Lecture Meeting At Bombay Chartered Accountants Society on ...

35

Lecture Meeting At Bombay Chartered Accountants Society on 4 th August 2010. 1 BY S. S. Gupta Chartered Accountant .

Transcript of Lecture Meeting At Bombay Chartered Accountants Society on ...

Lecture Meeting At Bombay Chartered Accountants Society

on 4th August 2010.

1

BY S. S. GuptaChartered Accountant .

The definition of ‘inputs’ as given inCenvat Credit Rules, 2002

(g) “input” means all goods, except light diesel oil, highspeed diesel oil and motor spirit, commonly known aspetrol, used in or in relation to the manufacture of finalproducts whether directly or indirectly and whethercontained in the final product or not, and includeslubricating oils, greases, cutting oils, coolants,accessories of the final products cleared along with thefinal product, goods used as paint, or as packingmaterial, or as fuel, or for generation of electricity orsteam used for manufacture of final products or for anyother purpose, within the factory of production.

2

Explanation 1. - The light diesel oil, high speeddiesel oil or motor spirit, commonly known aspetrol, shall not be treated as an input for anypurpose whatsoever.

Explanation 2. - Inputs include goods used in themanufacture of capital goods which are furtherused in the factory of the manufacturer;

3

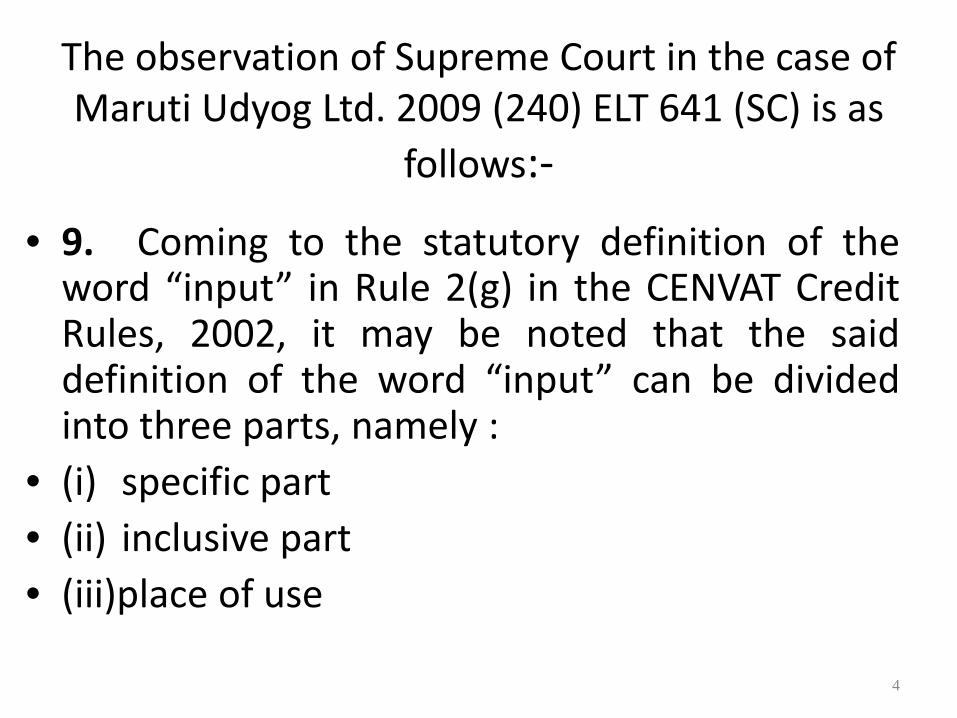

The observation of Supreme Court in the case of Maruti Udyog Ltd. 2009 (240) ELT 641 (SC) is as

follows:-

• 9. Coming to the statutory definition of theword “input” in Rule 2(g) in the CENVAT CreditRules, 2002, it may be noted that the saiddefinition of the word “input” can be dividedinto three parts, namely :

• (i) specific part• (ii) inclusive part• (iii)place of use

4

15. Coming to the analysis of the inclusive part of the definition one finds that it covers :

(a) Lubricating oils, greases, cutting oils and coolants;

(b) Accessories;(c) Paints;(d) Packing materials;(e) Input used as fuel;(f) Input used for generation of steam or

electricity.

