Leveraged and Mezzanine Finance

56

Dr. Ian Giddy New York University Leveraged and Mezzanine Finance

Transcript of Leveraged and Mezzanine Finance

Dr.

Ian

Gid

dy

New

Yor

k U

nive

rsity

Lev

erag

ed a

nd

Mez

zan

ine

Fin

ance

3Copyright ©2005 Ian H Giddy

Mez

zani

ne D

ebt

Mez

zani

ne D

ebt

NE

WC

O

Dis

kd

rive

bu

sin

ess

Eq

uit

y $0

.25b

Sen

ior

deb

t $1

bW

hat

sec

uri

ties

?W

hat

ret

urn

s?W

hat

inve

sto

rs?

Mez

zan

ine

4Copyright ©2005 Ian H Giddy

The

Fin

anci

ng S

pect

rum

The

Fin

anci

ng S

pect

rum

Expected Return

Ris

k

Sen

ior

secu

red

deb

tS

enio

r se

cure

d d

ebt

Eq

uit

yE

qu

ity

Sen

ior

un

secu

red

deb

tS

enio

r u

nse

cure

d d

ebt

Su

bo

rdin

ated

deb

tS

ub

ord

inat

ed d

ebt

Pre

ferr

ed e

qu

ity

Pre

ferr

ed e

qu

ity

Co

nve

rtib

le d

ebt

Co

nve

rtib

le d

ebt

5Copyright ©2005 Ian H Giddy

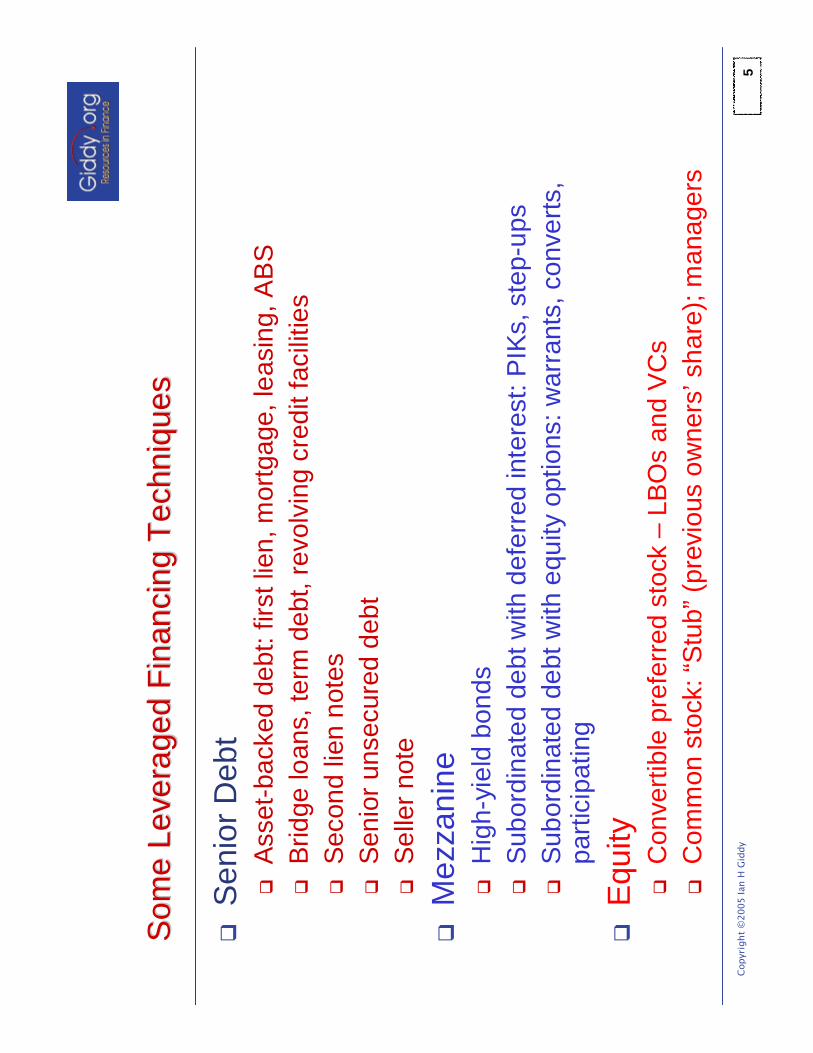

Som

e Le

vera

ged

Fin

anci

ng T

echn

ique

sS

ome

Leve

rage

d F

inan

cing

Tec

hniq

ues

�S

enio

r D

ebt

�A

sset

-bac

ked

debt

: firs

t lie

n, m

ortg

age,

leas

ing,

AB

S�

Brid

ge lo

ans,

term

deb

t, re

volv

ing

cred

it fa

cilit

ies

�S

econ

d lie

n no

tes

�S

enio

r un

secu

red

debt

�S

elle

r no

te

�M

ezza

nine

�H

igh-

yiel

d bo

nds

�S

ubor

dina

ted

debt

with

def

erre

d in

tere

st: P

IKs,

ste

p-up

s�

Sub

ordi

nate

d de

bt w

ith e

quity

opt

ions

: war

rant

s, c

onve

rts,

pa

rtic

ipat

ing

�E

quity

�C

onve

rtib

le p

refe

rred

sto

ck –

LBO

san

d V

Cs

�C

omm

on s

tock

: “S

tub”

