Legal & Regulatory Bulletin 23

20

EMPEA Legal & Regulatory Bulletin | FALL 2017 1 Legal & Regulatory Bulletin 23 Issue no. 23 | FALL 2017 CONTENTS 4 Structuring Funds for Investment in India: Maximizing Tax Efficiency for U.S. Investors 9 Foreign Investment in Distressed Debt in India: What’s the Best Vehicle? 12 Africa Insurance M&A: Global Insurers’ Next Frontier

Transcript of Legal & Regulatory Bulletin 23

EMPEA Legal & Regulatory Bulletin | FALL 2017 1

Legal &Regulatory Bulletin 23

Issu

e n

o.

23

| F

ALL

20

17

CONTENTS

4 Structuring Funds for Investment in India: Maximizing Tax Efficiency for U.S. Investors

9 Foreign Investment in Distressed Debt in India: What’s the Best Vehicle?

12 Africa Insurance M&A: Global Insurers’ Next Frontier

© 2017 EMPEA2

About EMPEA

EMPEA is the global industry association

for private capital in emerging markets. An

independent, non-profit organization, the

association’s membership comprises 300+

firms representing institutional investors, fund

managers and industry advisors who together

manage more than US$5 trillion in assets across

130 countries. Our members share EMPEA’s belief

that private capital is a highly suited investment

strategy in emerging markets, delivering attractive

long-term investment returns and promoting

the sustainable growth of companies and

economies. We support our members through

global authoritative intelligence, conferences,

networking, education and advocacy.

For more information, visit empea.org.

Publication Editorial Team Ann Marie Plubell Vice President, Regulatory Affairs

Production Assistance Ben Pierce Pierce Designers

© 2017 EMPEA. All rights reserved. The EMPEA Legal & Regulatory Bulletin is an EMPEA publication. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means—electronic, mechanical, photocopying, recording or otherwise—without the prior permission of EMPEA.

EMPEA | The Watergate Office Building | 2600 Virginia Avenue N.W., Suite 500 Washington, D.C. 20037-1905 USA

Phone: +1.202.333.8171 | Fax: +1.202.333.3162 | Web: empea.org

To learn more about EMPEA or to request a membership application, please send an email to [email protected].

EMPEA Legal & Regulatory Council

Mark Kenderdine-Davies (Chair) CDC Group plc

Carolyn Campbell Emerging Capital Partners

Antonio Felix de Araujo Cintra TozziniFreire Advogados

John Daghlian O’Melveny & Myers

Mark Davies King & Spalding

Folake Elias-Adebowale Udo Udoma & Belo-Osagie

Laura Friedrich Shearman & Sterling LLP

Geoffrey Kittredge Debevoise & Plimpton

Prakash Mehta Akin Gump Strauss Hauer & Feld LLP

Zia Mody AZB & Partners

Gordon Myers IFC

Peter O’Driscoll Orrick, Herrington & Sutcliffe LLP

Chike Obianwu Templars

Bayo Odubeko Norton Rose Fulbright

Paul Owers Actis

George Springsteen IFC Asset Management Company

Mara Topping White & Case LLP

Cindy Valentine Simmons & Simmons

Nigel Wellings Clifford Chance

Harald Zeiter Capital Dynamics

DISCLAIMER: This material should not be construed as professional legal advice and is intended solely as commentary on legal and regulatory developments affecting the private equity community in emerging markets. The views expressed in this bulletin are those of the authors and not necessarily those of their firms. If you would like to republish this bulletin or link to it from your website, please contact Holly Radel at [email protected].

EMPEA Legal & Regulatory Bulletin | FALL 2017 3

The EMPEA Fall Bulletin focuses on various topics including complex tax efficiency considerations for U.S. taxable and tax-exempt investors considering investment in India, challenges resulting from a decision to invest in Indian distressed debt, optimal investment structures following recent changes in the Indian Insolvency and Bankruptcy Code and an exploration of opportunities and challenges for those interested in acquiring African insurance businesses, particularly in Kenya, Nigeria and South Africa.

In this Bulletin our contributors deliberate on:

Structuring Funds for Investment in India to Maximize Tax Efficiency for U.S. Investors: What are the implications for both the U.S. taxable and tax-exempt investor in the current environment given treaty implications and Indian tax developments?

Foreign Investment in Distressed Debt in India Looks Interesting: What are the pros and cons of specific investment vehicles including the Alternative Investment Fund, the Asset Reconstruction Company and the Non-Banking Financial Institution when examined through the lens of developments in India’s securities, tax and bankruptcy laws?

Could Africa’s Insurance Industry be a Fresh Frontier for Merger and Acquisition Activity? What do the markets in Kenya, Nigeria and South Africa suggest?

A Letter from the Council Chair

EMPEA Regulatory Affairs Resources:

• EMPEA’s Regulatory Advocacy Resources support members as they seek to encourage legal and regulatory enabling environments in emerging markets that don’t disadvantage private investment. Contact: Ann Marie Plubell, VP, Regulatory Affairs [email protected].

• EMPEA Guidelines set out key legal and tax regimes optimal for the development of private equity and are now available in numerous languages including Arabic, Burmese, Chinese (simplified character), French, Portuguese, Russian, Spanish and Vietnamese on the EMPEA website.

• EMPEA Legal & Regulatory Council draws on deep subject matter expertise in the emerging markets practice to address trending concerns.

• EMPEA Legal & Regulatory Bulletin publishes key perspectives and insights of in-house counsel and leading practitioners into the current challenges and concerns of the emerging markets community.

• EMPEA Education Courses and Resources for Emerging Market Regulators, Pension and Policy Oversight Officials highlight the foundational issues relating to the development and regulation of private equity in developing economies.

The agendas for the forthcoming EMPEA and FT summits “Sustainable Investing in Emerging Markets” and “Private Equity Africa” in London offer thought leadership and content to enhance business strategies and product design for investors, fund managers and advisors including timely information on the diverse legal and regulatory environments where we invest. I look forward to meeting many of you in October. Might I also invite you to share your thoughts with me, Mark Kenderdine-Davies([email protected]) and Ann Marie Plubell, EMPEA VP, Regulatory Affairs at [email protected]?

Best wishes,

Mark Kenderdine-DaviesGeneral Counsel, CDC Group plcChair, EMPEA, Legal & Regulatory Council

© 2017 EMPEA4

IntroductionThe typical private equity model seeks to return capital and profits to investors with little to no entity or investment-level taxation, leaving potential tax drag, if any, at the investor level. In practice and in line with a global tax paradigm where capital gains are generally sourced to the residency of the investor, this means that tax on the exit of a portfolio company is generally imposed exclusively by the jurisdiction in which the investor is resident and not by the jurisdiction in which the portfolio company is located. Where local tax rules do not follow this paradigm, income tax treaties may reduce or eliminate local capital gains taxes, or to provide a credit for local capital gains taxes against taxes imposed by the investor’s home jurisdiction.

Investing in a manner that reduces or eliminates local taxes is crucial to enhancing returns to tax-exempt investors, as they make up a large

Structuring Funds for Investment in India: Maximizing Tax Efficiency for U.S. InvestorsBy Olivier De Moor and Brett Fieldston, Akin Gump Strauss Hauer & Feld LLP

portion of the investors that seek exposure to emerging market funds and, very generally, they are not subject to taxation in their home jurisdictions. In addition, for taxable investors reducing or eliminating local taxes may simplify tax reporting requirements in their jurisdictions of residence and limit the chance for “tax leakage” where the local tax rate exceeds the home tax rate or less than all of the local taxes are creditable.

In the case of India-focused investment platforms, fund sponsors often domicile their funds in Mauritius, where until recently they sought to avail themselves, among other potential benefits, of an exemption of Indian capital gains tax on disposition gains realized on a transfer of shares by a Mauritius resident fund under the India-Mauritius tax treaty. Effective as of April 1, 2017, subject to a transition period, the India-Mauritius tax treaty no longer provides for exemption from such Indian capital gains tax.1

The remainder of this article will discuss certain aspects of the current Indian tax regime that applies to capital gains, and the structuring of India-focused private equity funds in a manner that is intended to increase tax efficiency for U.S. tax-exempt and U.S. taxable investors.

