Lecture 12: Fast Reinforcement Learning Part II...

70

Lecture 12: Fast Reinforcement Learning Part II 2 Emma Brunskill CS234 Reinforcement Learning. Winter 2018 2 With many slides from or derived from David Silver, Worked Examples New Emma Brunskill (CS234 Reinforcement Learning. ) Lecture 12: Fast Reinforcement Learning Part II Winter 2018 1 / 70

Transcript of Lecture 12: Fast Reinforcement Learning Part II...

Lecture 12: Fast Reinforcement Learning Part II 2

Emma Brunskill

CS234 Reinforcement Learning.

Winter 2018

2With many slides from or derived from David Silver, Worked Examples NewEmma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 3 Winter 2018 1 / 70

Class Structure

Last time: Fast Learning, Exploration/Exploitation Part 1

This Time: Fast Learning Part II

Next time: Batch RL

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 4 Winter 2018 2 / 70

Table of Contents

1 Metrics for evaluating RL algorithms

2 Principles for RL Exploration

3 Probability Matching

4 Information State Search

5 MDPs

6 Principles for RL Exploration

7 Metrics for evaluating RL algorithms

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 5 Winter 2018 3 / 70

Performance Criteria of RL Algorithms

Empirical performance

Convergence (to something ...)

Asymptotic convergence to optimal policy

Finite sample guarantees: probably approximately correct

Regret (with respect to optimal decisions)

Optimal decisions given information have available

PAC uniform

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 6 Winter 2018 4 / 70

Table of Contents

1 Metrics for evaluating RL algorithms

2 Principles for RL Exploration

3 Probability Matching

4 Information State Search

5 MDPs

6 Principles for RL Exploration

7 Metrics for evaluating RL algorithms

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 7 Winter 2018 5 / 70

Principles

Naive Exploration (last time)

Optimistic Initialization (last time)

Optimism in the Face of Uncertainty (last time + this time)

Probability Matching (last time + this time)

Information State Search (this time)

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 8 Winter 2018 6 / 70

Multiarmed Bandits

Multi-armed bandit is a tuple of (A,R)

A : known set of m actions

Ra(r) = P[r | a] is an unknown probability distribution over rewards

At each step t the agent selects an action at ∈ AThe environment generates a reward rt ∼ Rat

Goal: Maximize cumulative reward∑t

τ=1 rτ

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 9 Winter 2018 7 / 70

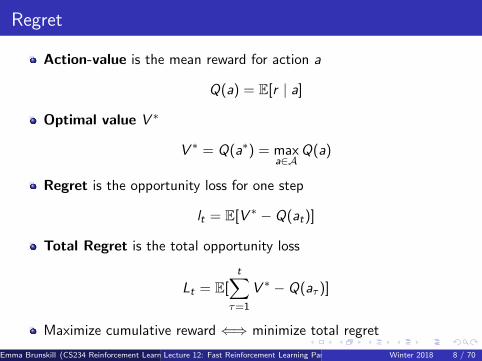

Regret

Action-value is the mean reward for action a

Q(a) = E[r | a]

Optimal value V ∗

V ∗ = Q(a∗) = maxa∈A

Q(a)

Regret is the opportunity loss for one step

lt = E[V ∗ − Q(at)]

Total Regret is the total opportunity loss

Lt = E[t∑

τ=1

V ∗ − Q(aτ )]

Maximize cumulative reward ⇐⇒ minimize total regret

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 10 Winter 2018 8 / 70

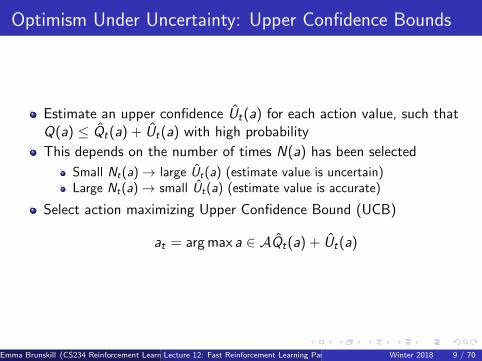

Optimism Under Uncertainty: Upper Confidence Bounds

Estimate an upper confidence Ut(a) for each action value, such thatQ(a) ≤ Qt(a) + Ut(a) with high probability

This depends on the number of times N(a) has been selected

Small Nt(a)→ large Ut(a) (estimate value is uncertain)Large Nt(a)→ small Ut(a) (estimate value is accurate)

Select action maximizing Upper Confidence Bound (UCB)

at = arg max a ∈ AQt(a) + Ut(a)

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 11 Winter 2018 9 / 70

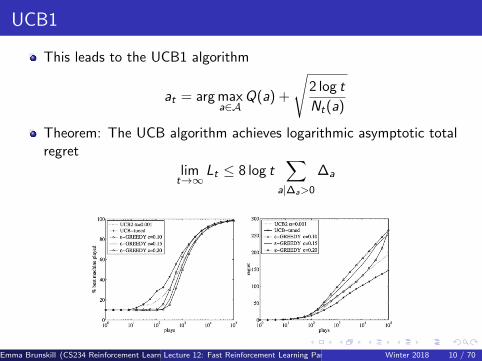

UCB1

This leads to the UCB1 algorithm

at = arg maxa∈A

Q(a) +

√2 log t

Nt(a)