5

‘16. In our earlier discussion, we have referred to twoconsiderations as irrelevant, namely, use of input in themanufacturing process, be it direct or indirect as also absenceof the input in the final product on account of the use of theexpression “used in or in relation to the manufacture of finalproduct”. Similarly, we are of the view that consideration suchas input being used as packing material, input used as fuel,input used for generation of electricity or steam, input used asan accessory and input used as paint are per se also notrelevant. All these considerations become relevant only whenthey are read with the expression “used in or in relation to themanufacture of final product” in the substantive/specific part ofthe definition. In each case it has to be established that inputsmentioned in the inclusive part is “used in or in relation to themanufacture of final product”. It is the functional utility of thesaid item which would constitute the relevant consideration.Unless and until the said input is used in or in relation to themanufacture of final product within the factory of production,the said item would not become an eligible input-----------------’.

6

The question for our consideration iswhether the same logic would apply to thedefinition of input services which is given inrule 2(l) of the Cenvat Credit Rules, 2004and reproduced below :-

‘input service’ means any service ,

a. used by a provider of taxable service forproviding an output service; or

b. used by the manufacturer, whether directlyor indirectly, in or in relation to themanufacture of the final products andclearance of final products from the place ofremoval.

7

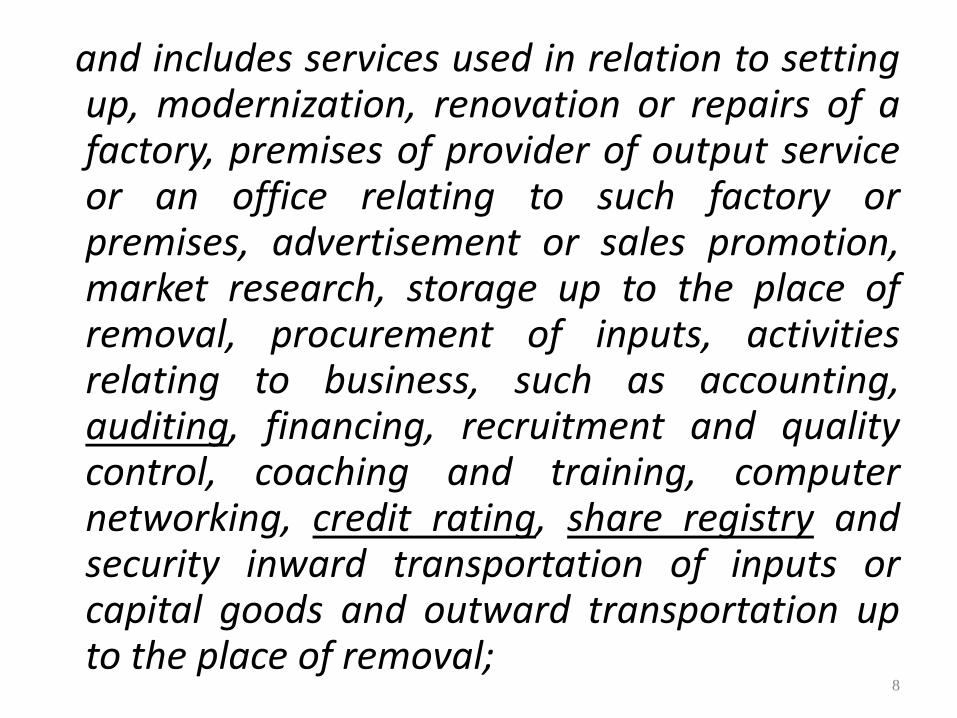

and includes services used in relation to settingup, modernization, renovation or repairs of afactory, premises of provider of output serviceor an office relating to such factory orpremises, advertisement or sales promotion,market research, storage up to the place ofremoval, procurement of inputs, activitiesrelating to business, such as accounting,auditing, financing, recruitment and qualitycontrol, coaching and training, computernetworking, credit rating, share registry andsecurity inward transportation of inputs orcapital goods and outward transportation upto the place of removal;

