Lecture 7: Policy Design: Health Insurance & Adverse...

25

Health Insurance Spending & Health Adverse Selection Lecture 7: Policy Design: Health Insurance & Adverse Selection Johannes Spinnewijn London School of Economics Lecture Notes for Ec426 1 / 25

Transcript of Lecture 7: Policy Design: Health Insurance & Adverse...

Health Insurance Spending & Health Adverse Selection

Lecture 7: Policy Design:Health Insurance & Adverse Selection

Johannes Spinnewijn

London School of Economics

Lecture Notes for Ec426

1 / 25

Health Insurance Spending & Health Adverse Selection

Outline

1 Health Insurance & Care

2 Rise in Spending & Impact on Health

3 Adverse selection: theory & empirics

2 / 25

Health Insurance Spending & Health Adverse Selection

Health Insurance

Different from other examples of social insurance

triangle relationship between customer, insurer and providerco-existence of private and public initiativerelation between health care and health outcomessome similar issues as with social security

Health is an important field because of enormous size andrapid growth

1950: 4% of GDP devoted to health care in US2003: 15% of GDP devoted to health care in US2075: 38% of GDP devoted to health care in US

Health economics is field in itself. We will focus on publicsector interventions

3 / 25

Health Insurance Spending & Health Adverse Selection

Health Care Spending in OECD Nations in 2002

Health Care Spending in OECD Nations in 2002

0

3

6

9

12

15

Slov

ak R

epub

licKo

rea

Mex

ico

Pola

ndLu

xem

bour

gTu

rkey

Finl

and

Irela

ndC

zech

Rep

ublic

Spai

nAu

stria

Uni

ted

Kin

gdom

Hun

gary

Japa

nIta

lyN

ew Z

eala

ndN

orw

ayD

enm

ark

Aust

ralia

Belg

ium

Net

herla

nds

Swed

enPo

rtuga

lG

reec

eC

anad

aFr

ance

Icel

and

Ger

man

ySw

itzer

land

Uni

ted

Sta

tes

Heal

th C

are

Spen

ding

(% o

f GDP

)

Source: Gruber (2007)

4 / 25

Health Insurance Spending & Health Adverse Selection

UK vs. US

UK: publicly funded health care system (NHS)

largest employer in UKinsures most types of careprivate health care for top-ups, only taken by 8%

Before ‘Obama-care’US tended to have less publicintervention than other developed countries

50% compared to 75% on average elsewheremedicare vs. medicaidinsurance provided by employers, large tax subsidy - financedwith payroll taxmany types of care uninsured, many people uninsured

5 / 25

Health Insurance Spending & Health Adverse Selection

Rise in Health Spending: Reasons?

General consensus: technological progress with moreexpensive methods (supply effect)

example: angioplasty: expensive but saves lifes (of somepatients...)

Newhouse (1992): residual argument (a la growth accounting)

only 1/4 to 1/2 of rise in spending can be explained by otherfacts

demand effects: aging, increased income, subsidized bygovernment, increased insuranceother supply effects: supplier induced demand(fee-for-service), malpractice

Limited direct evidence for impact of technological change

6 / 25

Health Insurance Spending & Health Adverse Selection

Health Spending vs. Health OutcomesIs increase in health spending a problem?

optimal health share is likely to grow with incomevoluntary choice to adopt (expensive) technological progressBUT prices are distorted due to insurance

Does health insurance / higher spending improve health?margin vs. average

evidence for "flat of the curve" health careextremely high average value of health improvements in thelast decennia

young vs. oldsubstantial impact of Medicaid (Currie & Gruber 1996)insignificant impact of Medicare (Card et al. 2008)

opportunity cost of each health policy (see RDD example)

How to measure health improvements? Are healthimprovements of ‘First Order’importance for insurancepolicies?

7 / 25

Health Insurance Spending & Health Adverse Selection

Opportunity Cost: An RDD Example

Source: Almond, Doyle, Kowalski and Williams (2009)8 / 25

Health Insurance Spending & Health Adverse Selection

Opportunity Cost: An RDD Example

Source: Almond, Doyle, Kowalski and Williams (2009)9 / 25

Health Insurance Spending & Health Adverse Selection Demand&Supply Heterogeneity Moral Hazard

Market Failures and Government Interventions1 Asymmetric Information:

heterogeneity of risk types → adverse selection in insurancemarketprice subsidies, insurance mandates,...

2 Externalities/Internalities/Consumer myopiatax subsidies for health insurance, government providedinsurancesin taxes (alcohol/cigarettes), fat tax,...

