Lecture 11 International Finance ECON 243 – Summer I, 2005 Prof. Steve Cunningham.

date post

21-Dec-2015Category

view

218download

1

Lecture 4Lecture 4

International FinanceInternational Finance

ECON 243 – Summer I, 2005ECON 243 – Summer I, 2005

Prof. Steve CunninghamProf. Steve Cunningham

Exchange Rate DeterminationExchange Rate Determinationin the Short Runin the Short Run

Asset market approachAsset market approach Focuses on short-run changes in the Focuses on short-run changes in the

demands and supplies for assets demands and supplies for assets denominated in different currenciesdenominated in different currencies

Incorporates a broader market approach Incorporates a broader market approach that considers all financial assets (not just that considers all financial assets (not just money)money)

Emphasizes short-run portfolio adjustments Emphasizes short-run portfolio adjustments by international investorsby international investors

Explains “Explains “overshootingovershooting”—the tendency for ”—the tendency for exchange rates to over-react to news or exchange rates to over-react to news or events.events.

Asset Market ApproachAsset Market Approach

The spot exchange rate of a foreign The spot exchange rate of a foreign currency (currency (ee) is ) is raisedraised on the short on the short run by:run by: A rise in the foreign interest rate A rise in the foreign interest rate

relative to our interest rate (relative to our interest rate (iiff – i – i )) A rise in the expected future spot A rise in the expected future spot

exchange rateexchange rate Both events create an incentive to Both events create an incentive to

accumulate (increase demand) the accumulate (increase demand) the currency, driving up the exchange rate.currency, driving up the exchange rate.

Determinants of ReturnsDeterminants of Returns

Recall that investors determine the Recall that investors determine the total returntotal return on their investment in a on their investment in a bond denominated in a foreign bond denominated in a foreign currency as the sum of:currency as the sum of: The The basic returnbasic return on the bond itself on the bond itself

(interest, “coupon rate”, or yield), and(interest, “coupon rate”, or yield), and The The expected gain or loss on the expected gain or loss on the

currencycurrency exchanges related to to the exchanges related to to the expected appreciation or depreciation of expected appreciation or depreciation of the currency.the currency.

Uncovered Interest ParityUncovered Interest Parity

Uncovered interest parity Uncovered interest parity (whether exact or approximate) (whether exact or approximate) links together four variables:links together four variables: The domestic interest rateThe domestic interest rate The foreign interest rateThe foreign interest rate The current spot exchange rateThe current spot exchange rate The expected future spot rateThe expected future spot rate

Short-runShort-run Determinants of Exchange RatesDeterminants of Exchange Rates

VariableVariable Direction of Int’l Financial Direction of Int’l Financial RepositioningRepositioning

Implication for the Implication for the Current Spot Current Spot Exchange RateExchange Rate

IncreasesIncreases Toward domestic-currency assetsToward domestic-currency assets e decreases (domestic e decreases (domestic currency appreciates)currency appreciates)

DecreasesDecreases Toward foreign-currency assetsToward foreign-currency assets e increases (domestic e increases (domestic currency depreciates)currency depreciates)

Domestic Interest RatesDomestic Interest Rates

Process:Process:Rise in Domestic Interest RatesRise in Domestic Interest Rates

1.1. The The domestic interest rate risesdomestic interest rate rises (foreign interest rate (foreign interest rate stays the same).stays the same).

2.2. Some investors in the two countries will want the Some investors in the two countries will want the domestic investments because of the relatively higher domestic investments because of the relatively higher returns. returns. Portfolios adjust in the direction of the Portfolios adjust in the direction of the domestic-currency assets.domestic-currency assets.

3.3. Foreign investors must buy domestic currency before Foreign investors must buy domestic currency before they can buy these bonds. This creates an increase in they can buy these bonds. This creates an increase in demand for domestic currency.demand for domestic currency.

4.4. Domestic investors will forego foreign bonds in favor of Domestic investors will forego foreign bonds in favor of the domestic ones, thereby reducing the supply of the domestic ones, thereby reducing the supply of domestic currency on the foreign exchange market.domestic currency on the foreign exchange market.

5.5. The increase in demand and the reduction of supply for The increase in demand and the reduction of supply for the domestic currency the domestic currency increases the current spot increases the current spot exchange rate for the domestic currencyexchange rate for the domestic currency..

Short-runShort-run Determinants of Exchange RatesDeterminants of Exchange Rates

VariableVariable Direction of Int’l Financial Direction of Int’l Financial RepositioningRepositioning

Implication for the Implication for the Current Spot Current Spot Exchange RateExchange Rate

IncreasesIncreases Toward foreign-currency assetsToward foreign-currency assets e increases (domestic e increases (domestic currency depreciates)currency depreciates)

DecreasesDecreases Toward domestic-currency assetsToward domestic-currency assets e decreases (domestic e decreases (domestic currency appreciates)currency appreciates)

Foreign Interest RatesForeign Interest Rates

Process:Process:Rise in Foreign Interest RatesRise in Foreign Interest Rates

1.1. The The foreign interest rate risesforeign interest rate rises (domestic interest rate (domestic interest rate stays the same).stays the same).

2.2. Some investors in the two countries will want the Some investors in the two countries will want the foreign investments because of the relatively higher foreign investments because of the relatively higher returns. returns. Portfolios adjust in the direction of the foreign-Portfolios adjust in the direction of the foreign-currency assets.currency assets.

3.3. Domestic investors must buy foreign currency before Domestic investors must buy foreign currency before they can buy these bonds. This creates an increase in they can buy these bonds. This creates an increase in demand for foreign currency.demand for foreign currency.

4.4. Foreign investors will forego domestic bonds in favor of Foreign investors will forego domestic bonds in favor of their own bonds, thereby reducing the supply of foreign their own bonds, thereby reducing the supply of foreign currency on the foreign exchange market.currency on the foreign exchange market.

5.5. The increase in demand and the reduction of supply for The increase in demand and the reduction of supply for the foreign currency the foreign currency increases the current spot increases the current spot exchange rate for the foreign currencyexchange rate for the foreign currency..