8

The definition of input services can bedivided in to five parts39. The definition of input service which has been

reproduced earlier, can be effectively divided into thefollowing five categories, in so far as a manufacturer isconcerned:

(i) Any service used by the manufacturer, whetherdirectly or indirectly, in or in relation to themanufacture of final products

(ii) Any service used by the manufacturer whetherdirectly or indirectly, in or in relation to clearance offinal products from the place of removal

9

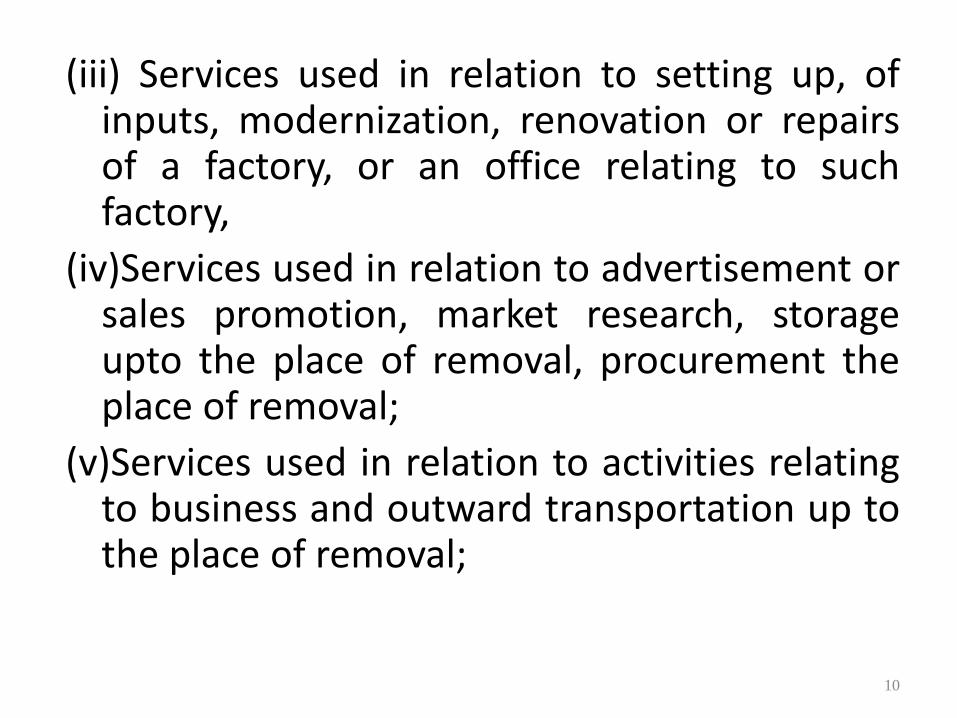

(iii) Services used in relation to setting up, ofinputs, modernization, renovation or repairsof a factory, or an office relating to suchfactory,

(iv)Services used in relation to advertisement orsales promotion, market research, storageupto the place of removal, procurement theplace of removal;

(v)Services used in relation to activities relatingto business and outward transportation up tothe place of removal;

10

Each limb of the definition of input service canbe considered asan independent benefit or concession or exemption. If anassessee can satisfy any one of the limbs of the above benefit,exemption or concession, then credit of the input servicewould be available. This would be so even if the assessee doesnot satisfy other limb/limbs of the above definition. Toillustrate, input services used in relation to setting up,modernization, renovation or repairs of a factory will beallowed as credit, even if they are assumed as not an activityrelating to business as long as they are associated directly orindirectly in relation to manufacture of final products andtransportation of final products upto the place of removal. Thiswould follow from the observation of the Supreme Court inKerala State Cooperative Marketing Federation Ltd. and Ors.Vs. Commissioner of Income-tax 1998 (5) SCC 48

11

Some of the expression in the definition likeShare registry, credit ratings has no relationshiptowards the manufacturing activity. Therefore, ifthe ratio of the judgment in the case of MarutiUdyog is applied to the definition of inputservices, these words would become redundant.Also, the interpretation of the expression‘activities relating to business’ as given in CocaCola India Pvt. Ltd. 2009 (15) STR 657 (Mum-HC)would get heavily restricted.

