Lecture 3: Country Risk - Harvard University 119/API-119 slides/L3... · Lecture 3: Country Risk 1....

23

API-119 - Prof.J.Frankel Lecture 3: Country Risk 1. The portfolio-balance model with default risk. 2. Default. 3. What determines sovereign spreads? 4. Debt Sustainability Analysis (DSA).

Transcript of Lecture 3: Country Risk - Harvard University 119/API-119 slides/L3... · Lecture 3: Country Risk 1....

API-119 - Prof.J.Frankel

Lecture 3: Country Risk

1. The portfolio-balance model with default risk.

2. Default.

3. What determines sovereign spreads?

4. Debt Sustainability Analysis (DSA).

API-119 - Prof.J.Frankel

• The portfolio-balance model can be very general (menu of assets).

– In Lecture 2, we considered a special case relevant to rich-country bonds: currency risk is the only risk.

– Some modifications are appropriate for developing-country debt, starting with the risk of default.

• One lesson of portfolio diversification theory: A country that borrows too much drives up the expected rate of return it must pay. The supply of funds is not infinitely elastic. -- especially for developing countries.

1. The portfolio balance model applied to country risk

Demand for assets issued by various countries f:

x i, t = Ai + [ρV]i -1 Et (r ft+1 – r dt+1) ;

• Now the expected return Et (r ft+1) subtracts from i ft

the probability of default times loss in event of default.

• Similarly, the variances & covariances factor in risks of loss through default.

• When perceptions of risk are high [ρV], interest rates must be high for investors to absorb given supplies of debt

– “risk off” in global financial markets.

API-119 - Prof.J.Frankel

API-119 - Prof.J.Frankel

Developing countries:

• are usually assumed to be debtors;

• Debt to foreigners was usually $-denominated (before 2000).

• Then, expected return = observed spread between interest rate on the country’s loans or bonds & risk-free $ rate, minus expected loss through default -- instead of rp .

• Denominator for Debt : More relevant than world wealth is

the country’s GDP or X. Why? Earnings determine ability to repay.

• Supply-of-lending-curve slopes up: when debt is large investors fear default & build a country risk premium into i.

• must pay a premium as compensation for default risk.

The view from the South

Source: Reinhart and Rogoff, This Time is Different: Eight Centuries of Financial Folly, 2011, pp.86-100.

2. Default

• Venezuela has defaulted 9 times since independence in 1821. • Nigeria has defaulted 5 times since independence in 1960. • Greece has been in default on its debt half the time since independence in 1829. • Spain has defaulted the most: 6 times in the 18th century, and 7 in the 19th.

Latin American

independence

Great Depression

The international debt crisis

GFC

Asia crisis

Why don’t debtor countries default more often, given absence of an international enforcement mechanism?

1. They want to preserve their creditworthiness, to borrow again in the future. Kletzer & Wright (2000), Amador (2003), Aguiar & Gopinath (2006), Arellano (2008), Yue (2010).

But: • Some find defaulters don’t seem to bear much of a penalty for long: Eichengreen (1987), Eichengreen & Portes (2000), Arellano (2009), Panizza, Sturzenegger & Zettelmeyer (2009).

• Not a sustainable repeated-game equilibrium: Bulow-Rogoff (1989).

2. Best answer (perhaps): Defaulters may lose access to international banking system, including trade credit.

Loss of credit disrupts production, even for export. Theory: Eaton & Gersovitz (RES 1981, EER 1986). Evidence: Rose (JDE 2005).

3. Cynical answer: Finance Ministers want to remain members in good standing of the international elite.

API-119 - Prof.J.Frankel

New finding: For some years after a restructuring, the defaulter is excluded from access to international finance.

Juan Cruces &

Christoph Trebesch,

2013, “Sovereign

Defaults: The Price

of Haircuts,” AEJ: Macro,

Fig.5, p. 111.