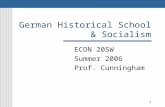

Process: Process: Interest Rates Change in Both Interest Rates Change in Both CountriesCountries

What if interest rates change in both What if interest rates change in both countries? (Exchange rates stay the countries? (Exchange rates stay the same.)same.) Examine the net effect by looking at the Examine the net effect by looking at the

interest rate differential interest rate differential i – ii – if f .. If the interest rate differential increases, If the interest rate differential increases,

then domestic rates have increased then domestic rates have increased relative to foreign rates, and portfolios will relative to foreign rates, and portfolios will adjust in favor of domestic-currency adjust in favor of domestic-currency assets, andassets, and

The domestic currency will appreciate.The domestic currency will appreciate.

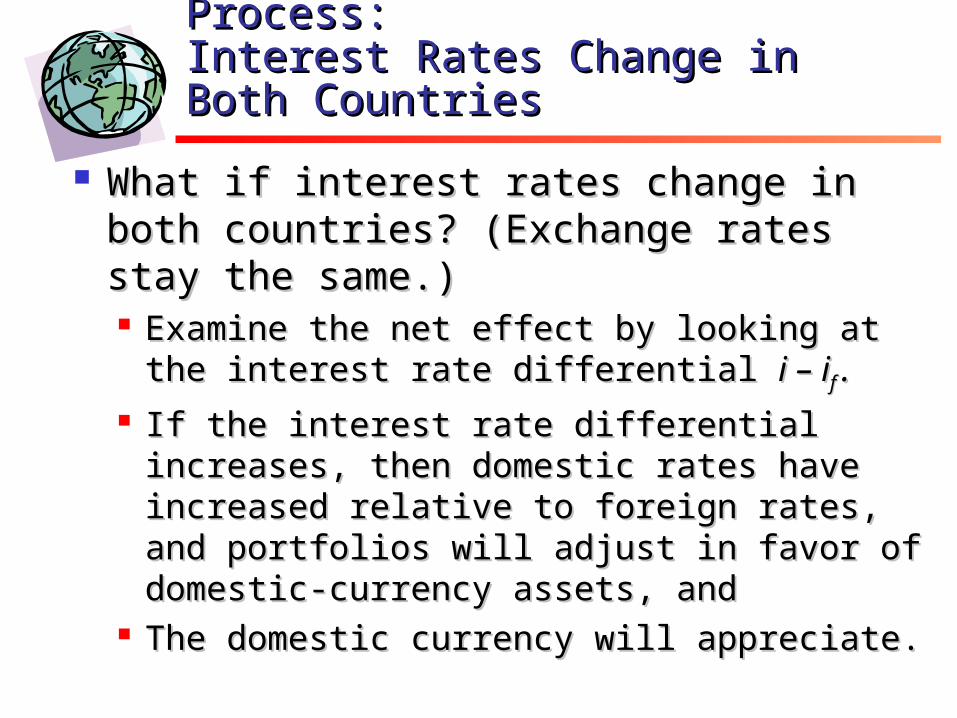

What causes interest rates to What causes interest rates to change?change?

The nominal interest rate The nominal interest rate ii is: is: i = r + i = r + ππe e (Fisher Equation)(Fisher Equation)

where where rr is the real interest rate and is the real interest rate and ππee is the expected inflation rate.is the expected inflation rate.

So nominal interest rates my change So nominal interest rates my change because:because: People’s expectations of future inflation People’s expectations of future inflation

have changed, orhave changed, or Real exchange rates have changed.Real exchange rates have changed.

What causes interest rates What causes interest rates change?change?

If the change in nominal interest rates is If the change in nominal interest rates is caused entirely by a change in caused entirely by a change in inflationary inflationary expectationsexpectations, real returns , real returns have nothave not changed, changed, and there is no reason for an asset shift and there is no reason for an asset shift toward assets denominated in the currency. toward assets denominated in the currency. The exchange rate will not change.The exchange rate will not change.

If the change in nominal rates is caused by a If the change in nominal rates is caused by a change in change in real interest ratesreal interest rates, then real , then real returns returns havehave changed, and investors will changed, and investors will shift portfolios accordingly. shift portfolios accordingly. The exchange The exchange rate will change.rate will change.

Short-runShort-run Determinants of Exchange RatesDeterminants of Exchange Rates

VariableVariable Direction of Int’l Financial Direction of Int’l Financial RepositioningRepositioning

Implication for the Implication for the Current Spot Current Spot Exchange RateExchange Rate

IncreasesIncreases Toward foreign-currency assetsToward foreign-currency assets e increases (domestic e increases (domestic currency depreciates)currency depreciates)

DecreasesDecreases Toward domestic-currency assetsToward domestic-currency assets e decreases (domestic e decreases (domestic currency appreciates)currency appreciates)

Expected Future Spot Exchange RateExpected Future Spot Exchange Rate

Process:Process:Rise in Expected Exchange RateRise in Expected Exchange Rate

Domestic investors Domestic investors expect the future spot exchange rate to be expect the future spot exchange rate to be higherhigher than previously expected. (“Their expectations are than previously expected. (“Their expectations are adjusted upward.”)adjusted upward.”)

They expect the foreign currency to appreciate more They expect the foreign currency to appreciate more (equivalently, they expect the domestic currency to (equivalently, they expect the domestic currency to depreciate less).depreciate less).

If the interest-rate differential is the same, they expect a If the interest-rate differential is the same, they expect a higher return on the exchange rate transaction “on the return higher return on the exchange rate transaction “on the return trip” to the domestic currency. trip” to the domestic currency. Thus they expect a higher total Thus they expect a higher total return based upon the appreciating currencyreturn based upon the appreciating currency..

Domestic investors Domestic investors adjust their portfolios toward the foreign-adjust their portfolios toward the foreign-currency assetscurrency assets..

To do so, they must first buy the foreign currency to be able To do so, they must first buy the foreign currency to be able to buy the foreign-currency assets.to buy the foreign-currency assets.

The demand for the foreign currency increases, and the spot The demand for the foreign currency increases, and the spot exchange rate increases.exchange rate increases. (Foreign currency appreciates.) (Foreign currency appreciates.)

What causes expectations What causes expectations changes?changes?