12

The Mumbai High Court has also in the case of CocaCola India Pvt. Ltd. 2009 (15) STR 657 has observedas follows with regard to activities relating tobusiness :-25. The expression "Business" is an integrated/continuousactivity and is not confined restricted to mere manufactureof the product. Therefore, activities in relation to businesscan cover all the activities that are related to the functioningof a business. The term "business" therefore, in our opinioncannot be given a restricted definition to say that business ofa manufacturer is to manufacture final products only. In acase like the present, business of assessee being anintegrated activity comprising of manufacture ofconcentrate, entering in to franchise agreement with bottlerspermitting use of brand name by bottlers promotion of brandname, etc. the expression will have to be seen in that contextSee (i) Pepsi Foods Ltd. Vs Collector 0 1996 (82) ELT 33, (ii)Pepsi Foods Ltd. Vs Collector 2003 (158) ELT 552 (SC) = (2003-TIOL-30-SC-CX)……………’ 13

’28………………...Similarly, in Eastern Investments Limited V/s CIT 1951 (20) ITR 1 = (2002-TIOL-519-SC-IT-LB) the Hon" ble Apex Court held as under:

" & Most commercial transactions are entered into forthe mutual benefit of both sides, or at any rate eachside hopes to gain something for itself. The test forpresent purposes is not whether the other partybenefited, nor indeed whether this was a prudenttransaction which resulted in ultimate gain to theappellant, but whether it was properly entered intoas a part of the appellants" legitimate commercialundertakings in order to indirectly facilitate thecarrying on of its business“…………………….’

14

There have been lot of controversy on this issuewhether the judgment of Coca Cola 2009 (15) STR 657will still prevail inspite of judgment in the case of MarutiUdyog Ltd. (Supra). There are contradictory judgment ofsingle members in this respect. The Tribunal in the caseof Vikram Ispat 2010 TIOL 900 CESTAT MUM hasrejected the appellants plea that Hon. High Court’decision in the case of Coco Cola shall be followed inpreference to Hon. Supreme Court’s ruling in the case ofMaruti Udyog ltd. Therefore, it means that for eachinput service in exercise with the manufacturing shall besubmitted.

15

However, the Tribunal has in the case of SemcoElectricals Pvt. Ltd. Vs. CCE, Pune 2010 TIOL 164CESTAT MUM has held that the judgment ofSupreme Court in the case of Maruti Udyog Ltdwas in the context of definition of inputs andnot of input services. Therefore, the ratio of thesaid judgment will not be applicable to theinterpretation of definition of input services.

16

The larger bench of Hon. Tribunal in the case ofVandana Global Ltd & Others 2010 TIOL 624CESTAT DEL-LB has decided the issue regardingliability of credit in respect of angles, joists,beams, channels, beams etc. The definition of‘input’ was amended with effect from 7th July2009. The explanation 2 to the definition ofinputs which was amended read as follows:-

17

Before the amendment, the said explanation 2 read as follows:-

Explanation 2. Input include goods used in the manufacture ofcapital goods which are further used in the factory of themanufacturer;

The said explanation 2 was amended by notification no. 16/2009-CE(NT) dated 07.07.2009 and after the amendment, it read asfollows :-

Explanation 2. - Input include goods used in the manufacture ofcapital goods which are further used in the factory of themanufacturer [but shall not include cement, angles, channels,Centrally Twisted Deform bar (CTD) or Thermo MechanicallyTreated bar (TMT) and other items used for construction of factoryshed, building or laying of foundation or making of structures forsupport of capital goods]