Disposition Gains under the India-Mauritius Tax Treaty and Indian Domestic LawIn May 2016, India and Mauritius signed a Protocol that amended the India-Mauritius tax treaty. Under the Protocol, Indian capital gains tax generally applies to gains arising from the alienation of shares acquired on or after April 1, 2017. For this purpose, alienation generally includes any sale, exchange, buy-back or other taxable disposition of shares by a Mauritius resident fund. There is a phase-in for the imposition of the Indian capital gains tax, where gains from shares

1. In addition, effective as of the same date, a mirroring exemption that was set forth in the India-Singapore tax treaty for Singapore resident funds is equally phased out. The considerations discussed in this article with respect to Mauritius-based private equity funds also apply to Singapore-based private equity funds.

EMPEA Legal & Regulatory Bulletin | FALL 2017 5

disposed of prior to April 1, 2019 will be subject to tax at 50% of the Indian tax rate; thereafter, gains from share dispositions will be subject to full Indian tax under the domestic rules of Indian taxation.2 Indian tax advisors should be consulted regarding the structuring of investments and the potential to claim other benefits under Indian tax treaties and/or to reduce or eliminate the amount of Indian tax due.

Absent the benefit of an income tax treaty, under Indian domestic law, the applicable capital gains tax rate for Mauritius resident funds with a long-only investment strategy is determined by reference to, among others, the holding period in such shares and the manner by which the shares are sold (over-the-counter versus on an exchange). The standard tax rate for long-term capital gains realized on unlisted shares (24-month holding period) or shares listed on an exchange (12-month holding period) is currently 10%. In the case of a sale of listed shares on an exchange with respect to which the Indian securities transaction tax (STT) was paid, long-term capital gains realized are exempt from Indian capital gains taxation. In the case of short-term capital gains realized, the tax rate is generally 40%, but a reduced rate may apply for such gains realized on listed shares with respect to which STT was paid. In addition, certain surcharges may apply.

India Investment Fund Structures from a U.S. Tax PerspectiveIndia-focused private equity funds or feeders domiciled in Mauritius (which are referred to as “offshore” funds from an Indian point of view, since they are generally managed and controlled outside of India) are generally structured as private limited companies denominated with share capital that are “hybrid” vehicles for U.S. tax purposes. As a hybrid, the offshore fund is treated as a corporation for Mauritius and Indian tax purposes (and the tax purposes of other jurisdictions), but intended to be treated as a partnership for U.S. tax purposes.3 The treatment of the offshore fund as a partnership for such purposes is effected by its filing an entity classification (or so-called “check the box”) election on Form 8832 with the U.S. Internal Revenue Service (IRS). The hybrid structure provides U.S. taxable investors with a “pass-through” investment structure, which is generally the most tax-efficient structure for them.4

Sponsors of India-focused private equity funds should note that establishing a fund or feeder as a Mauritius company likely precludes their upper-tier investors from claiming any Indian tax treaty benefits that they otherwise would have been able to claim in their own right. This is because any disposition gains or other income realized by the fund will not be considered realized by such investors for purposes of determining

whether a treaty claim is available (i.e., they are not the beneficial owner of such income for tax purposes). This potential detriment is of little practical relevance, however, unless the tax treaty between India and the jurisdiction of residence of the investor provides a more beneficial outcome than the treatment that applies to the offshore feeder under Indian domestic law. For instance, the India-U.S. tax treaty does not provide any benefit with respect to disposition gains realized in a standard investment fund context.

More recently, offshore funds have preferred investing through an Indian trust or partnership (the “onshore” fund), which serves as a master fund that is generally fiscally transparent from an Indian tax perspective and directly invests in Indian portfolio companies. The onshore fund, in addition to having the offshore fund as an investor, is generally structured as the investment vehicle for Indian resident investors, and as the vehicle through which affiliates of the fund sponsor receive their incentive or performance compensation (also known as “carried interest”). By structuring the performance compensation as a profits interest from an onshore Indian entity that is fiscally transparent for Indian tax purposes, rather than as a fee or through a share class in an offshore entity, fund sponsor affiliates expect to receive certain preferential tax treatment under Indian tax law. This position is generally consistent with

2. While beyond the scope of this article, since the Protocol under the India-Mauritius tax treaty only applies to shares, we note that certain equity trading strategies via swaps or other derivatives (e.g., an option or forward contract), may potentially continue to be eligible for exemption from Indian taxation under the India-Mauritius tax treaty depending on all facts and circumstances involved.

3. The Mauritius fund would need to monitor certain transfers of direct or indirect equity interests to avoid becoming subject to certain “publicly traded partnership” rules, which, very generally, may cause partnerships to be treated as corporations solely for U.S. tax purposes. So long as transfers of interests in the offshore fund are subject to market-standard restrictions, and transfers are not recognized by the fund except with sponsor consent, however, this risk should be remote.

4. A Mauritius fund generally also insulates non-Indian investors against the risk that potential Indian tax filing requirements apply as a result of underlying investments in Indian portfolio companies. Certain exceptions may apply, such as on transfer or redemption.

“ Investing in a manner that reduces or eliminates local taxes is crucial to enhancing returns to tax-exempt investors, as they make up a large portion of the investors that seek exposure to emerging market funds and, very generally, they are not subject to taxation in their home jurisdictions.

© 2017 EMPEA6

the preference of non-corporate U.S. taxable investors investing in a fund structured as a partnership for U.S. tax purposes, because it avoids limitations as to deductibility that would apply if the compensation is instead structured as an incentive fee. For U.S. tax purposes, the onshore fund is generally classified as a partnership and, as a precautionary measure, it typically also files an entity classification election on IRS Form 8832 to confirm such classification.

Through this single or double layer “partnership” structure, disposition gains realized in respect of shares of Indian portfolio companies (and dividends and interest, if any, paid by such portfolio companies), will pass through the onshore and offshore funds to U.S. investors for U.S. tax purposes. At the same time, the offshore fund will serve as a “blocker” that insulates U.S. investors from certain Indian tax consequences, meaning that the offshore fund will be the person that, among others, potentially makes a claim for benefits under the India-Mauritius tax treaty, files certain tax returns with (and, if necessary, remits taxes to) the Indian tax authorities, and generally would be the subject of any Indian tax audit.

Key U.S. Tax Considerations for U.S. InvestorsThe considerations for U.S. investors generally fall into one of two categories: U.S. tax-exempt versus U.S. taxable investors. The key U.S. tax considerations for each of these categories of investors are described below.

U.S. Tax-Exempt Investors – UDFI TaxationU.S. tax-exempt investors typically include university endowments, charitable foundations and pension plans. These investors are generally exempt from U.S. tax on their

investment income, such as dividends, interest and capital gains. However, if investment income is earned on a leveraged basis—either through direct borrowing by the U.S. tax-exempt investor or on a pass-through basis by partnerships in which the U.S. tax-exempt investor invests—then under the U.S. “unrelated debt-financed income” or UDFI rules, the U.S. tax-exempt investor generally will be subject to U.S. corporate taxation (generally at the rate of 35%, increased with potential state and local taxes) and filing requirements on the proportion of its income that is treated as leveraged.5 For example, if 50% of the U.S. tax-exempt investor’s investment was acquired with the use of borrowed funds, then 50% of the gains on the investment would be subject to U.S. corporate taxation and the remaining 50% would continue to be exempt from U.S. tax. In addition, the CFC and PFIC rules, each described below, do not apply to U.S. tax-exempt investors unless they debt-finance their investment.

In a typical private equity investment fund structure, including in the case of India-focused private equity funds, portfolio companies are oftentimes not acquired with leverage at the fund (i.e., offshore or onshore fund) level.6 Borrowing, if any, is generally undertaken at the portfolio company level. Portfolio companies, especially in the India market, are formed as companies under local law (and generally do not make check-the-box elections to be classified as pass-through entities for U.S. tax purposes). As a result, U.S. tax-exempt investors are not expected to recognize UDFI and are therefore not expected to be subject to U.S. tax on their profits, even if those profits were generated in part through leverage in the manner described above. That being said, U.S. tax-exempt investors will nonetheless bear the economic burden of any taxes imposed

5. U.S. tax-exempt investors are also subject to U.S. taxation on so-called “unrelated business taxable income” (UBTI) which may arise in case of an investment in a U.S. or non-U.S. operating company that is treated as fiscally transparent for U.S. tax purposes. However, in case of a fund focusing on a standard Indian equity strategy making investments in portfolio companies formed as public or private limited companies, UBTI issuesare generally not expected to arise.