Estimated from 67 restructurings,

1980-2009

API-119 - Prof.J.Frankel

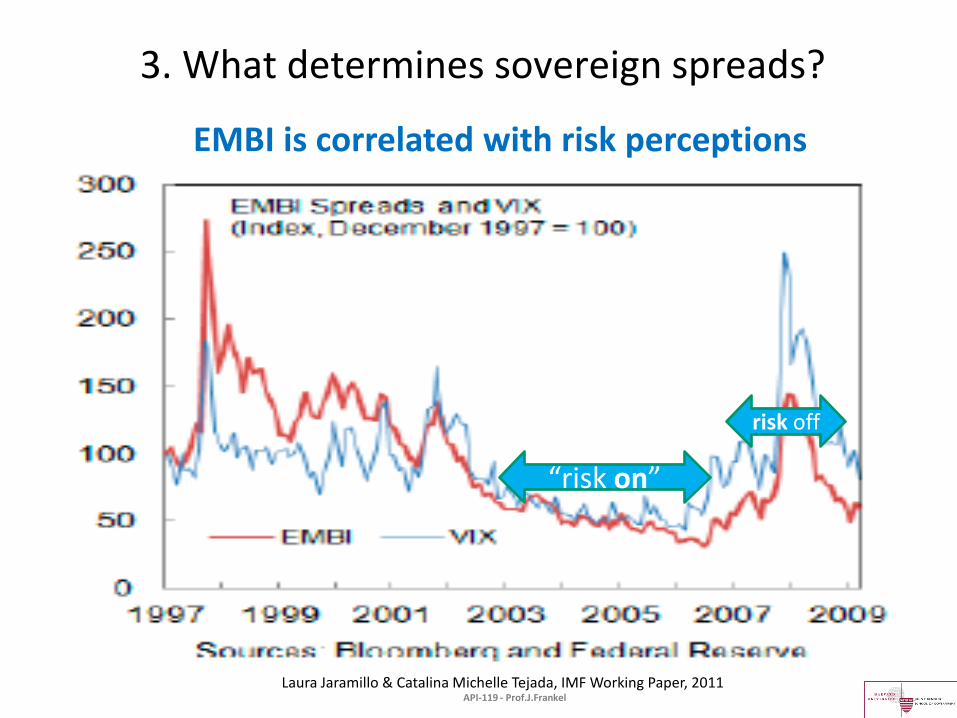

Laura Jaramillo & Catalina Michelle Tejada, IMF Working Paper, 2011

EMBI is correlated with risk perceptions

“risk on”

risk off

API-119 - Prof.J.Frankel

3. What determines sovereign spreads?

For some years after a restructuring, the defaulter has to pay higher interest rates,

especially if creditors had to take a big write-down (“haircut”).

Estimated, 1993-2010

Cruces & Trebesch, 2013, “Sovereign Defaults: The Price of Haircuts,” Fig.3.

