Legislative Economic Briefing

30

Legislative Economic Briefing January 19, 2012 Mississippi University Research Center Mississippi Institutions of Higher Learning Darrin Webb, State Economist [email protected] (601)432-6556 January 19, 2012 MS University Research Center, IHL 1

Transcript of Legislative Economic Briefing

Legislative Economic BriefingJanuary 19, 2012

Mississippi University Research CenterMississippi Institutions of Higher Learning

Darrin Webb, State [email protected]

(601)432-6556

January 19, 2012 MS University Research Center, IHL 1

Highlights• Ended 2011 on a strong note

• Economy will likely slow in the coming months

• Slow growth is the new norm– MS will be particularly challenged

• On track to make 2012 General Fund Estimate

January 19, 2012 MS University Research Center, IHL 2

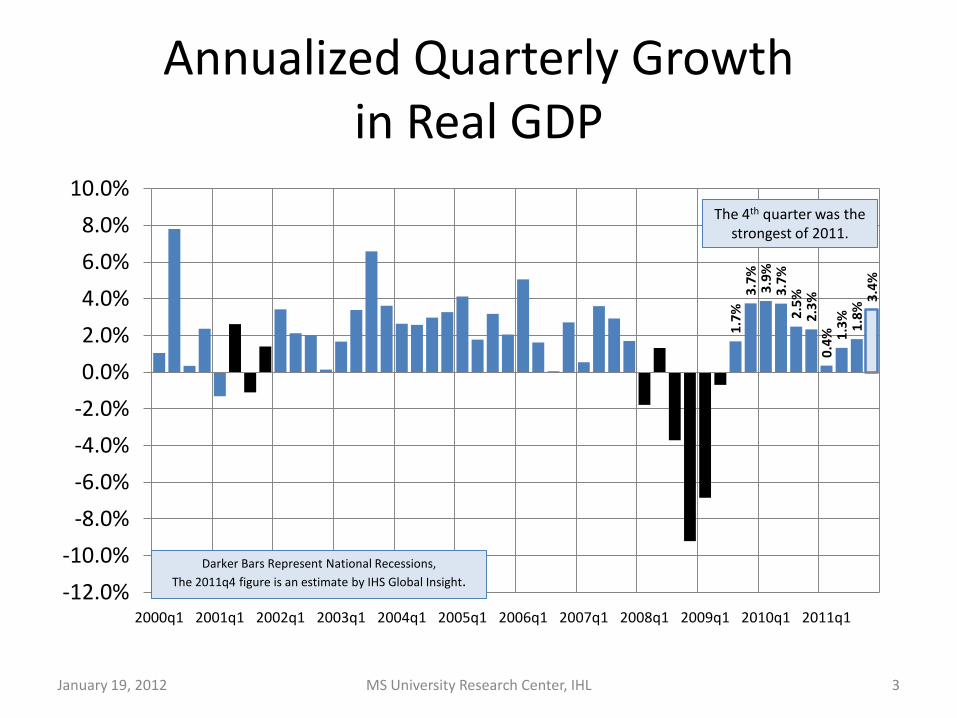

Annualized Quarterly Growth in Real GDP

1.7%

3.7%

3.9%

3.7%

2.5%

2.3%

0.4% 1.

3% 1.8%

3.4%

-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2000q1 2001q1 2002q1 2003q1 2004q1 2005q1 2006q1 2007q1 2008q1 2009q1 2010q1 2011q1

Darker Bars Represent National Recessions, The 2011q4 figure is an estimate by IHS Global Insight.

MS University Research Center, IHL 3January 19, 2012

The 4th quarter was the strongest of 2011.

