Letter of Credit Basicsdocshare01.docshare.tips/files/28677/286773732.pdf · Definition of Letter...

53

Letter of credit basics Letter of Credit Basics http://www.letterofcredit.biz/ What is Letter of Credit Letter of credit, in a broad perspective, is one of the payment methods in international trade. Some of the other payment methods in international trade are Cash-in- Advance, Documentary Collections and Open Account. All of these payment methods inherit different risk levels for exporters and importers. Letters of credit is the only payment method, which has a balanced risk structure for both parties. Figure 1: Payment Risk Diagram Key Points • To succeed in today’s global marketplace and win sales against International trade presents a spectrum of risk, which causes uncertainty over the timing of payments between the exporter (seller) and importer (foreign buyer). • For exporters, any sale is a gift until payment is received.

Transcript of Letter of Credit Basicsdocshare01.docshare.tips/files/28677/286773732.pdf · Definition of Letter...

Letter of credit basics Letter of Credit Basics http://www.letterofcredit.biz/What is Letter of Credit

Letter of credit, in a broad perspective, is one of the payment methods in

international trade.

Some of the other payment methods in international trade are Cash-in-Advance, Documentary Collections and Open Account. All of these payment methods inherit different risk levels for exporters and importers. Letters of creditis the only payment method, which has a balanced risk structure for both parties.

Figure 1: Payment Risk Diagram

Key Points

• To succeed in today’s global marketplace and win sales against International tradepresents a spectrum of risk, which causes uncertainty over the timing of payments between the exporter (seller) and importer (foreign buyer).

• For exporters, any sale is a gift until payment is received.

• Therefore, exporters want to receive payment as soon as possible, preferably as soon as an order is placed or before the goods are sent to the importer.

• For importers, any payment is a donation until the goods are received.

• Therefore, importers want to receive the goods as soon as possible but to delay payment as long as possible, preferably until after the goods are resold to generate enough income to pay the exporter.

Cash-in-Advance

With cash-in-advance payment terms, the exporter can avoid credit risk because payment is received before the ownership of the goods is transferred. Wire transfersand credit cards are the most commonly used cash-in-advance options available to exporters. However, requiring payment in advance is the least attractive option for the buyer, because it creates cash-flow problems. Foreign buyers are also concerned that the goods may not be sent if payment is made in advance. Thus, exporters who insist on this payment method as their sole manner of doing businessmay lose to competitors who offer more attractive payment terms.

Letters of Credit

Letters of credit (LCs) are one of the most secure instruments available to international traders. An LC is a commitment by a bank on behalf of the buyer that payment will be made to the exporter, provided that the terms and conditions stated in the LC have been met, as verified through the presentation of all required documents. The buyer pays his or her bank to render this service. An LC is useful when reliable credit information about a foreign buyer is difficult to obtain, but the exporter is satisfied with the creditworthiness of the buyer’s foreign bank. An LC also protects the buyer because no payment obligation arises until the goods have been shipped or delivered as promised.

Documentary Collections

A documentary collection (D/C) is a transaction whereby the exporter entrusts the collection of a payment to the remitting bank (exporter’s bank), which sends documents to a collecting bank (importer’s bank), along with instructions for payment. Funds are received from the importer and remitted to the exporter through the banks involved in the collection in exchange for those documents. D/Cs involve using a draft that requires the importer to pay the face amount either at sight (document against payment) or on a specified date (document against acceptance). The draft gives instructions that specify the documents required for the transfer of title to the goods. Although banks do act as facilitators for their clients, D/Cs offer no verification process and limited recourse in the event of non-payment. Drafts are generally less expensive than LCs.

Open Account

An open account transaction is a sale where the goods are shipped and delivered before payment is due, which is usually in 30 to 90 days. Obviously, this option is the most advantageous option to the importer in terms of cash flow and cost, but it is consequently the highest risk option for an exporter. Because of intense competition in export markets, foreign buyers often press exporters for open account terms since the extension of credit by the seller to the buyer is more common abroad. Therefore, exporters who are reluctant to extend credit may lose asale to their competitors. However, the exporter can offer competitive open accountterms while substantially mitigating the risk of non-payment by using of one or more of the appropriate trade finance techniques, such as export credit insurance.

We have explained above that letters of credit can limit the risks of importers

and exporters. However, how can letters of credit achieve this? Letters of credit

can balance the risks of exporters and importers because responsibility of LC

operations is given to a third party, to the banks. We will explain this later on

detailly.

Definition of Letter of Credit:

"Credit means any arrangement, however named or described, that

is irrevocable and thereby constitutes a definite undertaking of the issuing bank

to honour a complying presentation." (UCP 600, article 2)

This letter of credit definition is taken from the UCP 600 (ICC Uniform Customs

and Practice for Documentary Credits) which is the latest version of the rules

published by ICC (International Chamber of Commerce ) regulating the letters of

credit operations all around the world.

Role of the ICC and UCP in Letters of Credit

International trade is exchange of capital, goods, and services across

international borders between people whom belong to different languages,

cultures and laws. As letters of credit are a payment method of international

trade it is obvious that standardized rules are needed to govern letters of credit

in a global scale to make sure that letters of credit transactions run smoothly.

ICC, International Chamber of Commerce, is the organization that publishes the

standardized rules. The rules, which are called UCP, Uniform Customs and

Practice for Documentary Credits, are revised regularly. At the time of this text is

written sixth version of the UCP rules is in force.

In this first article, we have seen what letter of credit is, its definition, the rules

that apply to them and the organization that publishes these rules. In the next

article, we will examine types of letters of credit.

Types of Letters of Credit

Traveler's letters of credit, which were commonly used in eighteenth century, were the first financial instrument contains very similar characteristics with the contemporary letters of credit.

From traveler's letters of credit days to today's complex global economy, the letters of credit have been performing their duties as a secure andreliable payment method. Actually, during this period letters of credit have gained a very flexible structure that can satisfy different needs of different typesof international trade practitioners. In this article, we will discuss types of letters of credit.

Commercial Letters of Credit

Commercial letters of credit are mainly used as a primary payment tool in

international trade such as exporting and importing transactions. Majority of

commercial letters of credit are issued subject to the latest version of UCP

(Uniform Customs and Practice for Documentary Credits). The ICC publishes

UCP, which are the set of rules that governs the commercial letters of credit

procedures.

Standby Letters of Credit

Commercial letters of credit are a means of payment to be utilized when the

principal perform its duties. As an example, let us consider an exporter who

ships the goods according to the sales contract and apply to the nominated

bank for the payment. If the nominated bank decides that the presentation is

conforming to the terms and conditions of the credit and the UCP rules then

exporter will be paid. This situation is just contrary in standby letters of credit.

