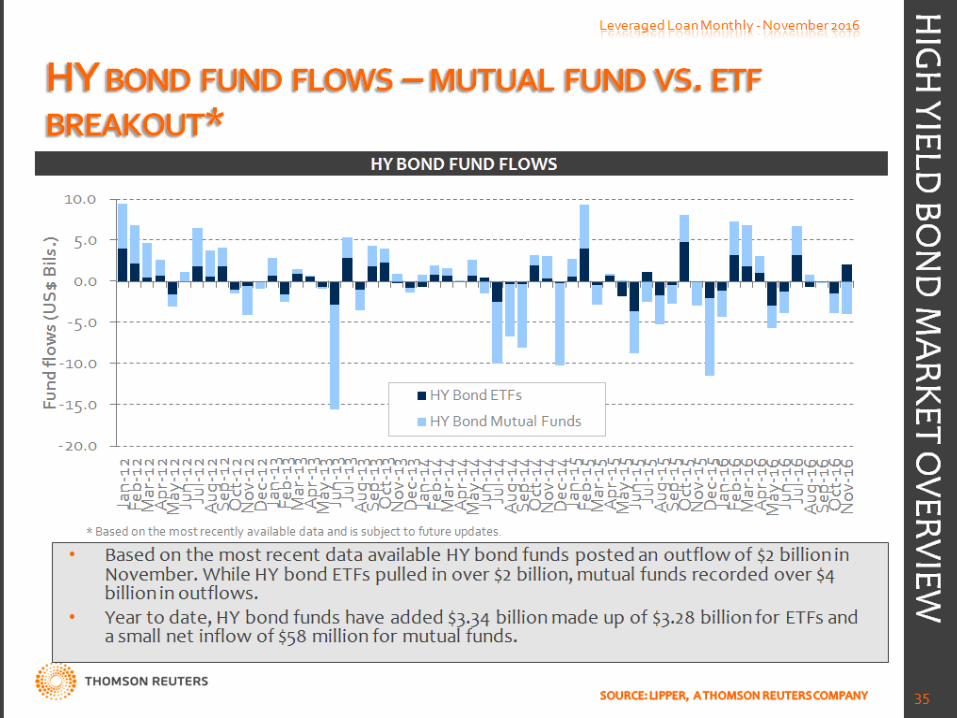

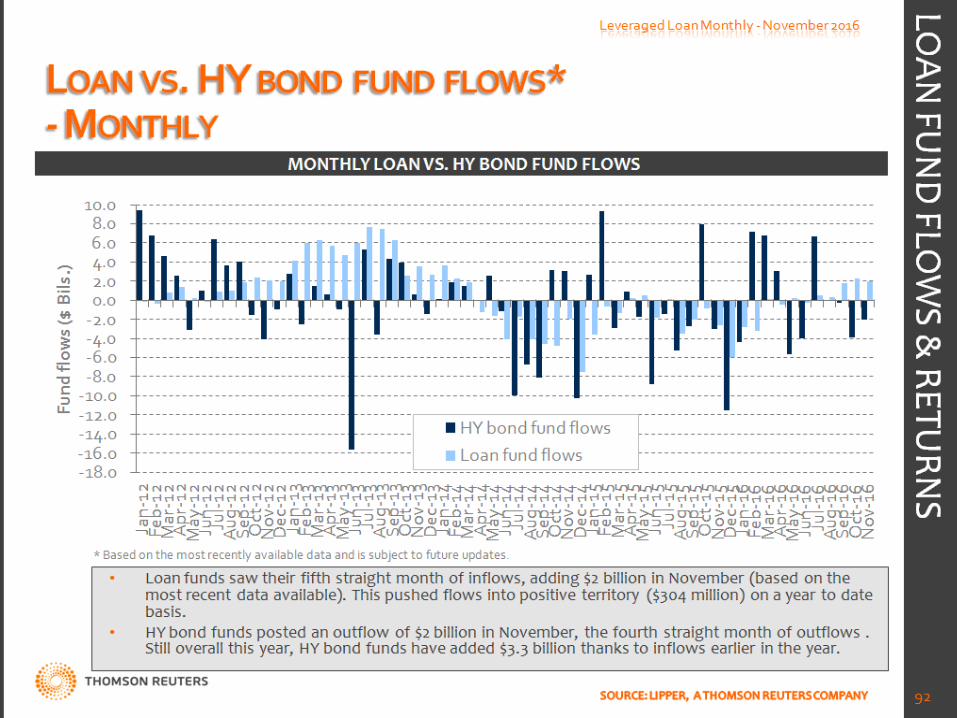

HY BOND FUND FLOWS

• Based on the most recent data available HY bond funds posted an outflow of $2 billion in November. While HY bond ETFs pulled in over $2 billion, mutual funds recorded over $4 billion in outflows.

• Year to date, HY bond funds have added $3.34 billion made up of $3.28 billion for ETFs and a small net inflow of $58 million for mutual funds.

HIG

H YIELD

BON

D M

ARKET OVERVIEW

* Based on the most recently available data and is subject to future updates.

INVESTOR OVERVIEW

U.S. CLO ASSETS UNDER MANAGEMENT

500 550 600 650 700 750 800 850 900 950 1,000 1,050 1,100

150 170 190 210 230 250 270 290 310 330 350 370 390 410 430 450

Jan-

13

Apr

-13

Jul-1

3

Oct

-13

Jan-

14

Apr

-14

Jul-1

4

Oct

-14

Jan-

15

Apr

-15

Jul-1

5

Oct

-15

Jan-

16

Apr

-16

Jul-1

6

Oct

-16

Num

ber o

f CLO

s in

sam

ple

CLO

Agg

rega

te P

rinc

ipal

B

alan

ce ($

Bils

.)

CLO APB Number of CLOs

Leveraged Loan Monthly - November 2016

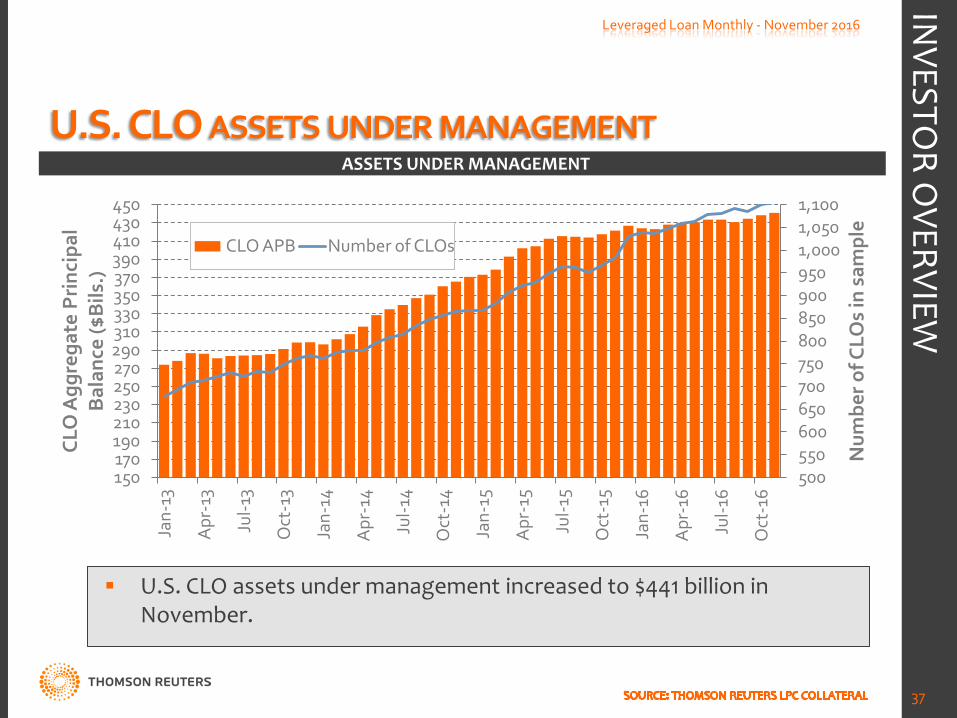

37

ASSETS UNDER MANAGEMENT

U.S. CLO assets under management increased to $441 billion in November.

INVESTO

R OVERVIEW

LOAN FUNDS AUM

0 20 40 60 80

100 120 140 160 180 200

Jan-

07

Jun-

07

Nov

-07

Apr

-08

Sep-

08

Feb-

09

Jul-0

9

Dec

-09

May

-10

Oct

-10

Mar

-11

Aug

-11

Jan-

12

Jun-

12

Nov

-12

Apr

-13

Sep-

13

Feb-

14

Jul-1

4

Dec

-14

May

-15

Oct

-15

Mar

-16

Aug

-16

Loan

mut

ual f

und

& E

TF A

UM

($

Bils

.)

Leveraged Loan Monthly - November 2016

38

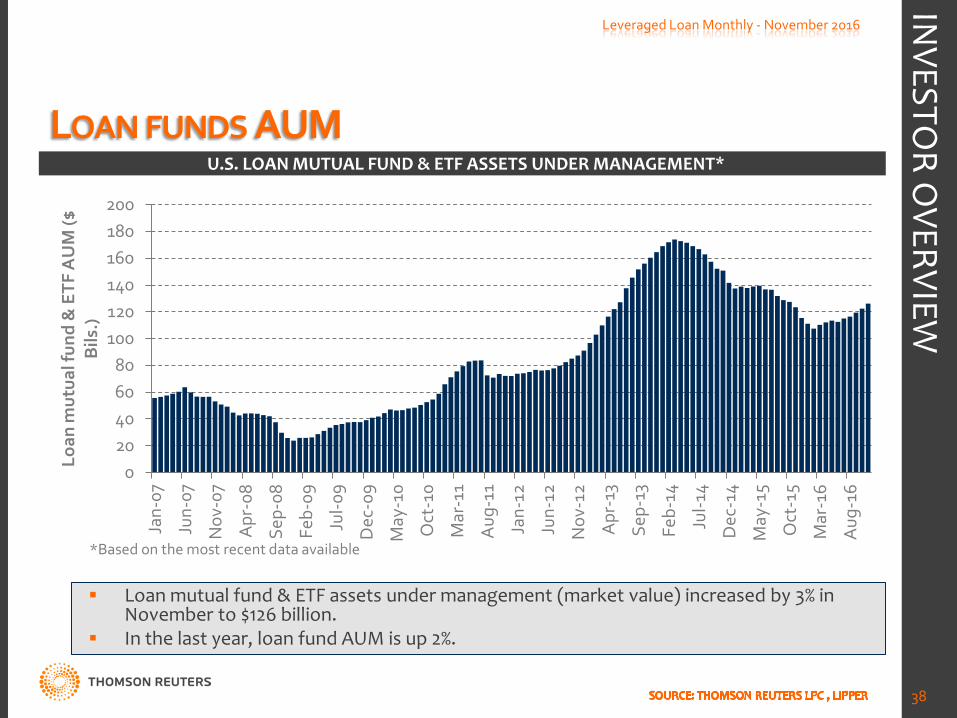

U.S. LOAN MUTUAL FUND & ETF ASSETS UNDER MANAGEMENT*

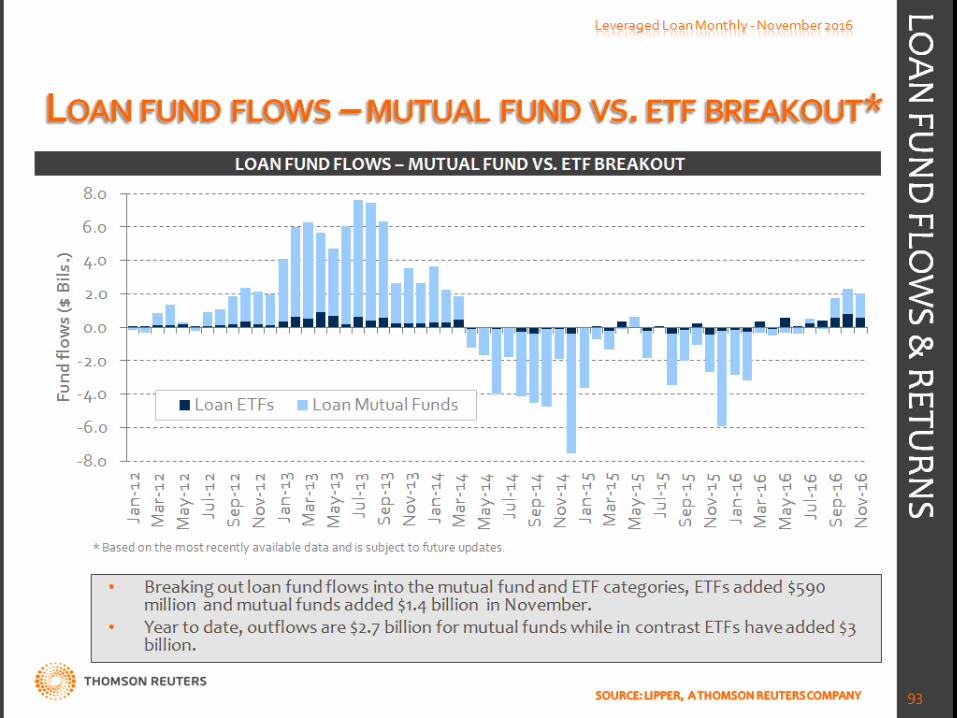

Loan mutual fund & ETF assets under management (market value) increased by 3% in November to $126 billion.

In the last year, loan fund AUM is up 2%.

INVESTO

R OVERVIEW

*Based on the most recent data available

INVESTOR SHARE OF INSTITUTIONAL LOAN OUTSTANDINGS

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

Aug

-12

Nov

-12

Feb-

13

May

-13

Aug

-13

Nov

-13

Feb-

14

May

-14

Aug

-14

Nov

-14

Feb-

15

May

-15

Aug

-15

Nov

-15

Feb-

16

May

-16

Aug

-16

Nov

-16

Inve

stor

sha

re o

f ins

titu

tion

al lo

an

outs

tand

ings

(%)

CLOs

Loan Funds (mutual funds & ETFs)

Other

Leveraged Loan Monthly - November 2016

39

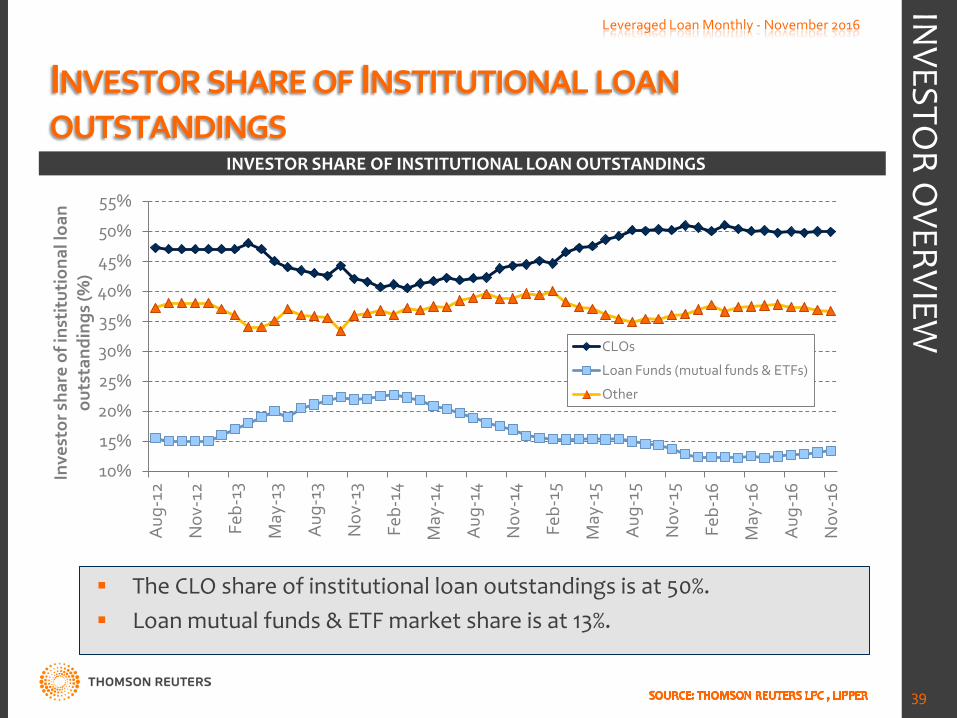

INVESTOR SHARE OF INSTITUTIONAL LOAN OUTSTANDINGS

The CLO share of institutional loan outstandings is at 50%. Loan mutual funds & ETF market share is at 13%.