API-119 - Prof.J.Frankel

especially the 1st 5 years

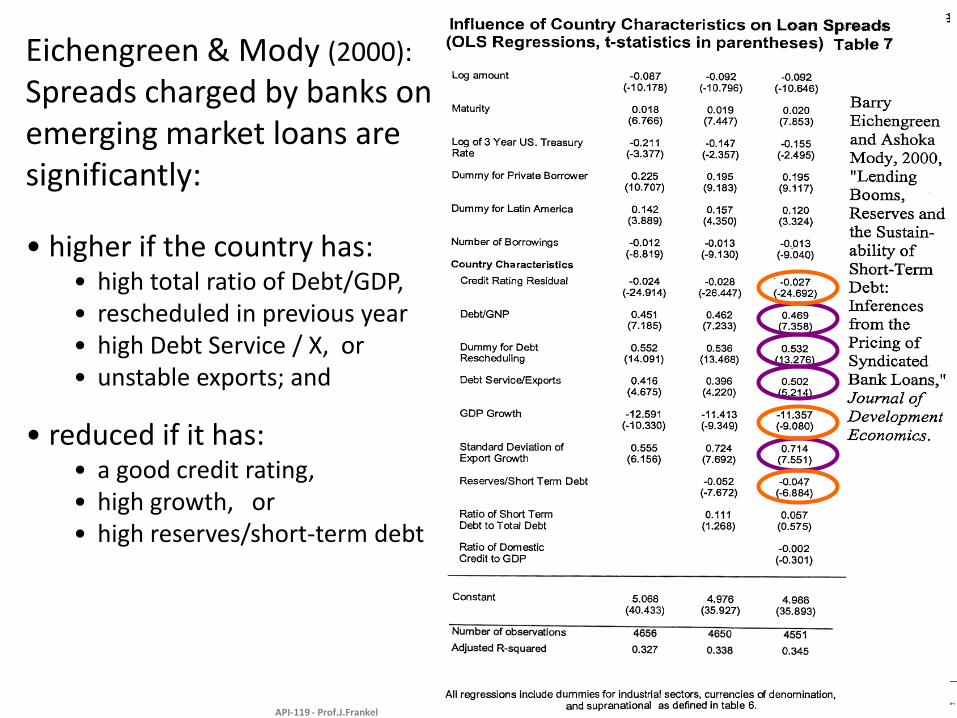

Eichengreen & Mody (2000):

Spreads charged by banks on emerging market loans are significantly:

• higher if the country has: • high total ratio of Debt/GDP, • rescheduled in previous year • high Debt Service / X, or • unstable exports; and

• reduced if it has: • a good credit rating, • high growth, or • high reserves/short-term debt

API-119 - Prof.J.Frankel

API-119 - Prof.J.Frankel

• The spread may rise steeply when Debt/GDP is high.

b

iSupply of

funds from world

investors

≡ Debt/GDP

Stiglitz: it may even bend backwards, due to rising risk of default.

• What determines if a country becomes “insolvent”?

• It depends not on the level of debt directly,

• but, rather, on whether the ratio b ≡ debt/GDP is on an unsustainable path.

API-119 - Prof.J.Frankel

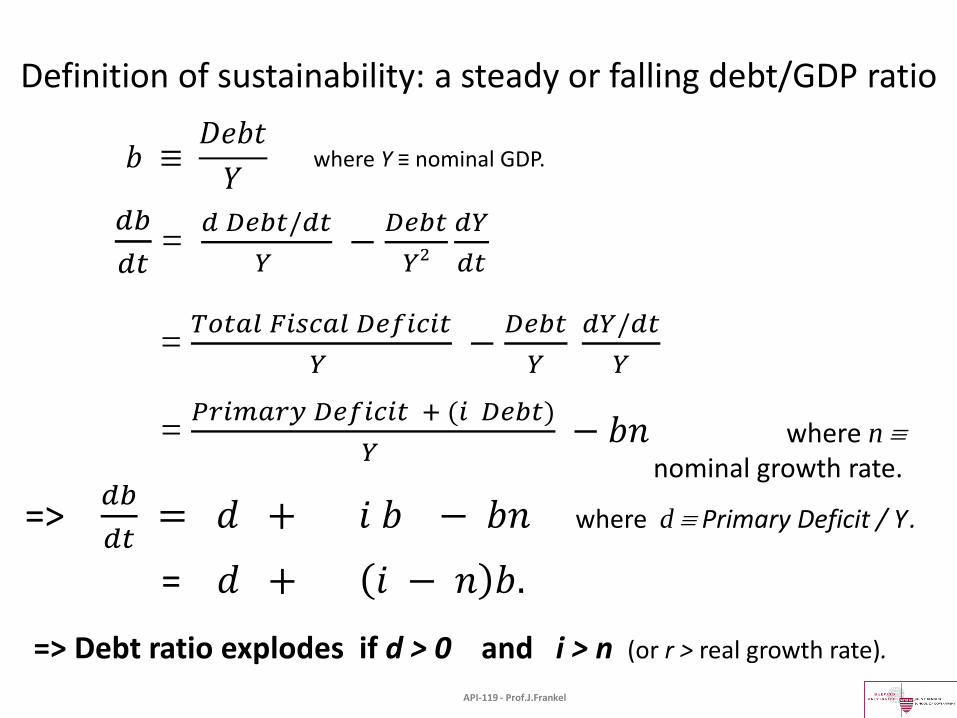

4. Debt dynamics:

where n nominal growth rate.