18

The Larger bench of Hon. Tribunal held that

a) The amendment which has been made isclarificatory in nature and hence retrospective. Itrelied upon the various clarifications issued by theCBEC

b) The cenvat is only a duty of excise of goodsproduced or manufacture. It is not a tax on thenature of value added tax which is usuallyimposed on all goods and services.

c) The phrase ‘capital goods’ has been defined in theCenvat Credit Rules. The foundation andsupporting structure embedded to earth will notqualify as capital goods in terms of the definition.Capital goods has to be goods

19

first and foundation and supporting structureembedded to earth are in the nature ofimmovable property and hence not goods.

d) The argument that the value of cement andsteel items used in foundation and buildingstructure support contribute to the value offinal product, therefore the credit shall beallowed has been turned down by SupremeCourt in the case of Maruti Udyog Ltd.

20

1) It is well established principle of statutoryprovisions that every statute is prima facie prospectiveunless it is expressly or by necessary implication made tohave retrospective operation. But the rule in general isapplicable where the object of the statute is to affectvested rights or to impose new burdens or to impairexisting obligations. Unless there are words in the statutesufficient to show the intention of the legislature to affectexisting rights, it is ‘deemed to be prospective only’.

The reliance is placed on the judgment in the case of ZileSign Vs. State of Haryana AIR 2004 SC 5100 & K. S.Paripuranam Vs. State of Kerala AIR 1995 (SC) 1012

21

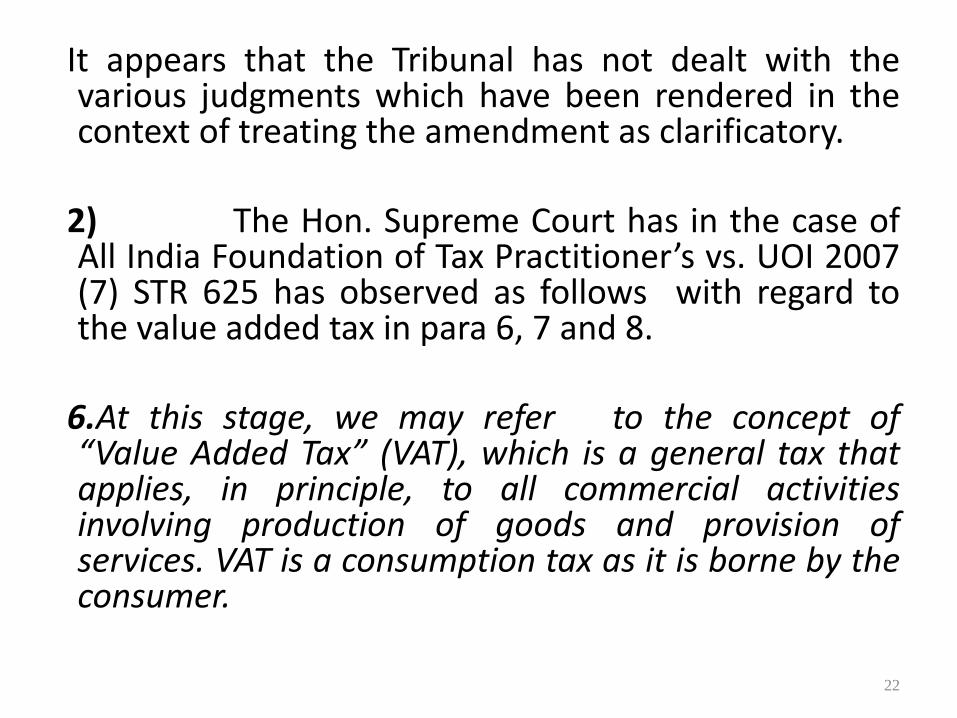

It appears that the Tribunal has not dealt with thevarious judgments which have been rendered in thecontext of treating the amendment as clarificatory.

