Lecture 6: Tax Incidence & SOverview3 RulesExtensionsGE TaxEmp. Incdnc Overview Course...

98

Admin RFH I&S Overview 3 Rules Extensions GE Tax Emp. Incdnc Lecture 6: Tax Incidence October 2, 2018

Transcript of Lecture 6: Tax Incidence & SOverview3 RulesExtensionsGE TaxEmp. Incdnc Overview Course...

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Lecture 6: Tax Incidence

October 2, 2018

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Overview

Course Administration

Ripped From Headlines

Income and Substitution Effects, Revisited

Taxation Overview

Three Rules of Tax Incidence

Tax Incidence Extensions

General Equilibrium Tax Incidence

Empirical Incidence of Taxation in the US

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Course Administration

1. Problem Sets• PS 6 posted• Returning PS 4• PS 4 answers posted

2. Midterm review• 10/13, 10:30 to 12:30• Funger 209• bring questions on old midterm

3. Final review session scheduled

4. Instructions for draft of elasticity memo

5. Anything else?

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Ripped from the Headlines

Next Week

Afternoon

Finder Presenter

San Gunter Boyd GardnerLena Nour Liam Goodwin

Evening

Finder Presenter

Tim Emmart DaQuan-Lee CookJulia Barrett Diego ScharifkerJohn Jacobs Virginia Bezerra de Menenzes

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Earned Income Tax CreditTax Credits for Low-Income Workers

• when benefits increase• substitution effect → more work• income effect → more work

• when benefits plateau• no change in price of work → no

substitution effect• income effect → more work

• when benefits decline• substitution effect → effective

wage declines → less work• income effect → more work

��������� ���� ������ ��� ������ ������ ��� ����� � ������ �� ��� �� ��� ���� �������

���!����"""#�$!!#�� ����������%�����&����!���&$����&���&������&�����&���&����� ��' ()*+,-./0)/ .)1 234.-10)/ 5+-6789 :;7< => ?9>=@A9? BC 9ADCEFG@9 GA? F9HGF? HCFIJ K> ACB9?L G HCFI9FM> :;7< @FCH> H=B8 9GD8 G??=B=CAGN ?CNNGF CO9GFA=A@> EAB=N F9GD8=A@ B89 PGQ=PEP RGNE9J 78=> DF9GB9> GA =AD9AB=R9 OCF S9CSN9 BC N9GR9 H9NOGF9 OCF HCFI GA? OCFNCHTHG@9 HCFI9F> BC =ADF9G>9 B89=F HCFI 8CEF>J78=> =AD9AB=R9 O9GBEF9 8G> PG?9 B89 :;7< 8=@8NU >EDD9>>OENJ VBE?=9> >8CH B8GB B89 :;7< 9ADCEFG@9> NGF@9 AEPW9F>CO >=A@N9 SGF9AB> BC N9GR9 H9NOGF9 OCF HCFIL 9>S9D=GNNU H89A B89 NGWCF PGFI9B => >BFCA@J

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Taxation Overview

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

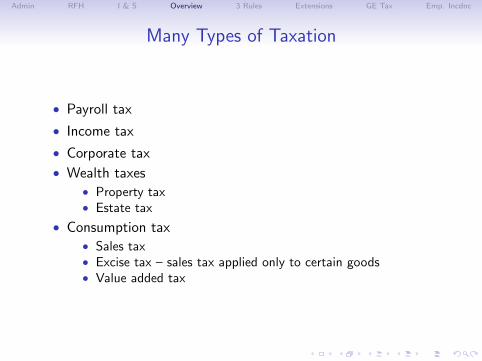

Many Types of Taxation

• Payroll tax

• Income tax

• Corporate tax

• Wealth taxes• Property tax• Estate tax

• Consumption tax• Sales tax• Excise tax – sales tax applied only to certain goods• Value added tax

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Type of Taxation Shifted Dramatically in US

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Key Tax Definitions

• Tax base: that on which the tax is levied• Base for property tax is value of properties• Base for sales tax is value of sales

• Tax rate: rate at which base is taxed• DC’s General tangible property and selected services tax rate is

5.75%• DC’s parking tax rate is 18%

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Three Rules

of Tax Incidence

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

You Levy a Tax – Who Pays?

The US income tax has shifted from a reliance on corporate taxesto income tax. Does this mean workers are paying more? “Whopays?” = tax incidence

Study the three rules of tax incidence

1. Statutory burden of tax 6= economic incidence of tax

2. Side of the market on which tax is imposed is irrelevant todistribution of tax burdens

3. Parties with inelastic supply or demand bear taxes

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

You Levy a Tax – Who Pays?

