Lenders/ Guarantors/Servicers – Who Does What and When? Presented by: Gretchen Bonfardine...

29

Lenders/ Guarantors/Servicers – Who Does What and When? Presented by: Gretchen Bonfardine Professional Services Consultant

Transcript of Lenders/ Guarantors/Servicers – Who Does What and When? Presented by: Gretchen Bonfardine...

Lenders/ Guarantors/Servicers – Who Does What and When?

Presented by: Gretchen Bonfardine

Professional Services Consultant

• What is a lender?

• What is a guarantor?

• What is a servicer?

• What does each do – from certification through repayment

Objectives

• Which entity provides the funds? – Lender– Guarantor– Servicer

• Which entity manages deferments and forbearances?– Lender– Guarantor– Servicer

Quiz

• Which entity is responsible for default prevention activities? – Lender– Guarantor– Servicer

• Which entity has federal oversight over the FFEL program?– Lender– Guarantor– Servicer

Quiz

• Who is responsible for contacting borrowers during the grace period to provide repayment options?– Lender– Guarantor– Servicer

Quiz

PlayersLender / Servicer

•Lender must administer its loan portfolio in compliance with the following:

–The Higher Education Act of 1965; Federal regulations; Federal directives, including Department guidance

such as Dear Colleague Letters/Dear Partner Letters; Guarantor policies, as outlined in the Common Manual; Other requirements and procedures provided by the guarantors with which the lender participates

•Lender usually contracts these activities out to a Servicer

Guarantor

•The federal oversight for the FFEL program

•Provides insurance to the lender that if the debt management efforts don’t work, and the borrower doesn’t repay, the Guarantor will repay the loan to the lender.

•If borrower fails to make payments and they go into ‘pre-claims’, the guarantor gets involved with due diligence activities

• Provides funding for loans

• Manages any loan changes until the loan has been fully disbursed and passed on to the servicer

Lender

• The following slides detail the lenders responsibilities. But most lenders contract these responsibilities out to servicers.

• It is ultimately the lender’s responsibility to ensure that all requirements are upheld, but it generally does so through it’s contracts with the servicer

Lender / Servicer

(including but not limited to…)• Respond within 30 days to all inquiries from the borrower

or endorser

• A lender is required to keep current, complete, and accurate records for each FFELP loan it holds. All records must be retrievable in a coherent hard copy format or in other media formats such as microform, computer file, optical disk, or CD-ROM.

Lender / Servicer – General Responsibilities

• A record of any adjustments that the lender receives to the borrower’s requested loan amount.

• Copy of the signed promissory note. The original or a true and exact copy of the promissory note must be retained until the loan is paid in full or assigned to the Department.

• The guarantee disclosure for each loan, with a record of any changes to the disclosure.

• Evidence of disbursement

Lender / Servicer – Record Keeping Requirements

• Documentation of the lender’s handling of any refunds issued by the student’s school.

• Documentation supporting any Social Security number change.

• Documentation of the date on which the student was no longer enrolled at least half time and the schools the student attended.

• Notice of address changes for the borrower or references.

• Documentation of all repayment terms established with the borrower, including the repayment start date and the amount and number of installments.

Lender / Servicer – Record Keeping Requirements

• A record of all payments received, including the dates, amounts, and way in which each payment was applied to the principal, interest, and other outstanding balances on the loan.

• Evidence of any deferment eligibility, including the beginning and ending dates for each.

• Documentation of any forbearance granted, including the beginning and ending dates for each.

• Documentation of all due diligence efforts.

• A record of each communication on the loan—other than regular reports by the lender showing that an account is current—between the lender and a credit bureau.

Lender / Servicer – Record Keeping Requirements

• The federal oversight for the FFEL program

• Provides insurance to the lender that if the debt management efforts don’t work, and the borrower doesn’t repay, the guarantor will repay the loan to the lender.

• If borrower fails to make payments and they go into ‘pre-claims’, the guarantor gets involved with due diligence activities

• Ultimately, the guarantor is responsible for default prevention activities. – What does your Guarantor do? – Do they go above and beyond their required activities?

Guarantor

• Provide Notice of Guarantee (NOG) to the school

• Provide Disclosure Statement to the borrower

• Provide default prevention programs and materials

Guarantor - General Responsibilities

• On behalf of the lender, administer all aspects of loan repayment

• This is who your borrowers will be interacting with throughout their entire repayment – it’s important to choose wisely! – How do your servicer partners compare? – Do they go over an above? – Do you know what they do?

Servicer - General Responsibilities

Life of Loan

Origination Period

• Lender – provides funding for the loan

• Guarantor – provides guarantee for the loan

• Once loan is fully disbursed, servicer gets loan info from lender

• Servicer tracks data (status changes, pre-payments, interest rate changes, etc.)