6. It should also be noted that private equity funds typically take the view that certain types of short-term leverage (e.g., to finance partnership expenses or bridge capital call notices) do not give rise to UDFI.

“ By structuring the performance compensation as a profits interest from an onshore Indian entity that is fiscally transparent for Indian tax purposes, rather than as a fee or through a share class in an offshore entity, fund sponsor affiliates expect to receive certain preferential tax treatment under Indian tax law.

EMPEA Legal & Regulatory Bulletin | FALL 2017 7

at the level of the offshore fund or lower in the fund structure, including any Indian capital gains taxes imposed on the offshore fund and not eliminated or reduced under the India-Mauritius tax treaty. As a result, the Indian capital gains tax would constitute an additional cost of making the investment and reduce the expected return to U.S. tax-exempt investors.

U.S. Taxable Investors – Tax Rates and CreditsU.S. taxable investors in Indian private equity funds are generally individuals and taxable trusts or estates, and can from time to time include U.S. corporations such as insurance companies. U.S. individuals and taxable trusts and estates are subject to the same tax rates, which under current law are up to 43.4% for ordinary income (interest and certain nonqualified dividends and capital gains realized on shares held for one year or less (short-term capital gains)) and 23.8% on capital gains realized on shares held for more than one year (long-term capital gains) and dividends that are eligible for preferential treatment under the “qualified dividend income” rules. U.S. corporations are subject to the same rate of tax (generally 35%) on both ordinary income and capital gains (whether short-term or long-term). State or local taxes may also apply. Individual U.S. taxable investors are unable to claim foreign tax credits (FTCs) for entity-level taxes paid by a corporation in which they are invested, which would generally include any Indian portfolio companies formed as public or private limited companies (certain corporate U.S. taxable investors are eligible to claim FTCs for local taxes paid by companies from which they receive dividends). However, subject to limitations and exceptions, all U.S. taxable investors are permitted to claim an FTC against their U.S. tax liability for taxes paid to local jurisdictions, provided that such taxes are directly

or indirectly incurred through a pass-through entity and are attributable to income treated as “foreign source” for U.S. tax purposes. (Very generally, under a mechanical rule the U.S. tax liability that can be offset is determined by reference to the ratio that the U.S. investor’s foreign-source income has over its worldwide income). Therefore, in the case of an India-focused private equity fund, dividends and interest paid by Indian companies should constitute foreign source income and any Indian withholding tax incurred with respect to such income should generally give rise to an FTC. On the other hand, capital gains realized by such investors are considered to be from U.S. sources for this purpose (and the distinction listed versus unlisted shares, or a long or short-term holding period is irrelevant in this regard). Therefore, U.S. taxable investors are generally unable to claim an FTC with respect to the Indian capital gains taxes described above that may apply upon exit by the private equity fund, unless they also realize other income from foreign sources (which may be from sources unrelated to the private equity fund). In addition, the India-U.S. tax treaty does not provide any additional relief in this regard (i.e., it does not cause disposition gains to be resourced for purposes of determining the availability of an FTC).

U.S. Taxable Investors – CFC and PFIC RegimesIn addition, when investing outside of the United States, U.S. taxable investors may be subject to the U.S. “controlled foreign corporation” (CFC) and “passive foreign investment company” (PFIC) rules. The CFC and PFIC rules, very generally, are intended to dissuade U.S. taxpayers from moving capital offshore to non-U.S. corporations where those non-U.S. corporations make investments in passive assets (including interest- and dividend-generating financial instruments) that could be made directly from the United States.

Under the CFC rules, if one or more U.S. persons that own 10% or more of the voting power of a non-U.S. corporation together own more than 50% of the voting power or value of an entity treated as a non-U.S. corporation, then the non-U.S. corporation will be treated as a CFC with respect to such 10% U.S. shareholders. As a result, each such 10% U.S. shareholder will be required to include in income, on a current basis, for U.S. tax purposes its pro rata share of the CFC’s “subpart F income,” which includes dividends, interest and capital gains, for the year, and a portion of its long-term capital gains attributable to non-subpart F accumulated earnings and profits may be subject to ordinary income tax rates. 10% U.S. shareholders of, as well as certain other U.S. persons involved with, non-U.S. corporations are required to provide information annually regarding the corporation on IRS Form 5471, as well as to report their subpart F income on IRS Form 5471 with their annual U.S. tax filings.

Under the PFIC rules, which can apply only to investors with respect to whom the CFC rules do not apply, if a non-U.S. corporation has 75% or more passive income (for example, interest, dividends or capital gains) or holds 50% or more of its assets for the production of passive income, then the non-U.S. corporation will be treated as a PFIC with respect to all relevant U.S. taxable investors, regardless of the size of shareholding and amount of voting power (or lack thereof). If a U.S. taxable investor is invested in a PFIC, then, very generally, it can elect to (i) defer U.S. taxation until it actually disposes of its shares, at which time it will pay taxes at ordinary income rather than long-term capital gains rates, plus an interest charge (the “excess inclusion” regime), or (ii) make a “qualified electing fund” (QEF) election with respect to the PFIC (and any lower-tier PFIC owned by the PFIC), which will require the U.S. taxable investor to take into account its pro

© 2017 EMPEA8

rata share of all of the PFIC’s earnings and profits for the year, but continue to recognize long-term capital gains on the disposition of shares (the QEF regime). U.S. taxable investors that hold a direct or indirect interest in a PFIC are required to report annually certain information regarding their ownership of the PFIC on IRS Form 8621. U.S. taxable persons that make a QEF election are required to obtain a PFIC annual information statement, as prescribed in the applicable U.S. regulations, from each non-U.S. corporation with respect to which an election is being made and to make/maintain such election, and to take into account its pro rata share of the PFIC’s earnings and profits, on an annual basis on IRS Form 8621. The CFC and PFIC filings, and in particular the making of the QEF election, are made by the first U.S. person (individual, corporation, partnership or taxable trust) in the chain of ownership above the offshore fund, and under certain circumstances duplicate filings may be required.

Even if CFC and PFIC filings are not required, certain U.S. persons transferring money offshore or investing in foreign partnerships and corporations may be required to file information reports with the IRS, including on IRS Form 926 and IRS Form 8865, among others.

In the context of an India-focused private equity fund, investment in the upper-tier fund entities themselves (namely the offshore fund and the onshore fund, and any other entity within the chain of entities holding shares in the portfolio company) will not be subject to the CFC or PFIC rules, so long as those entities are treated as pass-through entities for U.S. tax purposes. However, the underlying portfolio companies may qualify as CFCs or PFICs with respect to U.S. taxable investors, and their status as such will generally need to be tested

on an annual basis with respect to each portfolio company (and certain subsidiaries owned by each portfolio company). In general, Indian portfolio companies held by a private equity fund structured as an offshore fund in Mauritius tend not to be CFCs (given the diversity of ownership within the private equity fund). Even if they qualify as CFCs, their income generally constitutes “active” income from sales or services within India, or is otherwise not treated as a subpart F income. This renders the application of the CFC income inclusion rules without practical effect. Further, if a portfolio company is a CFC, then gain recognized on the disposition of the portfolio company may be recharacterized as dividends for U.S. tax purposes and taxed, in part, at ordinary income rates unless they are treated as qualified dividends by reference to the U.S.-India tax treaty and certain other conditions are met.

Similarly, Indian portfolio companies, as operating companies, tend not to be PFICs, although the application of a “passive assets” test under the PFIC rules and the per se treatment of cash on hand as a passive asset may render an otherwise active Indian operating company as a PFIC. As a result, U.S. taxable investors investing in an India-focused private equity fund should be mindful of the potential application to them of the CFC and PFIC rules. In this regard, they should ensure that the offshore fund and India-based manager are aware of the potential application of these rules, have procedures in place to monitor the circumstances under which these rules may apply and to provide U.S. taxable investors with the information that they require in order to comply with the rules and properly report their income. Commitments regarding CFC and PFIC monitoring, and the provision of information of related information, are generally obtained through side letters with the offshore fund or the fund sponsor.