(pr

evio

us o

wne

rs’ s

hare

); m

anag

ers

6Copyright ©2005 Ian H Giddy

Typ

ical

LB

O T

rans

actio

n S

truc

ture

Typ

ical

LB

O T

rans

actio

n S

truc

ture

Man

agem

ent

LBO

fund

s

Sub

deb

t hol

ders

4-7

year

s ex

it st

rate

gy25

-40%

20-3

0%E

quity

Pub

lic m

arke

t

Insu

ranc

e co

mpa

nies

Hed

ge fu

nds

LBO

/Mez

zani

ne

fund

s

7-10

yea

rs p

ayba

ck

1x-2

x E

BIT

DA

10-2

0%20

-30%

Mez

zani

ne

finan

cing

Com

mer

cial

ba

nks

Insu

ranc

e co

mpa

nies

5-7

year

s pa

ybac

k2x

-3x

EB

ITD

A2x

inte

rest

cov

erag

e

7-10

%50

-60%

Sen

ior

debt

Lik

ely

sou

rces

Len

din

g c

rite

ria

Co

st o

f ca

pit

alP

erce

nt

of

tran

sact

ion

Fin

anci

ng

7Copyright ©2005 Ian H Giddy

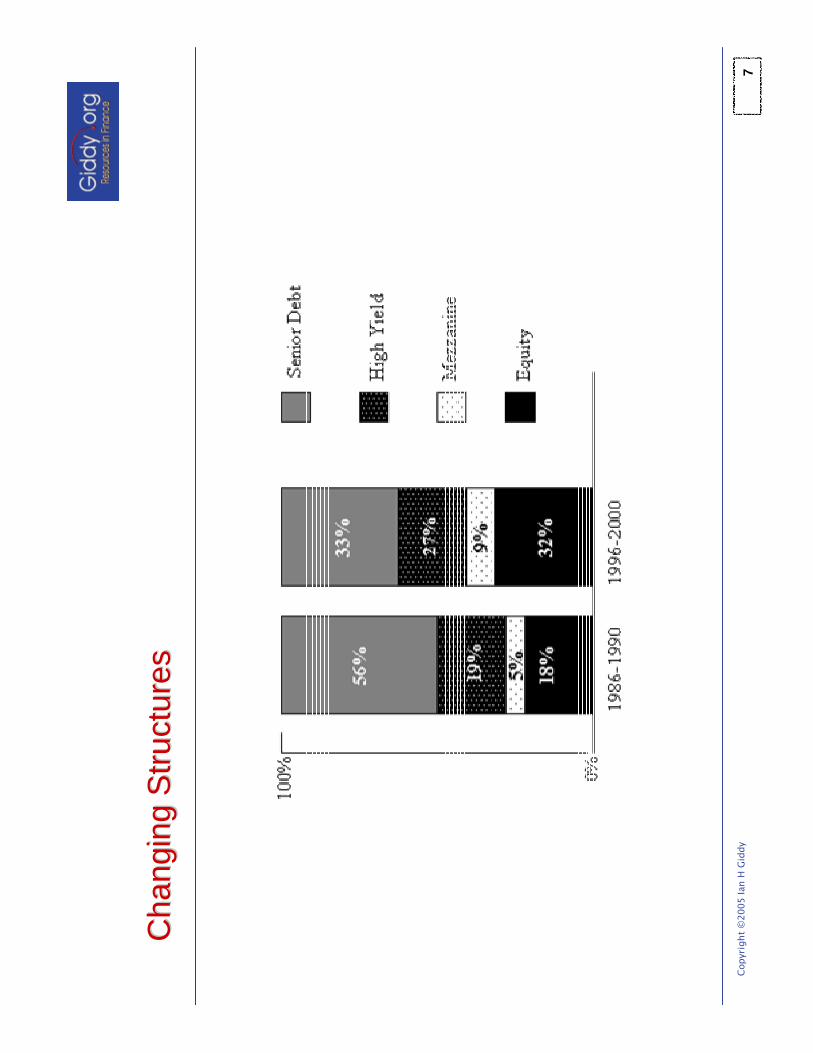

Cha

ngin

g S

truc

ture

sC

hang

ing

Str

uctu

res

8Copyright ©2005 Ian H Giddy

Leve

rage

d F

inan

ce M

ultip

les

Leve

rage

d F

inan

ce M

ultip

les

9Copyright ©2005 Ian H Giddy

Leve

rage

d Le

ndin

g fo

r A

cqui

sitio

nsLe

vera

ged

Lend

ing

for

Acq

uisi

tions

Off

er

sta

ge

De

al st

ag

e

Po

st-a

cq

uis

itio

n s

tag

e

Co

mm

itm

en

t to

Fi

na

nc

e

Brid

ge

Fin

an

cin

g

Re

fin

an

cin

g &

Sa

le o

f A

sse

ts

10Copyright ©2005 Ian H Giddy

Tra

ding

and

Tra

nsfe

rrin

g Lo

ans

Tra

ding

and

Tra

nsfe

rrin

g Lo

ans

AS

SIG

NM

EN

TA

SS

IGN

ME

NT

FU

LL

AS

SIG

NM

EN

TT

he s

ale

of a

llof

the

orig

inat

ing

lend

er’s

or

assi

gnor

’srig

hts

and

inte

rest

in a

cre

dit f

acili

tyto

a p

urch

aser

or

assi

gnee

.

FU

LL

AS

SIG

NM

EN

TT

he s

ale

of a

llof

the

orig

inat

ing

lend

er’s

or

assi

gnor

’srig

hts

and

inte

rest

in a

cre

dit f

acili

tyto

a p

urch

aser

or

assi

gnee

.

AS

SIG

NM

EN

TW

ITH

NO

VA

TIO

N

AS

SIG

NM

EN

TW

ITH

NO

VA

TIO

N

PA

RT

ICIP

AT

ION

PA

RT

ICIP

AT

ION

PA

RT

ICIP

AT

ION

Par

ticip

ants

hav

e de

rivat

ive

right

s,no

tdire

ct r

ight

s ag

ains

t

(or

oblig

atio

ns to

) th

ebo

rrow

er.

PA

RT

ICIP

AT

ION

Par

ticip

ants

hav

e de

rivat

ive

right

s,no

tdire

ct r

ight

s ag

ains

t

(or

oblig

atio

ns to

) th

ebo

rrow

er.

nL

IMIT

ED

VO

TIN

G P

AR

TIC

IPA

TIO

Nn

FU

LL

VO

TIN

G P

AR

TIC

IPA

TIO

Nn

FU

LL

PA

SS

-TH

RO

UG

H P

AR

TIC

IPA

TIO

N

nL

IMIT

ED

VO

TIN

G P

AR

TIC

IPA

TIO

Nn

FU

LL

VO

TIN

G P

AR

TIC

IPA

TIO

Nn

FU

LL

PA

SS

-TH

RO

UG

H P

AR

TIC

IPA

TIO

N

11Copyright ©2005 Ian H Giddy

Syn

dica

ted

Loan

s:S

yndi

cate

d Lo

ans:

Evo

lutio

n of

the

Mar

ket

Evo

lutio

n of

the

Mar

ket

12Copyright ©2005 Ian H Giddy

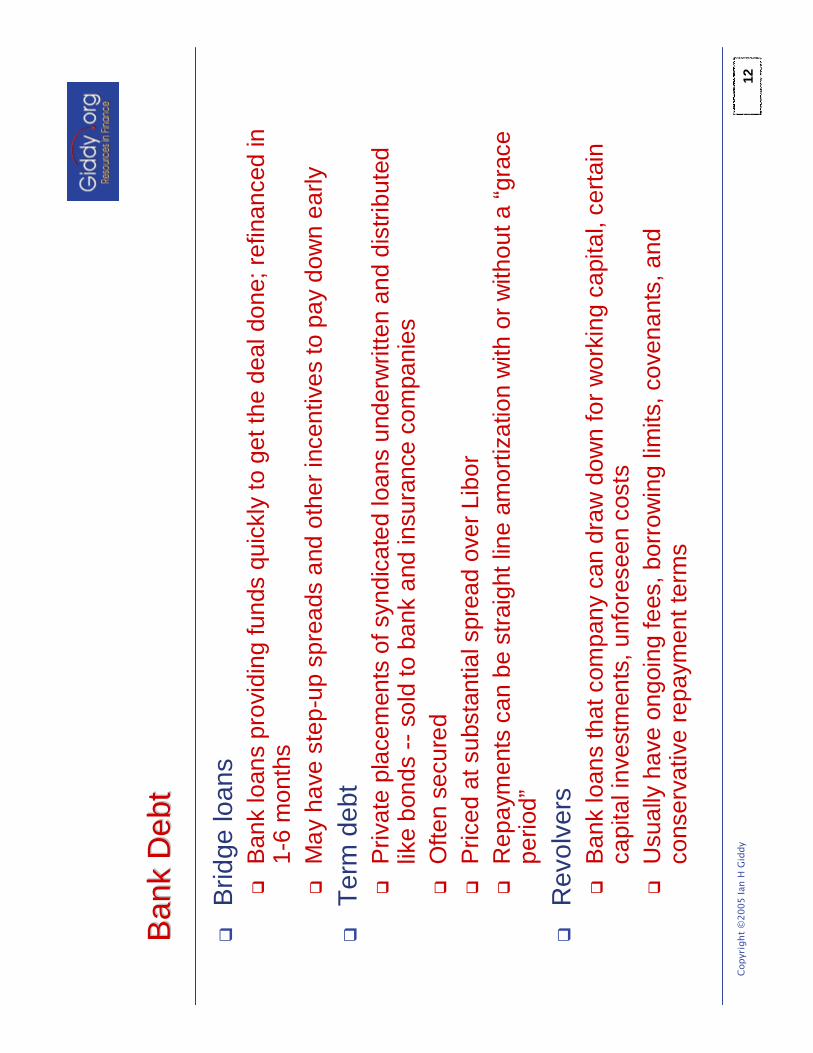

Ban

k D

ebt

Ban

k D

ebt

�B

ridge

loan

s�

Ban

k lo

ans

prov

idin

g fu

nds

quic

kly

to g

et th

e de

al d

one;

ref

inan

ced

in

1-6

mon

ths

�M

ay h

ave

step

-up

spre

ads

and

othe

r in

cent

ives

to p

ay d

own

early

�T

erm

deb

t�

Priv

ate

plac

emen

ts o

f syn

dica

ted

loan

s un

derw

ritte

n an

d di

strib

uted

lik

e bo

nds

--so

ld to

ban

k an

d in

sura

nce

com

pani

es�

Ofte

n se

cure

d �

Pric

ed a

t sub

stan

tial s

prea

d ov

er L

ibor

�R

epay

men

ts c

an b

e st

raig

ht li

ne a

mor

tizat

ion

with

or

with

out a

“gr

ace

perio

d”

�R

evol

vers

�B

ank

loan

s th

at c

ompa

ny c

an d

raw

dow

n fo

r w

orki

ng c

apita

l, ce

rtai

n ca

pita

l inv

estm

ents

, unf

ores

een

cost

s�

Usu

ally

hav

e on

goin

g fe

es, b

orro

win

g lim

its, c

oven

ants

, and

co

nser

vativ

e re

paym

ent t

erm

s

13Copyright ©2005 Ian H Giddy

Syn

dica

ted

Acq

uisi

tion

Loan

sS

yndi

cate

d A

cqui

sitio

n Lo

ans

�D

ebt i

nstr

umen

ts th

at h

ave

feat

ures

of p

ublic

deb

t suc

h as

an

activ

e se

cond

ary

mar

ket a

nd c

redi

t rat

ings

.�

Syn

dica

ted

loan

s ca

n be

bot

h se

cure

d an

d un

secu

red,

bu

t are

alw

ays

seni

or d

ebt.