=> Debt ratio explodes if d > 0 and i > n (or r > real growth rate).

where Y ≡ nominal GDP.

Definition of sustainability: a steady or falling debt/GDP ratio

API-119 - Prof.J.Frankel

= 𝑃𝑟𝑖𝑚𝑎𝑟𝑦 𝐷𝑒𝑓𝑖𝑐𝑖𝑡 + (𝑖 𝐷𝑒𝑏𝑡)

𝑌 − 𝑏𝑛

= 𝑇𝑜𝑡𝑎𝑙 𝐹𝑖𝑠𝑐𝑎𝑙 𝐷𝑒𝑓𝑖𝑐𝑖𝑡

𝑌 −

𝐷𝑒𝑏𝑡

𝑌 𝑑𝑌/𝑑𝑡

𝑌

𝑑𝑏

𝑑𝑡 =

𝑑 𝐷𝑒𝑏𝑡/𝑑𝑡

𝑌 −

𝐷𝑒𝑏𝑡

𝑌2

𝑑𝑌

𝑑𝑡

𝑏 ≡ 𝐷𝑒𝑏𝑡

𝑌

=> 𝑑𝑏

𝑑𝑡 = 𝑑 + 𝑖 𝑏 − 𝑏𝑛 where d Primary Deficit / Y .

= 𝑑 + 𝑖 − 𝑛 𝑏.

dt

db

Y

Debtb = d + (i - n) b. where

n nominal growth rate, and d primary deficit / Y .

n1

ius

i

b

range of explosive debt

range of

declining Debt/GDP ratio

0

db/dt=0

Debt dynamics line shows the relationship between b and (i-n), for db/dt = 0.

Even with a primary surplus (d<0), if i is high (relative to n), then b is on explosive path.

API-119 - Prof.J.Frankel

Debt dynamics, continued

• It is best to keep b low to begin with, especially for “debt-intolerant countries.”

• Otherwise, it may be hard to stay on the stable path • if

– i rises suddenly, • due to either a rise in world i* (e.g., 1982, 2016), or • an increase in risk concerns (e.g., 2008);

– or n exogenously slows down.

• Now add the upward-sloping supply of funds curve.

• i includes a default premium, which probably depends in turn on db/dt.

• => It may be difficult or impossible to escape the unstable path – without default, write-down, or restructuring of the debt, – or else inflating it away,

• if you are lucky enough to have borrowed in your own currency.