3 Other reasons for government provision or regulation;1 Suppliers exploiting asymmetric info about desirable care (e.g.,licensing of doctors, fixing physician salaries)

2 Incomplete market: ex-ante risk uninsured, since we cannotcontract before birth

3 Equity concerns: health inequality may directly enter socialwelfare function (e.g., in US, white infant mortality rate is6/1000; black is 14/1000)

10 / 25

Health Insurance Spending & Health Adverse Selection Demand&Supply Heterogeneity Moral Hazard

Adverse Selection as a Motivation for SIKey paper: Akerlof (1970), Rothschild and Stiglitz (1976)

environment with asymmetric information: individuals knowrisk of becoming sick but insurer does notmarket failure: underprovision of insurance (completeunravelling in extreme case)government intervention: through mandated insurance caninduce a Pareto improvement

Renewed interest: negative correlation puzzletheory predicts that high risk types buy more insurancecoverageempirically, the exact opposite is found in many insurancemarkets

Most recently: estimate welfare cost of asymmetricinformation

structural vs. reduced-form approachesstrong assumptions on importance of preferences

11 / 25

Health Insurance Spending & Health Adverse Selection Demand&Supply Heterogeneity Moral Hazard

Simple Demand and Supply of InsuranceBased on Einav, Finkelstein & Cullen (2010)

Consumers have the choice between contract H and L.Contract H provides more insurance coverage at additionalpremium p

Assume unobserved heterogeneity ζ determines both the valueand the cost of insurance.

Additive model:

v ≡ vH (ζ)− vL (ζ) ≡ π (ζ)︸ ︷︷ ︸‘risk’-term

+ r (ζ)︸︷︷︸‘preference’-term

π (ζ) equals the insurer’s cost of providing insurancer (ζ) captures the net-value of insurancefor CARA γ and normal risk x : π (ζ) = Ex , r (ζ) = γ

2 var (x)

12 / 25

Health Insurance Spending & Health Adverse Selection Demand&Supply Heterogeneity Moral Hazard

Heterogeneity in Risks: Adverse Selection

Buy contract H iff v (ζ) ≥ p,

Demand : D (p) = 1− Fv (p)

Cost of providing insurance depends on types buying insurance

Average Cost : AC (p) = E (π|v (ζ) ≥ p)Marginal Cost : MC (p) = E (π|v (ζ) = p)

More risky types tend to value insurance more such that thecost of providing insurance is increasing in p

13 / 25

Health Insurance Spending & Health Adverse Selection Demand&Supply Heterogeneity Moral Hazard

Adverse Selection

14 / 25

Health Insurance Spending & Health Adverse Selection Demand&Supply Heterogeneity Moral Hazard

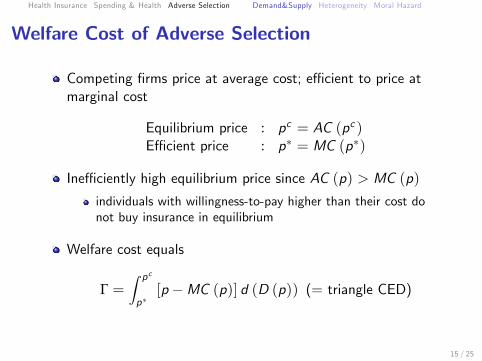

Welfare Cost of Adverse Selection

Competing firms price at average cost; effi cient to price atmarginal cost

Equilibrium price : pc = AC (pc )Effi cient price : p∗ = MC (p∗)

Ineffi ciently high equilibrium price since AC (p) > MC (p)

individuals with willingness-to-pay higher than their cost donot buy insurance in equilibrium

Welfare cost equals

Γ =∫ pc

p∗[p −MC (p)] d (D (p)) (= triangle CED)

15 / 25

Health Insurance Spending & Health Adverse Selection Demand&Supply Heterogeneity Moral Hazard

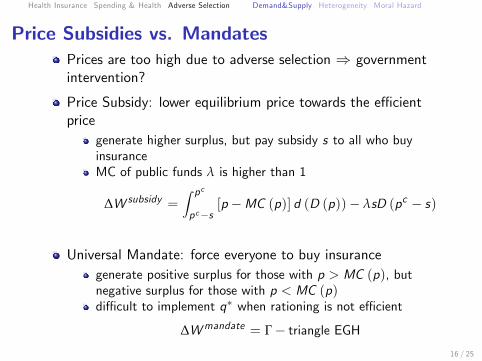

Price Subsidies vs. MandatesPrices are too high due to adverse selection ⇒ governmentintervention?

Price Subsidy: lower equilibrium price towards the effi cientprice

generate higher surplus, but pay subsidy s to all who buyinsuranceMC of public funds λ is higher than 1

∆W subsidy =∫ pcpc−s

[p −MC (p)] d (D (p))− λsD (pc − s)

Universal Mandate: force everyone to buy insurancegenerate positive surplus for those with p > MC (p), butnegative surplus for those with p < MC (p)diffi cult to implement q∗ when rationing is not effi cient

∆Wmandate = Γ− triangle EGH16 / 25

Health Insurance Spending & Health Adverse Selection Demand&Supply Heterogeneity Moral Hazard

Welfare Analysis using Suffi cient Statistics

Suffi cient to estimate demand curve and average cost curve

need information on available options, contract choices andthe medical claims for given pricesneed exogenous price variation as well

Approach allows to calculate welfare loss due to ineffi cientpricing and gain from policy interventions

Einav et al. (2010) analyze employer-provided healthinsurance

consider choice between high-deductible and low-deductiblecontractexploit variation in the premium across business unitsobserve how many buy and how much they claim

⇒ effi ciency cost is small (only 3% of total surplus), bothprice subsidy and mandate would decrease welfare!

