Legacy Gift Planning - Lakeside Ohio · • After donor’s death, remainder goes to charity. 9 Age...

22

1

Transcript of Legacy Gift Planning - Lakeside Ohio · • After donor’s death, remainder goes to charity. 9 Age...

1

Legacy Gift Planning:

Matching the Right Gift

to the Donors’ Circumstances

3

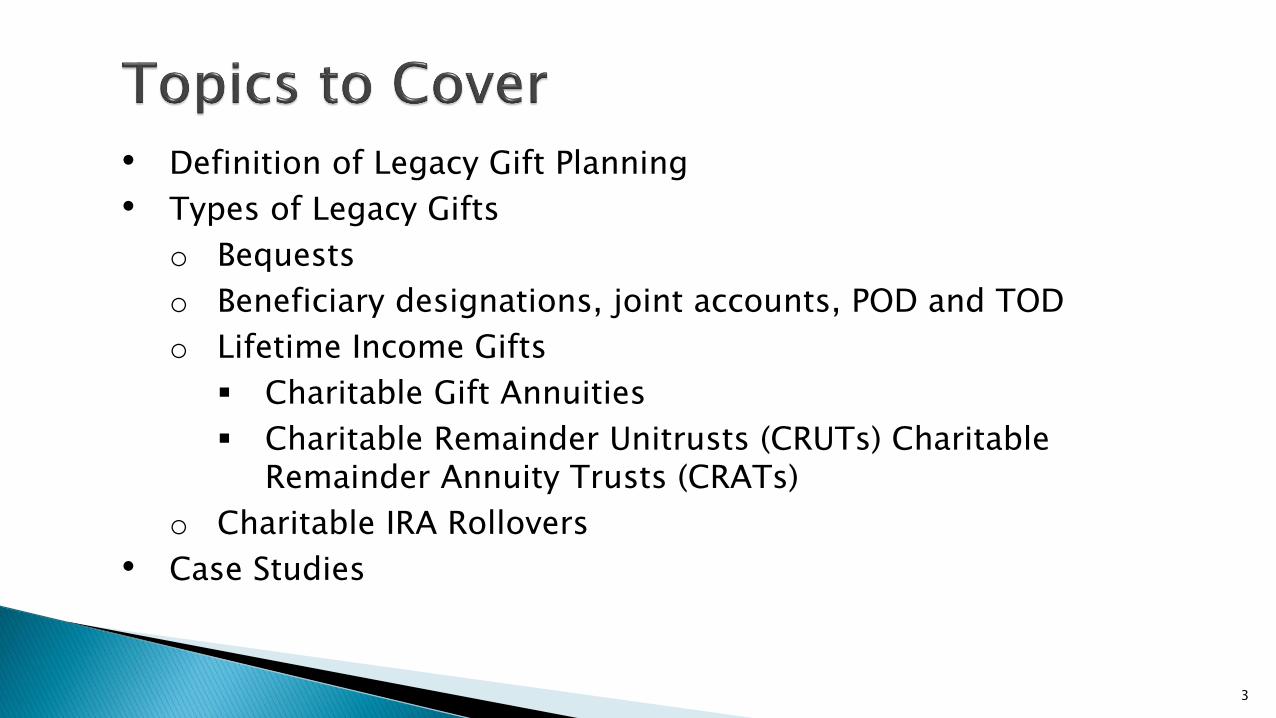

• Definition of Legacy Gift Planning

• Types of Legacy Gifts

o Bequests

o Beneficiary designations, joint accounts, POD and TOD

o Lifetime Income Gifts

Charitable Gift Annuities

Charitable Remainder Unitrusts (CRUTs) Charitable Remainder Annuity Trusts (CRATs)

o Charitable IRA Rollovers

• Case Studies

4

Charitable giving from accumulated resources rather than income.

Income

Wages Interest and dividends

Retirement income Social Security

Annuity payments

Accumulated Resources

Savings Accounts Real Estate

Personal Property Retirement Plans

Insurance Appreciated Securities

5

• A gift established by a provision in your will.