Bandwagoning Bandwagoning (Destabilizing)(Destabilizing) Speculative bubblesSpeculative bubbles

Belief in theories like PPP Belief in theories like PPP (Stabilizing)(Stabilizing) NewsNews

Changes in gov’t policiesChanges in gov’t policies National or int’l economic news or data National or int’l economic news or data

releases releases Political news or eventsPolitical news or events

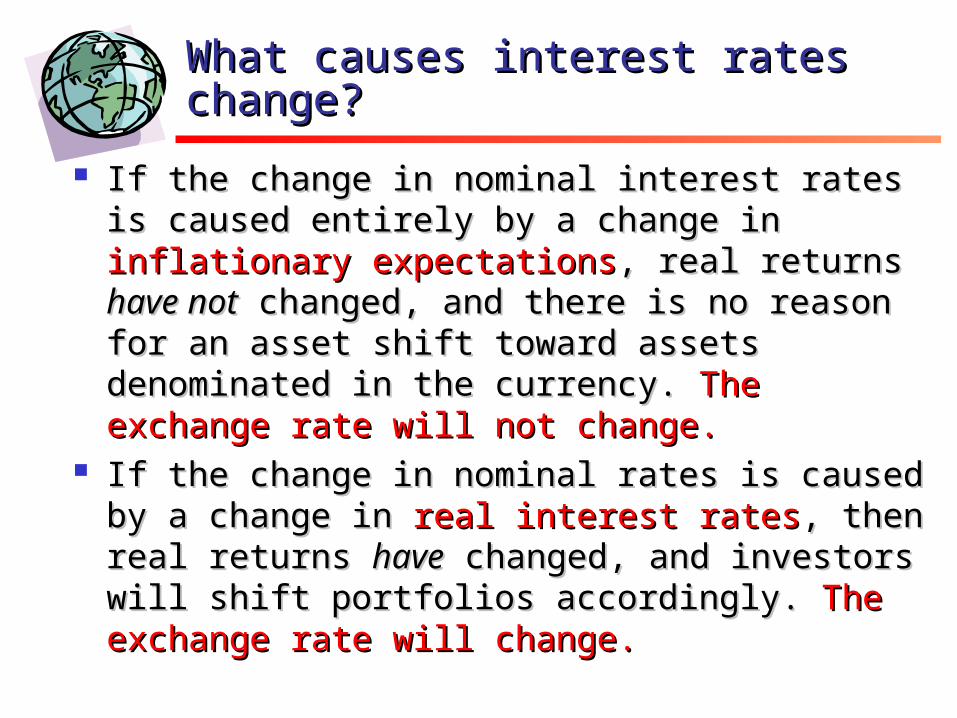

OvershootingOvershooting

Investors Investors cancan react rationally to react rationally to news in such a way as to drive the news in such a way as to drive the exchange rate exchange rate pastpast what they know what they know to be it ultimate long-run equilibrium to be it ultimate long-run equilibrium rate, and then slowly back to that rate, and then slowly back to that rate later on.rate later on.

That is, That is, in the short run, the in the short run, the exchange rate actually overshoots exchange rate actually overshoots its long-run value and then reverts its long-run value and then reverts back toward it.back toward it.

Overshooting SequenceOvershooting Sequence1.1. There is a one-time (unexpected) increase of the money stock by 10%.There is a one-time (unexpected) increase of the money stock by 10%.

2.2. If PPP and the monetary approach are correct, this should mean that in If PPP and the monetary approach are correct, this should mean that in the long run prices and the exchange rate should rise by 10%.the long run prices and the exchange rate should rise by 10%.

3.3. But prices are stickyBut prices are sticky, meaning that in the short run domestic prices do , meaning that in the short run domestic prices do not rise relative to foreign prices.not rise relative to foreign prices.

4.4. Because prices do not rise, the nominal money supply increase Because prices do not rise, the nominal money supply increase amounts to a real money supply increase, and real interest rates fall.amounts to a real money supply increase, and real interest rates fall.

5.5. With lower domestic interest rates, the interest rate differential shifts in With lower domestic interest rates, the interest rate differential shifts in favor of foreign-currency assets. The demand for foreign currency favor of foreign-currency assets. The demand for foreign currency assets and foreign currency increases.assets and foreign currency increases.

6.6. Because of PPP, investors also expect future spot exchange rates to rise Because of PPP, investors also expect future spot exchange rates to rise as well. So investors seek the higher returns resulting from as well. So investors seek the higher returns resulting from bothboth the the interest rate differential and the expect higher future spot exchange interest rate differential and the expect higher future spot exchange rates.rates.

7.7. This (5 and 6) results in the current spot exchange rate rising by This (5 and 6) results in the current spot exchange rate rising by moremore than 10%.than 10%.

8.8. As prices adjust and uncovered interest parity is restored, the exchange As prices adjust and uncovered interest parity is restored, the exchange rate shifts back toward its longer-run equilibrium value.rate shifts back toward its longer-run equilibrium value.

Overshooting: GraphicOvershooting: Graphic

Time

Original rs

10% higher

Time t0 when money supplyunexpectedly rises by 10%

Short-term PredictionShort-term Prediction In recent studies, like that by Frankel and Rose In recent studies, like that by Frankel and Rose

(1995), it appears that (1995), it appears that elaborate structural elaborate structural models are unable to predict any better than a models are unable to predict any better than a naïve modelnaïve model. That is to say that structural . That is to say that structural economic models are useless for predicting economic models are useless for predicting short-run changes in exchange rates.short-run changes in exchange rates.

A A naïve modelnaïve model is one in which the prediction is is one in which the prediction is that the next period’s rate will be the same as that the next period’s rate will be the same as the current period’s rate. (The current period’s the current period’s rate. (The current period’s rate is the best predictor of next period’s rate.) rate is the best predictor of next period’s rate.) This is a This is a random walk modelrandom walk model..

Short-term Prediction Short-term Prediction (Continued)(Continued)

Why are the results so poor?Why are the results so poor? Exchange rates react very strongly to Exchange rates react very strongly to

news.news. News, by definition, is random and News, by definition, is random and

unexpected. (Defies prediction)unexpected. (Defies prediction) OvershootingOvershooting Speculative BubblesSpeculative Bubbles

Self-fulfilling expectations?Self-fulfilling expectations? Trading based upon “technical models”Trading based upon “technical models”

Reasons for PoliciesReasons for Policies StabilizationStabilization—reduce the variability in the —reduce the variability in the

exchange rates to encourage trade.exchange rates to encourage trade. A government may want to keep the A government may want to keep the

exchange value of its currency low to exchange value of its currency low to encourage exports encourage exports and discourage imports. and discourage imports.