Theorem: The UCB algorithm achieves logarithmic asymptotic totalregret

limt→∞

Lt ≤ 8 log t∑

a|∆a>0

∆a

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 12 Winter 2018 10 / 70

Toy Example: Ways to Treat Broken Toes13

Consider deciding how to best treat patients with broken toes

Imagine have 3 possible options: (1) surgery (2) buddy taping thebroken toe with another toe, (3) do nothing

Outcome measure is binary variable: whether the toe has healed (+1)or not healed (0) after 6 weeks, as assessed by x-ray

13Note:This is a made up example. This is not the actual expected efficacies of thevarious treatment options for a broken toe

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 14 Winter 2018 11 / 70

Toy Example: Ways to Treat Broken Toes15

Consider deciding how to best treat patients with broken toes

Imagine have 3 common options: (1) surgery (2) surgical boot (3)buddy taping the broken toe with another toe

Outcome measure is binary variable: whether the toe has healed (+1)or not (0) after 6 weeks, as assessed by x-ray

Model as a multi-armed bandit with 3 arms, where each arm is aBernoulli variable with an unknown parameter θi

Check your understanding: what does a pull of an arm / taking anaction correspond to? Why is it reasonable to model this as amulti-armed bandit instead of a Markov decision process?

15Note:This is a made up example. This is not the actual expected efficacies of thevarious treatment options for a broken toe

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 16 Winter 2018 12 / 70

Toy Example: Ways to Treat Broken Toes17

Imagine true (unknown) parameters for each arm (action) are

surgery: Q(a1) = θ1 = .95buddy taping: Q(a2) = θ2 = .9doing nothing: Q(a3) = θ3 = .1

17Note:This is a made up example. This is not the actual expected efficacies of thevarious treatment options for a broken toe

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 18 Winter 2018 13 / 70

Toy Example: Ways to Treat Broken Toes, ThompsonSampling19

True (unknown) parameters for each arm (action) are

surgery: Q(a1) = θ1 = .95buddy taping: Q(a2) = θ2 = .9doing nothing: Q(a3) = θ3 = .1

Optimism under uncertainty, UCB1 (Auer, Cesa-Bianchi, Fischer2002)

1 Sample each arm once

19Note:This is a made up example. This is not the actual expected efficacies of thevarious treatment options for a broken toe

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 20 Winter 2018 14 / 70

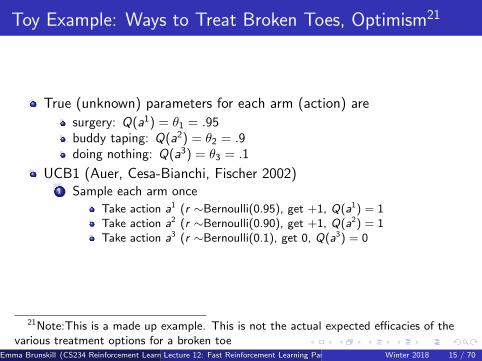

Toy Example: Ways to Treat Broken Toes, Optimism21

True (unknown) parameters for each arm (action) are

surgery: Q(a1) = θ1 = .95buddy taping: Q(a2) = θ2 = .9doing nothing: Q(a3) = θ3 = .1

UCB1 (Auer, Cesa-Bianchi, Fischer 2002)1 Sample each arm once

Take action a1 (r ∼Bernoulli(0.95), get +1, Q(a1) = 1Take action a2 (r ∼Bernoulli(0.90), get +1, Q(a2) = 1Take action a3 (r ∼Bernoulli(0.1), get 0, Q(a3) = 0

21Note:This is a made up example. This is not the actual expected efficacies of thevarious treatment options for a broken toe

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 22 Winter 2018 15 / 70

Toy Example: Ways to Treat Broken Toes, Optimism23

True (unknown) parameters for each arm (action) are

surgery: Q(a1) = θ1 = .95buddy taping: Q(a2) = θ2 = .9doing nothing: Q(a3) = θ3 = .1

UCB1 (Auer, Cesa-Bianchi, Fischer 2002)1 Sample each arm once

Take action a1 (r ∼Bernoulli(0.95), get +1, Q(a1) = 1Take action a2 (r ∼Bernoulli(0.90), get +1, Q(a2) = 1Take action a3 (r ∼Bernoulli(0.1), get 0, Q(a3) = 0

2 Set t = 3, Compute upper confidence bound on each action

ucb(a) = Q(a) +

√2lnt

Nt(a)

23Note:This is a made up example. This is not the actual expected efficacies of thevarious treatment options for a broken toe

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 24 Winter 2018 16 / 70

Toy Example: Ways to Treat Broken Toes, Optimism25

True (unknown) parameters for each arm (action) aresurgery: Q(a1) = θ1 = .95buddy taping: Q(a2) = θ2 = .9doing nothing: Q(a3) = θ3 = .1

UCB1 (Auer, Cesa-Bianchi, Fischer 2002)1 Sample each arm once

Take action a1 (r ∼Bernoulli(0.95), get +1, Q(a1) = 1Take action a2 (r ∼Bernoulli(0.90), get +1, Q(a2) = 1Take action a3 (r ∼Bernoulli(0.1), get 0, Q(a3) = 0

2 Set t = 3, Compute upper confidence bound on each action

ucb(a) = Q(a) +

√2lnt

Nt(a)

3 t = 3, Select action at = arg maxa ucb(a),4 Observe reward 15 Compute upper confidence bound on each action

25Note:This is a made up example. This is not the actual expected efficacies of thevarious treatment options for a broken toe