ConclusionStructuring investments to increase tax efficiency has always been a difficult task for funds with a diverse investor base and involves the consideration of multiple tax rules as they apply in varying circumstances. In the cross-border context, this task becomes even more challenging. In the case of an India-focused private equity fund, fund sponsors and their U.S. tax advisors will need to monitor closely Indian tax developments imposed on investment income/gains, as well as the tax status of each portfolio company within the platform for U.S. tax purposes. Special consideration also should be given to the rate at which Indian tax is imposed, as FTCs may not be available to be utilized by U.S. taxable investors, and U.S. tax-exempt investors would likely experience any Indian tax as a non-creditable/non-deductible investment expense.

About the Authors

Olivier De Moor is Partner at Akin Gump Strauss Hauer & Feld LLP

Brett Fieldston is Counsel at Gump Strauss Hauer & Feld LLP

EMPEA Legal & Regulatory Bulletin | FALL 2017 9

Introduction As India’s economy has grown, so has its stressed assets. Stressed assets, which comprise non-performing assets (NPAs), restructured loans, and written-off assets, account for about 16.6% of total loans, which is the highest level out of all major economies. This problem is acute in assets related to industries such as infrastructure, steel, iron, and cement. With the Indian government and the Reserve Bank of India (RBI) mandating Indian banks to clean their balance sheets and making efforts in bringing regulatory reforms in participation in the debt market and improving security enforcement process, foreign investors have patently made a bee-line to participate in the Indian distressed market through the use of investment vehicles. Today, there are 3 potential investment vehicles in India that foreign investors could choose from: (a) Alternative Investment Funds (AIFs), (b) Asset Reconstruction Companies (ARCs), and (c) Non-Banking Finance Companies (NBFCs). The decision on which vehicle to choose largely depends on 2 parameters: (a) the kind of instruments that foreign investors want exposure to, and (b) the level of control that foreign investors wish to exercise in identifying assets and their ultimate resolution.

AIF as a Debt Investment Vehicle and Key Considerations for Foreign Investor ParticipationAIFs: In 2012, the Indian securities regulator, the Securities and Exchange Board of India (SEBI), enacted regulations governing AIFs. AIFs are pooling vehicles (such as trusts, limited liability partnerships, companies and other body corporates) that can pool

Foreign Investment in Distressed Debt in India: What’s the Best Vehicle?By Ganesh Rao, Partner and Pallabi Ghosal, Senior Associate, with assistance provided by Nayan Banerjee, Associate, AZB & Partners

monies from both Indian resident and offshore investors for deployment in Indian and, to a limited extent, in foreign companies. Depending on the investment objective and strategy of the AIF, AIFs are categorized as Category I (venture capital, infrastructure, social venture, small and medium enterprise, and angel funds), Category III (primarily listed, hedge funds, complex structured products) and Category II (miscellaneous including debt and real estate funds) AIFs. A Category II AIF, being a debt fund, can invest primarily in debt securities (both listed and un-listed), most common being non-convertible debentures (NCDs). It cannot however provide loans. SEBI has adopted a light-touch approach in regulating AIFs and gives flexibility to AIF managers to operate AIFs. Pursuant to liberalization, foreign investors can now invest in AIFs without seeking any Indian governmental approvals. Typical models used by foreign investors today are as follows: (a) as passive investors, foreign investors’ capital is managed (along with other investors in the AIF pool) by a local partner who sources deals and decides which deals to invest in and divest from; (b) foreign investors work with a local partner to identify deals and the decision to invest or not is made by the foreign investor (the typical ‘separately managed account’ model); or (c) foreign investors enter into joint venture arrangements with the local partner/manager and jointly decide whether or not to make an investment and divestment.

Pros: If structured appropriately, using AIFs as a debt investment vehicle has a number of benefits, including: (a) under Indian income tax laws, Category II AIFs (including debt funds) have a ‘pass-through’ status i.e. the rate of tax payable by a foreign investor

is the same as what the foreign investor would have had to pay if the investment was made directly in the portfolio entity; (b) Category II AIFs are categorized as ‘Qualified Institutional Buyers’ (QIBs) and hence may be able to invest in security receipts (SRs) issued by ARCs (refer to section on ‘ARCs’); and (c) foreign investors can invest through the Category II AIF in listed and unlisted debt instruments which otherwise would require foreign investors to obtain a foreign portfolio investor (FPI) license and/or comply with RBI’s guidelines on external commercial borrowings, which could be onerous.

Cons: The key downsides to using a Category II AIF are as follows: (a) undertaking of leverage at the AIF level is restricted to only for meeting temporary funding requirements; (b) a Category II AIF is closed ended and has a limited life; and (c) a Category II AIF itself may have no special enforcement rights (refer to section on: “The Role of Insolvency and Bankruptcy Code, 2016 (IBC)”). Given the lack of enforcement rights, typically foreign investors use a combination of AIFs and ARCs and/or NBFCs.

Comparing Roles of ARCS and NBFCS: How Foreign Investors can ParticipateARCs: ARC is a registration that RBI gives to a company under the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (‘SARFAESI Act’). ARCs can act as managers to securitization trusts that acquire distressed debt. The securitization trusts then issue security receipts (SRs) in relation to the underlying debt portfolio that the trust has acquired,which in turn may be subscribed to by QIBs.

© 2017 EMPEA10

For the ARC to have skin in the game, they are required to subscribe (and hold until redemption) at least 15% of the SRs in each scheme. An ARC can acquire distressed debt portfolio in 2 ways: (a) by bidding in a public auction process; and (b) through bilateral arrangements between the holder of the debt and the purchaser. ARCs can acquire debt that meets a certain regulated grade of distress as prescribed by the RBI. Under the guidelines issued by the RBI, a bank offering stressed assets for sale shall offer the first right of refusal to ARCs which have already acquired the highest and at the same time a significant share (~25-30%) of the asset, for acquiring the asset by matching the highest bid. For undertaking such asset reconstruction, ARCs may charge management fees which are subject to limitations prescribed by the RBI.

Pursuant to liberalization, persons resident outside India can invest in the capital of ARCs up to 100% without seeking any approvals. However, the total shareholding of an individual FPI in an ARC should be below 10%, but if compliant with this requirement, an FPI can invest up to 100% of each tranche in SRs issued by ARCs. Despite liberalization, foreign investors still prefer partnering with local partners for participating in the debt portfolios of ARCs given that the local partners are better equipped to deal with regulatory and other demands on the ARC business.

NBFCs: An NBFC is a financial services company that is licensed by the RBI to operate in the Indian market. An NBFC is subject to the RBI mandated 50:50 test i.e. the company’s financial assets should be: (a) more than 50% of total assets (netted off by intangible assets); and (b) income from financial assets should be more than 50% of the gross income. NBFCs are broadly classified as deposit-taking or non-deposit taking and systemically or non-systemically important and depending on the classification, are required to maintain capital adequacy ratios prescribed by the RBI. Historically, NBFCs have been widely used as debt investment vehicles

A comparison table between ARCs and NBFCs is as follows:

CRITERIA ARCS NBFC (NON DEPOSIT TAKING)

Ease of structuring

Permitted to set up securitization trusts and issue SRs where the underlying asset is the financial asset and therefore, structuring returns to investors based on return on the underlying debt is relatively easy.

Not permitted to issue SRs, and therefore, alternative complex structures will need to be adopted in order to link the investor returns to the underlying debt.

Accounting Given that the ARC acquires the financial asset on the books of the trust, it does not have to make provisioning requirements on its own books for NPAs.

Given that the NBFC will be acquiring the financial assets in its own books, it will need to comply with provisioning requirements for NPAs.

Investment / loans

• Cannot give loans except to its own portfolio companies per regulations.

• Restricted options for investment by ARCs (e.g. government securities etc.).

Can invest in/give loan to companies which are not NPAs but distressed. This can help in turnaround of distressed companies.

RBI approval for change of management

Yes, for substantial changes of management (appointment of a director, managing director or CEO).