2) The Hon. Supreme Court has in the case ofAll India Foundation of Tax Practitioner’s vs. UOI 2007(7) STR 625 has observed as follows with regard tothe value added tax in para 6, 7 and 8.

6.At this stage, we may refer to the concept of“Value Added Tax” (VAT), which is a general tax thatapplies, in principle, to all commercial activitiesinvolving production of goods and provision ofservices. VAT is a consumption tax as it is borne by theconsumer.

22

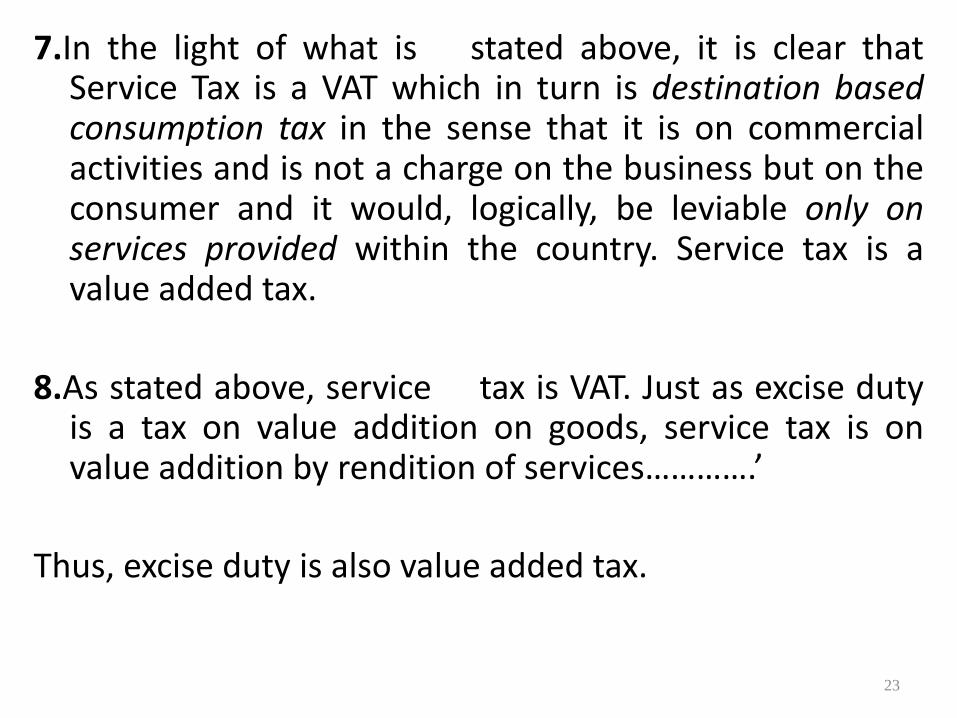

7.In the light of what is stated above, it is clear thatService Tax is a VAT which in turn is destination basedconsumption tax in the sense that it is on commercialactivities and is not a charge on the business but on theconsumer and it would, logically, be leviable only onservices provided within the country. Service tax is avalue added tax.

8.As stated above, service tax is VAT. Just as excise dutyis a tax on value addition on goods, service tax is onvalue addition by rendition of services………….’

Thus, excise duty is also value added tax.