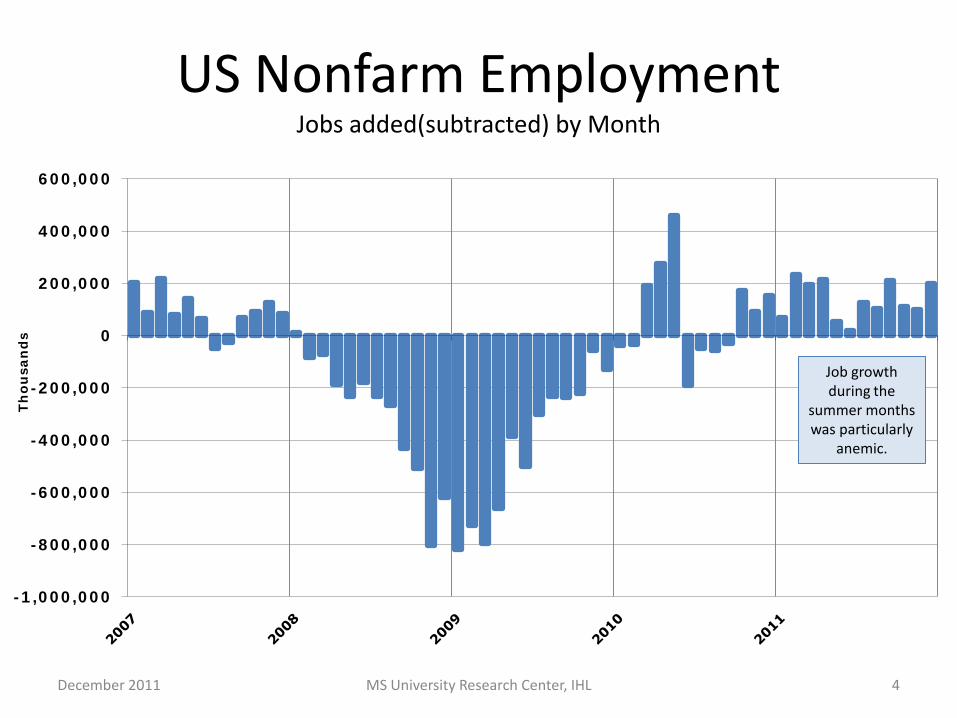

US Nonfarm EmploymentJobs added(subtracted) by Month

MS University Research Center, IHL 4

-1,000,000

-800,000

-600,000

-400,000

-200,000

0

200,000

400,000

600,000

Th

ou

san

ds

December 2011

Job growth during the

summer months was particularly

anemic.

US Nonfarm Employment

MS University Research Center, IHL 5

124,000

126,000

128,000

130,000

132,000

134,000

136,000

138,000

140,000

Th

ou

san

ds

Peak-to-trough loss 8.8 million Jobs or 6.3%

Gains since trough 2.7 million jobs. We

remain 4.4% below peak

January 19, 2012

Institute For Supply Management Indices

30.0

35.0

40.0

45.0

50.0

55.0

60.0

65.0Ja

n-07

Mar

-07

May

-07

Jul-0

7

Sep-

07

Nov

-07

Jan-

08

Mar

-08

May

-08

Jul-0

8

Sep-

08

Nov

-08

Jan-

09

Mar

-09

May

-09

Jul-0

9

Sep-

09

Nov

-09

Jan-

10

Mar

-10

May

-10

Jul-1

0

Sep-

10

Nov

-10

Jan-

11

Mar

-11

May

-11

Jul-1

1

Sep-

11

Nov

-11

ISM

Indi

ces:

abo

ve 5

0 is

exp

andi

ng

Manufacturing Index Nonmanufacturing Index

MS University Research Center, IHL 6January 19, 2012

An ISM Index above 50 says the industry is expanding. Below 50 indicates a

contraction. The ISM for MFG came close to 50 during the summer, but rose in the

fourth quarter. The Nonmanufacturing index trended downward as well, but rose

in December.

Real US Retail SalesAdjusted for Inflation

-15%

-10%

-5%

0%

5%

10%

$280,000

$290,000

$300,000

$310,000

$320,000

$330,000

$340,000

$350,000

Lin

e: G

row

th O

ver

Pri

or Y

ear

Bar

: Mon

thly

Sal

es M

illi

ons

of 2

00

4 $

MS University Research Center, IHL 7January 19, 2012

After adjusting for inflation, sales are still below the pre-recession level. Retailers saw slower growth in the 2011 Christmas shopping season

than in 2010.

U.S. Light Vehicle SalesOver 13 million units sold (annualized rate) for the past 4 months

9.0

11.0

13.0

15.0

17.0

19.0

21.0

23.0

Mill

ions

of U

nits

, SA

AR

MS University Research Center, IHL 8January 19, 2012

U.S. Consumer Sentiment Up from the low of August, but still low historically

50

60

70

80

90

100

110

120Ja

n-90

Oct

-90

Jul-9

1

Apr

-92

Jan-

93

Oct

-93

Jul-9

4

Apr

-95

Jan-

96

Oct

-96

Jul-9

7

Apr

-98

Jan-

99

Oct

-99

Jul-0

0

Apr

-01

Jan-

02

Oct

-02

Jul-0

3

Apr

-04

Jan-

05

Oct

-05

Jul-0

6

Apr

-07

Jan-

08

Oct

-08

Jul-0

9

Apr

-10

Jan-

11

Oct

-11

Uni

vers

ity o

f Mic

higa

n In

dex,

196

6 =

100

MS University Research Center, IHL 9January 19, 2012

National Federation of Independent Businesses Optimism Index

Jan-

07

Mar

-07

May

-07

Jul-0

7

Sep-

07

Nov

-07

Jan-

08

Mar

-08

May

-08

Jul-0

8

Sep-

08

Nov

-08

Jan-

09

Mar

-09

May

-09

Jul-0

9

Sep-

09

Nov

-09

Jan-

10

Mar

-10

May

-10

Jul-1

0

Sep-

10

Nov

-10

Jan-

11

Mar

-11

May

-11

Jul-1

1

Sep-

11

Nov

-11

80

82

84

86

88

90

92

94

96

98

100

NFI

B O

ptim

ism

Inde

x, 1

986=

100

MS University Research Center, IHL 10January 19, 2012

Small Businesses are less pessimistic than during the summer months, but have

not yet returned to their pre-recession optimism.

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

96.0

98.0

100.0

102.0

104.0

106.0

108.0

110.0Ja

n-07

Apr

-07

Jul-0

7

Oct

-07

Jan-

08

Apr

-08

Jul-0

8

Oct

-08

Jan-

09

Apr

-09

Jul-0

9

Oct

-09

Jan-

10

Apr

-10

Jul-1

0

Oct

-10

Jan-

11

Apr

-11

Jul-1

1

Oct

-11

Line

Gra

ph: G

row

th O

ver

Year

Ago

Bar G

raph

: Ind

ex 2

004=

100

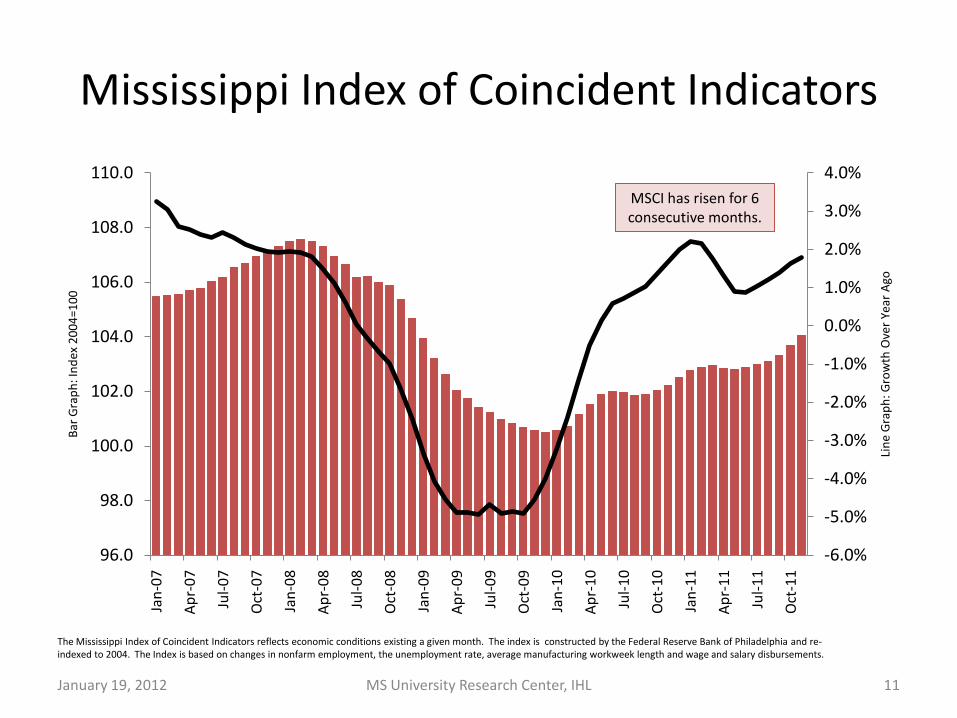

Mississippi Index of Coincident Indicators

11MS University Research Center, IHLJanuary 19, 2012

MSCI has risen for 6 consecutive months.

The Mississippi Index of Coincident Indicators reflects economic conditions existing a given month. The index is constructed by the Federal Reserve Bank of Philadelphia and re-indexed to 2004. The Index is based on changes in nonfarm employment, the unemployment rate, average manufacturing workweek length and wage and salary disbursements.

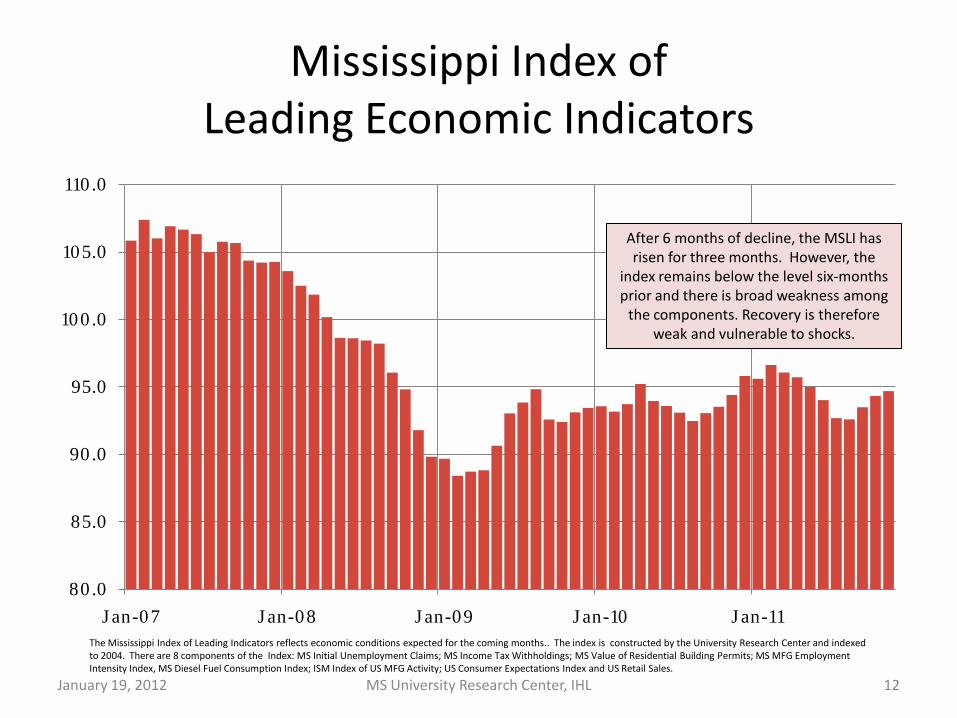

Mississippi Index of Leading Economic Indicators

80.0

85.0

90.0

95.0

100.0

105.0

110.0

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11

12MS University Research Center, IHL

After 6 months of decline, the MSLI has risen for three months. However, the

index remains below the level six-months prior and there is broad weakness among

the components. Recovery is therefore weak and vulnerable to shocks.

January 19, 2012

The Mississippi Index of Leading Indicators reflects economic conditions expected for the coming months.. The index is constructed by the University Research Center and indexed to 2004. There are 8 components of the Index: MS Initial Unemployment Claims; MS Income Tax Withholdings; MS Value of Residential Building Permits; MS MFG Employment Intensity Index, MS Diesel Fuel Consumption Index; ISM Index of US MFG Activity; US Consumer Expectations Index and US Retail Sales.

MS Nonfarm Employment

MS University Research Center, IHL 13

800

850

900

950

1,000

1,050

1,100

1,150

1,200

Th

ou

san

ds

Employment has risen for three consecutive months. Employment remains well below the peak of February

1,160.4 May 00

1,109.3 Jun 03

1,104.8 Nov 11

1,160.2 Feb 08

January 19, 2012

1,083.4 Feb 10

January 19, 2012 MS University Research Center, IHL 14

(1,576)Jones

(1,358)Warren

(1,025)Jackson

(1,022)De Soto

(940)Lauderdale

(906)Neshoba

(842)Lee

(781)Lowndes

(755)Union(742)

Lafayette

(733)Washington

(655)Adams

(633)Tunica

(625)Oktibbeha

(586)Alcorn

(568)Grenada

(563)Leflore

(529)Lincoln

(466)Claiborne

(461)Marshall

(445)Winston

(389)Wayne

(352)Marion

(335)Pearl River

(312)Clay

(235)Walthall

(234)Tippah

(214)Pike

(212)Covington

(193)Amite

(192)Sunflower

(188)Attala

(169)Bolivar

(153)Monroe

(152)Tishomingo

(120)Newton

(95)Itawamba

(85)Leake

(74)Jasper

(65)Lawrence

(61)Tate

(50)Yazoo

(42)Scott

(41)Kemper

(15)Perry

(5)Issaquena

5 George

6 Franklin

11 Quitman

15 Stone

16 Carroll

34 Holmes

37 Copiah

53 Simpson

59 Humphreys

64 Calhoun

70 Jefferson

80 Greene

81 Webster

84 Prentiss

86 Clarke

91 Coahoma

92 Montgomery 93

Choctaw

102 Benton

110 Pontotoc

114 Wilkinson

115 Noxubee

123 Chickasaw

123 Madison

128 Hancock

166 Tallahatchie

175 Forrest

176 Sharkey

185 Lamar

205 Smith

207 Jefferson Davis

395 Yalobusha

619 Rankin

693 Panola

758 Hinds

1,120 Harrison

DeclineLess than 100 Jobs GainedGreater than 100 Jobs Gained

Employment Gained (Lost) By County

2010-2011*

* The average employment for the January to November period is compared for both years.

46 Counties Lost Employment

MS Residential Building PermitsThree Month Moving Average Number of Units

20

220

420

620

820

1,020

1,220

1,420

1,620

1,820

Jan

-00

Jul-

00

Jan

-01

Jul-

01

Jan

-02

Jul-

02

Jan

-03

Jul-

03

Jan

-04

Jul-

04

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

7,615 Permits were issued in the 1st seven months of 2005.

During the same period of 2011, only 2,580 were issued. This is a 66% decrease.

15MS University Research Center, IHLJanuary 19, 2012

Permits trended upward in the second half of

2011

Other Mississippi Trends

• Real Withholdings have trended up in 2011, but are below pre-recession levels

• Initial and continued unemployment claims trended down in second half of 2011, after rising in the first half; Remain high by historical standards

• Diesel fuel consumption declined toward the end of 2011

January 19, 2012 MS University Research Center, IHL 16

The U.S. Economy Will Slow In first Half of 2012

• Inventory Boost will Fade

• Fundamental Weakness in the Economy – Weak housing sector

– High debt levels for consumer and government

– Consumers and businesses remain cautious

– Eurozone financial troubles may lead to some credit tightening in the U.S.

• Slower Global Economy

January 19, 2012 MS University Research Center, IHL 17

Growth In Real U.S. GDPHistorical and IHS Global Insight Baseline Projections

3.0%

1.8% 2.

0% 2.4%

3.4%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

MS University Research Center, IHL 18January 19, 2012

Growth In Real MS GDPHistorical and University Research Center Projections

1.1%

0.9%

1.7% 2.

1%

2.8%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

MS University Research Center, IHL 19January 19, 2012

Growth In Real U.S. GDP: PessimisticNOTE: Pessimistic does not imply worst case

1.7%

0.2% 0.

5%

3.1%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

MS University Research Center, IHL 20January 19, 2012

Probability of Recession 30%

Alternative Forecasts for MS Gross Domestic Product

-1.5-1.0-0.50.00.51.01.52.02.53.03.54.0

10Q

1

10Q

2

10Q

3

10Q

4

11Q

1

11Q

2

11Q

3

11Q

4

12Q

1

12Q

2

12Q

3

12Q

4

13Q

1

13Q

2

13Q

3

13Q

4

14Q

1

14Q

2

14Q

3

14Q

4

Ann

ualiz

ed P

erce

ntag

e G

row

th

Baseline (55% probablilty) High (15% probablilty) Low (30% probablilty)

January 19, 2012 MS University Research Center, IHL 21

US Jobs Lost Since January 2008

-10

-9

-8

-7

-6

-5

-4

-3

-2

-1

0Ja

n-08

Feb-

08M

ar-0

8A

pr-0

8M

ay-0

8Ju

n-08

Jul-0

8A

ug-0

8Se

p-08

Oct

-08

Nov

-08

Dec

-08

Jan-

09Fe

b-09

Mar

-09

Apr

-09

May

-09

Jun-

09Ju

l-09

Aug

-09

Sep-

09O

ct-0

9N

ov-0

9D

ec-0

9Ja

n-10

Feb-

10M

ar-1

0A

pr-1

0M

ay-1

0Ju

n-10

Jul-1

0A

ug-1

0Se

p-10

Oct

-10

Nov

-10

Dec

-10

Jan-

11Fe

b-11

Mar

-11

Apr

-11

May

-11

Jun-

11Ju

l-11

Aug

-11

Sep-

11O

ct-1

1N

ov-1

1D

ec-1

1

Mill

ions

Jan. 13, 2011 MS University Research Center, IHL 22

The depth of the recession means full recovery will take years.

MS Jobs Lost Since February 2008

-76,800-55,400

(90,000)

(80,000)

(70,000)

(60,000)

(50,000)

(40,000)

(30,000)

(20,000)

(10,000)

-Fe

b-08

Mar

-08

Apr

-08

May

-08

Jun-

08Ju

l-08

Aug

-08

Sep-

08O

ct-0

8N

ov-0

8D

ec-0

8Ja

n-09

Feb-

09M

ar-0

9A

pr-0

9M

ay-0

9Ju

n-09

Jul-0

9A

ug-0

9Se

p-09

Oct

-09

Nov

-09

Dec

-09

Jan-

10Fe

b-10

Mar

-10

Apr

-10

May

-10

Jun-

10Ju

l-10

Aug

-10

Sep-

10O

ct-1

0N

ov-1

0D

ec-1

0Ja

n-11

Feb-

11M

ar-1

1A

pr-1

1M

ay-1

1Ju

n-11

Jul-1

1A

ug-1

1Se

p-11

Oct

-11

Nov

-11

Jan. 13, 2011 MS University Research Center, IHL 23

Annual Growth in Real GDP

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

MS SE US

MS University Research Center, IHL 24January 19, 2012

Mississippi’s growth was below that of the Nation and Region in 9 out of

the past 13 years

Three Sources of Income, 2010MS is relatively dependent upon transfer payments

60.8% 64.7% 64.8%

13.1%16.1% 16.8%

26.1% 19.1% 18.5%

0%10%20%30%40%50%60%70%80%90%

100%

MS SE US

Earnings Dividends, Interest and Rent Transfer Payments

MS University Research Center, IHL 25January 19, 2012

$1.00 of Income In Mississippi by Source2010

Personal current transfer receipts, $0.26

Dividends, interest, and rent, $0.13

Farm earnings, $0.01

Forestry, fishing, etc. and mining, $0.01

Utilities, $0.01

Construction, $0.04 Manufacturing, $0.08 Wholesale/Retail, $0.07

Transportation and warehousing, $0.02

Information, $0.01

Finance and insurance, $0.02

Real estate and rental and leasing, $0.01

Professional, scientific, and technical services, $0.03

Management of companies and enterprises, $0.01

Administrative and waste management services, $0.02

Educational services, $0.01

Health care and social assistance, $0.07

Liesure and Hospitality, $0.03

Other services, except public administration, $0.02

Government and government enterprises, $0.15

MS University Research Center, IHL 26January 19, 2012

Federal Expenditures as a share of Gross Domestic Product, By State, 2010

13.0

%

15.7

%

16.1

%

16.4

%

16.6

%

16.9

%

17.4

%

17.6

%

18.4

%

18.7

%

18.8

%

19.3

%

19.5

%

19.9

%

20.6

%

20.7

%

21.3

%

21.4

%

21.8

%

22.1

%

22.3

%

22.8

%

22.9

%

23.6

%

23.7

%

23.8

%

23.9

%

24.3

%

25.0

%

25.1

%

25.4

%

25.6

%

25.7

%

25.7

%

26.1

%

27.0

%

28.2

%

28.3

%

28.4

%

28.8

%

28.9

%

29.8

% 31.2

%

32.1

%

32.2

%

32.6

%

32.7

%

33.3

% 35.1

%

35.1

%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

DE

NV

WY

MN NJ IL NY

CA NE TX NH CO OR IA UT

WA IN NC

MA WI

OH KS GA CT MI

SD RI LA FL ND AZ

PA AK ID OK

TN AR SC ME

MO VT MT HI

VA MS

MD AL

WV KY N

M

January 19, 2012 MS University Research Center, IHL 27

Federal expenditures represent almost a third of Mississippi’s GDP

MS General FundGrowth Over Prior Year

2.5%

5.1%

1.3%

9.1%

11.4%

9.7%

2.9%

5.9%6.5%

7.6%

2.8%2.1%

-2.1%

2.2%

4.0%

7.2%

12.8%

10.5%

3.1%

-4.2%-4.9%

2.3%1.3%

-0.6%

-8.00%

-3.00%

2.00%

7.00%

12.00%

17.00%19

90

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Jan. 13, 2011 MS University Research Center, IHL 28

Black Bars Represent National Recessions

Fiscal Year to Date Growth 3.9%Growth Needed Rest of Year

to Make November Revised Estimate 0.2%

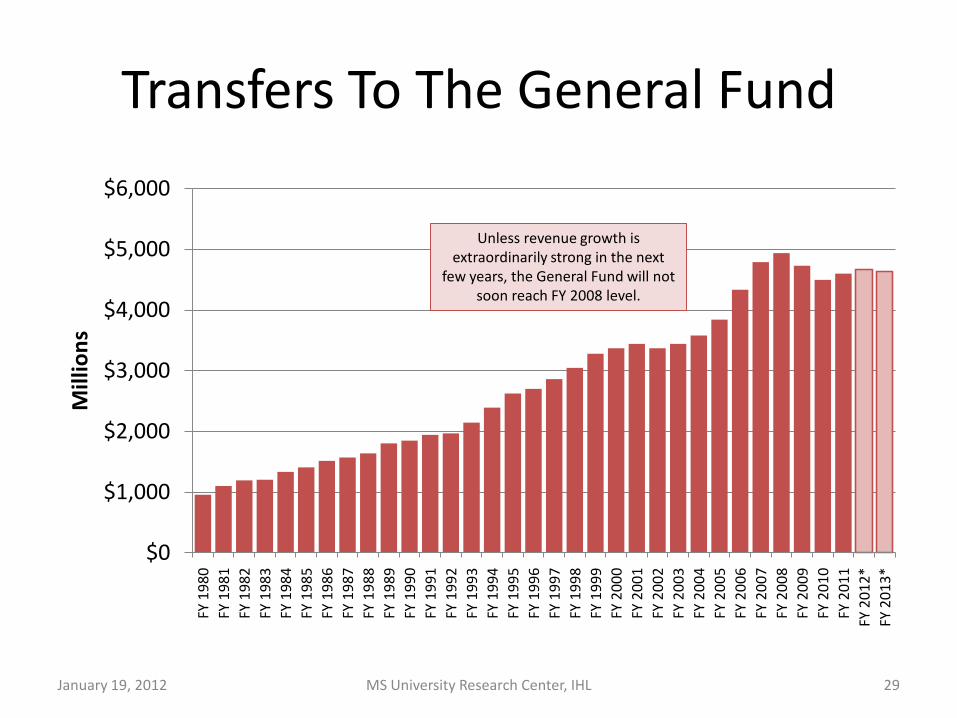

Transfers To The General Fund

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000FY

198

0FY

198

1FY

198

2FY

198

3FY

198

4FY

198

5FY

198

6FY

198

7FY

198

8FY

198

9FY

199

0FY

199

1FY

199

2FY

199

3FY

199

4FY

199

5FY

199

6FY

199

7FY

199

8FY

199

9FY

200

0FY

200

1FY

200

2FY

200

3FY

200

4FY

200

5FY

200

6FY

200

7FY

200

8FY

200

9FY

201

0FY

201

1FY

201

2*FY

201

3*

Mill

ions

MS University Research Center, IHL 29January 19, 2012

Unless revenue growth is extraordinarily strong in the next

few years, the General Fund will not soon reach FY 2008 level.

Highlights• Ended 2011 on a strong note

• Economy will likely slow in the coming months

• Slow growth is the new norm

• MS will be particularly challenged(1) Lower human capital

(2) Higher concentration in slow-growth industries

(3) Heavily dependent on federal expenditures which will likely grow slowly in the coming years

• On track to make 2012 General Fund Estimate

January 19, 2012 MS University Research Center, IHL 30