Responsibilities throughout life of loan

Interim Period

• A lender must provide repayment disclosure to a borrower within a specific time frame

– Stafford Loans

• No more than 240 days and no less than 30 days prior to the first payment due date

• Guarantors recommend 90 days

If lender receives returned mail, guarantors recommend that they immediately begin skip tracing in an effort to keep the borrower in good standing

Responsibilities throughout life of loan

Interim Period

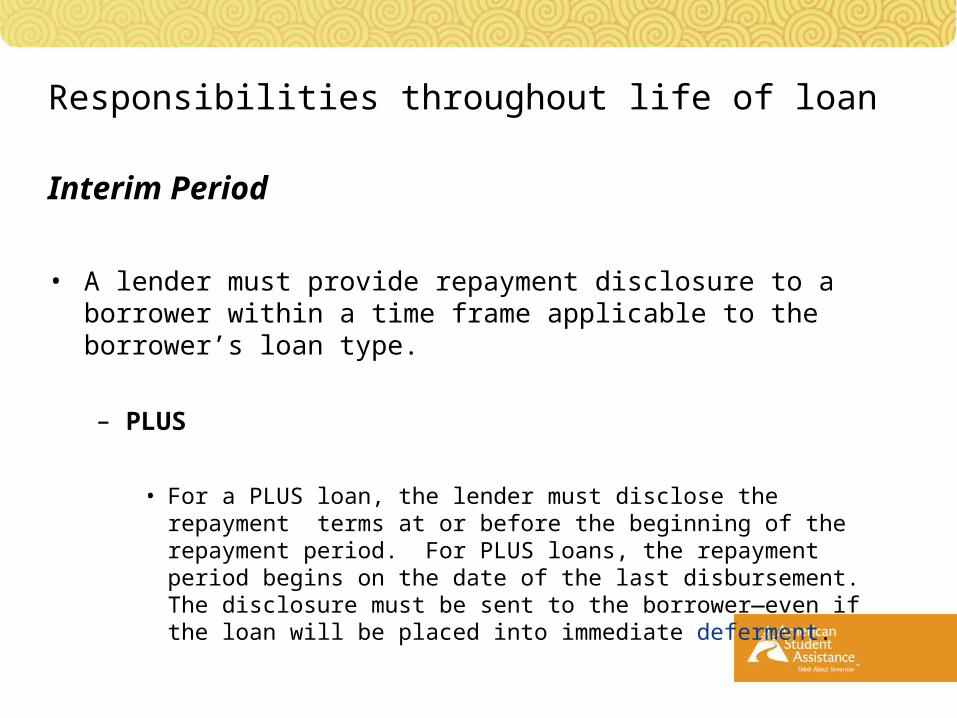

• A lender must provide repayment disclosure to a borrower within a time frame applicable to the borrower’s loan type.

– PLUS

• For a PLUS loan, the lender must disclose the repayment terms at or before the beginning of the repayment period. For PLUS loans, the repayment period begins on the date of the last disbursement. The disclosure must be sent to the borrower—even if the loan will be placed into immediate deferment.

Responsibilities throughout life of loan

Interim Period• It is the responsibility of the lender/servicer to be in contact with the

borrower

• Some guarantors will also provide debt management services / programs during this time as well

• Check with your servicers and guarantors to find out what activities they do. – Can they be coordinated for best service to the student?

– Can you coordinate the schools activities to supplement or support what your partners are doing?

Responsibilities throughout life of loan

Repayment Period

• Servicer updates guarantor with all changes to the loan throughout Interim and Repayment periods

• Servicer manages deferments and forbearances

• If borrower fails to make payments, the Servicer proceeds with required due diligence

Responsibilities throughout life of loan

Lender / Servicer must ensure that no gap in collection activity of greater than 45 days

1 – 15 days delinquent – at least one written notice or collection letter informing the borrower of the delinquency and urging the borrower to make payments sufficient to eliminate the delinquency

16–180 days delinquent - Make at least four diligent efforts (each consisting of one successful contact or two unsuccessful attempts) to contact the borrower by telephone. At least one diligent attempt to contact the borrower by telephone must occur on or before the 90th day of delinquency, and another must occur after that date.

Also send the borrower at least four written notices or collection letters informing the borrower of the delinquency and urging the borrower to make payments.

Due Diligence

181—270 Days Delinquent - The lender / servicer must engage in collection efforts that ensure that no gap in collection activity of greater than 45 days occurs through the 270th day of delinquency. These efforts must urge the borrower to make the required payments on the loan.

241 Days or More Delinquent - The lender / servicer must mail a final demand letter to the borrower anytime the loan becomes 241 days or more delinquent. The final demand letter must require the borrower to remit payment in full and warn that if the borrower defaults on the loan, the default will be reported to a national credit bureau. The lender / servicer must allow the borrower at least 30 days after the date the letter is mailed to respond to the final demand letter and to bring the loan out of default before filing a default claim on the loan.

Due Diligence

The lender / servicer must request default aversion assistance from the guarantor no earlier than the 60th day and no later than the 120th day of the borrower’s delinquency

271–360 Days Delinquent - The lender / servicer must file a default claim with the Guarantor no later than the 360th day of delinquency

A lender is encouraged to file a default claim on or after the 300th day of delinquency to permit the borrower the longest possible period in which to resolve the outstanding delinquency and avert default.

Due Diligence

Repayment Period

• The lender / servicer must request default aversion assistance from the guarantor no earlier than the 60th day and no later than the 120th day of the borrower’s delinquency

• When borrower makes a payment, the Servicer takes back full responsibility for administering repayment

• If borrower defaults, guarantor pays the claim and continues trying to rehabilitate the borrower

• The lender / servicer provides borrower with “Paid in Full” notice.

Responsibilities throughout life of loan

Divider Page Arial Italic 24 pt.

Questions

American Student Assistance®

100 Cambridge Street, Suite 1600Boston, MA 02114

(800) 999-9080(617) 728-4265 F A X(800) 999-0923 T D D

www.amsa.com