�Le

vera

ged

synd

icat

ed lo

ans

are

typi

cally

sen

ior

to a

ll ot

her

debt

in th

e bo

rrow

er’s

cap

ital s

truc

ture

, whi

le

synd

icat

ed lo

ans

of in

vest

men

t gra

de fi

rms

are

ofte

n at

th

e sa

me

leve

l of s

enio

rity

as s

enio

r bo

nds.

�G

ener

ally

cal

labl

e at

par

with

out p

enal

ty –

espe

cial

ly

impo

rtan

t in

leve

rage

d fin

ance

.

14Copyright ©2005 Ian H Giddy

New

Pla

yers

New

Pla

yers

17Copyright ©2005 Ian H Giddy

Cas

e S

tudy

: Fin

anci

ng th

e C

ase

Stu

dy: F

inan

cing

the

Val

vex

Val

vex

Acq

uisi

tion

Acq

uisi

tion

�W

ould

you

adv

ise

Con

nexi

onto

use

a s

yndi

cate

d lo

an

to fi

nanc

e its

pro

spec

tive

acqu

isiti

on?

�If

so, h

ow w

ould

it b

e st

ruct

ured

and

dis

trib

uted

? �

How

sho

uld

the

bank

eva

luat

e an

d pr

ice

the

risk?

18Copyright ©2005 Ian H Giddy

Brid

ge F

inan

cing

an

Acq

uisi

tion:

B

ridge

Fin

anci

ng a

n A

cqui

sitio

n: V

alve

xV

alve

x

Th

e C

on

text

�C

onne

xion

is th

e le

adin

g O

EM

sup

plie

r of

one

-way

air

conn

ectio

n va

lves

for

cabi

n pr

essu

rizat

ion

for

the

airli

ne in

dust

ry.

�B

y th

e ac

quiri

ng o

f the

ven

tilat

ion

valv

e di

visi

on o

f Val

vex

Inte

rnat

iona

l, C

onne

xion

was

abl

e to

incr

ease

its

wor

ld-w

ide

mar

ket

shar

e to

23%

F

inan

cin

g N

eed

ed�

Nee

ded

appr

oxim

atel

y E

UR

300

mill

ion

�T

otal

fina

ncin

g of

EU

R 3

01.6

mn:

GB

P 1

72 m

npu

rcha

se p

rice

as

wel

l as

finan

cing

for

gene

ral c

orpo

rate

pur

pose

s T

he

Ch

oic

e�

Use

d te

rm lo

an fu

lly u

nder

writ

ten

by S

ocG

en�

Thr

ee tr

anch

es:

�

EU

R 1

32 M

io. 7

-yea

r te

rm lo

an�

US

D 1

12.5

Mio

. 7-y

ear

term

loan

�E

UR

47

Mio

. 5-y

ear

revo

lver

19Copyright ©2005 Ian H Giddy

Ter

m S

heet

Ter

m S

heet

Source: http://pages.stern.nyu.edu/~igiddy/cases/connexion.doc

20Copyright ©2005 Ian H Giddy

CLO

Exa

mpl

eC

LO E

xam

ple

�S

enio

r lo

ans

now

be

ing

trad

ed a

nd

repa

ckag

ed in

to

asse

t-ba

cked

se

curit

ies

21Copyright ©2005 Ian H Giddy

CLO

Exa

mpl

eC

LO E

xam

ple

22Copyright ©2005 Ian H Giddy

Sub

ordi

nate

d D

ebt

Sub

ordi

nate

d D

ebt

�O

ptim

izat

ion

of fi

nanc

ial l

ever

age

�R

egul

ator

y-dr

iven

cap

ital r

equi

rem

ents

�R

ated

ass

et s

ecur

itiza

tions

(se

nior

-sub

str

uctu

re in

as

set-

back

ed s

ecur

ities

)�

Insi

der

or s

uppl

ier-

cred

it su

bord

inat

ion

(eg

in p

roje

ct

finan

ce)

�W

ork-

outs

and

res

truc

turin

gs (

exis

ting

borr

ower

s ag

ree

to s

enio

rity

of n

ew lo

ans,

to b

uy ti

me)

23Copyright ©2005 Ian H Giddy

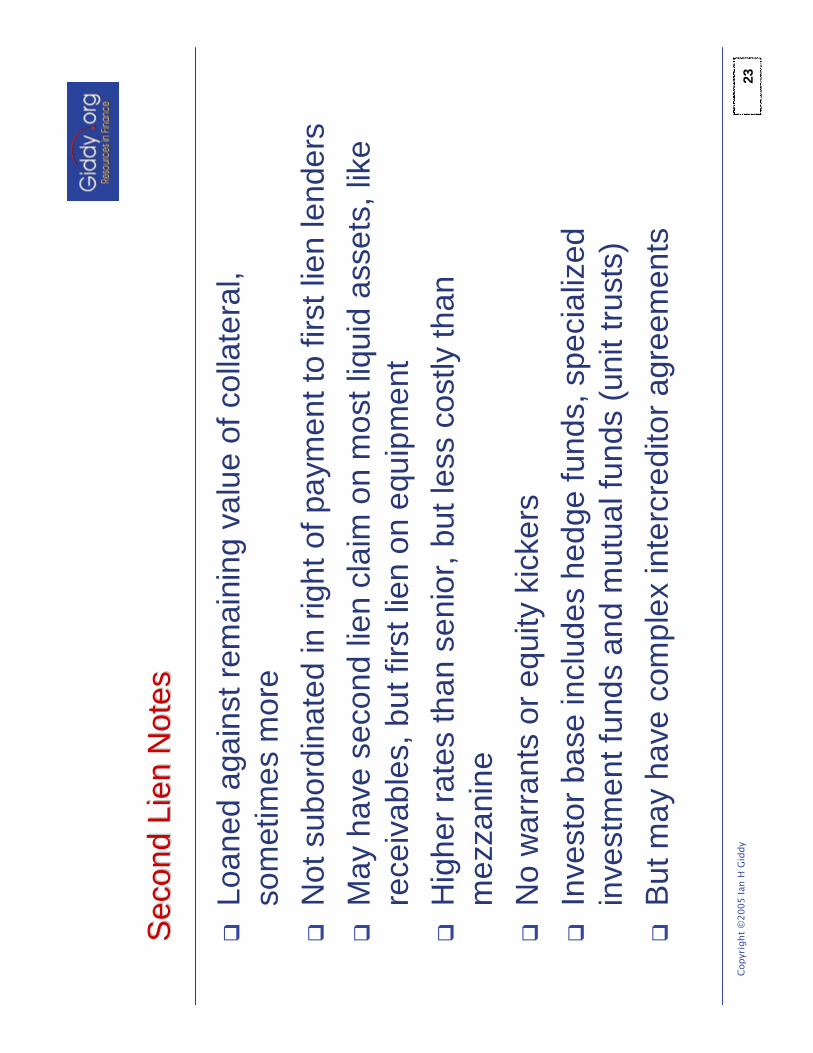

Sec

ond

Lien

Not

esS

econ

d Li

en N

otes

�Lo

aned

aga

inst

rem

aini

ng v

alue

of c

olla

tera

l, so

met

imes

mor

e�

Not

sub

ordi

nate

d in

rig

ht o

f pay

men

t to

first

lien

lend

ers

�M

ay h

ave

seco

nd li

en c

laim

on

mos

t liq

uid

asse

ts, l

ike

rece

ivab

les,

but

firs

t lie

n on

equ

ipm

ent

�H

ighe

r ra

tes

than

sen

ior,

but

less

cos

tly th

an

mez

zani

ne�

No

war

rant

s or

equ

ity k

icke

rs�

Inve

stor

bas

e in

clud

es h

edge

fund

s, s

peci

aliz

ed

inve

stm

ent f

unds

and

mut

ual f

unds

(un

it tr

usts

)�

But

may

hav

e co

mpl

ex in

terc

redi

tor

agre

emen

ts

24Copyright ©2005 Ian H Giddy

Sec

ond

Lien

Sec

ond

Lien

25Copyright ©2005 Ian H Giddy

Sec

ond

Lien

Sec

ond

Lien

26Copyright ©2005 Ian H Giddy

Exa

mpl

e of

Wor

ding

Exa

mpl

e of

Wor

ding

27Copyright ©2005 Ian H Giddy

Sel

ler

Not

esS

elle

r N

otes

�In

Mar

ch 2

003,

Bla

ckst

one

Gro

up a

cqui

red

TR

W A

utom

otiv

e fr

om

Nor

thro

p G

rum

man

for

$4.7

bill

ion.