The US income tax has shifted from a reliance on corporate taxesto income tax. Does this mean workers are paying more? “Whopays?” = tax incidence

Study the three rules of tax incidence

1. Statutory burden of tax 6= economic incidence of tax

2. Side of the market on which tax is imposed is irrelevant todistribution of tax burdens

3. Parties with inelastic supply or demand bear taxes

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Types of Taxation

• specific excise tax: per unit tax

• ad valorem tax: tax that is a fixed percentage of the sale price

We will present everything with a specific excise tax. Results areequally applicable to an ad valorem tax.

U.S. excise tax examples

• federal tax on bows, archery equipment and and arrow shafts

• gasoline

• wine, varying by type, highest on “naturally sparkling”

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Types of Taxation

• specific excise tax: per unit tax

• ad valorem tax: tax that is a fixed percentage of the sale price

We will present everything with a specific excise tax. Results areequally applicable to an ad valorem tax.

U.S. excise tax examples

• federal tax on bows, archery equipment and and arrow shafts

• gasoline

• wine, varying by type, highest on “naturally sparkling”

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Key Phrases

Incidence ≡ who pays the tax, or who “bears the burden” of thetax.

• Statutory incidence: determined by who pays the tax to thegovernment

• Economic incidence: determined by whose economic resourceschange due to the tax

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

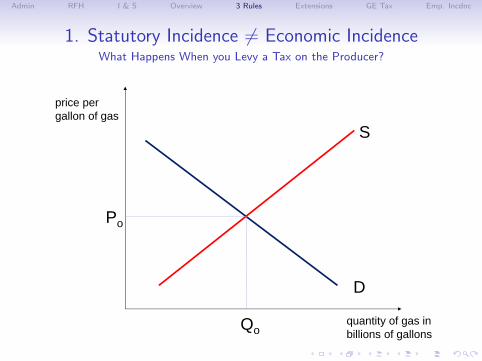

1. Statutory Incidence 6= Economic IncidenceWhat Happens When you Levy a Tax on the Producer?

price pergallon of gas

quantity of gas in billions of gallons

S

D

Qo

Po

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

1. Statutory Incidence 6= Economic IncidenceWhat Are the New Equilibrium Price and Quantity?

price pergallon of gas

quantity of gas in billions of gallons

S

D

S’

tax

Qo

Po

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

1. Statutory Incidence 6= Economic IncidenceHow Much Extra is the Consumer Paying?

price pergallon of gas

quantity of gas in billions of gallons

S

D

S’

tax

Qo

Po

Pn

Qn

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

1. Statutory Incidence 6= Economic IncidenceHow Much Does the Producer Sell for? And What Does He Keep?

price pergallon of gas

quantity of gas in billions of gallons

S

D

S’

tax

Qo

Po

Pn

Qn

consumer’s burden

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

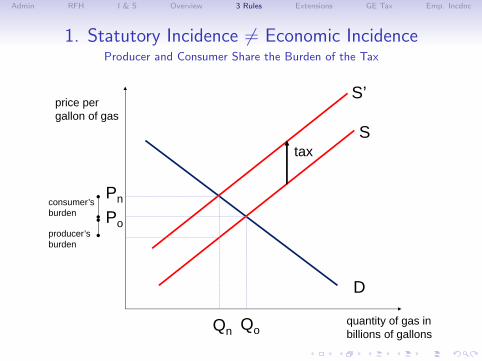

1. Statutory Incidence 6= Economic IncidenceProducer and Consumer Share the Burden of the Tax

price pergallon of gas

quantity of gas in billions of gallons

S

D

S’

tax

Qo

Po

Pn

Qn

consumer’s burden

producer’sburden

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Defining Tax Burdens

• a burden is a bad thing for producers or consumers

• burden is expressed as a positive number

• think of it as the net effect of positive and negative pricechanges from the tax

• from the producer and consumer viewpoint separately

• producer and consumer tax burden sum to the amount of thetax

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Defining Tax Burdens, Tax on Producer

• consumer tax burden= (post-tax price - pre-tax price) + per-unit tax payment byconsumer= benefit/loss in price change to consumer + per-unit taxpayment by consumer= (Pn − Po)+ per-unit tax payments by consumers= Pn − Po

• producer tax burden= (pre-tax price - post-tax price) + per-unit tax payment byproducer= per-unit tax payment by producer + benefit/loss in pricechange to producer= per-unit tax payments by producers −(Pn − Po)= tax− (Pn − Po)

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Defining Tax Burdens, Tax on Producer

• consumer tax burden= (post-tax price - pre-tax price) + per-unit tax payment byconsumer= benefit/loss in price change to consumer + per-unit taxpayment by consumer= (Pn − Po)+ per-unit tax payments by consumers= Pn − Po

• producer tax burden= (pre-tax price - post-tax price) + per-unit tax payment byproducer= per-unit tax payment by producer + benefit/loss in pricechange to producer= per-unit tax payments by producers −(Pn − Po)= tax− (Pn − Po)

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

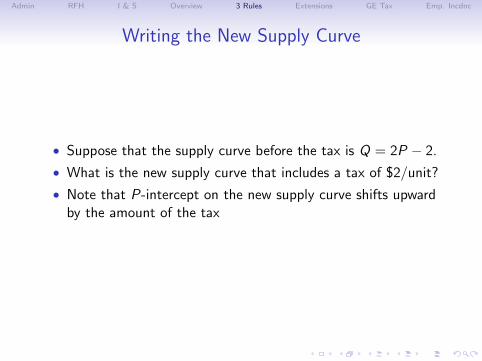

Writing the New Supply Curve

• Suppose that the supply curve before the tax is Q = 2P − 2.

• What is the new supply curve that includes a tax of $2/unit?

• Note that P-intercept on the new supply curve shifts upwardby the amount of the tax

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Writing the New Supply Curve

• Suppose that the supply curve before the tax is Q = 2P − 2.

• What is the new supply curve that includes a tax of $2/unit?

• Note that P-intercept on the new supply curve shifts upwardby the amount of the tax

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Writing the New Supply Curve: Equations

• The original supply curve is Q = 2P − 2• re-write in terms of P: P = 1 + (1/2)Q

• Note that Pat = Pbt + 2

• So we can write the after-tax supply curve as

P = 1 + (1/2)Q + 2

= 3 + (1/2)Q

• Note that you can re-write this as Q = 2P − 6

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

An Alternative Method to Finding New Supply

• Suppose that the supply curve before the tax is QS = 2P − 2.

• How does the supplier perceive a tax of $2/unit?

• Pat = Pbt + 2→ Pbt = Pat − 2• where at denotes the after tax price bt the before tax price in

the supply curve

• We’d like to know market supply as a function of the taxedprice: Qtax

S = f (P)

QtaxS = 2Pbt − 2

QtaxS = 2(Pat − 2)− 2

QtaxS = 2Pat − 4− 2 = 2Pat − 6

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

An Alternative Method to Finding New Supply

• Suppose that the supply curve before the tax is QS = 2P − 2.

• How does the supplier perceive a tax of $2/unit?• Pat = Pbt + 2→ Pbt = Pat − 2• where at denotes the after tax price bt the before tax price in

the supply curve

• We’d like to know market supply as a function of the taxedprice: Qtax

S = f (P)

QtaxS = 2Pbt − 2

QtaxS = 2(Pat − 2)− 2

QtaxS = 2Pat − 4− 2 = 2Pat − 6

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

2. Side of the Market on Which Tax is Imposed Irrelevantto Distribution of Tax Burden

• Suppose that the gasoline tax is levied on the consumer, notthe producer

• This means you buy some gas and send a check to thegovernment

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Consumer Pays TaxWhat Happens When you Levy a Tax on the Consumer?

price pergallon of gas

quantity of gas in billions of gallons

S

D

Qo

Po

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Consumer Pays TaxWhat Are the New Equilibrium Price and Quantity?

price pergallon of gas

quantity of gas in billions of gallons

S

Dt

Qo

Po

D’

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

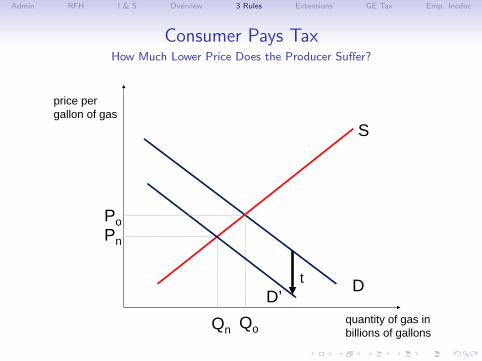

Consumer Pays TaxHow Much Lower Price Does the Producer Suffer?

price pergallon of gas

quantity of gas in billions of gallons

S

Dt

Qo

PoPn

Qn

D’

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

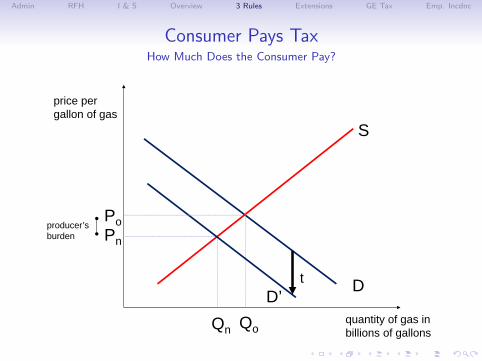

Consumer Pays TaxHow Much Does the Consumer Pay?

price pergallon of gas

quantity of gas in billions of gallons

S

Dt

Qo

PoPn

Qn

producer’sburden

D’

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Consumer Pays TaxProducer and Consumer Share the Burden of the Tax

price pergallon of gas

quantity of gas in billions of gallons

S

Dt

Qo

PoPn

Qn

consumer’s burden

D’

producer’sburden

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Consider Burdens

• When tax is levied on consumers• consumer burden

= t − (Po − Pn)• producer burden = Po − Pn

• total burden = t − (Po − Pn) + Po − Pn = t

• When tax is levied on producers• consumer burden = Pn − Po

• producer burden = t − (Pn − Po)• total burden = Pn − Po + t − (Pn − Po) = t

• Note that• In both cases, total burden is tax. t• The total price change faced by producers and consumers is

equal regardless of the side of the market with the tax

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Consider Burdens

• When tax is levied on consumers• consumer burden = t − (Po − Pn)• producer burden

= Po − Pn

• total burden = t − (Po − Pn) + Po − Pn = t

• When tax is levied on producers• consumer burden = Pn − Po

• producer burden = t − (Pn − Po)• total burden = Pn − Po + t − (Pn − Po) = t

• Note that• In both cases, total burden is tax. t• The total price change faced by producers and consumers is

equal regardless of the side of the market with the tax

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Consider Burdens

• When tax is levied on consumers• consumer burden = t − (Po − Pn)• producer burden = Po − Pn

• total burden

= t − (Po − Pn) + Po − Pn = t

• When tax is levied on producers• consumer burden = Pn − Po

• producer burden = t − (Pn − Po)• total burden = Pn − Po + t − (Pn − Po) = t

• Note that• In both cases, total burden is tax. t• The total price change faced by producers and consumers is

equal regardless of the side of the market with the tax

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Consider Burdens

• When tax is levied on consumers• consumer burden = t − (Po − Pn)• producer burden = Po − Pn

• total burden = t − (Po − Pn) + Po − Pn = t

• When tax is levied on producers• consumer burden = Pn − Po

• producer burden = t − (Pn − Po)• total burden = Pn − Po + t − (Pn − Po) = t

• Note that• In both cases, total burden is tax. t• The total price change faced by producers and consumers is

equal regardless of the side of the market with the tax

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Consider Burdens

• When tax is levied on consumers• consumer burden = t − (Po − Pn)• producer burden = Po − Pn

• total burden = t − (Po − Pn) + Po − Pn = t

• When tax is levied on producers• consumer burden = Pn − Po

• producer burden = t − (Pn − Po)• total burden = Pn − Po + t − (Pn − Po) = t

• Note that• In both cases, total burden is tax. t• The total price change faced by producers and consumers is

equal regardless of the side of the market with the tax

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Consider Burdens

• When tax is levied on consumers• consumer burden = t − (Po − Pn)• producer burden = Po − Pn

• total burden = t − (Po − Pn) + Po − Pn = t

• When tax is levied on producers• consumer burden = Pn − Po

• producer burden = t − (Pn − Po)• total burden = Pn − Po + t − (Pn − Po) = t

• Note that• In both cases, total burden is tax. t• The total price change faced by producers and consumers is

equal regardless of the side of the market with the tax

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Visual Comparison of Burdens

price pergallon of gas

quantity of gas in billions of gallons

S

D

S’

tax

Qo

Po

Pn

Qn

consumer’s burden

producer’sburden

price pergallon of gas

quantity of gas in billions of gallons

S

Dt

Qo

PoPn

Qn

consumer’s burden

D’

producer’sburden

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Tax Wedge

• Tax wedge is sum of consumer and producer burdens

• Does the wedge change if the tax is levied on consumers?

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

In-Class Problem

The demand for rutabagas is Q = 1, 900− 100P, and the supply ofrutabagas is Q = 300P − 100.

1. Re-write one of the curves if the producer bears the statutoryincidence of a $4/unit tax on the sale of rutabagas.

2. Who bears the economic incidence of this tax?

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

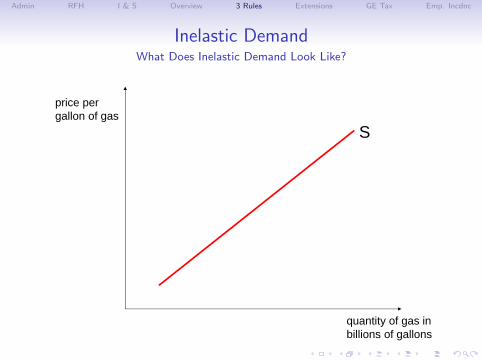

3. Inelastic Party Bears Tax Burden

• Return to statutory tax burden levied on producers

• Consider inelastic demand

• Consider elastic demand

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Inelastic DemandWhat Does Inelastic Demand Look Like?

price pergallon of gas

quantity of gas in billions of gallons

S

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Inelastic DemandWhat is the Original Equilibrium P and Q?

price pergallon of gas

quantity of gas in billions of gallons

SD

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

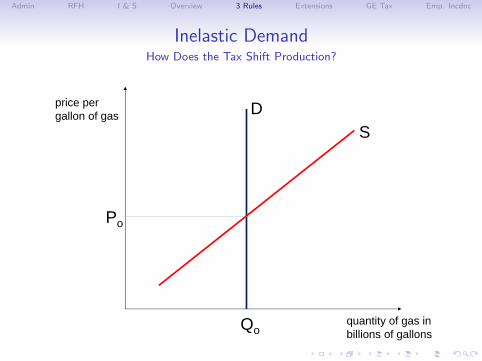

Inelastic DemandHow Does the Tax Shift Production?

price pergallon of gas

quantity of gas in billions of gallons

SD

Qo

Po

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Inelastic DemandWhat Are the New Equilibrium P and Q?

price pergallon of gas

quantity of gas in billions of gallons

SD

S’

tax

Qo

Po

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Inelastic DemandWhat is the Consumer’s Burden?

price pergallon of gas

quantity of gas in billions of gallons

SD

S’

tax

Qo=Qn

Po

Pn

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

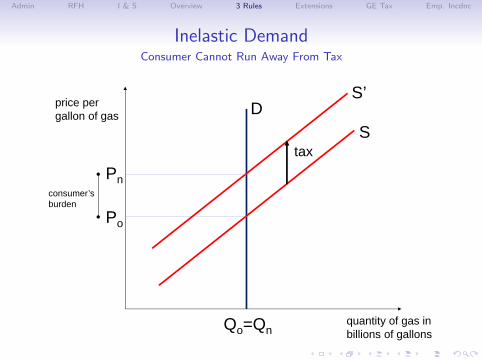

Inelastic DemandConsumer Cannot Run Away From Tax

price pergallon of gas

quantity of gas in billions of gallons

SD

S’

tax

Qo=Qn

Po

Pnconsumer’s burden

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Elastic DemandWhat Does Elastic Demand Look Like?

price pergallon of gas

quantity of gas in billions of gallons

S

Po

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

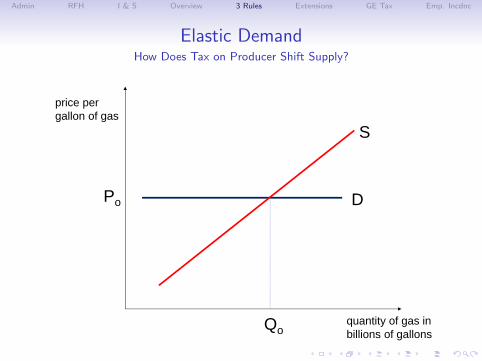

Elastic DemandHow Does Tax on Producer Shift Supply?

price pergallon of gas

quantity of gas in billions of gallons

S

DPo

Qo

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Elastic DemandWhat are the New Equilibrium P and Q?

price pergallon of gas

quantity of gas in billions of gallons

S

D

S’

tax

Po

Qo

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Elastic DemandProducer Bears Entire Burden

price pergallon of gas

quantity of gas in billions of gallons

S

D

S’

tax

Pn=Po

QoQn

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

And the Same is True for Supply

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Tax Incidence Extensions

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Three Extensions

1. Tax incidence in factor markets

2. (skip) Tax incidence in imperfectly competitive markets

3. (skip) Balanced budget tax incidence

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Tax Incidence in Factor Markets

• Suppose a tax is levied on a factor of production• tax on labor• tax on capital, such as land or steel

• Do wages decrease? Or do product prices increase?

• Who bears the burden of the tax?

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Tax Incidence in Factor Markets

• Suppose a tax is levied on a factor of production• tax on labor• tax on capital, such as land or steel

• Do wages decrease? Or do product prices increase?

• Who bears the burden of the tax?

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

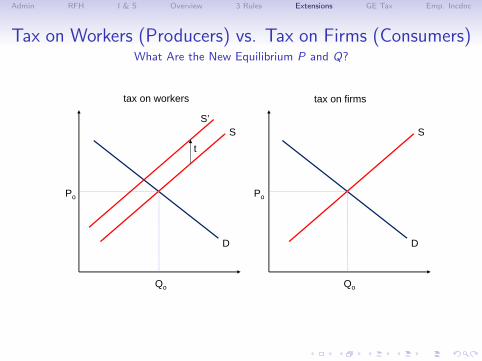

Tax on Workers

• Suppose the government decides to levy a tax on workers

• It can either charge workers via a payroll tax

• Or it can charge employers via a payroll tax

• Does it matter?

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Tax on Workers (Producers) vs. Tax on Firms (Consumers)How Does Tax on Workers (=Producers) Shift Supply?

tax on workers

D

S

Qo

Po

tax on firms

D

S

Qo

Po

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Tax on Workers (Producers) vs. Tax on Firms (Consumers)What Are the New Equilibrium P and Q?

tax on workers

D

S

Qo

Po

t

S’

tax on firms

D

S

Qo

Po

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

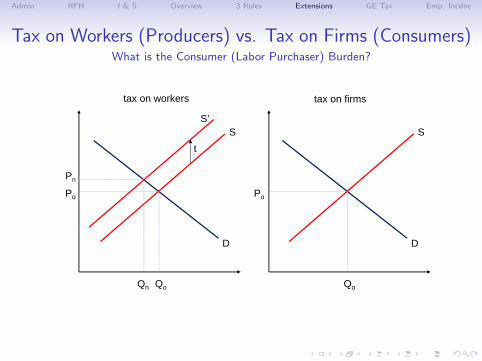

Tax on Workers (Producers) vs. Tax on Firms (Consumers)What is the Consumer (Labor Purchaser) Burden?

tax on workers

D

S

Qo

Po

t

Qn

Pn

S’

tax on firms

D

S

Qo

Po

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Tax on Workers (Producers) vs. Tax on Firms (Consumers)What is the Producer (Worker/Supplier) Burden?

tax on workers

D

S

Qo

Po

t

Qn

Pn

S’

tax on firms

D

S

Qo

Po

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Tax on Workers (Producers) vs. Tax on Firms (Consumers)What if Firms Pay the Payroll Tax?

tax on workers

D

S

Qo

Po

t

Qn

Pn

S’

tax on firms

D

S

Qo

Po

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Tax on Workers (Producers) vs. Tax on Firms (Consumers)New Equilibrium P and Q?

tax on workers

D

S

Qo

Po

t

Qn

Pn

S’

tax on firms

D

S

Qo

Po

D’

t

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

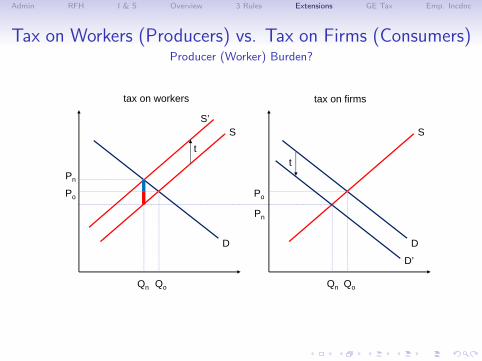

Tax on Workers (Producers) vs. Tax on Firms (Consumers)Producer (Worker) Burden?

tax on workers

D

S

Qo

Po

t

Qn

Pn

S’

tax on firms

D

S

Qo

Po

D’

t

Pn

Qn

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Tax on Workers (Producers) vs. Tax on Firms (Consumers)Consumer (Labor Purchaser) Burden?

tax on workers

D

S

Qo

Po

t

Qn

Pn

S’

tax on firms

D

S

Qo

Po

D’

t

Pn

Qn

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

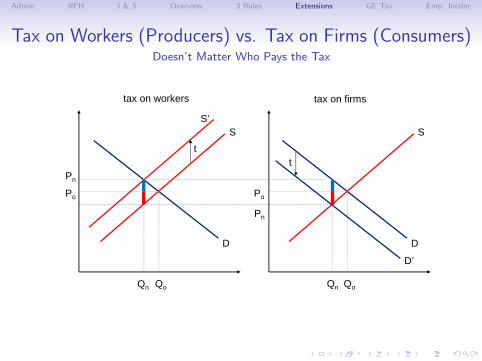

Tax on Workers (Producers) vs. Tax on Firms (Consumers)Doesn’t Matter Who Pays the Tax

tax on workers

D

S

Qo

Po

t

Qn

Pn

S’

tax on firms

D

S

Qo

Po

D’

t

Pn

Qn

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

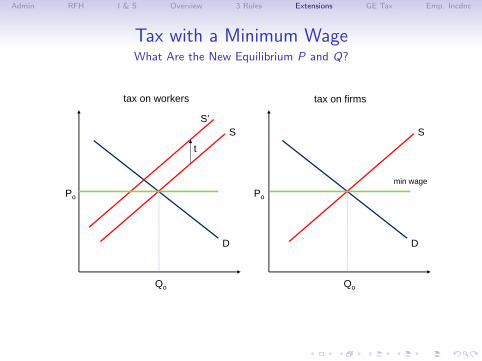

But What If There is an Impediment to Adjustment?

• Suppose that there is a minimum wage

• Compare payroll tax levied on workers

• To payroll tax levied on employers

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Tax with a Minimum WageHow Does Tax on Workers=Producers Shift Supply?

tax on workers

D

S

Qo

Po

tax on firms

D

S

Qo

Po

min wage

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Tax with a Minimum WageWhat Are the New Equilibrium P and Q?

tax on workers

D

S

Qo

Po

t

S’

tax on firms

D

S

Qo

Po

min wage

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

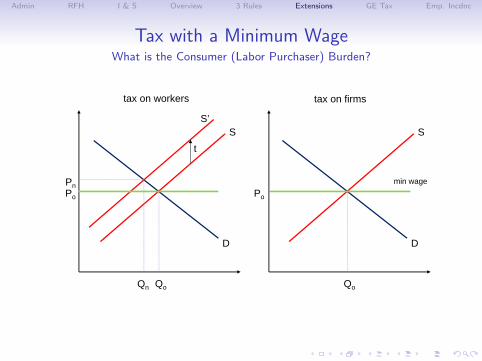

Tax with a Minimum WageWhat is the Consumer (Labor Purchaser) Burden?

tax on workers

D

S

Qo

Po

t

Qn

Pn

S’

tax on firms

D

S

Qo

Po

min wage

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Tax with a Minimum WageWhat is the Producer (Worker Supplier) Burden?

tax on workers

D

S

Qo

Po

t

Qn

Pn

S’

tax on firms

D

S

Qo

Po

min wage

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Tax with a Minimum WageWhat if Firms Pay the Payroll Tax?

tax on workers

D

S

Qo

Po

t

Qn

Pn

S’

tax on firms

D

S

Qo

Po

min wage

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Tax with a Minimum WageNew Equilibrium P and Q?

tax on workers

D

S

Qo

Po

t

Qn

Pn

S’

tax on firms

D

S

Qo

Po

D’

t

min wage

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Tax with a Minimum WageWhat Quantity of Workers Can Firms Get?

tax on workers

D

S

Qo

Po

t

Qn

Pn

S’

tax on firms

D

S

Qo

Po

D’

t

Pdesired

min wage

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

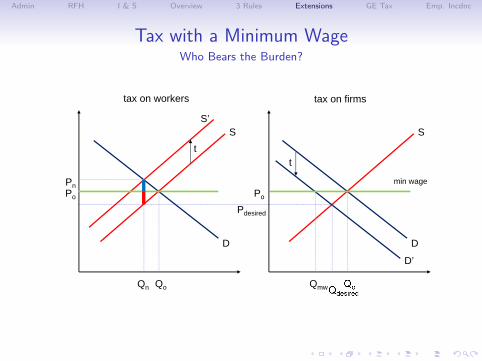

Tax with a Minimum WageWho Bears the Burden?

tax on workers

D

S

Qo

Po

t

Qn

Pn

S’

tax on firms

D

S

Qo

Po

D’

t

Pdesired

Qmw

min wage

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Tax with a Minimum WageConsumers of Labor (Firms) Bear the Burden

tax on workers

D

S

Qo

Po

t

Qn

Pn

S’

tax on firms

D

S

Qo

Po

D’

t

Pdesired

Qmw

min wage

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Summary of Taxes on Inputs

• Barriers to reaching the competitive market equilibrium canmatter for tax incidence

• Other barriers include workplace norms, such as norm for notcutting nominal wages

• More likely to see these features in input, rather than outputmarkets

• Therefore, the party on whom the tax is levied may mattermore in input than output markets

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

General Equilibrium

Tax Incidence

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

General Equilibrium Considerations

1. Illustrative example

2. Issues to consider• time period• scope• spillovers between product markets

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Taxing Restaurants in Lexington, MA