Yes for the following: (a) takeover or change of control (regardless of whether or not it results in a change of management); (b) the transfer of 26% of shares in the NBFC; or (c) a change of 30% of the board (excluding independent directors).

Stamp duty on acquisition of distressed debt portfolio

No (there is an exception under SARFAESI).

Yes.

Ability to borrow under the ECB guidelines

No, ARCs are not permitted to borrow under India’s ECB guidelines.

Yes, NBFCs are permitted to borrow under the ECB guidelines.

Tax implication Securitization trusts receive a complete tax pass through. The income is taxed in the hands of its investors. This would also apply to trusts set up by reconstruction companies or securitization companies for the purposes of the SARFAESI Act.

Dividends declared by NBFCs will be exempt in the hands of its shareholders, but the NBFC would be required to pay dividend distribution tax. Similarly, consideration paid by NBFCs to its shareholders pursuant to a share buy back would be exempt in the hands of its shareholders, but taxable in the hands of the NBFC.

Listing No current framework for listing of SRs. However, in its latest budget, the Indian government has allowed listing of SRs, and SEBI is expected to form guidelines for listing of SRs during the current financial year.

NBFCs can be listed

EMPEA Legal & Regulatory Bulletin | FALL 2017 11

primary because NBFCs are able to undertake a broad range of financial activities. However, up till now, NBFCs were not used for asset reconstruction due to lack of availability of powers under the SARFAESI Act. Pursuant to a recent notification, 196 NBFCs (having an asset size of INR 500 crores and above) have been notified as “financial institutions” and may, subject to certain restrictions, exercise rights given to ARCs under the SARFAESI Act. While the recent notification will likely give NBFCs greater power to be involved in the stressed assets industry, NBFCs (unlike ARCs) will not be able to issue SRs, thus restricting their ability to raise funds for acquiring financial assets. Foreign investment in NBFCs has been liberalized, and the earlier stipulations on capitalization by foreign investors, the quantum of existing foreign investment in the NBFC and the activity carried out by the NBFC have been done away with. Under the foreign direct investment policy, foreign investment of up to 100% is now permitted in NBFCs. However, foreign investment in NBFCs remains subject to regulations issued by financial sector regulators such as the RBI, the SEBI, and the Insurance Regulatory and Development Authority.

The role of Insolvency and Bankruptcy Code, 2016 (IBC) The provisions relating to corporate insolvency under the IBC were notified in December 2016. The IBC enables financial creditors (including ARCs and NBFCs to whom a financial debt is owed), operational creditors, or the company itself to initiate an insolvency resolution process. An application is made to the National Company Law Tribunal (NCLT) on a payment default of at least INR 100,000. Once the NCLT admits the application and

commences the insolvency resolution process, financial creditors assume control of the company. Financial creditors have a 180 day moratorium (extendable by 90 days) to effect a restructuring of the company, failing which the company is mandatorily liquidated. Unlike under the SARFAESI Act which enables creditors to enforce individual rights, the IBC is a collective insolvency procedure. Accordingly, once a process is commenced under the IBC, SARFAESI rights cannot be exercised as a moratorium is imposed on ‘any action to foreclose, recover or enforce any security interest’. The question that then arises is whether the IBC weakens the role of ARCs and NBFCs. For ARCs and NBFCs to be effective, they will need to enforce their rights under SARFAESI well before an insolvency is triggered under the IBC. Given that in most cases the company in question is on the verge of insolvency, it may be challenging to start and complete the SARFAESI process before IBC comes into play. However, the IBC is a new law that will take time to evolve and during this phase, SARFAESI tools should continue to be useful.

ConclusionFor foreign investors looking to access the Indian debt market, all 3 vehicles, i.e. AIFs, ARCs and NBFCs have their respective benefits depending on the kind of strategy that the foreign

investor investing in India has in mind. From an enforcement standpoint, an ARC may be more advantageous than an NBFC but both vehicles are expensive to establish, is time consuming and heavily regulated by the RBI. Further, ARCs have not been entirely successful in undertaking asset reconstruction largely because the purchase of debt has been expensive and significant cooperation is required from the shareholders and management of the company for the ARC to successfully undertake the reconstruction. Foreign investors will need to carefully analyse the nature of participation it would want in the debt portfolio before making a choice as to whether it wants to use one or a combination of debt investment vehicles for achieving desired results. It will also be critical to keep an eye on the evolution of the IBC in India and how successfully it is able to enforce rights of creditors.

About the Authors

Ganesh Rao is Partner at AZB & Partners

Pallabi Ghosalis is Senior Associate at AZB & Partners

“ Foreign investors will need to carefully analyse the nature of participation it would want in the debt portfolio before making a choice as to whether it wants to use one or a combination of debt investment vehicles for achieving desired results.

© 2017 EMPEA12

The insurance industry in general, and M&A opportunities in Africa, are still in their infancy, and this brings a range of opportunities for international insurers and investors. In contrast to more developed markets, most international insurers have little or no presence in Africa. This helps to explain the fact that Africa’s global market share in the insurance sector is roughly around 1.5%, and the continent’s average insurance penetration rate is 2.9%, falling to 0.9% excluding South Africa.1

These figures stand in even greater contrast compared to the rest of the developed and developing world because according to some metrics, the economic and corporate governance climate appears to be generally favourable for the development of insurance products in Africa and for companies looking to invest there. GDP in sub-Saharan Africa is forecast to grow between 2.6% and 3.2% by

Africa Insurance M&A: Global Insurers’ Next FrontierBy Geoffrey P. Burgess, James C. Scoville, Benjamin Lyon, Sayo Ogundele, Debevoise and Plimpton LLP

2018,2 foreign direct investment has increased by 5% to $50 billion over the past 15 years, and research suggests that a growing middle class is emerging who expect, and can afford, different categories of products from insurers as a consequence of a rising GDP per capita across Africa.3 Cutting against these favourable trends, it is estimated that falling commodity prices will cut growth across sub-Saharan Africa by 1% to around 4%, the slowest rate since the late 1990s. For example, in Nigeria, oil still accounts for roughly 70% of the country’s annual budget, leaving government spending highly dependent on global energy prices.

Meanwhile, the corporate governance, risk management and capital standards in many African countries are being strengthened, mirroring similar efforts being rolled out globally. For instance, European Solvency II – like regimes are being implemented in South Africa

and Kenya, bringing new capital and risk management requirements to insurers located there. Like elsewhere around the world, these new standards present opportunities to acquirers (for instance, if particular business lines are now suddenly more expensive for their current owners to hold), but difficulties for deal-making as well, as acquirers need to understand the new requirements and their impact on valuation and operations.

This article provides an overview of recent M&A activity in the insurance sector in Africa, including commentary on some of the key themes that we have identified. We also summarise some of the main regulatory and compliance issues that an international investor may face when investing in Africa, as well as provide a more in-depth view on the insurance markets in Kenya, Nigeria and South Africa.

1. KPMG, Insurance in Africa 2015, 6/3/2015.2. World Bank, Global Economic Forecast, June 2017.3. PWC, Insuring African Growth – Insurance Industry Analysis, March 2015.

EMPEA Legal & Regulatory Bulletin | FALL 2017 13

Recent M&A Activity and Opportunities in the Insurance SectorBetween 1 August 2016 and 1 August 2017, we have identified approximately 20 insurance M&A transactions involving targets based in Africa. Based on the publically available information on these deals, we have outlined the following themes:

First, there is a lack of qualitative data on Africa Insurance M&A transactions, which makes it difficult to evaluate any trends when it comes to individual and aggregate deal values. We assume that the consideration for most of these deals is significantly smaller compared to insurance deals internationally, given the low overall insurance penetration rates across the continent (excluding South Africa). The largest transaction that was publically disclosed in this period was the acquisition by Leapfrog of a minority stake in Enterprise Group Ltd (Ghana) (US$ 180m) in June 2017.