INVESTO

R OVERVIEW

CLO ISSUANCE VS. LOAN FUND FLOWS -MONTHLY

-8.0 -6.0 -4.0 -2.0 0.0 2.0 4.0 6.0 8.0

10.0 12.0 14.0 16.0 18.0 20.0

Jan-

12

Mar

-12

May

-12

Jul-1

2 Se

p-12

N

ov-1

2 Ja

n-13

M

ar-1

3 M

ay-1

3 Ju

l-13

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4 Se

p-14

N

ov-1

4 Ja

n-15

M

ar-1

5 M

ay-1

5 Ju

l-15

Sep-

15

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6 Se

p-16

N

ov-1

6

$ B

ils.

CLO Issuance Loan fund flows

Leveraged Loan Monthly - November 2016

40

MONTHLY CLO ISSUANCE VS. LOAN FUND FLOWS

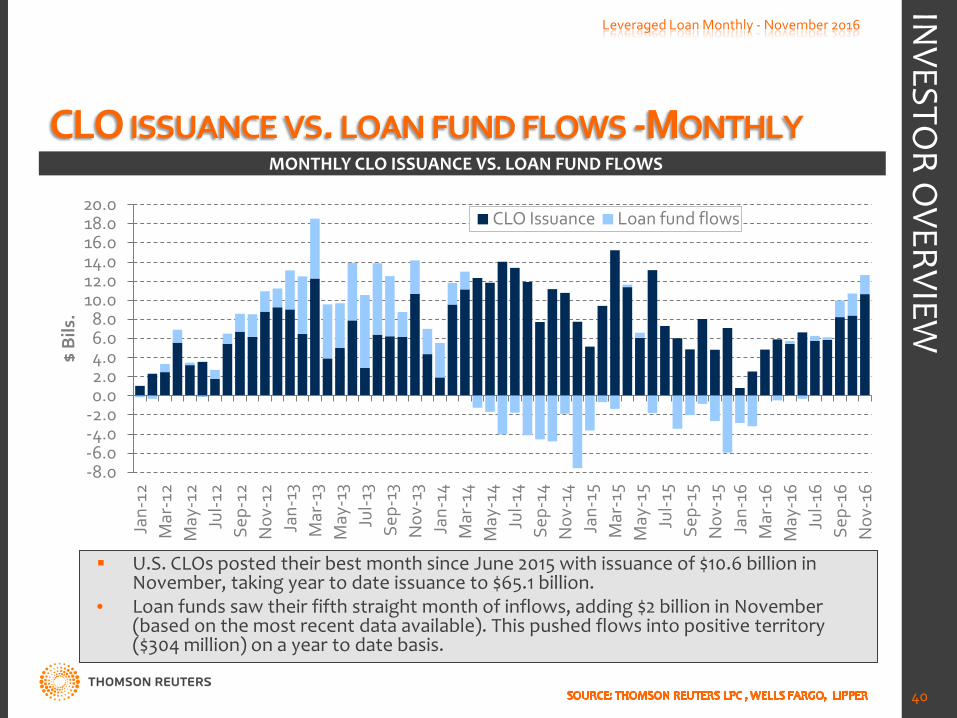

U.S. CLOs posted their best month since June 2015 with issuance of $10.6 billion in November, taking year to date issuance to $65.1 billion.

• Loan funds saw their fifth straight month of inflows, adding $2 billion in November (based on the most recent data available). This pushed flows into positive territory ($304 million) on a year to date basis.

INVESTO

R OVERVIEW

CLO MARKET ANALYSIS*

*Based on the most recently available data in Thomson Reuters LPC Collateral

U.S. CLO ISSUANCE - MONTHLY

0

5

10

15

20

25

30

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Jan-

11

Mar

-11

May

-11

Jul-1

1 Se

p-11

N

ov-1

1 Ja

n-12

M

ar-1

2 M

ay-1

2 Ju

l-12

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3 Se

p-13

N

ov-1

3 Ja

n-14

M

ar-1

4 M

ay-1

4 Ju

l-14

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5 Se

p-15

N

ov-1

5 Ja

n-16

M

ar-1

6 M

ay-1

6 Ju

l-16

Sep-

16

Nov

-16

Num

ber o

f CLO

s is

sued

CLO

Issu

ance

($B

ils.)

Issuance ($Bils.)

Count

Leveraged Loan Monthly - November 2016

42

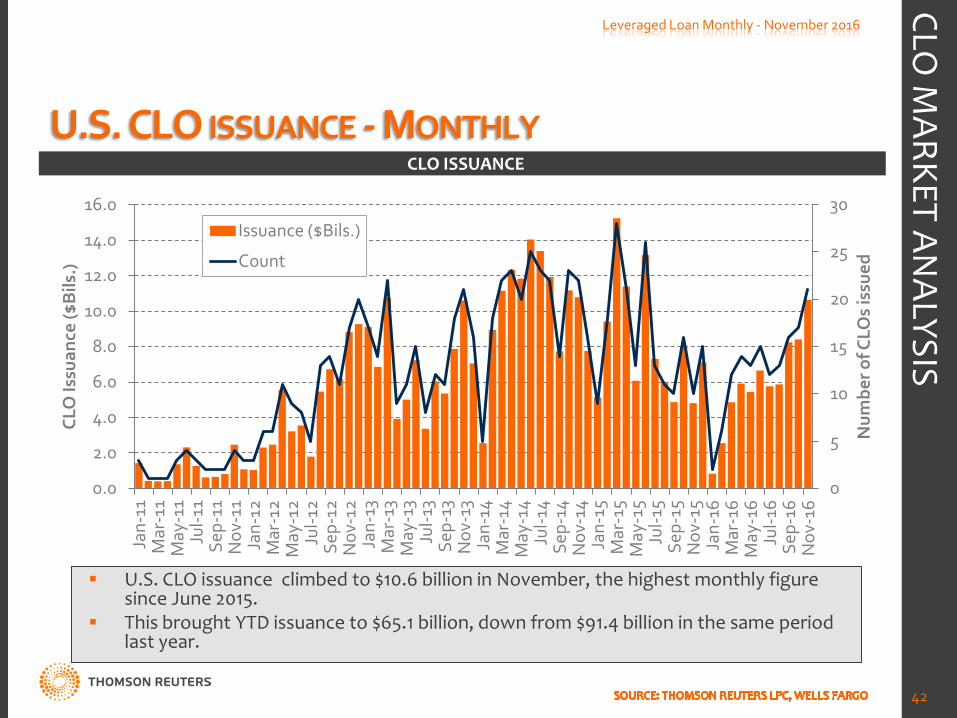

CLO ISSUANCE

U.S. CLO issuance climbed to $10.6 billion in November, the highest monthly figure since June 2015.

This brought YTD issuance to $65.1 billion, down from $91.4 billion in the same period last year.

CLO M

ARKET ANALYSIS

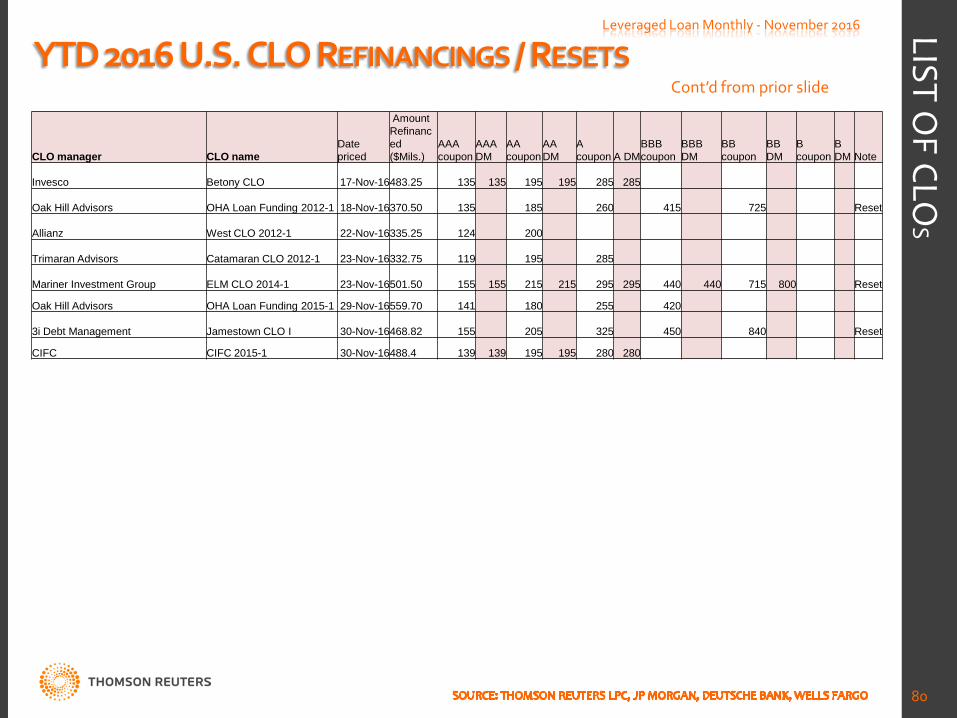

U.S. CLO REFINANCINGS & RESETS

0

2

4

6

8

10

12

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16

$ B

ils.

Leveraged Loan Monthly - November 2016

43

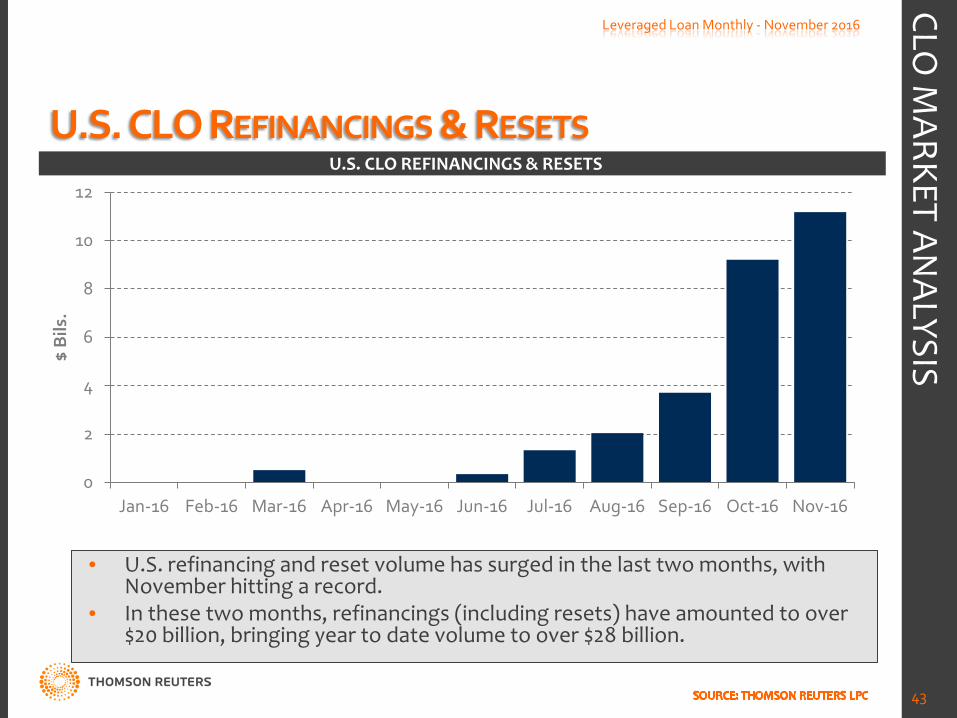

U.S. CLO REFINANCINGS & RESETS

• U.S. refinancing and reset volume has surged in the last two months, with November hitting a record.

• In these two months, refinancings (including resets) have amounted to over $20 billion, bringing year to date volume to over $28 billion.

CLO M

ARKET ANALYSIS

U.S. CLO AAA SPREADS

120

130

140

150

160

170

180

190

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16

AA

A d

isco

unt m

argi

n* (b

ps)

Average

Leveraged Loan Monthly - November 2016

44

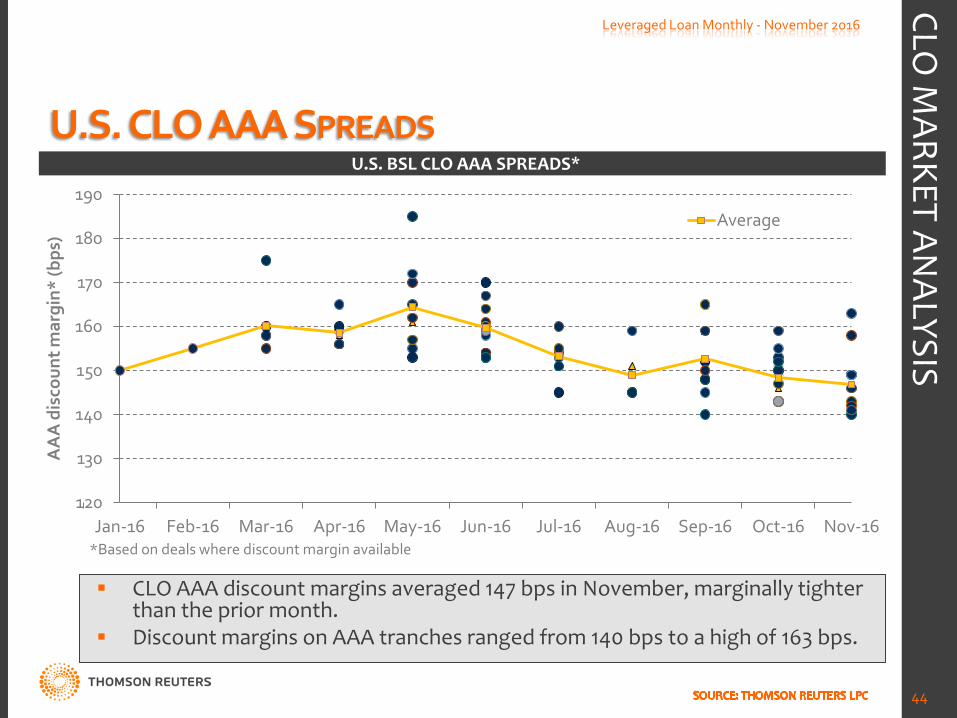

U.S. BSL CLO AAA SPREADS*

CLO AAA discount margins averaged 147 bps in November, marginally tighter than the prior month.