23

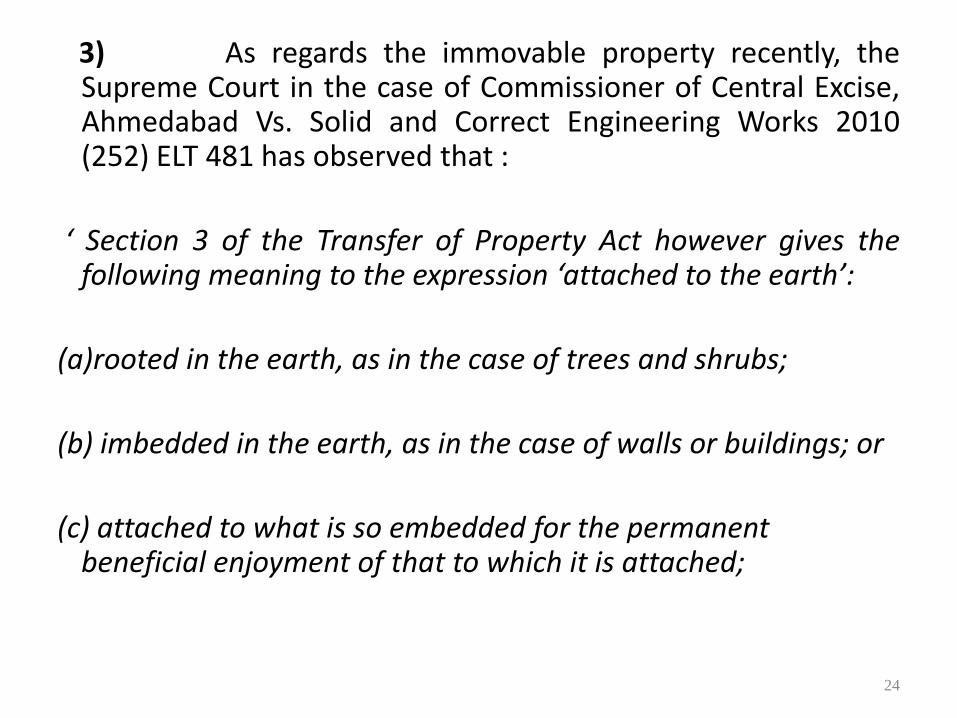

3) As regards the immovable property recently, theSupreme Court in the case of Commissioner of Central Excise,Ahmedabad Vs. Solid and Correct Engineering Works 2010(252) ELT 481 has observed that :

‘ Section 3 of the Transfer of Property Act however gives thefollowing meaning to the expression ‘attached to the earth’:

(a)rooted in the earth, as in the case of trees and shrubs;

(b) imbedded in the earth, as in the case of walls or buildings; or

(c) attached to what is so embedded for the permanent beneficial enjoyment of that to which it is attached;

24

19. It is evident from the above that the expression ‘ attached to theearth’ has three distinct dimensions viz. a) rooted in the earth as inthe case of tress and shrubs (b) imbedded in the earth as in the caseof walls or buildings or c) attached to what is imbedded for thepermanent beneficial enjoyment of that to which it is attached.Attachment of the plant in question with the help of nuts and bolts toa foundation not more than 1 ½ feet deep intended to providestability to the working of the plant and prevent vibration / wooblefree operation does not qualify for being described as attached to theearth under any one of the three clauses extracted above. That isbecause attachment of the plant to the foundation is not comparableor synonymous to trees and shrubs rooted in earth. It is also notsynonymous to imbedding in earth of the plant as in the case of wallsand buildings, for the obvious reason that a building imbedded in theearth is permanent and cannot be detached without demolition.Imbedding of a wall in the earth is also in no way comparable toattachment of a plant to a foundation meant only to provide stabilityto the plant especially because the attachment is not permanent andwhat is attached can be easily detached from the foundation. So alsothe attachment of the plant to the foundation at which it rests doesnot fall in third category, for an attachment to fall in that category itmust be for permanent beneficial enjoyment of that to which theplant is attached.

25

Thus, the meaning of the words ‘immovableproperty’ needs to be judged from theobservation of Supreme Court and Foundationof Supporting Structure even if they areimbedded to earth will not qualify as immovableproperty.

26

Judgment in the case of Kbace Tech Pvt. Ltd. 2010 TIOL564 CESTAT Mum observed as follows:-

Section 37 (2) allows the central government to makerules for the following:-

"(xvi) provide for the grant of a rebate of the duty paidon goods which are exported out of India or shippedfor consumption on a voyage to any port outside India(including interest thereon),"

27

"(xvia) provide for the credit of duty paid or deemed tohave been paid on the goods used in, or in relation tothe manufacture of excisable goods,“

"(xviaa) provide for credit of service tax leviable underChapter V of the Finance Act, 1994 (32 of 1994) paid orpayable on taxable services used in, or in relation to,the manufacture of excisable goods,“

"(xxviii) provide for the lapsing of credit of duty lyingunutilized with the manufacture of specified excisablegoods on an appointed date and also for not allowingsuch credit to be utilized for payment of any kind ofduty on any excisable goods on and from such date."