This leads on to the second trend that we identified: the majority of recent African insurance M&A has been limited to a handful of African jurisdictions. For example, the target company was based in South Africa in 13 of the 20 transactions we identified. We also did not identify any transactions where the target was not based in South Africa, Nigeria, Ghana, Zimbabwe or Malawi.4 We make multiple references in this article to the potential opportunities for insurers in “Africa”, but, for a multitude of reasons, Africa is not a homogenous continent that is suited to a “one size fits all” analysis. There are reasons to be optimistic that insurance M&A in the aforementioned jurisdictions has the

potential for significant growth in the short-to-medium term, but this should be evaluated alongside the fact that only a few countries in the continent (due to political, regulatory, economic or religious reasons) show positive signals that their insurance markets will develop significantly for the foreseeable future, especially considering the recent economic challenges facing most of the continent, such as falling commodity prices, weakening local currencies and higher borrowing costs due to central banks increasing their interest rates.

The final trend is that the majority of purchasers are South African, European or U.S. based insurance companies who are seeking either to consolidate their portfolios in existing markets, or to use the target vehicle as an entry-point into a new market in Africa. For example, the following major insurers have recently made investments in Africa: Prudential Financial Inc. (through its separate account managed by Leapfrog in Enterprise Group Limited (Ghana)), Prudential plc (in Zenith Bank (Nigeria)), AXA (in Mansard (Nigeria)), Old Mutual (in Oceanic Life (Nigeria), Provident Life (Ghana) and UAP Holdings (Kenya)), and Swiss Re (in Ledway Assurance (Nigeria)). We understand that none of the major insurance companies based in Asia have made or are imminently planning on making any acquisitions of insurers in Africa.

With a few exceptions, there is a notable absence of bank and private equity purchasers in the deals we reviewed. In the case of the former, we are seeing the growing use of bancassurance in more developed markets due to banks’ established infrastructure and existing client

base. By way of example, in July 2017 Prudential plc announced the acquisition of a majority stake in Zenith Life (Nigeria) and an exclusive bancassurance partnership with Zenith Bank in Nigeria. This, combined with the advancement of consumer facing technology and the growing use of “microinsurance”, could provide banks in Africa with unique opportunities to engage new and existing customers that are not available to non-bank competitors. Regulations in certain African jurisdictions, however, may prohibit a bank from directly or indirectly owning an insurance company or participating in insurance-related activities. We have seen increasing use of a “financial services” model whereby both a bank and an insurer are held as subsidiaries, allowing the group to provide services to each other and share infrastructure.

Investor Differentiation—Strategics v. Non-StrategicsOne area of interest for market participants is how insurance firms compete with non-strategic investors for acquisitions and partnerships with local insurance companies.

Some advantages that insurance companies have over non-strategic investors include technology and systems expertise, as well as the ability to transfer products that they have developed in their home markets. Insurers are also more likely to be subject to more stringent regulatory requirements, so this can help to facilitate the development of sound corporate governance in any local African target consolidated into their portfolio, as well as local regulatory

4. Sources: S&P, Capital IQ search.

“ Some advantages that insurance companies have over non-strategic investors include technology and systems expertise, as well as the ability to transfer products that they have developed in their home markets.

© 2017 EMPEA14

approvals. Finally, local insurance operators may prefer to collaborate with global insurance firms as they are perceived to be longer-term investors, and operating synergies that arise as a result of an acquisition or partnership may give the purchaser flexibility to pay a higher price than a non-strategic investor for the local insurer.

We expect there will be increased interest amongst non-strategic investors for African insurance companies. Some of the advantages accessible to non-strategic investors include a greater access to capital (there were 145 PE deals reported in Africa in 2016, amounting to US$3.8bn, versus US$2.5bn in 2015), and the ability to retain and incentivise management through attractive equity arrangements. Overall, we expect that the private equity investments will initially take the form of minority and majority investments (i.e., not 100% transactions) in insurance companies. Because of the challenges involved in the integration of new acquisitions into a multinational group structure from a legal, compliance, governance, reporting and parent policy compliance, a private equity firm can add value to an African target by conforming a target’s compliance policies and procedures to regulatory requirements that are applicable to the private equity investor. This will also help smooth an exit sale to a strategic company.

Life Insurance v. Non-Life InsuranceAccording to the Africa Insurance Organization, the total value of Africa’s insurance premiums was $64 billion in 2015, meaning Africa’s share of the global market was approximately 1.1% (US$20.4bn) for non-life insurance premiums and 1.8% (US$43.7bn) for life insurance premiums. Non-life insurance penetration levels in all African countries except for South Africa is lower than the global average of 2.7% with five countries (South Africa, Morocco, Egypt, Kenya and

Nigeria) accounting for 85% of total insurance premiums in Africa. Currency depreciation remains the main cause for the declining premium volumes in US$ terms, although only Nigeria and Libya experienced negative real premium growth (adjusted for inflation) in original currency terms in 2015.5

Life insurance remains underdeveloped for various reasons, including limited awareness of life insurance products and low average earnings across the continent making life insurance an unaffordable option for large parts of the population. The absence of reliable independent data on mortality and longevity statistics in Africa, due to the underdeveloped life insurance sector, may make it a less appealing area for investment.

As noted above, however, Africa has a growing middle class that can afford a broad range of insurance products, including life insurance services, so we would expect to see growth in this area as more international insurers enter high-growth opportunities in Africa. There are several markets where it may be impractical or unduly time-consuming for a strategic to obtain an insurance licence to operate from the local regulator. For some insurers, therefore, acquiring an existing life insurance company may be the most effective entry route into accessing an existing customer base in Africa, to which the insurer can then cross sell other insurance products in its existing portfolio.

Anti-Bribery ComplianceCorruption in some jurisdictions in Africa raises the costs and risks of doing business, deters international investment, distorts prices and hinders economic growth. There is a constantly evolving legal landscape attempting to fight corruption, with increasingly aggressive international and local legislation, regulation and enforcement. For example, anti-bribery laws applicable to companies that do business in the United Kingdom and the United States have an extraterritorial

“ Life insurance remains underdeveloped for various reasons, including limited awareness of life insurance products and low average earnings across the continent making life insurance an unaffordable option for large parts of the population. The absence of reliable independent data on mortality and longevity statistics in Africa, due to the underdeveloped life insurance sector, may make it a less appealing area for investment.

5. African Insurance Organisation, Africa Insurance Barometer 2017

reach, extending to portfolio companies and their representatives internationally. An insurer may also be penalised in its home jurisdiction for any breaches by a portfolio company. For example, there is a risk that criminal activities at or involving the target or entities that it controls could expose a U.S. insurer’s affiliates to being disqualified as a qualified professional asset manager (“QPAM”) under ERISA, and such status as a QPAM is generally required to provide investment management services to ERISA-covered plans. Disciplinary infractions involving the target could disqualify the target and a U.S. insurer’s affiliates from engaging in certain other activities under the U.S. securities laws.

EMPEA Legal & Regulatory Bulletin | FALL 2017 15

A foreign buyer should strive to undertake rigorous pre-transaction diligence in order to minimise its risks and ensure that it receives an appropriate valuation of the target company. It is not always possible, however, to perform complete anti-corruption diligence and there may be limitations as to the quality of information that an African seller is able to provide. To the extent that pre-transaction diligence is unable to be carried out, potential investors should ensure that they undertake post-transaction diligence to identify any anti-bribery risks as soon as possible.

The inclusion of contractual protections in a purchase agreement and shareholders’ and investment agreements may mitigate the risk of anti-bribery liability. These could include appropriate representations and warranties from the seller that it has complied with all relevant antibribery legislation and full audit rights for the investor of the target between signing and closing of the transaction to undertake continued diligence. Strong termination rights and post-closing indemnities should be built into the acquisition agreement if the local partner is found to have breached any anti-bribery undertakings. Further, the investor could seek an adjustment of the purchase price upon the occurrence of such an event. A foreign investor buyer should also have comprehensive governance rights in the shareholders’ agreement to ensure that its joint venture company complies with its regulatory obligations.

Enforcement IssuesLocal courts in Africa have a reputation for being weak, slow and inefficient, and local arbitration may be inadvisable. Therefore, we expect global investors, where possible, to submit to the jurisdiction of a non-African court or decide to arbitrate in the event of a dispute with its local partner. There are, however, some matters that cannot be contracted out under the laws of certain African

jurisdictions. Although most African jurisdictions are signatories to the New York Convention, which should, in theory, make the process of enforcing a foreign arbitral awards in a local court straightforward, there are some signatories to the Convention that have a poor record of enforcement.6 This should be borne in mind when selecting the seat of arbitration.