Discount margins on AAA tranches ranged from 140 bps to a high of 163 bps.

CLO M

ARKET ANALYSIS

*Based on deals where discount margin available

U.S. CLO AVERAGE SIZE

300

350

400

450

500

550

600

650

Jan-

13

Feb-

13

Mar

-13

Apr

-13

May

-13

Jun-

13

Jul-1

3 A

ug-1

3 Se

p-13

O

ct-1

3 N

ov-1

3 D

ec-1

3 Ja

n-14

Fe

b-14

M

ar-1

4 A

pr-1

4 M

ay-1

4 Ju

n-14

Ju

l-14

Aug

-14

Sep-

14

Oct

-14

Nov

-14

Dec

-14

Jan-

15

Feb-

15

Mar

-15

Apr

-15

May

-15

Jun-

15

Jul-1

5 A

ug-1

5 Se

p-15

O

ct-1

5 N

ov-1

5 D

ec-1

5 Ja

n-16

Fe

b-16

M

ar-1

6 A

pr-1

6 M

ay-1

6 Ju

n-16

Ju

l-16

Aug

-16

Sep-

16

Oct

-16

Nov

-16

$ M

ils.

Leveraged Loan Monthly - November 2016

45

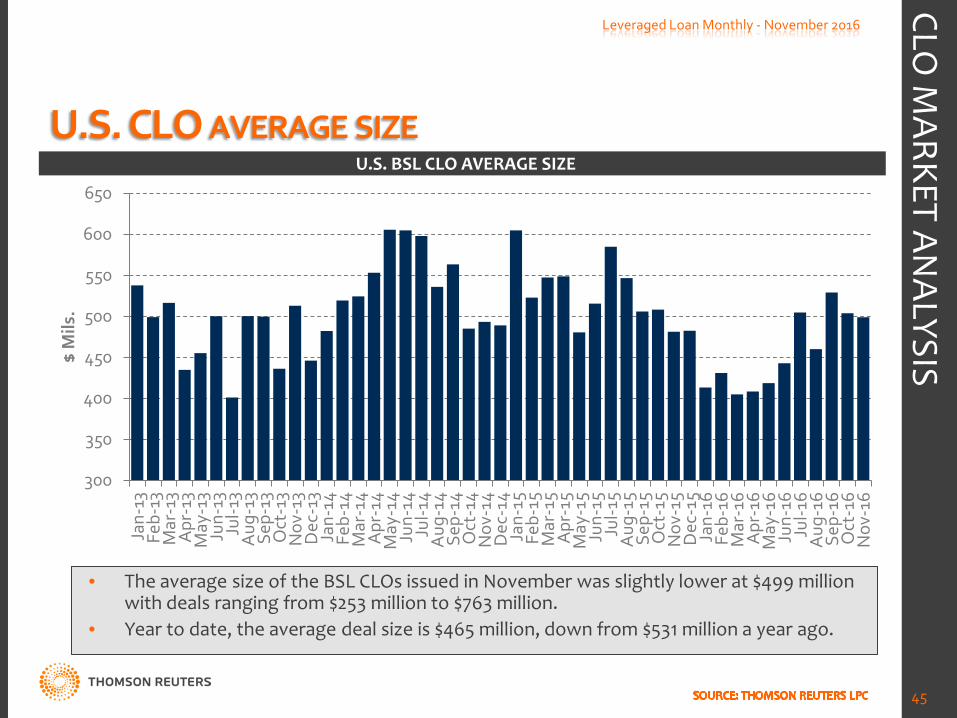

U.S. BSL CLO AVERAGE SIZE

• The average size of the BSL CLOs issued in November was slightly lower at $499 million with deals ranging from $253 million to $763 million.

• Year to date, the average deal size is $465 million, down from $531 million a year ago.

CLO M

ARKET ANALYSIS

EUROPEAN CLO ISSUANCE - MONTHLY

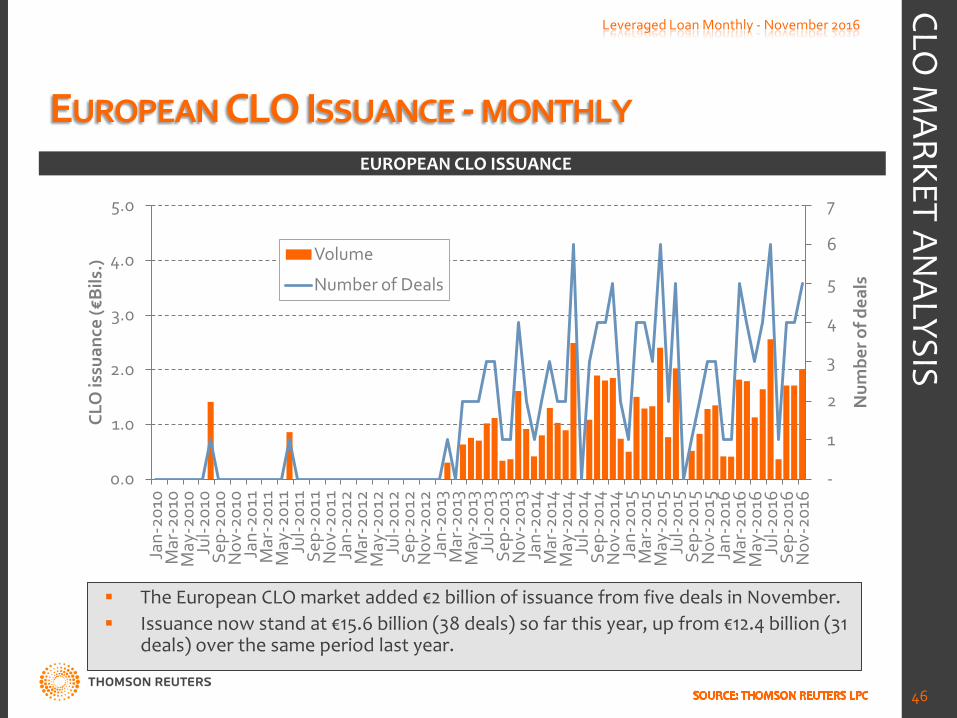

Leveraged Loan Monthly - November 2016

46

EUROPEAN CLO ISSUANCE

The European CLO market added €2 billion of issuance from five deals in November. Issuance now stand at €15.6 billion (38 deals) so far this year, up from €12.4 billion (31

deals) over the same period last year.

CLO M

ARKET ANALYSIS

-

1

2

3

4

5

6

7

0.0

1.0

2.0

3.0

4.0

5.0

Jan-

2010

M

ar-2

010

May

-201

0 Ju

l-201

0 Se

p-20

10

Nov

-201

0 Ja

n-20

11

Mar

-201

1 M

ay-2

011

Jul-2

011

Sep-

2011

N

ov-2

011

Jan-

2012

M

ar-2

012

May

-201

2 Ju

l-201

2 Se

p-20

12

Nov

-201

2 Ja

n-20

13

Mar

-201

3 M

ay-2

013

Jul-2

013

Sep-

2013

N

ov-2

013

Jan-

2014

M

ar-2

014

May

-201

4 Ju

l-201

4 Se

p-20

14

Nov

-201

4 Ja

n-20

15

Mar

-201

5 M

ay-2

015

Jul-2

015

Sep-

2015

N

ov-2

015

Jan-

2016

M

ar-2

016

May

-201

6 Ju

l-201

6 Se

p-20

16

Nov

-201

6

Num

ber o

f dea

ls

CLO

issu

ance

(€B

ils.)

Volume

Number of Deals

CLO ASSETS UNDER MANAGEMENT

0 50

100 150 200 250 300 350 400 450 500

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5

Sep-

15

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6

Sep-

16

Nov

-16

CLO

Agg

rega

te P

rinc

ipal

Bal

ance

($

USD

/Eur

o bi

ls.)

U.S.

Europe*

Leveraged Loan Monthly - November 2016

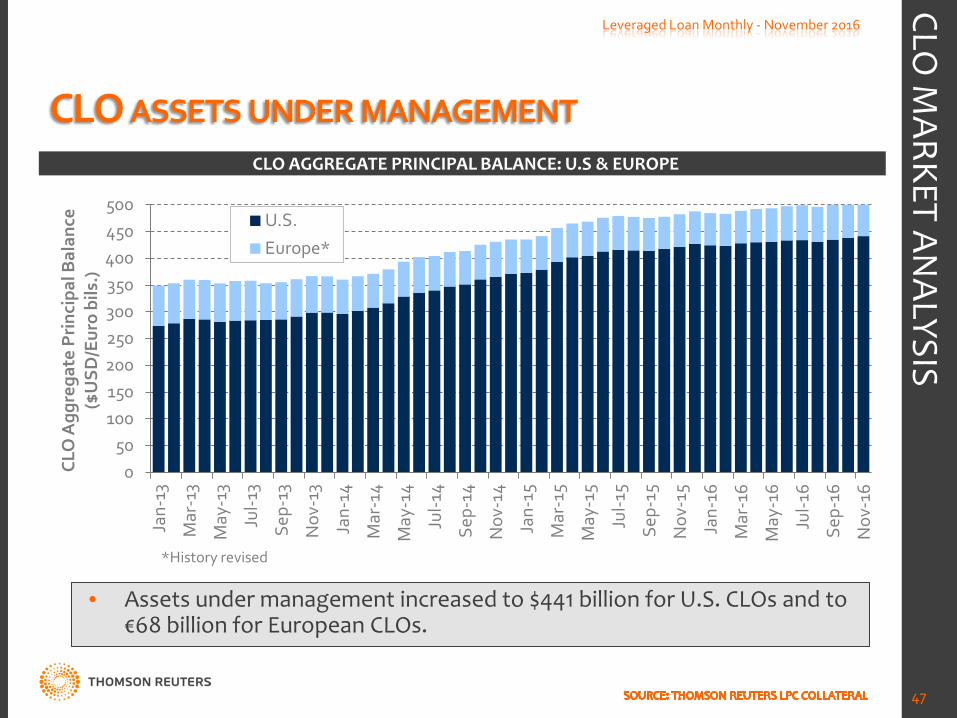

47

CLO AGGREGATE PRINCIPAL BALANCE: U.S & EUROPE

• Assets under management increased to $441 billion for U.S. CLOs and to €68 billion for European CLOs.

CLO M

ARKET ANALYSIS

*History revised

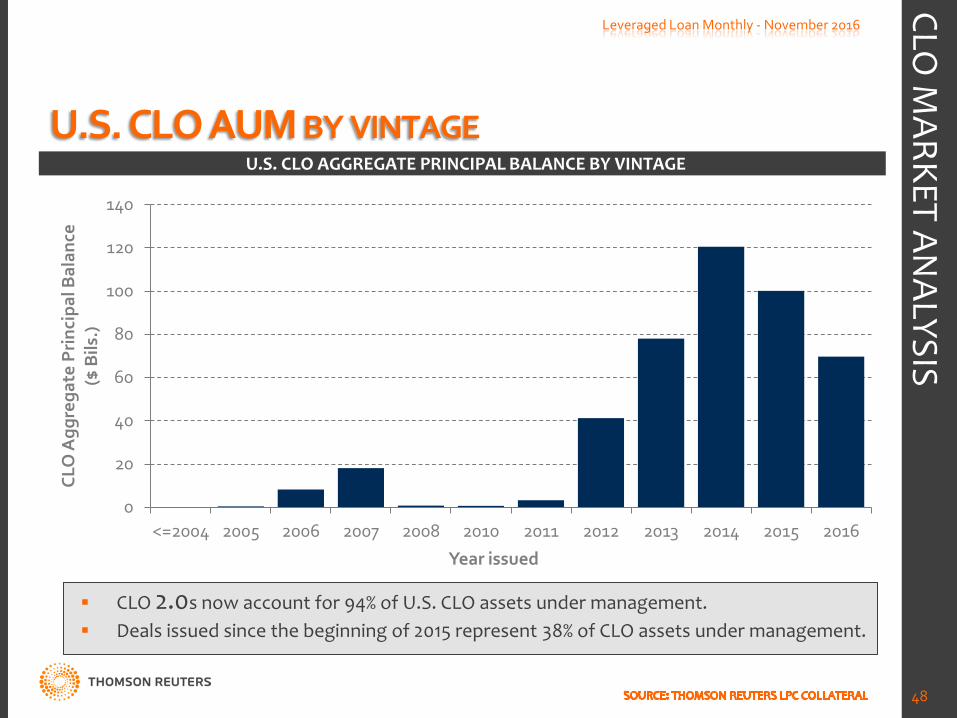

U.S. CLO AUM BY VINTAGE

0

20

40

60

80

100

120

140

<=2004 2005 2006 2007 2008 2010 2011 2012 2013 2014 2015 2016

CLO

Agg

rega

te P

rinc

ipal

Bal

ance

($

Bils

.)

48

U.S. CLO AGGREGATE PRINCIPAL BALANCE BY VINTAGE

CLO 2.0s now account for 94% of U.S. CLO assets under management. Deals issued since the beginning of 2015 represent 38% of CLO assets under management.

CLO M

ARKET ANALYSIS

Leveraged Loan Monthly - November 2016

Year issued

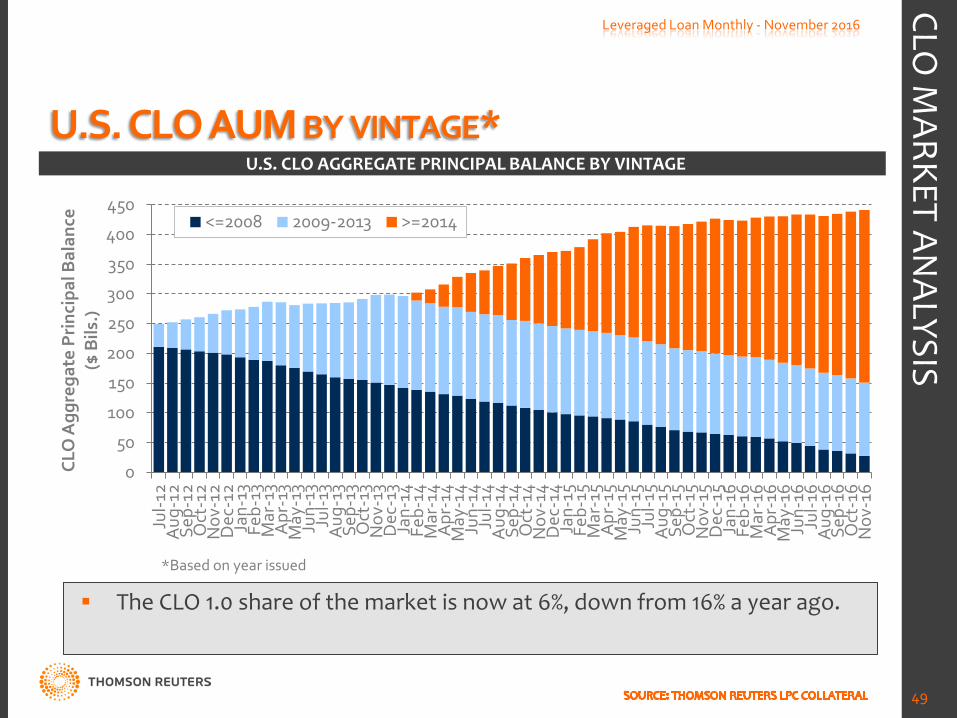

U.S. CLO AUM BY VINTAGE*

0

50

100

150

200

250

300

350

400

450

Jul-1

2 A

ug-1

2 Se

p-12

O

ct-1

2 N

ov-1

2 D

ec-1

2 Ja

n-13

Fe

b-13

M

ar-1

3 A

pr-1

3 M

ay-1

3 Ju

n-13

Ju

l-13

Aug

-13

Sep-

13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb-

14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-1

4 A

ug-1

4 Se

p-14

O

ct-1

4 N

ov-1

4 D

ec-1

4 Ja

n-15

Fe

b-15

M

ar-1

5 A

pr-1

5 M

ay-1

5 Ju

n-15

Ju

l-15

Aug

-15

Sep-

15

Oct

-15

Nov

-15

Dec

-15

Jan-

16

Feb-

16

Mar

-16

Apr

-16

May

-16

Jun-

16

Jul-1

6 A

ug-1

6 Se

p-16

O

ct-1

6 N

ov-1

6

CLO

Agg

rega

te P

rinc

ipal

Bal

ance

($

Bils

.)