A payment is made to the beneficiary of a standby letter of credit when there is

a breach of the principal's obligation. As an example, let us consider a

construction company that has been awarded with a tender. If this construction

company cannot fulfill its obligations under the project contract beneficiary of

the standby letter of credit can apply to the nominated bank for the payment.

However, the nominated bank considers only the terms and the conditions of

the standby letter of credit and the rules governing the credit when deciding a

complying presentation. One point that needs to be stressed is that standby

letters of credit have their own rules, which are called The International Standby

Practices 1998 (ISP98). They are also published by ICC. However, a standby

letter of credit can be issued subject to either the UCP or the ISP.

Revocable Letters of Credit

Revocable letters of credit give issuer the amendment or cancellation right of

the credit any time without prior notice to the beneficiary. Since revocable

letters of credit do not provide any protection to the beneficiary, they are not

used frequently. In addition, UCP 600 has no reference to revocable letters of

credit. All credits issued subject to UCP 600 are irrevocable unless otherwise

agreed between the parties.

Irrevocable Letters of Credit

Irrevocable Letters of Credit cannot be amended or cancelled without the

agreement of the credit parties. Unconfirmed irrevocable letters of credit cannot

be modified without the written consent of both the issuing bank and the

beneficiary. Confirmed irrevocable letters of credit need also confirming bank's

written consent in order any modification or cancellation to be effective.

Types of Letters of Credit - Page II

This is the second page of types of letters of credit.

Unconfirmed Letters of Credit

Unconfirmed Letters of Credit can be described as a letter of credit, which has

not been guaranteed or confirmed by any bank other than the bank that opened

it. In these types of credits, the only bank that undertakes to honor a complying

presentation is the issuing bank.

Confirmed Letters of Credit It would be easier to understand the confirmed letters of credit if we start from the definition of the confirmation. Confirmation means a definite undertaking of the confirming bank, in addition tothat of the issuing bank, to honor or negotiate a complying presentation. If a letter of credit's payment undertaking is guaranteed by a second bank, in addition to the bank originally issuing the credit this kind of credit is called confirmed letter of credit. The confirming bank agrees to pay or accept drafts against the credit even if the issuer refuses to do so. Only irrevocable credits can be confirmed.

Clean Letters of Credit :Below two different definitions of clean letters of credit are given.

A letter of credit payable upon presentation of the draft, without any supporting

document being required.(www.businessdictionary.com)

L/C that does not require any document other than a written demand for

payment by its beneficiary. In effect, a draft.(www.intracen.org)

Clean letters of credit are issued only by the request of the highest credit

standing companies. It is suitable for variety commercial situations where no

movement of goods is expected. Historically these types of credits have been

used in traveler's letters of credit. Today direct pay standby letter of credit can

be given as an example of clean letters of credit.

There are also some other form of letters of credits which deserve special

attention. We will discuss them by one by more in detail however; you can find

short description of each of them below.

Transferable Letters of Credit Transferable letter of credit is a documentary credit that is issued with the option to allow a trader to transfer its rights and obligations to the supplier. Back-to-Back Letters of Credit Arrangement in which one irrevocable letter of credit serves as the collateral for

another; the advising bank of the first letter of credit becomes the issuing bank

of the second L/C. Unlike transferable letters of credit, there are two separate

letter of credits exist in back-to-back letter of credit transactions.

Advance Payment (Red Clause) Letters of Credit

Letter of credit that carries a provision (traditionally written or typed in red ink)

which allows a seller to draw up to a fixed sum from the advising or paying-

bank, in advance of the shipment or before presenting the prescribed

documents.

Parties to Letters of Credit

This page dels with the parties of the letter of credit.

Main parties of Letter of Credit transaction such as

applicant,

beneficiary,

issuing bank,

confirming bank,

nominated bank,

will be disscussed in this article.

Applicant Applicant is the buyer of the goods or services supplied by the seller. Letter of

credit is opened by the issuing bank as per applicant's request. However,

applicant does not belong one of the parties to a letter of credit transaction. This

is because of the fact that letters of credit are separate transactions from the

sale or other contract on which they may be based.

Beneficiary

Beneficiary is the seller of the goods or the provider of the services in a standard

commercial letter of credit transaction. Letter of credit is opened by the issuing

bank in favor of the beneficiary.

Issuing Bank Issuing Bank is the bank that issues a letter of credit at the request of an

applicant or its own behalf. Issuing bank undertakes to honor a complying

presentation of the beneficiary without recourse.

Nominated Bank Nominated bank is the bank with which the credit is available or any bank in the

case of a credit available with any bank.

Advising Bank Advising bank is the bank that advises the credit at the request of the issuing

bank. An advising bank that is not a confirming bank advises the credit and any

amendmend without any obligation to honor.

Confirming Bank Confirming bank is the bank that adds its confirmation to a credit upon the

issuing bank's authorization or request. Confirming bank may or may not add its

confirmation to a letter of credit. This decision is up to confirming bank only.

However, once it adds its confirmation to the credit confirming is irrevocably

bound to honor or negotiate as of the time it adds its confirmation to the credit.

Even if the issuing bank fails to honor, confirming bank must pay to the

beneficiary.

Reimbursing Bank Reimbursing Bank shall mean the bank instructed and/or authorized to provide

reimbursement pursuant to a reimbursement authorization issued by the issuing

bank.

Risks in Letters of Credit

What are the risks in a letter of credit transaction? Risks in letters of Credit

Although letters of credit are a balanced payment method in terms of risk issues

for both exporters and importers, each letters of credit party bears some

amount of risk. As we have explained before letters of credit transactions are

handled by banks. This responsibility makes the banks one of the parties that

bears risks in a letter of credit transaction.

What are the risks of the letters of credit which are payable with 90% at sight and 10% usance after consignee accepts the quality of goods?

Risks in letters of credit can be discussed under four groups; general risks in

letters of credit, risks to the applicant, risks to the beneficiary and risks to the

banks.

General Risks in Letters of Credit:

Country Risk: (Political Risk)

The first risk factor that can be mentioned in the general risks group is the

country risk or the political risk. Let us assume that we are an exporter located

in a country X and we have a customer from the country Y. Our customer, which

is from the country Y, opened a L/C in favor of us. We have checked the L/C

conditions and they seem workable. We have produced and shipped the order as

per the L/C and transmit the required documents to the issuing bank before the

expiry date. The issuing bank found our presentation complying and informed us

that they will be honoring our payment claim at the maturity date. However,

before the maturity date due Country Y has changed its export regime, which

makes it impossible for the issuing bank to honor our presentation. This

illustrative is a good example of a country risks. Other examples of country risks

are mass riots, civil war, boycott, sovereign risk and transfer risk.