Counterparty credit risk is another issue to consider, as local partners are unlikely to have the same access to capital as some of the larger multinational insurers. Foreign investors should therefore consider obtaining offshore collateral, third-party guarantees and, where applicable, representation and warranty insurance prior to entering into an investment or joint venture arrangement with a local partner.

Bilateral investment treaties (BIT) may be available to protect investments against expropriation without adequate compensation. There are over 2,200 investment treaties in force and they can provide for international arbitration of treaty claims as an alternative to local courts. Depending on how a deal is structured it may be possible to benefit from more than one BIT.

Local MarketsAs mentioned above, Kenya, Nigeria and, in particular, South Africa currently dominate the insurance market in Africa and account for the vast majority of recent M&A transactions. Below is a brief summary of the key features of each of these jurisdictions for those looking to move into the insurance space. Annex I (pages 17-19) contains a further summary of the insurance markets for these jurisdictions.

Kenya and East AfricaAlthough there is no regulatory framework supporting a cross-border insurance regime in East Africa, there are ongoing discussions within the East Africa Community trading block and cooperation among the member

states geared towards having similar legal frameworks and combined regulatory supervision for cross-border transactions. Some steps have already been taken towards achieving this. For example, in relation to local ownership, the law in Kenya prescribing a minimum local ownership requirement was expanded to include East African citizens rather than just Kenyans. It is noteworthy that some of the other East Africa Community members, in particular Rwanda and Uganda, do not have any local ownership requirements, and it is hoped that this will influence the other East African jurisdictions. It is worth noting that the East African Insurance Supervisors Association (EAISA), whose role is to provide uniformity in the East African region, in 2016, developed a practical guide to oversee activities of insurance firms operating in more than once one country. It is envisaged that these guidelines will help in setting standards in insurance service delivery as well as increasing efficiency in the market. Further, the guidelines will make it possible for a regulator in one country to acquire necessary information from sister regulatory organizations concerning cross border insurance companies.

In Kenya, there is currently a significant focus on anti-money laundering and anti-bribery enforcement, which should make it easier for global insurers entering the market to institute and enforce their home nation AML requirements. The spotlight is also on merger control requirements, which are strict, and even seek to police mergers consummated offshore but with an effect in Kenya.

In many East African jurisdictions, bancassurance is key for distribution as banks already have the necessary infrastructure in place, as well as local relationships and trust. The financial services model has also recently grown in popularity as a way of structuring bancassurance offerings, with both the bank and the insurers as subsidiaries of the same non-operating holding parent.

6. E.g., IPCO (Nigeria Limited) v. Nigerian National Petroleum Corporation.

© 2017 EMPEA16

NigeriaPrivate equity firms are very active in the Nigerian market, joining European, North and West African entities, which are already active buyers. M&A is seen as the only realistic route to real growth for an insurer so there are many opportunities available. Local regulators have welcomed the presence of private equity investors into Nigeria, and we could begin to see insurers as secondary investors acquiring from PE firms once the PE investors have done the legwork, such as restructuring and implementing corporate governance arrangements.

Despite foreign direct investment in Nigeria reaching a record low of $624.87 million in the second quarter of 2015, the insurance industry in Nigeria is generally perceived as being one of the most welcoming jurisdictions for foreign investment in Africa. Nigerian law does not prohibit a foreign investor owning 100% of a local insurance company (although in practice, the Nigerian regulators would prefer a local company not to be wholly owned by foreign investors).

A key consideration when doing business in Nigeria is that regulation is often unclear, for instance regarding bancassurance, and enforcement of existing laws is relatively weak.

South AfricaThe new “Solvency II”style solvency and capital regulation which is being introduced in South Africa will change the market considerably. We are already seeing some players looking to diversify out of the market or redistribute their assets as it is unclear whether assets in other jurisdictions will be recognised for solvency purposes. Once the new regulation is brought into force and the market adjusts, South African insurers may attempt to enter the European market, and more European entities may begin looking to the South African market, although this could be some way off.

South Africa could be an attractive entry point from which to develop a broader African presence. However, it is important to bear in mind the Black Economic Empowerment codes, which apply to all entities operating in South Africa. An entity not complying with the codes may face difficulties in doing business in South Africa.

Conclusions—What Next for Industry Participants?South African insurers and other Pan-African consolidators are already actively making acquisitions in African developing markets. These deals combined with the lack of greenfield opportunities imply that global insurers looking to enter the market will need to develop their African insurance strategy and weigh-up the risks involved.

We expect that investors will initially focus on nonlife insurance in a handful of the most promising jurisdictions, including Kenya, Nigeria, South Africa and Ghana due to their fast growing economies and relatively stable legal and regulatory environments. In contrast, there are some jurisdictions in Africa where we do not envisage significant developments in the insurance M&A sector due to unacceptable regulatory constraints, political and economic uncertainty, and a lack of potential customers.

There are certain parallels between Africa today and Asia and Latin America in the 1980s, including a growing middle class, a developing financial sector and increasing political stability. Asia’s world premium of insurance volumes doubled between 1977 and 1992,7 and it would not be wholly surprising if a similar story emerges in respect of Africa today.

There are legitimate concerns over doing business in Africa due to political, economic and anti-bribery and corruption issues, although these risks should not be overplayed. Conducting

satisfactory jurisdictional, operational and historical due diligence, adopting stringent governance policies and obtaining appropriate contractual protections from a local partner should, as a whole, mitigate such risks to an acceptable level for a global insurer seeking to enter or develop its presence in Africa. It’s about time that global insurers realise that the Africa insurance market is a “giant waking up”8 and become a part of its success story.

Acknowledgments We would like to acknowledge the following individuals and firms for their invaluable contributions to this article:

Rosa Nduati-Mutero from Anjarwalla & Khanna in Kenya;

Gbolahan Elias from G. Elias & Co. in Nigeria; and

Kirsten Kern and Langelihle Mnyandu from Bowman’s in South Africa.

Please do not hesitate to contact us with any questions.

About the Authors

Geoffrey P. Burgess, Debevoise and Plimpton LLP

James C. Scoville, Debevoise and Plimpton LLP

Benjamin Lyon, Debevoise and Plimpton LLP

Sayo Ogundele, Debevoise and Plimpton LLP

7. J. Francois Outreville, Theory and Practice of Insurance, 2012.8. https://www.ft.com/content/bc87016a-2430-11e6-9d4d-c11776a5124d

EMPEA Legal & Regulatory Bulletin | FALL 2017 17

CATEGORY KENYA NIGERIA SOUTH AFRICA

Transparency International ranking (2016)

145/176 136/176 64/176

Population (millions) 48.46m 185.9m 55.9m

Life expectancy 62.13 years 53.05 years 57.44 years

GDP ($bn) 70.53bn 405.1bn 294.8bn

Insurance Penetration Rate (Premiums as % of GDP)

<3% <0.5% <14%

Total premiums—non-life insurance

$1.17bn $1.3bn $3.4bn

Total premiums—life insurance

$0.704bn $457bn Information not publicly available.

Market share—non-life insurance

Jubilee (11.58%)UAP (9.03%)APA (7.39%)CIC (6.91%)Britam (5.75%)Others (59.34%)

Leadway (12%)Custodian & Allied (6%)AIICO (5%)Others (77%)

Mutual and Federal Limited (R12.2bn)Outsurance Holdings Limited (R11.6bn)Santam Limited (R22.7bn)Zurich Insurance Company South Africa (R3bn)

Market Share—life insurance

Britam (23.51%)Jubilee (14.1)ICEA LION Life (13.04%)Pioneer Assurance (7.22)Sanlam Life (6.39%)Others (35.74%)

AIICO (18%)Niger Insurance (9%)Mutual Benefit Life (8%)Leadway (8%)Industrial & General (7%)Capital Express (6%)Others (44%)

DiscoveryLiberty Holdings LimitedMMI Holdings LimitedOld Mutual Life Assurance Company South AfricaSanlam Limited1

ANNEX IGhana, Kenya, Nigeria, and South Africa—an Overview9

The below table provides an overview of the insurance industry in each of Kenya, Nigeria and South Africa.