• The easiest way to make the biggest gift.

• Revocable – it can be changed.

• Can be for specific dollar amount or percentage.

• Can be a specific property.

• Can be contingent.

• Can be residual.

• Can take care of family and charities in the same document.

6

• Beneficiary Designations

o Life Insurance

o Retirement Accounts

• Joint property with right of survivorship

• POD and TOD accounts.

7

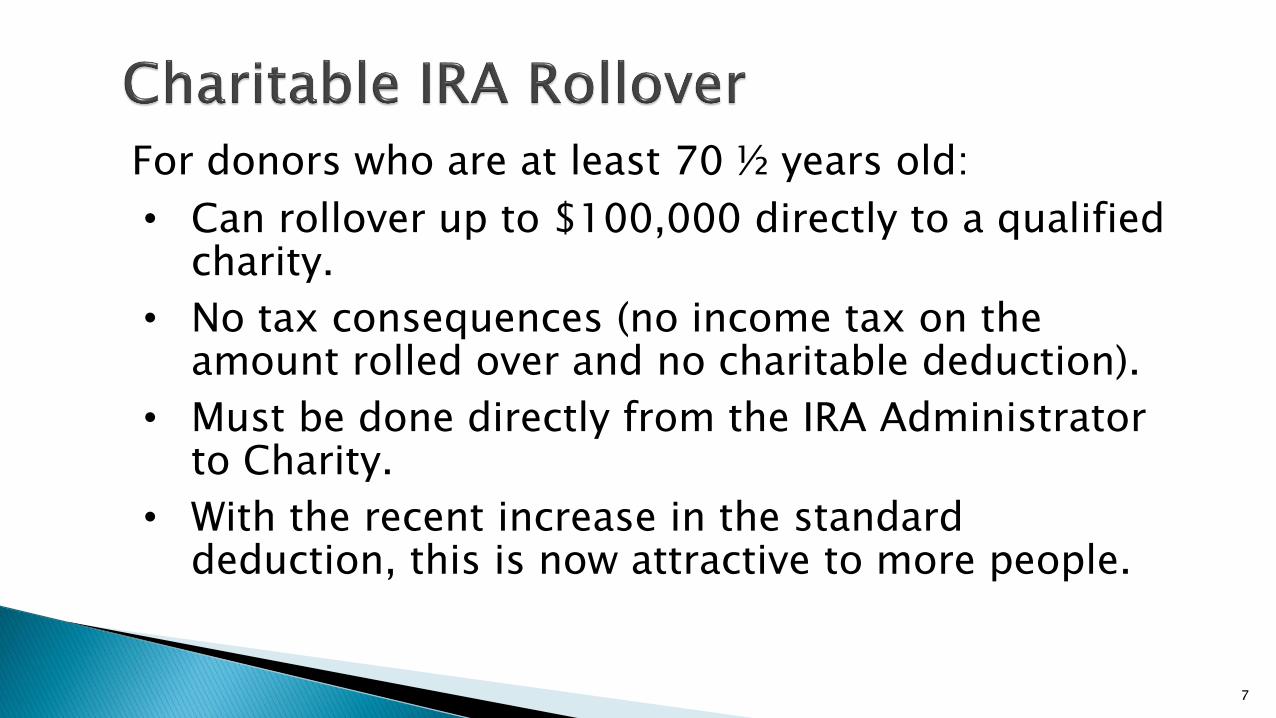

For donors who are at least 70 ½ years old:

• Can rollover up to $100,000 directly to a qualified charity.

• No tax consequences (no income tax on the amount rolled over and no charitable deduction).

• Must be done directly from the IRA Administrator to Charity.

• With the recent increase in the standard deduction, this is now attractive to more people.

8

A charitable gift annuity provides income during donor’s lifetime.