• Suppose that the city of Lexington, MA passes a restauranttax

• Suppose that demand is perfectly elastic – you can go to thenext town to eat dinner

• Who bears the tax: restaurants or diners?

the restaurants

• And what happens to the quantity of restaurant mealsconsumed? declines

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Taxing Restaurants in Lexington, MA

• Suppose that the city of Lexington, MA passes a restauranttax

• Suppose that demand is perfectly elastic – you can go to thenext town to eat dinner

• Who bears the tax: restaurants or diners? the restaurants

• And what happens to the quantity of restaurant mealsconsumed?

declines

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Taxing Restaurants in Lexington, MA

• Suppose that the city of Lexington, MA passes a restauranttax

• Suppose that demand is perfectly elastic – you can go to thenext town to eat dinner

• Who bears the tax: restaurants or diners? the restaurants

• And what happens to the quantity of restaurant mealsconsumed? declines

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

But That’s Not the End

• A restaurant doesn’t pay taxes. In the end, people pay taxes.

• Restaurants use capital and labor – who bears the burden?

• Perhaps in the short run, labor is more elastic than capital, socapital bears the burden =⇒ restaurant owner makes lessmoney

• In the long run? restaurants leave, and landowners make lessmoney

• In economics, land is the one absolutely fixed thing

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

But That’s Not the End

• A restaurant doesn’t pay taxes. In the end, people pay taxes.

• Restaurants use capital and labor – who bears the burden?

• Perhaps in the short run, labor is more elastic than capital, socapital bears the burden =⇒ restaurant owner makes lessmoney

• In the long run?

restaurants leave, and landowners make lessmoney

• In economics, land is the one absolutely fixed thing

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

But That’s Not the End

• A restaurant doesn’t pay taxes. In the end, people pay taxes.

• Restaurants use capital and labor – who bears the burden?

• Perhaps in the short run, labor is more elastic than capital, socapital bears the burden =⇒ restaurant owner makes lessmoney

• In the long run? restaurants leave, and landowners make lessmoney

• In economics, land is the one absolutely fixed thing

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

General Equilibrium Issues: Time Period

Overarching rule for general equilibrium tax incidence is to followthe incidence until you get to a person.

• Long and short-run elasticities should differ – examples?

• In general, the longer the period, the more elastic all factorsare

• Except for land!

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

General Equilibrium Issues: Time Period

Overarching rule for general equilibrium tax incidence is to followthe incidence until you get to a person.

• Long and short-run elasticities should differ – examples?

• In general, the longer the period, the more elastic all factorsare

• Except for land!

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

General Equilibrium Issues: Time Period

Overarching rule for general equilibrium tax incidence is to followthe incidence until you get to a person.

• Long and short-run elasticities should differ – examples?

• In general, the longer the period, the more elastic all factorsare

• Except for land!

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

General Equilibrium Issues: Scope

• Scope of tax matters: elasticity of response to tax onrestaurants in Lexington is different than tax on restaurants inMassachusetts

• Is the supply of workers for the state-wide tax more or lesselastic?

less elastic

• Compare tax on soda to tax on sugar

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

General Equilibrium Issues: Scope

• Scope of tax matters: elasticity of response to tax onrestaurants in Lexington is different than tax on restaurants inMassachusetts

• Is the supply of workers for the state-wide tax more or lesselastic? less elastic

• Compare tax on soda to tax on sugar

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

General Equilibrium Issues: Cross-Product Market Effects

• Tax from one market could spill over in another – examples?

• Textbook uses restaurant meals and babysitters

• Think tax on internet and Netflix usage

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Tax Incidence in the United States

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Distributional Analysis of Taxes Depends on AssumptionsAbout Incidence

Here’s what two major non-partisan organizations assume

Tax Type Incidence

Income by households that pay themPayroll by workers (even the employer part)Excise shifted to prices, so in proportion to consumption

Corporateshifted to owners of capital, so in proportion tocapital income

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Today: Tax Incidence

• Tax incidence: who bears the burden of the tax

1. Statutory incidence 6= economic incidence2. Without impediments, side of the market on which the tax is

levied does not impact incidence3. Less elastic factor bears the burden of the tax

• When there are impediments to reaching market equilibrium,which side of the market bears the tax matters

• General equilibrium tax incidence: the most inelastic factorbears the burden

• Rules of thumb for welfare analysis

Admin RFH I & S Overview 3 Rules Extensions GE Tax Emp. Incdnc

Next Class

• Midterm

• Have a good fall break – no class next week