9. Sources include: World Bank, Transparency International, IRA - Insurance Industry Report for the Period January – December 2016.

© 2017 EMPEA18

CATEGORY KENYA NIGERIA SOUTH AFRICA

Regulator Insurance Regulatory Authority (IRA)

National Insurance Commission (NAICOM)

Financial Services Board (FSB)

Key Legislation and Recent Developments

Insurance Act and subsidiary legislationThe Insurance (Amendment) Regulations 2017The Insurance (Amendment) Act 2016IRA Guidelines

Move from a rule-based to a risk-based regulatory regime under draft Insurance Bill, 2014, which would repeal and replace the Insurance Act.

Insurance Act 2003 Short-Term Insurance Act Long-Term Insurance Act

Developments: Move to adopt a “twin peak” regulatory environment with prudential regulation under Solvency Assessment and Management framework (similar to Europe’s Solvency II) and conduct of business regulations under the Retail Distribution Review framework.

Limits on Investments Government securities – up to 100%Cash deposits – up to 30%Equity securities – up to 30%Land and buildings – up to 50%Investment property – up to 70%Secured loans – up to 10%Mortgages – up to 20%Foreign investments – up to 5%Debt investments – up to 10%Fixed deposits – up to 95%Investment in related companies – up to 10%Policy Loans – up to 100%Real Estate Investment Trusts – up to 10%

Securities offered by any one company – up to 20%Quoted equity securities – up to 50%Unquoted equity securities with a minimum credit rating – up to 10%Federal Government securities – up to 100%State government securities with Federal Government guarantee – up to 20%Debt instruments – up to 10%Real estate - 35% (for life insurance funds) or 25% (for non-life insurance funds)

The Acts do not prescribe any proportional limit in relation to the ceiling of investments that an insurer can make into each asset class.

No more than 35% of total retail assets under management in respect of non-life insurers and the investment-linked business of life insurers may be invested outside South Africa.

Equality of treatment between domestic and foreign owned insurers

Yes Yes Yes

Restrictions on foreign ownership of an insurance company

Yes—at least 1/3 must be owned by East African Citizens.

No, but in practice, the Nigerian regulator is unlikely to allow a foreign company to own 100% of a Nigerian insurance company.

No, but no foreign company may own more than 25% of the shares in an insurer without the prior approval of the insurance regulator.

ANNEX I (continued)

EMPEA Legal & Regulatory Bulletin | FALL 2017 19

CATEGORY KENYA NIGERIA SOUTH AFRICA

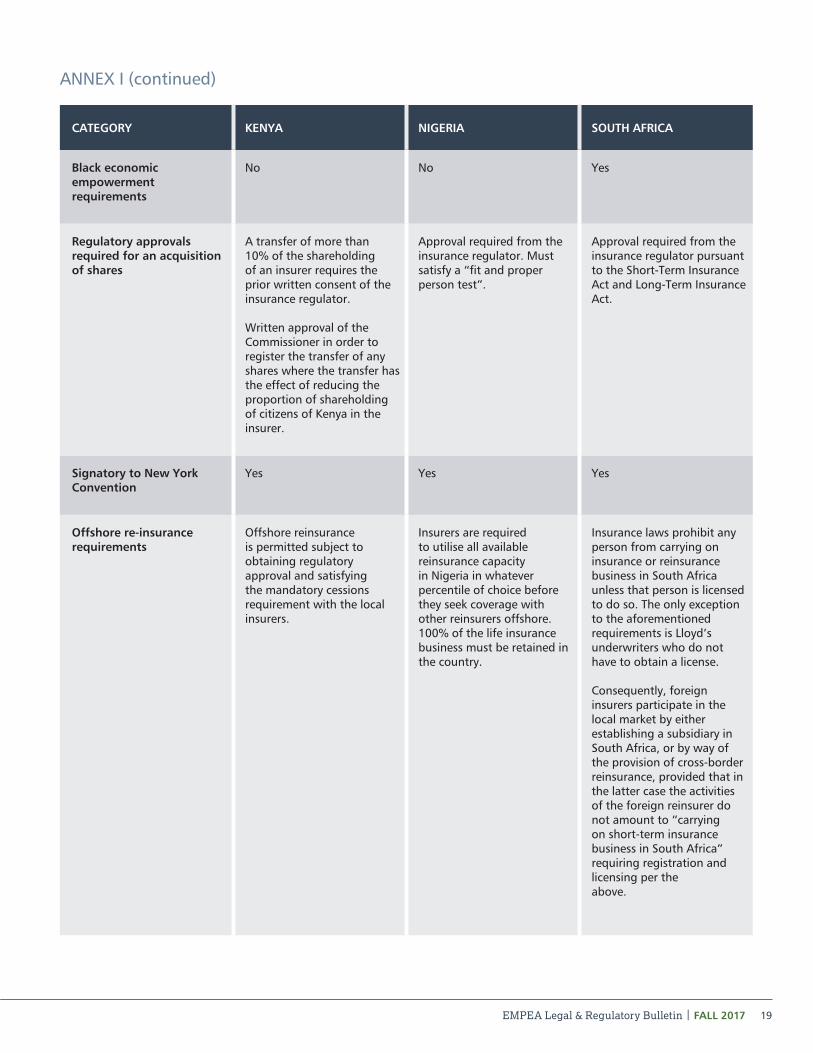

Black economic empowerment requirements

No No Yes

Regulatory approvals required for an acquisition of shares

A transfer of more than 10% of the shareholding of an insurer requires the prior written consent of the insurance regulator.

Written approval of the Commissioner in order to register the transfer of any shares where the transfer has the effect of reducing the proportion of shareholding of citizens of Kenya in the insurer.

Approval required from the insurance regulator. Must satisfy a “fit and proper person test”.

Approval required from the insurance regulator pursuant to the Short-Term Insurance Act and Long-Term Insurance Act.

Signatory to New York Convention

Yes Yes Yes

Offshore re-insurance requirements

Offshore reinsurance is permitted subject to obtaining regulatory approval and satisfying the mandatory cessions requirement with the local insurers.

Insurers are required to utilise all available reinsurance capacity in Nigeria in whatever percentile of choice before they seek coverage with other reinsurers offshore. 100% of the life insurance business must be retained in the country.

Insurance laws prohibit any person from carrying on insurance or reinsurance business in South Africa unless that person is licensed to do so. The only exceptionto the aforementioned requirements is Lloyd’s underwriters who do not have to obtain a license.

Consequently, foreign insurers participate in the local market by either establishing a subsidiary in South Africa, or by way of the provision of cross-border reinsurance, provided that in the latter case the activities of the foreign reinsurer do not amount to “carrying on short-term insurance business in South Africa” requiring registration and licensing per theabove.

ANNEX I (continued)

EMPEA’s regulatory advocacy resources support members

as they seek to encourage legal and regulatory enabling

environments in emerging markets that don’t disadvantage

private investment. Contact: Ann Marie Plubell, VP, Regulatory

Affairs at [email protected].

EMPEA Guidelines set out key legal and tax regimes optimal

for the development of private equity and are now available in

nine languages including Arabic, Burmese, Chinese (simplifi ed

character), Portuguese, Russian, Spanish and Vietnamese on

EMPEA.org.

EMPEA Legal & Regulatory Council draws on deep subject

matter expertise in the emerging markets practice to address

trending concerns such as insights on enforcement and

oversight, confl icts of interest management between investors

and fund managers, views on maturing funds’ portfolios,

expense transparency, changing oversight priorities and

emerging challenges such as cybersecurity and privacy.

EMPEA Legal & Regulatory Bulletin publishes key perspectives

and insights of in-house legal offi cers and leading practitioners

into the current challenges and concerns of the emerging

markets community. Articles are available on EMPEA's online

resource library at EMPEA.org and accessible by keyword search

as well as regional relevance.

EMPEA education courses and resources for emerging market

regulators, pension and policy oversight offi cials highlight the

foundational issues relating to the development and regulation

of private equity in developing economies.

EMPEA General Counsel Member Community engages the

unique perspective of general counsels, legal offi cers and inside

counsel on issues of concern, best practices and emerging

topics related to providing legal services and assuring integrity

to their fi rms and institutions.

Regulatory Aff airs

Resources: