Lecture - credit cards

17

Credit Cards

-

Upload

bwellington -

Category

Education

-

view

1.012 -

download

0

Transcript of Lecture - credit cards

Credit Cards

Credit Cards and Debt

✤ Consider: If offered an investment option that would give you a 15 to 20% return on your money would you take it?

✤ Well if your credit card is charging you 20% interest on borrowed money then paying off the balance of your card guarantees substantial savings. It is just as good as making a 20% return.

✤ Likewise, not paying off your balance is taking a 20% loss

What is a credit card?

• A credit account is a pre-approved loan for a certain amount of money each month.

• You are borrowing money from the bank, and the bank charges you interest for using their money.

Interest:Every time you don’t pay the full amount that you owe (each month), the bank charges you extra money.This charge is usually anything from 1% to 40% of what you owe the bank.This money is called interest, and it gets added to next month’s bill.

Let’s say you owe $1,000 on your credit card bill, but you only want to pay $100 of that bill right now (you’ll pay the rest later). You now owe $900.

But wait, the credit card company will charge you 10% interest on what you still owe. 10% of $900 = $90. So after interest, you now owe $990 for this month.

That means even though you paid $100 already, you still owe almost the entire $1,000 because of interest!

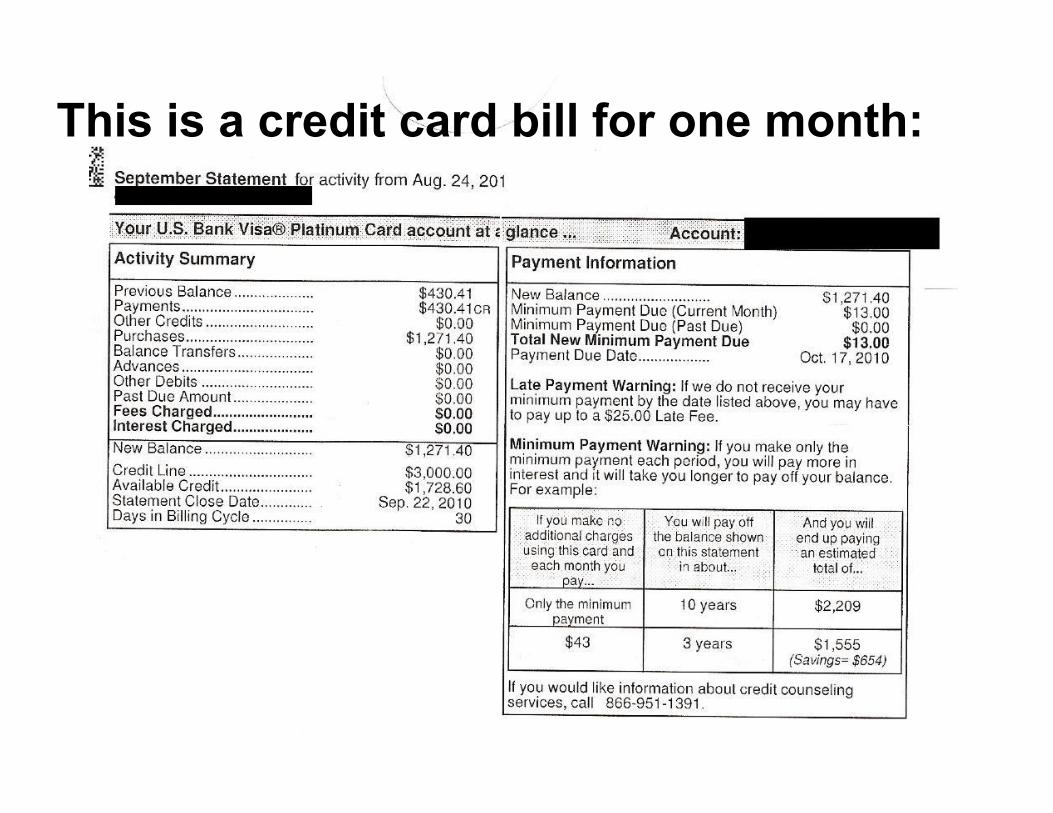

This is a credit card bill for one month:

If you pay your entire balance each month, you won’t pay ANY interest!

If you pay your entire balance each month, you won’t pay ANY interest!

Most people don’t!

How much you spent on your credit card in one month.

The amount of interest the bank is charging you for using their money.

The minimum monthly payment

The minimum percent of your bill you must pay per month.

How long it will take you to pay off ONE MONTH of credit card spending if you pay the minimum amount.

What you will pay in interest over that period of time.

How much you end up paying total by the end!

Let’s look at this one more time…

Example of Credit Debt: Read OnlyJohn and Jane both have $2,000 debt on their credit cards, which require a minimum payment of 3%, or $10, whichever is higher. Both are strapped for cash, but Jane manages to pay an extra $10 on top of her minimum monthly payments. John pays only the minimum.

Each month John and Jane are charged a 20% annual interest on their cards' outstanding balances. So, when John and Jane make payments, part of those payments go to paying interest and part go to the principal.

Here is the breakdown of the numbers for the first month of John's credit card debt:

Principal: $2,000 Interest: $33.33 ($2,000 x (1+20%/12)) Payment: $60 (3% of remaining balance) Principal Repayment: $26.67 Remaining Balance: $1,973.33 ($2,000 - $26.67)

These calculations are done every month until the credit card debt is paid off.

In the end, John pays $4,240 in total over 15 years to absolve the $2,000 in credit card debt. The interest that John pays over the 15 years totals $2,240, higher than the original credit card debt.

✤ Because Jane paid an extra $10 a month, she pays a total $3,276 over seven years to absolve the $2,000 in credit card debt. Jane pays a total $1,276 in interest.

✤ The extra $10 a month saves Jane almost $1,000 and cuts her repayment period by more than seven years

Example of Credit Debt: Read Only

Students and Credit Cards✤ A 2009 Sallie Mae study found that 92% of college students

who owned credit cards put textbooks, supplies and other school expenses on their cards.

✤ A full 1/3 placed tuition on a card

✤ For many students making minimum payments seems easy enough but new card users are by far the most frequent to fall behind on payments.

✤ Low or bad credit can follow you for years, hurting your chances to rent an apartment, buy a car, and receive loans for school and housing.

Your credit score is affected by how frequently you use your card, whether you pay the full balance, whether you pay on time, etc.

Credit scores are used later on to determine your reliability as a borrower.

It’s a permanent record.

You will need a strong credit score to:

-Buy a house -Rent a house -Buy a car -Get a loan -Get another credit card -Get a job

If you can’t pay your debts, you declare bankruptcy. Your credit score is ruined for ten years.

But the bank may also have to close if many of their borrowers declare bankruptcy!

This “credit disaster” helped lead to recession in 2008.

Debit Cards are different.• With debit, the money you spend comes

directly out of your checking account immediately.

– If you don’t have the money, your card is denied. You must pay now, not later!

– The bank is not lending you any money, so there is no interest! You only spend what you have.

– The bank is not hurt if you run out of money, because this isn’t a loan.

– However, debit cards do not affect your credit score.

![Credit cards[1]](https://static.fdocuments.in/doc/165x107/5551b7f1b4c905ca7f8b4b8d/credit-cards1.jpg)