In potentially inflationary periods, a In potentially inflationary periods, a government may want to keep the exchange government may want to keep the exchange value of its currency high to value of its currency high to encourage encourage importsimports and provide price competition and provide price competition designed to keep domestic prices in check.designed to keep domestic prices in check.

A strong currency or steady exchange rate A strong currency or steady exchange rate may be considered as a point of may be considered as a point of national national pridepride..

Government PoliciesGovernment Policies

Governments may adopt policies Governments may adopt policies toward the foreign exchange market toward the foreign exchange market in two forms:in two forms: Policies toward the exchange rates Policies toward the exchange rates

themselves, andthemselves, and Policies toward who is allowed to use the Policies toward who is allowed to use the

market, and for what purposes.market, and for what purposes.

Policies Toward Exchange Policies Toward Exchange RatesRates

Choice of regime:Choice of regime: Flexible exchange ratesFlexible exchange rates

Pure floatPure float Dirty/managed floatDirty/managed float

Fixed exchange ratesFixed exchange rates Degree and types of interventionDegree and types of intervention

Polices that Restrict AccessPolices that Restrict Access

No restrictionsNo restrictions Everyone is free to use the foreign exchange Everyone is free to use the foreign exchange

market. The country’s currency is fully market. The country’s currency is fully convertible into foreign currency for all uses.convertible into foreign currency for all uses.

Exchange ControlsExchange Controls Restrictions on the use of foreign exchange.Restrictions on the use of foreign exchange. Extreme forms include requiring that all Extreme forms include requiring that all

foreign payments be turned over to the foreign payments be turned over to the government. If anyone wants/needs “hard government. If anyone wants/needs “hard currency” they have to make a request to a currency” they have to make a request to a gov’t authority.gov’t authority.

Some controls involve allowing access to Some controls involve allowing access to foreign exchange markets for some kinds of foreign exchange markets for some kinds of transactions but not others. transactions but not others.

Capital ControlsCapital Controls

One example of exchange controls is for One example of exchange controls is for the gov’t to allow use of foreign exchange the gov’t to allow use of foreign exchange for import-export, but not for payments for import-export, but not for payments related to financial activities. related to financial activities.

Thus the currency is convertible for Thus the currency is convertible for “current transactions” but not for “current transactions” but not for “capital/financial” transactions.“capital/financial” transactions.

There may be limits on int’l financial There may be limits on int’l financial transactions, or special approvals required.transactions, or special approvals required.

Hence these are referred to as Hence these are referred to as capital capital controlscontrols..

Exchange Rate RegimesExchange Rate Regimes We will discuss the various types of We will discuss the various types of

regimes in the discussion that follows:regimes in the discussion that follows: Floating (Flexible) Exchange RateFloating (Flexible) Exchange Rate

Pure (clean) floatPure (clean) float Managed (dirty) floatManaged (dirty) float

Fixed Exchange RateFixed Exchange Rate Pegged exchange ratePegged exchange rate Adjustable pegAdjustable peg Crawling pegCrawling peg

In reality, there is a spectrum of In reality, there is a spectrum of possibilities ranging from pure float to possibilities ranging from pure float to permanent fix.permanent fix.

Floating Exchange RateFloating Exchange Rate Pure or clean floatPure or clean float: the government allows the : the government allows the

market to determine the exchange rate. The market to determine the exchange rate. The exchange rate is allowed to go to its exchange rate is allowed to go to its equilibrium, driven by private supply and equilibrium, driven by private supply and demand, at all times.demand, at all times.

Official interventionOfficial intervention is the act of the monetary is the act of the monetary authority of a country entering the foreign authority of a country entering the foreign exchange market with the intention of affecting exchange market with the intention of affecting supply and demand, and thus affecting the supply and demand, and thus affecting the equilibrium value of the exchange rate—driving equilibrium value of the exchange rate—driving the rate to a different value that would occur the rate to a different value that would occur by private supply and demand.by private supply and demand.

Floating Exchange Rate Floating Exchange Rate (Continued)(Continued)

A A managed or dirty floatmanaged or dirty float is an approach in is an approach in which the government generally allows the which the government generally allows the exchange rates to float, but periodically exchange rates to float, but periodically chooses to intervene to influence the market chooses to intervene to influence the market rate.rate.

Most governments adopting a floating Most governments adopting a floating exchange rate system do intervene and exchange rate system do intervene and attempt to manage their rates to some attempt to manage their rates to some extent.extent.

Often such intervention (these days) is Often such intervention (these days) is intended to intended to stabilize the currencystabilize the currency, reducing , reducing volatility or dampening short-run erratic volatility or dampening short-run erratic movements in the exchange rate. Thus they movements in the exchange rate. Thus they ““lean against the windlean against the wind”.”.

Fixed Exchange RatesFixed Exchange Rates

Under a fixed exchange rate Under a fixed exchange rate regime, the government sets the regime, the government sets the exchange rate it wants.exchange rate it wants. Some flexibility is allowed within a Some flexibility is allowed within a

narrow trading range, called a narrow trading range, called a bandband.. The official, chosen fixed rate is called The official, chosen fixed rate is called

the the par value par value or or central valuecentral value..

Fixed Exchange Rates Fixed Exchange Rates (Continued)(Continued)

Design of a fixed exchange rate Design of a fixed exchange rate system requires answers to the system requires answers to the following questions:following questions:

1.1. To what do you fix the value of the To what do you fix the value of the currency?currency?

2.2. When or how often do you change the When or how often do you change the fixed value?fixed value?

3.3. How do you defend the fixed value How do you defend the fixed value against market pressures?against market pressures?

Fixing the Value of the CurrencyFixing the Value of the Currency

Fix to goldFix to gold This was the way it was done a century ago.This was the way it was done a century ago. When all currencies are tied to the same When all currencies are tied to the same

commodity, they are all effectively tied to each commodity, they are all effectively tied to each other.other.

Fix to a “basket” of commoditiesFix to a “basket” of commodities (a (a commodity price index).commodity price index).

Fix to another currencyFix to another currency—from WWII until 1970 —from WWII until 1970 the U.S. fixed its currency to gold and most the U.S. fixed its currency to gold and most other nations fixed their currency to the U.S. other nations fixed their currency to the U.S. dollar.dollar.