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 26 Winter 2018 17 / 70

Toy Example: Ways to Treat Broken Toes, Optimism27

True (unknown) parameters for each arm (action) aresurgery: Q(a1) = θ1 = .95buddy taping: Q(a2) = θ2 = .9doing nothing: Q(a3) = θ3 = .1

UCB1 (Auer, Cesa-Bianchi, Fischer 2002)1 Sample each arm once

Take action a1 (r ∼Bernoulli(0.95), get +1, Q(a1) = 1Take action a2 (r ∼Bernoulli(0.90), get +1, Q(a2) = 1Take action a3 (r ∼Bernoulli(0.1), get 0, Q(a3) = 0

2 Set t = 3, Compute upper confidence bound on each action

ucb(a) = Q(a) +

√2lnt

Nt(a)

3 t = t + 1, Select action at = arg maxa ucb(a),4 Observe reward 15 Compute upper confidence bound on each action

27Note:This is a made up example. This is not the actual expected efficacies of thevarious treatment options for a broken toe

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 28 Winter 2018 18 / 70

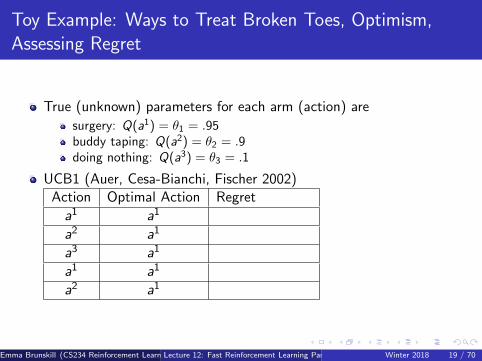

Toy Example: Ways to Treat Broken Toes, Optimism,Assessing Regret

True (unknown) parameters for each arm (action) are

surgery: Q(a1) = θ1 = .95buddy taping: Q(a2) = θ2 = .9doing nothing: Q(a3) = θ3 = .1

UCB1 (Auer, Cesa-Bianchi, Fischer 2002)Action Optimal Action Regret

a1 a1

a2 a1

a3 a1

a1 a1

a2 a1

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 29 Winter 2018 19 / 70

Check Your Understanding

An alternative would be to always select the arm with the highestlower bound

Why can this yield linear regret?

Consider a two arm case for simplicity

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 30 Winter 2018 20 / 70

Table of Contents

1 Metrics for evaluating RL algorithms

2 Principles for RL Exploration

3 Probability Matching

4 Information State Search

5 MDPs

6 Principles for RL Exploration

7 Metrics for evaluating RL algorithms

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 31 Winter 2018 21 / 70

Probability Matching

Assume have a parametric distribution over rewards for each arm

Probability matching selects action a according to probability that ais the optimal action

π(a | ht) = P[Q(a) > Q(a′), ∀a′ 6= a | ht ]

Probability matching is optimistic in the face of uncertainty

Uncertain actions have higher probability of being max

Can be difficult to compute analytically from posterior

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 32 Winter 2018 22 / 70

Thompson sampling implements probability matching

Thompson sampling:

π(a | ht) = P[Q(a) > Q(a′), ∀a′ 6= a | ht ]

= ER|ht

[1(a = arg max

a∈AQ(a))

]

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 33 Winter 2018 23 / 70

Thompson sampling implements probability matching

Thompson sampling:

π(a | ht) = P[Q(a) > Q(a′), ∀a′ 6= a | ht ]

= ER|ht

[1(a = arg max

a∈AQ(a))

]Use Bayes law to compute posterior distribution p[R | ht ]Sample a reward distribution R from posterior

Compute action-value function Q(a) = E[Ra]

Select action maximizing value on sample, at = arg maxa∈AQ(a)

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 34 Winter 2018 24 / 70

Thompson sampling implements probability matching

Thompson sampling achieves Lai and Robbins lower bound

Last checked: bounds for optimism are tighter than for Thomsponsampling

But empirically Thompson sampling can be extremely effective

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 35 Winter 2018 25 / 70

Thompson Sampling for News Article Recommendation(Chapelle and Li, 2010)

Contextual bandit: input context which impacts reward of each arm,context sampled iid each step

Arms = articles

Reward = click (+1) on article (Q(a)=click through rate)

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 36 Winter 2018 26 / 70

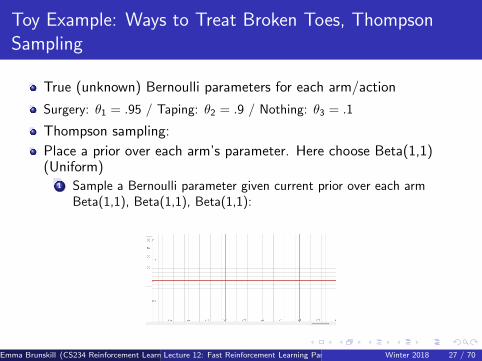

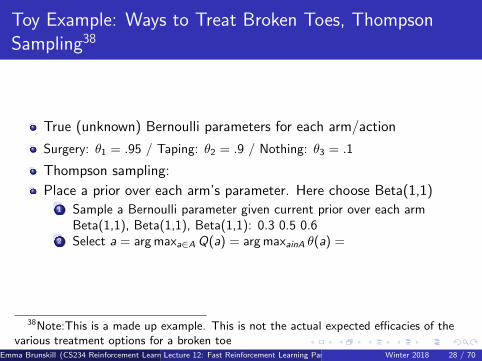

Toy Example: Ways to Treat Broken Toes, ThompsonSampling

True (unknown) Bernoulli parameters for each arm/action

Surgery: θ1 = .95 / Taping: θ2 = .9 / Nothing: θ3 = .1

Thompson sampling:

Place a prior over each arm’s parameter. Here choose Beta(1,1)(Uniform)

1 Sample a Bernoulli parameter given current prior over each armBeta(1,1), Beta(1,1), Beta(1,1):

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 37 Winter 2018 27 / 70

Toy Example: Ways to Treat Broken Toes, ThompsonSampling38

True (unknown) Bernoulli parameters for each arm/action

Surgery: θ1 = .95 / Taping: θ2 = .9 / Nothing: θ3 = .1

Thompson sampling:

Place a prior over each arm’s parameter. Here choose Beta(1,1)1 Sample a Bernoulli parameter given current prior over each arm

Beta(1,1), Beta(1,1), Beta(1,1): 0.3 0.5 0.62 Select a = arg maxa∈A Q(a) = arg maxainA θ(a) =

38Note:This is a made up example. This is not the actual expected efficacies of thevarious treatment options for a broken toe

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 39 Winter 2018 28 / 70

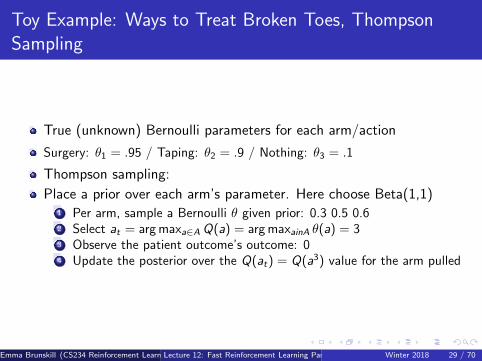

Toy Example: Ways to Treat Broken Toes, ThompsonSampling

True (unknown) Bernoulli parameters for each arm/action

Surgery: θ1 = .95 / Taping: θ2 = .9 / Nothing: θ3 = .1

Thompson sampling:

Place a prior over each arm’s parameter. Here choose Beta(1,1)1 Per arm, sample a Bernoulli θ given prior: 0.3 0.5 0.62 Select at = arg maxa∈A Q(a) = arg maxainA θ(a) = 33 Observe the patient outcome’s outcome: 04 Update the posterior over the Q(at) = Q(a3) value for the arm pulled

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 40 Winter 2018 29 / 70

Toy Example: Ways to Treat Broken Toes, ThompsonSampling

True (unknown) Bernoulli parameters for each arm/action

Surgery: θ1 = .95 / Taping: θ2 = .9 / Nothing: θ3 = .1

Thompson sampling:

Place a prior over each arm’s parameter. Here choose Beta(1,1)1 Sample a Bernoulli parameter given current prior over each arm

Beta(1,1), Beta(1,1), Beta(1,1): 0.3 0.5 0.62 Select at = arg maxa∈A Q(a) = arg maxainA θ(a) = 33 Observe the patient outcome’s outcome: 04 Update the posterior over the Q(at) = Q(a1) value for the arm pulled

Beta(c1, c2) is the conjugate distribution for BernoulliIf observe 1, c1 + 1 else if observe 0 c2 + 1

5 New posterior over Q value for arm pulled is:6 New posterior p(Q(a3)) = p(θ(a3) = Beta(1, 2)

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 41 Winter 2018 30 / 70

Toy Example: Ways to Treat Broken Toes, ThompsonSampling

True (unknown) Bernoulli parameters for each arm/action

Surgery: θ1 = .95 / Taping: θ2 = .9 / Nothing: θ3 = .1

Thompson sampling:

Place a prior over each arm’s parameter. Here choose Beta(1,1)1 Sample a Bernoulli parameter given current prior over each arm

Beta(1,1), Beta(1,1), Beta(1,1): 0.3 0.5 0.62 Select at = arg maxa∈A Q(a) = arg maxainA θ(a) = 13 Observe the patient outcome’s outcome: 04 New posterior p(Q(a1)) = p(θ(a1) = Beta(1, 2)

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 42 Winter 2018 31 / 70

Toy Example: Ways to Treat Broken Toes, ThompsonSampling

True (unknown) Bernoulli parameters for each arm/action

Surgery: θ1 = .95 / Taping: θ2 = .9 / Nothing: θ3 = .1

Thompson sampling:

Place a prior over each arm’s parameter. Here choose Beta(1,1)1 Sample a Bernoulli parameter given current prior over each arm

Beta(1,1), Beta(1,1), Beta(1,2): 0.7, 0.5, 0.3

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 43 Winter 2018 32 / 70

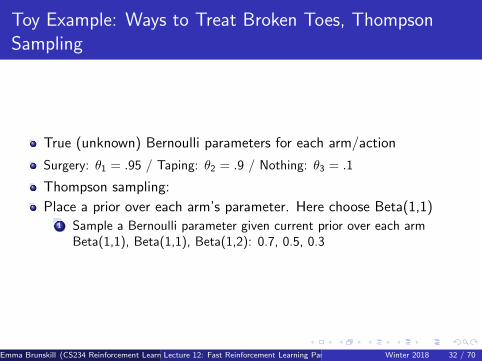

Toy Example: Ways to Treat Broken Toes, ThompsonSampling

True (unknown) Bernoulli parameters for each arm/action

Surgery: θ1 = .95 / Taping: θ2 = .9 / Nothing: θ3 = .1

Thompson sampling:

Place a prior over each arm’s parameter. Here choose Beta(1,1)1 Sample a Bernoulli parameter given current prior over each arm

Beta(1,1), Beta(1,1), Beta(1,2): 0.7, 0.5, 0.32 Select at = arg maxa∈A Q(a) = arg maxainA θ(a) = 13 Observe the patient outcome’s outcome: 14 New posterior p(Q(a1)) = p(θ(a1) = Beta(2, 1)

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 44 Winter 2018 33 / 70

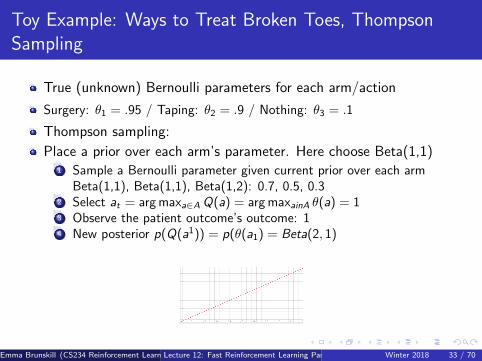

Toy Example: Ways to Treat Broken Toes, ThompsonSampling

True (unknown) Bernoulli parameters for each arm/action

Surgery: θ1 = .95 / Taping: θ2 = .9 / Nothing: θ3 = .1

Thompson sampling:Place a prior over each arm’s parameter. Here choose Beta(1,1)

1 Sample a Bernoulli parameter given current prior over each armBeta(2,1), Beta(1,1), Beta(1,2): 0.71, 0.65, 0.1

2 Select at = arg maxa∈A Q(a) = arg maxainA θ(a) = 13 Observe the patient outcome’s outcome: 14 New posterior p(Q(a1)) = p(θ(a1) = Beta(3, 1)

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 45 Winter 2018 34 / 70

Toy Example: Ways to Treat Broken Toes, ThompsonSampling

True (unknown) Bernoulli parameters for each arm/actionSurgery: θ1 = .95 / Taping: θ2 = .9 / Nothing: θ3 = .1

Thompson sampling:Place a prior over each arm’s parameter. Here choose Beta(1,1)

1 Sample a Bernoulli parameter given current prior over each armBeta(2,1), Beta(1,1), Beta(1,2): 0.75, 0.45, 0.4

2 Select at = arg maxa∈A Q(a) = arg maxainA θ(a) = 13 Observe the patient outcome’s outcome: 14 New posterior p(Q(a1)) = p(θ(a1) = Beta(4, 1)

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 46 Winter 2018 35 / 70

Toy Example: Ways to Treat Broken Toes, ThompsonSampling vs Optimism

Surgery: θ1 = .95 / Taping: θ2 = .9 / Nothing: θ3 = .1

How does the sequence of arm pulls compare in this example so far?Optimism TS Optimal Regret Optimism Regret TS

a1 a3

a2 a1

a3 a1

a1 a1

a2 a1

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 47 Winter 2018 36 / 70

Toy Example: Ways to Treat Broken Toes, ThompsonSampling vs Optimism

Surgery: θ1 = .95 / Taping: θ2 = .9 / Nothing: θ3 = .1

Incurred regret?Optimism TS Optimal Regret Optimism Regret TS

a1 a3 a1 0 0

a2 a1 a1 0.05

a3 a1 a1 0.85

a1 a1 a1 0

a2 a1 a1 0.05

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 48 Winter 2018 37 / 70

Alternate Metric: Probably Approximately Correct

Theoretical regret bounds specify how regret grows with T

Could be making lots of little mistakes or infrequent large ones

May care about bounding the number of non-small errors

More formally, probably approximately correct (PAC) results statethat the algorithm will choose an action a whose value is ε-optimal(Q(a) ≥ Q(a∗)− ε) with probability at least 1− δ on all but apolynomial number of steps

Polynomial in the problem parameters (# actions, ε, δ, etc)

Exist PAC algorithms based on optimism or Thompson sampling

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 49 Winter 2018 38 / 70

Toy Example: Probably Approximately Correct and Regret

Surgery: θ1 = .95 / Taping: θ2 = .9 / Nothing: θ3 = .1

Let ε = 0.05.

O = Optimism, TS = Thompson Sampling: W/in ε =I (Q(at) ≥ Q(a∗)− ε)

O TS Optimal O Regret O W/in ε TS Regret TS W/in εa1 a3 a1 0 0.85a2 a1 a1 0.05 0a3 a1 a1 0.85 0a1 a1 a1 0 0a2 a1 a1 0.05 0

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 50 Winter 2018 39 / 70

Toy Example: Probably Approximately Correct and Regret

Surgery: θ1 = .95 / Taping: θ2 = .9 / Nothing: θ3 = .1

Let ε = 0.05.

O = Optimism, TS = Thompson Sampling: W/in ε =I (Q(at) ≥ Q(a∗)− ε)

O TS Optimal O Regret O W/in ε TS Regret TS W/in εa1 a3 a1 0 Y 0.85 Na2 a1 a1 0.05 Y 0 Ya3 a1 a1 0.85 N 0 Ya1 a1 a1 0 Y 0 Ya2 a1 a1 0.05 Y 0 Y

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 51 Winter 2018 40 / 70

Table of Contents

1 Metrics for evaluating RL algorithms

2 Principles for RL Exploration

3 Probability Matching

4 Information State Search

5 MDPs

6 Principles for RL Exploration

7 Metrics for evaluating RL algorithms

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 52 Winter 2018 41 / 70

Relevant Background: Value of Information

Exploration is useful because it gains information

Can we quantify the value of information (VOI)?

How much reward a decision-maker would be prepared to pay in orderto have that information, prior to making a decisionLong-term reward after getting information - immediate reward

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 53 Winter 2018 42 / 70

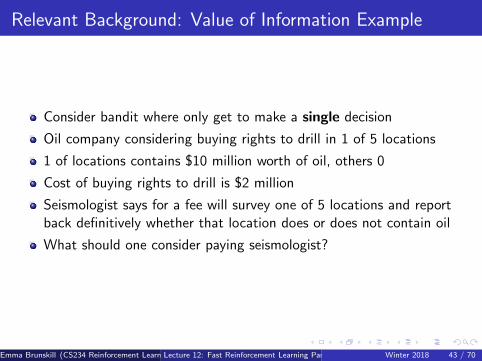

Relevant Background: Value of Information Example

Consider bandit where only get to make a single decision

Oil company considering buying rights to drill in 1 of 5 locations

1 of locations contains $10 million worth of oil, others 0

Cost of buying rights to drill is $2 million

Seismologist says for a fee will survey one of 5 locations and reportback definitively whether that location does or does not contain oil

What should one consider paying seismologist?

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 54 Winter 2018 43 / 70

Relevant Background: Value of Information Example

1 of locations contains $10 million worth of oil, others 0

Cost of buying rights to drill is $2 million

Seismologist says for a fee will survey one of 5 locations and reportback definitively whether that location does or does not contain oil

Value of information: expected profit if ask seismologist minusexpected profit if don’t askExpected profit if don’t ask:

Guess at random

=1

5(10− 2) +

4

5(0− 2) = 0 (1)

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 55 Winter 2018 44 / 70

Relevant Background: Value of Information Example

1 of locations contains $10 million worth of oil, others 0

Cost of buying rights to drill is $2 million

Seismologist says for a fee will survey one of 5 locations and reportback definitively whether that location does or does not contain oil

Value of information: expected profit if ask seismologist minusexpected profit if don’t askExpected profit if don’t ask:

Guess at random

=1

5(10− 2) +

4

5(0− 2) = 0 (2)

Expected profit if ask:If one surveyed has oil, expected profit is: 10− 2 = 8If one surveyed doesn’t have oil, expected profit: (guess at randomfrom other locations) 1

4 (10− 2)− 34 (−2) = 0.5

Weigh by probability will survey location with oil: = 15 8 + 4

5 0.5 = 2

VOI: 2− 0 = 2

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 56 Winter 2018 45 / 70

Relevant Background: Value of Information

Back to making a sequence of decisions under uncertainty

Information gain is higher in uncertain situations

But need to consider value of that information

Would it change our decisions?Expected utility benefit

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 57 Winter 2018 46 / 70

Information State Space

So far viewed bandits as a simple fully observable Markov decisionprocess (where actions don’t impact next state)

Beautiful idea: frame bandits as a partially observable Markovdecision process where the hidden state is the mean reward of eacharm

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 58 Winter 2018 47 / 70

Information State Space

So far viewed bandits as a simple fully observable Markov decisionprocess (where actions don’t impact next state)

Beautiful idea: frame bandits as a partially observable Markovdecision process where the hidden state is the mean reward of eacharm

(Hidden) State is static

Actions are same as before, pulling an arm

Observations: Sample from reward model given hidden state

POMDP planning = Optimal Bandit learning

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 59 Winter 2018 48 / 70

Information State Space

POMDP belief state / information state s is posterior over hiddenparameters (e.g. mean reward of each arm)

s is a statistic of the history, s = f (ht)

Each action a causes a transition to a new information state s ′ (byadding information), with probability Pa

s,s′

Equivalent to a POMDP

Or a MDP M = (S,A, P,R, γ) in augmented information statespace

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 60 Winter 2018 49 / 70

Bernoulli Bandits

Consider a Bernoulli bandit such that Ra = B(µa)

e.g. Win or lose a game with probability µa

Want to find which arm has the highest µaThe information state is s = (α, β)

αa counts the pulls of arm a where the reward was 0βa counts the pulls of arm a where the reward was 1

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 61 Winter 2018 50 / 70

Solving Information State Space Bandits

We now have an infinite MDP over information states

This MDP can be solved by reinforcement learning

Model-free reinforcement learning (e.g. Q-learning)

Bayesian model-based RL (e.g. Gittins indices)

This approach is known as Bayes-adaptive RL: Finds Bayes-optimalexploration/exploitation trade-off with respect to prior distribution

In other words, selects actions that maximize expected reward giveninformation have so far

Check your understanding: Can an algorithm that optimally solves aninformation state bandit have a non-zero regret? Why or why not?

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 62 Winter 2018 51 / 70

Bayes-Adaptive Bernoulli Bandits

Start with Beta(αa, βa) priorover reward function Ra

Each time a is selected,update posterior for Ra

Beta(αa + 1, βa) if r = 0Beta(αa, βa + 1) if r = 1

This defines transitionfunction P for theBayes-adaptive MDP

Information state (α, β)corresponds to reward modelBeta(α, β)

Each state transitioncorresponds to a Bayesianmodel update

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 63 Winter 2018 52 / 70

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 64 Winter 2018 53 / 70

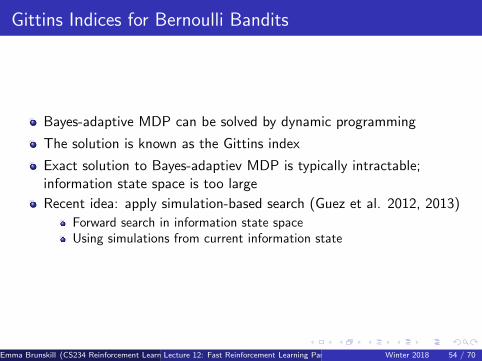

Gittins Indices for Bernoulli Bandits

Bayes-adaptive MDP can be solved by dynamic programming

The solution is known as the Gittins index

Exact solution to Bayes-adaptiev MDP is typically intractable;information state space is too large

Recent idea: apply simulation-based search (Guez et al. 2012, 2013)

Forward search in information state spaceUsing simulations from current information state

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 65 Winter 2018 54 / 70

Table of Contents

1 Metrics for evaluating RL algorithms

2 Principles for RL Exploration

3 Probability Matching

4 Information State Search

5 MDPs

6 Principles for RL Exploration

7 Metrics for evaluating RL algorithms

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 66 Winter 2018 55 / 70

Principles for Strategic Exploration

The sample principles for exploration/exploitation apply to MDPs

Naive ExplorationOptimistic InitializationOptimism in the Face of UncertaintyProbability MatchingInformation State Search

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 67 Winter 2018 56 / 70

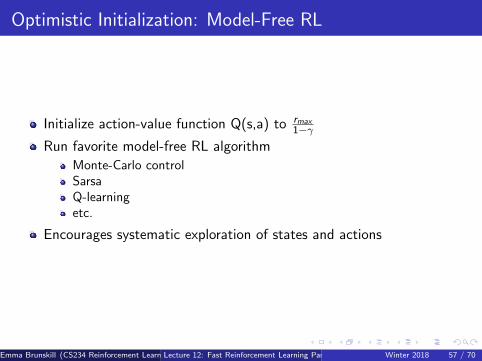

Optimistic Initialization: Model-Free RL

Initialize action-value function Q(s,a) to rmax1−γ

Run favorite model-free RL algorithm

Monte-Carlo controlSarsaQ-learningetc.

Encourages systematic exploration of states and actions

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 68 Winter 2018 57 / 70

Optimistic Initialization: Model-Based RL

Construct an optimistic model of the MDP

Initialize transitions to go to terminal state with rmax reward

Solve optimistic MDP by favorite planning algorithm

Encourages systematic exploration of states and actions

e.g. RMax algorithm (Brafman and Tennenholtz)

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 69 Winter 2018 58 / 70

UCB: Model-Based RL

Maximize UCB on action-value function Qπ(s, a)

at = arg maxa∈A

Q(st , a) + U(st , a)

Estimate uncertainty in policy evaluation (easy)Ignores uncertainty from policy improvement

Maximize UCB on optimal action-value function Q∗(s, a)

at = arg maxa∈A

Q(st , a) + U1(st , a) + U2(st , a)

Estimate uncertainty in policy evaluation (easy)plus uncertainty from policy improvement (hard)

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 70 Winter 2018 59 / 70

Bayesian Model-Based RL

Maintain posterior distribution over MDP models

Estimate both transition and rewards, p[P,R | ht ], whereht = (s1, a1, r1, . . . , st) is the history

Use posterior to guide exploration

Upper confidence bounds (Bayesian UCB)Probability matching (Thompson sampling)

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 71 Winter 2018 60 / 70

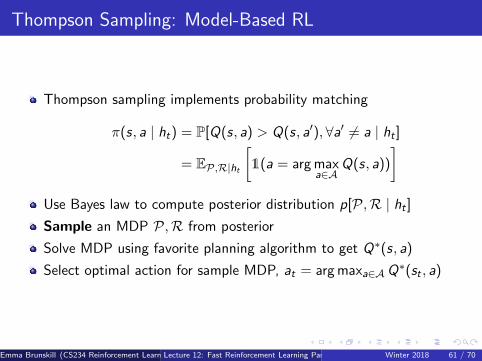

Thompson Sampling: Model-Based RL

Thompson sampling implements probability matching

π(s, a | ht) = P[Q(s, a) > Q(s, a′),∀a′ 6= a | ht ]

= EP,R|ht

[1(a = arg max

a∈AQ(s, a))

]Use Bayes law to compute posterior distribution p[P,R | ht ]Sample an MDP P,R from posterior

Solve MDP using favorite planning algorithm to get Q∗(s, a)

Select optimal action for sample MDP, at = arg maxa∈AQ∗(st , a)

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 72 Winter 2018 61 / 70

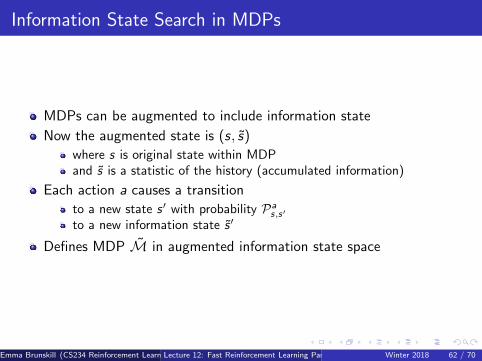

Information State Search in MDPs

MDPs can be augmented to include information state

Now the augmented state is (s, s)

where s is original state within MDPand s is a statistic of the history (accumulated information)

Each action a causes a transition

to a new state s ′ with probability Pas,s′

to a new information state s ′

Defines MDP M in augmented information state space

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 73 Winter 2018 62 / 70

Bayes Adaptive MDP

Posterior distribution over MDP model is an information state

st = P[P,R | ht ]

Augmented MDP over (s, s) is called Bayes-adaptive MDP

Solve this MDP to find optimal exploration/exploitation trade-off(with respect to prior)

However, Bayes-adaptive MDP is typically enormous

Simulation-based search has proven effective (Guez et al, 2012, 2013)

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 74 Winter 2018 63 / 70

Table of Contents

1 Metrics for evaluating RL algorithms

2 Principles for RL Exploration

3 Probability Matching

4 Information State Search

5 MDPs

6 Principles for RL Exploration

7 Metrics for evaluating RL algorithms

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 75 Winter 2018 64 / 70

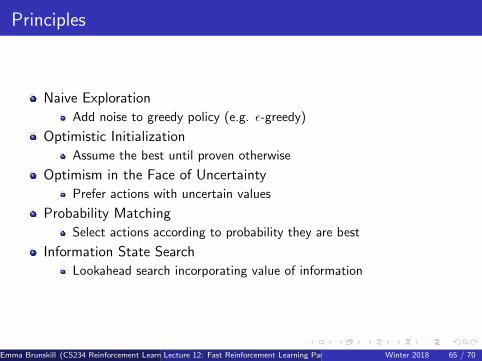

Principles

Naive Exploration

Add noise to greedy policy (e.g. ε-greedy)

Optimistic Initialization

Assume the best until proven otherwise

Optimism in the Face of Uncertainty

Prefer actions with uncertain values

Probability Matching

Select actions according to probability they are best

Information State Search

Lookahead search incorporating value of information

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 76 Winter 2018 65 / 70

Generalization and Strategic Exploration

Active area of ongoing research: combine generalization & strategicexploration

Many approaches are grounded by principles outlined here

Some examples:

Optimism under uncertainty: Bellemare et al. NIPS 2016; Ostrovski etal. ICML 2017; Tang et al. NIPS 2017Probability matching: Osband et al. NIPS 2016; Mandel et al. IJCAI2016

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 77 Winter 2018 66 / 70

Table of Contents

1 Metrics for evaluating RL algorithms

2 Principles for RL Exploration

3 Probability Matching

4 Information State Search

5 MDPs

6 Principles for RL Exploration

7 Metrics for evaluating RL algorithms

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 78 Winter 2018 67 / 70

Performance Criteria of RL Algorithms

Empirical performance

Convergence (to something ...)

Asymptotic convergence to optimal policy

Finite sample guarantees: probably approximately correct

Regret (with respect to optimal decisions)

Optimal decisions given information have available

PAC uniform (Dann, Tor, Brunskill NIPS 2017): stronger criteria,directly provides both PAC and regret bounds

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 79 Winter 2018 68 / 70

Summary: What You Are Expected to Know

Define the tension of exploration and exploitation in RL and why thisdoes not arise in supervised or unsupervised learning

Be able to define and compare different criteria for ”good”performance (empirical, convergence, asymptotic, regret, PAC)

Be able to map algorithms discussed in detail in class to theperformance criteria they satisfy

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 80 Winter 2018 69 / 70

Class Structure

Last time: Exploration and Exploitation Part I

This time: Exploration and Exploitation Part II

Next time: Batch RL

Emma Brunskill (CS234 Reinforcement Learning. )Lecture 12: Fast Reinforcement Learning Part II 81 Winter 2018 70 / 70

![Lecture 13: Fast Reinforcement Learning =1[1]With …web.stanford.edu/class/cs234/slides/lecture13_postclass.pdfThen after observed a reward r 2f0;1gthen updated posterior over is](https://static.fdocuments.in/doc/165x107/5d341b9b88c993b2278b631b/lecture-13-fast-reinforcement-learning-11with-web-after-observed-a-reward-r.jpg)

![Lecture 12: Fast Reinforcement Learning [1]With some ... · Lecture 12: Fast Reinforcement Learning 1 Emma Brunskill CS234 Reinforcement Learning Winter 2020 1With some slides derived](https://static.fdocuments.in/doc/165x107/5ed82f150fa3e705ec0dfdfc/lecture-12-fast-reinforcement-learning-1with-some-lecture-12-fast-reinforcement.jpg)

![Lecture 16: MCTS =1[1]With many slides from or derived ... · Lecture 16: MCTS 1 Emma Brunskill CS234 Reinforcement Learning. Winter 2018 1With many slides from or derived from David](https://static.fdocuments.in/doc/165x107/5e21ad4169fe1301e360183e/lecture-16-mcts-11with-many-slides-from-or-derived-lecture-16-mcts-1-emma.jpg)

![Lecture 16: MCTS =1[1]With many slides from or …...Lecture 16: MCTS 1 Emma Brunskill CS234 Reinforcement Learning. Winter 2018 1With many slides from or derived from David Silver](https://static.fdocuments.in/doc/165x107/5f31d9cdf90e4815e078b7d3/lecture-16-mcts-11with-many-slides-from-or-lecture-16-mcts-1-emma-brunskill.jpg)

![Lecture 12: Fast Reinforcement Learning [1]With …web.stanford.edu/class/cs234/slides/lecture12_postclass.pdfLecture 12: Fast Reinforcement Learning 1 Emma Brunskill CS234 Reinforcement](https://static.fdocuments.in/doc/165x107/5ea9dceb336dde7b5c510cf2/lecture-12-fast-reinforcement-learning-1with-web-lecture-12-fast-reinforcement.jpg)