API-119 - Prof.J.Frankel

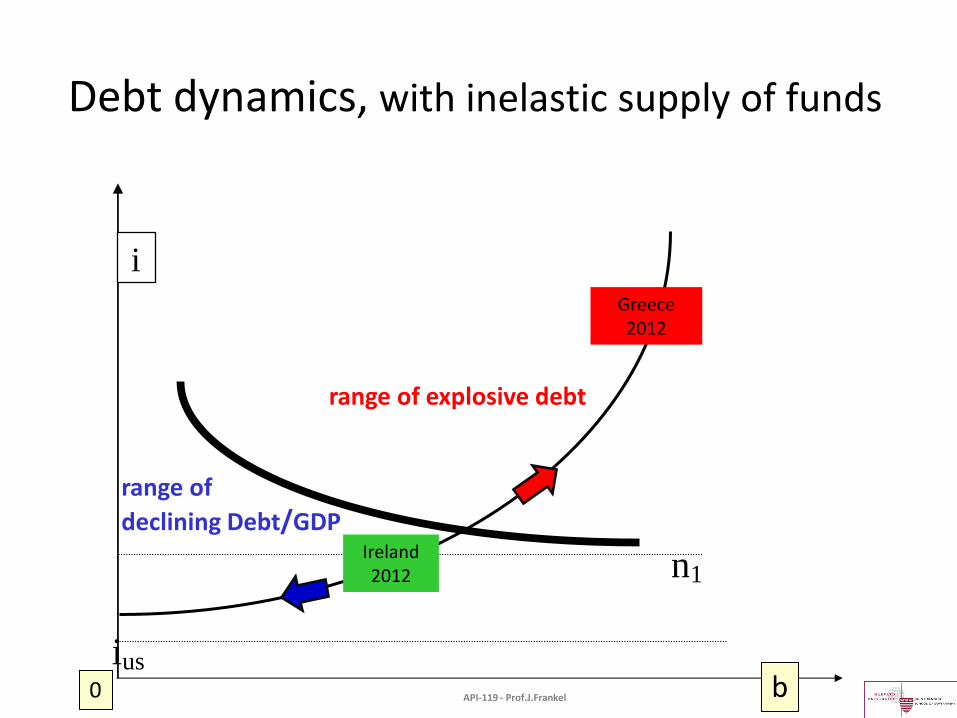

Debt dynamics, with inelastic supply of funds

n1

ius

i

b 0

Greece 2012

Ireland 2012

range of explosive debt

range of

declining Debt/GDP

API-119 - Prof.J.Frankel

Professor Jeffrey Frankel, Kennedy School, Harvard University

explosive debt path

API-119 - Prof.J.Frankel

Appendix 1: Debt dynamics graph, with possible unstable equilibrium

Y

Debtb

{

sovereign spread

Initial debt dynamics line

Supply of funds line

iUS

i

API-119 - Prof.J.Frankel

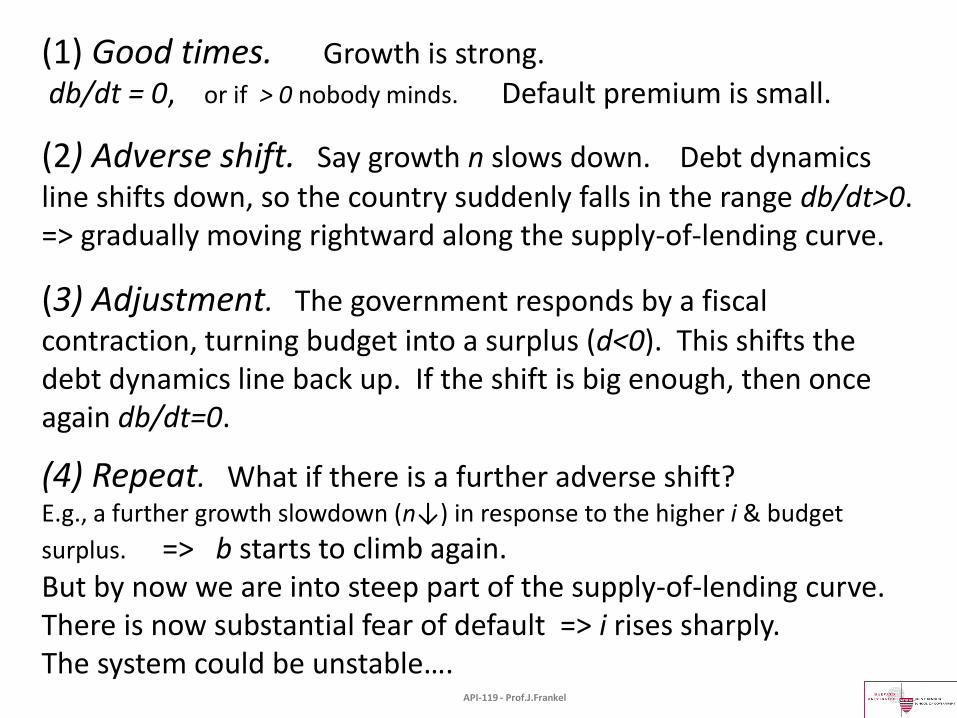

(1) Good times. Growth is strong. db/dt = 0, or if > 0 nobody minds. Default premium is small.

(2) Adverse shift. Say growth n slows down. Debt dynamics line shifts down, so the country suddenly falls in the range db/dt>0. => gradually moving rightward along the supply-of-lending curve.

(3) Adjustment. The government responds by a fiscal contraction, turning budget into a surplus (d<0). This shifts the debt dynamics line back up. If the shift is big enough, then once again db/dt=0.