�P

art o

f the

deb

t fin

anci

ng w

as a

600

mill

ion,

8%

pay

-in-k

ind

note

pa

yabl

e to

a s

ubsi

diar

y of

Nor

thro

p G

rum

man

Cor

pora

tion

�V

alue

d at

$34

8 m

illio

n on

a 1

5-ye

ar li

fe u

sing

a 1

2% d

isco

unt r

ate

�A

s of

Sep

tem

ber,

200

4, th

e ac

cret

ed b

ook

valu

e to

tale

d $4

17

mill

ion,

and

acc

rete

d fa

ce-v

alue

was

$67

8 m

illio

n

�T

hat m

onth

TR

W A

utom

otiv

e re

purc

hase

d th

e S

elle

r N

ote

and

settl

ed v

ario

us c

ontr

actu

al is

sues

ste

mm

ing

from

the

acqu

isiti

on,

for

a ne

t am

ount

of $

493.

5 m

illio

n.

28Copyright ©2005 Ian H Giddy

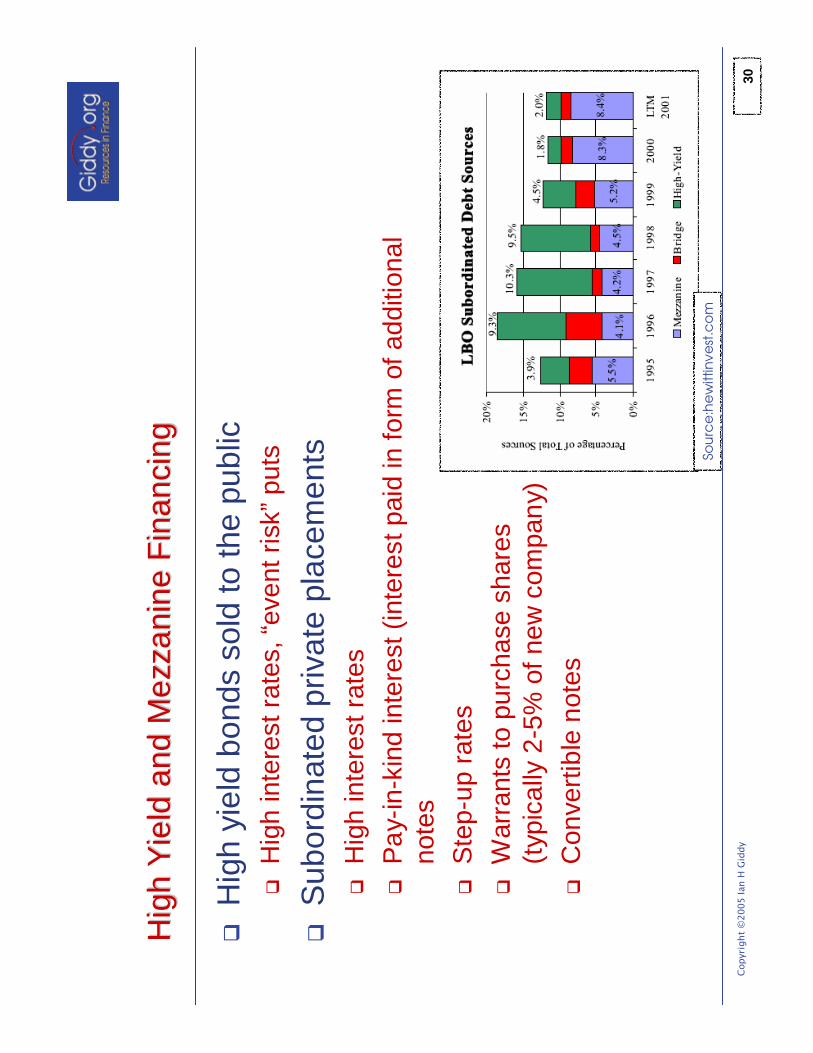

Hig

h Y

ield

and

Mez

zani

ne F

inan

cing

Hig

h Y

ield

and

Mez

zani

ne F

inan

cing

�H

igh

yiel

d bo

nds

sold

to th

e pu

blic

�H

igh

inte

rest

rat

es, “

even

t ris

k” p

uts

�S

ubor

dina

ted

priv

ate

plac

emen

ts�

Hig

h in

tere

st r

ates

�P

ay-

in-k

ind

inte

rest

(in

tere

st p

aid

in fo

rm o

f add

ition

al

note

s�

Ste

p-up

rat

es

�W

arra

nts

to p

urch

ase

shar

es

(typ

ical

ly 2

-5%

of n

ew c

ompa

ny)

�C

onve

rtib

le n

otes

So

urc

e:h

ew

ittin

ve

st.c

om

29Copyright ©2005 Ian H Giddy

Sal

eS

ale

-- and

and

-- Lea

seba

ck F

inan

cing

Leas

ebac

k F

inan

cing

�T

his

is a

n ag

reem

ent i

n w

hich

th

e ow

ner

of p

rope

rty

sells

th

at p

rope

rty

to a

per

son

or

inst

itutio

n an

d th

en le

ases

it

back

aga

in fo

r an

agr

eed

perio

d an

d re

ntal

. �

Leas

ebac

k is

ofte

n us

ed b

y co

mpa

nies

that

wan

t to

free

up

cap

ital t

ied

up in

bui

ldin

gs.

�T

he te

nant

/less

ee o

ften

has

som

e ki

nd o

f opt

ion

to b

uy

back

the

prop

erty

at t

he e

nd o

f th

e le

ase

perio

d.

Le

Me

ridie

n

Ho

tels

Ro

ya

l B

an

k o

f Sc

otla

nd

30Copyright ©2005 Ian H Giddy

Hig

h Y

ield

and

Mez

zani

ne F

inan

cing

Hig

h Y

ield

and

Mez

zani

ne F

inan

cing

�H

igh

yiel

d bo

nds

sold

to th

e pu

blic

�H

igh

inte

rest

rat

es, “

even

t ris

k” p

uts

�S

ubor

dina

ted

priv

ate

plac

emen

ts�

Hig

h in

tere

st r

ates

�P

ay-

in-k

ind

inte

rest

(in

tere

st p

aid

in fo

rm o

f add

ition

al

note

s�

Ste

p-up

rat

es

�W

arra

nts

to p

urch

ase

shar

es

(typ

ical

ly 2

-5%

of n

ew c

ompa

ny)

�C

onve

rtib

le n

otes

So

urc

e:h

ew

ittin

ve

st.c

om

31Copyright ©2005 Ian H Giddy

Hig

h Y

ield

Bon

dsH

igh

Yie

ld B

onds

So

urc

e:

inve

stin

gin

bo

nd

s.c

om

33Copyright ©2005 Ian H Giddy

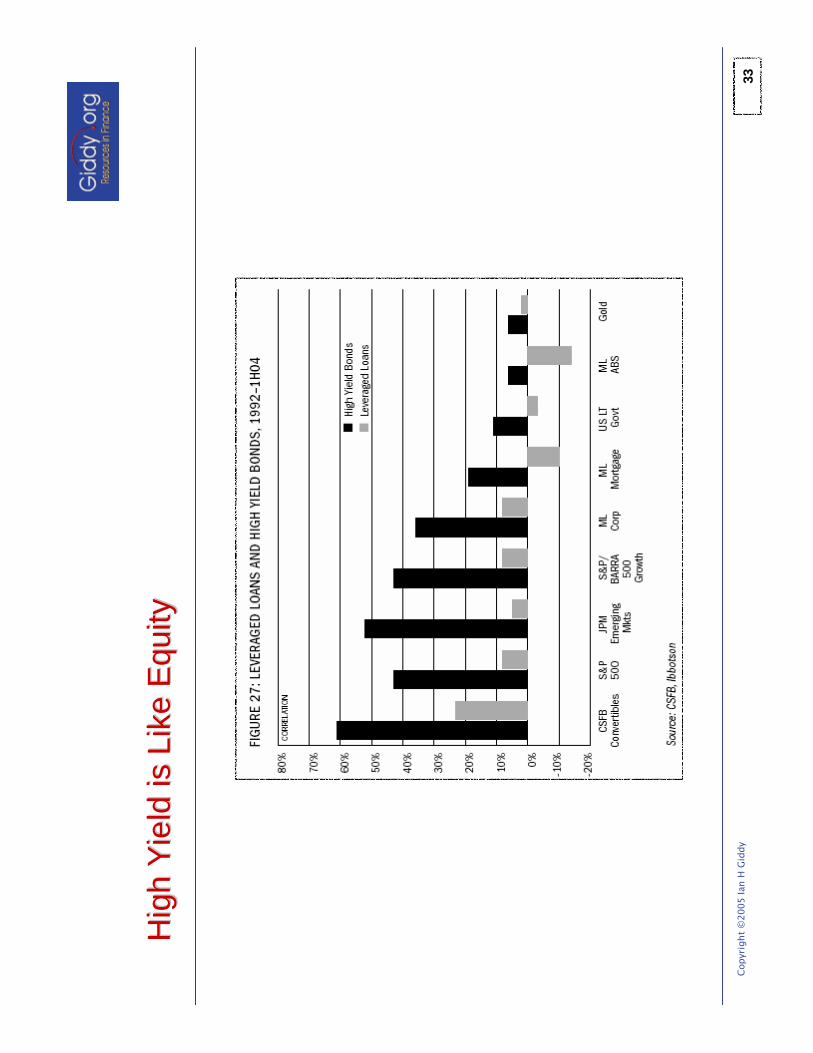

Hig

h Y

ield

is L

ike

Equ

ityH

igh

Yie

ld is

Lik

e E

quity

34Copyright ©2005 Ian H Giddy

Cas

e S

tudy

: C

ase

Stu

dy:

Pia

ggio

Pia

ggio

�W

ho b

uys

“spe

cula

tive

grad

e”

bond

s?�

Wha

t pro

tect

ions

do

high

yie

ld in

vest

ors

wan

t?

�W

hat y

ield

s do

thes

e in

vest

ors

expe

ct, a

nd

in w

hat f

orm

?

�W

hat d

id P

iagg

ioof

fer?

35Copyright ©2005 Ian H Giddy

US

Mez

zani

ne P

rovi

ders

(20

02)

US

Mez

zani

ne P

rovi

ders

(20

02)

36Copyright ©2005 Ian H Giddy

Mez

zani

ne’s

Big

Pro

blem

: Hig

h E

xpec

ted

Rat

e of

Ret

urn

Mez

zani

ne’s

Big

Pro

blem

: Hig

h E

xpec

ted

Rat

e of

Ret

urn

So

luti

on

s�

Dee

p di

scou

nt s

ubor

dina

ted

debt

�S

tep-

up r

ates

�S

ubor

dina

ted

debt

with

equ

ity w

arra

nts

�C

onve

rtib

le s

ubor

dina

ted

debt

�P

artic

ipat

ing

subo

rdin

ated

deb

t�

Put

tabl

esu

bord

inat

ed d

ebt

37Copyright ©2005 Ian H Giddy

Fro

m B

ank

of A

mer

ica:

Fro

m B

ank

of A

mer

ica:

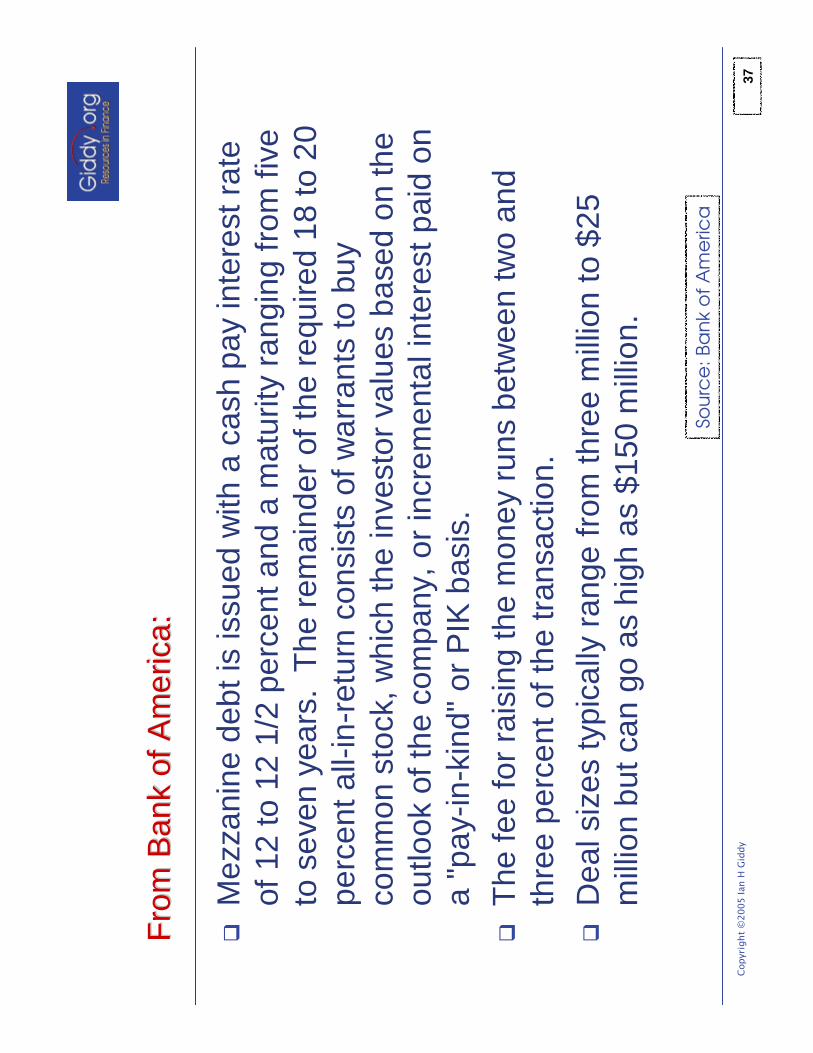

�M

ezza

nine

deb

t is

issu

ed w

ith a

cas

h pa

y in

tere

st r

ate

of 1

2 to

12

1/2

perc

ent a

nd a

mat

urity

ran

ging

from

five

to

sev

en y

ears

. T

he r

emai

nder

of t

he r

equi

red

18 to

20

perc

ent a

ll-in

-ret

urn

cons

ists

of w

arra

nts

to b

uy

com

mon

sto

ck, w

hich

the

inve

stor

val

ues

base

d on

the

outlo

ok o

f the

com

pany

, or

incr

emen

tal i

nter

est p

aid

on

a "p

ay-in

-kin

d" o

r P

IK b

asis

. �

The

fee

for

rais

ing

the

mon

ey r

uns

betw

een

two

and

thre

e pe

rcen

t of t

he tr

ansa

ctio

n.�

Dea

l siz

es ty

pica

lly r

ange

from

thre

e m

illio

n to

$25

m

illio

n bu

t can

go

as h

igh

as $

150

mill

ion.

