Lecture 5 & 6 Capital Stocks and Production Costs.

26

Lecture 5 & 6 Capital Stocks and Production Costs

-

Upload

aubrey-henderson -

Category

Documents

-

view

215 -

download

1

Transcript of Lecture 5 & 6 Capital Stocks and Production Costs.

Lecture 5 & 6

Capital Stocks and Production Costs

The nature of capital stocks

• Capital stockA quantity of any resource that is valued for its potential economic

contributions• InvestmentActions taken to increase the quantity or quality of a resource now,

in order to make benefits possible in the future• StockSomething whose quantity can be measured at a point in time• FlowSomething whose quantity can be measured only over a period of

time

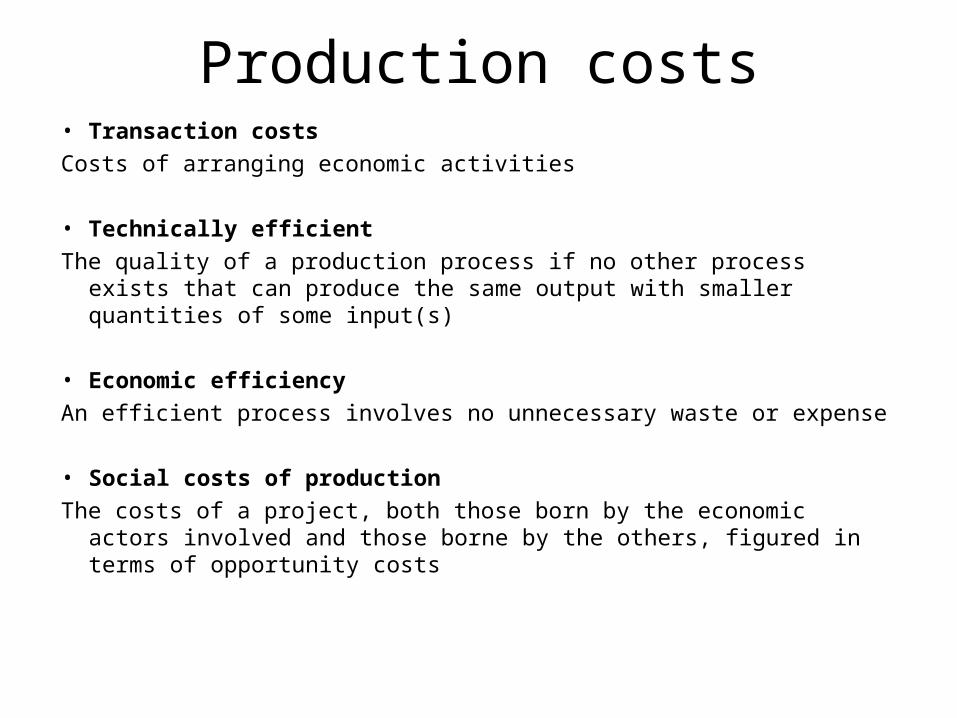

Stocks vs. flows

Additionsor Inflows

Subtractionsor Outflows

Stock

Stocks vs. flows

Deposits of $2000during January

Withdrawals of $1500during January

Balance of $500on January 1

Balance of $1000on February 1

Five forms of capital

• Natural capitalPhysical assets provided by nature• Manufactured capitalAll physical assets that have been made by people• Financial capitalFunds of purchasing power available to facilitate economic activity• Human capitalPeople’s capacity for labor and their individual knowledge and skills• Social capitalThe stock of trust, mutual understanding, shared values, and socially

held knowledge that facilitates the social coordination of economic activity

Production process: A few definitons

• Inputs: resources that go into production• Outputs: the results of production• Waste products: outputs that are not used either for

consumption or in a further production process• Production: transformation of resources or commodities

into things that will ultimately be useful for consumers• Final goods: goods that are ready for use by people• Intermediate goods: goods that will undergo further

processing before they are ready for use

Production costs• Accounting cost: the costs of a project, figured in terms

of monetary flows• Economic costs: the costs of a project, including

opportunity costs

Gail’s Costs of Farming Accounting Costs Seeds $20,000 Fertilizer 3,000 Fuel and transportation 5,000 Interest on bank loan 15,000 Depreciation of equipment 5,000 Total Accounting Costs $48,000

Opportunity Costs Forgone return on equity capital $12,000

Forgone salary 30,000 Total Additional Costs $42,000 Total Economic Costs $90,000

Production costs• Transaction costsCosts of arranging economic activities

• Technically efficientThe quality of a production process if no other process exists that can

produce the same output with smaller quantities of some input(s)

• Economic efficiencyAn efficient process involves no unnecessary waste or expense

• Social costs of productionThe costs of a project, both those born by the economic actors involved and

those borne by the others, figured in terms of opportunity costs

Production function

Production function

• Fixed inputAn input to the production that is fixed in quantity, no matter what

the level of production• Variable inputAn input to production the quantity of which can be quickly

changed, resulting in changes in the level of production• Short-run (for production processes)

A time period in which at least one input to the production cannot be varied in quantity

• Long-run (for production processes)

A time period in which all inputs to production can be varied in quantity

Graphing the relationship between an input and an output

0 1 2 63 875 9

110

170

160

100

140

150

120

130

4

Quantity of Variable Input: Nitrogen (bags)

Qua

ntity

of

Out

put:

C

orn

(bus

hels

)

(2, 127)

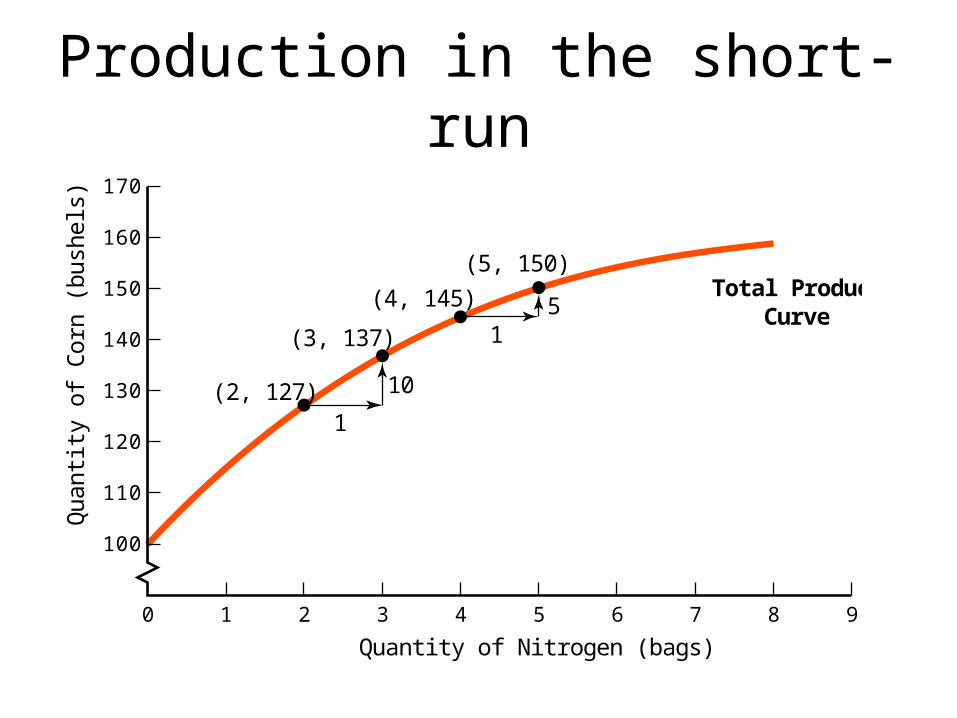

Total product curveA curve showing the total amount of output that can be produced when the quantity of one input is varied (other inputs are held fixed)

Production in the short-run

Marginal return:The additional quantity of output gained by using an additional unit of a variable input (with all other inputs held fixed)

Diminishing marginal returns:The use of an additional unit of a variable input produces a lesser additional quantity of output than did the previous unit of the input

Production in the short-run

0 1 2 63 875 9

110

170

160

100

140

150

120

130

4

Quantity of Nitrogen (bags)

Qu

an

tity

of

Co

rn (

bu

she

ls)

(2, 127)

(3, 137)

(4, 145)

(5, 150)

10

1

51

Total Product Curve

Production in the short-run

Quantity of the Variable Input

Qu

an

tity

of

Ou

tpu

t

(a)

Total Product Curve

Quantity of the Variable Input

Qu

an

tity

of

Ou

tpu

t

(c)

Total Product Curve

Quantity of the Variable Input

Qu

an

tity

of

Ou

tpu

t

(b)

Total Product Curve

Diminishing marginal returns:The use of an additional unit of a variable input produces a lesser additional quantity of output than did the previous unit of the input

Constant marginal returns:The use of an additional unit of a variable input produces the same quantity of additional output as the previous unit of the input

Increasing marginal returns:The use of an additional unit of a variable input produces a greater quantity of additional output than did the previous unit of the input

Production in the short-run

Range ofincreasingreturns

Range ofconstantreturns

Range ofdiminishingreturns

TotalProductCurve

Quantity of the Variable Input

Qu

an

tity

of

Ou

tpu

t

Costs in the short-run

Fixed cost: the cost associated with using fixed inputs, which is the same no matter what quantity of output is produced

Variable cost: the cost associated with using variable inputs, which rises with the quantity of output

Total cost: The sum of fixed cost and variable cost

Marginal cost: The cost associated with producing the last unit of output

Costs in the short-run

63

100 140120 160

510

560

500

540

550

520

530

Quantity of Corn (bushels)

Tota

l Co

st (

$)

Total Cost Curve

(157, 542)

(154, 536)

Total cost curve: a curve showing the total cost associated with producing various levels of output

Costs in the short-runMarginal Cost of Corn Production

(1) Quantity

of Nitrogen

(bags)

(2) Quantity of Corn

(bushels)

(3) Marginal Return to

Additional Nitrogen

(bushels of corn)

(7) Cost of

Additional Nitrogen

($ per bag)

(8) Marginal Cost in

Dollars per Bushel of Corn

($/bushel) = Column(7) ÷ Column(3)

0 100 -- -- -- 1 115 15 6 0.4 2 127 12 6 0.5 3 137 10 6 0.6 4 145 8 6 0.75 5 150 5 6 1.2 6 154 4 6 1.5 7 157 3 6 = 6 3 = 2 8 159 2 6 3

Range ofdecreasingmarginalcost

Range ofconstantmarginalcost

Range ofincreasingmarginalcost

TotalCostCurve

Tota

l Co

st (

$)

MarginalCostCurve

Quantity of Output

Quantity of Output

Ma

rgin

al C

ost

($

)

Constant marginal cost:The cost of producing an additional unit of output stays the same as more output is produced

Decreasing marginal cost:The cost of producing an additional unit of output falls as more output is produced

Increasing marginal cost:The cost of producing an additional unit of output rises as more output is produced

Production and costs in the long-run

• Average cost (or average total cost)

Cost per unit of output, computed as the total cost divided by the quantity of output produced

• Long-run average costThe cost of production, per unit of output when all inputs

can be varied in quantity

Production and costs in the long-run

Quantity of Output

Minimum efficientscale

Maximum efficientscale

Economiesof scale

Diseconomiesof scale

Constant returnsto scale

Lo

ng

-Ru

n A

vera

ge

Co

st (

$)

Long-Run AverageCost Curve

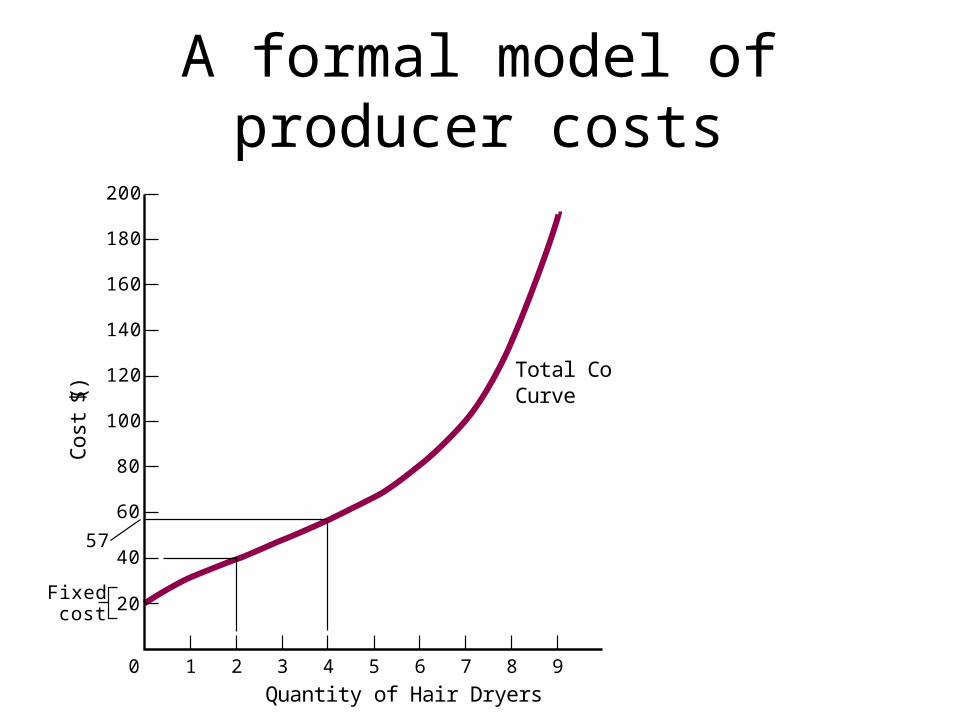

A formal model of producer costs

• Assumptions:– The only producer is the firm– The firm produces only one good, hair dryers– The firm has already decided on a scale of production and

made its choice of Technologies (so, we focus only on its costs in the short-run)

– There are no nonmonetary opportunity costs or externalities

– We have perfect information about the cost structure of the firm

– The firm’s production technology is characterized by diminishing returns to its variable inputs

A formal model of producer costs

Costs of Hair Dryer Production Quantity of Hair Dryers

Fixed Cost ($)

Marginal Cost ($)

Total Cost ($)

Average Total Cost

($)

Variable Cost ($)

Average Variable Cost ($)

0 20 -- 20 0 0.00

1 20 12 32 32.00 12 12.00

2 20 8 40 20.00 20 10.00

3 20 8 48 16.00 28 9.33

4 20 9 57 14.25 37 9.25

5 20 10 67 13.40 47 9.40

6 20 14 81 13.50 61 10.17

7 20 20 101 14.43 81 11.57

8 20 35 136 17.00 116 14.50 9 20 55 191 21.22 171 19.00

A formal model of producer costs

Total CostCurve

Fixedcost 20

40

60

57

80

100

120

140

160

180

200

9876543210

Quantity of Hair Dryers

Co

st (

$)

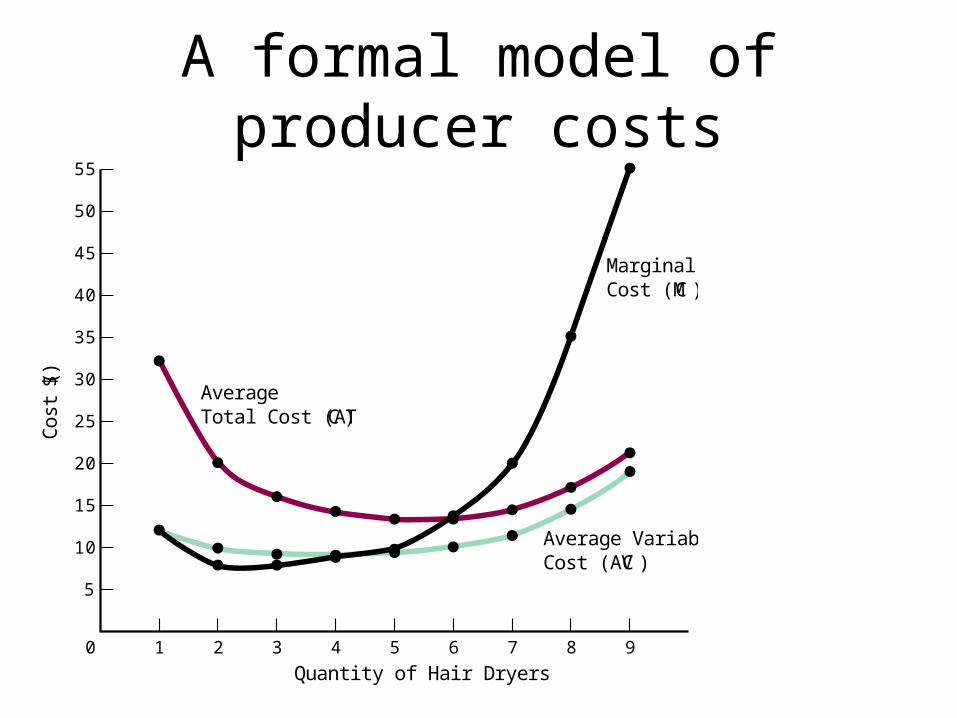

A formal model of producer costs

MarginalCost (MC)

AverageTotal Cost (AT C)

Average VariableCost (AVC)

9876543210

5

10

15

20

25

30

35

40

45

50

55

Quantity of Hair Dryers

Co

st (

$)

A formal model of producer costs

MarginalCost (MC)

AverageTotal Cost (AT C)

Average VariableCost (AVC)

Total Cost

9876543210

5

10

15

20

25

30

35

40

45

50

55

Quantity of Hair Dryers

Co

st (

$)