<=2008 2009-2013 >=2014

49

U.S. CLO AGGREGATE PRINCIPAL BALANCE BY VINTAGE

The CLO 1.0 share of the market is now at 6%, down from 16% a year ago.

CLO M

ARKET ANALYSIS

*Based on year issued

Leveraged Loan Monthly - November 2016

EUROPEAN CLO AUM BY VINTAGE

0

2

4

6

8

10

12

14

16

18

<=2004 2005 2006 2007 2008 2013 2014 2015 YTD 2016

CLO

Agg

rega

te P

rinc

ipal

Bal

ance

(€

Bils

.)

50

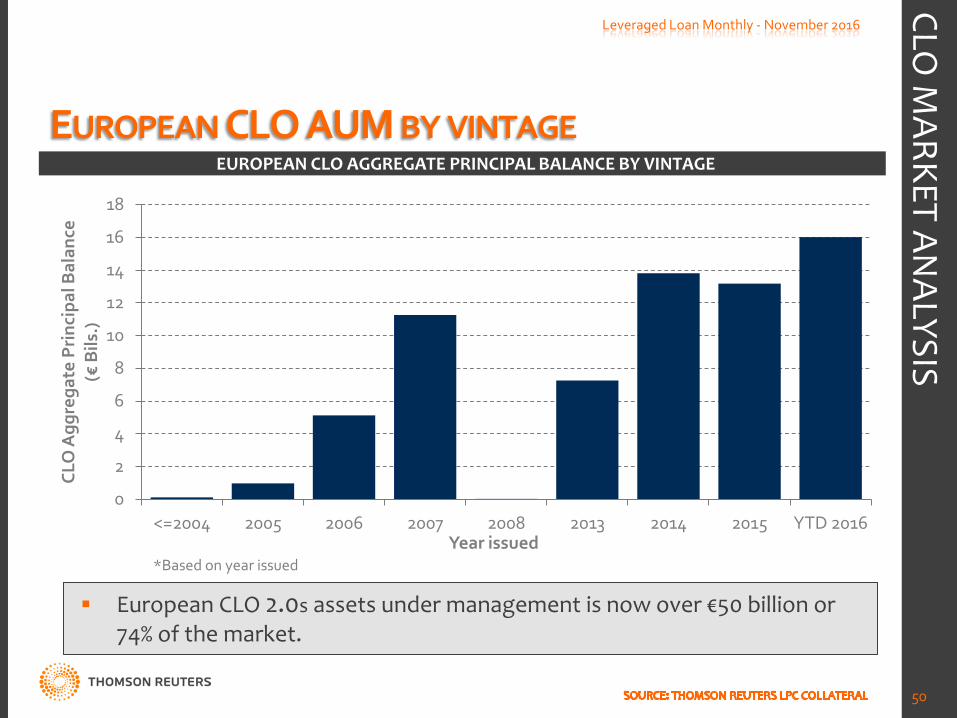

EUROPEAN CLO AGGREGATE PRINCIPAL BALANCE BY VINTAGE

European CLO 2.0s assets under management is now over €50 billion or 74% of the market.

CLO M

ARKET ANALYSIS

Leveraged Loan Monthly - November 2016

Year issued *Based on year issued

SHARE OF ASSETS HELD BY CLOS THAT ARE STILL IN / PAST THEIR STATED REINVESTMENT PERIOD

Leveraged Loan Monthly - November 2016

51

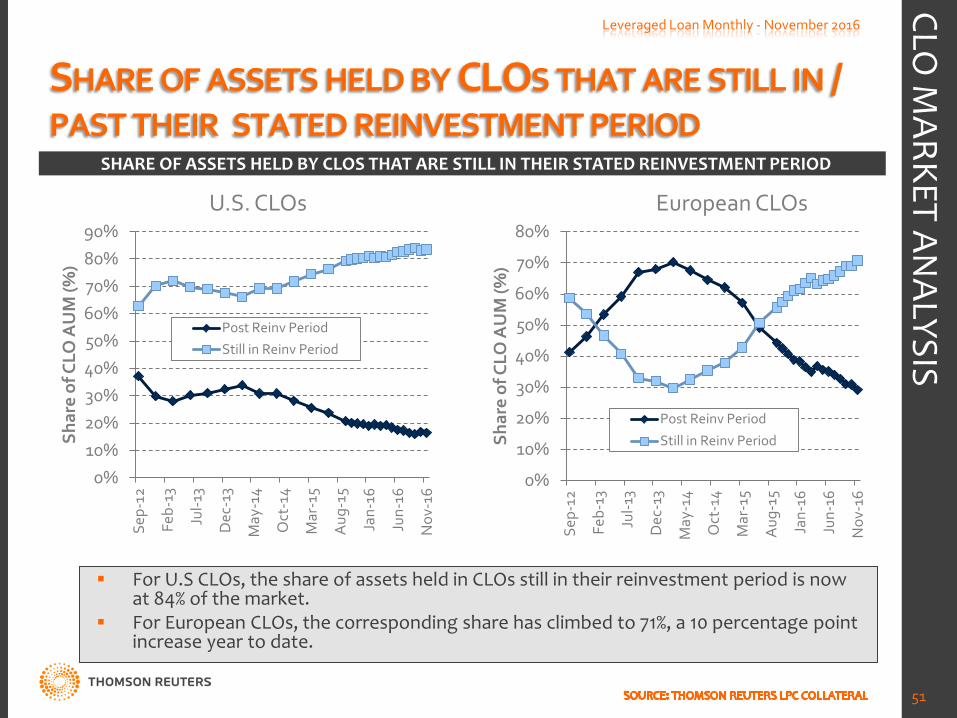

SHARE OF ASSETS HELD BY CLOS THAT ARE STILL IN THEIR STATED REINVESTMENT PERIOD

For U.S CLOs, the share of assets held in CLOs still in their reinvestment period is now at 84% of the market.

For European CLOs, the corresponding share has climbed to 71%, a 10 percentage point increase year to date.

CLO M

ARKET ANALYSIS

U.S. CLOs European CLOs

0%

10%

20%

30%

40%

50%

60%

70%

80%

Sep-

12

Feb-

13

Jul-1

3

Dec

-13

May

-14

Oct

-14

Mar

-15

Aug

-15

Jan-

16

Jun-

16

Nov

-16

Shar

e of

CLO

AU

M (%

)

Post Reinv Period

Still in Reinv Period

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Sep-

12

Feb-

13

Jul-1

3

Dec

-13

May

-14

Oct

-14

Mar

-15

Aug

-15

Jan-

16

Jun-

16

Nov

-16

Shar

e of

CLO

AU

M (%

)

Post Reinv Period Still in Reinv Period

TOP LOAN HOLDINGS IN U.S. CLO PORTFOLIOS Leveraged Loan Monthly - November 2016

52

CLO M

ARKET ANALYSIS

-

*Excludes CLOs not yet in LPC Collateral

Rank Issuer Approx. Amount

($Bils.)* 1 Valeant Pharmaceuticals 3.19 2 Asurion Corp 2.83 3 First Data Corp 2.79 4 Dell Inc 2.62 5 Community Health 2.57 6 Transdigm 2.55 7 Albertson 2.38 8 Numericable SAS 2.15 9 Charter Communications 2.06

10 Calpine Corp 2.03 11 Avago Technologies 1.96 12 Scientific Games 1.95 13 Univision Communications 1.92 14 American Airlines 1.86 15 Ineos Group Ltd 1.63 16 Formula One Group 1.50 17 Petsmart Inc 1.44 18 WME IMG Holdings LLC 1.39 19 Royalty Pharma 1.38 20 Level 3 Communications 1.36

Rank Issuer Approx. Amount

($Bils.)*

21 Advantage Sales & Marketing 1.32

22 BMC Software 1.29 23 Travelport Inc 1.27 24 Berry Plastics Corp 1.26

25 Pharmaceutical Product Development 1.25

26 Endo Pharmaceuticals 1.24 27 Federal-Mogul Corp 1.22 28 DTZ US Borrower LLC 1.18

29 Universal Services of America LP 1.17

30 MacDermid Inc 1.17 31 Dynegy Inc 1.16 32 Energy Transfer Equity LP 1.15 33 Tribune Co 1.15 34 Infor Global Solutions 1.15 35 Fortescue Metals Group 1.15 36 Protection One 1.14 37 ACOSTA 1.13 38 Western Digital Corp 1.13 39 Sabre Holdings Corp 1.11 40 Cablevision Systems Corp 1.09

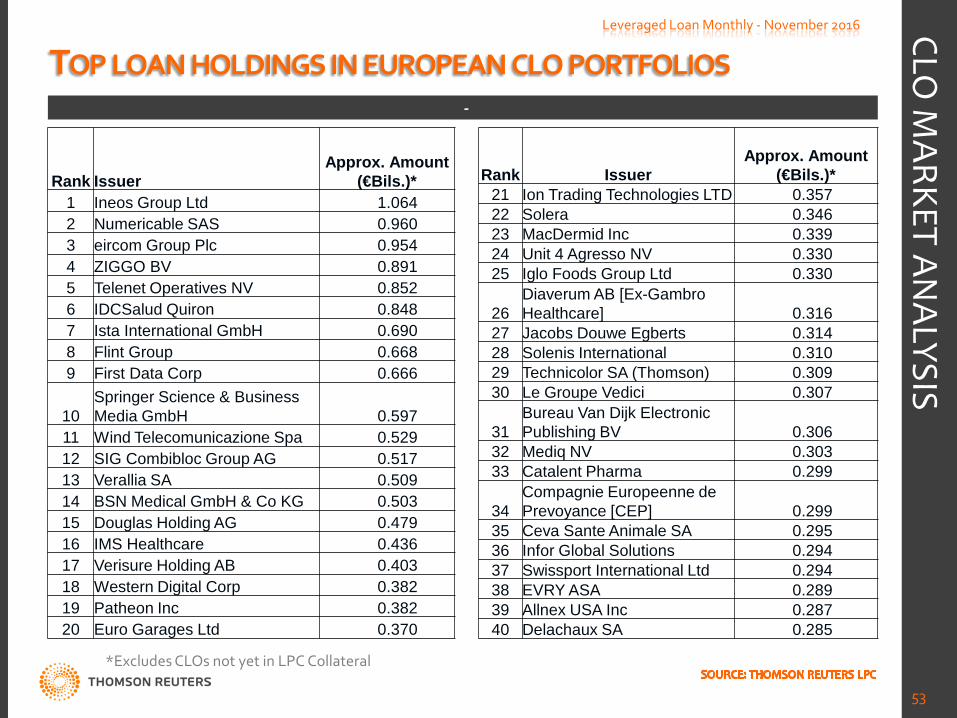

TOP LOAN HOLDINGS IN EUROPEAN CLO PORTFOLIOS Leveraged Loan Monthly - November 2016

53

CLO M

ARKET ANALYSIS

-

*Excludes CLOs not yet in LPC Collateral

Rank Issuer Approx. Amount

(€Bils.)* 1 Ineos Group Ltd 1.064 2 Numericable SAS 0.960 3 eircom Group Plc 0.954 4 ZIGGO BV 0.891 5 Telenet Operatives NV 0.852 6 IDCSalud Quiron 0.848 7 Ista International GmbH 0.690 8 Flint Group 0.668 9 First Data Corp 0.666

10 Springer Science & Business Media GmbH 0.597

11 Wind Telecomunicazione Spa 0.529 12 SIG Combibloc Group AG 0.517 13 Verallia SA 0.509 14 BSN Medical GmbH & Co KG 0.503 15 Douglas Holding AG 0.479 16 IMS Healthcare 0.436 17 Verisure Holding AB 0.403 18 Western Digital Corp 0.382 19 Patheon Inc 0.382 20 Euro Garages Ltd 0.370

Rank Issuer Approx. Amount

(€Bils.)* 21 Ion Trading Technologies LTD 0.357 22 Solera 0.346 23 MacDermid Inc 0.339 24 Unit 4 Agresso NV 0.330 25 Iglo Foods Group Ltd 0.330

26 Diaverum AB [Ex-Gambro Healthcare] 0.316

27 Jacobs Douwe Egberts 0.314 28 Solenis International 0.310 29 Technicolor SA (Thomson) 0.309 30 Le Groupe Vedici 0.307

31 Bureau Van Dijk Electronic Publishing BV 0.306

32 Mediq NV 0.303 33 Catalent Pharma 0.299

34 Compagnie Europeenne de Prevoyance [CEP] 0.299

35 Ceva Sante Animale SA 0.295 36 Infor Global Solutions 0.294 37 Swissport International Ltd 0.294 38 EVRY ASA 0.289 39 Allnex USA Inc 0.287 40 Delachaux SA 0.285