So

urc

e: B

an

k o

f A

me

ric

a

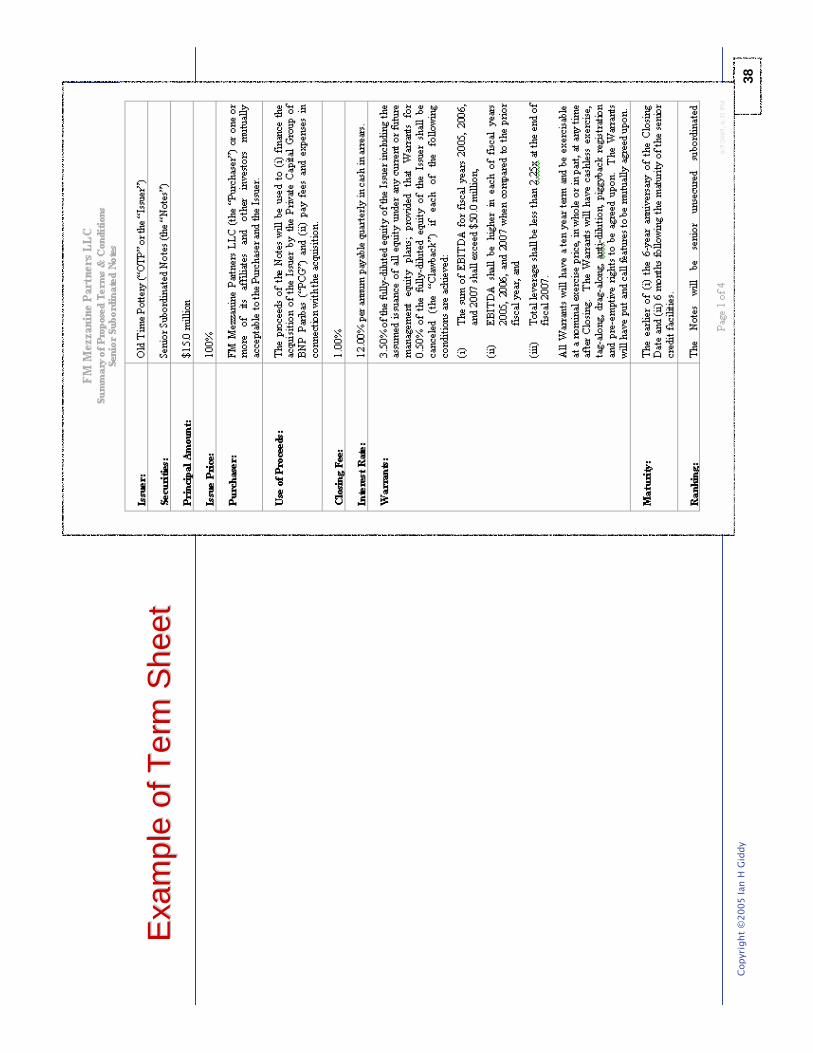

38Copyright ©2005 Ian H Giddy

Exa

mpl

e of

Ter

m S

heet

Exa

mpl

e of

Ter

m S

heet

39Copyright ©2005 Ian H Giddy

Eur

opea

n M

ezza

nine

: Som

e D

evel

opm

ents

Eur

opea

n M

ezza

nine

: Som

e D

evel

opm

ents

�S

ecur

ity. S

ome

bene

fit fr

om th

e sa

me

secu

rity-

colla

tera

l pa

ckag

e as

the

seni

or b

anks

(bu

t on

a se

cond

-ran

king

an

d su

bord

inat

ed b

asis

).�

“War

rant

less

" m

ezza

nine

.B

ased

on

the

emer

genc

e of

a

new

cla

ss o

f "in

stitu

tiona

l" m

ezza

nine

inve

stor

in E

urop

e,

who

vie

ws

mez

zani

ne a

s a

"cur

rent

pay

" as

set a

nd

eval

uate

s in

vest

men

ts b

ased

on

coup

on. (

Eg

CD

Os)

�“M

ezza

nine

not

es.”

Sec

uriti

es is

sued

by

the

hold

ing

com

pany

of t

he s

enio

r de

bt b

orro

wer

(as

for

a hi

gh-y

ield

is

sue)

, hav

e hi

gh-y

ield

-sty

le c

oven

ants

and

ben

efit

from

su

bord

inat

ed u

pstr

eam

gua

rant

ees

from

the

seni

or d

ebt

borr

ower

and

its

oper

atin

g su

bsid

iarie

s.

40Copyright ©2005 Ian H Giddy

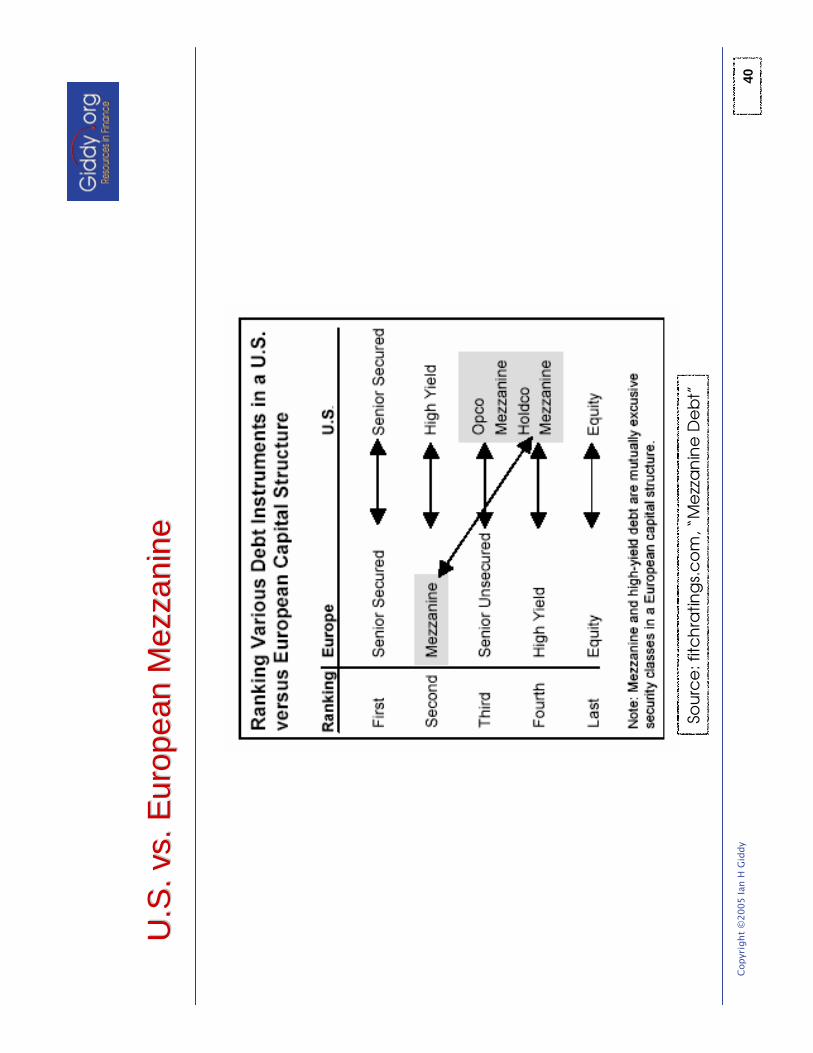

U.S

. vs.

Eur

opea

n M

ezza

nine

U.S

. vs.

Eur

opea

n M

ezza

nine

So

urc

e: fitc

hra

tin

gs.

co

m, “M

ezz

an

ine

De

bt”