Fix to a “basket” of currencies—takes Fix to a “basket” of currencies—takes advantage of averaging to reduce volatility advantage of averaging to reduce volatility and to insulate the currency.and to insulate the currency.

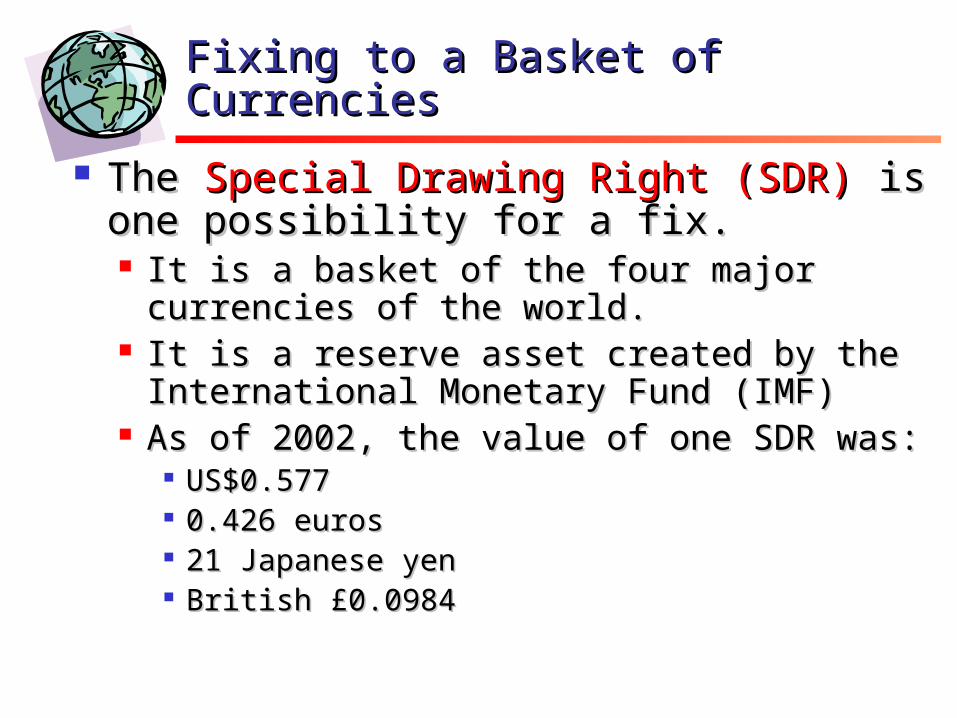

Fixing to a Basket of CurrenciesFixing to a Basket of Currencies

The The Special Drawing Right (SDR)Special Drawing Right (SDR) is is one possibility for a fix.one possibility for a fix. It is a basket of the four major currencies It is a basket of the four major currencies

of the world. of the world. It is a reserve asset created by the It is a reserve asset created by the

International Monetary Fund (IMF)International Monetary Fund (IMF) As of 2002, the value of one SDR was:As of 2002, the value of one SDR was:

US$0.577US$0.577 0.426 euros0.426 euros 21 Japanese yen21 Japanese yen British British £0.0984£0.0984

PegsPegs

Permanent fix?Permanent fix? Pegged exchange ratePegged exchange rate—implies that —implies that

the government probably will exercise the government probably will exercise its right, at some point(s), to “move” its right, at some point(s), to “move” the peg. the peg.

Adjustable pegAdjustable peg—implies that the gov’t —implies that the gov’t will adjust the level of the peg as will adjust the level of the peg as required in the face of substantial required in the face of substantial fundamental changes in the country’s fundamental changes in the country’s international position.international position.

Pegs Pegs (Continued)(Continued)

Crawling pegCrawling peg The exchange rate is changed often, The exchange rate is changed often,

but only by official revaluation.but only by official revaluation. Best of both worlds?Best of both worlds? Allows some Allows some

degree of stability and control, as well degree of stability and control, as well as some degree of flexibility.as some degree of flexibility.

The peg move according to some set of The peg move according to some set of indicators, or according to the gov’t indicators, or according to the gov’t monetary authority.monetary authority.

Central bankers set the rate much as the Central bankers set the rate much as the Fed changes the discount rate. Fed changes the discount rate.

Four ways to Defend the FixFour ways to Defend the Fix

InterventionIntervention, buying or selling in the foreign , buying or selling in the foreign exchange market to influence the equilibrium exchange market to influence the equilibrium spot exchange rate.spot exchange rate.

Exchange controlsExchange controls imposed by the gov’t restrict imposed by the gov’t restrict demand and/or supply. demand and/or supply.

Set domestic interest ratesSet domestic interest rates so as to influence so as to influence short-term capital flows, thus influencing the short-term capital flows, thus influencing the exchange rate by changing the supply and exchange rate by changing the supply and demand in the market.demand in the market.

Macroeconomic adjustmentsMacroeconomic adjustments (changes in fiscal (changes in fiscal or monetary policy) to influence supply and or monetary policy) to influence supply and demand in the foreign exchange market.demand in the foreign exchange market.

SurrenderSurrender

Of course the country can always Of course the country can always give up andgive up and Devalue or revalue its currencyDevalue or revalue its currency Switch to a floating exchange rate and Switch to a floating exchange rate and

allow the exchange rate to go to the allow the exchange rate to go to the market equilibrium rate.market equilibrium rate.