28

6. Section 94 of the Finance Act, 1994 allows the CentralGovernment to make rules to provide, interalia, for thefollowing:-

“ (ee) the credit of service tax paid on the services consumedfor providing a taxable service in case where the servicesconsumed and the service provided fall in the same categoryof taxable service.“

"(eee) the credit of service tax paid on the services consumedor duties paid or deemed to have been paid on goods usedfor providing a taxable service.“

"(g) grant of exemption to, or rebate of service tax paid on,taxable services which are exported out of India"

29

"(h) rebate of service tax paid or payable on thetaxable services consumed or duties paid ordeemed to have been paid on goods used forproviding taxable services which are exportedout of India.“

"(hh) rebate of service tax paid or payable on thetaxable services used as input services in themanufacturing or processing of goods exportedout of India under Section 93A."

30

It is evident from the above rules that thegovernment has power to make the rules forproviding credit of service tax paid on theservices consumed for providing such service.Since, the legislation has used the expression‘services consumed for providing technicalservices for the purpose of making rule’ . The rulemaking power has to be exercise within themandate of the statute and therefore each andevery service must be consumed in providing oftaxable service.

31

The meaning of the word ‘consumption’ has been elaborated in Anwar Khan Mehboob & Co. Vs. State of Mumbai 1960 (11) STC 698 (SC) as follows :-

“The act of consumption with which people are mostfamiliar occurs when they eat, or drink or smoke.Thus, we speak of people consuming bread, or fish ormeat, or vegetables, when they eat these articles ofgoods; we speak of people consuming tea or coffee orwater or wine, when they drink these articles of food;we speak of people consuming cigars or cigarettes orbidis, when they smoke these….. for each commodity,there is ordinarily what is generally considered to bethe final act of consumption. For some commodities,there may be even more than one kind of final

32

consumption. Thus grapes may be ‘finally consumed’ by eatingthem as fruits; they may also be consumed by making thewine prepared from ‘grapes’. Again, the final act ofconsumption may in some cases be spread over a considerableperiod of time. Books, articles or furniture and paintings maybe mentioned as examples. It may even happen in such casesthat after one consumer has performed part of the final act ofconsumption, another portion of the final act of consumptionmay be performed by his heir or successor-in-interest, atransferee, or even one who has obtained possession bywrongful means. But the fact that there is for each commoditywhat may be considered ordinarily to be the final act ofconsumption, should not make us forget that in reaching thestage at which this final act of consumption takes place thecommodity may pass through different stages of productionand for such different stages, there would exist one or moreintermediate acts of consumption.

33

It is well established principle that theprovisions which give powers to anyauthority must be liberally interpreted.The maximum latitude and freedommust be given in administering thelaw. Therefore restricting the creditonly to input services which areconsumed in providing the outputservices does not seem to be proper.

34

35

BALANCED VIEW PRESENTED BY

S.S.GUPTAChartered Accountant

OFFICE : 102-106, 1st Floor, Zaitoon Apartment, A-Wing,

182, Station Road,Opp. Municipal School,

Goregaon (W), Mumbai 400 062TEL: 022-28754127 / 28756146

E-MAIL : [email protected]

Hum Haunge Kamyab, Man me hain Vishwas.

![BOMBAY CHARTERED ACCOUNTANTS’ SOCIETY … · IDS Software Solutions ... Manoj Kumar Reddy, [2011] ... • Social Security and Pension • ESOP • Medical Insurance, ...](https://static.fdocuments.in/doc/165x107/5af34ae07f8b9a190c8b6805/bombay-chartered-accountants-society-software-solutions-manoj-kumar-reddy.jpg)