• Guaranteed Income for one or two lifetimes

• Tax advantages o Charitable contribution deduction for the year

of the gift o Part of the annuity income is tax-free

• Age-based rates

• After donor’s death, remainder goes to charity

9

Age Rate Annuity Tax Free

Portion

Charitable

Deduction

60 4.7% $470 $309 $2661

70 5.6% $560 $407 $3,686

80 7.3% $730 $581 $4,763

90 9.5% $950 $855 $6,152

• Offers more flexibility than a gift annuity

• Can pay a fixed amount of income (CRAT) or a fixed percentage of income (CRUT)

• Can be for life or a term of years

• Donor may be able to add to it (CRUT)

• Tax advantages

10

11

• TINKS • Retired • Both have defined benefit plans • No family or children • The millionaires next door. Issue: Losing sleep. “What’s going to happen to our stuff?”

12

Solution: Permanent Endowment with Foundation Both have wills made with contingent beneficiary: Rest, Residue, and Remainder to the Permanent Endowment.

13

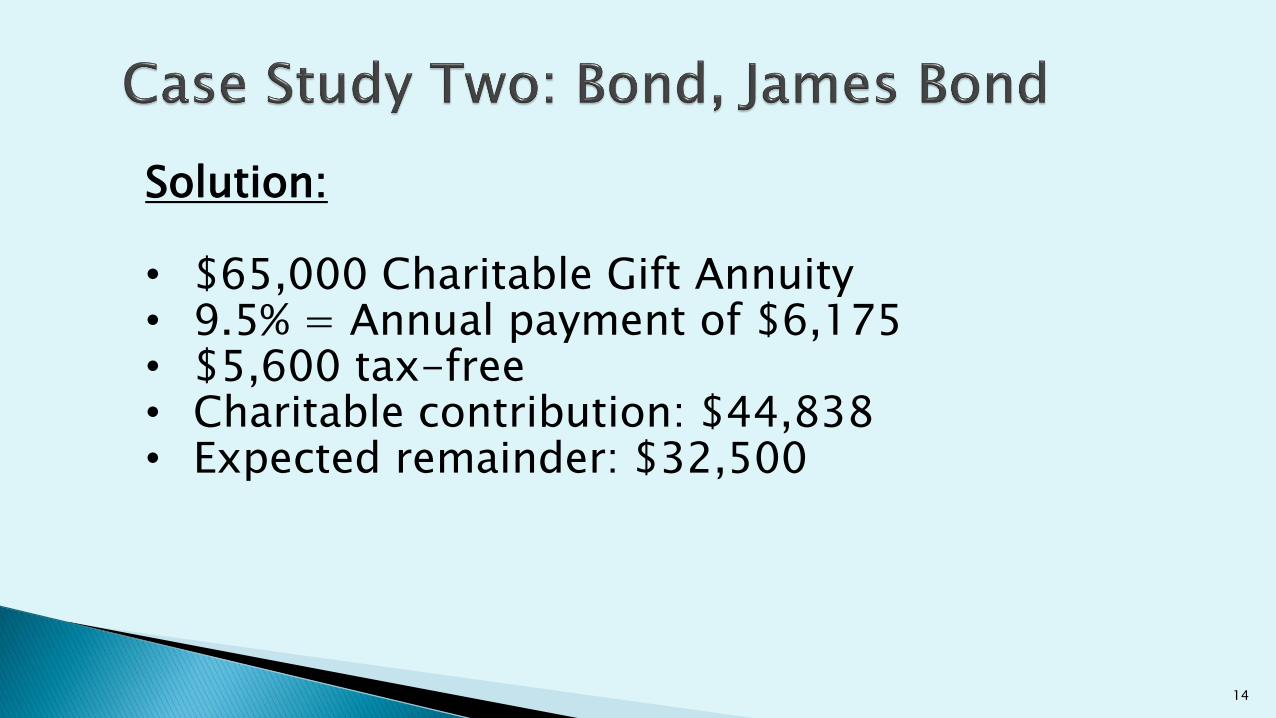

• 93 Years old • Never married, no children • He has $65,000 in redeemable bonds

paying him 6% • His bonds were called Issue: James needs to replace the income.

