Oct 2016 DISCUSSION Levelised Cost of Energy (LCOE ... - Solar

Upload

truonghanhCategory

view

220download

1

Levelised Costs of Power Generation

4th SEE Energy Dialogue

Thessaloniki 3-4 June 2010

Dr. Nick F Frydas

Contents

• What are levelised costs?“Levelised cost of generation is the discounted lifetime cost ofowning and operating a generation asset expressed on a per unit ofoutput basis (£/MWh). - Busbar Cost – No externalities exceptCarbon Price

• Recent trends in EPC prices• Recent trends in EPC prices

• Build up of EPC and overnight capex costs

• Base case assumptions

• Outlook for levelised costs

Who is Mott MacDonald?

One of the world’s largest management, engineering

and development consultancies

active in power, oil & gas, water, transport, buildings, communication, education, health etc.

Leading capability in power covering renewables, thermal and nuclear

We work in over 140 countriesWe work in over 140 countries

From 200 permanent offices

On some 16,000 projects

Over 14,000 staff

Turnover of ~ $1.5bn

Power Sector – Our Services

Project initiation & development

Design & Design & construction

Commissioning & operation

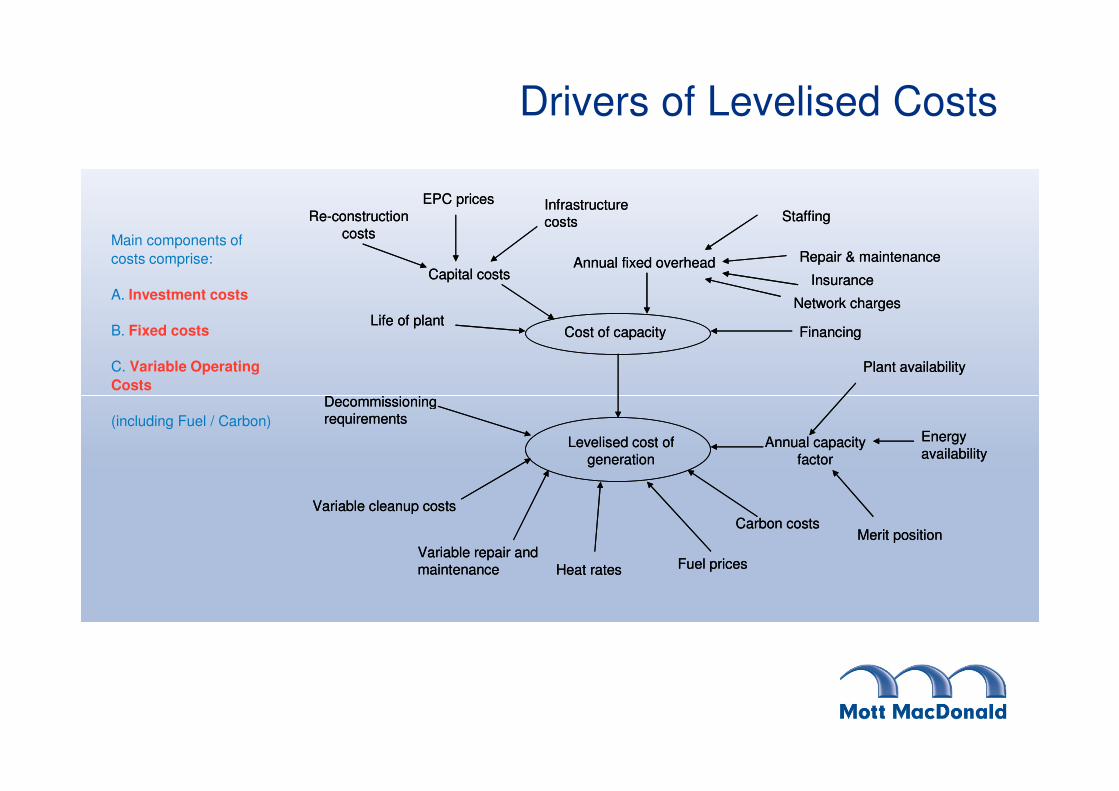

Drivers of Levelised Costs

Re-construction costs

EPC prices

Cost of capacity

Decommissioning

Plant availability

Financing

Annual fixed overhead

Staffing

Repair & maintenance

Insurance

Network chargesLife of plant

Capital costs

Infrastructure costsRe-construction

costs

EPC prices

Cost of capacity

Decommissioning

Plant availability

Financing

Annual fixed overhead

Staffing

Repair & maintenance

Insurance

Network chargesLife of plant

Capital costs

Infrastructure costs

Main components of

costs comprise:

A. Investment costs

B. Fixed costs

C. Variable Operating

Costs

Energy availability

Levelised cost of generation

Decommissioning requirements

Variable cleanup costs

Variable repair and maintenance Fuel prices

Carbon costs

Annual capacity factor

Merit position

Heat rates

Energy availability

Levelised cost of generation

Decommissioning requirements

Variable cleanup costs

Variable repair and maintenance Fuel prices

Carbon costs

Annual capacity factor

Merit position

Heat rates

(including Fuel / Carbon)

Levelised Cost - Main Components

• Pre-construction costs

• Capex including financing costs

• Annual overheads of plant (excludes central HQ

overheads)overheads)

• Variable non-fuel opex (var. O&M, ash disposal, etc.)

• Fuel and carbon

• CO2 transport and disposal

• Decommissioning

Technologies

Mainly looking “baseload” and >10MW

• CCGT, ASC Coal, IGCC + CCS variants

• Nuclear – EPR/AP1000

• Wind – on and offshore

• Biomass combustion 50MW/ 300MW

• Gas and biomass fired CHP

• Bio-methane (LFG, Sewage, AD of agri wastes)