TOP INDUSTRIES – U.S. CLOS

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Tech

nolo

gy

Hea

lthca

re

Reta

il &

Sup

erm

arke

ts

Busi

ness

Ser

vice

s Fi

nanc

ial S

ervi

ces

Gen

eral

…

Chem

ical

s, P

last

ics

& …

Br

oadc

astin

g Se

rvic

es

Tele

com

mun

icat

ions

Le

isur

e &

…

Who

lesa

le

Med

ia

Oil

and

Gas

U

tiliti

es

Aut

omot

ive

Aer

ospa

ce &

Def

ense

Be

vera

ge, F

ood

& …

Tr

ansp

orta

tion

Cons

truc

tion

Hot

el &

Gam

ing

Pape

r & P

acka

ging

Sh

ippi

ng

REIT

S Re

stau

rant

s M

inin

g A

gric

ultu

re

Text

iles &

App

arel

Re

al E

stat

e G

over

nmen

t

Shar

e of

U.S

. CLO

loan

ass

ets

Leveraged Loan Monthly - November 2016

54

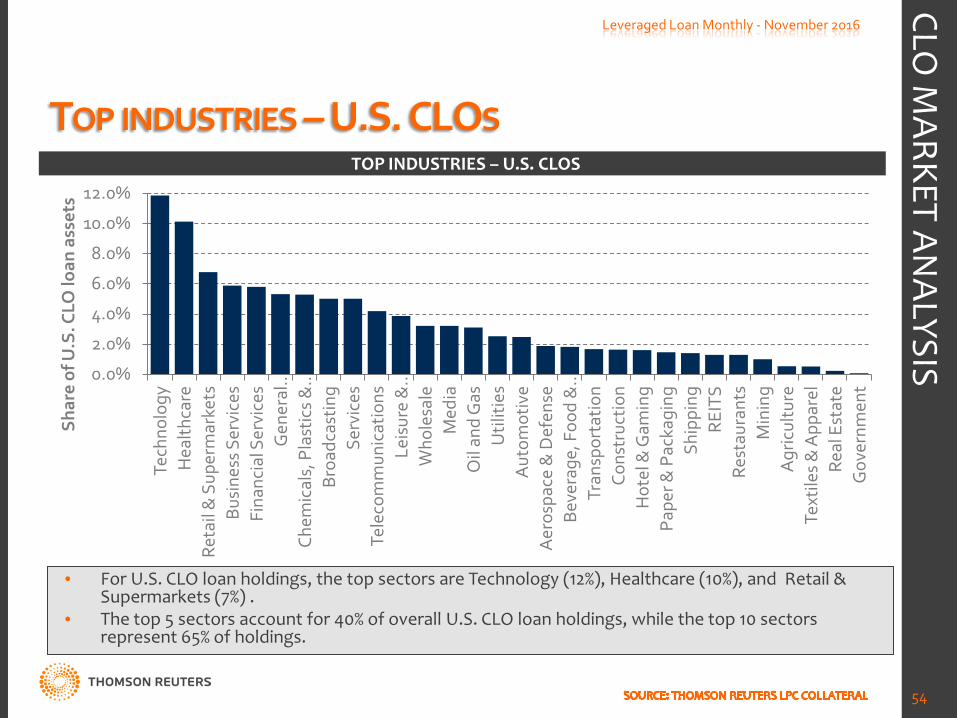

TOP INDUSTRIES – U.S. CLOS

• For U.S. CLO loan holdings, the top sectors are Technology (12%), Healthcare (10%), and Retail & Supermarkets (7%) .

• The top 5 sectors account for 40% of overall U.S. CLO loan holdings, while the top 10 sectors represent 65% of holdings.

CLO M

ARKET ANALYSIS

TOP INDUSTRIES – EUROPEAN CLOS

0.0% 2.0% 4.0% 6.0% 8.0%

10.0% 12.0% 14.0%

Hea

lthca

re

Gen

eral

…

Chem

ical

s, P

last

ics

& …

Te

chno

logy

Br

oadc

astin

g Fi

nanc

ial S

ervi

ces

Tele

com

mun

icat

ions

Bu

sine

ss S

ervi

ces

Serv

ices

Le

isur

e &

…

Reta

il &

Sup

erm

arke

ts

Beve

rage

, Foo

d, &

…

Who

lesa

le

Pape

r & P

acka

ging

M

edia

Tr

ansp

orta

tion

Real

Est

ate

Util

ities

A

utom

otiv

e Co

nstr

uctio

n Te

xtile

s & A

ppar

el

Hot

el &

Gam

ing

Ship

ping

G

over

nmen

t O

il an

d G

as

Agr

icul

ture

M

inin

g Re

stau

rant

s A

eros

pace

& D

efen

se

REIT

S

Shar

e of

Eur

opea

n CL

O lo

an a

sset

s

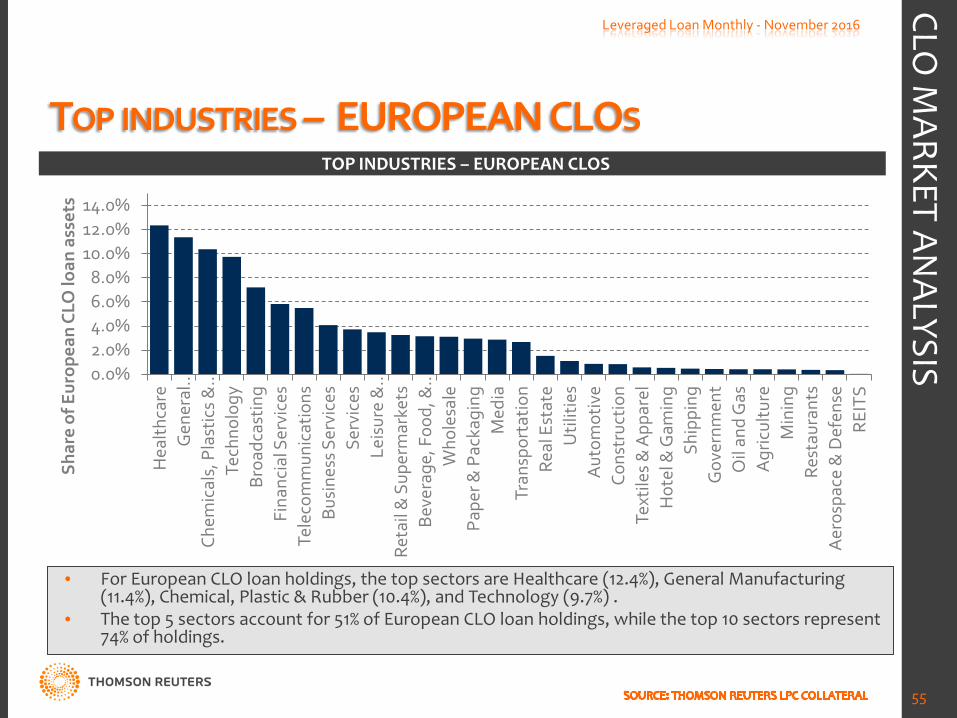

Leveraged Loan Monthly - November 2016

55

TOP INDUSTRIES – EUROPEAN CLOS

• For European CLO loan holdings, the top sectors are Healthcare (12.4%), General Manufacturing (11.4%), Chemical, Plastic & Rubber (10.4%), and Technology (9.7%) .

• The top 5 sectors account for 51% of European CLO loan holdings, while the top 10 sectors represent 74% of holdings.

CLO M

ARKET ANALYSIS

DISTRIBUTION OF SECONDARY MARKET PRICES OF LOAN ASSETS IN CLOS – U.S. CLOS

0%

10%

20%

30%

40%

50%

60%

<70 70 to <80 80 to <85 85 to <90 90 to <95 95 to <98 98 to <99 99 to <100 >=100

Shar

e of

loan

hol

ding

s

Avg. bid (% of par)

Dec-15 Jun-16 Sep-16 Oct-16 Nov-16

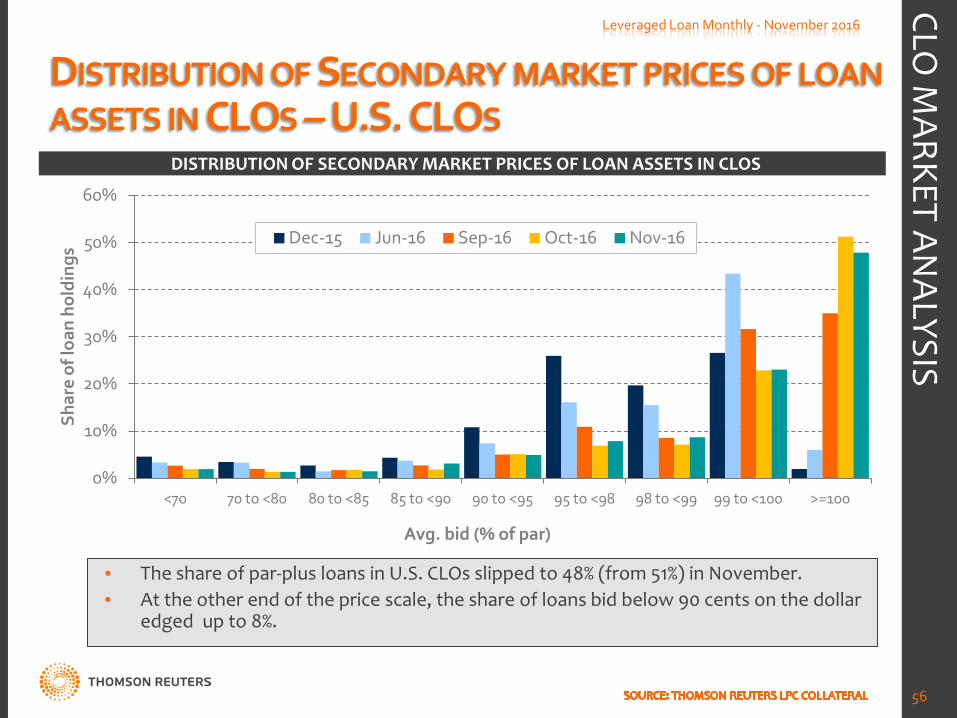

Leveraged Loan Monthly - November 2016

56

DISTRIBUTION OF SECONDARY MARKET PRICES OF LOAN ASSETS IN CLOS

• The share of par-plus loans in U.S. CLOs slipped to 48% (from 51%) in November. • At the other end of the price scale, the share of loans bid below 90 cents on the dollar

edged up to 8%.

CLO M

ARKET ANALYSIS

DISTRIBUTION OF SECONDARY MARKET PRICES OF LOAN ASSETS IN CLOS – EUROPEAN CLOS

0%

10%

20%

30%

40%

50%

60%

70%

80%

<70 70 to <80 80 to <85 85 to <90 90 to <95 95 to <98 98 to <99 99 to <100 >=100

Shar

e of

loan

hol

ding

s

Avg. bid (% of par)

Dec-15 Jun-16 Sep-16 Oct-16 Nov-16

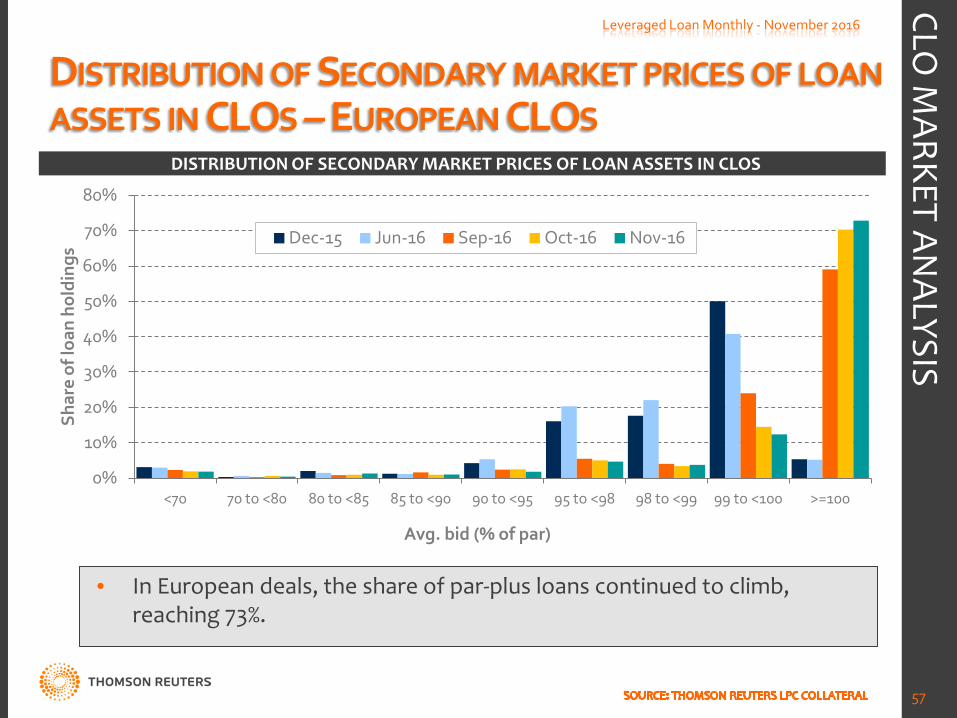

Leveraged Loan Monthly - November 2016

57

DISTRIBUTION OF SECONDARY MARKET PRICES OF LOAN ASSETS IN CLOS

• In European deals, the share of par-plus loans continued to climb, reaching 73%.

CLO M

ARKET ANALYSIS

AVERAGE BID OF U.S. CLO PORTFOLIOS (UNDERLYING ASSETS)

86.0

88.0

90.0

92.0

94.0

96.0

98.0

100.0

102.0

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5

Sep-

15

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6

Sep-

16

Bid

(% o

f par

)

US Avg. Bid

US Median Bid

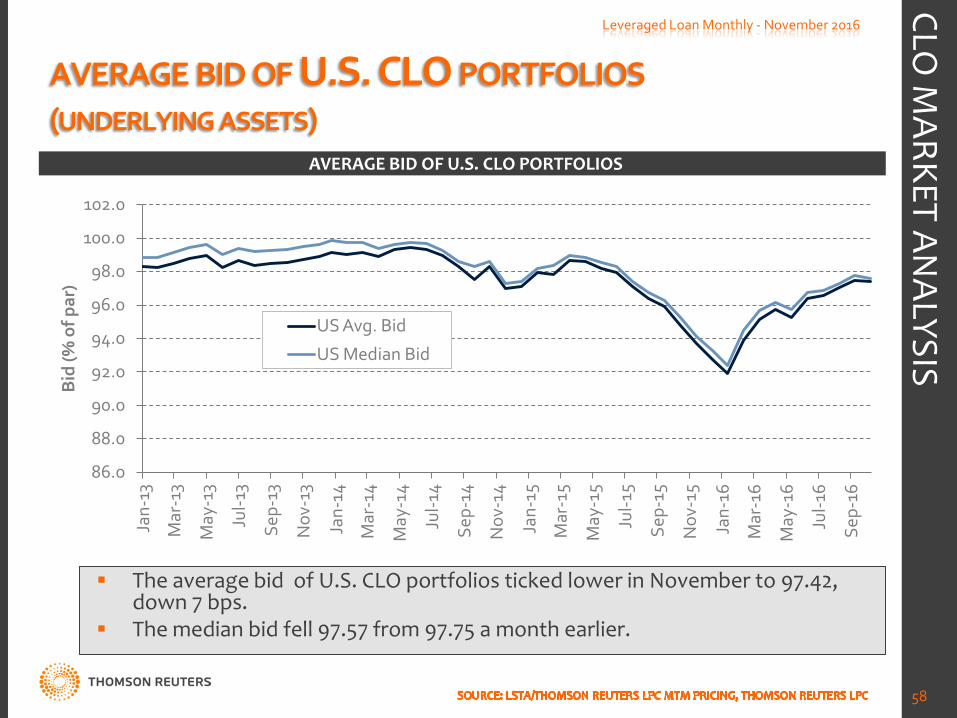

Leveraged Loan Monthly - November 2016

58

AVERAGE BID OF U.S. CLO PORTFOLIOS

The average bid of U.S. CLO portfolios ticked lower in November to 97.42, down 7 bps.

The median bid fell 97.57 from 97.75 a month earlier.