14

Solution: • $65,000 Charitable Gift Annuity • 9.5% = Annual payment of $6,175 • $5,600 tax-free • Charitable contribution: $44,838 • Expected remainder: $32,500

15

John: 70, retired. Two kids. Yoko: 62, working • Intended to retire to a home John owns in

West Virginia. • BUT, Yoko got a new job in Florida. • Wanted his WV home to benefit his church. • Wanted his kids to get benefit during his

lifetime. • Qualified appraisal: $80,000

16

John wanted a Charitable Gift Annuity that would make payments to his daughters. At the daughters’ ages, the rate is 4.3% Payments to kids: $3,440 But: Foundation’s Gift Acceptance Policy doesn’t permit real estate to be the basis of a CGA, and the policy has a minimum age for CGA recipients.

17

Solution: Donated the house to Foundation to create a NICRUT. Until the house sold, the trust payment would be the net income. After the house sold, it “flipped” to a regular 5% unitrust. The kids split 5% of the market value each year for their lives.

18

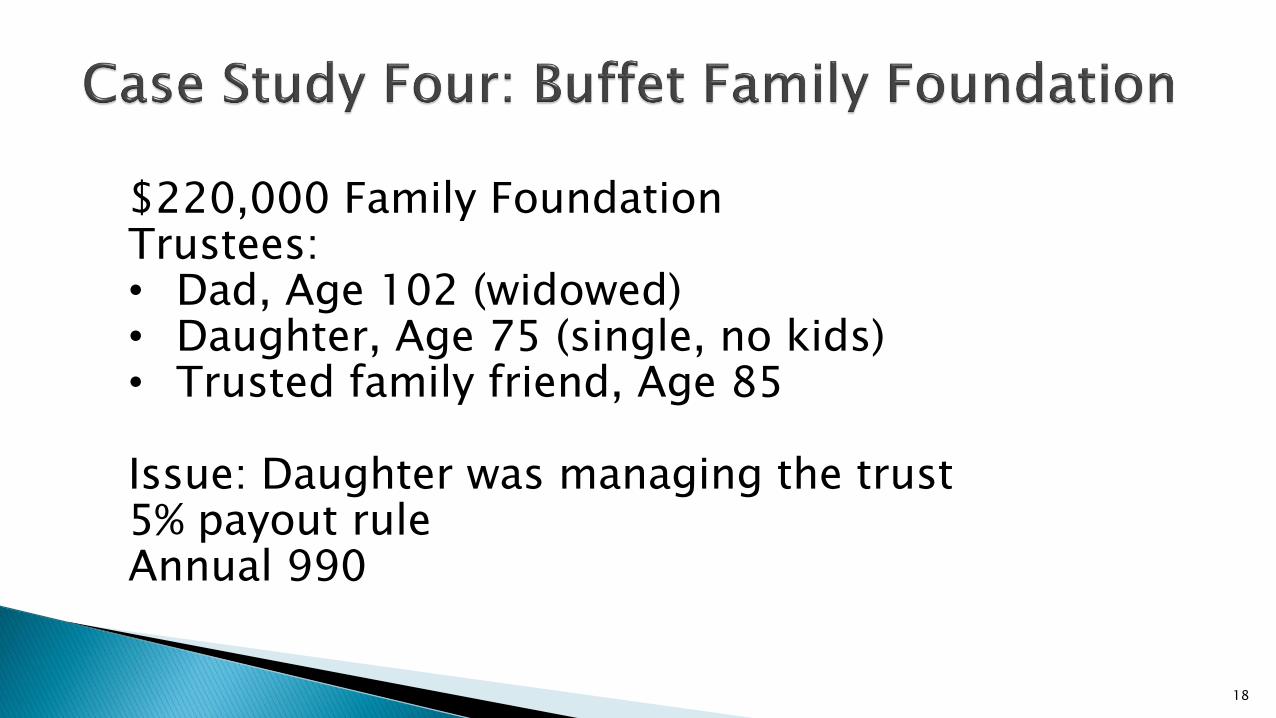

$220,000 Family Foundation Trustees: • Dad, Age 102 (widowed) • Daughter, Age 75 (single, no kids) • Trusted family friend, Age 85