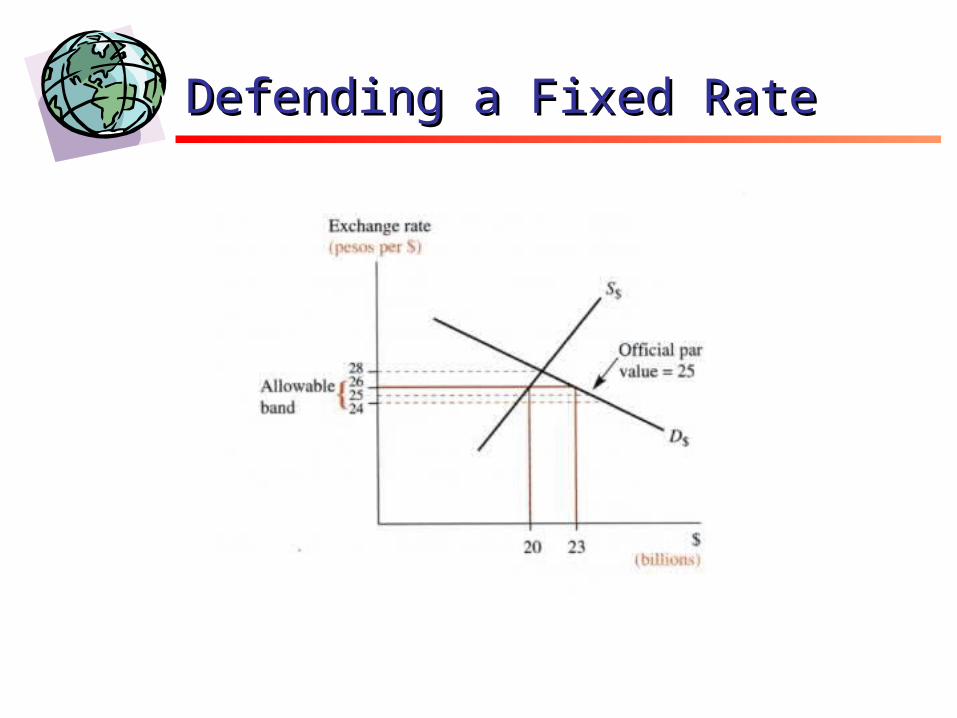

Defending the Fix--InterventionDefending the Fix--Intervention

Consider a country that is attempting Consider a country that is attempting to maintain a fixed rate of 25 pesos to to maintain a fixed rate of 25 pesos to the US dollar, with a band of the US dollar, with a band of ±4% (±1 ±4% (±1 peso).peso).

The market is pushing the exchange The market is pushing the exchange rate above the top of its band (i.e., to rate above the top of its band (i.e., to 28 pesos per dollar).28 pesos per dollar).

The monetary authority in the country The monetary authority in the country must enter the market and sell dollars must enter the market and sell dollars and buy their own pesos.and buy their own pesos.

Defending a Fixed RateDefending a Fixed Rate

Where does it get the Where does it get the dollars?dollars?

If it holds U.S. Treasury bonds as reserves, If it holds U.S. Treasury bonds as reserves, it sells the bonds on the international it sells the bonds on the international market in return for U.S. dollars. market in return for U.S. dollars.

If it holds assets denominated in, say, yen, If it holds assets denominated in, say, yen, it sells those assets for yen, and then it sells those assets for yen, and then trades the yen for dollars.trades the yen for dollars.

It may borrow the dollars from the IMF if it It may borrow the dollars from the IMF if it has a reserve position with the IMF.has a reserve position with the IMF.

It could sell gold or any other asset to raise It could sell gold or any other asset to raise dollars, or another currency tradable for dollars, or another currency tradable for dollars.dollars.

Swap LinesSwap Lines

The country The country maymay be able to borrow be able to borrow the dollars directly from the U.S. the dollars directly from the U.S. Federal Reserve. Federal Reserve.

It may have an agreement with the It may have an agreement with the Fed to “swap” each other’s currencies Fed to “swap” each other’s currencies on demand within certain on demand within certain parameters.parameters.

(The monetary authority may also (The monetary authority may also borrow from private sources.) borrow from private sources.)

Reserve CurrencyReserve Currency

Because the U.S. dollar is held by Because the U.S. dollar is held by monetary authorities in most monetary authorities in most countries, the U.S. can effectively countries, the U.S. can effectively borrow by issuing bonds and notes borrow by issuing bonds and notes and selling them to another monetary and selling them to another monetary authority. This makes the financing of authority. This makes the financing of deficits:deficits: Particularly easyParticularly easy Less burden on the domestic economyLess burden on the domestic economy

Sterilized Money?Sterilized Money? If the monetary authority engages in If the monetary authority engages in

exchange market intervention AND exchange market intervention AND separately takes other actions (makes separately takes other actions (makes other transactions, etc.) to insulate other transactions, etc.) to insulate the domestic economy from the the domestic economy from the foreign exchange transaction, this is foreign exchange transaction, this is called a called a sterilized interventionsterilized intervention and the and the secondary domestic market secondary domestic market transaction is called a transaction is called a sterilizationsterilization..

An intervention may be An intervention may be sterilizedsterilized or or unsterilizedunsterilized..

Temporary ImbalancesTemporary Imbalances

Financing Temporary Financing Temporary ImbalancesImbalances

The monetary authority makes The monetary authority makes offsetting transactions during the offsetting transactions during the periods of deficits and surpluses.periods of deficits and surpluses.

The monetary authority must ensure The monetary authority must ensure that private speculators do not see or that private speculators do not see or cannot take advantage of the swings.cannot take advantage of the swings.

The monetary authority must forecast The monetary authority must forecast correctly and time its interventions correctly and time its interventions well.well.

Financing Permanent Financing Permanent ImbalancesImbalances

What if the disequilibrium in the foreign What if the disequilibrium in the foreign exchange market is exchange market is fundamental fundamental ??

Consider a case in which the country is facing Consider a case in which the country is facing continuing downward pressure on its currency.continuing downward pressure on its currency.

The monetary authority must continually The monetary authority must continually intervene to sell foreign currency to maintain intervene to sell foreign currency to maintain its fix. its fix.

Eventually, the country will run out of reserves Eventually, the country will run out of reserves to sell and also run out of credit on which to to sell and also run out of credit on which to borrow reserves.borrow reserves.

Ultimately, it must devalue its currency.Ultimately, it must devalue its currency.

And worse…And worse…

If private investors catch on, seeing If private investors catch on, seeing the reserve losses in the monetary the reserve losses in the monetary authority, speculation regarding a authority, speculation regarding a devaluation will ensue. devaluation will ensue.

Speculators will sell domestic Speculators will sell domestic currency, requiring more interventioncurrency, requiring more intervention—they make things worse. —they make things worse.

The monetary authority runs out of The monetary authority runs out of reserves or must devalue sooner.reserves or must devalue sooner.

Exchange Control PoliciesExchange Control Policies

According to the IMF, in 2001, about 78 According to the IMF, in 2001, about 78 developing countries had comprehensive developing countries had comprehensive exchange controls in place.exchange controls in place.

The controls included requirements The controls included requirements related to related to Export proceedsExport proceeds Restrictions on payments for both current Restrictions on payments for both current

and capital transactionsand capital transactions About 40 countries had controls on About 40 countries had controls on

capital transactions.capital transactions.