• Hydro reservoir +PSP

Representative EPC prices: 1990-2009

EPC prices in nomial US Dollars

2000

2500

3000

3500U

S$/k

W

CCGT

Coal Plant

Hydro

0

500

1000

1500

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

US

$/k

W

Coal has developed a huge premium versus CCGT

Coal's EPC premium versus CCGT

1500

2000

0

500

1000

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

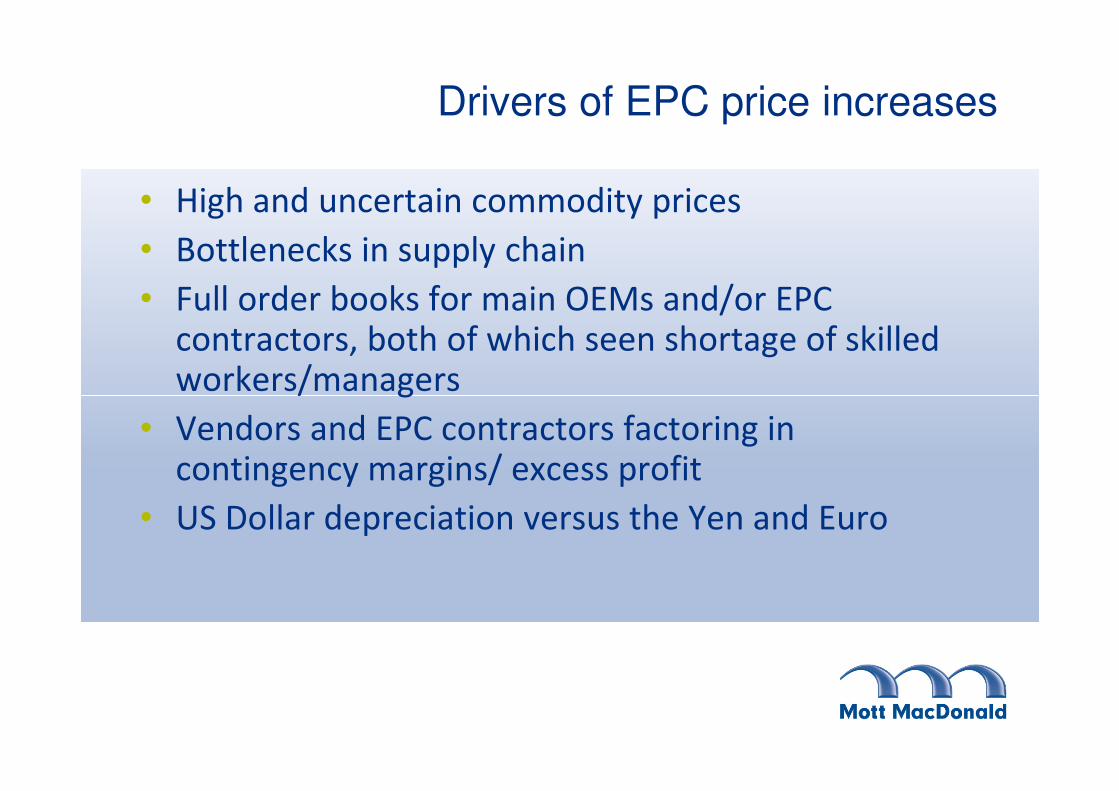

Drivers of EPC price increases

• High and uncertain commodity prices

• Bottlenecks in supply chain

• Full order books for main OEMs and/or EPC contractors, both of which seen shortage of skilled workers/managersworkers/managers

• Vendors and EPC contractors factoring in contingency margins/ excess profit

• US Dollar depreciation versus the Yen and Euro

Other drivers of EPC costs

• Hardware/process complexity

• Economies of scale

• Maturity of technology

• Jurisdictional risk• Jurisdictional risk

EPC options and costs by fuel type

Nuclear

Demanding biomass waste

Sewage gasMSW

Woody biomass

Easy biomass waste

CoalCoal

HFO

Landfill gas

Diesel

Natural gas

Industrial

GT Gas engine Aero GT

Large

boiler ST

Small boiler

ST

Indicative build-up of nuclear plant costs: $/kW

FOAK build up

Cost to build 3500

FOAK premium 700

Contractor's normal profit 300

OEM's risk premium 250OEM's risk premium 250

Headline EPC price 4750

Owners allowed contingency 750

Unallocated over-runs 500Total overnight EPC cost 6000

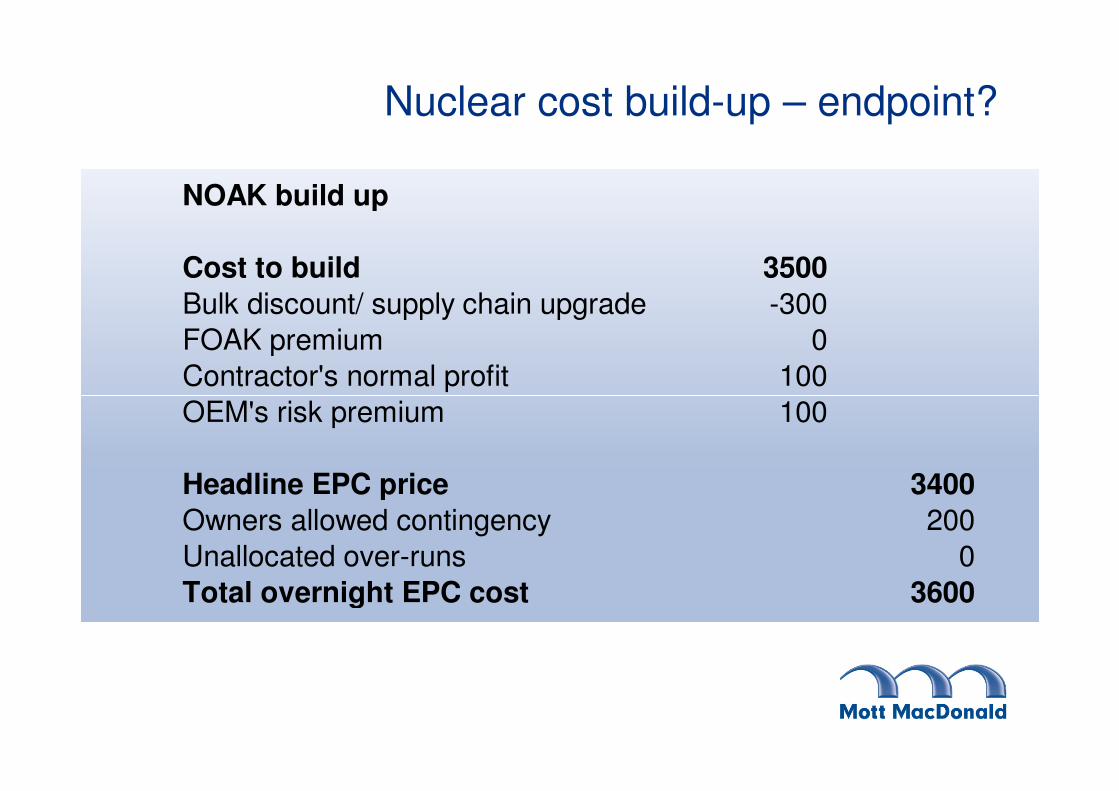

Nuclear cost build-up – endpoint?

NOAK build up

Cost to build 3500

Bulk discount/ supply chain upgrade -300

FOAK premium 0

Contractor's normal profit 100

OEM's risk premium 100

Headline EPC price 3400

Owners allowed contingency 200

Unallocated over-runs 0

Total overnight EPC cost 3600

Fixed opex

• What drives fixed opex? Core operating and

maintenance linked to specific capex cost (EPC

costs) – Insurance also?

• Some items like TNUoS and rates linked to • Some items like TNUoS and rates linked to

MW

• Seems to have risen with EPC prices

• Varies between 1.5% and 8% of capex

Base Case Assumptions

• Discount rate: 10%

• Used economic plant lives rather than loan terms

• Fuel prices taken from DECC projections – all scenarios higher than pre-2005 averagescenarios higher than pre-2005 average

• Carbon prices - MM central case £32/t

• General EPC prices – softening in medium term, then level

Fuel prices

DECCs high, mid and low coal and gas price

projections

150

200

Co

al:

$/t

@25G

J A

RA

(so

lid

lin

es)

0.75

1.00

Gas:

£/t

herm

NB

P (

bro

ken

lin

e)

Mid case has coal at £2.25/GJ

0

50

100

2009 2014 2019 2024 2029 2034 2039 2044 2049

Co

al:

$/t

@25G

J A

RA

(so

lid

lin

es)

0.00

0.25

0.50

Gas:

£/t

herm

NB

P (

bro

ken

lin

e)

at £2.25/GJ ($80/t) versus gas at £7.70/GJ (73ppt).

Carbon prices: £/tCO2, DECC versus MM

150

200

250

300

-

50

100

2009 2014 2019 2024 2029 2034 2039 2044 2049

Base Case Results

• ASC Coal and CCGT are lowest cost of main technologies excluding carbon, at £62/MWh

• Adding carbon at average price of €32/t makes CCGT least cost, at £74/MWh versus £82/MWh for coal (£108/MWh)

• CCGT+CCS and least cost coal+CCS costs £104-115/MWh, well above nuclear at under £99/MWh – In the longer term nuclear becomes the Least Cost Option at £67/MWhnuclear becomes the Least Cost Option at £67/MWh

• On-shore wind sits between ASC coal and nuclear at £94/MWh, while offshore wind well over CCS options at £157-185/MWh (£110-125/MWh)

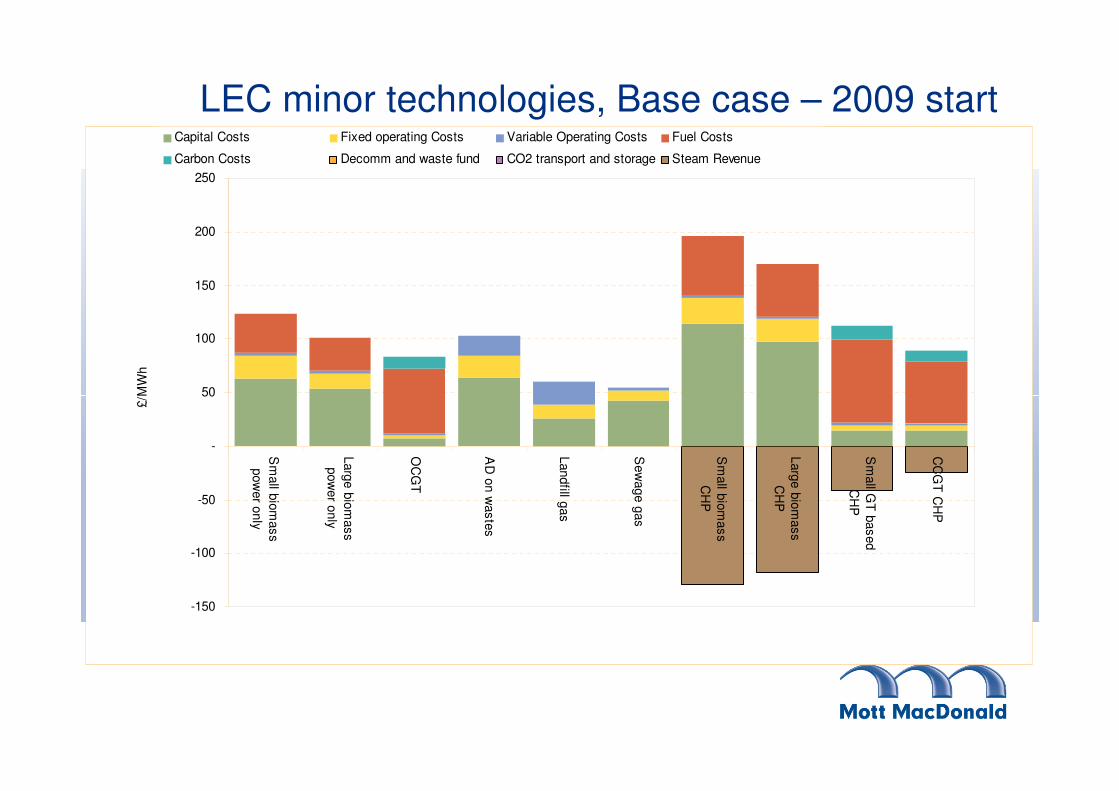

• Biomass CHP with 50% steam credit < £70/MWh (£102/MWh)

• LFG/SG < £60/MWh

LEC main technologies, Base case – 2009 start

80

100

120

140

160

180

200

£/M

Wh

Capital Costs Fixed operating Costs Variable Operating Costs Fuel Costs

Carbon Costs Decomm and w aste fund CO2 transport and storage

-

20

40

60

Ga

s P

lan

t - CC

GT

Ga

s P

lan

t - CC

GT

with

CC

S

Co

al P

lan

t - Pu

lve

rsie

d

fue

l, AS

C w

ith F

GD

Co

al P

lan

t - Pu

lve

rsie

d

fue

l, AS

C w

ith F

GD

an

d C

CS

Co

al P

lan

t - Pu

lve

rsie

d

fue

l, AS

C w

ith F

GD

an

d re

tro-fitte

d C

CS

Co

al P

lan

t - IGC

C

Co

al P

lan

t - IGC

C w

ith

CC

S

Win

d - O

ns

ho

re W

ind

Win

d - O

ffsh

ore

Win

d

Win

d - O

ffsh

ore

Win

d

R3

Nu

cle

ar - C

om

pa

ct

mo

du

lar P

WR

LEC premium versus CCGT, main technologies, Base case – 2009 start

40

60

80

100

120

0

20

40

Gas

Pla

nt -

CC

GT

CC

GT+C

CS

ASC

Coa

lC

oal+

CC

SC

oal+

CC

S retro

IGC

CIG

CC

+CC

SO

nsho

re w

ind

Offs

hore

win

dR

3 of

fsho

reN

ucle

ar P

WR

LEC minor technologies, Base case – 2009 start

50

100

150

200

250

£/M

Wh

Capital Costs Fixed operating Costs Variable Operating Costs Fuel Costs

Carbon Costs Decomm and waste fund CO2 transport and storage Steam Revenue

-150

-100

-50

-

50

Sm

all b

iom

ass

pow

er o

nly

Larg

e b

iom

ass

pow

er o

nly

OC

GT

AD

on w

aste

s

Landfill g

as

Sew

age g

as

Sm

all b

iom

ass

CH

P

Larg

e b

iom

ass

CH

P

Sm

all G

T b

ased

CH

P

CC

GT

CH

P

£/M

Wh

LEC premium versus CGGT, Base case – 2009 start

20

30

40

50

60

-30

-20

-10

-

10

Small

biomass

power

only

Large

biomass

power

only

OCGT AD on

wastes

Landfill

gas

Sewage

gas

Small

biomass

CHP

Large

biomass

CHP

Small GT

based

CHP

CCGT

CHP

LEC main technologies, project start 2020

60

80

100

120

140

£/M

Wh

Capital Costs Fixed operating Costs Variable Operating Costs Fuel Costs

Carbon Costs Decomm and w aste fund CO2 transport and storage

-

20

40

Ga

s P

lan

t - CC

GT

Ga

s P

lan

t - CC

GT

with

CC

S

Co

al P

lan

t - Pu

lve

rsie

d

fue

l, AS

C w

ith F

GD

Co

al P

lan

t - Pu

lve

rsie

d

fue

l, AS

C w

ith F

GD

an

d C

CS

Co

al P

lan

t - Pu

lve

rsie

d

fue

l, AS

C w

ith F

GD

an

d re

tro-fitte

d C

CS

Co

al P

lan

t - IGC

C

Co

al P

lan

t - IGC

C w

ith

CC

S

Win

d - O

ns

ho

re W

ind

Win

d - O

ffsh

ore

Win

d

Win

d - O

ffsh

ore

Win

d

R3

Nu

cle

ar - C

om

pa

ct

mo

du

lar P

WR

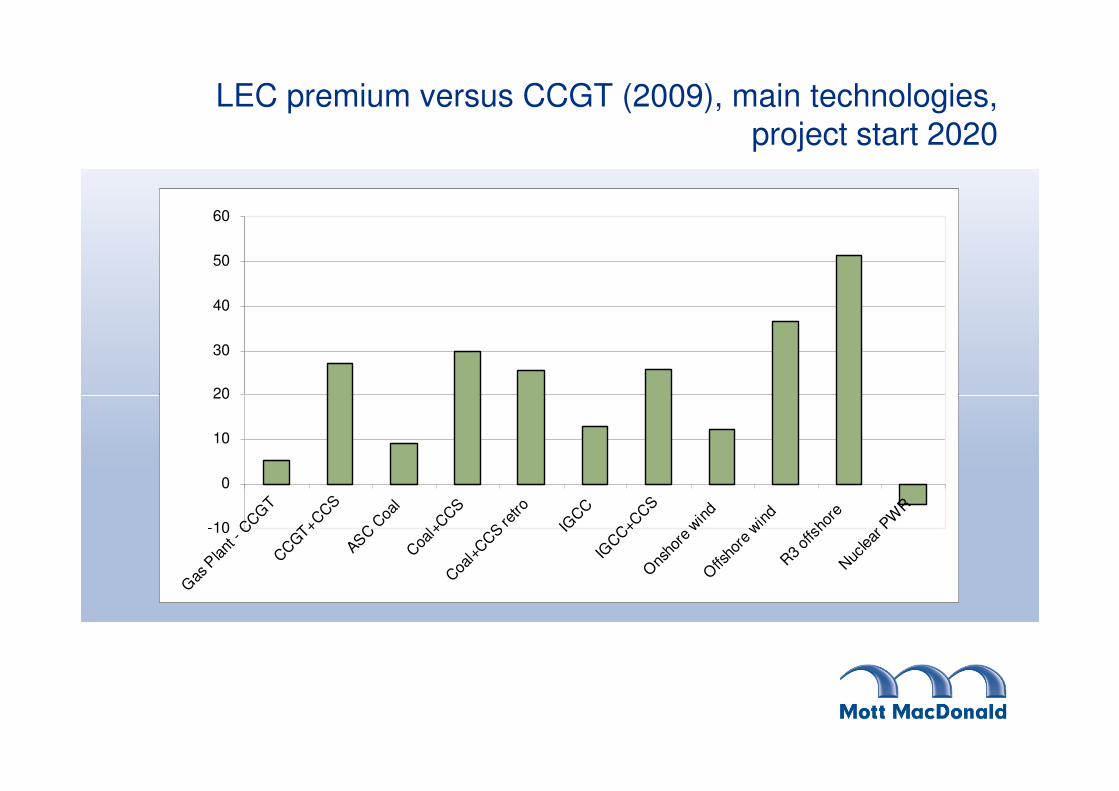

LEC premium versus CCGT (2009), main technologies, project start 2020

20

30

40

50

60

-10

0

10

20

Gas

Pla

nt -

CC

GT

CC

GT+C

CS

ASC

Coa

lC

oal+

CC

SC

oal+

CC

S retro

IGC

CIG

CC

+CC

SO

nsho

re w

ind

Offs

hore

win

dR

3 of

fsho

reN

ucle

ar P

WR

LEC minor technologies, project start 2020

50

100

150

200

£/M

Wh

Capital Costs Fixed operating Costs Variable Operating Costs Fuel Costs

Carbon Costs Decomm and waste fund CO2 transport and storage Steam Revenue

-150

-100

-50

- Sm

all b

iom

ass

pow

er o

nly

Larg

e b

iom

ass

pow

er o

nly

OC

GT

AD

on w

aste

s

Landfill g

as

Sew

age g

as

Sm

all b

iom

ass

CH

P

Larg

e b

iom

ass

CH

P

Sm

all G

T b

ased

CH

P

CC

GT

CH

P

£/M

Wh

LEC premium versus CCGT (2009), minor technologies, project start 2020

-10

-

10

20

30

40

Small

biomass

Large

biomass

OCGT AD on

wastes

Landfill

gas

Sewage

gas

Small

biomass

Large

biomass

Small GT

based

CCGT

CHP

-60

-50

-40

-30

-20

-10 biomass

power

only

biomass

power

only

wastes gas gas biomass

CHP

biomass

CHP

based

CHP

CHP

Results using DECC assumptions – main technologies

100

120

140

160

180

200

-

20

40

60

80

100

Current 2009 2013 2017 2017 all NOAK 2023 all NOAK

Gas - CCGT Gas - CCGT with CCS

ASC Coal - with FGD ASC Coal - with FGD and CCS

Coal - IGCC Coal - IGCC with CCS

Onshore Wind Offshore Wind

Offshore Wind R3 Nuclear - PWR

Conclusions

• Levelised costs for new plant will be higher than current prices

• CCGT will be the benchmark to beat in near to medium term –ASC coal £9/MWh above this, while nuclear and coal+CCS are £27-60/MWh above

• As nuclear, CCS and offshore wind move to NOAK status costs will fall markedlywill fall markedly

• In longer term nuclear looks a good deal and should substantially undercut CCS and offshore wind, and could even be less than CCGT without CCS

• But high FOAK premium creates special funding challenge for first units, even assuming all benign regulatory and market environment