41Copyright ©2005 Ian H Giddy

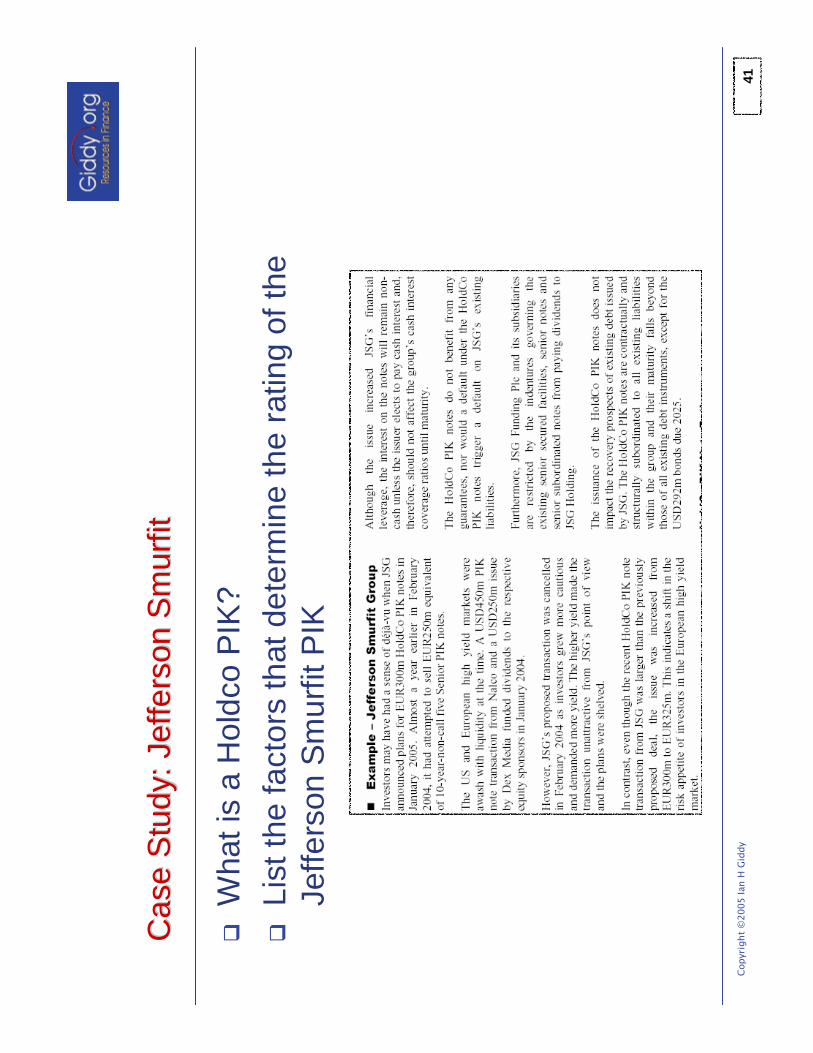

Cas

e S

tudy

: Jef

fers

on S

mur

fitC

ase

Stu

dy: J

effe

rson

Sm

urfit

�W

hat i

s a

Hol

dco

PIK

?�

List

the

fact

ors

that

det

erm

ine

the

ratin

g of

the

Jeffe

rson

Sm

urfit

PIK

42Copyright ©2005 Ian H Giddy

Mez

zani

ne D

ebt w

ith W

arra

nts

Mez

zani

ne D

ebt w

ith W

arra

nts

�T

ypic

ally

sub

ordi

nate

d de

bt w

ith a

ttach

ed e

quity

w

arra

nts

�P

rinci

pal i

s ty

pica

lly r

epai

d in

a lu

mp

sum

at t

he

mat

urity

of t

he lo

an -

-af

ter

seni

or d

ebt i

s re

paid

�

Cas

h co

upon

�

War

rant

s ar

e ty

pica

lly n

omin

ally

-pric

ed a

nd r

epre

sent

a

min

ority

sta

ke in

the

issu

er

43Copyright ©2005 Ian H Giddy

Pay

men

t in

Kin

dP

aym

ent i

n K

ind

44Copyright ©2005 Ian H Giddy

PIK

with

War

rant

sP

IK w

ith W

arra

nts

45Copyright ©2005 Ian H Giddy

Cas

e S

tudy

: Who

Got

the

War

rant

s?C

ase

Stu

dy: W

ho G

ot th

e W

arra

nts?

�In

a d

eal t

hat c

lose

d Ju

ne 1

2, B

rock

way

Mor

an

& P

artn

ers

purc

hase

d W

oods

trea

mC

orp.

, a

mak

er o

f wild

ani

mal

cag

e tr

aps,

rod

ent c

ontr

ol

devi

ces

and

pest

icid

es, f

rom

Frie

nd S

kole

r&

C

o. L

LC. T

he $

100

mill

ion

purc

hase

pric

e is

eq

uiva

lent

to b

etw

een

6.5

and

7x E

BIT

DA

. �

Of t

he e

quity

, Bro

ckw

ay c

ontr

ibut

ed 8

5% o

f the

to

tal,

with

man

agem

ent c

hipp

ing

in 1

0%.

Lend

ers

Ant

ares

Cap

ital C

orp.

and

Alli

ed

Cap

ital C

orp.

fill

in th

e re

mai

ning

5%

gap

. Tot

al

equi

ty r

epre

sent

s ap

prox

imat

ely

40%

of t

he

purc

hase

pric

e.

�O

n th

e de

bt s

ide,

Ant

ares

led

a $5

8 m

illio

n se

nior

faci

lity,

alo

ng w

ith M

erril

l Lyn

ch a

nd G

E

Cap

ital C

orp.

The

sen

ior

debt

com

pone

nt a

lso

cont

ains

a r

evol

ver

to b

e us

ed in

the

futu

re a

s w

orki

ng c

apita

l (an

d no

t inc

lude

d in

the

$100

m

illio

n pu

rcha

se p

rice)

. CIT

Priv

ate

Equ

ity a

nd

Den

ali A

dvis

ors

LLC

pro

vide

d a

subo

rdin

ated

no

te in

the

amou

nt o

f $17

mill

ion.

46Copyright ©2005 Ian H Giddy

Cos

t of t

he

Cos

t of t

he M

ezz

Mez

z ??

�S

enio

r de

bt: L

ibor

+ 3

.50%

, 4 y

ear

amor

tizat

ion

�S

ubor

dina

ted

note

s:

�7%

cas

h in

tere

st�

7% p

ay-in

-kin

d in

tere

st�

War

rant

s to

pur

chas

e 5%

of t

he c

ompa

ny’s

eq

uity

at $

0.05

per

sha

re�

Rep

aym

ent a

fter

5 ye

ars

or a

t exi

t eve

nt

�E

quity

27%

req

uire

d re

turn

47Copyright ©2005 Ian H Giddy

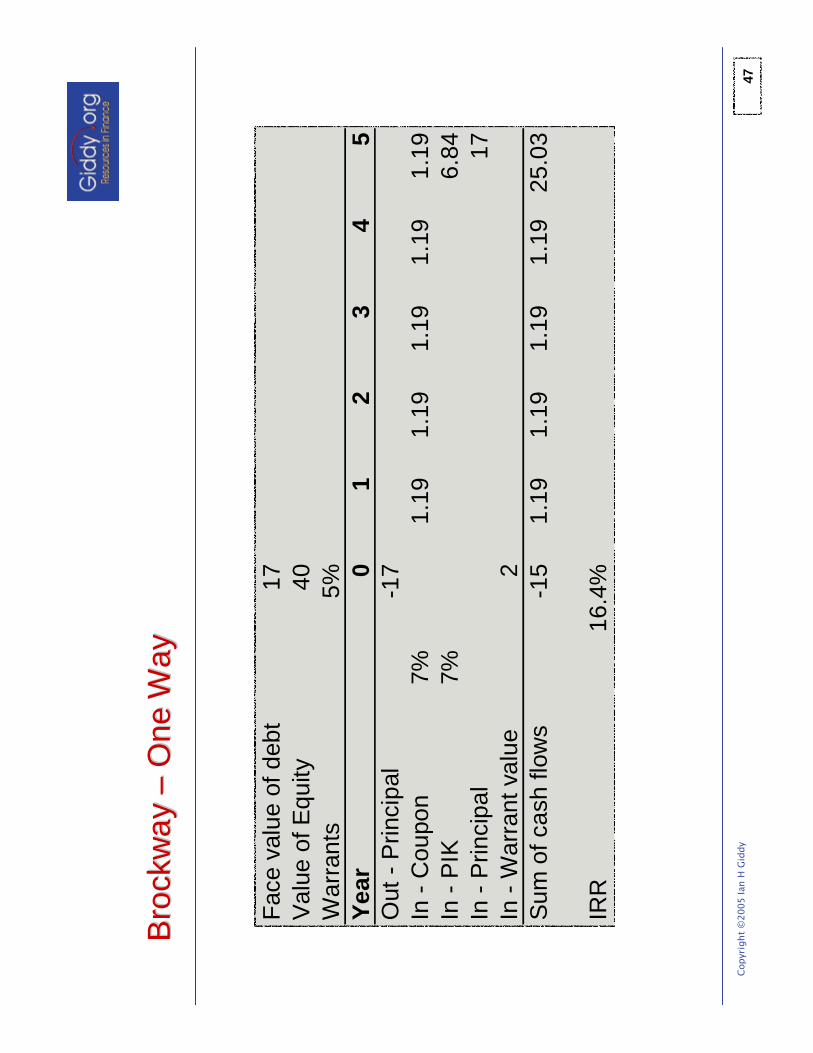

Bro

ckw

ay

Bro

ckw

ay ––

One

Way

One

Way

Fac

e va

lue

of d

ebt

17V

alue

of E

quity

40W

arra

nts

5%Y

ear

01

23

45

Out

- P

rinci

pal

-17

In -

Cou

pon

7%1.

191.

191.

191.

191.

19In

- P

IK7%

6.84

In -

Prin

cipa

l17

In -

War

rant

val

ue2

Sum

of c

ash

flow

s-1

51.

191.

191.

191.

1925

.03

IRR

16.4

%

48Copyright ©2005 Ian H Giddy

War

rant

sW

arra

nts

The

ore

tic

al

Va

lue

Ma

rke

t V

alu

eM

ark

et

Pre

miu

m

V a l u e o f W a r r a n t ($)

0P

ric

e P

er

Sha

re o

f C

om

mo

n S

toc

k (

$)

49Copyright ©2005 Ian H Giddy

War

rant

Agr

eem

ent

War

rant

Agr

eem

ent

50Copyright ©2005 Ian H Giddy

Cas

e S

tudy

: The

C

ase

Stu

dy: T

he W

oods

trea

mW

oods

trea

mT

erm

shee

tT

erm

shee

t

�E

xam

ine

this

term

shee

t. �

As

inve

stor

, whi

ch fe

atur

es

wou

ld y

ou in

sist

on?

�W

here

wou

ld y

ou b

e w

illin

g to

gi

ve w

ay?

51Copyright ©2005 Ian H Giddy

Do

Do

Con

vert

ible

sC

onve

rtib

les

Mak

e S

ense

as

Mez

zani

ne F

inan

ce?

Mak

e S

ense

as

Mez

zani

ne F

inan

ce?

Co

nve

rsio

nV

alu

e

Stra

igh

tB

on

d V

alu

e

Ma

rke

t V

alu

eM

ark

et

Pre

miu

m

V a l u e o f C o n v e r t i b l e B o n d ($)

0P

ric

e P

er

Sha

re o

f C

om

mo

n S

toc

k

52Copyright ©2005 Ian H Giddy

Pre

ferr

ed E

quity

Pre

ferr

ed E

quity

�Le

gally

a fo

rm o

f equ

ity�

Cla

im s

enio

r to

ord

inar

y eq

uity

�M

ay h

ave

fixed

div

iden

d, o

r m

ay b

e “p

artic

ipat

ing”

�B

ut c

anno

t trig

ger

liqui

datio

n if

paym

ent m

isse

d�

Par

val

ue d

eter

min

es li

quid

atio

n cl

aim

53Copyright ©2005 Ian H Giddy

Con

vert

ible

Pre

ferr

edC

onve

rtib

le P

refe

rred

�U

sed

by v

entu

re c

apita

l firm

s�

Per

mit

inve

stor

s to

par

ticip

ate

in g

row

th�

But

giv

e pr

efer

ence

in li

quid

atio

n if

the

vent

ure

fails

�A

nd d

isgu

ise

shar

e va

lue

(tax

!)�

A v

aria

nt –

PE

RC

S*

give

issu

er r

ight

to c

onve

rt in

to

com

mon

sto

ck

�*P

refe

rred

equ

ity r

edem

ptio

n cu

mul

ativ

e st

ock

54Copyright ©2005 Ian H Giddy

Per

form

ance

Per

form

ance

-- Lin

ked

Par

ticip

atio

n D

ebt

Link

ed P

artic

ipat

ion

Deb

t

�A

n al

tern

ativ

e fo

rm o

f mez

zani

ne�

Ofte

n ba

se in

tere

st r

ate

(fix

ed o

r flo

atin

g) p

lus

a pe

rfor

man

ce-li

nked

spr

ead

�E

xam

ples

:�

Inte

rest

rat

e lin

ked

to p

rofit

�In

tere

st r

ate

linke

d to

EB

ITD

A

�In

tere

st r

ate

linke

d to

sal

es

�W

hich

mak

es s

ense

, in

whi

ch s

ituat

ions

?

56Copyright ©2005 Ian H Giddy

Sum

mar

y: M

ezza

nine

and

Hig

h Y

ield

Deb

tS

umm

ary:

Mez

zani

ne a

nd H

igh

Yie

ld D

ebt

So

urc

e: fitc

hra

tin

gs.

co

m, “M

ezz

an

ine

De

bt”

57Copyright ©2005 Ian H Giddy

App

licat

ion:

Str

uctu

ring

the

Mez

zani

neA

pplic

atio

n: S

truc

turin

g th

e M

ezza

nine

�G

oal:

achi

eve

high

er r

etur

n w

ithou

t bur

deni

ng th

e co

mpa

ny o

r in

frin

ging

on

owne

r’s/s

pons

or’s

con

trol

�M

etho

ds: l

ower

inte

rest

rat

e pl

us p

artic

ipat

ion

in

the

com

pany

’s e

quity

or

perf

orm

ance

�W

arra

nts

�P

aym

ent l

inke

d to

turn

over

�P

aym

ent l

inke

d to

EB

ITD

A

�P

aym

ent l

inke

d to

afte

r-ta

x pr

ofit

�M

ay h

ave

a flo

or o

r a

cap

58Copyright ©2005 Ian H Giddy

Cas

e S

tudy

: Alb

ania

Brid

geC

ase

Stu

dy: A

lban

ia B

ridge

�T

he fo

llow

ing

prel

imin

ary

finan

cing

pla

n ha

s be

en p

ropo

sed.

It m

ust b

e re

fined

in o

rder

to m

eet a

ll th

e pa

rtie

s’ o

bjec

tives

and

pro

vide

a fa

ir re

turn

to in

vest

ors.

Can

yo

u h

elp

?Y

ou m

ay u

se th

e fin

anci

al

info

rmat

ion

prov

ided

in th

e sp

read

shee

t fin

anci

ng_a

bc.x

ls.

Sour

ce

EU

R m

illio

ns

%

Equ

ity/S

ubor

dina

ted

Loa

n

Alb

ania

n S

pons

or E

quit

y 3.

0

Dut

ch S

pons

or E

quit

y 2.

0

FMO

Sub

ordi

nate

d C

onve

rtib

le L

oan

2.0

Sub

tota

l 7.

0 48

.9%

Mez

zani

ne L

oan

a. F

MO

1.

5

Sub

tota

l 1.

5 8.

6%

Seni

or L

oan

a. B

ank

grou

p A

7.

0

b. B

ank

grou

p B

2.

5

Sub

tota

l 9.

5 52

.5%

Tot

al F

inan

cing

18

.0

100%

59Copyright ©2005 Ian H Giddy

Sha

ring

the

Ret

urns

Sha

ring

the

Ret

urns

Cas

h F

low

An

alys

is20

0520

0620

0720

0820

0920

10R

even

ue21

25.2

30.2

33.3

36.6

40.2

EB

ITA

3.15

3.8

4.5

6.7

7.3

8.0

+ D

epre

ciat

ion

22.

12.

22.

32.

42.

6-

Cap

ex-3

-3.2

-3.3

-3.5

-3.6

-3.8

- In

cr in

Net

Wor

king

Cap

-0.8

-0.4

-0.5

-0.3

-0.3

-0.4

FC

F B

efor

e F

inan

cing

1.4

2.3

2.9

5.2

5.8

6.4

�H

ow c

an w

e m

ake

thes

e ca

sh fl

ows

wor

k to

ach

ieve

the

desi

red

retu

rn fo

r al

l the

par

ties?

�S

pons

ors

�F

MO

as

mez

zani

ne in

vest

or

�S

enio

r le

nder

s

60Copyright ©2005 Ian H Giddy

Pos

tP

ost --

Dea

l Mez

zani

ne M

anag

emen

tD

eal M

ezza

nine

Man

agem

ent

�T

he A

BC

dea

l was

fina

nced

as

prop

osed

. It i

s tw

o ye

ars

late

r, a

nd s

ome

of th

e pr

ojec

ts h

ave

been

de

laye

d. A

s a

resu

lt, p

aym

ent h

as b

een

slow

er.

Cov

enan

ts m

ay n

ot b

e m

et. W

hat d

o w

e do

?

Cas

h F

low

An

alys

is20

0520

0620

0720

0820

0920

10R

even

ue21

22.1

24.3

27.9

30.7

33.8

EB

ITA

3.15

2.2

3.6

5.6

6.1

6.8

+ D

epre

ciat

ion

22.

12.

22.

32.

42.

6-

Cap

ex-3

-3.2

-3.3

-3.5

-3.6

-3.8

- In

cr in

Net

Wor

king

Cap

-0.8

-0.1

-0.2

-0.4

-0.3

-0.3

FC

F B

efor

e F

inan

cing

1.4

1.1

2.3

4.1

4.6

5.2

62Copyright ©2005 Ian H Giddy

Pro

f. Ia

n G

iddy

NY

U S

tern

Sch

ool o

f Bus

ines

sT

el +

1.64

6.80

80.7

46; F

ax 2

12.9

95.4

233

ian.

gidd

y@ny

u.ed

uW

eb: g

iddy

.org

Am

ster

dam

Inst

itute

of F

inan

ceT

el +

31 2

0 52

0016

0; F

ax +

31 2

0 52

0016

1 in

fo@

aif.n

lW

eb: a

if.nl

Con

tact

sC

onta

cts