Exchange Controls Exchange Controls (Continued)(Continued)

Many countries: Many countries: Had persistent BOP deficitsHad persistent BOP deficits Were defending a fixed exchange rateWere defending a fixed exchange rate Attempting to maintain that fix by Attempting to maintain that fix by

restricting their residents’ ability to buy restricting their residents’ ability to buy imports, travel abroad, or invest abroad.imports, travel abroad, or invest abroad.

Exchange controls operate similar to Exchange controls operate similar to quotas, limiting imports by limiting quotas, limiting imports by limiting the access to the currency with which the access to the currency with which to buy the imports.to buy the imports.

Exchange Controls Exchange Controls (Continued)(Continued)

Besides the direct welfare costs to Besides the direct welfare costs to society, exchange controls have other society, exchange controls have other effects:effects: Governments usually allocate the right to Governments usually allocate the right to

buy foreign currency according to buy foreign currency according to complicated rules.complicated rules.

This creates high administrative costs and high This creates high administrative costs and high private resource costs in dealing with the rules.private resource costs in dealing with the rules.

Governments also often allocate according to Governments also often allocate according to political pressures and not according to political pressures and not according to economic priorities, leading to economic economic priorities, leading to economic inefficiencies.inefficiencies.

Exchange Controls Exchange Controls (Continued)(Continued)

Additional costs (continued)Additional costs (continued) Predictably, people attempt to Predictably, people attempt to

circumvent the controls. This leads tocircumvent the controls. This leads to Parallel or “black” marketsParallel or “black” markets Government corruption and briberyGovernment corruption and bribery

1860-19131860-1913

The Gold Standard EmergesThe Gold Standard Emerges The relative prices of gold and silver viz a viz The relative prices of gold and silver viz a viz

the British pound resulted in silver leaving the British pound resulted in silver leaving Britain and gold going to Britain.Britain and gold going to Britain.

Gold discoveries in California, Australia, Gold discoveries in California, Australia, Alaska, and South Africa were large enough to Alaska, and South Africa were large enough to make gold popular, but not so large as to drive make gold popular, but not so large as to drive its price down.its price down.

Silver mining expanded and was more Silver mining expanded and was more abundant, driving its price down strongly.abundant, driving its price down strongly.

By 1870s, gold was the international standard. By 1870s, gold was the international standard. Most countries were fixing their currency to Most countries were fixing their currency to gold.gold.

Why wasn’t gold moving?Why wasn’t gold moving?

One apparent puzzle is “why aren’t there One apparent puzzle is “why aren’t there more gold shipments during this period to more gold shipments during this period to offset BOP imbalances under fixed offset BOP imbalances under fixed exchange rates?exchange rates?

Answer: Most countries were running Answer: Most countries were running payments surpluses (before WWI), and payments surpluses (before WWI), and had large gold supplies due to new gold had large gold supplies due to new gold finds and mines. finds and mines. Britain had payments deficits, but because its Britain had payments deficits, but because its

currency was a key reserve currency, it was currency was a key reserve currency, it was able to get most countries to hold its “IOUs”.able to get most countries to hold its “IOUs”.

Why wasn’t gold moving? Why wasn’t gold moving? (Continued)(Continued)

Everyone wanted to hold short-term Everyone wanted to hold short-term British financial assets.British financial assets. So if Britain want to “bring pounds home” it So if Britain want to “bring pounds home” it

could just raise the interest rates a little bit.could just raise the interest rates a little bit. Essentially, “bringing pounds home” would Essentially, “bringing pounds home” would

contract the entire world’s money supply.contract the entire world’s money supply. Central banks (etc.) were not engaged Central banks (etc.) were not engaged

in full employment policies.in full employment policies. The pre-WWI era was very tranquil.The pre-WWI era was very tranquil.

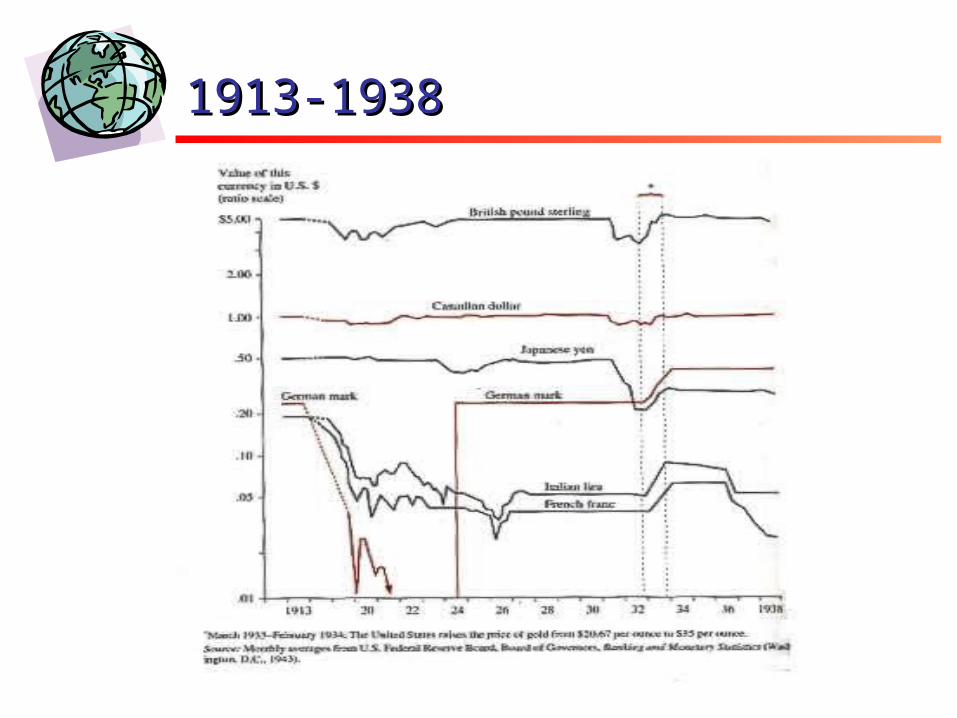

1913-19381913-1938

The Interwar PeriodThe Interwar Period

World War I (1914-1917)World War I (1914-1917) Post WWI Chaos (1919-1923)Post WWI Chaos (1919-1923) Britain’s Great Depression (1922-1939?)Britain’s Great Depression (1922-1939?) U.S. Great Depression (1929-1939, U.S. Great Depression (1929-1939,

worst in 1931-1934)worst in 1931-1934) British “pre-war parity” at $4.85556 British “pre-war parity” at $4.85556

(1925)(1925) German hyperinflation (1922-1923)German hyperinflation (1922-1923) Futility of fixed exchange rates?Futility of fixed exchange rates?