(4) Repeat. What if there is a further adverse shift? E.g., a further growth slowdown (n↓) in response to the higher i & budget

surplus. => b starts to climb again. But by now we are into steep part of the supply-of-lending curve. There is now substantial fear of default => i rises sharply. The system could be unstable….

API-119 - Prof.J.Frankel

• EM sovereign spreads, 1994-2008

• The blurring of lines between debt of advanced countries and developing countries, 2009-. – Since the crisis of the euro periphery began in Greece,

we have become aware that “advanced” countries also have sovereign default risk.

Appendix 2: Recent history of sovereign spreads

API-119 - Prof.J.Frankel

API-119 - Prof.J.Frankel

WesternAsset.com

Bpblogspot.com

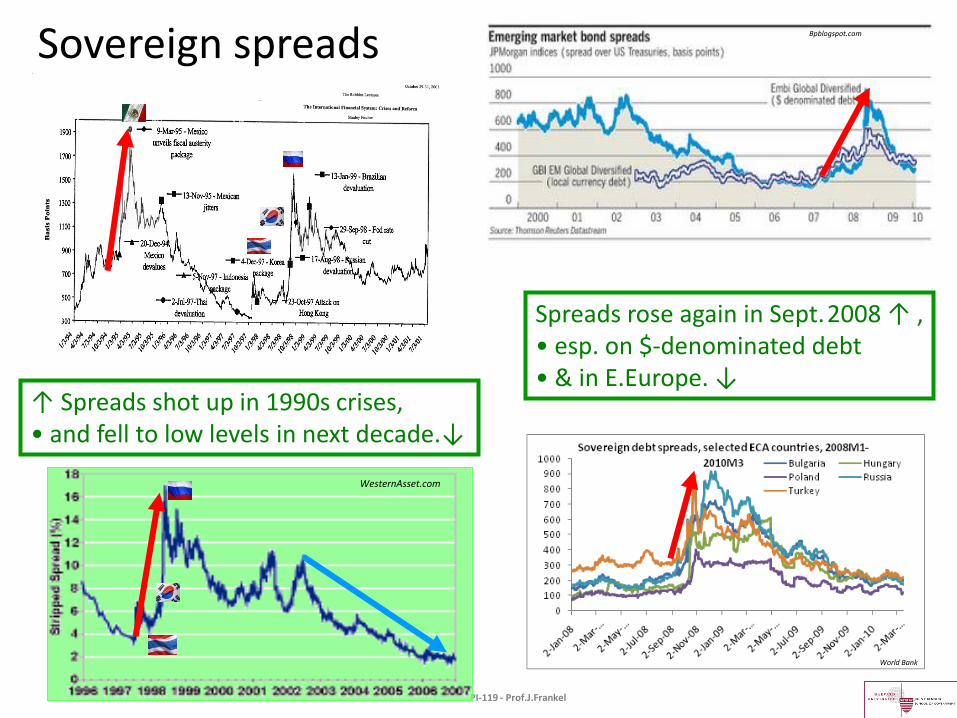

↑ Spreads shot up in 1990s crises, • and fell to low levels in next decade.↓

Spreads rose again in Sept. 2008 ↑ , • esp. on $-denominated debt • & in E.Europe. ↓

World Bank

Sovereign spreads

Spreads for Italy, Greece, & other Mediterranean members of € were near zero, from 2001 until 2008

and then shot up in 2010

Market Nighshift Nov. 16, 2011 API-119 - Prof.J.Frankel

Turkey is able to borrow in local currency (lira), but has to pay a high currency premium to do so.

{ Pure default risk premium on lira debt {

Total premium on

Turkey’s lira debt

over US treasuries

Schreger & Du, “Local Currency Sovereign Risk,” HU, 2013, Fig. 5

API-119 - Prof.J.Frankel

![0812 FAO - Country Responses to the Crisis[1]](https://static.fdocuments.in/doc/165x107/577d207d1a28ab4e1e93071e/0812-fao-country-responses-to-the-crisis1.jpg)