CLO M

ARKET ANALYSIS

AVERAGE BID OF EUROPEAN CLO PORTFOLIOS (UNDERLYING ASSETS)

86.0

88.0

90.0

92.0

94.0

96.0

98.0

100.0

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5

Sep-

15

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6

Sep-

16

Bid

(% o

f par

)

EUR Avg. Bid

EUR Median Bid

Leveraged Loan Monthly - November 2016

59

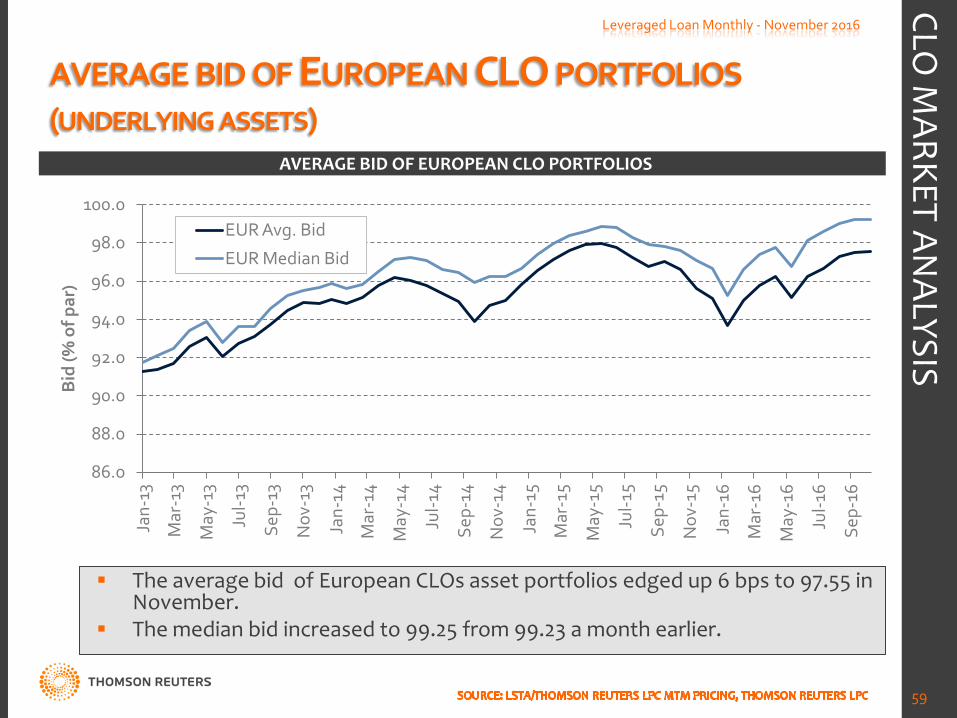

AVERAGE BID OF EUROPEAN CLO PORTFOLIOS

The average bid of European CLOs asset portfolios edged up 6 bps to 97.55 in November.

The median bid increased to 99.25 from 99.23 a month earlier.

CLO M

ARKET ANALYSIS

WEIGHTED AVERAGE BID OF CLO PORTFOLIOS: U.S. VS. EUROPE

0%

5%

10%

15%

20%

25%

30%

35%

40%

<80

80 to

<85

85 to

<86

86 to

<87

87 to

<88

88 to

<89

89 to

<90

90 to

<91

91 to

<92

92 to

<93

93 to

<94

94 to

<95

95 to

<96

96 to

<97

97 to

<98

98 to

<99

99 to

<10

0

>=10

0

Shar

e of

CLO

s

CLO weighted avg. bid

U.S.

Europe

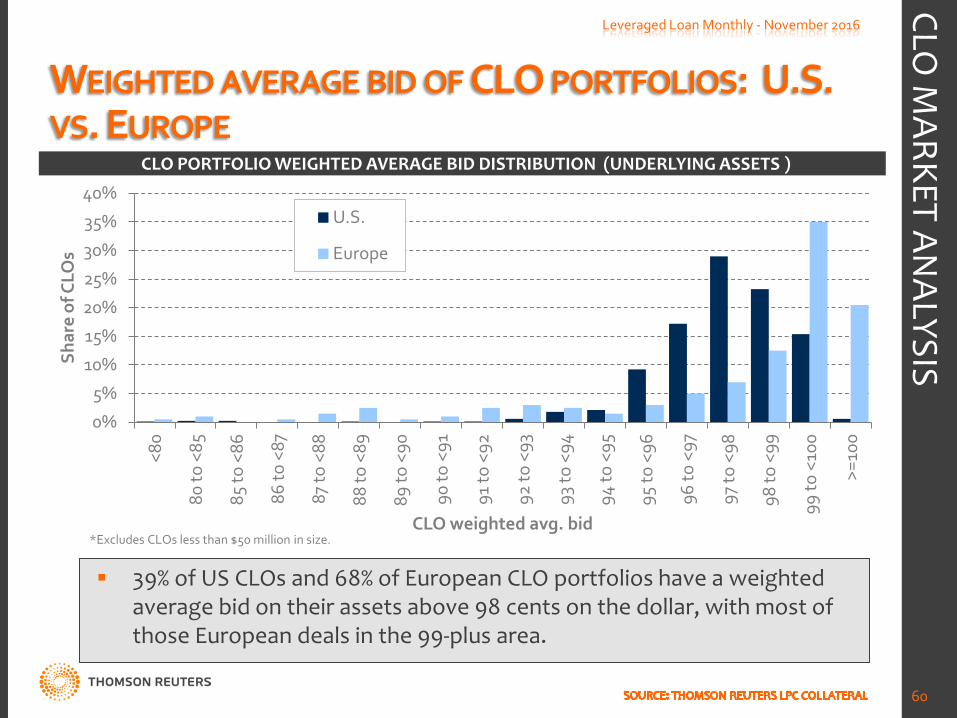

Leveraged Loan Monthly - November 2016

60

CLO PORTFOLIO WEIGHTED AVERAGE BID DISTRIBUTION (UNDERLYING ASSETS )

39% of US CLOs and 68% of European CLO portfolios have a weighted average bid on their assets above 98 cents on the dollar, with most of those European deals in the 99-plus area.

CLO M

ARKET ANALYSIS

*Excludes CLOs less than $50 million in size.

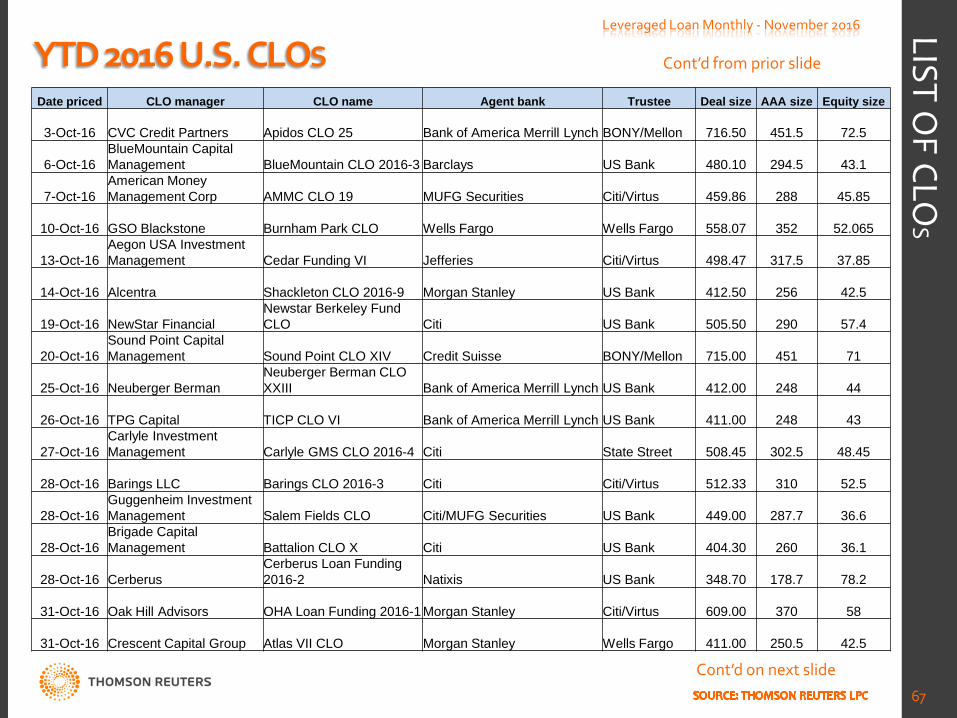

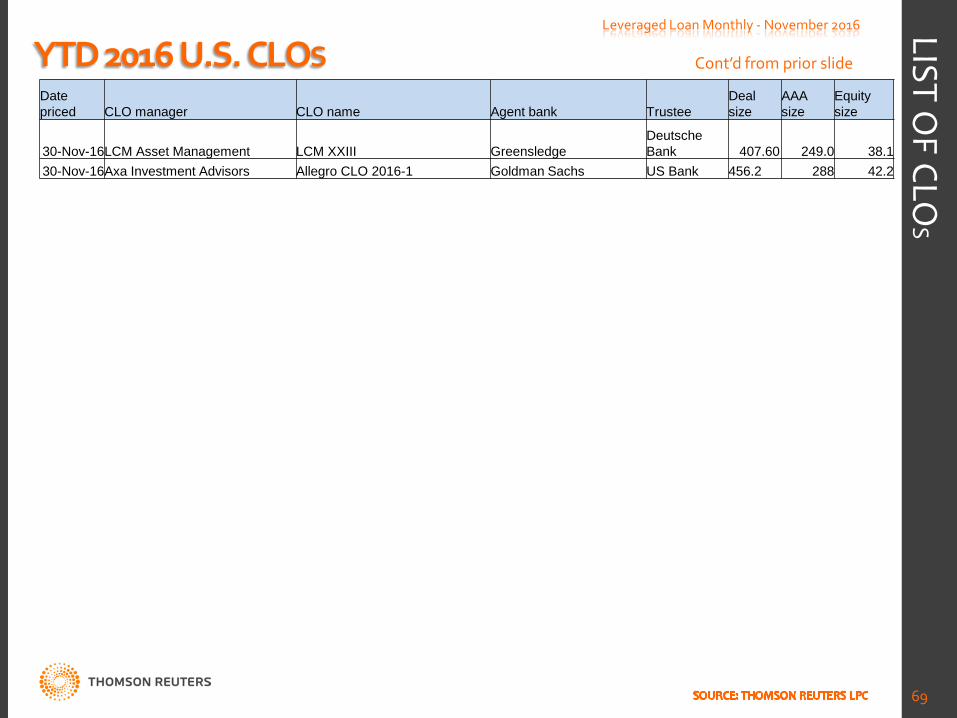

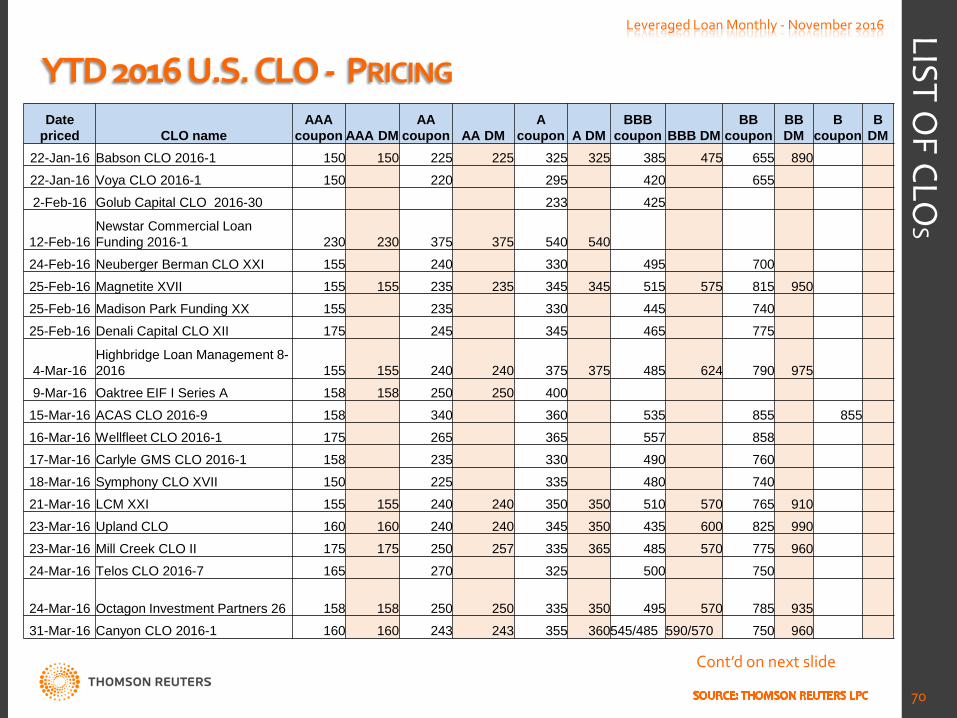

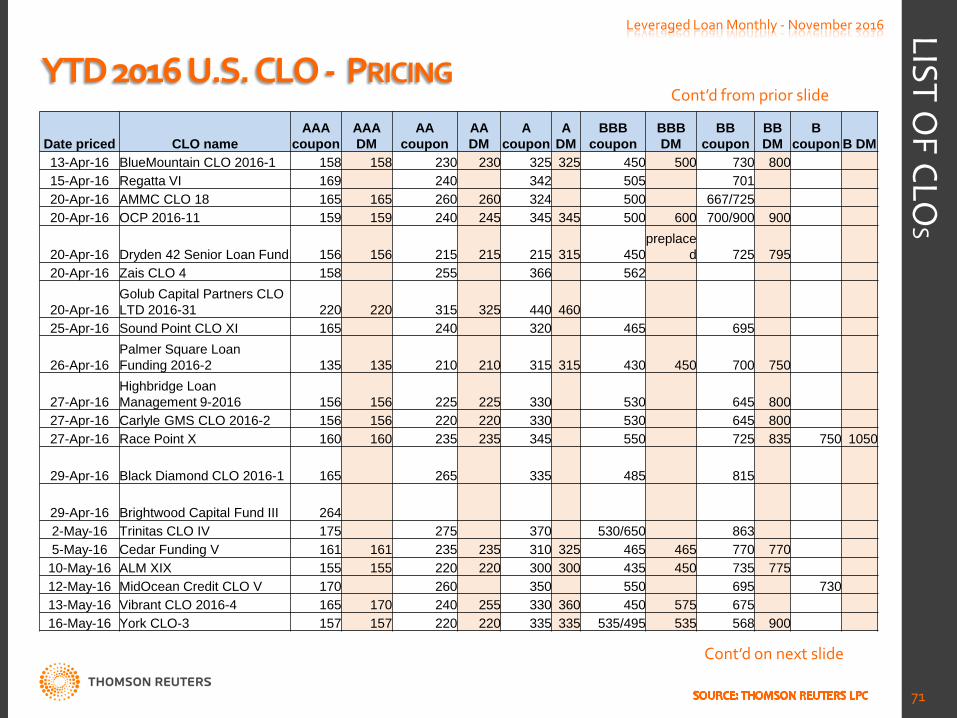

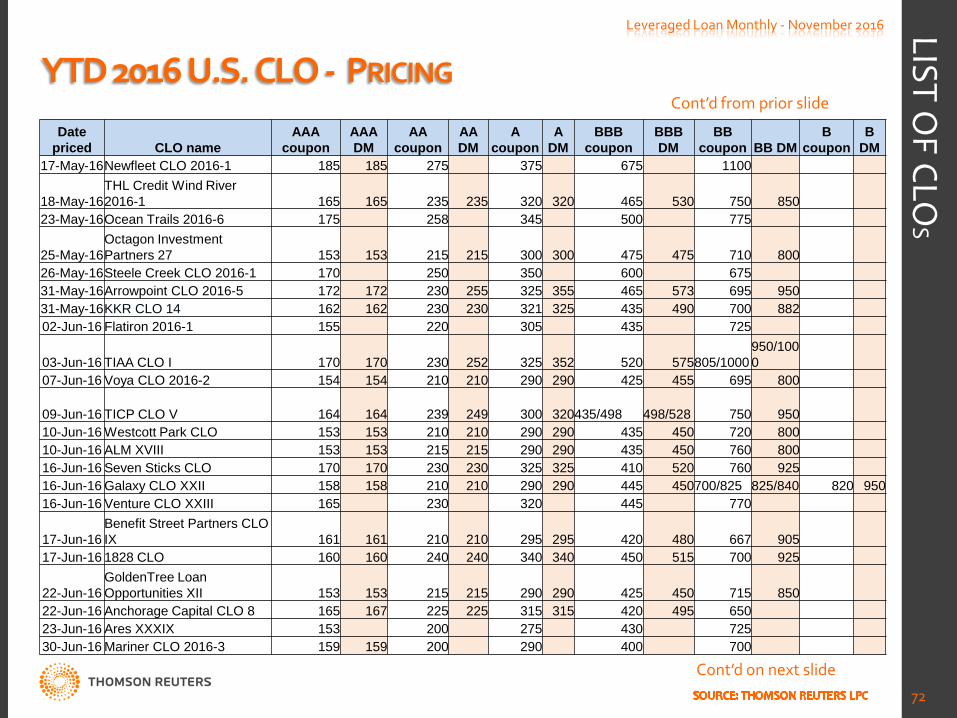

LIST OF RECENT CLOS / LEAGUE TABLES

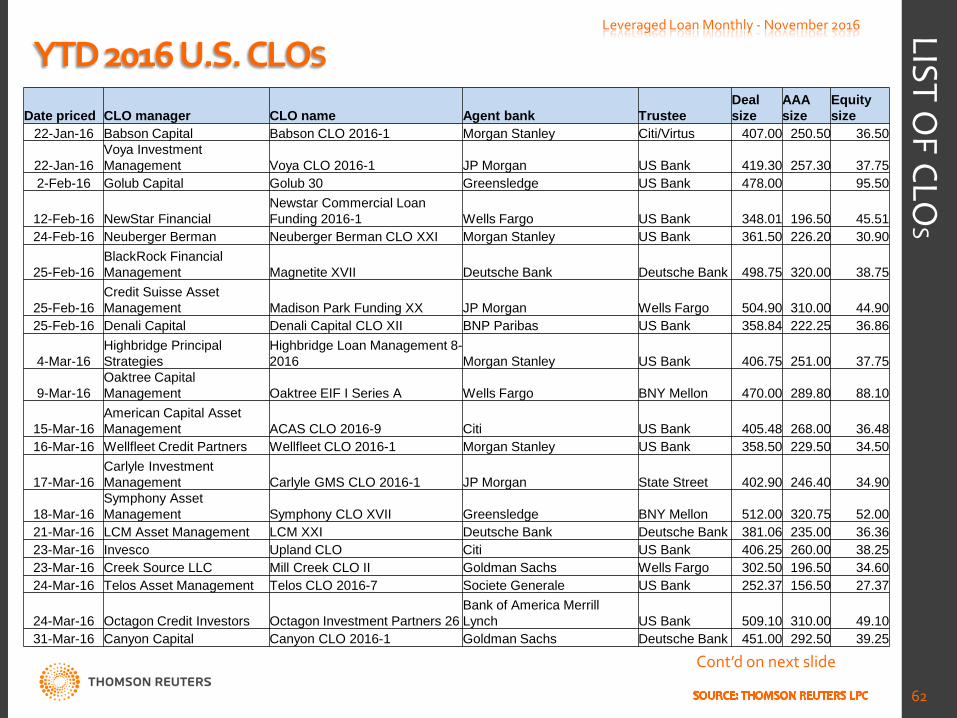

YTD 2016 U.S. CLOS Leveraged Loan Monthly - November 2016

62

LIST OF CLO

S

Cont’d on next slide

Date priced CLO manager CLO name Agent bank Trustee Deal size

AAA size

Equity size

22-Jan-16 Babson Capital Babson CLO 2016-1 Morgan Stanley Citi/Virtus 407.00 250.50 36.50

22-Jan-16 Voya Investment Management Voya CLO 2016-1 JP Morgan US Bank 419.30 257.30 37.75

2-Feb-16 Golub Capital Golub 30 Greensledge US Bank 478.00 95.50

12-Feb-16 NewStar Financial Newstar Commercial Loan Funding 2016-1 Wells Fargo US Bank 348.01 196.50 45.51

24-Feb-16 Neuberger Berman Neuberger Berman CLO XXI Morgan Stanley US Bank 361.50 226.20 30.90

25-Feb-16 BlackRock Financial Management Magnetite XVII Deutsche Bank Deutsche Bank 498.75 320.00 38.75

25-Feb-16 Credit Suisse Asset Management Madison Park Funding XX JP Morgan Wells Fargo 504.90 310.00 44.90

25-Feb-16 Denali Capital Denali Capital CLO XII BNP Paribas US Bank 358.84 222.25 36.86

4-Mar-16 Highbridge Principal Strategies

Highbridge Loan Management 8-2016 Morgan Stanley US Bank 406.75 251.00 37.75

9-Mar-16 Oaktree Capital Management Oaktree EIF I Series A Wells Fargo BNY Mellon 470.00 289.80 88.10

15-Mar-16 American Capital Asset Management ACAS CLO 2016-9 Citi US Bank 405.48 268.00 36.48

16-Mar-16 Wellfleet Credit Partners Wellfleet CLO 2016-1 Morgan Stanley US Bank 358.50 229.50 34.50

17-Mar-16 Carlyle Investment Management Carlyle GMS CLO 2016-1 JP Morgan State Street 402.90 246.40 34.90

18-Mar-16 Symphony Asset Management Symphony CLO XVII Greensledge BNY Mellon 512.00 320.75 52.00

21-Mar-16 LCM Asset Management LCM XXI Deutsche Bank Deutsche Bank 381.06 235.00 36.36 23-Mar-16 Invesco Upland CLO Citi US Bank 406.25 260.00 38.25 23-Mar-16 Creek Source LLC Mill Creek CLO II Goldman Sachs Wells Fargo 302.50 196.50 34.60 24-Mar-16 Telos Asset Management Telos CLO 2016-7 Societe Generale US Bank 252.37 156.50 27.37

24-Mar-16 Octagon Credit Investors Octagon Investment Partners 26 Bank of America Merrill Lynch US Bank 509.10 310.00 49.10

31-Mar-16 Canyon Capital Canyon CLO 2016-1 Goldman Sachs Deutsche Bank 451.00 292.50 39.25

YTD 2016 U.S. CLOS Leveraged Loan Monthly - November 2016

63

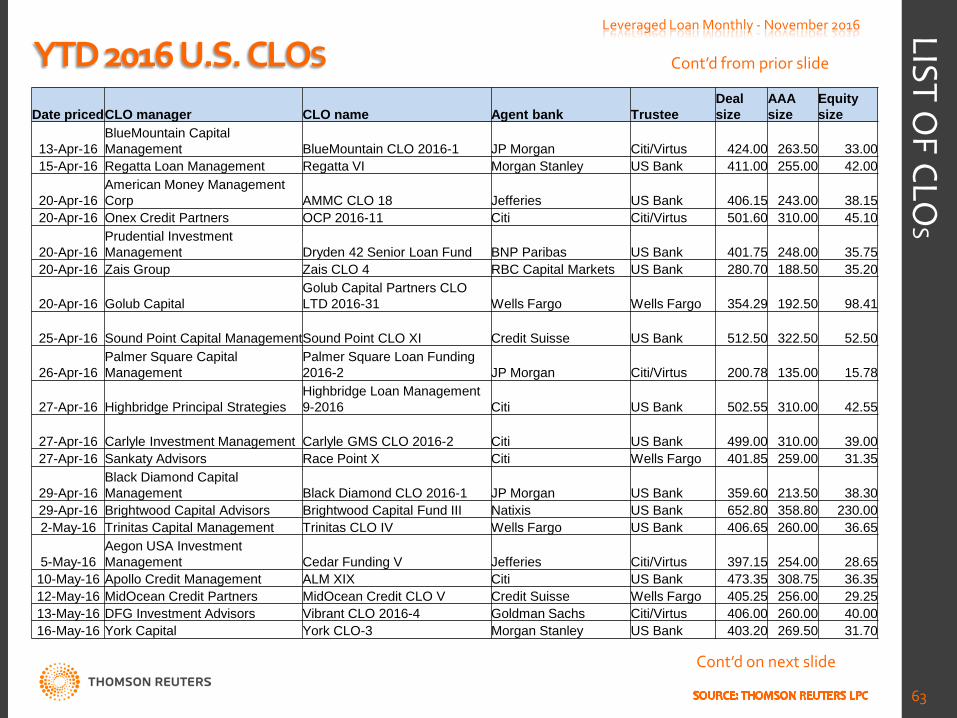

LIST OF CLO

S Cont’d from prior slide

Date priced CLO manager CLO name Agent bank Trustee Deal size

AAA size

Equity size

13-Apr-16 BlueMountain Capital Management BlueMountain CLO 2016-1 JP Morgan Citi/Virtus 424.00 263.50 33.00

15-Apr-16 Regatta Loan Management Regatta VI Morgan Stanley US Bank 411.00 255.00 42.00

20-Apr-16 American Money Management Corp AMMC CLO 18 Jefferies US Bank 406.15 243.00 38.15

20-Apr-16 Onex Credit Partners OCP 2016-11 Citi Citi/Virtus 501.60 310.00 45.10

20-Apr-16 Prudential Investment Management Dryden 42 Senior Loan Fund BNP Paribas US Bank 401.75 248.00 35.75

20-Apr-16 Zais Group Zais CLO 4 RBC Capital Markets US Bank 280.70 188.50 35.20

20-Apr-16 Golub Capital Golub Capital Partners CLO LTD 2016-31 Wells Fargo Wells Fargo 354.29 192.50 98.41

25-Apr-16 Sound Point Capital Management Sound Point CLO XI Credit Suisse US Bank 512.50 322.50 52.50

26-Apr-16 Palmer Square Capital Management

Palmer Square Loan Funding 2016-2 JP Morgan Citi/Virtus 200.78 135.00 15.78

27-Apr-16 Highbridge Principal Strategies Highbridge Loan Management 9-2016 Citi US Bank 502.55 310.00 42.55

27-Apr-16 Carlyle Investment Management Carlyle GMS CLO 2016-2 Citi US Bank 499.00 310.00 39.00 27-Apr-16 Sankaty Advisors Race Point X Citi Wells Fargo 401.85 259.00 31.35

29-Apr-16 Black Diamond Capital Management Black Diamond CLO 2016-1 JP Morgan US Bank 359.60 213.50 38.30

29-Apr-16 Brightwood Capital Advisors Brightwood Capital Fund III Natixis US Bank 652.80 358.80 230.00 2-May-16 Trinitas Capital Management Trinitas CLO IV Wells Fargo US Bank 406.65 260.00 36.65

5-May-16 Aegon USA Investment Management Cedar Funding V Jefferies Citi/Virtus 397.15 254.00 28.65

10-May-16 Apollo Credit Management ALM XIX Citi US Bank 473.35 308.75 36.35 12-May-16 MidOcean Credit Partners MidOcean Credit CLO V Credit Suisse Wells Fargo 405.25 256.00 29.25 13-May-16 DFG Investment Advisors Vibrant CLO 2016-4 Goldman Sachs Citi/Virtus 406.00 260.00 40.00 16-May-16 York Capital York CLO-3 Morgan Stanley US Bank 403.20 269.50 31.70

Cont’d on next slide

YTD 2016 U.S. CLOS Leveraged Loan Monthly - November 2016

64

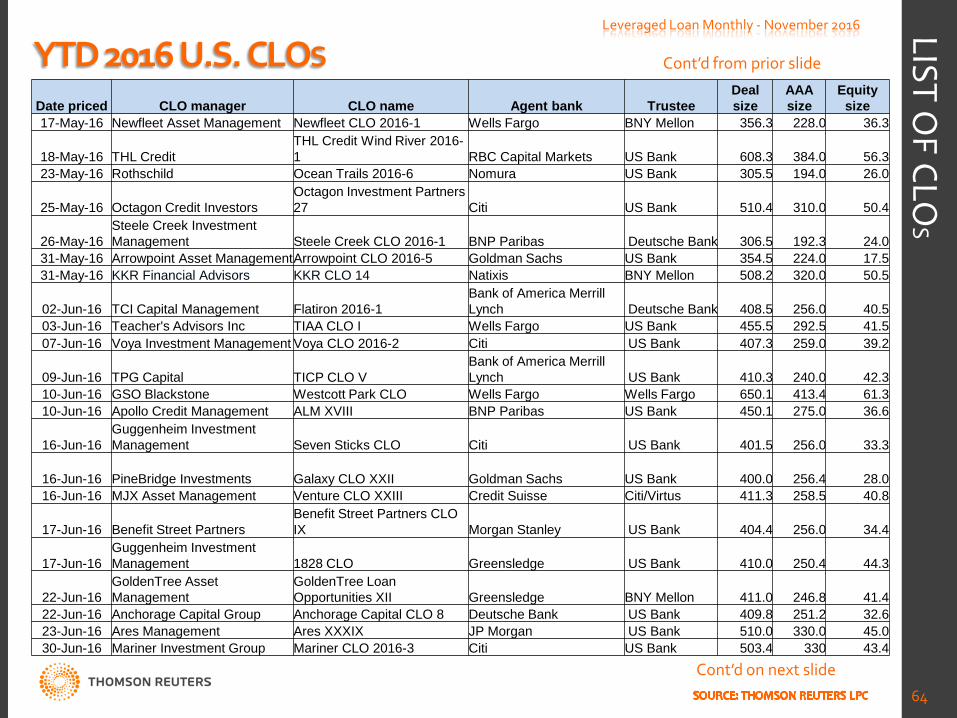

LIST OF CLO

S Cont’d from prior slide

Date priced CLO manager CLO name Agent bank Trustee Deal size

AAA size

Equity size

17-May-16 Newfleet Asset Management Newfleet CLO 2016-1 Wells Fargo BNY Mellon 356.3 228.0 36.3

18-May-16 THL Credit THL Credit Wind River 2016-1 RBC Capital Markets US Bank 608.3 384.0 56.3

23-May-16 Rothschild Ocean Trails 2016-6 Nomura US Bank 305.5 194.0 26.0

25-May-16 Octagon Credit Investors Octagon Investment Partners 27 Citi US Bank 510.4 310.0 50.4

26-May-16 Steele Creek Investment Management Steele Creek CLO 2016-1 BNP Paribas Deutsche Bank 306.5 192.3 24.0

31-May-16 Arrowpoint Asset Management Arrowpoint CLO 2016-5 Goldman Sachs US Bank 354.5 224.0 17.5 31-May-16 KKR Financial Advisors KKR CLO 14 Natixis BNY Mellon 508.2 320.0 50.5

02-Jun-16 TCI Capital Management Flatiron 2016-1 Bank of America Merrill Lynch Deutsche Bank 408.5 256.0 40.5

03-Jun-16 Teacher's Advisors Inc TIAA CLO I Wells Fargo US Bank 455.5 292.5 41.5 07-Jun-16 Voya Investment Management Voya CLO 2016-2 Citi US Bank 407.3 259.0 39.2

09-Jun-16 TPG Capital TICP CLO V Bank of America Merrill Lynch US Bank 410.3 240.0 42.3

10-Jun-16 GSO Blackstone Westcott Park CLO Wells Fargo Wells Fargo 650.1 413.4 61.3 10-Jun-16 Apollo Credit Management ALM XVIII BNP Paribas US Bank 450.1 275.0 36.6

16-Jun-16 Guggenheim Investment Management Seven Sticks CLO Citi US Bank 401.5 256.0 33.3

16-Jun-16 PineBridge Investments Galaxy CLO XXII Goldman Sachs US Bank 400.0 256.4 28.0 16-Jun-16 MJX Asset Management Venture CLO XXIII Credit Suisse Citi/Virtus 411.3 258.5 40.8

17-Jun-16 Benefit Street Partners Benefit Street Partners CLO IX Morgan Stanley US Bank 404.4 256.0 34.4

17-Jun-16 Guggenheim Investment Management 1828 CLO Greensledge US Bank 410.0 250.4 44.3

22-Jun-16 GoldenTree Asset Management

GoldenTree Loan Opportunities XII Greensledge BNY Mellon 411.0 246.8 41.4

22-Jun-16 Anchorage Capital Group Anchorage Capital CLO 8 Deutsche Bank US Bank 409.8 251.2 32.6 23-Jun-16 Ares Management Ares XXXIX JP Morgan US Bank 510.0 330.0 45.0 30-Jun-16 Mariner Investment Group Mariner CLO 2016-3 Citi US Bank 503.4 330 43.4

Cont’d on next slide

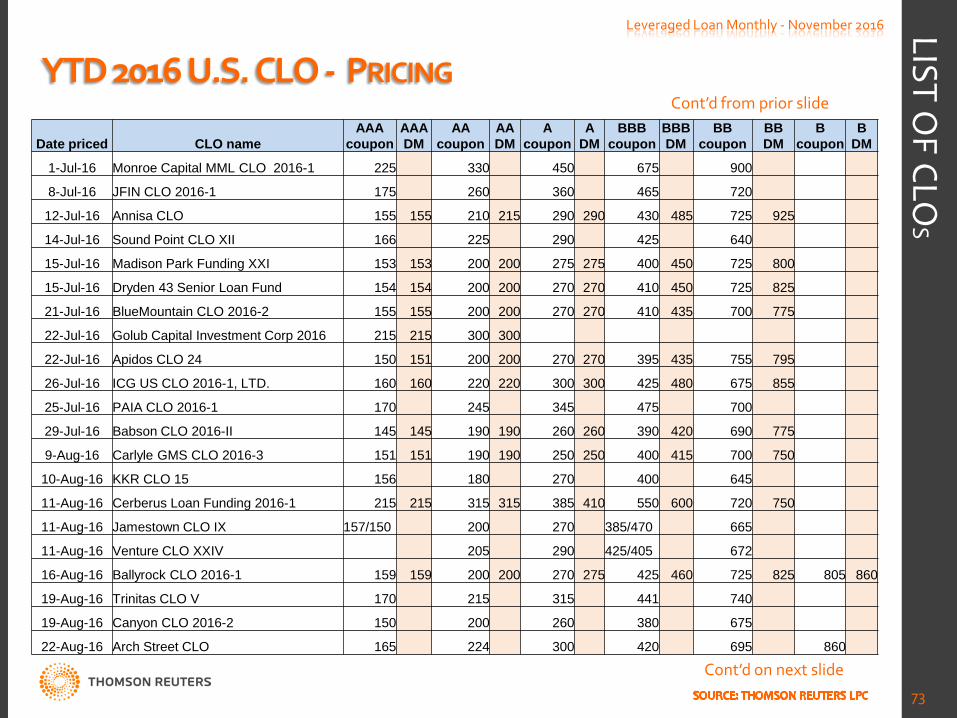

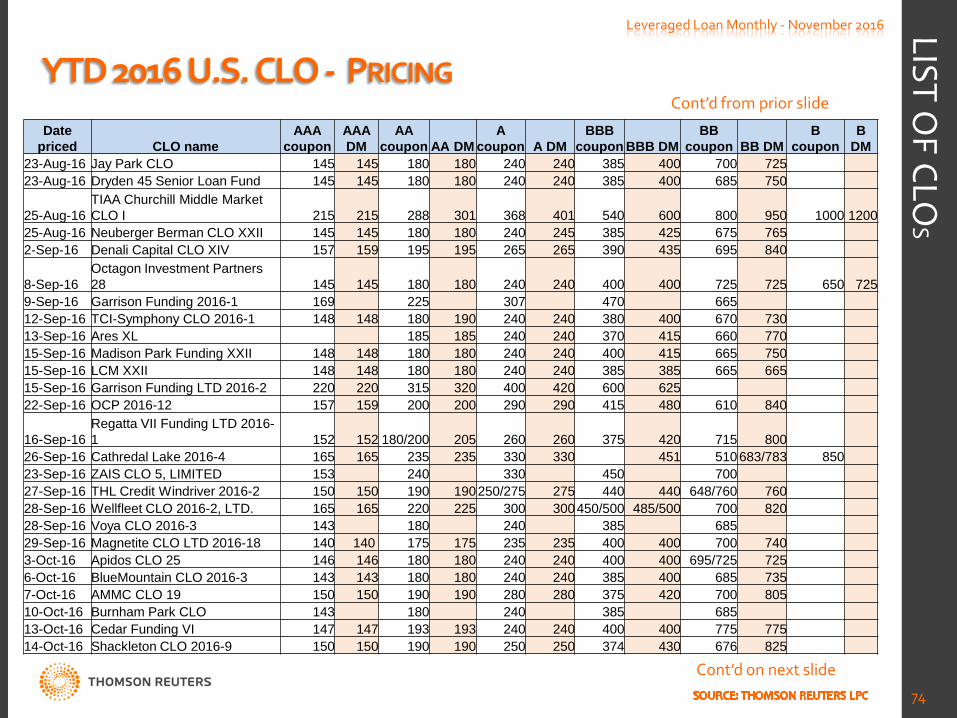

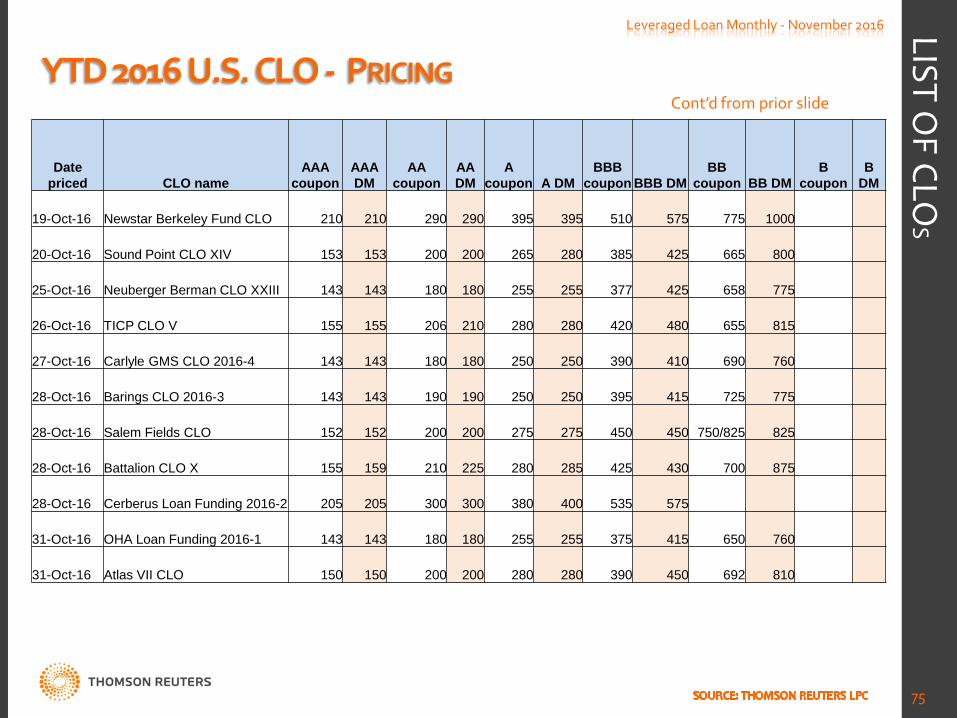

YTD 2016 U.S. CLOS Leveraged Loan Monthly - November 2016

65

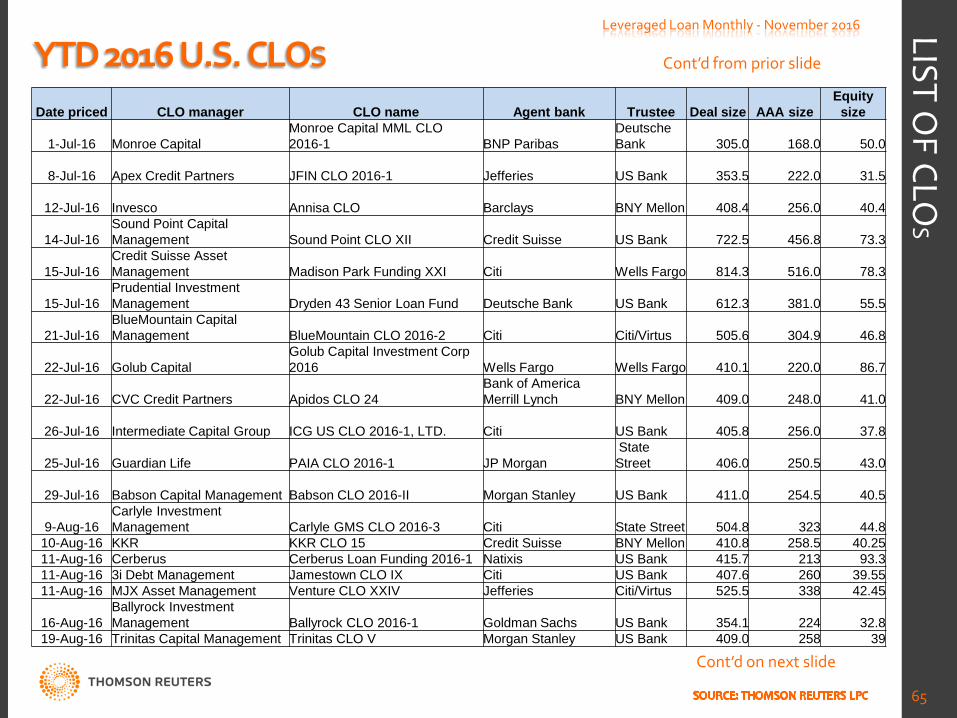

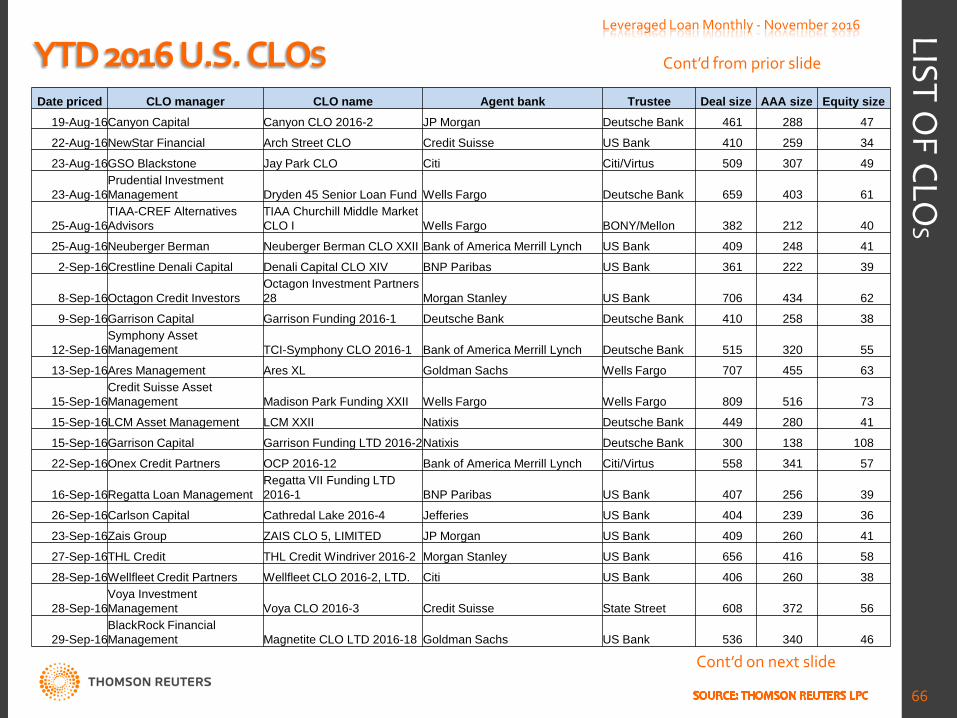

LIST OF CLO

S Cont’d from prior slide

Date priced CLO manager CLO name Agent bank Trustee Deal size AAA size Equity

size

1-Jul-16 Monroe Capital Monroe Capital MML CLO 2016-1 BNP Paribas

Deutsche Bank

305.0

168.0 50.0

8-Jul-16 Apex Credit Partners JFIN CLO 2016-1 Jefferies US Bank

353.5

222.0 31.5

12-Jul-16 Invesco Annisa CLO Barclays BNY Mellon

408.4

256.0 40.4

14-Jul-16 Sound Point Capital Management Sound Point CLO XII Credit Suisse US Bank

722.5

456.8 73.3

15-Jul-16 Credit Suisse Asset Management Madison Park Funding XXI Citi Wells Fargo

814.3

516.0 78.3

15-Jul-16 Prudential Investment Management Dryden 43 Senior Loan Fund Deutsche Bank US Bank

612.3

381.0 55.5

21-Jul-16 BlueMountain Capital Management BlueMountain CLO 2016-2 Citi Citi/Virtus

505.6

304.9 46.8

22-Jul-16 Golub Capital Golub Capital Investment Corp 2016 Wells Fargo Wells Fargo

410.1

220.0 86.7

22-Jul-16 CVC Credit Partners Apidos CLO 24 Bank of America Merrill Lynch BNY Mellon

409.0

248.0 41.0

26-Jul-16 Intermediate Capital Group ICG US CLO 2016-1, LTD. Citi US Bank

405.8

256.0 37.8