Conclusions from Interwar Conclusions from Interwar PeriodPeriod

Flexible exchange rates can be extremely Flexible exchange rates can be extremely volatile.volatile.

Fixed exchange rates can be nearly Fixed exchange rates can be nearly impossible to maintain in the face of impossible to maintain in the face of economic shocks.economic shocks.

Flexible exchange rates can cushion Flexible exchange rates can cushion international shocks, insulating economies international shocks, insulating economies from the economic shocks in other from the economic shocks in other economies.economies.

Speculation can be stabilizing.Speculation can be stabilizing. Domestic monetary and fiscal policy can Domestic monetary and fiscal policy can

be destabilizing.be destabilizing.

Bretton Woods, 1944Bretton Woods, 1944 Compromise based upon interwar Compromise based upon interwar

experience.experience. The U.S. had a huge BOP surplus since we The U.S. had a huge BOP surplus since we

were one of the few industrialized countries were one of the few industrialized countries still intact and producing.still intact and producing.

J.M. Keynes and Harry Dexter White J.M. Keynes and Harry Dexter White proposed:proposed: A new world central bank A new world central bank Fixed exchange rates, and Fixed exchange rates, and A new focus in individual and coordinated A new focus in individual and coordinated

macro policies directed toward BOP equilibrium.macro policies directed toward BOP equilibrium. Similar to the EU?Similar to the EU?

Bretton Woods Bretton Woods (Continued)(Continued)

The Bretton Woods SystemThe Bretton Woods System Adjustable pegAdjustable peg Short-run financing of a pegged par could be Short-run financing of a pegged par could be

financed by int’l reserves, but persistent financed by int’l reserves, but persistent “fundamental” disequilibria would require adjusting “fundamental” disequilibria would require adjusting the peg to revalue.the peg to revalue.

The IMF was created with reserves contributed by The IMF was created with reserves contributed by member nations. All member gov’ts can borrow to member nations. All member gov’ts can borrow to finance temporary deficits.finance temporary deficits.

The U.S. dollar was set at the official exchange rate The U.S. dollar was set at the official exchange rate of $35 per ounce of gold.of $35 per ounce of gold.

Other currencies fixed to a par with the U.S. dollar. Other currencies fixed to a par with the U.S. dollar. This is sometimes called a This is sometimes called a gold-exchange standardgold-exchange standard..

Bretton Woods Bretton Woods (continued)(continued)

The system became increasingly The system became increasingly unsustainable because:unsustainable because: Speculative pressures on weak currencies.Speculative pressures on weak currencies. As Europe (via the Marshall plan, etc.) and As Europe (via the Marshall plan, etc.) and

Japan recovered from the war, they Japan recovered from the war, they became very competitive and became net became very competitive and became net exporters. The U.S. fell into large official exporters. The U.S. fell into large official settlements balance deficits, and had to settlements balance deficits, and had to settle by shipping gold (reserves).settle by shipping gold (reserves).

Other countries became concerned about Other countries became concerned about the U.S.’s ability to pay.the U.S.’s ability to pay.

The U.S. was running out of gold.The U.S. was running out of gold.

Bretton Woods Bretton Woods (continued)(continued)

Unsustainable…Unsustainable… The U.S. tried minor exchange controls.The U.S. tried minor exchange controls. The U.S. could have devalued its currency relative to gold, The U.S. could have devalued its currency relative to gold,

but the Soviet Union and South Africa had large gold but the Soviet Union and South Africa had large gold reserves and would have gained politically from this. This reserves and would have gained politically from this. This was not considered politically viable.was not considered politically viable.

In August 1971, President Nixon suspended convertibility of In August 1971, President Nixon suspended convertibility of the dollar into gold. He also imposed a 10% temporary the dollar into gold. He also imposed a 10% temporary tariff on all imports until revaluation.tariff on all imports until revaluation.

Most currencies floated against the dollar until December Most currencies floated against the dollar until December 1971 when the Smithsonian Agreement attempted to repair 1971 when the Smithsonian Agreement attempted to repair the Bretton Woods system by a system of devaluations. the Bretton Woods system by a system of devaluations.

This agreement never really worked. By March 1973, most This agreement never really worked. By March 1973, most currencies had shifted to a floating regime against the currencies had shifted to a floating regime against the dollar.dollar.

1950-19811950-1981

Limited Anarchy?Limited Anarchy?

The current system is sometimes described The current system is sometimes described as a as a managed floating regimemanaged floating regime..

Some countries have attempted to resist Some countries have attempted to resist flexible rates.flexible rates. The European Economic Community (forerunner The European Economic Community (forerunner

of the European Union) tried to set up of the European Union) tried to set up maximum ranges of variance across their rates, maximum ranges of variance across their rates, setting up the “snake” within the “tunnel” in setting up the “snake” within the “tunnel” in December 1971 (allowing fluctuations—the December 1971 (allowing fluctuations—the snake—within a trading band—the tunnel)snake—within a trading band—the tunnel)

Quickly Britain, Italy, and France had their Quickly Britain, Italy, and France had their currencies move outside the agreed-upon band.currencies move outside the agreed-upon band.

U.S. Stance on ExchangeU.S. Stance on Exchange The U.S. has often (early 1970s, 1980-84, The U.S. has often (early 1970s, 1980-84,

1995-98) nearly ignored the exchange 1995-98) nearly ignored the exchange rate of the dollar against other rate of the dollar against other currencies. currencies.

The U.S. had effectively no policy, no The U.S. had effectively no policy, no exchange-market intervention during exchange-market intervention during these periods, leading to the phrase these periods, leading to the phrase ““policy of benign neglectpolicy of benign neglect”.”.

There have been a number of crises in There have been a number of crises in the markets, including the German the markets, including the German Reunification (1992-93) and the Asian Reunification (1992-93) and the Asian Crisis (1997).Crisis (1997).