17 / 25

Health Insurance Spending & Health Adverse Selection Demand&Supply Heterogeneity Moral Hazard

18 / 25

Health Insurance Spending & Health Adverse Selection Demand&Supply Heterogeneity Moral Hazard

Adverse Selection: Pricing vs. ScreeningAkerlof (1970):

presence of high risk types prices lower risk types out of themarketextreme unravelling: no one buys contract (except highest risktype) - even when everyone prefers to buy at actuarially fairpricemeasure of ineffi ciency:

E (π|v (ζ) ≥ p)− E (π|v (ζ) = p)

Rothschild and Stiglitz (1976):

previous approach takes contracts as givenallow insurers to provide a menu of contracts specifying priceánd coveragescreen low risk types by providing less insurance at reducedpremium

19 / 25

Health Insurance Spending & Health Adverse Selection Demand&Supply Heterogeneity Moral Hazard

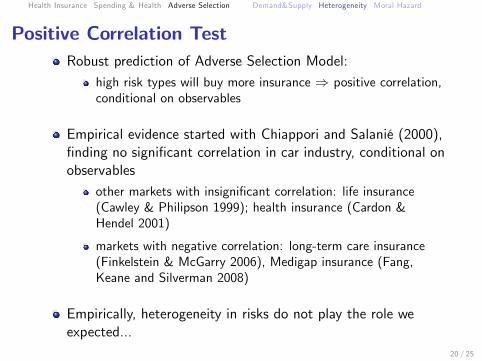

Positive Correlation TestRobust prediction of Adverse Selection Model:

high risk types will buy more insurance ⇒ positive correlation,conditional on observables

Empirical evidence started with Chiappori and Salanié (2000),finding no significant correlation in car industry, conditional onobservables

other markets with insignificant correlation: life insurance(Cawley & Philipson 1999); health insurance (Cardon &Hendel 2001)

markets with negative correlation: long-term care insurance(Finkelstein & McGarry 2006), Medigap insurance (Fang,Keane and Silverman 2008)

Empirically, heterogeneity in risks do not play the role weexpected...

20 / 25

Health Insurance Spending & Health Adverse Selection Demand&Supply Heterogeneity Moral Hazard

Heterogeneity in PreferencesCurrent literature conjectures the importance ofheterogeneous preferences

Back to model (v = π + r) - assume normal heterogeneity

MC curve simplifies to

MC (p (q)) = µπ +cov (π, v)var (v)

[p (q)− µv ]

MC curve flattens if the variance in preferences increasesMC curve is upward sloping ifcov (π, v) (= var (π) + cov (π, r)) < 0

Suffi cient statistics approach: unnecessary to uncover theunderlying heterogeneity

adverse selection if MC curve is decreasingadvantageous selection if MC curve is increasing

21 / 25

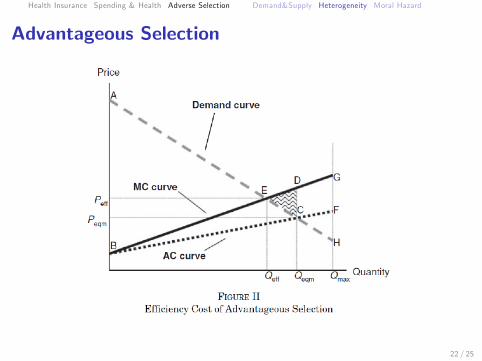

Health Insurance Spending & Health Adverse Selection Demand&Supply Heterogeneity Moral Hazard

Advantageous Selection

22 / 25

Health Insurance Spending & Health Adverse Selection Demand&Supply Heterogeneity Moral Hazard

Heterogeneity in Preferences?

While current empirical approaches attribute residualheterogeneity in demand to heterogeneous preferences, directevidence is limited.

Recent work questions stability of preferences for givenindividual across domains.

Suggests importance of other drivers of the demand forinsurance (risk perceptions, inertia, cognitive ability,...),possibly unrelated to the actual value of insurance.

23 / 25

Health Insurance Spending & Health Adverse Selection Demand&Supply Heterogeneity Moral Hazard

Adverse Selection vs. Moral HazardInsurance of medical care induces moral hazard

ex ante: less precautionary effortsex post: overconsumption of medical care

Moral hazard predicts the same positive correlation.insurers reduce insurance coverage to provide optimalincentives (either ex ante or ex post)very different from reducing insurance coverage to screen goodrisk types

How to distinguish from adverse selection?no precautionary efforts (life insurance/annuities)use experimental or quasi-experimental variationuse dynamic data

Moral hazard and heterogeneous preferences may explainnegative correlation-puzzle

people who are more risk-averse buy more insurance, but exertmore effort as well

24 / 25

Health Insurance Spending & Health Adverse Selection Demand&Supply Heterogeneity Moral Hazard

In Sum

Health insurance is a particular type of Social Insurance (careprovider, private vs. public, impact on health). Expenditureson health care are growing exponentially.

Private information about health risks may cause adverseselection; underprovision of insurance would justifygovernment interventions.

However, empirical evidence suggests minor role of people’srisk as a determinant of their insurance choice.

25 / 25