Issue: Daughter was managing the trust 5% payout rule Annual 990

19

Solution: • Dissolved the Family Foundation. • Created Donor Advised Fund with United

Methodist Foundation. • No payout rule • No IRS filings (Included in UM Foundation’s

990) • Former trustee is now adviser

20

• Ima is widowed, Age 90 • Has a will leaving estate to her two grown

daughters • Survivor’s pension plus her own pension • Owns $40,000 HH-series bonds • Wants to “get rid” of the bonds • Daughter had previously converted other

HH Bonds and thought it was a pain • Loves her church

21

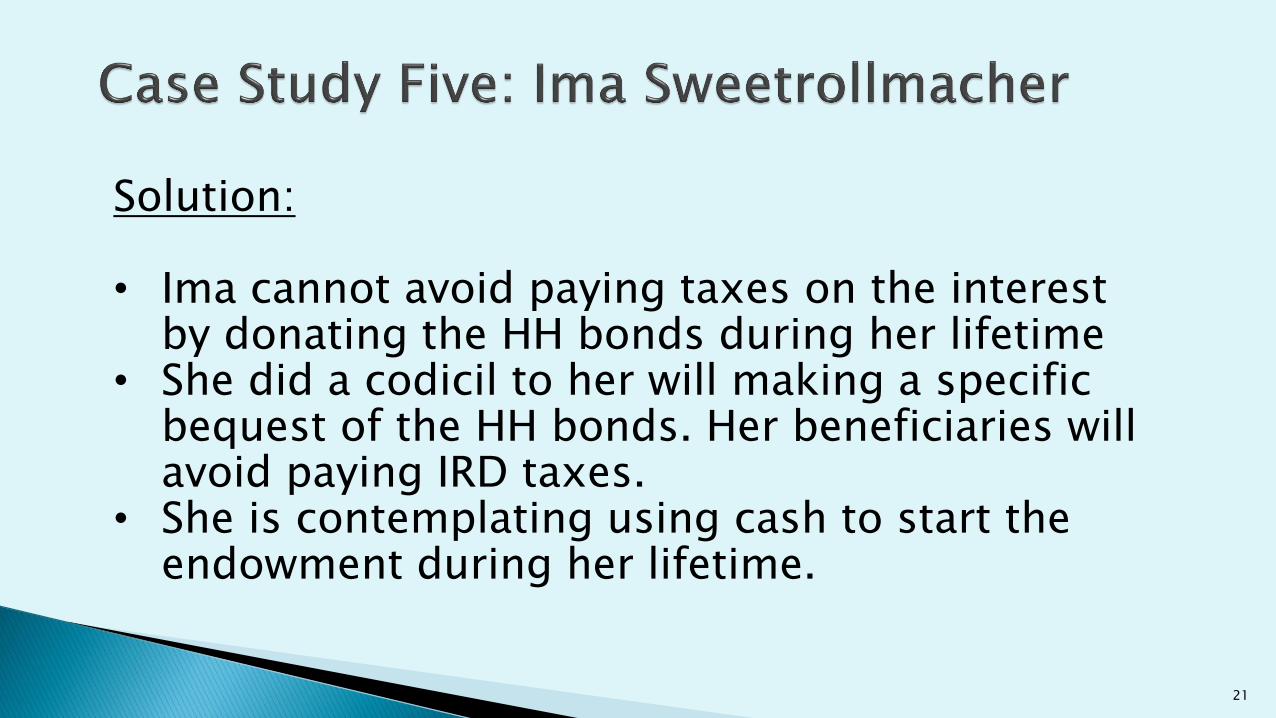

Solution: • Ima cannot avoid paying taxes on the interest

by donating the HH bonds during her lifetime • She did a codicil to her will making a specific

bequest of the HH bonds. Her beneficiaries will avoid paying IRD taxes.

• She is contemplating using cash to start the endowment during her lifetime.

17