Fraud Risk:

As we have described before all conditions stated in a letter of credit must be

connected to a document, otherwise banks will disregard such a condition. In

addition, banks deal with only documents but not goods, services or

performance to which the documents may relate. This feature of the letters of

credit is the source of the fraud risk at the same time. As an example, a

beneficiary of a certain letter of credit transaction can prepare fake documents,

which looks complying on their face, to make the presentation to the issuing

bank. As the documents are complying on their face, the issuing bank may

honor the presentation and in this case, the applicant must pay to the issuing

bank for the goods it will never be receiving. Beneficiaries of L/Cs bear also

fraud risks. This happens if an applicant issues a counterfeit letter of credit. In

this case, the beneficiary never receives its payment for the goods it has

shipped.

Risks to the Applicant:

In a letter of credit transaction, main risk factors for the applicants are non-

delivery, goods received with inferior quality, exchange rate risk and the issuing

bank's bankruptcy risk.

Risks to the Beneficiary:

In a letter of credit transaction, main risk factors for the beneficiaries are unable

to comply with letter of credit conditions, counterfeit L/C, issuing bank's failure

risk and issuing bank's country risk.

Risks to the Banks:

Every bank in a L/C transaction bears risks more or less. The risk amount

increases as responsibility of the bank increases.

Basic Letter of Credit Transaction

How letters of credit work in international trade? Commercial letter of credit transaction in simple language.

Understanding Letter of Credit Transaction

On this page I will try to explain you letter of credit process in a very simple way.

After reading this article you should understand the working mechanism of letter

of credit payment in general terms.

1. The starting point of the letter of credit process is the agreement upon the

sales terms between the exporter and the importer. Then they sign a sales

contract. It is important to stress here that letters of credit are not a sales

contract. Actually, letters of credit are independent structures from the sale or

other contract on which they may be based. Therefore, it should be kept in mind

that a good sales contract protects the party, which behaves in goodwill against

various kinds of risks.

2. After the sales contract has been signed, the importer (applicant) applies for

its bank to issue a letter of credit. The letter of credit application must be in

accordance with the terms of the sales agreement.

3. If the importer and its bank reach an agreement together on the working

conditions the importer's bank (issuing bank) issues its letter of credit. In case

the issuing bank and the exporter (beneficiary) are located at different

countries, the issuing bank may use another bank's services (advising bank) to

advise the credit to the beneficiary.

4. The advising bank advises the letter of credit to the beneficiary without any

undertaking to honor or negotiate. The advising bank has two responsibilities

against to the beneficiary. Advising bank's first responsibility is satisfy itself as to

the apparent authenticity of the credit and its second responsibility is to make

sure that the advice accurately reflects the terms and conditions of the credit

received.

5. The beneficiary should check the conditions of the credit as soon as it is

received from the advising bank. If some disparities have been detected

beneficiary should inform the applicant about these points and demand an

amendment. If letter of credit conditions seem reasonable to the beneficiary

then beneficiary starts producing the goods in order to make the shipment on or

before the latest shipment date stated in the L/C. The beneficiary ships the

order according to the terms and conditions stated in the credit.

6. When the goods are loaded, the exporter collects the documents, which are

requested by the credit and forwards them to the advising bank.

7. The advising bank posts the documents to the issuing bank on behalf of the

beneficiary.

8&9. The issuing bank checks the documents according to the terms and

conditions of the credit. In addition, the governing rules, which are mostly latest

version of the UCP are taken into account. If the documents are found complying

after the examination the issuing bank honors the payment claim.

10. The documents transmit to the applicant. The applicant uses these

documents to clear the goods from the customs.

Availability of Letters of Credit A credit must state whether it is available by sight payment, deferred payment, acceptance or negotiation. (UCP 600 - Article 6- b)

What does availability mean in a letter of credit

transaction?

In documentary credit terminology, availability refers to the availability of the

documents in exchange for the payment of the amount stated in the letter of

credit. UCP 600 defines four availability options ;

Sight Payment : Sight payment refers to the payment which is made as soon

as the complying presentation is seen by the issuing bank or the bank

nominated in the letter of credit. The nominated bank fulfills its payment

obligation with recourse basis. Nominated bank can demand the amount paid to

the beneficiary back in case of documents are found noncomplying by the

issuing bank. Nominated bank's payment obligation is not strict as the issuing or

the confirming bank's payment obligation. UCP 600 states that a nominated

bank is not obligated to accept the nomination directed to itself unless

nominated bank inform its acceptance of nomination expressly to the

beneficiary. Even in this situation UCP 600 assumes non payment by the

nominated bank and describe the roles of the issuing and confirming banks.

Deferred Payment : Deferred payment refers to the payment which is made

after a period of time that is specified also in the letter of credit. The payment

period is usually determined as specific number of days after the date of

presentation or the date of the transport document. Bill of exchange or draft is

not required under deferred payment.

Acceptance : Acceptance refers to acceptance of a bill of exchange which is

drawn on the bank mentioned in the letter of credit to be presented with the

other required documents and payment at the maturity.

Negotiation : Let us check the definition of the negotiation from the UCP 600 in

order to understand the term more clearly.

Negotiation means the purchase by the nominated bank of drafts (drawn on a

bank other than the nominated bank) and/or documents under a complying

presentation, by advancing or agreeing to advance funds to the beneficiary on

or before the banking day on which reimbursement is due to the nominated

bank. (UCP 600 - Article 2)

As can be seen from the above definition any letter of credit which is available

by negotiation could be issued in a way so that a draft may or may not be

required. Also the payment of the letter of credit may or may not be at sight. If

the nominated bank advance or agreeing to advance funds to the beneficiary

before it receives reimbursement from the issuing bank the negotiation

condition is fulfilled. This can happen in two ways. First possibility is, in a letter

of credit which is available by sight payment when the nominated bank

reimburse the beneficiary before it receives funds from the issuing bank. Second

possibility occurs when a letter of credit is available by negotiation requesting

presentation of a time draft, while the nominated bank reimburses the

beneficiary before the maturity date of the bill of exchange. (How does a

negotiable letter of credit work?)

When issuing a documentary credit via swift message banks show the

availability of a documentary credit in Field 41a.

MT 700 Issue of a Documentary Credit

Field 41a: Available With ... By ...

BY ACCEPTANCE

BY DEF PAYMENT

BY MIXED PYMT

BY NEGOTIATION

BY PAYMENT

Payment means payment at sight. Mixed payment is not directly covered under

UCP 600.

Confirmation and Confirmed Letter of Credit

What is confirmation in a letter of credit transaction? What

are the benefits of a confirmed lc?

Confirmation is a security tool for the exporters. Confirmation eliminates country

risk and insolvensy risk of the issuing bank.

How to add confirmation to a letter of credit?

How to add confirmation to a letter of credit? Confirmation gives additional payment guarantee to the exporters. On this

page you can find letter of credit confirmation process which is explained

with the help of a graphic illustration.

Figure 1 : Step by step explanation of letter of credit confirmationprocess.

Step 1 - Sale Contract: Exporter and Importer sign a sale contract. They

choose letter of credit as a payment method.

Step 2 - Confirmation Request on Sale Contract: On the sale

contract exporter demand from the importer that the letter of credit must

be confirmed. Exporters may want the credit to be confirmed by a bank

which is acceptable for them. In order to make sure that the credit would

not be confirmed by another bank which is not suitable for the exporter,

exporters should indicate this on the sale contract with a wording similar

stated bellows: "The documentary letter of credit should be issued in a

way so that it can be confirmed by a bank acceptable to the exporter".

Step 3 - Letter of Credit Application: Importer applies to his bank to

open the letter of credit.

Step 4 - Letter of Credit Issuance: Issuing bank issues the letter of

credit. The letter of credit must include "May Add" or "Confirm" codes in

field "Field 49: Confirmation Instructions".

Step 5 - Confirmation: Advising bank or another bank that the

beneficiary wants to have the letter of credit confirmed discuss the terms

and conditions of the confirmation. If both parties agree on the

confirmation conditions than the letter of credit will be confirmed.

Confirming bank should inform to the beneficiary that it has included its

confirmation to the letter of credit.

5 Things You Should Never Do When Working with a Letter of Credit for the First Time :

Do you know the most biggest mistakes that exporters do when

working with a letter of credit for the first time?

5 Things You Should Never Do When Working with a Letter of Credit for the First

Time, titled article is written by Ozgur Eker. You can find important failure points

for unexperienced exporters.

Most of the times letter of credit is not the first payment option for

exporters and importers. Exporters and importers tend to choose other

payment options such as cash against document, advance payment or

mixed payments over letters of credit. But as situation dictates foreign

traders have to use letter of credit in international trade transactions. On

this article I would like to explain 5 most costly mistakes that exporters

repeatedly make in their lc operations.

Most costly mistake 1 : Doing a business with an importer to whom

you have no real information...

Business is not a virtual thing. You should have a real knowledge about

your counter party before starting to do any kind of transaction. I have

seen a lot of exporters who tried to finish a transaction without having a

decent information about their buyers by just trusting a letter of credit.

Letter of credit does not protect you against any immoral buyer.

Please answer below questions to understand how much you know about

your buyer.

Table 1 : Customer questionnaire

How much do you know about your buyer?

Did I find this customer from a trade exhibition or a customervisit?

Yes No

Does my customer have any proven business relationship in my sector?

Yes No

Does my customer visit me before the business was initiated?

Yes No

Is there any positive feedback that I have gathered about mycustomer?

Yes No

Does transaction doable in regards to my buyer's perpective?

Yes No

If you can not answer "yes" to all of these questions immediately, than

you should be starting to re-think about the whole business. If you

answered more than 1 question negatively, than you should be very

careful about the trade transaction in terms of risk issues.

Most costly mistake 2 : entering business offers which are too

good to be true...

In most cases scammers seduce exporters with unbelievable proposals. They

do not bargain for the prices, they order big quantities, they promise to pay

"at sight" not "usance" terms. As a buyer if you do not intend to pay anything

than sky would be the limit for you. You can propose whatever you think

would be necessary to seal the deal. These proposals can be sum up as "too

good to be true" type business offers. If you meet a buyer one day who is

promising very favorable conditions to you, please keep in mind that you

might be loosing money at the end.

Most costly mistake 3 : underestimating risk factors associated

with the transaction

Businesses turn around on risk and profit axis, more you take risks, more you

can get profit. But some exporters lost their common sense and take too

much risks to make more profit in a short perod of time. This behavior

associated with an extreme risk taking behavior. However normally you

have to understand your risks very well before signing any contract with your

buyer. Than you should take preventive steps to reduce each risk level to

acceptable degrees. If you would like to learn more about risk factors in a

letter of credit transaction please follow this link.

Most costly mistake 4 : "I can do it in my way" perception...

Letters of credit are different than other payment methods in international

trade in terms of flexibility. Banks play a key role on lc transactions. Letter

of credit rules are strictly followed by banks. As a result you have to

prepare required documents as per credit terms, latest letter of credit

rules and standard banking practices. Otherwise you can not get your

payment under a letter of credit.

Most costly mistake 5 : lack of knowledge...As I have mentioned above letter of credit transactions are governed by

one of the most complicated rules of whole international trade practices.

In order to complete a letter of transaction without experiencing a

negative result, you need to understand how logistics, finance and

governmental procedures work very well. Also you need to be very careful

when reading the credit terms and conditions. You have to note down

every detail and clarify each point that can not be understood openly. Do

not be shy asking questions to issuing bank or confirming bank to

comprehend the credit.

Summary :

1 Learn who your buyer is. Try to get references of your buyer from your

sector. If needed make a financial investigation.

1 Be careful about too good business opportunities. Be aware of scammers.

1 Understand risk factors associated with your transaction

1 Accept the fact that letter of credit is not flexible in terms of regulations.

1 Learn the rules. Read the credit well. Eliminate all gray areas.

Confirmed L/C at Sight

Understanding the benefits of confirmed lc at sight.

What are the benefits of at sight confirmed letter of credit?

At sight payment is one of the payment terms in a letter of credit transaction.

Also confirmation means "a definite undertaking of the confirming bank , in

addition to that of the issuing bank, to honour or negotiate a complying

presentation" according to latest UCP rules.

UCP 600 defines four availability options ; A credit must state whether it is

available by sight payment, deferred payment, acceptance or negotiation (UCP

600 - Article 6- b). At sight payment is one of the payment terms in a letter of

credit transaction. Also confirmation means "a definite undertaking of the

confirming bank , in addition to that of the issuing bank, to honour or negotiate

a complying presentation" according to latest UCP rules. On this page I would

like to write about pros and cons of confirmation when letter of credit

is available with sight payment (l/c at sight)

Let us start by asking ourself a very simple question. Why sellers pay additional

money to have their L/Cs confirmed? The first reason is that sellers would like to

eliminate default risk of the issuing bank. Second reason is that they would like

to receive their payment sooner by removing the issuing bank out of the

equation.

Most of the small companies work with limited capital volume and they rely on

their suppliers credit terms such as 30 days after bill of lading date. Which

means that a seller have to pay to its supplier 30 days after he ships the goods.

This relatively short time could create problems in terms of cash flow, when we

take into account document examination period of 5 working day that each bank

has to examine the documents under a letter of credit presentation.

Confirmation would be a great solution for this problem. Under

unconfirmed letters of credit nominated banks in most cases send documents to

issuing banks and wait reimbursement. Nominated banks pay to the sellers only

after they have been reimbursed by the issuing banks. This is a relatively long

period of time and could exceed 30 days time allowance that sellers have to pay

to their suppliers.

Nomimated banks keep sending documents to issuing banks and wait

for reimbursement even under confirmed letters of credit. Unfortunately

confirmation couldn't eliminate the wait for reimbursement! Confirming banks

should pay against credits they confirmed without receiving reimbursement. But

in practice they pay without waiting reimbursement only when they have

determined that the issuing bank defaulted. Further, confirming banks unable to

tell us how long it might take to determine that the issuing bank had

defaulted! This is another example where theory does not match the

practice. UCP 600 sub-Article 8(a) clear enough. I will qoute related articles

from UCP 600 belows,

Article 8 - Confirming Bank Undertaking

a. Provided that the stipulated documents are presented to the confirming bank

or to any other nominated bank and that they constitute a complying

presentation, the confirming bank must:

i. honour, if the credit is available by

a. sight payment, deferred payment or acceptance with the confirming bank; ..."

I am asking now a simple question to banks, if you do not honour your

confirmation as per UCP rules why are you adding your confirmation to

lcs and charging confirmation cost to sellers?

What is Field 49: Confirmation Instructions?Field 49: Confirmation Instructions is a field in MT 700 swift message type that contains confirmation instructions for the Receiver.

Field 49: Confirmation Instructions :

This field contains confirmation instructions for the Receiver.

According to current letter of credit rules confirmation means a definite

undertaking of the confirming bank, in addition to that of the issuing bank,

to honour or negotiate a complying presentation.

According to current letter of credit rules confirming bank means the bank

that adds its confirmation to a credit upon the issuing bank's authorization

or request. As a result banks can not add their confirmations to the letter

of credit without having a confirmation request by the issuing banks.

According to current letter of credit rules a confirming bank is irrevocably

bound to honour or negotiate as of the time it adds its confirmation to the

credit.

Sample Field 49: Confirmation Instructions

MT 700

Field 49: Confirmation Instructions :

DEFINITION

This field contains confirmation instructions for the Receiver.

CODES

One of the following codes must be used.

CONFIRM The Receiver is requested to confirm the credit.

MAY ADD The Receiver may add its confirmation to the credit.

WITHOUT The Receiver is not requested to confirm the credit.

letterofcredit.biz is your gateway to International Trade Finance World designed &developed by a Certified Documentary Credit Specialist.

Most Recent ArticlesMust Read Articles

TradeFinanceForum.com

Join Trade Finance Forum Now.

Questions & Answers

How to Work with Letters of Credit

Case Studies and Examples

Must Read Articles

Most Recent Articles

Field 49: Confirmation Instructions :

This field contains confirmation instructions for the Receiver.

According to current letter of credit rules confirmation means a definite

undertaking of the confirming bank, in addition to that of the issuing bank,

to honour or negotiate a complying presentation.

According to current letter of credit rules confirming bank means the bank

that adds its confirmation to a credit upon the issuing bank's authorization

or request. As a result banks can not add their confirmations to the letter

of credit without having a confirmation request by the issuing banks.

According to current letter of credit rules a confirming bank is irrevocably

bound to honour or negotiate as of the time it adds its confirmation to the

credit.

Sample Field 49: Confirmation Instructions

MT 700

Field 49: Confirmation Instructions :

DEFINITION

This field contains confirmation instructions for the Receiver.

CODES

One of the following codes must be used.

CONFIRM The Receiver is requested to confirm the credit.

MAY ADD The Receiver may add its confirmation to the credit.

WITHOUT The Receiver is not requested to confirm the credit.

Keywords :Field 49: Confirmation Instructions , mt 700 swift, Standards MT Messages

Implementation Guidelines - Swift, SWIFT MT700 codes, SWIFTStandards - Category 7 -

Documentary Credits, What is swift mt 700 in banking, MT 700 sender definately is a LC issuing

bank, MT 700 Series, Complete MT700, MT700 codes, Mt700 swift format in doc, MT700 or MT760

or ISO 20022

Confirmation fees

Confirmation Fee

What is confirmaton fee?

Confirmation fee can be defined as charges collected by the confirming banks

against the risks they will be having to posses by confirming the letters of

credit. As I have explained below confirming banks undertake two main risk

factors with the confirmation: default risk of the issuing bank and political

risk of the issuing bank’s country.

Confirmation of a letter of credit is defined as an undertaking from a bank in

addition to the undertaking provided to the beneficiary by the issuing bank.

Beneficiary would like to eliminate the default risk of the issuing bank as well as

political risk by having the letter of credit confirmed to a bank which is located

within the same country.

Confirming banks could only honour or negotiate a complying presentation. As a

result beneficiaries have to present complying documents in order to obtain

funds under letters of credit from either the issuing bank or the confirming bank.

For this reason complying presentation is the key for the payment for both

confirmed letters of credit and unconfirmed letters of credit.

Confirming banks take the default risk of the issuing bank as well as non-

payment risk of the letter of credit originated from the political risk of the

issuing bank’s country over themselves from the moment they have added their

confirmation to the letters of credit. Even if a confirming bank could not receive

any reimbursement from the issuing bank he has to make payment to the

beneficiary against a complying presentation under the letter of credit which he

has confirmed.

You might be wondering why a confirming bank would take such risks and

confirm a letter of credit. The correct answer is very simple and straight forward;

to make more profit.

Examples of Confirmation Fees:

Confirmation Fee Format 1: Exporters First Help Bank of New York confirms this

credit and hereby undertakes to honor all drafts and documents presented in

strict compliance with the credit terms. Our confirmation charges USD3.120,48.

Confirmation Fee Format 2: We shall charge our confirmation commission of

4,000000 PCT p.a., min. EUR200.00 p.q.

p.a. : per annum (12 months or 360 days)

p.q. : per quarter (3 months)

Who should pay confirmation fees?

According to letter of credit rules all fees and charges related to credits should

be paid by the applicants. But we have learned long ago that this perfect world

indication is not valid under real life situations. In most cases applicants pay

only letter of credit issuance charges and let the banks collect all the remaining

fees from the beneficiaries. As a result confirmation fees will be paid by the

beneficiaries in most cases.

What happens if court stops payment of an irrevocable, confirmed letter of credit which is payable 90 days after sight due to low quality of goods?

What happens if court stops payment of an irrevocable, confirmed letter of credit which

is payable 90 days after sight due to low quality of goods?

In many countries letter of credit applicants able to prevent payment by

obtaining court orders forcing issuing banks from paying demands under their

letters of credit on the grounds of low quality goods shipment or fraud. Often

courts issue a temporary or preliminary injunction. On this case scenario we

demonstrate a court order that stops payment of an irrevocable confirmed

deferred payment letter of credit.

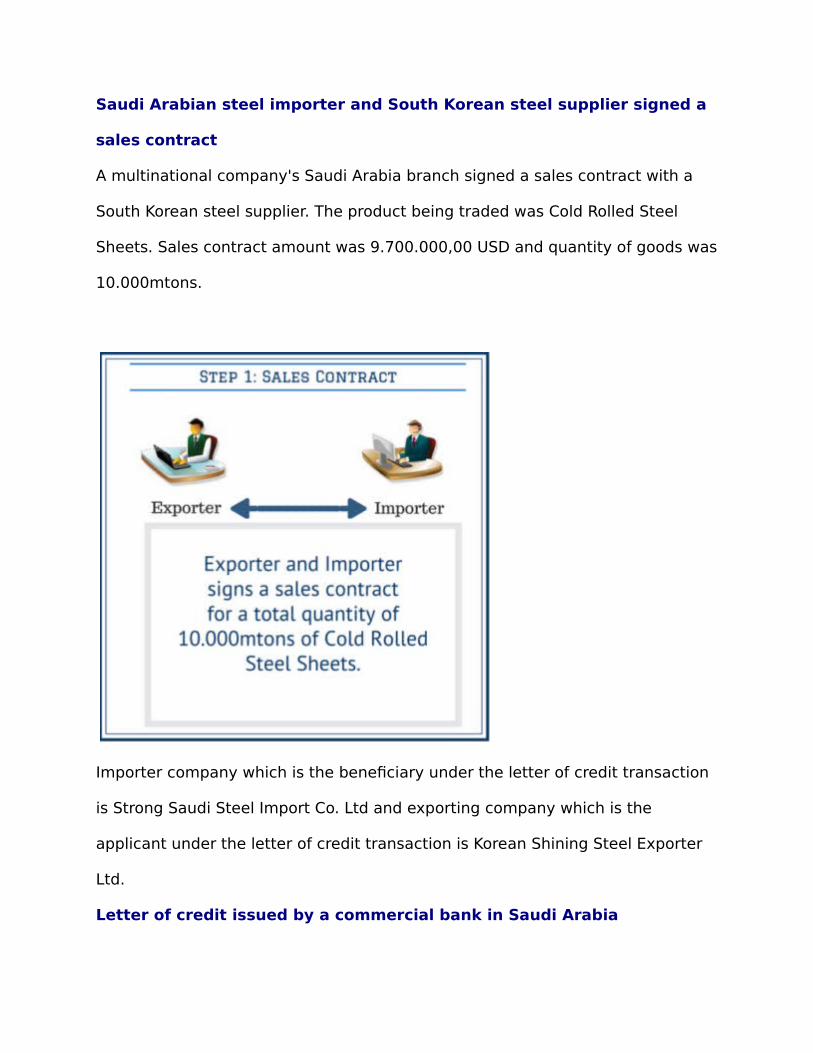

Saudi Arabian steel importer and South Korean steel supplier signed a

sales contract

A multinational company's Saudi Arabia branch signed a sales contract with a

South Korean steel supplier. The product being traded was Cold Rolled Steel

Sheets. Sales contract amount was 9.700.000,00 USD and quantity of goods was

10.000mtons.

Importer company which is the beneficiary under the letter of credit transaction

is Strong Saudi Steel Import Co. Ltd and exporting company which is the

applicant under the letter of credit transaction is Korean Shining Steel Exporter

Ltd.

Letter of credit issued by a commercial bank in Saudi Arabia

A Saudi Arabian commercial bank issued the letter of credit which is available by

a deferred payment payable 90 days after sight. Letter of credit is subject to

UCP 600 and it is irrevocable. Letter of credit is available with a South Korean

national commercial bank. Also issuing bank requested from the nominated

bank to confirm the credit.

You can find important details of the letter of credit on below MT 700 swift

message summary.

MT 700 Swift Message Summary----------------------- Message Header ---------------------------------Swift OUTPUT FIN 700 Issue of a Documentary CreditSender : ARABBANKSKSA SAUDI ARABIAN BANK (COMMERCIAL BRANCH) JEDDAH KSA

Receiver : TRADEBANKXXX

SOUTH KOREAN TRADE BANK (ALL SOUTH KOREAN OFFICES) SEOUL KR

40E: Applicable Rules

UCP LATEST VERSION

31D: Date and Place of Expiry

130106-SOUTH KOREA

50: Applicant

STRONG SAUDI STEEL IMPORT CO. LTD.

P.O. BOX 30000, JEDDAH

KINGDOM OF SAUDI ARABIA

59: Beneficiary - Name & Address

KOREAN SHINING STEEL EXPORTER LTD

(FULL BENEFS. NAME AND ADDRESS UNDER FIELD 47A ITEM NO.2)

32B: Currency Code, Amount

Currency : USD (US DOLLAR)

Amount : #9.700.000,00#

39B: Maximum Credit Amount

NOT EXCEEDING

41A: Available With...By... - BIC

TRADEBANKXXX

BY DEF PAYMENT

42P: Deferred Payment Details

90 DAYS AFTER SIGHT

49: Confirmation Instructions

CONFIRM

Letter of credit confirmed by South Korean Bank

South Korean bank, which was initially the nominated bank, confirmed the letter

of credit as per instructions received from the issuing bank. Once South Korean

bank confirmed the letter of credit, it became the confirming bank.

Under UCP 600 rules confirming banks have to honor complying presentations.

Confirming banks can also discount letters of credit upon exporters’ demand.

Complying presentation

After having the letter of credit confirmed, exporter arranged the shipment and

made the presentation to the South Korean Bank which is not only the

nominated bank but also the confirming bank.

Confirming bank checked the documents and found them complying. Confirming

bank determined that the documents have been presented was free of errors.

Confirming bank sent the documents to the issuing bank.

The issuing bank also confirmed, by an authenticated swift message

that, the acceptance of documents and the remittance of funds with a

value maturity date.

As it was mentioned earlier, the letter of credit is payable with a deferred

payment which is 90 days after sight. The exporter applied to the confirming

bank to discount the credit in order to get the payment in advance of the

maturity date of the credit.

Letter of credit discounted by South Korean confirming bank

Confirming bank and the exporter agreed on the terms and conditions of the

letter of credit discount and confirming bank negotiated the credit without

recourse basis. The confirming bank purchased the deferred payment

undertaking resulting from documents presented in full conformity with the

terms and conditions of the letter of credit and effected payment to the

beneficiary.

One week before the maturity date, the issuing bank informed the confirming

that the letter of credit payment has been stopped by the court order. In this

regards the issuing bank sent two subsequent authenticated SWIFT messages to

the confirming bank as follows:

MT 799 Swift Message Summary

On 18.February.2013, the following swift message was sent by confirming bank

to the issuing bank, which explained the objections of the confirming bank to the

court order and the issuing bank's standing.

"Please kindly be informed that we would like to draw your attention to the

following facts:

1.The Court Order dd. 15.February.2013 of the Court of First Instance is

addressed to your bank, in order to proceed with the suspension of payment

according to the instructions of applicant of L/C. This court order forbids your

payment to be effected to the beneficiary.

2.According to Art. 7c of the UCP 600 of ICC

a) your bank is obliged to reimburse the nominated bank, i.e. confirming bank,

at maturity

b) your undertaking to reimburse us is independent of your undertaking to the

beneficiary

3. According to Art. 12b of the UCP 600, you authorized us to prepay or purchase

a deferred payment undertaking incurred by us

4. As you are aware we prepaid the deferred payment undertaking to the

beneficiary.

As a matter of fact we, confirming bank, are the owner of the receivables and

entitled to receive the counter-value without any further delay. Summarizing the

above, we regard you as a highly reputable bank with an excellent standing and

experience in the international business, including documentary credits, and

thus anticipate your assistance in solving the pending problem by appealing

against the court order and to immediately remit funds in favour of our bank."

Issuing bank remained unanswered confirming bank's swift messages.

The confirming bank believed that the issuing bank is obliged to honour the

nominated bank's reimbursement claim immediately upon maturity, even if a

court order issued against the issuing bank prohibits payment to the beneficiary.

As the issuing bank remained silence the confirming bank applied to the ICC

banking commission for an opinion.

Conclusion:

ICC banking commission states that local law will prevail over the letter of credit

transaction. As a result banks must act according to court orders.

However, the credit was subject to UCP 600 and apparently contained no

exclusion to the rule appearing in sub-article 12 (b). Due to the content of sub-

article 12 (b) and sub-article 7 (c), the issuing bank should seek to resist such an

injunction in order to preserve the integrity of its credit and the UCP. It must be

expected that the issuing bank will seek to have the injunction removed by

referring the court to the appropriate articles of UCP 600 and the terms and

conditions of the credit. The issuing bank would also be well advised to inform

its applicant(s) of the content and effect of sub-article 12 (b) for this and any

future transactions. It is the responsibility of the applicant to cover any issues

concerning quality of goods in the documents called for and the data content

required to appear on those documents, and not to seek redress that affects the

right of a nominated bank to receive reimbursement in respect of a complying

presentation.

This case study created by the author based on the informations gathered from ICC Opinion R629

/ TA672rev.

Author:

Ozgur Eker is an independent trade finance consultant based in Izmir, Turkey.

He has been 10+ years of experience in international trade finance field. He is

also the founder of letterofcredit.biz.

As we have discussed earlier there are some risk factors exist for each party in a

letter of credit transaction. When we look at the risk issue from the beneficiaries'

perspective, we will observe two main risk factors that beneficiaries must bear ;

the country and the insolvency risk of the issuing bank. Confirmation can be

seen as a security mechanism which works in favour of the beneficiaries that

eliminates these two risk factors.

Let us look at the definitions of confirmation and confirming bank from the UCP

600 ;

"Confirmation means a definite undertaking of the confirming bank , in addition

to that of the issuing bank, to honour or negotiate a complying presentation."

"Confirming bank means the bank that adds its confirmation to a credit upon the

issuing bank's authorization or request."

As can be seen on the above definitions confirming bank adds its undertaking to

the letter of credit in addition to that of the issuing bank. In this way

beneficiaries receive a second payment guarantee from another bank.

Insolvency risk of the issuing bank is eliminated by addition of this second

payment guarantee to the letter of credit.

Mostly confirming banks and the beneficiaries are located in the same country

and when this is the case the country risk of the issuing bank is eliminated as a

bank which locates in the same country with the beneficiary adds its

undertaking to the letter of credit in addition to that of the issuing bank.

Confirmed Letter of Credit

After discussing the benefits of the confirmation in a letter of credit transaction,

let us examine the points that need to be take into consideration regarding the

confirmed letters of credit.

Only irrevocable letters of credit can be confirmed.

During the issuance phase of a letter of credit, the issuing bank should

"authorize or request" the potential confirming bank to add its

confirmation to the letter of credit.

No bank can be forced to add its confirmation to any letter of credit.

If a bank is authorized or requested by the issuing bank to confirm a credit

but is not prepared to do so, it must inform the issuing bank without delay

and may advise the credit without confirmation. (UCP 600 article 8 ii-d)

Confirming a letter of credit does not mean that confirming bank is

obligated to confirm any subsequent amendment or amendments.

A confirming bank is irrevocably bound to honour or negotiate as of the

time it adds its confirmation to the letter of credit. (UCP 600 article 8 ii-b )

Letter of Credit FeesHow to deal with high banking commissions under letters of credit as an

exporter?

Who pays letters of credit fees? Letters of credit have certain advantages asan international payment method. If you have enough knowledge and expertise on letters of credit field then you can use them wisely to get paid where no

http://www.letterofcredit.biz/How-to-deal-with-high-banking-commissions-under-letters-of-credit.html

other payment method works. No matter how many advantages letters of credit have they have one big disadvantage. They are expensive.

As a result you should understand your costs before finalizing a letter of credit

deal.

Why letters of credit are expensive comparing to other payment

methods?

Banks play a key role in letters of credit transactions. This is the main reason

why letters of credit are so expensive comparing to other payment

methods. Issuing banks open letters of credit for the account of applicants

and in favor of the beneficiaries. Issuing banks have to bear certain amount of

risks when they open letters of credit. They also let the applicants benefited

from their credit worthiness. As a commercial institution issuing banks provide

these services only for one reason. To earn more money, to make more

profit. Similarly confirming banks collect fees from the letter of credit parties

for the same reason. When confirming a letter of credit confirming banks may

have to bear substantial amount of non-payment risk. As a result

confirmation fees can sometimes climb to high values. As we have learnt that in

a typical letter of credit transaction there are other banks may exist in addition

to issuing bank and confirming bank such as advising bank, nominated

bank, reimbursing bank. Every additional bank means additional fees and

additional cost for either applicants or beneficiaries.

Who should pay bank charges in a letter of credit transaction?

We can answer this question by either looking at the rules or by looking at the

real life situations because what rules say is not what is really happening on

practice.

UCP 600's article related to charges of letters of credit is article 37 c: "A

bank instructing another bank to perform services is liable for any

commissions, fees, costs or expenses ("charges") incurred by that bank in

connection with its instructions. If a credit states that charges are for the

account of the beneficiary and charges cannot be collected or deducted

from proceeds, the issuing bank remains liable for payment of charges."

In real life situations applicant pay only issuing bank's charges and

remaining bank charges will be paid by the beneficiary unless beneficiary

is very strong against applicant. We need to look at field "71B: Charges"

in a letter of credit text issued by swift format to understand how bank

charges will be paid by letter of credit parties.

Samples :

o Issuing bank charges will be paid by applicant and all other cherges will

be paid by beneficiary : Field "71B: Charges : ALL BANKING CHARGES

OUTSIDE BRAZIL ARE FOR BENEFICIARY'S ACCOUNT." This letter of credit

issued by a Brazilian bank.

o Field "71B : Charges and Fees: OTHER THAN THE ISSUING BANKS ARE

FOR THE ACCOUNT OF THE BENEFICIARY. ISSUING BANK’S CHARGES ARE

FOR THE ACCOUNT OF THE APPLICANT."

Discrepancies : Biggest trouble for everyone in lc business

What does discrepancy mean in a letter of credit payment? How can

discrepancy be defined under a letter of credit transaction?

Perhaps discrepancies is one of the most complicated and "blurred" field in all

letters of credit terminology. One bank finds multiple discrepancies on a

document yet the same document found to be complying by another bank. But

how?

Transport Document Discrepancies

Multimodal Bill of Lading Discrepancies

Marine Bill of Lading Discrepancies

Non Negotiable Sea Waybill Discrepancies

Charter Party Bill of Lading Discrepancies

Road Transport Document Discrepancies

Air Transport Document Discrepancies

Rail Transport Document Discrepancies

Commercial Document Discrepancies

Commercial Invoice Discrepancies

Packing List Discrepancies

Weight List Discrepancies

Inspection Certificate

Certificate of Analysis

Pre-Export Verification of Conformity (PVoC) Certificate

Official Document Discrepancies

Certificate of Origin Discrepancies

Health Certificate

Consular Invoice, Legalized Invoice

Insurance Document Discrepancies

Insurance Policy Discrepancies

Almost all of the ICC opinions issued so far are related to complaints about

"alleged discrepancies". What we can see from the results of the ICC opinions is

that ICC Banking Committee does not agree with banks in most cases.

Definition : or lack of definition :

How can we define a discrepancy in a letter of credit transaction. Seriously is

there any reference to the definition of a discrepancy in the letter of credit

rules? Is it too simple to be forgotten? Or too complicated to define? What is the

definition of a discrepancy according the UCP 600 rules?

Inconsistency in Application :

Discrepancies can change from country to country, bank to bank, document

checker to document checker. Let me give you a real life example here. Couple

of years ago we have presented documents to the confirming bank under a set

of letters of credit consists of 10-15 pcs of independent letters of credit. All of

these small amount independent letters of credit have the same text and having

the same conditions. Description of goods, port of loading, port of discharge,

additional conditions all were the same. Just latest date of shipment and expiry

date were changing form one lc to another. First 3 presentations found to be

complying by the confirming bank. But on the 4th document set we received a

swift message "MT 734 Advice of a Refusal" indicating a discrepancy on the

certificate of origin. Lessons learned. Discrepancies can change from country to

country, bank to bank, document checker to document checker and

presentation to presentation.

and here is the results :

According to ICC Trade Finance Surveys on average %70 of letter of credit

presentations found to be discrepant on first presentation. This is a very

frustrating result. Everyone in letter of credit business should understand huge

negative effects of such a high volume of discrepant presentations.

Why banks find too much discrepancies on the documents :

Letter of credit rules are often find to be very complicated and hard to

understand by exporters and importers.

Most of the small and medium scale export and import companies do not

have enough resources to hire a letter of credit specialist in their

organizations.

Exporters and importers do give enough respect to letter of credit rules

and standard banking practices. exporters and importers think that they

can handle letters of credit with ease on their way. but the fact is different.

Letters of credit have very strict rules to follow.

Exporters do not allocate enough time to understand the letter of credit

text before starting to production and shipment.

Banks open over detailed letters of credit. Sometimes we see that banks

demand almost impossible conditions from the beneficiaries on their

letters of credit texts.

Banks issue foggy (not clear) letters of credit.

Banks examine documents too strictly.

What can be done to prevent discrepant presentations :

Pre - Document Preparation Stage :

Please keep in mind that whatever you do to prevent a possible discrepant

presentation, it is highly likely that you will be facing a discrepancy one of

the documents you have submitted. So it would be very wise for you to

keep your relations close with your customer.

Before entering a letter of credit transaction you need to learn the letter

of credit rules very well. You should buy one original copy of current letter

of credit rule book, UCP 600. Please follow this link how to find a copy of

UCP 600 online.

Before entering a letter of credit transaction you also need to be

familiarized with the International Standard Banking Practices. In order to

do that you should buy one original copy of current International Standard

Banking Practices book. Please follow this link to learn more

about International Standard Banking Practices.

You should starting to study letter of credit text as early as you can. As

one of the letter of credit guru indicated "you can not solve lc problems at

the presentation stage." The earlier you start to work on the letter of

credit text the better it would be.

Demand a letter of credit draft from your buyer before having the original

letter of credit issued. Work on this letter of credit draft carefully.

Check required documents field one by one. Make sure that you can

supply all the required documents as requested by the letter of credit.

Check additional conditions field one by one. Make sure that conditions

stated in this field is not going to create any problem for you on the

presentation stage.

If you find a condition or clause that you can not comply with get in touch

with your buyer to amend the letter of credit.

If you can not understand a condition or sentence on the letter of credit

text then you should get in touch with the issuing bank for clarification.

Document Preparation Stage :

Complete the documents as requested by the credit. Make sure that you

also take into account the letter of credit rules and international standard

banking practices when preparing the documents.

Make sure that signatures, authentication are made by requested persons

or institutions.

Make sure that you will be presented all required documents without any

absence.

Make sure that you presented correct number of originals and copies as

requested by the credit.

Make sure that the dates on the documents are in accordance with the

dates mentioned on the credit. For example you would not be making

either a late shipment or a late presentation.

Make sure that you will collect all requested documents by credit as soon

as you make the shipment. Once you collect all documents you need to

make the presentation without losing time.

After Presentation Stage :

Follow the situation of the documents day by day with the advising bank. Give

necessary information to your buyer. And stay in alert mode until you received

your payment.